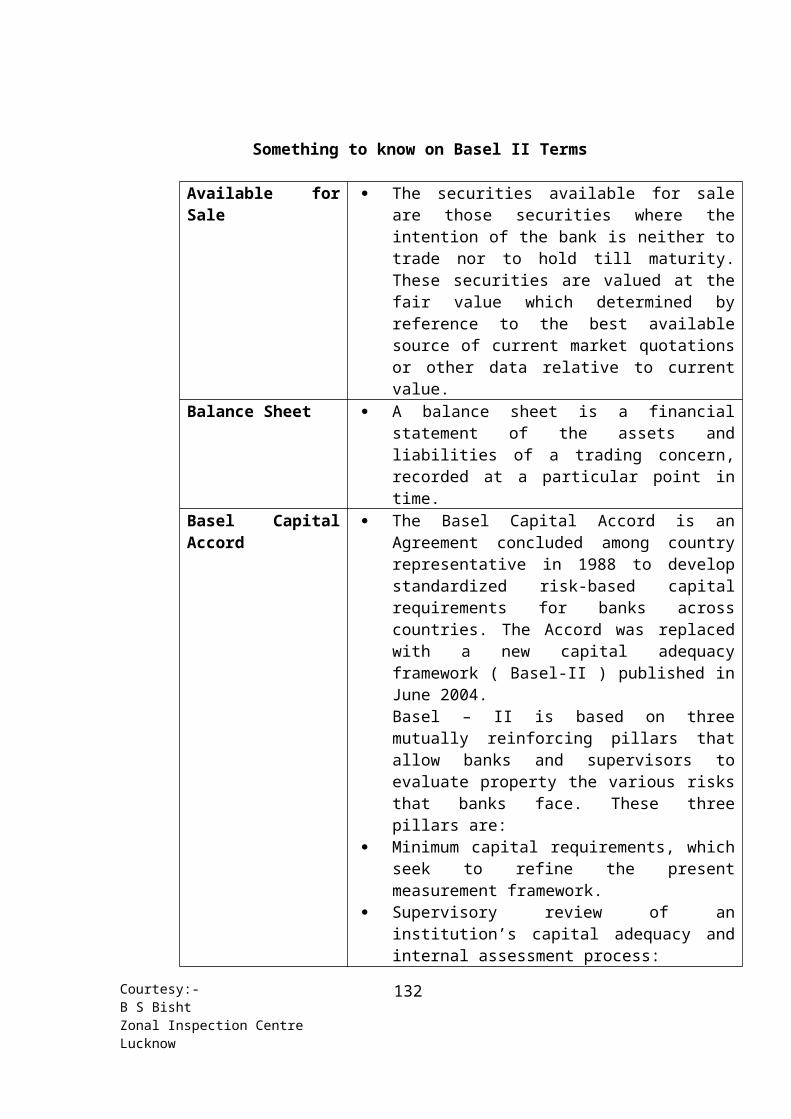

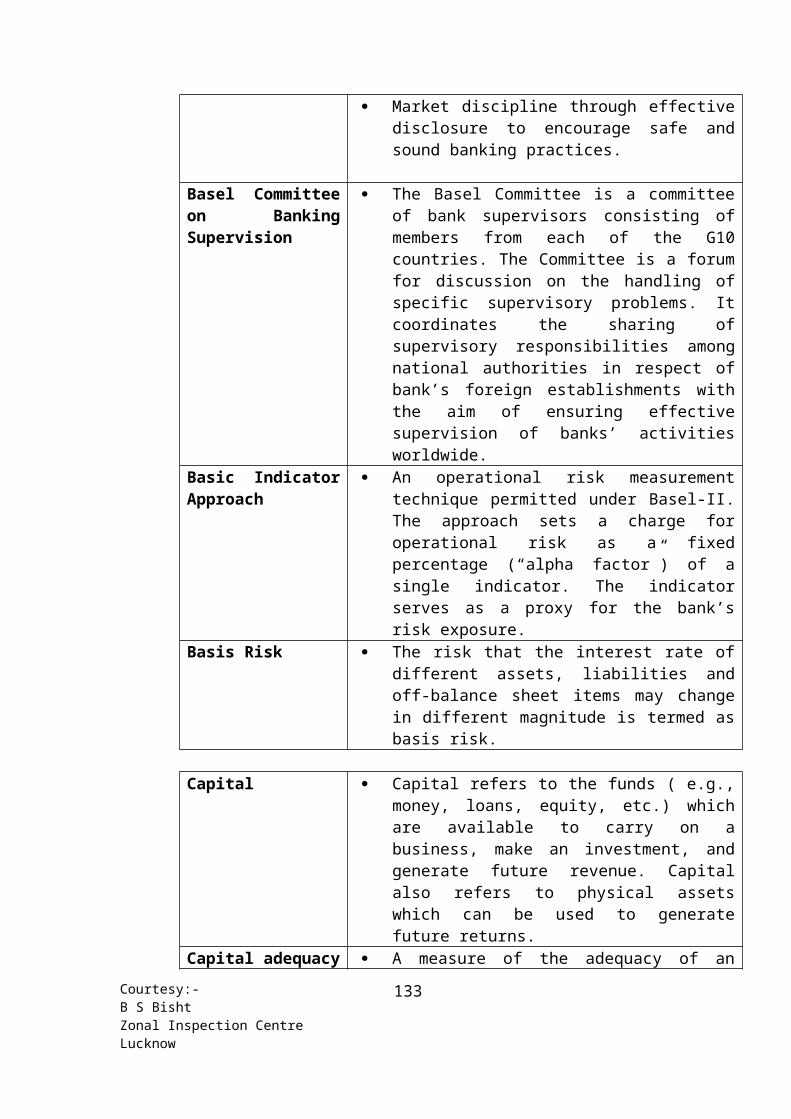

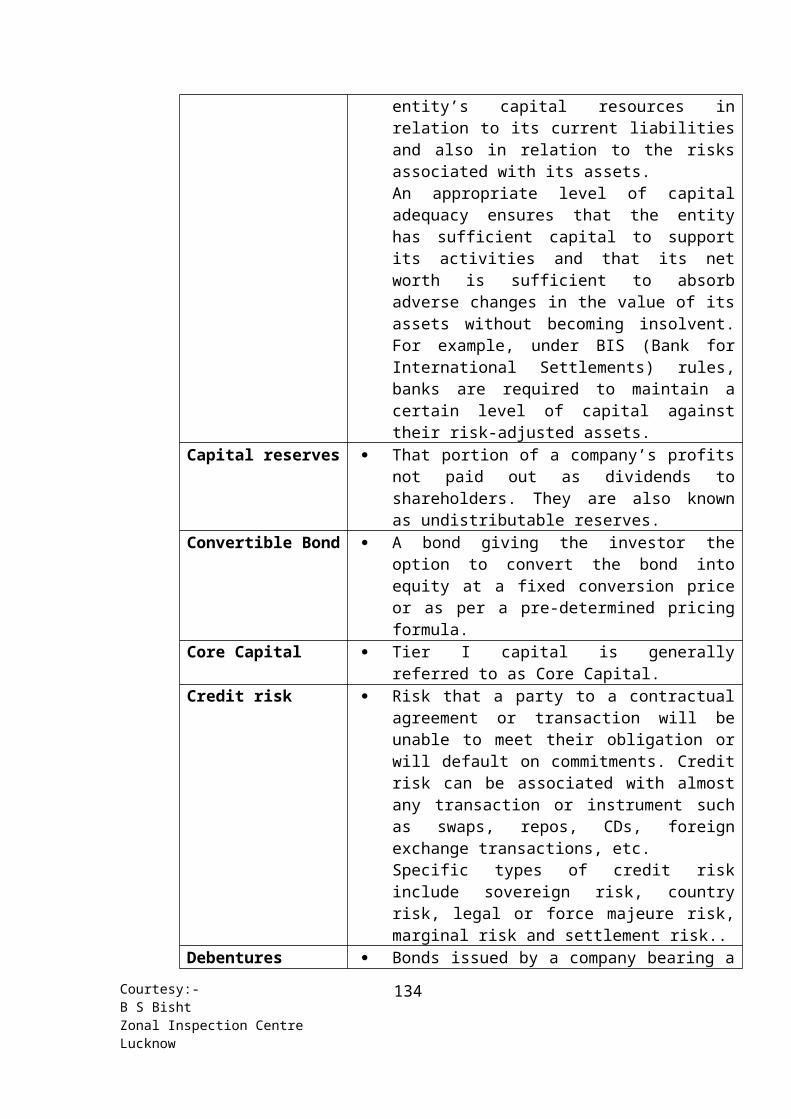

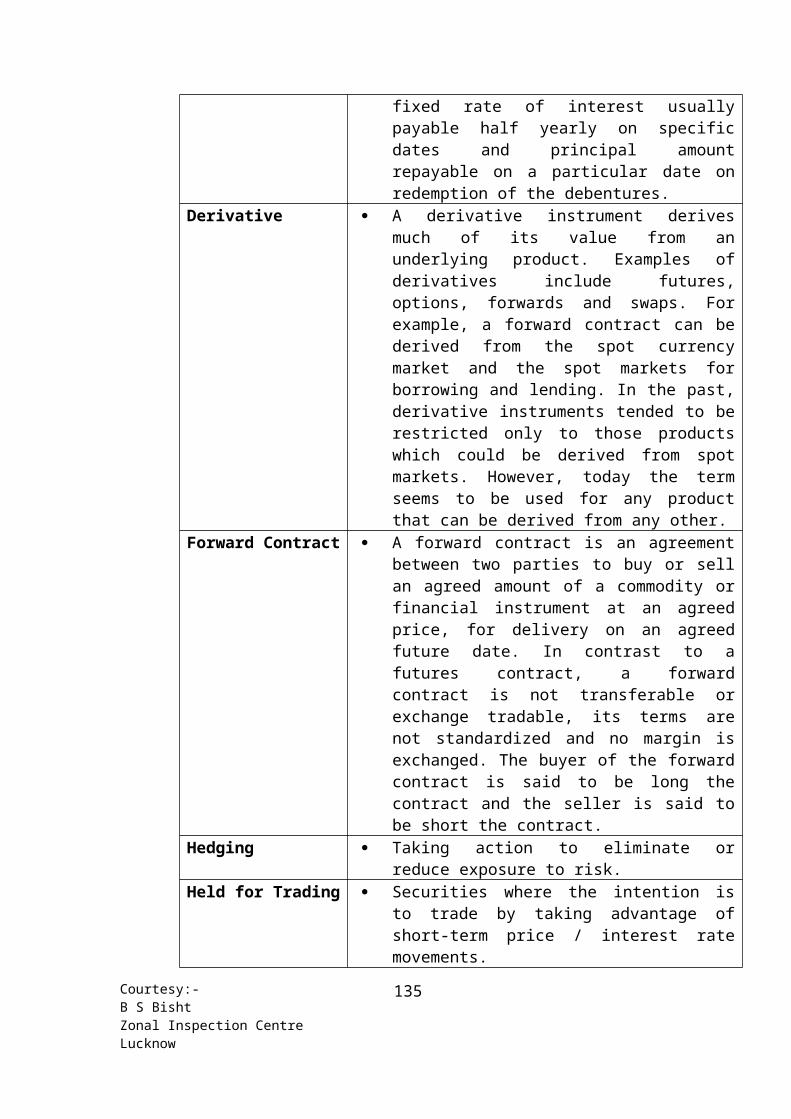

capsule on banking

TRANSCRIPT

CAPSULE

ON

BANKING TOPICSKnowledge is not simply another

commodity. On the contrary, knowledge is never used up. It

increases by diffusion and grows by dispersion.

B S BishtZonal Inspection CentreLucknow

Courtesy:-B S BishtZonal Inspection CentreLucknow

1

BANK OF BARODA

MAXIMISING GROWTH AND PROFIT THROUGH ENHANCED CUSTOMER ORIENTATION

Foreword

Ever since the banking sector reforms have picked up pace in late nineties and early twenties, there have been deluge of regulatory measures. At the same time, the banking industry has been witnessing unprecedented competition opening up wide and divergent choices to consumers. Banks have been facing stiff challenges to innovate and integrate their strategies to cope up with the semantic changes. Product innovation, smart negotiating skills to remain competitive in the market, care and concern for improved quality of customer service to achieve optimum customer satisfaction, application of IT skills, utilization of new IT infrastructure building up in the banks are some of the challenges confronting the banks.

Following such reform measures and initiatives in the financial sector, banks are witnessing inflow of large volumes of instructions/information. The media is publishing on an online basis a cross section of analysis of developments, central bank policy initiatives/announcements, interpretation of strategies of market players, shift of market shares of different players, perception of customers, opinion of analysts and so on. The combined impact adds further dimensions to the mass of information. There is thus a systemic force on the bankers to remain active and conversant with the spate of changes to maintain their operational efficiency. In the process, for aspiring bankers, knowledge management has assumed critical significance in the career progression and smart customer management.

In this background, it is felt essential to briefly bring out a synopsis of notes on banking development to enable the bankers to get first hand information on the various topics. I have taken up this rigorous job of compiling/rewriting some notes to make them compatible to the readers. Practicing fellow bankers can get apprised of various developments, which have already taken place. It also gives information on impending changes. I have sourced most of the information from RBI sites, bank sites and rewritten many of them to incorporate in the notes.

I am grateful to Dr K Srinivas Rao, Secretary to Board, who has inspired me in compiling these notes. I also take this opportunity to thank Ms Kiran, Corporate Accounts Department who has helped me in designing these notes. Any suggestions for improvement of the contents are welcome.

B.S. BISHT ZIC, Lucknow July 10, 2010

Courtesy:-B S BishtZonal Inspection CentreLucknow

2

MEMORY PAD FOR INTERVIEW

You may like to have a quick glance at the following

Sr. No.

Name of Topic / Issue

Reference Source

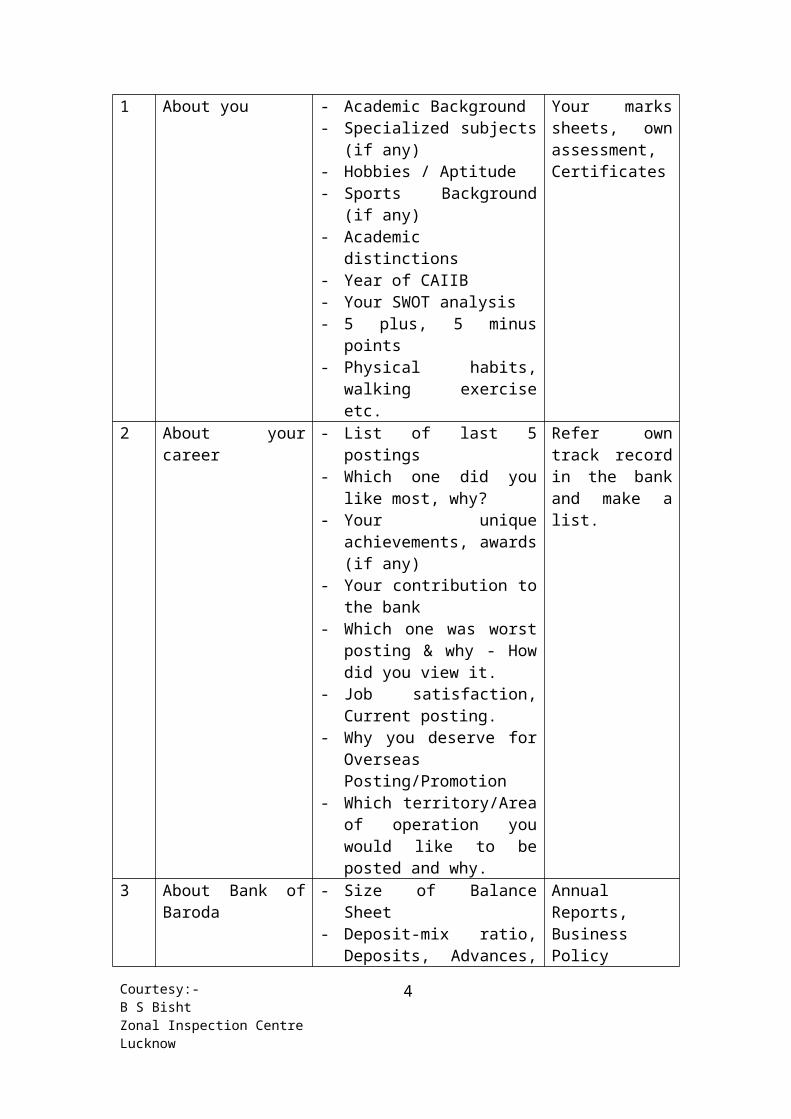

1 About you - Academic Background- Specialized subjects (if any)- Hobbies / Aptitude- Sports Background (if any)- Academic distinctions- Year of CAIIB- Your SWOT analysis- 5 plus, 5 minus points- Physical habits, walking

exercise etc.

Your marks sheets, own assessment, Certificates

2 About your career - List of last 5 postings- Which one did you like most,

why?- Your unique achievements,

awards (if any)- Your contribution to the bank- Which one was worst posting

& why - How did you view it.- Job satisfaction, Current

posting.- Why you deserve for

Overseas Posting/Promotion- Which territory/Area of

operation you would like to be posted and why.

Refer own track record in the bank and make a list.

3 About Bank of Baroda

- Size of Balance Sheet- Deposit-mix ratio, Deposits,

Advances, growth rate of 3 years

- Market Share among Public Sector Banks

- profitability trends- ROA/EPS/NPAs/ Provisions- What are our strengths?- What are our immediate

challenges?- How Competitive are we ?- Our bank’s status in the

industry

Annual Reports, Business Policy guidelines,

Courtesy:-B S BishtZonal Inspection CentreLucknow

3

- Business Policy Guidelines 2010-11

- International Operations growth of overseas operations

4 About the banking industry

- Reforms - Growth rates in the last 3

years - Bank rate, Deposit rates- challenges before PSBs- How new private bank’s have

affected PSBs. - Deposits, Advances, ROA- NPAs, Provisions- Prudential Standards- Transparency & Disclosure

Standards- Technology levels- Customer expectations

Newspaper clippings, annual report of RBI and Magazines

5 About the economy (India)

- GDP - last 3 years- Gross Domestic Savings- Industrial Growth Rate- Agricultural Growth Rate- Service Sector Growth Rate- Forex reserves- Exchange rate stability- Fiscal Deficit- Government borrowings- Country rating by Moody’s

and Standard and Poor

Newspaper clippings, Bank’s publications, RBI reports, Magazines

6 Basics of Foreign Exchange, which a prudent Banker is supposed to know.

-What is Foreign Exchange?-Exchange Rate-Letter of Credit-Stand By Letter of Credit-Packing Credit/Post Shipment -Credit-FEMA-E.C.B. -GDR-Derivative (Basic definition)-Swaps (Basic definition)-Options ((Basic definition)-Off shore Banking-Hedging (What does it mean)-LIBOR -Factoring-Forfeiting

Please go through notes in this book

Courtesy:-B S BishtZonal Inspection CentreLucknow

4

7 Other latest topics - Risk Management - Banking Sector Reforms- Full Convertibility- Sub Prime Crisis- Insurance Sector

liberalization- Entry of banks into Insurance- How much is our Foreign

Exchange Reserves- Present interest rate scenario

Paper clippings, copies of reports Bank’s Economic Digest.

Courtesy:-B S BishtZonal Inspection CentreLucknow

5

Make Written Test a Successful Event

1. On eve of examination you must have a good and normal sleep and a relaxed mind since a relaxed mind can think better and recall the facts quicker

2. On day before examination you should not study for longer period except for important revision aspect.

3. Avoid consumption of spicy/oily/heavy foods on the night previous to the examination.

4. Read each question carefully, before answering, as few questions are likely to be not so direct.

5. Objective type questions make the task of candidate easy only when he has total clarity about the fundamental aspects. Otherwise, these questions are risky to attempt since you do not get opportunity to express what you have in mind.

6. Plan your time answering the questions. Provide 5 to 10 minutes at the end for revising your answer.

7. While attempting your paper, the better understood questions should be solved first. Please do not get stuck to a particular question. If you find that you cannot recollect the answer immediately, skip it for the time being. You can come back to such questions later.

8. In case of descriptive answers, divide your answer into small point and give point wise answer for earning better score. Underline key words in answer.

9. Make your answer clear, specific and brief and do not go long or complex sentences.

10. Answer should not exceed the allowed space.11. Presentation of your answer plays a crucial role. Use appropriate terms wherever

necessary. Quote Sections/Acts/Committee names where you can. This will provide added credibility to your answers

12. Neatness and good handwriting creates a good impression in the mind of examiner13. Before handing over your answer book, make sure that you have written your Roll

No. and other particulars correctly and your answer sheet is properly stiched.14. It is not your luck but planning, preparation, continued effort and your belief that

you can succeed, produce positive result.

15. Wish you the best in all your endeavors.

Courtesy:-B S BishtZonal Inspection CentreLucknow

6

OUR LOGO

New Logo comprises the rising sun, radiating its rays across the letter form double B. What does this symbolize.

The rising sun is a symbol of change - the change from night to day. The Bank itself is changing and changing radically.

The sun is a universal symbol of energy. It gives, protects and sustains life. The Bank is a source of support for its customers.

The sun is universally recognized - across cultures and countries. Baroda is an international bank and the sun means the same thing across its global footprints.

There are 5 rays of the sun falling on the letterform double B. The 5 rays of the sun signify that the Baroda Sun's rays fall on and provide energy to its customers across the 5 continents.

The logo itself is at an angle. It is not straight, not at a perpendicular to the base. This means that the Bank is in a dynamic state - always pro-active, changing and responding to the change in the environment. It is not static but always on the move.

The second B in the double B letter form appears like a bird flying across the morning sky. It is like Baroda flying in with 20 th century values and into a new world of 21st

century efficiencies. It is this blend of hi-tech and hi-touch that should differentiate Baroda from private and foreign sector competition.

Baroda's new corporate colors are Vermillion, a shade of orange. The international Pantone code for Vermilion is 1655C. The RGB mix is 255:92:52 respectively. Vermilion is the sindoor - a powder worn by married women in many parts of the country. It symbolizes their loyalty to their husbands. The Vermilion for Baroda is a symbol of its loyalty to its customers. This color is reportedly not used by at least the top 500 banks of the world. This makes it unique and helps to differentiate Baroda from competition.

We call it the Baroda Sun.

Courtesy:-B S BishtZonal Inspection CentreLucknow

7

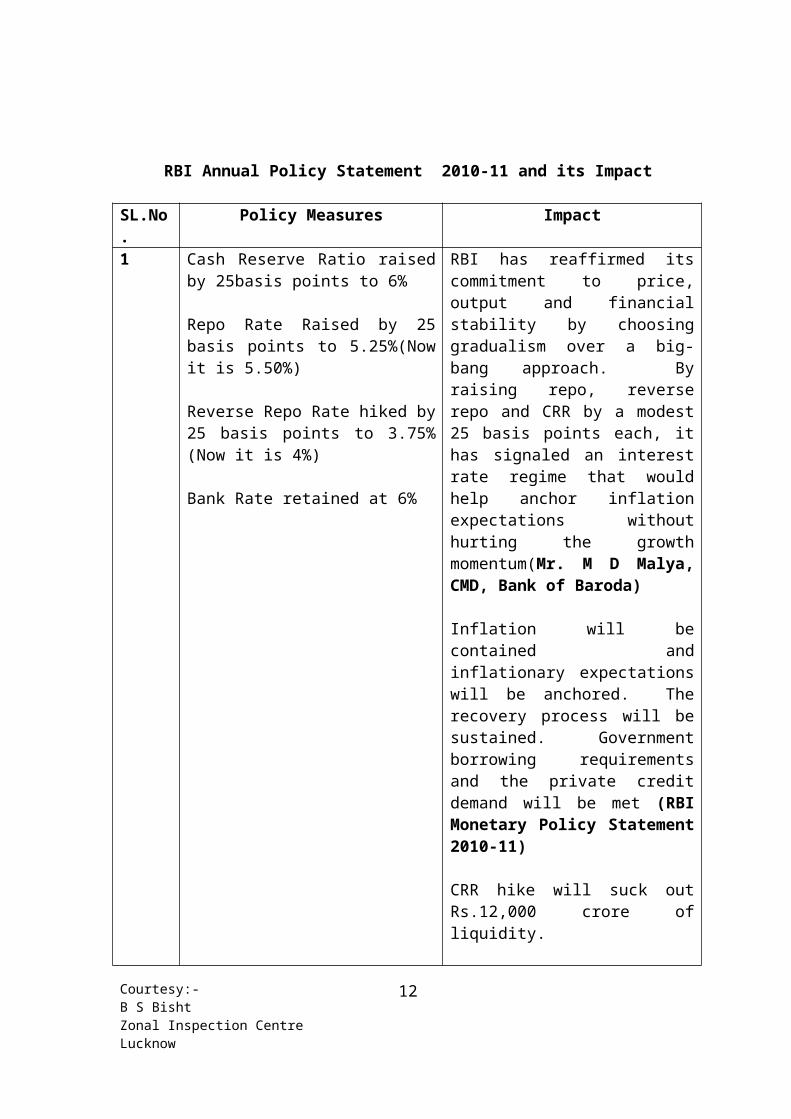

RBI Annual Policy Statement 2010-11 and its Impact

SL.No. Policy Measures Impact1 Cash Reserve Ratio raised by 25basis

points to 6%

Repo Rate Raised by 25 basis points to 5.25%(Now it is 5.50%)

Reverse Repo Rate hiked by 25 basis points to 3.75%(Now it is 4%)

Bank Rate retained at 6%

RBI has reaffirmed its commitment to price, output and financial stability by choosing gradualism over a big-bang approach. By raising repo, reverse repo and CRR by a modest 25 basis points each, it has signaled an interest rate regime that would help anchor inflation expectations without hurting the growth momentum(Mr. M D Malya, CMD, Bank of Baroda)

Inflation will be contained and inflationary expectations will be anchored. The recovery process will be sustained. Government borrowing requirements and the private credit demand will be met (RBI Monetary Policy Statement 2010-11)

CRR hike will suck out Rs.12,000 crore of liquidity.

The gradual withdrawal of easy monetary conditions is positive for growth.. An attempt to tame rising inflation

Lending rates may not be changed in the near future. Banks’ margins may come under pressure.

The RBI is presently facing the challenges of managing high inflation and need for supporting the growth levers. It has taken the economy well through the ‘managing crisis’ to ‘managing recovery’. Now the focus has shifted to ‘managing inflation’. The policy stance of RBI truly reflects these emerging concerns. This is balanced approach to support large government borrowing as well

Courtesy:-B S BishtZonal Inspection CentreLucknow

8

as private consumption demand. 2. RBI has allowed banks to park bonds

issued by companies engaged in infrastructure activities, and with a residual maturity of seven years, in the Held to Maturity bucket(HTM)

Banks will not have to show losses on securities parked in the HTM basket if market prices of these securities fall below the acquisition prices.

With no fear or erosion in the market value of HTM bonds, banks will be encouraged to invest in these papers.

RBI has facilitated the flow of banks’ funds to infrastructure sector without having to make a separate dispensation for such flows. This obviates the need for companies to provide huge margins to avail of loans

3. The RBI has allowed banks to show loans to road sector as ‘secured loans’ provided banks have the right to receive annuities, tolls collection and it is legally enforceable and irrevocable.

So far all loans to road sector were classified as ‘unsecured loans’ since the land on which the road is developed belongs to the government and thus cannot be taken as security by lenders.

The move will improve flow of credit to road sector.

The road sector is expected to receive boost with RBI announcing new measure to improve the flow of credit to the sector.

4. RBI has lowered the provisioning requirement on sub-standard loans on infrastructure loan accounts The provisioning of sub-standard loans have been lowered from 20% to 15%

Will help flow of banks funds to infrastructure sector.

Measures at Sl. No. 2 to 4 will support infrastructure requirement of around USD 1 trillion over next five to seven years.

5. RBI has permitted recognized stock exchanges to introduce plain vanilla currency options on the spot US Dollars/rupee exchange rate for residents.

At present, Indian Residents are permitted to trade in future contracts in four currency pairs on the two exchanges.

There are many advantages of options trading in the currency market. Options give buyers a right, but not the obligation, to exercise it. Options are also cheaper hedging tool

Courtesy:-B S BishtZonal Inspection CentreLucknow

9

compared to futures. In the future market, the investor has to pay the mark-to-market differences. In option, the risk is confined t the premium that has already been paid. The introduction of option trading is a welcome move. This will lead further deepening of the market Importers and exporters as well as commodity traders will find it convenient to hedge their positions in currency markets by buying or selling call or put options, depending jupon their requirements. While call options are bought when prices are expected to rise, pout options are bought when prices are expected to come down.

6. The RBI has allowed trading in interest rate futures (IRFs) on securities with short term maturities such as two-year and five-year securities and 91 days treasury bills.

At present only 10 year Government of India securities are available for trading under exchange-traded IFRs.

The introduction of these securities will surely fill the gap in the interest rate futures market.

More product will certainly deepen the interest rate derivative market and increase liquidity. At present the daily volume in IRFs is negligible.

7 RBI has extended the time for realizing the assets acquired by Assets Reconstruction Companies(ARCs) from five years to eight years. In addition, ARCs are allowed to acquire assets in their own books or directly in the books of the trust set up by them.

More time has been given ARCs to realize their assets.

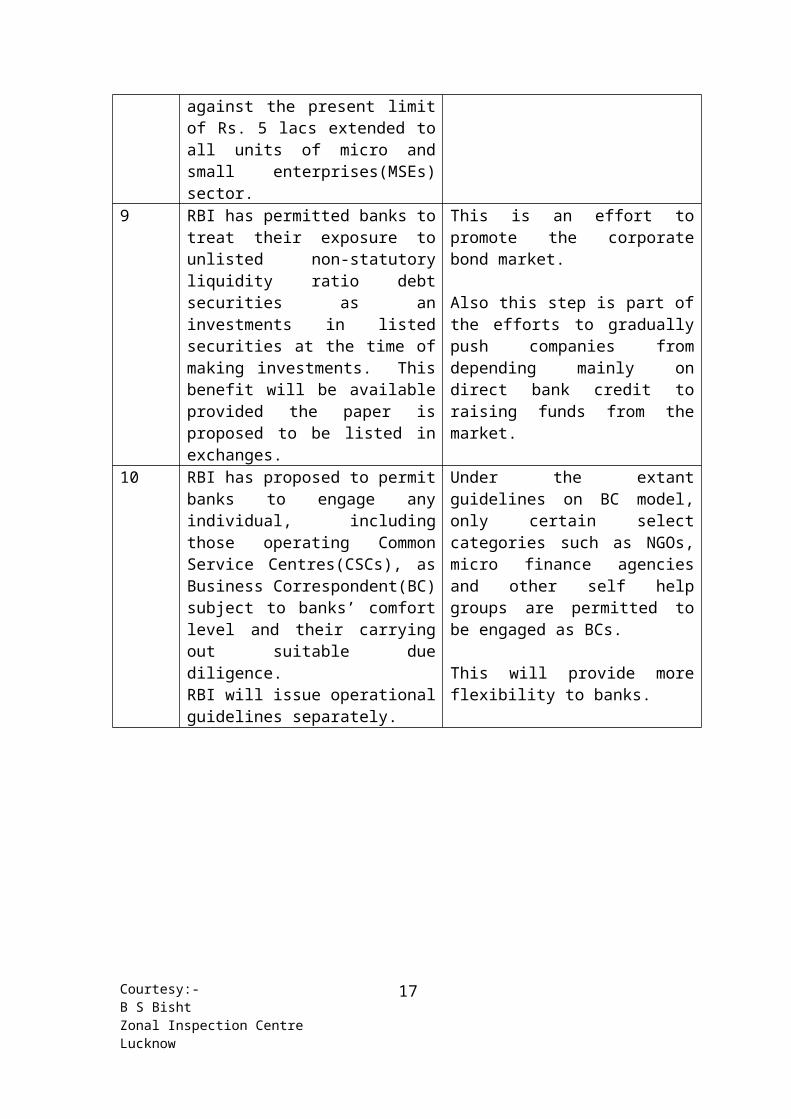

8 RBI has proposed to mandate banks not to insist on collateral security in case of loans up to Rs.10 lacs as against the present limit of Rs. 5 lacs extended to all units of micro and small enterprises(MSEs) sector.

RBI’s decision will be positive for MSE sector, benefiting large number of such enterprises.

9 RBI has permitted banks to treat their exposure to unlisted non-statutory liquidity ratio debt securities as an

This is an effort to promote the corporate bond market.

Courtesy:-B S BishtZonal Inspection CentreLucknow

10

investments in listed securities at the time of making investments. This benefit will be available provided the paper is proposed to be listed in exchanges.

Also this step is part of the efforts to gradually push companies from depending mainly on direct bank credit to raising funds from the market.

10 RBI has proposed to permit banks to engage any individual, including those operating Common Service Centres(CSCs), as Business Correspondent(BC) subject to banks’ comfort level and their carrying out suitable due diligence.RBI will issue operational guidelines separately.

Under the extant guidelines on BC model, only certain select categories such as NGOs, micro finance agencies and other self help groups are permitted to be engaged as BCs.

This will provide more flexibility to banks.

Courtesy:-B S BishtZonal Inspection CentreLucknow

11

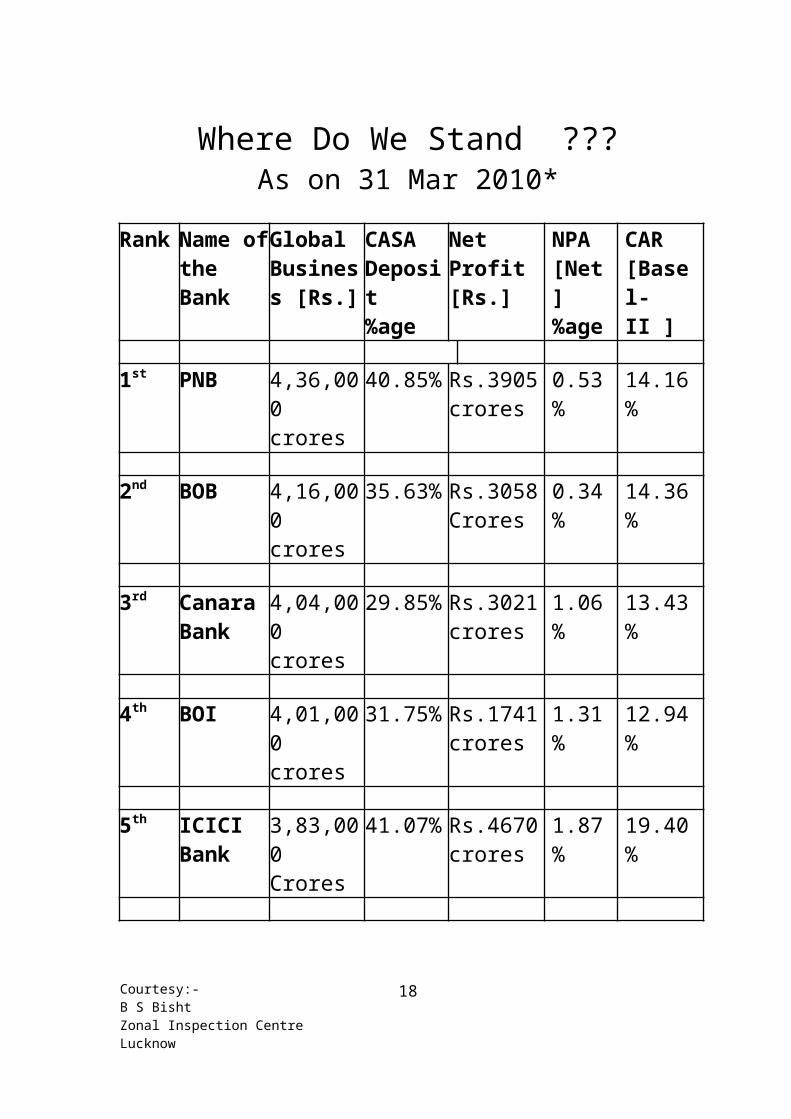

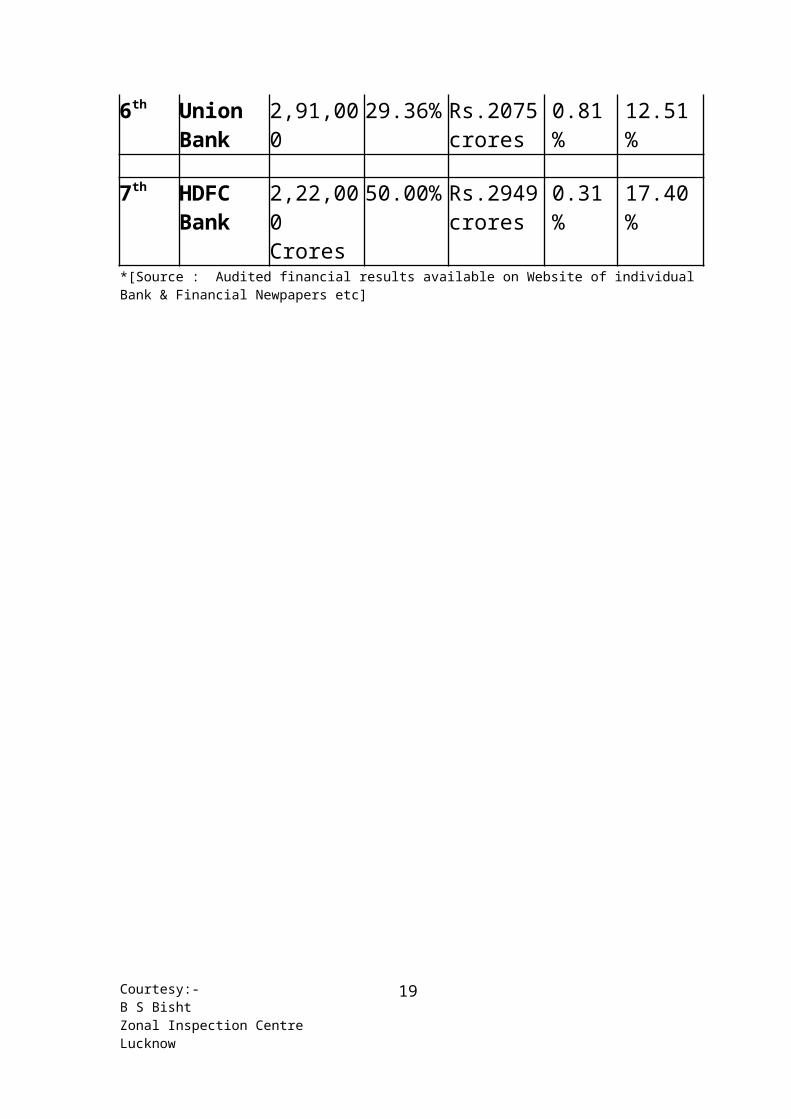

Where Do We Stand ???As on 31 Mar 2010*

Rank Name of the Bank

Global Business [Rs.]

CASA Deposit%age

Net Profit[Rs.]

NPA [Net]%age

CAR [Basel-II ]

1st PNB 4,36,000 crores

40.85% Rs.3905 crores

0.53% 14.16%

2nd BOB 4,16,000 crores

35.63% Rs.3058 Crores

0.34% 14.36%

3rd Canara Bank

4,04,000 crores

29.85% Rs.3021 crores

1.06% 13.43%

4th BOI 4,01,000 crores

31.75% Rs.1741 crores

1.31% 12.94%

5th ICICI Bank

3,83,000 Crores

41.07% Rs.4670 crores

1.87% 19.40%

6th Union Bank

2,91,000 29.36% Rs.2075crores

0.81% 12.51%

7th HDFC Bank

2,22,000Crores

50.00% Rs.2949crores

0.31% 17.40%

*[Source : Audited financial results available on Website of individual Bank & Financial Newpapers etc]

Courtesy:-B S BishtZonal Inspection CentreLucknow

12

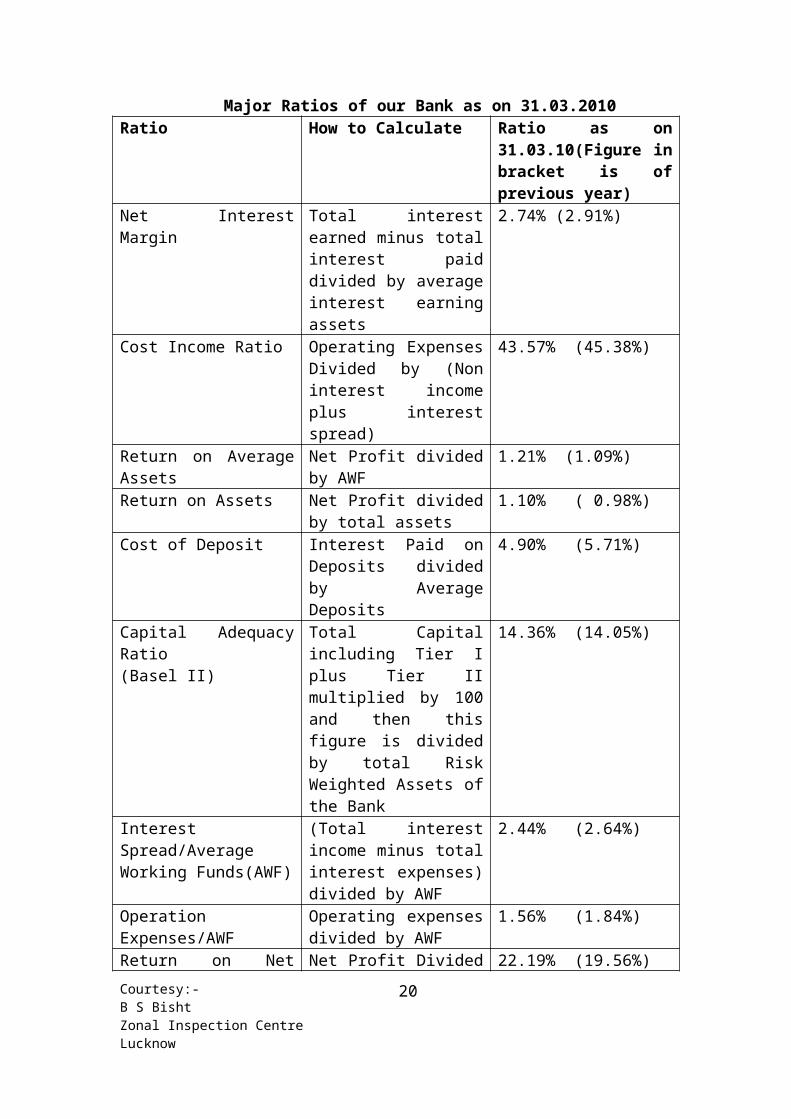

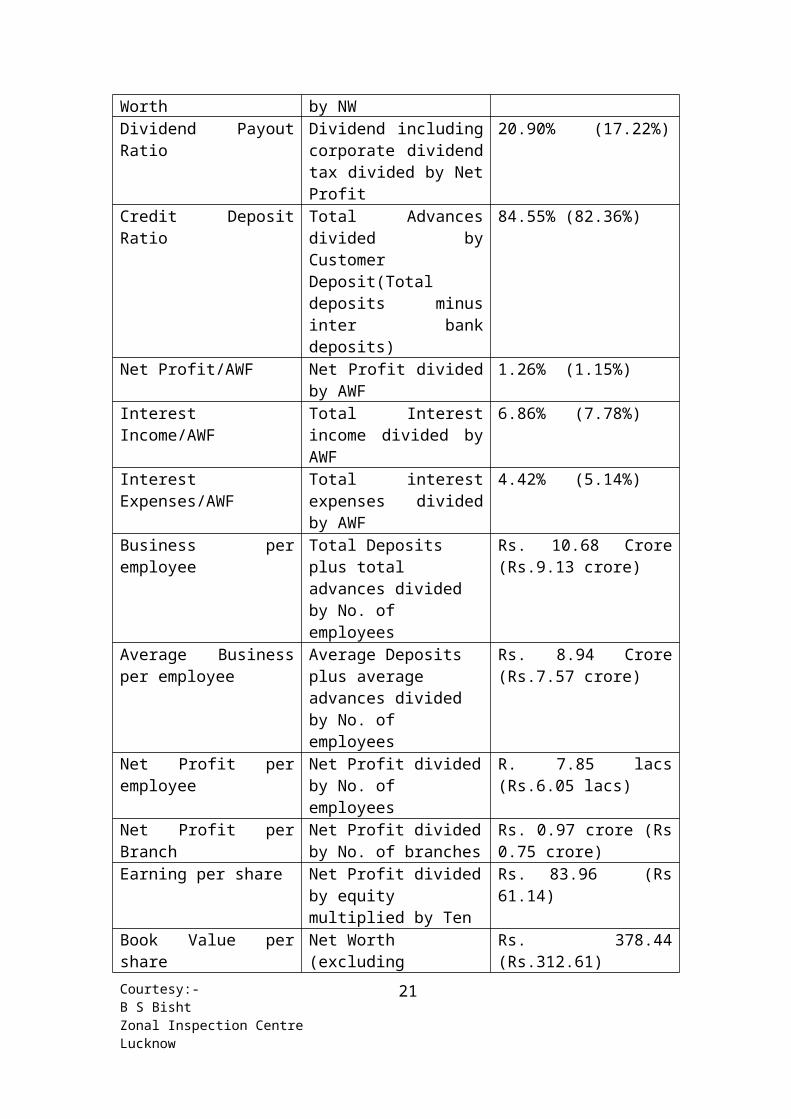

Major Ratios of our Bank as on 31.03.2010Ratio How to Calculate Ratio as on

31.03.10(Figure in bracket is of previous year)

Net Interest Margin Total interest earned minus total interest paid divided by average interest earning assets

2.74% (2.91%)

Cost Income Ratio Operating Expenses Divided by (Non interest income plus interest spread)

43.57% (45.38%)

Return on Average Assets Net Profit divided by AWF

1.21% (1.09%)

Return on Assets Net Profit divided by total assets

1.10% ( 0.98%)

Cost of Deposit Interest Paid on Deposits divided by Average Deposits

4.90% (5.71%)

Capital Adequacy Ratio(Basel II)

Total Capital including Tier I plus Tier II multiplied by 100 and then this figure is divided by total Risk Weighted Assets of the Bank

14.36% (14.05%)

Interest Spread/Average Working Funds(AWF)

(Total interest income minus total interest expenses) divided by AWF

2.44% (2.64%)

Operation Expenses/AWF Operating expenses divided by AWF

1.56% (1.84%)

Return on Net Worth Net Profit Divided by NW 22.19% (19.56%)Dividend Payout Ratio Dividend including

corporate dividend tax divided by Net Profit

20.90% (17.22%)

Credit Deposit Ratio Total Advances divided by Customer Deposit(Total deposits minus inter bank deposits)

84.55% (82.36%)

Net Profit/AWF Net Profit divided by AWF

1.26% (1.15%)

Interest Income/AWF Total Interest income divided by AWF

6.86% (7.78%)

Interest Expenses/AWF Total interest expenses divided by AWF

4.42% (5.14%)

Business per employee Total Deposits plus total advances divided by No. of employees

Rs. 10.68 Crore (Rs.9.13 crore)

Courtesy:-B S BishtZonal Inspection CentreLucknow

13

Average Business per employee

Average Deposits plus average advances divided by No. of employees

Rs. 8.94 Crore (Rs.7.57 crore)

Net Profit per employee Net Profit divided by No. of employees

R. 7.85 lacs (Rs.6.05 lacs)

Net Profit per Branch Net Profit divided by No. of branches

Rs. 0.97 crore (Rs 0.75 crore)

Earning per share Net Profit divided by equity multiplied by Ten

Rs. 83.96 (Rs 61.14)

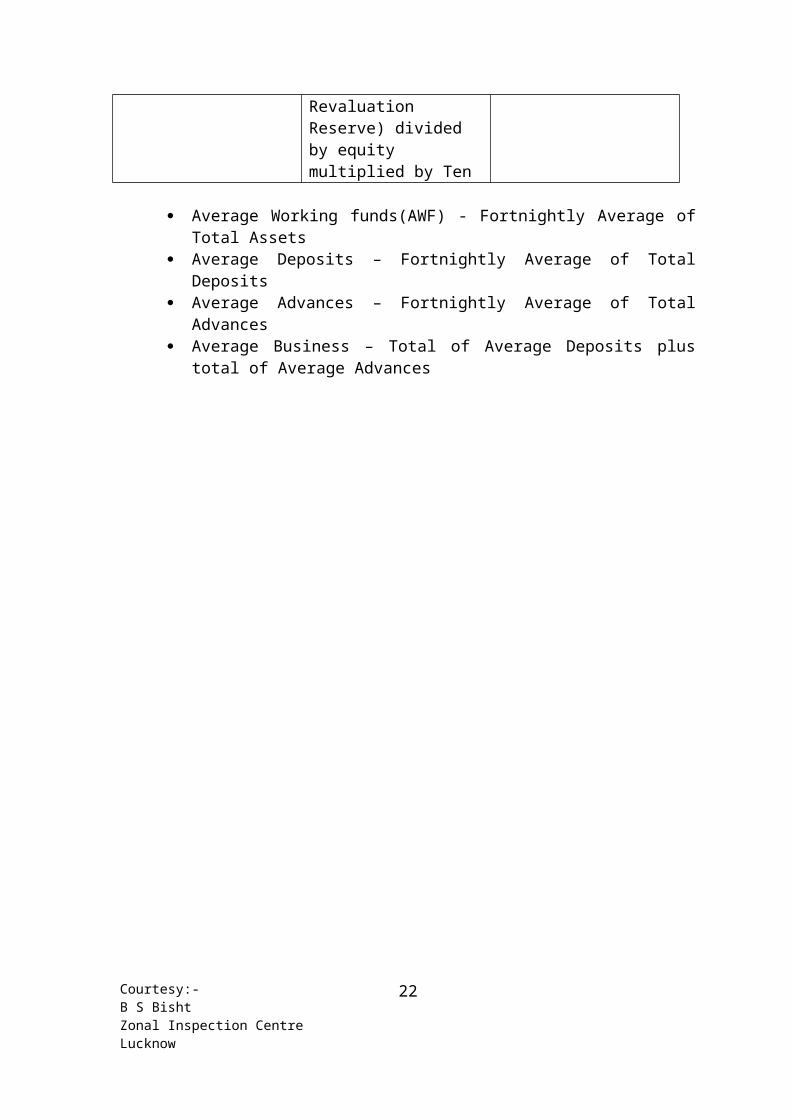

Book Value per share Net Worth (excluding Revaluation Reserve) divided by equity multiplied by Ten

Rs. 378.44 (Rs.312.61)

Average Working funds(AWF) - Fortnightly Average of Total Assets Average Deposits – Fortnightly Average of Total Deposits Average Advances – Fortnightly Average of Total Advances Average Business – Total of Average Deposits plus total of Average

Advances

Courtesy:-B S BishtZonal Inspection CentreLucknow

14

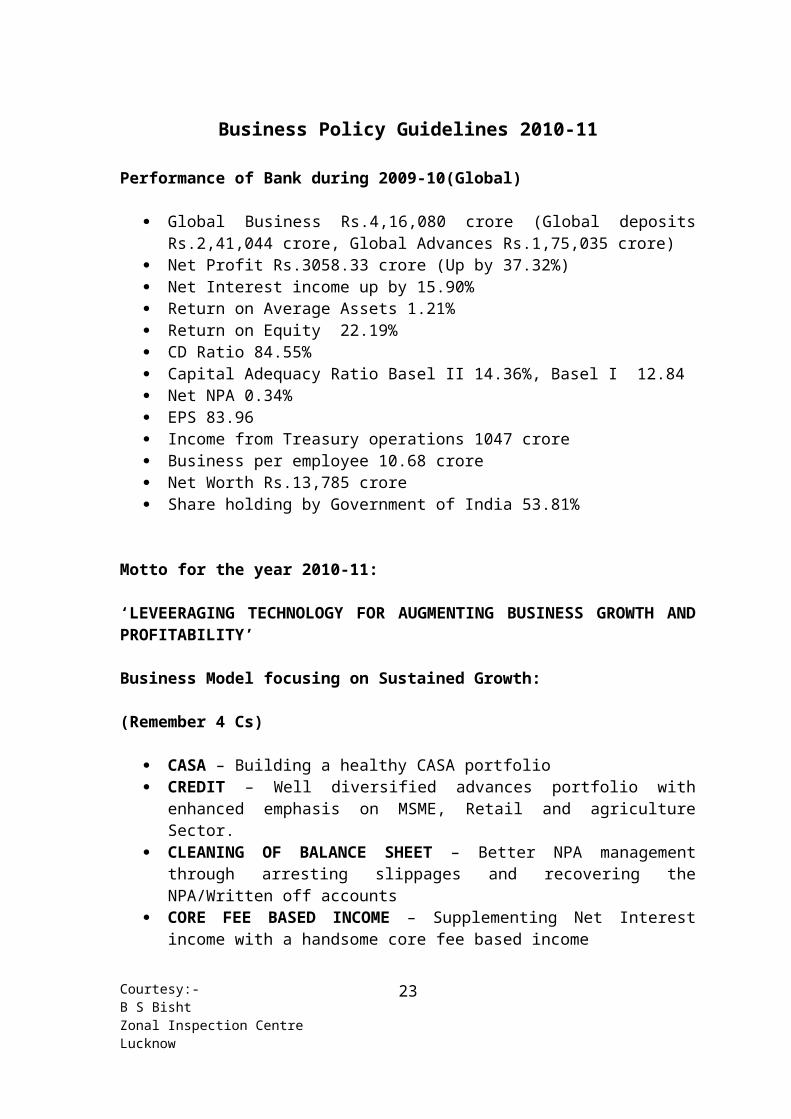

Business Policy Guidelines 2010-11

Performance of Bank during 2009-10(Global)

Global Business Rs.4,16,080 crore (Global deposits Rs.2,41,044 crore, Global Advances Rs.1,75,035 crore)

Net Profit Rs.3058.33 crore (Up by 37.32%) Net Interest income up by 15.90% Return on Average Assets 1.21% Return on Equity 22.19% CD Ratio 84.55% Capital Adequacy Ratio Basel II 14.36%, Basel I 12.84 Net NPA 0.34% EPS 83.96 Income from Treasury operations 1047 crore Business per employee 10.68 crore Net Worth Rs.13,785 crore Share holding by Government of India 53.81%

Motto for the year 2010-11:

‘LEVEERAGING TECHNOLOGY FOR AUGMENTING BUSINESS GROWTH AND PROFITABILITY’

Business Model focusing on Sustained Growth:

(Remember 4 Cs)

CASA – Building a healthy CASA portfolio CREDIT – Well diversified advances portfolio with enhanced emphasis on

MSME, Retail and agriculture Sector. CLEANING OF BALANCE SHEET – Better NPA management through

arresting slippages and recovering the NPA/Written off accounts CORE FEE BASED INCOME – Supplementing Net Interest income with a

handsome core fee based income

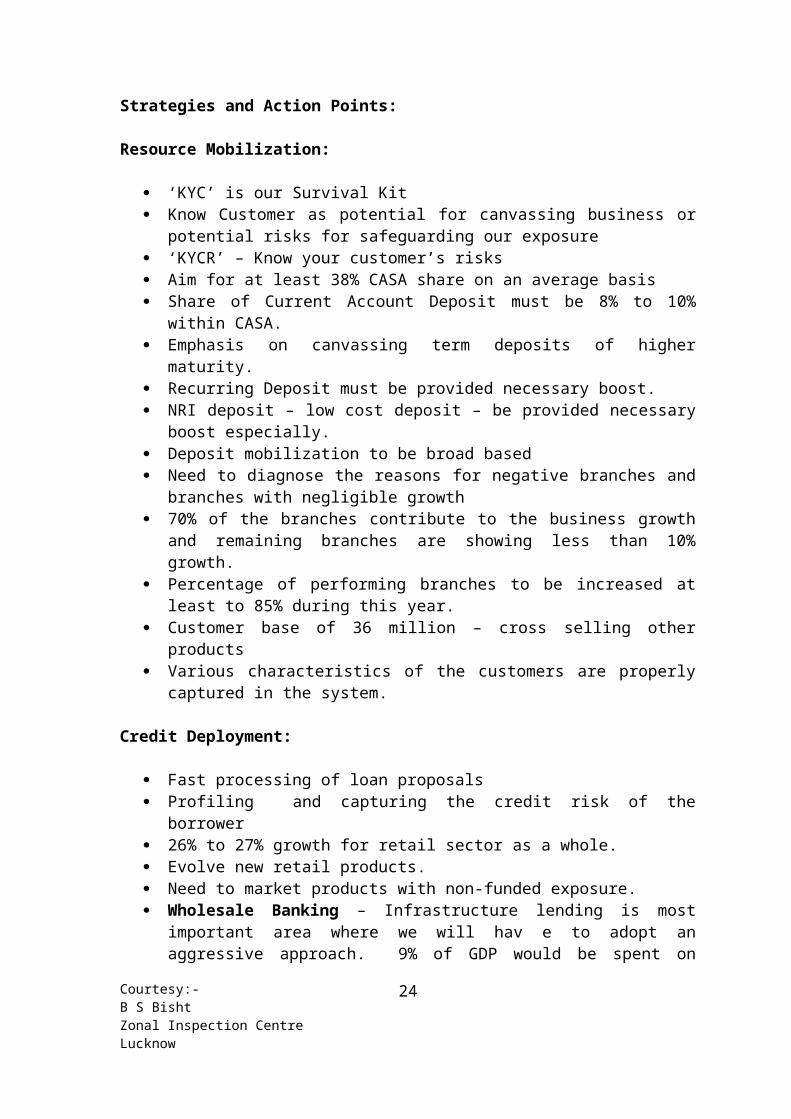

Strategies and Action Points:

Resource Mobilization:

‘KYC’ is our Survival Kit Know Customer as potential for canvassing business or potential risks for

safeguarding our exposure ‘KYCR’ – Know your customer’s risks Aim for at least 38% CASA share on an average basis Share of Current Account Deposit must be 8% to 10% within CASA.

Courtesy:-B S BishtZonal Inspection CentreLucknow

15

Emphasis on canvassing term deposits of higher maturity. Recurring Deposit must be provided necessary boost. NRI deposit – low cost deposit – be provided necessary boost especially. Deposit mobilization to be broad based Need to diagnose the reasons for negative branches and branches with negligible

growth 70% of the branches contribute to the business growth and remaining branches are

showing less than 10% growth. Percentage of performing branches to be increased at least to 85% during this

year. Customer base of 36 million – cross selling other products Various characteristics of the customers are properly captured in the system.

Credit Deployment:

Fast processing of loan proposals Profiling and capturing the credit risk of the borrower 26% to 27% growth for retail sector as a whole. Evolve new retail products. Need to market products with non-funded exposure. Wholesale Banking – Infrastructure lending is most important area where we will

hav e to adopt an aggressive approach. 9% of GDP would be spent on infrastructure products by 2014.. Auto sector, pharma, capital goods industries would be best bet in the near future. Strengthening existing relationships.

MSME Banking – Second largest source of employment. Account 40% of industrial production, 95% of industrial units and 34% of exports. Low credit availability. Comprises 95% of total industrial units, employing more than 65 million people. Yet only 8% of total bank credit finds its way into this sector. Ensure credit availability to this sector.

Rural and Agri. Banking – Bank is lagging behind on meeting the mandatory target of Direct Agriculture lending. Need to bridge this gap during this year. Branch expansion and use f Business facilitators. Agriculture credit without compromising on quality.

Retail Credit – Area still remains untapped. Housing loan constitute 44% of total retail loan. Estimated shortfall of 19.4 million housing units in India Ban should be able to tap and build the opportunities.

Non Interest Income:

NIM under pressure. .Necessity to augment non interest income. Not getting adequate attention.

Zone/Region to accept challenging targets for increasing fee based income Fee based income should be good enough to cover non interest expenses..

Government Business:- Good revenue generation opportunity. To create awareness amongst staff with regard to the profitability of the

Government Business.

Courtesy:-B S BishtZonal Inspection CentreLucknow

16

Popularize e-payment facility for payment of Direct and Indirect Taxes by non customers and/or Baroda Connect users.

Wealth Management:- ‘India will have one trillion dollar worth ingestible funds by 2012’ Target size of 42 million hose holds as against 13 million in 2007 ‘India First Life Insurance’ – a joint venture Large number of branches – should come forward for enrolling customers for life

products Tie up in the area of general insurance, asset management, equity trading, etc –

generate fee based income. .E-Business:-

The multiple delivery channels Baroda Connect, RTGS, NEFT Popularize e business facility amongst the clients. Net Based transactions through debit cards.

Asset Quality and NPA Management:-

Adopt risk mitigation techniques so that slippages can be avoided in the first place.

Not hesitate to employ all the tools of recovery that are at our disposal Need to guard against ‘take over’ of weak accounts. Improve Asset quality further. Capturing early warning signals in time and continuous dialogue with the

borrower can go a long way in arresting slippages which sometimes come as a last minute shock.

Developing alerts to catch warning signals. Target for cash recovery Rs.425 crore. Recovery Target in PWO/Write off

Rs.550 crore, Target for up gradation Rs.250 crore.

Customer Service:-

Staff to have complete and up dated knowledge about products. Prompt and hassle free service Educate customers about our products Prompt redressal of complaint under advice to customer. Seek guidance from higher authority without loss of time. Use of bank’s various IT initiatives Customers’ waiting time to be reduced. Make Bank of Baroda, the ‘Most Admired & Profitable Bank’

Courtesy:-B S BishtZonal Inspection CentreLucknow

17

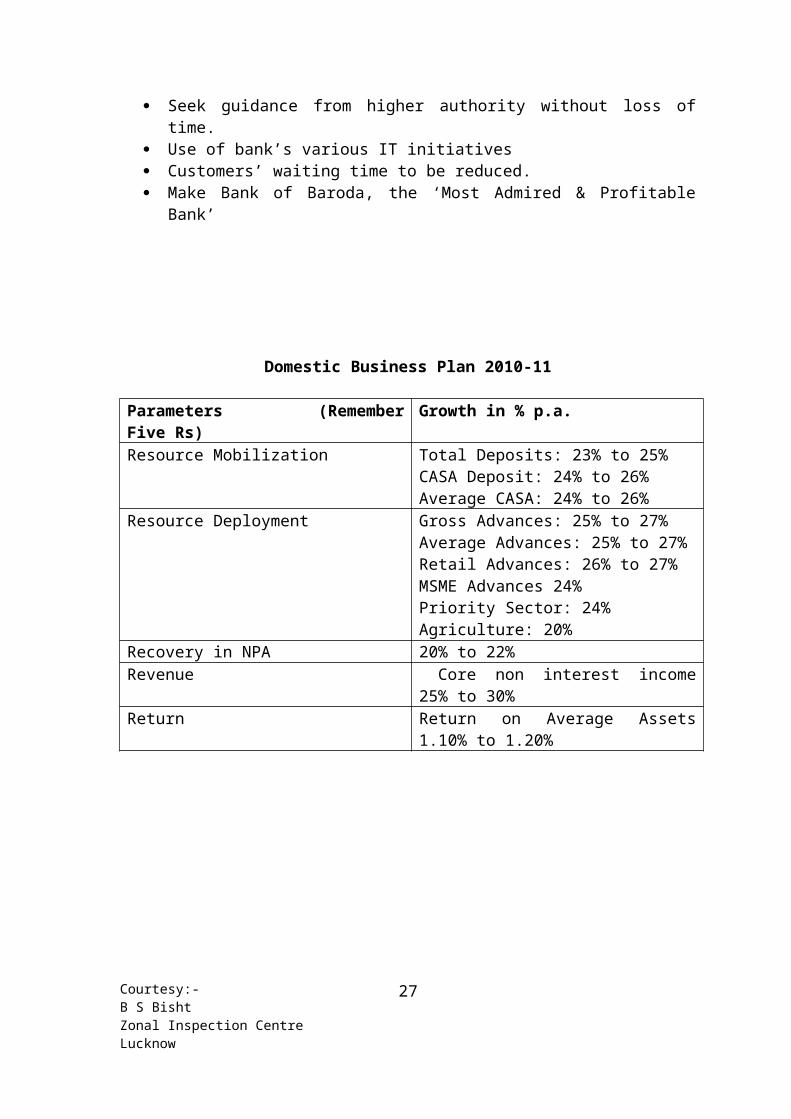

Domestic Business Plan 2010-11

Parameters (Remember Five Rs) Growth in % p.a.Resource Mobilization Total Deposits: 23% to 25%

CASA Deposit: 24% to 26%Average CASA: 24% to 26%

Resource Deployment Gross Advances: 25% to 27%Average Advances: 25% to 27%Retail Advances: 26% to 27%MSME Advances 24%Priority Sector: 24%Agriculture: 20%

Recovery in NPA 20% to 22%Revenue Core non interest income 25% to 30%Return Return on Average Assets 1.10% to 1.20%

Courtesy:-B S BishtZonal Inspection CentreLucknow

18

Courtesy:-B S BishtZonal Inspection CentreLucknow

19

TECHNOLOGY INITIATIVES DURING 2009-10

The Bank has achieved 100% CBS for all its domestic branches during September,2009.

The Bank’s Internet Banking, viz. Baroda Connect, is an important delivery channel, both for its retail and corporate customers, providing facility to transfer funds, query account status, pay both Direct and Indirect Taxes online, certain State Taxes, make payment of utility bill and book rail tickets, online inter bank payment using NEFT/RTGS. Online bill presentation and payment and shopping for selected portal and donation to selected temples SMS Alert facility are provided to eBanking customers To protect our customers from phishing attempts, beneficiary registration for third party fund transfer activities has been introduced. The Bank has also launched School Fee Collection Module.

The Bank has implemented the ATM Switch application to meet the Bank’s objective of integrating with a wide variety of front end delivery channels including ATM, POS, Payment, Gateway, Debit Card Management System and providing online authorization services by connecting to Bank’s Core Banking Solution, BASE 24 is fully operational for all domestic ATMs and for ATMs in 7 overseas territories. The Bank has launched School Fee Collection Module in August 2009 which enables payment of School/Institution fees through Bank’s ATM. The Bank has also implemented multiple accounts being linked to a single Debit Card. Debit Card is also enabled for online shopping to the merchant website.

The Bank has launched Phone Banking facility to customers, which enables them to get the Bank’s products information, enquire balances in their account, status of cheques, order statement of account through fax or email.

All CBS branches of the Bank are enabled for inter bank remittances through RTGS and NEFT.

The Bank has completed a 3D Secure Implementation under the Internet Payment Gateway Project (IPG). The IPG facilitates direct customer merchant transactions and settlement through the Bank’s central ATM Switch.

The Bank has launched Corporate Cash Management services, which enables its corporate customers to manage their funds efficiently through bulk payment services, local / outstation fund collection ( paper based or electronic) and liquidity through fund pooling facility.

The Bank has also launched Institutional Trading under the Online Trading Project on 17th October,2009.

The bank has implemented Global Treasury Solution in UK, UAE, Bahamas, Bahrain, Hong kong. The Global Treasury for India too went live on 14th December 2009.

The Bank’s Back office functions have been centralized at the branch level to relieve the operational staff from the loan of cumbersome back office functions and enable them to focus more on sales and service.

The Bank has set op three Regional Back Offices, at Baroda, Jaipur and Coimbatore, for the process of centralized account opening and issuance

Courtesy:-B S BishtZonal Inspection CentreLucknow

20

of personalized cheque book,. The Centralized Pension Payment Cell was also rolled out in Baroda on 7th October,2009.

The Bank has implemented Payment Messaging Solution (PMS) in 126 of its domestic branches ( B category branches ) and 13 overseas territories. The PMS facilitates Straight through Processing (STP) of SWIFT messages generated from the CBS, and also goes through the ALM (anti-money laundering) check.

The bank has fully implemented Enterprise wide General Ledger in India and in 19 overseas territories.

The Bank is also in the process of implementation of Data Warehouse Project (DWH). The DWH systems will enable the bank to use their data in making strategic decision and forecasting future business trends.

The Bank has already implemented Anti Money Laundering system (AML) in 14 overseas territories viz. Oman, UAE, Fiji, Mauritius, Seychelles, Tanzania, Bahamas, Kenya, Uganda, Guyana, Hongkong, Botswana,U.K., S. Africa. The AML has also been implemented in India and 14 overseas territories through a Batch Process mode.

The Bank has successfully implemented the Human Resource Networking for Employees Service with the main objective of creating a centralized database of its employees for facilitating decision making, promotion and selection exercise as also for automating other HR processes. In Payroll, Salary module, e-TDS modules have been implemented for all domestic offices in India. The “Leave Module” has also been launched and the employees are provided with the functionality of self service.

To ensure Business Continuity at all times, the Bank has implemented a state –of-the-art Data Centre and also a Disaster Recovery (DR) Site. The drills are being conducted at regular intervals and the operations are transferred to the DR site seamlessly to ensure continuity of operations at all times.

Courtesy:-B S BishtZonal Inspection CentreLucknow

21

How to emerge as winner in Competitive Environment:-

a. Reorienting our systems and procedures towards customer convenience & enhanced customer satisfaction.

b. Formulating and adhering to best corporate governance practices with an aim to set high standard of ethical values, transparency and disciplined approach to achieve excellence.

c. Focussing upon a consistent and broad-based resource mobilisation plan.

d. Enlarging the base of retail customers by leveraging technology besides implementing many technology based initiatives.

e. Diversifying the Loan Book and managing the credit risk.f. Penetrating deeper into hitherto unbanked centres/ customer

segments.g. Aggressively canvassing non-fund based business so as to improve

the share of fee based income.h. Maintaining a fine balance between the Size (Top line) and the

Strength (Bottom line) of the Balance Sheet by managing Net Interest Margin (NIM), Risk Profile of the Bank and improving the Cost-Income Ratio.

i. Enhancing the image of the Bank as a Customer Centric Organization.

Key Challenges Bank is facing to - day:

Maintaining and enhancing our market share in domestic and international arena. Protecting our NIM Increasing the proportion of low cost deposits in our deposit base to control the

cost of funds. Increasing our Non fund based income or Fee-based income. Asset Quality Management in the wake of sustained credit demand. Product and service innovation. Hiring and retaining best talents and skills.

Courtesy:-B S BishtZonal Inspection CentreLucknow

22

NAVNIRMAANBARODA NEXT

As a learning organization and an organization which is continuously evolving, we an not remain static. Market place dynamics have triggered transformation in progressive organizations in order to grow. We have launched a comprehensive transformation programme called “NAVNIRMANNA”. It will be centered around our customers and our employees, and will have two core elements – business process reengineering (BPR) and organization restructuring. Primarily, the main objectives of this program revolves around the following :

Ensure best in class customer service. Streamline processes to make life simpler for employees and customers. Equip you with the best tools and techniques to discharge your roles

effectively. Align the Bank’s organization structure and systems to help build “Baroda

Next” and drive the new strategy. This initiative will focus on solving the challenges that we face in our respective roles and will work with our ideas in making change happens at all levels in the organization. The Bank’s success will be defined by our success. We have partnered with McKinsey & Company in this exciting journey and have also put in place a dedicated team from our side for anchoring this effort and taking this initiative forward to each and every nook and corner of the organization. It is programme which is enormous not only in its scope and magnitude but also in the value and benefits that it brings to the Bank and to each one of us, individually.

Courtesy:-B S BishtZonal Inspection CentreLucknow

23

HR Initiatives:

‘SAMPARK’ – SOS Helpline for employees. Under this Help line, employees who are in distress can directly approach CMD for immediate relief. Matters requiring urgent attention like life and death issues, medical emergency, overwhelming circumstances in the personal life of employees, hardships due to natural calamities etc. are dealt on priority and relief is provided, where required.

‘PARAMARSH’ - Personal Counseling services for employees. The centre is set up to provide psychological assistance and guidance to employees to enable them to overcome any stress, complexities, conflicts in their personal and professional lives through experienced clinical counselors. It works on the principle of neutrality and confidentiality.

‘KHOJ’- A talent Identification & Development Programme to nurture talented human resources.

PASAS- Performance Appraisal System for Award Staff. With a view to bring an organization wide performance culture, hitherto uncovered category of employees i.e. clerical and sub staff has been brought under a new performance appraisal system called PASAS

Project Leap – Leadership development initiative for grooming and developing 300 leaders with the help of Grow Talent Co Ltd. The process involves (a) Identifying a competency framework for future leaders in Bank. (b) Administration of psychometric instruments and 360 degree feedback for each identified executive for building on their strength and working in the areas where development is needed.(c) Classroom orientation and Action Learning Projects (d) Succession Planning

HR Blueprint for business driven HR Reforms - Board approved strategy paper outlining various organization wide HR Reforms/Interventions

Ideaonline@ .com.- To harness the power of small ideas. The programme is designed to identify, select, groom and deploy the talented staff in key functions/roles. Special fast track career growth opportunities are lined up for the right candidates.

Introduction of Performance-linked Incentive Scheme.

Courtesy:-B S BishtZonal Inspection CentreLucknow

24

BANK’S CORE STRENGTH

A large public sector bank with modern and contemporary personality. As per Bankers’ Magazine, London its world Rank is 283 among Prime Banks

Uninterrupted Record of profit making. Strong domestic presence throughout the country Bank’s operation extended in 26 countries Global business Rs.4,16,080.00 crore as on 31.03.2010 Has been able to withstand to the turbulence more effectively during 2009-10

mainly due to its strong fundamentals Providing financial services to over 36 million customers across globe Baroda SUN- is a well accepted and recognized brand of Indian

Banking Industry Bank the common values of Honesty, Simplicity, Dedication and commitment Bank’s rapid and significant Technology progression Bank has been enjoying ‘trust and confidence’ of its stakeholders over a period of

time. Bank met its stakeholders’ expectations in terms of performance, transparency,

corporate governance and integrity in guidance during the last couple of years. Bank’s presence in all leading financial centers of the world like London,

Brussels, New York, Bhamas, Dubai, Hong Kong and Singapore. Bank’s international operations account for 24% of Bank’s global business and

around 29% of its net profits.

BANK’S MAJOR WEAKNESSES

Very little sales focus. 80% of work force at branch level is doing something

except selling.

Inflexible and sub-optimimum staffing at Branch level

Low utilization of alternate delivery channels. ATM utilization is 1%. Figures

for internet, phone banking channels are in fact negligible.

3% to 4% of branch staff is spent in selling. Best practice is 50% to 60% on

selling activities.

Staffing is not matched with customer arrival time.

Product per customer ratio is 1.2. Best practice is around 3.

Courtesy:-B S BishtZonal Inspection CentreLucknow

25

Multi-Specialist Banking-Redefinition of Critical Business Segments

In Bank’s Business Policy Guidelines 2007-08, corporate moto was chosen as ‘Moving towards Multi-specialist Banking’. This most has been chosen, as ‘one- size-fits-for all’ approach has become redundant and irrelevant in the face of fierce competition and specialized banking.

Business segmentation if the practice of dividing the customer base into homogenous groups whose requirements, needs and behavior are similar in specific ways such as age, gender, interests, spending habits, type of business, activity and so on. Business segmentation allows organizations to target groups effectively and allocate resources to best effect.

Business segmentation allows managers to:- Divide market into meaningful and measurable segments. Determine the profit potential of each segment by analyzing the revenue and cost

impacts of serving each segments. Target segments according to their profit potential and the organization’s ability to

serve them in an efficient way. Invest resources to tailor product, service and marketing and distribution programs

to match the needs of each target segment. Measure performance of each segment and adjust the segmentation approach over

time as market conditions change. Advantages of Business Segmentation:

To prioritize new product development efforts To develop customized marketing programs To design and develop specific distribution strategy. To fine tune processes required to serve each customer segment. To determine appropriate product pricing. To plan for skill set requirement in people. To determine strategy to increase the ‘Share of Wallet’.

As the Bank embarks on its journey to transform into a ‘Multi-Specialist Bank’, the Bank would need to segment its business and its customers into strategic business segments/units(SBUs). For this purpose, it would be imperative to measure and monitor Bank’s performance by the strategically defined business segments as opposed to current monitoring mechanism, which focuses primarily on performance by geographically(by Zones/Regions) and by outstanding balances in deposits and advances.

To focus more clearly on the current and emerging business opportunities.In order to move towards ‘Multi-specialist Banking, the Bank has redefined its line of business into 4 critical business segments i.e. Retail, SME, Wholesale and Rural/Agri Business. Each segment is being headed by a General Manager at Baroda Corporate Centre.

Courtesy:-B S BishtZonal Inspection CentreLucknow

26

Retail Banking Labiality Side – All individual, HUF, sole proprietorship firms and institutions

permitted by RBI to open Savings Bank Account(except Clubs & Trusts) Assets Side – Consumption/Personal loans to all individuals, including, including

NRIs, irrespective of credit limits. Small Business Loans to individuals and Sole proprietorship firms engaged in

small business, retail trade, self-employed, professionals – rendering services(other than agriculture & manufacturing) –with credit limit upto Rs.1 crore

SME Banking Small Scale Industries(SSI) – as per regulatory definition. Micro, Small and Medium Enterprises – as per regulatory definition. All other entities with their annual sales turnover of Rs. 1 crore to Rs.150 crore. Individuals and sole proprietorship firms engaged in small business with credit

limit of over Rs.1 crore. Clubs, Trusts etc.

Wholesale Banking(Mid corporate and Large Corporate) Entities (including private sector, PSU and Foreign) with their annual

sales/income turnover of over Rs.150 crore. Customers irrespective of their annual turnover – (i) Financial Institutions,

including banks, and all types of NBFCs(excluding RRBs sponsored by our bank) (ii) Central and State Governments (iii) Associate/sister concerns of Wholesale Banking Customers.

Large Corporates – Customers with their annual sales turnover of over Rs.500 crore.

Mid Corporates – Customers with their annual sales turnover of Rs.100 crore to Rs.500 crore.

Rural/Agri. Banking Two dimension – (i) Based on agri. Business Banking (ii) Based on geographical

location of branches. Direct Agriculture and Indirect Agriculture. Micro Finance. Value Chain enhancement of agri-business by alliances with agri-corporates. RRBs sponsored by our Bank All other banking business (Assets & Liabilities) i.e. SME and Retail segment

business at semi urban and rural branches. Rural and Agri. Business Segment will exclude all Wholesale Banking segment

customers.

ROLE OF BRANCH MANAGERS IN THE NEW CONTEXT

Courtesy:-B S BishtZonal Inspection CentreLucknow

27

With the implementation of CBS in large number of branches across the country, Branch Managers will have the added responsibility to fully leverage technology for business development, customer acquisition and improving service delivery quality. From transaction processing, they have to elevate their role to driving the marketing and selling efforts at the branches. Besides marketing of Bank’s products, they have also to drive marketing of third party products at the branch counters. Branch Manager’s role will also include transforming their branches into ‘Sale and Service Centres’ and ensuring highest level of customer satisfaction and zero customer complaints.

Electronic Products & Services

Transaction-enabled internet banking for Anywhere Banking. Mobile Banking/Phone Banking – for information services. ATM cum Debit Cards in association with VISA Electron for 24 Hour Banking. Baroda easy Pay – an electronic Bill Presentment & Payment Facility. Rapid Funds2India – an on line money transfer service to India from UAE, Oman,

UK and Mauritus BOB Cash Reach-A cash management product for corporates. RTGS – An interbank electronic fund transfer facility for customers. NEFT – An interbank electronic fund transfer facility. Central Funds Management System(CFMS) – An on line Negotiated Dealing

System for Government Securities. Electronic Data Interchange(EDI) – for payment of custom duty and duty

drawback. Web Based Lending Automation Process System(LAPS) – for corporate and retail

lending. Corporate internet & e mail – A Web based electronic communication information

Sharing and Knowledge Management System

SME Products

Baroda Laghu Udhyami Credit Card Baroda Artisans Credit Card Loan under Technology Upgradation Fund Scheme for Textile units Loans under Credit Linked Capital Subsidy Scheme. Composite Loans to SSI Units. Collateral Free Loans under Credit Guarantee Fund Trust Scheme Loans under National Equity Fund Schemed SME Short Term Loan SME Medium Term Loan Baroda SME Gold Card Loans under KVIC Margin Money Scheme Scheme for Financing Energy Efficiency Projects Baroda Overdraft against Land & Building Baroda Vidyasthali Loan Baroda SME Pack

Courtesy:-B S BishtZonal Inspection CentreLucknow

28

Rural Products

Loans to Agriculture and Allied Activities Micro credit through Self Help Groups (SHGs) Baroda Kisan Credit Card Baroda General Credit Card Baroda Rural Internet Kiosk Finance Scheme

Retail Products

Baroda Home Loan Baroda Education Loan Baroda Auto Loan Baroda Mortgage Loan Baroda Personal Loan Baroda Ashrey (Reverse Mortgage Loan) Baroda Loan to Doctors Baroda Traders Loan Baroda Loan against Securities Loan against Future Rent Receivables

Courtesy:-B S BishtZonal Inspection CentreLucknow

29

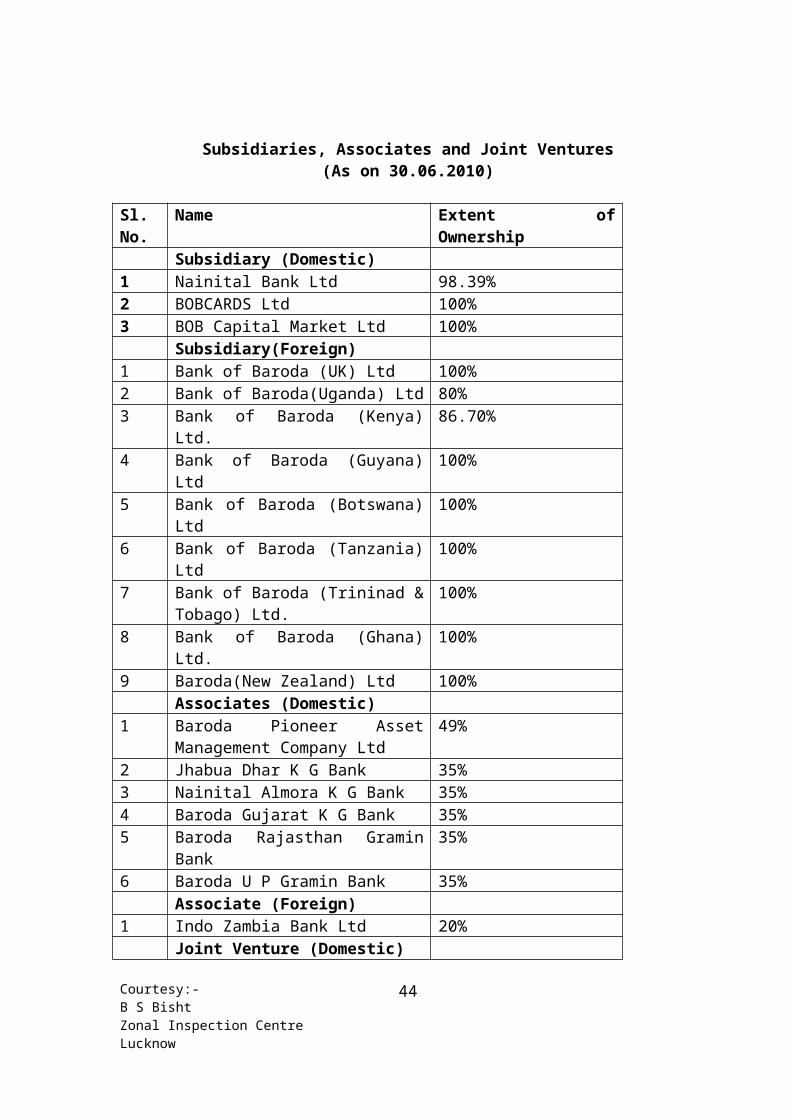

Subsidiaries, Associates and Joint Ventures(As on 30.06.2010)

Sl. No.

Name Extent of Ownership

Subsidiary (Domestic)1 Nainital Bank Ltd 98.39%2 BOBCARDS Ltd 100%3 BOB Capital Market Ltd 100%

Subsidiary(Foreign)1 Bank of Baroda (UK) Ltd 100%2 Bank of Baroda(Uganda) Ltd 80%3 Bank of Baroda (Kenya) Ltd. 86.70%4 Bank of Baroda (Guyana) Ltd 100%5 Bank of Baroda (Botswana) Ltd 100%6 Bank of Baroda (Tanzania) Ltd 100%7 Bank of Baroda (Trininad & Tobago)

Ltd.100%

8 Bank of Baroda (Ghana) Ltd. 100%9 Baroda(New Zealand) Ltd 100%

Associates (Domestic)1 Baroda Pioneer Asset Management

Company Ltd49%

2 Jhabua Dhar K G Bank 35%3 Nainital Almora K G Bank 35%4 Baroda Gujarat K G Bank 35%5 Baroda Rajasthan Gramin Bank 35%6 Baroda U P Gramin Bank 35%

Associate (Foreign)1 Indo Zambia Bank Ltd 20%

Joint Venture (Domestic)1 India First Life Insurance Co Ltd. 44%

Representative Offices1 Thailand2 Malaysia3 Australia

Off – shore Banking 5- OBU Nassau, OBU Mauritus, OBU Mumbai, OBU Singapure, OBU Baharain

Total 81 Overseas Offices in 26 countries (as on 30.06.2010) .

Courtesy:-B S BishtZonal Inspection CentreLucknow

30

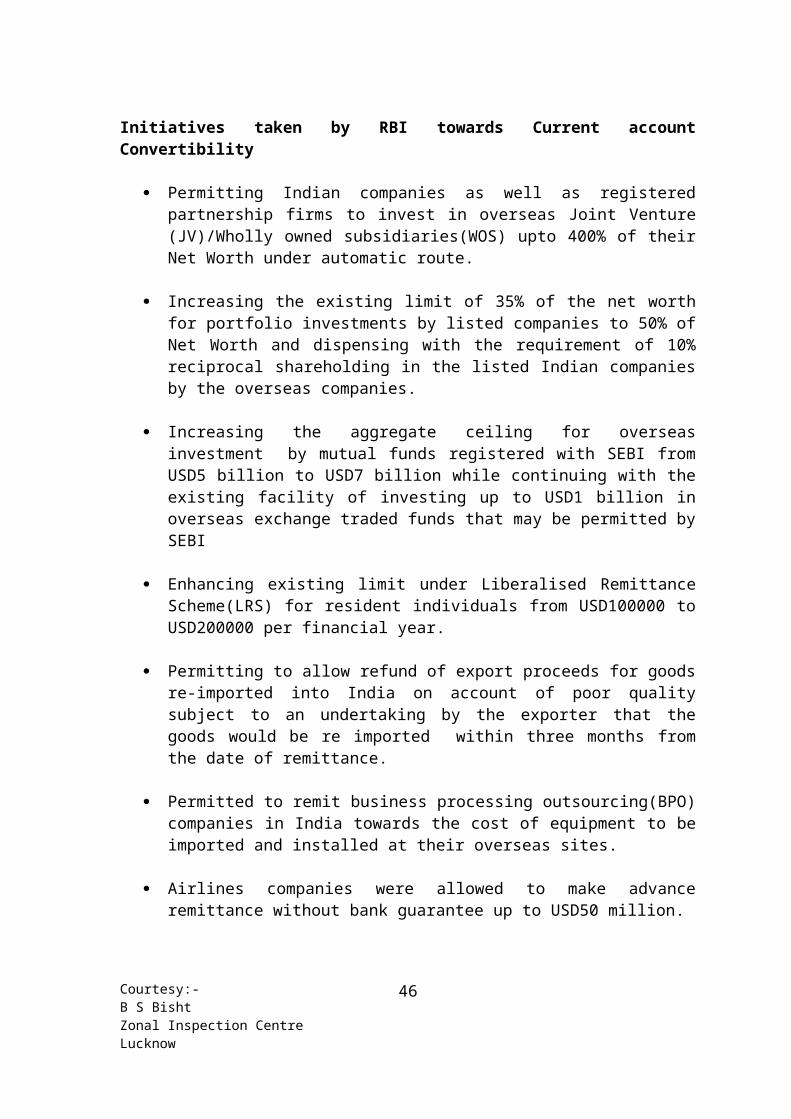

Initiatives taken by RBI towards Current account Convertibility

Permitting Indian companies as well as registered partnership firms to invest in overseas Joint Venture (JV)/Wholly owned subsidiaries(WOS) upto 400% of their Net Worth under automatic route.

Increasing the existing limit of 35% of the net worth for portfolio investments by listed companies to 50% of Net Worth and dispensing with the requirement of 10% reciprocal shareholding in the listed Indian companies by the overseas companies.

Increasing the aggregate ceiling for overseas investment by mutual funds registered with SEBI from USD5 billion to USD7 billion while continuing with the existing facility of investing up to USD1 billion in overseas exchange traded funds that may be permitted by SEBI

Enhancing existing limit under Liberalised Remittance Scheme(LRS) for resident individuals from USD100000 to USD200000 per financial year.

Permitting to allow refund of export proceeds for goods re-imported into India on account of poor quality subject to an undertaking by the exporter that the goods would be re imported within three months from the date of remittance.

Permitted to remit business processing outsourcing(BPO) companies in India towards the cost of equipment to be imported and installed at their overseas sites.

Airlines companies were allowed to make advance remittance without bank guarantee up to USD50 million.

To allow reimbursement of pre incorporation expenses incurred in India up to five percent of the investment brought in or USD100,000 whichever is higher.

Indian corporates with a proven track record were allowed to make remittances out of their foreign exchange earnings for setting up chairs outside India.

Banks were delegated powers to allow donations by Indian Corporates for specified purposes, subject to a limit of one per cent of the foreign exchange earnings during the previous three financial years or USD 5 million whichever is less

The limit for consultancy services procured from outside India by Indian companies executing infrastructure projects has been enhanced from USD 1 million to USD 10 million per project.

Interest Rate ceiling on FCNR(B) was increased to LIBOR/Swap rate plus 25bps of respective maturity of the currency. Interest rate on NRE Deposit increased to USD LIBOT/Swap Rate plus 100bps for the respective maturity.

Courtesy:-B S BishtZonal Inspection CentreLucknow

31

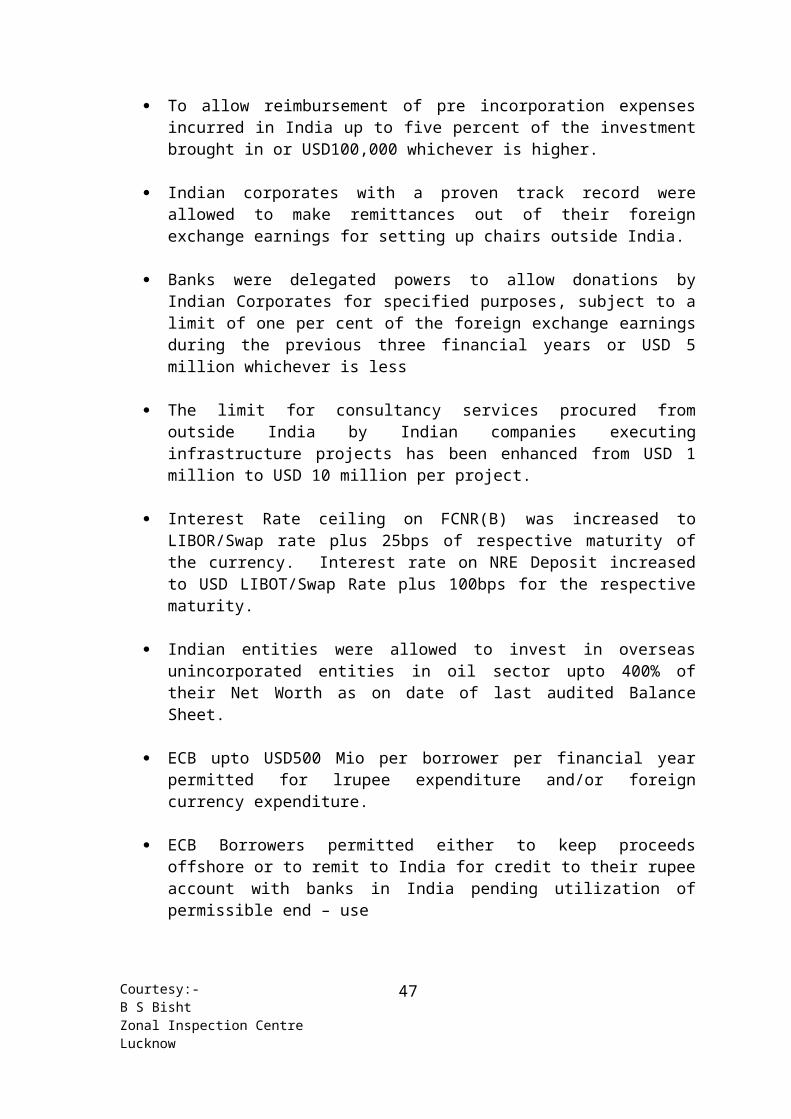

Indian entities were allowed to invest in overseas unincorporated entities in oil sector upto 400% of their Net Worth as on date of last audited Balance Sheet.

ECB upto USD500 Mio per borrower per financial year permitted for lrupee expenditure and/or foreign currency expenditure.

ECB Borrowers permitted either to keep proceeds offshore or to remit to India for credit to their rupee account with banks in India pending utilization of permissible end – use

AD Category I Banks permitted to convey ‘No objection’ under FEMA for creation of charge over immovable assets and financial securities and issue of corporate or personal guarantees on behalf of borrowers in favour of overseas lenders to secure ECB under automatic/approval Route.

The limit of USD100000.00 enhanced to USD300000.00 for making remittances for imports where the import documents are directly received by importer from overseas supplier.

The limit for advance remittance for import of .services without bank guarantee enhanced rom USD10000.00 to USD500000.00

Banks are allowed to borrow funds from their overseas branches and correspondents upto a limit of 50% of their unimpaired Tier I capital as at the close of previous quarter or upto 10 Million whichever is higher.

Exchange Traded currency future started on 29.08.08

Courtesy:-B S BishtZonal Inspection CentreLucknow

32

NRI

Person who is not resident Indian

Person resident outside India who is citizen of India or person of Indian origin

To obtain declaration Under FEMA 1999- that transaction is not designed to contravene or evade the provisions of the act or any directions under the actIn case of reason to believe - report to RBI

Who is NRI?

Abroad - employment or carrying out business or vocation or any other purpose indicating indefinite period stay outside India

Indians working abroad on assignments - Fgn Govt, UNO, IMF Officers of Govt PSU deputed abroad on assignment with Fgn Govt

Organization posted to their own offices

Persons of India Origin Persons of Indian Origin citizen of any other country other than Bangladesh

and Pakistan if he:- Holds Indian Passport He/his parents/grand parents were citizen of India by virtue of Constitution of

India of the Citizenship Act 1955

Students studying abroad are NRI provided Intention to stay for uncertain period

Schemes- NRE/NRO/FCNR Accounts

NRE Account

Prescribed application form Undertaking to inform his date of arrival in India Documentary evidence to confirm his NRI status In case of temporary visit satisfy that he is not ceased to be Non-resident Joint Account - with Non Resident only

Credits: - Remittance to India Cheque on Foreign Currency account T/Cs issued outside India Currency - CDF if US$5000/- T/C -CDF if US $10000/- T/C Currency to be tendered by himself Transfer from NRE/FCNR account Interest

Courtesy:-B S BishtZonal Inspection CentreLucknow

33

Interest on Govt. securities provided---- Maturity proceeds of Govt. securities provided--- Refund of share/debenture subscription provided--- Refund of earnest money deposited with House building agencies provided Transfer from EEFC/RFC/ Current income - rent, dividend, pension, interest provided AD is satisfied and

income tax is deducted. Any other credit permitted by RBI

Debits:- Local disbursements Remittance outside India Transfer to NRE/FCNR account of Account holder Investments provided it is covered by regulations made Any other permitted by RBI

Interest: - Savings Bank- Rate of interest applicable to Domestic Savings Bank account FD - should not exceed LIBOR/Swap rate for US$ of corresponding maturity

plus 175 basis points . The period of deposit is 1 to 3 years. Bank may exceed the period but interest

will be applicable for max period of 3 years only.

NRE Savings Deposits

The interest rate on NRE savings deposit accounts would be at the rate applicable to domestic savings deposits .

TOD- Rs.50000 max upto 2 weeks To be cleared by Inward Remittance

Overdue Deposit - Max period 14 days for overdue interestRate applicable (i) date of maturity (ii) date of renewal whichever is less

Premature withdrawal:- Bank will allow Depositors be made aware of penal interest No penalty for RFC deposit NRE- to FCNR (B) penalty provision is applicable.

FCNR (B)

Period 1 to5 years

Interest should not exceed LIBOR/Swaps plus 100 bps for corresponding maturity

Interest payment- 360 days a year. One year deposit, no compounding effectChange of status - continue till maturity

Courtesy:-B S BishtZonal Inspection CentreLucknow

34

Nomination

Taxation

POA- Not allowed

Premature withdrawal - Penalty provision to be clearly brought to the knowledge of a/c holder. Otherwise has to be borne by bank

Overdue interest - same

Forward cover - allowed

NRO Accounts

Eligible- A person/entity resident outside IndiaFor putting through bonafide transactionBangladesh/Pakistani nationality require prior approval of RBI

Types -

Joint A/c - with resident allowed

Credits- same as NRI Sale proceeds of assets including immovable property acquired out of

rupee/foreign currency or by way of inheritance.Debits-

Local payment subject to compliance Current income remitted outside India In case of NRI/PIO remittance upto US$ one Million per financial year for

bonafide purpose to the satisfaction of AD

Sale proceed of immovable property:- Remittance allowed upto One Mio US Dollars per financial year without any lock in periodCitizen of foreign state - not of Pakistan, Bangladesh, Nepal, Bhutan

Has retired Has inherited assets from person resident in India Is widow of resident outside India and has inherited assets May remit unto US $ 1 million per calendar year on production of

documentary evidence

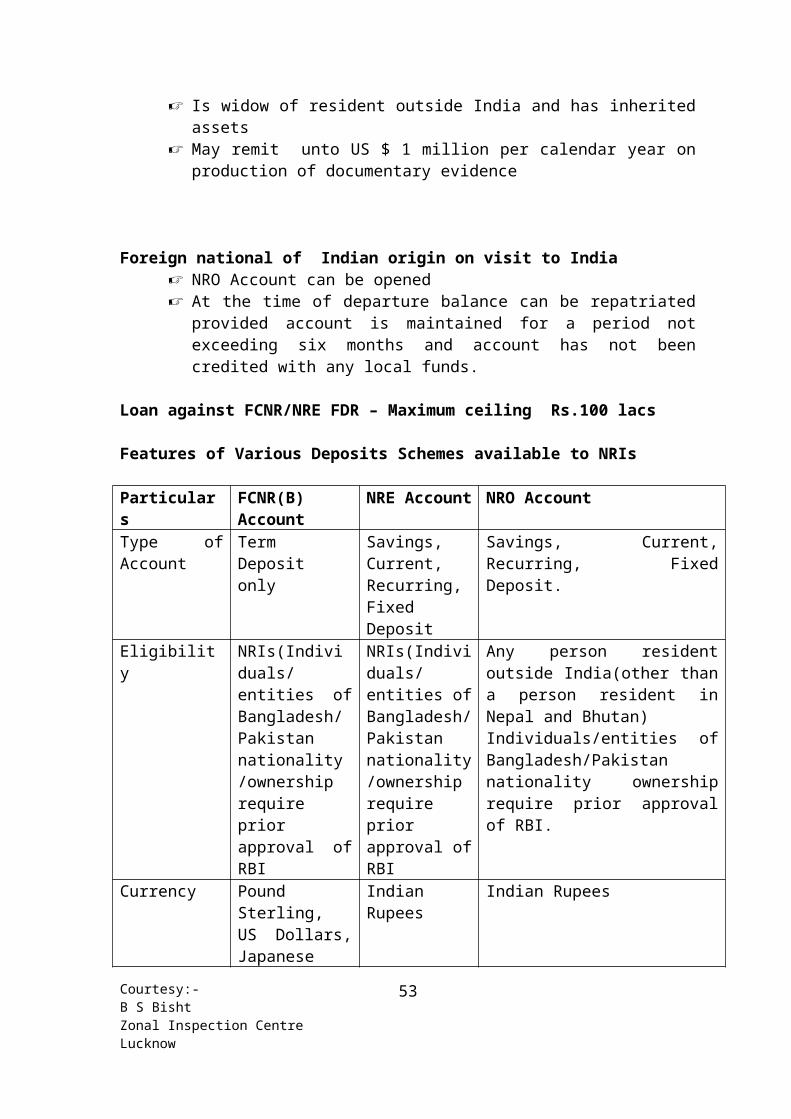

Foreign national of Indian origin on visit to India

Courtesy:-B S BishtZonal Inspection CentreLucknow

35

NRO Account can be opened At the time of departure balance can be repatriated provided account is

maintained for a period not exceeding six months and account has not been credited with any local funds.

Loan against FCNR/NRE FDR – Maximum ceiling Rs.100 lacs

Features of Various Deposits Schemes available to NRIs

Particulars FCNR(B) Account

NRE Account NRO Account

Type of Account

Term Deposit only

Savings, Current, Recurring, Fixed Deposit

Savings, Current, Recurring, Fixed Deposit.

Eligibility NRIs(Individuals/entities of Bangladesh/Pakistan nationality/ownership require prior approval of RBI

NRIs(Individuals/entities of Bangladesh/Pakistan nationality/ownership require prior approval of RBI

Any person resident outside India(other than a person resident in Nepal and Bhutan)Individuals/entities of Bangladesh/Pakistan nationality ownership require prior approval of RBI.

Currency Pound Sterling, US Dollars, Japanese Yen, Euro, Australian Dollar and Canadian Dollars

Indian Rupees Indian Rupees

Interest Subject of cap LIBOR/SWAP plus 100bps of respective currency/maturities

Fixed Deposit:-Subject to cap should not exceed LIBOR/Swap rates for US Dollars of corresponding maturity plus 175 basis points

Savings Bank:-Rate applicable to Domestic Savings Bank Account

Fixed Deposit:-Banks are free to determine interest rates

Savings Bank:-Rate applicable to Domestic Savings Bank Account

Courtesy:-B S BishtZonal Inspection CentreLucknow

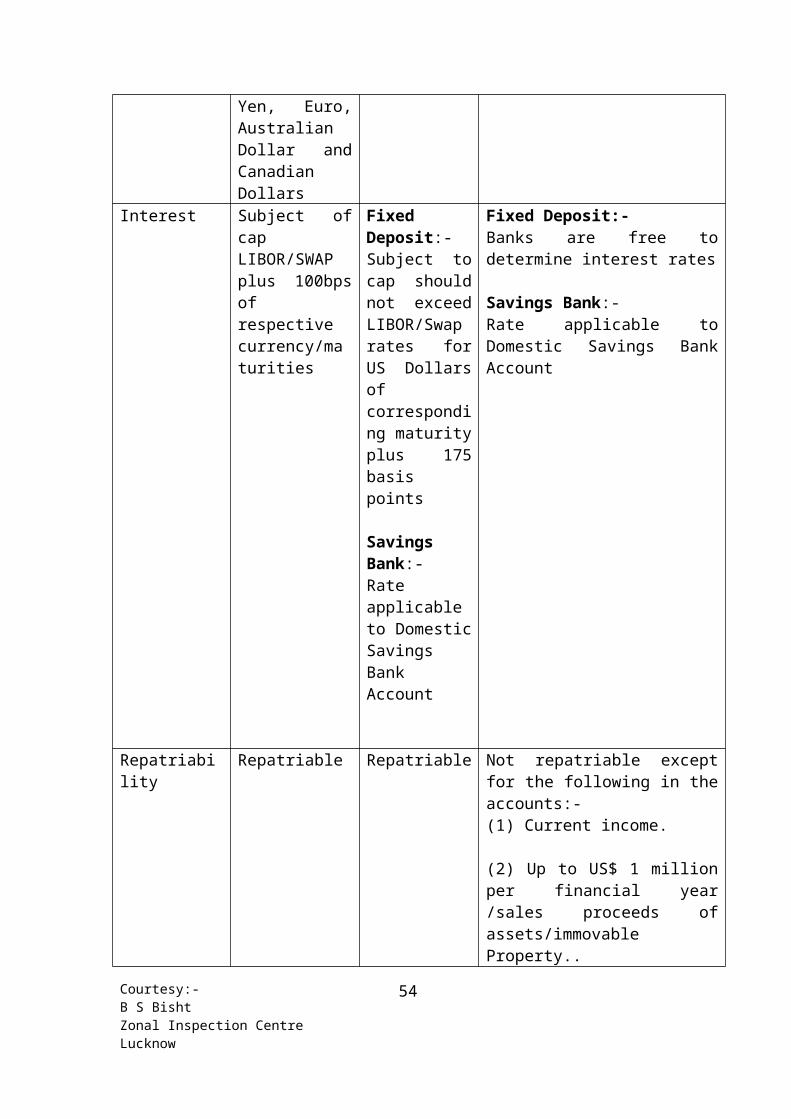

36

Repatriability Repatriable Repatriable Not repatriable except for the following in the accounts:-(1) Current income.

(2) Up to US$ 1 million per financial year /sales proceeds of assets/immovable Property..

Loan against FCNR/NRE Deposits

Max Rs100 lacs Max Rs100 lacs

When a person resident in India leaves India for Nepal and Bhutan for taking up employment or for carrying on business or vocation or for any other purposes indicating his intention to stay in Nepal and Bhutan for an uncertain period, his existing account will continue as a resident account. Such account should not be designated as on Resident (Ordinary) Rupee Account (NRO)

Authorised Dealers may open and maintain NRE/FCNR(B) accounts of persons resident in Nepal and Bhutan who are citizens of India or of Indian Origin, provided the funds for opening these accounts are remitted in freely convertible foreign exchange. Interest earned in NRE/FCNR(B) accounts can be remitted only in Indian Rupees to NRIs and Person of Indian Origin resident in Nepal and Bhutan

Authorised dealers may open and maintain Rupee accounts for a person resident in Nepal/Bhutan.

Courtesy:-B S BishtZonal Inspection CentreLucknow

37

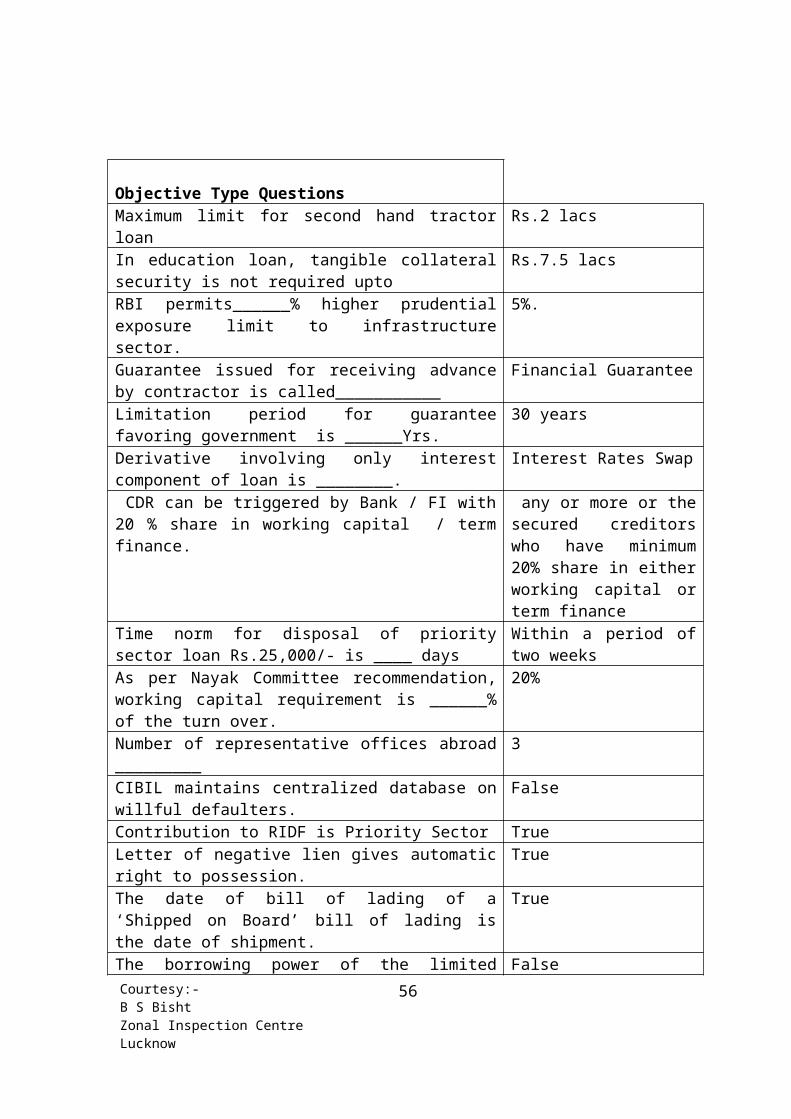

Objective Type QuestionsMaximum limit for second hand tractor loan Rs.2 lacsIn education loan, tangible collateral security is not required upto

Rs.7.5 lacs

RBI permits______% higher prudential exposure limit to infrastructure sector.

5%.

Guarantee issued for receiving advance by contractor is called___________

Financial Guarantee

Limitation period for guarantee favoring government is ______Yrs.

30 years

Derivative involving only interest component of loan is ________.

Interest Rates Swap

CDR can be triggered by Bank / FI with 20 % share in working capital / term finance.

any or more or the secured creditors who have minimum 20% share in either working capital or term finance

Time norm for disposal of priority sector loan Rs.25,000/- is ____ days

Within a period of two weeks

As per Nayak Committee recommendation, working capital requirement is ______% of the turn over.

20%

Number of representative offices abroad _________ 3CIBIL maintains centralized database on willful defaulters. FalseContribution to RIDF is Priority Sector TrueLetter of negative lien gives automatic right to possession. TrueThe date of bill of lading of a ‘Shipped on Board’ bill of lading is the date of shipment.

True

The borrowing power of the limited company are defined in its’ article of association.

False

OMNIBOB is a transaction based Internet Banking. FalseA substandard account referred to CDR becomes standard account.

False

Base Rateis based on cost of funds. TrueUnutilized portion of ceiling prescribed in investment in shares of previous financial year can be carried over.

False

Banks can sell goods under pledge without issuing notice to borrower / guarantor.

False

Fresh BP for adjustment of overdue BP is ever greening. TrueConfirming bank assumes the status of LC opening Bank. TrueFinancing of supply bill is through Receipted ChallanOperative limit in working capital is determined on the basis of

QIS

Adhoc becomes NPA when not Renewed within 180 days

Courtesy:-B S BishtZonal Inspection CentreLucknow

38

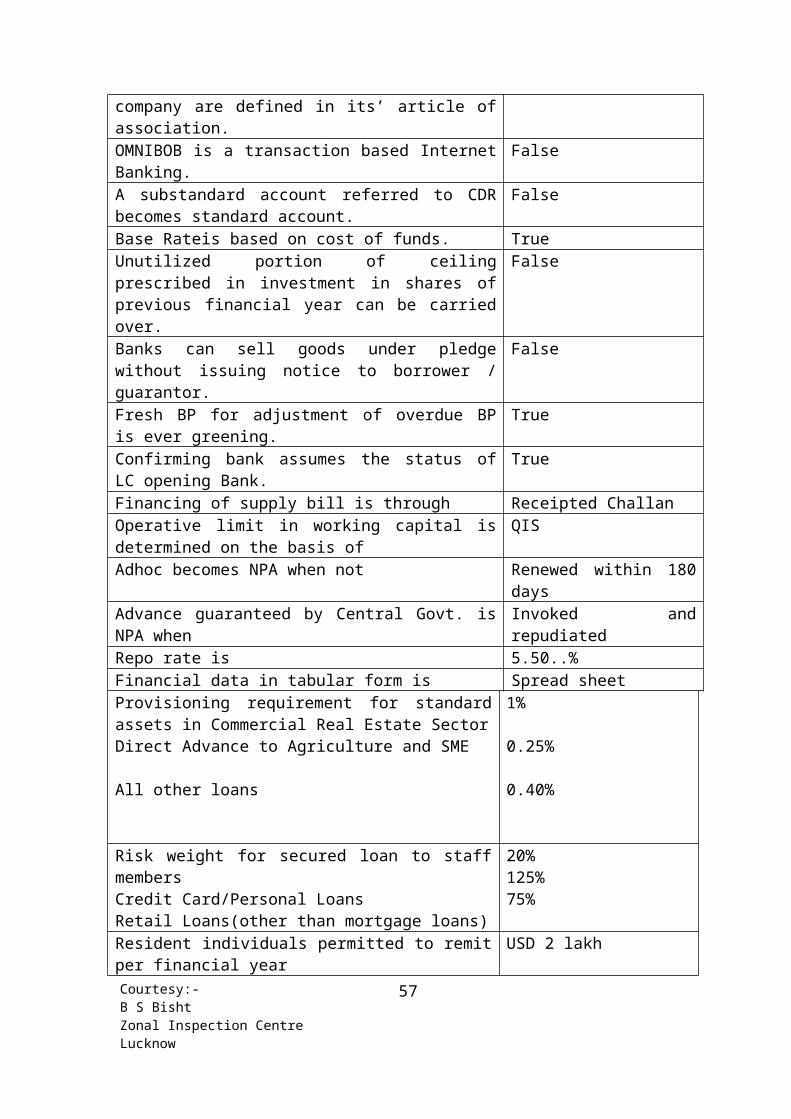

Advance guaranteed by Central Govt. is NPA when Invoked and repudiatedRepo rate is 5.50..%Financial data in tabular form is Spread sheetProvisioning requirement for standard assets in Commercial Real Estate SectorDirect Advance to Agriculture and SME

All other loans

1%

0.25%

0.40%

Risk weight for secured loan to staff membersCredit Card/Personal LoansRetail Loans(other than mortgage loans)

20%125%75%

Resident individuals permitted to remit per financial year USD 2 lakhInterest on CRR balance with RBI 0%Hypothecation has been defined under which act SARFAESI Act 2002Limitation period for demand loan 3 yearsSpecial mention accounts Which are overdue beyond

30daysCeiling on Investment in plant and machinery for Small Enterprises

Rs. 5 crore

ESOPs Employee stock option planMaximum amount for compensation that Ombudsman can award

Rs. 10 lakh

Courtesy:-B S BishtZonal Inspection CentreLucknow

39

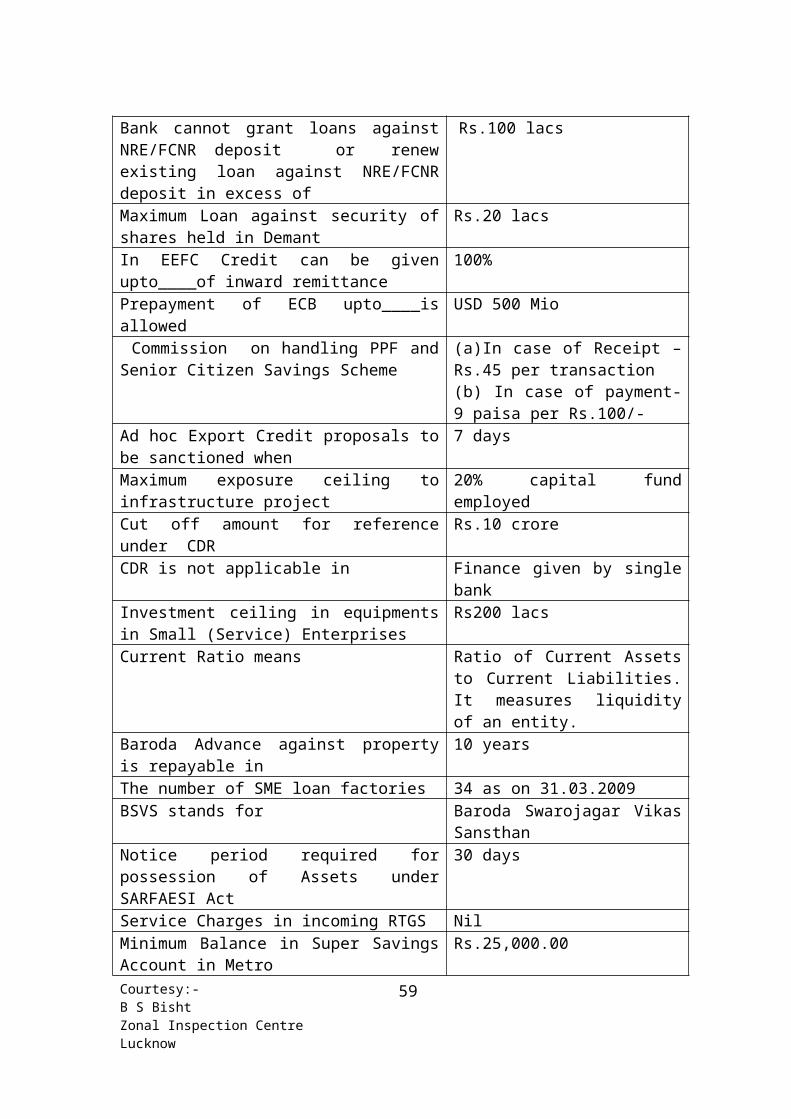

Bank cannot grant loans against NRE/FCNR deposit or renew existing loan against NRE/FCNR deposit in excess of

Rs.100 lacs

Maximum Loan against security of shares held in Demant

Rs.20 lacs

In EEFC Credit can be given upto____of inward remittance

100%

Prepayment of ECB upto____is allowed USD 500 Mio Commission on handling PPF and Senior Citizen Savings Scheme

(a)In case of Receipt –Rs.45 per transaction(b) In case of payment- 9 paisa per Rs.100/-

Ad hoc Export Credit proposals to be sanctioned when

7 days

Maximum exposure ceiling to infrastructure project

20% capital fund employed

Cut off amount for reference under CDR Rs.10 croreCDR is not applicable in Finance given by single bankInvestment ceiling in equipments in Small (Service) Enterprises

Rs200 lacs

Current Ratio means Ratio of Current Assets to Current Liabilities. It measures liquidity of an entity.

Baroda Advance against property is repayable in 10 yearsThe number of SME loan factories 34 as on 31.03.2009BSVS stands for Baroda Swarojagar Vikas SansthanNotice period required for possession of Assets under SARFAESI Act

30 days

Service Charges in incoming RTGS NilMinimum Balance in Super Savings Account in Metro

Rs.25,000.00

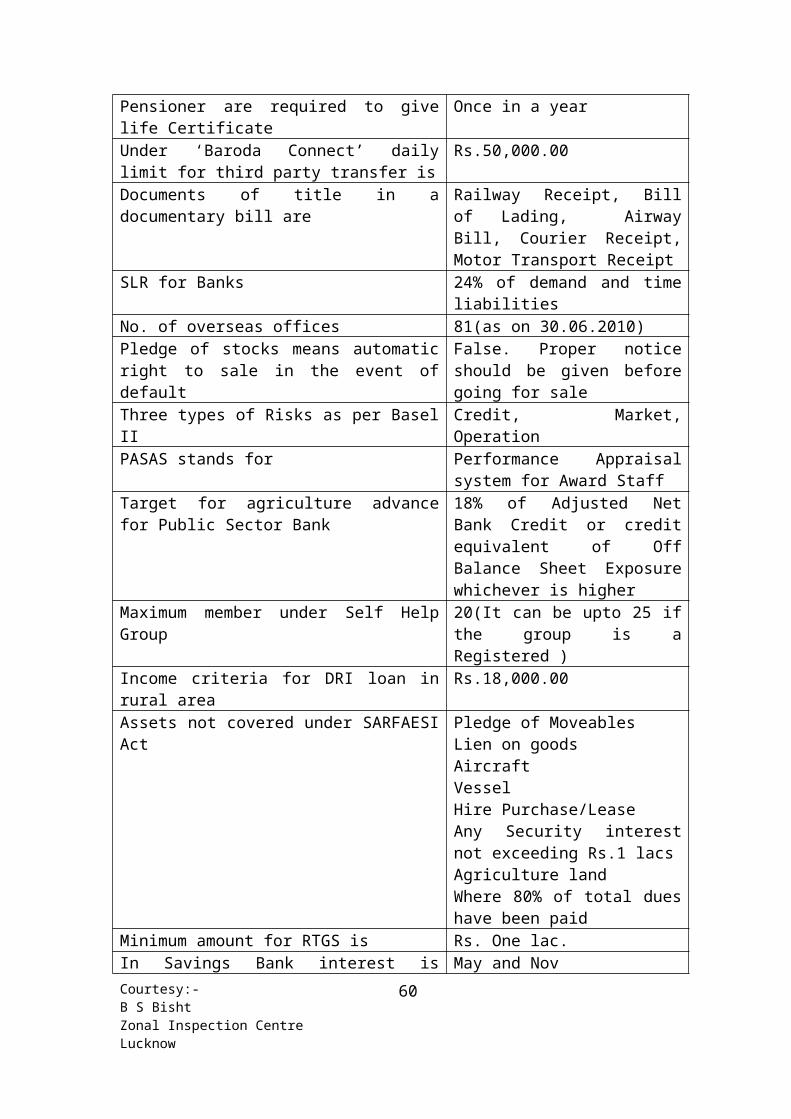

Pensioner are required to give life Certificate Once in a yearUnder ‘Baroda Connect’ daily limit for third party transfer is

Rs.50,000.00

Documents of title in a documentary bill are Railway Receipt, Bill of Lading, Airway Bill, Courier Receipt, Motor Transport Receipt

SLR for Banks 24% of demand and time liabilitiesNo. of overseas offices 81(as on 30.06.2010)Pledge of stocks means automatic right to sale in the event of default

False. Proper notice should be given before going for sale

Three types of Risks as per Basel II Credit, Market, OperationPASAS stands for Performance Appraisal system for

Award StaffTarget for agriculture advance for Public Sector Bank

18% of Adjusted Net Bank Credit or credit equivalent of Off Balance Sheet Exposure whichever is

Courtesy:-B S BishtZonal Inspection CentreLucknow

40

higher Maximum member under Self Help Group 20(It can be upto 25 if the group is

a Registered )Income criteria for DRI loan in rural area Rs.18,000.00Assets not covered under SARFAESI Act Pledge of Moveables

Lien on goodsAircraftVesselHire Purchase/LeaseAny Security interest not exceeding Rs.1 lacsAgriculture landWhere 80% of total dues have been paid

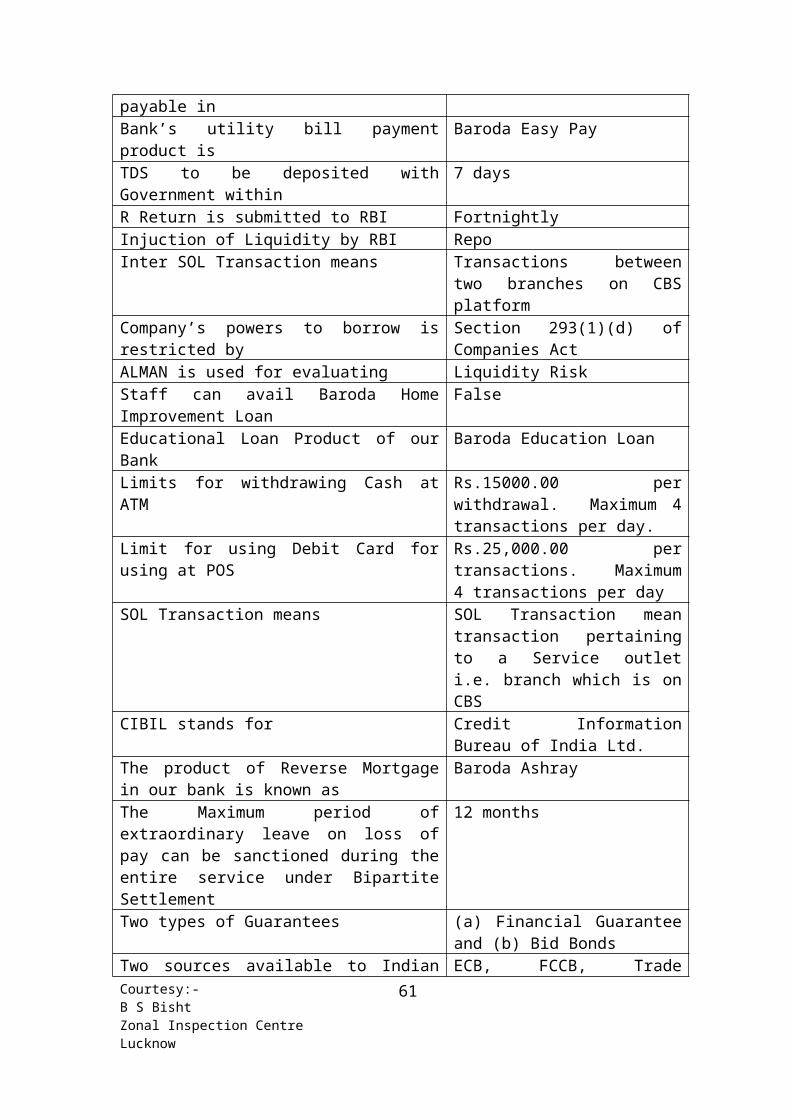

Minimum amount for RTGS is Rs. One lac.In Savings Bank interest is payable in May and NovBank’s utility bill payment product is Baroda Easy PayTDS to be deposited with Government within 7 daysR Return is submitted to RBI FortnightlyInjuction of Liquidity by RBI RepoInter SOL Transaction means Transactions between two branches

on CBS platformCompany’s powers to borrow is restricted by Section 293(1)(d) of Companies

ActALMAN is used for evaluating Liquidity RiskStaff can avail Baroda Home Improvement Loan FalseEducational Loan Product of our Bank Baroda Education LoanLimits for withdrawing Cash at ATM Rs.15000.00 per withdrawal.

Maximum 4 transactions per day.Limit for using Debit Card for using at POS Rs.25,000.00 per transactions.

Maximum 4 transactions per day SOL Transaction means SOL Transaction mean transaction

pertaining to a Service outlet i.e. branch which is on CBS

CIBIL stands for Credit Information Bureau of India Ltd.

The product of Reverse Mortgage in our bank is known as

Baroda Ashray

The Maximum period of extraordinary leave on loss of pay can be sanctioned during the entire service under Bipartite Settlement

12 months

Two types of Guarantees (a) Financial Guarantee and (b) Bid Bonds

Two sources available to Indian Corporate to raise resources from overseas markets

ECB, FCCB, Trade Credit, ADRs, GDRs

Software used for processing text document MS Word or Lotus Word ProGold coin sold by bank have purity level of 24 karat 999.9 purePunishment prescribed under Section 138 of (a) Twice the amount of cheque (b) Courtesy:-B S BishtZonal Inspection CentreLucknow

41

Negotiable Instrument Act Imprisonment upto 2 years and/or both

Interest payable on CRR maintained by the Bank is

Zero

Bank Rate 6% ( 30.06.2010)CRR 6% (30.06.2010)Reverse Repo 4%(30.06.2010)TDS on interest payable on NRO deposit 30% plus education cess 0.90%

However, countries where we have agreement on Avoidance of Double Taxation(ADT), TDS ranges from 10% to 20%.

Margin on Property mortgaged in Baroda Traders Loan A/c

40% on the value of immovable property

Quarterly Average Balance required to be maintained in Savings Bank A/c

Rs. 500.00 in rural and semi urban areas and Rs.1000.00 in Urban and Metro areas

Quarterly Average Balance in Current A/c (General)

Rs.1000.00 in rural and semi urban areas and Rs.10,000.00 in Urban and Metro areas.

Courtesy:-B S BishtZonal Inspection CentreLucknow

42

To Ensure Customer Service – seek answers to questions like:-

Who are our customers in terms of income levels, balance maintained etc.?

Who are our profitable customers? Who are our aggrieved customers? How quickly do we redress the complaints? Which products our customers want more than the others? Which services are delivered efficiently & which are not? Can we serve the customers in a more cost-effective manner? Are all our customers aware about alternate delivery channels? Do our customers have problems in accessing our delivery

channels? Do we offer good ambience to our customers? Do we have effective channels to communicate important

changes, new products, pricing etc. to our customers? Do we seek new contacts through our existing customers? Do we cross sell loan / third party products to existing

customers? Do we know our potential customers? Do we have action plan and timelines for adding new customers?

Strategies for Resource Mobilization:

Focus area should be CASA deposits. Consistent growth in CASA will continue should be the hallmark of our deposit growth strategy.

Branch specific strategies to be chalked out to ensure growth in CASA. Rural and Semi-urban branches should provide special focus for Savings Bank Deposits. Metro and Urban branches to concentrate on Current and Savings Bank Deposits.

Branches in Residential areas should take challenging targets for canvassing Savings Bank deposits due to their locational advantage. Similarly market area branches to be guided to canvass higher current account deposits.

As a principal strategy Corporates to be approached for Salary accounts with a bouquet of services such as home loans, e-banking, anywhere banking etc.

Branches have been provided with the list of current account holders having balances of Rs 2.50 lacs and above. These customers should be contacted at regular intervals not only to ensure increase in such deposits but to mobilize additional business through upselling and cross selling and also generating non-fund based business.

Accounts having balances of Rs 5 lacs and above in Savings Bank should be personally monitored by the Branch Managers.

Courtesy:-B S BishtZonal Inspection CentreLucknow

43

Branches, supplemented by marketing teams, to adopt sales and marketing as a regular activity for client acquisition.

New client focus in marketing to be on HNIs, holding potential of large balances.

Alternate delivery channels like ATMs, Debit Cards, Mobile Banking, SMS Banking etc. should be popularized. Debit Cards, ATM cards and facility of Baroda Connect should invariably be provided to all active Savings Bank customers.

Specialised NRI branches and branches having NRE Cells should be given higher targets to canvass NRI deposits in keeping with our strong foothold abroad.

Campaigns for Savings Bank Accounts and Current Accounts should be organized on regular basis.

Holding regular customer-meets will help branches in redressing the grievances of the customers as well as help in making close contacts with the existing and potential customers.

Branches to seek referrals for new clients from existing good customers. Visits to be constantly followed up by phone/letter/e-mail/further visits.

Customer satisfaction survey to be carried out. Regular customer meets every month in which different

customers be called each time.

Strategies for SME Banking:

At present Bank is having 35 SME Loan factories, which should be re-invigorated to increase SME advances. The sanctions accorded by the SMELF should be disbursed at the earliest.

Separate targets should be allocated to SMELF for fund based and non-fund based advances.

Cluster approach for financing under specific scheme should be given boost in Gujarat, Rajasthan, Greater Mumbai and Southern Zone.

Bank has signed -5- MOUs with various reputed organizations and companies to increase SME advances. Opportunities arising from such alliances should be explored fully.

Bank has already announced relief measures to be considered on a case to case basis such as reduction in margin money, allowing drawing against domestic receivables, extending moratorium and sanctioning additional limit for WCDL etc. This will provide necessary boost to the SME segment.

Good cooperation and collaboration between SMELFs and concerned branches to ensure best delivery to customers.

Strategies for Rural & Agri Banking:

Courtesy:-B S BishtZonal Inspection CentreLucknow

44

Launching campaigns for production and investment credit. Formulating Area Specific Schemes. During the year 2008-09, Bank

introduced scheme for financing farmers of sugar cane for Uttar Pradesh, Northern Zone and Maharastra and Goa Zone. More such schemes to be launched during the year.

Exploring the possibilities of tie-ups with Agro Processing Units for financing farmers.

Organising Conclaves/ Workshops of field functionaries to sensitize them for achieving better growth in agriculture advances.

Organising Mega Credit Camps/ Credit Camps to give desired boost to the growth of advances.

Conducting special training programmes to upgrade the credit skills of the officers.

Exploring the possibility of opening special agriculture-thrust branches.

Taking benefit of Agriculture Rural Debt Relief scheme. It has to be exploited properly to increase our agriculture lending.

Strategies for Retail Credit

Line functionaries should familiarize themselves with the new product basket and aggressively canvass retail business.

Bank has entered into a tie up with Maruti Suzuki India Ltd., Mahindra & Mahindra, Tata Motors and Hyundai Motors India Ltd. at corporate level for boosting the sale of Car Loan portfolio. Opportunities arising from such tie up should be explored fully.

There is a huge un-satiated demand for home loans. The easy liquidity and supportive policy prescriptions have created a conducive environment for increasing the home loan portfolio. What is required is a planned strategy to tap the business potential. HNIs, higher income earning employees of PSUs & Corporate Firms should be targeted.

Retail Loan festival campaigns should be launched to increase the Retail Loan portfolio.

Retail Loan factories to form dedicated teams specialising in home loans.

Strategies for increasing Non Interest Income

CFS and Mid-Corporate branches need to focus on LC/BG commission,

Market area branches should focus on income from remittances. Officers to be deputed to large corporates / PSEs with a solitary aim

of canvassing LC / BG business and giving them specific targets. CFS and other large branches must aim to get at least our

proportionate share of non-fund based business (in the consortium/ multiple banking) – vis-à-vis sanctioned limits and utilization.

Concessions in charges to be regulated / conservatively given. Courtesy:-B S BishtZonal Inspection CentreLucknow

45

Existing charges to be reviewed as these NFB facilities also attract Capital adequacy norms.

Ensure maximum recovery in PWO Accounts We should have a focused approach for increasing Turnover in Govt.

Business. Timely remittance of funds collected under Govt. Business in order to avoid penalty. Popularize e-payment facility. It provides excellent opportunities for canvassing high net worth tax assesses. Tapping pension accounts.

Need to concentrate on Profits fro Forex Transaction Income from sale of third party products and Gold coins is another

important area where innovative strategies need to be tried out. We cannot afford to lose income through revenue leakages. Ensure

that human negligence does not get the better of Bank’s legitimate revenue.

Strategies for Wealth Management Business:

Sales team of IRDA/AMFI certified staff to be deployed in a strategic manner at some target branches.

To collaborate with Asset Management Companies for mutual fund products to enhance product offerings.

Bank to launch its own e-trading platform for offering 3-in-1 (Savings/demat/trading) account during the year (through BOB capital).

To endeavour to become clearing and settlement banker for NSE and MCX.

Strategies for NPA Management:-

Identified Recovery Champions should be given challenging targets for recovery. They should make continuous follow up with the borrowers to canvass compromise proposals.

Special drive should be launched for Recovery of NPAs. Recovery camps should be organized to give boost to the recovery drive.

Lok Adalats should be periodically convened to quickly settle the cases and recover the due amount.

Wherever notice has been issued under SARFAESI Act, all-out efforts should be made to take possession of the assets.

Branches having NPAs of below Rs 5 lacs, should be converted into ‘Zero NPA’ branches.

Sale of assets on individual and portfolio basis should be taken up on priority basis.

Canvass maximum compromise proposals under Bank’s OTS scheme.

Targets of recovery in Prudential Write off (PWO) should be allotted to identified Recovery champions at branch level to recover as much as possible in view of huge sum of money lying outstanding in these accounts.

Courtesy:-B S BishtZonal Inspection CentreLucknow

46

Restructuring of accounts in eligible cases to be undertaken on case to case basis.

Customer Service Orientation:-

Be easily accessible to customers at all levels. Manager and other key functionaries to regularly interact with

customers. In all medium & bigger branches a floor manager to regularly

monitor and help smooth flow of transactions and guide the customers.

Zero tolerance for ill behaviour with customers. Front-end staff to be pleasant, smiling and proactive.

Steps initiated by Bank towards Harnessing Human Capital:-

Bank has taken a series of HR initiatives like a record number of promotions, extending pecuniary benefits, proper placements and postings, employee empowerment through internal and external trainings, strong succession planning, lateral recruitment of talent from market and improved communication across the organization. In addition to the above, Bank has taken forward the technology-based Business Transformation Process by operationalising many more projects which will bring convenience not only to the customers but also improve productivity of employees of the Bank. The Management has been constantly working towards creating a congenial working environment in the Bank to enhance operational efficiency and employee productivity.

How to increase Savings Bank Portfolio:

Quality Savings Bank Accounts Tell the customer about our more than 1950 CBS Branches

Customer should be made aware of our various other delivery channels such as e banking, On line payment of indirect taxes and e- payment services, RTGS, NEFT, Debit Cards, SMS Alerts and large number of ATMs create competive advantage and increase our customer base

Mobilize quality SB Accounts

Corporate Salary Accounts

Popularize ‘Baroda Bachat Mitra’ which enables OD against Time Deposit in Savings Bank A/c

Targets – Big and Mid companies, Corporate Salary Accounts, Teacher, Doctors, Business persons, Big farmers

Courtesy:-B S BishtZonal Inspection CentreLucknow

47

Incentives – Free Accident insurance cover up to Rs. 1 lac for one year, Free Debit Card, Free E banking

Demonstrate our dedication and devotion to organization.

Take this challenge and make camapaign splendid success