capital markets industry insights - q4 2015

TRANSCRIPT

Industry Insights:

Capital Markets

Q4 2015

Highlights

Credit market conditions continue to be compelling for middle market issuers in spite of recent capital markets volatility.

While credit standards have tightened for middle market issuers, the effect has been quite modest relative to corrections in the commodity, equity and high yield markets.

Investor composition is evolving…commercial banks and BDCs are curtailing activity while non-banks and credit funds are filling the void.

Structural protections typical of private financings represent heightened value relative to “covenant light” structures.

With the “normalization” of monetary policy having begun in December, the pace and magnitude of subsequent rate hikes have become topics of prime focus among market participants.

The availability of attractively priced and structured credit for middle market transactions continued largely unabated in the fourth quarter. The market experienced 1) a modest increase in pricing and 2) a tightening of leverage parameters, but far less so than we observed with respect to large cap transactions. Macroeconomic conditions continued to be strong domestically (notably, labor market conditions), though heightened geopolitical concerns and the dramatic downturn in commodity prices tempered risk appetite.

We noted a significant bifurcating of underwriting standards among institutional genres this quarter. Commercial bank appetite moderated, both in terms of bite size and volume, as did BDC appetite. Conversely, non-banks and credit funds stepped up to fill the void and, at this writing, represent the more compelling credit sources in the middle market.

Market participants were, and remain, laser focused on domestic monetary policy and Federal Reserve actions. While the inaugural rate hike that occurred in December was almost universally

anticipated, the pace and magnitude of subsequent hikes is far less certain. Though a base case expectation of cumulative 100 basis point increases in each of the next two years has been communicated by the Fed, the overarching qualifier of “data dependency” introduces a nontrivial element of ambiguity that will keep credit market participants on edge.

In summary, we anticipate a continued strong credit environment for middle market issuers contemplating refinancings, acquisition financings, leveraged recapitalizations and leveraging for growth. We observed 1) the cost of floating rate debt corrected this past quarter by approximately 50 basis points, representing a combination of base rate increase and spread widening, and 2) senior leverage multiples tightened by one quarter to one half a turn. We noted no material correction in fixed rate subordinated debt pricing nor in total leverage appetite. Relative to the far more significant corrections experienced in the large cap market, as well as in the equity and commodity markets, we believe the credit markets represent a compelling financing opportunity for middle market issuers.

Capital Markets Industry Insights – Q4 2015

Executive Summary

Duff & Phelps 2

Indicative Middle Market Credit Parameters

Leverage Multiples EBITDA of $10MM - $20MM EBITDA of $20MM - $50MM

Senior Debt 2.25x - 3.25x 2.50x - 3.75x

Total Debt 3.50x - 4.25x 3.75x - 4.50x

Pricing EBITDA of $10MM - $20MM EBITDA of $20MM - $50MM

First Lien Libor + 3.00% - 4.00% (bank) Libor + 4.00% - 6.00% (non-bank)

Libor + 2.75% - 3.50% (bank) Libor + 4.00% - 6.00% (non-bank)

Second Lien Libor + 6.50% - 9.50% Libor + 6.00% - 9.00%

Subordinated Debt 11.00% - 13.00% 10.00% - 12.00%

Unitranche Libor + 6.00% - 8.50% Libor + 5.50% - 8.00%

New Issuance

Primary issuance volume of leveraged loans and, in particular, high yield bonds declined significantly in the fourth quarter. Many investors took a wait-and-see approach due in large part to uncertainty about the timing of Fed policy actions and a perceived decline in secondary market liquidity.

0

50

100

150

4Q15

3Q15

2Q15

1Q15

4Q14

3Q14

2Q14

1Q14

4Q13

3Q13

2Q13

1Q13

4Q12

3Q12

2Q12

1Q12

50

150

250

350

450

Total Bond Volume ($B) Number of Deals

121.0

314

79.6

296

133.0

349107.7

321

111.2

322

116.3

333

105.2

263

90.3

279

88.1

259

122.1

370 102.6

286

90.9

257

114.0

295

104.8

27882.6

195

48.1

131

Total High-Yield Bond Issuance

Total Loan Issuance

Duff & Phelps 3

0

50

100

150

200

250

300

350

400

4Q15

3Q15

2Q15

1Q15

4Q14

3Q14

2Q14

1Q14

4Q13

3Q13

2Q13

1Q13

4Q12

3Q12

2Q12

1Q12

200

400

600

800

1000

149.7

414

229.2

485

295.5

623

147.3

462

268.7

727233.5

703

291.2

786

284.8

713

287.4

794

231.1

689

346.9

797

346.4

675

255.1

728

147.0

484

169.3

530161.1

516

Total Loan Volume ($B) Number of Deals

Source: SDC Platinum

Source: SDC Platinum

Capital Markets Industry Insights – Q4 2015

New Issuance - Continued

Duff & Phelps 4

Total Loan Issuance (EBITDA < $50MM)Issuance in the energy and power sector essentially ground to a halt this quarter—a decline of 81% on the quarter and 43% for the year—as commodity market conditions became increasingly problematic for producers and service providers. Further, collateral base redeterminations triggered credit line downsizings throughout the sector.

0

50

100

150

200

250

4Q15

3Q15

2Q15

1Q15

4Q14

3Q14

2Q14

1Q14

4Q13

3Q13

2Q13

1Q13

4Q12

3Q12

2Q12

1Q12

Total Loan Volume ($B) Number of Deals

420 441

396

544

666

575

653

595

661

601

380

500

420

351

200

400

600

800

92.2

110.8

86.0

155.1

225.0217.0

139.3

185.6 194.5 195.9

154.6 152.3

80.0

157.5

136.2

97.5

613 604

Source: SDC Platinum

U.S. High Yield Bonds by Industry

Total Volume ($B)

0.0

30.0

60.0

90.0

120.0

Financials

Energy and Power

Healthca

re

Industrials

Materials

Consumer S

taples

Consumer P

roducts

and Services

Telecommunica

tions

Retail

Real Esta

te

Media and

Entertainment

High Technology

20142015

Source: SDC Platinum

Capital Markets Industry Insights – Q4 2015

Yield (%)

4.5

5.5

6.5

7.5

9.5

8.5

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jan-16Jul-15

Barclays U.S. Corporate High YieldS&P/LSDA U.S. Leveraged Loan 100

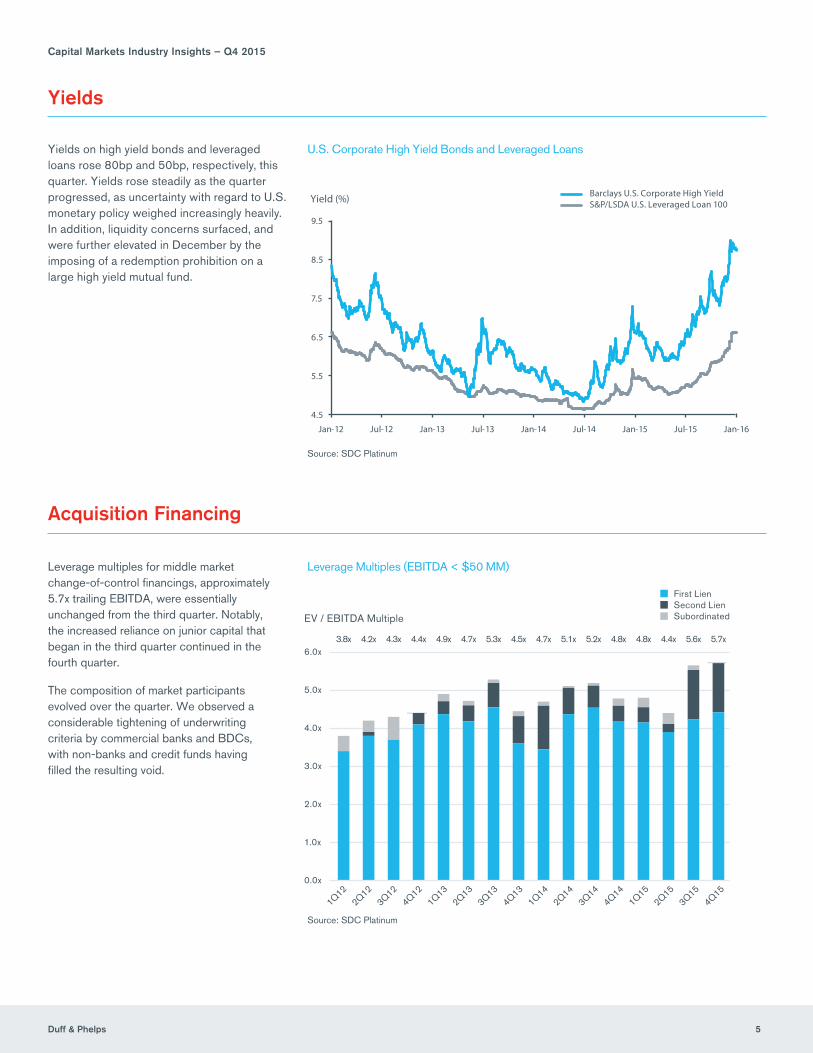

Yields

Yields on high yield bonds and leveraged loans rose 80bp and 50bp, respectively, this quarter. Yields rose steadily as the quarter progressed, as uncertainty with regard to U.S. monetary policy weighed increasingly heavily. In addition, liquidity concerns surfaced, and were further elevated in December by the imposing of a redemption prohibition on a large high yield mutual fund.

Source: SDC Platinum

Duff & Phelps 5

U.S. Corporate High Yield Bonds and Leveraged Loans

Acquisition Financing

Leverage multiples for middle market change-of-control financings, approximately 5.7x trailing EBITDA, were essentially unchanged from the third quarter. Notably, the increased reliance on junior capital that began in the third quarter continued in the fourth quarter.

The composition of market participants evolved over the quarter. We observed a considerable tightening of underwriting criteria by commercial banks and BDCs, with non-banks and credit funds having filled the resulting void.

Leverage Multiples (EBITDA < $50 MM)

4Q153Q15

2Q151Q15

4Q143Q14

2Q141Q14

4Q133Q13

2Q131Q13

4Q123Q12

2Q121Q12

3.8x 4.2x 4.3x 4.4x 4.9x 4.7x 5.3x 4.5x 4.7x 5.1x 5.2x 4.8x 4.8x 4.4x 5.6x 5.7x

EV / EBITDA Multiple

First LienSecond LienSubordinated

0.0x

1.0x

2.0x

3.0x

4.0x

5.0x

6.0x

Source: SDC Platinum

Capital Markets Industry Insights – Q4 2015

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

0.0%

1.0%

2.0%

3.0%

4.0%

Yield (%)

10 year

2 year

5 year

100

150

200

250

300

Jan-12 Jul -12 Jan-13 Jul -13 Jan-14 Jul -14 Jan-15 Jan-16Jul -15

Spread (bps)

Macroeconomic Update

The US economy continued to demonstrate consistent, though modest, growth fostered most notably by accommodative monetary policy. Labor market conditions were particularly affirming. Equity markets recovered from a downturn in the third quarter, with the S&P 500 rising 8.5% in the fourth quarter.

Evolving monetary policy, commodity price volatility and geopolitical events all garnered keen attention from market players this quarter.

The Federal Reserve’s decision to begin the process of monetary policy “normalization” was a seminal event this quarter. The increase in the Fed Funds Rate target that occurred on December 16th, and the anticipation of subsequent rate hikes over the next two years, triggered a flattening of the yield curve and a modest rise in all-in yields on floating rate debt.

Source: Bloomberg

Source: Bloomberg

2 Year vs. 10 Year Treasury Spread

2, 5 and 10 Year Treasury Yields

Duff & Phelps 6

Capital Markets Industry Insights – Q4 2015

Macroeconomic Update - Continued

Source: Capital IQ

U.S. Employment

Global Commodity Indices

Duff & Phelps 7

Commodities continued to suffer dramatic price declines, reflecting worries about global growth prospects. In 2015, copper prices declined by 39.5%, crude by 64.0%, and coal by 92.3%. The accelerated decline in crude prices in recent weeks also reflects anticipated supply growth, triggered in no small part by OPEC’s December 4th decision to increase production.

In addition, concerns about a slowdown of growth in China, foreign policy tensions with Iran and Russia, and acts of terrorism all warranted concern by market participants.

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

5.0%

4.0%

6.0%

7.0%

9.0%

8.0%

Unemployment Rate

0

100

200

300

400

500

Jobs Added (thousands)

Source: Federal Reserve

Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

(100.0%)

(80.0%)

(60.0%)

(40.0%)

(20.0%)

0.0%

20.0%

Dow Jones U.S. Coal IndexS&P GSCI Crude Oil IndexS&P GSCI Copper Index

Capital Markets Industry Insights – Q4 2015

Conclusion

Duff & Phelps 8

The availability of attractively priced and structured credit for middle market transactions continued largely unabated in the fourth quarter. While credit standards tightened modestly, agregate demand for new issuance was robust. Demand was particularly strong among non-banks and credit funds, while commercial bank and BDC appetite waned. We are mindful, however, of potential headwinds, most notably regarding volatility in the equity and commodity markets and the pace at which accommodative monetary policy is unwound.

Capital Markets Industry Insights – Q4 2015

For more information please visit: www.duffandphelps.com

About Duff & PhelpsDuff & Phelps is the premier global valuation and corporate finance advisor with expertise in complex valuation, dispute and legal management consulting, M&A, restructuring, and compliance and regulatory consulting. The firm’s more than 2,000 employees serve a diverse range of clients from offices around the world.

M&A advisory and capital raising services in the United States are provided by Duff & Phelps Securities, LLC. Member FINRA/SIPC. Pagemill Partners is a Division of Duff & Phelps Securities, LLC. M&A advisory and capital raising services in the United Kingdom and Germany are provided by Duff & Phelps Securities Ltd., which is authorized and regulated by the Financial Conduct Authority.

Duff & Phelps Copyright © 2016 Duff & Phelps LLC. All rights reserved.

Michael BrillHead of U.S. Private Capital Markets+1 212 871 [email protected]

Bob Bartell, CFAGlobal Head of Corporate Finance +1 312 697 [email protected]

Steve BurtGlobal Head of M&A+1 312 697 [email protected]

Dave AlthoffGlobal Co-head of Industrials M&A+1 312 697 [email protected]

Josh Benn Global Head of Consumer, Retail, Food, and Restaurants+1 212 450 [email protected]

Brian CullenHead of U.S. Restructuring+1 424 249 [email protected]

Brooks DexterGlobal Head of Healthcare M&A+1 424 249 [email protected]

Ross FletcherHead of Canada M&A +1 416 361 [email protected]

Brian PawluckManaging Director, Canada Restructuring+1 416 364 [email protected]

Kevin IudicelloManaging Director, Technology M&A+1 650 354 [email protected]

Jon MelzerGlobal Co-head of Industrials M&A+1 212 450 [email protected]

Jim RebelloGlobal Head of Energy M&A+1 713 986 [email protected]

Contact Us