capital market day - · pdf fileprocess technology division agri ... procter & gamble...

TRANSCRIPT

Capital Market DayOctober 9th, 2002Our brand is about performance

Sigge HaraldssonPresident and CEOAlfa Laval Group

© Alfa Laval Slide 3 www.alfalaval.com

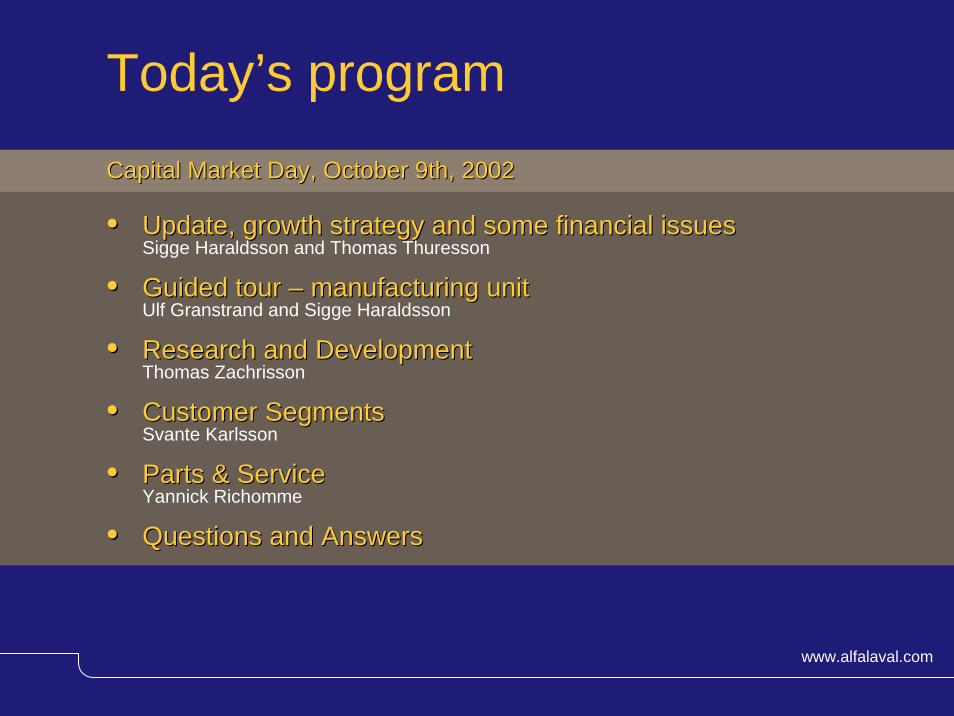

Today’s programCapital Market Day, October 9th, 2002Capital Market Day, October 9th, 2002

•• Update, growth strategy and some financial issuesUpdate, growth strategy and some financial issuesSigge Haraldsson and Thomas Thuresson

•• Guided tour Guided tour –– manufacturing unitmanufacturing unitUlf Granstrand and Sigge Haraldsson

•• Research and DevelopmentResearch and DevelopmentThomas Zachrisson

•• Customer Customer SSegmentsegmentsSvante Karlsson

•• Parts & ServiceParts & ServiceYannick Richomme

•• Questions and AnswersQuestions and Answers

© Alfa Laval Slide 4 www.alfalaval.com

Q302 Interim Report

•• Release 7:30 AM CET, October 31Release 7:30 AM CET, October 31stst..

•• RoadshowRoadshow, Stockholm, London and Copenhagen, Stockholm, London and Copenhagen

October October 3131stst 09:00 AM CET 09:00 AM CET Group breakfast in StockholmGroup breakfast in Stockholm, , including conference callincluding conference call

October October 3131stst 04:00 PM CET04:00 PM CET Conference callConference call

November 1November 1stst 12:30 AM GMT 12:30 AM GMT Group lunch in LondonGroup lunch in London

© Alfa Laval Slide 5 www.alfalaval.com

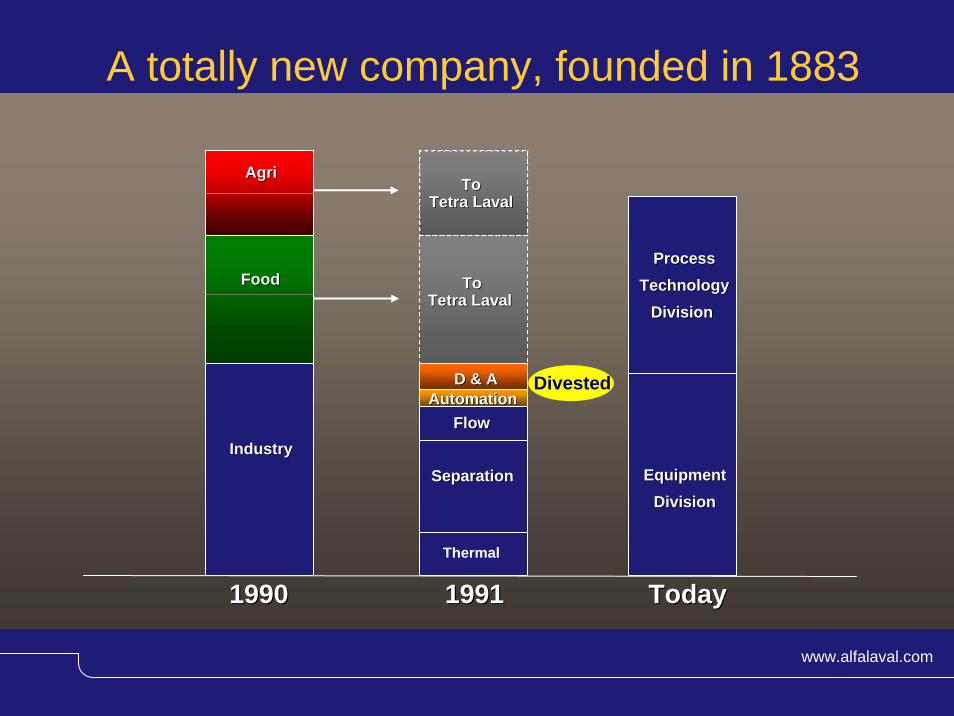

A totally new company, founded in 1883

Thermal

EquipmentEquipmentDivisionDivision

Industry Industry

Separation Separation

FoodFoodProcessProcess

TechnologyTechnologyDivisionDivision

AgriAgri

Flow Flow AutomationAutomation

D & AD & A Divested

To To Tetra Laval Tetra Laval

19901990 19911991 TodayToday

ToToTetra Laval Tetra Laval

© Alfa Laval Slide 6 www.alfalaval.com

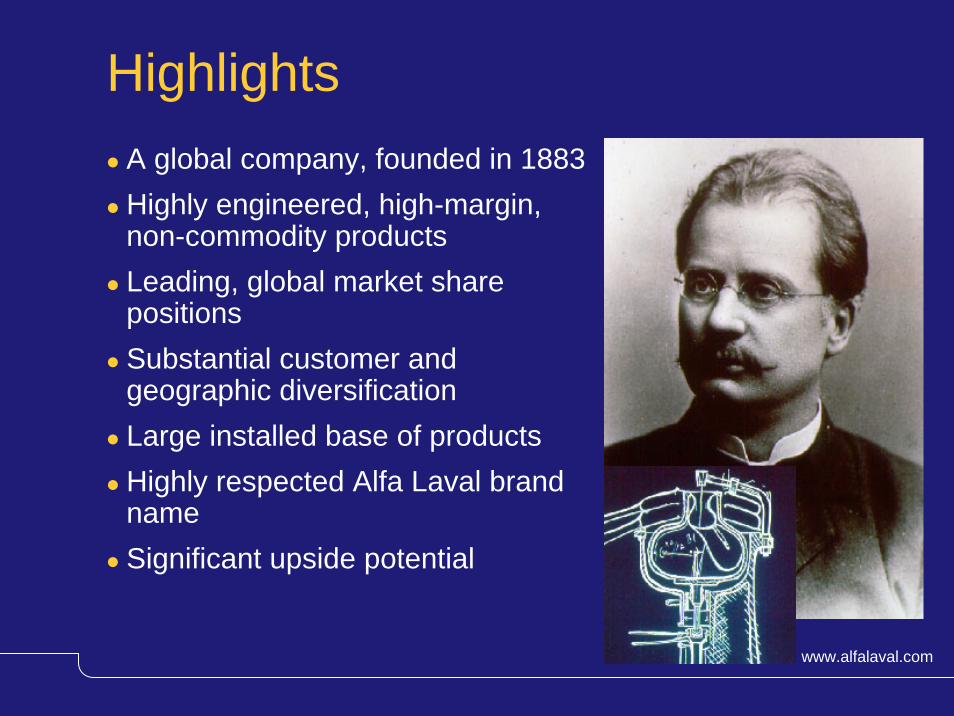

HighlightsA global company, founded in 1883Highly engineered, high-margin, non-commodity productsLeading, global market share positionsSubstantial customer and geographic diversificationLarge installed base of productsHighly respected Alfa Laval brand nameSignificant upside potential

© Alfa Laval Slide 7 www.alfalaval.com

A global company

Year 200Year 20011

• Total sales: MSEK 15,830• No. of employees: 9,259• 20 production units• 70 service centres• Sales Companies in 50 countries • Other sales representation in more than 45 countries

© Alfa Laval Slide 8 www.alfalaval.com

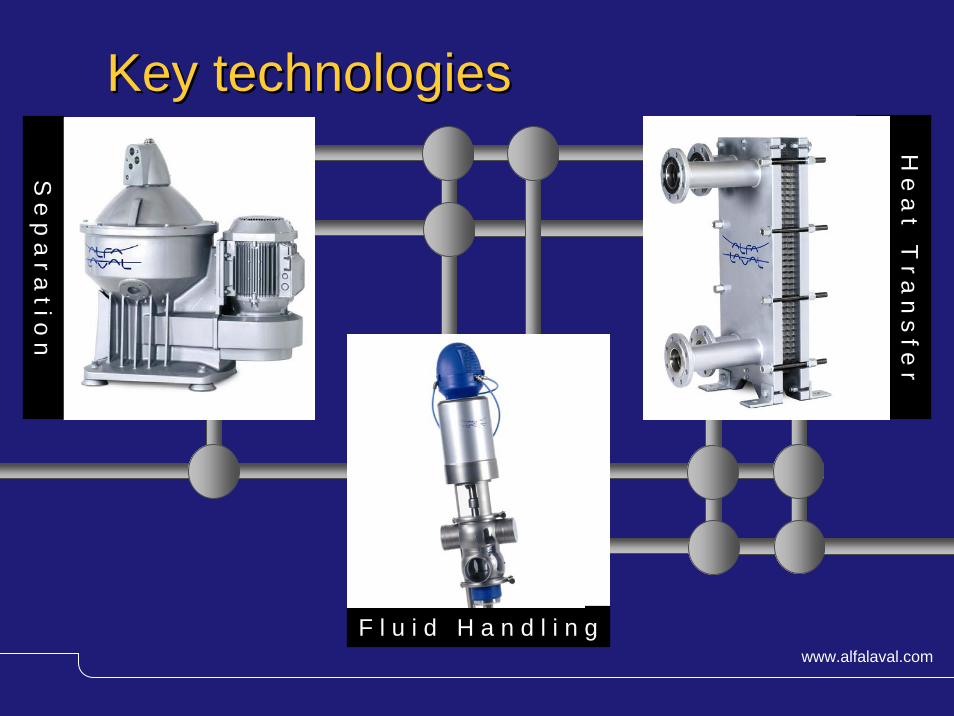

Key technologiesKey technologies

S e p a r a t i o n

F l u i d H a n d l i n g

H e a t T r a n s f e r

© Alfa Laval Slide 9 www.alfalaval.com

Capital salesCapital sales//core product groupcore product group

Capital sales 2001

Heat TransferHeat Transfer47%47%SeparationSeparation

33%33%

Fluid HandlingFluid Handling20%20%

Heat Transfer Separation Fluid Handling

Market share36%

Market share24%

Market share10%

© Alfa Laval Slide 10 www.alfalaval.com

Examples of End-User Markets

Heating and Cooling

Fresh water generation

Brewing

Personal Care / Biopharm

Refrigeration

© Alfa Laval Slide 11 www.alfalaval.com

Diversified blue chip customersBASFBayerBPCargillChevronCoca-ColaDanoneDu PontExxonHeinekenMobilNestleProcter & GambleTetra PakUnileverYork

© Alfa Laval Slide 12 www.alfalaval.com

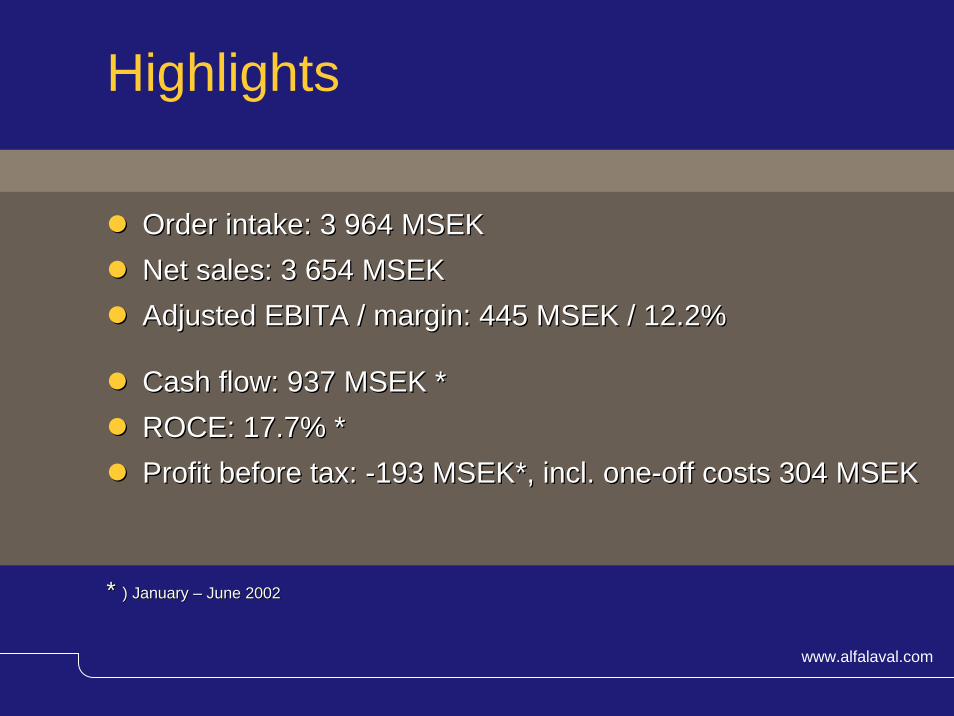

Highlights

Order intake: 3 964 MSEKOrder intake: 3 964 MSEKNet sales: 3 654 MSEKNet sales: 3 654 MSEKAdjusted EBITA / margin: 445 MSEK / 12.2%Adjusted EBITA / margin: 445 MSEK / 12.2%

Cash flow: 937 MSEK *Cash flow: 937 MSEK *ROCE: 17.7% *ROCE: 17.7% *Profit before tax: Profit before tax: --193 MSEK*, incl. one193 MSEK*, incl. one--off costsoff costs 304 MSEK304 MSEK

* * ) January ) January –– June 2002June 2002

© Alfa Laval Slide 13 www.alfalaval.com

Q on Q vs. last year (like for like)

-10

-8

-6

-4

-2

0

2

4

Q102 Q202 Jan-June 02

Orders receivedOrders received

-10

-8

-6

-4

-2

0

2

4

Q102 Q202 Jan-June 02

Net salesNet sales

© Alfa Laval Slide 14 www.alfalaval.com

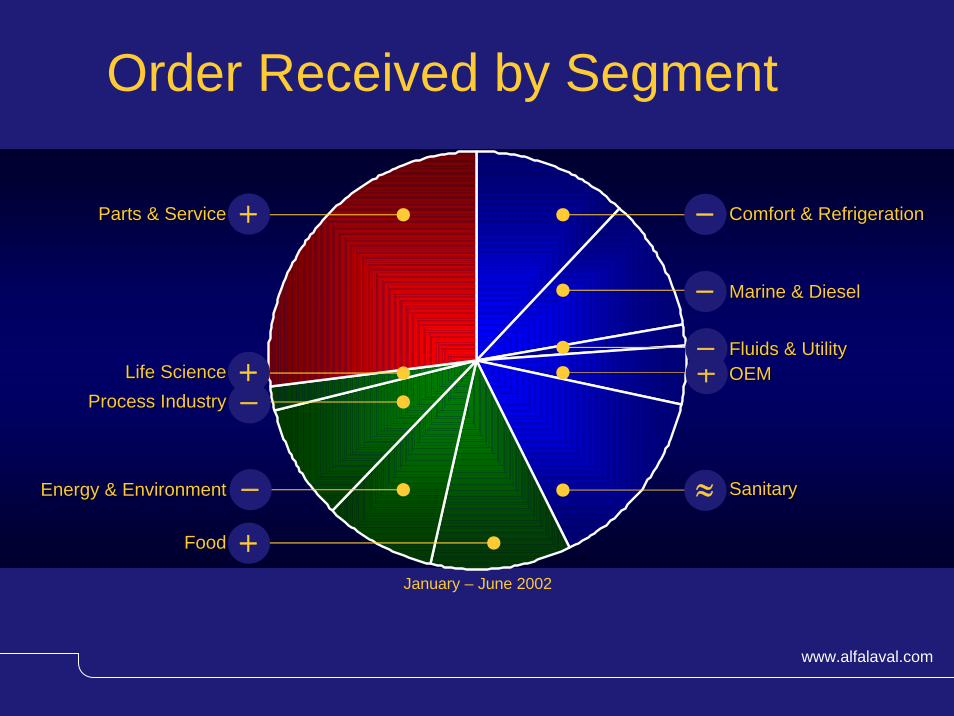

Order Received by Segment

January – June 2002

Comfort & RefrigerationComfort & Refrigeration

SanitarySanitary

Marine & DieselMarine & Diesel

Fluids & UtilityFluids & UtilityOEMOEM

Parts & ServiceParts & Service

Life ScienceLife ScienceProcess IndustryProcess Industry

Energy & EnvironmentEnergy & Environment

FoodFood

+

−

∼ ∼

−

−

+

−

−

+

+

© Alfa Laval Slide 15 www.alfalaval.com

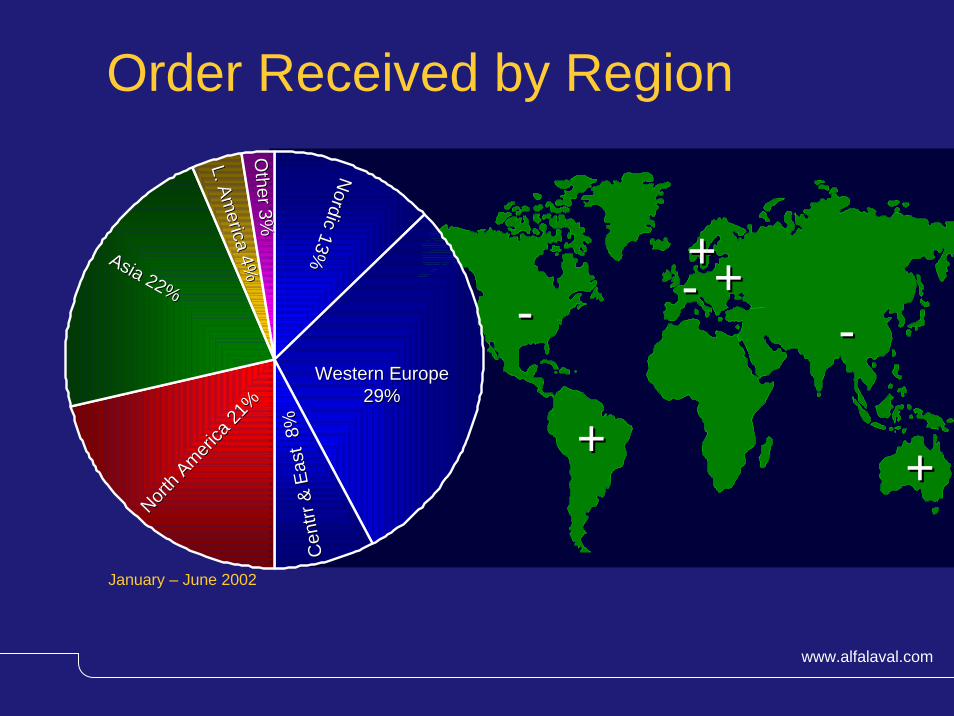

Order Received by Region

Cen

trrC

entrr

& Ea

st 8

%&

East

8%

North A

merica

21%

North A

merica

21%

Asia 22%

Asia 22%

L. America 4%

L. America 4%

Other 3%

Other 3%

Western EuropeWestern Europe29%29%

Nordic 13%

Nordic 13%

++

-- --++++

--

++

January – June 2002

© Alfa Laval Slide 16 www.alfalaval.com

Adjusted EBITA / Margin *MSEK and in percent of salesMSEK and in percent of sales

* Adjusted EBITA – ”Earnings before interests, taxes, amortization of goodwill and step up values and comparison distortion items.”

0

100

200

300

400

500

600

700

800

900

0,0

2,0

4,0

6,0

8,0

10,0

12,0

14,0

JanJan--June 00June 00 JulyJuly--Dec 00Dec 00 JanJan--June 01June 01 JulyJuly--Dec 01Dec 01 JanJan--June 02June 02

© Alfa Laval Slide 17 www.alfalaval.com

Reengineering

© Alfa Laval Slide 18 www.alfalaval.com

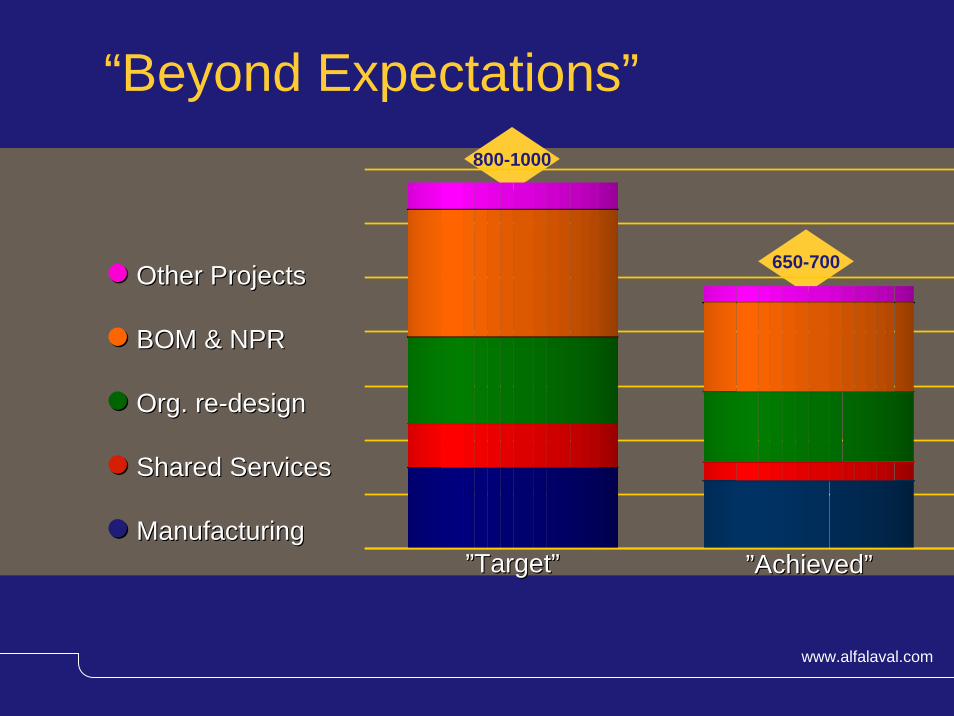

800-1000

650-700

“Beyond Expectations”

Other ProjectsOther Projects

BOM & NPRBOM & NPR

Org. reOrg. re--designdesign

Shared ServicesShared Services

ManufacturingManufacturing””TargetTarget”” ””AchievedAchieved””

Financials A couple of ”your issues”

Thomas ThuressonCFOAlfa Laval Group

© Alfa Laval Slide 20 www.alfalaval.com

Net sales

Adjusted EBITA

Amortization of goodwill

and step-up

Financial net

Comparison distortion items

Profit before tax

Profit after tax

Consolidated Profit and LossMSEK 1.1-30.6 2002 1.1-30.6 2001

Proforma*1.1-30.6 2002

6,916

807

- 252

- 217

0

338

210

6,916

807

- 252

- 399

- 348

- 193

- 321

7,259

851

- 254

- 551

0

46

35

* Based on new capital structure and exclusive of comparison distortion items.

© Alfa Laval Slide 21 www.alfalaval.com

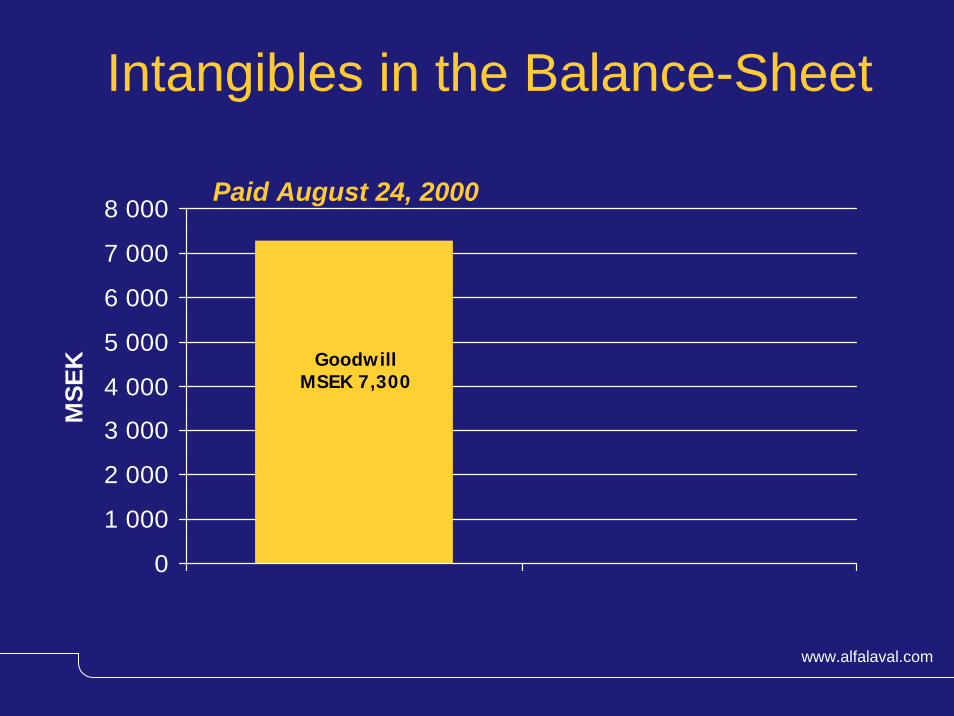

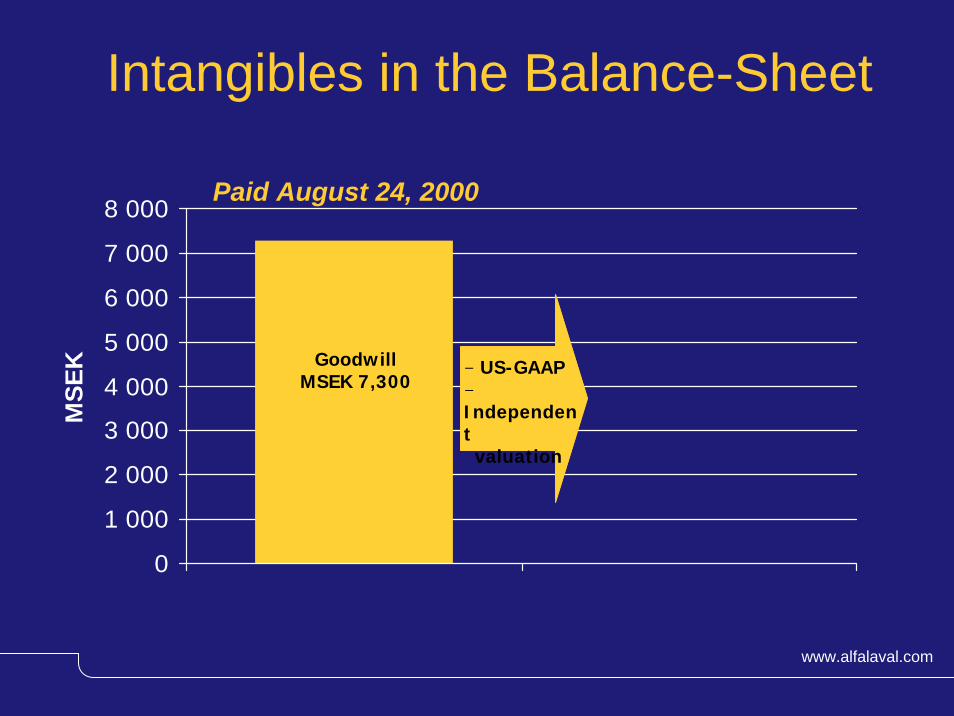

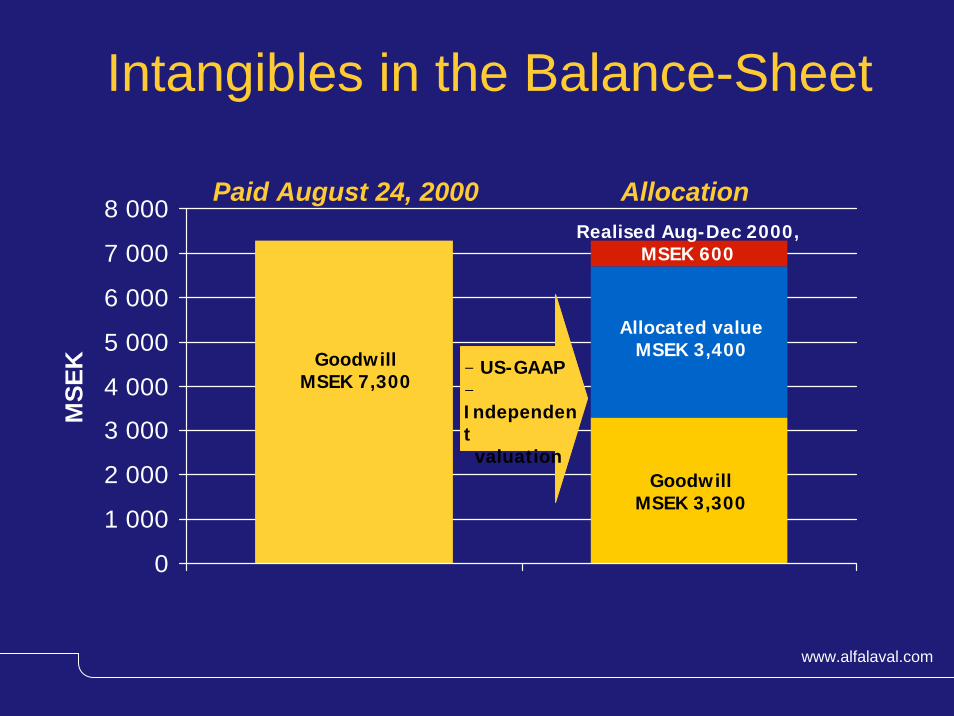

Intangibles in the Balance-Sheet

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

MSE

K

Paid August 24, 2000

GoodwillMSEK 7,300

© Alfa Laval Slide 22 www.alfalaval.com

Intangibles in the Balance-Sheet

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

MSE

K

Paid August 24, 2000

- US-GAAP-Independent

valuation

GoodwillMSEK 7,300

© Alfa Laval Slide 23 www.alfalaval.com

Intangibles in the Balance-Sheet

0

1 000

2 000

3 000

4 000

5 000

6 000

7 000

8 000

MSE

K

Paid August 24, 2000 Allocation

- US-GAAP-Independent

valuation Goodwill

MSEK 3,300

Allocated valueMSEK 3,400

Realised Aug-Dec 2000,MSEK 600

GoodwillMSEK 7,300

© Alfa Laval Slide 24 www.alfalaval.com

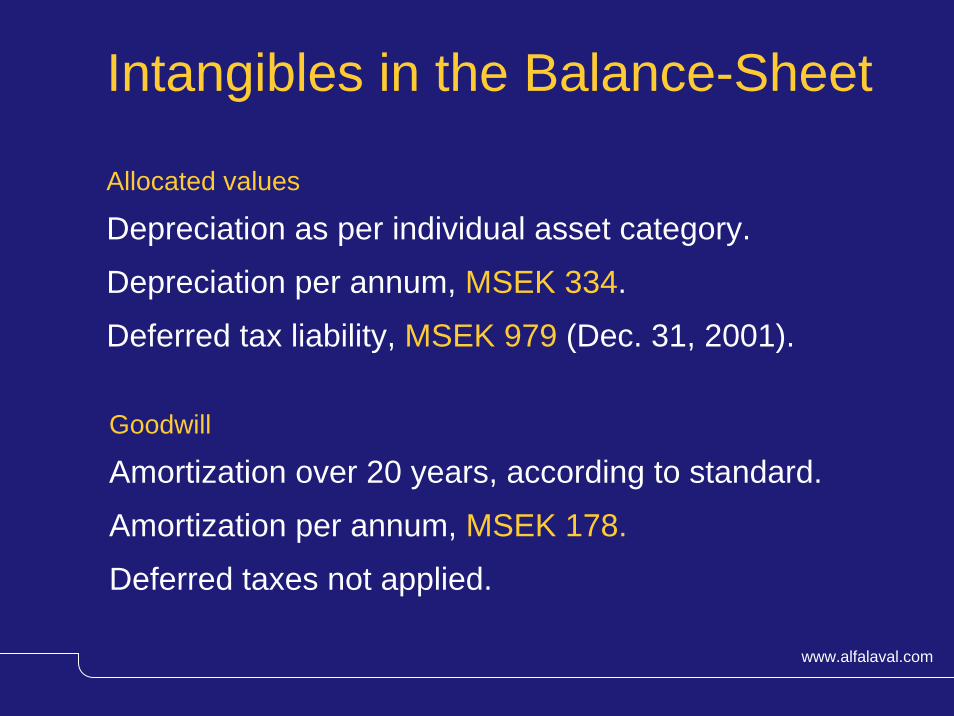

Intangibles in the Balance-Sheet

Allocated values

Depreciation as per individual asset category.

Depreciation per annum, MSEK 334.

Deferred tax liability, MSEK 979 (Dec. 31, 2001).

Goodwill

Amortization over 20 years, according to standard.

Amortization per annum, MSEK 178.

Deferred taxes not applied.

© Alfa Laval Slide 25 www.alfalaval.com

Cash and Deposits

Financial Debt

- Credit institutions

- Bond

- Other

IRS’s

Capital. financing costs

Financial Debt and Financial Net

+ 957

3,919

1,298

27

(78)

As perJune 30, 2002

MSEK

Proforma*Financial Income/ Cost

MSEK

*Calculated on an annual base

+ 19

176

157

28012

Net 4,286 408

(2 %)

(4 1/2%)

(12 1/8 %)

(7%)

(Until 9/03)

Assumptions

© Alfa Laval Slide 26 www.alfalaval.com

EBITDA

Working capital

Taxes paid

Cash flow from operating activities

Capital expenditures

Divestments

Acquisitions*

Provisions

Cash flow from investing activities

Cash flow from financing activities

Net increasein cash and bank

978

117

- 158

937

- 152

61

- 368

- 27

- 486

- 237

214

978

117

- 158

937

- 152

-

-

- 27

- 179

- 212

546

MSEK 1.1-30.6 2002Proforma

1.1-30.6 2002

Cash-flow statement

* Vendor Warrant, MEUR 40

© Alfa Laval Slide 27 www.alfalaval.com

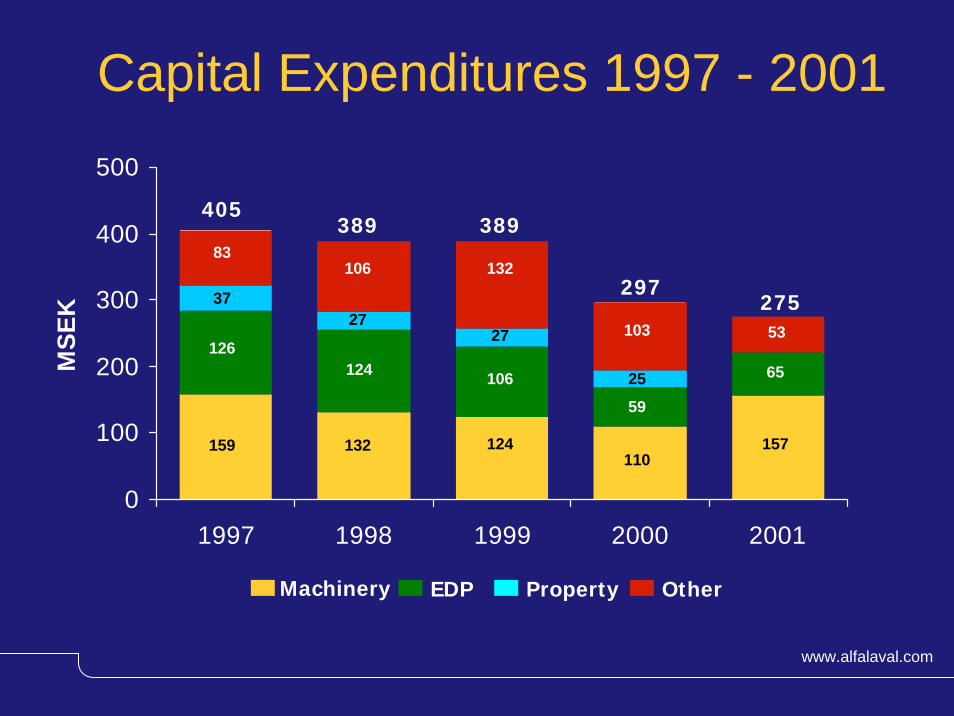

Capital Expenditures 1997 - 2001

0

100

200

300

400

500

1997 1998 1999 2000 2001

MSE

K

EDP Property Other

405389 389

297

Machinery

275

159

126

37

83

132

124

27

106

124

106

27

132

110

59

25

103

157

65

53

© Alfa Laval Slide 28 www.alfalaval.com

Key ratios

RatioRatio

Earnings Per Share(proforma)

Earnings Per Share(proforma, excl. goodwillamortization and step-updepreciation

Cash Earnings Per Share(proforma)

RemarksRemarks

- Current number of shares- New capital structure- Exclusive of comparison distortion items

- As above adding back goodwill amortization and step-up depreciation

- New capital structure- Excl. disposals and

acquisitions

JanuaryJanuary--June 2002 June 2002

Before tax, SEK 3.03After tax SEK 1.88

Before tax SEK 5.28After tax SEK 4.14

Before tax SEK 6.30After tax SEK 4.89

© Alfa Laval Slide 29 www.alfalaval.com

Reengineering

© Alfa Laval Slide 30 www.alfalaval.com

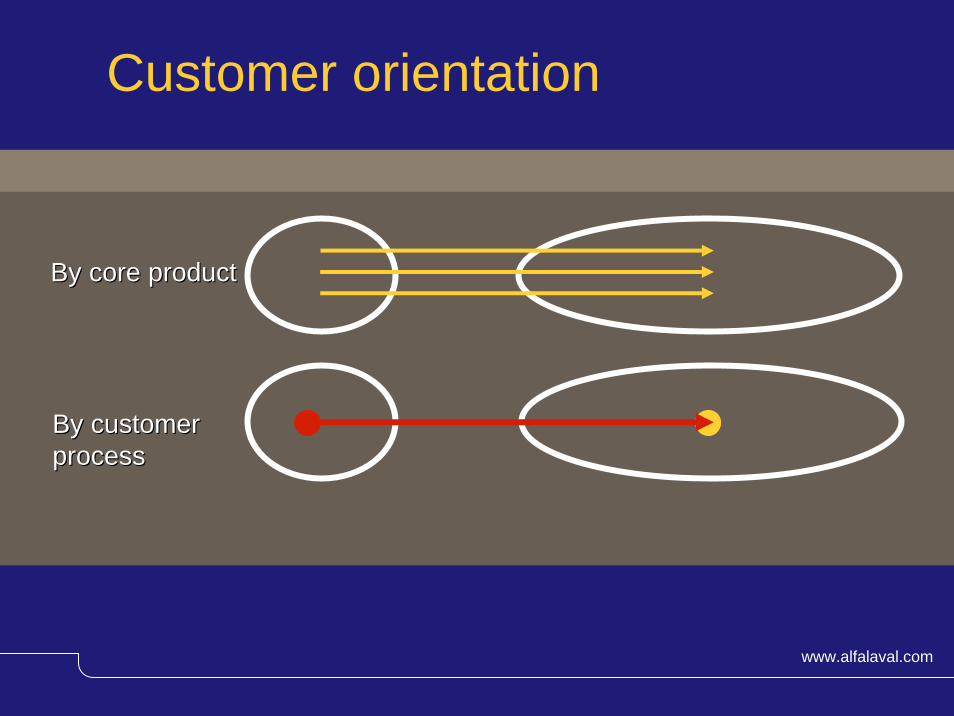

Customer orientation

By core productBy core product

By customer By customer processprocess

© Alfa Laval Slide 31 www.alfalaval.com

Reengineering

© Alfa Laval Slide 32 www.alfalaval.com

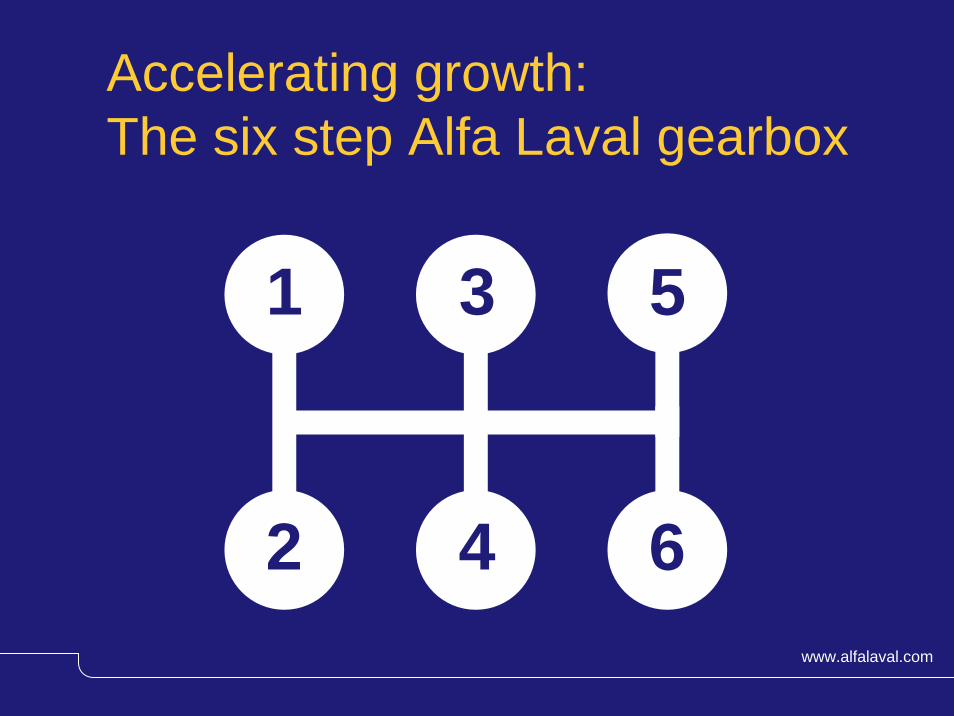

Accelerating growth: The six step Alfa Laval gearbox

1 3 5

2 4 6

© Alfa Laval Slide 33 www.alfalaval.com

The drivers behind Alfa Laval’s growth strategy

1 3 5

2 4 6

1st gear: EExistingxisting range of productsproducts

2nd gear: MMarketarket--driven R&Ddriven R&D

3rd gear: Focus on customer segmentscustomer segments

4th gear: Strong commitment to Parts & ServiceParts & Service

5th gear: Exploitation of new market conceptsnew market concepts

6th gear: Ambition to add new core productsnew core products

© Alfa Laval Slide 34 www.alfalaval.com

666

3 51

2

4

1

22

53

4

551

6

The six step Alfa Laval gearboxExistingExistingproductsproducts

CustomerCustomersegmentssegments

New marketNew marketconceptsconcepts

MarketMarket--drivendrivenR&DR&D

Parts & ServiceParts & Service New coreNew coreproductsproducts

44

44

© Alfa Laval Slide 35 www.alfalaval.com

666

3 51

2 4

1

2

53

4

55

2

1

6

3

4

5

6

The six step Alfa Laval gearboxExistingExistingproductsproducts

CustomerCustomersegmentssegments

New marketNew marketconceptsconcepts

MarketMarket--drivendrivenR&DR&D

Parts & ServiceParts & Service New coreNew coreproductsproducts

All six gears willgive us an annual average growth of5 % over a business cycle.