capital market advisory council “cmac” and financial

TRANSCRIPT

CAPITAL MARKET ADVISORY COUNCIL “CMAC”

AND FINANCIAL SECTOR DEVELOPMENT PROGRAM

IN KIGALI RWANDA

A Thesis

presented to the School of

Postgraduate Studies and research

Kampala International University

Kampala, Uganda

In partial Fulfillment of the requirements for the degree

Master of business administration

By:

NDATSIKIRA Constantin

MBA/2003 1/DF

September, 2011

DECLARATION A

“This thesis is my original work and has not been presented for a Degree or any

other academic award in my University or institution of learning”

~ C~≤7~FifName and signature of candidate

~2~\ (0 j~otiDate

DECLARATION B

“I/we confirm that the work reported in this thesis was carried out by candidate

under my/our supervision”.

d~a_ frL~-c~3I ____________

Name and signature of supervisor Name and signature of su

pci-visor

~I)~ (~~i ________

Date Date

APPROVAL SHEET

This dissertation entitled Capital market advisory council (CMAC) and fi

nancial sector development program in Kigali, Rwanda prepared and

submitted by NDATSIKIRA Constantin in partial fulfillment of requirement for

the degree of Masters of business administration has been examined and

approved by the panel on oral ex~iination with a grade of PASSED.

Name and ii. of Chairman

L ~< ~ Ntu/~LclMName and sig. of Supervisor Name and sig. of Panelist

I,’6~~n ~.a a

Nam and sig. of panelist Name and sig. of panelist

Date of Comprehensive Examination:

Grade

Name and sig. of Director, SPGSR

Name and Sig. of DVC, SPGSR

DEDICATION

This book is a dedication to my Parents Mr. Rwigema Martin and Mukakarisa

Eugenie, my brothers and sisters, Monica, Francine, Pacifique, Delice and John

Claude.

This book is also a dedication to my beloved REGINE.

iv

AKNOWLEDGEMEgr

I would like to thank the AlmIghty God for enablIng me to complete thisreport. I would like also to thank my supervisor Dr D. L Klblkyo for all the assistance that he has given me throughout my research. I would like also to thankDc Kibuuka, Dr YAHYA Ibrahlm, Mr. MALINGA R. and all KIU staff and teachersfor all the support and the assistance they gave me throughout my study. FinallyI thank all dass comrades for theIr encouragement May the almIghty God reward abundantly,

NDATSIKIRA Constantin

V

ABSTARCT

The study investigated the effect of capital market on financial sector

development in Rwanda. From population 150, a sample of 132 respondents

was interviewed. Analysis of data was by regression analysis.

The objectives of the study were to determine the profile of respondents, to de

termine how CMAC contribute, to better financial intermediation in the area; to

identify the market of development services put in place by CMAC in order to

continue building the reputation as an innovative financier and to establish the

significant relationship between capital market advisory and financial sector de

velopment programme.

The findings of the study, following the research questions, revealed that there is

a strong relationship between Capital market and development of financial sector

in Rwanda because CMAC, through its stock exchange market will help to facili

tate financial institutions to get loans by buying securities, to provide services

like increasing incomes of investors, enhancing economic growth, and creating

employment, to increase the profits of financial institutions, and to attract more

financial companies to join Rwanda stock exchange market. The research re

vealed that, CMAC has a strong intervention in promotion of investor protection,

insuring that markets are fair, efficient and transparent so as financial sector

gets vibrant.

In order to enable a smooth transition into the effective operation of capital mar

ket in Rwanda there is need to implement the following policy recommendations.

There is a need to develop the confidence in the public for investing in capital

market by the increased public awareness aimed at educating the public about

CMAC and RSE operations.

Development of an effective legal system to increase the safety and complete

removal of uncertainty regarding the benefits of the resulting investments, guar

anteed stable banking sector, enforcement of capital market regulations so that

there is continued encouragement of the public in the bond market.

vi

TABLE OF CONTENTS

CHAPTER PAGE

ONE THE PROBLEM AND ITS SCOPE 1

Background of the Study i

Statement of the Problem 3

Purpose of the Study 4

Objective of the study 5

Research Questions 5

Hypothesis 5

Scope 6

Significance of the Study 6

Operational Definitions of Key Terms 7

TWO REVIEW OF RELATED LITERATURE 9

Concepts, Ideas, Opinions from Authors/Experts 9

Theoretical Perspectives 14

Related Studies 17

THREE METHODOLOGY 19

Research Design 19

Research Population

Sample Size 19

Sampling Procedure 20

Data collection Instrument 20

Validity and Reliability of the Instrument 21

Data Gathering Procedures 22

Data Analysis 23

Limitations of the Study 23

vii

FOUR PRESENTATION, ANALYSIS AND INTEPRETATION OF

DATA 25

Introduction 25

FIVE FINDINGS, CONCLUSIONS,

RECOMMENDATIONS 36

Findings 36

Conclusions 38

Recommendations 39

REFERENCES 41

APPENDICES 45

Append~x I - Transmittal Letter 45

Append~x II - Clearance from Ethics Committee 46

Append~x III - Informed Consent 47

Appendix IV - Research Instruments 48

Curriculum Vitae 55

viii

LIST OF TABLES

Table 1: Profile of respondents 25

Table 2: ContrIbutIon of CMAC to better financIal Intermediation In the area 29

Table 3: IdentIficatIon of the CMAC market of development services 31

Table 4: The effectiveness of CMAC In financIal sector development program ofRwanda 33

TableS: Pearson’s CorrelatIons 35

ix

LIST OF FIGURES

Figure I: Schema of the study 16

x

LIST OF ACRONYMS

BNR Banque Nationale Du Rwanda

CMAC Capital Market Advisory Council

RSE Rwanda Stock Exchange Market

GDP Gross Domestic Product

OTC Over The Counter

ROTC Rwanda Over The Counter Market

U.K United Kingdom

US United Nations

FSA Financial Services Authority

KCB Kenya Commercial Bank

BB Berkley Bank

CVI Content Validity Index

xi

CHAPTER ONE

THE PROBLEM AND ITS SCOPE

Back ground of the study

All economies fundamentally require government planning authorities for

finance, banking, insurance and retirement. Of equal importance is the capital

markets authority, which, however, does not have to be under the government.

Such is the global trend; the New York, and London Stock Exchanges were all

started by private entities. In Africa, the World Bank has influenced financial re

forms to ignite capital markets through legislation to provide security for the in

vestors (Kinyua, 2004).

Capital Markets benefits its clients by offering complete capital markets

solutions anywhere around the globe. Investment Properties, working in tandem

with Debt & Equity Finance, assures clients that all alternative recapitalization

strategies are evaluated. When working with buyers of assets offered by Invest

ment Properties, optimal debt structures are often secured, enabling borrowers

to obtain more loan proceeds at attractive terms and sellers to achieve better

results. By encompassing debt and equity solutions, the group ultimately pro

vides investors with the maximum flexibility to achieve their capital needs

(Bohnsted, 2000)

Recall that a capital market is where the supply and demand for long term

stock funds is channeled. In this market, stocks and other financial investments

are traded amongst capable financial investors who can obtain long term funds

by way of issuing stocks and bonds, (Kinyua, 2004).

An organized capital market or stock market has three components.

These are: One, the listed securities or stocks issued either by Government or

companies; Two, the investors or the public who own the securities, and Three,

the intermediaries or middlemen called stockbrokers.

The stockbrokers are members of the OTC market who are authorized to

sell and buy shares or bonds on behalf of the investing public.

(htt://cmauganda.co.ug/about/about.htm). Therefore a capital market is a mar

ket where stocks are bought and sold, Buyers and sellers of stocks meet at the

capital market to transact business, A capital market is a part of a stock market

or a securities market or a stock exchange (Bohnsted, 2000).

The capital market plays several roles in the mobilization of savings

amongst the various participants of the economy. They help in the monitoring

and control of the firms operating such as stockbrokers, dealers, and investment

advisors (Alile,1992), The authority and the security assist on the mobilization

of financial resources where the authority curries outs investment advises to

prospective investments. The market assists in the protection of the investors

‘interest through encouraging transparency by the listed companies, (Kother,

2003).The capital markets and security exchange affect the growth of the econ

omy by way of creation of liquidity in the economy.

The securities exchange aid as a means of exchange for the prospective

buyers and sellers in the market. Capital Markets combines the company’s in

vestment sales and mortgage banking businesses into a single, fully-integrated

global service offering.

2

The financial, sector is all the wholesale, retail, formal and informal

institutions in an economy offering financial services to consumers, businesse~

and other financial institutions. In its broadest definition, it includes everything

from banks, stock exchanges, and insurers, to credit unions, microfinance institu

tions and money lenders.

Financial sector on the other hand covers the short-term money market and

foreign exchange market operated by the Central Bank, the long-term capital

market, commercial and specialized banks, non-bank financial institutions and

microfi nance institutions (Sanvart, 1986).

The overarching vision of the financial sector development is to develop a stable

and sound financial sector that is sufficiently deep and broad, capable of effi

ciently mobilizing and allocating resources to address the development needs of

the economy and reduce poverty. The scope of financial sector development

program is to address weaknesses in access to finance, capital market develop

ment, regulation of non-bank financial institutions and payment system.

Statement of the prob~em

The financial sector assessment report (FSAP) describes the Rwandan

financial sector as narrow, shallow with an oligopolistic banking sector and very

narrow penetration of insurance services as well as undefined financial products.

The FSAP further recognized, wide interest rate spread, poor savings rate, scarci

ty of long term capital, unregulated pension and insurance sectors and a mal

functioning payment system. In addition, financial sector development which

should normally play a significant role in bridging this gap is steel weak, lacked

adequate financial management systems, and hard weak internal controls and

poor governance structures.

Rwanda lacked long term capital and market-based debt or equity products es

sential for its economic development strategy.

3

While the banking sector was exclusively liquid, the funds were short term

in nature. As results, mortgages and investment projects were financed on very

short maturity terms of around Syears. This weakness was exacerbated by lack

of efficient mechanisms for banks to transform the long term assets on their

books into liquid funds.

The financial sector in the gross domestic product (GDP) remains small at

5.2% in 2007.By the same year, it has been discovered that savings and invest

ment are still very low currently at 0.5% (Financial Sector development plan,

2007). The government has conducted an assessment of the financial sector and

designed a Financial Sector Development Program which contains specific actions

to develop the banking sector, microfinance and access to credit, long-term

finance and capital markets, contractual savings (insurance and pension) and

payment Systems. Finally the main challenge of the Rwandan financial sector is

inadequate institutional, organizational, and human resources capacity (Rusaga

ra, 2007).To overcome this enormous challenge, it is essential to build capacity

in all these dimensions. The Financial Sector Development Program is an impor

tant step, forward, especially in its emphasis on institutional development. That is

why the researcher has been interested on the effectiveness of capital market

advisory council in the financial sector development of Rwanda.

Purpose of the Study

The purpose of this study is to establish the relationship between the

capital market advisory council and the development of financial sector in Rwan

da. The Government has pursued positive steps to address this problem especial

ly through the strengthening of micro finance institutions and through promoting

stock exchange market (New Vision, 2010).

4

Research Objectives

The general objective of this study is the effectiveness of capital market

advisory council (CMAC) in financial sector development program in Rwanda,

The specific objectives are:

(i) To determine the profile of respondents in terms of objectives.

(ii) To determine how CMAC contribute to better financial intermedia

tion in the area.

(iii) To identify the market of development services put in place by

CMAC in order to continue building the reputation as an innovative

financier.

iv. To establish the effectiveness of CMAC in financial sector develop

ment program of Rwanda.

Research questions

(i) What are the profile respondents?

(ii) What is the contribution of Capital market in development of fi

nancial sector?

(iii) What are development services put in place by CMAC in order to

continue building the reputation as an innovative financier?

(iv) What is the level of effectiveness relationship between capital mar

ket advisory in financial sector development program?

Hypothes~s of the study

There is no significant relationship between the creation of capital mai ket

advisory council and development of financial sector in Rwanda.

5

Scope of the study

The geographical scope

The study will be conducted in Rwanda, the area which has only one word

that is KIGALI city. This area was selected because it is where CMAC is located

and most of the people in the area use CMAC services.

The theoretical scope

The study concentrated on establishing the relationship between tha fi

nancial sector development programs in Rwanda using capital market advisory

council. The study basically considered the services rendered by CMAC in Rwan

da, how have contribution to development of financial sector in the area.

The content scope

The study focused. on capital market advisory council and financial sector

development programs.

S~gnificance of the Study

This study will be significant in the following aspects: The CMAC will con

tribute to the financial sector development programs with the variety of services

offered and their various activities. The recommendation to be made after the

analysis of the collected data will help the entire financial systems to design ef

fective policies that will address the development of financial sector in Rwanda.

The study will help the business community not only to rely on banking

and other microfinance inst1tutions as a source of long term financing, but also to

increase on the listing of the stock exchange.

6

The study will also contribute to the information data bank in respect of capi

tal and securities exchange on which few studies have been carried out so far.

The study will also be used by different scholars in higher institutions of learn

ing, libraries and the public.

The information derived from the study will provide financial analysts, policy

formulators and researchers with the basic for the further research in Rwanda.

Operation Definitions of Key Terms

Capital Market Advisory Council

Capital Market Advisory Council is a council which admitted seven mem

bers to operate in the Rwanda OTC market, There are three categories of mem

bership, these are Stockbrokers, Dealers and Sponsors, the stockbrokers buy and

sell both in their own behalf and on behalf of the investing public, dealers trade

with their own funds. Capital market can also be defined as the market for long

terms, It is composed of borrowers and lenders. The rate of interest is deter

mined by demand and supply forces. Long term capital instruments include; or

dinary shares or equity, fixed interest capital, that is to say preference share cap

ital and debentures,

Capital markets

Capital markets include; stock exchange, investment companies insurance com

panies, building societies, pension funds, commercial banks, and many others,

Usually capital markets are divided in two: Securities market which is a market

for terms securities, like shares, debentures, Stocks, bonds and many others,

The second is a loan market which is a market for long term loans like mortgage

finance, lease finance and many others. Capital market has to insure transparen

cy by listed companies about their books of accounts.

7

The flnancia~ sector

The financial sector is defined as all the wholesale, retail, formal and informal

institutions in an economy offering financial services to consumers, businesses

and other financial institutions, In its broadest definition, it includes everything

from banks, stock exchanges, and insurers, to credit unions, microfinance institu

tions and money lenders.

Financial sector however, covers the short-term money market and foreign ex

change market operated by the Central Bank, the long-term capital market,

Commercial and specialized banks, non-bank financial institutions and microfin

ance institutions.

8

CHAPTER TWO

REVIEW OF RELATED LITERATURE

Concepts, Ideas, Op~nions from Authors/Experts

Capitall market

capital market is a market for securities (debt or equity), where business

enterprises (companies) and governments can raise long-term funds. It is de

fined as a market in which money is provided for periods longer than a year, as

the raising of short-term funds takes place on other markets (e.g., the money

market). The capital market includes the stock market (equity securities) and the

bond market (debt). Financial regulators, such as the UK’s Financial Services Au

thority (FSA) or the U.S. Securities and Exchange Commission (SEC), oversee the

capital markets in their designated jurisdictions to ensure that investors are pro

tected against fraud, among other duties.( Sullivan, Arthur; Steven M. Sheflin

,2003).

Capita~ markets

Capital markets may be classified as primary markets and secondary mar

kets. In primary markets, new stock or bond issues are sold to investors via a

mechanism known as underwriting. In the secondary markets, existing securities

are sold and bought among investors or traders, usually on a securities ex

change, over-the-counter, or elsewhere (Pearson Prentice, 2003, Hall. pp. 283).

Long time ago, stock market based financial systems have been associated with

the 1gth century UK, which was the first country to go through industrial revolu

tion, and 20th century US which was the first country to go through post industri

al revolution (Bohnsedt, 2000).

9

The bank based financial sector developments were associated with France,

Germany, and Japan. There have been numerous literatures on the comparative

relationship between capital market and financial sector development in an

economy (Alile, 1992).

Capital Market is one of the significant aspects of every financial market. Broadly

speaking the capital market is a market for financial assets which have a long or

indefinite maturity. Unlike money market instruments the capital market instru

ments become mature for the period above one year. It is an institutional ar

rangement to borrow and lend money for a longer period of time. It consists of

financial institutions which play the role of lenders in the capital market. Business

units and corporate are the borrowers in the capital market, Capital market in

volves various instruments which can be used for financial transactions, Capita!

market provides.long term debt and equity finance for the government and the

corporate sector (Harris, 1913).

Like the money market capital market is also very important. It plays a

significant role in the national economy. A developed, dynamic and vibrant capi

tal market can immensely contribute for speedy economic growth and develop

ment. Let us get acquainted with the important functions and role of the capital

market:

MobiJ~zation of Savings: Capital market is an important source for mo

bilizing idle savings from the economy. It mobilizes funds from people for further

investments in the productive channels of an economy. In that sense it activates

the ideal monetary resources and puts them in proper investments (Wrights,

2002).

Capllta~ Formation: Capital market helps in capital formation. Capital

formation is net addition to the existing stock of capital in the economy. Through

mobilization of ideal resources it generates savings; the mobilized savings are

10

made available to various segments such as agriculture, industry, etc. This

helps in increasing capital formation (Postel, 1994).

Provision of Investment Avenue: Capital market raises resources for

longer periods of time. Thus it provides an investment avenue for people who

wish to invest resources for a long period of time. It provides suitable interest

rate returns also to investors. Instruments such as bonds, equities, units of mu

tual funds, insurance policies, etc. definitely provides diverse investment avenue

for the public.

Speed up Economic Growth and Development: Capital market en

hances production and productivity in the national economy. As it makes funds

available for long period of time, the financial requirements of business houses

are met by the capital market, It helps in research and development. This helps

in, increasing production and productivity in economy by generation of employ

ment and development of infrastructure.

Proper Regulation of Funds: Capital markets not only helps in fund

mobilization, but it also helps in proper allocation of these resources. It can have

regulation over the resources so that it can direct funds in a qualitative manner.

Service Provision: As an important financial set up capital market provides var

ious types of services. It includes long term and medium term loans to industry,

underwriting services, consultancy services, export finance, etc. These services

help the manufacturing sector in a large spectrum.

Continuous Availability of Funds: Capital market is place where the invest

ment avenue is continuously available for long term investment,

11

This is a liquid market as it makes fund available on continues basis, Both buyers

and seller can easily buy and sell securities as they are continuously available.

Basically capital market transactions are related to the stock exchanges. Thus

marketability in the capital market becomes easy. These are the important func

tions of the capital market.

Government is involved in creating and enabling policy, legal, and regula

tory environment for development of securities markets and train government

regulators on how to oversee the marketplaces. The Securities Markets Group is

also an active thought leader striving to advance knowledge in a variety of secur

ities market areas via papers, books, toolkits, and workshops.

Private individual’s also participate in active dialogue with key international

securities organizations, such as International Organization of Securities Com

missions (IOSCO), to improve the standard setting process applied to developing

countries. The private individuals’ work involves operations around the world,

ranging from single country to regional and global prolects (Fama F. Eugine,

1970).

They focused on strengthening the enabling legal and regulatory environ

ment, supporting the development of market infrastructure and participants, and

helping to bring new and innovative transactions to market.

Financial sector development program is the short-term money market

and foreign ex-change market operated by the Central Bank, Commercial and

specialized banks, non-bank financial institutions and microfinance institutions. In

this regard, the specific objectives of Financial Sector Development Program con

sist of: expanding access to credit and financial services to the whole population

across the country in both urban and rural areas, enhancing savings mobilization,

especially long-term savings; and, Channeling long-term capital for productive

investments (Harris, 1913).

12

Financial Sector Development Program provides a program loan to support

vital policy reforms in the financial sector, a project loan to facilitate program

implementation; and an associated technical assistance to institutionalize skills

and capacity development in the financial sector and promote the sector’s

growth, (Asian development bank, 2007)

The program’s aim is to reduce legal, regulatory, and supervisory constraints on

the financial sector; strengthen corporate governance and promote greater

commercial orientation in financial institutions; establish a surveillance system for

anti—money laundering (AML) and combating the financing of terrorism (CFT) to

support security and stability in the financial sector; develop national accounting

and auditing policies and standards for reliable financial reporting; establish a

credit information bureau to improve credit decisions to sustain capacity devel

opment by developing and setting up a training institute for the financial sector,

(Gavelle, 1999).

This is a program which gives an overview of the country’s economic de

velopment, financial sector development, and recent political transformation de

tails regarding the country’s compliance, (www.businessweek.com).

This program has been implemented in the Royal Monetary Authority

(RMA), which is Bhutan’s central bank, implemented the prudential financial sec

tor development program measures in 2009 to tighten monetary policy and

make the financial sector more resilient. It raised cash reserve and minimum

capital requirements and also revised the provisioning requirements for doubtlul

loans to minimize potential adverse impacts from risky lending.

Otherwise, developments in the financial market have generally been positive

and the entry of more banks and another insurance company into the financial

sector is expected to bring greater competition and new technology.

I—,

The link between capital market and financial sector is that the capital market is

essential to issue and trade long-term securities currently comprising of Treasury

bonds, and corporate bonds; contrary to T-bills (short-term tenor of less than

one year) issued and traded on the money market, T-bonds (long-term tenor of

more than one year) are essential to raise capital for public and private invest

ments, with the issuance and trading of equities (Gravelle, 1999).Seward for

example concluded that capital market and banks seem to complement each

other in transferring financial resources from households to firms (Seward,2004),

Investment in the stock markets also provides a source of income. Shares.

pay dividends when companies declare profits and decide to distribute part of

the profit to shareholders. International evidence on the link between financial

sector development and improvements of financial sector is in living standards

Indicated by the measures to the access in finance, analyzes of the determi

nants, and evaluations of the impact of finance on growth, equity and poverty

reduction, increasingly shedding light on the benefits of financial sector devel

opment ( Greenwood smith, 1996).

Theoretical Perspectives

This study will be based on systems theory. Systems theory focuses on

the arrangement of and relations between the parts which connect them into a

whole rather than reducing an entity to the properties of its parts or elements

(von Bertalanffy, 1968). This particular organization determines a system, which

is independent of the concrete substance of the elements. Thus, the same con

cepts and principles of organization underlie the different disciplines, providing a

basis for their unification (von Bertalanffy, 1968).

14

Simply put, a system is an organized collection of parts (or subsystems)

that are highly integrated to accomplish an overall goal. The system has various

inputs, which go through certain processes to produce certain outputs, which

together, accomplish the overall desired goal for the system. So a system is

usually made up of many smaller systems, or subsystems. For example, an or

ganization is made up of many administrative and management functions, prod

ucts, services, groups and individuals. If one part of the system is changed, the

nature of the overall system is often changed, as well — by definition then, the

system is systemic, meaning relating to, or affecting, the entire system, (von

Bertalanffy, 1968).

A system can be said to consist of four things, The first is objects — the

parts, elements, or variables within the system. These may be physical or ab

stract or both, depending on the nature of the system.

Second, a system consists of attributes — the qualities or properties of the sys

tem and its objects. Third, a system had internal relationships among its objects.

Fourth, systems exist in an environment. A system, then, is a set of things that

affect one another within an environment and form a larger pattern that is dif

ferent from any of the parts, (L. von Bertalanffy, 1968).

If any of the parts or activities in the system seems weakened or misa

ligned, the system makes necessary adjustments to more effectively achieve its

goals.

15

SCHEMA OF THE STUDY

F~gure I: Schema of the study

Source: vaHous authors

The above conceptual framework shows a relationship between capital

market advisory council and financial sector development programs, Independent

variable as capital market advisory council and dependent variable as financial

sector development programs.

Capital market advisory council provides services that include financial in

termediation (savings, credits schemes, insurance, capital market development

services), social intermediation (group formation, shareholders training) and

market of development services (the prices of stock go up, put in a better finan

cial position and will continue building the reputation as an innovative financier.)

When companies participate in capital market and are listed on the stock ex

change, they raise more capital and this contributes to their development.

Th~

Capitall market advF~sory councN (CMAC)

- Financial intermediation- Market of development services-security market forexample shares, debentures, stocks...-loan market for example mortgage finance,

Process

Economk factors

- Exchange rates

- Interest rates

-Monetary policy

Demand and supply

- Regulatory framework

Finanda~ Sector devellopment program.

- Greater access to credit- Employment increase- Raise capital-Increased investment opportunity-selling more shares-economic expansion

16

However, there are other economic factors that intervene like the exchange rate

keeps on increasing and decreasing, monetary policy, demand and supply of

money and regulatory framework which regulates and controls the economy.

These economic factors have come in to affect the financial sector development

programs in Rwanda, with Greater access to credit, Employment increase, Rais

ing capital, increased investment opportunity, selling more shares, economic ex

pansion and among others.

However the ability of Rwandans to use such services and capital market to pro

vide the services effectively will depend on the contextual factors like increased

levels of income, increased investment opportunities and to allow the shares of

privatized companies to gain a domestic listing that will influence the services

provided by the CMAC and the activities to be undertaken by the Rwandans that

enhance development. Give the above factors, the impact of capital market advi

sory council (CMAC) in financial sector development program in Rwanda will be

realized through greater access to credit, trade development and grow of wealth

if the CMAC services are used by Rwandans

Related studies

Various forms of literature have looked at the relationship between capital

market and development of financial sector. As capital market is defined as a

market in which long term debt and equity instruments are bought and sold

(Marchart, 2004). Long time ago, stock market based financial systems have

been associated with the 19th century UK, which was the first country to go

through industrial revolution, and 20th century US which was the first country to

go through post industrial revolution. The bank based financial sector deveiop

ments were associated with France, Germany, and Japan.

17

There have been numerous literatures on the comparative relationship between

capital market and financial sector development in an economy (Alile, 1992).

Seward for example concluded that capital market and banks seem to comple

ment each other in transferring financial resources from households to firms

(Seward, 2001).

Modern growth. th~aory

It identifies two specific channels through which the financial sector might

affect long-run growth: through its impact on capital accumulation (including

human as well as physical capital) and through its impact on the rate of techno

logical progress (Levine (1997).

These effects arise from the intermediation role provided by financial institutions

which enable the financial sector to: mobilise savings for investment; facilitate

and encourage inflows of foreign capital (including FDI, portfolio investment and

bonds, and remittances); and optimise the allocation of capital between compet

ing uses, ensuring that capital goes to its most productive use. Levine (1997)

Levine (1997) identifies five basic functions of financial intermediaries which give

rise to Savings mobilisation, Risk management, Acquiring information about in

vestment opportunities, Monitoring borrowers and exerting corporate control,

facilitating the exchange of goods and services (Levine, 1997).

18

CHAPTER THREE

RESEARCH METHODOLOGY

Research design

The research was based on a descriptive survey design and a cross sec

tional design based on structured questionnaire. This is because he collected in

formation from a random sample that had been drawn from a target population.

The sample chosen represented a cross section of the target population. This

was because they were categories of different participants that are from CMAC,

RSE, and customers of financial institutions and these were studied at one point

in time depending on their characteristics. This research design is used as a sys

tematic collection and presentation of data to give a clear insight with an aim to

discover the extent of the problem. Also both quantitative and qualitative me

thods were used to establish relationship between variables.

Research population

The study population consisted of 40 staff members (There are three cat

egories of membership: These are Stockbrokers, Dealers and Sponsors) from

CMAC, 50 from RSE, and 60 customers. So the total population is 150

Sample size

During conducting research, it is often impossible, impractical or too ex~

pensive to collect data from all population of analysis included in the research

problem. Thus a smaller number of a sample is often chosen to represent the

relevant attributes of the whole sets of population.

19

In selecting the research sample size, the following formula for sample

size determination was used:

Nn= 2

1 + Ne

Where: n is sample size, N represents population, CL represents the level of signi

ficance. Here ct= 0~05. (Slovin,1994).

Sampflng procedure

The research considered the staff members of CMAC. Therefore, the study

included CMAC staff and Members of the Rwanda OTC Market. The survey popu

lation included 36 staff members of the selected capital market, the 44 members

from RSE, and 52 customers. So the total population is132 members who inter

viewed include loan officers, officers in charge of training, administrative officers,

and buyers and sellers who met in one place for the exchange of securities.

The study comprised of 150 respondents of which only 132 responded

representing an overall 88% which was considered to be adequate for arriving at

an informed decision.

To get a clear picture of the nature and accurate information about opera

tion of capital market advisory council in the development of financial sector in

Rwanda, the researcher gathered information from CMAC, RSE as operator in the

market and the data from CUSTOMERS.

Research instrument

This study utilized questionnaires to obtain data from the respondents.

The questionnaires designed and administered by the researcher. The question

naire included both closed and open-ended questions. This method was selected

because it is easy to administer questionnaires; it saves time, it helps to collect

information that was applicable to the study,

20

Research procedure

The researcher obtained an introductory letter from Kampala International

University and presented it to selected CMAC. Respondents especially the CMAC

staff consulted in advance in their respective places and appointments was made

to fill the questionnaires, The questionnaire has been done face to face with the

selected respondents.

Vall~dfty and Rell~abH~ty of the instruments

As mentioned earlier, the questionnaires have been used in collecting the

data for this study. In order to determine the validity of that instrument, an ex

ercise of data collection was firstly carried out using a group of people from an

area assumed to having similar characteristics as the sample of the study. In ad

dition, the instrument was presented to the supervisor for validation related to

face validity, content validity and the appropriateness and clarity of questions

and their ability to generate the required information. Afterwards, necessary

amendments were applied before the actual data collection process.

The reliability of questionnaires was tested using the Cronbach Alpha

Coefficient method of internal and the computed reliability coefficients will be

shown in the table (Cronbach, 1990).

Furthermore a content \Ialidity index was calculated as suggested by amin’s for

mula,

rCVI=

fl

Where: CVI is coefficient of validity index, R is the number of item declared valid,

and N as the total number of item.

21

Tabilel

Content VaNdity Index of The questions

Questbnnafre Content vaNd~ty index (CVI)

Items on the contribution of CMAC to

better financial intermediation in the 24

area, the market of development CVI= =0.857

services put in place by CMAC in order 28

to continue building the reputation as

an innovative financier, and

formulation of development program

base on the findings were 28

The table 2 above shows that out of 28 questions, 24 were proved valid and with

respect to Amin’s formula the content validity index is 0.857. Therefore, the instrument

was proved valid.

Data Gather~ng procedures

The data collection process started after the approval of the proposal and an

introduction letter was acquired from the office of the director of School of

postgraduate Studies and research.

22

The questionnaire was reviewed for possible typographical letter before

the distribution.

Finally the introduction letter was presented to the selected capital market advi

sory council office, to the general office of Rwanda stock exchange, and to some

financial institutions; and the researcher requested an opportunity to provide

explanations pertaining to his study and the questionnaire was distributed.

Given that the distribution of questionnaires was hard work, the researcher

looked for assistant to help him in the distribution of questionnaire in order to

ease the task.

Data anallys~s

The data was collected was scrutinized and edited to eliminate any errors.

The collected data was also coded; this is the process of translating edited res

ponses into numerical figure. A complete coding schedule was done to ensure

that various responses obtained classified into meaningful forms so as to bring

out the patterns that are essential clearly. The study also used both qualitative

and quantitative analysis. The research used the general tables, charts and per

centages to establish the relationship between CMAC and financial sector devel

opment programs.

In addition to that, Microsoft excel and SPSS were used for processinç1 and

analyzing of quantitative data. In the analysis, relationship between independent

variable of the study ant dependent variable was examined and analyzed using

tables, graphs, and charts.

Umitat~ons of the study

The limitations that the researcher proposes to be a countered during the

study include: The researcher personally administering the questionnaires and

this would spend a lot of time and well trained research assistants have be also

used.

23

Finding appropriate time to fill questionnaires was hard since the staff

members of the selected CMAC had other activities outside office and also during

office hours they can be busy with office work. For buyer and sellers served by

CMAC they can have limited time in their transactions .However the researcher

will arrange with the Members of the Rwanda stock exchange Market, The state

members of the selected capital market and buyer as well as sellers served by

CMAC when to fill the questionnaire.

They were instances of some respondents resisting completion of the

questionnaires due to fear of conflict of the regulatory authorities but since they

were assured of confidentiality the researcher got the necessary information. The

last limitation was that they were instance of the respondents delaying respond

ing to the questionnaires as they were no financial rewards. Despite all the

above impediments, sufficient and reliable data were collected witch made me

arrive at a better, meaningful and conclusive research study.

24

CHAPTER FOURPRESENTATION, ANALYSIS AND INERPRETATION OF DATA

ProfUe of RespondentsTable 2 presents data on the general profile of respondents.

The profile characteristics of interests in this study were age, gender,

occupation and profession of respondents were asked to provide their profile

information using a closed ended questionnaire and results were summarized

using frequencies and percentage distributions as indicated in table 2.

Tab~e 1

ProfNe of respondents

N=132

Category Frequency Percentage(%)

Gender Male 93 70Female 39 30

Age group Between20-35 10 7.536-65 113 85.565+ 9 7

Levd of EducationCertificate 5 4

Bach. Degree 90 68Masters 37 28

PhD 0 0occupation 4.2

~Businesspersons 93 7017

Civil servants 23 13

Others 11 58

Profession 36Stockbrokers 76 7

Dealers 47 36

Loan officers 9 7

Source~ Primary Data 2011

25

In Table 2 shows that the respondents covered by the research, male

were 93 (70%) while female constituted 39 (30) respectively and therefore, the

male population constituted the majority of respondents. The researcher needed

to know the age distribution of respondents to help categorize the respondents

in Rwanda capital market.

The research reveals that majority of respondents 113 (85~5 %) were

in the 36-65 years age bracket, followed by 10 (7~5%) in the 20-35 years age

bracket. The table also shows that 9 (7%) respondents were in 65+ year’s age

bracket.

The researcher also round it necessary to determine the educational levels

of the respondents as that is the main determinant of the buying and selling se

curities that is most appropriate for especially those participants with low levels

of education and fresh graduates. The level of both education and participants

determines to some extent the level of capital market development on one hand

and financial sector development in general.

Thus, from the table, it can he observed that respondents hold a range of

educational qualifications from High school certificates, Bachelors’ Degrees and

Masters’ Degrees. Most of the respondents constituting majority of the total res

pondents 90 (68%) have Bachelors’ Degrees, followed by those with Masters’

Degrees with 37 (28%) and 5 (4%) of the respondents are holders of high

school certificates and none of the respondents have PhDs. The differences in

qualifications determine the placement of respondents on different posts in

CMAC. Placement is also done with respect to the grade at which the post is and

the hierarchy of the administration. Senior management positions are occupied

by those with higher levels of education, training and experience whereas most

positions are held by junior officers with Bachelors’ Degrees and followed by

those with college certificates who serve as office messengers, cleaners and

26

kitchen staff. This hierarchy of administration (in form of grades) creates room to

carry out a SWOT staff analysis to ascertain improvement needs or promotion to

those that merit it and this help in promotion of CMAC and thus promotion of

financial sector in Rwanda.

The study also sought to find out the occupation of the respondents have

rendered to the organization to enable us put their responses into proper pers

pective. Table 2 above represents the categories of occupations in CMAC as indi

cated by the respondents. The study reveals that respondents who were busi

nesspersons were 93 (700/c), civil servants were 23(l7%), and others were 11

(l3%). Majority of respondents were businesspersons.

The study finally sought to find out the professions of the respondents

have participated to the organization to enable us put their responses into proper

perspective. Table 2 above represents the categories of professions in CMAC as

indicated by the respondents. The study reveals that respondents who were

stockbrokers were 76 (58°k), dealers were 47(36%), and loan officers were 9

(7%). Majority of respondents were stockbrokers.

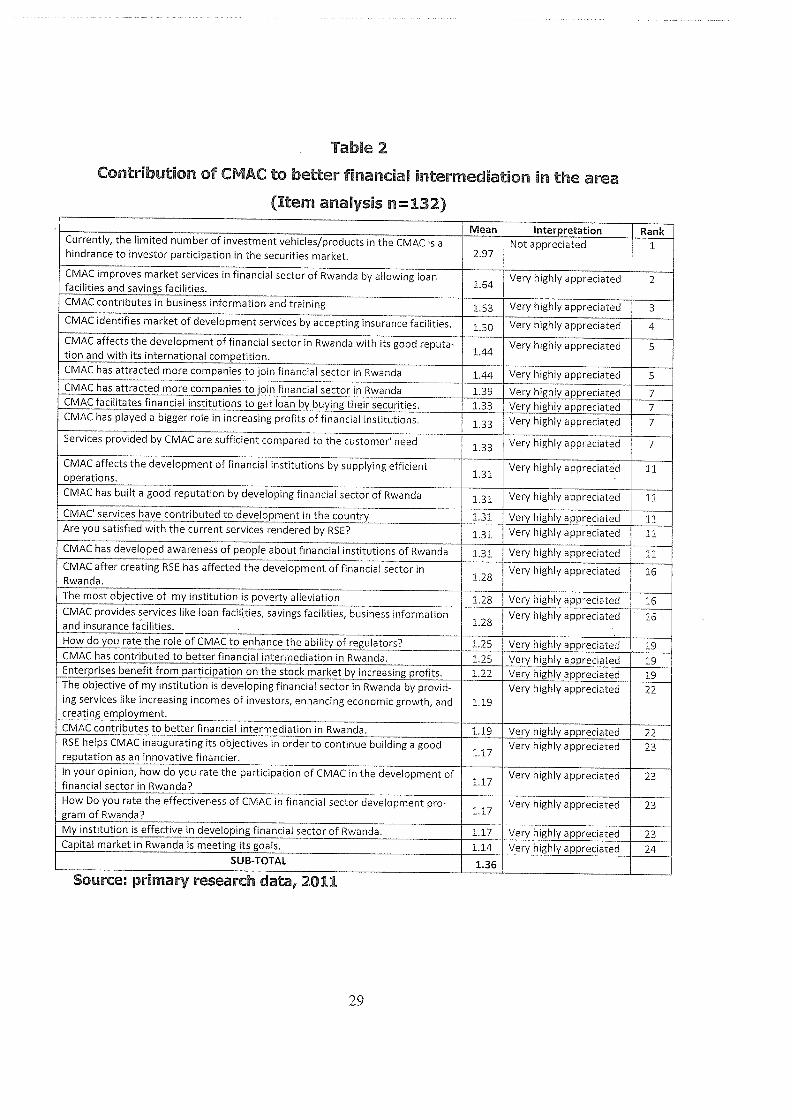

Contr~bution of CMAC to better flnanda~ intermed~atbn in the area

The second objective of this study was to determine how CMAC contribute

to better financial intermediation in the area. This was concerned with the devel

opment of awareness of people about financial institutions of Rwanda; how

CMAC has played a bigger role in increasing profits of financial institutions.

Following the results, we have obtained that there is a great contribution of

CMAC in financial intermediation. For example from April 2007 to March 2008,

many achievements were recorded, including, the minimum capital requirement

for banks was increased from RwF 1.5 billion to RwF 5.0 billion in order to in

crease the financial robustness and resilience of banks which are all complying

(www.cmac.org.rw).

27

The Central Bank Act through CMAC was amended to allow the BNR to re

gulate non-bank financial institutions, including insurance companies and pension

funds; prudential regulation and supervision is essential to promote confidence

and maintain the stability of the financial system (www.cmac.org.rw).

The Microfinance Policy implementation Strategy was completed to lay the

ground for the development of microfinance activities and a supporting Microfin

ance Law was submitted to Parliament. Government support to capacity building

and professional management will help increase access to finance by allRwan

dans and the efficient of microfinance institution. Also both credit and capacity

building funds for microfinance institutions were approved by the cabinet and will

be established soon to provide long-term sustainable refinancing access to MFIs

in form of external lines of credit and also enable MFIs access liquidity to invest

and obtain earnings. A capacity building fund on the other hand aims at develop

ing professional management and sustainability of microfinance institutions

(Rusagara, 2008). Table 3 concerned with the development of awareness of

people about financial institutions of Rwanda; how CMAC has played a bigger

role in increasing profits of financial institutions.

Following the below results, we have obtained that there is a great contri

bution of CMAC in financial intermediation with total mean of 1.36.

28

Tabile 2

Contr~bution of CMAC to better flnanda~ ~ntermed~at~on ~n the area

(Item anallysis n=132)

Mean Interpretation RankCurrently, the limited number of investment vehicles/products in the CMAC is a Not appreciated ihindrance to investor participation in the securities market. 2.97

CMAC improves market services in financial sector of Rwanda by allowing loan 1 64 Very highly appreciated 2facilities and savings facilities.CMAC contributes in business information and training 153 Very highly appreciated 3

CMAC identifies market of development services by accepting insurance facikties. 1.50 Very highly appreciated 4

CMAC affects the development of financial sector in Rwanda with its good reputa- 144 Very highly appreciated 5tion and with its international competition.CMAC has attracted more companies to join financial sector in Rwanda 1.44 Very highly appreciated 5

CMAC has attracted more companies to join financial sector in Rwanda 1.39 Very highly appreciated 7CMAC facilitates financial institutions to get loan by buying their securities. 1.33 Very highly appreciated 7CMAC has played a bigger role in increasing profits of financial institutions. 1.33 Very highly appreciated 7

Services provided by CMAC are sufficient compared to the customer need 1.33 Very highly appraciated 7

CMAC affects the development of financial institutions by supplying efficient 131 Very highly appreciated 11operations.CMAC has built a good reputation by developing financial sector of Rwanda 1.31 Very highly appreciated 11

CMAC services have contributed to development in the country 1.31 Very highly appreciated 11Are you satisfied with the current services rendered by RSE? 1.31 Very highly appreciated 11

CMAC has developed awareness of people about financial institutions of Rwanda 1.31 Very highly appreciated 11

CMAC after creating RSE has affected the development of financial sector in 1 28 Very highly appreciated 16Rwanda.The most objective of my institution is poverty alleviation — 1.28 Very highly appmciated 16CMAC provides services like loan facihties, savings facilities, business information 1 28 Very highly appreciated 16and insurance facilities. .

How do you rate the role of CMAC to enhance the ability of regulators? 1.25 Very highly appreciated 19CMAC has contributed to better financial intermediation in Rwanda. 1.25 Very highly appreciated 19Enterprises benefit from participation on the stock market by increasing profits. 1.22 Very highly appreciated 19The objective of my institution is developing financial sector in Rwanda by provid- Very highly appreciated 22ing services like increasing incomes of investors, enhancing economic growth, and 1.19creating employment.CMAC contributes to better financial intermediation in Rwanda. 1.19 Very highly appreciated 22RSE helps CMAC inaugurating its objectives in order to continue building a good 1.17 Very highly appreciated 23reputation as an innovative financmer.In your opinion, how do you rate the participahon of CMAC in the development of 1 17 Very highly appreciated 23financial sector in Rwanda? .

How Do you rate the effectiveness of CMAC in financial sector development pro- ~ 17 Very highly appreciated 23gram of Rwanda?My institution is effective in developing financial sector of Rwanda. 1.17 Very highly appreciated 23Capital market in Rwanda is meeting its goals. 1.14 Very highly appreciated 24

SUB-TOTAL 1.36

Source: pr~mary research data, 2011

29

Table 3 shows that all of the activities of CMAC were rated very hi~hly

by participants of RSE and bank clients, with the exception of CMAC products,

(See table 2). This is because CMAC products and vehicles were considered not

appreciated all of them by participants.

The most reasons for this are that there are still narrow scopes of in

vestment products on the security exchange market and thus create a disincen

tive for investment in capital market. Another reason is that all of the activities

are only based in Kigali. So businesspersons from other areas do not have oppor

tunity on regular publications on the current issues and listing requirements. So

the overall analysis revealed that there is very high contribution of CMAC to bet

ter financial intermediation in Rwanda. Following the objective one the research

revealed that there is high significant contribution of CMAC to better financial

intermediation with mean of 1.36.

Market of development servkes put ~n place by CMAC ~n order to con~

tinue buNding the reputation as an innovat~ve finander

The third objective of this study was to identify the market of develop

ment services put in place by CMAC in order to continue building a reputation as

an innovative financier. This was concerned with the services provided by CMAC

like loan facilities, savings facilities, business information and insurance facilities

on how they continue building the reputation as an innovative financier. The ta

ble 3 shows that all of the services rendered by CMAC were rated very highly by

members of CMAC, participants in RSE and bank clients, with the exception of

CMAC products that they disagree with the limitation of investment vehicles as a

hindrance to investor participation. (See table 3).The results are presented in

ta ble3.

Table 3

Identification of the CMAC market of development services

(n=132)

~__F.I Mean Inter RankCurrently, the limited number of investment vehicles/products in the CMAC 2 7~ Low 1is a hindrance to investor participation in the securities market.CMAC contributes in business information and training 1.63 High 2~.CMAC improves market services in financial sector of Rwanda by allowing 1 (2 High 3loan facilities and savings facilities.CMAC identifies market of development services by accepting insurance 1 (2 High 3facilities.CMAC affects the development of financial sector in Rwanda with its good ~ High 5reputation and with its international competition. 3

Services provided by CMAC are sufficient compared to the customer need 1.29 High 6RSE helps CMAC inaugurating its objectives in order to continue building a 1 25 High 7good reputation as an innovative financier.CMAC after creating RSE has affected the development of financial sector ii~ 1 17 High 8Rwanda.In your opinion, how do you rate the participation of CMAC in the develop- 1 17 High 8ment of financial sector in Rwanda?~ 1.17 High 8The most objective of my institution is poverty alleviation 1.17 High 8CMAC provides services like loan facilities, savings facilities, business in- 1 15 High 12formation and insurance facilities.Are you satisfied with the current services rendered by RSE? 1.13 High 13

CMAC has contributed to better financial intermediation in Rwanda. 1.13 13CMAC’ services have conti~ibuted to development in the country 1.13 High 13CMAC has built a good reputation by developing financial sector of Rwanda 1.12 High 16Enterprises benefit from participation on the stock market by increasing prof. 1 12 High 16its.CMAC has attracted more companies to join financial sector in Rwanda 1.10 High 18

CMAC affects the development of financial institutions by supplying effi- 1 10 High 18cient operations.How do you rate the role ofCMAC to enhance the ability of regulators? 1.10 High 18

CMAC has played a bigger role in increasing profits of financial institutions. 1.10 High 18CMAC has developed awareness of people about financial institutions of 1 10 High 18RwandaCMAC contributes to better financial intermediation in Rwanda, 1 .08 High 23Capital market in Rwanda is meeting its goals. 1.06 High 24

How Do you rate the effectiveness of CMAC in financial sector development 1 06 High 24program of Rwanda? .

CMAC facilitates financial institutions to get loan by buying their securities. 1.06 High 24My institution is effective in developing financial sector ofRwanda. 1.04 High 27The objective of my institution is developing financial sector in Rwanda by High 28providing services like increasing incomes of investors, enhancing economic 1.02growth, and creating employment.

SUB-TOTAL 1.24Source: primary research data, 2011.

3

Following the results given by respondents in the table 3 above CMAC

provides the market of development services like loan facilities, savings facilities,

business information and insurance facilities, increasing incomes of investors,

enhancing economic growth, and creating employment, the research revealed

that CMAC is very significant in building the reputation as an innovative financier

with the mean of 1.2411.

The results revealed also that CMAC provides services like loan facilities,

savings facilities, business information and insurance facilities and it continues

building the good reputation as an innovative financier (www.CMAC.rw), This

was concerned with the services provided by CMAC like loan facilities, savings

facilities, business information and insurance facilities on how they continue

building the reputation as an innovative financier. The results on the table 3

which shows that CMAC is very significant in building the reputation as an inno

viate finance

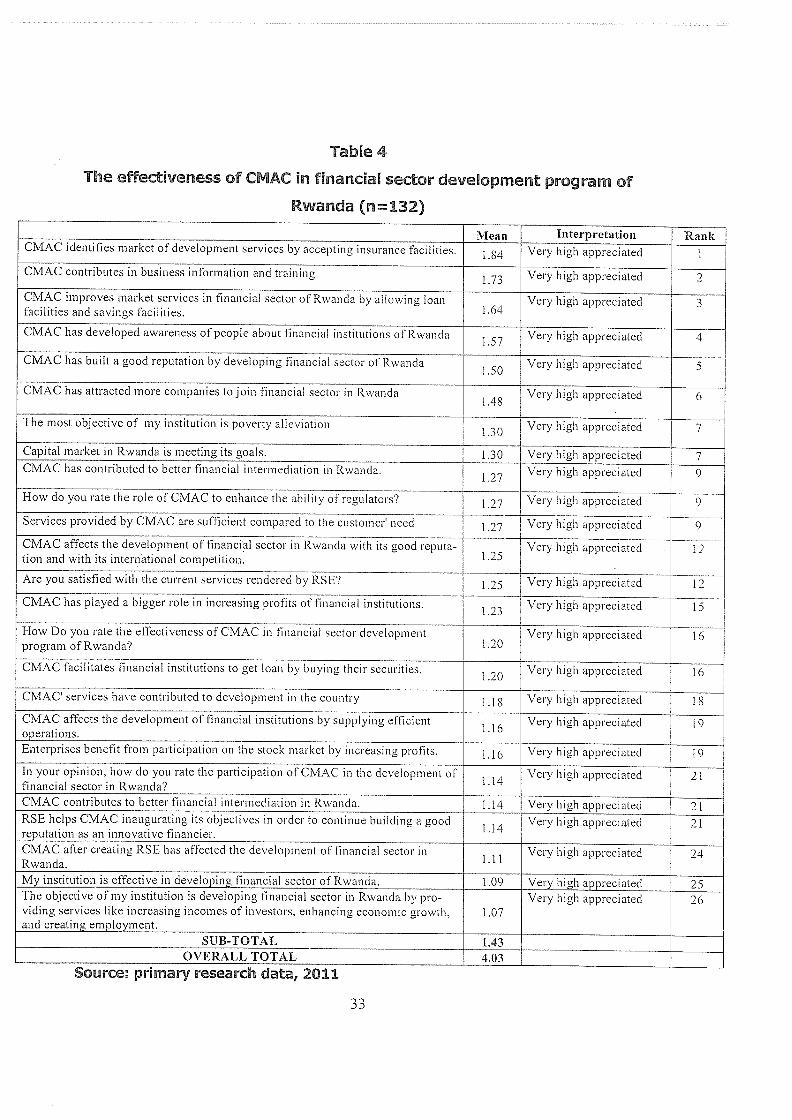

The effectiveness of CMAC ~n finandall sector dev&opment program of

Rwanda

The fourth objective was to the effectiveness of CMAC in financial sector devel

opment program of Rwanda.This was concerned with the participant’s views in

Rwanda stock exchange market. Kigali, as the campaign to promote a saving

culture among the Rwandan population intensifies; the Capital Markets Advisory

Council (CMAC) has welcomed the initiative as timely and important. CMAC the

body charged with the regulation of the capital markets in Rwanda as well as

ensuring long term savings says the campaign will boost the overall national sav

ings (www.cmac.org.rw). The responses were presented in the table 4.10:

Tabile 4

The effectiveness of CMAC hi finandall sector devebpment program of

Rwanda (n=132)

CMAC improves market services in financial sector of Rwanda by allowing loan Very high appreciated 3facilities and savings facilities. 1.64

CMAC has developed awareness of people about financial institutions of Rwanda 1 57 Very high appreciated 4

CMAC has built a good reputation by developing financial sector of Rwanda 1 50 Very high appreciated 5

CMAC has attracted more companies to join financial sector in Rwanda 1 48 Very high appreciated 6

The most objective of my institution is poverty alleviation 1.30 Very high appreciated — 7

Capital market in Rwanda is meeting its goals. 1.30 Very high appreciated 7CMAC has contributed to better financial intermediation in Rwanda. 1.27 Very high appreciated 9

How do you rate the role of CMAC to enhance the ability of regulators? 1~7 Very high appreciated 9

Services provided by CMAC are sufficient compared to the customer need 1.27 Very high appreciated 9

CMAC affects the development of financial sector in Rwanda with its good reputa- Very high appreciated 12tion and with its international competition. 1.25

Are you satisfied with the current services rendered by RSE? 1.25 Very high appreciated 12

CMAC has played a bigger role in increasing profits of financial institutions. 1 23 Very high appreciated 15

How Do you rate the effectiveness of CMAC in financial sector development Very high appreciated 16program of Rwanda? 1.20

CMAC facilitates financial institutions to get loan by buying their securities. 1 20 Very high appreciated 16

CMAC’ services have contributed to development in the country 1.18 Very high appreciated 18

CMAC affects the development of financial institutions by supplying efficient 1 16 Very high appreciated 19operations. . —~

Enterprises benefit from participation on the stock market by increasing profits. 1.16 Very high appreciated 19

In your opinion, how do you rate the participation of CMAC in the development of 1 14 Very high appreciated 21financial sector in Rwanda?CMAC contributes to better financial intermediation in Rwanda. 1.14 Very high appreciated — 21RSE helps CMAC inaugurating its objectives in order to continue building a good 1 14 Very high appreciated 21reputation as an innovative financier.CMAC after creating RSE has affected the development of financial sector iii 1 11 Very high appreciated 24Rwanda.My institution is effective in developing financial sector of Rwanda. 1.09 Very high appreciated 25The objective of my institution is developing financial sector in Rwanda by pro- Very high appreciated 26viding services like increasing incomes of investors, enhancing economic growth. 1.07and creating employment.

SUB-TOTAL 1.43OVERALL TOTAL 4.03

_____________________________ Mea aCMAC identifies market of development services by accepting insurance facilities. 1.84

CMAC contributes in business information and training

— InterpretationVery high appreciated

Very high appreciated

Rank

2

Source: primary research data, 2011

The table 4 revealed that all of the participants either in CMAC, RSE or the

clients of the banks have appredated the creation of CMAC and RSE in the pro

motion of financial sector in Rwanda with a mean of 1.4310 (see table 4.) This

high significant relationship between CMAC and financial sector development

program pushed a researcher to formulate the following development program:

expanding access to credit and financial services to the whole population across

the country in both urban and rural areas, enhancing savings mobilization, espe

cially long-term savings; and, Channeling long-term capital for productive in

vestments.

Capital Markets Advisory Council (CMAC) has welcomed the initiative as

timely and important. CMAC the body charged with the regulation of the capital

markets in Rwanda as well as ensuring long term savings says the campaign will

boost the overall national savings (www.cmac.org.rw). The responses were pre

sented in the table 4. The results revealed that this program includes Quality

services for fund managers, institutions, banks, corporations, government agen

cies, endowments and foundations, and high-net-worth individuals, and this re

vealed that there is high Significance relationship between Capital market Advi

sory Council and Financial sector development program using the participant’s

views in Rwanda stock exchange market with the mean of 1.43.

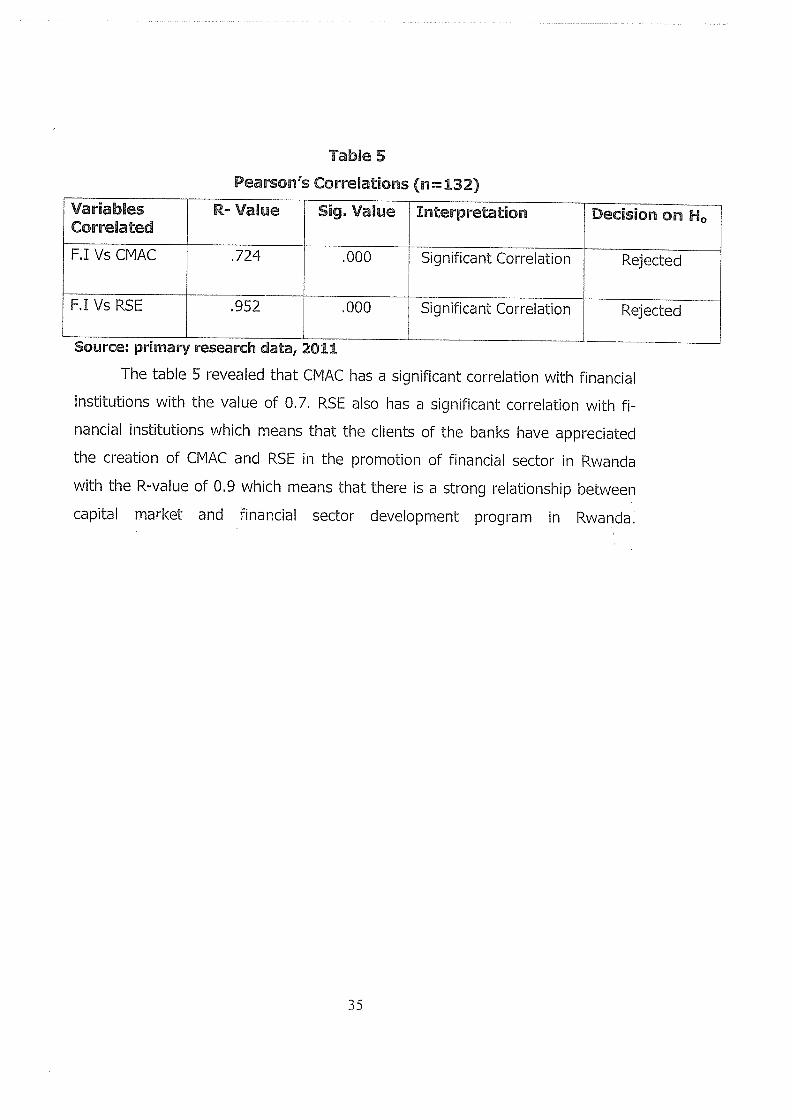

Significance relationship between Capital market Advisory Council and

Financial sector development program using the participant’s views in

Rwanda stock exchange market

Table 5 shows a significant relationship between CMAC, RSE and financial

institutions. CMAC is correlated with the financial institutions on the mean value

of 0.7. RSE also has a significant correlation with financial institution with the

mean value of 0.9 which means that the clients of the banks have appreciated

the creation of CMAC and RSE in the promotion of financial sector in Rwanda

with the R-value of 0.9.the results are shown in the tableS,

34

Pearson’s

Table 5

Correlations (n=132)

Variables R~ Value Sign Value Interpretation Decision on H0Correlated

F.I Vs CMAC .724 .000 Significant Correlation Rejected

F.I Vs RSE .952 .000 Significant Correlation Rejected

Source: primary research data, 2011

The table 5 revealed that CMAC has a significant correlation with financial

institutions with the value of 0.7. RSE also has a significant correlation with fi~

nancial institutions which means that the clients of the banks have appreciated

the creation of CMAC and RSE in the promotion of financial sector in Rwanda

with the R-value of 0.9 which means that there is a strong relationship between

capital market and financial sector development program in Rwanda

35

CHAPTER FIVE

FINDINGS, CONCLUSION, RECOMMENDATIONS

The study was carried out to evaluate the effectiveness of the CMAC on

financial sector development program of Rwanda, The findings from the study

revealed that there is a strong significant relationship between Capital market

advisory council and financial sector development program of Rwanda. The ob

jectives of the study were to evaluate the effectiveness of capital market advi

sory council (CMAC) in financial sector development program in Rwanda, to de

termine the profile of respondents, to determine how CMAC contribute to better

financial intermediation in the area, to identify the market of development ser

vices put in place by CMAC in order to continue building the reputation as an in

novative financier, to formulate development program base on the findings of

the study. The above intended objectives of the study were followed in the

course of conducting the research.

FINDINGS

Following the main objective of the study which intended to study the ef

fectiveness of capital market advisory council (CMAC) in financial sector devel

opment program in Rwanda, the findings of the study revealed that the introduc

tion of capital market advisory council and the creation of Rwanda stock ex

change market are efficient in the development of financial sector in the country.

So, the research revealed that there is a strong relationship between Capi

tal market and development of financial sector development program in Rwanda

because CMAC, through its stock exchange market will help to facilitate financial

institutions to get loans by buying securities, to provide services like increasing

incomes of investors, enhancing economic growth, and creating employment, to

increase the profits of financial institutions, and to attract more financial compa

nies to join Rwanda stoc~k exchange market.

36

The objective one of the study intended to determine the profile of the

respondents in terms of their sex, their age, their level of education, and their

occupation in their respective organizations.

The findings revealed that both CMAC, RSE as well as in Fl, majority of

respondents were between 46-55 years old. CMAC had 42%, while F.I had 35%

and RSE with 57%. The findings also revealed that in CMAC, RSE, and F.I, the

number of male overweighed the number of female with respective percentages

of 77% in RI, 72% in CMAC and 61°k in RSE. So, the average percentage was

70% of male. The findings also revealed that majority of the respondents hold

tertiary level of education that is batcher’s degree and above. In F,I they were

6l.5%, while in CMAC were 94.4% and in RSIE were 54.5%. The findings also,

revealed that more of respondents were businesspersons with 76%in F.I 69% in

CMAC, and 645 in RSE,

Following the second objective which was to determine how CMAC contri

bute to better financial intermediation, the study revealed that CMAC supplies

efficient operations, developing financial sector in Rwanda by providing services

like increasing incomes of investors, enhancing economic growth, and creating

employment, and also greater access to credit will further fuel the construction

boom that accounts for much of the economic growth currently being recorded

in Kigali. So this shows that CMAC contributes match to better financial intermed

iation. (www.rse.Co.rw)

Furthermore, following the third objective which was to identify the market of

development services put in place by CMAC in order to continue building the

reputation as an innovative financier, the study revealed that this was concerned

with the services provided by CMAC like loan facilities, savings facilities, business

information and insurance facilities to the buyers and sellers of stocks and they

have contributed to development in the country.

37

The last objective was to formulate development program base on the

findings, the study revealed that this program includes Quality services for fund

managers, institutions, banks, corporations, government agencies, endowments

and foundations, and high-net-worth individuals.

Thus the general conclusion of the findings was that CMAC is efficient in the de

velopment of financial sector in the country, and the living standards of the pop

ulation too, This however ~s because CMAC’services have contributed to devel

opment in the country, CMAC improves services in financial sector of Rwanda by

allowing loan facilities and savings facilities, contributes in business information

and training, identifies market of development services by accepting insurance

facilities.

CONCLUSONS

The capital market advisory and Rwanda stock exchange market have a

significant relationship and are also effective to the financial sector development

program of Rwanda. This is because by its creation savings and investment have

increased constantly. There is agreement between the theory and the practice of

CMAC, RSE in the promotion of financial sector in Rwanda. This has motivated

more companies/organizations to the listing on the security market.

Furthermore the theory states that a company has to be in operation and must

have published its audited statements for at least one year and must be profita

ble to be eligible for listing. This has been major incentive for companies to list

their securities on the security market and the public investing in such securties.

Also other incentives would include withholding tax exemption on dividends iaid

by listed companies, reduced corporation tax rate for listed companies and ex

emption from value added tax for supplies supplied by listed companies.

The Rwandan financial sector also should present adequate institutional, organi

zational and human capacity so as to give potentiality to investors to list the enti

ties on the stock exchange.

Finally the researcher saw the possibility that there would be increased

concern by major institutional investors that would cause funds to beef up their

business practices.

RECOMMENDATIONSThe findings revealed that there have been major incentives for compa

nies to list their securities on the security market and the public investing in such

securities, however, lack of trust and confidence, limited incentives for listed

companies. In order to enable a smooth transition into the effective operation of

capital market in Rwanda there is need to implement the following policy rec

ommendations.

There is a need to develop the confidence in the public for investing in

capital market by the increased public awareness aimed at educating the public

about CMAC and RSE operations. Development of an effective legal system toincrease the safety and complete removal of uncertainty regarding the benefits

of the resulting investments, guaranteed stable banking sector, enforcement of

capital market regulations so that there is continued encouragement of the pub

lic in the bond market,

Capital market advisory council and Rwanda stock exchange market

should develop a documentary highlighting those organizations that have in

vested in stocks and their benefits. For instance shareholders who invested mas

sively in RSE, BRALIRWA, BK and in KCB, when the stocks were first introduced.

The last recommendation is that decentralization is a strong key to development.

Currently the capital market advisory council and Rwanda stock exchange are

located in Kigali and so are all the brokerage firms. They should make the cam

paign as they travel to other regions.

Furthermore, the government should speed up the process of divestiture process

of the underperforming government parastatals. This process will attract poten

tial investors who will inject in the operations of such companies substantial

amounts of money, turning around the company and thus leading to the overall

development of the country

AREAS FOR FURTHER RESEARCH

This research insisted on capital market advisory council and financial sector de

velopment program. However the researcher will assess the relationship between

capital market and the performance of the listed companies on the security ex

change.

The researcher will assess the relationship between the listed companies on the

development of the Rwandan economy.

40

REFERENCES

Amin, E.M., (2005), 5oci~l science research: conception,, methodology and analy

sLs 1st ed, Kampala: Makerere University.

Anu p1 ndi, Ravi, et a I. Managing Business Process Flows: Principles of Operations

Management. 2nd ed. Upper Saddle River, NJ: Pearson Prentice Hall,

2004.

Bertalanffy, V. L. (1968), General Systems Theory, New York: Braziller. available

on http://pespmcl.vub.ac.be/systheorhtml

Harris, F. W. Operatio)7s Cost (Factory Management Series), Chicago: Shaw

(1915).

Harris, F.W. How Many Parts To Make At Once Factory, The Magazine of Man

agement, 10(2), 135-136, 152 (1913).

http://enwikipedia.org.wiki, free encyclopedia retrieved 30 May 2010

Laszlo, E. (1972). The systems view of the world The natural philosophy of the

new developments in the sciences. New York: George Brazillier.

MINECOFIN (2009), Program Information Document (PID), Kigali, Report No.:

AB4542.

Rusagara, C. (2008), Financial Sector Development Program (FSDP): Case of

Rwanda, Kigali: NBR.

Wilson, R. H. A Scientific Routine for Stock Control” Harvard Business Review,

13, 116-128

Joseph Ki nyua,” Business Process Flows: Principles of Operations Management.

2nd ed. Upper Saddle River, NJ: Pearson Prentice Hall, 2004.

41

Alile H. I.(1992): “Establishing a stock market : Nigerian Experience, presented

at an International conference on” Promoting Capital Markets in Africa’~

Abuja, Nigeria, 11-13 November 1992.