capital management issues and icaap - finity consulting€¦ · to further segment the analysis we...

TRANSCRIPT

Capital Management Issues

and ICAAP

Scott Collings

18 October 2012

Copyright 2012 | Finity Consulting

2

Agenda

Capital Adequacy - Recent industry experience

Implications of new LAGIC rules

• Investment strategy

• Reinsurance

• Capital structure

ICAAP – setting capital management trigger levels

3

Capital Adequacy Trends

An exciting decade for Industry capital

Started with HIH imploding, Royal Commission

APRA and a new prudential regime introduced ‘02

The Good times:

• tort reform, benign event experience and solid

investment markets

Were followed by the Not So Good times:

• Heavy natural event experience, GFC, poor

investment markets and sharply lower interest rates

. . . and then came LAGIC . . .

4

Capital Adequacy Trends

Analysis of insurer solvency trends

Using APRA and ISC company level data

Analysis restricted to only active ‘typical’ insurers

• Excluded: runoff, LMI, Medical, Captives

• Results weighted by minimum capital requirement

5

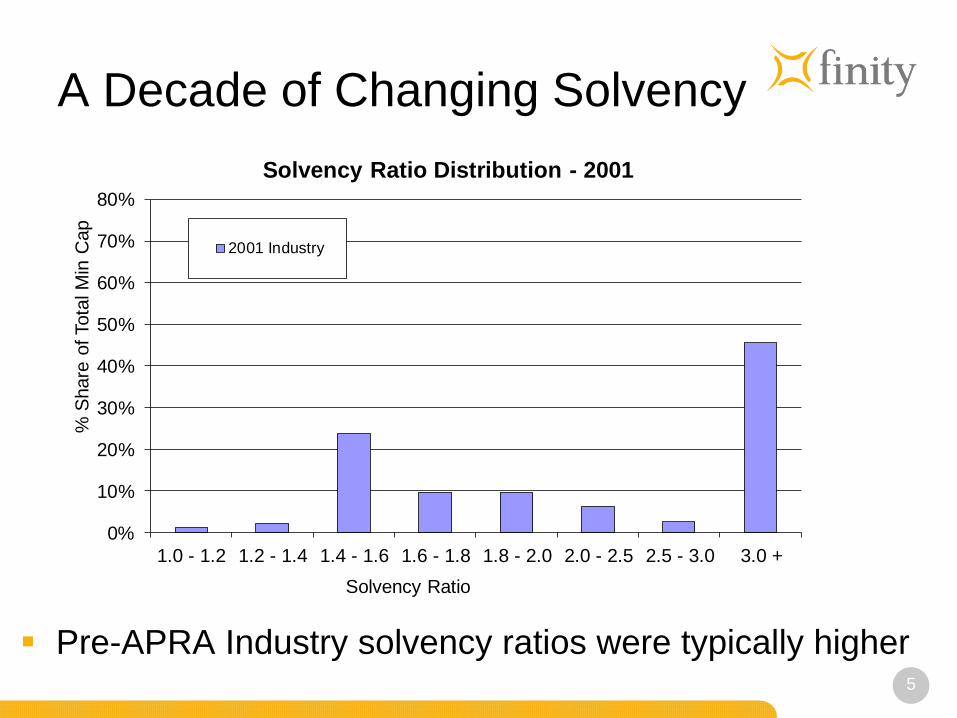

A Decade of Changing Solvency

Pre-APRA Industry solvency ratios were typically higher

0%

10%

20%

30%

40%

50%

60%

70%

80%

1.0 - 1.2 1.2 - 1.4 1.4 - 1.6 1.6 - 1.8 1.8 - 2.0 2.0 - 2.5 2.5 - 3.0 3.0 +

% S

hare

of Tota

l M

in C

ap

Solvency Ratio

Solvency Ratio Distribution - 2001

2001 Industry

6

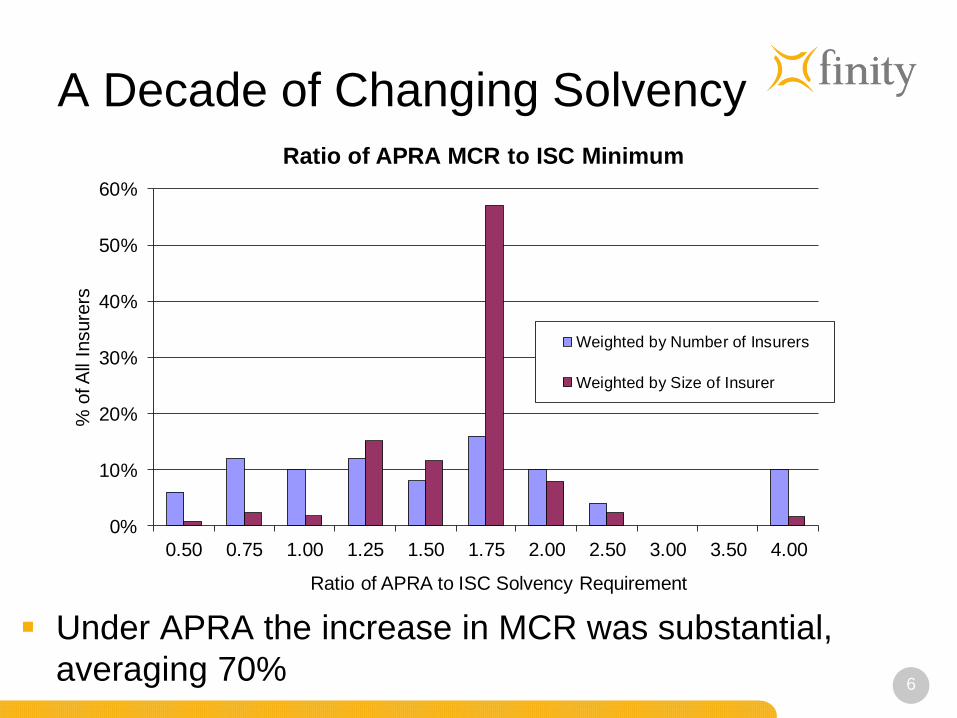

A Decade of Changing Solvency

Under APRA the increase in MCR was substantial,

averaging 70%

0%

10%

20%

30%

40%

50%

60%

0.50 0.75 1.00 1.25 1.50 1.75 2.00 2.50 3.00 3.50 4.00

% o

f A

ll In

sure

rs

Ratio of APRA to ISC Solvency Requirement

Ratio of APRA MCR to ISC Minimum

Weighted by Number of Insurers

Weighted by Size of Insurer

7

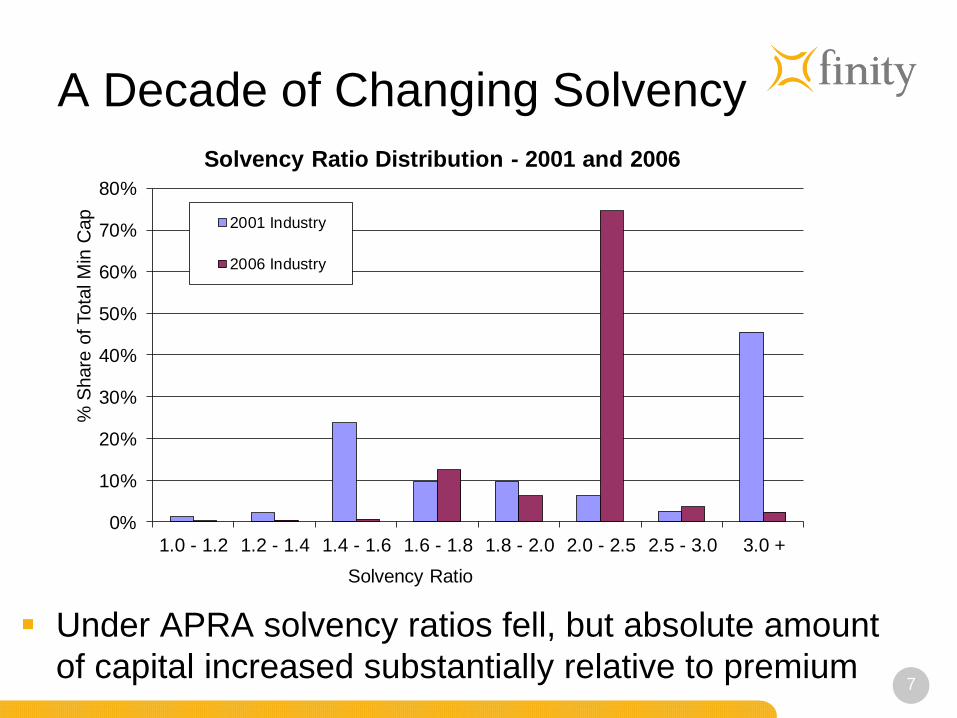

A Decade of Changing Solvency

Under APRA solvency ratios fell, but absolute amount

of capital increased substantially relative to premium

0%

10%

20%

30%

40%

50%

60%

70%

80%

1.0 - 1.2 1.2 - 1.4 1.4 - 1.6 1.6 - 1.8 1.8 - 2.0 2.0 - 2.5 2.5 - 3.0 3.0 +

% S

hare

of Tota

l M

in C

ap

Solvency Ratio

Solvency Ratio Distribution - 2001 and 2006

2001 Industry

2006 Industry

8

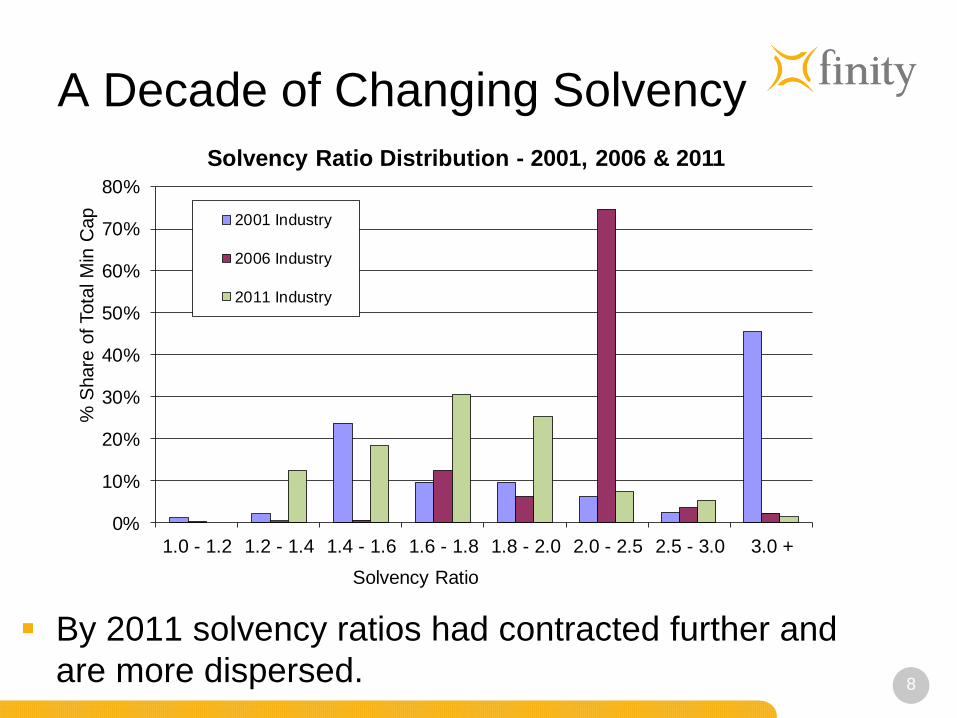

A Decade of Changing Solvency

By 2011 solvency ratios had contracted further and

are more dispersed.

0%

10%

20%

30%

40%

50%

60%

70%

80%

1.0 - 1.2 1.2 - 1.4 1.4 - 1.6 1.6 - 1.8 1.8 - 2.0 2.0 - 2.5 2.5 - 3.0 3.0 +

% S

hare

of Tota

l M

in C

ap

Solvency Ratio

Solvency Ratio Distribution - 2001, 2006 & 2011

2001 Industry

2006 Industry

2011 Industry

9

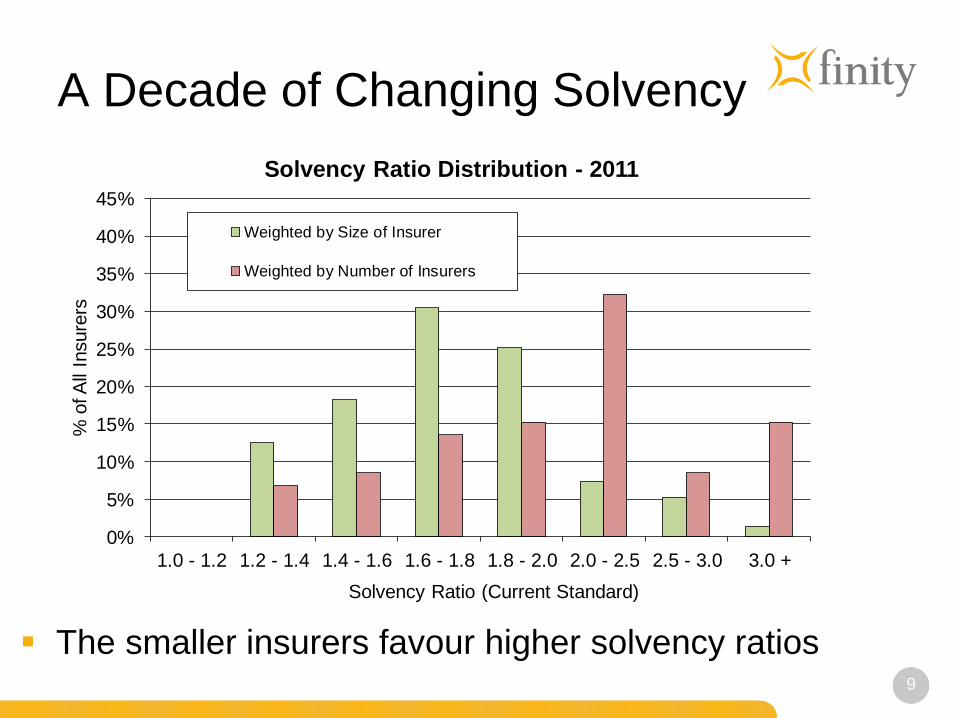

A Decade of Changing Solvency

The smaller insurers favour higher solvency ratios

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

1.0 - 1.2 1.2 - 1.4 1.4 - 1.6 1.6 - 1.8 1.8 - 2.0 2.0 - 2.5 2.5 - 3.0 3.0 +

% o

f A

ll In

sure

rs

Solvency Ratio (Current Standard)

Solvency Ratio Distribution - 2011

Weighted by Size of Insurer

Weighted by Number of Insurers

10

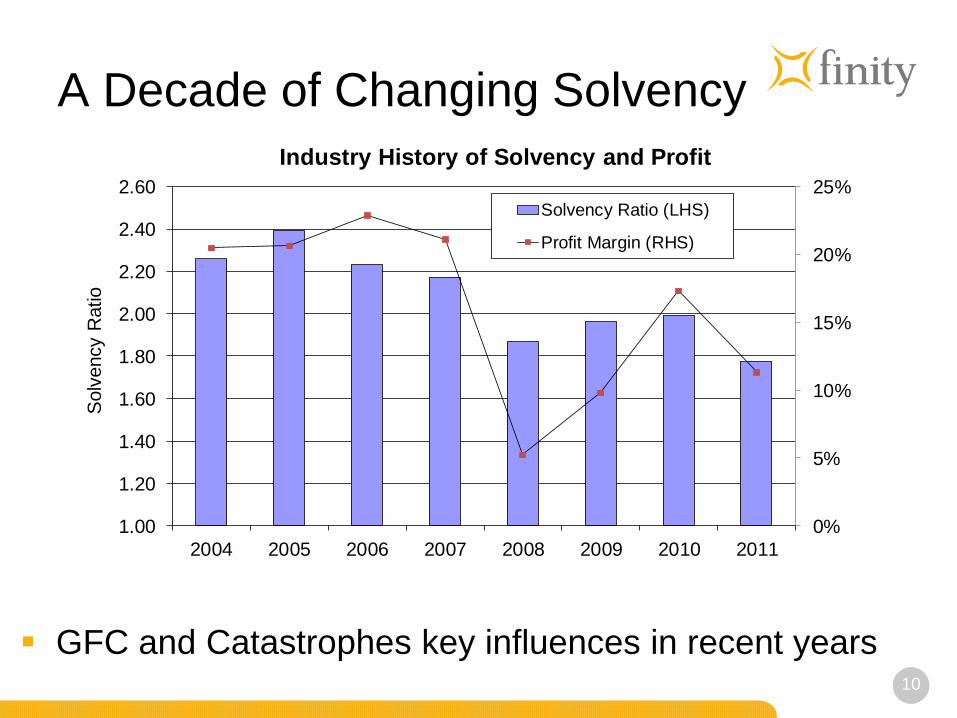

A Decade of Changing Solvency

GFC and Catastrophes key influences in recent years

0%

5%

10%

15%

20%

25%

1.00

1.20

1.40

1.60

1.80

2.00

2.20

2.40

2.60

2004 2005 2006 2007 2008 2009 2010 2011

Solv

ency R

atio

Industry History of Solvency and Profit

Solvency Ratio (LHS)

Profit Margin (RHS)

11

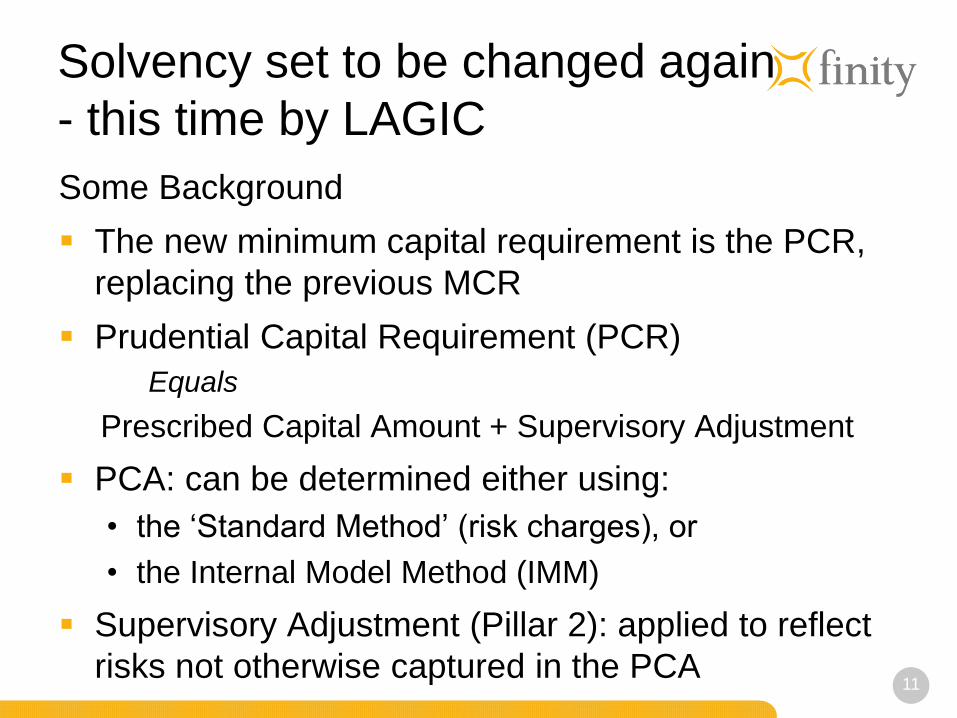

Solvency set to be changed again

- this time by LAGIC

Some Background

The new minimum capital requirement is the PCR,

replacing the previous MCR

Prudential Capital Requirement (PCR)

Equals

Prescribed Capital Amount + Supervisory Adjustment

PCA: can be determined either using:

• the ‘Standard Method’ (risk charges), or

• the Internal Model Method (IMM)

Supervisory Adjustment (Pillar 2): applied to reflect

risks not otherwise captured in the PCA

12

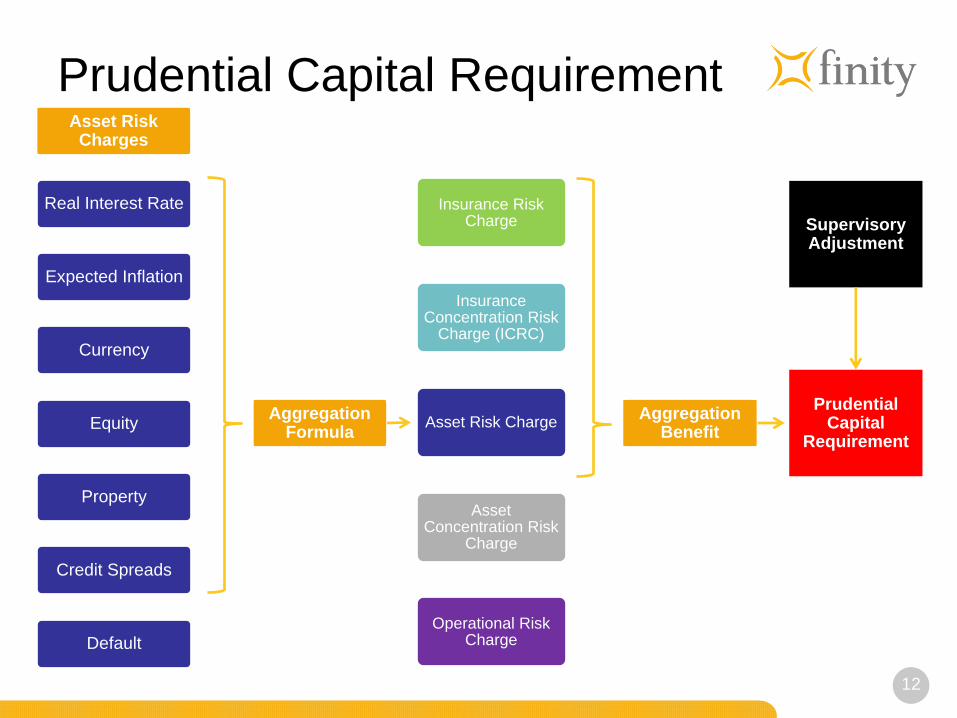

Prudential Capital Requirement

Real Interest Rate

Expected Inflation

Currency

Equity

Property

Credit Spreads

Default

Asset Risk Charges

Aggregation Formula

Insurance Risk Charge

Insurance Concentration Risk

Charge (ICRC)

Asset Risk Charge

Asset Concentration Risk

Charge

Operational Risk Charge

Aggregation Benefit

Prudential Capital

Requirement

Supervisory Adjustment

13

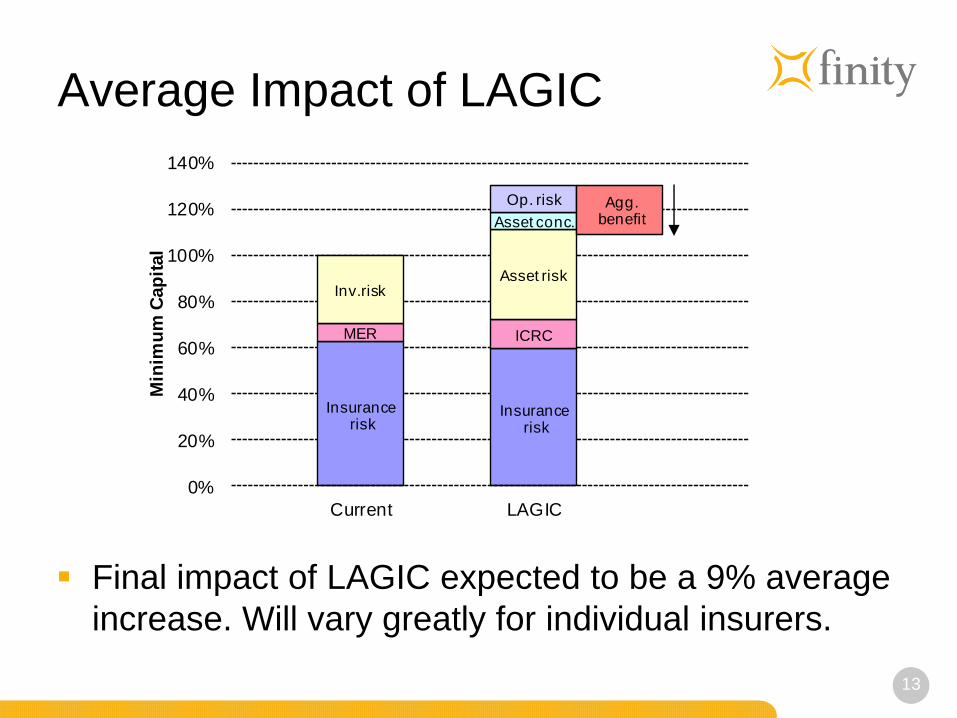

Average Impact of LAGIC

Final impact of LAGIC expected to be a 9% average

increase. Will vary greatly for individual insurers.

Insurancerisk

Insurancerisk

MER ICRC

Inv.riskAsset risk

Asset conc.

Op. risk Agg. benefit

0%

20%

40%

60%

80%

100%

120%

140%

Current LAGIC

Min

imu

m C

ap

ital

14

Equity Investment Risk Charges

The Asset Risk formula is now more complex

• Current rule is a 20% charge on value of equities

• New rule is: Value x (1 – d / D)

• Where d = current dividend yield on ASX200, and

• D= stressed dividend yield = d - 2.5%

The new ‘effective’ charge varies, depending on:

• Other types of investments held due to the asset risk

aggregation (diversification) formula, and

• Liability risk charges due to the ‘aggregation benefit’

We have modelled the new risk charge formula to

compare it with the existing basis.

• Observed range of div yields last 5 years in asx200

15

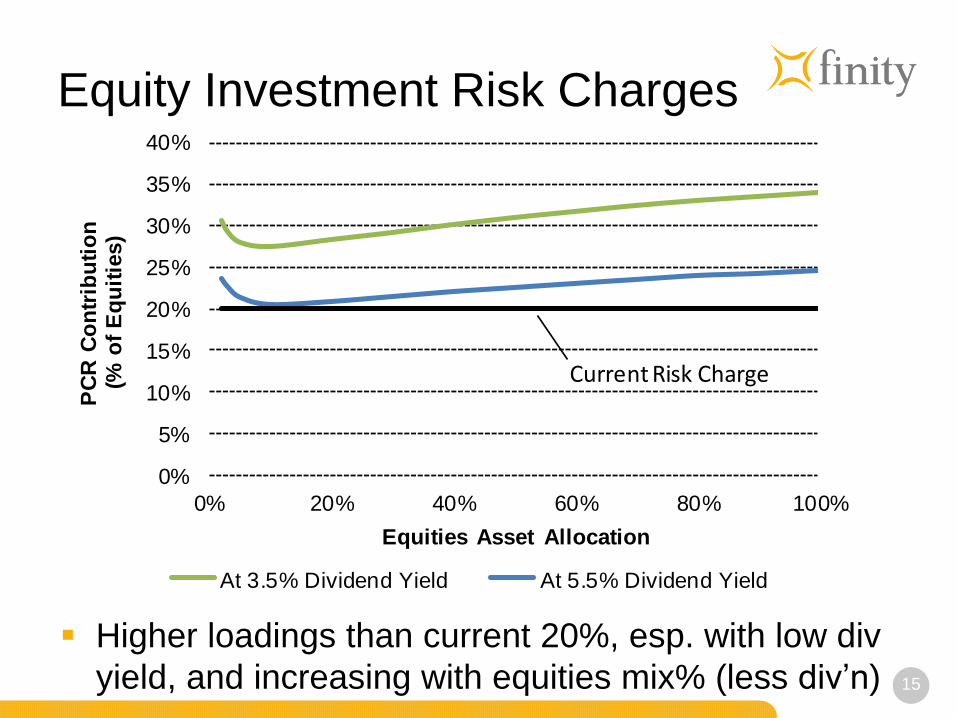

Equity Investment Risk Charges

Higher loadings than current 20%, esp. with low div

yield, and increasing with equities mix% (less div’n)

0%

5%

10%

15%

20%

25%

30%

35%

40%

0% 20% 40% 60% 80% 100%

PC

R C

on

trib

uti

on

(%

of

Eq

uit

ies)

Equities Asset Allocation

At 3.5% Dividend Yield At 5.5% Dividend Yield

Current Risk Charge

16

Duration Matching Risk Charge Actually 2 different asset risk charges:

• Real interest rate charge

• Revalue assets and liabilities cashflows

• Stresses = +0.25 and -0.20 x nominal rate

• Added to nominal discount rates and real rates,

• Expected inflation risk charge

• Stresses = +1.25% and -1.00%

• Added to nominal disc rates and expected inflation

The net effect of these produces a charge linked to

difference between Liability duration and Investment

Asset duration

17

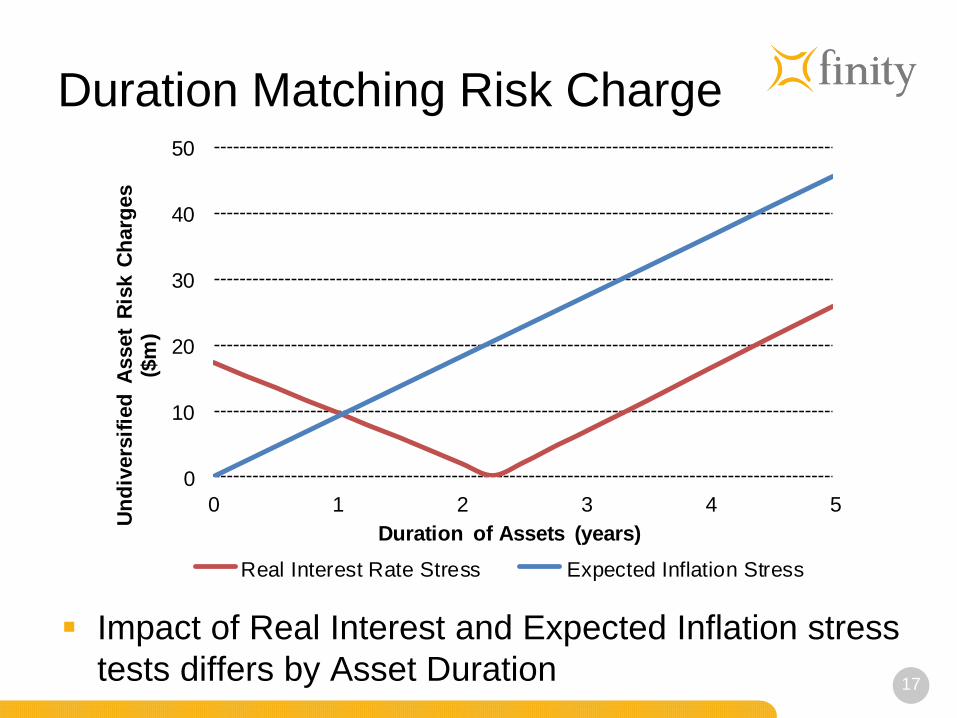

Duration Matching Risk Charge

Impact of Real Interest and Expected Inflation stress

tests differs by Asset Duration

0

10

20

30

40

50

0 1 2 3 4 5

Un

div

ers

ifie

d A

sset

Ris

k C

harg

es

($m

)

Duration of Assets (years)

Real Interest Rate Stress Expected Inflation Stress

18

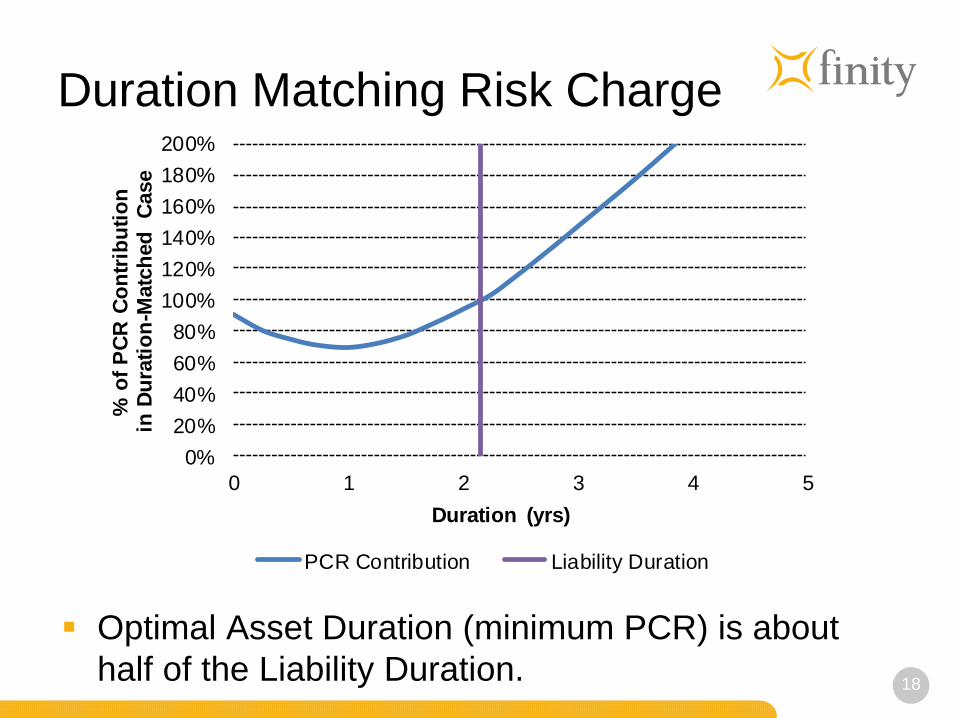

Duration Matching Risk Charge

Optimal Asset Duration (minimum PCR) is about

half of the Liability Duration.

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

0 1 2 3 4 5

% o

f P

CR

Co

ntr

ibu

tio

nin

Du

rati

on

-Matc

hed

C

ase

Duration (yrs)

PCR Contribution Liability Duration

19

Liability Concentration Risk Maximum Event Retention (MER) to be replaced by Insurance

Concentration Risk Charge (ICRC) for accumulation exposures

For those with ‘natural perils’ exposure there will be a vertical

requirement (similar to MER) and a horizontal requirement

Vertical considers 1-in-200 year event (WOP)

Horizontal consists of 2 tests

• H(3) considers three 1-in-10 year events

• H(4) considers four 1-in-6 year events

• Net off the amount of annual ‘expected’ event costs

• Based on assumptions in the premium liability valuation

• Horizontal only applies from 1 January 2014

Most insurer’s have property cat retentions below 1-in-6 year events

• Therefore, H(4) will typically be the most important calculation

20

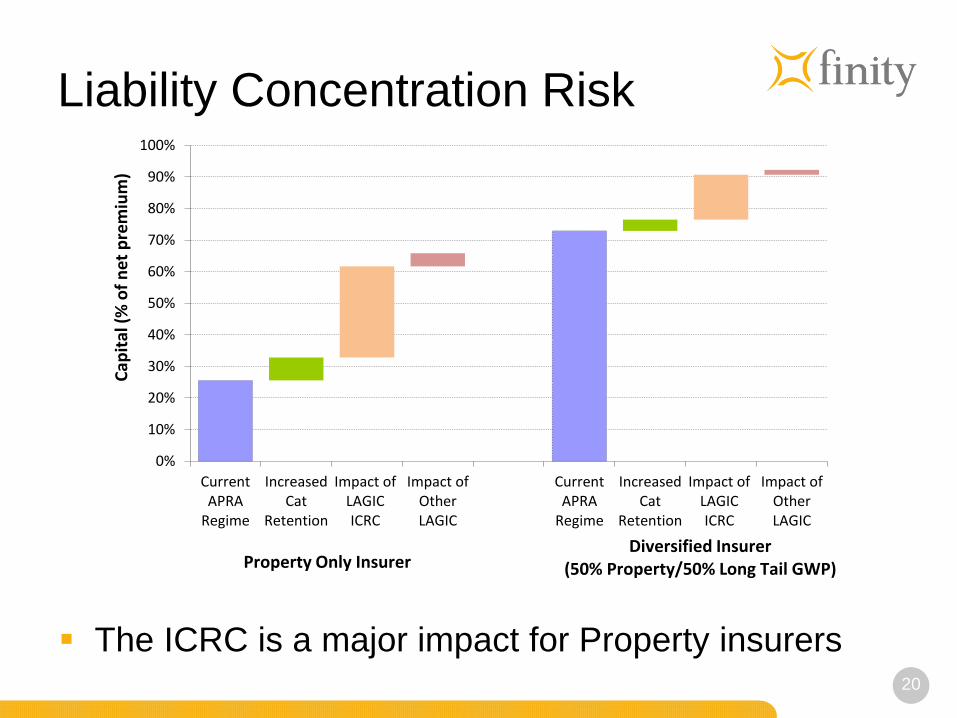

Liability Concentration Risk

The ICRC is a major impact for Property insurers

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

CurrentAPRA

Regime

IncreasedCat

Retention

Impact ofLAGICICRC

Impact ofOtherLAGIC

CurrentAPRA

Regime

IncreasedCat

Retention

Impact ofLAGICICRC

Impact ofOtherLAGIC

Cap

ital

(%

of

net

pre

miu

m)

Property Only InsurerDiversified Insurer

(50% Property/50% Long Tail GWP)

21

Capital Base components

Rules for Tier 1 and Tier 2 capital have changed

Proportion of capital base made up of higher quality

capital elements will increase substantially –

• Common Equity Tier 1 (CET1) must be greater than

60% of PCR (currently 37.5%)

• Tier 1 must be greater than 80% of PCR (currently 50%)

• Capital Base must be greater than PCR

22

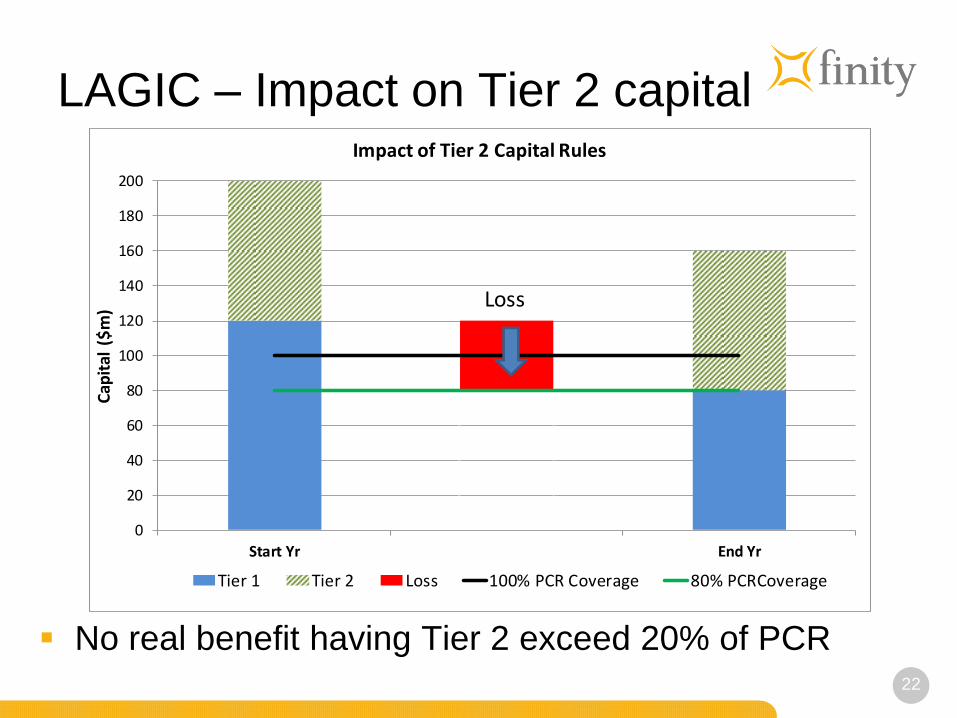

LAGIC – Impact on Tier 2 capital

No real benefit having Tier 2 exceed 20% of PCR

0

20

40

60

80

100

120

140

160

180

200

Start Yr End Yr

Cap

ital

($

m)

Impact of Tier 2 Capital Rules

Tier 1 Tier 2 Loss 100% PCR Coverage 80% PCRCoverage

Loss

23

ICAAP Capital Trigger Levels

A key aspect of an ICAAP is setting the capital levels

that will trigger specific capital management

responses

Each Insurer needs to consider:

• Future volatility of annual profit (and hence capital)

• Important capital thresholds where a capital

management decision is required

• Likelihood of breaching those thresholds

• The Board’s Risk Appetite

Understanding the potential variability of profits will

be key to matching risk appetite with trigger levels.

24

ICAAP Capital Trigger Levels

We have conducted Capital Volatility research

based on historical results of Australian insurers.

We used ISC and APRA company level statistics

• Selected only active insurers (no ‘run-off’ insurers)

• Excluded captives, LMI and Medical Indemnity

• Deleted any clearly incorrect data

The key statistic we used is :

• Net Profit (after-tax) / Minimum Capital Requirement

For pre-APRA periods the minimum solvency capital

was scaled up (x1.6) to approximate the APRA MCR

25

ICAAP Capital Trigger Levels

Average net profit was equal to 0.25 x MCR

• Equivalent to a 10-12% ROC

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0%

4%

8%

12%

16%

20%

24%

28%

32%

36%

40%

-0.8 -0.6 -0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1.0 1.2

Cu

mu

lati

ve P

rob

abil

ity

Pro

bab

ilit

y

Annual Change in Capital Adequacy Multiple

26

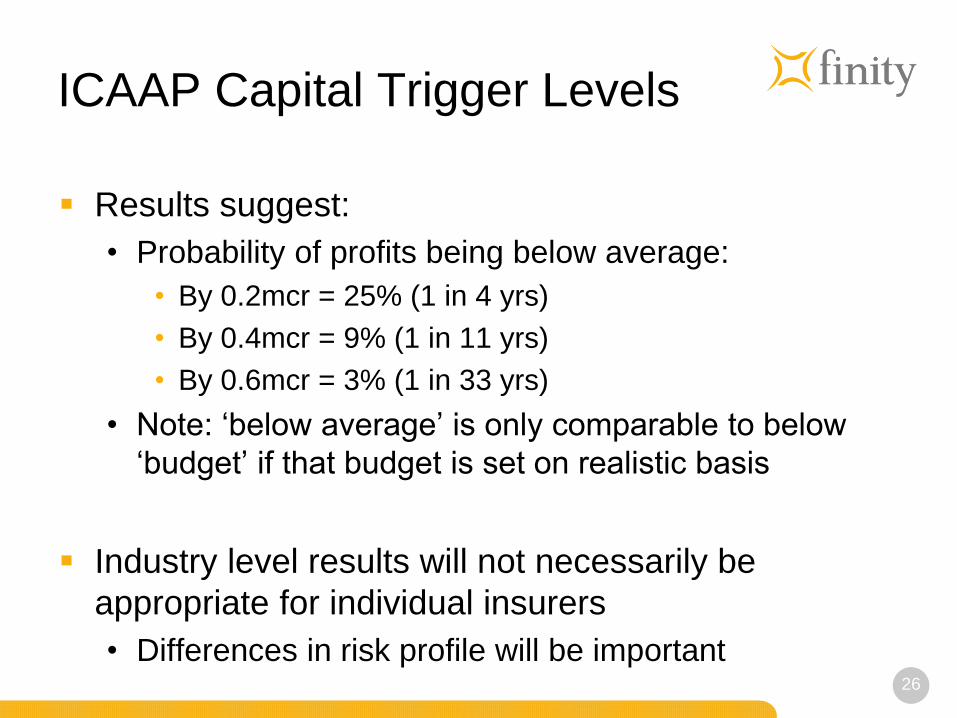

ICAAP Capital Trigger Levels

Results suggest:

• Probability of profits being below average:

• By 0.2mcr = 25% (1 in 4 yrs)

• By 0.4mcr = 9% (1 in 11 yrs)

• By 0.6mcr = 3% (1 in 33 yrs)

• Note: ‘below average’ is only comparable to below

‘budget’ if that budget is set on realistic basis

Industry level results will not necessarily be

appropriate for individual insurers

• Differences in risk profile will be important

27

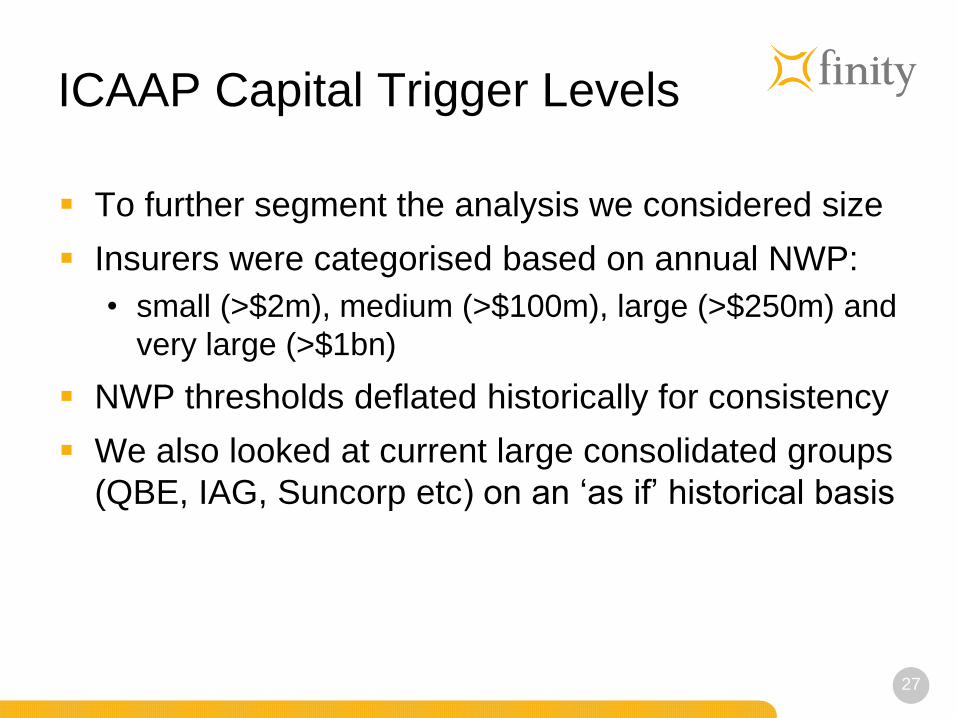

ICAAP Capital Trigger Levels

To further segment the analysis we considered size

Insurers were categorised based on annual NWP:

• small (>$2m), medium (>$100m), large (>$250m) and

very large (>$1bn)

NWP thresholds deflated historically for consistency

We also looked at current large consolidated groups

(QBE, IAG, Suncorp etc) on an ‘as if’ historical basis

28

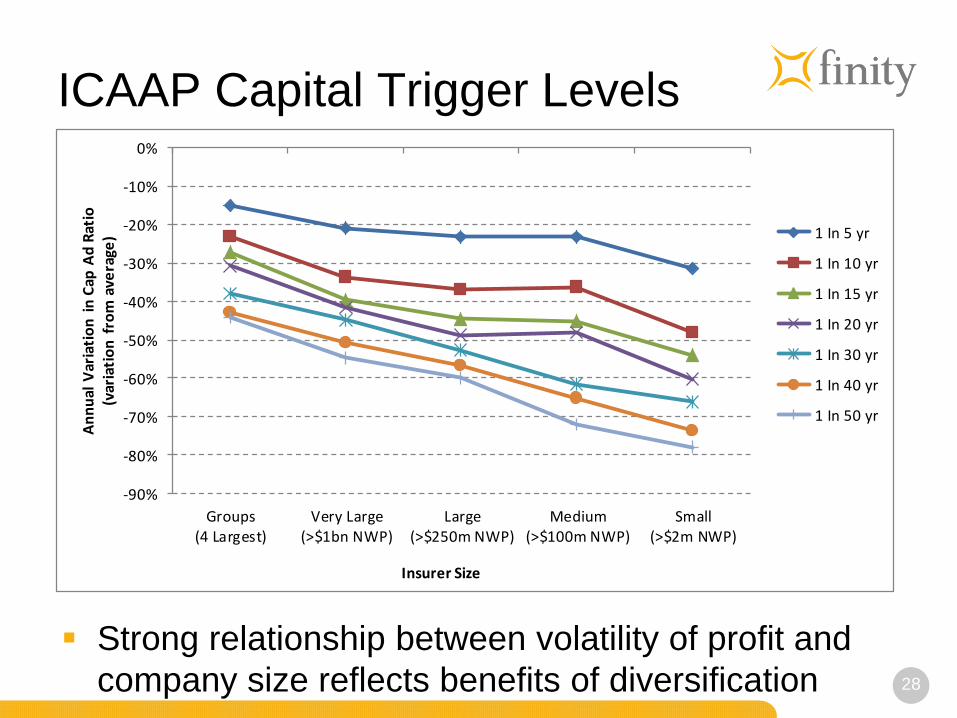

ICAAP Capital Trigger Levels

Strong relationship between volatility of profit and

company size reflects benefits of diversification

-90%

-80%

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Groups(4 Largest)

Very Large(>$1bn NWP)

Large(>$250m NWP)

Medium(>$100m NWP)

Small(>$2m NWP)

An

nu

al V

aria

tio

n i

n C

ap A

d R

atio

(var

iati

on

fro

m a

vera

ge)

Insurer Size

1 In 5 yr

1 In 10 yr

1 In 15 yr

1 In 20 yr

1 In 30 yr

1 In 40 yr

1 In 50 yr

29

Summary

‘Average’ impact of LAGIC is relatively small, but

differential impact by Insurer may be substantial

Strategic responses to the new capital standards

• Reduced use of Tier 2 capital instruments

• Heightened focus on ALM and duration matching

• Tendency to invest assets ‘short’

• Reduced incentive to hold equities

• Strong desire to buy horizontal reinsurance cover

ICAAP will increase focus on profit volatility and

optimising risk profile to reduce capital requirements

30

Disclaimer

This presentation was made to the Finity Niche

Insurer Conference on 18 October 2012. It may be

incomplete in that the speaker may have discussed

or qualified matters not incorporated into the slides

The information is general in nature and may not be

applicable to your particular situation. It is not

actuarial advice and Finity Consulting will accept no

liability for any use to which it is put

If you have any questions or comments, the author

or another member of the Finity Consulting team

would be pleased to hear from you. Please contact

us on 02 8252 3300