capability development and decision incongruence … · capability development and decision...

TRANSCRIPT

CAPABILITY DEVELOPMENT AND DECISIONINCONGRUENCE IN STRATEGIC OPPORTUNITYPURSUIT

J. ROBERT MITCHELL1* and DEAN A. SHEPHERD2

1Richard Ivey School of Business, University of Western Ontario, London,Ontario, Canada2Kelley School of Business, Indiana University, Bloomington, Indiana, U.S.A.

In strategic opportunity pursuit, decision incongruence (the gap between the decision-makingrationale that an individual conveys to others and the rationale that informs his/her actualdecisions) can lead to difficulties achieving the commitment necessary to grow a venture. Tounderstand why some individuals have greater decision incongruence in strategic opportunitypursuit than others, we conducted a field experiment to test how a configuration oftheoretically-based capability-building mechanisms—codification, general human capital, andspecific human capital—affected 127 CEOs’ decision incongruence. The results indicate thatcodification decreases decision incongruence the most for CEOs with low general but highspecific human capital. Copyright © 2012 Strategic Management Society.

‘Being in control, I don’t have to report to otherpartners or shareholders and I don’t have to explainto many people about why I make a decision. I guessI will be willing to give up some of my control whenI need further financing in my business.’ – Female,age 39

‘The business has changed so much, now that wehave over 100 employees. I’ve always run it from thehip, and I just can’t do that anymore. I have to do acrosscheck [of my decisions].’ – Male, age 61

INTRODUCTION

These quotations exemplify a tension that exists inentrepreneurship: as a business grows, the entrepre-

neur faces a need to rely more on other stakeholdersand a need to increase the involvement of thesestakeholders in decision making (cf. Kor, 2003). Asthe quotations also illustrate, one important elementof such involvement is the articulation of knowledgeabout why the individual’s decision makes sense.However, as Nisbett and Wilson (1977: 247)famously suggested, just as we can ‘know more thanwe can tell’ (as a result of our tacit knowledge), sotoo can we ‘tell more than we can know’ (as a resultof difficulties accessing cognitive processes). Theunderlying premise of their research is that individu-als are typically unable to engage in true introspec-tion about their cognitive processes and that anyassertions they make about these processes may notactually reflect the reality of these processes.

While Nisbett and Wilson’s (1977) findings have ageneral appeal and applicability, they are not freefrom criticism (Ericsson and Simon, 1980; Sabiniand Silver, 1981; White, 1980; White, 1988; Wrightand Rip, 1981). In one notable critique, Smith andMiller (1978: 361) recognized the potential strengthof the findings, but nonetheless emphasized theimportance of understanding ‘when (not whether)

Keywords: opportunity; capabilities; codification; knowledgeresources; conjoint; experiment*Correspondence to: J. Robert Mitchell, Richard Ivey School ofBusiness, University of Western Ontario, 1151 Richmond StreetNorth, London, ON N6A 3K7, Canada. E-mail: [email protected]

bs_bs_banner

Strategic Entrepreneurship JournalStrat. Entrepreneurship J., 6: 355–381 (2012)

Published online in Wiley Online Library (wileyonlinelibrary.com). DOI: 10.1002/sej.1145

Copyright © 2012 Strategic Management Society

people are able to report accurately on their mentalprocesses.’ It is to this issue that we speak in thecurrent article. That is, while the question of when(not whether) individuals can access mental pro-cesses is clearly germane in general, we see entre-preneurship specifically as a domain wherein theboundary conditions of such access are highlysalient, especially given the need for entrepreneursto ‘justify their ventures to relevant others to gainmuch-needed support and legitimacy’ (Cornelissenand Clarke, 2010: 539).

Relating this back to the quotations with which webegan, in an effort to understand ‘how, by whom, andwith what effects opportunities to create future goodsand services are discovered, evaluated, and exploited’(Shane and Venkataraman, 2000: 218), we seek tounderstand the conditions that would enable individu-als to better articulate knowledge of their decisionmaking about opportunities. Prior research on capa-bilities highlights how the ability to accurately articu-late simple rules about opportunities results in betterperformance for firms (Bingham and Eisenhardt,2011; Bingham, Eisenhardt, and Furr, 2007). Ourexpectation is that improved performance can result,for instance, as a result of individuals being able toconvey this essential information to important others,thereby gaining their support in the strategic1 pursuitof these opportunities. In decision making about newopportunities for a firm to pursue (whether the firm benew or existing), where the broader environment isuncertain, novel and often hurried (Baron, 1998;Bourgeois and Eisenhardt, 1988; McGrath andNerkar, 2004), the importance of conveying themeaning underlying decision making such that it canbe understood by others is often essential (cf. Corne-lissen and Clarke, 2010; Hill and Levenhagen, 1995;McMullen and Shepherd, 2006). This is especiallytrue when the entrepreneurial team is important to thepursuit of an entrepreneurial opportunity (cf. Cooperand Daily, 1997; West, 2007).

Of course, we recognize that knowledge of suchmeaning can be manufactured and, indeed, in manycases is (the underlying premise of the work ofNisbett and Wilson [1977]). Then again, in certaincases it is also not manufactured (Ericsson andSimon, 1980; Smith and Miller, 1978; Wilson andKraft, 1990). We seek to better understand underwhat conditions this may be the case. In doing so, we

suggest that for the individual who must convey theplausibility of the opportunity idea to others in orderto gain their support (cf. Bonner and Baumann,2012; Jelinek and Litterer, 1995; Weick, Sutcliffe,and Obstfeld, 2005), being able to convey the knowl-edge about decision making—i.e., the logic under-lying the simple rules about opportunities (Binghamand Eisenhardt, 2011; Bingham et al., 2007)—issuperior to conveying knowledge that is not accu-rate. This is true whether or not the decision turns outto be the ‘correct’ decision. Indeed, stakeholders arebetter positioned to gauge the correctness of a deci-sion when the information that is conveyed to themabout that decision is more accurate (Hirokawa,Erbert, and Hurst, 1996).2

Thus, while we recognize that certain individualsmay have an easier time convincing others to supportthem in their pursuit of opportunity (as a result ofcharisma, expertise, trustworthiness, social skills,signaling, etc. [cf. Alvarez and Barney, 2005; Baronand Markman, 2003; Spence, 1973]), a low degree ofdecision incongruence—defined as the gap betweenthe decision-making rationale that an individualconveys to others and the rationale that informs his/her actual decisions—will likewise be beneficialbecause it reflects a reduction of error (and, as aresult, a more accurate and clearer depiction of risks[cf. Argyris and Schön, 1974; Hackner and Hisrich,2001]). And although our use of a quasi-field experi-ment to test our hypotheses with individual CEOsprecludes our ability to explicitly measure the per-formance benefits of a low degree of decision incon-gruence on group- or firm-level outcomes, previousresearch highlights how decreasing decision incon-gruence can enable key stakeholders to better gaugethe correctness of a decision about an opportunity(Shepherd, 1999; Zacharakis and Meyer, 1998). Thiscan, in turn, increase needed buy-in from these keystakeholders (cf. Brush, Greene, and Hart, 2001;Kor, 2003; Miller and Ireland, 2005) and can, as aresult, facilitate coordination and higher-qualitygroup decision making (cf. Bonner and Baumann,2012; Hirokawa et al., 1996; van Dijk, de Kwaads-teniet, and De Cremer, 2009) and, importantly,improved performance (Bingham and Eisenhardt,2011; Bingham et al., 2007).

1 We view opportunity pursuit as strategic in the sense that itrequires the commitment of important resources, it sets impor-tant precedents, and it directs important firm-level actions(Mintzberg, Raisinghani, and Théorêt, 1976).

2 We nevertheless acknowledge that when an individual canpursue an opportunity without the need to convince others tojoin him or her (e.g., external parties to supply financialresources, potential joint venture partners, etc.), being able toconvey knowledge about the actual logic underlying decisionmaking may be less relevant.

356 J. Robert Mitchell and D. A. Shepherd

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

To understand the specific conditions wherebysome individuals are able to decrease decision incon-gruence in opportunity decision making (Smith andMiller, 1978), we draw upon capabilities research inour theorizing (Zander and Kogut, 1995; Zollo andWinter, 2002). Our rationale for doing so is foundedupon the importance of key learning mechanismsthat assist in the development of capabilities: expe-rience accumulation and knowledge codification,which can enable certain tacit knowledge that is‘bound up in action’ to be shared (Poole, Seibold,and McPhee, 1996; Zollo and Winter, 2002). Ofcourse, we acknowledge that the tacitness of knowl-edge is a matter of degree (Winter, 1987). Some tacitknowledge that is not articulated is nonethelessarticulable (Winter, 1987). As Winter (1987: 172)described, ‘the failure to articulate what is articu-lable may be a more severe handicap for the transferof knowledge than tacitness itself.’ It is this knowl-edge that is articulable but not yet articulated that weaddress herein. In doing so, we hypothesize that thatthe extent of decision incongruence about opportu-nities will depend on the configuration of CEO’sapplication of knowledge codification as acapability-building activity in decision making andtheir experience—including both general humancapital and specific entrepreneurial human capital(Zollo and Winter, 2002).

We make three primary contributions. First, wecontribute to theory that has looked at the difficultiesof accurately articulating mental processes (Ericssonand Simon, 1980; Sabini and Silver, 1981; Smith andMiller, 1978; White, 1980; White, 1988; Wright andRip, 1981) by seeking to better understand theboundary conditions underlying decision incongru-ence in strategic opportunity pursuit. These efforts inthe domain of strategic opportunity pursuit can thenserve as the starting point for understanding howdecision incongruence may be reduced in other stra-tegic decision-making contexts. Second, our investi-gation of differences in CEOs’ general and specificentrepreneurial human capital adds richness to dis-cussions about differences across entrepreneurs(Sarasvathy, 2004). While prior research has inves-tigated the effects of thinking differences betweenentrepreneurs and non-entrepreneurs on behavior(e.g., Begley and Boyd, 1987; Busenitz and Barney,1997; Forbes, 2005), our study also investigates howthe combination of general and specific entrepre-neurial human capital impacts the extent to whichknowledge codification enables a reduction in deci-sion incongruence, thereby contributing to a rich

literature on human capital in entrepreneurship(Becker, 1964; Corbett, 2007; Dimov and Shepherd,2005; Gimeno et al., 1997; Wright et al., 2007).Finally, we contribute to research on capabilities byfurther illustrating the conditions under whichknowledge codification is beneficial and when it isnot (cf. Collis, 1994; Zollo and Winter, 2002).

Our research proceeds as follows: in the nextsection, we develop the concept of decision incon-gruence and position it as an individual-level con-struct that has implications for entrepreneurial actionthat also involves others. Next, we draw on capabili-ties research to develop our hypotheses explainingheterogeneity in decision incongruence. We then testthese hypotheses and report the results. Finally, wediscuss the theoretical and practical implications ofour study.

DECISION INCONGRUENCE

Decision incongruence reflects the gap between thedecision-making rationale that an individual conveysto others and the rationale that informs his/her actualdecisions (cf. Argyris and Schön, 1974; Smith andMiller, 1978). Evidence that individuals may have adifficult time articulating their thinking is well docu-mented in past decision-making research (cf.Argyris, 1977; Argyris and Schön, 1974; Nisbett andWilson, 1977), whether it involves executives havinga difficult time articulating corporate acquisitiondecisions (Stahl and Zimmerer, 1984) or venturecapitalists struggling to articulate their investmentdecisions (Shepherd, 1999; Zacharakis and Meyer,1998). In entrepreneurship, the downside of decisionincongruence is especially salient when the pursuitof opportunity is understood as depending on morethan one person (Cooper and Daily, 1997) and when,as the prior quotations illustrate, support from theseothers (either financially or otherwise) is needed.When an individual can pursue an opportunitywithout the need to convince these others to supporthim or her (financially or otherwise), decision incon-gruence is likely less (negatively) impactful. Butwhen stakeholders—potential partners, investors,lenders, employees, customers, and suppliers as wellas spouses, other family members, and friends—aremaking the decision about whether to support thepursuit of a specific opportunity, decision incongru-ence is implicated. Our argument is that individualsare best positioned to secure stakeholder supportwhen the rationale for pursuing an opportunity is

Opportunity, Capability Development, and Decision Incongruence 357

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

accurately portrayed (cf. Hackner and Hisrich,2001), which we suggest is more likely to occurwhen decision incongruence is low.

But there is an irony. One of the key elements thatenables opportunity pursuit—the asymmetricknowledge gained by the individual in the process ofopportunity creation (cf. Alvarez and Barney,2008)—also represents a potential stumbling block.If the individual cannot share this knowledge withrelevant stakeholders through accurate articulation,these stakeholders are, in turn, less able to use thisinformation to gain confidence in and providesupport for the individual pursuing the opportunity(Alavi and Leidner, 2001). Because the communica-tion of knowledge anchors one end of a proposed‘spiral of organizational knowledge creation’(Nonaka, 1994: 20), any inaccuracies in an individu-al’s communicated knowledge about strategicopportunity pursuit that result from decision incon-gruence may be magnified as the process of oppor-tunity pursuit unfolds. Further, any inaccuracies inan individual’s communicated knowledge aboutstrategic opportunity pursuit that lead potentialinvestors to underestimate risks can, in turn, ‘mak[e]it generally harder for entrepreneurs to financeoperations . . . even for those companies withhealthy financial structures and prospects’ (Hacknerand Hisrich, 2001: 87).

To understand the conditions whereby some indi-viduals are able to decrease decision incongruence inopportunity decision making more than others and tounderstand how this understanding matters in entre-preneurship, we adopt a configurational approach. Inthis approach, we draw on capability theory (see e.g.,Leiblein, 2011; Zander and Kogut, 1995; Zollo andWinter, 2002) to suggest that differences in theextent of decision incongruence about opportunitiesdepend, in part, on the configuration of learningmechanisms that underlie capability-building activi-ties in strategic opportunity pursuit (Zollo andWinter, 2002). As we discuss in more depth in thenext section, we hypothesize that it is the configura-tion of general human capital, specific entrepreneur-ial human capital, and knowledge codification (ascapability-building mechanisms) that explains deci-sion incongruence.

KNOWLEDGE CODIFICATION ANDEXPERIENCE ACCUMULATION

In complex and ambiguous entrepreneurial environ-ments (see, e.g., Hill and Levenhagen, 1995; Licht-

enstein et al., 2007) where information asymmetriesbetween economic actors are likely high (cf. Hayek,1945; Shane, 2000), decision incongruence is antici-pated to be prevalent (cf. Argyris, 1976; Nisbett andWilson, 1977) and potentially costly as a result ofdifficulties gaining support from others (Brush et al.,2001; Miller and Ireland, 2005). And while decreas-ing the imitability of knowledge to make it moreusable by decision makers within firms is notwithout cost (Coff, Coff, and Eastvold, 2006; Dier-ickx and Cool, 1989), the cost of inaccuracy anderror may exceed the cost of imitability (cf. Hacknerand Hisrich, 2001)—especially given that the abilityto share one’s own knowledge is vital to the creationand renewal of firms (cf. Floyd and Wooldridge,1999; Szulanski, 1996; Von Hippel, 1994; Zanderand Kogut, 1995). This is evident for the individualsquoted earlier. For their businesses to grow, the indi-viduals needed to develop the capability to sharetheir knowledge about their decision making(Zander and Kogut, 1995; Zollo and Winter, 2002).

While the focus of capability theory tends towardthe establishment of organizational capabilities(Leiblein, 2011; Teece, Pisano, and Shuen, 1997),the insights it offers also relate to the capabilities ofentrepreneurial individuals (Felin and Hesterly,2007; Teece, 2007). Bringing together individual-level and organizational-level capabilities research,Zollo and Winter (2002: 340) highlight the roles ofknowledge codification, knowledge articulation, andexperience accumulation as capability-buildingmechanisms. Because decision incongruencereflects an inability to accurately articulate knowl-edge, we devote our attention to the capability-building properties associated with the configurationof (1) knowledge codification and (2) experienceaccumulation as they concern the accurate articula-tion that is exemplified in reduced decision incon-gruence.

Knowledge codification anddecision incongruence

Knowledge codification refers to the ‘conversion ofknowledge into messages which can be then pro-cessed as information’ (Cowan and Foray, 1997:596). Herein, the knowledge of interest is knowledgeabout opportunity decision making. In previousresearch, the application of knowledge codificationprocesses has been suggested to result in increasedaccuracy, coordination, and efficiency (Cowan,David, and Foray, 2000; Cowan and Foray, 1997;

358 J. Robert Mitchell and D. A. Shepherd

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

Zander and Kogut, 1995). Knowledge codificationhas also been linked to the establishment of operat-ing routines and the development of the capabilitiesthat enable innovation and allow for existing rou-tines to be modified (Cohendet and Meyer-Krahmer,2001; Grimaldi and Torrisi, 2001; Lazaric,Mangolte, and Massue, 2003; Zollo and Winter,2002). Along similar lines, knowledge codificationcan also serve as a signal of the capabilities pos-sessed by an organization (Cohendet and Meyer-Krahmer, 2001). Conversely, in addition to thepotential cost in time and effort of codification, it isalso possible to overcodify knowledge if the processsomehow prevents individuals from generating newknowledge, if it leads to organizational inertia, or ifit becomes a commodity that is of less value to theorganization as a result (Cohendet and Meyer-Krahmer, 2001; Cowan et al., 2000). In this sense,knowing the boundaries of when codificationdecreases decision incongruence (and when it doesnot) will be beneficial to decision makers decidingwhether or not to codify their knowledge.

In our discussion of decision incongruence, whichindicates difficulties in articulation, the distinctionsbetween knowledge codification and knowledgearticulation matter (cf. Zollo and Winter, 2002).Whereas knowledge articulation involves saying,knowledge codification involves the conversion ofknowledge into identifiable rules and relationshipswhich are then physically recorded so they can bebetter communicated (Cowan and Foray, 1997;Kogut and Zander, 1992). Like knowledge articula-tion, knowledge codification involves the transfor-mation of tacit knowledge into explicit knowledge(Nonaka, 1994). However, unlike articulation, whichcan exacerbate error as a result of manufacturedlogic (Branch, 1961; Nisbett and Wilson, 1977),knowledge codification goes further and forces ‘thedrawing of explicit conclusions about the actionimplications of experience’ (Zollo and Winter, 2002:349). It requires an individual to expose the under-lying logic of his/her beliefs and reveal implicitassumptions (Zollo and Winter, 2002: 342). Thus,while inconsistencies in beliefs and implicit assump-tions can lead to inaccuracies in articulation (Nisbettand Wilson, 1977), knowledge codification mayserve as a countervailing force that instead increasesthe accuracy of beliefs—at least in certain instances,as our configurational model is intended to illustrate(Smith and Miller, 1978).

For our purposes, knowledge codification occursas decision makers structure their knowledge about

their decision making into identifiable rules andrelationships which are then recorded (Cowan,2001; Cowan and Foray, 1997; Kogut and Zander,1992). Because this process makes causal linkagesexplicit (Zollo and Winter, 2002: 342), knowledgecodification can also serve to calibrate what indi-viduals say they do to what they actually do,reflecting a kind of learning that facilitates a moreaccurate, clear, and justifiable representation ofknowledge (cf. Argyris and Schön, 1974). In thisway, decision makers who codify their knowledgemight be expected to have lower decision incon-gruence than those decision makers who do not.Thus,

Hypothesis 1: Decision makers who engage inknowledge codification will have lower decisionincongruence in strategic opportunity pursuitthan those who do not engage in knowledgecodification.

Experience accumulation and human capital

But the story is not so simple. As we have described,while this expectation that knowledge codificationcan decrease decision incongruence in generalwould seem to make sense given previous research(Cowan et al., 2000; Cowan and Foray, 1997;Zander and Kogut, 1995), our expectation is that theefficacy of knowledge codification in decreasingdecision incongruence in opportunity decisionmaking depends on the kinds of experience accumu-lated by the individuals making these opportunitydecisions (cf. Baron, 2009; Dew et al., 2009; Zolloand Winter, 2002). Herein, we conceptualize thisexperience in terms of: (1) general human capitaland (2) specific entrepreneurial human capital(Becker, 1964; Corbett, 2007; Dimov and Shepherd,2005; Gibbons and Waldman, 2004; Gimeno et al.,1997). As we will elaborate, in our configurationalapproach, we expect that each type of human capitalwill uniquely shape the influence that codificationhas in the reduction of decision incongruence. Thisexpectation, that general human capital and specificentrepreneurial human capital will have differentialeffects on decision incongruence, is consistent withprior research on human capital in entrepreneurshipand strategic management that has found differencesin the effects of each type of human capital (e.g.,Colombo and Grilli, 2005; Dimov and Shepherd,2005; Pennings, Lee, and van Witteloostuijn, 1998;Zarutskie, 2010).

Opportunity, Capability Development, and Decision Incongruence 359

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

General human capital

From the perspective of prior entrepreneurshipresearch, general human capital is defined as thebasic knowledge stock that an individual possesses(Becker, 1964) that is gained through education andoverall experience (Corbett, 2007; Dimov and Shep-herd, 2005; Gimeno et al., 1997; Wright et al.,2007). This knowledge can come in the form of lifeexperience that comes with age, work experience, orcompletion of university education (Cooper,Gimeno-Gascon, and Woo, 1994; Davidsson andHonig, 2003; Gimeno et al., 1997). As prior researchindicates, this experience is key to economic out-comes generally (Becker, 1964), but also for entre-preneurship specifically. Indeed, the impact of suchexperience is evident in the effect of general humancapital on entry and engagement in entrepreneurship(Davidsson and Honig, 2003), innovation (Marveland Lumpkin, 2007), growth (Colombo and Grilli,2005), and firm performance (Gimeno et al., 1997).

In practice, general human capital and the knowl-edge codification process have similar characteris-tics. Like codification, which entails the conversionof knowledge into identifiable rules and relation-ships which are then recorded so they can be bettercommunicated (Cowan and Foray, 1997; Kogut andZander, 1992), the development of general humancapital frequently involves the formalization ofknowledge in the form of ‘formal’ education orinvestments in general training (Davidsson andHonig, 2003; Preisendörfer and Voss, 1990). For thisreason, the very processes that lead to the develop-ment of general human capital—through the transferof knowledge between individuals (Wright et al.,2007)—are likely to act as substitutes for knowledgecodification as a result of experience and expertise in‘formalizing’ knowledge. In this sense, generalhuman capital may minimize any impact that codi-fication would have on decision incongruencebecause of its substitutionary role. Thus,

Hypothesis 2: In strategic opportunity pursuit,the impact of knowledge codification on loweringdecision incongruence will be less for decisionmakers with high general human capital than forthose with low general human capital.

Specific entrepreneurial human capital

While general human capital represents broad-basedknowledge that can be shared between individuals(Wright et al., 2007), prior research has defined spe-

cific human capital as the knowledge and ability thatis gained through experience in a particular industryor task setting (Becker, 1964; Cooper et al., 1994;Corbett, 2007). Because of the task specific nature ofspecific human capital (Gibbons and Waldman,2004; Preisendörfer and Voss, 1990), it is essential tofirst understand the nature of the task in question. Inour study, we investigate decision making in strate-gic opportunity pursuit, which plays an importantrole in entrepreneurial action (Busenitz and Barney,1997; McMullen and Shepherd, 2006). In strategicopportunity pursuit, the ‘task-specific learning bydoing’ that results in specific entrepreneurial humancapital (Gibbons and Waldman, 2004: 203) can comefrom experience founding a venture, experience in aspecific industry, or experience pursuing opportuni-ties through starting other ventures (Cooper et al.,1994; Dimov and Shepherd, 2005; Patzelt, 2010).Those individuals who have experience in foundinga venture will have firm-specific experience withstrategic decision making and technology-specificexpertise surrounding that decision making which,in combination, form the basis of the venture (Kor,2003; Patzelt, 2010). Likewise, those with greaterindustry-specific experience will have an under-standing of the industry that gives them insight intocompetitive forces of the industry, especially of theopportunities that might exist in the industry (Kor,2003). This experience identifying and pursuingother opportunities represents a task that is of centralimportance to new venture creation (cf.Alvarez andBusenitz, 2001; Baron, 2007).

The ‘learning-by-doing’ elements of specificentrepreneurial human capital (Gibbons andWaldman, 2004; Preisendörfer and Voss, 1990) areespecially salient for understanding how specificentrepreneurial human capital will have a distinctlydifferent impact on the effectiveness of knowledgecodification relative to general human capital. Forinstance, prior research suggests that founders, as aresult of learning-by-doing, possess tacit knowledgethat can serve as a resource, but may at the same timebe difficult to share with other important stakehold-ers (Kor, 2003; Winter, 1987). Indeed, the very pro-cesses that lead to the creation of this specificentrepreneurial human capital also lead this knowl-edge to be more tacit and holistic in nature (Gordon,1992; Simon, 1987) and, as a result, harder to com-municate (Gordon, 1992; Mieg, 2001).

For those with high general human capital, thepossession of specific entrepreneurial human capitalshould not represent a problem, as their experience

360 J. Robert Mitchell and D. A. Shepherd

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

transferring knowledge between individuals (Wrightet al., 2007) can serve to assist them in communicat-ing this knowledge to others. Similarly, those withlittle specific entrepreneurial human capital in thefirst place lack the tacit knowledge that comprisesspecific entrepreneurial human capital and, as aresult are likely to see minimal benefit from knowl-edge codification. Instead, their knowledge isexpected to be more conscious and effortfullyemployed (cf. Mitchell, Friga, and Mitchell, 2005).For those who lack general human capital butpossess specific entrepreneurial human capital,knowledge codification is expected to be essentialbecause it will assist them in making causal linkagesexplicit (Zollo and Winter, 2002) and will serve tocalibrate what individuals say they are doing andwhat they are actually doing (Argyris and Schön,1974). Those with neither general human capital norspecific entrepreneurial human capital do notpossess tacit knowledge in the first place. For them,the simple rules about opportunities are alreadyexplicitly represented in the mind. In this sense, weexpect decision makers with both low general humancapital and low specific entrepreneurial humancapital to enjoy little benefit from knowledge codi-fication. Conversely, however, we expect decisionmakers who have a configuration of low generalhuman capital but high specific entrepreneurialhuman capital to especially benefit from codifyingtheir knowledge. Thus,

Hypothesis 3: In strategic opportunity pursuit,the impact of knowledge codification on loweringdecision incongruence will be greater for deci-sion makers with high specific entrepreneurialhuman capital than for those with low specificentrepreneurial human capital, but more so whengeneral human capital is low than when it is high.

RESEARCH METHODS

We tested our hypotheses in a quasi-field experimentwith a pretest, posttest control group design (Camp-bell and Fiske, 1959) that involved both decision-level data collection (in the form of a metric conjointanalysis task) and individual-level data collection (inthe form of an experimental manipulation and a setof self-report questionnaires). Our rationale foradopting such an experimental approach was three-fold. First, a field experiment provided externalvalidity (cf. Cook and Campbell, 1979) in that it

allowed us to investigate the decision incongruenceof CEOs who actively make decisions about oppor-tunities for their firm. Second, a field experimentprovided internal validity (cf. Cook and Campbell,1979) in that it allowed us to randomly assign CEOsto an experimental condition (a knowledge codifica-tion task) or control condition (a distracter task),thereby allowing us to control for confoundingeffects (Campbell and Fiske, 1959). Through use ofa premanipulation measure of decision incongruence(Time 1) and postmanipulation measure of decisionincongruence (Time 2), we could then test thehypothesized effects of our experimental manipula-tion on decision incongruence. Third, use of a nesteddesign in a field experiment (strategic decisionsabout opportunities, nested within individuals) per-mitted us to more accurately measure decisionincongruence by capturing the gap between thedecision-making rationale that informs the CEO’sactual decisions (using metric conjoint analysis) andthe decision-making rationale that the CEO conveysto others (using a set of self-report questions), whilealso allowing us to capture the individual-level vari-ables that are central to our model. In the followingsubsections, we describe the procedures of our fieldexperiment in more detail.

Data gathering

To test our hypotheses, we identified a sample ofCEOs using the OneSource CorpTech database. Weused CEOs in technology firms3 because of an expec-tation that CEOs operating in high-ambiguity (Hilland Levenhagen, 1995; Stone and Brush, 1996) andhigh-velocity (Eisenhardt, 1989) environmentswould face a need to constantly seek and, thus,actively make decisions about new opportunities fortheir firm (Hughes, 1990). With this database, weidentified companies based on three criteria: (1) geo-graphical location, (2) the inclusion of informationabout the CEO, and (3) firm size. First, geographiclocation was important because the study requiredone-on-one meetings with CEOs. Accordingly, wecontacted only companies in the surrounding threearea codes of a large Midwestern city (i.e., within athree-hour drive). Second, because our focus was onthe strategic decisions about opportunity pursuit, weincluded only firms for which information aboutthe CEO of the company was provided. We did so

3 We note that the CorpTech database includes both high-techand low-tech firms.

Opportunity, Capability Development, and Decision Incongruence 361

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

because of the CEO’s central role in decisions aboutopportunity. This meant that we excluded firms thatonly provided contact information for a chairman ofthe board, a plant manager, a vice president, etc.Lastly, and related to the previous point, firm size wasan important consideration in the research because,practically speaking, we anticipated that CEOs insmall- to medium-sized firms (10 to 500 employees)would likely have a larger role in making specificdecisions about which opportunities to pursue thanCEOs in large firms (500+ employees). This meantthat we excluded firms which, in the database,reported less than 10 or more than 500 employees.Alltold, there were 459 firms that met these criteria.

To arrive at the final sample and to ensure that itwas representative of the larger population, we ran-domly selected a subsample of 240 CEOs at thesecompanies to contact over a five-month period. Atotal of 127 of the CEOs agreed to participate (anumber consistent with other field experiments [e.g.,McNatt and Judge, 2004]) to result in a response rateof 53 percent.4 The data were collected in-personwith each of the CEOs at their office in an hour-longmeeting. To test for participation bias, we used logis-tic regression, wherein we regressed whether or not aCEO responded (1 or 0) on firm age, firm size, andfirm type (information that we had for all 240 firms).None of the factors in the regression were signifi-cant, thus providing no evidence of participationbias. The mean age of CEOs’ firms was 35 years(median age was 24 years) and the mean size ofCEOs’ firms was 98 employees with $23 million insales (median size was 40 employees with $5 millionin sales). The mean age of CEOs was 52 years(median age was 51 years), 95 percent of the samplewere men, and 58 percent of the CEOs werefounders of the firm.

To investigate whether differences exist beyondaccumulated experience between those with lowversus high general human capital and low versushigh specific entrepreneurial human capital, we fol-lowed Baron and Ensley (2006) and comparedsamples. We did so between samples of low and highgeneral human capital and between samples of lowand high specific entrepreneurial human capital. Indoing so, we specifically investigated whether differ-ences existed in: task motivation, overconfidence,general self-efficacy, entrepreneurial self-efficacy,

metacognitive knowledge, metacognitive experi-ence, fear of failure, gender, firm age, firm size, andfirm type (independent versus subsidiary). Theresults indicated that differences (p < 0.05) existedbetween samples for firm age (specific entrepreneur-ial human capital only) and firm size (general humancapital and specific entrepreneurial human capital).Consequently, both firm age and firm size wereincluded as controls in later analyses.

Research design and task

As we have described, decision incongruenceinvolves the gap between the decision-making ratio-nale that an individual conveys to others and thedecision-making rationale that informs his/her actualdecisions. We next discuss each aspect of decisionincongruence, beginning with how we captured thedecision-making rationale that informs CEOs’ actualdecisions, followed by how we capture the decision-making rationale the CEOs conveyed. In the mea-sures section, we then discuss how the two rationalesare combined to calculate decision incongruence.

Actual decision-making rationale

To capture each an individual’s actual decisionmaking about strategic opportunity pursuit, we useda metric conjoint analysis decision-making task(Louviere, 1988; Priem, 1992). Metric conjointanalysis is useful because it allows for an investiga-tion of the underlying decision structure of eachdecision maker’s strategic decisions. It does so bybreaking down these decisions into their componentparts (Priem and Harrison, 1994; Shepherd andZacharakis, 1997). In this approach, we created 16hypothetical opportunity situations, which reflectedvariation among four theoretically relevant attributesin strategic opportunity decision making. The fourattributes of the decision-making task were based ona model of entrepreneurial action that reflects thedecision to commit firm resources to the exploitationof opportunities (McMullen and Shepherd, 2006):the extent to which he/she is motivated and knowl-edgeable to pursue the opportunity in an uncertainenvironment (e.g., Baron, 2006; Krueger, 1993;Krueger, Reilly, and Carsrud, 2000; McMullen andShepherd, 2006; Mitchell and Shepherd, 2010). Welink this model to the respective attributes we used inthe decision-making task in the next paragraph.

We conceptualized the motivation aspect of thedecision to commit resources to opportunity pursuit

4 All but four of the participants were firm CEOs (the four whowere not participated at the request of the CEO once thepurpose of the study was made clear).

362 J. Robert Mitchell and D. A. Shepherd

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

as the potential value of an opportunity. Thisattribute reflects the profit predicted to result fromthe decision to allocate resources to the full-scaleexploitation of the opportunity (Venkataraman,1997). We conceptualized the knowledge aspect ofthe decision to commit resources to opportunitypursuit as knowledge relatedness. This attributereflects the extent to which the CEO believes he/shehas the knowledge necessary to exploit the opportu-nity (Krueger and Brazeal, 1994). We conceptual-ized the environmental aspect of the decision tocommit resources to opportunity pursuit as thewindow of opportunity and the number of potentialopportunities. The window of opportunity attributereflects the length of time available to profitablyinvest in the potential opportunity, and the number ofpotential opportunities reflects the number of otherpotential opportunities that could be pursued instead.

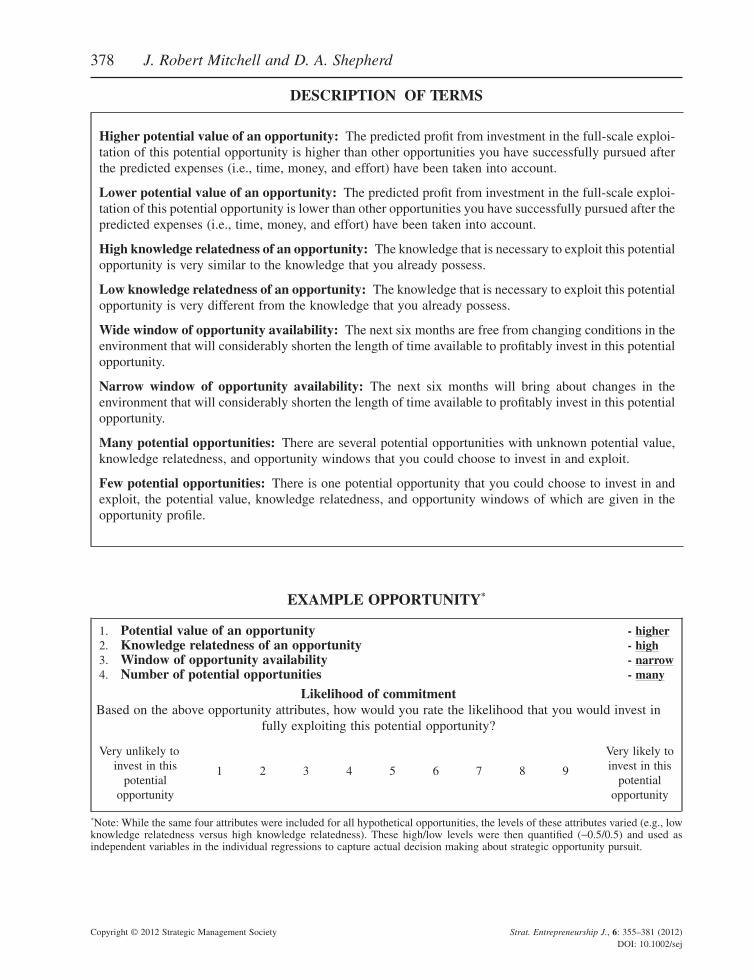

Prior to use of these four attributes in our fieldexperiment, we conducted a pretest in which weasked CEOs of firms like those in our sample if theattributes were relevant to their strategic decisionsabout opportunity pursuit. They confirmed theappropriateness of the presented attributes. In thehypothetical opportunity profiles, we varied each ofthe attributes at two levels (e.g., high knowledgerelatedness or low knowledge relatedness) and pro-vided a definition of each attribute at each level.These definitions, the instruction for this task, and anexample opportunity are included in Appendix A.

After viewing a hypothetical opportunity profilethat had a specific combination of these attributes,decision makers indicated their likelihood of invest-ing in that opportunity (see Appendix A for one of thehypothetical opportunities used). We measured like-lihood of investment with a nine-point scale anchoredby ‘very likely to invest in this opportunity’ (9) and‘very unlikely to invest in this opportunity’ (1). Tocontrol for variance and increase the task-domainapplicability, in the instructions we asked decisionmakers to assume that: (1) other than the informationprovided in the profiles, the hypothetical opportuni-ties presented were similar to other entrepreneurialopportunities they have ‘seen’ in all respects; (2) theyhad the resources (or access to the resources) to investin an opportunity if they chose to do so; (3) they weremaking decisions about these opportunities for theircurrent firm; and (4) they were making decisionsabout these opportunities in their current industry andeconomic environment. Additionally, in the instruc-tions we asked decision makers to use their expertisein the decision-making task. In this way, we did not

presume that there was one correct way of makingdecisions nor did the testing of our hypotheses requireit. For instance, while we might expect decisionmakers to invest in opportunities that were related toknowledge they already possess, this was not arequirement for our study of decision incongruence.Instead, each entrepreneur determined what was anopportunity for himself/herself.

To shorten the amount of time required in thisdecision-making task (Green and Srinivasan, 1990),we used an orthogonal fractional factorial design(i.e., no correlation between attributes across oppor-tunities).This reduced the number of required hypo-thetical profiles (Hahn and Shapiro, 1966), which wethen replicated so we could estimate individualsubject error (bringing the final number of hypotheti-cal opportunity profiles in the decision-making taskto 16—eight profiles, each replicated one time).With this design, we were able to test for the maineffects of all of the opportunity attributes on likeli-hood of investment, as well as three two-way inter-actions. For example, we were able to determine thedegree to which a specific decision maker empha-sized knowledge relatedness in his/her strategicdecisions about opportunity pursuit (a main effect)as well the degree to which this emphasis on knowl-edge relatedness was contingent on window ofopportunity in their strategic decisions about oppor-tunity pursuit (an interaction effect). Although thisdesign did not allow us to test all higher-order (inter-action) relationships among the attributes, the abilityto test four main effects and three interaction effectsis sufficient for our measure of decision incongru-ence because ‘decision policies’ with more thanthree contingent relationships are rare (Louviere,1988). To test for possible order effects, we createdfour versions of the profiles that varied the order ofthe attributes and the order of the profiles. There wasnot a significant difference between the versions (p >0.10) and, therefore, order effects are unlikely toconfound our findings. To familiarize decisionmakers with the task, we utilized a practice profilethat was not used in subsequent analyses.

Using metric conjoint analysis, we were then ableto calculate a separate regression equation for eachdecision maker that captured his/her actual decisionmaking about strategic opportunity pursuit. In thisregression equation, the standardized beta weightsreflected the importance of and emphasis on theopportunity attributes (or combinations of attributes)in an individual’s strategic decision making aboutopportunity pursuit. As an illustration, an individu-

Opportunity, Capability Development, and Decision Incongruence 363

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

al’s Time 1 actual decision making might look asfollows: potential value (b = 0.497, p < 0.01), knowl-edge relatedness (b = 0.417, p < 0.01), window ofopportunity (b = 0.139, n.s.), number of potentialopportunities (b = 0.218, p < 0.05), knowledge relat-edness ¥ window of opportunity (b = -0.139, n.s.),knowledge relatedness ¥ number of potential oppor-tunities (b = -0.218, p < 0.05), and window of oppor-tunity ¥ number of potential opportunities (b =0.616, p < 0.001). The regression results of thedecision-making rationale that informs this individu-al’s actual decisions at Time 1 can then be comparedto what the individual says he/she did at Time 1, aswe now describe.

Decision-making rationale conveyed

To capture the decision-making rationale an indi-vidual conveys about strategic opportunity pursuit,we utilized a carefully-constructed set of self-reportmeasures. We first asked decision makers to discusstheir own decision making by asking, ‘When assess-ing the previous profiles, what things did you con-sider when making your investment decisions?’ Thisopen-ended self-report question about the attributesthey used in their strategic decision making aboutopportunity pursuit (e.g., potential value, knowledgerelatedness, etc.) allowed individuals to describetheir decision making free from suggestive cuing. Byasking decision makers whether they were morelikely to invest when an attribute was at a high level(e.g., high knowledge relatedness) or a low level(e.g., low knowledge relatedness), we were able todetermine the sign/direction for the factors they con-sidered to play significant roles in their decisions (anecessary piece of information for comparison towhat they actually did). A self-report interactioneffect between two attributes was recorded whendecision makers suggested that the importance ofone attribute depended on another and was clarifiedby asking if they were describing the effect ofAttribute A on Attribute B. When such an effect waspresent, we asked decision makers if having a highlevel of Attribute A was more important or lessimportant when Attribute B was at a high level.Again, this allowed us to determine the sign/direction of any self-reported interaction effects.Consistent with prior research (Viswesvaran andBarrick, 1992), we then asked decision makers toassign a score (0 to 100) for each of the attributes andinteractions of attributes they said they used in theirdecisions based on its importance to their decisions.

This score permitted comparison with what an indi-vidual actually said he/she did.

Sequence of experimental protocol

In the experiment, decision makers engaged in themetric conjoint analysis decision-making task (tocapture the CEOs’ actual decision-making ratio-nale), followed by the self-report measure (tocapture the decision-making rationale the CEOs con-veyed) both before and after the knowledge codifi-cation experimental manipulation. This means that atTime 1, decision makers evaluated the 16 opportu-nity profiles plus three additional profiles5 whichwere to be used in the knowledge codificationmanipulation, followed by the self-report measuresdescribing their decision making. At Time 2, deci-sion makers again evaluated the 16 original oppor-tunity profiles, followed by the self-report measuresdescribing their decision making. While the sameopportunity profiles were used at Time 1 and Time 2so as to permit a comparison at Time 1 and Time 2,the profiles were relabeled to mask the repetition.Following the Time 2 self-report measures, weadministered a questionnaire that captured addi-tional relevant data from decision makers. Figure 1visually depicts the temporal sequence of the fieldexperiment protocol.

Measures

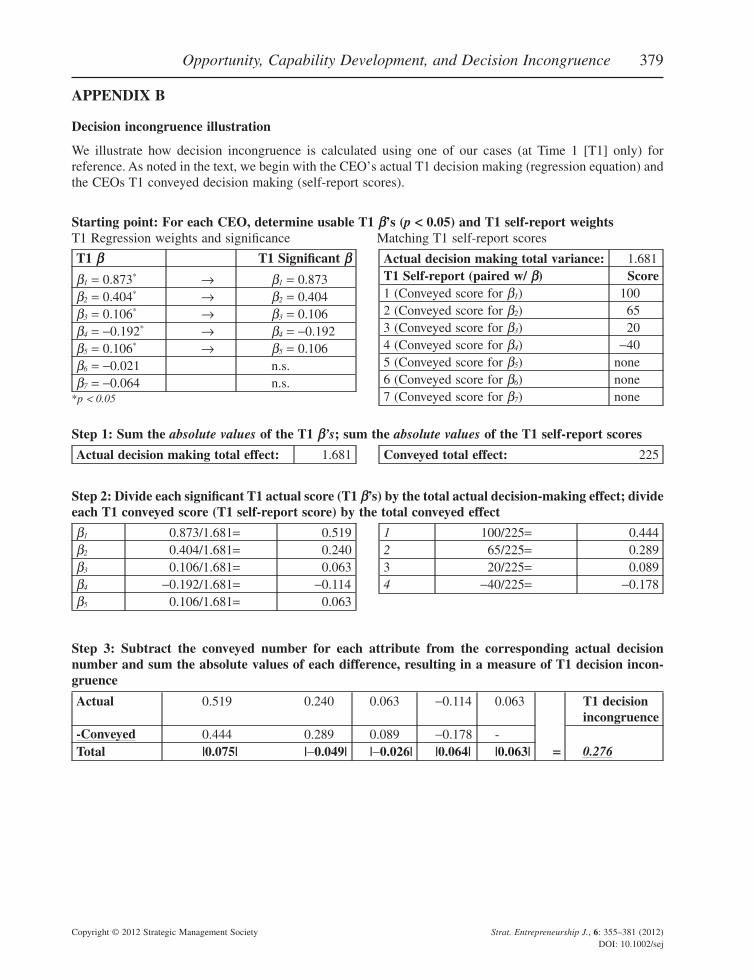

Decision incongruence

We measured decision incongruence by taking thedifference between an individual decision maker’smetric conjoint analysis regression results and his/her self-report measures (Viswesvaran and Barrick,1992). To calculate this difference, both the metricconjoint analysis regression result and the self-reportmeasure had to be expressed quantitatively and com-parably. Based on each decision maker’s regressionequation, we first established which attributes(knowledge relatedness, value, etc.) were significant(p < 0.05) for each individual at both Time 1 andTime 2. Again, each individual had separate regres-sion equations for both Time 1 and Time 2, meaningthat there were two unique sets of regression resultsper person. The individual beta weights of theseregression equations represented the importance of

5 These three additional opportunity profiles were differentfrom (and were presented after) the 16 Time 1 opportunityprofiles.

364 J. Robert Mitchell and D. A. Shepherd

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

and emphasis on each attribute or combination ofattributes in the decision maker’s strategic decisionsabout opportunity pursuit at either Time 1 or Time 2.To reduce the prospect of error in our measure, weused only significant beta weights (p < 0.05).

To arrive at a measure of decision incongruencefor each decision maker at Time 1 and at Time 2, wecalculated the gap between decision makers’ stan-dardized regression coefficients (actual decisionmaking) with their self-report scores (conveyed deci-sion making) for each attribute or interaction ofattributes (e.g., one for knowledge relatedness, onefor value, etc.). This allowed us to ‘compare applesto apples’ in calculating the gap, as we now explain.

To arrive at a number reflecting an individual’sactual decision making, we first summed the signifi-cant standardized regression coefficients for eachdecision maker to result in a decision maker-specificmeasure of the total actual effect for each decisionmaker. We then divided each of the decision maker’ssignificant standardized coefficients by the measureof total actual effect to result in a decision maker-specific percentage of actual effects explained byeach attribute. We followed a similar process toarrive at a number for the self-report measures ofeach attribute. We first summed the absolute valuesof the self-report scores that each decision makergave for each attribute to result in a decision-maker-specific measure of the total conveyed effect for eachdecision maker. We then divided each of the decisionmaker’s self-report scores by this total conveyedeffect to result in a decision maker-specific percent-age of conveyed effects explained by each attribute(or interaction of attributes).

Next, a difference score was calculated for eachattribute by matching and subtracting the scores thatindividuals conveyed from the corresponding scores

they actually used. The absolute value of each dif-ference represented the gap for each respectiveattribute. Finally, we summed the values represent-ing the gap between what an individual actually didand what the individual said he/she did to result in atotal measure of decision incongruence for eachdecision maker. As we later note, decision incongru-ence at Time 1 was included as a covariate control,with decision incongruence at Time 2 as the depen-dent variable. Appendix B provides an illustration ofour decision incongruence calculation for one of theCEOs in our study.

Knowledge codification

In operationalizing knowledge codification, we ran-domly assigned the decision makers to either anexperimental condition or a control condition. In theexperimental condition, we asked decision makers tovisually describe their decisions using visual depic-tions of the four opportunity attributes (knowledgerelatedness, value, etc.) and uni-/bidirectional arrowsof varying thickness to indicate importance. Withthese visual depictions and arrows, decision makerscodified knowledge that was related to the opportu-nity decision-making task. For instance, as theexample in Appendix C depicts, this CEO codifiedthe following effects on likelihood of investment (A):knowledge relatedness (B) and potential value (C) aslarge main effects; number of potential opportunities(D) as a medium main effect; window of opportunity(E) as a small main effect; and knowledge related-ness (B) and potential value (C) as having a largeinteraction effect. After developing a visual model,we then asked decision makers in the experimentalcondition to use the codified model to talk throughthe three extra hypothetical opportunities they hadevaluated during the first decision task.

Experimental

manipulation

Time 2

measurement

Post-experiment

questionnaire

· Gen. human capital

· Spec. human capital

· Firm characteristics

· Other Individual factors

Debriefing

Actual decision making

· 16 experiment profiles

Self-report of decision making

· Main effects

· Moderating effects

Knowledge codification

· Control condition

· Experimental condition

Instructions

Actual decision making

· 1 practice profile

· 16 experiment profiles

· 3 extra profiles

Self-report of decision making

· Main effects

· Moderating effects

Post-experiment

questionnaire

Instructions/time

1 measurement

Figure 1. Temporal sequence of the field experiment(Progression of the field experiment during the one-hour interview)

Opportunity, Capability Development, and Decision Incongruence 365

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

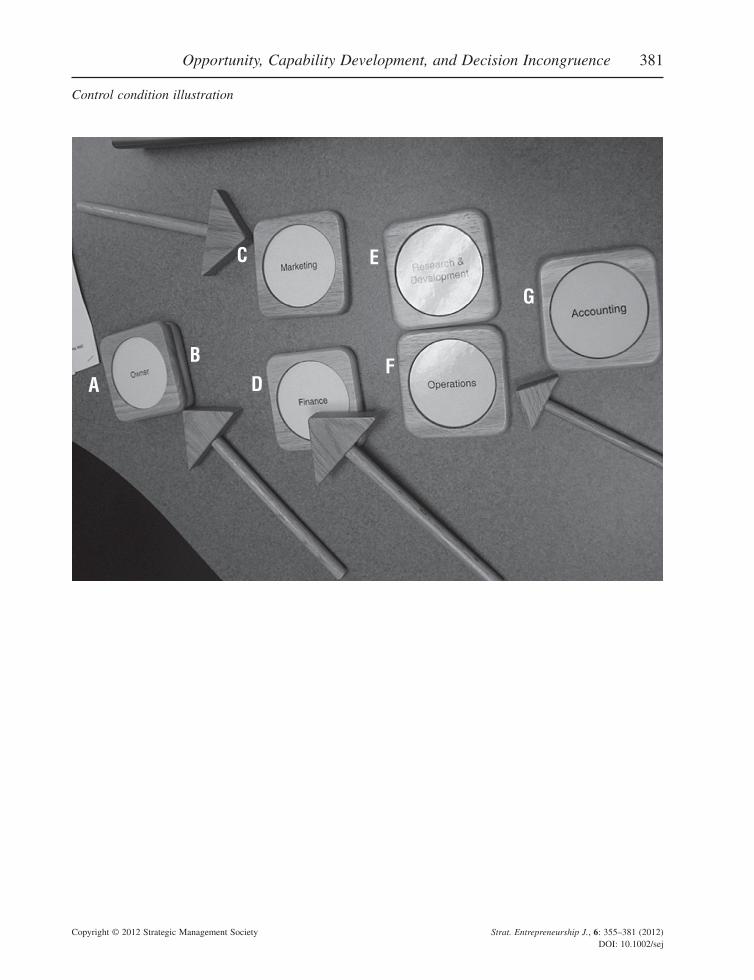

In contrast, we gave decision makers in the controlcondition a distracter task, wherein we asked them tovisually describe how their decisions about opportu-nities related to their firm using visual depictions ofvarious aspects/levels of firm structure (president/CEO, owner, operations, accounting, etc.) and uni-/bidirectional arrows of varying thickness to indicateimportance. With these visual depictions and arrows,decision makers codified knowledge that was unre-lated to the opportunity decision-making task. Forinstance, as the example in Appendix C depicts, thisdecision maker codified the owner (A), president/CEO (B), marketing (C), and finance (D) as having alarge role in decisions about opportunities; researchand development (E) and operations (F) as having amedium role; and accounting (G) as having a negli-gible role. Decision makers in the control conditiondid not develop or record a model of opportunitypursuit and were not presented the three extra hypo-thetical opportunities they had evaluated during thefirst decision task.

General and specific entrepreneurial human capital

For our measures of both general human capital andspecific entrepreneurial human capital, we followedan approach that is similar to prior research in entre-preneurship (e.g., Corbett, 2007; Dimov and Shep-herd, 2005; Gimeno et al., 1997). For our measure ofgeneral human capital, we created an index consist-ing of standardized values for CEO’s age, education(university degree versus none), and total work expe-rience. For our measure of specific entrepreneurialhuman capital, we created an index consisting ofstandardized values for each CEO’s industry-specific work experience, status as a founder of thefirm, and the number of other start-ups in whichhe/she had been involved. We note that the numberof other start-ups was log transformed because thisitem was not normally distributed.

Control variables

We also sought to control for other potential sourcesof variance in decision incongruence. First, we con-trolled for decision complexity, which reflected thenumber of attributes used by a decision maker in adecision (Nutt, 1998). This was measured as themaximum number of significant attributes for eachCEO at Time 1 or Time 2 (ranging from 1 to 7). Weexpected that those who had more complex decisionpolicies might also have a more difficult time

conveying their decision, simply because therewould be more to convey. Second, we controlled forindividuals’ erratic decisions (Mitchell, Shepherd,and Sharfman, 2011a), which reflected (and wasmeasured as) a change in decision makers’ actualdecision-making rationale between Time 1 and Time2. Our expectation was that those individuals whoare more erratic in their decisions might also have amore difficult time conveying their decision-makingrationale. Third, as noted previously, we followedBaron and Ensley (2006) and compared samples as away of understanding whether differences existbeyond accumulated experience between those withlow versus high general human capital and lowversus high specific entrepreneurial human capital.Because the results indicated that differences (p <0.05) existed between samples for firm age and firmsize, both firm age and firm size are included ascontrols. Finally, decision makers were randomlyassigned to the experimental or control condition,which controlled for other potential sources of vari-ance (Campbell and Stanley, 1963).

In our regression analysis, we included pretestscores as covariates because they provide ‘a moresensitive test of possible differences among treat-ments’ (Huck and McLean, 1975: 516). As such,decision incongruence at Time 1 was included as acontrol variable, with decision incongruence at Time2 as a dependent variable. Of the 127 decisionmakers in the study, two had actual decision policieswith no significant effects and conjoint analysisresponses that were unreliable (i.e., their responseson the replicated eight profiles were not significantlycorrelated with their original eight). Consequently,we excluded both cases from the analysis, resultingin a total sample of 125.

RESULTS

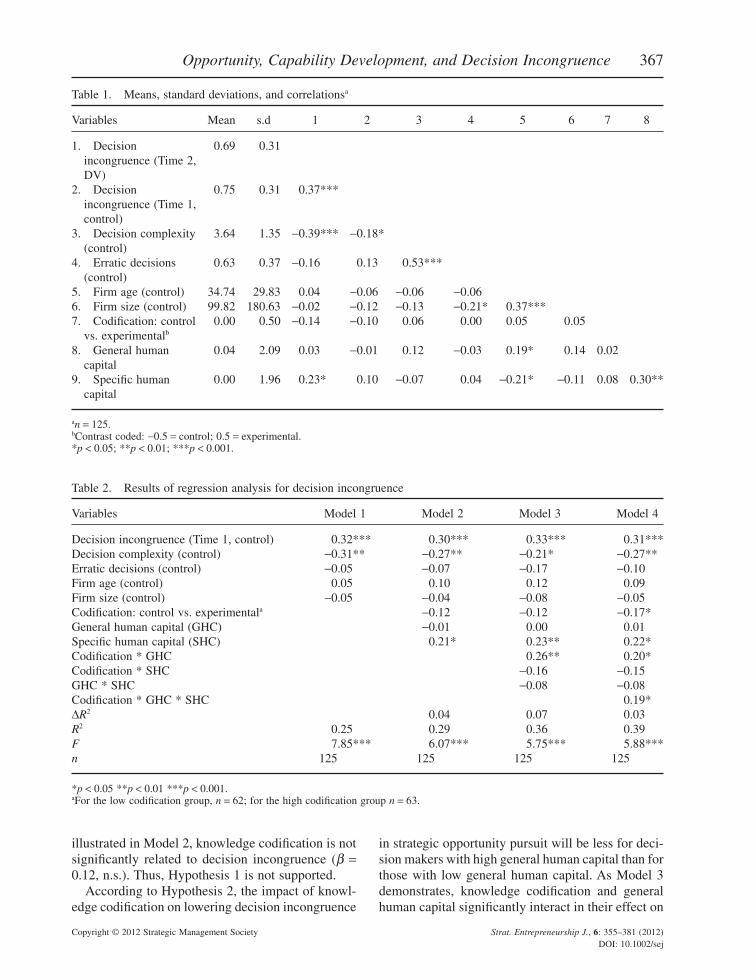

Table 1 shows the means, standard deviations, andcorrelations. To check for multicollinearity, weexamined the variance inflation factors. All of thevariables in the models were considerably lower thanthe recommended value of 10 (Neter et al., 1996).Table 2 summarizes the regression results. Accord-ing to Hypothesis 1, decision makers who useknowledge codification to describe their strategicdecisions about opportunity pursuit will have lowerdecision incongruence than those decision makerswho do not use knowledge codification. As is

366 J. Robert Mitchell and D. A. Shepherd

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

illustrated in Model 2, knowledge codification is notsignificantly related to decision incongruence (b =0.12, n.s.). Thus, Hypothesis 1 is not supported.

According to Hypothesis 2, the impact of knowl-edge codification on lowering decision incongruence

in strategic opportunity pursuit will be less for deci-sion makers with high general human capital than forthose with low general human capital. As Model 3demonstrates, knowledge codification and generalhuman capital significantly interact in their effect on

Table 1. Means, standard deviations, and correlationsa

Variables Mean s.d 1 2 3 4 5 6 7 8

1. Decisionincongruence (Time 2,DV)

0.69 0.31

2. Decisionincongruence (Time 1,control)

0.75 0.31 0.37***

3. Decision complexity(control)

3.64 1.35 -0.39*** -0.18*

4. Erratic decisions(control)

0.63 0.37 -0.16 0.13 0.53***

5. Firm age (control) 34.74 29.83 0.04 -0.06 -0.06 -0.066. Firm size (control) 99.82 180.63 -0.02 -0.12 -0.13 -0.21* 0.37***7. Codification: control

vs. experimentalb0.00 0.50 -0.14 -0.10 0.06 0.00 0.05 0.05

8. General humancapital

0.04 2.09 0.03 -0.01 0.12 -0.03 0.19* 0.14 0.02

9. Specific humancapital

0.00 1.96 0.23* 0.10 -0.07 0.04 -0.21* -0.11 0.08 0.30**

an = 125.bContrast coded: -0.5 = control; 0.5 = experimental.*p < 0.05; **p < 0.01; ***p < 0.001.

Table 2. Results of regression analysis for decision incongruence

Variables Model 1 Model 2 Model 3 Model 4

Decision incongruence (Time 1, control) 0.32*** 0.30*** 0.33*** 0.31***Decision complexity (control) -0.31** -0.27** -0.21* -0.27**Erratic decisions (control) -0.05 -0.07 -0.17 -0.10Firm age (control) 0.05 0.10 0.12 0.09Firm size (control) -0.05 -0.04 -0.08 -0.05Codification: control vs. experimentala -0.12 -0.12 -0.17*General human capital (GHC) -0.01 0.00 0.01Specific human capital (SHC) 0.21* 0.23** 0.22*Codification * GHC 0.26** 0.20*Codification * SHC -0.16 -0.15GHC * SHC -0.08 -0.08Codification * GHC * SHC 0.19*DR2 0.04 0.07 0.03R2 0.25 0.29 0.36 0.39F 7.85*** 6.07*** 5.75*** 5.88***n 125 125 125 125

*p < 0.05 **p < 0.01 ***p < 0.001.aFor the low codification group, n = 62; for the high codification group n = 63.

Opportunity, Capability Development, and Decision Incongruence 367

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

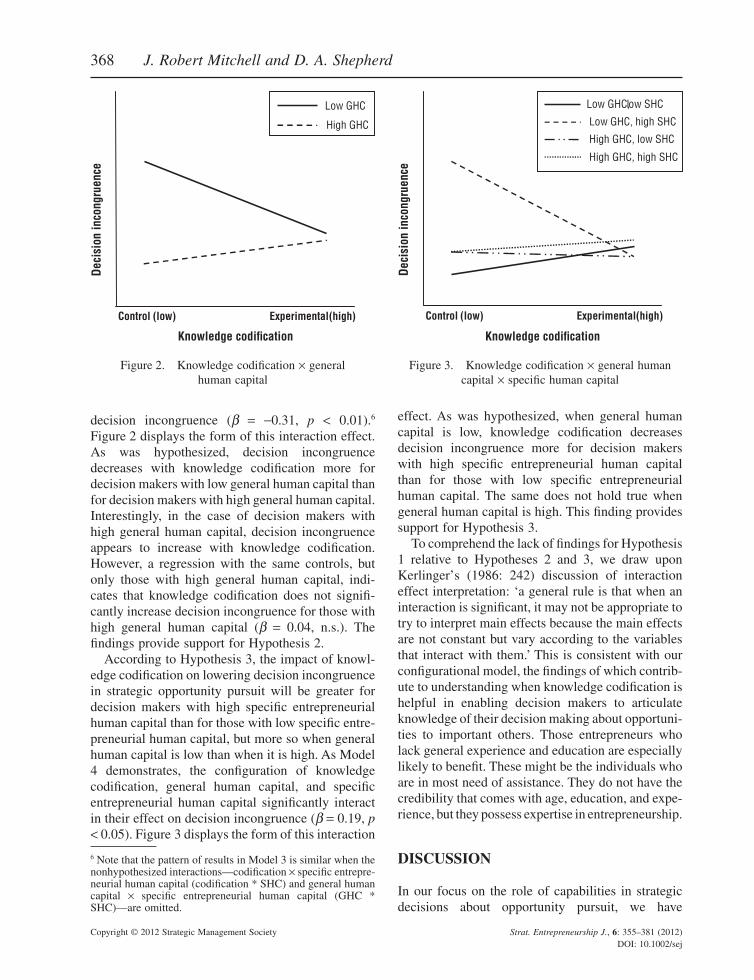

decision incongruence (b = -0.31, p < 0.01).6

Figure 2 displays the form of this interaction effect.As was hypothesized, decision incongruencedecreases with knowledge codification more fordecision makers with low general human capital thanfor decision makers with high general human capital.Interestingly, in the case of decision makers withhigh general human capital, decision incongruenceappears to increase with knowledge codification.However, a regression with the same controls, butonly those with high general human capital, indi-cates that knowledge codification does not signifi-cantly increase decision incongruence for those withhigh general human capital (b = 0.04, n.s.). Thefindings provide support for Hypothesis 2.

According to Hypothesis 3, the impact of knowl-edge codification on lowering decision incongruencein strategic opportunity pursuit will be greater fordecision makers with high specific entrepreneurialhuman capital than for those with low specific entre-preneurial human capital, but more so when generalhuman capital is low than when it is high. As Model4 demonstrates, the configuration of knowledgecodification, general human capital, and specificentrepreneurial human capital significantly interactin their effect on decision incongruence (b = 0.19, p< 0.05). Figure 3 displays the form of this interaction

effect. As was hypothesized, when general humancapital is low, knowledge codification decreasesdecision incongruence more for decision makerswith high specific entrepreneurial human capitalthan for those with low specific entrepreneurialhuman capital. The same does not hold true whengeneral human capital is high. This finding providessupport for Hypothesis 3.

To comprehend the lack of findings for Hypothesis1 relative to Hypotheses 2 and 3, we draw uponKerlinger’s (1986: 242) discussion of interactioneffect interpretation: ‘a general rule is that when aninteraction is significant, it may not be appropriate totry to interpret main effects because the main effectsare not constant but vary according to the variablesthat interact with them.’ This is consistent with ourconfigurational model, the findings of which contrib-ute to understanding when knowledge codification ishelpful in enabling decision makers to articulateknowledge of their decision making about opportuni-ties to important others. Those entrepreneurs wholack general experience and education are especiallylikely to benefit. These might be the individuals whoare in most need of assistance. They do not have thecredibility that comes with age, education, and expe-rience, but they possess expertise in entrepreneurship.

DISCUSSION

In our focus on the role of capabilities in strategicdecisions about opportunity pursuit, we have

6 Note that the pattern of results in Model 3 is similar when thenonhypothesized interactions—codification ¥ specific entrepre-neurial human capital (codification * SHC) and general humancapital ¥ specific entrepreneurial human capital (GHC *SHC)—are omitted.

Deci

sion

inco

ngru

ence

Control (low) Experimental(high)

Knowledge codification

Low GHC

High GHC

Figure 2. Knowledge codification ¥ generalhuman capital

Deci

sion

inco

ngru

ence

Control (low) Experimental(high)

Knowledge codification

Low GHC, low SHC

Low GHC, high SHC

High GHC, low SHC

High GHC, high SHC

Figure 3. Knowledge codification ¥ general humancapital ¥ specific human capital

368 J. Robert Mitchell and D. A. Shepherd

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

indirectly adopted a resource-based view of decisionmaking (cf. Amit and Schoemaker, 1993; Barney,1991; Peteraf, 1993; Wernerfelt, 1984). Our findingsrelated to decision incongruence contribute to thisever growing and deepening area of inquiry bygiving additional attention to the role of knowledgecodification as a capability that certain individualscan develop to assist them in their strategic opportu-nity pursuit. We see these findings as particularlysalient considering the importance of entrepreneurialaction to organizational renewal (Barringer andBluedorn, 1999; Hitt et al., 2001; Zahra and Covin,1995). Thus, in the following subsections, we linkour findings to extant entrepreneurship and resource-based research, underscore the implications of ourfindings for practice, and acknowledge the limita-tions of this study, while highlighting future researchpossibilities.

Implications for theory

We see three primary contributions of this research.First, the extreme conditions that occur in the pursuitof opportunities lead us to view entrepreneurship asan ideal context in which to explore cognition(Baron, 1998). Specifically, in our investigation ofdecision incongruence, we clarify the boundary con-ditions of when individuals may face difficulties inconveying the simple rules they use in their decisionmaking about opportunities (cf. Bingham et al.,2007; Smith and Miller, 1978), while also suggestingsome potential remedies of such difficulties. We findthat the impact of knowledge codification on lower-ing decision incongruence in strategic opportunitypursuit is greater for decision makers with high spe-cific entrepreneurial human capital than for thosewith low specific entrepreneurial human capital, butmore so when general human capital is low thanwhen it is high. In this sense, not only does ourresearch contribute to an understanding of the impor-tance of certain learning mechanisms in the pursuitof opportunity (Zander and Kogut, 1995; Zollo andWinter, 2002), but it also speaks to the larger ques-tion of ‘when (not whether) people are able to reportaccurately on their mental processes’ (Smith andMiller, 1978: 361).

Our research also captures three of the four keyelements called for in a socially situated view ofentrepreneurial cognition (see, e.g., Mitchell et al.,2011b; Smith and Semin, 2004). That is, we adopt anaction-oriented perspective with our focus on strate-gic decision making in opportunity pursuit, which

plays an important role in entrepreneurial action (cf.Busenitz and Barney, 1997; McMullen and Shep-herd, 2006). Knowledge codification itself likewiserepresents a kind of embodied action, in that itrequires more than just saying, but rather physicallyrecording knowledge that has been converted intoidentifiable rules and relationships (Cowan andForay, 1997; Kogut and Zander, 1992). Similarly,our approach is implicitly situated in our positioningof decreased decision incongruence as a way toincrease an individual’s ability get ‘buy-in’ from keystakeholders (cf. Brush et al., 2001; Kor, 2003;Miller and Ireland, 2005), thereby enabling coordi-nation, higher-quality group decision making andbetter firm performance (cf. Bingham et al., 2007;Bonner and Baumann, 2012; Hirokawa et al., 1996;van Dijk et al., 2009). However, as we note in a latersection, future research is needed to understand howcognition might be distributed across social agents.

These broader contributions notwithstanding, theprimary focus of our article is entrepreneurial deci-sion making. Given the importance of strategicopportunity pursuit to organizational renewal (Bar-ringer and Bluedorn, 1999; Hitt et al., 2001; Zahraand Covin, 1995), our findings would seem to beespecially salient. Indeed, the ability to reduce deci-sion incongruence can be viewed as a resource forcertain entrepreneurial ventures (Alvarez and Bus-enitz, 2001) because those entrepreneurs who canaccurately convey to others the rationale that under-lies their decisions should be more likely to succeedin strategic opportunity pursuit (cf. Bingham et al.,2007; Brush et al., 2001; Miller and Ireland, 2005).Although opportunity pursuit does represent animportant strategic context (Dess and Lumpkin,2005), it is only one of many important strategicdecision-making contexts in entrepreneurship.Therefore, we wonder what our results may suggestfor other decision-making contexts, especiallywhether the configuration of general human capitaland specific entrepreneurial human capital shape theeffectiveness of a knowledge codification capabilityin reducing decision incongruence for other deci-sions, such as those related to sources of funding,modes of opportunity exploitation (including alli-ance formation), and exit.

A second theoretical contribution of this studyinvolves our finding that the capability-buildingexperience of those with specific entrepreneurialhuman capital, but limited general human capital,has a differential effect on decision incongruence instrategic opportunity pursuit. For us, understanding

Opportunity, Capability Development, and Decision Incongruence 369

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

the differences in approaches to strategic opportu-nity pursuit between those with entrepreneurialexperience and those without adds to research thathas investigated differences between entrepreneursand nonentrepreneurs (e.g., Baron, 1999; McGrath,MacMillan, and Scheinberg, 1992; Mitchell et al.,2002) by furthering understanding of differences incategories of entrepreneurs (Sarasvathy, 2004).Indeed, our results relating to general human capitalwould seem to support the contingent effects of cat-egories of entrepreneurs, especially in terms ofdimensions that may not seem at first glance to beexpressly entrepreneurial in nature.

Along these lines, our results support the idea thatthe capability-building activities in strategic deci-sions about opportunity pursuit are not equal and,thus, should differ in their application by differenttypes of entrepreneurs. While knowledge codifica-tion may be less critical for those with high generalhuman capital, it appears to be highly important forthose with low general human capital and highspecific entrepreneurial human capital. In this way,our findings contribute to prior research that hasaddressed how differences in entrepreneurialexperience can result in behavioral differences (e.g.,Begley and Boyd, 1987; Busenitz and Barney, 1997;Forbes, 2005). In our study, this difference is seen inthe differential ability to articulate knowledge ofdecision making about opportunities.

Third, our configurational findings, that theimpact of knowledge codification on decision incon-gruence will be greater for those with low generalhuman capital and high specific entrepreneurialhuman capital than others, also contributes to capa-bilities research (e.g., Barney, 1986; Hall, 1993;Zahra, Sapienza, and Davidsson, 2006) by furtherillustrating the benefits and boundaries of knowledgecodification as a learning mechanism (Zander andKogut, 1995; Zollo and Winter, 2002). In this sense,we illustrate how and when knowledge codificationrepresents a potential dynamic capability (cf. Teeceet al., 1997; Winter, 2003). By investigating thisquestion in terms of decision incongruence, webegin to bridge the organizational knowledge, orga-nizational routines, and heuristics literatures (cf.Bingham and Eisenhardt, 2011). We do so by dem-onstrating how knowledge codification and experi-ence, as learning mechanisms that underlie theevolution of routines (Zander and Kogut, 1995;Zollo and Winter, 2002), can be useful in the articu-lation and application of the heuristics (simple rules)that underlie the pursuit of opportunities (cf.

Bingham and Eisenhardt, 2011; Bingham et al.,2007).

To this latter point, individuals’ understanding ofhow the combination of experience and knowledgecodification can reduce decision incongruence is askill that can then be used as a mechanism to developand adapt other organizational capabilities and rou-tines (Zollo and Winter, 2002). Moreover, our find-ings support the idea that knowledge codificationand experience are mechanisms that can facilitate thecreation of dynamic capabilities insofar as they canfacilitate diffusion of knowledge related to a specificcapability (Nonaka, 1994; Zollo and Winter,2002)—in this case, the heuristics underlying strate-gic opportunity pursuit. Thus, a dynamic capabilityis created insofar as an understanding of the configu-ration of knowledge codification and experience canbe used to increase the usefulness of similar knowl-edge in other situations and circumstances.

In speaking of dynamic capabilities, Collis (1994:151) noted that because dynamic capabilities canalways be superseded by higher-order capabilities,researchers should not simply extol the virtues ofcapabilities devoid of context, but should insteadseek to ‘generate lists of the enormous variety ofcapabilities and develop normative prescriptions foractually building those capabilities’ in a particulartemporal context. Our finding about the boundariesin usefulness of knowledge codification represents astep in this direction. That is, our results illustrate aparticular temporal context (i.e., strategic opportu-nity pursuit) wherein there exists a capability differ-ential (i.e., knowledge codification that is morebeneficial to certain individuals than others). Thus,future research is warranted to investigate the poten-tial performance effects of such knowledge codifica-tion differences. It may be, for instance, that incontext of a start-up, any potential negative effects ofcommunicating tacit knowledge can be counteredwhile still preserving the positive effects (cf.Berman, Down, and Hill, 2002; Coff et al., 2006).

Implications for practice

The findings reported herein can directly assistentrepreneurs. It is often the case that decisionsabout opportunities are taken on faith alone (Millerand Ireland, 2005: 25). Through knowledge codifi-cation, however, those with low general humancapital, but high specific entrepreneurial humancapital, can decrease decision incongruence aboutstrategic opportunity pursuit and, in so doing, may

370 J. Robert Mitchell and D. A. Shepherd

Copyright © 2012 Strategic Management Society Strat. Entrepreneurship J., 6: 355–381 (2012)DOI: 10.1002/sej

be in a better position to gain access to criticalresources from others who might otherwise withholdresources due to knowledge asymmetries (Hayek,1945; Miller and Ireland, 2005). Of course, decisionmakers who rely on ‘bootstrap financing’ in thepursuit of opportunity can be less concerned aboutdecision incongruence. However, from a practicalperspective, the individual seeking external financ-ing who possesses high specific entrepreneurialhuman capital, but low general human capital, mayspecifically benefit from decreased decision incon-gruence. Indeed, as a result of low general humancapital, such an individual might lack some credibil-ity with potential stakeholders (cf. Spence, 1973,2002) but at the same time be well positioned topursue opportunity as a result of high specific entre-preneurial capital. For him/her, decreasing decisionincongruence may be especially useful.

Knowledge codification may also provide achannel for understanding other difficult-to-communicate knowledge in entrepreneurial organi-zations (Hedlund, 1994; Osterloh and Frey, 2000;Stenmark, 2001). Knowledge codification may, forinstance, provide a novel mechanism for individualsto reduce the ‘glitches’ in strategic opportunitypursuit that can arise as a result of insufficientknowledge sharing (Hoopes and Postrel, 1999).Once understood, knowledge codification can alsolead to the creation of the organizational and struc-turing documents and systems that are the founda-tion of replicable routines surrounding the use oftacit knowledge (Nelson and Winter, 1982). Practi-cally speaking, individuals who understand how tobenefit from knowledge codification in one decision-making area (i.e., strategic opportunity pursuit) maythen replicate these new routines for articulation inthe management of other areas of strategic decisionmaking.

Limitations and future research

Within this section, we discuss the limitations of ourstudy and (when applicable) link them to the yetunanswered questions that are implied. First, ourinvestigation has been limited to decision incongru-ence in strategic opportunity pursuit. We haveadopted this approach because strategic opportunitypursuit represents decision making that is importantto the creation, renewal, and survival of organiza-tions (Barringer and Bluedorn, 1999; Hitt et al.,2001; Zahra and Covin, 1995). However, we alsoexpect that problems of decision incongruence will

extend beyond strategic opportunity pursuit. Indeed,generalizability considerations require that othertypes of strategic decision making be explored aswell. Thus, future research must ask whether deci-sion incongruence occurs in multiple settings andwhether knowledge codification has a similar impactin other strategic decision-making contexts.

Second, we tested our theory in an experimentalfield setting (cf. Harrison and List, 2004). In con-ducting a field experiment, we were able to controlfor ‘noise’ that exists in strategic opportunity pursuit,while at the same time provide a realistic context forthe decision maker (making decisions about theseopportunities for their current firm and in the currentindustry and economic environment). Of course, weacknowledge that the CEOs in our study made deci-sions about ‘hypothetical’ versus ‘actual’ opportuni-ties. However, our decision to use an experimentalapproach was guided by our desire to understand theconditions that would enable individuals to betterarticulate knowledge of their decision making aboutopportunities. Our use of hypothetical opportunitiesin a metric conjoint analysis specifically allowed usto obtain such real-time information about decisionsthat could then be compared with the information theCEOs conveyed through self-reports. In futureresearch, however, these findings could be general-ized to more ‘natural’ field settings (Harrison andList, 2004).