canned tuna in the middle east: a market searching for...

TRANSCRIPT

Canned Tuna in the Middle East: A market searching for profit ? May 2018

Arnab Sengupta

This document aims to answer the following:

Key Questions

Is Middle East an interesting market for canned tuna?

1

Parameters of tuna consumption we should know while entering ME

2

What should be done to gain more market share

3

Table of Contents

Middle East Food Retail

How to we consume Tuna

Tuna Market Overview

Middle East Tuna Market: Overview

4

Frozen is limited to very niche sushi stores and some

local coastal catch near Oman and

Yemen. Catching's are seasonal, near

coast and not consistent

Tuna consumption in Middle East and North African is primarily in canned format some local catch, negligible in frozen format. In canned format the market is around $800M

The region does not have any non tariff barriers. Arab league 0% rest of the world 5%. Sustainability growing interest. Though a region

bound by language and religion, tuna eating hobbits differ.

Growing Interest from international brands, though the market is driven by familiarity and heritage. Rio Mare, John West carving a niche in the premium segment. Growth for profit, current mantra

5

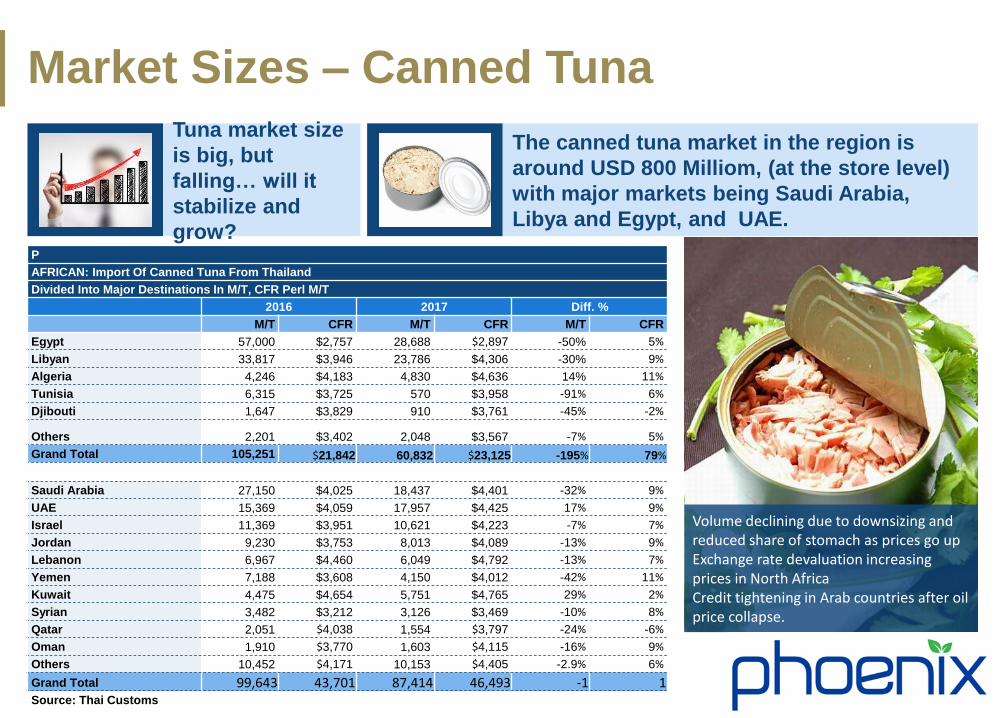

Market Sizes – Canned Tuna

5

Tuna market size

is big, but

falling… will it

stabilize and

grow?

The canned tuna market in the region is

around USD 800 Milliom, (at the store level)

with major markets being Saudi Arabia,

Libya and Egypt, and UAE.

Volume declining due to downsizing and reduced share of stomach as prices go up Exchange rate devaluation increasing prices in North Africa Credit tightening in Arab countries after oil price collapse.

P

AFRICAN: Import Of Canned Tuna From Thailand

Divided Into Major Destinations In M/T, CFR Perl M/T

2016 2017 Diff. %

M/T CFR M/T CFR M/T CFR

Egypt 57,000 $2,757 28,688 $2,897 -50% 5%

Libyan 33,817 $3,946 23,786 $4,306 -30% 9%

Algeria 4,246 $4,183 4,830 $4,636 14% 11%

Tunisia 6,315 $3,725 570 $3,958 -91% 6%

Djibouti 1,647 $3,829 910 $3,761 -45% -2%

Others 2,201 $3,402 2,048 $3,567 -7% 5%

Grand Total 105,251 $21,842 60,832 $23,125 -195% 79%

Saudi Arabia 27,150 $4,025 18,437 $4,401 -32% 9%

UAE 15,369 $4,059 17,957 $4,425 17% 9%

Israel 11,369 $3,951 10,621 $4,223 -7% 7%

Jordan 9,230 $3,753 8,013 $4,089 -13% 9%

Lebanon 6,967 $4,460 6,049 $4,792 -13% 7%

Yemen 7,188 $3,608 4,150 $4,012 -42% 11%

Kuwait 4,475 $4,654 5,751 $4,765 29% 2%

Syrian 3,482 $3,212 3,126 $3,469 -10% 8%

Qatar 2,051 $4,038 1,554 $3,797 -24% -6%

Oman 1,910 $3,770 1,603 $4,115 -16% 9%

Others 10,452 $4,171 10,153 $4,405 -2.9% 6%

Grand Total 99,643 43,701 87,414 46,493 -1 1 Source: Thai Customs

Tuna Value Trend

Sinusoidal Volume Behavior with 50%+ Value Captured by Libya and Egypt

6

Tuna Volumes Full Year Trend Tuna Value Market Distribution

4

29

22 2327

40

36 3633

22

36 35 33

4 46

2016 Val by mkt in USD

2014 Val by mkt in USD

2

2015 Val by mkt in USD

3

2

2013 Val by mkt in USD

3

UAE LIBYA KWT KSA EGY

1,555

3,0133,0922,9992,578

3,401

2,092

2,193

2,2052,0801,8721,967

3,000

4,000

1,000

2,000

0

2,206

1,431

2011 12 13 14 15 16 17

Mid-East VOL-FCL Africa VOL-FCL

60,000

70,000

75,000

55,000

50,000

0

65,000 51,910

15

73,412 66,636

48,299

17 16

59,388 66,734

57,074

14

69,779

74,202

13

44,938

64,253

12

58,330 63,614

73,882

2011

ME Avg. Price per FCL in USD

A Africa Avg. Price per FCL

7

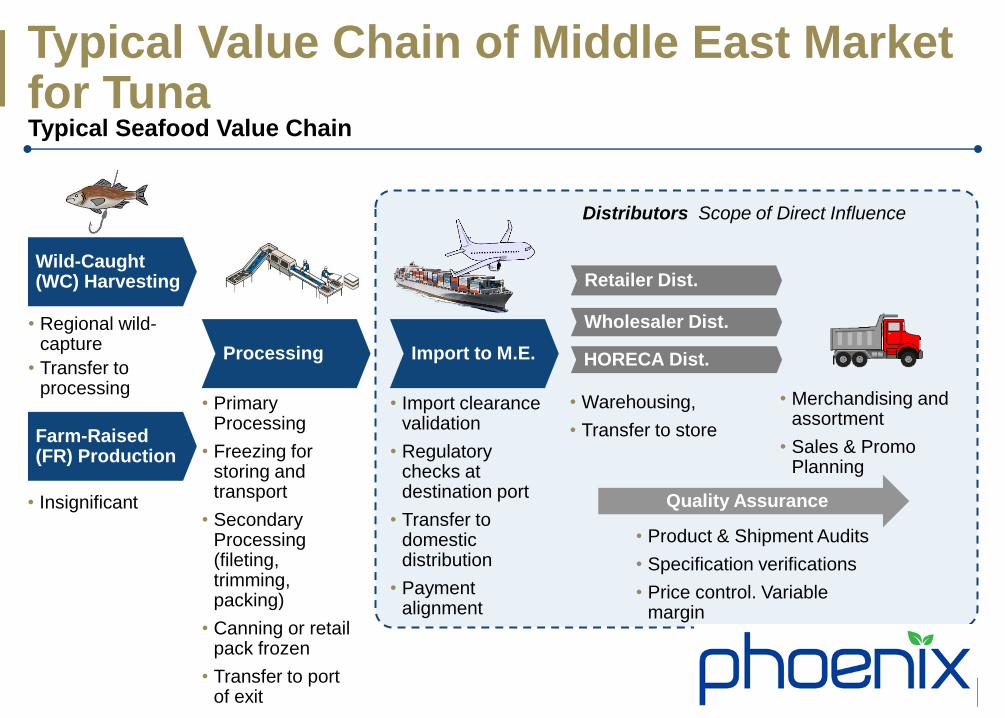

Typical Value Chain of Middle East Market for Tuna Typical Seafood Value Chain

Wild-Caught (WC) Harvesting

Processing

Farm-Raised (FR) Production

Import to M.E.

Retailer Dist.

• Primary Processing

• Freezing for storing and transport

• Secondary Processing (fileting, trimming, packing)

• Canning or retail pack frozen

• Transfer to port of exit

• Import clearance validation

• Regulatory checks at destination port

• Transfer to domestic distribution

• Payment alignment

• Merchandising and assortment

• Sales & Promo Planning

• Warehousing,

• Transfer to store

• Regional wild-capture

• Transfer to processing

• Insignificant

Distributors Scope of Direct Influence

Wholesaler Dist.

HORECA Dist.

Quality Assurance

• Product & Shipment Audits

• Specification verifications

• Price control. Variable margin

Table of Contents

Middle East Food Retail

How to we consume Tuna

Tuna Market Overview

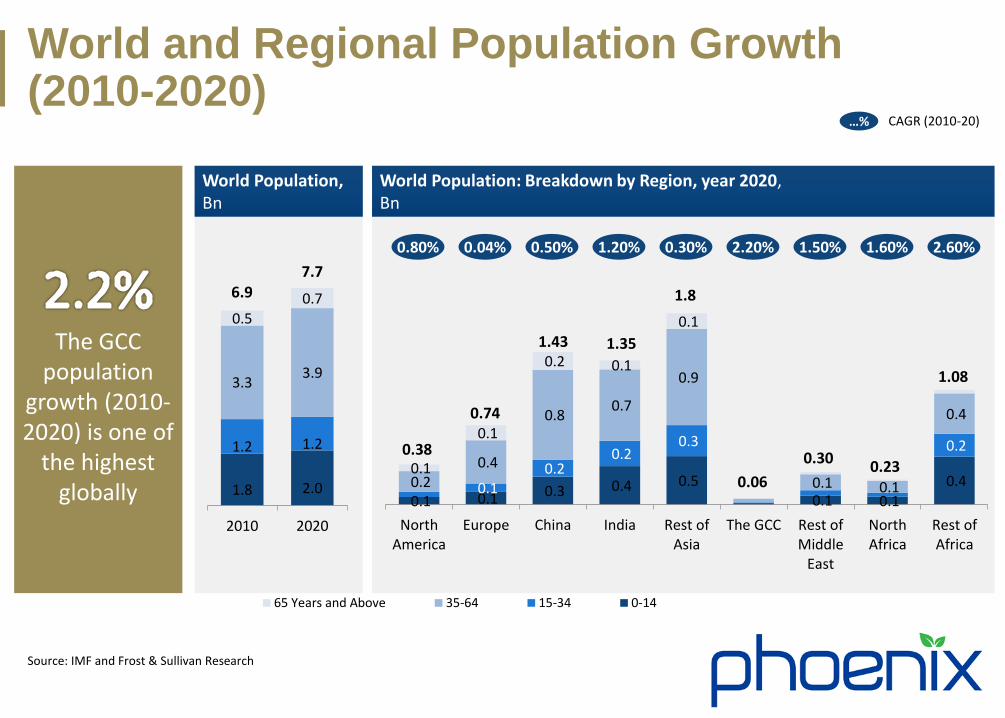

World and Regional Population Growth (2010-2020)

9

The GCC population

growth (2010-2020) is one of

the highest globally

World Population, Bn

World Population: Breakdown by Region, year 2020, Bn

1.8

2.0

1.2

1.2

3.3

3.9

0.5 0.7

2010 2020

0.1 0.1 0.3 0.4 0.5 0.1 0.1

0.4 0.1 0.2

0.2 0.3 0.2

0.2 0.4

0.8 0.7

0.9

0.1 0.1

0.4

0.1

0.1

0.2 0.1

0.1

NorthAmerica

Europe China India Rest ofAsia

The GCC Rest ofMiddle

East

NorthAfrica

Rest ofAfrica

65 Years and Above 35-64 15-34 0-14

6.9 7.7

0.38

0.74

1.43 1.35

1.8

0.06

0.30 0.23

1.08

0.80% 0.04% 0.50% 1.20% 0.30% 2.20% 1.50% 1.60% 2.60%

…% CAGR (2010-20)

Source: IMF and Frost & Sullivan Research

Catering to the new generation consumer is key in the GCC

10

The GCC Population, Mn.

11.0 11.6 12.7 14.1

14.2 18.5 19.7 20.9

9.7

14.3 19.0

23.1

0.9

1.0

1.3

1.9

2005 2010 2015 2020

0-14 15-34 35-64 65 Years and Above

Classification/ Categorisation of the Consumer segments

Generation X - Typically born before the 70s. • Has less impact of the Oil boom in the GCC and more into

traditional consumer behaviour with relative loyalty to a few brands

Generation Y/ Millennials – Born in the 80s and 90s. • Self-involved, Dependent, Racially and Ethnically diverse

group raised during the explosion of TV and Internet. Less loyal towards brands

Generation Z – Born after 2000 • Anxious, Highly connected, living in an age of high-tech

communication, technology driven lifestyles and prolific use of social media with mindful of the future

39%

35%

24%

Source: Frost & Sullivan Research

Generation Y+Z account on

overall population by 2020 and are

highly influential on Generation

X purchases

Megatrends Shaping up the Food & Beverages Sector

11

Meg

atre

nd

s

Growing Baseline

Market

POPULATION

Improving rate of

organization of the

Industry

URBANIZATION

‘Good For You’

Campaign

HEALTH &

WELLNESS

Exposure to

multicuisine /

products

GLOBALISATION

Change in Lifestyles

Growing Income Healthy Food Choice to Choose Quick Serve

Food Retail Product

Categories Micro

Segmentation Processed Food

Product Level Impact Industry Level Impact

Res

ult

of

Meg

atre

nd

s

Creating a Pool of Sub Trends

Categorizing consumer trends

12

Nutritional Facts

Increasing habit of reading labels to

understand product claims and

nutritional facts

Functional Products

Look out for functional products which reduce risk of chronic diseases

beyond basic nutritional functions

Consumption Experience

Products which suit ‘Snackification’ while skipping

conventional meals.

Good for you!

No artificial ingredients,

low fat, high fibre and organic version of

products

Packaging

Something which offers ease towards multiple

consumption occasions on the go. Also, which

suits the ‘Style Statement’

Taste

Product which is new to

the palate

Source: Frost & Sullivan Research

Which segment companies should act?

13

BREAKFAST

SNACKS

LUNCH

DINNER

Ready to eat, Protein based breakfast offering added benefits

Opportunity for

• Meat processing companies

• Bakery companies

• Breakfast cereal companies

Target consumer segment

• Entire range of consumers

• Probably focus on kids

Products with benefits

Opportunity for

• Dairy companies

• Beverage companies

• Snack companies

• Nutraceutical companies

Target consumer segment

• Generation Y and Generation Z

Table of Contents

Middle East Food Retail

How to we consume Tuna

Tuna Market Overview

Consumer Insights

15

Cooking still a domain of Housewife

The majority of consumers claim to do most of the cooking themselves

– Some get help from house maid or other members of the family

Working women rely heavily on housemaid

Cooking seen to be the duty of a good wife and mother

– Some do not openly admit to getting help

Men feel that only the lady of the house should cook, seen as a matter of pride

– Makes him feel important if she cares enough to cook for him

Housewife is always

challenged to prepare

dishes all will like

16

Lunch is the Main Meal of the Day

Lunch requires the most planning and preparation

– More complex / heavy

– Entire family sits together

– Main meal of the day

Dinner is often unplanned and spur of the moment

– Lighter

– More diverse / variety

– Family may eat independently

Breakfast is a very individual meal

– Except Fridays which turns into brunch

– Light cold dishes mostly

– Diverse / variety of dishes

Lunch in Arab world can happen

at 5pm meal when we sit

together and eat

DINNER

LUNCH

BREAKFAST

17

TUNA BUYING HABITS

18

Insights

Tuna is a staple available in every household

– Stocked quite heavily by the majority

Most families consume Tuna at least 2 times a week. In some cases consumption goes up 4 -5 times a week

For the majority Tuna is used more for dinner and lunch and often at parties and for outings (Picnics)

It is also seen as nutritious and liked by children who often do not like fresh fish

Tuna is considered quick and versatile and liked by the entire family

Often for short notice – unplanned meals

Tuna is considered on

economic dish for

everyday use-but also

seen as a commodity

19

Insights for us.

The number of cans consumed per occasion are quite high when used in main dish

Opportunity for family pack / economy pack

Overall, consumers are aware of different type of tuna, but in some cases the terminology used is not common to the industry

There is little awareness off difference between solid pack and other.

– Clearest distinction is between flakes and chunk tuna - prefer chunks

Few consumers take note or consider the oil type in which the tuna is packed.

– Majority agree it should be a light oil

Most consumers are aware of Tuna in brine, but use is limited to use when dieting.

Do not like fishy smell.

20

Tuna Category is Driven by Familiarity Mainly. BRAND CONSIDERATION Driving BRAND EQUITY Equity Drivers For Tuna

Sources of

Brand Equity

Industry Norms

Awareness: 30% Familiarity: 10% Associations: 60%

Awareness 11%

Familiarity 64%

Association 25%

Based on FMCG & Retail categories

Importance of Association Factors in Tuna

LIGHT & HIGH QUALITY

HEALTHY & PROVIDES VALUE

AESTHETICS MEAT QUALITIES

8% 8% 7% 2%

21 Source: Winning Brands Categories

Canned Tuna MENA – Positive and Negative Factors

22

Negative factors

New food option/Packing

Matured category

Low margin, trade uninterested

Status of low cost protein

My tuna recipe

Positive factors

Variety of eating usage for tuna

Side dish, cooked to sandwich

Recognition of healthy option

Part of growing up

Costal fishing heritage

Growing market

+ −

Communication Review

Communication: Tuna middle East

24

Merchandising support growing

ATL in certain

premium brands,

category lead by Rio Mare

Internet based tools are gaining popularity

Mostly promotions,

with secondary

display

Activations

25

In-Store

26

In-Store Presence

27

From the Internet

Communication review

28

Going beyond display campaigns few tuna brands are building

microsites on popular portals that included games/competitions

as well as content sharing and knowledge sharing about tuna

Digital

29

30

Opportunities in the Middle East Market Seafood Category Overview

Sourcing Process • Tuna pricing is driven by commodity

index hence spot purchased in favorable periods

• A mix of and spot buy are popular. Usually contacts are in 20 fcl or 2 fcl lots

ME Internal Demand • Market demand's cheap source for

protein. Tuna satisfy key criteria • Devaluation of regional currencies in

North Africa. • Demand of tuna at the HORECA level • Demand falling, lead by North Africa

Market Outlook • Canned tuna market in Middle East has

seen more than 20% dip this year due to currency.

• Frozen Fresh tuna demand increasing in GCC.

• Pet food market in UAE 65% of human food

Restaurant Items • Focus on Horeca needs. Ready to serve

sushi, pouch tuna, opportunity to grow

Pet Food • Hit directly, high margin category.

Allowing for efficiency gaps

Tuna • Efficiency of production, work on

packaging and printing technology. • Catering size opportunities

Key Strategic Initiatives

Benefits Potential

~M USD

Low hanging fruits

Thank you [email protected]

Main markets for Tuna in the region. Libya, KSA and Egypt.

33

Libya is the largest per capita tuna consumer in the world.

With its small population, it consumes more chunks pack than Egypt around 3 Million cases of 48 cans in 2016, a low year.

KSA is a growing market for chunks pack, while being predominantly a solid market.

The market of chunks and flakes are around 22% of around 3.3 M Cs Total market.

Tunisia and Algeria are potential markets, which are protected by hi tariff for non Arab league tuna, competition is limited.

Domestic consumption of tuna in Egypt is around 6.5 M cases of 48, of which 48% are flakes and rest chunks& solid.

Tunisia

Libya KSA

Algeria Egypt

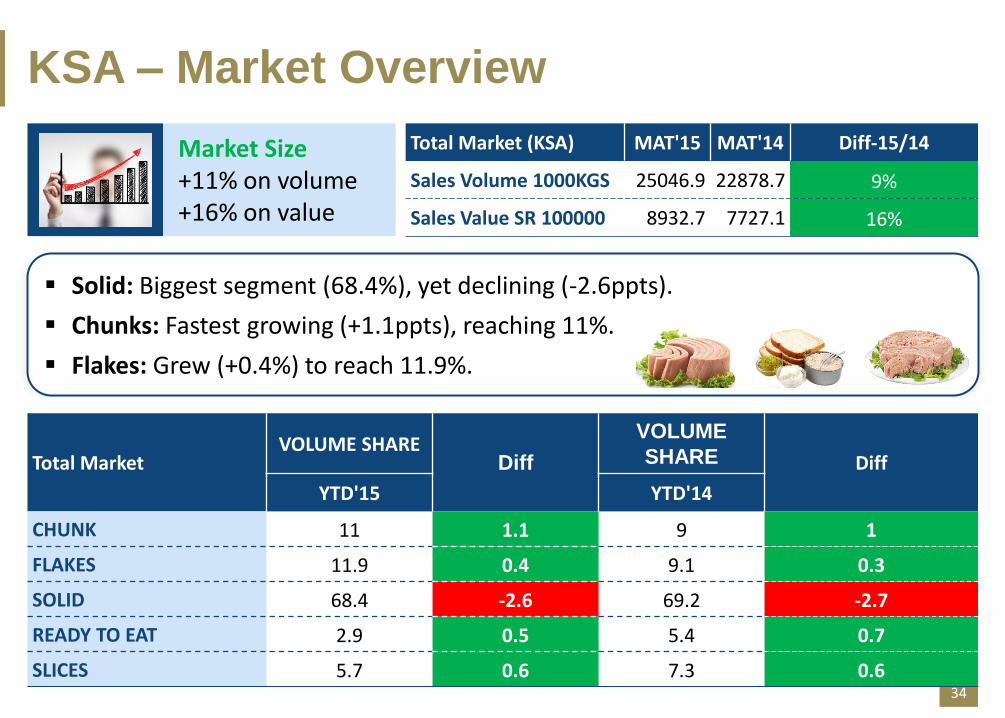

KSA – Market Overview

34

Market Size +11% on volume +16% on value

Total Market (KSA) MAT'15 MAT'14 Diff-15/14

Sales Volume 1000KGS 25046.9 22878.7 9%

Sales Value SR 100000 8932.7 7727.1 16%

Solid: Biggest segment (68.4%), yet declining (-2.6ppts).

Chunks: Fastest growing (+1.1ppts), reaching 11%.

Flakes: Grew (+0.4%) to reach 11.9%.

Total Market VOLUME SHARE

Diff

VOLUME

SHARE Diff

YTD'15 YTD'14

CHUNK 11 1.1 9 1

FLAKES 11.9 0.4 9.1 0.3

SOLID 68.4 -2.6 69.2 -2.7

READY TO EAT 2.9 0.5 5.4 0.7

SLICES 5.7 0.6 7.3 0.6

Egypt – Market Overview

Market Size -8.5% on volume -5.5% on value

Total Market MAT'15 MAT'14 Diff-15/14

Sales Volume 1000KGS 61901 72590 -8.5%

Sales Value LE 100000 25770 24655 +5.5%

Flakes: Biggest segment (53.2)% declined a few points (2.3%)

Solid: Growing segment (13.7%), growing

Chunks: Fastest growing (+1.1ppts), reaching 30.8%

Egypt currency has devalued ( 8.5 to 18) pushing the

prices in the market

35

Solid: Remains to be the largest cut at 54.9% (flat vs. YA), followed by

Chunks: at 18.8% (also flat), then

Flakes: at 16.2% (+0.4ppts)

UAE – Market Overview

36

Market Size +6% (volume and value)

Total Market MAT'15 MAT'14 Percentage Growth

Sales Volume 1000 KGS 3781.9 3554.5 6%

Sales Value 1000 AED 144165 132041 6%

Total Market VOLUME SHARE

Diff YTD'15 YTD'14

SOLID 54.9 55.0 -0.1

CHUNK 19.8 18.7 0.0

FLAKES 17.2 15.8 1.4

READY TO EAT 7.9 7.6 0.3

SLICES 1.4 2.8 -0.4