canadian fdi forum - area development

TRANSCRIPT

Canadian FDI Forum Opening Remarks for the 1st Edition

Gregg Wassmansdorf

Senior Managing Director, Consulting

(416) 998-8848

October 31, 2016

October 2016 | 1

Speaker

Gregg

Wassmansdorf

U.S. and Canadian citizen

Senior Managing Director, Consulting, NGKF

17 years in Management Consulting

Real Estate Portfolio Strategy

Corporate Location Strategy

Economic Incentives

October 2016 | 2

1. Introduction to Foreign Direct Investment (“FDI”)

2. The Canadian FDI Context

3. A Site Selectors Perspective

Objectives

October 2016 | 3

Congratulations!

October 2016 | 4

Geography is (not) Dead

2005: Thomas Friedman

Globalization levels playing field

Geography becomes less relevant

“Flatteners” bring the world together

“Innovate with no need to emigrate”

2005: Richard Florida

Globalization is uneven & unequal

Benefits & costs are geography-specific

Culture, education, innovation, wealth,

competitiveness are highly localized

October 2016 | 5

Geography is (not) Dead

“We’ve all been trained to believe in this ancient adage that geography

is destiny. I argue in fact connectivity is destiny.”

October 2016 | 6

Foreign Direct Investment | Key Themes

Notes: Figures are inclusive of all FDI flows. Percentage changes are 2014 to 2015.

Source: “Global Investment Trends 2015, Key Messages,” UNCTAD, 2016.

FDI is increasingly complex and ubiquitous

October 2016 | 7

FDI Inflows | Global by Group of Economies

Notes: Billions of dollars. Trend line is approximate.

Source: UNCTAD “World Investment Report 2015”, via conversableeconomist.blogspot.ca/2015/09/snapshots-of-foreign-direct-investment.html

FDI growth, volatility, and rising share toward developing economies is the norm

October 2016 | 8

FDI Outflows | Developing Economies in Context

Notes: Values in billions of dollars. Shares are in percentages.

Source: UNCTAD “World Investment Report 2015”, via conversableeconomist.blogspot.ca/2015/09/snapshots-of-foreign-direct-investment.html

Developing economies increasingly ‘senders’, not just ‘receivers’

October 2016 | 9

Canada Inward FDI

Notes:

Source: Conference Board of Canada via www.conferenceboard.ca/hcp/hot-topics/inwardfdi.aspx

Long-range trend capturing global FDI is negative . . .

October 2016 | 10

Canada Inward FDI

Notes:

Source: Conference Board of Canada via www.conferenceboard.ca/hcp/hot-topics/inwardfdi.aspx

Canada still gets “more than it’s fair share” of FDI (barely)

October 2016 | 11

Canada Inward FDI

Notes: Refers to “greenfield” investment only (not deb/ or equity flows and not M&A activity).

Source: “Canada Inward FDI - fDi Report, January 2013 to September 2016.” fDi Markets.

200 – 450 opportunities annually

October 2016 | 12

Canada Inward FDI

Notes: Refers to “greenfield” investment only (not deb/ or equity flows and not M&A activity).

Source: “Canada Inward FDI - fDi Report, January 2013 to September 2016.” fDi Markets.

Volatility stems from corporate planning, currency fluctuations, policy changes, etc.

October 2016 | 13

Canada Inward FDI

Source: “Canada Inward FDI - fDi Report, January 2013 to September 2016.” fDi Markets.

Top 3 metros capture 36 - 50% of investment, jobs, and projects; 953 other cities received FDI

October 2016 | 14

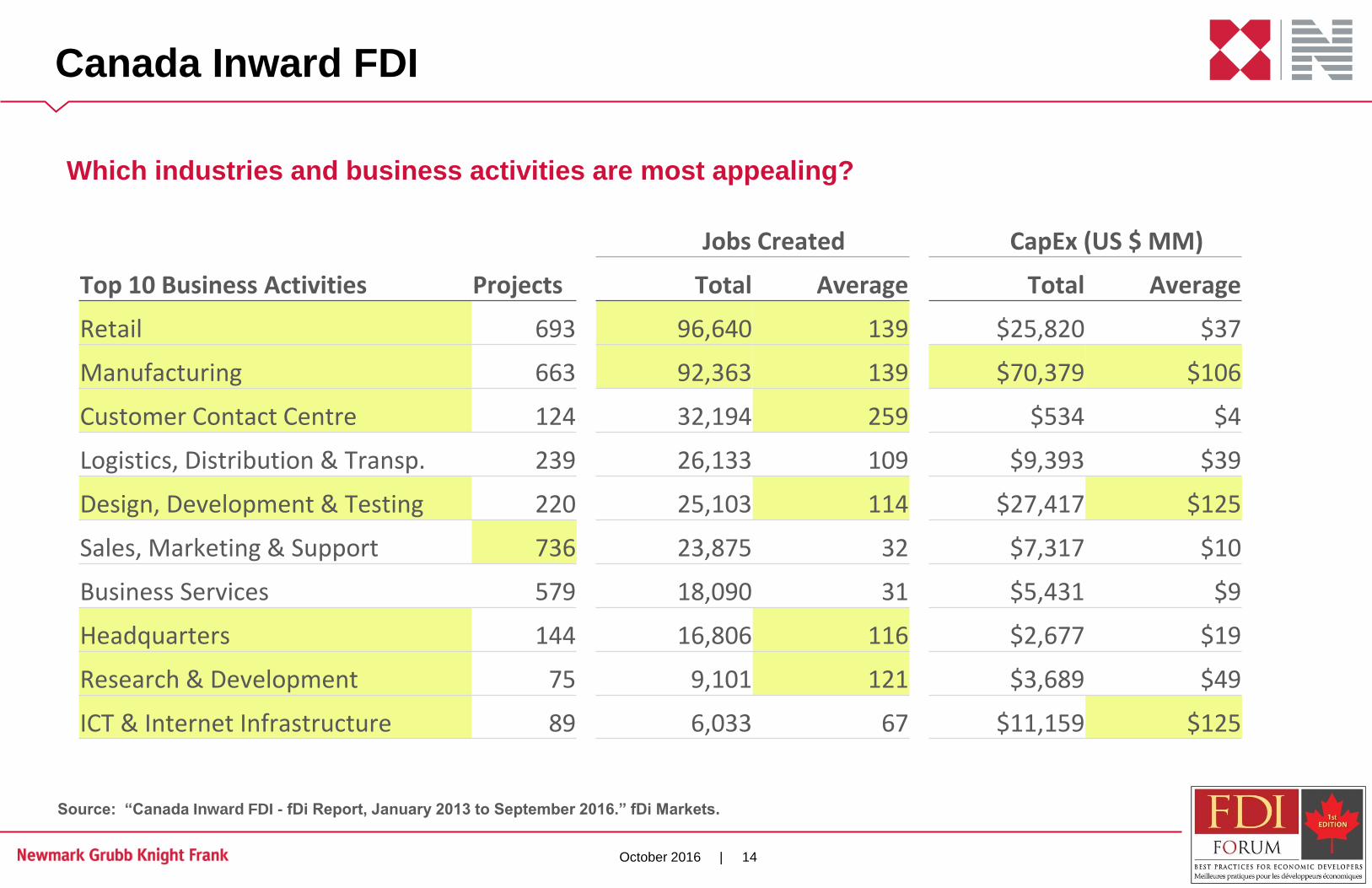

Canada Inward FDI

Source: “Canada Inward FDI - fDi Report, January 2013 to September 2016.” fDi Markets.

Which industries and business activities are most appealing?

Jobs Created CapEx (US $ MM)

Top 10 Business Activities Projects Total Average Total Average

Retail 693 96,640 139 $25,820 $37

Manufacturing 663 92,363 139 $70,379 $106

Customer Contact Centre 124 32,194 259 $534 $4

Logistics, Distribution & Transp. 239 26,133 109 $9,393 $39

Design, Development & Testing 220 25,103 114 $27,417 $125

Sales, Marketing & Support 736 23,875 32 $7,317 $10

Business Services 579 18,090 31 $5,431 $9

Headquarters 144 16,806 116 $2,677 $19

Research & Development 75 9,101 121 $3,689 $49

ICT & Internet Infrastructure 89 6,033 67 $11,159 $125

October 2016 | 15

Why Canada?

World Economies by PPP (2000-2014),

growth proportional by area:

China $18.10 trillion | Canada $1.6 trillion.

What’s compelling about the world’s 11th largest economy?

October 2016 | 16

Why Canada?

Business Environment of the G-7 Countries,

Rank for Forecast Period 2015-2019

7th

6th

5th

4th

3rd

2nd

1st

Canada U.S. Germany U.K. France Japan Italy

Rank

Source: The Economist Intelligence Unit, August 2015

October 2016 | 17

Why Canada?

Foreign Direct Investment Confidence

Source: AT Kearney 2015.

October 2016 | 18

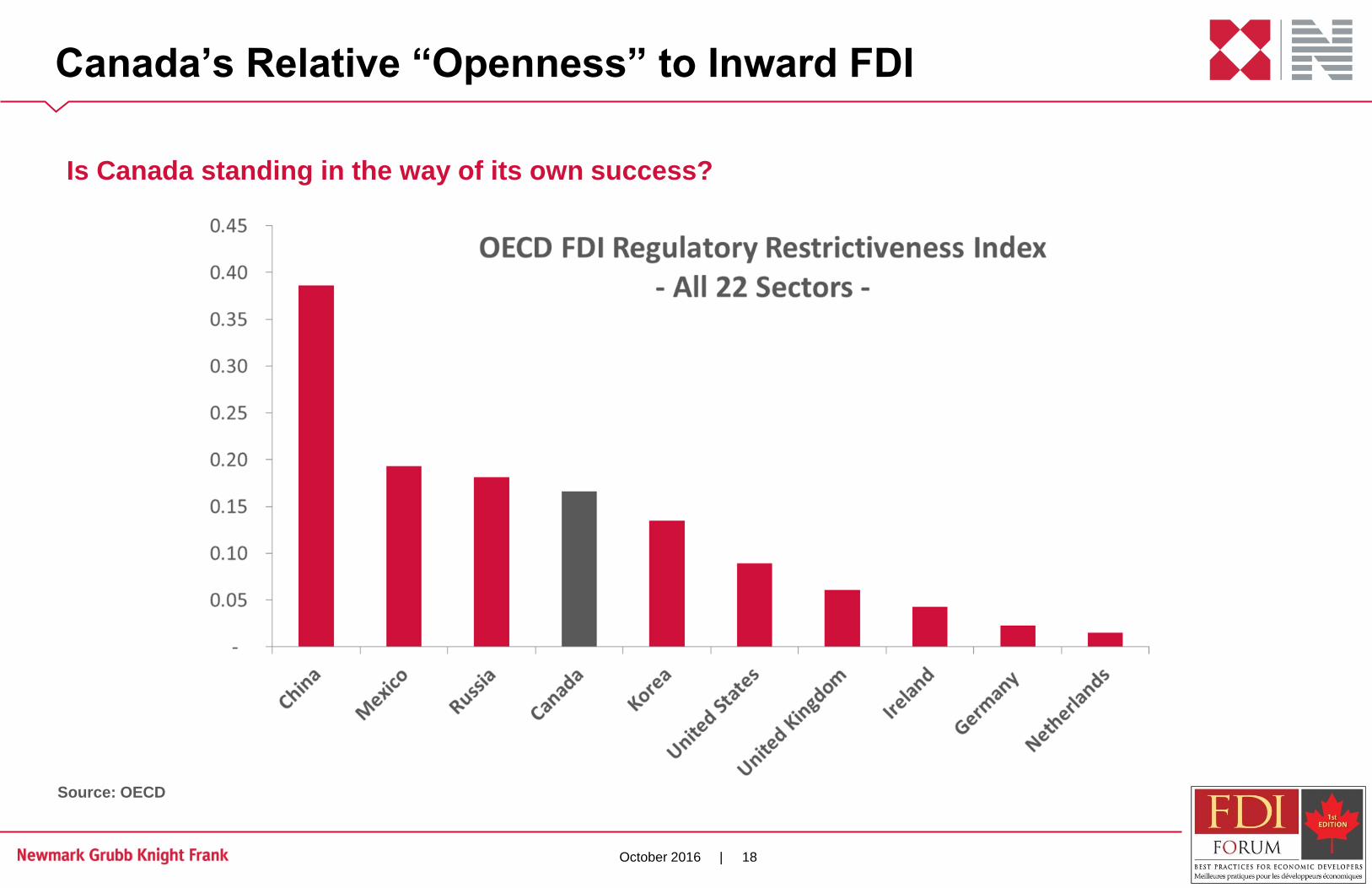

Source: OECD

Canada’s Relative “Openness” to Inward FDI

Is Canada standing in the way of its own success?

October 2016 | 19

Canada Inward FDI

Notes: Refers to “greenfield” investment only (not deb/ or equity flows and not M&A activity).

Source: “Canada Inward FDI - fDi Report, January 2013 to September 2016.” fDi Markets.

Which factors are within your sphere of influence?

October 2016 | 20

Canada Inward FDI

Source: Area Development “Corporate Executive Survey 2014”

“CEO Survey” . . . Primary reasons for moving / relocating facilities (North America):

Source: Area Development “Corporate Executive Survey 2014”

Proximity to Suppliers 74%

Labor Availability 61%

High Taxes 52%

Labor Costs 48%

Excessive Government Regulations 44%

Poor Infrastructure 9%

Quality of Life Concerns 9%

Healthcare Costs 4%

October 2016 | 21

Project Site

Existing New

Ownership

Local

Foreign

Source: Wassmansdorf 2016

Local Economic Development Context for FDI

Home-Grown Expansion

(“BRE”)

“FDI”

Inbound

Greenfield

“FDI”

Expansion

Mandate

What’s your

strategy for

each?

How will you

prioritize?

October 2016 | 22

Why Canada?

Globe & Mail.

February 5, 2013.

October 2016 | 23

The Competition Never Stops

October 27, 2016 | Mike Pare | Times Free Press

Germany is second in direct foreign investment in Tennessee behind

Japan, and the state's top economic developers will seek even more

business in a new mission next week to Europe's biggest economy.

Gov. Bill Haslam will lead the effort, starting Monday with four days

of meetings with German executives who already operate in

Tennessee and pitching the state's advantages to other companies

interested in setting up shop in the Southeast.

Some 103 German-owned companies have invested nearly $5.3

billion in Tennessee and employ almost 14,000 people, according to

the state.

Tennessee ranked No. 1 nationally for job creation resulting from

all foreign direct investment in 2015, according to IBM-PLI's 2016

Global Location Trends report. Tennesseans," Haslam said in a

statement.

Tennessee seeking more business from Germany

October 2016 | 24

The Competition Never Stops

Source: DLA Piper and KPMG.

October 2016 | 25

Growth & New Market Access

“Triggers” for Corporate Location Change

What is the

Canadian value

proposition to

satisfy the “drivers”

of each corporate

change event?

What is your

provincial or metro

solution?

+

$$ $

l l

l

l

l

l

l

l l

l Inefficiency

Rising Costs

Changing Business Climate

Industry Attraction / Clustering

October 2016 | 26

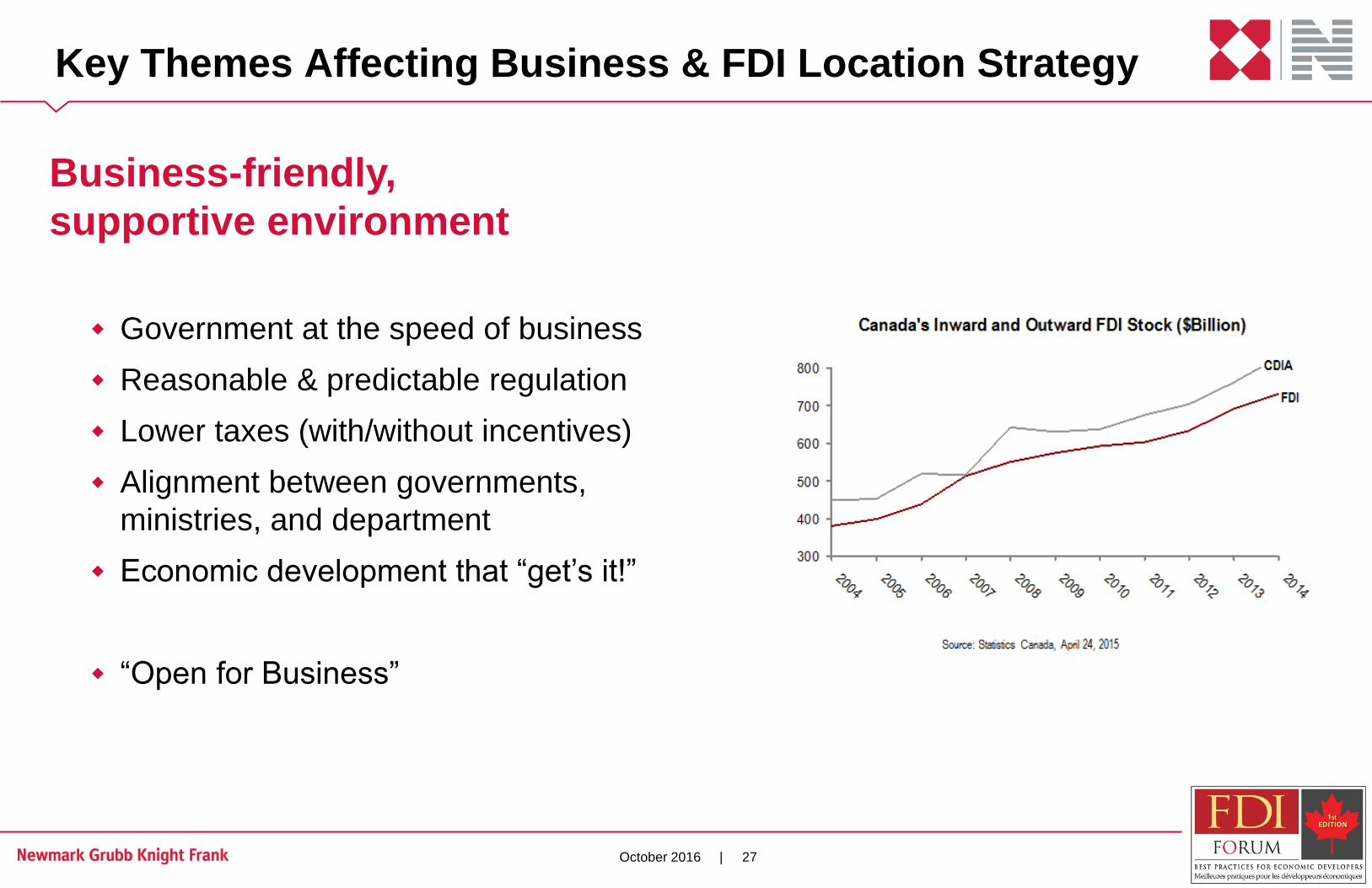

Key Themes Affecting Business & FDI Location Strategy

Overall business

competitiveness &

quality of life

October 2016 | 27

Key Themes Affecting Business & FDI Location Strategy

Business-friendly,

supportive environment

Government at the speed of business

Reasonable & predictable regulation

Lower taxes (with/without incentives)

Alignment between governments,

ministries, and department

Economic development that “get’s it!”

“Open for Business”

October 2016 | 28

Key Themes Affecting Business & FDI Location Strategy

Affordable costs of doing business

and cost of living.

o

o

o

October 2016 | 29

Key Themes Affecting Business & FDI Location Strategy

Sizeable, well-skilled

workforce

Cost

Quality

Reliability

Productivity

Trained / Trainable

“Sustainability” /

Education “Pipeline”

October 2016 | 30

Key Themes Affecting Business & FDI Location Strategy

Education & training

Variety of high quality training

& academic institutions providing

a wide array of needed skills

and talent.

o Trades

o Diplomas

o Degrees

o International (Re)certifications

o “Centers of Excellence”

Percentage of Individuals Aged 25-64 Having Attained Post-

Secondary Education - Top 10 OECD Countries

53.0

47.0 47.044.0 43.0 42.0 41.0 41.0 41.0 40.0 40.0

0

10

20

30

40

50

60

CanadaIsr

ael

Japan

USA

S. Korea UK

Ireland

Luxembourg

Finland

Norway

Australia

%

Source: OECD, Education at a Glance, Interim Report, January 2015

October 2016 | 31

Key Themes Affecting Business & FDI Location Strategy

Economic “clusters” of

business activity & innovation

October 2016 | 32

Key Themes Affecting Business & FDI Location Strategy

Energy abundance

& competitiveness

Supply

Cost

Reliability

Generation Mix

Partnership

October 2016 | 33

Key Themes Affecting Business & FDI Location Strategy

Transportation & supply chain

infrastructure

Excellent transportation and supply chain

infrastructure & connectivity.

o Air – Passenger

o Air – Freight

o Seaport

o Rail

o Highway

o Multi-Modal

Supply chains are more dispersed and more complex.

Source: Parag Khanna. Connectography (2016).

United Arab Emirates (2012):

Khalifa Port Receives Post Panamax STS Container Cranes

October 2016 | 34

Key Themes Affecting Business & FDI Location Strategy

Market access & growth

Domestic consumer & B2B

market growth

Export expansion

Reduced costs through the

global value chain

October 2016 | 35

Key Themes Affecting Business & FDI Location Strategy

Wide variety of serviced, available

buildings and sites.

Robust commercial real estate sector

Public investment in infrastructure

Planning, Zoning, Building & Council aligned

Creative options:

o Public ownership

o “Certified Sites”

and “Shovel Ready” Programs

October 2016 | 36

Key Themes Affecting Business & FDI Location Strategy

Minimal natural and human risks.

38 countries rated “Very High Risk” by Aon

October 2016 | 37

Key Themes Affecting Business & FDI Location Strategy

Quality of place & Standard of living

October 2016 | 38

Weaknesses to Probe, Challenge & Improve

Economic incentives

Government at the speed of business

Labour market regulations and skills gaps

Local taxes on real property and development charges

Energy costs are rising and vary greatly

Openness to foreign direct investment

Innovation & productivity

We must “Sell” and “Facilitate” better

October 2016 | 39

Key Themes Affecting Business & FDI Location Strategy

Economic development excellence

Canadian economic development is getting better . . . and must keep going!

Professional staff

Business, technical, and sales knowledge

Political leadership that supports investment

“One window” approach

“Public – Utility – Private – Academic” collaboration

Ongoing “BRE” support for local and global growth

October 2016 | 40

Our Aspirational Message to the World