cadila healthcare: recommends dividend @ 240% for fy15; maintain buy

TRANSCRIPT

4

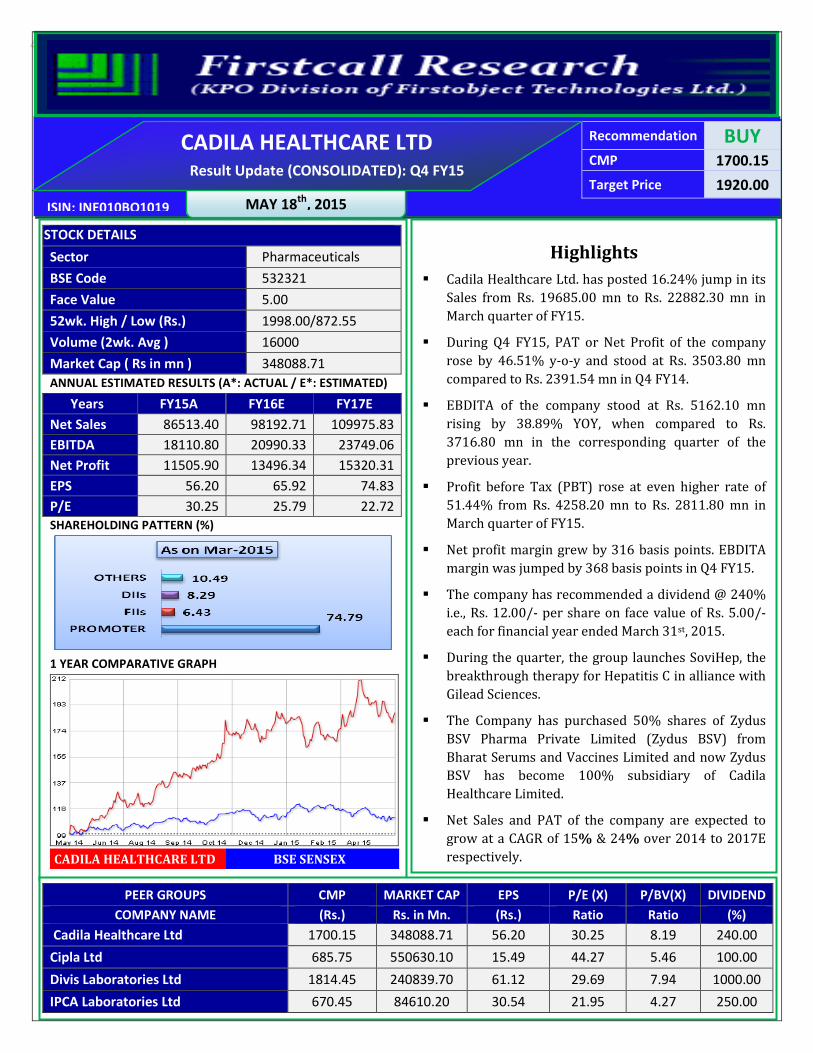

Recommendation BUY CMP 1700.15

Target Price 1920.00

ISIN: INE010BO1019 MAY 18th

, 2015

CADILA HEALTHCARE LTD

Result Update (CONSOLIDATED): Q4 FY15

STOCK DETAILS

Sector Pharmaceuticals

BSE Code 532321

Face Value 5.00

52wk. High / Low (Rs.) 1998.00/872.55

Volume (2wk. Avg ) 16000

Market Cap ( Rs in mn ) 348088.71

ANNUAL ESTIMATED RESULTS (A*: ACTUAL / E*: ESTIMATED)

Years FY15A FY16E FY17E

Net Sales 86513.40 98192.71 109975.83

EBITDA 18110.80 20990.33 23749.06

Net Profit 11505.90 13496.34 15320.31

EPS 56.20 65.92 74.83

P/E 30.25 25.79 22.72

SHAREHOLDING PATTERN (%)

1 YEAR COMPARATIVE GRAPH

CADILA HEALTHCARE LTD BSE SENSEX

Highlights

� Cadila Healthcare Ltd. has posted 16.24% jump in its

Sales from Rs. 19685.00 mn to Rs. 22882.30 mn in

March quarter of FY15.

� During Q4 FY15, PAT or Net Profit of the company

rose by 46.51% y-o-y and stood at Rs. 3503.80 mn

compared to Rs. 2391.54 mn in Q4 FY14.

� EBDITA of the company stood at Rs. 5162.10 mn

rising by 38.89% YOY, when compared to Rs.

3716.80 mn in the corresponding quarter of the

previous year.

� Profit before Tax (PBT) rose at even higher rate of

51.44% from Rs. 4258.20 mn to Rs. 2811.80 mn in

March quarter of FY15.

� Net profit margin grew by 316 basis points. EBDITA

margin was jumped by 368 basis points in Q4 FY15.

� The company has recommended a dividend @ 240%

i.e., Rs. 12.00/- per share on face value of Rs. 5.00/-

each for financial year ended March 31st, 2015.

� During the quarter, the group launches SoviHep, the

breakthrough therapy for Hepatitis C in alliance with

Gilead Sciences.

� The Company has purchased 50% shares of Zydus

BSV Pharma Private Limited (Zydus BSV) from

Bharat Serums and Vaccines Limited and now Zydus

BSV has become 100% subsidiary of Cadila

Healthcare Limited.

� Net Sales and PAT of the company are expected to

grow at a CAGR of 15% & 24% over 2014 to 2017E

respectively.

PEER GROUPS CMP MARKET CAP EPS P/E (X) P/BV(X) DIVIDEND

COMPANY NAME (Rs.) Rs. in Mn. (Rs.) Ratio Ratio (%)

Cadila Healthcare Ltd 1700.15 348088.71 56.20 30.25 8.19 240.00

Cipla Ltd 685.75 550630.10 15.49 44.27 5.46 100.00

Divis Laboratories Ltd 1814.45 240839.70 61.12 29.69 7.94 1000.00

IPCA Laboratories Ltd 670.45 84610.20 30.54 21.95 4.27 250.00

Analysis & Recommendation- BUY

For the 4th quarter ended March 31st, 2015, Zydus Cadila reported Net sales of Rs. 22882.30 mn, up by 16.24%

from Rs. 19685.00 mn in the corresponding quarter of the previous year on a consolidated basis. The net profit

is up by 46.51% to Rs. 353.80 mn from Rs. 2391.54 mn in the 4th quarter of FY 2014-15. Profit before Tax

(PBT) rose at even higher rate of 51.44% from Rs. 4258.20 mn to Rs. 2811.80 mn in March quarter of FY15. Net

profit margin grew by 316 basis points. EBDITA margin was jumped by 368 basis points in Q4 FY15.

Strengthening its regulatory pipeline, the group filed 38 ANDAs during the year 2014-15 with the US FDA,

taking the cumulative filings to 260. The group received 8 ANDA approvals during the year taking the total to

99 product approvals. The group’s R&D pipeline which comprises 25 biologics (incl. novel biologics), is being

developed to treat auto immune disorders like arthritis, cancer, infertility and stroke. The group also made

brisk progress in its biologics research programme advancing its pipeline of mABs. The group also initiated

global clinical trials for one of the first generation biosimilars, which is currently being marketed in India.

Company has consolidated the Branded Generic business in the key markets of Asia Pacific, Africa and Middle

East. Thus we recommend BUY for the scrip with target price of Rs. 1920.00 for medium and long term.

Quarterly Highlights

Q4 FY15

During the quarter, Net sales of the company rose by 16.24% and stands at Rs. 22882.30 mn from Rs. 19685.00

mn in corresponding quarter of previous year. In Q4 FY15, Net profit was increased by 46.51% to Rs. 3503.80 mn

from Rs. 2391.54 mn in Q4 FY14. EBDITA increased by 38.89% from Rs. 5162.10 mn to Rs. 3716.80 mn in Q4

FY15. Net profit margin grew by 316 basis points. EBDITA margin was jumped by 368 basis points. Profit before

Tax also rose by 51.44% at Rs. 4258.20 mn in Q4 FY15.

Months Mar-15 Mar-14 % Change

Net sales 22882.30 19685.00 16.24

Net Profit 3503.80 2391.54 46.51

Net Profit Margin (%) 15.31% 12.15% 316 BP

EBITDA 5162.10 3716.80 38.89

EBITDA Margin (%) 22.56% 18.88% 368 BP

Profit Before Tax 4258.20 2811.80 51.44

Interest -162.80 -240.40 -32.28

PBT 4258.20 2811.80 51.44

Break up of Expenditure

Latest Updates

• The Company has purchased 50% shares of Zydus BSV Pharma Private Limited (Zydus BSV) from Bharat

Serums and Vaccines Limited and now Zydus BSV has become 100% subsidiary of Cadila Healthcare

Limited.

• During the quarter, the group launches SoviHep, the breakthrough therapy for Hepatitis C in alliance with

Gilead Sciences.

• The company has recommended a dividend @ 240% i.e., Rs. 12.00/- per share on face value of Rs. 5.00/-

each for financial year ended March 31st, 2015.

• During the year 2014-15, group filed 38 ANDAs with the US FDA, taking the cumulative filings to 260. The

group received 8 ANDA approvals during the year taking the total to 99 product approvals.

The Standalone results for the Quarter ended March 31st, 2015

The Company has posted a net profit of Rs. 3470.60 million for the quarter ended March 31, 2015 as compared to

Rs. 2166.80 million for the quarter ended March 31, 2014. Total Income has increased from Rs. 11218.90 million

for the quarter ended March 31, 2014 to Rs. 14688.50 million for the quarter ended March 31, 2015.

Rs. In Mn Q4 FY15 Q4 FY14 CHNG %

Material Consumed 4505.40 4195.60 7.38%

Stock in Trade 3114.70 3362.00 -7.36%

Employee Benefit Exp. 3140.80 2735.70 14.81%

Dep. & Amortz. Exp. 755.40 527.80 43.12%

Other Exp. 6761.50 5587.50 21.01%

COMPANY PROFILE

Zydus Cadila, a global healthcare provider was founded by Late Mr. Ramanbhai B. Patel in 1952. In 1995, the

group restructured its operations and emerged with a new identity under the aegis of Zydus group as Cadila

Healthcare Ltd. Cadila Healthcare is the flagship company of Zydus Cadila group. The group, headquartered in

Ahmedabad develops, manufactures and markets broad range of healthcare products ranging from API to

formulations, animal health products and cosmeceuticals. The Zydus Cadila group has global operations in four

continents spread across USA, Europe, Japan, Brazil, South Africa and 25 other emerging markets.

Zydus Cadila is a leading player in the cardiovascular, gastrointestinal and women's healthcare segments. The

group has strong presence in respiratory, pain management, CNS, anti-infectives, oncology, neurosciences,

dermatology and nephrology segments. It has been able to maintain overall position and market share through

faster growing lifestyle segments. The group has several in-licensing alliances with global multinationals such

as Schering AG, Boehringer Ingelheim, Viatris, etc. The portfolio of products of the group is over 200 which are

marketed by a specialized field force of about 3,000. With one of the strongest distribution channels in the

industry, the group reaches out to 100000 chemists and serves 200000 doctors including physicians,

specialists and super specialists.

Zydus Wellness Ltd., spearheads the group's presence in the consumer and wellness segment. The products of

the company comprises of Sugar Free Gold– India’s No.1 sweetener with a market share of over 70%, Sugar Free

Natura– a zero calorie sucralose based sugar substitute, Sugar Free D’lite– a low calorie healthy drink and

Nutralite– a premium cholesterol-free table spread. Nutralite has emerged as the second largest brand in the

category of butter and butter substitutes. In addition to that the company also caters to the skincare segment

with its Everyuth and Dermacare brands, which occupy a unique distinction of being a ‘skincare brand from a

healthcare company’. Enriched with the power of natural ingredients, EverYuth has a strong presence in

advanced skincare segments like soap-free, face washes, face masks, scrubs etc.

FINANCIAL STATEMENTS & ESTIMATIONS (CONSOLIDATED) (A*- Actual, E* -Estimations & Rs. In Millions)

Balance Sheet as on March 31st, 2014 to 2017E

Cadila Healthcare Ltd FY14A FY15A FY16E FY17E

EQUITY AND LIABILITIES:

Shareholders’ Funds:

• Share Capital 1023.70 1023.70 1023.70 1023.70

• Reserves and Surplus 33366.20 41491.70 50785.84 60689.08

Net worth (a) 34389.90 42515.40 51809.54 61712.78

Minority Interest (b) 1442.70 1688.90 1992.90 2202.16

Non-Current Liabilities:

• Long-term borrowings 13622.30 11504.20 9893.61 8666.80

• Deferred Tax Liabilities [Net] 960.80 585.60 480.19 398.56

• Other Long Term Liabilities 547.80 421.40 358.19 315.21

• Long Term Provisions 760.60 1106.30 1305.43 1475.14

Total Non- Current liabilities (c) 15891.50 13617.50 12037.43 10855.71

Current Liabilities:

• Short-term borrowings 9023.80 11835.50 13729.18 15184.47

• Trade Payables 9108.00 10908.70 12435.92 13679.51

• Other Current Liabilities 7080.60 6282.30 5654.07 5145.20

• Short Term Provisions 2926.90 3623.10 4094.10 4503.51

Current Liabilities (d) 28139.30 32649.60 35913.27 38512.70

Total Liabilities (a+b+c+d) 79863.40 90471.40 101753.14 113283.35

ASSETS:

Non-Current Assets:

• Fixed Assets 32803.20 34170.20 35331.99 36179.95

• Goodwill on consolidation (net) 7350.00 7330.90 7550.83 7898.17

• Non Current Investments 221.90 331.60 391.29 449.98

• Long Term Loans and Advances 5110.50 6371.40 7518.25 8420.44

Total Non Current Assets (e) 45485.60 48204.10 50792.35 52948.54

Current Assets:

• Current Investments 643.70 1212.40 1757.98 2285.37

• Inventories 13674.90 15356.80 17046.05 18750.65

• Trade Receivables 11336.50 15883.90 20871.10 26399.15

• Cash and Bank Balances 5488.20 6698.90 8038.68 9517.80

• Short Term Loans and Advances 2548.80 2408.20 2504.53 2587.40

• Other Current Assets 685.70 707.10 742.46 794.43

Total Current Assets (f) 34377.80 42267.30 50960.79 60334.80

Total Assets (e+f) 79863.40 90471.40 101753.14 113283.35

Annual Profit & Loss Statement for the period of 2014to 2017E

Value(Rs.in.mn) FY14A FY15A FY16E FY17E

Description 12m 12m 12m 12m

Net Sales 72240.30 86513.40 98192.71 109975.83

Other Income 506.70 553.70 664.44 764.11

Total Income 72747.00 87067.10 98857.15 110739.94

Expenditure -60238.90 -68956.30 -77866.82 -86990.88

Operating Profit 12508.10 18110.80 20990.33 23749.06

Interest -901.90 -678.60 -696.24 -753.34

Gross profit 11606.20 17432.20 20294.09 22995.72

Depreciation -2012.30 -2872.50 -3289.01 -3604.76

Exceptional Items -171.50 -104.40 -42.88 -101.27

Profit Before Tax 9422.40 14455.30 16962.20 19289.69

Tax -1060.10 -2594.20 -3087.12 -3568.59

Profit After Tax 8362.30 11861.10 13875.08 15721.10

Extraordinary Items 0.00 21.40 16.69 18.36

Minority Interest -326.40 -376.60 -395.43 -419.16

Net Profit 8035.90 11505.90 13496.34 15320.31

Equity capital 1023.70 1023.70 1023.70 1023.70

Reserves 33366.20 41491.70 50785.84 60689.08

Face value 5.00 5.00 5.00 5.00

EPS 39.25 56.20 65.92 74.83

Quarterly Profit & Loss Statement for the period of 30th Sept, 2014 to 30th June, 2015E

Value(Rs.in.mn) 30-Sep-14 31-Dec-14 31-Mar-15 30-Jun-15E

Description 3m 3m 3m 3m

Net sales 21080.00 21894.60 22882.30 23898.27

Other income 146.10 100.10 203.40 178.99

Total Income 21226.10 21994.70 23085.70 24077.27

Expenditure -16870.10 -17422.50 -17923.60 -18784.04

Operating profit 4356.00 4572.20 5162.10 5293.22

Interest -172.60 -162.40 -162.80 -123.73

Gross profit 4183.40 4409.80 4999.30 5169.49

Depreciation -732.90 -707.20 -755.40 -879.29

Exceptional Items 2.30 46.10 14.30 17.30

Profit Before Tax 3452.80 3748.70 4258.20 4307.51

Tax -571.30 -791.00 -707.50 -775.35

Profit After Tax 2881.50 2957.70 3550.70 3532.16

Extraordinary Items -0.38 -0.39 21.40 15.41

Minority Interest -100.60 -138.60 -68.30 -60.10

Net Profit 2780.52 2818.71 3503.80 3487.46

Equity capital 1023.70 1023.70 1023.70 1023.70

Face value 5.00 5.00 5.00 5.00

EPS 13.58 13.77 17.11 17.03

Ratio Analysis

Particulars FY14A FY15A FY16E FY17E

EPS (Rs.) 39.25 56.20 65.92 74.83

EBITDA Margin (%) 17.31% 20.93% 21.38% 21.59%

PBT Margin (%) 13.04% 16.71% 17.27% 17.54%

PAT Margin (%) 11.58% 13.71% 14.13% 14.30%

P/E Ratio (x) 43.32 30.25 25.79 22.72

ROE (%) 24.32% 27.90% 26.78% 25.47%

ROCE (%) 25.46% 31.86% 32.19% 31.97%

Debt Equity Ratio 0.66 0.55 0.46 0.39

EV/EBITDA (x) 29.15 20.07 17.24 15.16

Book Value (Rs.) 167.97 207.66 253.05 301.42

P/BV 10.12 8.19 6.72 5.64

Charts

OUTLOOK AND CONCLUSION

� At the current market price of Rs.1700.15 the stock P/E ratio is at 25.79 x FY16E and 22.72 x FY17E

respectively.

� Earning per share (EPS) of the company for the earnings for FY16E and FY17E is seen at Rs. 65.92 and Rs

74.83 respectively.

� Net Sales and PAT of the company are expected to grow at a CAGR of 15% and 24% over 2014 to 2017E

respectively.

� On the basis of EV/EBITDA, the stock trades at 17.24 x for FY16E and 15.16 x for FY17E.

� Price to Book Value of the stock is expected to be 6.72 x and 5.64 x respectively for FY16E and FY17E.

� We recommend ‘BUY’ in this particular scrip with a target price of Rs.1920.00 for Medium to Long term

investment.

INDUSTRY OVERVIEW

The Indian pharmaceuticals market is third largest in terms of volume and thirteen largest in terms of value, as

per a pharmaceuticals sector analysis report by equity master. The market is dominated majorly by branded

generics which constitute nearly 70 to 80 per cent of the market. Considered to be a highly fragmented industry,

consolidation has increasingly become an important feature of the Indian pharmaceutical market.

India has achieved an eminent global position in pharma sector. The country also has a huge pool of scientists

and engineers who have the potential to take the industry to a very high level.

The UN-backed Medicines Patents Pool has signed six sub-licences with Aurobindo, Cipla, Desano, Emcure,

Hetero Labs and Laurus Labs, allowing them to make generic anti-AIDS medicine Tenofovir Alafenamide (TAF)

for 112 developing countries.

Market Size

The Indian pharmaceutical industry is estimated to grow at 20 per cent compound annual growth rate (CAGR)

over the next five years, as per India Ratings, a Fitch Group company. Indian pharmaceutical manufacturing

facilities registered with US Food and Drug Administration (FDA) as on March 2014 was the highest at 523 for

any country outside the US.

Gujarat clocked the highest growth rate in pharmaceuticals market at 22.4 per cent during November 2014,

surpassing the industry growth rate, which grew by 10.9 per cent, as per data from the market research firm

AIOCD Pharma softtech AWACS.

Also, growing at an average rate of about 20 per cent, India's biotechnology industry comprising bio-

pharmaceuticals, bio-services, bio-agriculture, bio-industry and bioinformatics may reach the US$ 7 billion mark

by the end of FY15.

Investments

The Union Cabinet has given its approval to amend the existing FDI policy in the pharmaceutical sector in order

to cover medical devices. The Cabinet has allowed FDI up to 100 per cent under the automatic route for

manufacturing of medical devices subject to specified conditions.

The drugs and pharmaceuticals sector attracted cumulative foreign direct investment (FDI) inflows worth US$

12,813.02 million between April 2000 and December 2014, according to data released by the Department of

Industrial Policy and Promotion (DIPP).

Some of the major investments in the Indian pharmaceutical sector are as follows:

• Stelis Biopharma has announced the ground-breaking for construction of its customised, multi-product,

biopharmaceutical manufacturing facility at Bio-Xcell Biotechnology Park in Nusajaya, Johor, Malaysia's park

and ecosystem for industrial and healthcare biotechnology at a total project investment amount of US$ 60

million.

• Pharma major Strides Arcolab has entered into a licensing agreement with US-based Gilead Sciences Inc to

manufacture and distribute the latter's low-cost Tenofovir Alafenamide (TAF) product used for HIV

treatment in developing countries. The licence to manufacture Gilead's low-cost drug extends to 112

countries.

• Apollo Hospitals Enterprise (AHEL) plans to add another 2,000 beds over the next two financial years, at a

cost of around Rs 15000.00 mn (US$ 242.57 million), as per Founder and Executive Chairman, Apollo

Hospitals.

• CDC, the UK’s development finance institution, has invested US$ 48 million in Narayana Hrudayalaya

hospitals, a multi-speciality healthcare provider. With this investment, Narayana Health will expand

affordable treatment in eastern, central and western India.

• Cadila Healthcare Ltd has announced the launch of a biosimilar for Adalimumab - the world’s largest selling

drug for rheumatoid arthritis and other auto immune disorders. The drug will be marketed under the brand

name Exemptia at one-fifth of the price for the branded version-Humira.

• Torrent Pharmaceuticals has entered into an exclusive licensing agreement with Reliance Life Sciences for

marketing three biosimilars in India — Rituximab, Adalimumab and Cetuximab.

• Piramal Enterprises Ltd has acquired US-based Coldstream Laboratories for US$ 30.6 million in an all-cash

transaction.

• Indian Immunologicals Ltd (IIL) plans to set up a new vaccine manufacturing facility in Pondicherry with an

investment of Rs 3000.00 mn (US$ 48.53 million).

• SRF Ltd has acquired Global DuPont Dymel, the pharmaceutical propellant business of DuPont, for US$ 20

million.

Government Initiatives

The Government of India has unveiled 'Pharma Vision 2020' aimed at making India a global leader in end-to-end

drug manufacture. It has reduced approval time for new facilities to boost investments. Further, the government

has also put in place mechanisms such as the Drug Price Control Order and the National Pharmaceutical Pricing

Authority to address the issue of affordability and availability of medicines.

Romania is keen to tie up with the Indian pharmaceutical companies for research and develop new drugs.

"Romania will collaborate with India for license acquisition to sale India's drugs in Europe," reported by,

Counselor in Ministry of health in Romania at GCCI. The country will tie up with the Indian pharmaceutical

companies for research and develop new drugs.

Some of the major initiatives taken by the government to promote the pharmaceutical sector in India are as

follows:

� Indian and global companies have expressed 175 investment intentions worth Rs 10000.00 mn (US$ 161.78

million) in the pharmaceutical sector of Gujarat. The memorandums of understanding (MoUs) would be

signed during the Vibrant Gujarat Summit.

� Telangana has proposed to set up India's largest integrated pharmaceutical city spread over 11,000 acres

near Hyderabad, complete with effluent treatment plants and a township for employees, in a bid to attract

investment of Rs 300000.00 mn (US$ 4.85 billion) in phases. Hyderabad, which is known as the bulk drug

capital of India, accounts for nearly a fifth of India's exports of drugs, which stood at Rs 900000.00 mn (US$

14.56 billion) in 2013-14.

Road Ahead

The Indian pharma market size is expected to grow to US$ 85 billion by 2020. The growth in Indian domestic

market will be on back of increasing consumer spending, rapid urbanisation, raising healthcare insurance and so

on.

Going forward, better growth in domestic sales will depend on the ability of companies to align their product

portfolio towards chronic therapies for diseases such as such as cardiovascular, anti-diabetes, anti-depressants

and anti-cancers are on the rise.

Moreover, the government has been taking several cost effective measures in order to bring down healthcare

expenses. Thus, governments are focusing on speedy introduction of generic drugs into the market. This too will

benefit Indian pharma companies. In addition, the thrust on rural health programmes, life saving drugs and

preventive vaccines also augurs well for the pharma companies.

Disclaimer:

This document is prepared by our research analysts and it does not constitute an offer or solicitation for the purchase

or sale of any financial instrument or as an official confirmation of any transaction. The information contained herein is

from publicly available data or other sources believed to be reliable but we do not represent that it is accurate or

complete and it should not be relied on as such. Firstcall Research or any of its affiliates shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information

contained in this report. Firstcall Research and/ or its affiliates and/or employees will not be liable for the recipients’

investment decision based on this document.

Firstcall India Equity Research: Email – [email protected]

C.V.S.L.Kameswari Pharma & Diversified

U. Janaki Rao Capital Goods

B. Anil Kumar Auto, IT & FMCG

M. Vinayak Rao Diversified

G. Amarender Diversified

Firstcall Research Provides

Industry Research on all the Sectors and Equity Research on Major Companies

forming part of Listed and Unlisted Segments

For Further Details Contact:

Tel.: 022-2527 2510/2527 6077 / 25276089 Telefax: 022-25276089

040-20000235 /20000233

E-mail: [email protected]

www.firstcallresearch.com