by the public sector, for the public sector finance seminar spring 2015 presented by cathryn walker

TRANSCRIPT

By the public sector, for the public sector

Finance SeminarSpring 2015

Presented by

Cathryn Walker

By the public sector, for the public sector

• FIRST SESSION

Agenda

Schools Finance Team2015-16 BudgetPupil PremiumHigh Needs Funding 2015-16EYSFF 2015-16

• SECOND SESSION

School Balances 2014-15 (SB1)Universal Infant FSMCFR 2014-15Audit – Purchasing & Payments Pupil PremiumYear End 2014-15Housekeeping

By the public sector, for the public sector

LGSS Schools Finance Staffing

By the public sector, for the public sector

Helpdesk UpdateDue to current absence /sickness we have identified a short term solution to ensure we can cover the helpdesk over the published times. If you contact the normal FMS6 helpdesk and experience no answer please do try again but if you are still unsuccessful there are alternative mobile numbers that you can contact instead. These numbers are 07708 276240 or 07523 502583. Please note these arrangements only apply over the published helpdesk times of Monday to Friday 9.00 to 4.00pm (closed 12.30 to 1.00pm for lunch)

By the public sector, for the public sector

Schools Budgets 2015-16

• Minimum Funding Guarantee of minus 1.5% or cap of 8.1% (was 4.5% 2014-15 ) on Schools Block funding.

• Basis for funding:– October 2014 Pupil Census for per pupil

allocations – January 2015 Pupil Census for Pupil Premium

grant

By the public sector, for the public sector

2015/16 Settlement ValuesDSG

£520.8m(£496.7m in 2014-15)

SCHOOLS BLOCK

£425.7m(£394.8m in 2014-15)

£30.9m

EARLY YEARS BLOCK

£28.5m(£27.0m in 2014-15)

£1.5m

HIGH NEEDS BLOCK

£66.4m(£65.7m in 2014-15)

£0.7m

OTHER

£0.2m(£9.2m in 2014-15)

£9.0m

By the public sector, for the public sector

Headlines (excl non recouping)• Changes in school pupil numbers in the Schools Oct 2014 census

2014/15(October

2013 census)

2015/16(October

2014 census)

Change

Reception Uplift 104.5 104.0 (0.5)

Primary 59,546.5 61,165.5 1,619.0

Secondary 35,291.0 34,834.5 (456.5)

SEN Units and Resourced Provision (581.0) (420.0) 161.0

Total 94,361.0 95,684.0 1,323

By the public sector, for the public sector

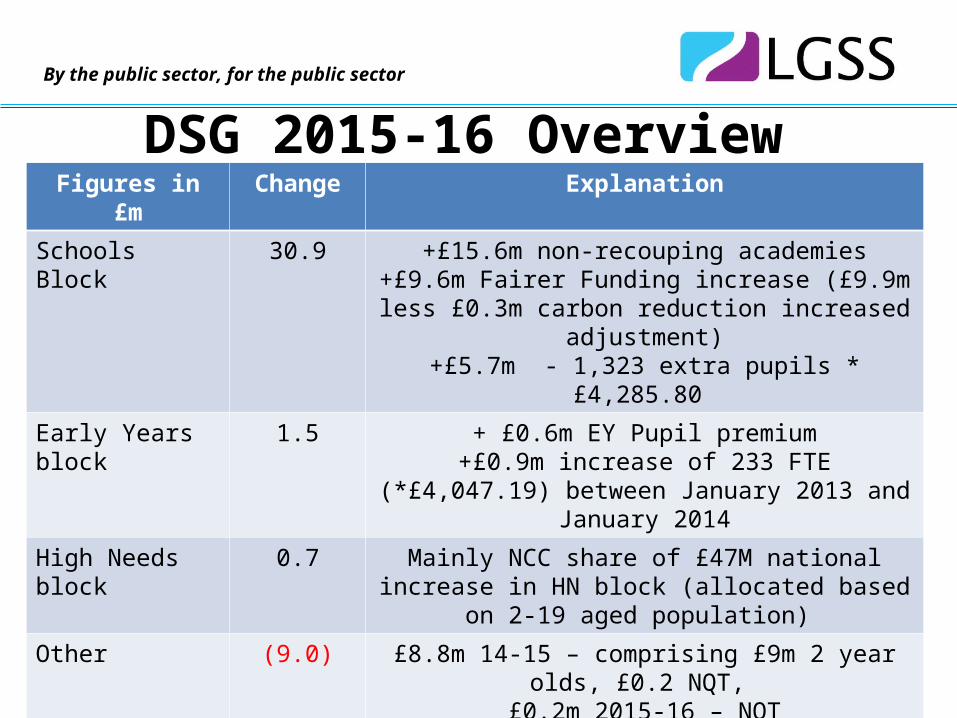

DSG 2015-16 OverviewFigures in £m Change Explanation

Schools Block 30.9 +£15.6m non-recouping academies+£9.6m Fairer Funding increase (£9.9m less £0.3m

carbon reduction increased adjustment)+£5.7m - 1,323 extra pupils * £4,285.80

Early Years block 1.5 + £0.6m EY Pupil premium +£0.9m increase of 233 FTE (*£4,047.19) between

January 2013 and January 2014

High Needs block 0.7 Mainly NCC share of £47M national increase in HN block (allocated based on 2-19 aged population)

Other (9.0) £8.8m 14-15 – comprising £9m 2 year olds, £0.2 NQT, £0.2m 2015-16 – NQT

TOTAL 24.1

Note – for ease of comparison £0.4 m Carbon reduction deduction in 2014-15 has been shown against schools block (for 14-15) as this is where the EFA have ‘included’ it in 2015-16

By the public sector, for the public sector

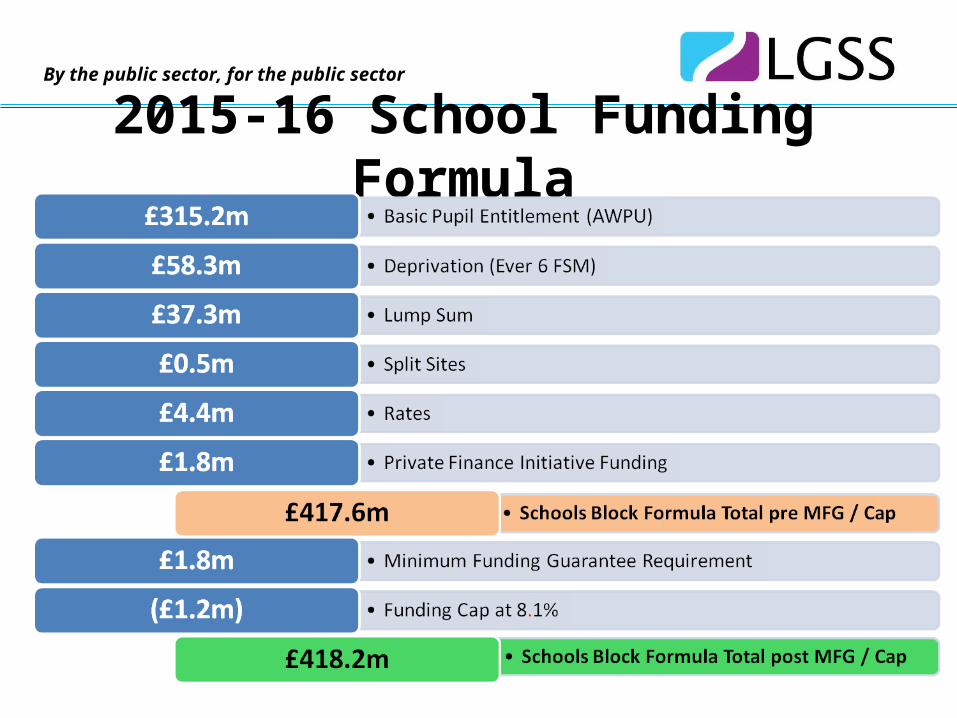

2015-16 School Funding Formula

By the public sector, for the public sector

Additional One Off Allocation• The one off impact on the funding formula for 2015-16

only is as follows.

By the public sector, for the public sector

Changes to Unit Rates2014/15

base value

(£)

2015/16 Base increase from Fairer Funding

(£)

2015/16 One off increase

(£)

Total 2015/16

(£)

Primary AWPU 2,588 73 23 2,684

Sec KS3 AWPU 3,781 68 30 3,879

Sec KS4 AWPU 4,280 68 30 4,378

Primary lump sum

125,000 0 15,000 140,000

Secondary lump sum

125,000 0 50,000 175,000

By the public sector, for the public sector

Budget Headlines 2016-17• 2016-17 will be the final year when one-off funding will be

released on a similar scale and primary and secondary schools should plan their budget accordingly.

• One off funding will also be paid to Nursery schools and special schools in 2015-16 and 2016-17. In 2015-16 this will be added to the nursery school lump sum in the EYSFF and the special schools one off addition will be included in the budget top ups in June 2015.

• The primary/secondary funding rate for Northamptonshire in 2015-16 is 1:1.34. This compares to an overall rate across all local authorities for 2014-15 of 1:1.27. This ratio, and if we should be moving closer to the national average rate, will need to be considered in planning for 2016-17.

By the public sector, for the public sector

National Copyright licences• A Single National License as in 2014/15 covering :

• Copyright Licensing Agency (CLA)• Schools Printed Music Licence (SPML)• Newspaper Licensing Authority (NLA)• Education Recording Agency (ERA)• Motion Picture Licensing Company (MPLC)• Filmbank Distributors Ltd (for the PVSL)– ADDITIONS for 2015/16• Mechanical Copyright Protection Society (MCPS)• Christian Copyright Licensing International (CCLI)• Performing Rights Society (PPL)• Phonographic performance Limited (PPL)

• 2015/16 Includes LA maintained nursery schools and non recoupment academies

By the public sector, for the public sector

School Budgets 2015-16

The following elements are shown on the website, treated as being part of schools final budgets and reflected in the cash advances to maintained schools:

1)High Needs Place funding – Special Schools & Units / Resourced Provisions

2)Primary and Secondary Schools formula budgets

3)The cash advances split is April 12% and 8% in the 11 subsequent months.

By the public sector, for the public sector

Indicative School Budgets 2015-16The following indicative elements will either be added to the website in March 2015 or confirmed/allocated during 2015-16. These are included in the monthly top ups: a.Mainstream 6th form allocations - from the EFAb.Devolved Formula Capital (DFC)c.Allocations from the High Needs Paneld.Pupil Premium – Main FSM shown in indicative budgets. Other elements paid as information received from the EFA or paid termly linked to LAC children.e.High needs top upsf.High needs element 3 top ups for pupils in SEN units or resourced provisiong.Special schools element 3 high needs allocationsh.UIFSMi.Pupil Growth funding

By the public sector, for the public sector

Pupil Premium

Pupil Premium Category

2013/14£

2014/15£

2015/16£

Change £

3 and 4 year old EYSFF pupils – per hour per eligible child

0 0 0.53 0.53

Primary 953 1,300 1320 20

Secondary 900 935 935 0

Looked After Children (Pupil Premium Plus)

900 1,900 1900 0

Service Child 300 300 300 0

By the public sector, for the public sector

Pupil premium changes 14-15 Contd

• Northamptonshire have piloted the new early years pupil premium from January 2015 – 53p per pupil per hour – addition to EYSFF for 3 to 4 year olds NOT 2 year olds.

By the public sector, for the public sector

High Needs Funding 2015/16

• High Needs EFA DSG 2015-16 funding announced in December

• Schools Forum January and March 2015 discussions on high needs pressures, funding and high needs funding rates

• Working to create a new RAS (Resource Allocation System) to use across all of high needs including Education, Health and Care (EHC) plans and reviewing existing statements

By the public sector, for the public sector

High Needs Funding 2015/16

Guidance on all areas included in high needs funding guidance on NCC website

Increasing financial pressures from increasing high needs numbers - mainly in special schools

Queries to: [email protected]

By the public sector, for the public sector

Special school budgets 2015/16• Numbers for place funding change from

September 2015. Numbers are based on actual October 2014 numbers. EFA principle of lagged funding.

• Numbers and therefore funding are continuing to increase.

• The increased cost for 2015-16 has been funded by increased High Needs DSG funding (£0.7m), top slice from schools fairer funding DSG allocation of £1.9m and moving budgets within the high needs block.

By the public sector, for the public sector

EYSFF 2015/16• 3-4 year olds EYSFF will include new EY pupil

premium

• EYSFF being reviewed for 15-16. In addition to pupil premium distributing additional £0.6 million from fairer funding allocation and central savings.

• Discussed at Forum Oct and Dec 14, Jan and March 2015.

• http://www.northamptonshire.gov.uk/en/councilservices/educationandlearning/services/schlfin/pages/schoolsforum.aspx

By the public sector, for the public sector

EYSFF 2015/16• EYSFF rates and elements decided and

published, including indicative budgets, late March 2015. Proposed changes include :

• Increase in base rate for both 2 and 3,4 year olds EYSFF. Main proposed changes to 3,4 yr EYSFF:

• Additional funding for maintained school providers

• New SEN factor

• Significant changes in quality funding factors

• Changes in deprivation formula element

By the public sector, for the public sector

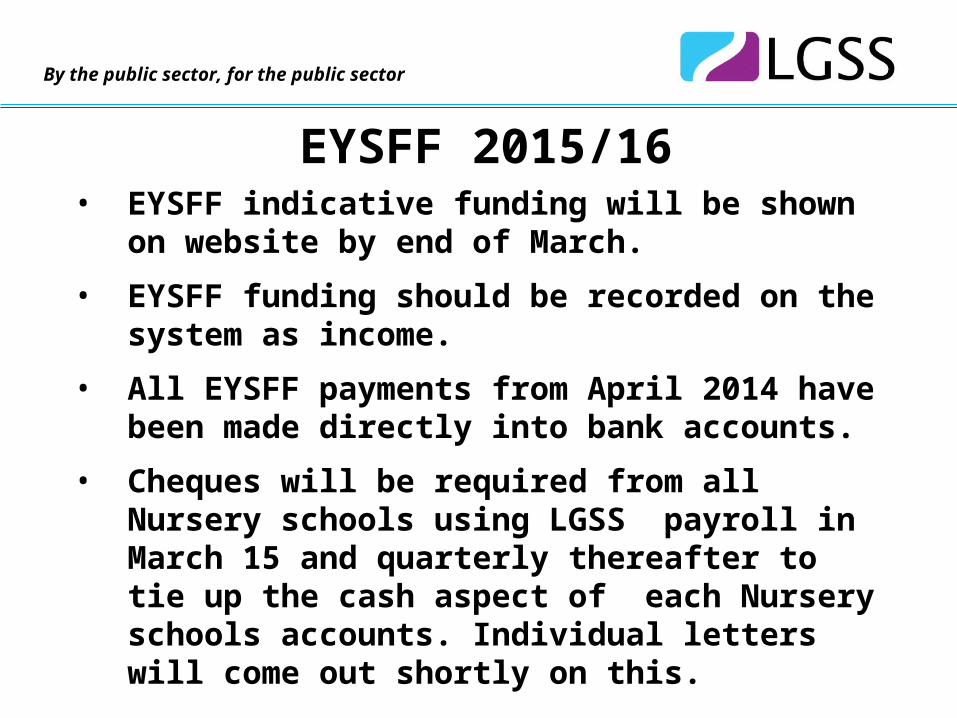

EYSFF 2015/16• EYSFF indicative funding will be shown on

website by end of March.

• EYSFF funding should be recorded on the system as income.

• All EYSFF payments from April 2014 have been made directly into bank accounts.

• Cheques will be required from all Nursery schools using LGSS payroll in March 15 and quarterly thereafter to tie up the cash aspect of each Nursery schools accounts. Individual letters will come out shortly on this.

By the public sector, for the public sector

Other Grants

PE Sports Grant is applicable for 3 Academic Years ending August 16. Schools will receive 7/12ths in January 16 and 5/12ths in May 16.

Devolved Formula Capital - £4000 lump sum and £11.25 per pupil – Primary / Nursery, £16.88 – Secondary, £33.75 – Special as at census January 14.

By the public sector, for the public sector

Budget Proposal• This needs to be submitted to LGSS finance by 1st May.

• When submitting your budget for 2015-2016 you need to ensure that you have populated the carryforward columns to match the SB1 form.

• At the point of submission we need both the proposal form and the 3yr plan.

• Failure to follow these guideline could result in a delay in the budget acceptance process.

By the public sector, for the public sector

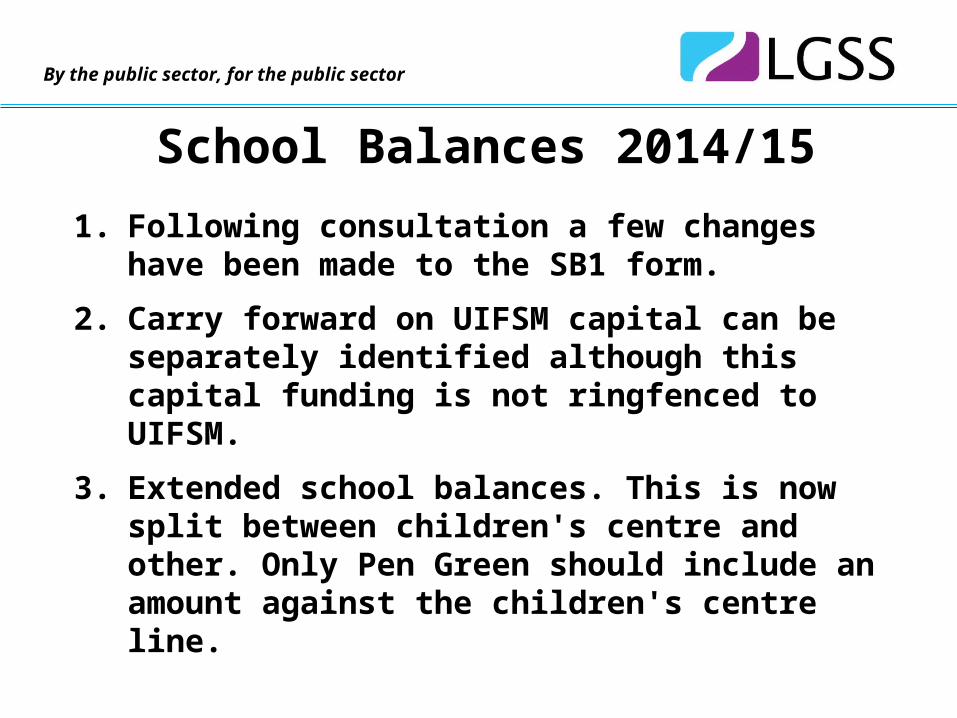

School Balances 2014/15

1. Following consultation a few changes have been made to the SB1 form.

2. Carry forward on UIFSM capital can be separately identified although this capital funding is not ringfenced to UIFSM.

3. Extended school balances. This is now split between children's centre and other. Only Pen Green should include an amount against the children's centre line.

By the public sector, for the public sector

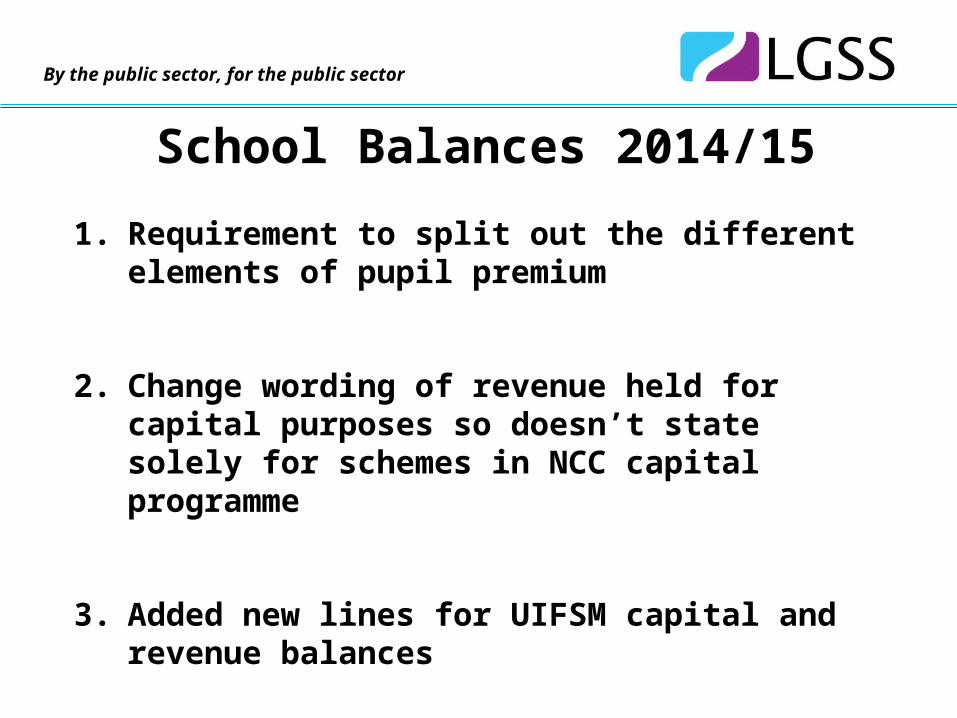

School Balances 2014/15

1. Requirement to split out the different elements of pupil premium

2. Change wording of revenue held for capital purposes so doesn’t state solely for schemes in NCC capital programme

3. Added new lines for UIFSM capital and revenue balances

By the public sector, for the public sector

Universal Infant FSM (UIFSM)

Nourish schools

Charges match grant allocated so no need to accrue or separately identify any UIFSM revenue on the SB 1 form.

In 2015-16 charges will reflect adjusted UIFSM grant allocation April 15 to July 15

By the public sector, for the public sector

Universal Infant FSM

Non Nourish schools

Schools will have paid a different amount to the main UIFSM formula revenue funding for the September 14 to March 15 period. This should be reflected in the grant adjustment for the September 14 to March 15 period information and amount from the EFA.

Non Nourish schools are able to include this on the 2014-15 year end SB1 form. (can be a ‘+’ (clawback expected) or ‘-’ (additional funding anticipated)

By the public sector, for the public sector

Schools Forum

Below is a link to the link to the website to see the latest information.

•Schools Forum - Northamptonshire County Council

Schools are recommended to read Forum Matters when published to keep up to date with latest developments.

By the public sector, for the public sector

CFR Reporting 2014-15Schools should check:

a) the current report is correct when compared to Oracle and the Cumulative Expense Analysis report.

b) the CFR apportionment has been actioned correctly

c) the Validation report for codes not mapped and missing expenditure / PFI Charges / Bad Debt as per update notes.

d) that income codes are in credit and expenditure codes are positive. Usually due to accruals.

e) That a valid email address has been entered.

By the public sector, for the public sector

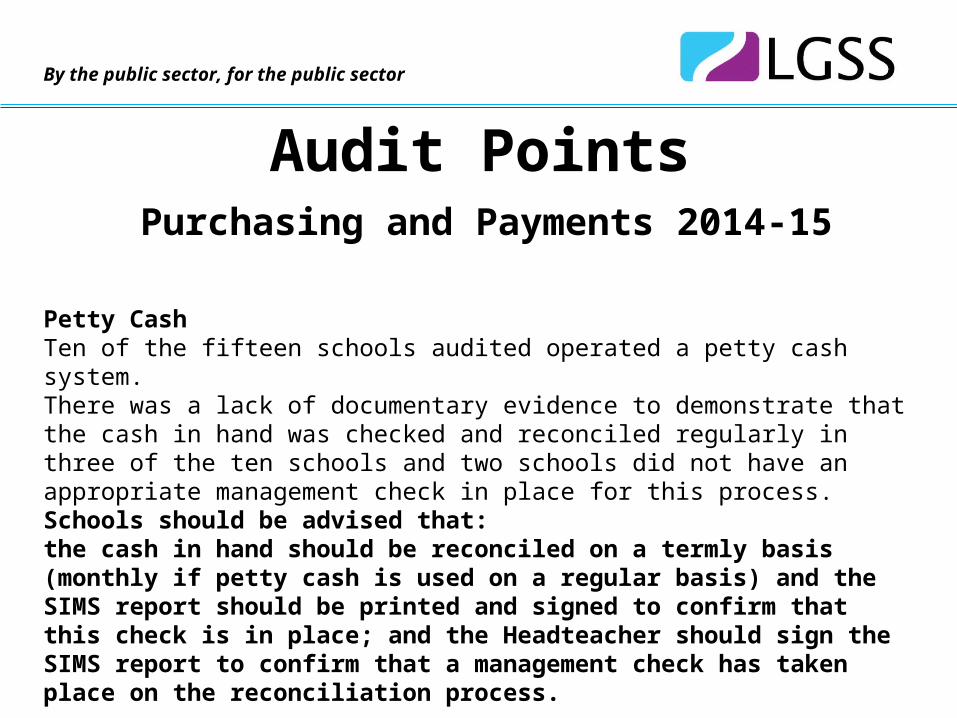

Audit PointsPurchasing and Payments 2014-15

Petty Cash Ten of the fifteen schools audited operated a petty cash system. There was a lack of documentary evidence to demonstrate that the cash in hand was checked and reconciled regularly in three of the ten schools and two schools did not have an appropriate management check in place for this process. Schools should be advised that: the cash in hand should be reconciled on a termly basis (monthly if petty cash is used on a regular basis) and the SIMS report should be printed and signed to confirm that this check is in place; and the Headteacher should sign the SIMS report to confirm that a management check has taken place on the reconciliation process.

By the public sector, for the public sector

Payment for Goods and Services Fourteen of the fifteen schools audited were aware that additional checks were required to confirm the self employed status of individuals providing services to the school; however, no additional checks had been carried out in eight of the fourteen schools. Schools should be advised that they must check the employment status of all individuals who supply services to the school.

Procurement Card Twelve of the fifteen schools audited had a procurement card / cards in place; however, the Governors had not approved maximum limits for the procurement card / cards and the card holders in three of these schools. Although appropriate records were maintained, adequate controls were not in place for the authorisation of the Headteacher’s card statements in nine of the twelve schools. Schools should be advised that Financial Regulations state that: Governors’ should approve maximum limits for the schools procurement card / cards and the card holders; and the receipts and statement for the Headteacher’s card should be checked and authorised by the Chair of Governors / Chair of Finance Committee.

By the public sector, for the public sector

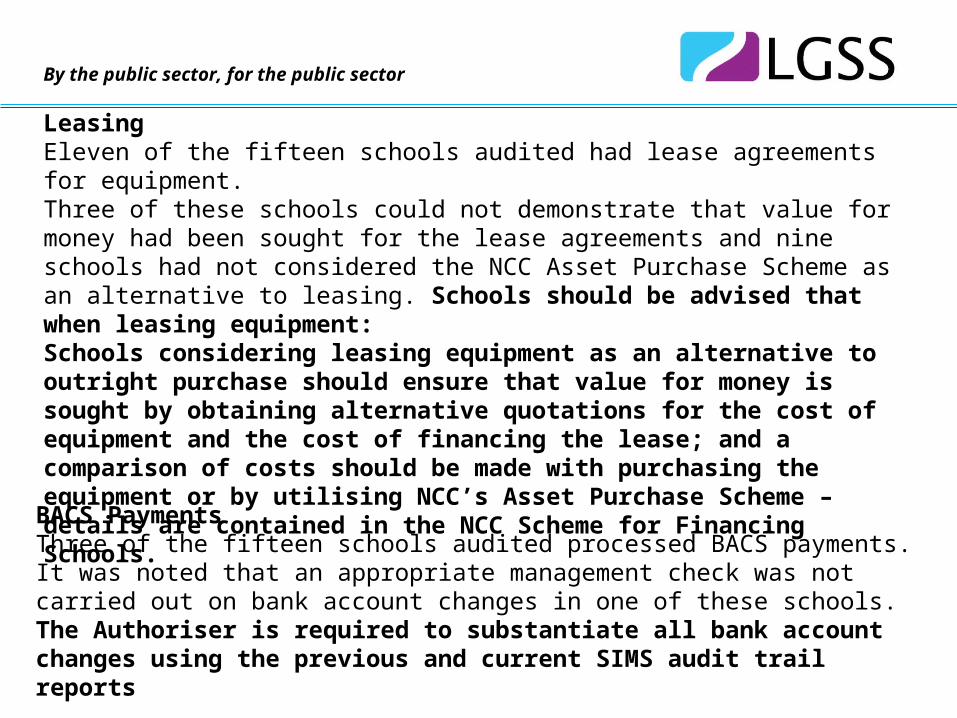

BACS Payments Three of the fifteen schools audited processed BACS payments. It was noted that an appropriate management check was not carried out on bank account changes in one of these schools. The Authoriser is required to substantiate all bank account changes using the previous and current SIMS audit trail reports

Leasing Eleven of the fifteen schools audited had lease agreements for equipment. Three of these schools could not demonstrate that value for money had been sought for the lease agreements and nine schools had not considered the NCC Asset Purchase Scheme as an alternative to leasing. Schools should be advised that when leasing equipment: Schools considering leasing equipment as an alternative to outright purchase should ensure that value for money is sought by obtaining alternative quotations for the cost of equipment and the cost of financing the lease; and a comparison of costs should be made with purchasing the equipment or by utilising NCC’s Asset Purchase Scheme – details are contained in the NCC Scheme for Financing Schools.

By the public sector, for the public sector

Local Bank Account An up to date mandate was not held on file in two of the fifteen schools audited. Fourteen of the fifteen schools audited had a manual cheque book; however, two of these schools did not have systems in place for monitoring the sequential use of manual cheques. In addition, nine of the fifteen schools audited had printable cheque stationery; four of these schools did not have systems in place for monitoring the sequential use of these cheques. Schools may not have appropriate cheque signatories in place if an up to date mandate is not held on file. Schools should be advised that Financial Regulations state that: an up to date mandate should be held on file in the school; control should be exercised over all cheques issued including ensuring that cheques are used in a systematic manner and in number sequence. School Management should sign the manual cheque book stub to confirm that this management check is in place; and the current cheque run report and the previous cheque run report should be provided to the cheque signatories in order for them to be able to confirm the sequential use of cheque stationery.

By the public sector, for the public sector

Good practice identified Payment for Goods and Services: Checks were in place to confirm that schools only paid for goods and services they had received; Schools ensured that VAT was only reclaimed when appropriate VAT invoices were received; Procedures were in place to ensure that invoices were appropriately authorised; and Cheque signatories checked the cheques they signed to the invoices.

Procurement Card: Appropriate controls were in place for the security of procurement cards.

Petty Cash: Agreed levels of petty cash were in place; Petty cash purchases were authorised before staff were reimbursed; and Reimbursed individuals signed to confirm receipt of monies.

By the public sector, for the public sector

Good practice identified continued

Local Bank Account: Spoiled and cancelled cheques were retained; Cheque book stubs included details regarding who the cheque was made payable to, the amount and the date; and Bank reconciliations were completed each month and management checks were in place.

BACS Payments: Appropriate reports / documentation were provided to the Authoriser; Appropriate management checks were in place for the BACS transfer fileThe BACS transfer file was released by the Headteacher; and Smart cards and PIN numbers were held securely.

By the public sector, for the public sector

Pupil Premium Audit There is no standard method to be followed or records that must be maintained;

Schools must however have sufficient evidence to demonstrate how this funding has been allocated and spent within the budget and how it has been used to support pupils and raise standards;

OFSTED are now focusing more closely on these aspects when inspecting schools.

By the public sector, for the public sector

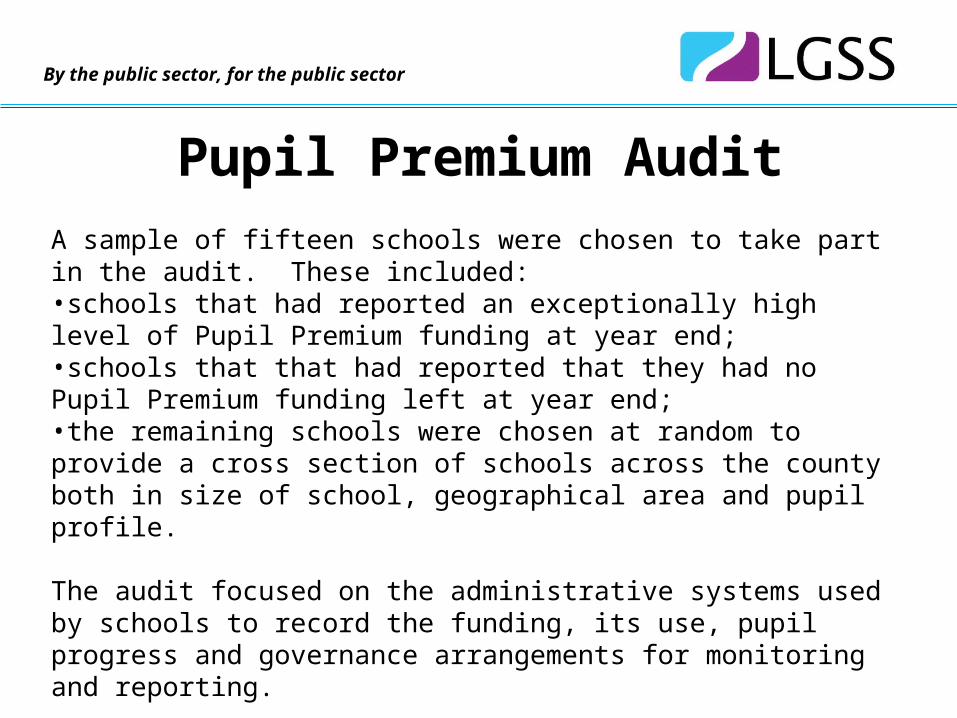

Pupil Premium AuditA sample of fifteen schools were chosen to take part in the audit. These included:•schools that had reported an exceptionally high level of Pupil Premium funding at year end;•schools that that had reported that they had no Pupil Premium funding left at year end;•the remaining schools were chosen at random to provide a cross section of schools across the county both in size of school, geographical area and pupil profile.

The audit focused on the administrative systems used by schools to record the funding, its use, pupil progress and governance arrangements for monitoring and reporting.

By the public sector, for the public sector

Pupil Premium AuditAreas of Good PracticeGood practice identified Finance •Procedures were in place to ensure that all Pupil Premium Funding was delegated to schools and periodic reconciliations to confirm this were completed by the Principal Accountant;•All schools could identify in their accounts the Pupil Premium funding and how it was being used;•Schools either had dedicated cost centre(s) to achieve this and or had recorded the funding and expenditure on spreadsheets;•Most schools had calculated the costs of the interventions and support for each pupil;•Governing bodies were advised of the level of Pupil Premium Funding when setting the budget for the year;

By the public sector, for the public sector

Pupil Premium AuditAreas of Good PracticeGood practice identified Finance •Financial Monitoring reports for Pupil Premium Funding were available showing the budget and expenditure to date and balances held;•Year end balances of pupil funding were reported to Governors;•Schools Forum had monitored the level of Pupil Premium balances reported and where these were exceptionally high were challenging schools on this; •Schools publicised to parents the advantages of registering for Free School Meals and the benefits this would bring i.e more funding to the school and increased support and or resources for pupils;•For LAC NCC had introduced measures to require schools to state their forecast and actual spend of Pupil Premium funding.

By the public sector, for the public sector

Pupil Premium AuditPupil Records•Records were in place to record the interventions and support provided to Pupil Premium pupils;•Progress of Pupil Premium children in key areas was monitored;•Interventions were reviewed. Governance •All schools had a designated senior member of staff and a governor responsible for overseeing Pupil Premium;•Governors completed visits to review Pupil Premium records and for support provided to these children;•Governors minutes recorded that they discussed the use of Pupil Premium funding and challenged Headteachers on the impact this was having;•There was evidence that Governors had sharpened their focus on Pupil Premium, this was now a standing item on the agenda of most Governing Body meetings and / or on Governor Committee meetings;•Reports on progress of the Pupil premium children were provided to Governors, comparing their performance with that of other pupils.

By the public sector, for the public sector

2014-15 ClosedownKey Points:• VAT Year End date is close of business 23 Mar

15.• No transactions to be carried out on SIMS after

23rd March except payroll and accruals.• Don’t cancel any cheques on FMS6 between

year end and completing the year end bank reconciliation.

By the public sector, for the public sector

2014-15 ClosedownKey Points:• Ensure the LB26 is on track to balance at year

end. Be reminded that if there is a variance we will use Oracle for the year end position.

• You CANNOT accrue for any internal (NCC) suppliers.

By the public sector, for the public sector

2014-15 Closedown (cont)• All instructions, timelines and forms are on our website

(Guidance and Procedures – Year End webpage).• Key dates:

– 14 Mar 15 – deadline for Lease returns.– 24 Mar 15 – midday deadline for VAT return– 24 Mar 15 – midday deadline for the Balances & Reserves– 24 Mar 15 – close of business deadline for LB9 (Accruals)– 25 Mar 15 – deadline for payroll returns (own payroll)– 25 Mar 15 – deadline for payroll creditors (own payroll)

By the public sector, for the public sector

2014-15 Closedown (cont)– 13 Apr 15 – Period 12 Reports Issued to Schools– 15 Apr 15 – deadline for year end bank reconciliation.– 16 Apr 15 – deadline for year end SIMS/Oracle reconciliation.– 17 Apr 15 – deadline for comments on period 12 Oracle reports.– 24 Apr 15 – LGSS Finance Issues SB1 form & LB25 Return– 24 Apr 15 – deadline for year end reports (LB8)– 1 May 15 – deadline for School Balances Return (SB1)– 15 May 15 – deadline for Confirmation of Final Closure (LB14)

By the public sector, for the public sector

Financial Regulations state that alternative quotations should be obtained for all high value purchases to demonstrate that value for money has been sought.

Schools should be advised that as a minimum:

•two written quotations should be obtained for goods or services over £1000 and less than £10,000 in value; •three written quotations should be obtained for goods or services over £10,000 and up to £30,000; •goods and services over £30,000 are subject to a formal tender process; and •evidence should be retained in the school to prove that best value has been sought and to demonstrate this to the Governing Body.

Quotes & Tenders

By the public sector, for the public sector

Housekeeping

National Insurance Tables – 2015/16

This is now available on the website Update No 58.

Teaching & Support Staff Superannuation Rates 15/16

These are now available on the website Update No 59.

By the public sector, for the public sector

Housekeeping

Virements / Journals & Payroll Journals

These will only be accepted if on the templates, any paper copies received will be returned.

Official (SIMS) orders must be raised for all goods and services with the exception of utilities, rents, rates and telephones.

By the public sector, for the public sector

Questions?