business & strategy update -...

TRANSCRIPT

© 2007 ASM

Q3 2007 Results

Proprietary Information

Business & Strategy Update

© 2007 ASM Q3 2007 ResultsProprietary Information 2

Safe Harbor Statements

All matters discussed in this business and strategy update, except for any historical data, are forward-looking statements. Forward-looking statements involve risks and uncertainties that could cause actual results to differ materially from those in the forward-looking statements. These include, but are not limited to, economic conditions and trends in the semiconductor industry generally and the timing of the industry cycles specifically, currency fluctuations, the timing of significant orders, market acceptance of new products, competitive factors, litigation involving intellectual property, shareholder and other issues, commercial and economic disruption due to natural disasters, terrorist activity, armed conflict or political instability, epidemics and other risks indicated in the Company's filings from time to time with the U.S. Securities and Exchange Commission. All statements are made as of the date provided and we assume no obligation nor intend to update or revise any forward-looking statements to reflect future developments or circumstances.

© 2007 ASM Q3 2007 ResultsProprietary Information 3

ASMI’s Organizational Structure

• ASMI has a dual listing on NASDAQ (1981) and AEX (1996)• Significant trading volumes on both exchanges

Total employment as of September 30, 2007

ASMEuropeASM

EuropeASM

AmericaASM

AmericaASM

JapanASM

Japan

100.0% 53.35%

MalaysiaMalaysia SingaporeSingapore ChinaChina Hong KongHong Kong

ASM PacificTechnologyASM PacificTechnology

HKSE

ASM Back End

ASM Back End

ASMFront End

ASMFront End

ASM InternationalASM International

2172

761 553 388 198 10046

618 887 7196 1043

12242

otherother

302

Front-endManufacturing

Singapore

Front-endManufacturing

Singapore272

ASMFar East

ASMFar East

© 2007 ASM Q3 2007 ResultsProprietary Information 4

• Front-end:- Front-end good progress on its road to profitability- Innovative technologies for established product

lines and product lines under development (incl. ALD)

- Increased focus on S.E. Asian market, incl. FEMS• Back-end:

- #1 worldwide and growing- Broadening field of applications

• Synergies between Front-end and Back-end:- Present operational synergies- Future technological synergies

Investment Highlights

© 2007 ASM Q3 2007 ResultsProprietary Information 5

Addressable Markets Estimate 2007

Assembly$ 3.8 B

Deposition$ 9.5 B

Test$ 12.3 B

Other wafer process$ 4.7 B

Etch & Clean

$ 7.9 B

Lithography$ 9.9 B

(Total $ 48.1 Billion)

Source: VLSI Research Inc., June 2007

Depositionin 2012$ 11.5 B Assembly

In 2012$ 4.3 B

© 2007 ASM Q3 2007 ResultsProprietary Information 6

ASMI’s Market Leadership in faster growing segments

2012E

3769

633

219

413

1490

1615

248

430334941Back End (overall)(equipment 80%, leadframes 20%)

Advanced Developments:

1105543emerging interest- RTP

521191strong position- Atomic Layer CVD

11703572of which Low-k films

223314363- Plasma Enhanced CVD

178014983- Vertical Furnace

5482261- Epitaxy (Si, SiGe)

2007E2006

Current Position

Market Segment

Front End

Market Estimate (US$ mill.)*

* VLSI Research Inc., June 2007

© 2007 ASM Q3 2007 ResultsProprietary Information 7

ASM: IP Powerhouse

• In 2007 a different approach by IEEE

• Ranking per sector• ASMI amongst the 4

strongest IP companies in the sector, which are all large companies

• All others behind

IEEE Spectrum, November 2006

13691941ElectronicsHitachi Ltd.Japan

10

1492109Semiconductor Equipment Manufacturing

ASM International NV.Netherlands

9

1603413Automotive and PartsDelphitechnologiesInc.United States

8

1699780Computer Systems and Software

Microsoft Corp.United States

7

1832371Semiconductor Equipment Manufacturing

Applied Materials Inc.United States

6

1856419SemiconductorManufacturing

Broadcom Corp.United States

5

23641553SemiconductorManufacturing

Intel Corp.United States

4

27561810Computer Systems and Software

Hewlett-Packard Co.United States

3

30842972Computer Systems and Software

IBM Corp.United States

2

33961569SemiconductorManufacturing

Micron Technology IncUnited States

1

PipelinePower

2005 U.SPatents

IndustryCompanyCountry

Rank

Top 10 Patent CompaniesIEEE Spectrum, November 2007

© 2007 ASM Q3 2007 ResultsProprietary Information 8

Further steps to profitability Front-end

To be achieved by:• Sales growth to outperform the industry over the cycle

• Market share gains in PECVD, VF and SiGe & Strained Si• Strengthened Asian network• ALD (TP / CP) to gain critical mass and well on its way in 2007

• Costs reduction• Improvement in gross margins due to Asian cost relocation and other programs• Lower relative R&D costs by scrutinizing R&D program

• Cash Flow improvements• Significant improvement in working capital• Reduction in capital expenditures as percentage of net sales

Targets:• 2007

• Positive net earnings and positive operating cashflow

• 2009 – Further• Operating margins in line with Front-end peer universe

© 2007 ASM Q3 2007 ResultsProprietary Information 9

The strong aspects of ASMI’s corporate structure

• Current and future operational synergies between ASMI and ASMPT• Front-end manufacturing in Singapore (FEMS)• IC wafer production shift to Asia accelerating• Decision makers in Asia (Samsung, TSMC, Hynix, etc.)

• Future convergence in technology between Front-end and Back-end• Industry dynamics will drive further improvements and more

efficient processes• These developments require integrated Front-end and Back-end

process and manufacturing technologies, as validated by the leading industry players

Great opportunities in Back-end and Front-end

© 2007 ASM Q3 2007 ResultsProprietary Information 10

Move to Asia facilitated by link to ASMPT

• Manufacturing generic subassemblies and components to replace outsourcing in US and Europe• Benefit from lower labour rates (60-70%)• Benefit from skilled labour in flexible market• Benefit from lower local prices for materials and components

• Gross Margin improvement by 1.5% in 2006 realised • Target GM improvement ~4% in 2007 and more to be expected

© 2007 ASM Q3 2007 ResultsProprietary Information 11

Trend towards new IC Packaging

• Fully integrated 3D die to die connected system• This shows an initial wafer with functional silicon• Two additional layers of functional silicon have been bonded to it

Specifics:

• Different functionality on top of each other• Direct die to die connection• High precision placement of die’s• Addressable market could be order of magnitude USD 200 – 300 million in five years time

© 2007 ASM

Q3 2007 Results

Proprietary Information

Wafer Processing

Front End

© 2007 ASM Q3 2007 ResultsProprietary Information 13

ASMI Front-End Global Operations

Asia

Business UnitsPECVD Products

CP Products

Asia office and manufacturing facilities

Tama & Nagaoka, JapanManufacturing Singapore

(FEMS)Marketing & Service

Units inTaiwan, China,

Korea,SingaporeResearch center Korea

Europe

Business UnitsVertical Furnaces

RTP Products

HQ , Europe office and manufacturing facilitiesBilthoven and Almere,

Netherlands

Research Centers in Belgium and Finland

USA

Business UnitsEpitaxy Products

TP Products

US office and manufacturing facilities

Phoenix, Arizona

© 2007 ASM Q3 2007 ResultsProprietary Information 14

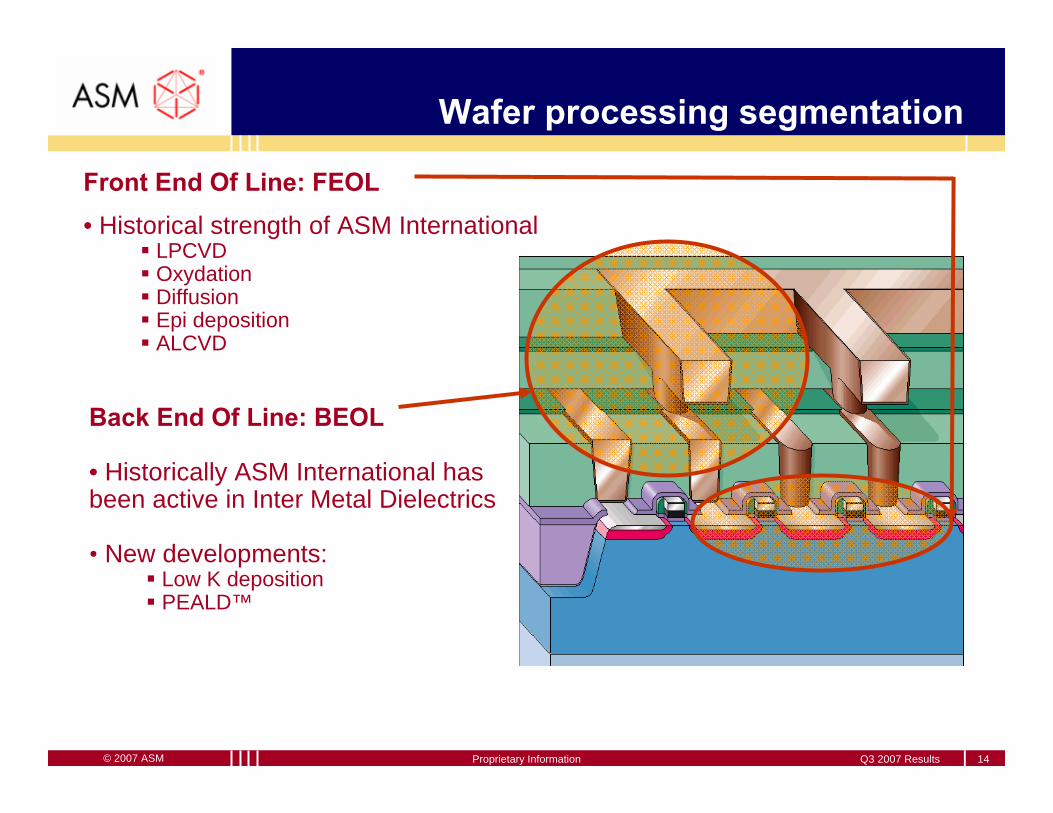

Wafer processing segmentation

Back End Of Line: BEOL

• Historically ASM International has been active in Inter Metal Dielectrics

• New developments:Low K depositionPEALD™

Front End Of Line: FEOL• Historical strength of ASM International

LPCVDOxydationDiffusionEpi depositionALCVD

© 2007 ASM Q3 2007 ResultsProprietary Information 15

Front End technology drivers

• ASMI’s solutions:- Established products

Vertical furnaceSilcore chemistryTiN depositionBatch ALCVD

EpitaxySiGe Epi DepositionStrained Silicon

PECVDSuperior Low-k chemistryNano Carbon Polymer

- New productsAtomic Layer Deposition

High-k Gate DielectricsHigh-k Capacitor Dielectrics

RTPNew Technical Approach:“ Levitor® ”

• Semiconductors becoming smaller, better performing,faster switching and lower power consumption:Line widths < 65 nm, Ultra thin films, New materials

© 2007 ASM Q3 2007 ResultsProprietary Information 16

Front-end’s strategy in S.E. Asia

Customer wins in TaiwanTSMC Nanya

Promos Winbond

Inotera Powerchip

Rexchip

Conclusion:

All major players are in the ASM customer base

Approach in KoreaSamsung Hynix

Magnachip Dongbu HiTek

LG Siltron

Unique enabling technology:

NCP hardmaskGapFill Low-k process

China is following

© 2007 ASM Q3 2007 ResultsProprietary Information 17

Vertical Furnace

ASMI Vertical furnaces (Advance® 400 Series)• ASMI has the largest installed base in 300mm vertical furnaces• Smart Batch and Batch ALD configurations• Target future market share of 30%• This is almost triple the historic overall market share in vertical furnaces

FEOL

A412™

© 2007 ASM Q3 2007 ResultsProprietary Information 18

Epitaxy

• Market leader in Silicon Germanium (and SiGeC)- New material in high

frequency transistors for broadband wireless communications

- ASMI is the market leader (70+%)

• New Activities- Strained Silicon- SOI applications

FEOL

Epsilon®

© 2007 ASM Q3 2007 ResultsProprietary Information 19

PECVD

ASMI Solutions- Low-K PECVD Aurora®

New application- NCP (Nano Carbon Polymer)

Back End of LineInterconnectMany layers of Metal and IMD

<100 nm generations:- Low-K for IMD

BEOL

Dragon®

Eagle®

© 2007 ASM Q3 2007 ResultsProprietary Information 20

Atomic Layer Deposition

• Thermal (ALD) and Plasma enhanced (PEALD) solutions

• Technology to control deposition one atomic layer by one atomic layer, resulting in ultra-thin films

• Response to Smaller Line Geometries and high Aspect Ratio’s

• Gate-stack, capacitor dielectrics, diffusion barriers, Cu seed layers

• Design-in with top IC manufacturers • Strong patent portfolio and technology lead over

competition

FEOL/BEOL

Transistor Gate Dielectrics DRAM High K capacitor dielectrics

Polygon®

© 2007 ASM Q3 2007 ResultsProprietary Information 21

RTP

• Paradigm Shift Rapid Thermal Processing (RTP) Concept- Conventional: Radiation- ASMI’s Levitor®: Conduction

• Emissivity Independent- Improved uniformity

• Cost reduction: min. 30 %- Ten times more energy efficient- Faster (75 wph)- Low cost

• Targeting ≤65 nm Technology

FEOL

Levitor®

Levitor®

© 2007 ASM Q3 2007 ResultsProprietary Information 22

The use of the 3rd Dimension will change the Industry

Improvements in speed, cost and

power consumption

3D Processor/Memory Stacking

Intel, ISS 2007; VLSI 2006(top), Samsung IEDM 2006 (Bottom)

3D in the Front-end of Line

Improvements in drive current and density

3D SystemIntegration

Improvements infunctionality

and formfactor

© 2007 ASM Q3 2007 ResultsProprietary Information 23

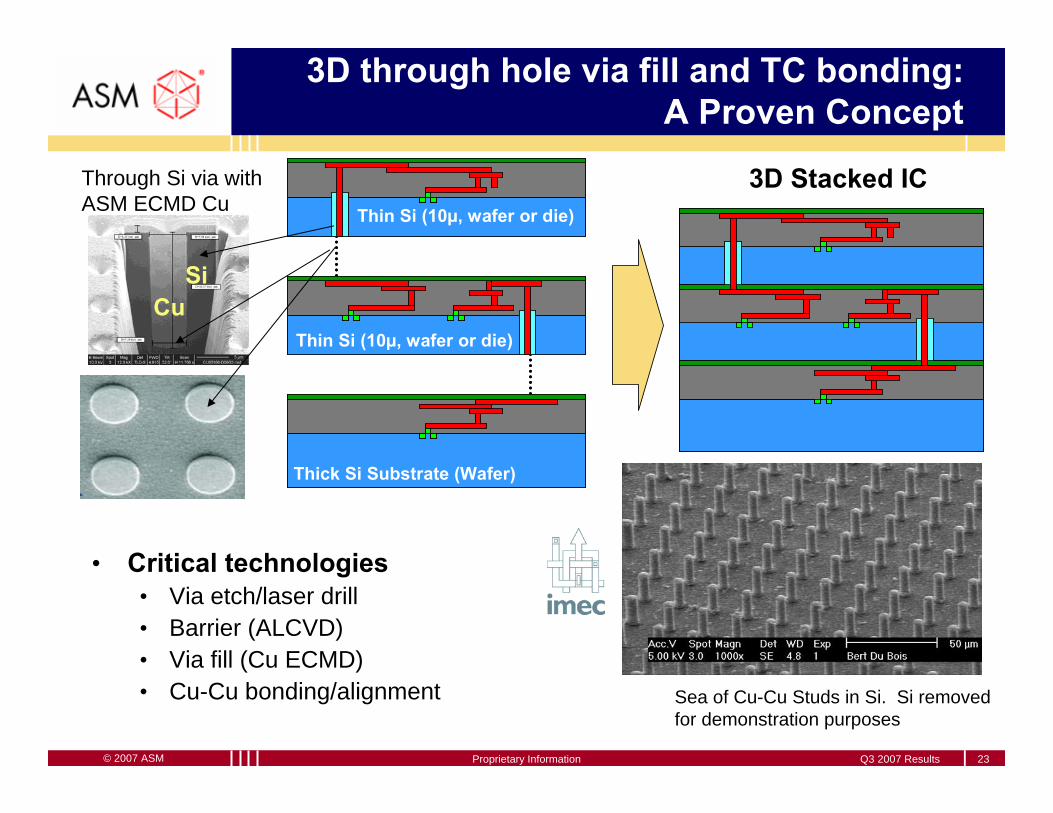

Thin Si (10µ, wafer or die)

Thin Si (10µ, wafer or die)

Thick Si Substrate (Wafer)

Thin Si (10µ, wafer or die)

Thin Si (10µ, wafer or die)

Thick Si Substrate (Wafer)

3D Stacked IC

3D through hole via fill and TC bonding:A Proven Concept

• Critical technologies• Via etch/laser drill• Barrier (ALCVD) • Via fill (Cu ECMD) • Cu-Cu bonding/alignment Sea of Cu-Cu Studs in Si. Si removed

for demonstration purposes

Through Si via with ASM ECMD Cu

CuSi

© 2007 ASM

Q3 2007 Results

Proprietary Information

Wafer Assembly & Encapsulation

Back End

© 2007 ASM Q3 2007 ResultsProprietary Information 25

ASMI Back End global operations

Asia

Business Unitsall Back End products

HQ, office and manufacturing facilities

Hong Kong

Manufacturingfacilities in

Singapore, Shenzhen (PRC),

and Malaysia

Europe

Sales and Service Unit

European officeBilthoven, Netherlands

USA

Sales and Service Unit

US officeSan Jose, California

© 2007 ASM Q3 2007 ResultsProprietary Information 26

Product strategy

• ASMI supplies equipment to the Back End of the semiconductor manufacturing industry

• ASMI’s tools are used to assemble chips into its final package

Back End processes

Wirebonder

Diebonder Flip Chip Trim & Form &

Test HandlerMoulding

ASMI’s tools

Wire bonding

Flip Chip,BGAbonding

Die Bonding Moulding Trim & Form

© 2007 ASM Q3 2007 ResultsProprietary Information 27

Business strategy:Broadening field of applications

• ASMI supplies equipment to the Back End of the semiconductor manufacturing industry

• ASMPT’s tools are used in an ever growing area of applications

• Not only IC assembly and packaging but also:• CMOS image sensors• Power LED• SD memory cards• Chip-on-glass (COG)• Package on Package (POP)• RFID applicationsMajor progress in 2006 and 2007

© 2007 ASM Q3 2007 ResultsProprietary Information 28

Business drivers

Technology Drivers:• Size of packages

• Finer pitch ball bonding capability• Advanced technologies

• Flip Chip, Chip Scale Packages, Ball Grid Array (BGA), Stacked Die, System in Package (SiP), Wafer Level Packaging (WLP)

Cost Driver:• Cost of Ownership

• Low cost solutions• Automation

• Integration of assembly and packaging steps

© 2007 ASM Q3 2007 ResultsProprietary Information 29

Gold Wire Bonder

Q2 2007 High speed 30 micron pad pitch capability• Eagle Xtreme™ for 30 micron, < 50 ms per wire

Q3 2004 dual bond head capability• Twin Eagle™ for 180% capacity

Eagle Xtreme™

TwinEagle™

© 2007 ASM Q3 2007 ResultsProprietary Information 30

Die Bonding

Introduced Q2 2007:MCM12

Multi Chip Module• Versatile & flexible bonding

processes in single machine• Achieving pro-long MTBA• High throughput• High placement accuracy

MCM12

Introduced Q3 2007: COG 900• Chip-On-Glass Die bonder for LCD application

COG 900

© 2007 ASM Q3 2007 ResultsProprietary Information 31

Flip Chip Bonding

Advantages:• Minimum footprint• Higher I/O connection flexibility• Improved electrical reliability• Improved thermal capabilities• Low cost assembly

Market still relatively small

AD 800/900 series

AD 819

AD 900

© 2007 ASM Q3 2007 ResultsProprietary Information 32

Operations

SINGAPORE

HONG KONG

PARTS &

SUBASSEMBLIES

PARTS &SUBASSEMBLIES

CHINA

MALAYSIA

PARTS &

SUBASSEMBLIES

CUSTOMERS

© 2007 ASM Q3 2007 ResultsProprietary Information 33

ASMPT: Nr. 1 worldwide+growing

Equipment revenue Benchmarking

0.60

0.911.160.95

1.30

0.49

0.96

1.46

3.35

1.221.44

2.12

3.193.52

0.56

0.86

1.50

0.420.720.55

0.42

0.85

0.59

1.200.77

0.520.50

0.750.84

1.26

0.54

0.960.72

0.57

1.15

0.62

1.76

0.30

0.920.64

0.92

0.770.60

1.35

0.39 0.560.340.31

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

ASMK&SBESITowaShinkawaESEC

H1 2007 Equipment Revenue

45.5

46.3

47.3

49.7

100

0 25 50 75 100

ASM

K&S +AlphsemBESI

Shinkawa

Towa

US$M245.5

121.9

116.2

113.6

111.8

%

© 2007 ASM

Q3 2007 Results

Proprietary Information

Financial Overview

© 2007 ASM Q3 2007 ResultsProprietary Information 35

Net Sales

155 164 153 133182

337267 287

356 358409

149 135 169155

233

224

252295

399 367

468

380

556

0

250

500

750

1000

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Front End Back End

Euro millions

* *

* All figures continued operations

© 2007 ASM Q3 2007 ResultsProprietary Information 36

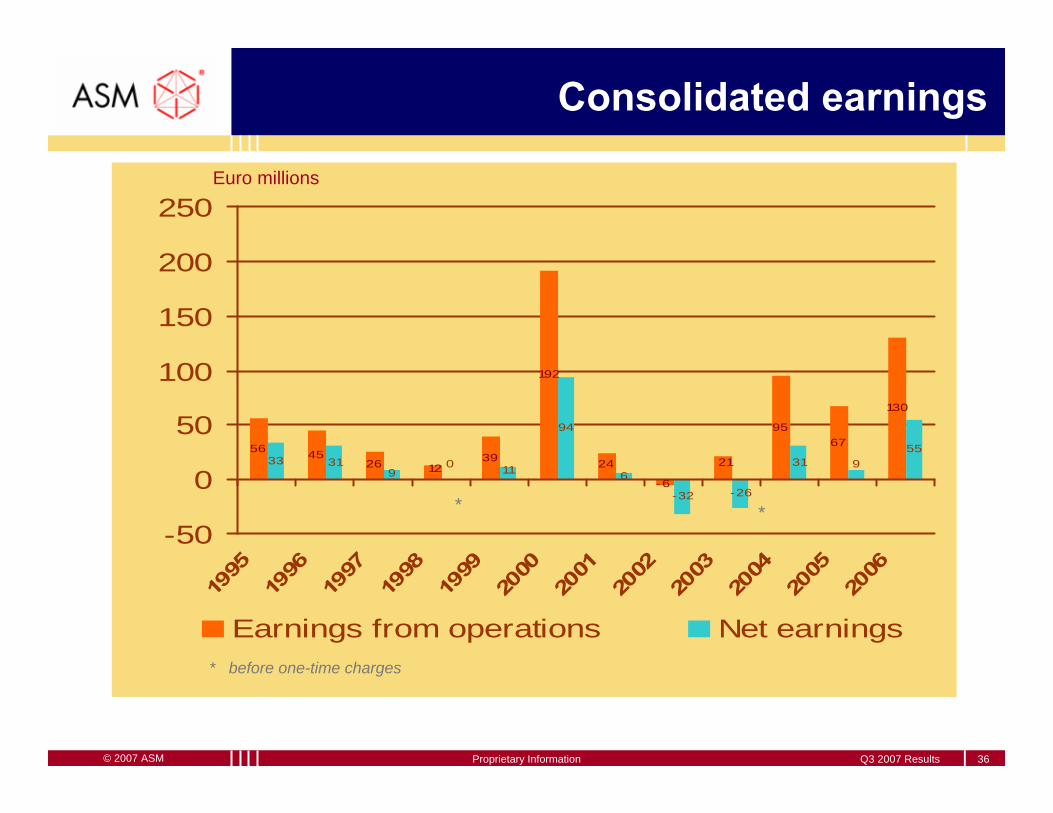

Consolidated earnings

5626 39

192

9567

130

33 31 0

94

-32 -26

31 955

21

-612 24

45119 6

-50

0

50

100

150

200

250

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

Earnings from operations Net earnings* before one-time charges

*

Euro millions

*

© 2007 ASM Q3 2007 ResultsProprietary Information 37

Consolidated Statement of Continuing Operationsper quarter

Euro millions

Net Sales 213.4 254.7 253.5

Gross Profit 83.0 96.9 97.2

SGA (29.2) (32.9) (33.3)R&D (21.9) (21.5) (21.2)other (0.1) (0.1) (0.1)

Earnings from Op. (EBIT) 31.7 42.4 42.6

Net Earnings (after minority interest) 13.9 20.8 20.0

Diluted Net Earnings per share 0.26 0.35 0.34

Q3 2006 Q3 2007**Q2 2007*

* Excluding € 5.9 million expense resulting from extinguishment of convertible debt** Excluding € 4.1 million expense resulting from extinguishment of convertible debt

© 2007 ASM Q3 2007 ResultsProprietary Information 38

Consolidated Cash Flow Statements

Euro millions FY 2005 FY 2006 3/4 2007

Net Cash from Operations 50.7 143.8 69.1

Net Cash from/for Investments (45.6) (30.1) (30.8)

Net Cash before Financing 5.1 113.7 38.3

Net Cash from/for Financing (109.7) (41.8) (85.9)

Net Change in Cash (83.6) 58.9 (52.0)

Ending Cash Balance 135.0 193.9 141.9

CAPEX ( net of Sale PPE ) 43.7 36.6 30.1

Ending Working Capital 236.0 227.1 278.0WC in days sales 119 94 108

© 2007 ASM Q3 2007 ResultsProprietary Information 39

Euro millions Dec 2005 Dec 2006 Sep 2007

Cash and Cash Equivalents 135 ¹ 194 ¹ 142 ¹Other Current Assets 426 423 493Property, Plant & Equipment 163 151 147Goodwill 73 54 51Other Assets 15 10 9 Total Assets 812 832 842

ST Debt ( incl. Current LT Debt ) 28 27 30Other Current Liabilities 195 208 234LT Bank Debt / Convertible Subord. Bonds 229 202 160Other Long Term Liabilities 2 4 4 Total Liabilities 454 441 428

Minority Interest in Subsidiary 120 115 108Shareholders’ Equity 238 276 306 Total Equity & Liabilities 812 832 842

¹) of which cash availability for Front-end 55 105 99

Consolidated Balance Sheet

© 2007 ASM Q3 2007 ResultsProprietary Information 40

Backlog

• Q3 2007 New orders : € 198 million, down 13% from last quarter. • 68% of Q3 equipment orders booked in FE were for 300mm • Q3 2007 Book-to-Bill : 0,78 (Book-to-Bill in Q2 2007 was 0,89) • Ending Backlog : € 187 million (with roughly 49% in Back-end and 51% in Front-end)

050

100150200250300350400450

Q11998

Q4 Q3 Q2 Q12001

Q4 Q3 Q2 Q12004

Q4 Q3 Q22006

Q12007

BEFETotal

Euro millions

© 2007 ASM Q3 2007 ResultsProprietary Information 41

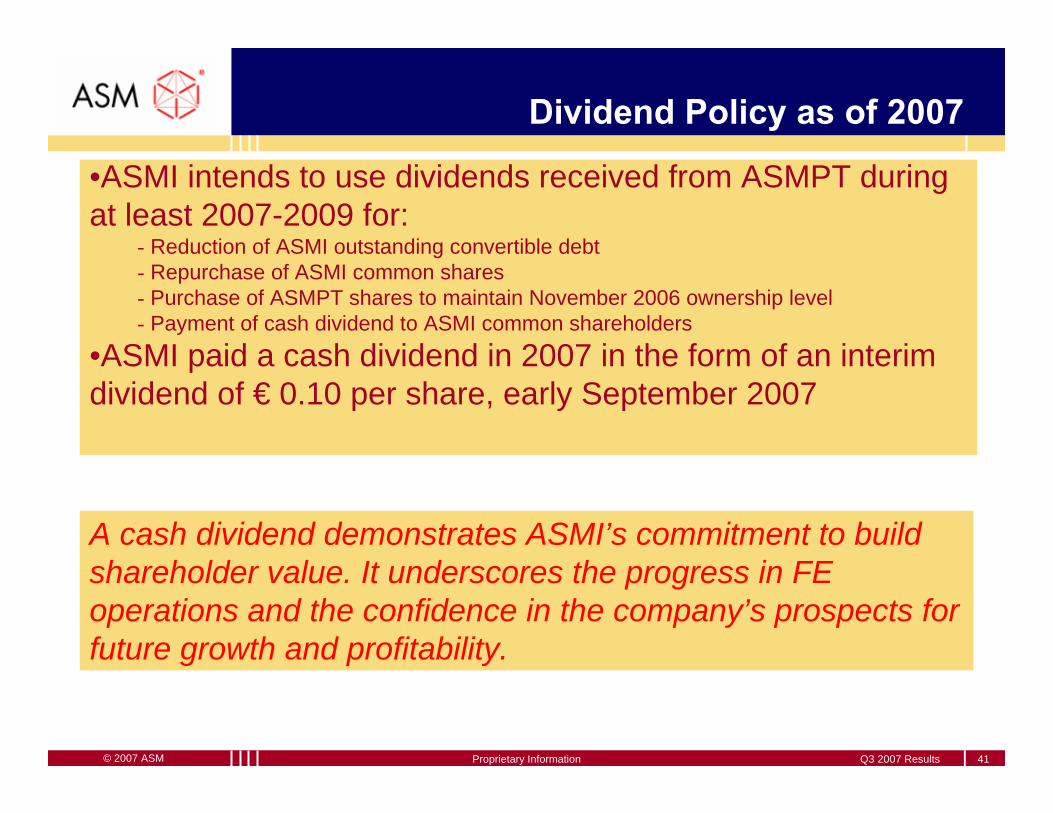

Dividend Policy as of 2007

•ASMI intends to use dividends received from ASMPT during at least 2007-2009 for:

- Reduction of ASMI outstanding convertible debt- Repurchase of ASMI common shares- Purchase of ASMPT shares to maintain November 2006 ownership level- Payment of cash dividend to ASMI common shareholders

•ASMI paid a cash dividend in 2007 in the form of an interim dividend of € 0.10 per share, early September 2007

A cash dividend demonstrates ASMI’s commitment to build shareholder value. It underscores the progress in FE operations and the confidence in the company’s prospects for future growth and profitability.

© 2007 ASM Q3 2007 ResultsProprietary Information 42

Outlook as per October 29, 2007

• Front-end order intake in Q4 2007 expected to increase compared to Q3.

• Front-end revenue level in Q4 2007 expected to be slightly below Q3 level.

• We reiterate our expectation for FE net earnings in 2007 (excluding negative impact related to the buyback of convertiblebonds).

• Back-end operations is expected to deliver strong sales and profitability in Q4 2007.

• Back-end is expected to show record sales and profitability levels for 2007, measured in local currency.

© 2007 ASM

Q3 2007 Results

Proprietary Information