business process management journal - université … · business process management journal ......

TRANSCRIPT

Business Process Management JournalEmerald Article: Pursuing quality and environmental performance: Initiatives and supporting processesMarie-Josée Roy, Olivier Boiral, Pascal Paillé

Article information:

To cite this document: Marie-Josée Roy, Olivier Boiral, Pascal Paillé, (2013),"Pursuing quality and environmental performance: Initiatives and supporting processes", Business Process Management Journal, Vol. 19 Iss: 1 pp. 30 - 53

Permanent link to this document: http://dx.doi.org/10.1108/14637151311294859

Downloaded on: 31-01-2013

References: This document contains references to 91 other documents

To copy this document: [email protected]

Access to this document was granted through an Emerald subscription provided by UNIVERSITE LAVAL

For Authors: If you would like to write for this, or any other Emerald publication, then please use our Emerald for Authors service. Information about how to choose which publication to write for and submission guidelines are available for all. Please visit www.emeraldinsight.com/authors for more information.

About Emerald www.emeraldinsight.comWith over forty years' experience, Emerald Group Publishing is a leading independent publisher of global research with impact in business, society, public policy and education. In total, Emerald publishes over 275 journals and more than 130 book series, as well as an extensive range of online products and services. Emerald is both COUNTER 3 and TRANSFER compliant. The organization is a partner of the Committee on Publication Ethics (COPE) and also works with Portico and the LOCKSS initiative for digital archive preservation.

*Related content and download information correct at time of download.

Pursuing quality andenvironmental performanceInitiatives and supporting processes

Marie-Josee Roy, Olivier Boiral and Pascal PailleFaculty of Administrative Sciences, University Laval, Quebec, Canada

Abstract

Purpose – The aim of this study is to focus on manufacturing small to medium-sized enterprises(SMEs) that are simultaneously pursuing quality and environmental objectives. Specifically, the paperexamines: the specific motivations and resources of SMEs that have chosen to pursue both priorities,the types of initiatives these SMEs have implemented, and whether pursuing both priorities iscorrelated with various facets of organizational performance.

Design/methodology/approach – This study gathered data from a sample of 254 ISO 9000 andISO 14000 certified Canadian SMEs. Data collection was based on a survey questionnaire sent to arandom sample of 1,514 companies.

Findings – The results highlighted significant differences between the SMEs holding both theISO 9000 and 14000 certifications and those holding only the 9000 ISO certification. Each group wasshown to have distinct motivations and resources and to have implemented different types ofinitiatives to address environmental concerns. Each group was positively correlated with differentfacets of organizational performance.

Research limitations/implications – This study’s findings contribute to the environmental and SMEliterature on this very complex topic by providing relevant empirical evidence based on primary data.

Practical implications – The results should provide guidance to manufacturing SMEs currentlyexamining how to address environmental issues. SMEs need to address these issues carefully andunderstand the potential trade-offs and consequences associated with their decisions.

Originality/value – An important contribution of this study is its detailed characterization ofenvironmental initiatives, drawing on insights derived from the environmental, accounting andmanagement literature. By using the analytical framework of organizational citizenship behaviours,the characterization also included informal and behavioural aspects often neglected in environmentalmanagement studies.

Keywords ISO 14000, ISO 9000 series, Environmental strategy,Organizational citizenship behaviors for the environment, SME, Small to medium-sized enterprises,Canada

Paper type Research paper

1. IntroductionWith growing pressure to improve environmental performance, large and smallcompanies alike are increasingly confronted by environmental issues. Much has beenwritten about how best to integrate these new factors into decision-making processes,however environmental management programs and systems are often developed bylarge corporations and reflect their experiences and strategies (Battisti and Perry, 2011;Fassin et al., 2011). The applicability of these tools, techniques and programs to smalland medium enterprises (SMEs), which represent the vast majority of businesses, mustbe examined, as these companies evaluate how best to respond to environmentalpressures, the long term implications of the available options, and how to efficiently

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1463-7154.htm

BPMJ19,1

30

Business Process ManagementJournalVol. 19 No. 1, 2013pp. 30-53q Emerald Group Publishing Limited1463-7154DOI 10.1108/14637151311294859

integrate those options into their corporate strategy (Hillary, 2003; Miles et al., 1999).However, this type of examination can be a challenging task. Environmental initiativesare often embedded in a complex and indivisible whole which comprises processes,values and behaviours. Furthermore, because there are similarities between wastereduction objectives and quality control goals, environmental initiatives are often anintegral part of quality programs (Karapetrovic and Willborn, 1998; Molina-Azorın et al.,2009a; Roy et al., 2001).

Some small and medium manufacturers have chosen to examine the environmentalimpacts of their decisions about product design, process design and operationalprocedures as part of their efforts toward quality improvement. Others have decided tobuild on these capabilities and implement formal programs such as the ISO 14001 standardto explicitly address environmental concerns. While both approaches could prove useful inaddressing environmental issues, little is known about the characteristics of the SMEswho are pursuing quality and environmental performance goals simultaneously, and theconsequences of this particular option for organizational performance (Karapetrovic, 2002;Karapetrovic and Willborn, 1998; Husband and Mandal, 1999). Indeed, although there aresimilarities and synergies between quality assurance and environmental programs,environmental performance is increasingly being considered as a separate and distinctcompetitive priority in the manufacturing strategy literature (Ambec and Lanoie, 2008;de Burgos-Jimenez and Cespedes Lorente, 2001). In addition, because competitive prioritiesguide the pattern of strategic decisions and choices in specific directions, attempting toaddress multiple priorities simultaneously may involve trade-offs and compromises,potentially affecting performance (Skinner, 1969; Wheelwright, 1984). Bureaucraticproblems potentially impacting organizational efficiency and effectiveness may alsoarise in companies who choose to seek certification for both quality and environmentalmanagement systems (EMS) (Molina-Azorın et al., 2009a; Zeng et al., 2005, 2007).

This study focuses on SMEs that are simultaneously pursuing quality andenvironmental objectives. The study sample was comprised of 254 Canadian SMEswith ISO 9000 certification only (182 SMEs) or with both ISO 9000 and 14000certifications (72 SMEs). Specifically, we examined whether there were significantdifferences between both groups in terms of:

. specific motivations and resources;

. the types of initiatives implemented; and

. elements of organizational performance.

In order to get more insight into potential differences between both groups, we alsoperformed correlation and regression analyses to examine relationships betweenvariables for each group. Main results highlighted significant differences between SMEsholding both the ISO 9000 and 14000 certifications and those holding only the 9000ISO certification. Each group was shown to have distinct motivations and resources andto have implemented different types of initiatives to address environmental concerns.The results also demonstrated that each group was positively correlated with differentfacets of organizational performance.

An examination of these issues should provide guidance to managers as they tryto integrate environmental issues into their decision-making processes. With manystudies suggesting that there are significant benefits to being proactive on theseissues (Clemens, 2006; Lefebvre et al., 2003; Simpson et al., 2004), it is essential for SMEs

Quality andenvironmental

performance

31

to leverage or develop the appropriate capabilities, initiatives, and behaviours to addressenvironmental concerns. Although there is a growing body of literature on SMEs andenvironmental management (del Brıo and Junquera, 2003; Hillary, 2000, 2003; Miles et al.,1999; Hitchens et al., 2003; McKeiver and Gadenne, 2005), our knowledge about thesespecific issues is still fragmented. Also, studies on the ISO 9000 and ISO 14000 standardstypically focus on the integration process of these management systems andcomparisons between the two standards in terms of potential motivation factors,benefits, or international diffusion (Karapetrovic and Willborn, 1998; Poksinska et al.,2003; Casadesus et al., 2008; Albuquerque et al., 2007). The motivations, resources,initiatives and impacts on performances of SMEs holding both the ISO 9000 and 14000standards have clearly remained under explored. This study thus contributes to theliterature by shedding light on the motivations and consequences of integrating both theISO 9000 and ISO 14000 standards. Furthermore, few studies have focused explicitlyon the type of environmental initiatives certified SMEs have implemented. In thisstudy, we characterized environmental initiatives both broadly and explicitly, includingthose associated with product and process modifications and the supporting managerialactivities, as well as individual, voluntary and informal activities associated withorganizational citizenship behaviors (OCBs). Defined as actions that are “discretionary,not directly or explicitly recognized by the formal reward system” (Organ et al., 2006,p. 3), OCBs are particularly relevant to discussions of environmental initiatives. Studiesof environmental management have been essentially focused on decisions frommanagers and formal management systems: policy, objectives, pollution preventionprograms, strategies, sustainability reports, etc. As a result, the role of unplanned,discretionary and informal initiatives in the workplace has been largely overlooked.However, such can play an essential role in the greening process of organizations(Daily et al., 2009; Ramus and Killmer, 2007; Boiral, 2009), particularly in the smallbusiness context, where the influence of the company’s owner/manager is crucial andpresent throughout the entire organization (Naffziger et al., 2003; Schaper, 2002).

The article first presents a brief literature review and conceptual framework.Sections 2 and 3 present the methodological aspects and the main results, respectively.A discussion of the results and their implications for future research and managerialpractices is presented in the last section.

2. Literature review and conceptual frameworkAlthough often under less scrutiny from environmental groups than are largercorporations, SMEs are also under pressure to improve environmental performance.Yet, while the largest companies have begun integrating environmental managementinto their corporate strategy, studies show that small businesses are lagging behind inthis respect (Darnall et al., 2010; Revell and Rutherford, 2003; Worthington and Patton,2005). Significant differences exist among small businesses in terms of organizationalculture, planning processes and resource availability (Darnall and Edwards, 2006;Darnall et al., 2010; Battisti and Perry, 2011). These differences may influence theunderlying motivations to improve environmental performance and the type ofenvironmental solutions considered, as well as their implementation (Masurel, 2007;Gadenne et al., 2009; Schaper, 2002; Dean et al., 1998). In order to examine these issues, andto provide guidance to companies examining whether and how to address environmentalissues, we developed a conceptual framework that focuses on three elements:

BPMJ19,1

32

the organizational context of the SMEs, their environmental initiatives and theirperformance. As shown in Figure 1, we examined whether SMEs that have decided tofocus on both quality and environmental objectives differed significantly from thosepursuing only quality objectives in terms of these three elements. Because of thesimilarities between quality and environmental objectives, and because environmentalinitiatives are becoming less and less separable from activities that target productivityand quality improvement (Karapetrovic, 2002; Husband and Mandal, 1999; Boiral, 2011),both types of companies should be examined to identify specific differences.

The impacts of pursuing quality and environmental performance can be analyzedthrough the ISO 9000 and ISO 14000 certification, which have been adopted by more than1 million organizations around the world (International Organization for Standardization,2009; Boiral, 2011). We compared the organizational characteristics (size, motivation andinternationalization), environmental initiatives (operations, managerial, accounting andOCBs) and performance (financial, environmental and innovation) of SMEs with ISO 9000certification to those with both ISO 9000 and 14000 certification.

2.1 Organizational contextSeveral aspects of the organizational context of SMEs can impact their level ofenvironmental responsiveness. Because they are strong drivers of environmentalperformance, we examined the size, underlying motivations and level ofinternationalization of each company included in the study. As mentioned, it has beenreported that larger corporations have made more progress in environmentalmanagement and that they are more likely to implement the technologies, programsand systems needed to improve environmental performance (Darnall et al., 2010; Hillary,2000; Revell and Rutherford, 2003; Worthington and Patton, 2005). Larger firms appearto have greater access to the knowledge and resources that allow them to integrateenvironmental concerns into their corporate activities. Furthermore, environmentalinvestments require long-term vision, but strategic management of SMEs is often orientedtoward short-term profitability, creating potential barriers to this type of investment(Dean et al., 1998; Lepoutre and Heene, 2006). In addition, unlike larger corporations,

Figure 1.Conceptual framework

Quality andenvironmental

performance

33

SMEs do not have planning personnel to contemplate strategic long-term issues likeenvironmental management (Haksever, 1996). Finally, compared to large organizations,SMEs generally have less standardized and formalized management practices (Lee andPalmer, 1999; Mintzberg and Quinn, 1991). From this perspective, SMEs do not seem wellequipped to take on the paperwork required by ISO certification (Boiral, 2003; Curkovicand Pagell, 1999).

While the efforts of SMEs to improve their environmental performance may bemotivated by environmental concerns and willingness to demonstrate a commitmentto environmental issues, they may also be motivated by strategic and business factors(Gadenne et al., 2009; Masurel, 2007; Dean et al., 1998). Several authors have suggestedthat environmental leadership can lead to competitive advantages through costreduction, increased market share or greater access to capital (Ambec and Lanoie, 2008;Molina-Azorın et al., 2009b; Porter and van der Linde, 1995). Some SMEs have startedto exploit this opportunity by developing more environmentally sensitive products andtechnologies that meet customer expectations, changes often facilitated by close clientrelations and increased customer focus (Preuss and Perschke, 2009; Dean et al., 1998).The globalization of markets has also helped promote greener manufacturingprocesses. Several studies have reported that increased international activities werepositively associated with environmental performance (Kennelly and Lewis, 2002;Gonzalez-Benito and Gonzalez-Benito, 2006). Specifically, the ISO 14000 certificationcan provide international firms with a competitive advantage among suppliers,creating an incentive to improve environmental performance (Bansal and Hunter, 2003;Bellesi et al., 2005; Kitazawa and Sarkis, 2000).

The arguments presented above suggest that the two groups we examined would beexpected to differ significantly on organizational variables. Indeed, these studies revealthat size, motivations, and internationalization are powerful determinants of thedecision to adopt the ISO 14000 standard (Bansal and Hunter, 2003; Bansal andBogner, 2002; Bellesi et al., 2005; Casadesus et al., 2008; Yin and Schmeidler, 2009;Kitazawa and Sarkis, 2000). Hence, we propose that these elements are also associatedwith companies that hold both standards. Specifically, we expect that SMEs which arecertified for both ISO 9000 and 14000 will be significantly and positively associatedwith greater size, stronger business and environmental motivation and higher levels ofinternationalization.

2.2 Environmental initiativesThe second component of our conceptual framework is environmental initiatives.As seen in Figure 1, we focused on four types of initiatives: modifications to theproducts/processes, managerial initiatives, environmental costing tools and OCBs.These types of initiatives were chosen because they provide the basis for a broadcharacterization of environmental initiatives that included specific modifications toproducts and processes and the supporting initiatives. They also allowed us to includeinformal individual initiatives. To improve their overall environmental performance,companies have implemented various measures and initiatives over the years. As manycompanies are moving away from end-of-pipe solutions toward pollution prevention,they are now examining the product’s life cycle including raw material acquisition,manufacturing and processing, use and reuse (Boiral, 2005; Darnall and Edwards, 2006;Oldenburg and Geiser, 1997). Other initiatives include the implementation of EMS

BPMJ19,1

34

to address environmental issues in a comprehensive manner (Biondi et al., 2000; Darnalland Edwards, 2006; McKeiver and Gadenne, 2005). An EMS generally includes thebasic elements of an overall management system covering organizational structure,planning activities, responsibilities and procedures. Such comprehensive systems assistcompanies in coordinating activities and motivating employees to implement theirenvironmental strategy (Melnyk et al., 2003; Yin and Schmeidler, 2009). Many haveargued that without a systematic, formal implementation process, the quality of thestrategy is likely to suffer and companies may not reap all the benefits associated withimproved environmental performance (Chavan, 2005; Melnyk et al., 2003; Yin andSchmeidler, 2009).

Environmental costing methodologies are also valuable supporting tools during boththe resource allocation process and tracking of the costs and benefits of environmentalactivities. Managers who comprehend the full scope of a product’s environmentalimpacts are often better equipped to make investments in pollution prevention, ratherthan looking only at the end of the pipe for solutions (Darnall and Edwards, 2006; Boiral,2005). Unfortunately, most companies acknowledge that they do not have a system thatadequately identifies and tracks past, current or future environmental costs (Darnalland Edwards, 2006; Epstein, 2008; Henri and Journeault, 2010). Thus, manyenvironmental costs are hidden in overhead and general administrative accounts, andno assignment is made to the activities or products that engendered those costs (Henriand Journeault, 2010). Some larger corporations have been experimenting with a numberof techniques that can help both with monetizing environmental externalities and withaccounting for uncertainty and risk, however few SMEs use such sophisticated capitalbudgeting techniques to analyze potential investments. Danielson and Scott (2006)report that the payback method is still the most popular budgeting approach and thatdecisions are often driven by an act of faith in a new technology or the perception of anopportunity. The choice of this method can be explained in part by factors such as lack offinancial expertise, short-term vision and shortage of capital. However, the use of suchmethods can create significant barriers to environmental investments, as they typicallyignore the time value of money (Epstein and Roy, 2000).

The last element we examined to characterize environmental initiatives relates tothe behaviour of the owner/manager. In the small business context, the influence of thecompany’s owner/manager is crucial and felt throughout the organization. Further,in the specific context of environmental management, study results confirm thatowner/managers play a predominant role in related decisions (Battisti and Perry, 2011;Darnall and Edwards, 2006; Perez-Sanchez et al., 2003). Accordingly, it is essential toexamine their attitudes and values toward environmental issues, and the behaviours theyexhibit or foster (Fassin et al., 2011; Gadenne et al., 2009; Lepoutre and Heene, 2006;Schaper, 2002). In order to measure some of these factors, we used the analyticalframework of OCBs, which is being increasingly used to study how motivations andbehaviours can impact organizational development. A number of such studies – focusingon individual behaviours that are discretionary and not explicitly recognized by theformal reward system – have demonstrated that citizenship initiatives can play a keyrole in improving organizational operations and effectiveness (MacKenzie et al., 1998;Organ et al., 2006; Podsakoff et al., 2000; Van Dyne et al., 1994). In a recent article, Boiral(2009) examined how this framework can be applied to the environmental practices oforganizations. Drawing attention to the fact that most studies in the environmental

Quality andenvironmental

performance

35

management literature center on formal, explicit and managerial responses to pressuresfor improved environmental performance, Boiral has suggested that the OCB frameworkmay be relevant to examining the role of individual and voluntary environmentalbehaviours in the workplace. Arguing that the development of preventive approachesrequires employee participation and voluntary pro-environmental behaviours in theworkplace, he proposed that these behaviours can play an essential role in organizationalgreening. He also suggested that OCBs can facilitate the implementation of formalmanagement systems requiring the active participation of all employees.

The arguments presented above suggest that the two groups of companies weexamined would be expected to differ significantly in terms of the environmentalinitiatives they have implemented. Indeed, these studies reveal that those types ofinitiatives are more likely to be associated with ISO 14000 certified companies, which issupposed to promote various environmental management practices (Melnyk et al., 2003;Potoski and Prakash, 2005; Hanna et al., 2000; Fielding, 1999; Shin and Chen, 2000).Hence, we propose that these initiatives are more likely to be associated with companiesthat hold both standards. Specifically, we expect that SMEs which are certified for bothISO 9000 and 14000 will be significantly and positively associated with each type ofenvironmental initiative (operations, managerial, accounting, and OCB) when comparedto those which hold ISO 9000 certification only.

2.3 Organizational performanceFinally, we examined whether there are significant differences in performance betweenthe two groups. The links between financial and environmental performance havebeen closely examined in the literature. While some have focused on the impact of aproactive environmental strategy on financial performance in order to examine thepossibilities for win-win approaches (Ambec and Lanoie, 2008; Molina-Azorın et al.,2009b; Porter and van der Linde, 1995; Christmann, 2000), others have examinedfinancial performance as a potential barrier to environmental investments (Drake et al.,2004; Boyd and McClelland, 1999; Lepoutre and Heene, 2006; Sharma, 2000).

There is much empirical evidence from both larger companies and SMEs that tendsto demonstrate that, beyond reducing the environmental impacts of their activities,environmental initiatives often result in increased productivity and innovation, which inturn lead to competitive advantages and improved financial performance (Ambec andLanoie, 2008; Clemens, 2006; Lefebvre et al., 2003; Molina-Azorın et al., 2009b). However,although these studies have underscored a significant relationship betweenenvironmental performance and financial performance, the precise nature and theimplications of this relationship still remain somewhat unclear (Roy et al., 2001;Aragon-Correa and Rubio-Lopez, 2007). Indeed, an alternative explanation could residewith the limitations that a company’s financial situation may impose on strategyformulation. A precarious financial situation may orient a company’s investments towardshort-term profitability, while solid financials may offer a greater capacity to absorb therisks and uncertainty related to proactive environmental strategies (Sharma, 2000).Furthermore, in the case of SMEs, the lack of financial resources has been identified as oneof the main barriers to engaging in social and environmental initiatives (Lepoutre andHeene, 2006; Miles et al., 1999).

An alternate view of these issues is provided by the manufacturing strategyliterature, where there is considerable debate about whether firms can efficiently focus

BPMJ19,1

36

on multiple priorities simultaneously. Certain authors have argued that becauseenvironmental performance can lead to competitive advantage, it should be considered atthe same level of strategic importance as other manufacturing objectives such as costs,quality, deliveries and flexibility (de Burgos-Jimenez and Cespedes Lorente, 2001). Inaddition, because competitive priorities guide the pattern of strategic decisions andchoices in specific directions, emphasizing multiple priorities simultaneously couldinvolve trade-offs and compromises which may potentially affect performance. However,some researchers have moved away from this model and have suggested that firms canachieve a balance among various priorities. This is in keeping with the cumulative orsynergies theory of performance, which suggests that companies can perform well onseveral levels simultaneously (Ferdows and De Meyer, 1990; Rosenzweig and Roth, 2004).Cumulative performance theorists would argue that improvements in one area ofperformance can reinforce capabilities in other areas and that firms do not have to choosebetween competitive objectives. For example, the promotion of environmental bestpractices such as pollution prevention technologies can develop capabilities contributingto innovation, cost-reduction and improvement of organizational effectiveness(Christmann, 2000). Moreover, similarities and reported potential synergies betweenenvironmental and quality management could help ISO 14001 certified firms build onquality experience for overall improved performance (Boiral, 2011; Poksinska et al., 2003;Pun et al., 1999; Zeng et al., 2005, 2007). However, it has been reported that ISO certificationis often accompanied by more paperwork (Boiral, 2003, 2011; Walgenbach, 2001).Bureaucratic problems could arise in companies that choose to seek certification for bothquality and EMS. Implementing both ISO 9000 and ISO 14001 requires duplication ofmany management tasks, which could impact the efficiency and effectiveness of theorganization (Molina-Azorin et al., 2009a; Zeng et al., 2005).

However, generally speaking, the implementation of ISO 14001 has been associatedin the literature with improvements of environmental, innovation, and economicperformance (Standards Council of Canada, 2000; Melnyk et al., 2003; Potoski andPrakash, 2005; Pun and Hui, 2001). Consequently, we expect that SMEs that are certifiedfor both management systems will be significantly associated with greater levels ofenvironmental, financial and innovation performance.

3. Methodology3.1 Sample and data collectionGiven the growing number of companies certifying to either or both ISO 9000 andISO 14000 standards, we were able to proceed with an empirical study that focuses onthese companies. This study gathered data from a sample of 254 ISO 9000 and ISO 14000certified Canadian SMEs, to characterize differences between SMEs that are certified forboth management systems and those that hold ISO 9000 certification. Data collectionwas based on a survey questionnaire sent to a random sample of 1,514 companies listedin the Scott’s Directory database. Only ISO certified (either ISO 9000 or ISO 14000)manufacturing facilities with 20 employees or more were selected from the originallist. The pre-tested questionnaire was sent to the highest member of the managementteam. A total of 319 usable questionnaires were received, for a response rate of21.1 percent. However, because the focus of this study was on SMEs, companies withmore that 500 employees (65 companies) were not considered for further analysis, givinga final sample size of 254 responding SMEs.

Quality andenvironmental

performance

37

3.2 Research variablesOrganizational context

(1) Size. The company size was measured based on the number of employees.

(2) Motivation. A list of seven possible motivations found in the literature waspresented to the respondents. Using Likert-type scales (where 1 – no influence atall and 5 – very strong influence), the respondents were asked to indicate the extentto which each possible motivation influenced their environmental commitment.Principal-components factor analyses were conducted to assess theunidimensionality on construct scales. These analyses resulted in two distinctconstructs:. environmental motivation, including items related to environmental

concerns and public demonstration of commitment; and. business motivation, including items related to business imperatives.

Table I presents a complete list of items included in each construct and theassociated reliability measures.

(3) Internationalization. Respondents were asked to indicate the percentage of theirforeign sales.

Environmental initiatives. Operations. Using a list adapted from Melnyk et al. (2003), respondents were asked

to indicate to what extent each environmental initiative had been implemented(Likert-type scales, where 1 – not at all and 5 – to a great extent).

. Managerial. A list of statements related to typical requirements for an EMS waspresented to respondents and they were asked to indicate to what extent eachenvironmental initiative had been implemented (Likert-type scales, where 1 – notat all implemented and 5 – fully implemented).

. Environmental cost tracking (accounting). A list of items adapted from theInternational Guidance Document of Environmental Management Accounting(IFAC, 2005) and the work of Parker (1999) was presented to the respondents andthey were asked to indicate the extent to which each listed environmental costwas explicitly tracked by their organization (Likert-type scales, where 1 – not atall to 5 – to a great extent).

. Environmental OCB. A list of statements adapted from Boiral (2009) was presentedand respondents were asked to indicate whether these statements accuratelydescribed their conduct with respect to environmental issues inside theirorganization (Likert-type scales, where 1 – totally disagree to 5 – totally agree).

Performance variables. Environmental. Using a Likert-type scale (1 – much worse, 5 – much better),

respondents were asked to rate their environmental performance (over the pastthree years) relative to others in their industry on items adapted from Judge andDouglas (1998).

. Financial. Using a Likert-type scale (1 – much worse, 5 – much better), respondentswere asked to rate their financial performance (over the past three years) relativeto others in their industry on items adapted from Judge and Douglas (1998).

BPMJ19,1

38

Variables Items a

Environmentalmotivation

Public demonstration of environmental stewardship 0.77Reducing environmental impacts and pollutionTop managers’ social responsibility and ethical concernsDemonstrating environmental leadership in our industry

Business motivation Increasing shareholder value 0.72Customer requirementGreater access to capital

Operation activities Redesigning product/process to eliminate potential environmentalproblems

0.77

Replacing a material that may cause environmental problems with amore ecological materialReducing the use of environmentally sensitive materials/componentswithin your processes/products

Managerial activities Publishing an environmental policy 0.81Determining specific targets for environmental performancePublishing an annual environmental reportUsing an environmental management systemDetermining environmental criteria for purchasing decisionsMaking employees more responsible for the environmental performanceMonitoring environmental performance

OCB I help employees understand our environmental problems 0.89I am volunteer for projects, initiatives or events related to ourenvironmental issuesI propose new practices that improve our environmentalperformanceI undertake environmental initiatives that enhance our imageI participate actively in environmental eventsI perform voluntary environmental actions and initiatives in my dailyactivities

Environmentalcosting

Regulatory costs(permits, fines, consultant fees, legal costs)

0.82

Recycling and waste disposal costsRemediation costsEfficiency control costsEnvironmental management and control system costsLess tangible costs (e.g. potential future liability, company image)

Environmentalperformance

Regulatory compliance 0.87Environmental impactsManagement environmental riskWater pollutionAir emission levelsGreenhouse gas (GHG) emissionsOverall environmental performance

Financialperformance

Sales growth 0.88ProfitsReturn on sales

Notes: Statistical reliability was assessed by computing the Cronbach’s a; Ahire and Devaraj (2001)recommend a threshold of 0.50 for emerging construct scales and 0.70 for maturing constructs;principal-components factor analyses were conducted to assess unidimensionality on construct scales;for each cases, only one factor explained variance

Table I.Construct items and

reliability

Quality andenvironmental

performance

39

. Innovation. Respondents were asked whether or not, during the last three years,they introduced any new or significantly improved products (goods or services)on the market.

4. Results4.1 t-tests analysesUsing the statistical program SPSS, analyses were performed on a sample consistingof 254 SMEs, which ranged from 25 to 500 employees (mean ¼ 208.2; standarddeviation ¼ 118.2). The sample was first divided into two groups according to their typeof ISO certification. The first group consisted of SMEs that were ISO 9000 certified only(n ¼ 182) and the second group included SMEs that held both ISO 9000 and ISO 14000certification (n ¼ 72). Independent samples t-tests and cross tabulations were thenconducted to examine potential significant differences between the two groups.

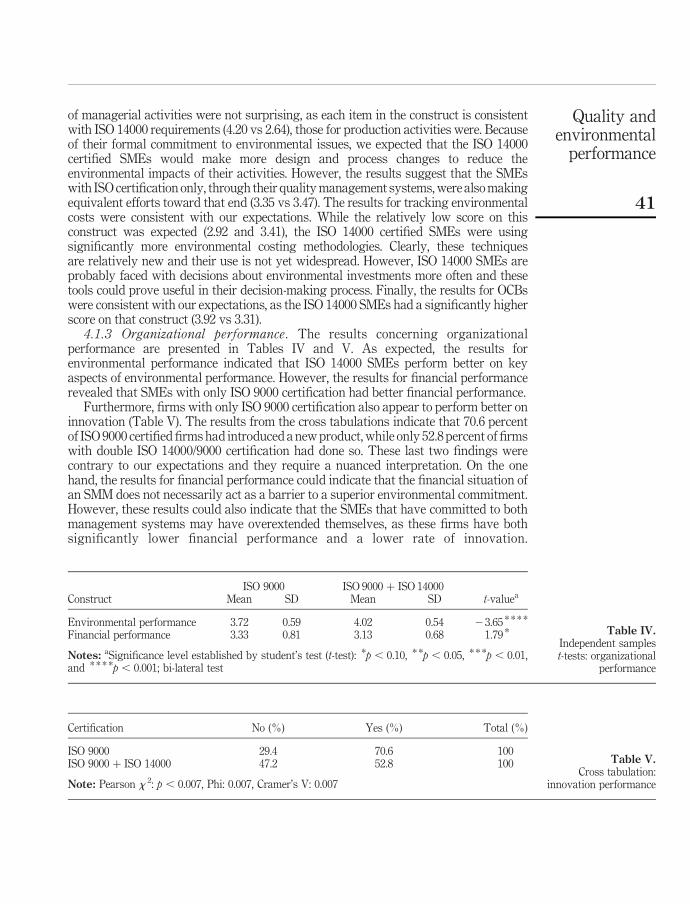

4.1.1 Organizational context. As shown in Table II, the two groups differedsignificantly on several variables related to the firm’s organizational context. The resultsconcerning the level of internationalization and the number of employees are certainlyconsistent with our expectations and confirm that these factors are positive forcestoward a greener process. SMEs with both ISO certifications were indeed larger firms(average number of employees, 242.92) and their percentage of foreign sales was alsomuch higher (65.68 percent). However, the results about underlying motivations forreducing the environmental impacts of business activities were not completely consistentwith our expectations. While the companies with both ISO certifications did report higherlevels of environmental motivation (4.00 vs 3.56), surprisingly, they did not reportsignificantly higher levels of business motivation.

4.1.2 Environmental initiatives. The results concerning the environmental initiativesimplemented by the SMEs are presented in Table III. While the results for implementation

ISO 9000 ISO 9000 þ ISO 14000Construct/variable Mean SD Mean SD t-valuea

Business motivations 2.97 1.02 2.99 0.98 20.010Environmental motivations 3.56 0.87 4.00 0.58 24.60 * * * *

Percentage of foreign sales 44.89 30.84 65.68 30.37 24.26 * * * *

Number of employees 195.02 116.02 241.92 117.99 22.89 * * *

Notes: aSignificance level established by student’s test (t-test): *p , 0.10, * *p , 0.05, * * *p , 0.01,and * * * *p , 0.001; bi-lateral test

Table II.Independent samplest-tests: organizationalcontext

ISO 9000 ISO 9000 þ ISO 14000Construct Mean SD Mean SD t-valuea

Operations activities 3.35 0.95 3.47 0.71 21.22Managerial activities 2.64 1.01 4.20 0.53 216.07 * * * *

Environmental accounting 2.92 0.94 3.41 0.76 24.67 * * * *

OCB 3.31 0.97 3.92 0.59 25.94 * * * *

Notes: aSignificance level established by student’s test (t-test): *p , 0.10, * *p , 0.05, * * *p , 0.01,and * * * *p , 0.001; bi-lateral test

Table III.Independent samplest-tests: environmentalinitiatives

BPMJ19,1

40

of managerial activities were not surprising, as each item in the construct is consistentwith ISO 14000 requirements (4.20 vs 2.64), those for production activities were. Becauseof their formal commitment to environmental issues, we expected that the ISO 14000certified SMEs would make more design and process changes to reduce theenvironmental impacts of their activities. However, the results suggest that the SMEswith ISO certification only, through their quality management systems, were also makingequivalent efforts toward that end (3.35 vs 3.47). The results for tracking environmentalcosts were consistent with our expectations. While the relatively low score on thisconstruct was expected (2.92 and 3.41), the ISO 14000 certified SMEs were usingsignificantly more environmental costing methodologies. Clearly, these techniquesare relatively new and their use is not yet widespread. However, ISO 14000 SMEs areprobably faced with decisions about environmental investments more often and thesetools could prove useful in their decision-making process. Finally, the results for OCBswere consistent with our expectations, as the ISO 14000 SMEs had a significantly higherscore on that construct (3.92 vs 3.31).

4.1.3 Organizational performance. The results concerning organizationalperformance are presented in Tables IV and V. As expected, the results forenvironmental performance indicated that ISO 14000 SMEs perform better on keyaspects of environmental performance. However, the results for financial performancerevealed that SMEs with only ISO 9000 certification had better financial performance.

Furthermore, firms with only ISO 9000 certification also appear to perform better oninnovation (Table V). The results from the cross tabulations indicate that 70.6 percentof ISO 9000 certified firms had introduced a new product, while only 52.8 percent of firmswith double ISO 14000/9000 certification had done so. These last two findings werecontrary to our expectations and they require a nuanced interpretation. On the onehand, the results for financial performance could indicate that the financial situation ofan SMM does not necessarily act as a barrier to a superior environmental commitment.However, these results could also indicate that the SMEs that have committed to bothmanagement systems may have overextended themselves, as these firms have bothsignificantly lower financial performance and a lower rate of innovation.

Certification No (%) Yes (%) Total (%)

ISO 9000 29.4 70.6 100ISO 9000 þ ISO 14000 47.2 52.8 100

Note: Pearson x 2: p , 0.007, Phi: 0.007, Cramer’s V: 0.007

Table V.Cross tabulation:

innovation performance

ISO 9000 ISO 9000 þ ISO 14000Construct Mean SD Mean SD t-valuea

Environmental performance 3.72 0.59 4.02 0.54 23.65 * * * *

Financial performance 3.33 0.81 3.13 0.68 1.79 *

Notes: aSignificance level established by student’s test (t-test): *p , 0.10, * *p , 0.05, * * *p , 0.01,and * * * *p , 0.001; bi-lateral test

Table IV.Independent samplest-tests: organizational

performance

Quality andenvironmental

performance

41

Clearly, these results may add to the debate over the existence of trade-offs betweenenvironmental protection and corporate competitiveness. Indeed, they do not supportthe win-win rationale, in which a commitment to environmental protection could alsotranslate into superior financial performance or greater innovation. However, ourfindings could also reflect the increased bureaucracy and reduced flexibility oftenassociated with ISO managements systems. Hence, the double certification may haveproven problematic for those SMEs.

4.2 Correlation and regression analysesIn order to gain more insight into potential differences between both groups, we alsoexamined relationships among variables for each group by performing correlation andregression analyses (business motivations and operations activities were not includedin these analyses, as t-tests revealed that they were not statistically significant).

Table VI provides correlations among the variables (means and standard deviationsare provided in Tables II-IV). Of the 28 correlations, 13 are significant for the ISO 9000group, only five are significant for the ISO 9000 þ ISO 14000 group. Significantcorrelations range from r ¼ 0.17, p , 0.05 to r ¼ 0.54, p , 0.01 for the ISO 9000 group,and from r ¼ 0.24, p , 0.05 to r ¼ 0.37, p , 0.01 for the ISO 9000 þ ISO 14000 group.These results suggest a stronger association between all environmental initiatives(managerial, environmental accounting, and environmental OCB) in the case of SMEs thathave a single certification. In the case of this particular group, results also indicate thatenvironmental motivation is strongly correlated with these environmental initiatives.

The variance inflation factor (VIF) test was used to detect possible multicollinearityamong variables. Data indicate the absence of multicollinearity if the VIF value rangesbetween 0.10 and 10 (Neter et al., 1989). In our study, the VIF value ranges, for the

1 2 3 4 5 6 7 8

ISO 9000 group1. Size2. Env. motivation 0.033. Internalization 0.10 0.114. Managerial 0.09 0.25 * * 0.035. Accounting 0.00 0.42 * * 0.12 0.54 * *

6. OCB 0.08 0.21 * * 0.06 0.36 * * 0.45 * *

7. EP 0.17 * 0.07 0.10 0.29 * * 0.36 * * 0.46 * *

8. FP 20.03 20.07 0.03 0.09 0.23 * * 0.18 * 0.17 * –ISO 9000 þ 14000 group1. Size2. Env. motivation 20.013. Internalization 0.37 * * 0.084. Managerial 0.04 20.04 0.155. Accounting 20.08 0.10 20.05 0.28 *

6. OCB 20.08 0.07 0.26 0.09 0.097. EP 20.31 * * 20.10 0.02 0.30 * * 0.24 * 0.108. FP 0.07 20.17 20.03 0.02 0.19 0.18 0.17 –

Notes: Significant at: *p , 0.05 and * *p , 0.01; EP – environmental performance; FP – financialperformance

Table VI.Correlation matrix

BPMJ19,1

42

ISO 9000 group, from 1.22 (environmental motivation) to 1.72 (environmentalperformance), and for the ISO 9000 þ ISO 14000 group from 1.04 (internalization) to1.92 (accounting).

Hierarchical regressions were performed to analyze relative contributions oforganizational elements and environmental initiatives to both environmental andfinancial performance. While in Step 1, size, motivation, and internalization wereintroduced as SME characteristics, in Step 2, managerial, accounting, and OCB wereintroduced as environmental initiatives.

The results of the regression analysis for environmental performance are reported inTable VII. Whereas organizational context elements (size, motivation, and internalization)entered together at Step 1 failed to explain a significant amount of variance for theISO 9000 group, R 2 ¼ 0.04, F(3,122) ¼ 1.75, ns, organizational context elements explaina significant amount of variance for the ISO 9000 þ ISO 14000 group, R 2 ¼ 0.18,F(3,119) ¼ 3.29, p , 0.05. Environmental initiatives entered at Step 2 produced asignificant change in explained variance for the ISO 9000 group, DR 2 ¼ 0.24,F(3,122) ¼ 7.96, p , 0.000, and for the ISO 9000 þ ISO 14000 group, DR 2 ¼ 0.11,F(3,119) ¼ 2.86, p , 0.05. In addition, while size and motivation are related negatively(b ¼ 20.39, p ¼ 0.009) and positively (b ¼ 0.30, p ¼ 0.04) to environmental performanceonly for the ISO 9000 þ ISO 14000 group, no relationship was found for internalization.Finally, while managerial is not related to environmental performance for neithergroups, accounting (b ¼ 0.21, p ¼ 0.04) and OCB (b ¼ 0.33, p ¼ 0.000) are related toenvironmental performance only for the ISO 9000 group. Hence, among theseenvironmental initiatives, these last two seem to be powerful drivers of environmentalperformance for the ISO 9000 group.

The results of the regression analysis for financial performance are reported inTable VIII. Whereas organizational context elements (size, motivation, and internalization)entered together at Step 1 failed to explain a significant amount of variance for theISO 9000 group, R 2 ¼ 0.00, F(3,43) ¼ 0.38, ns, and for the ISO 9000 þ ISO 14000 group,R 2 ¼ 0.06, F(3,40) ¼ 1.05, ns. Environmental initiatives entered at Step 2 produced

ISO 9000 ISO 9000 þ ISO 14000b t-value b t-value

Organizational contextSize 0.16 1.854 20.39 * * 22.710Motivation 0.05 0.651 0.30 * 2.082Internalization 0.07 0.825 20.10 20.758R 2 0.04 0.18Test F 1.75 3.29 *

Environmental initiativesManagerial 0.10 1.103 0.20 1.356Accounting 0.21 * 2.204 0.18 1.273OCB 0.33 * * * 3.732 0.09 20.672R 2 0.286 0.296DR 2 0.245 0.112Test F 7.96 * * * 2.86 *

Notes: Significant at: *p , 0.05, * *p , 0.01, and * * *p , 0.000; b – standardized coefficients

Table VII.Results for environmental

performance

Quality andenvironmental

performance

43

a significant change in explained variance only for the ISO 9000 group, DR 2 ¼ 0.11,F(3,40) ¼ 4.99, p ¼ 0.02, and failed to explain a significant change for theISO 9000 þ ISO 14000 group. In addition, for the ISO 9000 group, and the ISO 9000sample þ ISO 14000 group size (b ¼ 20.08, ns;b ¼ 20.08, ns), motivation (b ¼ 0.05, ns;b ¼ 20.04, ns) and internalization (b ¼ 20.02, ns; b ¼ 20.22, ns) are not related toorganizational performance. Finally, while managerialb ¼ 20.12, ns;b ¼ 20.00, ns) andOCB (b ¼ 0.10, ns; b ¼ 0.25, ns) are not related to organizational performance for eithergroups, accounting (b ¼ 0.35, p ¼ 0.003) is related to financial performance for theISO 9000 group only.

5. Discussion and conclusionAlthough pressures for improved environmental performance continue to intensify,our knowledge of the resources and initiatives that could prove beneficial for SMEs intheir efforts to develop and implement appropriate environmental strategies remainssomewhat limited. Companies now need to develop appropriate skills and otherresources to address these new challenges and reap the potential benefits associatedwith a proactive environmental strategy. Attempts to gain a better understanding ofthese issues are thus helpful for both researchers and practitioners. This studydemonstrates that SMEs that have decided to pursue both quality and EMS arecorrelated with specific context and performance variables and have implementeddifferent types of initiatives when compared to SMEs that have implemented a qualitymanagement system only. However, the results of our analysis were not consistentwith all of our expectations.

First, with respect to context variables, the results confirm that size andinternationalization are indeed positive forces toward environmental responsiveness.Nonetheless, the results indicate that ISO 14000 certification was not associated withhigher levels of business motivation, raising questions about potential missedopportunities. There is evidence in the literature suggesting that formal EMS arecorrelated with many facets of operational efficiency and increased profitability

ISO 9001 ISO 9000 þ ISO 14000b t-value b t-value

Organizational contextSize 20.08 20.966 20.08 20.529Motivation 0.05 0.554 20.04 0.258Internalization 20.02 20.222 20.22 21.534R 2 0.00 0.06Test F 0.38 1.05Environmental initiativesManagerial 20.12 21.116 20.00 20.016Accounting 0.35 * * 3.006 0.24 1.524OCB 0.10 1.095 0.25 1.586R 2 0.120 0.180DR 2 0.111 0.111Test F 4.99 * * 1.46

Notes: Significant at: p , 0.05 and * *p , 0.01; b – standardized coefficients

Table VIII.Results for financialperformance

BPMJ19,1

44

(Melnyk et al., 2003; Molina-Azorin et al., 2009; Kitazawa and Sarkis, 2000; Miles et al.,1999). Hence, the ISO 14001 standard could bring about improvements that extendfar beyond the management of a firm’s environmental impacts and the publicdemonstration of environmental stewardship (Standards Council of Canada, 2000;Potoski and Prakash, 2005; Bansal and Bogner, 2002; Boiral, 2011). Second, the resultsconcerning environmental initiatives and behaviours reveal that SMEs that were alsocertified for the environmental standard scored significantly higher on most types ofinitiatives. However, similar scores for production activities raise questions aboutthese SMEs’ actual commitment to environmental issues. These results could alsoindicate that quality managements systems are indeed a good vehicle for the integrationof environmental issues. Our results certainly confirm the strong similarities andpossible synergies between both types of management systems (Karapetrovic andWillborn, 1998; Poksinska et al., 2003; Boiral, 2011). The results for supportingmanagerial activities, environmental costing tools and OCBs were consistent with ourexpectations. The specific results for OCBs demonstrate that environmental OCBsshould not be regarded as simply an alternative to explicit management practices, asthey can coexist with more formal systems such as the ISO 14001 standard. Moreover,our results indicate that the explicit management practices associated with the ISO 14001standard can encourage the emergence of voluntary and non-rewarded initiatives.Generally speaking, our results are consistent with initial expectations and the emergingliterature on the importance of OCB for improving environmental practices (Daily et al.,2009; Ramus and Killmer, 2007; Boiral, 2009; Boiral and Paille, 2012). In addition, ourresults suggest that the ISO 14001 standard also encourages tracking of environmentalcosts, as this certification was correlated with a significantly higher score on thatconstruct. Further, for those SMEs that were certified to the ISO 9000 standard only,correlation analyses certainly highlighted a strong association between three of the fourenvironmental initiatives (OCB, environmental accounting, managerial activities).These results suggest that these SMEs are also committed to the implementation of keyprocesses and activities to support their efforts.

Finally, the results for the performance variables were not all consistent with ourexpectations. In the case of environmental performance, our t-tests revealed a positive andsignificant correlation between SMEs with the double certification and environmentalperformance. Furthermore, when examining what specific environmental initiativeswere positively associated with environmental performance, regression analysis resultspointed to two specific ones in the case of ISO 9000 SMEs (environmental accounting andenvironmental OCB). As for the ISO 14000 þ ISO 9000 group, we were not able to identifyspecific initiatives, as results were not statistically significant.

Regarding results about innovation and financial performance, we found that onlyISO 9000 SMEs had superior financial and innovation performance. The surprising resultsregarding a possible link to financial performance certainly add to the debate aboutwhether and how environmental management can contribute to corporate performance(Ambec and Lanoie, 2008; Porter and van der Linde, 1995; Christmann, 2000; Drake et al.,2004). Regressions analyses have shed some light into these results by highlighting,in the case of the ISO 9000 group, a strong association between environmental accountinginitiatives and financial performance. Again, our results underscore the importance ofthese particular initiatives as part of an overall environmental strategy.

Quality andenvironmental

performance

45

Although our analysis does not allow us to identify the precise nature of the linksbetween environmental initiatives and financial performance, it raises questions aboutthe ability of SMEs to pursue both quality and environmental objectives simultaneously.However, these results must undoubtedly be interpreted in the context of this study,which deals with SMEs that have decided to pursue these objectives by certificationfor both standards. As such, our results point to the potential difficulties associated withthe integration of both standards. Obviously, the increased bureaucracy and lack offlexibility often denounced by certain studies on ISO certification (Boiral, 2003, 2011;Walgenbach, 2001) could partly explain our results.

The overall results of this study demonstrate that significant differences existbetween SMEs with single or double certification, and that context variables andperformance variables can shape decisions about environmental management.Consequently, this study’s findings contribute to the environmental and SMEliterature on this very complex topic by providing relevant empirical evidence based onprimary data. We make the following contributions to the literature. First, this studyprovides a detailed characterization of environmental initiatives, drawing on insightsderived from the environmental, accounting and management literature. By using theanalytical framework of organizational citizenship behaviours, our characterizationalso included informal and behavioural aspects often neglected in environmentalmanagement studies. While formal and explicit measures are indispensable in dealingwith environmental issues, they tend to overlook the human aspects of environmentalactions (Boiral, 2009). Second, by focusing on these two groups, we were able to drawattention to the specific case of manufacturing SMEs that hold both certifications andhow they compare to those that only hold the ISO 9000 certification. Although moreand more organizations across the world adopt both ISO 14000 and ISO 9000 standards(Standards Council of Canada, 2000), the implications of integrating simultaneouslythese two standards have remained largely unexplored. The few studies focused on bothISO 9000 and ISO 14000 have explored the technical similarities between these twostandards (Karapetrovic and Willborn, 1998), the comparison of their benefits and keysuccess factors (Poksinska et al., 2003; Boiral, 2011) and their international diffusionprocess (Casadesus et al., 2008; Albuquerque et al., 2007). Nevertheless, the ins and outsof adopting both ISO 14000 and ISO 9000 standards have clearly been ignored in theliterature. This study makes a contribution to this emerging literature by providingmuch needed empirical evidence about specific elements that characterize theorganizational context, the environmental initiatives, and organizational performanceof these manufacturing SMEs that hold both standards and have highlighted potentialavenues leading to improved environmental and financial performance.

The results of this study will also have implications for management and should helpprovide guidance to SMEs currently examining how to address environmental issues.SMEs need to address these issues carefully and understand the potential trade-offs andconsequences associated with their decisions. First, it would seem appropriate for firmsto take better advantage of the synergies between quality management systems andenvironmental management. Our results suggest that quality management systemsseem to be a good vehicle for profiting from such synergies. Within their existingmanagement systems, ISO 9000 certified SMEs have indeed made comparable changes totheir products and processes in order to reduce the environmental impacts of theirmanufacturing activities. This similarity can be explained by the evolution in the

BPMJ19,1

46

approaches to environmental management. While in the past these approaches focusedon palliative measures, currently initiatives increasingly tend to try to minimizeenvironmental impacts before production is completed and are progressively lessseparable from activities targeting improved productivity and competitiveness, such astotal quality management (Darnall and Edwards, 2006; Oldenburg and Geiser, 1997;Christmann, 2000; Boiral, 2005).

Second, the overall low mean scores on environmental accounting suggest that somethought should be devoted to implementing appropriate systems to track environmentalcosts. Indeed, our results have shown strong links between environmental accountingand both financial and environmental performance for the ISO 9000 group. Improvinginvestment decisions for environmental projects is becoming increasingly important forall companies, as improved environmental performance may require major investmentsin newer and cleaner technologies. In the case of SMEs, the limited use of environmentalcosting tools may create significant barriers to a better understanding of environmentalissues and their long-term impacts on profitability. While some of the more complextechniques used to assess environmental costs may be inappropriate, considering thelikely benefits of the analysis compared to the likely cost of accumulating and analyzingnecessary data, SMEs should strive to improve their current decision-making processesto more effectively incorporate the long-term costs and benefits of their decisions. Third,consideration should be given to the various ways environmental OCBs can be promotedwithin organizations. Our results reveal that top managers/owners of theISO 14000 þ ISO 9000 certified SMEs exhibited more of these behaviours within theirorganization. Since the behaviour of the leadership further encourages environmentalinitiatives throughout the entire organization, they are important to mobilizingemployees toward reducing the company’s environmental impact. Also, results fromregression analyses revealed that OCBs were positively associated with environmentalperformance in the case of the ISO 9000 group. These results indicate that formal EMSsuch as the ISO 14000 system are not a prerequisite for OCBs, as various factors canfavour their development (Boiral, 2009; Daily et al., 2009; Ramus and Killmer, 2007).Indeed, the development of a pro-environmental culture, implementation of voluntaryprograms, and appropriate training and information can all contribute to a favourablecontext for OCBs and should be considered by SMEs as relevant means to improveenvironmental performance (Boiral, 2009).

Although this study enhances our knowledge of the challenges and consequencesassociated with decisions regarding environmental issues, the results obtained mustbe interpreted in the context of the study’s limitations. First, the study relies heavily onperceptual measures. Although perceptual measures are often used in the managementliterature (Ketokivi and Schroeder, 2004), perceptions may also lead to bias. Second,this study focuses on Canadian SMEs. Given the importance of the regulatoryenvironment in environmental decisions, caution should be exercised when generalizingto non-Canadians firms; cross-country comparative analyses could help identifypotential differences. Third, because there are fewer companies that hold bothcertifications, analyses were done using different sample sizes. Clearly, as the number ofcompanies that hold both certifications increases (Standards Council of Canada, 2000;Boiral, 2011), it would be important to examine this topic while using comparablesamples. Lastly, our analysis does not take into account the level of integration of the

Quality andenvironmental

performance

47

management systems when companies were certified for two standards. The natureof such integration could prove critical to the effective both objectives.

This study’s findings and limitations point to several interesting avenues for futureresearch. Clearly, the examination of the nature of the integration of both managementsystems still requires much investigation. Studies about the specific impacts of theintegration of management systems on environmental, quality and financialperformance would be valuable. Such studies would allow us to identify specificareas of improvement for the SMEs. Undoubtedly, with both ISO standards becomingbusiness requirements for many organizations, there may be a temptation to implementthe standard without consideration to the broader, strategic perspective. Some SMEsmay implement the standard simply to be certified by a potential third party and meet aspecific customer requirement or improve their public image. SMEs that implement thestandard with such limited goals do so with minimum disruption to the organization. Inthis case, the management systems are not well integrated throughout the organizationand any potential benefits could go unnoticed. Future research could explore this issuethrough qualitative studies in order to analyze in depth the challenges and successfactors of adopting both ISO 9000 and ISO 14000 standards: internalization of thesestandards, employees mobilization, documentation management, impacts on qualityand environmental management, risks of bureaucracy, possible contradictions betweenrhetoric and practices, etc.

References

Ahire, S.L. and Devaraj, S. (2001), “An empirical comparison of statistical construct validationapproaches”, IEEE Transactions on Engineering Management, Vol. 48 No. 3, pp. 319-29.

Albuquerque, P., Bronnenberg, B.J. and Corbett, C. (2007), “A spatiotemporal analysis of theglobal diffusion of ISO 9000 and ISO 14000 certification”, Management Science, Vol. 53No. 3, pp. 451-68.

Ambec, S. and Lanoie, P. (2008), “Does it pay to be green? A systematic overview”, Academy ofManagement Perspectives, Vol. 22 No. 4, pp. 45-62.

Aragon-Correa, J.A. and Rubio-Lopez, E. (2007), “Proactive corporate environmental strategies:myths and misunderstandings”, Long Range Planning, Vol. 40 No. 3, pp. 357-81.

Bansal, P. and Bogner, W.C. (2002), “Deciding on ISO 14001: economics, institutions, andcontext”, Long Range Planning, Vol. 35 No. 3, pp. 269-90.

Bansal, P. and Hunter, T. (2003), “Strategic explanations for the early adoption of ISO 14001”,Journal of Business Ethics, Vol. 46 No. 3, pp. 289-99.

Battisti, M. and Perry, M. (2011), “Walking the talk? Environmental responsibility from theperspective of small-business owners”, Corporate Social Responsibility andEnvironmental Management, Vol. 18 No. 3, pp. 172-85.

Bellesi, F., Lehrer, D. and Alon, T. (2005), “Comparative advantage: the impact of ISO 14001environmental certification on exports”, Environmental Science & Technology, Vol. 39No. 7, pp. 1943-53.

Biondi, V., Frey, M. and Iraldo, F. (2000), “Environmental management systems and SMEs”,Greener Management International, Vol. 29, pp. 55-69.

Boiral, O. (2003), “ISO 9000, outside the iron cage”, Organization Science, Vol. 14 No. 6, pp. 720-37.

Boiral, O. (2005), “The impact of operator involvement in pollution reduction: case studies in Canadianchemical companies”, Business Strategy and the Environment, Vol. 14 No. 6, pp. 339-60.

BPMJ19,1

48

Boiral, O. (2009), “Greening the corporation through organizational citizenship behaviors”,Journal of Business Ethics, Vol. 87 No. 2, pp. 221-36.

Boiral, O. (2011), “Managing with ISO systems: lessons from practice”, Long Range Planning,Vol. 44 No. 3, pp. 197-220.

Boiral, O. and Paille, P. (2012), “Organizational citizenship behaviour for the environment:measurement and validation”, Journal of Business Ethics, Vol. 109 No. 4, available at:www.springerlink.com/content/8144372443571185/

Boyd, G.A. and McClelland, J.D. (1999), “The impact of environmental constraints onproductivity improvement in integrated paper plants”, Journal of EnvironmentalEconomics and Management, Vol. 38 No. 2, pp. 121-42.

Casadesus, M., Marimon, F. and Heras, I. (2008), “ISO 14001 diffusion after the success of theISO 9001 model”, Journal of Cleaner Production, Vol. 16, pp. 1741-54.

Chavan, M. (2005), “An appraisal of environment management systems: a competitive advantagefor small businesses”, Management of Environmental Quality, Vol. 16 No. 5, pp. 444-63.

Christmann, P. (2000), “Effects of ‘best practices’ of environmental management on costadvantage: the role of complementary assets”, Academy of Management Journal, Vol. 43No. 4, pp. 663-80.

Clemens, B. (2006), “Economic incentives and small firms: does it pay to be green?”, Journal ofBusiness Research, Vol. 59 No. 4, pp. 492-500.

Curkovic, S. and Pagell, M. (1999), “A critical examination of the ability of ISO 9000 certificationto lead to a competitive advantage”, Journal of Quality Management, Vol. 4 No. 1, pp. 51-67.

Daily, B.F., Bishop, J.W. and Govindarajulu, N. (2009), “A conceptual model for organizationalcitizenship behavior directed toward the environment”, Business and Society, Vol. 48 No. 2,pp. 243-56.

Danielson, M.G. and Scott, J.A. (2006), “The capital budgeting decisions of small businesses”,Journal of Applied Finance, Vol. 16 No. 2, pp. 45-56.

Darnall, N. and Edwards, D. (2006), “Predicting the cost of environmental management systemadoption: the role of capabilities, resources and ownership structure”, StrategicManagement Journal, Vol. 27 No. 4, pp. 301-20.

Darnall, N., Henriques, I. and Sadorsky, P. (2010), “Adopting proactive environmental strategy:the influence of stakeholders and firm size”, The Journal of Management Studies, Vol. 47No. 6, pp. 1072-94.

Dean, T.J., Brown, R.L. and Bamford, C.E. (1998), “Differences in large and small firm responsesto environmental context: strategic implications from a comparative analysis of businessformations”, Strategic Management Journal, Vol. 19 No. 8, pp. 709-28.

de Burgos-Jimenez, J. and Cespedes Lorente, J. (2001), “Environmental performance as anoperations objective”, International Journal of Operations & Production Management,Vol. 21 No. 12, pp. 1553-72.

del Brıo, J.A. and Junquera, B. (2003), “A review literature on environmental innovationmanagement in SMEs: implications for public policies”, Technovation, Vol. 23 No. 12,pp. 939-48.

Drake, F., Purvis, M. and Hunt, J. (2004), “Meeting the environmental challenge: a case of win-winor lose-win? A study of the UK banking and refrigeration industries”, Business Strategyand the Environment, Vol. 13 No. 3, pp. 172-86.

Epstein, M.J. (2008), Making Sustainability Work: Best Practices in Managing and MeasuringCorporate Social, Environmental and Economic Impacts, Berrett-Koehler Publishers,San Francisco, CA.

Quality andenvironmental

performance

49

Epstein, M.J. and Roy, M.J. (2000), “Strategic evaluation of environmental projects in SMEs”,Environmental Quality Management, Vol. 9 No. 3, pp. 37-47.

Fassin, Y., Van Rossem, A. and Buelens, M. (2011), “Small-business owner-managers’perceptions of business ethics and CSR-related concepts”, Journal of Business Ethics,Vol. 98 No. 3, pp. 425-53.

Ferdows, K. and De Meyer, A. (1990), “Lasting improvements in manufacturing performance:in search of a new theory”, Journal of Operations Management, Vol. 9 No. 2, pp. 168-84.

Fielding, S. (1999), “Going for the green: ISO 14001 delivers profits”, Industrial Management,Vol. 41 No. 2, pp. 31-4.

Gadenne, D.L., Jessica Kennedy, J. and McKeiver, C. (2009), “An empirical study of environmentalawareness and practices in SMEs”, Journal of Business Ethics, Vol. 84 No. 1, pp. 45-63.

Gonzalez-Benito, J. and Gonzalez-Benito, O. (2006), “A review of determinant factors of environmentalproactivity”, Business Strategy and the Environment, Vol. 15 No. 2, pp. 87-102.

Haksever, C. (1996), “Total quality management in the small business environment”, BusinessHorizons, Vol. 39 No. 2, pp. 33-40.

Hanna, M.D., Newman, W.R. and Johnson, P. (2000), “Linking operational and environmentalimprovement trough employee involvement”, International Journal of Operations &Production Management, Vol. 20 No. 2, pp. 148-65.

Henri, J.F. and Journeault, M. (2010), “Eco-control: the influence of management control systemson environmental and economic performance”, Accounting, Organizations and Society,Vol. 35 No. 1, pp. 63-80.

Hillary, R. (2000), Small and Medium-sized Enterprises and the Environment BusinessImperatives, Greenleaf Publishing, Sheffield.

Hillary, R. (2003), “Environmental management systems and the smaller enterprise”, Journal ofCleaner Production, Vol. 12 No. 6, pp. 561-9.

Hitchens, D., Clausen, J., Trainor, M., Keil, M. and Thankappan, S. (2003), “Competitiveness,environmental performance and management of SMEs”, Greener ManagementInternational, Vol. 44, pp. 45-57.

Husband, S. and Mandal, P. (1999), “A conceptual model for quality integrated management insmall and medium size enterprises”, International Journal of Quality & ReliabilityManagement, Vol. 16 No. 7, pp. 609-713.

IFAC (2005), Environmental Management Accounting, International Federation of Accountants,New York, NY.

International Organization for Standardization (2009), The ISO Survey, available at: ISO CentralSecretariat, www.iso.org/iso/survey2009.pdf

Judge, W.Q. and Douglas, T.J. (1998), “Performance implications of incorporating naturalenvironmental issues into the planning process: an empirical assessment”, Journal ofManagement Studies, Vol. 35 No. 2, pp. 241-62.

Karapetrovic, S. (2002), “Strategies for the integration of management systems and standards”,TQM Magazine, Vol. 14 No. 1, pp. 61-7.

Karapetrovic, S. and Willborn, W. (1998), “Integration of quality and environmental managementsystems”, TQM Magazine, Vol. 10 No. 3, pp. 204-13.

Kennelly, J.J. and Lewis, E.E. (2002), “Degree of internationalization and corporate environmentalperformance: is there a link?”, International Journal of Management, Vol. 19 No. 3,pp. 478-89.

BPMJ19,1

50

Ketokivi, M.A. and Schroeder, R.G. (2004), “Perceptual measures of performance: fact or fiction?”,Journal of Operations Management, Vol. 22 No. 3, pp. 247-64.

Kitazawa, S. and Sarkis, J. (2000), “The relationship between ISO 14001 and continuous sourcereduction programs”, International Journal of Operations & Production Management,Vol. 20 No. 2, pp. 225-48.

Lee, K.S. and Palmer, E. (1999), “An empirical examination of ISO 9000-registered companies inNew Zealand”, Total Quality Management, Vol. 10 No. 6, pp. 887-99.

Lefebvre, E., Lefebvre, L.A. and Talbot, S. (2003), “Determinants and impacts of environmentalperformance in SMEs”, R&D Management, Vol. 33 No. 3, pp. 263-83.

Lepoutre, J. and Heene, A. (2006), “Investigating the impact of firm size on small business socialresponsibility: a critical review”, Journal of Business Ethics, Vol. 67 No. 3, pp. 257-73.

McKeiver, C. and Gadenne, D. (2005), “Environmental management systems in small andmedium business”, International Small Business Journal, Vol. 23 No. 5, pp. 513-36.

MacKenzie, S., Podsakoff, P. and Ahearne, M. (1998), “Some possible antecedents andconsequences of in-role and extra-role salesperson performance”, Journal of Marketing,Vol. 62 No. 3, pp. 87-98.

Masurel, E. (2007), “Why SMEs invest in environmental measures: sustainability evidence fromsmall and medium-sized printing firms”, Business Strategy and the Environment, Vol. 16No. 3, pp. 190-201.

Melnyk, S.A., Sroufe, R.P. and Calantone, R. (2003), “Assessing the impact of environmentalmanagement systems on corporate and environmental performance”, Journal ofOperations Management, Vol. 21 No. 3, pp. 329-51.

Miles, M.P., Munilla, L.S. and McClurg, T. (1999), “The impact of ISO 14000 environmentalmanagement standards on small and medium sized enterprises”, Journal of QualityManagement, Vol. 4 No. 1, pp. 111-22.

Mintzberg, H. and Quinn, J. (1991), The Strategy Process, Prentice-Hall, Englewood Cliffs, NJ.

Molina-Azorın, J.F., Claver-Cortes, E., Lopez-Gamero, M.D. and Tarı, J.J. (2009a), “Greenmanagement and financial performance: a literature review”, Management Decision,Vol. 47 No. 7, pp. 1080-100.

Molina-Azorın, J.F., Juan, J., Tarı, J.J., Claver-Cortes, E. and Lopez-Gamero, M.D. (2009b),“Quality management, environmental management and firm performance: a review ofempirical studies and issues of integration”, International Journal of Management Reviews,Vol. 11 No. 2, pp. 197-222.

Naffziger, D.W., Ahmed, N.U. and Montagno, R.V. (2003), “Perceptions of environmentalconsciousness in US small businesses: an empirical study”, SAM Advanced ManagementJournal, Vol. 68 No. 2, pp. 23-32.

Neter, J., Wasserman, W. and Kutner, M.H. (1989), Applied Linear Regression Models,Richard D. Irwin, Homewood, IL.

Oldenburg, K.U. and Geiser, K. (1997), “Pollution prevention and/or industrial ecology?”, Journalof Cleaner Production, Vol. 5 Nos 1/2, pp. 103-8.

Organ, D., Podsakoff, P. and MacKenzie, S. (2006), Organizational Citizenship Behavior:Its Nature, Antecedents, and Consequences, Sage, Thousand Oaks, CA.

Parker, L.D. (1999), Environmental Costing: An Exploratory Examination, Australian Society ofCertified Practising Accountants (Ed.), Melbourne.

Perez-Sanchez, D., Barton, J.R. and Bower, D. (2003), “Implementing environmental managementin SMEs”, Corporate Social-Responsibility and Environmental Management, Vol. 10 No. 2,pp. 67-77.

Quality andenvironmental

performance

51

Podsakoff, P.M., MacKenzie, S.B., Paine, J.B. and Bachrach, D.G. (2000), “Organizationalcitizenship behaviors: a critical review of the theoretical and empirical literature andsuggestions for future research”, Journal of Management, Vol. 26 No. 3, pp. 513-63.

Poksinska, B., Dahlgaard, J.J. and Eklund, J.A.E. (2003), “Implementing ISO 14000 in Sweden:motives, benefits and comparisons with ISO 9000”, International Journal of Quality &Reliability Management, Vol. 20 No. 5, pp. 585-606.

Porter, M.E. and van der Linde, C. (1995), “Toward a new conception of theenvironment-competitiveness relationship”, Journal of Economic Perspectives, Vol. 9No. 4, pp. 97-118.

Potoski, M. and Prakash, A. (2005), “Green clubs and voluntary governance: ISO 14001 andfirms’ regulatory compliance”, American Journal of Political Science, Vol. 49 No. 2,pp. 235-48.

Preuss, L. and Perschke, J. (2009), “Slipstreaming the larger boats: social responsibility inmedium-sized businesses”, Journal of Business Ethics, Vol. 92 No. 4, pp. 531-51.

Pun, K.F. and Hui, I.K. (2001), “An analytical hierarchy process assessment of the ISO 14001environmental management system”, Integrated Manufacturing Systems, Vol. 12 No. 5,pp. 333-45.

Pun, K.F., Chin, K.S. and Lau, H. (1999), “A self-assessed quality management system based onintegration of MNQA/ISO 9000/ISO 14000”, International Journal of Quality & ReliabilityManagement, Vol. 16 No. 6, pp. 606-29.

Ramus, C.A. and Killmer, A.B. (2007), “Corporate greening through prosocial extrarolebehaviours – a conceptual framework for employee motivation”, Business Strategy and theEnvironment, Vol. 16 No. 8, pp. 554-70.

Revell, A. and Rutherford, R. (2003), “UK environmental policy and the small firm: broadeningthe focus”, Business Strategy and the Environment, Vol. 12 No. 1, pp. 26-35.

Rosenzweig, E.D. and Roth, A.V. (2004), “Towards a theory of competitive progression: evidencefrom high-tech manufacturing”, Production and Operations Management, Vol. 13 No. 4,pp. 354-68.

Roy, M.J., Boiral, O. and Legare, D. (2001), “Environmental commitment and manufacturingexcellence: a comparative study within Canadian industry”, Business Strategy and theEnvironment, Vol. 10 No. 5, pp. 257-68.

Schaper, M. (2002), “Small firms and environmental management”, International Small BusinessJournal, Vol. 20 No. 3, pp. 235-51.

Sharma, S. (2000), “Managerial interpretations and organizational context as predictors ofcorporate choice of environmental strategy”, Academy of Management Journal, Vol. 43No. 4, pp. 681-97.

Shin, R.W. and Chen, Y.C. (2000), “Seizing global opportunities for accomplishing agenciesmissions: the case of ISO 14000”, Public Administration Quarterly, Vol. 24 No. 1, pp. 68-94.

Simpson, M., Taylor, N. and Barker, K. (2004), “Environmental responsibility in SMEs: does itdeliver competitive advantage?”, Business Strategy and the Environment, Vol. 13 No. 3,pp. 156-71.

Skinner, W. (1969), “Manufacturing – missing link in corporate strategy”, Harvard BusinessReview, May-June, pp. 136-45.

Standards Council of Canada (2000), Management Systems Standards: The Story So Far,Standards Council of Canada, Ottawa.

BPMJ19,1

52

Van Dyne, L., Graham, J.W. and Dienesch, R.M. (1994), “Organizational citizenship behavior:construct redefinition, measurement and validation”, Academy of Management Journal,Vol. 37 No. 4, pp. 765-802.

Walgenbach, P. (2001), “The production of distrust by means of producing trust”, OrganizationStudies, Vol. 22 No. 4, pp. 693-714.

Wheelwright, S.C. (1984), “Manufacturing strategy: defining the missing link”, StrategicManagement Journal, Vol. 5 No. 1, pp. 77-91.

Worthington, I. and Patton, D. (2005), “Strategic intent in the management of the greenenvironment within SMEs an analysis of the UK screen-printing sector”, Long RangePlanning, Vol. 38 No. 2, pp. 197-212.

Yin, H. and Schmeidler, P. (2009), “Why do standardized ISO 14001 environmental managementsystems lead to heterogeneous environmental outcomes?”, Business Strategy and theEnvironment, Vol. 18 No. 7, pp. 469-86.