business fluctuations and forecasting week 3 sf intermediate economics professor mcaleese

TRANSCRIPT

Business Fluctuations and Forecasting

Week 3

SF Intermediate Economics

Professor McAleese

THE BUSINESS CYCLE WILL NOT DISAPPEAR ….

The inevitability of the business cycle, as it used to be called, I take for granted. Good times bring into existence: first, incompetent business executives; second, wrongful government policies; and, third, speculators. Working together, they ensure the eventual bust.

J K Galbraith “Challenges of the New Millennium” Finance and

Development December 1999 p 5

A MORE UPBEAT VIEW ….

It is not enough to assert that since there have always been business cycles there

always will be business cycles. Understanding what causes business cycles

and how these causes have changed suggests that business cycles will not be as important in the future as they were in the

past.S. Weber “The end of the business cycle” Foreign Affairs July 1997

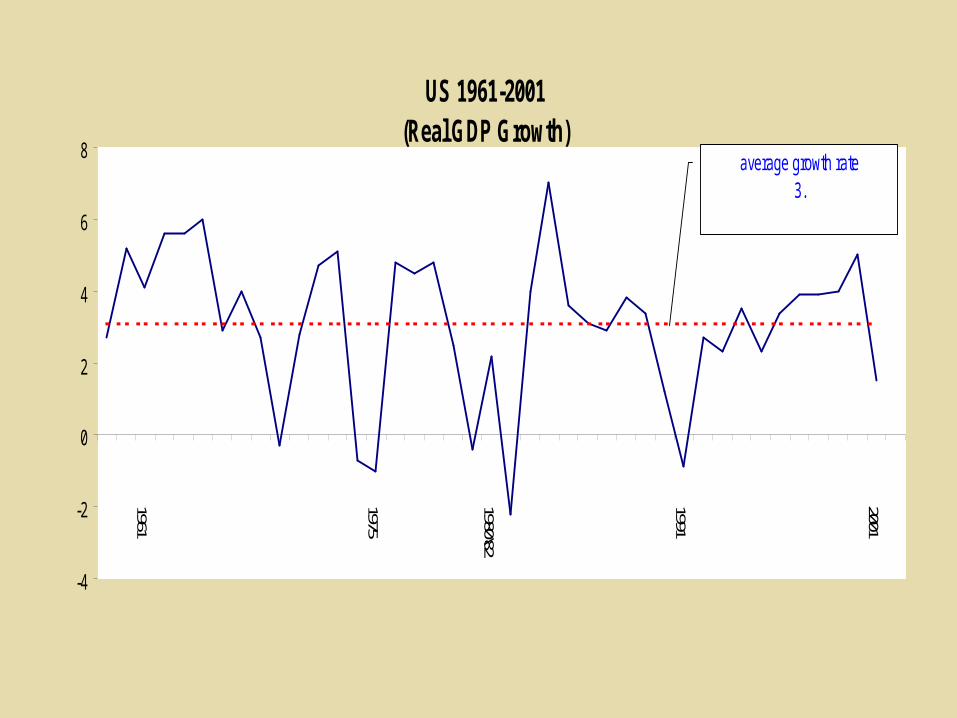

US 1961-2001(Real GDP Growth)

-4

-2

0

2

4

6

8

1961

1975

1980\82

1991

2001

average growth rate3.

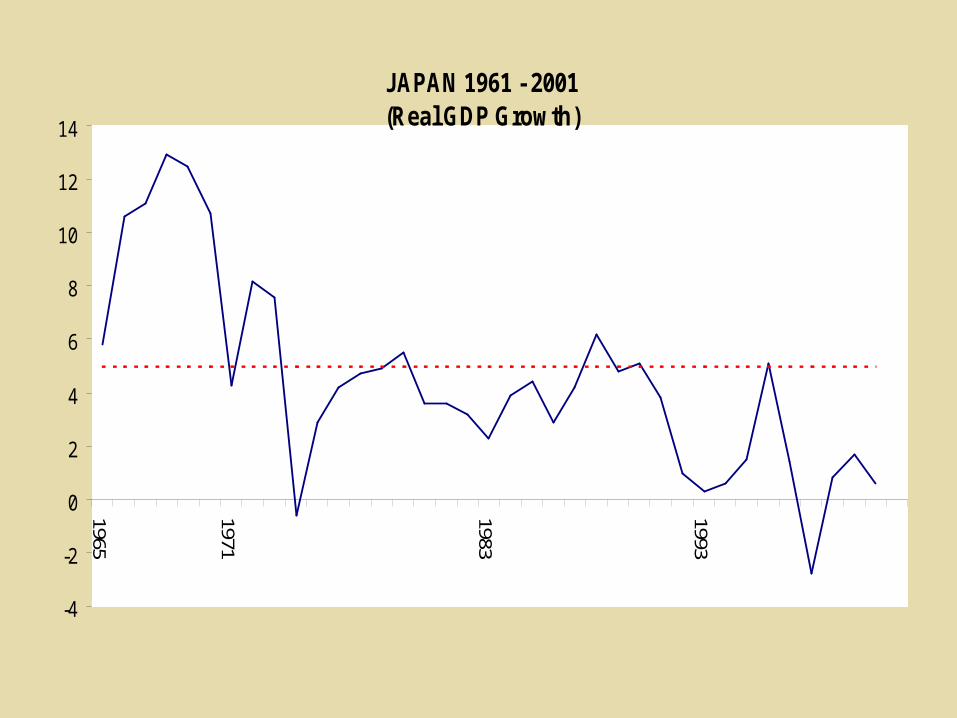

JAPAN 1961 - 2001(Real GDP Growth)

-4

-2

0

2

4

6

8

10

12

14

1965

1971

1983

1993

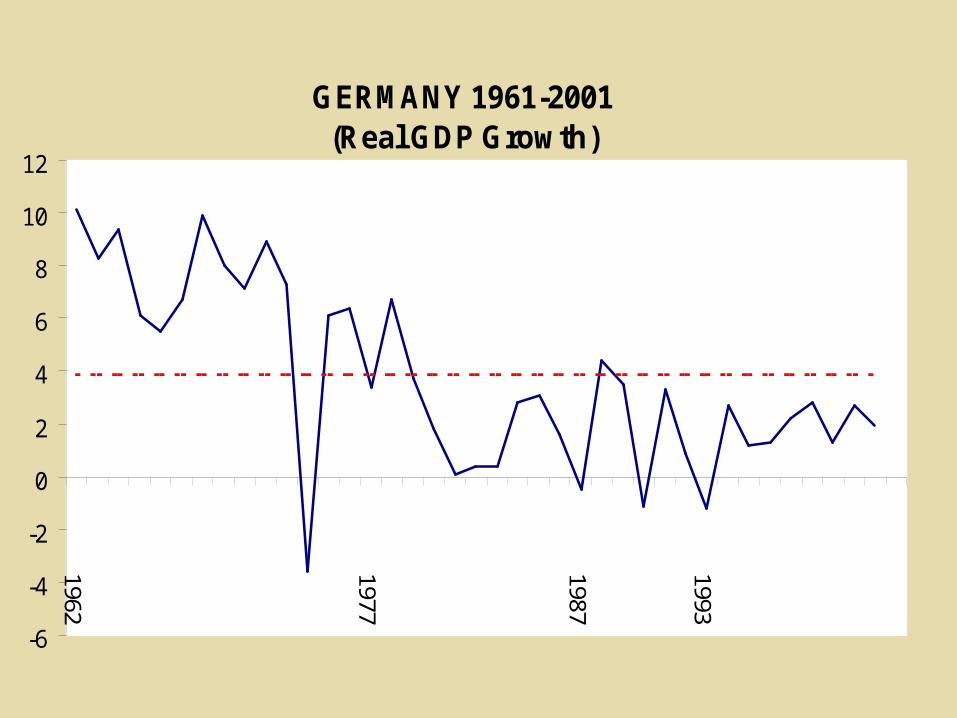

GERMANY 1961-2001(Real GDP Growth)

-6

-4

-2

0

2

4

6

8

10

12

1962

1977

1987

1993

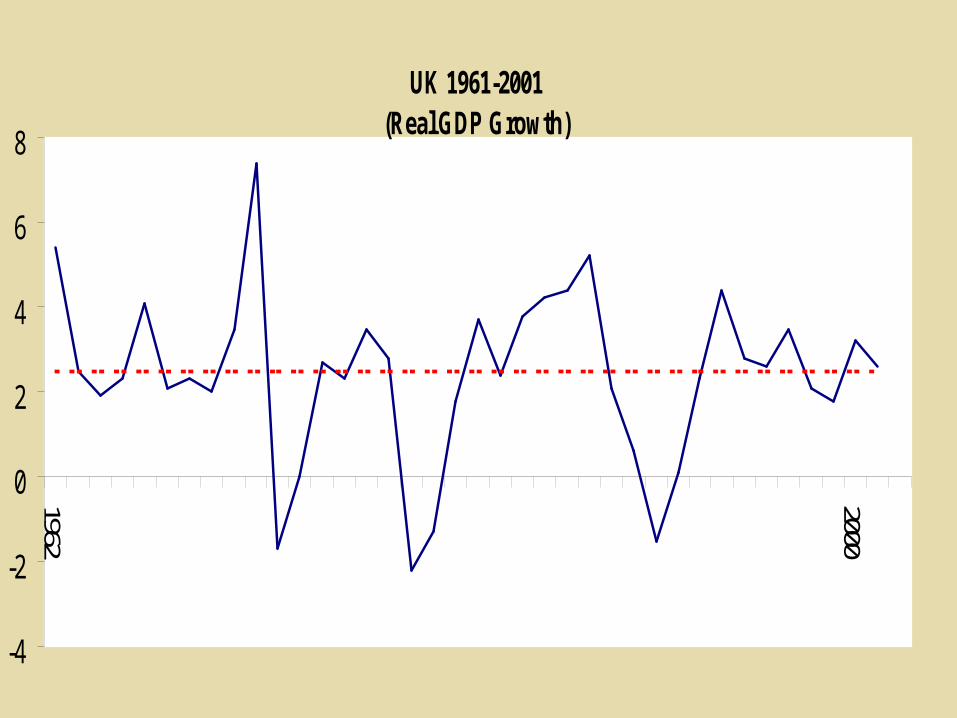

UK 1961-2001(Real GDP Growth)

-4

-2

0

2

4

6

8

1962

2000

OUTLINE

What are business fluctuations?

Why do they matter?

What causes them?

What can be done about them?

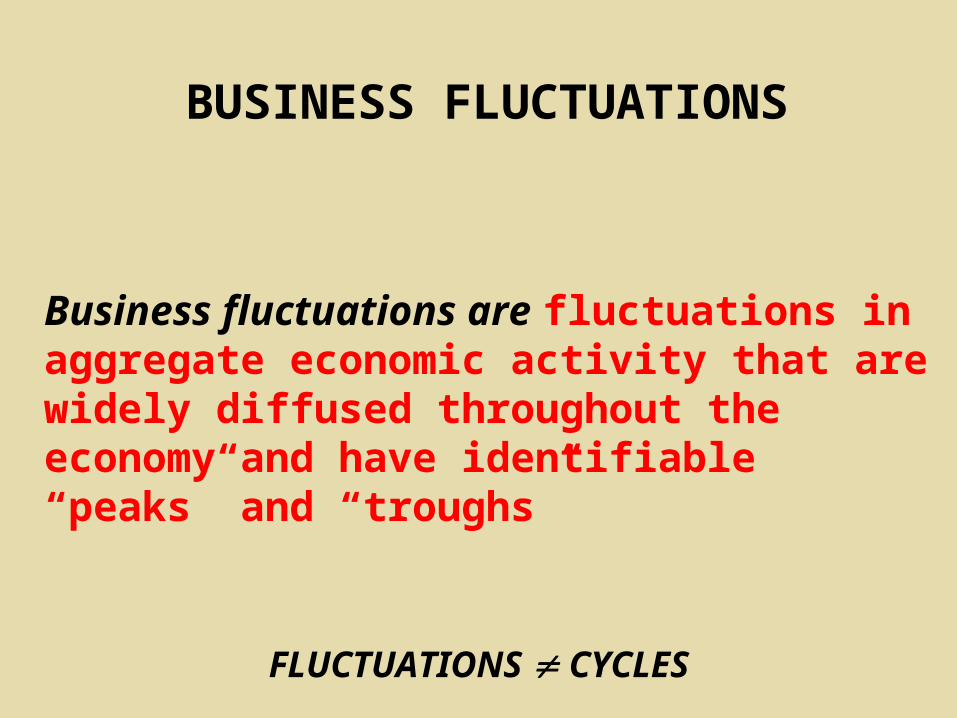

BUSINESS FLUCTUATIONS

Business fluctuations are fluctuations in aggregate economic activity that are widely diffused throughout the economy and have identifiable “peaks” and “troughs”

FLUCTUATIONS CYCLES

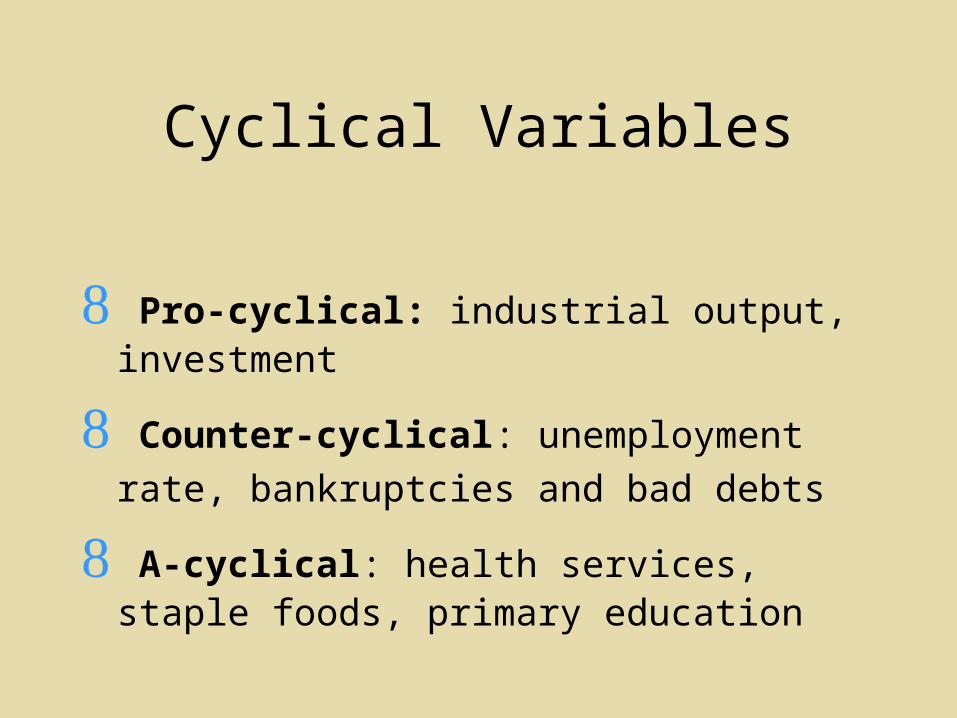

Cyclical Variables

Pro-cyclical: industrial output, investment

Counter-cyclical: unemployment rate,

bankruptcies and bad debts

A-cyclical: health services, staple foods, primary education

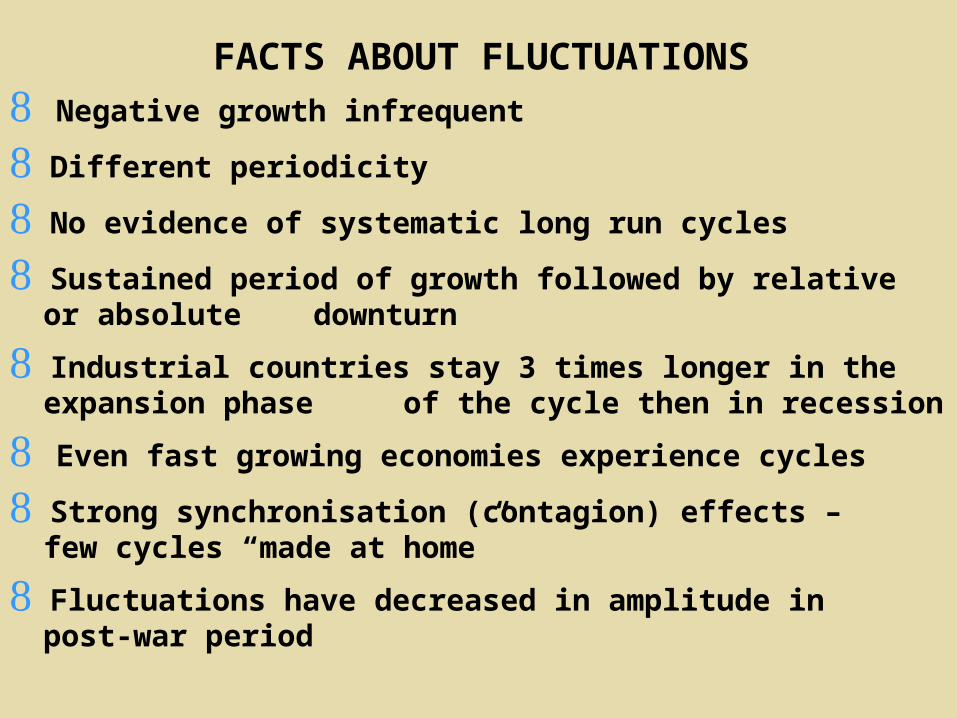

FACTS ABOUT FLUCTUATIONS

Negative growth infrequent

Different periodicity

No evidence of systematic long run cycles

Sustained period of growth followed by relative or absolute downturn

Industrial countries stay 3 times longer in the expansion phase of the cycle then in recession

Even fast growing economies experience cycles

Strong synchronisation (contagion) effects – few cycles “made at home”

Fluctuations have decreased in amplitude in post-war period

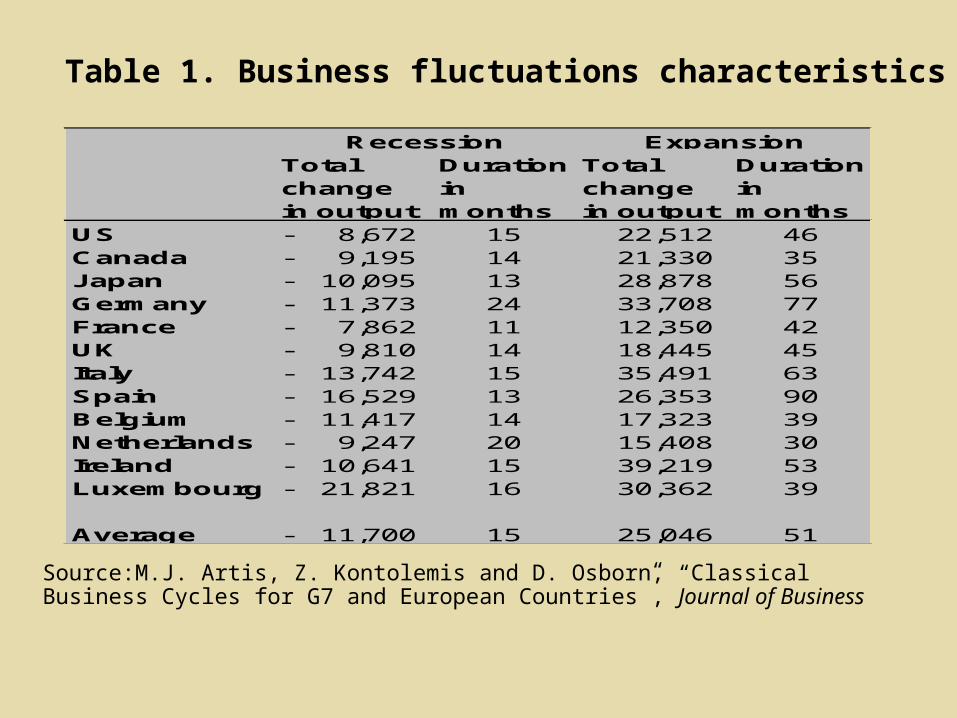

Table 1. Business fluctuations characteristics

Source:M.J. Artis, Z. Kontolemis and D. Osborn, “Classical Business Cycles for G7 and European Countries”, Journal of Business

Total change in output

Duration in months

Total change in output

Duration in months

US 8,672- 15 22,512 46Canada 9,195- 14 21,330 35Japan 10,095- 13 28,878 56Germany 11,373- 24 33,708 77France 7,862- 11 12,350 42UK 9,810- 14 18,445 45Italy 13,742- 15 35,491 63Spain 16,529- 13 26,353 90Belgium 11,417- 14 17,323 39Netherlands 9,247- 20 15,408 30Ireland 10,641- 15 39,219 53Luxembourg 21,821- 16 30,362 39

Average 11,700- 15 25,046 51

Recession Expansion

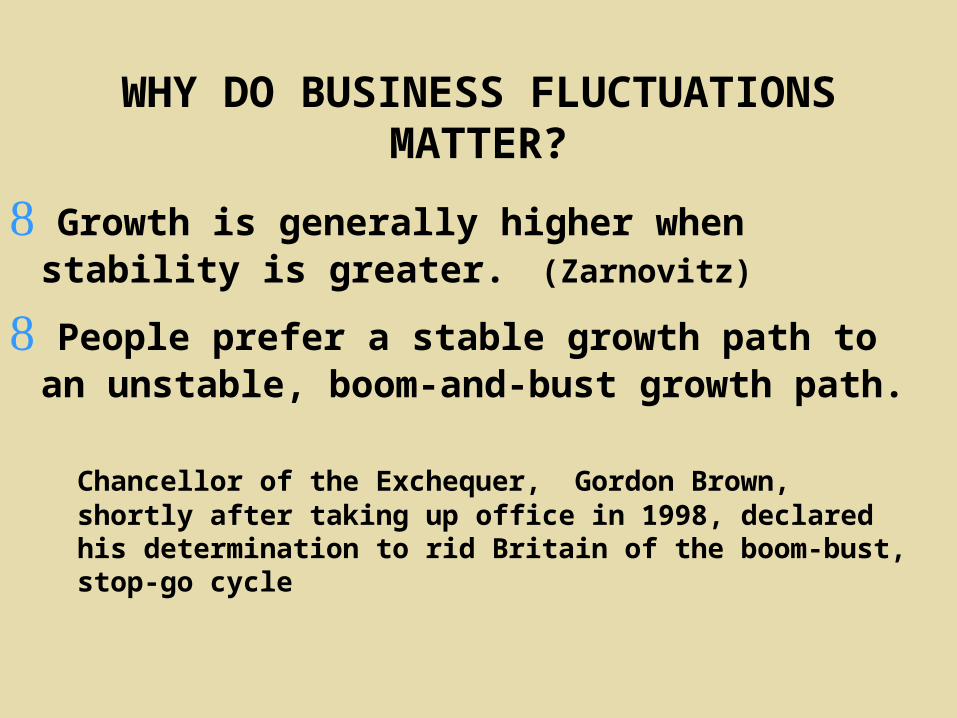

WHY DO BUSINESS FLUCTUATIONS MATTER?

Growth is generally higher when stability is greater. (Zarnovitz)

People prefer a stable growth path to an unstable, boom-and-bust growth path.

Chancellor of the Exchequer, Gordon Brown, shortly after taking up office in 1998, declared his determination to rid Britain of the boom-bust, stop-go cycle

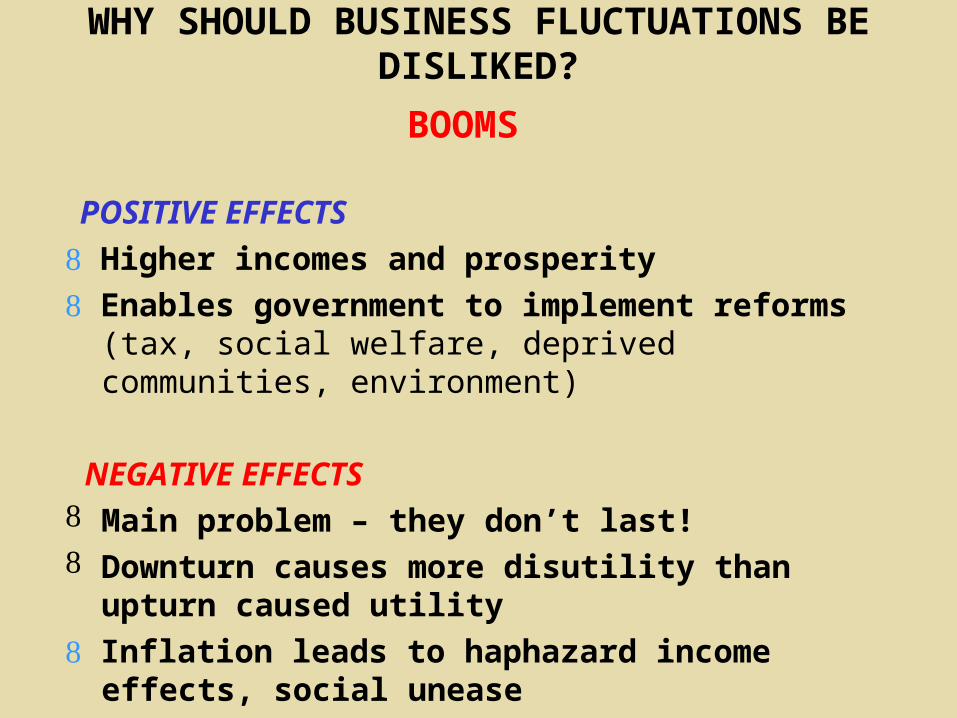

WHY SHOULD BUSINESS FLUCTUATIONS BE DISLIKED?

BOOMS

POSITIVE EFFECTS

Higher incomes and prosperity

Enables government to implement reforms (tax, social welfare, deprived communities, environment)

NEGATIVE EFFECTS Main problem – they don’t last! Downturn causes more disutility than upturn caused

utility

Inflation leads to haphazard income effects, social unease

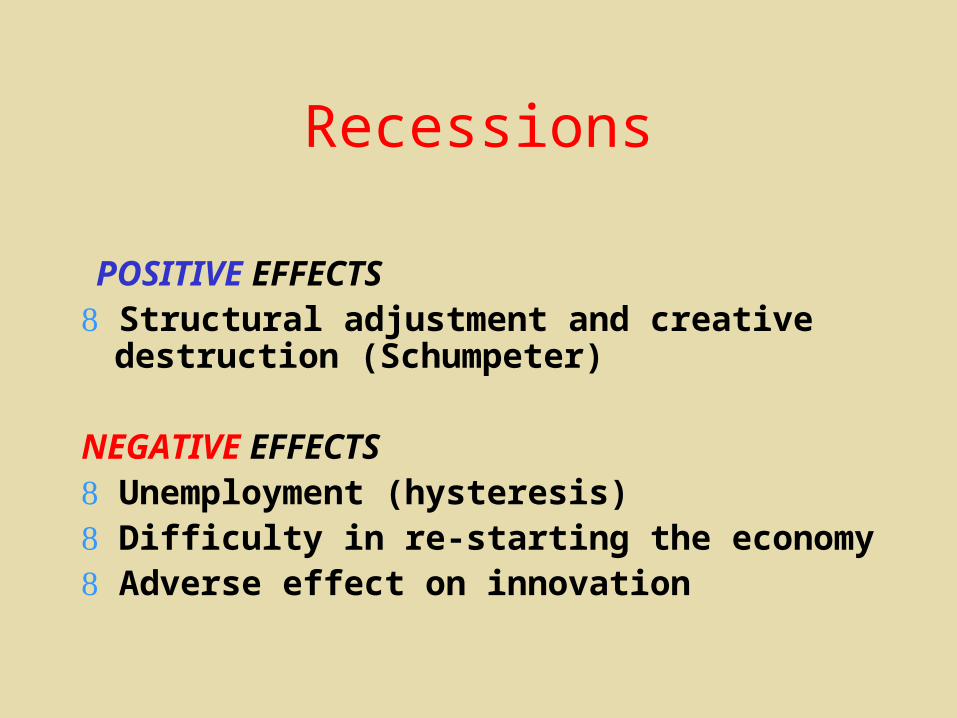

Recessions

POSITIVE EFFECTS Structural adjustment and creative destruction

(Schumpeter)

NEGATIVE EFFECTS Unemployment (hysteresis) Difficulty in re-starting the economy Adverse effect on innovation

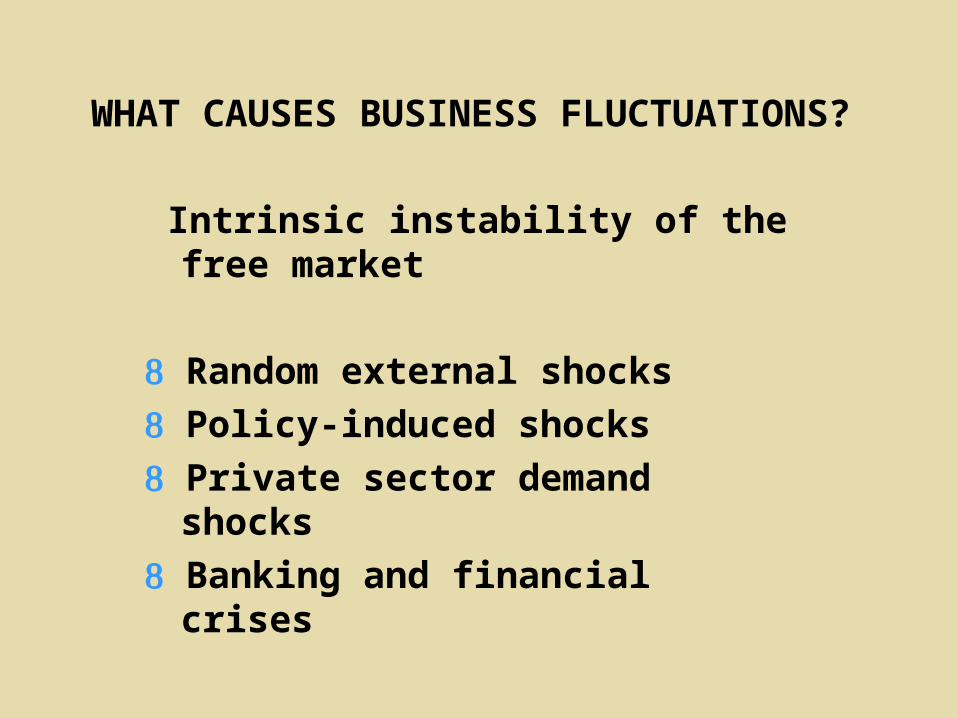

WHAT CAUSES BUSINESS FLUCTUATIONS?

Intrinsic instability of the free market

Random external shocks

Policy-induced shocks

Private sector demand shocks

Banking and financial crises

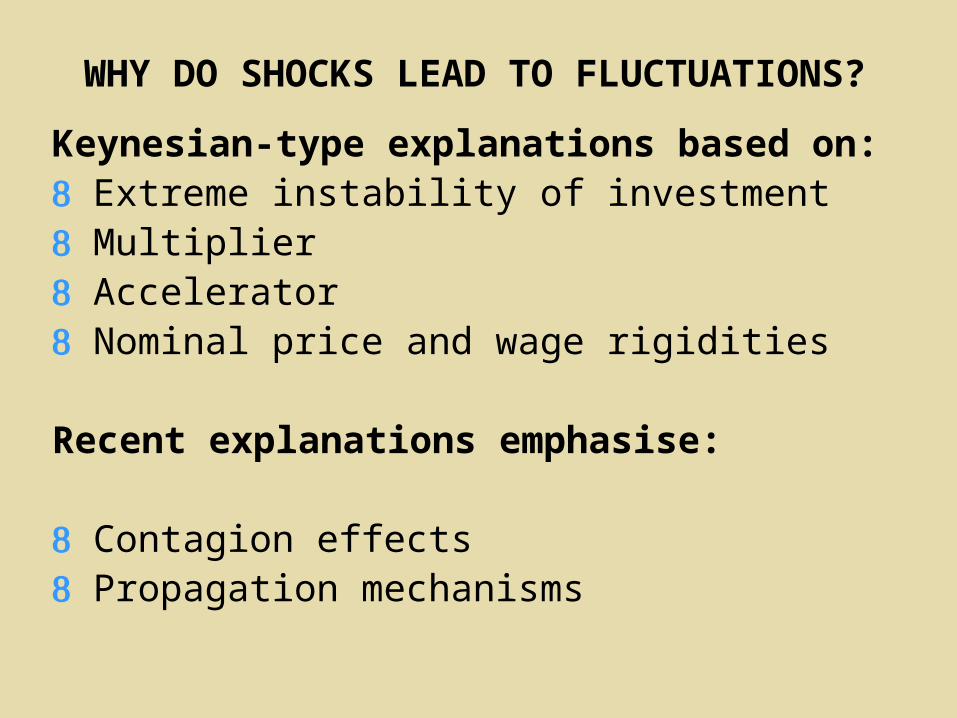

WHY DO SHOCKS LEAD TO FLUCTUATIONS?

Keynesian-type explanations based on: Extreme instability of investment Multiplier Accelerator Nominal price and wage rigidities

Recent explanations emphasise:

Contagion effects Propagation mechanisms

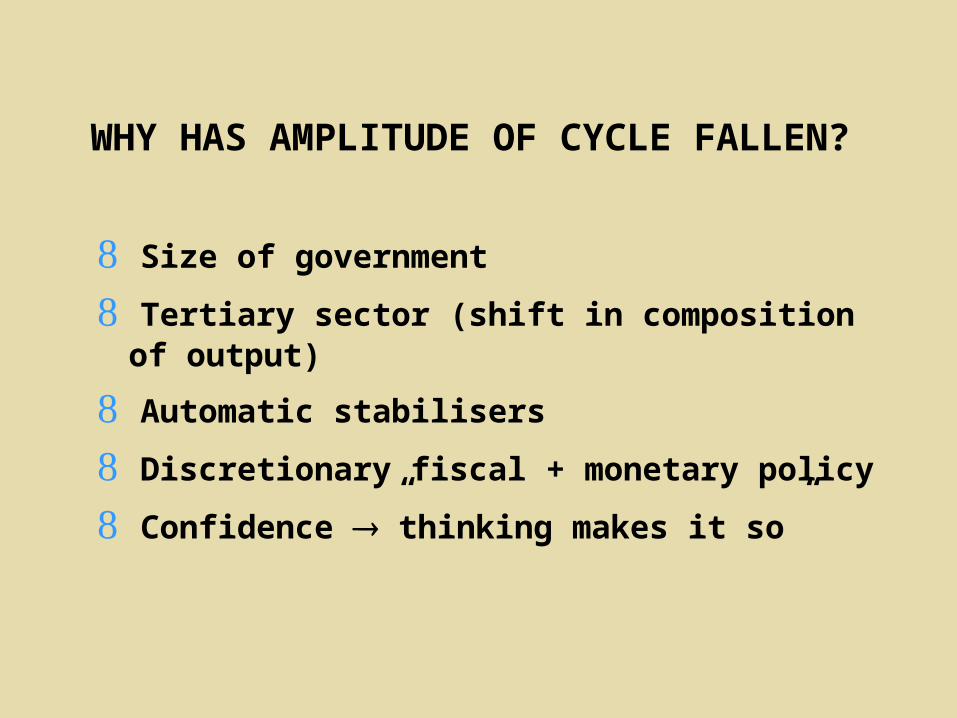

WHY HAS AMPLITUDE OF CYCLE FALLEN?

Size of government

Tertiary sector (shift in composition of output)

Automatic stabilisers

Discretionary fiscal + monetary policy

Confidence ”thinking makes it so”

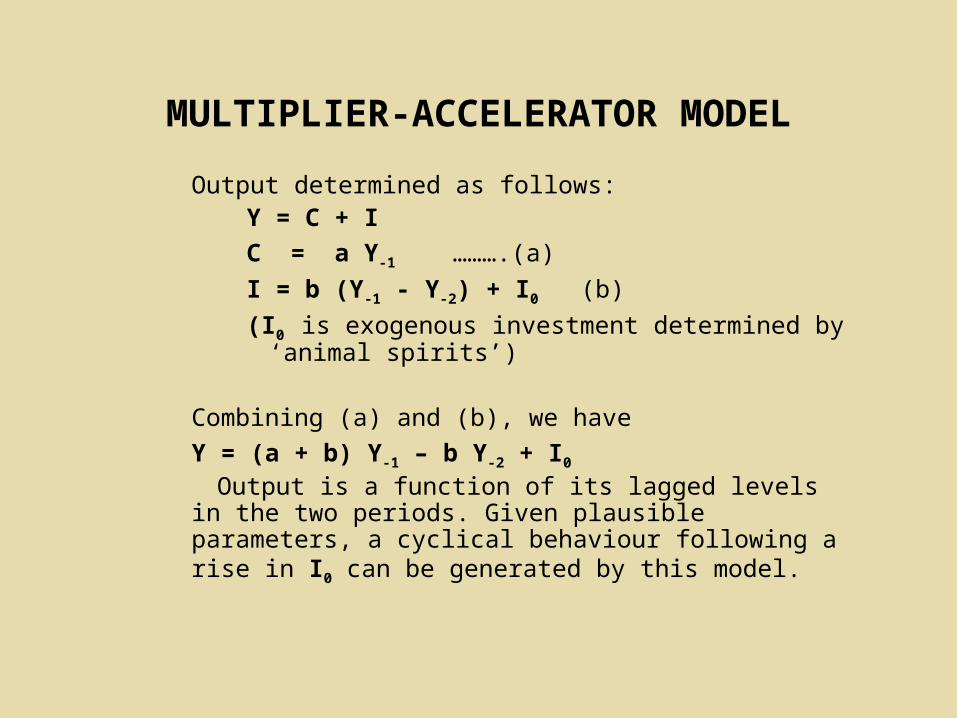

MULTIPLIER-ACCELERATOR MODEL

Output determined as follows:Y = C + I

C = a Y-1 ……….(a)

I = b (Y-1 - Y-2) + I0 (b)

(I0 is exogenous investment determined by ‘animal spirits’)

Combining (a) and (b), we have

Y = (a + b) Y-1 – b Y-2 + I0

Output is a function of its lagged levels in the two periods. Given plausible parameters, a cyclical behaviour following a rise in I0 can be generated by this model.

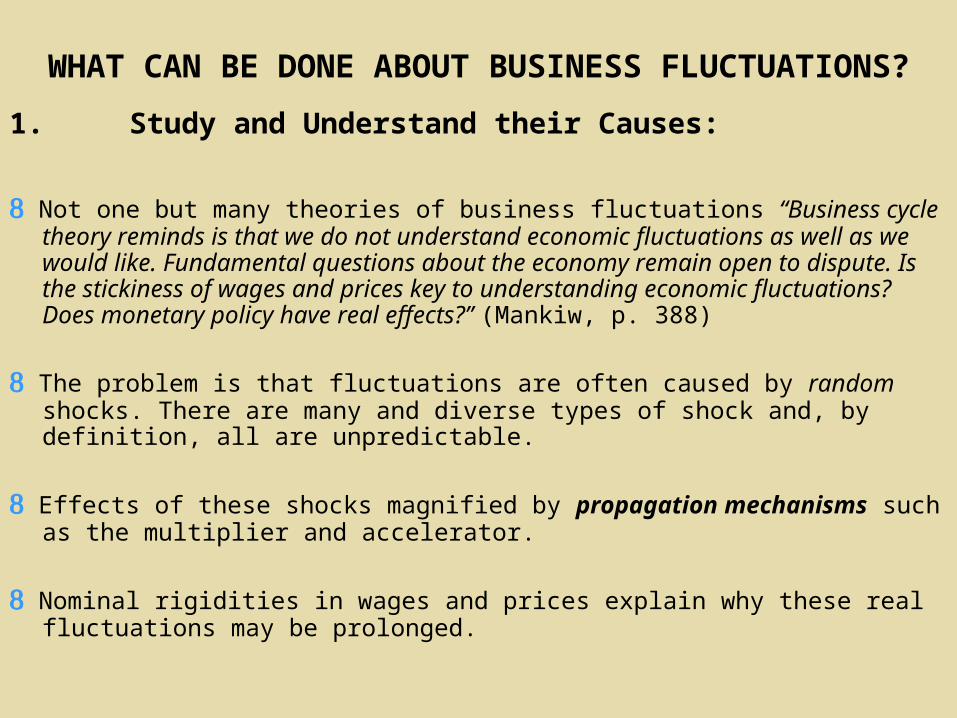

WHAT CAN BE DONE ABOUT BUSINESS FLUCTUATIONS?

1. Study and Understand their Causes:

Not one but many theories of business fluctuations “Business cycle theory reminds is that we do not understand economic fluctuations as well as we would like. Fundamental questions about the economy remain open to dispute. Is the stickiness of wages and prices key to understanding economic fluctuations? Does monetary policy have real effects?” (Mankiw, p. 388)

The problem is that fluctuations are often caused by random shocks. There are many and diverse types of shock and, by definition, all are unpredictable.

Effects of these shocks magnified by propagation mechanisms such as the multiplier and accelerator.

Nominal rigidities in wages and prices explain why these real fluctuations may be prolonged.

2. Establish Best Possible Estimates of Potential GNP and Derive Reliable, Timely Estimates of Current GNP

To derive potential GNP estimates, careful modelling of the economy needed. This is an on-going exercise.

3. Implement counter-cyclical fiscal policy

Dismal record of many governments’ fiscal policy – often pro-cyclical instead of counter-cyclical.

Solution may be to implement coarse tuning rather than fine-tuning policies

Adhere to strict overall guidelines

4. Manage Monetary Policy so that Price Stability is the Central Objective

Bad monetary policy, and inflation, can be sources, not cures, of business fluctuations because of ‘long and variable’ lags between monetary policy action and its effects on the real economy

5. …. but allow for some counter-cyclical role Hence only limited scope for counter-cyclical intervention

6. Government can also Help by ‘Talking Down’ Booms and ‘Talking Up’ Recessions

….but such verbal of symbolic interventions are of limited value in practice

CONCLUSIONS

Government has on balance diminished the overall amplitude of fluctuations.

Bad economic policies have created fluctuations in the past

Policy activism means that the danger of extreme collapse and boom is diminished. There has been a permanent raising of the ‘floor’ of the business cycle and a lowering of the ‘ceiling.’ Policy is difficult because nobody is quite sure when these ceilings and floors are near to being reached.

Danger of really serious Japanese-type downturn cannot be ruled out.

REPEATING HISTORY: IS THE WORLD ECONOMY

ENTERING INTO A SERIOUS DOWNTURN?

THINK ABOUT THIS QUESTION DURING THE NEXT WEEKS –

AND SEE IMF WORLD ECONOMIC OUTLOOK MAY 2001

(NOW IN LIBRARY)