busi 331 real estate investment analysis and advanced ... · pdf filebusi 331 real estate...

TRANSCRIPT

Real Estate Division

BUSI 331 Real Estate Investment Analysis and Advanced Income Appraisal

Len Sherwood

3

REAL ESTATE DIVISION

UNIVERSITY OF BRITISH COLUMBIA

Topics:

• Introduction • Overview of Real Estate Assets and Markets• Analysis of Income and Expenses• Introduction to Leasing• Lease Analysis• Taxation of Real Estate Investments• Questions

4

REAL ESTATE DIVISION

•The lesson will take about 1.5 hours and will be followed by a free-for-all question and answer session. During the presentation please do not hesitate to ask questions and/or provide your opinion.

Introduction

5

REAL ESTATE DIVISION

This webinar is intended primarily to help you to understand concepts and proper procedures. Only the major points of the text will be addressed.

Goal

6

REAL ESTATE DIVISION

Investment Analysis vs. Appraisal

Investment Analysis: Value to the Owner based on a set ofowner-defined criteria and circumstances:

• Required Rate of Return (RRR)• Risk tolerance• Cash flows (income) versus appreciation (capital gain)• Financing• Tax status

7

REAL ESTATE DIVISION

UNIVERSITY OF BRITISH COLUMBIA

Investment Analysis vs. Appraisal

Appraisal: Market Value

• Uses an analytical framework to determine the value of property in the eyes of the market as opposed to an individual• Concerned with cash flows from the property on a before financing, before tax basis• Net Operating Income (NOI) measures the cash return from the property

8

REAL ESTATE DIVISION

UNIVERSITY OF BRITISH COLUMBIA

Point to Ponder

“Much learning does not teach a person to have intelligence”..Heraclitus-5th Century BC

9

REAL ESTATE DIVISION

What is intelligence? It is the capacity to reason, to ask questions, and that is what we must do as appraisers and consultants. Learn these BUSI 331 procedures, by all means, but do not apply them blindly.

10

REAL ESTATE DIVISION

CHAPTER ONEOVERVIEW

11

REAL ESTATE DIVISION

Two types of students for this course:•Appraisers•Consultants

This course is of interest to both types.

Of interest to

12

REAL ESTATE DIVISION

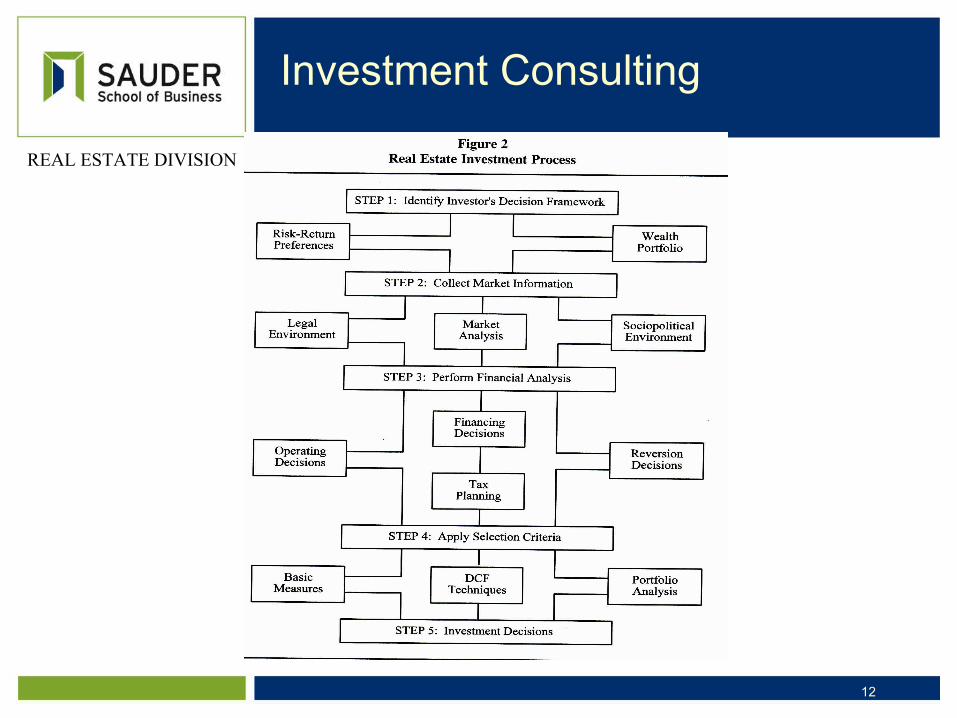

Investment Consulting

13

REAL ESTATE DIVISION

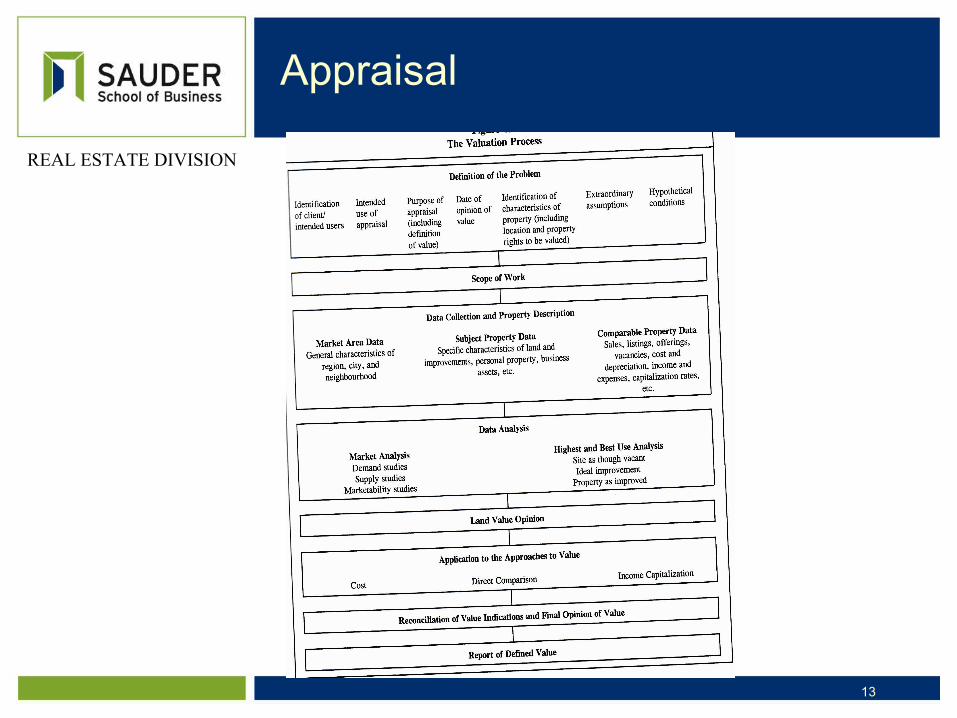

Appraisal

14

REAL ESTATE DIVISION

Basic formula is NI/OAR = MVNI from supply and demand;OAR = measure of risk

All valuations reflect risk-return

Overview

15

REAL ESTATE DIVISION

Advantages of RE Investments

•High returns•Inflation hedge•Financial leverage•Tax sheltering

16

REAL ESTATE DIVISION

•Financial risk (increases with leverage)•Interest rate risk (as per financial)•Illiquidity•Management

Disadvantages of RE Investments

17

REAL ESTATE DIVISION

Pay attention to fundamentals:•Net rent obtainable•Quality of tenants•Quality of real estate

Tax benefit is secondary due to impact of tax law changes at any time (MURBs)

Fundamentals

18

REAL ESTATE DIVISION

Ref. P 1.12. Log1.05 2=n (use Excel “log” function) to find that at 5% mv will double in 14 years.

Rule of thumb: 70/i = years for mv to double.e.g. 70/.05 = 14 years.

Rule of Thumb

19

REAL ESTATE DIVISION

CHAPTER TWOANALYSIS OF

INCOME AND EXPENSES

20

REAL ESTATE DIVISION

The whole point of this chapter is to demonstrate how to properly estimate net operating income of the subject property

GOAL

21

REAL ESTATE DIVISION

Process

•Analyze operating history•Find and analyze market rents and expenses•If s.p. operation is similar to market use s.p. NOI for valuation•If not, investigate why not and adjust as required.

The following slides illustrate this process.

22

REAL ESTATE DIVISION

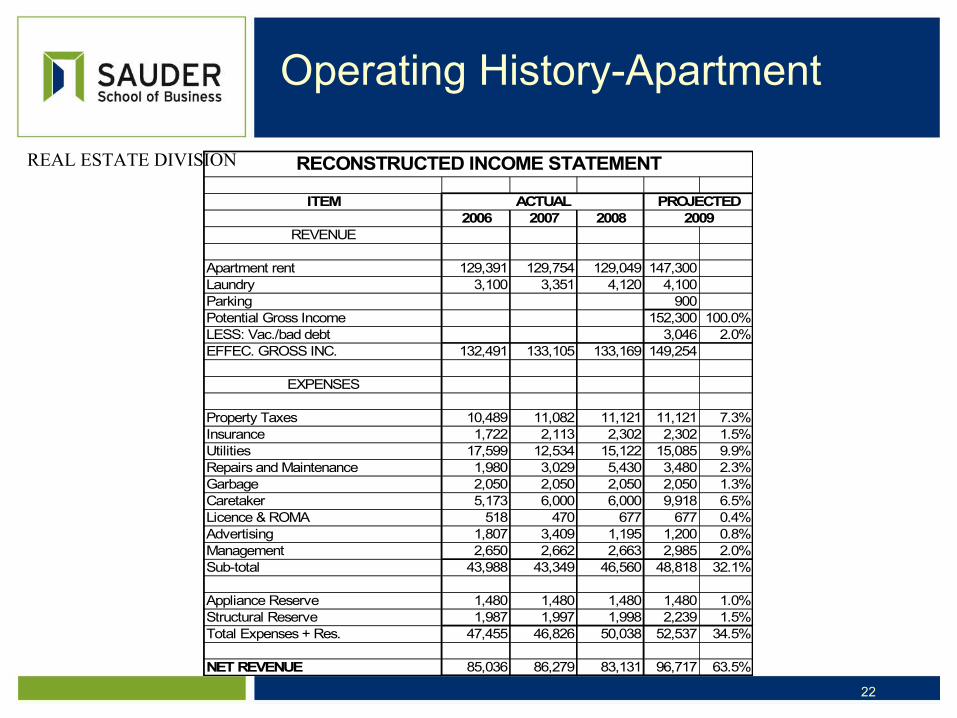

Operating History-Apartment

RECONSTRUCTED INCOME STATEMENT

ITEM PROJECTED2006 2007 2008 2009

REVENUE

Apartment rent 129,391 129,754 129,049 147,300Laundry 3,100 3,351 4,120 4,100Parking 900Potential Gross Income 152,300 100.0%LESS: Vac./bad debt 3,046 2.0%EFFEC. GROSS INC. 132,491 133,105 133,169 149,254

EXPENSES

Property Taxes 10,489 11,082 11,121 11,121 7.3%Insurance 1,722 2,113 2,302 2,302 1.5%Utilities 17,599 12,534 15,122 15,085 9.9%Repairs and Maintenance 1,980 3,029 5,430 3,480 2.3%Garbage 2,050 2,050 2,050 2,050 1.3%Caretaker 5,173 6,000 6,000 9,918 6.5%Licence & ROMA 518 470 677 677 0.4%Advertising 1,807 3,409 1,195 1,200 0.8%Management 2,650 2,662 2,663 2,985 2.0%Sub-total 43,988 43,349 46,560 48,818 32.1%

Appliance Reserve 1,480 1,480 1,480 1,480 1.0%Structural Reserve 1,987 1,997 1,998 2,239 1.5%Total Expenses + Res. 47,455 46,826 50,038 52,537 34.5%

NET REVENUE 85,036 86,279 83,131 96,717 63.5%

ACTUAL

23

REAL ESTATE DIVISION

Rental spreadsheet-Retail

Lease Term Area Rate Mcon RateStreet Date Yrs SF $Net Adj CAM $Gr Remarks

Douglas Apr-08 5 2,329 14.80 15.24 8.83 24.07Renovated. HVAC. Rent averaged $14/$15/$15/$15/$15. 2 months fixturing with commencement June 2008.

Bay Aug-08 5 1,447 17.60 17.70 9.59 27.29 Plaza location. Finished main floor office.

Blanshard Jul-08 5 17,000 20.00 20.24 8.00 28.24 Renewal. Jordan's furniture. Interior unit Blanshard Square plaza. Good.

Gorge E. Mar-07 5 1,368 22.00 24.38 7.00 31.38Built 1951. Garden store. Rent averaged $18/20/22/24/26. Good condition. Finished space. No TIs. CAM estimated.

Pandora Sep-08 5 1,100 20.00 20.00 9.00 29.00 Good finished office space leased to mortgage broker. Good parking at $100 per stall. No Tis.

RETAIL LEASES

Rental Rate Trend with Building Class

0.00

10.00

20.00

30.00

0.00

Building Class

Renta

l Rate

Per

Squ

are F

oot

24

REAL ESTATE DIVISION

When comparing market rents of retail, office and industrial properties ensure all (including s.p.) are based on rentable area as per BOMA standard.

BOMA

25

REAL ESTATE DIVISION

In Victoria, expenses/EGI are typically 30% to 35%. S.P. For 2008 is 38%.Why? Rents are below market because owner has not been diligent, but expenses are at market, so use market rents for valuation.

Ratio Analysis

26

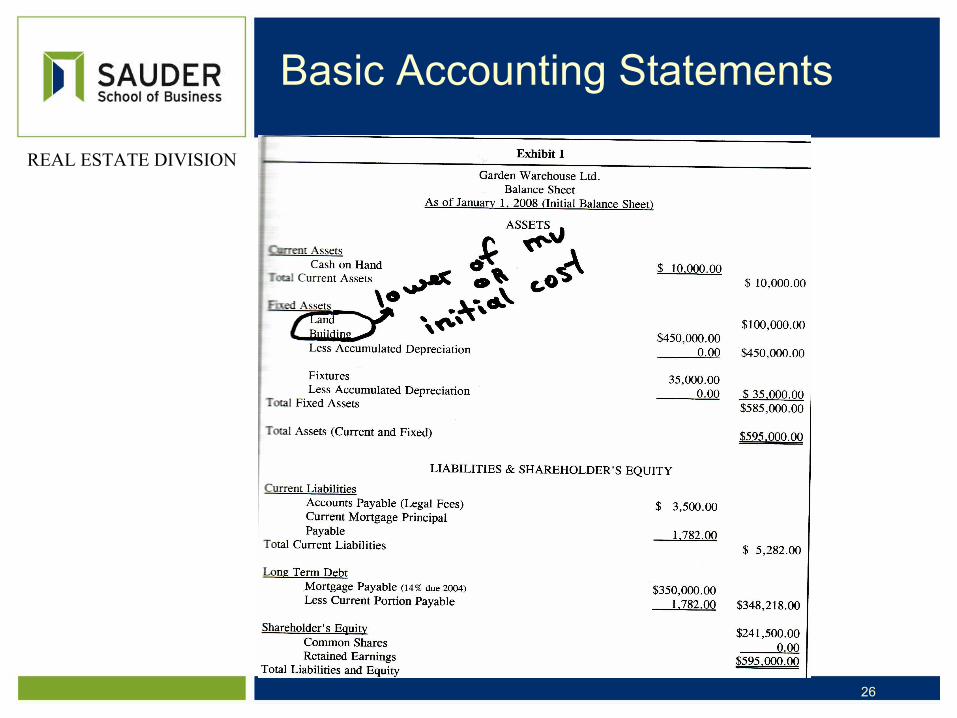

REAL ESTATE DIVISION

Basic Accounting Statements

27

REAL ESTATE DIVISION

Income StatementAccounting vs for tax

28

REAL ESTATE DIVISION

Appraisal: NOI is before tax and financing because this creates common denominator for comparison of investments.

Forecasting: Appraisal vs Investing

29

REAL ESTATE DIVISION

GRM-direct comparison method

OCR-typical return on investment for a particular income-property type.

Ratio Analysis

30

REAL ESTATE DIVISION

P. 2.20. This applies in situations where landlord pays expenses such as for apartments, but does not normally affect retail/office/industrial properties that are usually rented on an absolute net basis.

Operating Leverage

31

REAL ESTATE DIVISION

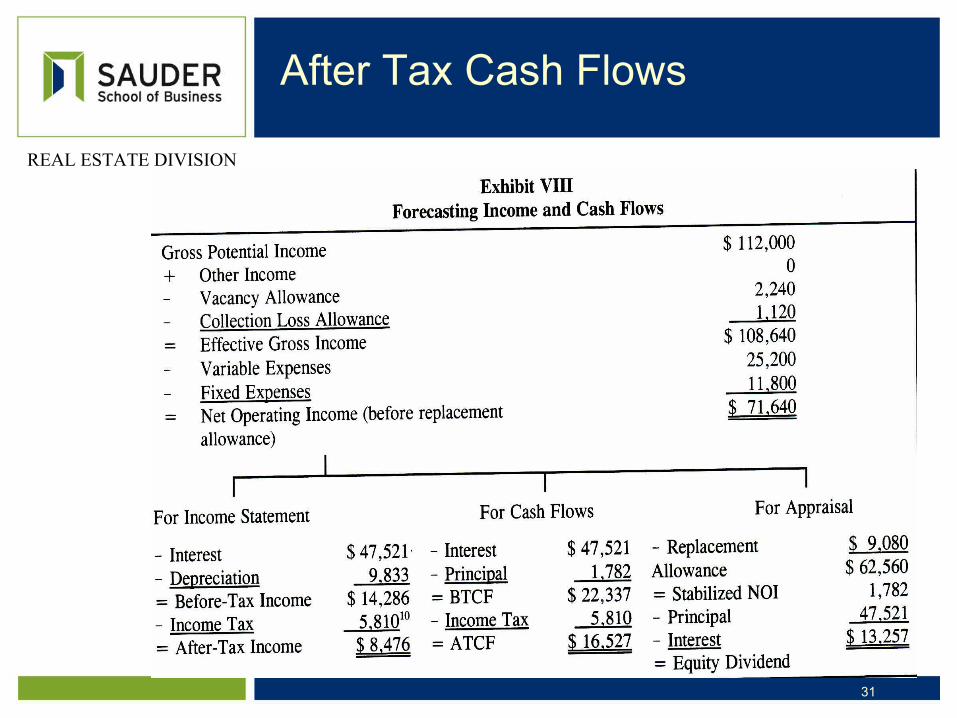

After Tax Cash Flows

32

REAL ESTATE DIVISION

PARAMETERS:•Investment horizon•Cash flow forecasts (lease and market)•Reversion estimate

These statements must be discounted to NPV

Pro Forma Statements

33

REAL ESTATE DIVISION

We all use DCF, but do we understand it?If an investor requires a return on investment (ROI) of 10% he will invest $100 today to receive $110 a year from now. This is the foundational concept of DCF.

Discounted Cash Flow Concept

34

REAL ESTATE DIVISION

What do we mean by present value?$110 received one year from now, at an investor's required rate (discount rate) of 10% has a value today of $110/(1+10%) = $100. $100 plus 10% = $110.

Present Value

35

REAL ESTATE DIVISION

Let's see how well you can apply DCF. Here is a multiple-choice question. You have three minutes to tackle it.

TEST

36

REAL ESTATE DIVISION

Ref p.2.33. FV of property is increased at a 6% rate. Does not account for differing income and expense rate changes. Better to base reversion on projected NOI and projected cap rate.

Reversionary Value

37

REAL ESTATE DIVISION

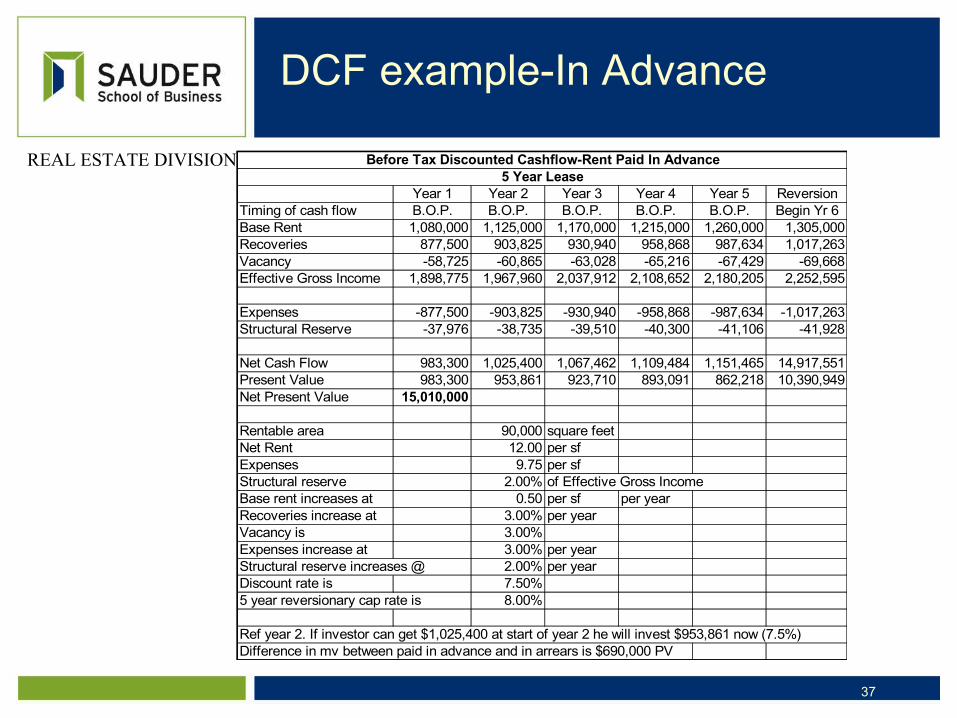

DCF example-In Advance

Year 1 Year 2 Year 3 Year 4 Year 5 ReversionTiming of cash flow B.O.P. B.O.P. B.O.P. B.O.P. B.O.P. Begin Yr 6Base Rent 1,080,000 1,125,000 1,170,000 1,215,000 1,260,000 1,305,000Recoveries 877,500 903,825 930,940 958,868 987,634 1,017,263Vacancy -58,725 -60,865 -63,028 -65,216 -67,429 -69,668Effective Gross Income 1,898,775 1,967,960 2,037,912 2,108,652 2,180,205 2,252,595

Expenses -877,500 -903,825 -930,940 -958,868 -987,634 -1,017,263Structural Reserve -37,976 -38,735 -39,510 -40,300 -41,106 -41,928

Net Cash Flow 983,300 1,025,400 1,067,462 1,109,484 1,151,465 14,917,551Present Value 983,300 953,861 923,710 893,091 862,218 10,390,949Net Present Value 15,010,000

Rentable area 90,000 square feetNet Rent 12.00 per sfExpenses 9.75 per sfStructural reserve 2.00% of Effective Gross IncomeBase rent increases at 0.50 per sf per yearRecoveries increase at 3.00% per yearVacancy is 3.00%Expenses increase at 3.00% per yearStructural reserve increases @ 2.00% per yearDiscount rate is 7.50%5 year reversionary cap rate is 8.00%

Ref year 2. If investor can get $1,025,400 at start of year 2 he will invest $953,861 now (7.5%)Difference in mv between paid in advance and in arrears is $690,000 PV

Before Tax Discounted Cashflow-Rent Paid In Advance5 Year Lease

38

REAL ESTATE DIVISION

Rent paid in arrears

Year 1 Year 2 Year 3 Year 4 Year 5 ReversionTiming of cash flow E.O.P. E.O.P. E.O.P. E.O.P. E.O.P. End Yr 5Base Rent 1,080,000 1,125,000 1,170,000 1,215,000 1,260,000Recoveries 877,500 903,825 930,940 958,868 987,634Vacancy -58,725 -60,865 -63,028 -65,216 -67,429Effective Gross Income 1,898,775 1,967,960 2,037,912 2,108,652 2,180,205

Expenses -877,500 -903,825 -930,940 -958,868 -987,634Structural Reserve -37,976 -38,735 -39,510 -40,300 -41,106

Net Cash Flow 983,300 1,025,400 1,067,462 1,109,484 1,151,465 14,393,313Present Value 914,697 887,312 859,265 830,782 802,063 10,025,787Net Present Value 14,320,000

Before Tax Discounted Cashflow-Rent Paid In Arrears5 Year Lease

39

REAL ESTATE DIVISION

Be careful when timing cashflows. As you can see from the foregoing it can have a marked impact on market value. In advance, reversion is based on income at beginning of year 6, in arrears it is based on end of year 5 income.

Note about DCF

43

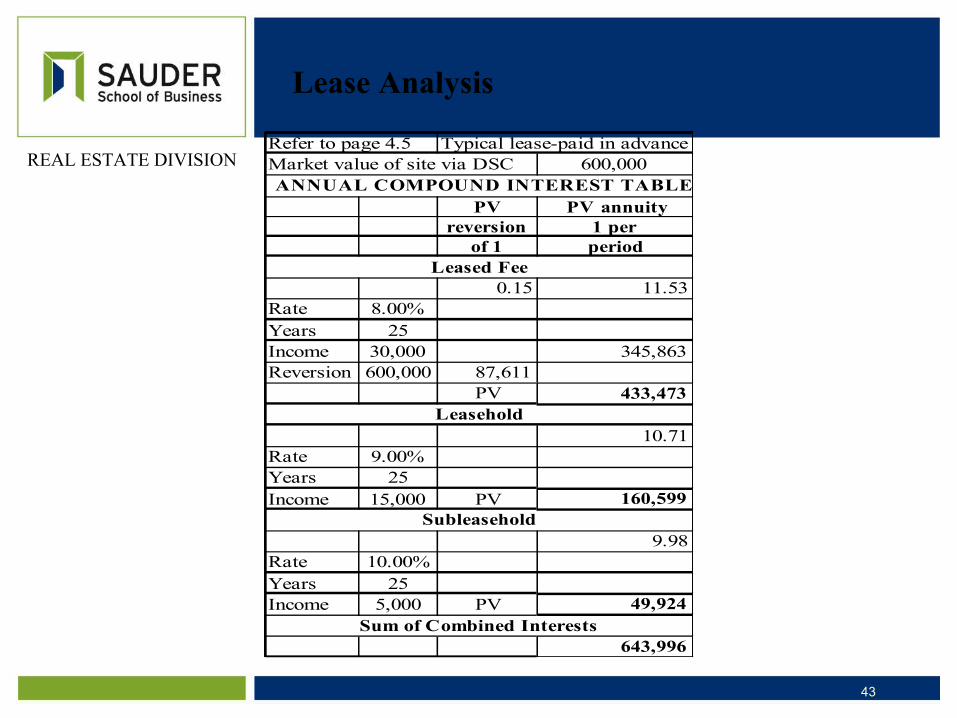

REAL ESTATE DIVISIONRefer to page 4.5 Typical lease-paid in advanceMarket value of site via DSC 600,000

PV PV annuityreversion 1 per

of 1 period

0.15 11.53Rate 8.00%Years 25Income 30,000 345,863Reversion 600,000 87,611

PV 433,473

10.71Rate 9.00%Years 25Income 15,000 PV 160,599

9.98Rate 10.00%Years 25Income 5,000 PV 49,924

643,996Sum of Combined Interests

ANNUAL COMPOUND INTEREST TABLE

Leased Fee

Leasehold

Subleasehold

Lease Analysis

1

REAL ESTATE DIVISION

INTRODUCTION TO LEASING

CHAPTER THREE

2

REAL ESTATE DIVISION

A lease is the lifeblood of an income-property. A property with a vacant building is difficult to sell unless, of course, its value is all in its site; and it will sell for less than a fully leased property.

THE LEASE

3

REAL ESTATE DIVISION

•Names•Estate being created•Premises description•Commencement date•Term•Rent and payment method•Signatures•Covenants and conditions

MAIN ELEMENTS OF A LEASE

4

REAL ESTATE DIVISION

•Net lease-tenant pays base rent plus all expenses•Gross lease-tenant only pays base rent

LEASE TYPES

5

REAL ESTATE DIVISION

For retail/office and industrial properties gross leases are becoming rare. Check the lease and back-out any expenses paid by landlord to find net rent that actually goes into the landlord's pocket.

GROSS LEASE

6

REAL ESTATE DIVISION

Face rates shown in net leases are often stated as net rates but do not reflect tenant inducements provided by the landlord or repayment of fixturing paid for by the landlord.

BE CAREFUL-NET LEASE

7

REAL ESTATE DIVISION

Read the lease carefully and interview the landlord. Adjust the face rate for any landlord TIs such as free parking, free rent for fixturing time, and payments made by landlord towards tenant improvements. The result is net effective rent that goes to the landlord

Net Income-Net Lease

8

REAL ESTATE DIVISION

Try this test.

TEST (mc2)

9

REAL ESTATE DIVISION

•Cumbersome to remove when lease terminates•Information available for competition•Requires greater management including registrable plan by a surveyor.

Lease registration

10

REAL ESTATE DIVISION

Have a go at this question.

TEST (mc3)

11

REAL ESTATE DIVISION

•Inflation hedge•Minimum management (mainly net leases)•Tax benefits (lease to avoid cap gains tax)•Security•Marketability (good tenant=lower risk)•Mortgageability (good tenant=lower risk)•Simpler default procedure (easier to evict than foreclose)

LEASE BENEFITS TO LESSOR

12

REAL ESTATE DIVISION

•Financing technique (no need to purchase, equivalent to 100% mortgage)•Tax benefits (rent is deductible)•Security (provides firm rental term)•Sale leaseback (cash and tax benefits)

LEASE BENEFITS TO LESSEE

13

REAL ESTATE DIVISION

•Bradford-Bank of Montreal•Quadra and McKenzie-Telus•Toronto-4-unit industrial building•Victoria-waterfront site

IMPACT OF LEASES ON MV

14

REAL ESTATE DIVISION

Try this question

TEST (mc4)

15

REAL ESTATE DIVISION

Methods of establishing lease rate:•% of upland mv adjusted for zones of value•Comparison with similar waterlot rates

WATERLOT LEASE

16

REAL ESTATE DIVISION

LEASE ANALYSIS

CHAPTER FOUR

17

REAL ESTATE DIVISION

Small differences in net operating income create large value differences when capitalized, particularly when the market is strong and cap rates are low. A $1 psf rental error at 6.0% cap for a 30,000 sf building is an mv error of $500,000

BE CAREFUL OUT THERE

18

REAL ESTATE DIVISION

•Estimate MV with market rents then adjust for pv of leasehold interests (use this)•Estimate mv and allocate value between leased fee and leasehold interests (seldom used)

INCOME VALUATION METHODS

19

REAL ESTATE DIVISIONRefer to page 4.5 Typical lease-paid in advanceMarket value of site via DSC 600,000

PV PV annuityreversion 1 per

of 1 period

0.15 11.53Rate 8.00%Years 25Income 30,000 345,863Reversion 600,000 87,611

PV 433,473

10.71Rate 9.00%Years 25Income 15,000 PV 160,599

9.98Rate 10.00%Years 25Income 5,000 PV 49,924

643,996Sum of Combined Interests

ANNUAL COMPOUND INTEREST TABLE

Leased Fee

Leasehold

Subleasehold

Example of Allocation-25 Year Term

20

REAL ESTATE DIVISION

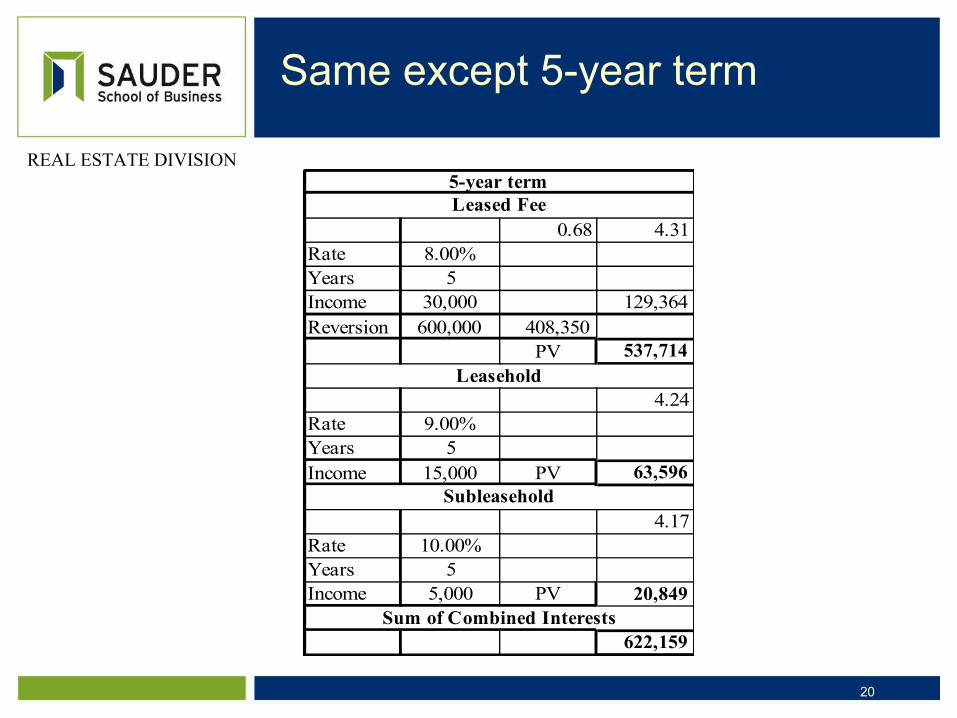

Same except 5-year term

0.68 4.31Rate 8.00%Years 5Income 30,000 129,364Reversion 600,000 408,350

PV 537,714

4.24Rate 9.00%Years 5Income 15,000 PV 63,596

4.17Rate 10.00%Years 5Income 5,000 PV 20,849

622,159Sum of Combined Interests

5-year termLeased Fee

Leasehold

Subleasehold

21

REAL ESTATE DIVISION

Very difficult to estimate remaining economic life of a building for reversionary adjustment and unrealistic to include in discounted cashflow. Cap rate normally adjusts for quality and condition of building. Older building with low reversion value=higher cap

Improved Property Lease-p 4.9

22

REAL ESTATE DIVISION

The valuation problem illustrated on page 4.12 is so unusual that we won't spend much time on it. Just remember that this type of problem is handled by drawing timelines, estimating NPV of each of the interests, and summing them.

COMPLICATED LEASE PROBLEM

23

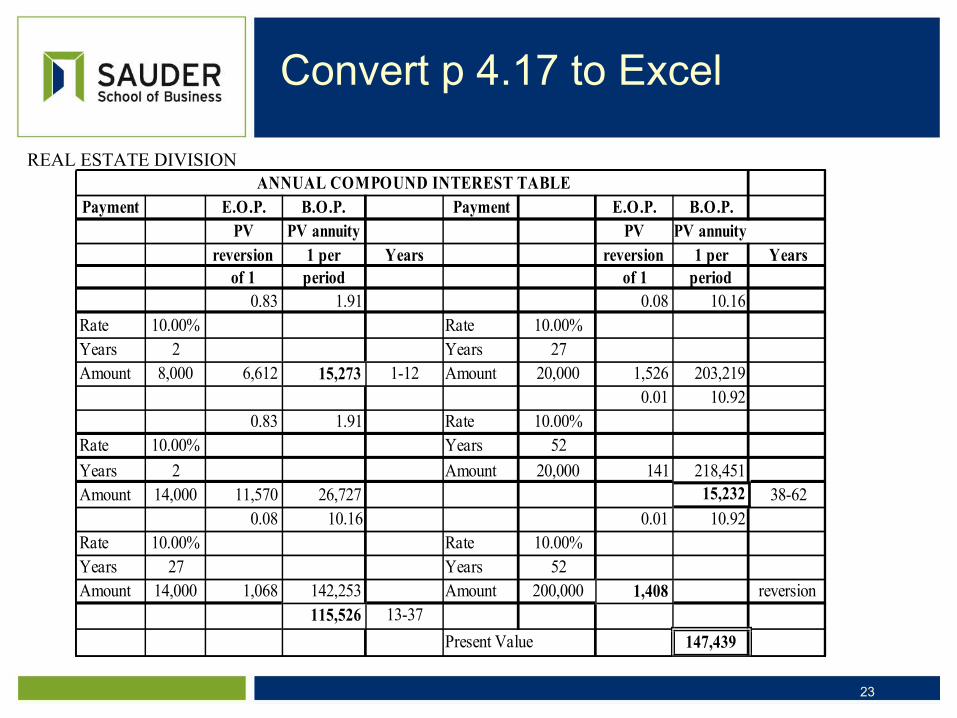

REAL ESTATE DIVISION

Convert p 4.17 to Excel

Payment E.O.P. B.O.P. Payment E.O.P. B.O.P.PV PV annuity PV PV annuity

reversion 1 per Years reversion 1 per Yearsof 1 period of 1 period

0.83 1.91 0.08 10.16Rate 10.00% Rate 10.00%Years 2 Years 27Amount 8,000 6,612 15,273 1-12 Amount 20,000 1,526 203,219

0.01 10.920.83 1.91 Rate 10.00%

Rate 10.00% Years 52Years 2 Amount 20,000 141 218,451Amount 14,000 11,570 26,727 15,232 38-62

0.08 10.16 0.01 10.92Rate 10.00% Rate 10.00%Years 27 Years 52Amount 14,000 1,068 142,253 Amount 200,000 1,408 reversion

115,526 13-37Present Value 147,439

ANNUAL COMPOUND INTEREST TABLE

24

REAL ESTATE DIVISION

Shopping centres and food stores tend to have percentage leases, but lenders rely on base rates. Most percentage leases I've valued did not reach percentage rent trigger levels and stayed at base rates.

PERCENTAGE RENT

25

REAL ESTATE DIVISION

Doctored documents in Newmarket

Due diligence-verify, verify, verify

Do not assume

PRACTITIONER BEWARE

26

REAL ESTATE DIVISION

If valuing an improved property and a ground lease is in place with no renewal options, beware. MV of lessee's interest only extends to the end of the ground lease. Always check title. Know the interest you are analyzing.

GROUND LEASE IMPACT

27

REAL ESTATE DIVISION

TAXATION OFREAL ESTATE INVESTMENTS

CHAPTER FIVE

28

REAL ESTATE DIVISION

Unless you are an accountant, don't act like one.

BEST ADVICE