bus 4254/20/2015 1 legal liability bus 4254/20/2015 2

TRANSCRIPT

BUS 425 4/20/20154/20/2015 1

legal liability

BUS 425 4/20/20154/20/2015 2

BUS 425 4/20/20154/20/2015 3

Cases to study

Common Law (Torts)

Ultramares Corp v Touche (1931)

Credit Alliance v Arthur Andersen (1986)

Rusch Factors v. Levin (1968)

Restatement Second of Torts (1977)

Rosenblum v Adler (1983)

Statute Law

Securities Act of 1933 Section 11

Securities & Exchange Act of 1934 Sec 10b-5

Ernst & Ernst v Hochfelder (1976)

BUS 425 4/20/20154/20/2015 4

vocabulary

BUS 425 4/20/20154/20/2015 5

Peter

describe business failure

BUS 425 4/20/20154/20/2015 6

Juancarlos

define audit risk

BUS 425 4/20/20154/20/2015 7

Algernon

describe limited liability partnership LLP

BUS 425 4/20/20154/20/2015 8

LLP limited liability partnership

• Taxed like a general partnership• Partners are personally liable for the

partnership’s debts and obligations• Partners are personally liable for their own acts,

and the acts of others under their supervision

• Partners are not personally liable for liabilities arising from negligent acts of other partners and employees not under their supervision

BUS 425 4/20/20154/20/2015 9

statute law common law

breach of contract tort

joint & several liab proportionate liab

standard of care

privity of contract v. third parties

near privity

BUS 425 4/20/20154/20/2015 10

David

describe common law

describe statute law

BUS 425 4/20/20154/20/2015 11

common lawcontract law (applies to the audit client)

tort law (applies to third parties)

statute lawSecurities Act of 1933

Securities Exchange Act of 1934Foreign Corrupt Practices Act of 1977

The Sarbanes Oxley Act of 2002

BUS 425 4/20/20154/20/2015 12

State Law Federal Law

Common Law Auditors auditors

Statute Law auditors Auditors

BUS 425 4/20/20154/20/2015 13

Common Law

BUS 425 4/20/20154/20/2015 14

Jeff

What is the difference between a

Breach of Contractand a

Tort

BUS 425 4/20/20154/20/2015 15

Tort

• American Heritage DictionaryAmerican Heritage Dictionary

• A wrongful act, damage, or injury done willfully, negligently, or in circumstances involving strict liability, but not involving a breach of contract.

BUS 425 4/20/20154/20/2015 16

Pei

What type of action would we expect

The audit client to file against the auditor?

Some one who invested in the audit client to file against the auditor?

BUS 425 4/20/20154/20/2015 17

Bart

Discuss the difference between

joint and several liability

proportionate liability

BUS 425 4/20/20154/20/2015 18

standard of care

ordinary negligence

gross negligence

recklessnessconstructive fraud

fraud

BUS 425 4/20/20154/20/2015 19

John

discuss ordinary negligence

BUS 425 4/20/20154/20/2015 20

Cody

discuss gross negligence

BUS 425 4/20/20154/20/2015 21

Garren

discuss fraud

BUS 425 4/20/20154/20/2015 22

what standard of care (level of performance)

is unacceptable for a professional ?

Melissa

BUS 425 4/20/20154/20/2015 23

Breach of Contract

what standard of care unacceptable if the plaintiff has privity of contract and brings the lawsuit under breach of contract ?

Emily

BUS 425 4/20/20154/20/2015 24

Common Law - Tort

In order to recover from an auditor under common law, the plaintiff must prove

•Duty to perform•Breach of Duty•Losses•Causation

BUS 425 4/20/20154/20/2015 25

Burden of ProofThird-party investors must demonstrate

• Auditor had a Duty to perform• Breach of Duty – the Auditor was negligent, did

not exercise due professional care• Contributory negligence not an issue in most cases dealing with third party

investors

• They suffered a Loss• Causation – the loss was caused by reliance on

financial statements which were materially misstated

BUS 425 4/20/20154/20/2015 26

when talking about Common Law Tort

(if the plaintiff is not in privity of contract with the auditor)

• Where fraud or gross negligence is present, most jurisdictions expand the rights of third party investors who do not have privity of contract.

• Where fraud or gross negligence is present, we assume the auditor will be held liable to third parties using the financial statements.

BUS 425 4/20/20154/20/2015 27

Common Law - Tort (not in privity)

third parties

To which third parties are we liable for

Ordinary Negligence ?

BUS 425 4/20/20154/20/2015 28

Jeanette

Different jurisdictions hold auditors liable for ordinary negligence to different ‘classes of third parties’

what are the three different classes of

“third parties”

BUS 425 4/20/20154/20/2015 29

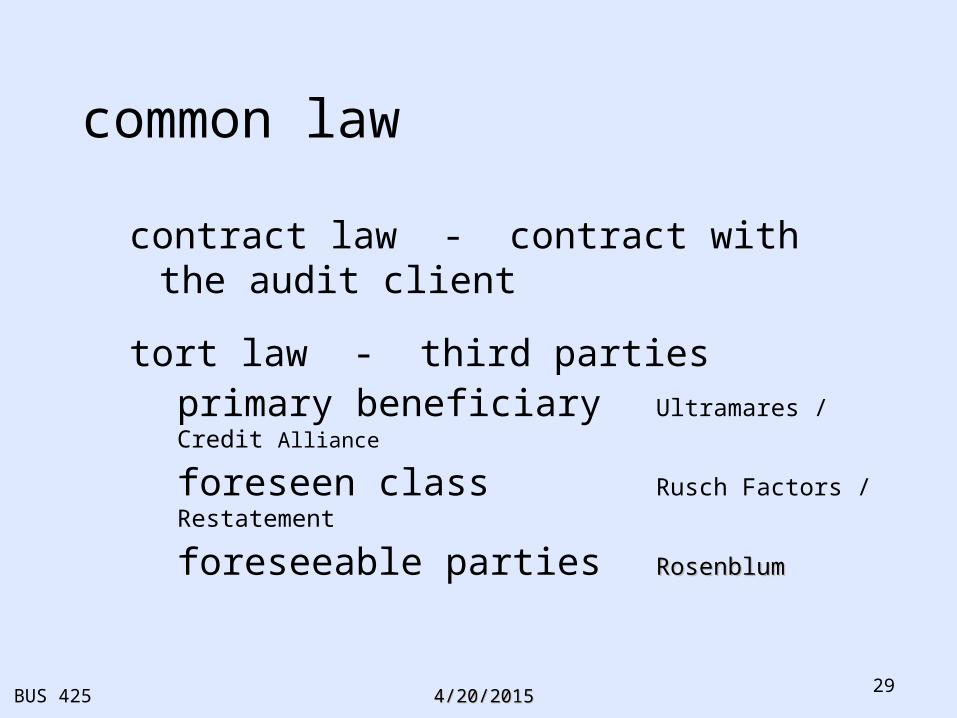

common law

contract law - contract with the audit client

tort law - third partiesprimary beneficiary Ultramares / Credit Alliance

foreseen class Rusch Factors / Restatement

foreseeable parties RosenblumRosenblum

BUS 425 4/20/20154/20/2015 30

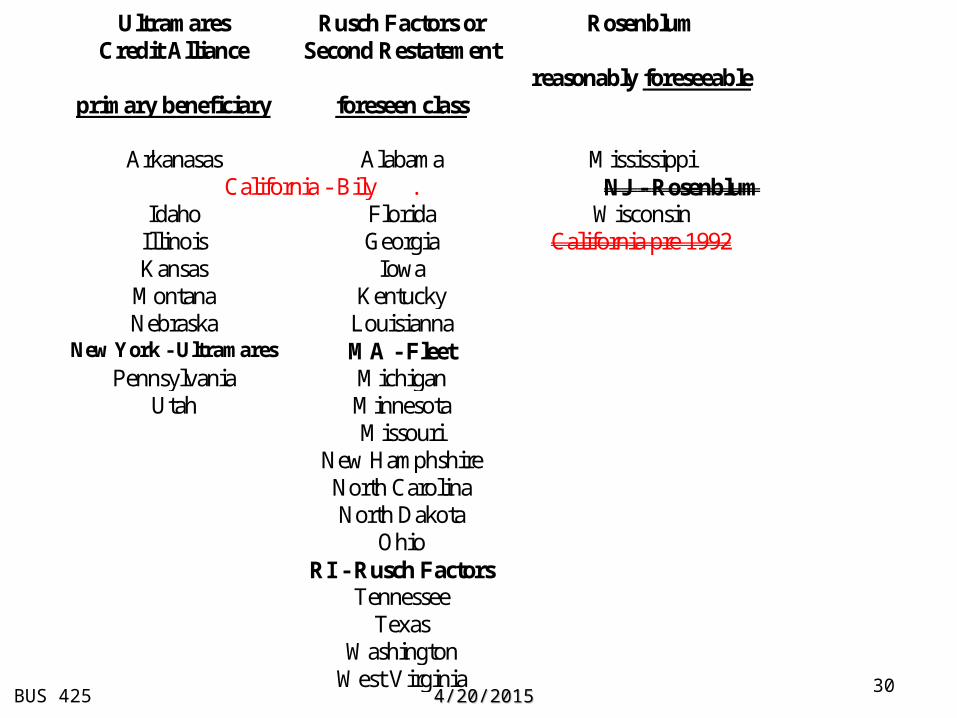

Ultramares Credit Alliance

Rusch Factors or Second Restatement

Rosenblum

primary beneficiary

foreseen class

reasonably foreseeable

Arkanasas Alabama Mississippi

California - Bily . NJ - Rosenblum Idaho Florida Wisconsin

Illinois Georgia California pre 1992 Kansas Iowa

Montana Kentucky Nebraska Louisianna

New York - Ultramares MA - Fleet Pennsylvania Michigan

Utah Minnesota Missouri New Hamphshire North Carolina North Dakota Ohio RI - Rusch Factors Tennessee Texas Washington West Virginia

BUS 425 4/20/20154/20/2015 31

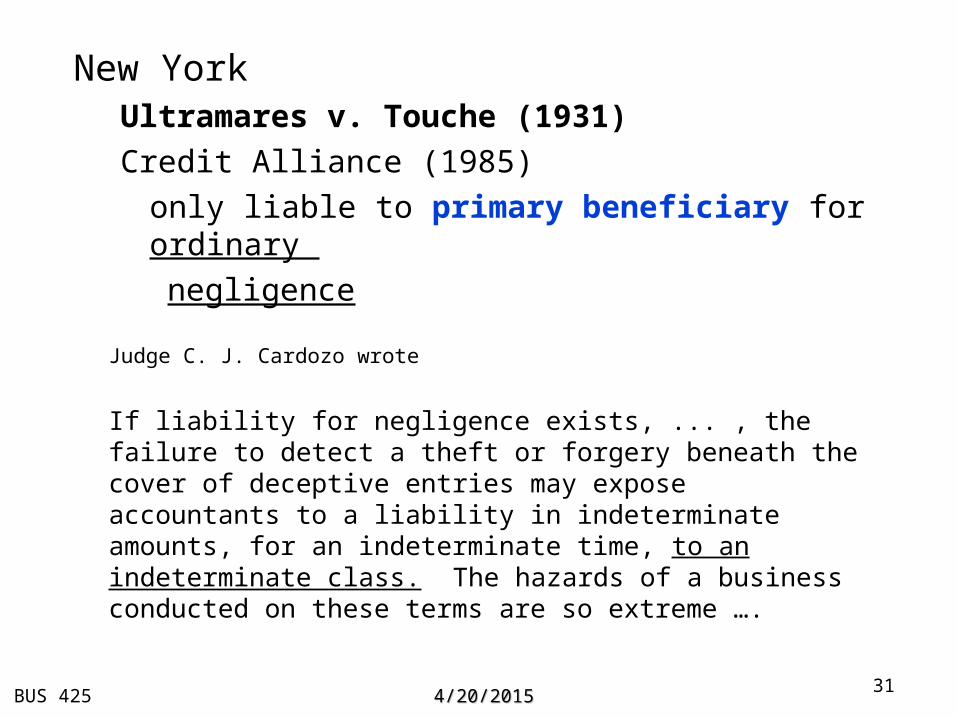

New YorkUltramares v. Touche (1931)

Credit Alliance (1985)

only liable to primary beneficiary for ordinary

negligence

Judge C. J. Cardozo wrote

If liability for negligence exists, ... , the failure to detect a theft or forgery beneath the cover of deceptive entries may expose accountants to a liability in indeterminate amounts, for an indeterminate time, to an indeterminate class. The hazards of a business conducted on these terms are so extreme ….

BUS 425 4/20/20154/20/2015 32

New YorkUltramares (1931)

Credit Alliance v Arthur Andersen (1985)

only liable to primary beneficiary for ordinary negligence

• accountant must have been aware that the financial reports were to be used for a particular purpose

• In furtherance of which a known party(ies) was intended to rely• There must have been some conduct on the part of the

accountants which evinces the accountant’s understanding of that party(ies) reliance.

• New York Superior Court

BUS 425 4/20/20154/20/2015 33

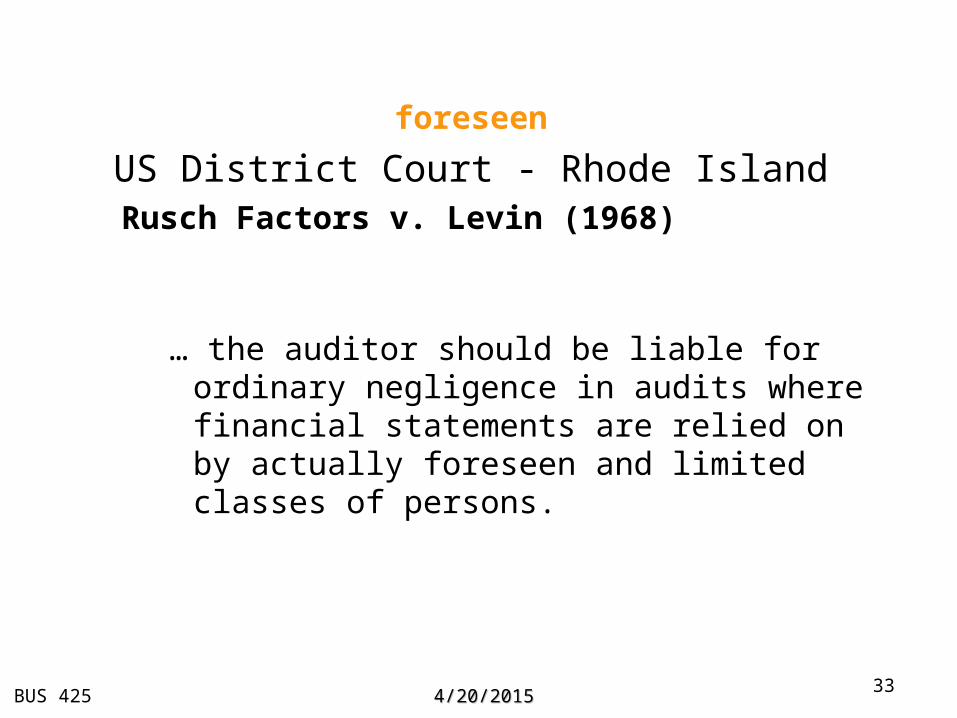

foreseen

US District Court - Rhode IslandRusch Factors v. Levin (1968)

… the auditor should be liable for ordinary negligence in audits where financial statements are relied on by actually foreseen and limited classes of persons.

BUS 425 4/20/20154/20/2015 34

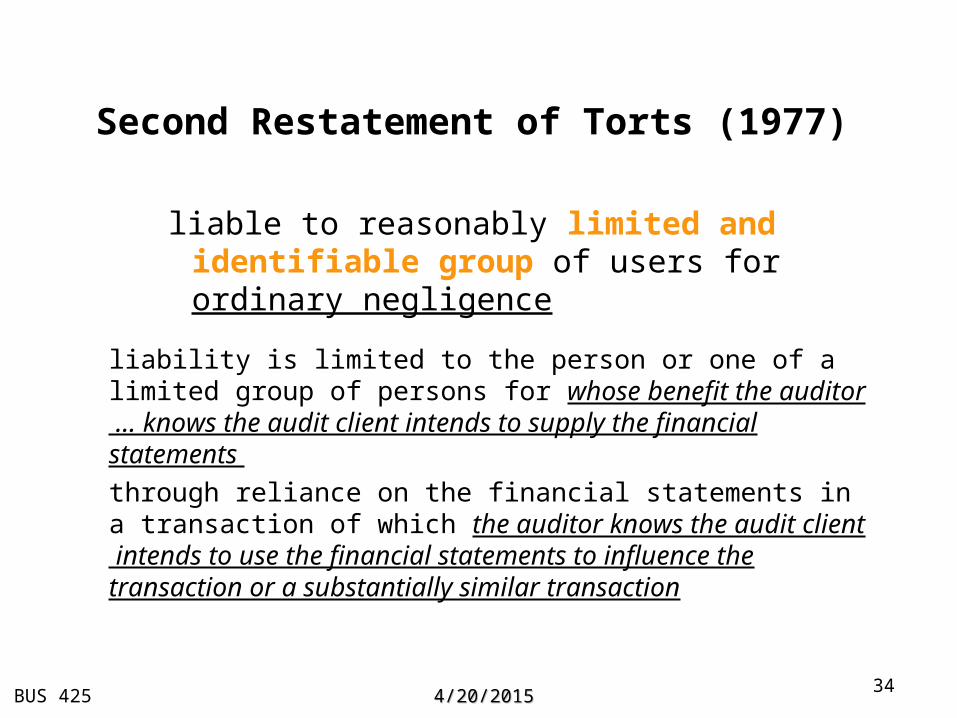

Second Restatement of Torts (1977)

liable to reasonably limited and identifiable group of users for ordinary negligence

liability is limited to the person or one of a limited group of persons for whose benefit the auditor … knows the audit client intends to supply the financial statements

through reliance on the financial statements in a transaction of which the auditor knows the audit client intends to use the financial statements to influence the transaction or a substantially similar transaction

BUS 425 4/20/20154/20/2015 35

Second Restatement of Torts (1977)

liable to reasonably limited and identifiable group of users for ordinary negligence

an auditor is liable for negligence to a third party only if (s)he intends to supply the information for the benefit of one or more third parties in a specific transaction or type of transaction identified to the supplier.

BUS 425 4/20/20154/20/2015 36

• To offer a simple illustration … an auditor engaged to perform an audit and render a report to a third person whom the auditor knows is considering a $ 10 million investment in the client's business is on notice of a specific potential liability. It may then act to encounter, limit or avoid the risk.

• In contrast, an auditor who is simply asked for a generic audit and report to the client has no comparable notice.

BUS 425 4/20/20154/20/2015 37

• For example, the auditor may be held liable to a third party lender if the auditor is informed by the client that the audit will be used to obtain a $ 50,000 loan, even if the specific lender remains unnamed or the client names one lender and then borrows from another.

BUS 425 4/20/20154/20/2015 38

• Similarly, there is no liability when the client's transaction (as represented to the auditor) changes so as to increase materially the audit risk, e.g., a third person originally considers selling goods to the client on credit and later buys a controlling interest in the client's stock, both in reliance on the auditor's report.

BUS 425 4/20/20154/20/2015 39

• Under the Restatement rule, an auditor retained to conduct an annual audit and to furnish an opinion for no particular purpose generally undertakes no duty to third parties.

• …• The client uses the financial statements to obtain a

loan from bank. Because of negligence, the auditor issues an unmodified opinion upon a balance sheet that materially misstates the financial position … through reliance upon it the bank suffers …. a loss."

• Consistent with the text of section 552, the authors conclude: "The auditor is not liable to the bank."

BUS 425 4/20/20154/20/2015 40

New Jersey (Supreme Court of N.J)

Rosenblum v Adler (1983) p. 120

liable to reasonably foreseeable parties for ordinary negligence

BUS 425 4/20/20154/20/2015 41

remember,

there is a body of federal common law

but most common law pertaining to securities is state common law

each state has its own body of common law

so, we will make up an example and move our example around the country

BUS 425 4/20/20154/20/2015 42

New York

Mary bought some Kar Sales, Inc. common stock

Kar Sales, Inc. is not publicly traded. They are not required to file with the SEC

Kar Sales, Inc. had their financial statements audited …. In order to get a bank loan.

They told their auditor they were having their financial statements audited to get a …….. bank loan.

Kar Sales, Inc. suffers a major loss and is going bankrupt

BUS 425 4/20/20154/20/2015 43

primary beneficiary

( state courts of New York )

BUS 425 4/20/20154/20/2015 44

Mary files a common law claim in a New York court

Mary can show that the auditor was negligent

Is Mary likely to prevail?

To which case will the N.Y. courts look for guidance about auditors’ liability ?

Priya

BUS 425 4/20/20154/20/2015 45

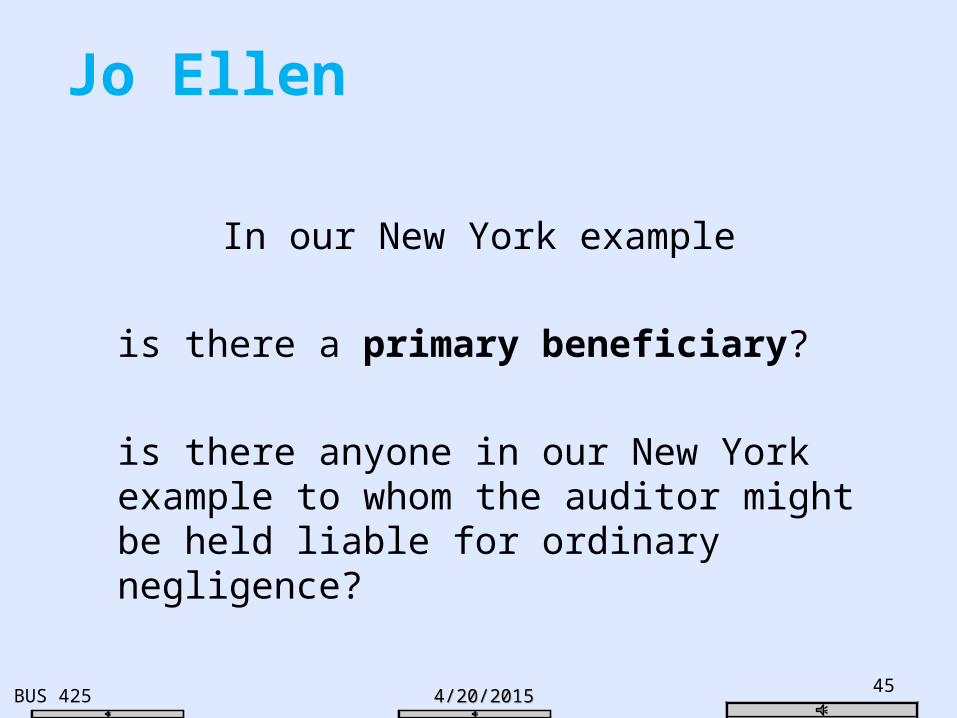

In our New York example

is there a primary beneficiary?

is there anyone in our New York example to whom the auditor might be held liable for ordinary negligence?

Jo Ellen

BUS 425 4/20/20154/20/2015 46

standard of care (in New York)

ordinary negligence primary beneficiaries yesforeseen class no

foreseeable parties no

gross negligence primary beneficiaries yes

recklessness foreseen class yes

constructive fraud foreseeable parties yes

fraud

BUS 425 4/20/20154/20/2015 47

let’s move our example toRhode Island

Mary bought some Kar Sales, Inc. common stock

Kar Sales, Inc. is not publicly traded. They are not required to file with the SEC

Kar Sales, Inc. had their financial statements audited …. In order to get a bank loan.

They told their auditor they were having their financial statements audited to get a …….. bank loan.

Kar Sales, Inc. suffers a major loss and is going bankrupt

BUS 425 4/20/20154/20/2015 48

foreseen class

( state courts of Rhode Island)

BUS 425 4/20/20154/20/2015 49

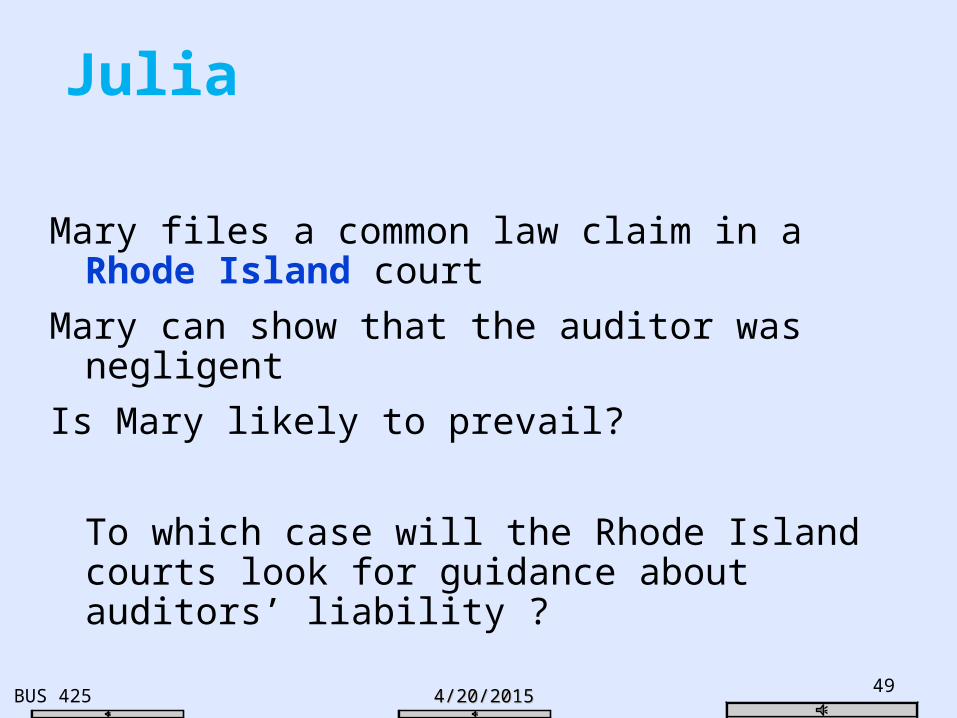

Mary files a common law claim in a Rhode Island court

Mary can show that the auditor was negligent

Is Mary likely to prevail?

To which case will the Rhode Island courts look for guidance about auditors’ liability ?

Julia

BUS 425 4/20/20154/20/2015 50

In our Rhode Island example

is there anyone in our Rhode Island example who might be an actually foreseen and limited class of persons or a foreseen party to whom the auditor would be liable for ordinary negligence?

Mackenzie

BUS 425 4/20/20154/20/2015 51

standard of care (in Rhode Island)

ordinary negligence primary beneficiaries yesforeseen class yes

foreseeable parties no

gross negligence primary beneficiaries yes

recklessness foreseen class yes

constructive fraud foreseeable parties yes

fraud

BUS 425 4/20/20154/20/2015 52

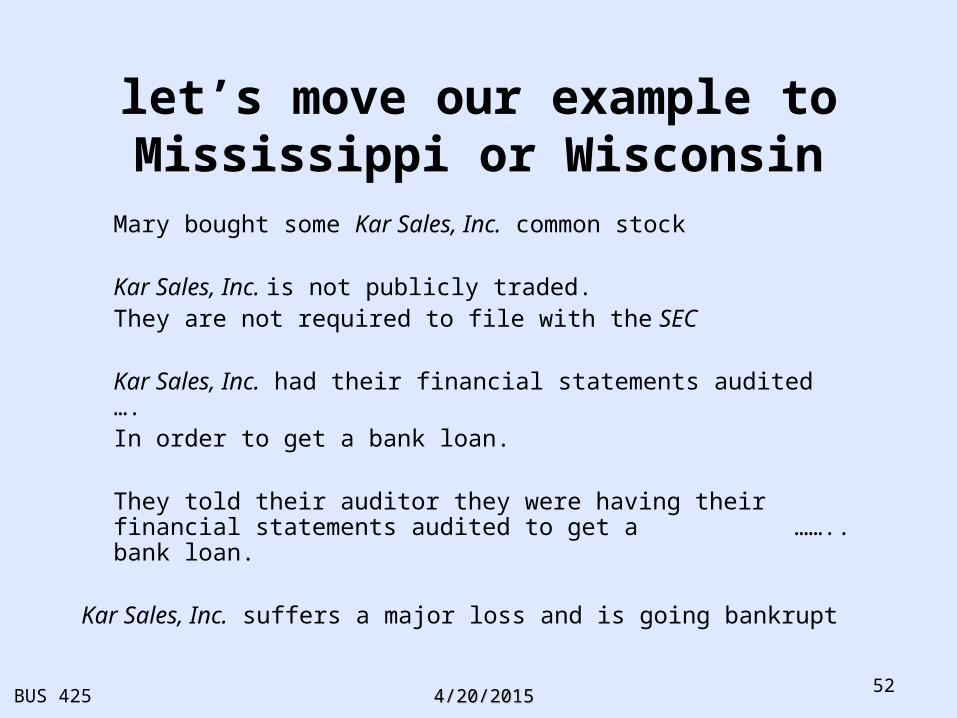

let’s move our example to Mississippi or Wisconsin

Mary bought some Kar Sales, Inc. common stock

Kar Sales, Inc. is not publicly traded. They are not required to file with the SEC

Kar Sales, Inc. had their financial statements audited …. In order to get a bank loan.

They told their auditor they were having their financial statements audited to get a …….. bank loan.

Kar Sales, Inc. suffers a major loss and is going bankrupt

BUS 425 4/20/20154/20/2015 53

reasonably foreseeable parties

( state courts of Mississippi or Wisconsin )

BUS 425 4/20/20154/20/2015 54

Mary files a common law claim in a Mississippi court

Mary can show that the auditor was negligent

Is Mary likely to prevail?

To which case will the Mississippi courts look for guidance about auditors’ liability ?

Meredith

BUS 425 4/20/20154/20/2015 55

BUS 425 4/20/20154/20/2015 56

who, in our Mississippi example, would be a reasonably foreseeable party ?

Jordan

BUS 425 4/20/20154/20/2015 57

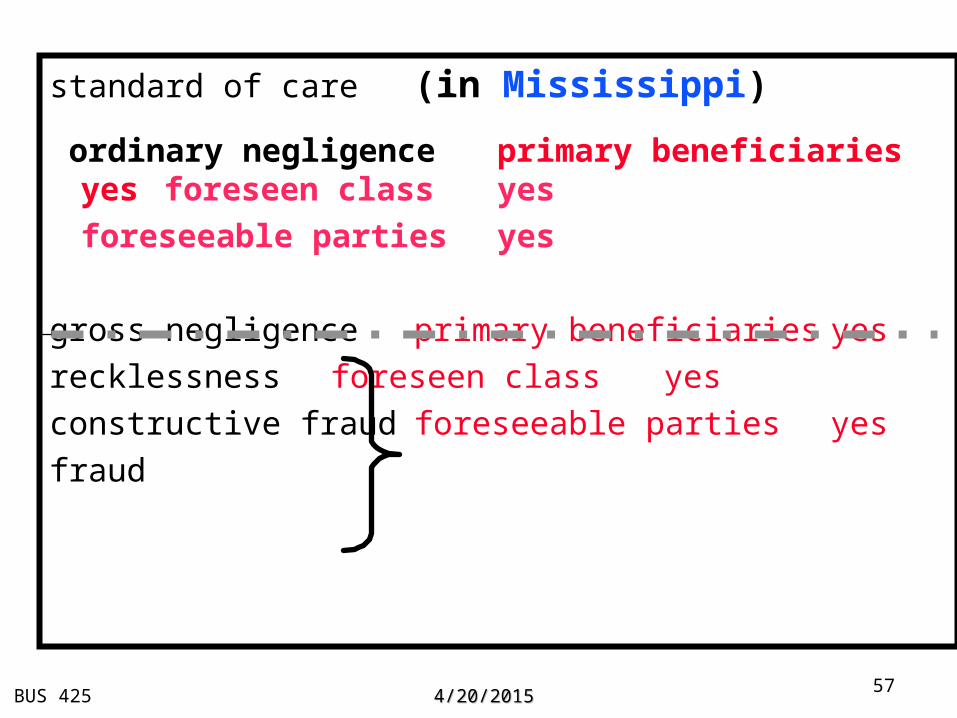

standard of care (in Mississippi)

ordinary negligence primary beneficiaries yesforeseen class yes

foreseeable parties yes

gross negligence primary beneficiaries yes

recklessness foreseen class yes

constructive fraud foreseeable parties yes

fraud

BUS 425 4/20/20154/20/2015 58

Ultramares Credit Alliance

Rusch Factors or Second Restatement

Rosenblum

primary beneficiary

foreseen class

reasonably foreseeable

Arkanasas Alabama Mississippi

California - Bily . NJ - Rosenblum Idaho Florida Wisconsin

Illinois Georgia California pre 1992 Kansas Iowa

Montana Kentucky Nebraska Louisianna

New York - Ultramares MA - Fleet Pennsylvania Michigan

Utah Minnesota Missouri New Hamphshire North Carolina North Dakota Ohio RI - Rusch Factors Tennessee Texas Washington West Virginia

BUS 425 4/20/20154/20/2015 59

Securities Lawstart here

BUS 425 4/20/20154/20/2015 60

Securities Law

• Securities Act of 1933 ( section 11 )

• Securities Exchange Act of 1934 ( section 10 b-5 )

– Foreign Corrupt Practices Act (1977)– Sarbanes-Oxley Act (2002)

BUS 425 4/20/20154/20/2015 61

Geri, the General Manager of Kar Sales Inc., which is a closely held (not publicly owned) company in San Luis Obispo

Geri the Gen. Manager owns stock in Kar Sales Inc.

Geri needs some money, so she writes her friend Mary, who lives in New York, and asks her if she would like to buy some of her Kar Sales Inc. stock

Geri also mails a copy of Kar Sales Inc. financial statements which have been audited by Miller LLP to Mary

Mary buys some stock from Geri

BUS 425 4/20/20154/20/2015 62

Kar Sales Inc. suffers a large loss and is going bankrupt

BUS 425 4/20/20154/20/2015 63

Securities Act of 1933

BUS 425 4/20/20154/20/2015 64

Mary’s attorney believes she can show that the auditor was negligent

is Mary likely to prevail if she sues under the Securities Act of 1933

Joseph

BUS 425 4/20/20154/20/2015 65

Securities Act of 1933 initial public offerings

any person acquiring the security

plaintiff (the person acquiring in this case) is not required to show reliance

auditor liable for ordinary negligence

BUS 425 4/20/20154/20/2015 66

Securities Act of 1933 section 11

any part of the registration statement ... contained an untrue statement of a material fact or omitted to state a material fact

BUS 425 4/20/20154/20/2015 67

standard of care under 1933 Act

ordinary negligence

gross negligence

recklessness

constructive fraud

fraud

BUS 425 4/20/20154/20/2015 68

Levi

what type of stock transactions does the 1933 Securities Act regulate ?

what type of stock transactions does the 1934 Securities Exchange Act regulate ?

BUS 425 4/20/20154/20/2015 69

Securities Act of 1933

who sells stock in an “IPO” ?

who produces the financial statements ?

whose interests need be protected in an IPO?

BUS 425 4/20/20154/20/2015 70

Peter

who sells stock in an “IPO” ?

who produces the financial statements ?

whose interests need be protected in an IPO?

BUS 425 4/20/20154/20/2015 71

Securities Exchange Act of 1934

BUS 425 4/20/20154/20/2015 72

Geri, the General Manager of Kar Sales Inc., which is a closely held (not publicly owned) company in San Luis Obispo

Geri the Gen. Manager owns stock in Kar Sales Inc.

Geri needs some money, so she writes her friend Mary, who lives in New York, and asks her to buy some of her stock

Geri also mails a copy of Kar Sales Inc. financial statements which have been audited by Miller LLP to Mary

Mary buys some stock from Geri

BUS 425 4/20/20154/20/2015 73

Kar Sales Inc. suffers a large loss and is going bankrupt

BUS 425 4/20/20154/20/2015 74

Mary’s attorney thinks she can show that the auditor was negligent

Is Mary likely to prevail if she sues under the Securities Exchange Act of 1934

Remember: Mary lives in New York and the General Manager of Kar Sales Inc. mailed the audited financial statements to her from SLO

Juancarlos

BUS 425 4/20/20154/20/2015 75

Securities Exchange Act of 1934 section 10b-5

... by use of any means or instrumentality of interstate commerce or of the mails, or of any facility of any national securities exchange

to employ, any device, scheme or artifice to defraud

to make any untrue statement of material fact of to omit to make

to engage in any practice or course of business which operates as a fraud or deceit upon any person...

BUS 425 4/20/20154/20/2015 76

What is the applicable “standard of care” under the

Securities Exchange Act of 1934 ?

Is Mary likely to prevail under the 1934 Act if she can prove the auditor was negligent ?

Algernon

BUS 425 4/20/20154/20/2015 77

Securities Exchange Act of 1934secondary markets

any person acquiring or selling the security

plaintiff must show reliance

Hochfelder p. 123

auditor is not liable for ordinary negligence

BUS 425 4/20/20154/20/2015 78

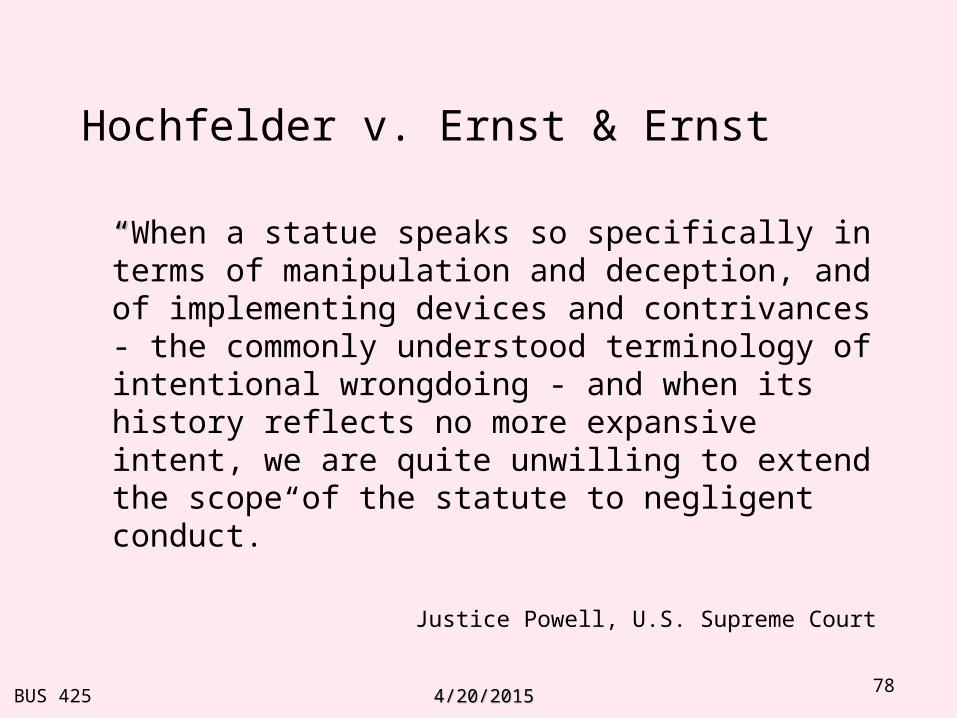

Hochfelder v. Ernst & Ernst

““When a statue speaks so specifically in terms of manipulation and deception, and of implementing devices and contrivances - the commonly understood terminology of intentional wrongdoing - and when its history reflects no more expansive intent, we are quite unwilling to extend the scope of the statute to negligent conduct.”

Justice Powell, U.S. Supreme Court

BUS 425 4/20/20154/20/2015 79

standard of care

ordinary negligence

gross negligence

recklessness

constructive fraud

fraud

BUS 425 4/20/20154/20/2015 80

David

who sells stock in the “secondary markets”?

who produces the financial statements ?

whose interests need be protected in secondary market exchanges ?

BUS 425 4/20/20154/20/2015 81

SUMMARY OF DIFFERENCES BETWEEN 1933 AND 1934 ACTS

Item 1933 Act 1934 Act

Plaintiff Any person

acquiring Either buyer or seller

Plaintiff must prove reliance

No Yes

Defendant liable for ordinary negliegence

Yes No

BUS 425 4/20/20154/20/2015 82

Do we agree that auditors, or any professionals, should be liable for gross negligence, recklessness, constructive fraud, or fraud?

Notice that the Federal Security’s Laws don’t offer investors recourse for ‘ordinary negligence’ in the secondary markets

BUS 425 4/20/20154/20/2015 83

In order to manage legal liability

Understand the client’s business

Document your work

Professional skepticism

BUS 425 4/20/20154/20/2015 84

Professional skepticism

An attitude that includes a questioning mind and a critical assessment of audit evidence.

`` Auditors should not assume that management is dishonest, but the possibility of dishonesty should be considered. At the same time, auditors should not assume that management is unquestionably honest.

BUS 425 4/20/20154/20/2015 85

timing is important

BUS 425 4/20/20154/20/2015 86

common law liability to third partiesfor ordinary negligence

1931 Ultramares New York

1968 Rusch Factors Rhode Island

1983 Rosenblum New Jersey

BUS 425 4/20/20154/20/2015 87

common law liability to third partiesfor ordinary negligence

in California (Supreme Court of CA)

• 1986– International Mortgage (foreseeable parties)

BUS 425 4/20/20154/20/2015 88

BUS 425 4/20/20154/20/2015 89

Ultramares Credit Alliance

Rusch Factors or Second Restatement

Rosenblum

primary beneficiary

foreseen class

reasonably foreseeable

Arkanasas Alabama Mississippi

. NJ - Rosenblum Idaho Florida Wisconsin

Illinois Georgia California pre 1992 Kansas Iowa

Montana Kentucky Nebraska Louisianna

New York - Ultramares MA - Fleet Pennsylvania Michigan

Utah Minnesota Missouri New Hamphshire North Carolina North Dakota Ohio RI - Rusch Factors Tennessee Texas Washington West Virginia

BUS 425 4/20/20154/20/2015 90

common law liability to third partiesfor ordinary negligence

in California (Supreme Court of CA)

• 1986– International Mortgage (foreseeable parties)

• 1993– Bily (primary beneficiary)

BUS 425 4/20/20154/20/2015 91

Ultramares Credit Alliance

Rusch Factors or Second Restatement

Rosenblum

primary beneficiary

foreseen class

reasonably foreseeable

Arkanasas Alabama Mississippi

California - Bily . NJ - Rosenblum Idaho Florida Wisconsin

Illinois Georgia California pre 1992 Kansas Iowa

Montana Kentucky Nebraska Louisianna

New York - Ultramares MA - Fleet Pennsylvania Michigan

Utah Minnesota Missouri New Hamphshire North Carolina North Dakota Ohio RI - Rusch Factors Tennessee Texas Washington West Virginia

BUS 425 4/20/20154/20/2015 92

things are getting better

BUS 425 4/20/20154/20/2015 93

JOURNAL OF ACCOUNTANCY, AUGUST 1994

GAININGA NEW BALANCEIN THE COURTSSome of the liability burden has disappeared-but a heavey weight remains.

by Randall K Hanson and Joanne W. Rockness

BUS 425 4/20/20154/20/2015 94

BUS 425 4/20/20154/20/2015 95

Reeves v. Ernst & Young

RICO treble damagesracketeer influenced and corrupt practices act

with regards to auditors

U.S. Supreme Court took the teeth out of Federal RICO laws

RICO requires some participation in the operation or management of the enterprise

BUS 425 4/20/20154/20/2015 96

Aid and Abet• To assist another in the commission of a crime by

words or conduct.• The person who aids and abets participates in the

commission of a crime by performing some overt act or by giving advice or encouragement. He or she must share the criminal intent of the person who actually commits the crime, but it is not necessary for the aider and abettor to be physically present at the scene of the crime.

• An aider and abettor is a party to a crime and may be criminally liable as a principal, an accessory before the fact, or an accessory after the fact.

• West's Encyclopedia of American Law, edition 2. Copyright 2008 The Gale Group, Inc. All rights West's Encyclopedia of American Law, edition 2. Copyright 2008 The Gale Group, Inc. All rights reserved.reserved.

BUS 425 4/20/20154/20/2015 97

Central Bank of Denver v. First Interstate BankU.S. Supreme Court 1994

investors and other private parties are no longer able to bring suits against auditors for ‘aiding and abetting’

under section 10B of the Securities Exchange Act of 1934

BUS 425 4/20/20154/20/2015 98

The Private Securities Litigation Reform Act of 1995

amends the Securities Exchange Act of 1934

… liable solely for the portion of the judgment that corresponds to the percentage of responsibility

proportionate liability

Unless it is determined that the person knowingly committed a violation of securities law. In which case they would be jointly and severally liable.

BUS 425 4/20/20154/20/2015 99

The Securities Litigation UniformStandards Act of 1998

with regard to securities litigation

Requires that class action suits with 50 or more parties must be filed in the FEDERAL COURTS.

BUS 425 4/20/20154/20/2015 100

New Jersey Rosenblum v Adler foreseeable parties

N.J.S.A. 2A:53A-25 1995 statute

New Jersey state legislature has subsequently passed legislation that defines auditors liability

because of this statute auditors are no longer liable to foreseeable parties for ordinary negligence in N.J.

BUS 425 4/20/20154/20/2015 101

we still teach Rosenblum even though New Jersey has passed legislation that overturns this case

because the concept of foreseeable parties is still a valid legal concept and Mississippi and Wisconsin adhere to the concept of foreseeable parties

BUS 425 4/20/20154/20/2015 102

BUS 425 4/20/20154/20/2015 103

BUS 425 4/20/20154/20/2015 104