bulletin no. 2002–44 november 4, 2002 highlights of this … · highlights of this issue these...

TRANSCRIPT

HIGHLIGHTSOF THIS ISSUEThese synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

SPECIAL ANNOUNCEMENT

Announcement 2002–101, page 800.This announcement solicts applications from potential part-ners to participate in the 2003 IRS Individual e-file Partner-ship Program. The partnership opportunities are a result ofRRA 98, which requires the IRS to receive 80 percent of allreturns electronically by 2007. RRA 98 authorized the IRSCommissioner to promote the benefits of and encourage theuse of e-file services through partnerships with various en-tities that offer low cost tax preparation and electronic fil-ing of income tax returns for qualified taxpayers. Thoseapplicants that are accepted as partners will have a link(s)and description(s) of their services placed on the IRS web-site at www.irs.gov (IRS e-file Partners Page).

INCOME TAX

Rev. Rul. 2002–69, page 760.Business expenses; interest; lease-in/lease-out transac-tions. A taxpayer may not deduct currently, under sections 162and 163 of the Code, rent and interest paid or incurred in con-nection with a lease-in/lease-out (LILO) transaction that prop-erly is characterized as conferring only a future interest inproperty. Rev. Rul. 99–14 modified and superseded.

Rev. Rul. 2002–71, page 763.Notional principal contract (NPC). This ruling provides guid-ance on the timing of recognition of gain or loss on the termi-nation of a notional principal contract that hedges a portion ofthe term of a debt instrument issued by the taxpayer.

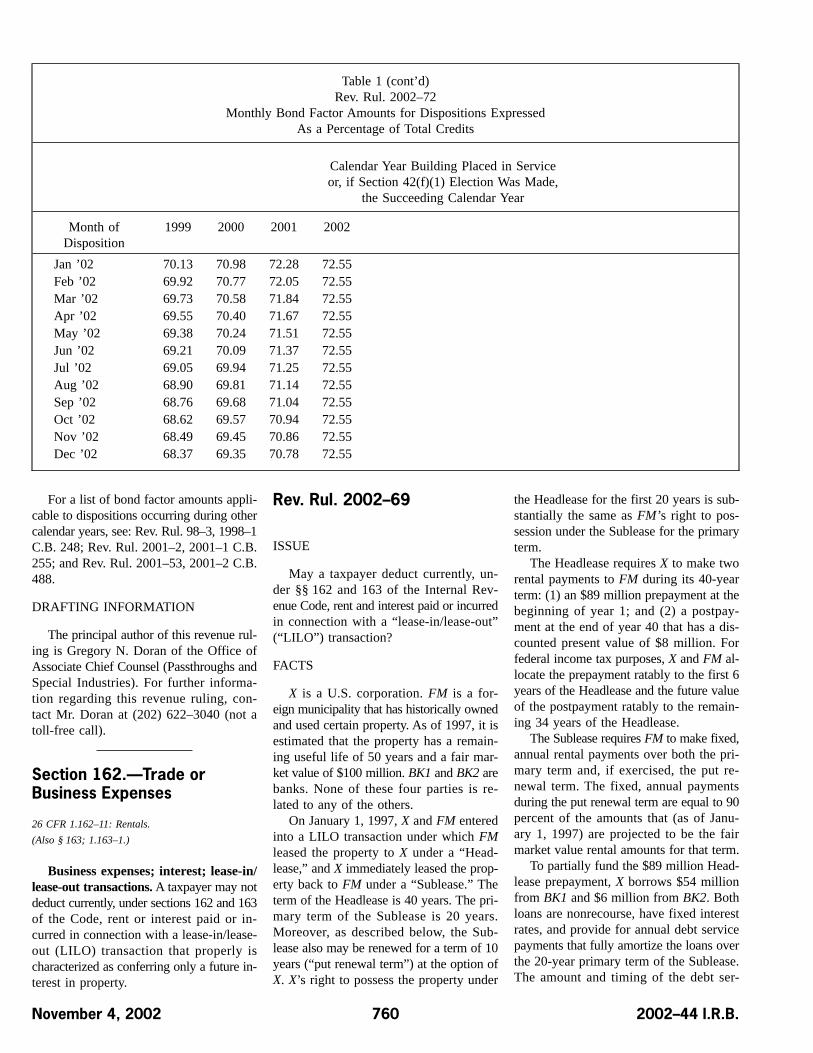

Rev. Rul. 2002–72, page 759.Low-income housing credit; satisfactory bond; “bond fac-tor” amounts for the period October through December2002. This ruling announces the monthly bond factor amountsto be used by taxpayers who dispose of qualified low-incomebuildings or interests therein during the period October through

December 2002. This ruling also provides a summary of the bondfactor amounts for dispositions occurring during the period Janu-ary through September 2002.

REG–112306–00, page 767.Proposed regulations under section 1296 of the Code containprocedures for certain United States persons holding market-able stock in a passive foreign investment company (PFIC) to electmark to market treatment for that stock. A public hearing isscheduled for November 6, 2002.

REG–150313–01, page 777.Proposed regulations under sections 302, 304, and other sec-tions of the Code provide guidance regarding the treatment ofthe basis of redeemed stock when a distribution in redemptionof such stock is treated as a dividend. The regulations also pro-vide guidance regarding certain acquisitions of stock by re-lated corporations that are treated as distributions in redemptionof stock. A public hearing is scheduled for February 20, 2003.

Notice 2002–70, page 765.This notice alerts taxpayers and their representatives about cer-tain reinsurance transactions intended to shift income to off-shore related companies purported to be insurance companiesthat are subject to little or no U.S. federal income tax. These trans-actions often do not generate the federal tax benefits that tax-payers claim are allowable for federal income tax purposes. Thisnotice also alerts taxpayers, their representatives, and promot-ers of these transactions, to certain reporting and record keep-ing obligations and penalties that they may be subject to withrespect to these transactions.

Announcement 2002–100, page 799.This document contains corrections to proposed regulations un-der section 1503(d) of the Code (REG–106879–00, 2002–34I.R.B. 402) relating to the events that require the recapture of dualconsolidated losses.

Bulletin No. 2002–44November 4, 2002

Finding Lists begin on page ii.Index for July through October begins on page v.

Announcement 2002–102, page 802.This document changes the date of a scheduled public hearingand extends the public comment period on proposed regula-tions (REG–136311–01, 2002–36 I.R.B. 485) that relate to whena foreign corporation engaged in the international operation ofships or aircraft may exclude its U.S. source income from grossincome for U.S. federal income tax purposes. The hearing is re-scheduled from November 12, 2002, to November 25, 2002.

EMPLOYEE PLANS

REG–124667–02, page 791.Proposed regulations under section 417 of the Code would con-solidate the content requirements applicable to explanations ofqualified joint and survivor annuities and qualified preretire-ment survivor annuities payable from certain retirement plans.In addition, these regulations would specify requirements for dis-closing the relative value of optional forms of benefit that are pay-able from certain retirement plans in lieu of a qualified joint andsurvivor annuity. A public hearing is scheduled for January 14,2003.

November 4, 2002 2002–44 I.R.B.

The IRS Mission

Provide America’s taxpayers top quality service by helping themunderstand and meet their tax responsibilities and by applyingthe tax law with integrity and fairness to all.

IntroductionThe Internal Revenue Bulletin is the authoritative instrument of theCommissioner of Internal Revenue for announcing official rul-ings and procedures of the Internal Revenue Service and for pub-lishing Treasury Decisions, Executive Orders, Tax Conventions,legislation, court decisions, and other items of general inter-est. It is published weekly and may be obtained from the Super-intendent of Documents on a subscription basis. Bulletin contentsare consolidated semiannually into Cumulative Bulletins, whichare sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletin all sub-stantive rulings necessary to promote a uniform application ofthe tax laws, including all rulings that supersede, revoke, modify,or amend any of those previously published in the Bulletin. All pub-lished rulings apply retroactively unless otherwise indicated. Pro-cedures relating solely to matters of internal management arenot published; however, statements of internal practices and pro-cedures that affect the rights and duties of taxpayers are pub-lished.

Revenue rulings represent the conclusions of the Service on theapplication of the law to the pivotal facts stated in the revenueruling. In those based on positions taken in rulings to taxpay-ers or technical advice to Service field offices, identifying de-tails and information of a confidential nature are deleted to preventunwarranted invasions of privacy and to comply with statutoryrequirements.

Rulings and procedures reported in the Bulletin do not have theforce and effect of Treasury Department Regulations, but theymay be used as precedents. Unpublished rulings will not be re-lied on, used, or cited as precedents by Service personnel in thedisposition of other cases. In applying published rulings and pro-cedures, the effect of subsequent legislation, regulations, court

decisions, rulings, and procedures must be considered, and Ser-vice personnel and others concerned are cautioned against reach-ing the same conclusions in other cases unless the facts andcircumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I. — 1986 Code.This part includes rulings and decisions based on provisions ofthe Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows: Subpart A, TaxConventions and Other Related Items, and Subpart B, Legisla-tion and Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellaneous.To the extent practicable, pertinent cross references to these sub-jects are contained in the other Parts and Subparts. Also in-cluded in this part are Bank Secrecy Act Administrative Rulings.Bank Secrecy Act Administrative Rulings are issued by the De-partment of the Treasury’s Office of the Assistant Secretary (En-forcement).

Part IV.—Items of General Interest.This part includes notices of proposed rulemakings, disbar-ment and suspension lists, and announcements.

The first Bulletin for each month includes a cumulative index forthe matters published during the preceding months. Thesemonthly indexes are cumulated on a semiannual basis, and arepublished in the first Bulletin of the succeeding semiannual pe-riod, respectively.

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents, U.S. Government Printing Office, Washington, DC 20402.

2002–44 I.R.B. November 4, 2002

Part I. Rulings and Decisions Under the Internal Revenue Code of 1986

Section 42.—Low-IncomeHousing Credit

Low-income housing credit; satisfac-tory bond; “bond factor” amounts for theperiod October through December 2002.This ruling announces the monthly bondfactor amounts to be used by taxpayers whodispose of qualified low-income build-ings or interests therein during the periodOctober through December 2002. This rul-ing also provides a summary of the bondfactor amounts for dispositions occuringduring the period January through Septem-ber 2002.

Rev. Rul. 2002–72

In Rev. Rul. 90–60, 1990–2 C.B. 3, theInternal Revenue Service provided guid-

ance to taxpayers concerning the generalmethodology used by the Treasury Depart-ment in computing the bond factor amountsused in calculating the amount of bond con-sidered satisfactory by the Secretary un-der § 42(j)(6) of the Internal Revenue Code.It further announced that the Secretarywould publish in the Internal Revenue Bul-letin a table of “bond factor” amounts fordispositions occurring during each calen-dar month.

Rev. Proc. 99–11, 1999–1 C.B. 275, es-tablished a collateral program as an alter-native to providing a surety bond fortaxpayers to avoid or defer recapture of thelow-income housing tax credits under§ 42(j)(6). Under this program, taxpayers

may establish a Treasury Direct Accountand pledge certain United States Treasurysecurities to the Internal Revenue Serviceas security.

This revenue ruling provides in Table 1the bond factor amounts for calculating theamount of bond considered satisfactory un-der § 42(j)(6) or the amount of UnitedStates Treasury securities to pledge in aTreasury Direct Account under Rev. Proc.99–11 for dispositions of qualified low-income buildings or interests therein dur-ing the period October through December2002. Table 1 also provides a summary ofthe bond factor amounts for dispositions oc-curring during the period January throughSeptember 2002.

Table 1Rev. Rul. 2002–72

Monthly Bond Factor Amounts for Dispositions ExpressedAs a Percentage of Total Credits

Calendar Year Building Placed in Serviceor, if Section 42(f)(1) Election Was Made,

the Succeeding Calendar Year

Month ofDisposition

1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998

Jan ’02 17.76 32.73 45.44 56.24 65.46 65.92 66.46 66.99 67.63 68.35 69.24Feb ’02 17.76 32.73 45.44 56.24 65.46 65.75 66.28 66.80 67.44 68.16 69.05Mar ’02 17.76 32.73 45.44 56.24 65.46 65.57 66.10 66.62 67.26 67.98 68.86Apr ’02 17.76 32.73 45.44 56.24 65.46 65.40 65.93 66.45 67.08 67.80 68.68May ’02 17.76 32.73 45.44 56.24 65.46 65.23 65.76 66.27 66.91 67.62 68.50Jun ’02 17.76 32.73 45.44 56.24 65.46 65.06 65.59 66.11 66.74 67.46 68.33Jul ’02 17.76 32.73 45.44 56.24 65.46 64.90 65.42 65.94 66.58 67.29 68.17Aug ’02 17.76 32.73 45.44 56.24 65.46 64.74 65.26 65.78 66.42 67.13 68.01Sep ’02 17.76 32.73 45.44 56.24 65.46 64.58 65.10 65.62 66.26 66.98 67.86Oct ’02 17.76 32.73 45.44 56.24 65.46 64.43 64.95 65.47 66.11 66.83 67.72Nov ’02 17.76 32.73 45.44 56.24 65.46 64.27 64.80 65.32 65.96 66.68 67.58Dec ’02 17.76 32.73 45.44 56.24 65.46 64.12 64.65 65.17 65.81 66.54 67.44

2002–44 I.R.B. 759 November 4, 2002

Table 1 (cont’d)Rev. Rul. 2002–72

Monthly Bond Factor Amounts for Dispositions ExpressedAs a Percentage of Total Credits

Calendar Year Building Placed in Serviceor, if Section 42(f)(1) Election Was Made,

the Succeeding Calendar Year

Month ofDisposition

1999 2000 2001 2002

Jan ’02 70.13 70.98 72.28 72.55Feb ’02 69.92 70.77 72.05 72.55Mar ’02 69.73 70.58 71.84 72.55Apr ’02 69.55 70.40 71.67 72.55May ’02 69.38 70.24 71.51 72.55Jun ’02 69.21 70.09 71.37 72.55Jul ’02 69.05 69.94 71.25 72.55Aug ’02 68.90 69.81 71.14 72.55Sep ’02 68.76 69.68 71.04 72.55Oct ’02 68.62 69.57 70.94 72.55Nov ’02 68.49 69.45 70.86 72.55Dec ’02 68.37 69.35 70.78 72.55

For a list of bond factor amounts appli-cable to dispositions occurring during othercalendar years, see: Rev. Rul. 98–3, 1998–1C.B. 248; Rev. Rul. 2001–2, 2001–1 C.B.255; and Rev. Rul. 2001–53, 2001–2 C.B.488.

DRAFTING INFORMATION

The principal author of this revenue rul-ing is Gregory N. Doran of the Office ofAssociate Chief Counsel (Passthroughs andSpecial Industries). For further informa-tion regarding this revenue ruling, con-tact Mr. Doran at (202) 622–3040 (not atoll-free call).

Section 162.—Trade orBusiness Expenses

26 CFR 1.162–11: Rentals.

(Also § 163; 1.163–1.)

Business expenses; interest; lease-in/lease-out transactions. A taxpayer may notdeduct currently, under sections 162 and 163of the Code, rent or interest paid or in-curred in connection with a lease-in/lease-out (LILO) transaction that properly ischaracterized as conferring only a future in-terest in property.

Rev. Rul. 2002–69

ISSUE

May a taxpayer deduct currently, un-der §§ 162 and 163 of the Internal Rev-enue Code, rent and interest paid or incurredin connection with a “lease-in/lease-out”(“LILO”) transaction?

FACTS

X is a U.S. corporation. FM is a for-eign municipality that has historically ownedand used certain property. As of 1997, it isestimated that the property has a remain-ing useful life of 50 years and a fair mar-ket value of $100 million. BK1 and BK2 arebanks. None of these four parties is re-lated to any of the others.

On January 1, 1997, X and FM enteredinto a LILO transaction under which FMleased the property to X under a “Head-lease,” and X immediately leased the prop-erty back to FM under a “Sublease.” Theterm of the Headlease is 40 years. The pri-mary term of the Sublease is 20 years.Moreover, as described below, the Sub-lease also may be renewed for a term of 10years (“put renewal term”) at the option ofX. X’s right to possess the property under

the Headlease for the first 20 years is sub-stantially the same as FM’s right to pos-session under the Sublease for the primaryterm.

The Headlease requires X to make tworental payments to FM during its 40-yearterm: (1) an $89 million prepayment at thebeginning of year 1; and (2) a postpay-ment at the end of year 40 that has a dis-counted present value of $8 million. Forfederal income tax purposes, X and FM al-locate the prepayment ratably to the first 6years of the Headlease and the future valueof the postpayment ratably to the remain-ing 34 years of the Headlease.

The Sublease requires FM to make fixed,annual rental payments over both the pri-mary term and, if exercised, the put re-newal term. The fixed, annual paymentsduring the put renewal term are equal to 90percent of the amounts that (as of Janu-ary 1, 1997) are projected to be the fairmarket value rental amounts for that term.

To partially fund the $89 million Head-lease prepayment, X borrows $54 millionfrom BK1 and $6 million from BK2. Bothloans are nonrecourse, have fixed interestrates, and provide for annual debt servicepayments that fully amortize the loans overthe 20-year primary term of the Sublease.The amount and timing of the debt ser-

November 4, 2002 760 2002–44 I.R.B.

vice payments mirror the amount and tim-ing of the Sublease payments due duringthe primary term of the Sublease. The re-maining $29 million of the Headlease pre-payment is provided by X.

Upon receiving the $89 million Head-lease prepayment, FM deposits $54 mil-lion into a deposit account with an affiliateof BK1 and $6 million into a deposit ac-count with an affiliate of BK2. The depos-its with the affiliates of BK1 and BK2 earninterest at the same rates as the loans fromBK1 and BK2. FM directs the affiliate ofBK1 to pay BK1 annual amounts equal to90 percent of FM’s annual rent obliga-tion under the Sublease (that is, amountssufficient to satisfy X’s debt service obli-gation to BK1). The parties treat theseamounts as having been paid from the af-filiate to FM, then from FM to X as rentalpayments, and finally from X to BK1 asdebt service payments. In addition, FMpledges the deposit account to X as secu-rity for FM’s obligations under the Sub-lease, while X, in turn, pledges its interestin FM’s pledge to BK1 as security for X’sobligations under the loan from BK1. Simi-larly, FM directs the affiliate of BK2 to payBK2 annual amounts equal to 10 percent ofFM’s annual rent obligation under the Sub-lease (that is, amounts sufficient to sat-isfy X’s debt service obligation to BK2). Theparties treat these amounts as having beenpaid from the affiliate to FM, then from FMto X as rental payments, and finally fromX to BK2 as debt service payments. Al-though FM’s deposit with the BK2 affili-ate is not pledged, the parties understandthat FM will use the account to pay the re-maining 10 percent of FM’s annual rent ob-ligation under the Sublease.

As a result of the foregoing arrange-ment, X’s obligation to make the propertyavailable under the 20-year primary termof the Sublease is completely offset by X’sright to use the property under the Head-lease. X’s obligation to make debt servicepayments on the loans from BK1 and BK2is completely offset by X’s right to re-ceive Sublease rentals from FM. More-over, X’s exposure to the risk that FM willnot make the rent payments is further lim-ited by the arrangements with the affili-ates of BK1 and BK2. In the case of theloan from BK1, X’s economic risk is elimi-nated through the defeasance arrangement.In the case of the $6 million loan from BK2,X’s economic risk, although not elimi-

nated, is substantially reduced through thedeposit arrangement. As a result, neitherbank requires an independent source offunds to make the loans, or bears signifi-cant risk of nonpayment. In short, duringthe primary Sublease term, the transac-tion is characterized by reciprocal and cir-cular obligations that offset one another.

At the end of the Sublease primary term,FM has a fixed-payment option to pur-chase from X the Headlease residual (theright to use the property beyond the Sub-lease primary term subject to the obliga-tion to make the rent postpayment) for afixed exercise price equal to 105 percent ofthe amount that (as of January 1, 1997) isprojected to be the future fair market valueof the Headlease residual. If FM exercisesthe option, the transaction is terminated atthat point, and X receives the exercise priceof the option and is not required to makeany portion of the postpayment due un-der the Headlease. If FM does not exer-cise the option, X may elect to (1) use theproperty itself for the remaining term of theHeadlease, (2) lease the property to an-other person for the remaining term of theHeadlease, or (3) compel FM to lease theproperty for the 10-year put renewal termof the Sublease. If FM does not exercise thefixed-payment option and X exercises its putrenewal option, X will receive rents that areequal to 90 percent of the amounts that are(as of January 1, 1997) projected to be thefair market rents for that term. If the ac-tual fair market rents in 20 years turn outto be less than the amount specified in theput renewal option and FM does not ex-ercise the fixed-payment option, X will beable to compel FM to lease the property forrents that are greater than the then fair mar-ket rental value. Thus, as a practical mat-ter, the fixed-payment option and putrenewal option operate to “collar” the valueof the Headlease residual during the pri-mary term.

In addition, X has nominal exposure toFM’s credit under the fixed-payment op-tion and, if exercised, the put renewal term.At the inception of the transaction, X re-quires FM to invest $15 million of theHeadlease prepayment in highly-rated debtsecurities that will mature in an amount suf-ficient to fund the fixed amount due un-der the fixed-payment option, and to pledgethese debt securities to X. This arrange-ment ensures that FM is able to make thepayment under the fixed-payment option.

Having economically defeased both itsrental obligations under the Sublease andits fixed-payment under the fixed-paymentoption, FM keeps the remaining portion ofthe Headlease prepayment as its return onthe transaction. If FM does not exercise thefixed-payment option and X exercises theput renewal option, X can require FM topurchase a letter of credit guaranteeing theput renewal rents. If FM does not obtain theletter of credit, FM must exercise the fixed-payment option.

For tax purposes, X claims deductionsfor interest on the loans and for the allo-cated rents on the Headlease. X includes ingross income the rents received on the Sub-lease. If the fixed-payment option is exer-cised, X also includes the option price andrecaptures rent deductions taken during theprimary Sublease term that are attribut-able to the postpayment it is no longer re-quired to make.

LAW AND ANALYSIS

X and FM’s allocations of the prepay-ment and the postpayment for federal in-come tax purposes meet the uneven rent testcontained in proposed § 467 regulations(§ 1.467–3(c)(2)(i)), and under those regu-lations the Headlease would not be treatedas a disqualified leaseback or long-termagreement subject to constant rental ac-crual. Because this LILO transaction wasentered into after June 3, 1996, and on orbefore May 18, 1999, the provisions of theproposed regulations are available. See§ 1.467–9(c). For later years, however, fi-nal § 467 regulations effective May 18,1999, treat the prepayment of rent as re-sulting in a deemed loan from X to FM andrequire the imputation of interest income toX. § 1.467–4. Moreover, X’s rent deduc-tion would be subject to proportional rentrules that reflect the time value of moneyconcept. See § 1.467–2(c).

The substance of a transaction, not itsform, governs its tax treatment. Gregory v.Helvering, 293 U.S. 465 (1935). In FrankLyon Co. v. United States, 435 U.S. 561,573 (1978), the United States SupremeCourt stated, “In applying the doctrine ofsubstance over form, the Court has lookedto the objective economic realities of atransaction rather than to the particular formthe parties employed.” The Court evalu-ated the substance of the transaction inFrank Lyon to determine that it was in-deed a sale/leaseback, as it was structured,

2002–44 I.R.B. 761 November 4, 2002

rather than a financing. The Court subse-quently relied on its approach in Frank Lyonto recharacterize a sale and repurchase offederal securities as a loan, finding that theeconomic realities of the transaction did notsupport the form chosen by the taxpayer.Nebraska Dep’t of Revenue v. Loewen-stein, 513 U.S. 123 (1994).

Where parties have in form entered intotwo separate transactions that result in off-setting obligations, the courts often havecollapsed the offsetting obligations and re-characterized the two transactions as a singletransaction. In Rogers v. United States, 281F.3d 1108 (10th Cir. 2002), the part-owner(Fogelman) of a professional baseball teamthat was organized as an S corporation bor-rowed money from the S corporation. Thenonrecourse loan was secured by Fogel-man’s ownership interest in the corpora-tion and his existing option to purchase therest of the shares from the taxpayer (Kauff-man), the other owner of the team. Fogel-man also granted the corporation an optionto purchase both his shares and his exist-ing option to buy Kauffman’s shares. Theoption price was an amount equal to theoutstanding loan balance. The corpora-tion exercised its option immediately but de-ferred closing until the due date ofFogelman’s loan, five months later. On thatdate, Fogelman transferred his shares in thecorporation to the corporation in lieu of itsforeclosure on the loan. The corporationclaimed that the shares had no value at thattime and deducted the loan amount as a baddebt, which was passed through to Kauff-man.

The court in Rogers applied the sub-stance over form doctrine to collapse theloan and the option transaction into a re-demption of Fogelman’s stock in exchangefor cash. Fogelman had no incentive to re-pay the loan because any reduction in theloan balance would reduce the option price.The immediate exercise of the option pre-cluded any attempt by Fogelman to repaythe loan and keep the stock. On the basisof those facts, among others, the court heldthat the substance of the transaction was asale of Fogelman’s stock to the corpora-tion.

In Bussing v. Commissioner, 88 T.C. 449,reconsideration denied, 89 T.C. 1050(1987), a Swiss subsidiary of a computerleasing company (AG) purchased com-puter equipment in a sale/leaseback trans-action involving a five-year lease.

Subsequently, AG purportedly sold theequipment to a domestic corporation(Sutton), which in turn purportedly sold in-terests in the equipment to the taxpayer(Bussing) and four other individual inves-tors. Bussing acquired his interest in thecomputer equipment subject to the under-lying lease by paying cash, short-termpromissory notes, and a long-term prom-issory note to Sutton. Bussing then leasedhis interest in the equipment back to AG fornine years. The rents due Bussing from AGequaled Bussing’s annual payments on thelong-term promissory note to Sutton for thefirst three years and were supposed to gen-erate nominal annual cash flow thereaf-ter.

The court first disregarded Sutton’s par-ticipation in the transactions on substanceover form grounds. It then held thatBussing’s long-term indebtedness also mustbe disregarded because it was completelyoffset by AG’s rent payments in a “pur-ported sale-leaseback pursuant to which therespective lease and debt obligations flowbetween only two parties.” Id. at 458. Thecourt stated,

The respective obligations between AGand Bussing cancel each other out. Anypossible claim by AG with respect to thenote is fully offset by AG’s rental obli-gation to Bussing. . . . Bussing, effec-tively, will never be required to make anypayments on his debt obligation, a fea-ture of the transaction that we believe theparties intended to achieve.

Id. After collapsing the offsetting loan andlease, the court concluded that Bussing hadacquired an interest in a joint venture withAG and the other investors to the extent ofhis cash payment only.

Courts have similarly disregarded theparties’ obligations in purported install-ment sales where the taxpayer received aninstallment note that was offset by someother arrangement between the two par-ties, indicating that the maker of the notewould not be called upon to pay the in-stallment obligation. See Rickey v. Com-missioner, 502 F.2d 748 (9th Cir. 1974),aff ’g 54 T.C. 680 (1970). Although tax-payers are entitled to arrange the terms ofa sale in order to qualify for the install-ment method, “the arrangements must havesubstance and must reflect the true situa-tion rather than being merely the formaldocumentation of the terms of the sale.” Id.at 752–53, quoting 54 T.C. 680 at 694. See

also United States v. Ingalls, 399 F.2d 143(5th Cir. 1968); Blue Flame Gas Co. v.Commissioner, 54 T.C. 584 (1970); Green-field v. Commissioner, T.C. Memo. 1982–617; Big “D” Development Corp. v.Commissioner, T.C. Memo. 1971–148, aff’dper curiam, 453 F.2d 1365 (5th Cir.1972).

Similarly, the Headlease and Subleaseimpose offsetting obligations that must bedisregarded, regardless of whether othercomponents of the LILO transaction are re-spected. During the first 20 years of itsterm, the Headlease confers to X a right touse the property that is immediately re-versed by the Sublease grant to FM of sub-stantially the same right to use property. Inthe LILO transaction, the Sublease inter-est retained by FM is of the same natureas the Headlease interest conveyed to X. Be-cause the transfer and retransfer of the rightto possess the property for the first 20 yearsare disregarded as offsetting obligations, thetransaction that remains is, at best, a trans-fer of funds from X to FM in exchange forFM’s obligation to repay those funds andprovide X the right to begin to lease theproperty in 20 years.

An analogous situation occurs when theconveyance of property is accompanied bythe retention of some interest in the sameproperty. If the interest retained is of sub-stantially the same nature as the interestconveyed, only a future interest is con-veyed. In McCully Ashlock v. Commis-sioner, 18 T.C. 405 (1952), acq., 1952–2C.B. 1, taxpayer had acquired propertythrough a deed dated June 6, 1945. Theseller, however, had retained the right topossession and rentals through August 15,1947. The court found that taxpayer had ac-quired only a future interest in the prop-erty because “the trustees [sellers] not onlyretained the rents legally but they also re-tained control and benefits of ownership.”Id. at 411. Consequently, rentals from theproperty were income to the seller.

Similarly, in Kruesel v. United States,63–2 U.S. Tax Cas. (CCH) ¶ 9714 (D.Minn. 1963), the court concluded that tax-payer had transferred only a future, re-mainder interest in property and reserveda life estate. The government had unsuc-cessfully argued that taxpayer had sold itsentire interest in the property and the tax-payer’s amount realized on the sale in-cluded the value of a right to occupancyprovided to the taxpayer by the buyer.

November 4, 2002 762 2002–44 I.R.B.

In contrast, in Alstores Realty Corp. v.Commissioner, 46 T.C. 363 (1966), acq.,1967–2 C.B.1, the court held that a sale ofproperty accompanied by the reservation ofa right of occupancy did not result in thetransfer of only a future interest because theseller’s right of occupancy was in the na-ture of a leasehold interest, because the pur-chaser acquired the benefits and burdens ofownership of the property.

Alstores can be distinguished fromMcCully Ashlock and Kruesel. McCullyAshlock and Kruesel conclude that wherea retained interest is of the same nature asthe interest conveyed, only a future inter-est has been transferred. In Alstores, the in-terests were not of the same nature.

Similarly, the LILO transaction is dis-tinguishable from the transaction involvedin Comdisco, Inc. v. Commissioner, 756F.2d 569 (7th Cir. 1985). In that case, equip-ment was subject to end user leases, and thelessor of that equipment assigned an inter-est to taxpayer in a transaction designed togive the taxpayer investment tax credits. Thetaxpayer’s entitlement to the credits de-pended on whether it had the status oflessee/sublessor. In concluding that it did,the court noted a number of factors thatsupported taxpayer’s claim that it had ac-quired a leasehold interest. The taxpayerwas obligated to the lessor in the event ofa default by the sublessee. The taxpayer re-let certain equipment after one sublease hadexpired. In connection with another sub-lease, the taxpayer was responsible for rentto its assignor in excess of amounts paid bythe sublessee directly to the assignor. Thecourt also emphasized the regulatory re-strictions on direct leases between the as-signor and the end users. Id. at 576–77.Unlike Comdisco, in the LILO transac-tion the headlessor and the sublessee are thesame party. Further, in the LILO transac-tion the headlessee/sublessor is not mate-rially exposed to the risk that the sublesseewill fail to make rent payments.

Section 162(a)(3) permits a deduction forrentals and other payments required to bemade as a condition to the continued useor possession, for purposes of the trade orbusiness, of property. Because X does notacquire a current leasehold interest in theproperty, it is not entitled to current de-ductions for rent. The $29 million “eq-uity” portion of the Headlease prepaymentis, effectively, a payment for at most X’sright under the Headlease to lease the prop-

erty 20 years hence for a term of 20 years.(Economically, $29 million is an overpay-ment for the value of any right that X ob-tains to lease the property in the future. Xwas willing to overpay in this manner, how-ever, in order to induce FM to participatein the transaction.). In accordance with§ 467, the $29 million “equity” portion ofthe Headlease prepayment is deductible overthe 20-year residual term of the Head-lease (the 10-year put renewal term and the10-year “shirttail” period). Alternatively, inthe event FM exercises its fixed-price op-tion at the end of the primary term of theSublease, X will have gain or loss equal tothe difference between the option price andX’s cost of acquiring a right to the Head-lease residual term. Section 1001.

The remainder of the Headlease pre-payment, $60 million, must be disregarded,because the “loans” that purportedly fi-nance this portion of the Headlease pre-payment are without substance. In Bridgesv. Commissioner, 39 T.C. 1064, aff’d 325F.2d 180 (4th Cir. 1963), taxpayer “bor-rowed” funds from banks and used thefunds to purchase Treasury notes, which thebanks held as collateral and ultimately soldto satisfy taxpayer’s debts. The court’s ra-tionale for disallowing taxpayer’s deduc-tions of prepaid interest is equally applicablehere:

[P]etitioner at no time had the uncon-trolled use of any additional money, of thebonds, or of the interest on the bonds. Heassumed no risk of a rise or fall in themarket price of the bonds and could nottake advantage of such. His payment tothe bank was not for the use or forbear-ance of money; it was for the purchaseof a rigged sales price for the bonds andfor a tax deduction. Petitioner incurred nogenuine indebtedness, within the mean-ing of the statute, and as a payment of in-terest, this transaction was also a sham.

Id. at 1078–79. Neither X nor FM obtainuse of the “borrowed” funds. The “loans”purportedly are made to finance X’s acqui-sition of the Headlease interest. But thatleasehold interest is substantially offset byan interdependent Sublease with the Head-lessor. What remains can only be enjoyedafter 20 years and after the loans have been“repaid” using “rents” from a Sublease thatitself lacks substance. Under the circum-stances, the loans are disregarded.

Although this ruling refers to a for-eign municipality and its property, the analy-

sis and holding apply as well to LILOtransactions that involve or include domes-tic tax-exempt or tax-indifferent entities.

HOLDING

A taxpayer may not deduct currently, un-der §§ 162 and 163, rent or interest paid orincurred in connection with a LILO trans-action that properly is characterized as con-ferring only a future interest in property.

Where appropriate, the Service will con-tinue to disallow the tax benefits claimedin connection with LILO transactions uponother grounds, including that the substanceover form doctrine requires their rechar-acterization as financing arrangements andthat they are to be disregarded for lack ofeconomic substance.

EFFECT ON OTHER DOCUMENTS

Rev. Rul. 99–14, 1999–1 C.B. 835, ismodified and superseded.

DRAFTING INFORMATION

The principal author of this revenue rul-ing is John Aramburu of the Office of As-sociate Chief Counsel (Income Tax &Accounting). For further information re-garding this revenue ruling, contact Mr.Aramburu at (202) 622–4960 (not a toll-free call).

Section 163.—Interest

26 CFR 1.162–17: Interest deduction in general.

May a taxpayer deduct currently, under § 163, in-terest paid or incurred in connection with a lease-in/lease-out (LILO) transaction that properly ischaracterized as conferring only a future interest inproperty. See Rev. Rul. 2002–69, page 760.

Section 446.—General Rulefor Methods of Accounting

(Also 26 CFR 1.446–4)

Notional principal contract (NPC).This ruling provides guidance on the tim-ing of recognition of gain or loss on the ter-mination of a notional principal contract thathedges a portion of the term of a debt in-strument issued by the taxpayer.

2002–44 I.R.B. 763 November 4, 2002

Rev. Rul. 2002–71

ISSUE

When should a taxpayer take into ac-count gain or loss on the termination of anotional principal contract (NPC) thathedges a portion of the term of a debt in-strument issued by the taxpayer?

FACTS

Situation 1

Taxpayer TP uses the calendar year asits taxable year. On the first day of Year 1,TP issues a debt instrument. The debt in-strument has a 10-year term and providesfor interest to be paid annually at a fixedrate. Contemporaneously with the issu-ance of the debt instrument, TP also en-ters into an NPC with a 5-year term thatconverts the fixed rate payments under thedebt instrument into floating rate payments.That is, the NPC provides for TP to re-ceive payments equal to the product of thefixed rate on the debt instrument and a no-tional amount equal to the principal amountof the debt instrument in exchange for pay-ments by TP equal to the product of a float-ing rate and the same notional amount.Pursuant to § 1.1221–2(f), TP properly iden-tifies the NPC as a hedging transaction cov-ering Year 1 through Year 5 of the debtinstrument and complies with the other re-quirements necessary for the NPC to betreated as a hedge under §§ 1.1221–2 and1.446–4. TP terminates the NPC on the lastday of Year 2 and either receives or makesa termination payment.

Situation 2

The facts are the same as Situation 1,but, in addition, TP retires the debt instru-ment in Year 4.

LAW

Section 1.446–4(a) provides that a hedg-ing transaction as defined in § 1.1221–2(b) must be accounted for under the rulesset forth in § 1.446–4.

Section 1.446–4(b) provides that themethod of accounting used by a taxpayer

for a hedging transaction must clearly re-flect income. Section 1.446–4(b) furtherprovides that to clearly reflect income, themethod used for a hedging transaction mustreasonably match the timing of income, de-duction, gain, or loss from the hedgingtransaction with the timing of income, de-duction, gain, or loss from the item beinghedged.

Section 1.446–4(e)(4) provides that gainor loss from a transaction that hedges a debtinstrument issued or to be issued by a tax-payer, or a debt instrument held or to beheld by a taxpayer, must be accounted forby reference to the terms of the debt in-strument and the period or periods to whichthe hedge relates. A hedge of an instru-ment that provides for interest to be paidat a fixed rate or a qualified floating rate,for example, generally is accounted for us-ing constant yield principles. Thus, assum-ing that a fixed rate or qualified floating rateinstrument remains outstanding, hedginggain or loss is taken into account in thesame periods in which it would be takeninto account if it adjusted the yield of theinstrument over the term to which the hedgerelates. Section 1.446–4(e)(4) provides, asan example, that gain or loss realized on atransaction that hedged an anticipated fixedrate borrowing for its entire term is ac-counted for, solely for purposes of§ 1.446–4, as if it decreased or increasedthe issue price of the debt instrument. How-ever, in all events, the taxpayer’s method,as actually applied to the taxpayer’s hedg-ing transactions, must clearly reflect in-come by meeting the matching requirementof § 1.446–4(b). See § 1.446–4(e) (intro-ductory sentences).

ANALYSIS

Situation 1

Unlike the hedging transaction describedin § 1.446–4(e)(4) that hedges a fixed rateborrowing over its entire term, TP’s NPCdoes not hedge the entire term of the debtinstrument. Rather, TP’s NPC hedges, andrelates only to, Year 1 through Year 5 of the10-year term of the debt instrument. Priorto its termination on the last day of Year 2,the NPC would have continued to hedgeYear 3 through Year 5 of the debt instru-

ment, and TP generally would have beenrequired to take into account the remain-ing income, deduction, gain, or loss overthe period from Year 3 through Year 5. Thetermination payment made or received byTP represents the present value of the ex-tinguished rights and obligations under theNPC for Year 3 through Year 5. There-fore, the gain or loss from the hedgingtransaction relates to Year 3 through Year5. To clearly reflect income in accordancewith the matching requirement of § 1.446–4(b), TP must take into account the gain orloss from terminating the NPC over the pe-riod from Year 3 through Year 5.

Situation 2

Following the analysis from Situation 1,TP would have already taken into accountin Year 3 a portion of the gain or loss fromtermination of the NPC in Year 2. How-ever, upon retiring the debt instrument inYear 4, TP’s remaining gain or loss fromthe termination of the NPC should be rec-ognized in order to match the timing of in-come, deduction, gain, or loss from thehedging transaction with the timing of in-come, deduction, gain, or loss from the itembeing hedged.

HOLDING

(1) In Situation 1, TP must account forthe gain or loss arising from terminating theNPC over the period from Year 3 throughYear 5, the remaining period to which theterminated hedge relates.

(2) In Situation 2, TP takes into ac-count in Year 3 a portion of the gain or lossarising from the termination of the NPC andtakes into account in Year 4 the remain-ing balance of the gain or loss from the ter-minated hedge.

DRAFTING INFORMATION

The principal authors of this revenue rul-ing are K. Scott Brown and ClayLittlefield of the Office of Associate ChiefCounsel (Financial Institutions and Prod-ucts). For further information regarding thisrevenue ruling, contact Messrs. Brown orLittlefield at (202) 622–3920 (not a toll-free call).

November 4, 2002 764 2002–44 I.R.B.

Part III. Administrative, Procedural, and Miscellaneous

Certain ReinsuranceArrangements

Notice 2002–70

The Internal Revenue Service and Trea-sury Department have become aware of atype of transaction, described below, thatis being used by taxpayers to shift incomefrom taxpayers to related companies pur-ported to be insurance companies that aresubject to little or no U.S. federal incometax. This notice alerts taxpayers and theirrepresentatives that these transactions of-ten do not generate the federal tax ben-efits that taxpayers claim are allowable forfederal income tax purposes. This noticealso alerts taxpayers, their representatives,and promoters of these transactions, to cer-tain reporting and record keeping obliga-tions and penalties that they may be subjectto with respect to these transactions.

The transaction generally involves a tax-payer (“Taxpayer”) (typically a service pro-vider, automobile dealer, lender, or retailer)that offers its customers the opportunity topurchase an insurance contract through Tax-payer in connection with the products orservices being sold. The insurance pro-vides coverage for repair or replacementcosts if the product breaks down or is lost,stolen, or damaged, or coverage for the cus-tomer’s payment obligations in case the cus-tomer dies, or becomes disabled orunemployed.

Taxpayer offers the insurance to its cus-tomers by acting as an insurance agent foran unrelated insurance company (“Com-pany X”). Taxpayer receives a sales com-mission from Company X equal to apercentage of the premiums paid by Tax-payer’s customers. Taxpayer forms awholly-owned corporation (“Company Y”),typically in a foreign country, to reinsurethe policies sold by Taxpayer. Promoterssometimes refer to these companies as pro-ducer owned reinsurance companies or“PORCs”. If Company Y is a foreign cor-poration, it typically elects to be treated asa domestic insurance company under§ 953(d) of the Internal Revenue Code.Company Y takes the position that it is en-titled to the benefits of § 501(c)(15) (pro-viding that non-life insurance companies aretax exempt if premiums written for the tax-

able year do not exceed $350,000), § 806(providing a deduction for certain life in-surance companies with life insurance com-pany taxable income not in excess of$15,000,000), or § 831(b) (allowing quali-fying non-life insurance companies whosenet written premiums are between $350,000and $1,200,000 to elect to be taxed solelyon investment income).

Taxpayer receives premiums from itscustomers and remits those premiums (typi-cally net of its sales commission) to Com-pany X. Company X pays any claims andstate premium taxes due and retains anamount from the premiums received fromTaxpayer. Under Company Y’s reinsur-ance agreement with Company X, Com-pany Y reinsures all insurance policies thatTaxpayer sells to its customers. CompanyX transfers the remainder of the premi-ums to Company Y as reinsurance premi-ums.

ANALYSIS

Many of the transactions described inthis notice have been designed to use a re-insurance arrangement to divert incomeproperly attributable to Taxpayer to Com-pany Y, Taxpayer’s wholly-owned reinsur-ance company that is subject to little or nofederal income tax. The Service intends tochallenge the purported tax benefits fromthese transactions on a number of grounds.

First, depending upon the facts and cir-cumstances, the Service may assert thatCompany Y is not an insurance companyfor federal income tax purposes. For fed-eral income tax purposes, an insurance com-pany is a company whose primary andpredominant business activity during thetaxable year is the issuing of insurance orannuity contracts or the reinsuring of risksunderwritten by insurance companies.§ 1.801–3(a) of the Income Tax Regula-tions; § 816(a) (which provides that a com-pany will be treated as an insurancecompany for federal income tax purposesonly if “more than half of the business” ofthat company is the issuing of insurance orannuity contracts or the reinsuring of risksunderwritten by insurance companies).While a taxpayer’s name, charter powers,and state regulation help to indicate the ac-tivities in which it may properly engage,whether the taxpayer qualifies as an insur-ance company for tax purposes depends on

its actual activities during the year. Inter-American Life Ins. Co. v. Commissioner, 56T.C. 497, 506–08 (1971), aff ’d per cu-riam, 469 F.2d 697 (9th Cir. 1972) (tax-payer whose predominant source of incomewas from investments did not qualify as aninsurance company); see also Bowers v.Lawyers Mortgage Co., 285 U.S. 182, 188(1932). To qualify as an insurance com-pany, a taxpayer “must use its capital andefforts primarily in earning income from theissuance of contracts of insurance.” In-dus. Life Ins. Co. v. United States, 344 F.Supp. 870, 877 (D. S.C. 1972), aff’d percuriam, 481 F.2d 609 (4th Cir. 1973). Todetermine whether Company Y qualifies asan insurance company, all of the relevantfacts will be considered, including but notlimited to, the size and activities of anystaff, whether Company Y engages in othertrades or businesses, and its sources of in-come. See generally Lawyers Mortgage Co.at 188–90; Indus. Life Ins. Co., at 875–77; Cardinal Life Ins. Co. v. United States,300 F. Supp. 387, 391–92 (N.D. Tex. 1969),rev’d on other grounds, 425 F. 2d 1328 (5thCir. 1970); Serv. Life Ins. Co. v. UnitedStates, 189 F. Supp. 282, 285–86 (D. Neb.1960), aff’d on other grounds, 293 F.2d 72(8th Cir. 1961); Inter-Am. Life Ins. Co., at506–08 ; Nat’l. Capital Ins. Co. of the Dist.of Columbia v. Commissioner, 28 B.T.A.1079, 1085–86 (1933).

If Company Y is not an insurance com-pany, it is not entitled to the benefits of§§ 501(c)(15), 806, or 831(b). Further, ifCompany Y is a foreign corporation and isnot an insurance company, any electionCompany Y made under § 953(d) is notvalid and Company Y will be treated as acontrolled foreign corporation as defined in§ 957. In such a case, Taxpayer will betreated as a U.S. shareholder of CompanyY and generally will include in its gross in-come on a current basis any subpart F in-come of Company Y. See § 951(a) and (b).In addition, Company Y will not qualify forthe exceptions from subpart F income un-der §§ 953(a)(2) and 954(i) for certain in-surance income because those exceptionsare only available to a foreign corpora-tion that, among other requirements, is en-gaged in the insurance business and wouldbe subject to tax under subchapter L if suchcorporation were a domestic corporation.See § 953(e)(3)(C).

2002–44 I.R.B. 765 November 4, 2002

Second, the Service may apply §§ 482or 845 to allocate income from CompanyY to Taxpayer if necessary clearly to re-flect the income of Taxpayer and Com-pany Y. Section 482 provides the Secretarywith authority to allocate gross income, de-ductions, credits or allowances among per-sons owned or controlled directly orindirectly by the same interests, if such al-location is necessary to prevent evasion oftaxes or clearly to reflect income. The § 482regulations provide that in determining thetaxable income of a controlled person, thestandard to be applied is that of a persondealing at arm’s length with an uncon-trolled person. § 1.482–1(b)(1). Section 482may apply to a transaction between two ormore controlled persons notwithstandingthat an uncontrolled person participates inthe transaction as an intermediary. See GACProduce Co. v. Commissioner, T.C.M.1999–134. If, as a result of the reinsur-ance transaction, Taxpayer’s income is notconsistent with the arm’s length standard,then § 482 authorizes the Secretary to al-locate income from Company Y to Tax-payer. Section 845(a) allows the Service toreallocate income, deductions, assets, re-serves, credits, and other items between twoor more related parties who are parties toa reinsurance agreement. Thus, such itemsmay be reallocated from Company Y toTaxpayer under the authority of § 845(a).

Third, in appropriate cases, the Ser-vice may disregard the insurance and re-insurance arrangements, and thereby requireTaxpayer to recognize an additional por-tion of premiums received from its cus-tomers as its income, if the arrangementsare shams in fact or shams in substance. SeeKirchman v. Commissioner, 862 F.2d 1486,1492 (11th Cir. 1989). Courts have distin-guished between “shams in fact” where thereported transactions never occurred and“shams in substance” which actually oc-curred but lack the substance their form rep-resents. ACM Partnership v. Commissioner,157 F.3d 231, 247 n. 30 (3d Cir. 1998), cert.denied, 526 U.S. 1017 (2002) (citationsomitted). In determining whether a trans-action constitutes a sham in substance, botha majority of the Courts of Appeals and theTax Court consider two related factors, eco-nomic substance apart from tax conse-quences, and business purpose. See ACMPartnership; Karr v. Commissioner, 924F.2d 1018, 1023 (11th Cir. 1991), cert. de-nied, 502 U.S. 1082 (1992); James v. Com-

missioner, 899 F.2d 905, 908–09 (10th Cir.1990); Shriver v. Commissioner, 899 F.2d724, 727 (8th Cir. 1990); Rose v. Commis-sioner, 868 F.2d 851, 853 (6th Cir. 1989);Kirchman. Although a taxpayer has the rightto arrange its affairs to reduce its tax li-ability, the substance of a transaction mustgovern its tax consequences regardless ofthe form in which the transaction is cast.See Gregory v. Helvering, 293 U.S. 465,469 (1935). If the transactions involvingTaxpayer, Company X, and Company Y aredisregarded, the income of Company Y isincome of Taxpayer. See Wright v. Com-missioner, T.C.M. 1993–328.

Transactions that are the same as, or sub-stantially similar to, the transaction de-scribed in this notice that involve taxpayersclaiming entitlement to the benefits of§§ 501(c)(15), 806, or 831(b) are identi-fied as “listed transactions” for purposes of§ 1.6011–4T(b)(2) of the temporary In-come Tax Regulations and § 301.6111–2T(b)(2) of the temporary Procedure andAdministration Regulations. See also§ 301.6112–1T, A–4. Independent of theirclassification as “listed transactions” for pur-poses of §§ 1.6011–4T(b)(2) and 301.6111–2T(b)(2), transactions that are the same as,or substantially similar to, the transactiondescribed in this notice may already be sub-ject to the disclosure requirements of§ 6011, the tax shelter registration require-ments of § 6111, or the list maintenance re-quirements of § 6112 (§§ 1.6011–4T,301.6111–1T, 301.6111–2T and 301.6112–1T, A–3 and A–4).

Persons who are required to satisfy theregistration requirement of § 6111 with re-spect to the transactions described in thisnotice and who fail to do so may be sub-ject to the penalty under § 6707(a). Per-sons who are required to satisfy the list-keeping requirement of § 6112 with respectto the transactions described in this no-tice and who fail to do so may be subjectto the penalty under § 6708(a). In addi-tion, the Service may impose penalties onparticipants in these transactions or sub-stantially similar transactions involving tax-payers claiming entitlement to the benefitsof §§ 501(c)(15), 806, or 831(b) or, as ap-plicable, on persons who participate in thepromotion or reporting of such transac-tions, including the accuracy-related pen-alty under § 6662, the return preparerpenalty under § 6694, the promoter pen-

alty under § 6700, and the aiding and abet-ting penalty under § 6701.

The principal authors of this notice areJohn Glover of the Office of AssociateChief Counsel (Financial Institutions andProducts) and Theodore Setzer and SheilaRamaswamy of the Office of AssociateChief Counsel (International). For furtherinformation regarding this notice, contactMr. Glover at (202) 622–3970 orMr. Setzer or Ms. Ramaswamy (202) 622–3870 (not a toll-free call).

November 4, 2002 766 2002–44 I.R.B.

Part IV. Items of General Interest

Notice of ProposedRulemaking and Notice ofPublic Hearing

Electing Mark to Market forMarketable Stock

REG–112306–00

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Notice of proposedrulemaking and notice of public hearing.

SUMMARY: This document contains pro-cedures for certain United States personsholding marketable stock in a passive for-eign investment company (PFIC) to electmark to market treatment for that stock un-der section 1296 and related provisions ofsections 1291 and 1295. These proposedregulations affect United States personsowning marketable stock in a PFIC. Thisdocument also provides notice of a pub-lic hearing on these proposed regulations.

DATES: Written comments and outlines oforal comments to be presented at the pub-lic hearing scheduled for November 6, 2002,at 10 a.m., must be received by October 16,2002.

ADDRESSES: Send submissions to:CC:IT&A:RU (REG–112306–00), room5226, Internal Revenue Service, POB 7604,Ben Franklin Station, Washington, DC20044. In the alternative, submissions maybe hand delivered between the hours of8 a.m. and 5 p.m. to: CC:IT&A:RU (REG–112306–00), Courier’s Desk, Internal Rev-enue Building, 1111 Constitution Avenue,NW, Washington, DC. Alternatively, tax-payers may submit comments electroni-cally directly to the IRS Internet site at:www.irs.gov/regs. The public hearing willbe held in room 4718, Internal RevenueService Building, 1111 Consitiution Av-enue, NW, Washington, DC.

FOR FURTHER INFORMATIONCONTACT: Concerning the regulations,Mark Pollard at (202) 622–3850, concern-ing submissions and the hearing, Ms. Lanita

Vandyke (202) 622–7180 (not toll-free num-bers).

SUPPLEMENTARY INFORMATION:

Background

Since the enactment of the Tax ReformAct of 1986, United States persons that ownPFIC stock have been subject to two al-ternative tax regimes: the interest chargerules under section 1291 of the InternalRevenue Code (Code) and the qualifiedelecting fund (QEF) rules under section1293. Congress recognized that the inter-est charge rules are a substantial source ofcomplexity for PFIC shareholders and thatsome shareholders would prefer the cur-rent inclusion method afforded by the QEFregime, but are unable to obtain the nec-essary information from the PFIC. See H.R.Rep. No. 105–148, at 533 (1997); S. Rep.No. 105–33 at 94 (1997). Accordingly, Con-gress enacted new section 1296 in the Tax-payer Relief Act of 1997 to provideshareholders with an alternative method toinclude income currently with respect totheir interest in a PFIC by allowing themto elect to mark to market their PFIC stockprovided the stock is marketable. In 1998,Congress enacted certain technical correc-tions to section 1296 and related provi-sions, including rules to address the overlapbetween the PFIC and other mark to mar-ket provisions in the Code. IRS Restruc-turing and Reform Act of 1998, section6011(c).

Proposed § 1.1291–8 (INTL–656–87,1992–1 C.B. 1124) had been published onApril 1, 1992 (57 FR 11024). This pro-posed regulation would have provided anelection for certain regulated investmentcompanies (RICs) to use a mark to mar-ket method for their PFIC stock. Although§ 1.1291–8 was originally proposed to beeffective prospectively, the IRS subse-quently notified taxpayers that the pro-posed regulations, when finalized, wouldpermit this limited mark to market elec-tion to be made only for taxable years end-ing after March 31, 1992, and before April1, 1993. Notice 92–53, 1992–2 C.B. 384.As a result of the enactment of section1296, proposed § 1.1291–8 was withdrawn(64 FR 5015); see also Notice 99–14,1999–1 C.B. 736.

On January 25, 2000, final regulationswere published under section 1296(e) (2000final regulations). T.D. 8867, 2000–1 C.B.620 [65 FR 3817]. The 2000 final regula-tions provide guidance regarding the defi-nition of marketable stock for purposes ofsection 1296.

In General

United States persons who own market-able stock (as defined in section 1296(e))in a PFIC may elect to mark to market thatstock annually pursuant to section 1296(section 1296 election). United States per-sons making a section 1296 election withrespect to PFIC stock (section 1296 stock)are not subject to the generally applicableinterest charge regime of section 1291. Thesection 1296 election is available to UnitedStates persons and controlled foreign cor-porations (CFCs) that own, or are treatedas owning, marketable stock in a PFIC.

Explanation of Provisions

A. Changes to Proposed § 1.1291–1(c):Coordination of PFIC Rules and otherMark to Market Provisions

Except for the coordination rules dis-cussed herein, section 1291(d)(1) providesthat the interest charge regime does not ap-ply in the case of PFIC stock that is markedto market under (i) section 1296, or (ii) sec-tion 475 or any other provision of chap-ter 1 of the Code. This regulation revises§ 1.1291–1(c), 57 FR 11024, proposed April1, 1992, to incorporate this coordination ruleand to clarify that the interest charge re-gime does not apply to a United States per-son that marks to market its PFIC stockunder any provision of chapter 1 of theCode, without regard to whether such re-gime is mandatory or elective. Proposed§ 1.1295–1(i)(3) and proposed § 1.1296–1(h)(3)(i) further clarify that, with respectto taxation under a mark to market provi-sion other than under section 1296, this co-ordination rule applies without regard towhether the taxpayer also has made a sec-tion 1296 election or a QEF election withrespect to such stock, by providing that ei-ther election is automatically terminated im-mediately following the close of thetaxpayer’s taxable year preceding the firsttaxable year for which the stock of the PFIC

2002–44 I.R.B. 767 November 4, 2002

is subject to the mark to market regime un-der another provision of chapter 1 of theCode.

The proposed regulations also providea special rule for situations where a tax-payer owns PFIC stock that becomes sub-ject to a mark to market regime other thansection 1296 after the first taxable year ofthe taxpayer’s holding period. In such in-stances, the taxpayer must apply the coor-dination rules of § 1.1291–1(c)(3)(ii) for thefirst taxable year that such other mark tomarket regime applies. Thereafter, the gen-eral rule above, overriding the applica-tion of the section 1291, QEF and PFICmark to market regimes, applies for all sub-sequent taxable years provided that thePFIC stock continues to be marked to mar-ket under another provision of chapter 1 ofthe Code.

B. Changes to § 1.1295–1

1. Revocation of QEF election

The proposed regulations also provideguidance on the coordination of the markto market provisions under section 1296with the existing rules for QEFs. In gen-eral, the Service considered the circum-stances in which a taxpayer would bepermitted to switch from one regime to an-other in light of the relative administra-tive burdens imposed under each set ofrules, and the stated intent of Congress thatone of the purposes for enacting section1296 was to provide another alternative tothe interest charge rules of section 1291 thatwould be available in instances where tax-payers cannot obtain sufficient informa-tion to make a QEF election. See H.R. Rep.No. 105–148, at 533 (1997); S. Rep. No.105–33 at 94 (1997). Accordingly, the pro-posed regulations are structured to facili-tate an election for mark to market treatmentby permitting a taxpayer with an existingQEF election to make a section 1296 elec-tion and terminate the existing QEF elec-tion without requiring consent of theCommissioner. In instances where a tax-payer has an existing section 1296 elec-tion, it is permitted to make a QEF electiononly if the section 1296 election is termi-nated as provided by section 1296 and theregulations thereunder (e.g., if the PFICstock ceases to be marketable) or is re-voked with consent of the Commissioner.

2. Re-election of QEF regime

The proposed regulations further pro-vide that if the section 1296 election is sub-sequently terminated or revoked, other thanbecause the taxpayer marks to market un-der another provision of the Code, (e.g., be-cause the stock is no longer marketable),the shareholder will be subject to tax un-der section 1291, unless a new QEF elec-tion is made. Section 1.1295–1(i)(4)currently provides that without the Com-missioner’s consent, a shareholder whoseQEF election was invalidated, terminated,or revoked may not make a new QEF elec-tion with respect to the PFIC before thesixth taxable year ending after the tax-able year in which the invalidation, termi-nation, or revocation became effective. Theregulations propose to amend § 1.1295–1(i) to provide an exception for situationswhere a United States person’s QEF elec-tion was terminated because it elected tomark to market such stock under section1296, and the 1296 election was subse-quently terminated because the stock ceasedto be marketable. A similar exception is pro-vided for situations where a United Statesperson’s QEF election is terminated be-cause its PFIC stock is marked to marketunder another provision of chapter 1 of theCode, and such provision subsequentlyceases to apply. In either circumstance, con-sent of the Commissioner will not be re-quired for the United States person to re-elect QEF status prior to the sixth taxableyear ending after the taxable year that itsQEF election was terminated. In situa-tions where a QEF election is terminatedbecause a United States person makes a sec-tion 1296 election, and then this election ter-minates for some reason other than thestock ceasing to be marketable (e.g., pur-suant to the consent of the Commissionerunder proposed § 1.1296–1(h)(3)(A)), a tax-payer may request consent under § 1.1295–1(i) to make a new QEF election prior tosuch sixth taxable year.

Special issues arise in situations wherea taxpayer makes a QEF election with re-spect to stock that was previously markedto market under section 1296 (or where ataxpayer re-elects QEF treatment after a ter-mination of mark-to-market treatment). Insuch situations, the taxpayer shifts from an-nual inclusions under the mark to marketrules that are based on the amount of un-realized gain (or loss) in the stock of thePFIC, to annual inclusions of a pro rata

share of the ordinary earnings and long-term capital gain of a PFIC under the QEFrules. For example, unrealized items thatwere reflected in annual mark to market in-clusions could be taken into account sub-sequently under the QEF rules whenrealized. These issues presently are ad-dressed through the respective basis ad-justments provided for under the QEF andmark to market rules. See sections 1293(d)and 1296(b). Comments are requested onpossible alternative approaches for address-ing this situation with a view toward en-suring administrability and avoidingadditional complexity.

C. Addition of § 1.1296–1

1. Effect of election

The proposed regulations provide that,on the last day of a taxable year to whicha section 1296 election applies, the UnitedStates person recognizes gain to the ex-tent that the fair market value of section1296 stock exceeds its adjusted basis. Anysuch gain shall be treated as ordinary in-come. To the extent that the adjusted ba-sis of section 1296 stock exceeds its fairmarket value, the United States person maytake a deduction equal to the lesser of theamount of such excess or the unreversed in-clusions with respect to such stock. Anysuch deduction will be treated as an ordi-nary loss.

Under former proposed § 1.1291–8, cer-tain RICs were permitted to mark to mar-ket PFIC stock. For RICs that elect to markto market their PFIC stock under section1296, the unreversed inclusions includeamounts that were included in gross in-come under former proposed § 1.1291–8with respect to that stock for prior tax-able years. See Notice 92–53, 1992–2 C.B.384.

The proposed regulations also addressthe application of section 1296 in taxableyears in which the foreign corporation hasceased to be a PFIC under section 1297(a),and is not treated as a PFIC under sec-tion 1298(b)(1) (the once a PFIC, alwaysa PFIC rule). The proposed regulationsclarify that there will be no mark to mar-ket inclusions or deductions for taxableyears in which the foreign corporation is nota PFIC. The suspension of mark to mar-ket treatment while the foreign corpora-tion is not a PFIC is consistent with§ 1.1295–1(c)(2)(ii), which provides that ashareholder that has made a QEF election

November 4, 2002 768 2002–44 I.R.B.

with respect to stock of a foreign corpo-ration is not required to include its pro ratashare of ordinary income and capital gainsunder section 1293 for years in which theforeign corporation is not a PFIC.

In order to accomplish this suspensionof mark to market treatment, the proposedregulations start a new holding period, forall purposes of the PFIC rules, in stock thatis marked to market under section 1296 be-ginning on the first day of the first tax-able year beginning after the last taxableyear for which section 1296 applied. Ac-cordingly, prior periods during which theforeign corporation was a PFIC, but forwhich the shareholder had a section 1296election in effect, are not included in suchshareholder’s holding period for purposesof applying section 1298(b)(1).

Cessation of a foreign corporation’s sta-tus as a PFIC will not, however, termi-nate a section 1296 election (although ashareholder may request consent of theCommissioner to revoke the election in suchinstance, as discussed below). Thus, if theforeign corporation once again becomes aPFIC in any taxable year after a year inwhich it is not treated as a PFIC, the share-holder’s original section 1296 election con-tinues to apply and the shareholder mustmark to market the PFIC stock for suchyear.

2. Adjustment to basis

The proposed regulations provide that aUnited States person will increase the ad-justed basis of its section 1296 stock by theamount of mark to market gain recognized.Conversely, if the United States person isentitled to a deduction under this section,the adjusted basis of its section 1296 stockis decreased by the amount of such deduc-tion.

If a United States person owns section1296 stock through a foreign partnership,foreign trust, or foreign estate, the basisrules apply to both the United States per-son and the entity or entities through whichthe United States person is considered toown the stock. The increase or decrease inthe adjusted basis of the stock in the handsof the foreign partnership, foreign trust, orforeign estate will be solely attributable tothe electing United States person (in a man-ner similar to an adjustment under sec-tion 743(b)), and will apply only forpurposes of determining the subsequent U.S.income tax treatment of the United States

person with respect to such stock. The IRSconsidered imposing reporting and recordkeeping requirements on the foreign enti-ties to track the adjustments to the ad-justed basis of any section 1296 stock theyheld directly or indirectly. The IRS de-cided not to adopt this approach in the pro-posed regulations because one of themotivations for the enactment of section1296 was to provide an alternative tax re-gime to section 1291 for taxpayers thatcould not obtain sufficient information froma PFIC to make a QEF election. Com-ments are requested about other approachesfor satisfying the compliance obligations ofU.S. persons making a section 1296 elec-tion and the intervening entity or entitiesthrough which such stock is owned.

The taxpayer and the entity throughwhich the taxpayer owns section 1296 stockmay have different taxable years. Consis-tent with the general approach of sections706(a), 652(c), and 662(c), a United Statesperson who owns stock in a PFIC throughany foreign partnership, foreign trust, or for-eign estate determines the mark to mar-ket gain or mark to market loss withreference to the last day of the taxable yearof the foreign partnership, foreign trust orforeign estate and then includes that gainor loss in the taxable year of such UnitedStates person that includes the last day ofthe taxable year of the entity.

Finally, if PFIC stock is acquired froma decedent by bequest, devise, or inherit-ance (or by the decedent’s estate) and amark to market election was in effect on thedecedent’s date of death, the adjusted ba-sis of such stock in the hands of the re-cipient will be equal to the lesser of thebasis determined under section 1014 or theadjusted basis of the stock in the hands ofthe decedent immediately prior to his or herdeath.

3. Rule for individuals that becomesubject to United States income taxation

The proposed regulations provide that ifany individual becomes a United States per-son in a taxable year beginning after De-cember 31, 1997, the adjusted basis (beforeany adjustments resulting from the mark tomarket election are made) of any stock ina PFIC owned by such individual on thefirst day of such taxable year shall betreated as being the greater of its fair mar-ket value on such first day or its adjustedbasis on such first day. This special rule for

determining the taxpayer’s adjusted basiswill apply only for purposes of section 1296and the regulations thereunder. Accord-ingly, any gain or loss recognized on thedisposition of section 1296 stock that is at-tributable to the period before the indi-vidual became a United States person willbe subject to the general rules of the Code,including any limitation on the deductibil-ity of a loss, for example, under section1211.

4. Indirect ownership of PFIC stock

Except as discussed below in the caseof eligible RICs, the proposed regulationsapply the specific attribution rules of sec-tion 1296(g) in determining whether PFICstock is considered owned by a taxpayer forpurposes of section 1296 and, therefore,with respect to which the taxpayer is per-mitted to make a section 1296 election.Thus, a United States person will be per-mitted to make a section 1296 election withrespect to stock owned through a foreignpartnership, foreign trust, or foreign es-tate. In general, stock owned by or for suchentities will be considered as being ownedproportionately by its partners or benefi-ciaries. For purposes of this rule, stockowned, directly or indirectly, by or for a for-eign trust described in sections 671 through679, shall be considered as being ownedproportionately by its grantors or other per-sons treated as owners under sections 671through 679 of any portion of the trust thatincludes the stock.

The section 1296(g) attribution rules donot attribute ownership through foreign cor-porations. Accordingly, a United States per-son will not be permitted to make a section1296 election with respect to stock ownedindirectly through a foreign corporation.However, as discussed below, in instanceswhere the foreign corporation is a CFC, theforeign corporation is permitted to make asection 1296 election directly.

Special attribution rules for eligible RICsare provided in § 1.1296(e)–1(f). There isa different attribution rule for RICs be-cause section 1296(e)(2), which provides aspecial rule for RICs, states that stockowned, directly or indirectly, by the RIC,without reference to the ownership attri-bution rules in section 1296(g), shall betreated as marketable stock. This approachis consistent with former proposed§ 1.1291–8, which permitted certain RICsto mark to market PFIC stock that it owned

2002–44 I.R.B. 769 November 4, 2002

directly or indirectly.An issue not addressed in these pro-

posed regulations is the treatment of cer-tain situations involving multiple tiers ofPFICs. For example, assume a United Statesperson owns marketable stock in a PFIC,that itself owns stock in a second PFIC, theownership of which is attributable to theUnited States person under section1298(a)(2). If the United States personmakes a section 1296 election with re-spect to stock of the upper-tier PFIC, theannual mark to market inclusions of in-come under section 1296 will be based onthe fair market value of the upper-tier PFICstock, whose value should reflect the valueof the lower-tier PFIC, as such stock is anasset of the upper-tier PFIC. However, un-der current law, the United States personcontinues to be subject to taxation with re-spect to its indirect ownership of the lower-tier PFIC under section 1291 on any excessdistributions from the lower-tier PFIC orgain from an indirect disposition of thelower-tier PFIC stock (although the con-sequences from the tiered ownership maybe ameliorated by adjustments to the ba-sis of the upper-tier PFIC stock). See pro-posed §§ 1.1291–2(f), and 1.1291–3(e).Similar issues arise if the United States per-son makes a QEF election with respect tothe lower-tier PFIC. Comments are re-quested regarding coordination rules or otheradjustments that may be appropriate to ad-dress this situation and similar structures in-volving a United States person that ownsstock directly and indirectly in tiers ofPFICs.

5. Treatment of CFCs as United Statespersons

A CFC that owns PFIC stock is treatedas a United States person for purposes ofsection 1296 and, as noted above, is per-mitted to make a section 1296 election di-rectly. If a section 1296 election is madewith respect to PFIC stock owned by a CFCdirectly, or treated as owned by a CFC ap-plying the section 1296(g) attribution rules,then any mark to market gains are includedin the gross income of the CFC as for-eign personal holding company income un-der section 954(c)(1)(A) and any mark tomarket losses are treated as deductions al-locable to such foreign personal holdingcompany income for purposes of comput-ing net foreign base company income un-der § 1.954–1(c).

Under the proposed regulations, if a sec-tion 1296 election is made for a CFC withrespect to its PFIC stock, the PFIC rules donot also apply separately to any UnitedStates shareholder, as defined in section951(b), with respect to its pro rata share ofthe PFIC stock held by the CFC. Instead,the United States shareholder generally willrecognize the mark to market gain as an in-clusion of income under section 951(a).Thus, United States shareholders of CFCsare appropriately excluded from the appli-cation of section 1291 if a section 1296election is made by the CFC. This rule,however, does not apply to United Statespersons who own stock of the CFC but arenot United States shareholders within themeaning of section 951(b). Those UnitedStates persons continue to be subject to thePFIC provisions with respect to the stockof such foreign corporation, and may availthemselves of a QEF election. This rule isconsistent with the CFC/PFIC overlap rulein section 1297(e), which eliminates the ap-plication of the PFIC provisions solely forUnited States shareholders of the entity thatis both a PFIC and a CFC. Finally, com-ments are requested about whether simi-lar rules should apply to United Statespersons that are United States sharehold-ers of a CFC solely by application of sec-tion 953(c)(1)(A).

6. Elections

The proposed regulations provide that aUnited States person may make a section1296 election for a taxable year begin-ning after December 31, 1997, by the duedate (including extensions) of the UnitedStates person’s federal income tax return.The proposed regulations further providethat a section 1296 election of a CFC ismade by its controlling United States share-holders by the due date (including exten-sions) of their federal income tax returnsin accordance with the general rules forelections by a CFC under § 1.964–1(c)(5).

The proposed regulations provide that asection 1296 election applies to the year forwhich made and to each succeeding yearunless the election is terminated or re-voked. A section 1296 election automati-cally terminates when (i) the PFIC stockceases to be marketable, or (ii) when thePFIC stock is marked to market under an-other provision of chapter 1 of the Code.A section 1296 election also may be re-voked with the consent of the Commis-

sioner. Such consent will only be granted,however, upon a showing of a substantialchange in circumstances. Similar rules ap-ply in the case of the revocation of a QEFelection.

7. Coordination rules for first year ofelection

Finally, the proposed regulations pro-vide coordination rules that apply to the firsttaxable year to which section 1296 ap-plies. A United States person (other than aRIC) whose holding period includes a pe-riod when the foreign corporation was aPFIC and for which a QEF election had notbeen made generally will be subject to sec-tion 1291 in the year of the election andsubject to section 1296 in subsequent years.Special rules also apply to RICs for the firstyear in which a section 1296 election ap-plies.

D. Changes to § 1.1296(e)–1(b)