bulgaria in the international ski market · bulgaria in the international ski market ... snowboard...

TRANSCRIPT

La

ure

nt

Va

na

t

LV/25/03/2016

Bulgaria in the international ski market

Round table for the Development of the Winter/Ski tourism

Sofia – 11 February 2016

page 2

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Agenda

The state of the industry today

International flows

Regional focus

page 3

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Market metrics

Skier : one person practising ski, snowboard or other downhill slide, independent of the rate of practice.

Skier visit : one person visiting a ski area for all or any part of a day or night for the purpose of skiing, snowboarding, or other downhill sliding. Skier visits include full-day, half-day, night, complimentary, adult, child, season pass and any other type of ticket that gives a skier/snowboarder the use of an area's facilities.

La

ure

nt

Va

na

t

LV/25/03/2016

The state of the industry today

page 5

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

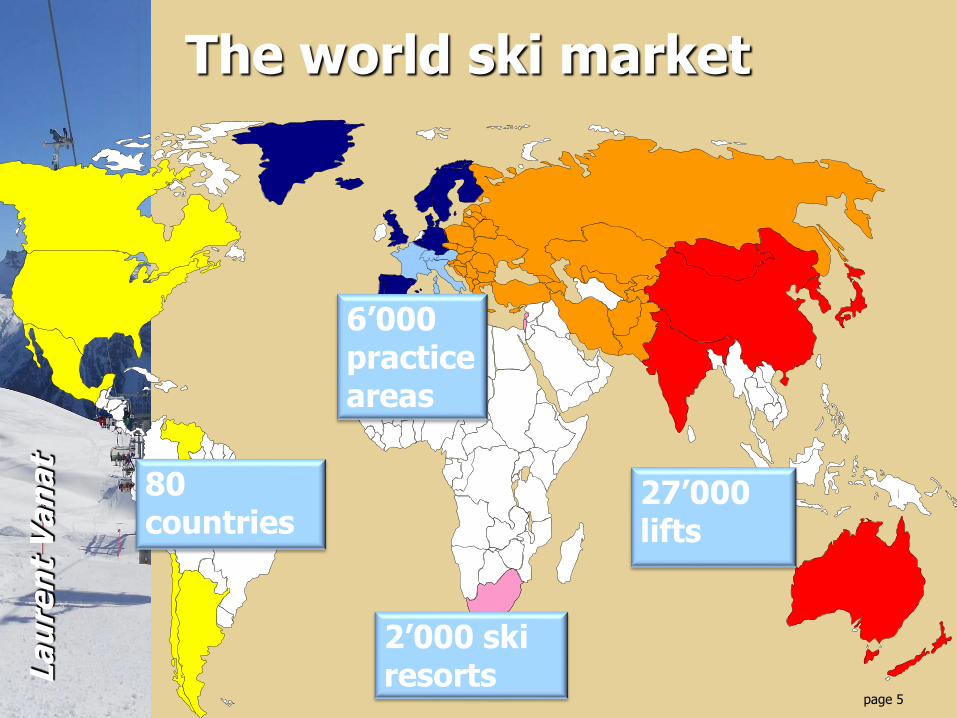

The world ski market

27’000 lifts

6’000 practice areas

80 countries

2’000 ski resorts

page 6

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Who are the skiers ?

Spread of the skiers upon country of origin (125 million skiers estimated worldwide)

Eastern Europe &

Central Asia15%

Asia & Pacific18%

Various1%

Alps15%

Western Europe26%

America25%

page 7

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Where do they ski ?

Market share in the worldwide skier visits (400 million yearly skier visits)

Eastern Europe &

Central Asia10%

America21%

Asia & Pacific15%

Various0%

Alps43%

Western Europe11%

page 8

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

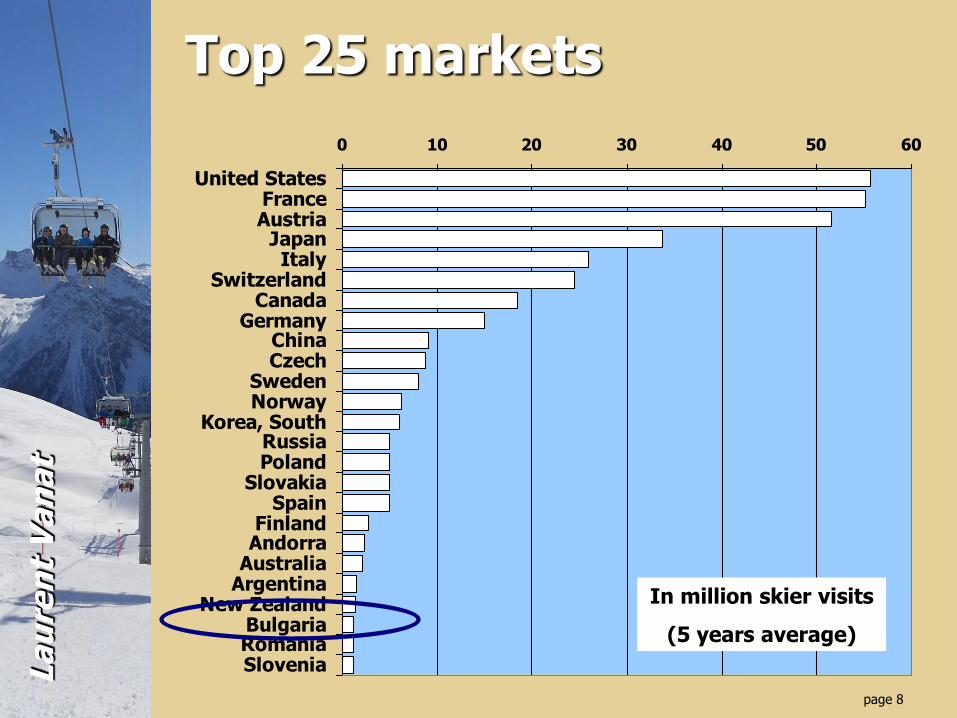

0 10 20 30 40 50 60

United StatesFranceAustria

JapanItaly

SwitzerlandCanada

GermanyChinaCzech

SwedenNorway

Korea, SouthRussiaPoland

SlovakiaSpain

FinlandAndorra

AustraliaArgentina

New ZealandBulgariaRomaniaSlovenia

Top 25 markets

In million skier visits

(5 years average)

page 9

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Majors73%

Others27%

Major players (countries)

A limited number of countries concentrate most of the attendance

7 countries

70 countries

page 10

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

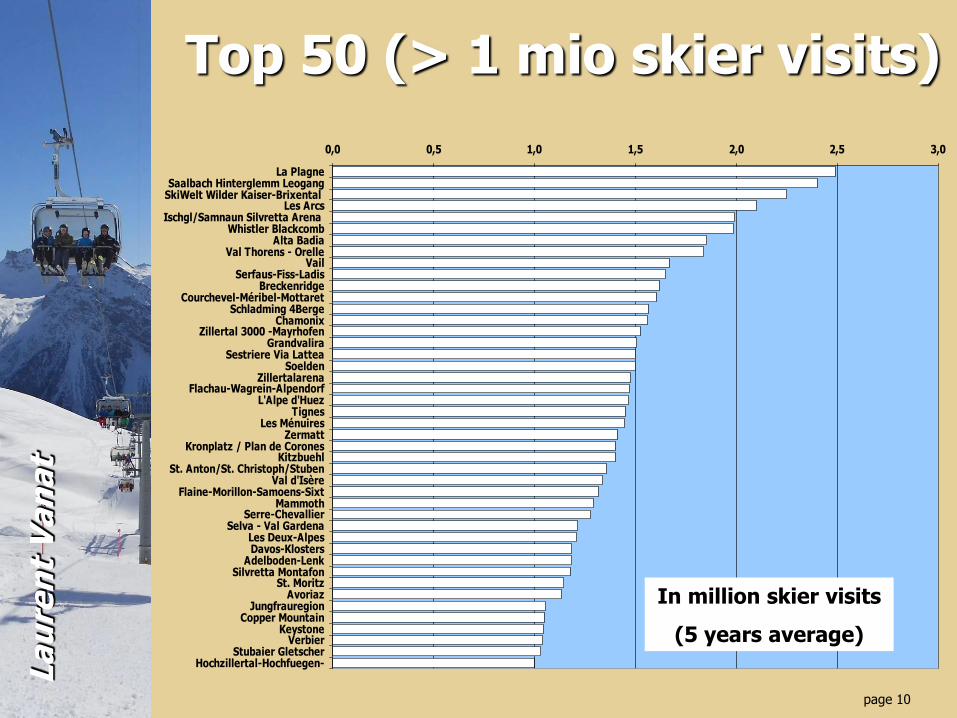

0,0 0,5 1,0 1,5 2,0 2,5 3,0

La PlagneSaalbach Hinterglemm Leogang

SkiWelt Wilder Kaiser-Brixental Les Arcs

Ischgl/Samnaun Silvretta Arena Whistler Blackcomb

Alta BadiaVal Thorens - Orelle

VailSerfaus-Fiss-Ladis

BreckenridgeCourchevel-Méribel-Mottaret

Schladming 4BergeChamonix

Zillertal 3000 -MayrhofenGrandvalira

Sestriere Via LatteaSoelden

ZillertalarenaFlachau-Wagrein-Alpendorf

L'Alpe d'HuezTignes

Les MénuiresZermatt

Kronplatz / Plan de CoronesKitzbuehl

St. Anton/St. Christoph/StubenVal d'Isère

Flaine-Morillon-Samoens-SixtMammoth

Serre-ChevallierSelva - Val Gardena

Les Deux-AlpesDavos-Klosters

Adelboden-LenkSilvretta Montafon

St. MoritzAvoriaz

JungfrauregionCopper Mountain

KeystoneVerbier

Stubaier GletscherHochzillertal-Hochfuegen-

Top 50 (> 1 mio skier visits)

In million skier visits

(5 years average)

page 11

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Top 50 resorts

37 of the largest ski resorts are located in the Alps

Alps84%

Western Europe

2%

America14%

page 12

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

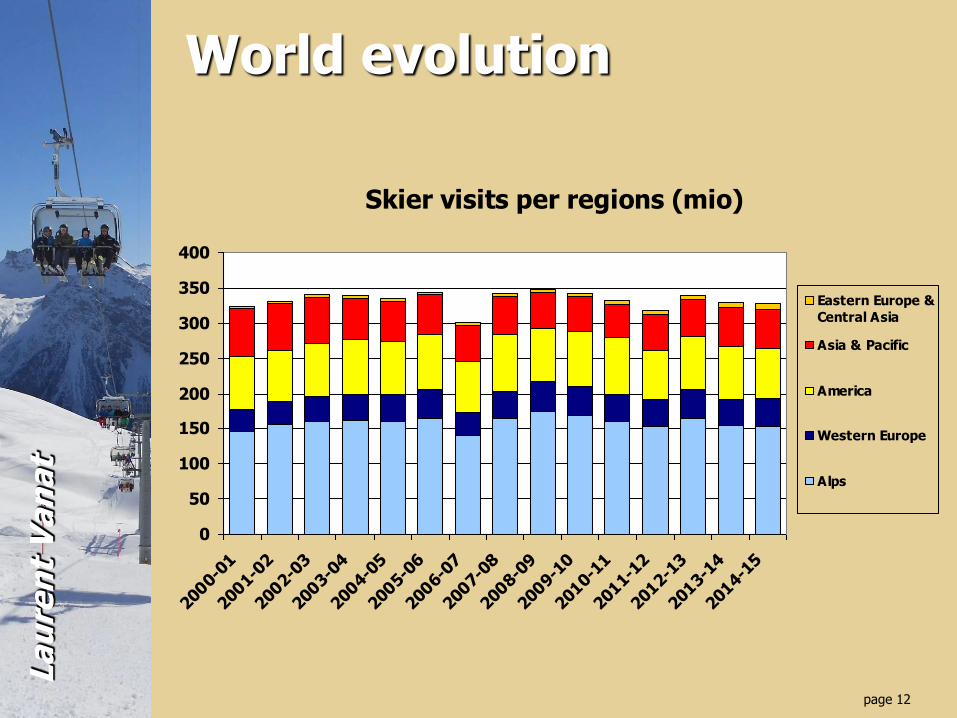

World evolution

Skier visits per regions (mio)

0

50

100

150

200

250

300

350

400

2000-01

2001-02

2002-03

2003-04

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

Eastern Europe &Central Asia

Asia & Pacific

America

Western Europe

Alps

page 13

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Evolution of 5-years average skier visits per regionsBase 100 for season 2004/05

80

85

90

95

100

105

110

115

120

2004-05

2005-06

2006-07

2007-08

2008-09

2009-10

2010-11

2011-12

2012-13

2013-14

2014-15

Alps

WesternEurope

America

Asia & Pacific

Regional evolution

General inflection point in 2012/13

page 14

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Why this opposite inflexion ?

Mature stage of the industry in Europe

– Aging and stagnating population, baby-boomers retiring

– Failure to gain new skiers

– Increasing competing activities

– Few innovation

– Inability to develop the 4-season activity

– Weak marketing

Developing / redeveloping stage in Asia

– Young generations

– Sport becoming fashionable

– Japan seems to enter into a recovery phase

La

ure

nt

Va

na

t

LV/25/03/2016

International skiers flows

page 16

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

National skiers

The national customer base is very strong in most of the big players. Foreign visitors concentrate on a few top international resorts.

Proportion foreign skiers

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

An

do

rra

Au

str

ia

No

rwa

y

Sw

itze

rla

nd

Ne

w Z

ea

lan

d

Ch

ile

Cze

ch

Re

pu

blic

Ita

ly

Fra

nce

Slo

va

kia

Arg

en

tin

a

Fin

lan

d

Slo

ve

nia

Sw

ed

en

Po

lan

d

Ca

na

da

Ge

rma

ny

Ko

rea

, S

ou

th

Sp

ain

Ja

pa

n

Un

ite

d S

tate

s

Ro

ma

nia

Ru

ssia

Au

str

alia

Ch

ina

Nationals Foreign

page 17

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

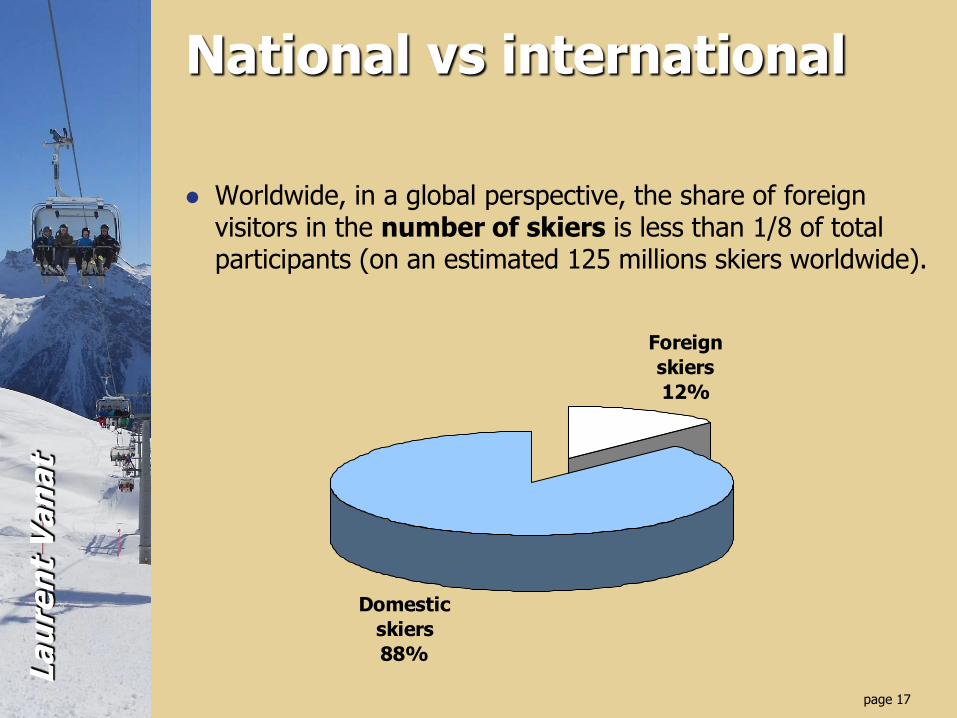

National vs international

Worldwide, in a global perspective, the share of foreign visitors in the number of skiers is less than 1/8 of total participants (on an estimated 125 millions skiers worldwide).

Foreign skiers12%

Domestic skiers88%

page 18

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Top 10 inbound markets

Few big players; ski is mostly a domestic market !

In million inbound skiers

0,0 1,0 2,0 3,0 4,0 5,0

Austria

France

Italy

Switzerland

Czech Republic

United States

Andorra

Norway

Canada

Japan

page 19

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Top 10 outbound markets

Only 2 big providers; issue of markets’ ski culture

In million outbound skiers

0,0 0,5 1,0 1,5 2,0 2,5 3,0 3,5 4,0 4,5

Germany

United Kingdom

Netherlands

Belgium

Switzerland

Russia

Denmark

Spain

France

Poland

page 20

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

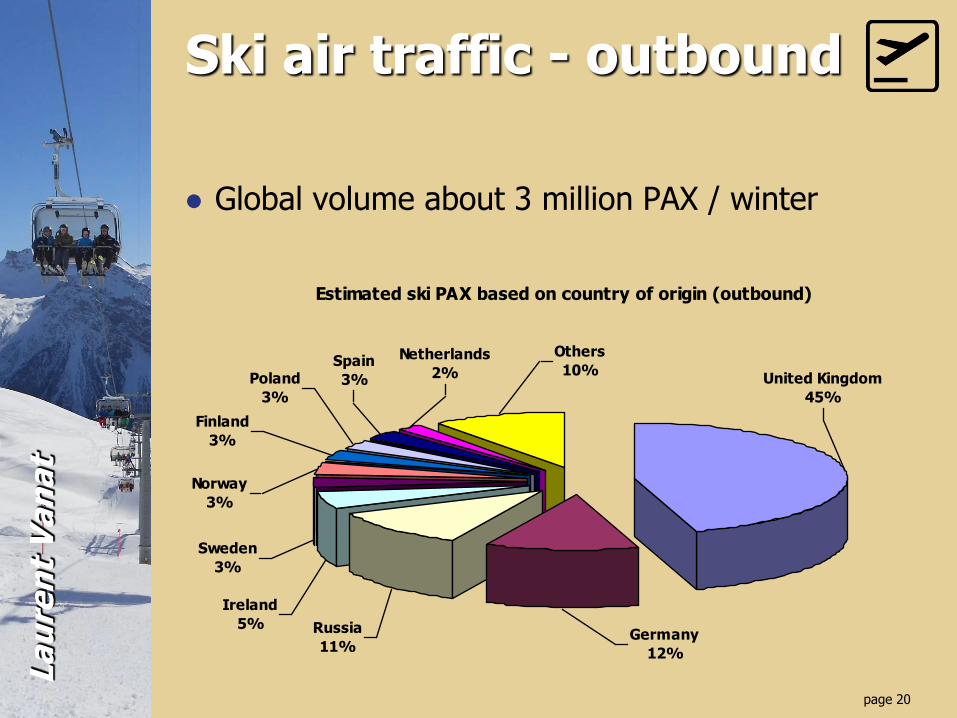

Ski air traffic - outbound

Global volume about 3 million PAX / winter

Estimated ski PAX based on country of origin (outbound)

Netherlands2%

Germany12%

Others10%

Finland3%

Poland3%

Norway3%

Ireland5%

Sweden3%

Russia11%

Spain3% United Kingdom

45%

page 21

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

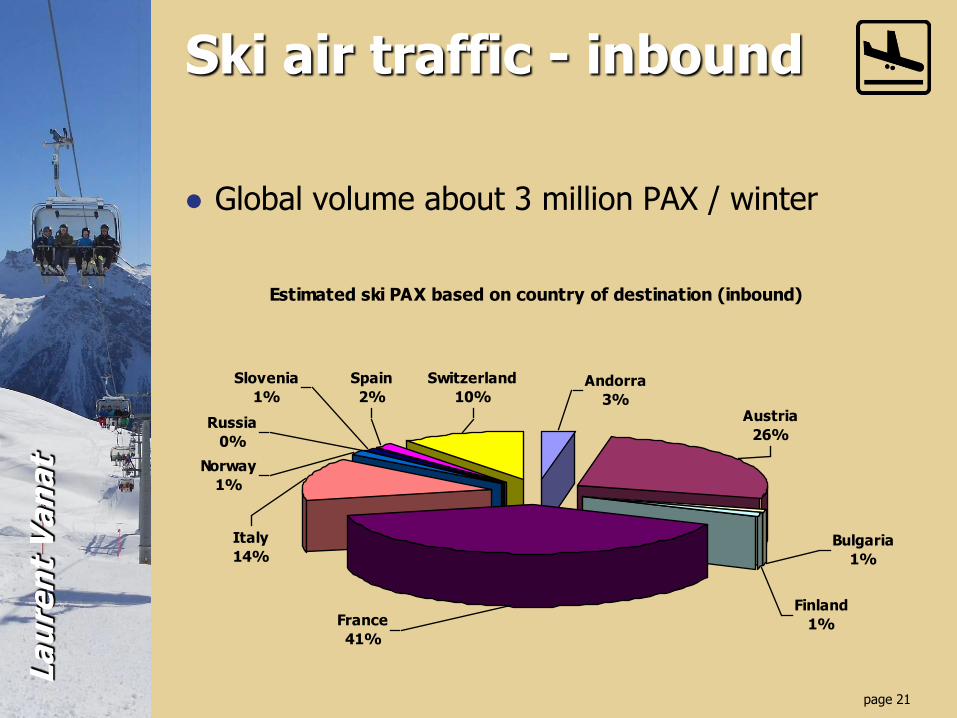

Ski air traffic - inbound

Global volume about 3 million PAX / winter

Estimated ski PAX based on country of destination (inbound)

France41%

Austria26%

Andorra3%

Switzerland10%

Russia0%

Italy14%

Spain2%

Norway1%

Slovenia1%

Bulgaria1%

Finland1%

La

ure

nt

Va

na

t

LV/25/03/2016

Regional focus

page 23

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

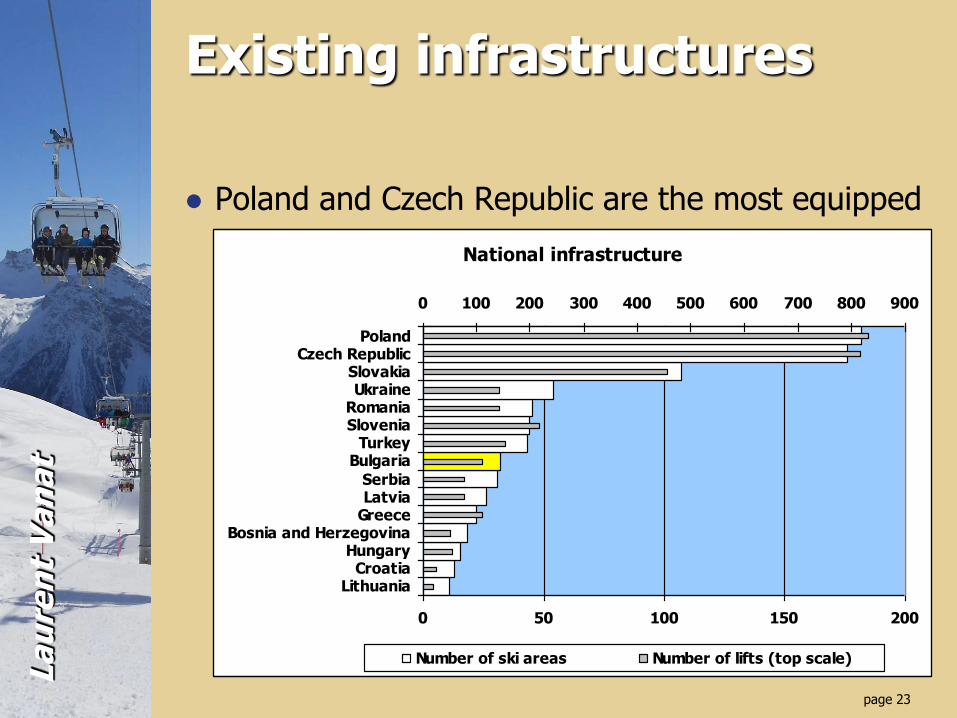

Existing infrastructures

Poland and Czech Republic are the most equipped

National infrastructure

0 50 100 150 200

LithuaniaCroatia

HungaryBosnia and Herzegovina

GreeceLatviaSerbia

BulgariaTurkey

SloveniaRomaniaUkraine

SlovakiaCzech Republic

Poland

0 100 200 300 400 500 600 700 800 900

Number of ski areas Number of lifts (top scale)

page 24

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

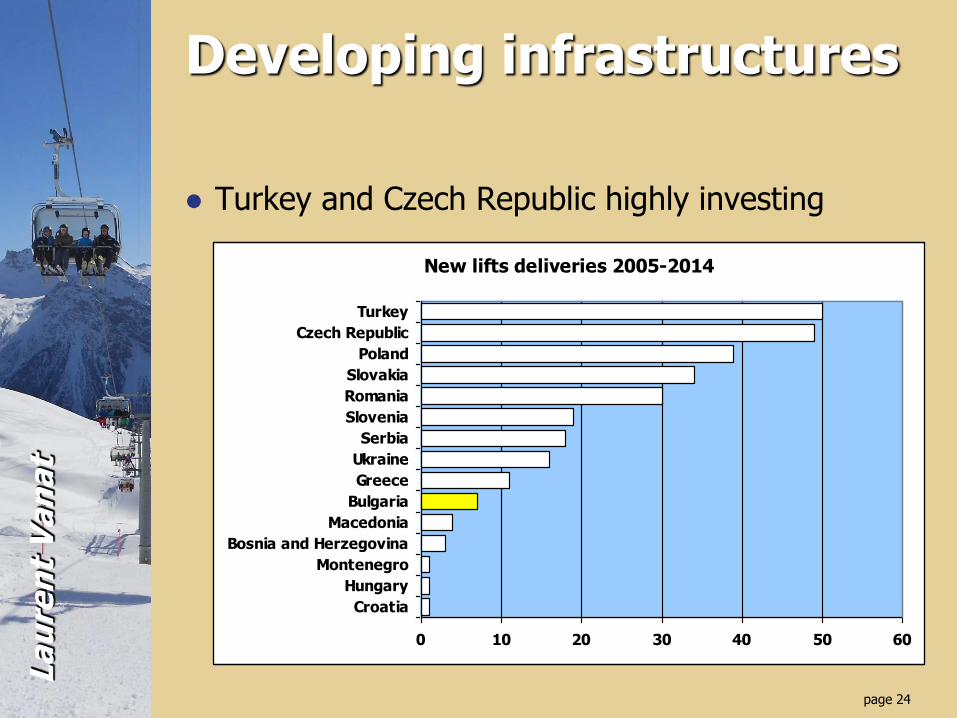

Developing infrastructures

Turkey and Czech Republic highly investing

New lifts deliveries 2005-2014

0 10 20 30 40 50 60

Croatia

Hungary

Montenegro

Bosnia and Herzegovina

Macedonia

Bulgaria

Greece

Ukraine

Serbia

Slovenia

Romania

Slovakia

Poland

Czech Republic

Turkey

page 25

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

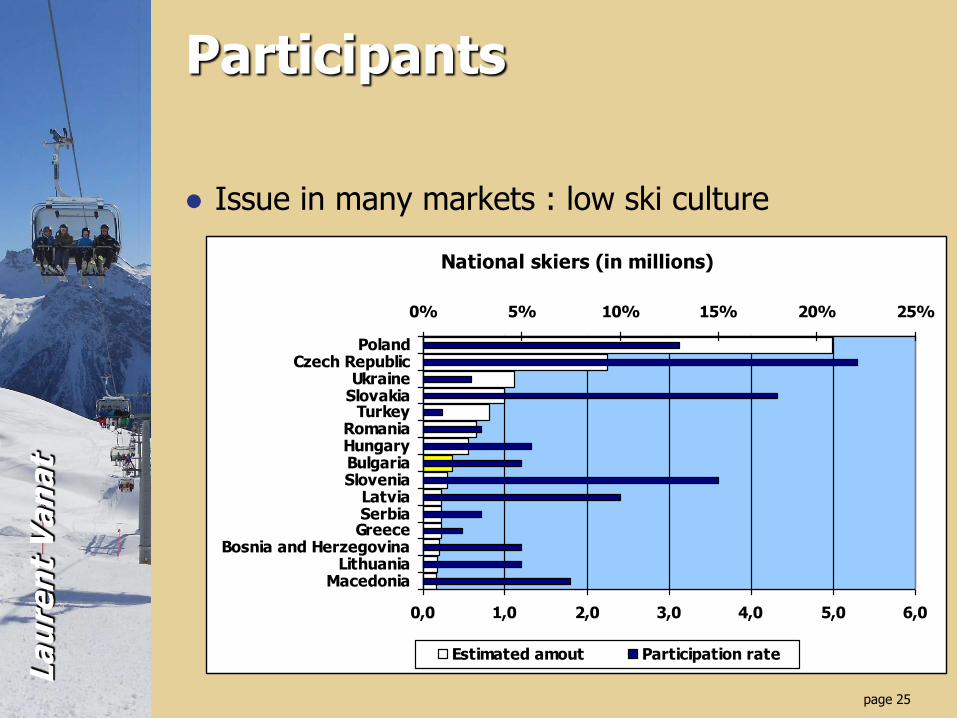

Participants

Issue in many markets : low ski culture

National skiers (in millions)

0,0 1,0 2,0 3,0 4,0 5,0 6,0

MacedoniaLithuania

Bosnia and HerzegovinaGreeceSerbiaLatvia

SloveniaBulgariaHungaryRomania

TurkeySlovakiaUkraine

Czech RepublicPoland

0% 5% 10% 15% 20% 25%

Estimated amout Participation rate

page 26

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Participants

Average loyalty to the sport not very high

Yearly skier visits per national skier

0 1 2 3 4

HungaryPoland

LithuaniaBosnia and

UkraineTurkey

MacedoniaRomania

Czech RepublicBulgaria

SerbiaLatvia

SloveniaGreece

Slovakia

page 27

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

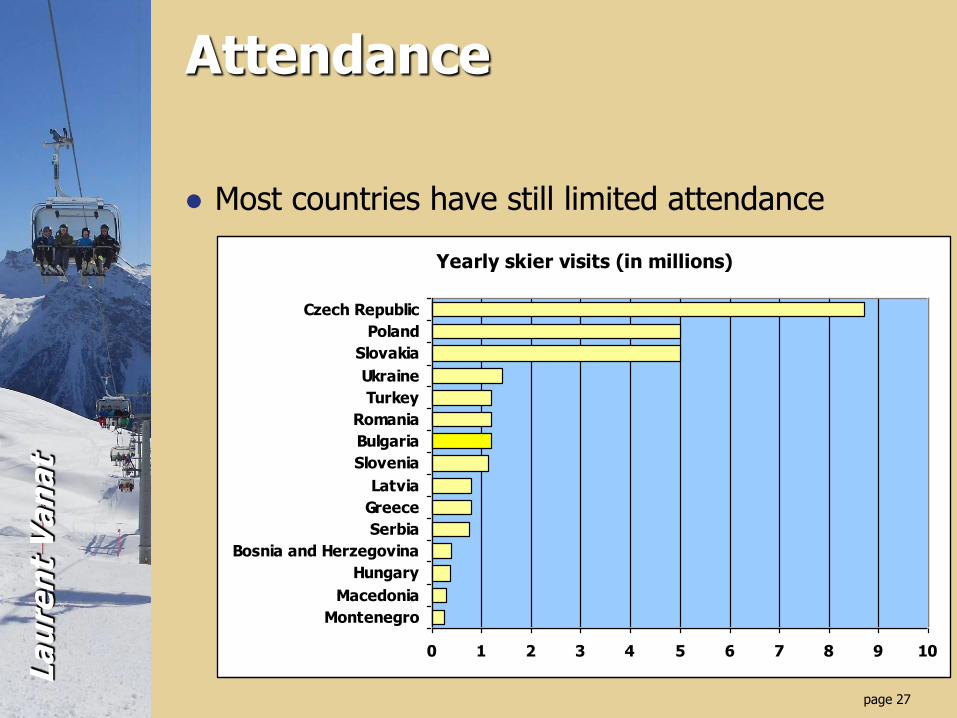

Attendance

Most countries have still limited attendance

Yearly skier visits (in millions)

0 1 2 3 4 5 6 7 8 9 10

Montenegro

Macedonia

Hungary

Bosnia and Herzegovina

Serbia

Greece

Latvia

Slovenia

Bulgaria

Romania

Turkey

Ukraine

Slovakia

Poland

Czech Republic

La

ure

nt

Va

na

t

LV/25/03/2016

Conclusion

page 29

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

Future prospects

The European supply market is flattening

Most markets are and will remain domestic

The challenge is to gain and retain local skiers

Prospective 2020 : 420 mio skier visits

page 30

La

ure

nt

Va

na

t

La

ure

nt

Va

na

t

For further reference

Available from

www.vanat.ch page Publications

La

ure

nt

Va

na

t

LV/25/03/2016

Laurent Vanat

19, Margelle

CH - 1224 Geneva

Tel / voicemail : +4122 349 8440

E-mail : [email protected]

Website : www.vanat.ch

Laurent Vanat