building the european digital … · • akamai, alcatel-lucent, amazon, ard/wdr, bbc, belgacom,...

TRANSCRIPT

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

BUILDING THE EUROPEAN DIGITAL INFRASTRUCTURE 2011 CEO ROUNDTABLE: ONE YEAR LATER

Collective Industry Findings from the CEO Roundtable on Broadband Investment to Sustain Internet Growth

GABRIELLE GAUTHEY, EVP ALCATEL-LUCENT 20 June 2012

2

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

CROSS-INDUSTRY CEO INITIATIVE

EuropeanCommissionVP for the

Digital Agenda Neelie Kroes

HOW TO ADDRESS BB INVESTMENT CHALLENGES (3/03/11 – 13/07/11)

Objectives were to find the NGA dynamics which will foster investment and help Europe in reaching the Digital Agenda broadband targets by 2020

New approach beyond existing initiatives scope Inclusive: Not a carrier-centric initiative but an industry-wide effort

embarking all ecosystem partiesExecutive led: 2 CEOs meetings in Brussels hosted by the CommissionerForward looking: Embracing and driving change towards a new 2015+ cross-

industry standards use rather than preserving status-quo

Change ahead needed !Need for 200 B€ investment in a context of

…Declining revenues of Service Providers …Changing business models with Over-The-Tops

From 3 working groups to CEOs 11 proposals Wg1 -« New business models for Internet development »Wg2 -« Technical Framework for Digital Delivery - Interoperability and Standardization »Wg3 -« Investment framework and financing sources to foster NGA roll-out »

• Akamai, Alcatel-Lucent, Amazon, ARD/WDR, BBC, Belgacom, Bertelsmann AG , BT, Cisco, Cogent, Deutsche Telekom, eBay, EIB, Ericsson, Facebook, Fastweb, Google, Mediaset, Microsoft, Netlog / Massive Media, Nokia, NSN, Orange, Prisa, RIM, Samsung, Sony , Sony Music , Telecom Italia, Telefonica, Tel, a Sonera, Virgin Media, Vodafone, Voddler, Wind, Vivendi, Fnac.com, Skype, Apple, BSkyB, Eircom, Exalead, Free – Iliad, Level 3, News Corp, Spotify, Tele2, Zed, TVN, Sigma TV

Participating companies

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

4

THE CONTEXT IS CHALLENGING DATA EXPLOSION, SUPPLY SIDE, POSITIVE ROI

DEMAND SIDE IS IN CONTROL THIS IS VERY DEMANDING

(WIRELESS) SUPPLY IS CHALLENGING OPERATORS ARE LOOSING VALUE

Less revenues for more investment required : how to unlock the network value to meet the user demand ?

Smart phone density From 400 to 12,800 per km2 in 2016

Mobile data traffic x 25 times over 2011 - 2016

Data over mobile 70% of networks traffic by 2016

Source: Arthur D. Little, Exane BNP Paribas, Analysys Mason, IDATENote 2: NGA includes wireline technologies providing ultra fast broadband (all FTTx technologies and DOCSIS 3.0)

NGA ROLL-OUT WALL OF INVESTMENT, EU IS LAGGING BEHING

North America65% 10-30%

Europe

Japan - Korea

35% 5-10%

80% >40%

Homes passed

Homes connected

Legend

World, 2010

North America and Asia-Pacific have taken the lead of NGA networks deployment2

U.S. (2012) : • 8 M subs• 22M Home passed

China (2011) :• 38 M FTTx subsFTTH Forecast :• 80 M homes passed end 2013• 100 M homes passed end 2015

6

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

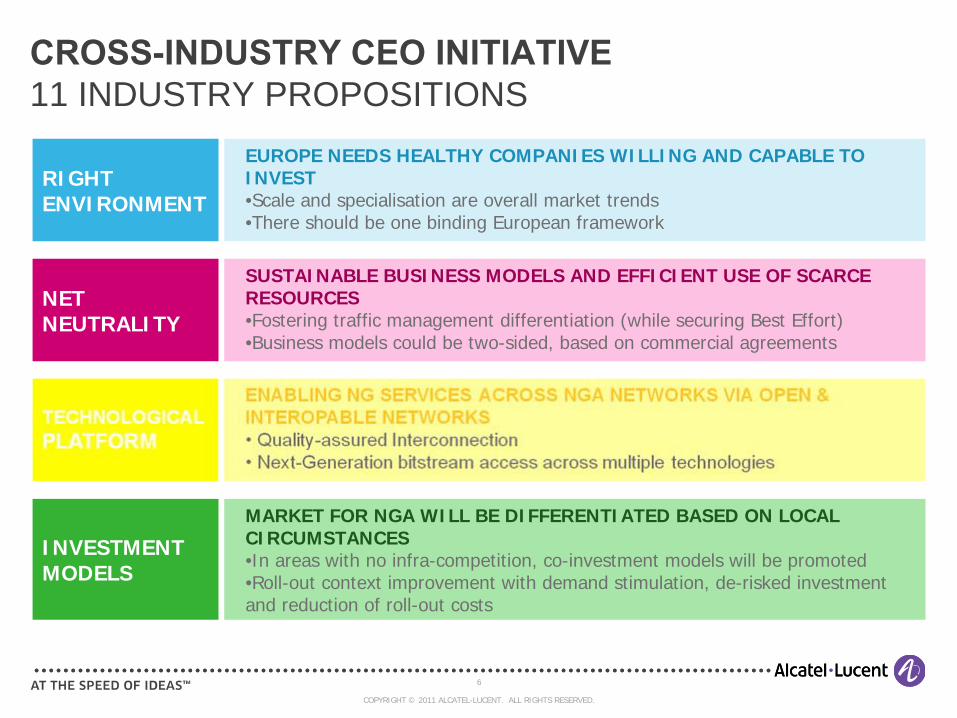

CROSS-INDUSTRY CEO INITIATIVE 11 INDUSTRY PROPOSITIONS

RIGHTENVIRONMENT

EUROPE NEEDS HEALTHY COMPANIES WILLING AND CAPABLE TO INVEST•Scale and specialisation are overall market trends•There should be one binding European framework

NET NEUTRALITY

SUSTAINABLE BUSINESS MODELS AND EFFICIENT USE OF SCARCE RESOURCES•Fostering traffic management differentiation (while securing Best Effort)•Business models could be two-sided, based on commercial agreements

INVESTMENT MODELS

MARKET FOR NGA WILL BE DIFFERENTIATED BASED ON LOCAL CIRCUMSTANCES•In areas with no infra-competition, co-investment models will be promoted •Roll-out context improvement with demand stimulation, de-risked investment and reduction of roll-out costs

COPYRIGHT © 2011 ALCATEL-LUCENT. ALL RIGHTS RESERVED.

7

MIX OF TECHNOLOGIES TO MEET DA TARGETS FTTX FOR COST-EFFECTIVE AND QUICK ROLL-OUTS

• All technologies (LTE included) require fiber deep in the network• Ensure “Active” infrastructure-based competition

ADSLx CO

FTTN VDSL2

FTTB (apartment building)

FTTH (single house)

0

5

10

15

1

FTTx fiber investment can be leveraged for FTTH

CAPEX (index) Source: Alcatel-Lucent

Access HW

CPE Civil works

MDU cabling

Cabinet Fiber

FTTN

FTTB/Curb

FTTHVDSL2 20-50 Mbps

ADSL2+ 10-20 Mbps

VDSL2 Bonding 40-80 Mbps

VDSL2 20-50 Mbps

VDSL2 40-80 Mbps

Vectoring50-100 Mbps

PON/P2P 100+ Mbps

Vectoring 50-100 Mbps

co

FTTB/Curb

FTTA

LTE 30 Mbps

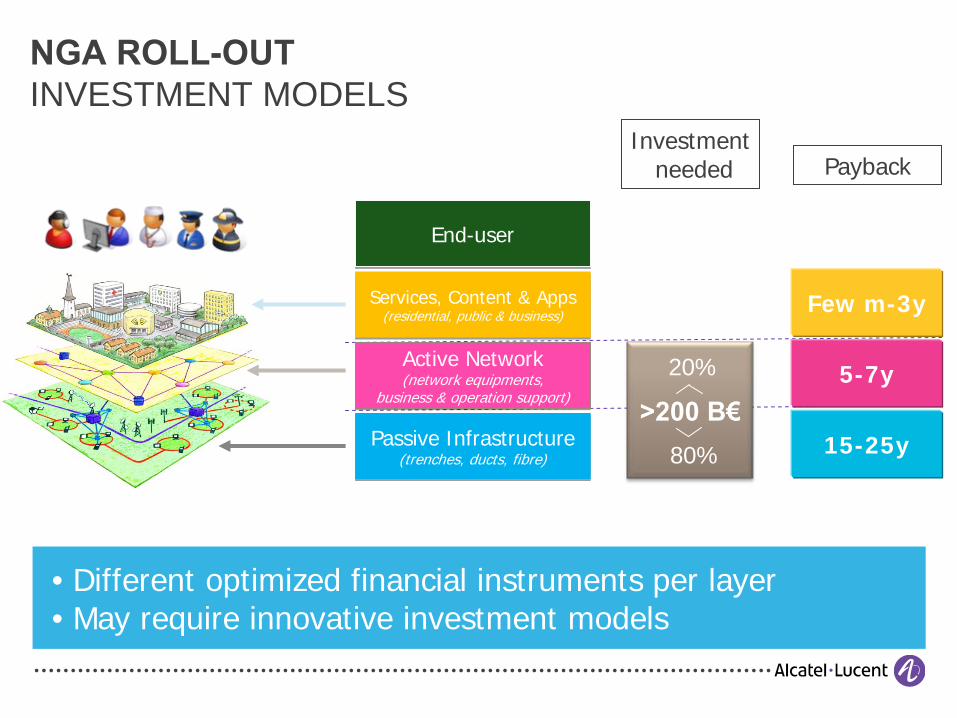

NGA ROLL-OUT INVESTMENT MODELS

• Different optimized financial instruments per layer• May require innovative investment models

Services, Content & Apps (residential, public & business)

Services, Content & Apps (residential, public & business)

Active Network(network equipments,

business & operation support)

Active Network(network equipments,

business & operation support)

Passive Infrastructure(trenches, ducts, fibre)

Passive Infrastructure(trenches, ducts, fibre)

End-userEnd-user

>200 B€

Investment needed Payback

Few m-3y

5-7y

15-25y

20%

80%

ROI

RiskNGA roll out

Lack of investment in NGA networks

NO FIT BETWEEN INVESTMENT PROFILES AND NGA OPPORTUNITIES

Infrastructure

Funds

Telecom Operators

Insufficient ROI:• Cherry picking• Digital Gap• Wait and see

High risk :•No focus on Telecom• Wait and see

Solution calls for: CAPEX reduction to increase ROI, lower risk via long-term usage contract

very low

Indication of sectorial funds focus over the next two years

0 1 2 3 4 5

10.Infrastructure� services

1.Energy

2.Roads

3.Rail/Metro

4.Ports

5.Airports

6.Water

7.Waste

8.PPP/PFI

9.Telecoms

TELECOM INDUSTRY DOES NOT SEEM TO FULLY MEET THE REQUIREMENTS OF INFRASTRUCTURE FUNDS

Source: Contribution, Deloitte 2010, Arthur D. Little

Conditions for infrastructure funds to invest

Investors seeking exposure to a periodic, stable and guaranteed cash flows

Need for a regulated market with contained competition and strong barriers to entry

Necessity to make investments fit with infrastructure funds’ risk profile:

Advocate for separation of passive layer vs. active and retail to lower risk on the passive layer part

Guarantee of a single fibre network in case of operating cable operators and a maximum of two fibre networks in a given area where there is no cable operators

Participation of the incumbent in the Netco

very high

NON-LISTED INFRASTRUCTURE FUNDS: 41 B€ SINCE 2003…

Source: Preqin

12

9

1413

24

5

18

10

0,1 0,9

4,4 4,8

15,213,6

2,8

9,3

3

0

5

10

15

20

25

30

2003 2004 2005 2006 2007 2008 2009 2010 2011Nombre de Fonds levés / en levée Montant total levé / en levée (Md$)

Many Infrastructure funds are available

• Local circumstances will prevail for NGA roll-out – No One-size fits all

• In some areas, infrastructure competition already fierce (presence of cable operators) will lead to mixed FTTx access technologies (fibre closer to end-user premises)

• In policy-driven areas, public intervention will be required -

• Solutions should not only be built on geographic segmentation but also with a layered approach, allowing co-investing models – and use of derisking financial instruments

• In all areas, Mobile demand is also driving progressive migration towards fibre backhauling

NGA INVESTMENT MODELS MAIN OUTCOMES

Intervention from long term investors would be a key enabler to improve current NGA roll-out dynamics