building products & materials - harriswilliams.com · ... dynamics within the global building...

TRANSCRIPT

www.harriswilliams.de

Harris Williams & Co. Ltd is a private limited company incorporated under English law having its registered office at 5th Floor, 6 St. Andrew Street, London EC4A 3AE, UK, registered with the Registrar of Companies for England and Wales under company number 7078852. Directors: Mr. Christopher Williams, Mr. Ned Valentine, Mr. Paul Poggi and Mr. Thierry Monjauze, authorised and regulated by the Financial Conduct Authority.

Harris Williams & Co. Ltd Niederlassung Frankfurt (German branch) is registered in the Commercial Register (Handelsregister) of the Local Court (Amtsgericht) of Frankfurt am Main, Germany, under registration number HRB 96687, having its business address at Bockenheimer Landstrasse 33-35, 60325 Frankfurt am Main, Germany. Permanent Representative (Ständiger Vertreter) of the Branch Niederlassung: Mr. Jeffery H. Perkins.

BUILDING PRODUCTS & MATERIALSINDUSTRY UPDATE │ APRIL 2015

PAGE |

BUILDING PRODUCTS AND MATERIALS GROUP OVERVIEW

CONTENTS WHAT WE’RE READING ECONOMIC UPDATE M&A MARKET TRENDS PUBLIC MARKETS PUBLIC COMPARABLES M&A ACTIVITY

CONTACTSMike HoganManaging [email protected]+1 (804) 915-0104

Ryan NelsonManaging [email protected]+1 (804) 915-0121

Trey PackardVice [email protected]+1 (804) 887-6016

INTRODUCTION

Harris Williams & Co. is pleased to present our Building Products & Materials IndustryUpdate for April 2015. This report provides commentary and analysis on currentcapital market trends and merger and acquisition dynamics within the globalbuilding products and materials industry.

We hope you find this edition helpful and encourage you to contact us directly ifyou would like to discuss our perspective on current industry trends and M&Aopportunities or our relevant industry experience.

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

OUR PRACTICE

Harris Williams & Co. is a leading advisor to the building products and materialsindustry. Our significant experience covers a broad range of end markets,industries, and business models.

Construction Materials

Building Products

Distribution & Services

has been acquired by

a portfolio company of

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a subsidiary of

has been acquired by

Select Atlanta, Georgia

aggregates assets of LaFarge

SA have been acquired byhas been acquired by

a division of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

Aggregates Asphalt Aluminum Bricks Clay Glass Precast Concrete / Ready Mix Steel Stone

Acoustical Cabinets & Countertops Carpet and Flooring Gypsum / Wallboard Electrical Fixtures HVAC Lumber Plumbing Fixtures

Roofing Siding Tools and Hardware Windows & Doors

Architectural and Engineering Installation and Contracting Lumber and Hardware Plumbing Roofing and Siding Site Development Wallboard

Construction Materials Building Products Distribution &

Services

has been acquired by

a portfolio company of

has been acquired by

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

a division of

a portfolio company of

has been acquired by

a subsidiary of

has been acquired by

www.harriswilliams.de

1

PAGE |

WHAT WE’RE READING

SAWLOG PRICES DECLINED IN MANY COUNTRIES IN 2014

BFS ANTES $1.63 BILLION FOR PROBUILD TO FORM DISTRIBUTION GIANT

AMERICA, HERE IS THE FUTURE OF YOUR HOUSING MARKET

HOLCIM-LAFARGE MERGER IS ON AGAIN

Forrest Industry Network 4/7/2015Sawlog prices declined in many countries during 2014 and the GSPI price index in the 4Q/14 was at the lowest level intwo years, reports the Wood Resource Quarterly. For the third consecutive quarter, the GSPI price index fell inthe 4Q/2014 to the lowest level in two years, reports the Wood Resource Quarterly. The biggest price declines the pastyear have occurred in Europe, Latin America and Oceania, while prices in North America have remained stablethanks to healthy domestic demand for lumber.

Read the full article here.

Builder Online 4/13/2015PROSALES chief editor Craig Webb has an early take on the Builders FirstSource (BFS) announcement that it willacquire ProBuild in an all-cash deal worth $1.63 billion. The acquisition creates America's biggest pro-oriented buildingmaterial supplier, a $6.1 billion giant with operations from Florida to Alaska. Just as home building companies areconsolidating to capture scale and market diversification opportunities during the early innings of recovery, thedistribution channel is now streamlining itself to simplify the flow of building materials, products, and supplies to jobsites.

Read the full article here.

Business Insider 4/13/2015Homebuilding activity is coming back to life. On Monday, as the spring selling season kicks in, RBC Capital Marketsupgraded its forecasts for housing starts through 2017. In a note to clients, RBC's Robert Wetenhall wrote: "We areraising our forecast for housing starts in 2015, 2016 and 2017 to 1.1 MM (+10%), 1.2 MM (+9%) and 1.25 MM (+4%) ... Thisis an obvious positive for the spring selling season and leads us to believe that our preferred names (DR Horton, LennarCorporation, and PulteGroup) among the public builders can potentially meet or beat consensus estimates driven bystrong demand and solid ASP growth."

Read the full article here.

Concrete Construction 3/23/2015A proposed $44.27 billion merger between Switzerland-based Holcim Ltd. and France's Lafarge SA, is moving forwardagain, after the two companies came to an agreement over some changes in the original terms over the stockholdershare exchange ratio and exactly who will lead the combined operation. According to the press release, Both partiesagreed on a new exchange ratio of 9 Holcim shares for 10 Lafarge shares. A new Chief Executive Officer for thecombined group, to be proposed by the Lafarge Board and accepted by the Holcim Board, will be appointed asfrom the closing of the transaction.

Read the full article here.

INDUSTRY UPDATE │ APRIL 2015

SAND DEMAND SLIPS

Aggregates Research 4/13/2015US sand mines, including 63 in Wisconsin and six in Minnesota, are projected to ship significantly less sand to oil drillersin 2015, compared with last year, when companies like Fairmount Santrol, US Silica and Superior Silica Sands setproduction records, industry sources say. "This whole ripple effect has taken hold and it is going to continue," saidRichard Shearer, CEO of Superior Silica Sands, a Texas-based company that operates sand mines in Wisconsin. "Thereare peak cycles and trough cycles, and we have hit a trough."

Read the full article here.

BUILDING PRODUCTS AND MATERIALS

2

PAGE |

94

96

98

100

102

104

106

108

110

(1.0%)

(0.5%)

0.0%

0.5%

1.0%

1.5%

2.0%

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

ECONOMIC UPDATE

INDUSTRIAL PRODUCTION INDEX

BUILDING PRODUCTS AND MATERIALS

GDP

Real GDP increased by 0.5% in the fourthquarter of 2014, and overall GDPincreased 2.4% in 2014, compared to anincrease of 2.2% for 2013

The increase in 2014 reflected positivecontributions from PCE, nonresidentialfixed investment, exports, state and localgovernment spending, private inventoryinvestment, and residential fixedinvestment

Current dollar GDP increased 3.9%, or$650.8 billion, in 2014, compared to anincrease of 3.7%, or $604.9 billion in 2013

The U.S. economy seems to be slowingtowards a medium-term trend, however, astrong dollar, jobs, wages and sentimentare expected to drive consumer spending

Industrial production increased 0.1% inFebruary after decreasing .3% in January

Manufacturing output fell for the thirdstraight month and decreased 0.2% inFebruary, while the mining index fell 2.5%

Utilities output jumped 7.3% due to thedemand for heating caused by especiallycold temperatures around the country

Capacity Utilization for the industrial sectordecreased to 78.9% in February, nearly 1.2%below its long-run (1972-2014) average

Manufacturing production is forecast togrow 3.5% in 2015, due to job gains andinvestments in natural gas infrastructure, thehousing supply chain, transportationinfrastructure, factory automation, medicalcare expansion, and increasing confidence

Seasonally AdjustedSources: Bureau of Economic Analysis

Seasonally AdjustedSources: Board of Governors of the Federal Reserve System

(Change in billions of dollars)

(Indexed to 2007)

INDUSTRY UPDATE │ APRIL 2015

3

PAGE |

ECONOMIC UPDATE

PERSONAL CONSUMPTION EXPENDITURES

ECONOMIC SENTIMENT

In February, personal income increased$58.6 billion, or 0.4%, while personalconsumption expenditures (PCE)increased $11.8 billion, or 0.1%

PCE, personal interest payments, andpersonal current transfer paymentsincreased $14.2 billion in February, instark contrast to a decrease of $25.4billion in January

Proprietors’ income decreased $7.0billion in February, compared to adecrease of $11.7 billion in January afterthe holiday shopping season

The economic sentiment index measureshow consumers view prospects for theirown financial situation, how they view thenear-term general economy prospects,and their long-term view of economicprospects

The Leading Economic Index (LEI) for theU.S. improved again in February, drivenmostly by positive contributions frombuilding permits and financial components

For the six months ending February 2015,the leading economic index increased2.4% (approximately a 5% annual rate),slower than the growth of 3.7% during theprevious six months

The largest positive contributors forFebruary were the interest rate spread,stock prices, building permits, the LeadingCredit Index, consumer businessexpectations, and manufacturers’ neworders for consumer goods

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Indexed to 2010Sources: The Conference Board

(percentage change in 6-month rolling average)

(indexed to 2010)

Sources: The Federal Reserve Bank of St. Louis

0.00%

0.10%

0.20%

0.30%

0.40%

0.50%

0.60%

Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13 Jul-13 Jan-14 Jul-14 Jan-15

100

107

114

121

128

Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14

4

PAGE |

ECONOMIC UPDATE

CONSUMER CONFIDENCE INDEX (CCI)

KEY INTEREST RATES

The Consumer Confidence Indeximproved to 101.3 in March, up from 98.8in February

The increase was driven by an improvedshort-term outlook for both incomeprospects and employment, althoughconsumers were less enthusiastic aboutbusiness conditions

Consumer confidence is currently 8.81%higher than the year-end 2014 rate, and30.71% higher than the year-end 2013rate

The 30-year mortgage rate declined inMarch 2015 to 3.77%, the lowest ratesince May 2013

The current mortgage rate is 57 basispoints lower than the rate in March 2014

It is still unclear when the Fed plans toraise rates, but it is expected sometimelater this year through practices the Fedrefers to as “policy normalization”

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

0

20

40

60

80

100

120

Indexed to 1985Sources: The Conference Board

Seasonally AdjustedSources: Federal Reserve Bank of St. Louis

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

30-Yr Mortgage Rates 10-Yr Treasury Effective Federal Funds Rate

5

PAGE |

ECONOMIC UPDATE

U.S. NON-RESIDENTIAL CONSTRUCTION

U.S. HOUSING STARTS U.S. housing starts in February were at a

seasonally adjusted annual rate of897,000, 17% below the January estimateof 1,081,000, and 3% below the estimatefor February 2014

This decrease in housing starts wasattributable to major drop-offs in multi-family homes, as well as single-familyhomes, which accounts forapproximately two-thirds of the market

February’s drop in housing starts was thelargest decline since 2011, and primarilydue to plunging temperatures andsnowstorms across the country

Housing starts continue to rebound fromunprecedented lows reached in 2009,yet remain ~30% below the 50-yearaverage of 1.5 million starts per year andare still below the average cyclical low of1.0 million

Single family homes are ~37% below thehistorical average of 1.0 million, whilemulti-family starts are just 16% below theirlong-term average of 418,000

New residential construction is projectedto grow at a 22% CAGR from 2014 to 2018

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Sources: Census Bureau; projections are derived from census of 11 reputable sources

0

500

1,000

1,500

2,000

2,500

1960 1968 1976 1984 1992 2000 2008 2016PSingle Family Multi Family50-Year Average Average Recesion Low

(units in 000’s)2014 Housing Starts: ~30% below 50-year average

Feb. 2015 Total: 897M-o-M Δ: (17%)Y-o-Y Δ: (3%)

Non-residential construction has laggedin recovery compared to otherconstruction markets, and is stillsignificantly below historical peak levels

Non-residential construction decreasedfrom January to February by .1%, anddecreased by 1.9% from the same perioda year ago

Several sectors within non-residentialconstruction that continue to seespending increases includemanufacturing, amusement andrecreation, office, and sewage andwaste disposal

-12.0%

-8.0%

-4.0%

0.0%

4.0%

8.0%

12.0%

$450

$500

$550

$600

$650

$700

$750

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Non-Residential Construction Non-Residential Construction M-o-M Change

($ in billions)

Seasonally Adjusted Annual RateSources: U.S. Department of Commerce: Census Bureau

6

PAGE |

ECONOMIC UPDATE

REPAIR AND REMODELING SPEND

U.S. REMODELING MARKET INDEX

Repair and remodeling spend reachedover $155 billion in 2014, and continuesto experience significant growth ashomeowners invest in their homes

Repair and remodeling spend is lesscyclical than new construction andprovides stability to the overall market

R&R spend dropped just 10% from 2007to 2009 as consumers chose to invest inrepairs and remodels in lieu of makingsubstantial investment in new homes

Growth for 2014 – 2018 is projected at aCAGR of 4.4%

In the fourth quarter of 2014, theRemodeling Market Index (RMI) posted arecord-high result of 60, the seventhconsecutive quarter for an RMI over 50.

An RMI over 50 indicate that remodelersare reporting higher activity than theprevious quarter. The overall RMIaverages the indicators of current andfuture remodeling activity.

All four subcomponents of the RMI futureindex, bids, commitments for threemonths, job backlog, and appointmentsfor proposals saw increases over the priorperiod.

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Sources: McGraw Hill

40

45

50

55

60

65

Q12012

Q32012

Q12013

Q32013

Q12014

Q32014

Index values greater than 50 indicate activity higher than

the previous quarter

Sources: National Association of Home Builders

$0

$50

$100

$150

$200

2002 2004 2006 2008 2010 2012 2014 2016P 2018P

($ in billions)

2014 – 2018 CAGR: 4.4%

7

PAGE |

0

10

20

30

40

50

60

70

Q12010

Q22010

Q32010

Q42010

Q12011

Q22011

Q32011

Q42011

Q12012

Q22012

Q32012

Q42012

Q12013

Q22013

Q32013

Q42013

Q12014

Q22014

Q32014

Q42014

Q12015

Num

ber

of A

nno

unce

d M

&A

Dea

lsM&A MARKET TRENDS

MARKET OBSERVATIONS

BUILDING PRODUCTS QUARTERLY M&A ACTIVITY

Global M&A deal volume in 2014 was $3.5 trillion, a 47% increase from 2013 levels and the strongest annualperiod since 2007

− Deal volume in the Americas increased 51% over 2013 totals, accruing $2.1 trillion in activity from 15,734announced deals

− European M&A activity increased 55% over 2013 levels, and Asia Pacific M&A accounted for the strongestannual period in the region since 1908

North American building products deal activity in 2014 increased by approximately 20% from the prior year

Credit conditions remain issuer-friendly, and leveraged loan multiples remain robust, with average debt multiplesapproximately 4.8x EBITDA for issuers through February 2015

Large corporations continue to drive M&A activity with bloated cash balances, soaring stock prices, andrelatively inexpensive credit

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Note: Includes all building products, construction materials, or forest products, for M&A transactions announced in the U.S. or CanadaSource: Capital IQ, S&P Leveraged Commentary & Data, Thomson Reuters, Bloomberg, Markit Economics, Investment News.

Total Transactions: 176YOY Change: 35.4%

Total Transactions: 202YOY Change: 14.8%

Total Transactions: 191YOY Change: (5.4%)

Total Transactions: 156YOY Change: (18.3%)

Total Transactions: 187YOY Change: 19.9%

8

PAGE |

SELECT SECTOR OVERVIEWS & TRENDS

AGGREGATES

ASPHALT

CEMENT AND CONCRETE

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Description

Broad category of materials such as crushed rock, manufactured sand,natural sand, and gravel

Most-used material in the world, after water

Industry Commentary:

Markets are local in nature due to high shipping costs

Major players include Lafarge, Cemex, CRH, Heidelberg Cement, MartinMarietta, Vulcan Materials and a large number of independent operators

Demand derived from total construction spending, which is based onglobal, national, regional and local economic conditions. 25 billion tons ofaggregates are used per year globally, roughly four tons per person

U.S. Aggregates Consumption (values in millions of metric tons)

Description

Paving and roofing materials include asphalt and tar-paving mixtures andblocks, shingles, roofing cements, and coatings

Industry Commentary:

Asphalt is used over 85% of the time in U.S. highway and road construction

MAP 21 regulations extend and fund federal highway programs, includingover $120 billion for infrastructure programs

Industry planning for the next highway bill is underway and will developfurther in 2015

Simultaneously, resurgent U.S. housing activity supports asphalt shingle androofing cement demand

U.S. Refinery Net Production of Asphalt and Road Oil

(thousands of barrels)

Description

Portland, natural, masonry, pozzolanic and other hydraulic cements.

Typically, manufacturers also thermally treat and mine or quarry lime.

Industry Commentary:

U.S. cement consumption has historically exceeded domestic productioncapacity.

Concrete has been gaining share over asphalt since 2008.

U.S. cement capacity and import terminals are largely owned orcontrolled by international producers.

Significant barriers to entry exist for new cement capacity.

Transportation costs lead to regional markets.

U.S. Cement Consumption Outlook (millions of metric tons)

Source: U.S. Geological Survey

Source: U.S. Energy Information Administration

Source: PCA, Eagle Materials, and IBIS

1,450 1,160 1,160 1,160 1,170 1,190

1,060

838 805 810 839 847

0

500

1,000

1,500

2,000

2,500

3,000

2008 2009 2010 2011 2012 2013

Stone Sand/Gravel

4,000

8,000

12,000

16,000

20,000

0

20

40

60

80

100

120

2007 2009 2011 2013 2015P

Government Residential Non-residential

9

PAGE |

SELECT SECTOR OVERVIEWS & TRENDS

LUMBER AND WOOD PRODUCTS

ROOFING

WINDOWS AND DOORS

Description

Lumber, boards, beams, bolts oriented strand board, poles, shingles, siding,and wood chips

Industry Commentary:

70% of U.S. lumber demand is driven by housing, including new constructionand remodeling

This year’s first-quarter lumber price slide was significant, Random LengthsFraming Lumber Composite Price lost $47 due to poor weather and slowerthan expected start to 2015

Dealers’ three-month sales expectations surged with warmer and drierweather, Random Length surveys matched or exceeded record high levels

Framing Lumber Composite Price Index

($ per thousand board feet)

Source: Random Lengths

Description

Roofing market includes bituminous, wood, and tile roofing used in residentialapplications and metal elastomeric, and plastic roofing used in non-residential applications

Industry Commentary:

Demand for roofing is closely linked to building construction expenditures, buthas been more sheltered than other building products markets from thehousing slump due to the nondiscretionary need for roof repair andreplacement

Houses need to be re-roofed every fifteen years on average and the agingU.S. housing stock will drive continued demand for replacement

Additionally, renewed strength in new housing construction and a generallystronger economic climate will support growth

Source: Freedonia

Roofing Demand by Primary Segment

Description

Windows and doors market includes metal, wood, and plastic windows anddoors for residential and non-residential markets

Industry Commentary:

Window and door demand is primarily driven by new commercial andresidential construction as well as repair and remodel spending

Annual home improvement spending is expected to decelerate from 6.3% inthe first quarter of 2015 to 1.6% by the third quarter due in part to amoderating house price gains

As first-time buyers begin to return to the market home improvement andhousing starts should make a strong push back towards long-term levels

Leading Indicator of Remolding Activity ($ in billions)

Source: The Joint Center for Housing Studies of Harvard University

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

$100$150$200$250$300$350$400$450$500

Residential Reroofing

49.4%

Nonresidential Reroofing

34.5%

New Residential9.1%

New Nonresidential

7.0%

$80

$90

$100

$110

$120

$130

$140

$150

Q1'11 Q1'12 Q1'13 Q1'14 Q1'15E

10

PAGE |

SELECT SECTOR OVERVIEWS & TRENDS

WALLBOARD AND PLASTER

HVAC

PLUMBING FIXTURES AND FITTINGS

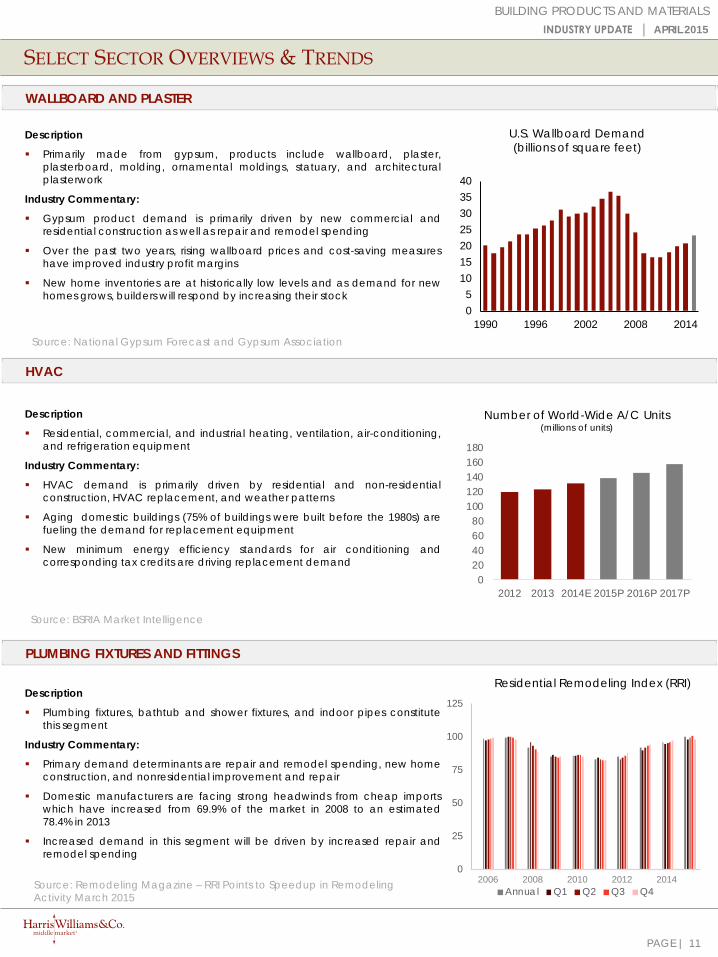

Description

Primarily made from gypsum, products include wallboard, plaster,plasterboard, molding, ornamental moldings, statuary, and architecturalplasterwork

Industry Commentary:

Gypsum product demand is primarily driven by new commercial andresidential construction as well as repair and remodel spending

Over the past two years, rising wallboard prices and cost-saving measureshave improved industry profit margins

New home inventories are at historically low levels and as demand for newhomes grows, builders will respond by increasing their stock

U.S. Wallboard Demand(billions of square feet)

Source: National Gypsum Forecast and Gypsum Association

Description

Residential, commercial, and industrial heating, ventilation, air-conditioning,and refrigeration equipment

Industry Commentary:

HVAC demand is primarily driven by residential and non-residentialconstruction, HVAC replacement, and weather patterns

Aging domestic buildings (75% of buildings were built before the 1980s) arefueling the demand for replacement equipment

New minimum energy efficiency standards for air conditioning andcorresponding tax credits are driving replacement demand

Number of World-Wide A/C Units(millions of units)

Source: BSRIA Market Intelligence

Description

Plumbing fixtures, bathtub and shower fixtures, and indoor pipes constitutethis segment

Industry Commentary:

Primary demand determinants are repair and remodel spending, new homeconstruction, and nonresidential improvement and repair

Domestic manufacturers are facing strong headwinds from cheap importswhich have increased from 69.9% of the market in 2008 to an estimated78.4% in 2013

Increased demand in this segment will be driven by increased repair andremodel spending

Residential Remodeling Index (RRI)

Source: Remodeling Magazine – RRI Points to Speedup in Remodeling Activity March 2015

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

020406080

100120140160180

2012 2013 2014E 2015P 2016P 2017P

0

25

50

75

100

125

Annual Q1 Q2 Q3 Q42006 2008 2010 2012 2014

05

10152025303540

1990 1996 2002 2008 2014

11

PAGE |

(60%)

(40%)

(20%)

0%

20%

40%

60%

80%

100%

120%

140%

Apr-10 Oct-10 Apr-11 Oct-11 Apr-12 Oct-12 Apr-13 Oct-13 Apr-14 Oct-14 Apr-15

Building Materials Index Building Products Index Building Products Distributors Index S&P 500 Index

PUBLIC MARKETS

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

12

MEDIAN TEV / 2015 EBITDA

MEDIAN REVENUE GROWTH (2014 – 2015P)

MEDIAN EBITDA MARGIN (2013 – 2015P) MEDIAN EBITDA GROWTH (2014E-2015P)

MEDIAN CAPEX / REVENUE (2015E)

MEDIAN REVENUE GROWTH (2011 – 2014)

HISTORICAL STOCK PRICES (MARCH 16TH, 2010 - MARCH 16TH, 2015)

11.0x

10.5x

10.2x

Building Products Distributors

Building Products

Building Materials

8.5%

8.7%

7.3%

Building Products Distributors

Building Products

Building Materials

5.4%

6.4%

5.7%

Building Products Distributors

Building Products

Building Materials

4.3%

12.8%

16.7%

Building Products Distributors

Building Products

Building Materials

10.2%

16.7%

12.0%

Building Products Distributors

Building Products

Building Materials

0.9%

2.9%

6.3%

Building Products Distributors

Building Products

Building Materials

PAGE |

As of April 14, 2015 ($ in Millions, except per share amounts)

PUBLIC COMPARABLES

BUILDING MATERIALS

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Stock PerformanceCurrent % of 2014 TEV / EBITDA

Price LTM High Mkt Cap TEV Revenue EBITDA Margin 2015 2016

Aggregates and CementHolcim Ltd. $76.37 90.1% $24,885 $37,469 $19,238 $3,755 19.5% 9.3x 8.3xCRH plc $26.35 96.6% 21,507 24,316 22,892 1,972 8.6% 10.9x 9.2xLafarge S.A. $66.86 92.7% 19,242 31,224 15,546 3,139 20.2% 9.7x 8.6xHeidelbergCement AG $80.48 99.1% 15,124 23,705 15,281 2,472 16.2% 8.7x 8.0xCEMEX, S.A.B. de C.V. $0.98 83.9% 12,258 28,766 14,228 2,482 17.4% 9.7x 8.4xVulcan Materials Company $83.33 96.6% 10,979 12,844 2,994 575 19.2% 15.6x 12.3xMartin Marietta Materials Inc. $138.11 94.5% 9,207 10,686 2,679 588 22.0% 12.3x 10.4xEagle Materials Inc. $85.05 80.5% 4,235 4,739 1,032 284 27.5% 10.4x 8.5xSummit Materials, Inc. $21.06 94.3% 490 1,761 1,204 173 14.4% 9.0x 7.5x

Median 94.3% 19.2% 9.7x 8.5x

Mean 92.0% 18.3% 10.6x 9.0x

Heavy Construction MaterialsCRH plc $26.35 96.6% $21,507 $24,316 $22,892 $1,972 8.6% 10.9x 9.2xJames Hardie Industries plc $12.12 99.5% 5,401 5,710 1,622 348 21.5% 13.9x 11.5xBoral Limited $5.06 98.9% 3,960 4,641 3,643 335 9.2% 10.2x 9.1xHeadwaters Incorporated $18.66 100.0% 1,353 1,814 825 134 16.2% 11.0x 9.8xU.S. Concrete, Inc. $33.41 93.5% 472 663 704 70 9.9% 7.6x 6.3x

Median 98.9% 20.0% 10.9x 7.7x

Mean 97.7% 13.1% 10.7x 9.2x

Lumber and Wood ProductsWeyerhaeuser Co. $32.21 87.0% $16,682 $20,518 7,693 $1,722 22.4% 11.3x 10.1xWest Fraser Timber Co. Ltd. $48.75 78.1% 4,055 4,402 3,330 497 14.9% 7.4x 5.9xCanfor Corp. $19.26 75.9% 2,584 2,893 2,891 442 15.3% 6.1x 4.6xLouisiana-Pacific Corp. $16.14 90.9% 2,289 2,518 1,935 16 0.8% 22.8x 8.7xBoise Cascade Company $37.15 84.6% 1,471 1,609 3,574 196 5.5% 7.4x 6.3xNorbord, Inc. $19.94 83.2% 1,079 1,455 1,198 89 7.4% 10.6x 4.3xUniversal Forest Products Inc. $53.13 94.5% 1,061 1,160 2,660 130 4.9% 7.5x 6.9x

Median 84.6% 7.4% 7.5x 6.3x

Mean 84.9% 14.7% 8.6x 6.7x

Overall Median 93.5% 15.3% 10.2x 8.5x

Overall Mean 91.0% 14.4% 10.6x 8.3x

13

PAGE |

PUBLIC COMPARABLES

BUILDING PRODUCTS

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Stock PerformanceCurrent % of 2014 TEV / EBITDA

Price LTM High Mkt Cap TEV Revenue EBITDA Margin 2015 2016

ASSA ABLOY AB $62.38 99.9% $23,095 $25,277 $7,265 $1,312 18.1% 17.8x 16.5xMohawk Industries Inc. $183.86 97.6% 13,438 15,599 7,803 1,161 14.9% 11.4x 10.1xMasco Corporation $26.57 97.0% 9,262 11,201 8,521 1,003 11.8% 10.0x 9.2xFortune Brands Home & Security, Inc. $46.14 95.8% 7,346 7,828 4,014 498 12.4% 12.7x 10.8xLennox International, Inc. $111.20 98.4% 5,003 5,891 3,367 387 11.5% 12.9x 11.4xOwens Corning $42.83 97.5% 5,065 7,058 5,276 717 13.6% 9.2x 8.2xUSG Corporation $26.28 79.9% 3,821 5,707 3,724 454 12.2% 9.8x 8.3xKingspan Group plc $19.80 98.4% 3,486 3,656 2,289 229 10.0% 14.1x 12.3xArmstrong World Industries, Inc. $56.38 94.1% 3,108 3,977 2,515 313 12.5% 10.6x 9.3xMasonite International Corporation $69.69 99.7% 2,098 2,444 1,838 117 6.3% 13.3x 10.4xTrex Co. Inc. $54.20 93.9% 1,739 1,729 392 84 21.4% 16.4x 13.4xNortek Inc. $87.75 95.1% 1,427 2,715 2,546 242 9.5% 8.5x 7.9xInterface Inc. $20.89 97.7% 1,387 1,596 1,004 113 11.3% 11.2x 10.0xNCI Building Systems Inc. $16.71 77.1% 1,233 1,667 1,383 69 5.0% 12.0x 9.5xContinental Building Products, Inc. $22.87 96.6% 1,009 1,343 425 115 27.0% 9.6x 8.1xAmerican Woodmark Corp. $53.47 94.7% 850 710 807 57 7.0% 9.2x NATyman plc $4.61 92.1% 774 905 547 84 15.4% 9.7x 8.8xPly Gem Holdings, Inc $13.05 88.8% 886 1,846 1,567 119 7.6% 10.5x 7.9xQuanex Building Products Corporation $19.14 87.8% 643 580 597 45 7.5% 9.5x 7.9xPGT, Inc. $11.09 97.5% 529 680 306 44 14.2% 9.8x 8.0xNorcraft Companies, Inc. $25.73 98.9% 445 545 370 51 13.8% 8.8x 7.5x

Overall Median 96.6% 12.2% 10.5x 9.2x

Overall Mean 94.2% 12.5% 11.3x 9.8x

As of April 14, 2015 ($ in Millions, except per share amounts)

14

PAGE |

PUBLIC COMPARABLES

DISTRIBUTORS

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Stock PerformanceCurrent % of 2014 TEV / EBITDA

Price LTM High Mkt Cap TEV Revenue EBITDA Margin 2015 2016

Wolseley plc $60.11 96.8% $15,633 $17,476 $20,129 $1,377 6.8% 11.5x 10.3xBeacon Roofing Supply, Inc. $31.87 84.0% 1,577 1,803 2,371 126 5.3% 11.0x 9.3xRichelieu Hardware Ltd. $50.36 97.7% 986 981 567 67 11.9% 14.2x 13.0xBuilders FirstSource, Inc. $6.90 78.8% 678 1,044 1,604 61 3.8% 11.9x 9.0xStock Building Supply Holdings, Inc. $17.89 85.3% 468 560 1,296 32 2.5% 10.6x 7.6xHardwoods Distribution Inc. $10.37 93.1% 173 204 389 22 5.7% 8.5x 7.7xCanWel Building Materials Group Ltd. $4.66 89.5% 134 239 656 25 3.8% 9.8x 9.1xBluelinx Holdings Inc. $1.09 74.1% 97 526 1,979 23 1.2% NA NA

Overall Median 87.4% 4.5% 11.0x 9.1x

Overall Mean 87.4% 5.1% 11.1x 9.4x

As of April 14, 2015 ($ in Millions, except per share amounts)

15

PAGE |

M&A TRANSACTIONS

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Date Target Vertical Business Description Acquirer

4/7/2015 Northland Construction Supplies Ltd.

Distribtion Northland Construction Supplies Ltd. supplies goods to concrete construction, ceramic, and masonry industries.

National Concrete Accessories

4/2/2015 Ferrara Brothers Building Materials Corp.

Building Materials Ferrara Brothers Building Materials Corp. manufactures concrete. U.S. Concrete, Inc.

3/31/2015 Design Specialties, Inc. Building Products Design Specialties, Inc. manufactures glass fireplace doors. Blackthorne Partners LTD.

3/30/2015 Norcraft Companies, Inc. Building Products Norcraft Companies, Inc. manufactures kitchen and bathroom cabinetry in the United States and Canada.

Fortune Brands Home & Security, Inc.

3/30/2015 AFC Industries, Inc. Distribtion AFC Industries, Inc. engages in the purchase, distribution, assembly, and packaging of fasteners and related hardware products.

Incline Equity Partners; Incline Equity Partners I I I , L.P.

3/27/2015 PrimeSource Building Products, Inc.

Distribtion PrimeSource Building Products, Inc. distributes fasteners and building materials.

Platinum Equity, LLC

3/26/2015 Martin Fireproofing Corporation

Building Products Martin Fireproofing Corporation manufactures, sells, and installs specialty roof deck solutions.

Innovative Metals Company, Inc.

3/25/2015 Pinnacle Stone & Tile LLC Building Products Pinnacle Stone & Tile LLC manufactures and installs countertops, shower and bath surrounds, fireplaces, vanities, floor inlays, and custom projects in Northern California.

L.A.R.K. Industries, Inc.

3/25/2015 J & B Materials, Inc. Building Materials J & B Materials, Inc. is a supplier of drywall, metal studs, plaster, pool, and general building materials.

Gypsum Management and Supply, Inc.

3/19/2015 Pipeline Supply, Inc. Distribtion Pipeline Supply, Inc. operates as a wholesale distributor of plumbing, HVAC, hydronics, radiant floor heating, sewer, water, and well supplies.

Dakota Supply Group, Inc.

3/17/2015 Thermoseal Industries, LLC Building Materials Thermoseal Industries, LLC develops, produces, and sells insulating glass units to the commercial refrigeration, oven, test laboratory, and architectural markets.

Senneca Holdings

3/12/2015 Fry Reglet Corporation, Axiom & Serpentina Ceiling Systems

Building Products Axiom & Serpentina Ceiling Systems of Fry Reglet Corporation, a ceiling systems manufacturer, was acquired by Worthington Armstrong Venture.

Worthington Armstrong Venture

3/9/2015 Easi-Serv Products Inc. Building Products Easi-Serv Products Inc. designs and manufactures drive-thru windows, food conveyors, and glass patios.

Franke Foodserv ice Systems, Inc.

3/7/2015 Mechoshade Systems, Inc. Building Products Mechoshade Systems, Inc. prov ides manual, motorized, and automated solar-shading and room-darkening solutions.

Springs Window Fashions LLC

3/7/2015 Mechoshade Systems, Inc. Building Products Mechoshade Systems, Inc. prov ides manual, motorized, and automated solar-shading and room-darkening solutions.

Springs Window Fashions LLC

3/2/2015 Lampert Yards, Inc. Distribution Lamperts is a leading building material distributor prov iding windows, doors, roofing, siding, insulation, millwork, cabinets, and framing materials to professional builders and consumers in their local markets.

US LBM Holdings, LLC

3/2/2015 BMI Products of Northern California Inc.

Building Materials BMI Products of Northern California Inc. manufactures silo systems for construction needs.

Sika AG

2/26/2015 Zero International, Inc. Building Products Zero International, Inc. designs and manufactures a range of specialized sealing systems for doors and windows.

Schlage Lock Company LLC

2/26/2015 Atis Group Inc. Building Products Atis Group Inc. manufactures and distributes doors and windows and high performance energy-efficient products for the construction and home improvement markets.

Desjardins Business Capital régional et coopératif

2/25/2015 J. A. Jack & Sons, Inc. Building Materials J. A. Jack & Sons, Inc. mines and processes limestone. Harrison Gypsum, LLC

16

PAGE |

M&A TRANSACTIONS

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Date Target Vertical Business Description Acquirer

2/24/2015 Right Away Redy Mix, Inc. Building Materials Right Away Redy Mix, Inc. prov ides ready-mix, aggregate, and concrete pumping products and serv ices.

U.S. Concrete, Inc.

2/18/2015 Maryland Materials, Inc. Building Materials Maryland Materials, Inc. engages in mining and producing granite and traprock products.

Bluegrass Materials Company, LLC

1/29/2015 Preferred Sands of Canada, ULC, Assets of Hanson Lake Facility

Building Materials Preferred Proppants, LLC, Assets of Hanson Lake Facility comprises silica sand mining assets.

Hilco Industrial, LLC; Gordon Brothers Group, LLC, Investment Arm

1/29/2015 B&L Wholesale Supply Building Materials B&L Wholesale Supply is a Northeastern distributor of roofing and related residential and commercial building products, supplies, and serv ices

SRS Distribution

1/7/2015 Wameling Drywall Corp. Distribution Wameling Drywall Corp., doing business as Gilbert Supply Company, supplies building products.

American Builders & Contractors Supply Co., Inc.

12/29/2014 AGC Flat Glass North America, Inc.

Building Materials AGC Flat Glass North America, Inc. fabricates Commercial Glass in the United States.

Trulite Glass Company, LLC

12/23/2014 PFB Corp. Building Products PFB Corporation is engaged in manufacturing and marketing insulating building products primarily for the residential and commercial construction projects in North America.

Aeonian Capital Corporation

12/23/2014 Empire Truss Ltd. Building Products Empire Truss Ltd. manufactures custom design roof trusses and floor trusses, and distributes engineered wood products.

Builders FirstSource, Inc.

12/15/2014 Lumber Specialties, Ltd. Distribution Lumber Specialties, Ltd. manufactures and distributes structural building components for customers in the United States.

US LBM Holdings, LLC

12/15/2014 Distribution International, Inc.

Distribution Distribution International, Inc. distributes thermal and acoustical insulation and related supplies for maintenance and repair operations worldwide.

Advent International Corporation

12/11/2014 Diamond Concrete, Inc. Building Materials Diamond Concrete, Inc. manufactures and distributes concrete. U.S. Concrete, Inc.

12/9/2014 Standard Roofings, Inc. Distribution Standard Roofings, Inc., doing business as The Standard Group, distributes exterior building products to builders, contractors, architects, and homeowners.

American Builders & Contractors Supply Co., Inc.

12/8/2014 Scofield Construction Serv ices, LLC

Building Materials Scofield Construction Serv ices, LLC, through its subsidiaries, produces ready-mix concrete.

Redi-Mix, L.P.

12/8/2014 American Masons' & Building Supply Co.

Distribution American Masons' & Building Supply Co. supplies building materials in the Greater Hartford area.

US LBM Holdings, LLC

12/2/2014 HD Supply Distribution Serv ices, LLC

Distribution HD Supply Distribution Serv ices, LLC distributes select building products to national and regional hardware retailers, and the professional market in North America.

The Home Depot, Inc.

12/1/2014 Handcrafted Homes, LLC Building Products Handcrafted Homes, LLC produces modular homes in the United States. Innovative Building Systems LLC

11/25/2014 Wallboard Supply Company, Inc.

Distribution Wallboard Supply Company, Inc. distributes and installs building materials to commercial and residential construction industries in New England.

US LBM Holdings, LLC

11/19/2014 Atlas Homewares, Inc. Building Products Atlas Homewares, Inc. designs decorative hardware products. Top Knobs, Inc.

11/19/2014 Airxcel, Inc. Building Products Airxcel, Inc. designs and manufactures air conditioning, heating, ventilating, and related appliances.

Yukon Partners; One Rock Capital Partners, LLC

11/19/2014 Acanthus Industries Inc. Building Products Acanthus Industries Inc. designs and manufactures architectural wood products in Canada.

Art for Everyday, Inc.

17

PAGE |

M&A TRANSACTIONS

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Date Target Vertical Business Description Acquirer

11/19/2014 Acanthus Industries Inc. Building Products Acanthus Industries Inc. designs and manufactures architectural wood products in Canada.

Art for Everyday, Inc.

11/19/2014 Texas Tempered Glass, Inc. Building Materials Texas Tempered Glass, Inc. is a glass fabricator serv ing commercial and residential end markets in the United States and abroad.

Trulite Glass & Aluminum Solutions, LLC

11/18/2014 Architectural Elements LLC Building Products Architectural Elements LLC manufactures and distributes doors, windows, and hardware for residential and commercial construction in the United States.

FP2D, LLC

11/18/2014 Brooklyn Navy Yard Modular-Construction Facility

Building Products Brooklyn Navy Yard Modular-Construction Facility comprises a construction facility that constructs residential units.

Forest City Ratner Companies, LLC

11/14/2014 Alcoa Heating & Cooling Building Products Alcoa Heating & Cooling prov ides installation and serv ice support for HVAC systems, tankless gas water heaters, and home generators.

MK Russell & Abbott

11/13/2014 Peachtree Communities Group, Inc.

Building Products Peachtree Communities, Inc. builds homes/residences in Atlanta. Century Communities, Inc.

11/11/2014 Vicwest Inc Building Products Vicwest Inc. manufactures and distributes building construction products and steel containment products North America and internationally.

Kingspan Group plc

11/11/2014 Southern Fastening Systems, Inc.

Distribution Southern Fastening Systems, Inc. distributes tools and fasteners for wood construction projects and manufacturing operations.

Carlson Systems, LLC

11/10/2014 Industrial Noise Control, Inc.

Building Products Industrial Noise Control, Inc. manufactures and distributes industrial noise control products and systems for applications in industrial, commercial, architectural, and environmental markets.

United Process, Inc.

11/10/2014 CENTRIA Incorporated Building Materials CENTRIA Incorporated designs, develops, and manufactures engineered wall, roof, and floor systems, as well as prov ides coil coating serv ices.

Steelbuilding.com, Inc.; NCI Group, Inc.

11/8/2014 Trussbilt LLC Building Products Trussbilt LLC. designs and manufactures security products. Coastal Plain Ventures, LLC

11/7/2014 Henkens Equipment, Inc. Building Products Henkens Equipment, Inc. is engaged in the sale of agricultural and construction equipment.

Butler Ag Equipment

11/5/2014 Connor Sport Court International, Inc.

Building Products Connor Sport Court International, Inc. designs and builds sports surfacing and flooring products.

Gerflor USA, Inc.

11/4/2014 Hanson Structural Precast, Inc.

Building Materials Hanson Structural Precast, Inc. manufactures and supplies structural and architectural precast components.

Wells Concrete Products, Inc.

11/3/2014 Watertown Plumbing And Heating Supply Co., Inc.

Distribution Watertown Supply, a Div ision of F.W. Webb Company is a wholesale distributor specializing in piping, plumbing, and heating repair parts for commercial/industrial/institutional facilities maintenance.

F.W. Webb Company

10/31/2014 Damron Sand & Gravel, Inc.

Building Materials Damron Sand & Gravel, Inc. manufactures and supplies sand and gravel in Lubbock, Texas.

PB Materials Holdings, Inc.

10/27/2014 TMI, LLC Building Products TMI, LLC extrudes and manufactures flexible polyv inyl chloride (PVC) and energy control doors.

River Associates Investments, LLC

10/23/2014 Peterson Industries, Inc. Building Products Peterson Industries, Inc. manufactures and distributes tub enclosures, shower enclosures and doors, mirror closet doors, and sliding glass patio doors.

Aldora Aluminum and Glass Products Inc.

10/21/2014 Tarragon Homes LLC Building Products Tarragon Homes LLC prov ides homebuilding serv ices. AVEW Holdings Inc.

10/21/2014 New York Sand & Stone, LLC

Building Materials Distributor

New York Sand & Stone, LLC supplies construction materials in the New York City market.

Eastern Concrete Materials, Inc.

18

PAGE |

REPRESENTATIVE BUILDING PRODUCTS TRANSACTIONS

BUILDING PRODUCTS AND MATERIALS

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

a portfolio company ofhas been acquired by

a portfolio company of

has been acquired by

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

a division of

has been acquired by

has been acquired by

a division of

has been acquired by

has been acquired by

a portfolio company of

has been acquired by

a division of

a division of

has been acquired by

and a portfolio company of

has been acquired by

a portfolio company of

a subsidiary of

has been acquired by

A Private Investor Group

has completed a recapitalization

with

a portfolio company of

has been acquired by

a subsidiary of

has been acquired by

a portfolio company of

Select Atlanta, Georgia aggregates assets of LaFarge SA have been acquired

by

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company ofhas been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

have been acquired by

The Wichita, Kansas aggregates, concrete,

asphalt, and paving assets

of LaFarge SA

a division of

has been acquired by

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

a portfolio company of

has been acquired by

Strategic Industries, LLC

Private Investors

has been acquired by

a portfolio company of

has purchased certain assets of

INDUSTRY UPDATE │ APRIL 2015

19

Energy & Power

IndustrialsHealthcare & Life Sciences

Transportation & Logistics

Aerospace, Defense & Government

Services

Business Services

Building Products & Materials

Technology, Media & Telecom

Specialty Distribution

Consumer

PAGE |

HARRIS WILLIAMS & CO. OFFICE LOCATIONS

UNITED STATES EUROPE

BostonTwo International Place24th FloorBoston, Massachusetts 02110Phone: +1 (617) 482-7501Fax: +1 (617) 482-7503

Cleveland1900 East 9th Street20th FloorCleveland, Ohio 44114Phone: +1 (216) 689-2400Fax: +1 (216) 689-2401

Minneapolis222 South 9th StreetSuite 3350Minneapolis, Minnesota 55402Phone: +1 (612) 359-2700Fax: +1 (612) 359-2701

Philadelphia1600 Market Street21st FloorPhiladelphia, Pennsylvania 19103Phone: +1 (267) 675-5900Fax: +1 (267) 675-5901

Richmond (U.S. Headquarters)1001 Haxall Point9th FloorRichmond, Virginia 23219Phone: +1 (804) 648-0072Fax: +1 (804) 648-0073

San Francisco575 Market Street31st FloorSan Francisco, California 94105, USAPhone: +1 (415) 288-4260Fax: +1 (415) 288-4269

FrankfurtBockenheimer Landstrasse 33-3560325 FrankfurtGermanyPhone: +49 069 3650638 00Fax: +49 069 3650638 01

London63 Brook StreetLondon W1K 4HS, EnglandPhone: +44 (0) 20 7518 8900Fax: +44 (0) 20 7526 2187

NETWORK OFFICES

BeijingHong KongMumbai

New DelhiShanghai

Building Products & Materials

Harris Williams & Co. has a broad range of industry expertise, which creates powerful opportunities.Our clients benefit from our deep-sector experience, integrated industry intelligence andcollaboration across the firm, and our commitment to learning what makes them unique. For moreinformation, visit our website.

OUR FIRM

20

PAGE |

HARRIS WILLIAMS & CO.

BUILDING PRODUCTS AND MATERIALSINDUSTRY UPDATE │ APRIL 2015

Bureau of Economic Analysis

Capital IQ

Eurostat

Freedonia

Global Industry Analysts

IBIS

PNC Economic Outlook

S&P Leveraged Commentary & Data

The Wall Street Journal

Thomson Financial – SDC Database

Thomson Reuters

U.S. Census Bureau

DISCLOSURES

SOURCES

Harris Williams & Co. (www.harriswilliams.com and www.harriswilliams.de) is a preeminent middle market investment bank focused on the advisory needs of clients worldwide. The firm has deep industry knowledge, global transaction expertise, and an unwavering commitment to excellence. Harris Williams & Co. provides sell-side and acquisition advisory, restructuring advisory, board advisory, private placements, and capital markets advisory services.

Harris Williams & Co. Ltd is a private limited company incorporated under English law having its registered office at 5th Floor, 6 St. Andrew Street, London EC4A 3AE, UK, registered with the Registrar of Companies for England and Wales under company number 7078852. Directors: Mr. Christopher Williams, Mr. Ned Valentine, Mr. Paul Poggi and Mr. Thierry Monjauze, authorised and regulated by the Financial Conduct Authority.

Harris Williams & Co. Ltd Niederlassung Frankfurt (German branch) is registered in the Commercial Register (Handelsregister) of the Local Court (Amtsgericht) of Frankfurt am Main, Germany, under registration number HRB 96687, having its business address at Bockenheimer Landstrasse 33-35, 60325 Frankfurt am Main, Germany. Permanent Representative (Ständiger Vertreter) of the Branch Niederlassung: Mr. Jeffery H. Perkins.

The information and views contained in this report were prepared by Harris Williams & Co. (“Harris Williams”). It is not a research report, as such term is defined by applicable law and regulations, and is provided for informational purposes only. It is not to be construed as an offer to buy or sell or a solicitation of an offer to buy or sell any financial instruments or to participate in any particular trading strategy. The information contained herein is believed by Harris Williams to be reliable, but Harris Williams makes no representation as to the accuracy or completeness of such information. Harris Williams and/or its affiliates may be market makers or specialists in, act as advisers or lenders to, have positions in and effect transactions in securities of companies mentioned herein and also may provide, may have provided, or may seek to provide investment banking services for those companies. In addition, Harris Williams and/or its affiliates or their respective officers, directors and employees may hold long or short positions in the securities, options thereon or other related financial products of companies discussed herein. Opinions, estimates and projections in this report constitute Harris Williams’ judgment and are subject to change without notice. The financial instruments discussed in this report may not be suitable for all investors, and investors must make their own investment decisions using their own independent advisors as they believe necessary and based upon their specific financial situations and investment objectives. Also, past performance is not necessarily indicative of future results. No part of this material may be copied or duplicated in any form or by any means, or redistributed, without Harris Williams’ prior written consent.

Copyright© 2015 Harris Williams & Co., all rights reserved.

21