building partnerships - valley first · john robertson, chair of the board ... developer/builder |...

TRANSCRIPT

P e n t i c t o n K e r e m e o s P r i n c e t o n O l i v e r K e l o w n a V e r n o n P e a c h l a n d A r m s t r o n g L u m b y K a m l o o p s w w w . v a l l e y f i r s t . c o m2 0 0 3 a n n u a l r e p o r t

Building Partnerships

2 0 0 3 A n n u a l R e p o r t | 3

Colleen Lister, Vice Chair

Partner at Harvey, Lister & Webb Incorporated, Certified General

Accountants | Rotarian, primary work is organizing the annu-

al Rotary Wheels Car Show | Wife and mother of 1 son, grand-

mother of 6 | Enjoys travelling, working in her yard, taking

long walks, fine dining and reading.

John Robertson, Chair of the Board

Retired | Volunteer at local church |

Husband and father of 2, grandfather of 3 |

Enjoys working on do-it-yourself house proj-

ects, golfing and boating.

Adolf Illichmann

Founder of Illichmann’s Meats, Sausages &

Gourmet Foods Ltd. | First President of

Liedertafel Choir | Rotarian since 1980 |

Served for 7 years on the Advisory Committee

at OUC for Food Preparation | Husband and

father of 3, grandfather of 7 | Enjoys fishing,

travelling, reading and listening to music.

▼

▼

▼

Valley First Credit Union is owned by the members and shareholders it serves. The Credit

Union has a 9 member Board of Directors, elected to represent the membership of Valley First.

As individuals, Valley First’s directors come from all walks of life and bring experience from

many different facets of business and the community to their role which, collectively, allows

them to manage and operate the Credit Union in the best interests of the membership. At

Valley First we take pride in the fact that decisions are made locally, based on first-hand knowl-

edge of the B.C. Interior economy.

Board of Directors

w w w . v a l l e y f i r s t . c o m 2 0 0 3 a n n u a l r e p o r t

Ta b l e o f Co n t e n t s

3 Board of Directors

6 Executive Group

7 Chair’s Message

8 President & CEO’s Report

12 Partners with your Community

14 Commercial Lending

16 2003 Consolidated Financial Statements

27 Corporate Directory

wealthmanagement

insurance

banking

Larry Stevens

Notary Public – Stevens & Stevens | Church

volunteer | Rotarian | Princeton General

Hospital and Ridgewood Lodge Foundation

board member | Husband and father of 3,

grandfather of 4 | Enjoys fishing, golfing and

riding motorcycles.

Rick Willie

Business Education Department Head and Teacher at Penticton Secondary School teach-

ing Multimedia, Marketing and Entrepreneurship | Coach of High School Tennis Team |

Director for the South Okanagan Tennis Association | Past Tennis Commissioner for the

BC Secondary Schools Tennis Association (2000 - 2002) | Husband and father of 1 |

Enjoys reading, playing tennis and tinkering with carpentry and mechanics.

▼

▼

Kevin Campbell

Resource Management Consultant | Part-time farmer |

Director of Kindale Developmental Association | Husband

and father of 2 | Enjoys playing hockey and gardening.

▼

2 0 0 3 A n n u a l R e p o r t | 4

Lanny Martiniuk

Grape Grower | Winery Consultant | Partner in local

winery | Husband and father of 3 | Vintage British sports-

car enthusiast.

Liz Goodison

Retired | Volunteer at a second hand clothing store,

called the “Care Closet” | Widowed mother of 5,

grandmother of 6 - soon to be 7 | Enjoys gardening,

golfing, travelling, knitting and doing needlework.

President of Rikhi Development Corporation –

Developer/Builder | Self employed orchardist |

Volunteer at the Summerland Hindu Temple |

Public Member, Real Estate Council of BC | Husband

and father of 3 | Enjoys reading and travelling.

Ramesh Rikhi

▼

▼

▼

Board of Directors Continued

2 0 0 3 A n n u a l R e p o r t | 5

At Valley First our vision is to be the predominant finan-

cial institution in the region. This means providing the very

best products and services at competitive rates and first-class

service to our members and clients.

Building partnerships with our members and our communities is what

we’re all about. Our goal is to determine their needs and respond with the

products, services and support necessary to assist them in meeting their finan-

cial goals.

2 0 0 3 A n n u a l R e p o r t | 6

Harley Biddlecombe

(President & Chief Executive Officer)

Jackie Horton

(Vice President,Corporate Administration& Human Resources)

Ted Houston

(Vice President,Commercial Banking &Subsidiary Operations)

Robert Mowat

(Vice President,Systems, Finance & Chief Financial Officer)

Bob Lindsay

(Senior Vice President,Retail Banking)

2 0 0 3 A n n u a l R e p o r t | 7

Focusing on the corporate vision and the mandates set out in the credit union’s strategic plan,

the activities of 2003 resulted in another busy year for your board of directors.

Despite fierce competition in the region for financial services and the added environmental

challenges and economic impact our communities faced during the devastating fires in our

region over the summer, the credit union’s fiscal performance and the success of the business

strategies deployed by our committed staff all made for one of the most rewarding and mem-

orable years in your credit union’s history.

Valley First’s premier banking branch in Kamloops opened its doors in bright new premises in

January 2003 in the heart of downtown Kamloops. The branch has enjoyed tremendous suc-

cess since moving to the new location and with a strong and knowledgeable team leading

the way, we are pleased to report that our 14th branch has made significant strides in gar-

nering new business for the credit union both on the retail and commercial side of the port-

folio. Through the development of strong business and community partnerships over the

past year, the Valley First brand has become a household name in Kamloops.

For much of 2003, Valley First’s activities and concentration shifted away from the heavy

emphasis on branching and expansion of the previous decade to focus on developing,

enhancing and customizing our products and services to achieve and retain a greater share

of our members’ financial business. While a number of our branches already boast a relative-

ly high concentration of marketshare in their respective communities, opportunities to attract

new marketshare and build mutually profitable relationships in some of the larger markets

was a focal point for Valley First in the past year and will continue to be a fundamental part of

your credit union’s growth strategies.

Your board spent considerable time over the past year challenging and educating itself in the

area of corporate governance and best practices. With a strong desire for continuous learn-

ing, the board has, through ongoing educational sessions, increased its knowledge in many

key areas of the credit union’s business operations. This has served to deepen our under-

standing of the obstacles and challenges our staff face and enabled us to lead the credit

union through the competitive landscape of the past year.

As outlined in more detail in this report, our commitment to partnering with our communi-

ties remains a core part of our credit union’s values and our strategic plan. Over the past year,

Valley First Financial Group was proud to actively support over 100 non-profit organizations

and events throughout our trade area. Through corporate donations, sponsorships and other

partnership opportunities, we are committed to building, delivering and enhancing services

that meet the needs of our communities and the various community groups we serve. Our

staff continues to represent the credit union philosophy of “People Before Profits” through

their tireless volunteerism. Whether participating in Valley First sponsored activities or dedi-

cating their personal time to serve on community boards and participate in fundraising

efforts, the unwavering commitment of our staff never ceases to amaze and inspire this board.

The Okanagan wild fires this past summer challenged all of us to pull together as a commu-

nity and it was no more evident than during this trying time just how much our staff care.

Many were actively involved in emergency response services or volunteering at the various

community command centres and worked long hours lending their support to the thousands

of firefighters and other emergency personnel who came out to assist us.

As we reflect on a year not soon to be forgotten, I would be remiss if I did not recognize the

people that make this credit union so successful. I salute my fellow board members for their

input, leadership and direction. The growth and success we have achieved as an organization

is directly attributable to the motivation, inspiration and leadership of our senior manage-

ment group as well as the superior service provided to our members and clients by staff at all

levels of the organization. Last but not least, this report would not be complete without

thanking our shareholders and clients for your loyalty and patronage.

From all of us at Valley First Credit Union and Valley First

Insurance Services Ltd., it has been an honour to serve

you for another year.

On behalf of the Board

John Robertson, Chair

Chair’s Message

Valley FirstExecutive Group

2 0 0 3 A n n u a l R e p o r t | 8

It gives us great pride to report to the membership on the activities and growth of your credit union over the past year. As an organization, we are continually focusing on the future and

challenging ourselves to find ways to meet and exceed our members’ expectations. Focusing on our members’ needs is the common thread that ties all of our efforts together. The success

of the programs and services we have implemented over the past year, coupled with the testimonials that we receive on a regular basis from our members and clients, confirms that we are

hitting the mark in achieving and exceeding the high standards of service excellence we have set for ourselves.

A Record Year in Financial PerformanceWithout a doubt, 2003 will be remembered as one of the strongest financial performances for the credit union in many years. The year concluded

with total assets at $759.0 million, an increase of $83 million, (12%) over 2002. The branch system, on a consolidated basis, achieved record gains

in 2003 in both loans and deposits. Retail lending, buoyed by a good economy and expanded broker relationships, grew by $48.0 million an

increase of 11.9%, by far the best year in the company’s history. Commercial lending, broadening our base in the active Kelowna market, also expe-

rienced a banner year, recording growth of $52.4 million.

Strong growth was also evident in deposits where total deposits grew by $75.0 million (11.0%). The growth was particularly strong in new demand

deposits where the portfolio increased by $41.0 million, (17.0%), a reflection of improved products that were readily accepted by the membership.

With such intense competition in the financial marketplace, this kind of growth is unprecedented for Valley First.

Net income for the credit union for 2003 was $3.98 million, an increase of 23% over the previous year. This pushed retained earnings and con-

tributed surplus for the organization to over $21.0 million. The credit union continues to maintain a very strong capital position with a combina-

tion of equity shares, retained earnings and contributed surplus.

At the beginning of 2003, interest rates were expected to rise and continue to rise throughout 2004. In fact rates declined, which normally would

put pressure on the financial margin of the credit union and consequently reduce net income. Through the use of derivative products, including

interest rate exchange contracts and forward rate agreements, the financial margin of the credit union actually increased in a marketplace of

declining rates. The use of derivatives in a prudent and conservative fashion was a key component of the credit union’s financial success for 2003.

The credit union maintains a portfolio of high-grade securities in the form of government and corporate bonds denominated in both Canadian

and U.S. funds. The purpose of this is to provide enhanced yields to the credit union over short periods of time when the demand for loans slows.

When demand increases the credit union can use a combination of short-term borrowings and bond sales to fund the loan demand. During the

year because the market value of the bonds increased, the sale of these securities also resulted in one-time gains arising from premiums on sale.

Overhead expenses, including salaries, data processing, marketing and occupancy costs were all well controlled and within budgetary expecta-

tions.

These record setting accomplishments are a direct result of the commitment and dedication of our staff to the organization.

2 0 0 3 A n n u a l R e p o r t | 9

Wealth ManagementManagement of our members’ retirement funds and investments has become a heightened focus in

the credit union over the past year. Staffed with six professional planners and a number of in branch

representatives, your credit union is proud to offer the finest in wealth management services, dedi-

cated to your financial well-being.

Throughout 2003, focus has been on training and education so that our staff will be in a position to

continue to offer current, reliable and relevant financial advice. Twelve of our credit union staff are

currently enrolled in the Canadian Securities Course which will lead to Professional Financial Planner

or Certified Financial Planner status adding further value to the relationships with our members.

In 2003 we welcomed two new planners to the credit union: Graham Cope at our new Kamloops

branch and T. Scott Boyd looking after our members’ needs at the Armstrong, Vernon and Lumby

branches.

MemberCARE® was introduced in 2003. Backed by the large CUMIS group of companies,

MemberCARE® offers, through our planners, a comprehensive line of life, disability, critical illness and

other insurance products for the benefit of our members.

The popular radio program,“Dollars & Sense,” featuring our planners and other professionals, contin-

ued to be broadcast in the Kelowna and South Okanagan markets and was expanded, late in 2003,

to the Kamloops marketplace. The program offers intelligent investment advice in a professional,

friendly format.

ServiceCheck® In 2002, the credit union commit-

ted to the purchase and installation of a

system dedicated to the enhancement

and enrichment of member relation-

ships. Now entering Phase II of the

Customer Relationship Management

process, the credit union has introduced

a new member service, which has been

branded “ServiceCheck®”. ServiceCheck®

offers our members an opportunity to

review, with a professional service repre-

sentative, their existing banking arrange-

ments, fee and interest structure and

their current and future banking needs.

Often this leads to a reduction in fee and

interest charges and an increase in inter-

est income. It is a commitment of this

credit union to continue to offer products

and services through an extensive

branch network staffed with knowledge-

able, helpful, professional and friendly

staff. We encourage all of our members

to ask about ServiceCheck® when they

next visit one of our branches.

Banking System ConversionIn 2003 we successfully converted Valley First’s Armstrong and Lumby

branches to the VisionWest banking system, allowing our members to

access multi branch banking in those branches. This significant under-

taking was the last phase of the integration of the two former

Armstrong Spallumcheen Savings and Credit Union branches into the

Valley First branch network.

Member Satisfaction SurveyThe credit union, through the research firm, Corporate Insights, conducted a com-

prehensive member satisfaction survey in May 2003. Your input confirmed our

position as one of the finest providers of financial services in British Columbia

naming Valley First “Best in Class” in six important member service categories.

However, we will not rest on our laurels. Our commitment to you is clear and

strong – we will provide the finest in financial services and products tailored to

your needs and continue to measure our performance by asking you on a regu-

larly scheduled basis.

Retail Banking ServicesAt the end of the year, our members noticed a change in their bank statements

as the credit union shifted to new technology and a more efficient way in deliv-

ering your account statements. Cheque Imaging has eliminated the costly and

time consuming process of filing and storing your numerous cancelled cheques

by providing a clean and simple “picture” of each of your cheques along with

your monthly statement. This is part of our continuing effort to make your bank-

ing easier.

Competition for financial services remains extremely competitive. At Valley First

our goal is to provide a broad range of products and services that meet the spe-

cific needs of our members and clients. Being locally owned and operated, we

take pride in the fact that we can be proactive and responsive to the local mar-

ket and we enjoyed great success in building new marketshare and attracting

new members during 2003 as a result of some aggressive and unique retail

banking product offerings.

President & CEO’s Report

2 0 0 3 A n n u a l R e p o r t | 1 0 2 0 0 3 A n n u a l R e p o r t | 1 1

Looking Ahead to 2004As an organization, we look forward to the year ahead with renewed energy and excitement. The financial services industry continues to change

rapidly and competition in our region is expected to increase. Business strategies in 2004 will address structure and the methodology we adopt

to drive business development and achieve and retain a greater share of our members’ financial business.

Growth and expansion in both retail and commercial banking activities will be key to the credit union’s successful business strategies.

The credit union’s activities will focus on the delivery of competitive products and services and personalized service aimed at building and sus-

taining mutually beneficial relationships with our members and clients.

We are pleased to report that a number of Valley First’s branches will undergo significant structural upgrades during 2004 to enhance service to

our membership. The Oliver branch, originally opened in 1984, will undergo a substantial renovation starting in April, to address growth require-

ments.

The Peachtree Mall branch in Penticton will be relocated to a freestanding building as part of the revitalization project of the Peachtree

Shopping Centre during 2004. The new location will be in the general vicinity of the branch’s current location but will be situated closer to Skaha

Lake Road. Services will be expanded to include general insurance, wealth management and a drive-through automatic teller machine to com-

plement existing services. The revitalization of the shopping centre is expected to substantially enhance retail business activity in the area.

Organizational growth and continued demands on our Head Office administration group has resulted in the need to develop a longer-term

growth strategy for physical premises. In the latter part of 2003,Valley First acquired the building lot next to its Head Office building in Penticton

and plans will begin during 2004 to address a two-year phased construction and expansion plan to meet current and future operational require-

ments.

During 2003, the credit union also secured a lease to erect its fourth branch in Kelowna at the corner of Kane Road and Glenmore Road.

Construction will commence in the Spring with a planned grand opening in the Fall 2004. This is a prime location for Valley First and presents a

significant opportunity to deliver credit union services in an area of Kelowna historically underserved by credit unions.

These plans, coupled with our ongoing service commitments, will make for another busy and excit-

ing year ahead. While ongoing changes in our industry together with heavy competition in our

region will no doubt present new challenges for Valley First Financial Group, we remain committed

to our vision to be the predominant financial institution in our region and more importantly, your

financial services provider of choice.

Harley Biddlecombe

President & Chief Executive Officer

Human ResourcesAttraction and retention of the best employees is paramount to Valley First’s growth and success strategies for the future. Valley First

members tell us time and time again and the 2003 member survey brought this point home, that it’s our staff and the superior service

they deliver that makes Valley First their preferred financial service provider.

Staff complement was increased in a number of key areas during 2003 to support the ongoing delivery of professional services and to

meet consumer demands. This resulted in a very active year for the Human Resources Department in terms of recruitment and employ-

ee development.

Training was delivered in many important areas related to business development and sales and service throughout 2003 to increase

staff knowledge and support our focus on identifying members’needs and developing stronger financial relationships with them. With

the heightened attention on terrorism, fraud, privacy and security in today’s business sectors, sound and prudent business practices

demand that we provide our staff with timely and comprehensive training in these areas to ensure that we do all we can do to protect

your privacy and the security of your financial business and information. This has and will continue to be an ongoing part of our train-

ing curriculum at Valley First.

Succession planning was another area that received a lot of management attention over the past year and remains top of mind when

recruitment opportunities arise. We face the same challenges as other organizations where many of our senior personnel will be retir-

ing over the next 1-5 years. We must ensure we have identified successors within the organization trained and ready to assume these

roles when the time comes.

During 2003, the credit union said a fond farewell to Al Ackland, Vice President of Credit, as he retired after 13 years with Valley First.

Mr. Ackland’s dedication to Valley First and his prudent management and adjudication of our credit portfolio has been an integral part

of the credit union’s ability to effectively manage risk. Following our succession plans and with Mr. Ackland’s retirement, Ted Houston

was appointed Vice President, Commercial Banking and Subsidiary Operations and will now oversee the credit union’s commercial

credit activities as well as continuing to oversee the activities of our wholly owned insurance subsidiary, Valley First Insurance

Services Ltd.

Underpinning all of our human resource initiatives is our commitment to attract, develop and retain quality employees by providing a

good working environment and opportunities for growth and continuous learning within the organization.

Just as we need the continual feedback from our membership to gauge our success, we also depend on direct input from staff to

ensure ongoing satisfaction with Valley First as their employer. During 2003, a comprehensive Employee Satisfaction Survey was con-

ducted of Valley First’s 330+ employees and the results affirmed our belief, that we have a very committed and motivated workforce.

Like any organization of our size there are always areas to improve on and through the survey process and working directly with staff,

we have developed a detailed action plan to address how we will improve in some areas and build on our strengths.

Information TechnologyAlways balancing cost versus return for our

shareholders, advances in Information

Technology at Valley First continue apace

with industry developments to ensure that

we continue to serve our members in a way

that meets their expectations. New initia-

tives in 2003 included, as mentioned previ-

ously, the introduction of cheque imaging,

which provides an array of benefits to the

membership and reduces production and

mailing costs. Other developments may have

been less visible to our members but are

instrumental in maintaining and enhancing

our high commitments to service, in safe-

guarding our member’s information security

and ensuring operational continuity. These

included the introduction of a new internal

e-mail system, a new loans origination sys-

tem, a new policy issuing system for the

insurance subsidiary and new data-backup

systems.

Some internal developments will continue in

2004 but the main focus will shift back to

member information access, including a new

on-line loan application and enhancements

to our corporate website and MemberDirect

Internet Banking system that will provide

enhanced functionality for our members

who prefer the convenience of reviewing

their financial information and paying their

bills on-line.

Valley First InsuranceServices Ltd.As anticipated, 2003 proved to be a very

challenging year as underwriting guide-

lines intensified and reduced capacity

forced premiums to rise. These factors,

coupled with record fire destruction in

the Okanagan last summer, placed con-

siderable stress on the system. We are

proud of the conscientious efforts of our

insurance staff.

The insurance industry is still sorting

itself out from the problems that

emerged in 2002. Lenient underwriting

practices, artificially low premiums, high

loss ratios and declining revenues from

investment activities have, in general,

impaired some insurers’ capacities to

write new business. We expect to see

easing of the current hard market and a

return to more traditional practices in

2004.

Valley First Insurance Services plans to

expand its commercial and business

insurance offerings in 2004 and will be

developing programs to meet the needs

of the credit union’s commercial mem-

bers for introduction during the second

quarter of the year.

President & CEO’s Report Continued

At Valley First Credit Union we take great pride in being connected to the communities we serve. In 2003,we sponsored over 100 different events and charities including a leadership role in bringing the firstever Okanagan International Children’s Festival to Penticton, major involvement throughout theOkanagan with the Canadian Cancer Society’s “Relay For Life”, the Interior Provincial Exhibition,the Peachland Wellness Center and sponsorship of the Kamloops Bantam Hockey tourna-ment, just to name a few!

We also continued to support the arts! In 2003, Valley First Credit Union contributed tothe One World Arts & Culture Society, the Okanagan School of the Arts and the firstannual Okanagan Vocal Arts Festival as well as a number of other cultural activities.

We’re proud to be a part of the fabric that makes the south central BC region sucha great place to call home.

Partners with your Community

2 0 0 3 A n n u a l R e p o r t | 1 2 2 0 0 3 A n n u a l R e p o r t | 1 3

Harold Hoey, Founding Member

During a recent interview,one of the founding members of Valley First Credit Union,

Mr. Harold Hoey, discussed the many changes he has witnessed at the credit union.

“We were members of the Knights of Pythius when we started the credit union in

1947 in Penticton. I was holder of passbook #20. The credit union operated with the

help of volunteers. We did the accounting, deposits and loans. I recall that 10 of us

chipped in and paid $12.50 each to purchase a safe! We each took the value out in

shares. It’s been an amazing period of growth at Valley First. I’m happy to say that

friendly service is still what impresses me the most”.

Mr. Hoey worked in the O.L. Jones Furniture store before joining the post office

where he worked for 28 years before retiring in 1980. Mr. Hoey now spends his

retirement looking after his wife of many years who suffers from the effects of

Alzheimer Disease. He speaks fondly of the friendly and helpful staff at Main Branch

where he still does his banking. Says Mr.Hoey,“I enjoy the fact that everyone knows

me by name!”

Judy Sentes, Executive Director O.S.N.S,Community Member O.S.N.S Child Development Centre

“We can’t say enough about the wonderful contributions Valley First

has made to the O.S.N.S. As government sources of our funding

become ever more challenged, our partnership with Valley First is

vital in maintaining our services for Early Intervention for birth to

school age children. Valley First has supported us with our

Evergreen Ball which raised $23,000, they’ve assisted us with our

annual raffles which raised over $35, 000 and provided significant

volunteer time with our cable-TV telethon which saw over $57,000

pledged to the O.S.N.S. We are proud and privileged with your part-

nership and applaud Valley First Credit Union’s spirit of community!”

▼▼

John and Carolyn Bratton,Retail Banking Members

“We found that complementing the competitive

rates was service that we were thoroughly delight-

ed with! These were the key elements for us to

move our mortgage, investment and day-to-day

banking business to Valley First Credit Union. We

were unhappy with the poor service and feeling like

a number at our previous financial institution. We

found that Valley First offered service above and

beyond the norm”.

Mr.Bratton explained that he also enjoyed the fact that Valley First was a responsible corporate citizen and noticed that local-

ly owned, locally operated,Valley First Credit Union, was investing in Kamloops through community involvement as well as

in developing a large new branch facility. He also expressed his distaste for the inability to “reach a real person”on the phone

at the chartered bank he was previously involved with. “At Valley First you always reach a ‘real person’whenever you call dur-

ing regular business hours,”says Mr.Bratton. They now have several mortgages at Valley First Credit Union as they have pur-

chased other properties for family members and have moved their investment portfolio to in-branch Investment Advisor

Graham Cope B.Sc. We certainly appreciate their kind comments and their business.

▼

From left to right :Christopher Koster,

Shelby Sturko,Mackenzie Vunak,

Judy Sentes

Here’s what some of our partners say...

Mill Creek - Kelowna

Brandt’s Crossing - Kelowna

Stonebridge Lodge - Big White Ski Resort

Cherry Lane Towers - Penticton

2 0 0 3 A n n u a l R e p o r t | 1 52 0 0 3 A n n u a l R e p o r t | 1 4

Commercial Lending

Kettle Valley Estates - Kelowna

Ramada Inn - Penticton

Great Canadian Oil Change - Kelowna

The expansion of commercial proper-ties in our service area is unprece-dented and Valley First is excited tobe part of this incredible growth. OurCommercial Lending Division hasexperienced enormous success in thedevelopment of a number of proper-ties in Kamloops and the OkanaganValley. From subdivision develop-ments to ski resort properties, ValleyFirst Credit Union is widely recog-nized as the financial services partnerto get the job done!

Here’s what our businessmembers say about us...“The Commercial Lending Division atValley First Credit Union is the mostknowledgeable lending team I’veever dealt with. Their expertise isunparalleled, plus we like the fact thatdecisions are made locally… andquickly!”Robin Agur, Ramada Inn - Penticton

“I couldn’t be more pleased with theservice and support from Valley First.The staff is excellent. I deal with com-mercial lenders across the prairiesand throughout BC and Valley FirstCredit Union is a leader! Plus, whenyou call, you always get a real personat the other end of the phone!”Dennis Skuter, Stonebridge Lodge - Big White Ski Resort, Kelowna

“Valley First Credit Union has beenwonderful to us! They came on boardwhen we really needed a financial insti-tution to get our project completedand provided incredible assistance.They’re so helpful and friendly! Wedealt with several other financial insti-tutions but now we’ve moved all of ourbusiness to Valley First.”Gay Kleitzke,Kamloops Hospice Society

Commercial Banking Branches Penticton 490-2700

Kelowna 860-1900

Vernon 558-5266

Armstrong 546-3191

Kamloops 374-4924

Princeton 295-3171

w w w . v a l l e y f i r s t . c o m 2 0 0 3 a n n u a l r e p o r t

Valley First Credit UnionConsolidated Financial Statements

17 Management’s Responsibility | Auditors’ Report

18 Consolidated Balance Sheet

18 Consolidated Statement of Earnings and Retained Earnings

19 Consolidated Statement of Cash Flows

19 Notes to the Consolidated Financial Statements

December 31, 2003

2 0 0 3 A n n u a l R e p o r t | 1 7

Grant Thornton LLP

Chartered Accountants

Management Consultants

Auditors' Report

To the Members of Valley First Credit Union

We have audited the consolidated balance sheet of Valley First Credit Union as at

December 31, 2003 and the consolidated statements of earnings and retained earn-

ings and cash flows for the year then ended. These financial statements are the

responsibility of the Credit Union's management. Our responsibility is to express an

opinion on these consolidated financial statements based on our audit.

We conducted our audit in accordance with Canadian generally accepted auditing

standards. Those standards require that we plan and perform an audit to obtain rea-

sonable assurance whether the consolidated financial statements are free of materi-

al misstatement. An audit includes examining, on a test basis, evidence supporting

the amounts and disclosures in the financial statements. An audit also includes

assessing the accounting principles used and significant estimates made by man-

agement, as well as evaluating the overall financial statement presentation.

In our opinion, these consolidated financial statements present fairly, in all material

respects, the financial position of the Credit Union as at December 31, 2003 and the

results of its operations and cash flows for the year then ended in accordance with

Canadian generally accepted accounting principles. As required by the Financial

Institutions Act of British Columbia, we report that, in our opinion, those principles

have been applied on a basis consistent with that of the preceding year.

Kelowna, B.C.

January 30, 2004 Chartered Accountants

For the year ended December 31, 2003

Management’s Responsibility

These financial statements have been prepared by the management of Valley First,

which is responsible for their reliability, completeness and integrity. They were devel-

oped in accordance with the requirements of the Financial Institutions Act and conform

in all material aspects with Canadian generally accepted accounting principles. The

financial information presented in the Annual Report is consistent with the financial

statement.

Systems of internal control and reporting procedures are designed to provide reason-

able assurance that the financial records are complete and accurate so as to safeguard

the assets of the organization. These systems include establishment and communica-

tion of standards of business conduct throughout all levels of the organization to pre-

vent conflicts of interest and unauthorized disclosure and to provide assurance that all

transactions are authorized and proper records maintained. Further, they are reviewed

by the Credit Union's external auditors and the Credit Union is subject to periodic exam-

ination by the Financial Institutions Commission.

The Board of Directors has approved the financial statements. The Audit Committee of

the Board,comprised of three directors and the President & CEO,has reviewed the state-

ments with the external auditors in detail and received regular reports on internal con-

trol findings.

Grant Thornton the external independent auditor appointed by the membership,exam-

ined the financial statements of the Credit Union in accordance with the generally

accepted auditing standards. They have had full and free access to the Internal Auditor

and the Audit Committee of the Board. Their report follows.

Harley BiddlecombePresident & Chief Executive Officer

Robert G. Mowat, B.Comm, CGA

Vice President, Systems,

Finance & Chief Financial Officer

Consolidated Financial Statements

Consolidated Statement of Cash Flows

Year Ended December 31 2003 2002

Increase(decrease) in cash resources

Operating activitiesNet earnings $ 4,634,380 $ 3,640,362Adjustments to determine cash flows:Provision for loan losses 486,062 329,973Amortization 1,404,468 1,369,666Change in interest accruals 1,874,248 (1,618,469)Future income taxes (217,282) 23,378Other 1,578,126 464,362

9,760,002 4,209,272Financing activitiesDeposits, net of withdrawals 73,701,230 4 0,594,256Borrowings 1,044,450 8,876,550Change in equity shares 1,400,826 6,713,641Dividends on equity shares, net (654,009) (685,891)

75,492,497 55,498,556Investing activitiesLoans, net of repayments (82,719,451) (52,321,741)Investment and other 1,013,328 962,765Purchase of capital assets (2,941,815) (2,054,718)Purchase of goodwill - (304,753)Proceeds from the disposal of assets 262,085 7,483

(84,385,853) (53,710,964)

Net increase in cash resources 866,646 5,996,864

Cash resources, beginning of year 75,943,779 69,946,915

Cash resources, end of year $ 76,810,425 $75,943,779

Supplementary cash flow information

Interest paid $ 16,285,074 $19,595,119Income taxes paid $ 1,255,705 $ 914,916

Consolidated Balance Sheet

December 31 2003 2002

Assets

Cash resources (Note 3) $ 76,810,425 $ 75,943,779Loans (Note 4) 639,398,580 556,871,259Investment and other (Note 5) 27,499,947 28,513,275Capital assets (Note 6) 11,912,459 10,655,989Goodwill (Note 7) 3,909,590 3,909,590

$ 759,531,001 $ 675,893,892

Liabilities and equity

Deposits (Note 8) $ 689,540,311 $ 613,809,075Payables and accruals 5,908,517 4,428,291Borrowings (Note 9) 14,921,000 13,876,550

710,369,828 632,113,916

Equity shares (Note 10) 27,668,297 26,267,471Contributed Surplus 3,836,405 3,836,405Retained earnings 17,656,471 13,676,100

49,161,173 43,779,976

$ 759,531,001 $ 675,893,892

Commitments (Note 18)

On behalf of the Board

Chair of the Board Chair, Audit Committee

Consolidated Financial Statements Continued

2 0 0 3 A n n u a l R e p o r t | 1 8 2 0 0 3 A n n u a l R e p o r t | 1 9

Consolidated Statements of Earnings and Retained Earnings

Year Ended December 31 2003 2002

Financial incomeLoans $ 35,586,571 $ 31,555,447Investment and other 6,370,000 6,717,562

41,956,571 38,273,009Financial expenseDeposits 18,276,448 18,046,191Borrowings 989,586 884,011

19,266,034 18,930,202

Financial margin 22,690,537 19,342,807

Provision for loan losses (Note 4) 486,062 329,97322,204,475 19,012,834

Other income (Note 12) 11,764,727 10,594,770

Operating margin 33,969,202 29,607,604

Operating expenses (Note 13) 28,137,892 24,827,966

Earnings before income taxes 5,831,310 4,779,638

Income taxes (Note 14)Current 1,414,212 1,119,328Future (217,282) 23,378

1,196,930 1,142,706

Net earnings 4,634,380 3,636,932

Retained earnings, beginning of year 13,676,100 10,725,059Dividends on equity shares, net of tax($139,884; 2002 - $146,501) (654,009) (685,891)

Retained earnings, end of year $ 17,656,471 $ 13,676,100

1. Governing legislation and operations

The Credit Union is incorporated under the Credit Union Incorporation Act of BritishColumbia; and the operation of the Credit Union is subject to the Financial InstitutionsAct of British Columbia. The Credit Union serves members principally in the Interiorof British Columbia.

2. Summary of accounting policies

Principles of consolidationThe consolidated financial statements include the accounts of the Credit Union andits wholly-owned subsidiaries, Valley First Insurance Services Ltd., Western InteriorFinancial Ltd. and 617667 B.C. Ltd. All significant intercompany transactions andaccounts have been eliminated.

Use of estimatesManagement has made estimates and assumptions that affect the amounts reportedin preparing these financial statements. Actual results could differ from those esti-mates.

LoansLoans are carried at the unpaid principal plus accrued interest less an allowanceestablished to provide against probable losses on ultimate realization of the loanportfolio. Loans considered uncollectible are written off.

Loan interestInterest income from loans is recorded on the accrual method, except where a loan isimpaired. Interest received on an impaired loan is recognized in earnings only if thereis no doubt as to the collectibility of the carrying value of the loan.

Loan feesNet fees earned and costs incurred in connection with lending activity are deferredand amortized over the term of the underlying loans.

Allowance for loan lossesThe allowance for impairment is maintained at a level considered adequate to absorbanticipated credit losses. Specific allowances are provided for specifically identifiedloans that have become impaired. A loan is classified as impaired generally at the ear-lier of when, in the opinion of management, there is reasonable doubt as to the col-lectibility of principal and interest, when interest is 90 days past due, or financialreporting is significantly in arrears.

Notes to the Consolidated Financial Statements

See accompanying notes to the financial statements See accompanying notes to the financial statements

December 31, 2003December 31, 2003

2. Summary of accounting policies continued

Specific allowances are supplemented by general allowances. The general allowancerepresents the best estimate of probable losses within the portion of the portfoliothat has not been specifically identified as impaired. The amount is establishedthrough the application of expected loss factors to outstanding balances.

InvestmentsPortfolio investments are recorded at the lower of cost and market.

SharesShares are classified as liabilities or as member equity according to their terms. Whereshares are redeemable at the option of the member, either on demand or on with-drawal from membership, the shares are classified as liabilities. Where shares areredeemable at the discretion of the Credit Union board of directors, the shares areclassified as equity. Dividends on equity shares less related income tax reductions arecharged against retained earnings in the year they are declared.

Capital assetsCapital assets are stated at cost. Amortization is computed on the straight-linemethod at rates varying between 2% and 25%. Leasehold improvements are writtenoff over the term of the lease and the first renewal period or ten years whichever is thelesser.

GoodwillGoodwill represents the excess purchase price of acquired businesses over the fairvalue of the net assets acquired. Goodwill purchased prior to June 30, 2002 was amor-tized using the straight-line method over its estimated period of benefit, not exceed-ing 40 years. The company annually compares the carrying value of goodwill to theestimated undiscounted future cash flows that may be generated by the related busi-nesses and recognizes in net income any impairment to the net recoverable amount.

Goodwill acquired subsequent to July 1, 2002 is not amortized. Goodwill is reviewedby management on at least an annual basis to determine whether there is an impair-ment in value. Goodwill is tested between annual tests when an event or circum-stance occurs that more likely than not reduces the fair value of the goodwill belowits carrying value.

An impairment in value is calculated based on the fair value of estimated recoverabil-ity through projected cash flows, earnings and fair value of the Company’s assetscompared to the carrying value of the goodwill. Any loss on impairment during theyear will be charged to earnings.Income taxes

The Credit Union follows the asset and liability method of accounting for incometaxes, whereby future tax assets and liabilities are recognized for the expected futuretax consequences attributable to differences between the financial statement carry-ing amount of existing assets and liabilities and their respective taxes bases and oper-ating loss and tax credit carry forwards. Future tax assets and liabilities are measuredusing enacted or substantially enacted tax rates expected to apply to taxable incomein the years in which those temporary differences are expected to be recovered or set-tled.

Net future income tax assets and liabilities are included in payables and accruals.

Derivative Financial InstrumentsThe Credit Union enters into derivative financial instruments to manage its exposureto fluctuations in interest rates. Interest income and expenses for these contracts areaccounted for on the accrual basis over the term of the contract. Gains and losses onsettlement of these derivative financial instruments are recognized in earnings theperiod in which they occur.

Revised accounting standards that govern when deferral and amortization account-ing treatment is permitted will become effective for fiscal 2004. As a result, premiums,gains and losses of derivative financial instruments that do not qualify for deferral andamortization accounting treatment under the revised standards will be recorded inthe statement of earnings in the period that they are incurred.The earnings impact ofthe revised standard will depend on the risk management strategies used and marketvolatility.

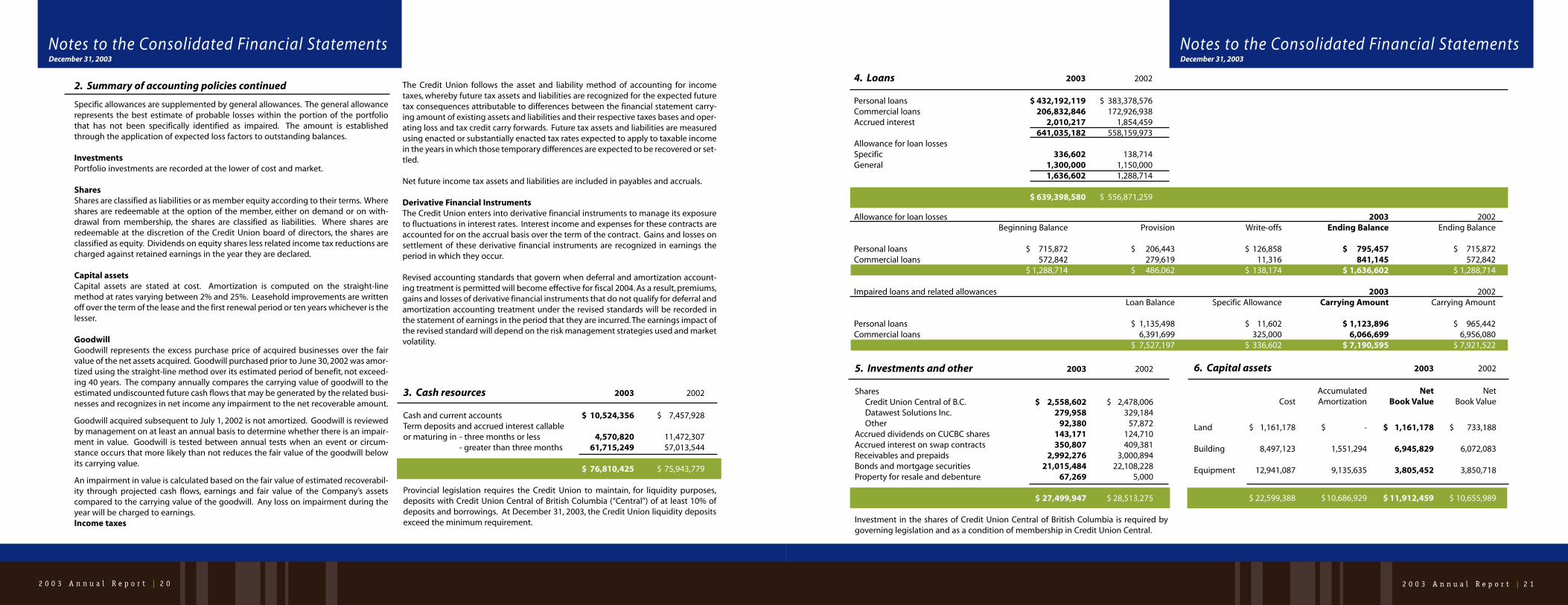

2 0 0 3 A n n u a l R e p o r t | 2 0 2 0 0 3 A n n u a l R e p o r t | 2 1

Notes to the Consolidated Financial Statements

3. Cash resources 2003 2002

Cash and current accounts $ 10,524,356 $ 7,457,928 Term deposits and accrued interest callableor maturing in - three months or less 4,570,820 11,472,307

- greater than three months 61,715,249 57,013,544

$ 76,810,425 $ 75,943,779

Provincial legislation requires the Credit Union to maintain, for liquidity purposes,deposits with Credit Union Central of British Columbia (“Central”) of at least 10% ofdeposits and borrowings. At December 31, 2003, the Credit Union liquidity depositsexceed the minimum requirement.

Allowance for loan losses 2003 2002Beginning Balance Provision Write-offs Ending Balance Ending Balance

Personal loans $ 715,872 $ 206,443 $ 126,858 $ 795,457 $ 715,872Commercial loans 572,842 279,619 11,316 841,145 572,842

$ 1,288,714 $ 486,062 $ 138,174 $ 1,636,602 $ 1,288,714

Impaired loans and related allowances 2003 2002Loan Balance Specific Allowance Carrying Amount Carrying Amount

Personal loans $ 1,135,498 $ 11,602 $ 1,123,896 $ 965,442Commercial loans 6,391,699 325,000 6,066,699 6,956,080

$ 7,527,197 $ 336,602 $ 7,190,595 $ 7,921,522

4. Loans 2003 2002

Personal loans $ 432,192,119 $ 383,378,576Commercial loans 206,832,846 172,926,938Accrued interest 2,010,217 1,854,459

641,035,182 558,159,973Allowance for loan lossesSpecific 336,602 138,714General 1,300,000 1,150,000

1,636,602 1,288,714

$ 639,398,580 $ 556,871,259

5. Investments and other 2003 2002

SharesCredit Union Central of B.C. $ 2,558,602 $ 2,478,006Datawest Solutions Inc. 279,958 329,184Other 92,380 57,872

Accrued dividends on CUCBC shares 143,171 124,710Accrued interest on swap contracts 350,807 409,381Receivables and prepaids 2,992,276 3,000,894Bonds and mortgage securities 21,015,484 22,108,228Property for resale and debenture 67,269 5,000

$ 27,499,947 $ 28,513,275

Investment in the shares of Credit Union Central of British Columbia is required bygoverning legislation and as a condition of membership in Credit Union Central.

6. Capital assets 2003 2002

Accumulated Net Net Cost Amortization Book Value Book Value

Land $ 1,161,178 $ - $ 1,161,178 $ 733,188

Building 8,497,123 1,551,294 6,945,829 6,072,083

Equipment 12,941,087 9,135,635 3,805,452 3,850,718

$ 22,599,388 $10,686,929 $ 11,912,459 $ 10,655,989

December 31, 2003

Notes to the Consolidated Financial StatementsDecember 31, 2003

2 0 0 3 A n n u a l R e p o r t | 2 2 2 0 0 3 A n n u a l R e p o r t | 2 3

7. Goodwill 2003 2002

Goodwill $ 6,487,160 $ 6,487,160Less: accumulated amortization (2,577,570) (2,577,570)

$ 3,909,590 $ 3,909,590

Notes to the Consolidated Financial Statements

8. Deposits 2003 2002

Demand $ 238,242,402 $ 197,402,472Municipal deposits 12,458,091 10,594,640Term 313,465,360 299,286,318Registered savings plans 116,591,504 99,772,697Accrued interest 8,782,954 6,752,948

$ 689,540,311 $ 613,809,075

9. Borrowings 2003 2002

Credit Union Central of BC $ 5,000,000 $ -CIBC 9,921,000 13,876,550

$ 14,921,000 $ 13,876,550

The Credit Union has available to it, through Credit Union Central of B.C., an operat-ing line and term loan facility of $26.2 million secured by a general security agree-ment and the general assignment of book debts.

The Credit Union maintains a $40 million credit facility with the Canadian ImperialBank of Commerce. The advances are secured by a general security agreement overcertain insured residential mortgages and a priority agreement from Credit UnionCentral of B.C. recognizing CIBC’s interests.

10. Equity shares

Capital of the Credit Union is divided into three classes of equity shares, all having apar value of $1. Funds invested in these shares are not guaranteed by the CreditUnion Deposit Insurance Corporation of British Columbia. Redemption of equityshares may be subject to certain restrictions.

2003 2002

Class A Membership Equity SharesUnder the Credit Union rules, members are requiredto hold at least 25 membership equity shares.Membership equity shares pay dividends at thediscretion of the directors in the form of cash oradditional shares. These shares are redeemable under certain conditions at the discretion of the directors to a maximum of 10% of the issued and outstanding shares in any one year. $ 1,681,180 $ 1,705,942

Class B Investment Equity SharesInvestment equity shares pay dividends at thediscretion of the directors in the form of cash oradditional shares. These shares are redeemable under certain conditions at the discretion of the directors to a maximum of 10% of the issued and outstanding shares in any one year. 14,686,917 11,879,758

Class C Retirement Plan Equity SharesRetirement plan equity shares pay dividends in the form of additional shares or cash credited to an RRSP of the same class. These shares are redeemable, subject to the discretion of the board of directors. There is no limit on the number of shares which may be held by a member. 11,169,569 12,528,220

Provision for dividends on equity shares 130,631 153,551

$ 27,668,297 $ 26,267,471

11. Capital requirements

The Credit Union is required under governing legislation to maintain a minimumlevel of certain types of investments. In addition, the Act prescribes minimum lev-els of capital based on prescribed risk weighted values being applied to certainCredit Union assets. At December 31, 2003, the Credit Union exceeded the mini-mum required capital base.

12. Other income 2003 2002

Chequing services and commissions $ 5,260,392 $ 4,769,769Commissions 3,820,020 3,486,963Loan fees and other 2,684,315 2,338,038

$11,764,727 $10,594,770

13. Operating expenses 2003 2002

Advertising and promotion $ 696,493 $ 534,369Amortization 1,404,468 1,369,666Capital taxes 515,900 477,835Data processing 2,374,698 2,711,373Office and operating expenses 7,210,033 6,064,109Salaries and employee benefits 15,936,300 13,670,614

$28,137,892 $24,827,966

14. Income taxes

The total provision for income taxes in the statement of earnings and retainedearnings is at a rate less than the combined federal and provincial statutory incometax rates of the applicable year for the following reasons:

2003 2002

Combined federal and provincial statutory income tax rate 37.62% 39.62%

Decrease in rate due to:Rate reduction applicable to credit unions (20.00%) (22.00%)Other, net 2.90% 6.29%

Effective income tax rate 20.52% 23.91%

The components of future income tax balances included in payables and accruals are as follows:

Future income tax assets (liabilities)Allowance for credit losses $ 238,802 $ (21,278)Deferred items 83,715 38,937Other (204,614) (187,438)

Net future income tax assets (liabilities) $ 117,903 $ (169,779)

December 31, 2003

Notes to the Consolidated Financial StatementsDecember 31, 2003

2 0 0 3 A n n u a l R e p o r t | 2 4 2 0 0 3 A n n u a l R e p o r t | 2 5

Notes to the Consolidated Financial Statements

Interest Sensitive Balances Non-Interest 2003 2002Sensitive Total Total

Average Within Greater thanRates 1 year 1 year

AssetsCash resources 3.49% 15,074,998 49,919,480 11,815,947 76,810,425 75,943,779Loans 5.91% 362,514,633 276,510,332 373,615 639,398,580 556,871,259Other assets 4,201,769 16,813,715 22,306,512 43,321,996 43,078,854

381,791,400 343,243,527 34,496,074 759,531,001 675,893,892

Liabilities and Members’ EquityDeposits 3.98% 243,170,677 318,695,015 127,674,619 689,540,311 613,809,075Other 4.50% 14,921,000 55,069,690 69,990,690 62,084,817

258,091,677 318,695,015 182,744,309 759,531,001 675,893,892

Balance Sheet Mismatch 123,699,723 24,548,512 (148,248,235) - -

Interest Rate Swaps, net (97,000,000) 97,000,000 - - -

Net Mismatch 2003 26,699,723 121,548,512 (148,248,235) - -

Net Mismatch 2002 (141,742,000) 116,790,000 24,952,000 - -

15. Interest rate sensitivity

The Credit Union is exposed to interest rate risk as a consequence of the mismatch, or gap between the assets, liabilities and off-balance sheet instruments scheduled toreprice on particular dates.

Maturity dates substantially coincide with interest adjustment dates. Amounts with floating interest rates, or due on demand, are classified as maturing within one year,regardless of maturity. Amounts that are not interest sensitive are grouped together, regardless of maturity.

The table below does not incorporate management’s expectation of future events where repricing or maturity dates of certain loans and deposits may differ significantlyfrom the contractual dates.

2003 2002

Fair value Fair valueEstimated over (under) over (under)

Book Value Fair Value Book Value Book Value

AssetsCash resources $ 76,810,425 $ 79,424,983 $ 2,614,558 $ 3,077,000Loans 639,398,580 646,856,984 7,458,404 4,272,000Investments and other 27,499,947 27,571,528 71,581 -

LiabilitiesDeposits $ 689,540,311 $ 702,569,904 $ 13,029,593 $ 12,380,000Payables and accruals 5,908,517 5,908,517 - -Borrowings 14,921,000 14,921,000 - -

Equity shares 27,668,297 27,668,297 - -

Derivatives - 1,693,224 1,693,224 2,520,460

16. Fair values of financial instruments

The estimated fair values of financial instruments are designed to approximate values at which these instruments could be exchanged in a current market. However, manyof the financial instruments lack an available trading market and therefore fair values are based on estimates.

No fair values have been determined for capital assets or any other asset or liability that is not a financial instrument. The fair values of cash resources, variable rate loans anddeposits, other assets and liabilities are assumed to equal their book values. The fair values of fixed rate loans and deposits are determined by discounting the expected futurecash flows at the estimated current market rates for loans and deposits with similar characteristics.

Changes in interest rates are the main cause of changes in the fair value of the Credit Union’s financial instruments. The Credit Union’s financial instruments are carried at his-torical cost and are not adjusted to reflect increases or decreases in fair value due to interest rate changes.

December 31, 2003

Notes to the Consolidated Financial StatementsDecember 31, 2003

2 0 0 3 A n n u a l R e p o r t | 2 6 2 0 0 3 A n n u a l R e p o r t | 2 7

17. Off balance sheet

Funds under administrationOff balance sheet funds under administration by the credit union are comprised ofloans that have been sold, loans that have been syndicated and are administeredin the capacity as an agent and investment portfolios including mutual fundaccounts managed on behalf of the members. Off balance sheet funds are notincluded in the balance sheet.

2003 2002Sold loans $31,129,953 $23,207,710Syndicated loans $33,113,116 $17,213,566Mutual funds $90,382,603 $71,111,056

Derivative financial instrumentsAt December 31, 2003, the Credit Union has outstanding interest rate swap con-tracts in the notional amount of $131,500,000 (2002 – $104,500,000) maturing atvarying dates to 2008. Interest rate swaps involve the exchange of interest flowsbetween two parties on a specified notional principal amount for a pre-deter-mined period at agreed upon fixed and floating rates. Principal amounts are notexchanged and are not indicative of credit exposure.

The Credit Union has an outstanding forward rate agreement in the notionalamount of $10,000,000 (2002 – Nil) maturing April 22, 2004.

Principal amounts are not exchanged and are not indicative of credit exposure.TheCredit Union manages credit risk by dealing with creditworthy counterparties andsetting limits for investments with those counterparties.

Letters of creditIn the normal course of business, the Credit Union enters into various off-balancesheet commitments such as letters of credit. Letters of credit are not reflected inthe balance sheet. At December 31, 2003, the Credit Union has outstanding lettersof credit on behalf of members in the amount of $8,522,827 (2002 - $5,009,333).

LoansAs at December 31, 2003 the Credit Union had committed to certain loans which, ifthey had been fully advanced, would amount to $73,543,078 (2002 - $52,810,816).

Notes to the Consolidated Financial Statements

18. Commitments

Certain branch premises are leased for terms extending to 2008. Total rentals underthese leases for the next five years are $5,610,488.

19. Related party transaction

At December 31, 2003, loans to directors, officers and related parties amounted to$7,816,972 (2002 - $7,067,146).

During the year, directors received in their capacity as directors remunerationtotalling $65,000 in aggregate (2002 - $61,098).

20. Comparative figures

The financial statements as of December 31, 2002 and for the year then ended wereaudited by other auditors who expressed an opinion without reservation on thosestatements in their report dated February 7, 2003. In addition, certain comparativefigures for 2002 have been reclassified to conform with the current year’s presenta-tion.

Head Office

3rd Floor, 184 Main StreetPenticton, BC V2A 8G7Phone (250) 490-2720Fax (250) 490-2721

Credit Union Branches

PENTICTON

MAIN BRANCH184 Main StreetBranch Manager: Dale BoisclairManager, Commercial Banking:Michael Murison

CHERRY LANE 135 – 2111 Main StreetBranch Manager: Jerry McKenna

PEACHTREE MALL 166 – 275 Green AvenueBranch Manager:Lorraine Richardson

KEREMEOSBox 250, 704 7th AvenueBranch Manager: Leslie Rakow

PRINCETONBox 190, 114 Tapton AvenueBranch Manager: Kevin Kelbert

OLIVERBox 340, Oliver Place MallBranch Manager: Betty Neufield

KELOWNA

DOWNTOWN KELOWNA507 Bernard AvenueBranch Manager: Lorne EttingerManager, Commercial Banking:David Trask

GUISACHAN VILLAGE 101 – 2395 Gordon DriveBranch Manager: Ron Minion

ORCHARD PLAZA1860 Cooper RoadBranch Manager: Viki May

VERNON

3322 31st AvenueBranch Manager: Marv Krause

PEACHLAND

Box 24,24 – 5500 Clements CrescentBranch Manager:Marion Henselwood

ARMSTRONG

Box 400, 2575 Patterson AvenueAssistant Vice President & Branch Manager: Tony Fergusson

LUMBY

Box 1029, 2109 Shuswap AvenueManager, Personal Banking:Marlene Stark

KAMLOOPS

180 Seymour StreetBranch Manager: Heikki HollantiManager, Commercial Banking:Jim Lamond

Insurance Offices

PENTICTON

MAIN BRANCH184 Main StreetOffice Supervisor: Linda Johnson

CHERRY LANE135B – 2111 Main StreetOffice Supervisor: Carol Chow

KELOWNA

GUISACHAN VILLAGE103 – 2395 Gordon DriveOffice Supervisor: Carol Handsor

VERNON

3009 34th StreetOffice Supervisor: Brandie Wernicke

VILLAGE GREEN MALL90 – 4900 27th StreetOffice Supervisor: Virginia Lavery

LUMBY

Box 799, 1965 Shuswap AvenueOffice Supervisor:Delma Wiedeman

PEACHLAND

26 – 5500 Clements CrescentOffice Supervisor: Linda Kenzle

PRINCETON

Box 2448, 114 Tapton Avenue Office Supervisor: Linda Thompson

ARMSTRONG

Box 10, 2595 Pleasant Valley Blvd.Office Supervisor: Gail Howard

Wealth ManagementOffices

PENTICTON

MAIN BRANCH184 Main StreetSenior Manager,Wealth Management:Kevin Tom* Financial Planner:Hugh Desjardins

CHERRY LANE 135 – 2111 Main StreetFinancial Planner: Bruce LeFranc

PEACHTREE MALL166 – 275 Green Avenue* Financial Planner: Jeff Olensky

KELOWNA

DOWNTOWN KELOWNA507 Bernard Avenue* Financial Planner: Jay Christensen

GUISACHAN VILLAGE103 – 2395 Gordon Drive* Financial Planner: Jay Christensen

PEACHLAND

26 – 5500 Clements Crescent* Financial Planner: Jeff Olensky

VERNON

3009 34th Street* Financial Planner: T. Scott Boyd

PRINCETON

Box 2448, 114 Tapton Avenue* Financial Planner:Hugh Desjardins

LUMBY

Box 799, 1965 Shuswap Avenue* Financial Planner: T. Scott Boyd

ARMSTRONG

2595 Pleasant Valley Blvd.* Financial Planner: T. Scott Boyd

OLIVER

Box 340, Oliver Place Mall* Financial Planner: Jeff Olensky

KEREMEOS

Box 250, 704 7th Avenue* Financial Planner:Hugh Desjardins

KAMLOOPS

180 Seymour StreetFinancial Planner: Graham Cope

Corporate InformationBoard of Directors

John Robertson – Chair

Colleen Lister – Vice Chair

Kevin Campbell – Director

Liz Goodison – Director

Adolf Illichmann – Director

Lanny Martiniuk –Director

Ramesh Rikhi – Director

Larry Stevens – Director

Rick Willie – Director

Senior Executive

Harley BiddlecombePresident & Chief Executive Officer

Robert LindsaySenior Vice President, Retail Banking

Jackie HortonVice President, Corporate Administration & Human Resources

Ted HoustonVice President, Commercial Banking & Subsidiary Operations

Robert MowatVice President, Systems, Finance & Chief Financial Officer

Paulette RennieVice President, Sales & Branch Operations

Tom BijvoetAssistant Vice President,Information Technology

Susan EssonAssistant Vice President, Controller

Peter KvietinskasAssistant Vice President, Commercial Credit

Kelly McGiffinAssistant Vice President, Sales & Service

Ron SmithAssistant Vice President,Commercial Banking

David SimpsonGeneral Manager,Valley First Insurance Services Ltd.

* Contact branch for availability

December 31, 2003