building mineral linkages and economic diversification the ... value addition in ghana... · the...

TRANSCRIPT

Building mineral linkages and economic diversification – the case of Ghana and ECOWAS

John SloanAfrican Minerals Development Centre

Outline of Presentation

1. The Africa Mining Vision context and scope of this initiative

2. Mining Sector’s Contribution to Value Addition

3. Opportunities for Local Production

4. Spatial and Regional Potential

5. Challenges and Policy Recommendations

The Africa Mining Vision context and scope of this initiative

The Africa Mining Vision

• Adopted by African Heads of State in 2009

• Advocates for a fundamental shift towards harnessing minerals for inclusive and sustainable opportunities

• The only African-owned transformative framework on minerals

• Moves away from focus on mineral rents/revenues

• Focus on mainstreaming mineral sector into broad-based development.

• African Minerals Development Centre established as an implementing agency of the AMV.

• Work on establishing linkages is central to AMDC’s activities

Strategic considerations for our engagement

• A part of the Country Mining Vision Process to domesticate key tenets of the AMV and complement Government’s own reform agenda.

• Purpose: To depart from the traditional raw material dependence and overcome vulnerability to boom-bust cycles.

• Strategic value: Sub-region is at a crossroads, extraction is increasing, mineral-based economic and industrial transformation high on agenda

• More than a ‘project’: a long-term engagement to identify opportunities in upstream and downstream linkages in the entire extractive sector (mining as well as hydrocarbons).

• An inclusive dialogue process: Our engagement and support includes a range stakeholders – policy makers, private sector, think-tanks, …

Scope of initiative and steps taken

• Roll-out in three phases:

– Phase 1 (NOW): Analysis of opportunities in upstream value creation in mining

– Phase 2: Analysis of downstream linkage potential in mining (including artisanal small scale mining and industrial minerals - starting soon)

– Phase 3: Analysis of sidestream linkages with the hydrocarbon sector

• Steps thus far:1. Request from Government of Ghana to identify potential mineral linkages;

2. Study of regional upstream opportunities completed;

3. Results discussed with and validated by stakeholders (public, private, etc)

4. Approval of Cabinet Memo by EMT endorsing this initiative for value-addition

5. Workshop and launch of National Supplier Development Programme (NSDP)

Analysis undertaken

Research approach – analysis of opportunities in upstream value creation:

– Assessing the state of upstream industrial linkages in West Africa

– Identifying opportunities and means to scale-up local procurement along a

set of realizable products (BGR);

– Studied challenges in the business environment, capacities and institutional

constraints;

– Considering economic clustering and means to link mining and industry;

– Proposing an NSDP to support domestic industries.

Mining Sector’s Contribution to Value Addition

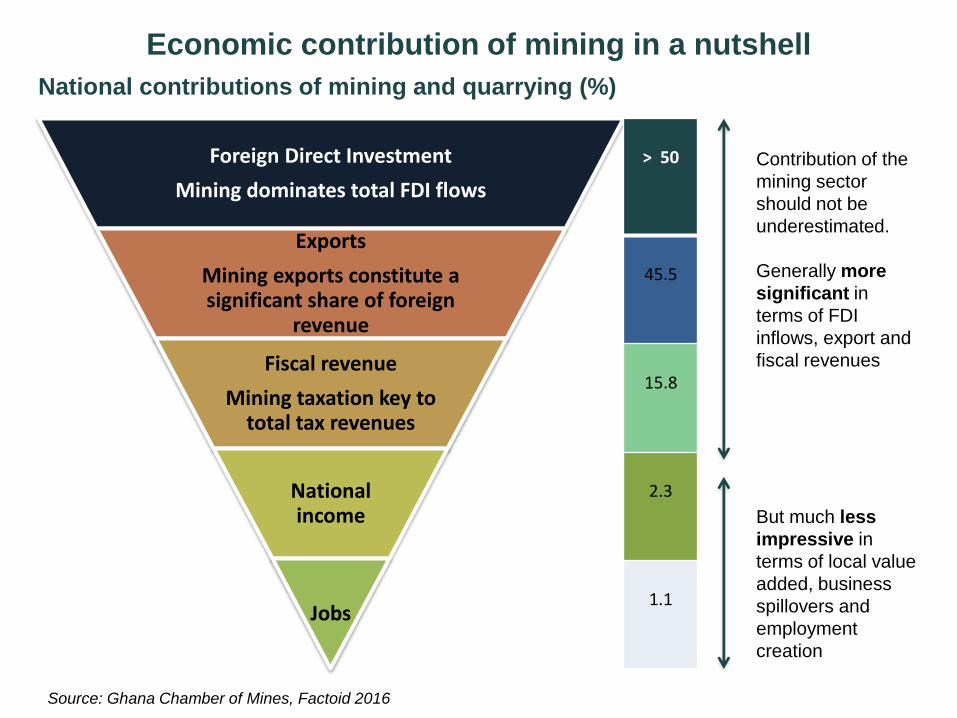

Foreign Direct Investment

Mining dominates total FDI flows

Exports

Mining exports constitute a significant share of foreign

revenue

Fiscal revenue

Mining taxation key to total tax revenues

National income

Jobs

> 50

45.5

15.8

2.3

1.1

National contributions of mining and quarrying (%)

Economic contribution of mining in a nutshell

Contribution of the

mining sector

should not be

underestimated.

Generally more

significant in

terms of FDI

inflows, export and

fiscal revenues

But much less

impressive in

terms of local value

added, business

spillovers and

employment

creation

Source: Ghana Chamber of Mines, Factoid 2016

US$, million 2015 2016

Total Local Purchases (incl. energy) 1492,9 48% 1690,97 52%

Total Local Purchases (excl. Diesel & Electric Power) 865,6 28% 1013,8 31%

Total Local Purchase on Diesel and Energy 627,3 20% 677,2 21%Payment to employees 429,97 14% 435,6 13%Total Fiscal payments 377,3 12% 427,23 13%

Expenditure on Corporate Social Investment 17,8 0,6% 12,2 0,4%Total mineral revenue 3118,1 3257,6

Meanwhile, the industry reported in-country contributions as follows

Source: Ghana Chamber of Mines, 2016

0 200 400 600 800 1000 1200 1400 1600 1800

Total Local Purchases (incl. energy)

Total Local Purchases (excl. Diesel & Electric Power)

Payment to employees

Total Fiscal payments

Expenditure on Corporate Social Investment

Mining companies' in-country expenditure 2015-16 (US$, million)

2016

2015

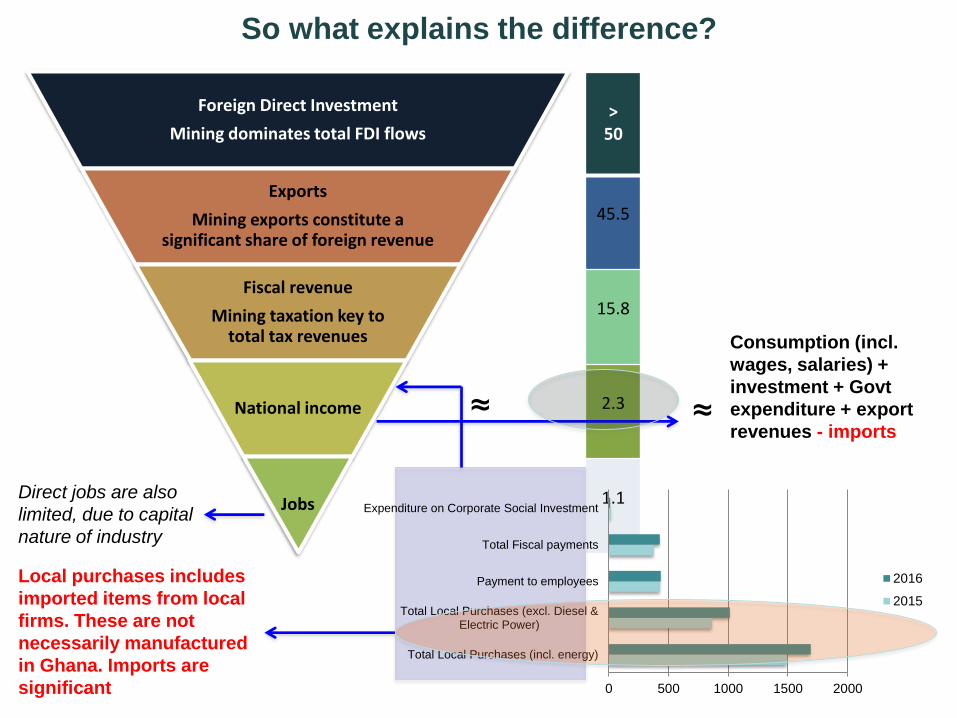

> 50

45.5

15.8

2.3

1.1

Foreign Direct Investment

Mining dominates total FDI flows

Exports

Mining exports constitute a significant share of foreign revenue

Fiscal revenue

Mining taxation key to total tax revenues

National income

Jobs

So what explains the difference?

Consumption (incl.

wages, salaries) +

investment + Govt

expenditure + export

revenues - imports

Local purchases includes

imported items from local

firms. These are not

necessarily manufactured

in Ghana. Imports are

significant

≈

Direct jobs are also

limited, due to capital

nature of industry

≈

0 500 1000 1500 2000

Total Local Purchases (incl. energy)

Total Local Purchases (excl. Diesel &Electric Power)

Payment to employees

Total Fiscal payments

Expenditure on Corporate Social Investment

2016

2015

Goods or services 1st

edition of LC, 2014

2nd

edition of LC 2016

Forthcoming 3

rd Edition of

LC, 2018* 1 Grinding media 2 Explosive (emulsion) 3 Cement and cement product/ grout 4 Quick and hydrated lime 5 Electric cables 6 High Density Polyethylene (HDPE) and PVC

pipes

7 General lubricants 8 Re-treading tyres 9 Bolts and nuts

10 Crucibles 11 Plastic sample bags 12 Calico bags 13 Bullion boxes 14 Chain link, fencing, wire netting, barbed wire

etc

15 Conveyor rollers 16 Metal/ PVC core trays 17 Overall and work clothes 18 Haulage services 19 Catering services 20 Activated carbon* 21 Ammonium sulphate* 22 Chemicals (caustic soda)* 23 Mill liners* 24 Motor re-winding and re-furbishing* 25 Rock bolts and split-sets* 26 Steel products (plate, angles, brackets,

sprockets)*

27 Ventilation ducting* 28 Wood products* 29 Yelomine pipes*

Local Content Requirements under LI 2173 of 2012

Local content regulation: total procurement based on procurement plans and list

of 8 products (LI 2173) assessed in 2016

Based on the assessment made by the Minerals Commission in 2016, mining

companies purchased 73.3% of the initial 8 products listed on Regulation LI 2173

from “local” sources. However, when calculated against the total purchases

made, this was equivalent to only 8.4% (if fuel is incl) and 14.5% without fuel

Source: Minerals Commission, 2016

Product

2015 Total

procurement

(US$)

2015 Total local

procurement (US$)

2015 2015 True local

procurement

(US$)

2015 % True local

% local

1. Grinding Media 62,3 28,13 45,2 17,89 63,6

2. Heavy duty electrical cables 1,35 0,95 70,4 0,49 36.1

3. HDPE/PVC pipes 9,77 9,75 99,8 9,73 86.7

4. General lubricants 11,22 10,93 97,4 10,93 50.1

5. Quick/ hydrated lime 21,81 21,81 100,0 21,81 100

6. Tyre re-treading 0,75 0,75 100,0 0,75 100

7. Explosives 63,29 63,29 100,0 63,3 100

8. Cement 0,77 0,77 100,0 0,77 100

Total (8 items on LI 2172, 2015) 171,25 136,38 79,6 125,66 73.3

Total purchases including diesel and energy, 2015 1492,9 9,1 8,4

Total Local Purchases (excl. Diesel & Electric Power) 865,6 15,8 14,5

What prevents local sourcing?

• Reliability of supply and quality of manufactured inputs listed as KEY CONSTRAINT to sourcing higher value goods locally.

• ECA (2013): local sourcing accounted for 67-79% of total spending by three largest gold mining firms, BUT this does not reflect value addition or domestic ownership.

• ACET (2015): 20% of spending by mining firms went to local procurement, but figure does not reflect ownership of suppliers.

• These issues persist regardless of commodity prices, need for change in approach as per the AMV.

Opportunities for Local Production

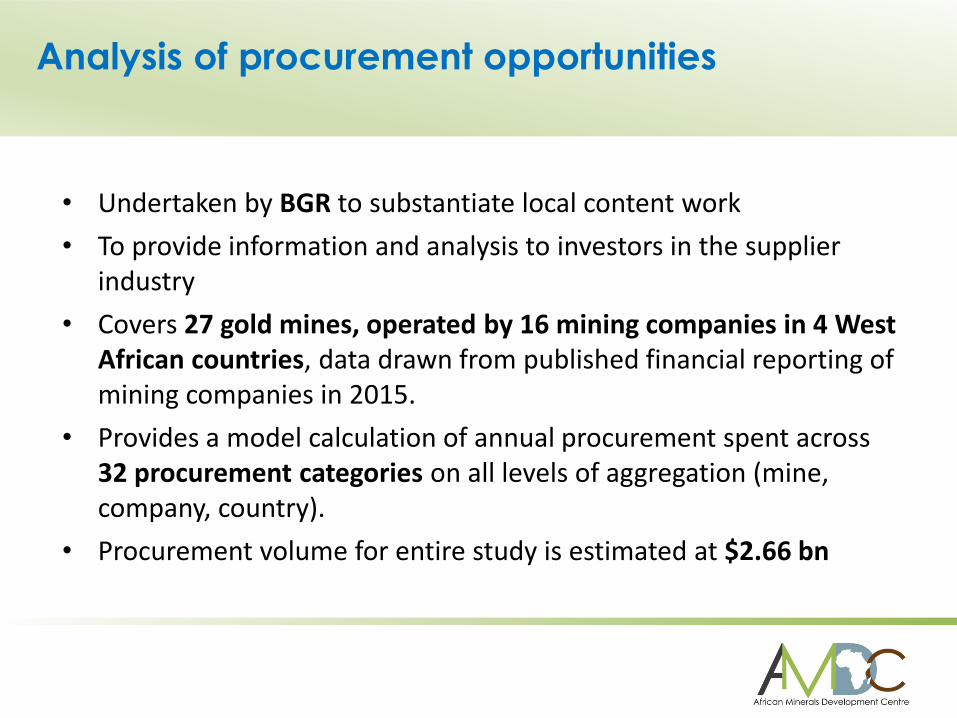

Analysis of procurement opportunities

• Undertaken by BGR to substantiate local content work

• To provide information and analysis to investors in the supplier industry

• Covers 27 gold mines, operated by 16 mining companies in 4 West African countries, data drawn from published financial reporting of mining companies in 2015.

• Provides a model calculation of annual procurement spent across 32 procurement categories on all levels of aggregation (mine, company, country).

• Procurement volume for entire study is estimated at $2.66 bn

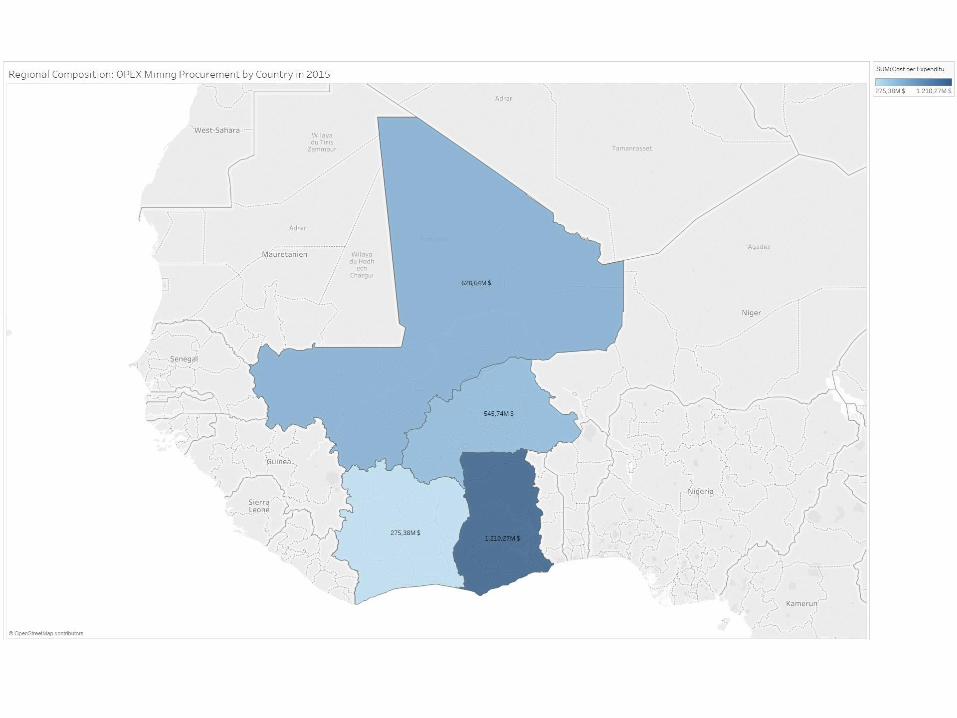

Local procurement opportunities are significant

.00 20.00 40.00 60.00 80.00 100.00 120.00 140.00 160.00 180.00

Fuel and lubricants - power

Other reagents

Fuel and lubricants - mining

Spare parts and opex equipment

Grinding media

Electricity

Explosives and accessories

Lime

Tyres

Geological and exploration services

Supply chain services

Analysis and testing

Environmental services

Equipment & Plant maintenance & repair

Safety and protective equipment

Site related services

Drilling equipment and services

Food and beverages

Construction, and related materials and services

Electrical equipment and supplies

Exploration consumables

Equipment rental

Feasibility, design and engineering

Corporate / Admin services

Telecommunications

Water services (including general waste management)

Personnel related services

Office supplies and equipment

Electronic equipment and supplies

General maintenance & repair

Camp / site supplies

Total procurement by top categories for Ghana, 2015, US$ million

Source: BGR Procurement Model

Spatial and Regional Potential

Mineral-industrial cluster to spur value chains

• Significant opportunities in geographical and sectoral clusters

• Cluster – concentrated development of a set of economic activities. Can be regional- sectoral- or export-focus: SEZs, EPZs, industrial parks etc.

• Multiplier and agglomeration effects in output, productivity, employment, knowledge spillovers.

• Avenues for both upstream and downstream linkages, as per AMV

• What strategic clusters are possible, what policy interventions are needed?

• How can the NSDP help mineral-industrial clusters succeed?

Opportunity: Ghana / West Africa Mineral Supply Cluster

• A Mineral Supply Cluster can draw on our assets (mineral endowments and mining activities; existing zones) to coordinate support to suppliers.

• Overcome regional concentration: manufacturing less distributed geographically than minerals – ie Ghana mainly around major cities (i.e. 25% of manufacturing in greater Accra, 25% in Ashanti).

• Mineral Supply Cluster to support industrialization initiatives – One District One Factory, etc.

• Ensure that establishment of factories based on: existing business environment, past industrialization efforts, resource endowments, human capital, connectivity to other districts, regions and countries.

• Link export-oriented nature of existing zones domestically

Regional Opportunities

• ECOWAS – 15 country and over $700 billion GDP region.

• Regional role of some clusters/zones (Suame manufacturing cluster)

• Region’s imports feature many manufactures / industrial goods.

• Cluster to help reach minimum threshold for efficiency (aluminum, steel etc)

• Joint ventures with other West African firms

• Capitalize on emerging and increasing mineral producers’ growing supply needs (Nigeria)

• Re-think on how ROOs, regional trade and industrial policy rules can fit in to and enhance cluster strategy

Challenges and Policy Recommendations

Overall Policy Landscape and constraints

• Mining and even industry framework too focused on rent maximisation, insufficient emphasis on supply chain development and broader linkages with other economic sectors

• Currently key policy is Local Content – needed but not sufficient – there is still very little to show in terms of value addition.

• A number of supply-side constraints became apparent

• Insufficient policy coherence, coordination and consistency (e.g. duty exemptions for inputs; Free Zone cap on domestic supply; capital requirements on foreign investment seems to limit FDI or JVs with local firms; etc. )

• No systematic approach to or strategy to reinforce industrial capacity and capacity of service providers.

Industry and even manufacturing still commodity-driven

Industrial value-added growth Manufacturing value-added growth

0

5

10

15

20

25

30

35

40

45

2007 2008 2009 2010 2011 2012 2013 2014 2015

Gro

wth

rat

e (%

)

-5

0

5

10

15

20

2007 2008 2009 2010 2011 2012 2013 2014 2015G

row

th r

ate

(%)

Improving the business climate and opportunities

for local firms

• Firms face barriers including administrative procedures; latent levels of

infrastructure particularly energy, transport; etc.

• Need to address these competitiveness and cost-of-doing-business

challenges, to reach small local firms with significant potential.

• Pursue beneficial state-business relations and collaborative partnerships,

including within private sector between local buyers and sellers.

• Properly harness Local Content – address challenges facing local suppliers,

entrenched interests etc. and revise it to be comprehensive across the

region.

Expanding and enriching the local market

• Pursue market opportunities as modeled by BGR

• Harness regional opportunities – market size matters.

• Need upstream mining supply chains to go beyond the mining sector.

• Link policy with industrialization of region and individual countries

including devising means for IP implementation.

• Also strategic interventions in aluminium, petrochemicals, iron and

steel, salt etc.

Boosting skills to stimulate value addition across

sectors

• A highly educated workforce is important to ensure proper technology and

knowledge transfers and spillovers.

• Yet labour productivity remains low by international standards. Skills

mismatches impact on the absorptive capacity of the supply chain. The quality

of the workforce is a major challenge

Options to address this:

• Comprehensive cross-sector skills development programme and

competitiveness and productivity council

• Assessment of capabilities and skills gaps

• Link TVET better with needs of future activities, orient towards STEM fields

• Facilitate movement of professionals across region

• Boost R&D, improve climate for innovation

Potential impact

• A regional economy both taking advantage of naturally occurring linkages and directly promoting new linkages between the mineral sector and economy at large

• Several suppliers serving the national and ECOWAS markets

• More firms and activities which feed into existing Free Zones and other clustering initiatives

• Job creation in higher-value fields

• A strengthened institutional structure supporting cross-discipline policy making across Ministries and other stakeholders

• Success in tandem with goals for broad, cross-sector industrialization

Thank You!