building a sustainable business at us$1,300/oz gold price

TRANSCRIPT

Building a Sustainable Business At US$1,300/oz Gold Price

Denver Gold Forum Nick Holland

16 September 2014

2

Forward looking statements

Certain statements in this document constitute “forward looking statements” within the meaning of Section 27A of the US Securities Act of

1933 and Section 21E of the US Securities Exchange Act of 1934.

In particular, the forward looking statements in this document include among others those relating to the Damang Exploration Target

Statement; the Far Southeast Exploration Target Statement; commodity prices; demand for gold and other metals and minerals; interest

rate expectations; exploration and production costs; levels of expected production; Gold Fields’ growth pipeline; levels and expected

benefits of current and planned capital expenditures; future reserve, resource and other mineralisation levels; and the extent of cost

efficiencies and savings to be achieved. Such forward looking statements involve known and unknown risks, uncertainties and other

important factors that could cause the actual results, performance or achievements of the company to be materially different from the future

results, performance or achievements expressed or implied by such forward looking statements. Such risks, uncertainties and other

important factors include among others: economic, business and political conditions in South Africa, Ghana, Australia, Peru and elsewhere;

the ability to achieve anticipated efficiencies and other cost savings in connection with past and future acquisitions, exploration and

development activities; decreases in the market price of gold and/or copper; hazards associated with underground and surface gold mining;

labour disruptions; availability terms and deployment of capital or credit; changes in government regulations, particularly taxation and

environmental regulations; and new legislation affecting mining and mineral rights; changes in exchange rates; currency devaluations; the

availability and cost of raw and finished materials; the cost of energy and water; inflation and other macro-economic factors, industrial

action, temporary stoppages of mines for safety and unplanned maintenance reasons; and the impact of the AIDS and other occupational

health risks experienced by Gold Fields’ employees.

These forward looking statements speak only as of the date of this document. Gold Fields undertakes no obligation to update publicly or

release any revisions to these forward looking statements to reflect events or circumstances after the date of this document or to reflect the

occurrence of unanticipated events.

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

3

The Transformation of Gold Fields

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

The Journey Started With The Speech To The Melbourne Mining Club

Building A Sustainable Business At US$1,300/oz

What Investors Want

Aug 2012

Portfolio Review

Aug - Dec 2012

Sibanye Gold

Dec - Jan 2012

New Cash Strategy

2013 Business PlanA New Paradigm

15 April 2013

Gold Price

< US$1,300/oz

A Fundamental Shift In Strategy

Focus on free cash flow and growing the margin

“It’s all about cash – not ounces for the sake of ounces”

4

The Transformation of Gold Fields

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Six Strategic Themes

Focus on Total Shareholder Returns

>15% Free Cash Flow Margin at US$1,300/oz Gold

Underway

Underway

Commitments Made On 22 August 2013

1. Focus on free cash flow

Structural shift in cost base

>15% free cash flow at a US$1,300/oz gold price

No marginal mining, no high-grading, maintain cut-off grades

Protect sustainability of ore bodies by investing in development and stripping

2. Reboot and deliver South Deep

3. Drive brownfields exploration

4. No greenfields exploration & projects and divest

non-core assets

5. Strengthen balance sheet

6. Pay dividends

5

451,000

496,000

598,000

557,000 548,000

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

US

$/o

z

Ounces

Production and Costs

Gold Produced Gold Price AIC

The Transformation of Gold Fields

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

AIC Down 30% from US$1,572/oz (Q2 13) to US$1,093/oz (Q2 14)

A Sustainable, Structural Shift In The Cost Base

6

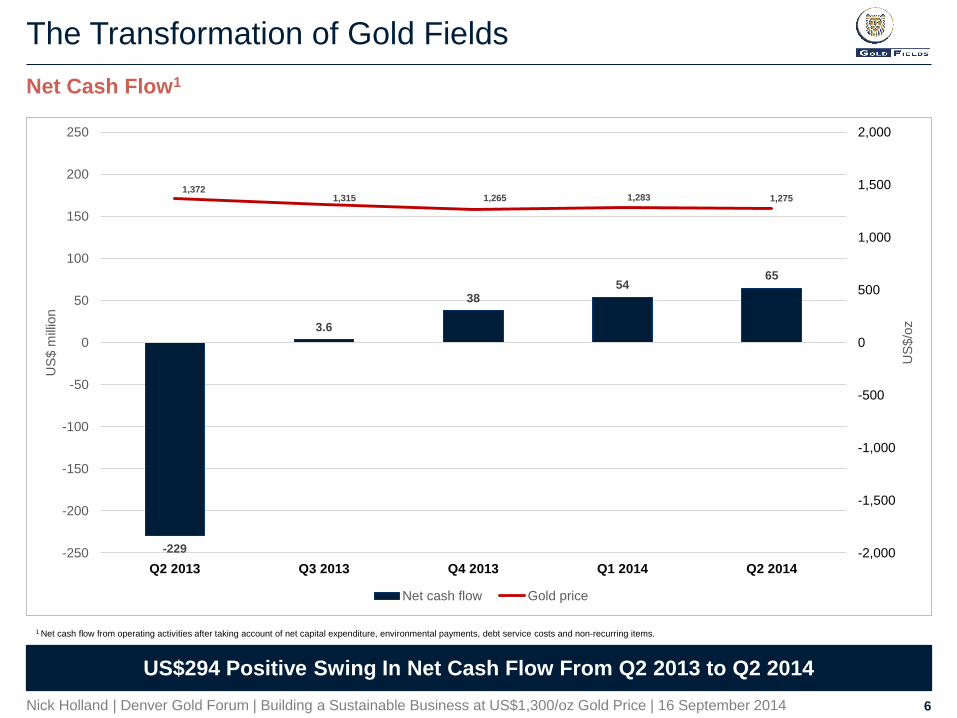

The Transformation of Gold Fields

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Net Cash Flow1

US$294 Positive Swing In Net Cash Flow From Q2 2013 to Q2 2014

-229

3.6

3854

65

1,3721,315 1,265 1,283 1,275

-2,000

-1,500

-1,000

-500

0

500

1,000

1,500

2,000

-250

-200

-150

-100

-50

0

50

100

150

200

250

Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014

US

$/o

z

US

$ m

illio

n

Net cash flow Gold price

1 Net cash flow from operating activities after taking account of net capital expenditure, environmental payments, debt service costs and non-recurring items.

7

The Transformation of Gold Fields

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Creating Value Through Corporate Restructuring (Announced 29 November 2012)

+47% TSR Despite 26% Fall In Gold Price

Source: Bloomberg

47%

-20%-26% -30%

-40% -43% -45%-55% -55%

-61% -61%-80%

-60%

-40%

-20%

0%

20%

40%

60%

GFI & SibanyeCombined

Randgold Goldcorp Agnico Eagle Newmont Anglogold Barrick Yamana Newcrest Harmony Kinross

Total Shareholder Returns28 November 2012 to 3 September 2014

1,000

1,100

1,200

1,300

1,400

1,500

1,600

1,700

1,800

Gold Price28 November 2012 to 3 September 2014

28 Nov 2012

US$1,719.69/oz

3 Sep 2014

US$1,269.40/oz

8

The Transformation of Gold Fields

● H1 2014 - Net debt reduced by US$100m to US$1,635m

● Net Debt to EBITDA reduced to 1.47X1

● Maturity date on US$715m of debt extended, on same terms, from November 2015 to

November 2017

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Balance Sheet Further Strengthened

If We Make The Earnings, We Will Pay The Dividend

1 12-month rolling historical average

H1 2014 Dividend

● ZAR0.20 per share

● In line with dividend policy of paying out 25% to 35% of normalised earnings

Targeting Net Debt To EBITDA of 1X

9

The Transformation of Gold Fields

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Active Portfolio Management

Re-invest Proceeds in Debt Reduction or Value Adding Acquisitions

Woodjam

British Columbia

“The wrong metal”

Asosa

Ethiopia

“The wrong address”

Yanfolila

Mali

“Franchise / hurdle rates”

Royalty

Portfolio

“Value release”

Talas

Kyrgysztan

“The wrong address”

Arctic Platinum Project

Finland

“The wrong metal”

Chucapaca

Peru

“Franchise / hurdle rates”Salares Norte

Chile

“Great optionality”

FSE

Phillippines

“Great optionality”

Sold

Disposal Underway

Retain

10

The Transformation of Gold Fields

● Short term bonus (Annual)

Based on Board approved annual operational plans and targets

Includes parameters for operational sustainability

● Long term bonus (Three year cycle)

Cash rather than shares ensures no shareholder dilution

Introduces downside – if threshold is not achieved, no bonus

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Alignment of Executive and Senior Management Incentives With Shareholders

If Shareholders Win We Win, If Shareholders Lose, We Lose

Free

Cash Flow

Total

Shareholder

Returns

15% Free Cash Flow

Margin

US WACC

6% Real

compounded

(Threshold)

50%

Weighting

50%

Weighting

+ = BONUS

Australia Region

12

Australia Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Gold Fields Australia: A Robust Portfolio

Targeting One Million Ounces at AIC Below US$1,050/oz

256.9

83.4 84.6

66.0

22.9

1 042

1,372

692

1,010

1,228

0

200

400

600

800

1,000

1,200

1,400

1,600

Region St Ives Granny Smith Agnew/Lawlers Darlot

0

50

100

150

200

250

300

Q2 2014 Production and AIC By Mine

Production AIC

US

$/o

z

Ko

z

13

Australia Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Yilgarn South Acquisition: Key Performance Indicators

Leverage Operational Expertise

KPI Unit GFI 9 Months ABX 9 Months Comments

Safety TRIFR 7.72 15.51 Actual injuries - 11 under GFI vs 30 under ABX

Ore Processed Kt 1,931 2,274Only mining ore that contributes to the required

margin

Head Grade g/t 6.29 5.08 As above

Gold Production Koz 367,540 341,466

All In Sustaining Cost A$/oz 982 1,243

Gold Price A$/oz 1,398 1,464

Free Cash Flow Margin % 28% 11% Efficiencies have compensated for gold price

14

RESOURCE EXTENSION &

EXPLORATION

DISCOVERY

RESOURCE

4.3 Moz

Australia Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

St Ives Gold Mine

Investment in Exploration Underpins Reserve Replacement

RESERVE

2.0 Moz • Strong endowment

• Exploration >A$25m pa

• Speedway Trend project pipeline

• Extensions to current mines

2013 2019 LoM Extension PotentialLoM

~12 Moz

produced

since 1980

● Orogenic style of mineralisation

● 127,556 ha of granted tenements with

significant exploration potential

● Circa 16 Moz discovered and 12 Moz

produced since 1980

● Significant new discoveries with potential to

extend mine life beyond 10 years

Neptune – High grade open pit - Paleoplacer

System

• Mineral Resources: 5.5mt @3.3g/t for 0.58

Moz

• Mineral Reserves: 2.9mt @ 3.4g/t for 0.32

Moz

Invincible High grade open pit and

underground >2 Moz potential

• Mineral Resources: 9.2mt @ 4.50g/t for 1.33

Moz

• Mineral Reserves: 3.7mt @ 4.09g/t for 0.49

Moz

0

5

10

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Moz Consistent Reserve Replacement History

Reserves Production Cumm Production

Optimisation Opportunities

Neptune in production in H2 2014 - expected to underpin improved

H2 2014

Invincible in production in H1 2015 – consolidate open pit mining

in one higher grade pit

Fast-track exploration of Invincible and Speedway Trend for life

extension

15

Australia Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Agnew / Lawlers Gold Mine

A Long-Term Steady Producer With Long-Life Potential

● Orogenic style of mineralisation

● 78,547 ha of granted tenements with significant exploration

potential

● Circa 11 Moz discovered and 7 Moz produced since 1985

● Significant on-site ore reserve extension and new

exploration opportunities with potential to extend mine life

beyond 10 years

Lawlers

• Lateral extensions to the existing 200, 500, 600 and 700

series

• Repeat of horizontal lodes at depth

• Hidden Secret underexplored

Agnew

• New discoveries in FBH and Link Drive area between

Kim and FBH

• Kath, Waroonga North,

• Depth and lateral exploration opportunities in all

directions

Optimisation Opportunities

High grade FBH and Link Drive area to underpin 2015 plan

Shallower Kath and Waroonga North opportunities fast-tracked

Cinderella “boundary pillar” between Agnew and Lawlers not

explored

0

0.5

1

1.5

2

2.5

3

3.5

4

F2001 F2002 F2003 F2004 F2005 F2006 F2007 F2008 F2009 F2010 F2011 F2012 F2013

Millio

n O

un

ce

s

Reserves and Production

Reserves Production Cumulative Production

RESOURCE EXTENSION &

EXPLORATION

DISCOVERY

RESOURCE

3.66 Moz

RESERVE

0.95 Moz

• Extensive exploration pipeline

across combined land package

• Resource growth targeted at

600/700 Series, Kath, Hidden

Secret & Cinderella

• New FBH-Link model to drive 2015

planning

2013 2019 LoM Extension PotentialLoM

~7 Moz

produced

since 1985

16

Australia Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 20147

Granny Smith Gold Mine

A Great Address for Significant Discoveries

● Orogenic style of mineralisation

● 61,774 ha of granted tenements with significant exploration

potential

● >20 Moz mined in the Laverton region including ~ 2.5 Moz

from Grannny Smith, ~ 8 Moz from Wallaby and ~10 Moz

from Sunrise

● Significant on-site ore reserve extension and new

exploration opportunities with potential to extend mine life

beyond 15 years

Wallaby Underground

• Horizontal lenses repeat at depth with higher grades

Lake Carey under-explored

• 2 World Class deposits on the margin of Lake Carey

- Wallaby and Sunrise Dam – analogue for Lake Le

Froy at St Ives

• No significant or systematic exploration since 2005

Large tenement position with multiple targets

Optimisation Opportunities

Wallaby resource conversion and exploration at depth

Improved extraction ratio through potential use of paste fill

CIL plant under-utilised – 50% upside

RESOURCE EXTENSION &

EXPLORATION

DISCOVERY

RESOURCE

3.3 Moz

RESERVE

0.8 Moz • Extensions to Wallaby footprint

• System potential down to Z150

• District exploration gaining traction

• New gravity circuit in 2014

2013 2020 LoM Extension PotentialLoM

~7 Moz

produced

since 1989

West Africa Region

18

West Africa Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Gold Fields Ghana: Significant Potential Beyond Current Resource Life

Targeting One Million Ounces at AIC Below US$1,000/oz

181.3

140.7

40.5

1,0841,026

1,282

0

200

400

600

800

1,000

1,200

1,400

Region Tarkwa Damang

0

20

40

60

80

100

120

140

160

180

200

Q2 2014 Production and AIC By Mine

Production AIC

US

$/o

zKo

z

19

West Africa Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Tarkwa Gold Mine

A Gold Fields Franchise Asset Generating Significant Cash

● Wits Style Paleoplacer mineralisation

● 20,825 ha of granted tenements with significant

exploration potential at existing pits and on-site

● Significant on-site ore reserve extension and new

exploration opportunities with potential to extend

mine life beyond 15 years

Upside potential in current pits

• Last drilled at a gold price of circa

US$400/oz

Hydrothermal overlay on property

• Significant exploration targets

Reserve upside resulting from structural cost

reduction

Optimisation Opportunities

Optimisation of Mill from 12 Mtpa to +13 Mtpa by early 2015

PPA agreement with independent third party

Teberebie pillar expansion (AGA ground exchange)

RESOURCE EXTENSION &

EXPLORATION

DISCOVERY

RESOURCE

10.3 Moz

RESERVE

7.3 Moz• Very well understood ore bodies

• Exploration expanding beyond

Resource conversion

• District soil sampling project

• Blue Ridge exploration potential

2013 2030 LoM Extension PotentialLoM

~9.4 Moz

produced

since 1997

20

West Africa Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Damang Gold Mine

Returning to Profitability, Targeting >15% Free Cash Flow Margin

● Hydrothermal Paleoplacer mineralisation

● 25,016 ha of granted tenements

● Significant exploration potential on 30 km strike

length between Tarkwa and Damang

● Upside potential at historic satellite pits last mined

at a gold price of circa US$400/oz

Optimisation Opportunities Underway

Significant reserve upside - exploration focus on 30 km strike

Improved plant availability, reduced dilution, recoveries and

throughput

RESOURCE EXTENSION &

EXPLORATION

DISCOVERY

RESOURCE

6.6 Moz

RESERVE

1.1 Moz • Exploration aligned to turnaround

strategy

• Extensions to active pits

• Targeting high grade hydrothermal

prospects

2013 2019 LoM Extension PotentialLoM

~4.03 Moz

produced

since 1997

South America Region

22

South America Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Cerro Corona Copper/Gold Mine

The Most Profitable Mine In The Group

● Cu/Au porphyry mineralisation

● 2,765 ha of mining concession

● Continued outperformance against resource model

● Upgrades to the crushing facility positively

impacting throughput of increasingly harder ore

Optimisation Opportunities Underway

Future capital reduced through cancellation of TSF raise and

review of cheaper alternatives

Potential to increase reserves by ~ 30% through TSF and WSF

optionality

RESOURCE EXTENSION &

EXPLORATION

DISCOVERY

RESOURCE

3.3 Moz Au

1,124 Mlb CuRESERVE

2.0 Moz Au

712 Mlb Cu

2013 2023 LoM Extension PotentialLoM

~2.0 Moz

Au eq produced

since 2008

• 2014 re-logging project to

better define Geo-metallurgy

• Upgraded crushing facility

• TSF options being assessed

to increase LoM footprint

South Africa Region

24

South Africa Region

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

South Deep Project

Positioning The Mine For Success in the Medium Term

Steady state production: 650 Koz to 700 Koz p.a.@ AIC of

US$900/oz by the end of 2017

Destress Step Change

Improved Productivity

Operator & Technician Skills

Fleet Availability & Utilisation

Ore Handling Infrastructure

● Ground Support Programme

Affected majority of production and destress areas

Commenced mid-May

Completed end-September

Expected to provide stability for life-of-mine

● Critical interventions fast-tracked

Labour refresher training

Machine maintenance

● Initial review of destress mining method underway – pilot

projects being mobilised

● Long-term build-up plan remains in place

● Cash break-even expected in H1 2015

RESOURCE EXTENSION &

EXPLORATION

DISCOVERY

RESOURCE

76.2 Moz

RESERVE

38.2 Moz

• Massive, multi-layered

palaeoplacer with high

predictability

• Grade control and LIB drilling

continues to be effective

• Improved regional pillar

configuration being reviewed

• Pilot destress mining

2013 2087 LoM Extension PotentialLoM

~15 Moz

produced

since 1968

25

South Deep Project

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Reviewing The Mining Method

De-Risking The Build-Up Plan

• International Geotechnical Advisory Board (IGAB)

- Industry leading experts from across the globe

- Reviewed South Deep’s destress mining methodology over past seven months

- Two alternative mining methods identified

• Both methods piloted in areas outside current plan - Q4 2014 to Q4 2015

• Both are Single-pass systems compared to current three-pass system

1. 4x4 Metre Destress Method

- Increases dimensions of excavations from 2.2(high) X 5.0(wide) metre to 4.0(high) X 4.0(wide) metre

- Allows the use of conventional mining equipment as opposed to low profile equipment

- Alleviates logistical constraints and facilitate a fully mechanised mining process

- Interim step, pending decision on the Inclined Slot Method

2. Inclined Slot Method

- Entirely removes the need for conventional destress mining as destress is inherent in the new mining design

- Potential to de-risk build-up plan and future production

Conclusions

27

Conclusions

Nick Holland | Denver Gold Forum | Building a Sustainable Business at US$1,300/oz Gold Price | 16 September 2014

Its All About Cash!

1. Focus on free cash flow

Structural shift in cost base

>15% free cash flow at a US$1,300/oz gold price

No marginal mining, no high-grading, maintain cut-off grades

Protect sustainability of ore bodies by investing in development and stripping

2. Reboot and deliver South Deep

3. Drive brownfields exploration

4. No greenfields exploration & projects and divest non-core assets

5. Strengthen balance sheet

6. Pay dividends

Building a Sustainable Business At US$1,300/oz Gold Price

Denver Gold Forum Nick Holland

16 September 2014