building a financial plan: theory and case

TRANSCRIPT

GOVERNANCE AND ACCOUNTING IN SMES

PROF. ENRICO BRACCI

Lecture 3-BisBuilding a Financial Plan: theory and case

2Prof. Enrico Bracci Basic financial accounting

Research shows:

A significant positive relationship exists between

formal planning in small companies and their

financial performances

But, significant numbers of entrepreneurs run

their companies without any kind of financial plan!

Financial planning and forecasting

3Prof. Enrico Bracci Basic financial accounting

Planning in its general sense is the act of

quantifying objectives in financial terms:

It assists managers in decision making process in

an organization

It acts as a communication tool

It motivates people to run towards goals

Role of planning and forecasting

4Prof. Enrico Bracci Basic financial accounting

Projected financial statements answer questions such as:

What profit can the business expect to earn?

If the founder’s profit objective is xxx€, what sales level

must the business achieve?

What fixed and variable expenses can the owner expect

at that level of sales?

They estimate the profitability and the overall financial

condition of the business in the immediate future

They are an integral part of convincing potential lenders

and investors to provide the financing needed to get the

company off the ground or to expand

Creating Projected (or pro-forma) Financial Statements

5Prof. Enrico Bracci Basic financial accounting

Creating Projected Financial Statements: an overview

Foundation for financial forecast- Business model , marketing analysis and forecast- Business model assumptions

Forecast (Pro forma) financial elememts

Cash flow forecast- From operations- From investing- From exernal sources of financing

Projected start-up capital requirements

Forecast revenue

Forecast expenses

Financing plan(Sources of funds)

Forecasted balance sheet

Current assetsFixed assetsTotal assets

LiabiltiesOwners’ equity

Total Liabilities & OE

Forecasted incomestatement

SalesExpenses

DepreciationOperating income

InterestTaxes

Net Income

6Prof. Enrico Bracci Basic financial accounting

Building a financial plan

Case and solution

Case study

7Prof. Enrico Bracci 7 Basic financial accounting

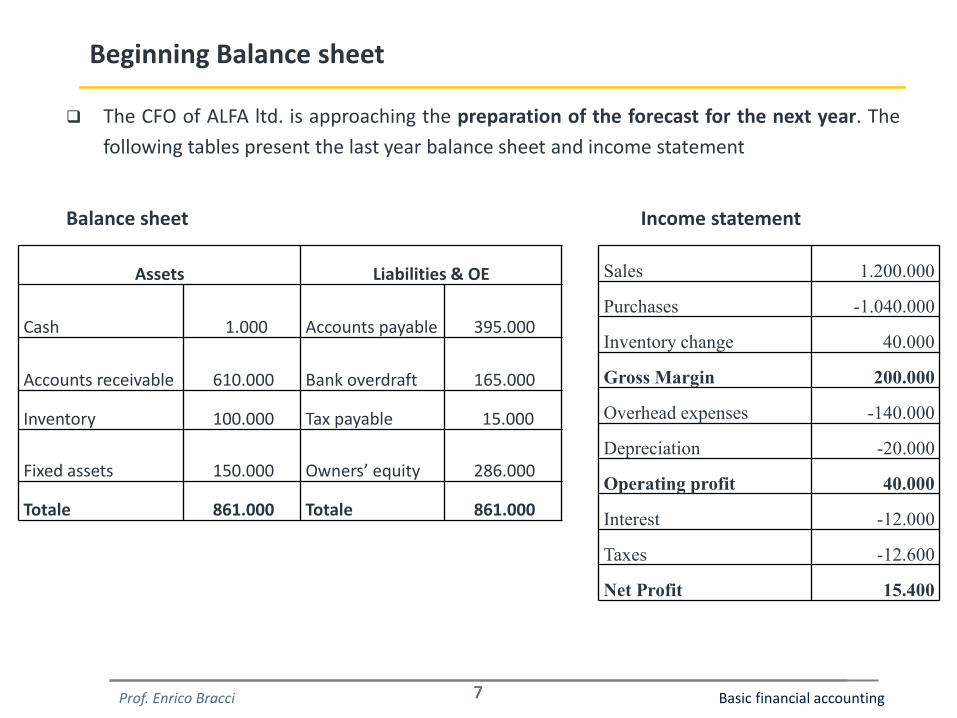

Beginning Balance sheet

The CFO of ALFA ltd. is approaching the preparation of the forecast for the next year. The

following tables present the last year balance sheet and income statement

Balance sheet Income statement

Assets Liabilities & OE

Cash 1.000 Accounts payable 395.000

Accounts receivable 610.000 Bank overdraft 165.000

Inventory 100.000 Tax payable 15.000

Fixed assets 150.000 Owners’ equity 286.000

Totale 861.000 Totale 861.000

Sales 1.200.000

Purchases -1.040.000

Inventory change 40.000

Gross Margin 200.000

Overhead expenses -140.000

Depreciation -20.000

Operating profit 40.000

Interest -12.000

Taxes -12.600

Net Profit 15.400

8Prof. Enrico Bracci 8Prof. Enrico Bracci Basic financial accounting

Hypothesis

Sales forecasted 1.500.000

COGS as % of sales 83,333%

Inventory period ratio 35,3 days

Overhead expenses 180.000

Depreciation 20.000

Collection period ratio 90 days

Payment period ratio 60 days

Interest rate on loan 6%

payed in December

considering the average bank

position expected

Tax rate 45%

Non-current expenses (in June t+1) 500

End of period Cash 1.000

Month of tax payment June

Sales and expenditure equally distributed along the year

COGS = Purchases + Beginning inventory – ending inventory

Purchases= COGS- Beginning Inventory + Ending InventoryEnding inventory= (COGS/360) x Inventory period ratio in days

Accounts receivable = (Sales/360) x Collection period ratio in days

Accounts paybale = (Purchases/360) x Payment period ratio in days

9Prof. Enrico Bracci 9 Basic financial accounting

Preparation of the forecast : steps

Considering the various hypothesis given students are required to prepare for the next year:

1) Income statement;

2) Balance sheet;

3) Monthly cash flow statement.

10Prof. Enrico Bracci 10Prof. Enrico Bracci Basic financial accounting

Income statement

We need to estimate the interestbefore closing the IS

According to the HypothesisSales 1.500.000

We use the combined equations of COGS and Ending InventoryPurchases= COGS- Beginning Inventory + Ending InventoryEnding Inventory = (COGS/360) x Inventory turnover in daysSubstituting:COGS= (1.500.000*83,33%)= 1.250.000Ending inventory = (1.250.000/360) x 35,3 = 122.569Purchases= 1.250.000-100.000+122.569Inventory change = 22.569

Purchases 1.272.569 -

Inventory change 22.569

Gross Margin 250.000

Overhead expenses 180.000 -

Depreciation 20.000 -

Operating profit 50.000

Non current expense 500 -

Interest

Profit before taxes

Taxes

Net Profit

11Prof. Enrico Bracci 11Prof. Enrico Bracci Basic financial accounting

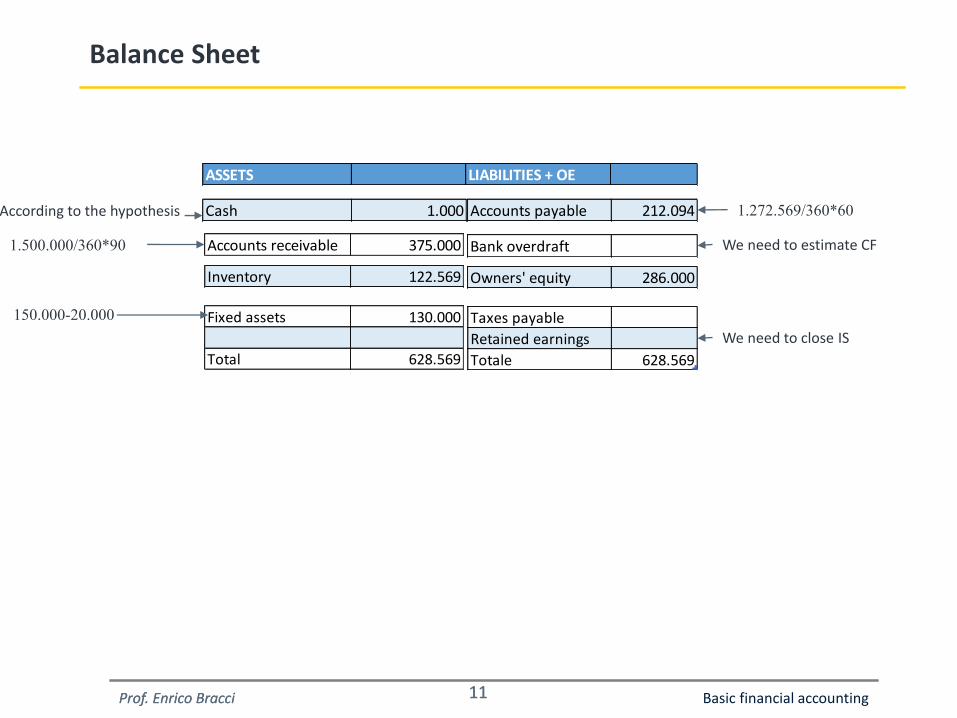

Balance Sheet

ASSETS LIABILITIES + OE

Cash 1.000According to the hypothesis

Accounts receivable 375.0001.500.000/360*90

Inventory 122.569

150.000-20.000

Accounts payable 212.094 1.272.569/360*60

Bank overdraft We need to estimate CF

Owners' equity 286.000

Fixed assets 130.000

Total 628.569

Taxes payable

Retained earnings

Totale 628.569

We need to close IS

12Prof. Enrico Bracci 12Prof. Enrico Bracci Basic financial accounting

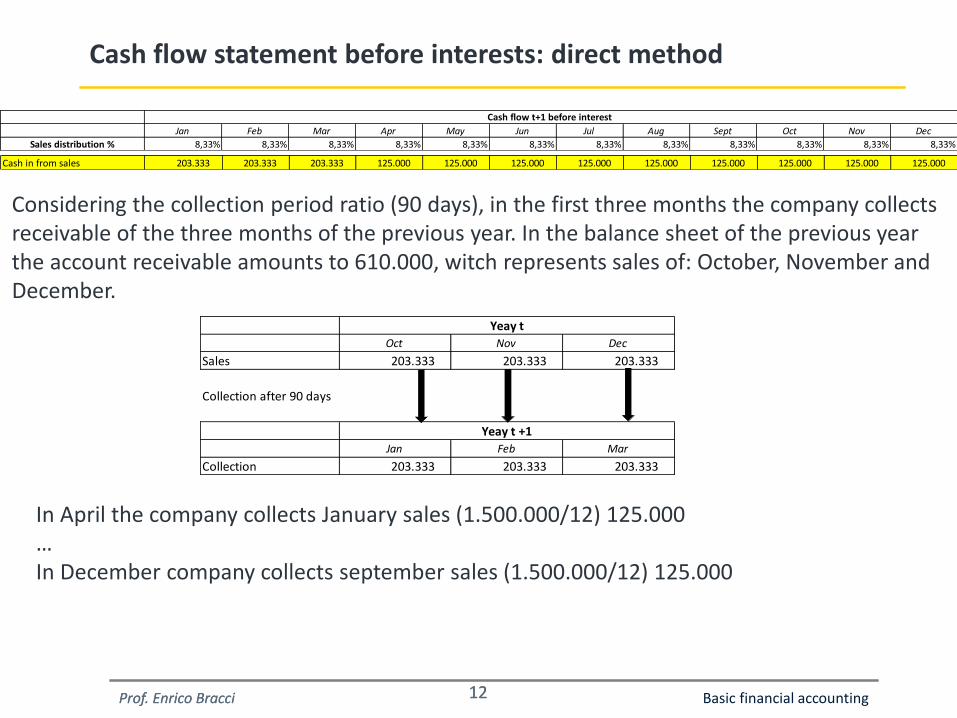

Cash flow statement before interests: direct method

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec

Sales distribution % 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33%

Cash flow t+1 before interest

Considering the collection period ratio (90 days), in the first three months the company collects receivable of the three months of the previous year. In the balance sheet of the previous year the account receivable amounts to 610.000, witch represents sales of: October, November and December.

Oct Nov Dec

Sales 203.333 203.333 203.333

Collection after 90 days

Jan Feb Mar

Collection 203.333 203.333 203.333

Yeay t

Yeay t +1

In April the company collects January sales (1.500.000/12) 125.000…In December company collects september sales (1.500.000/12) 125.000

Cash in from sales 203.333 203.333 203.333 125.000 125.000 125.000 125.000 125.000 125.000 125.000 125.000 125.000

13Prof. Enrico Bracci 13Prof. Enrico Bracci Basic financial accounting

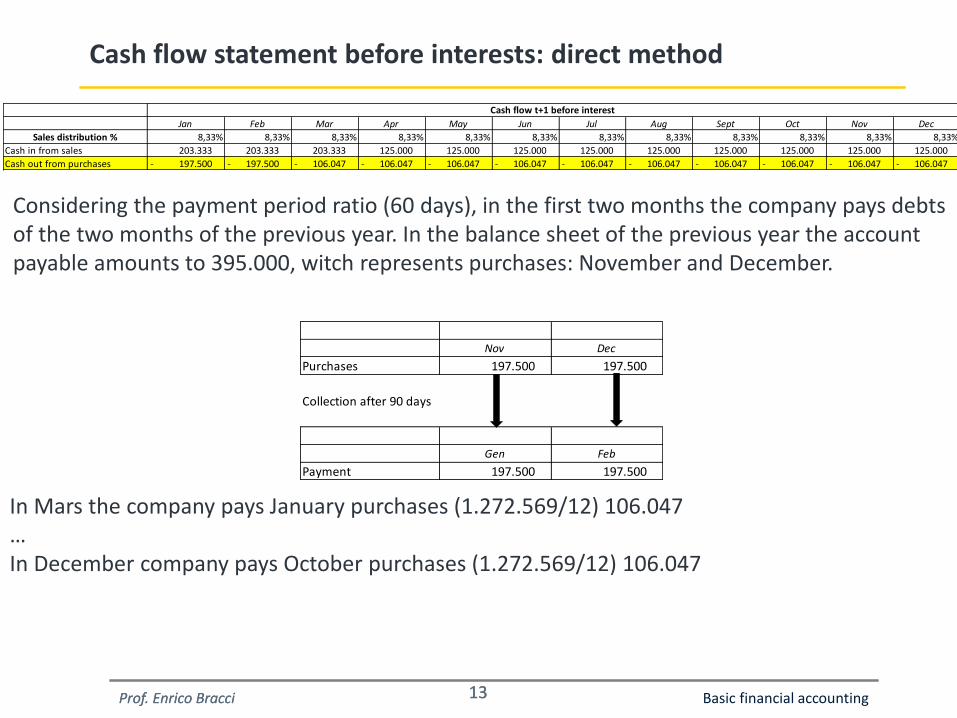

Cash flow statement before interests: direct method

Considering the payment period ratio (60 days), in the first two months the company pays debts of the two months of the previous year. In the balance sheet of the previous year the account payable amounts to 395.000, witch represents purchases: November and December.

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec

Sales distribution % 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33%

Cash in from sales 203.333 203.333 203.333 125.000 125.000 125.000 125.000 125.000 125.000 125.000 125.000 125.000

Cash out from purchases 197.500 - 197.500 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 -

Cash flow t+1 before interest

Nov Dec

Purchases 197.500 197.500

Collection after 90 days

Gen Feb

Payment 197.500 197.500

In Mars the company pays January purchases (1.272.569/12) 106.047…In December company pays October purchases (1.272.569/12) 106.047

14Prof. Enrico Bracci 14Prof. Enrico Bracci Basic financial accounting

Cash flow statement before interests: direct method

Now it is possible to compute the interests considering the average bank position expected:Interest = (165.000+80.975)/2 x 6% = €7.379,14

Overhead 15.000 (180.000/12) per month;In June the company pays the previous year's taxes and extraordinary expenses

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec

Sales distribution % 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33% 8,33%

Cash in from sales 203.333 203.333 203.333 125.000 125.000 125.000 125.000 125.000 125.000 125.000 125.000 125.000

Cash out from purchases 197.500 - 197.500 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 - 106.047 -

Cash out from overhead 15.000 - 15.000 - 15.000 - 15.000 - 15.000 - 15.000 - 15.000 - 15.000 - 15.000 - 15.000 - 15.000 - 15.000 -

Cash flow from operations 9.167 - 9.167 - 82.286 3.953 3.953 3.953 3.953 3.953 3.953 3.953 3.953 3.953

Taxes -15.000

Extraordinary expenses -500

Beginning bank balance -165.000 174.167 - 183.333 - 101.047 - 97.095 - 93.142 - 104.690 - 100.737 - 96.785 - 92.832 - 88.880 - 84.927 -

Ending bank balance 174.167 - 183.333 - 101.047 - 97.095 - 93.142 - 104.690 - 100.737 - 96.785 - 92.832 - 88.880 - 84.927 - 80.975 -

Cash flow t+1 before interest

15Prof. Enrico Bracci 15Prof. Enrico Bracci Basic financial accounting

Cash flow statement considering interests: direct method

Interests are payed in december

Cash flow t+1

Jan Feb Mar Apr May Jun Jul Aug Sept Oct Nov Dec

Sales distribution % 8.33% 8.33% 8.33% 8.33% 8.33% 8.33% 8.33% 8.33% 8.33% 8.33% 8.33% 8.33%

Cash in from sales 203,333 203,333 203,333 125,000 125,000 125,000 125,000 125,000 125,000 125,000 125,000 125,000

Cash out from purchases - 197,500 - 197,500 - 106,047 - 106,047 - 106,047 - 106,047 - 106,047 - 106,047 - 106,047 - 106,047 - 106,047 - 106,047

Cash out from overhead - 15,000 - 15,000 - 15,000 - 15,000 - 15,000 - 15,000 - 15,000 - 15,000 - 15,000 - 15,000 - 15,000 - 15,000

Cash flow from operations - 9,167 - 9,167 82,286 3,953 3,953 3,953 3,953 3,953 3,953 3,953 3,953 3,953

Taxes -15,000

Extraordinary expenses -500

Interest - 7,379

Beginning bank balance -165,000 - 174,167 - 183,333 - 101,047 - 97,095 - 93,142 - 104,690 - 100,737 - 96,785 - 92,832 - 88,880 - 84,927

Ending bank balance - 174,167 - 183,333 - 101,047 - 97,095 - 93,142 - 104,690 - 100,737 - 96,785 - 92,832 - 88,880 - 84,927 - 88,354

16Prof. Enrico Bracci 16 Basic financial accounting

Income statement

From cash flow

Taxes rate 45%

Sales 1,500,000

Purchases - 1,272,569

Inventory change 22,569

Gross Margin 250,000

Overhead expenses - 180,000

Depreciation - 20,000

Operating profit 50,000

Non current expense - 500

Interest - 7,379

Profit before taxes 42,121

Taxes - 18,954

Net Profit 23,166

17Prof. Enrico Bracci 17 Basic financial accounting

Balance Sheet

From cash flow statement

From income statement

From income statement

ASSETS LIABILITIES + OE

Cash 1,000 Accounts payable 212,095

Accounts receivable 375,000 Bank overdraft 88,354

Inventory 122,569 Owners' equity 286,000

Fixed assets 130,000 Taxes payable 18,954

Retained earnings 23,166

Total 628,569 Totale 628,569