budgeting procedures and economic performance in eu hagen

TRANSCRIPT

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 1/85

BCN ICHPBRSCOMMISSIOII OF THE EUROPEAIT COMMUTTITIES O DIBECTORATE-GEITERAT FOR ECOTTOMIC AilO FIIIAITCIAI

AIFAIRS

Number 96 October 1992

pudgeting Proceduresand Fiscal Performance

in the European Communities

J0rgen von Hagen*

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 2/85

Economic Papers are written by the Staff of the Directorate-General for Economic and Financial Affairs, or by expertsworking in association with them. The Papers are intended toincrease awareness of the technical work being done by the staffand to seek comments and suggesfions for f urther analyses.They may not be quoted without authorisation. Views expressedrepresent exclusively the positions of the author and do notnecessa rily correspond with those of the Commission of theEuropean Communities. Comments and enquiries shou/d beaddress ed to:

The Directorate-General for Economic and Financial Affairs,

Commission of the European Communities,200, rue de la Loi1 049 B russe ls, Be lg i u m

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 3/85

336 1tJ 3

~ ·ECONOMIC P PERS ~ ?

Number9 October 1992

jJudgeting Proceduresand Fiscal Performance

n the European Communities

Jiirgen von Hagen

• University ofMan nheim .Ind iana University School ofBusi ness, and CEPR

This research was supportedy

the Commissionof

European Communities. The views expressed inthis paper are those of the author and do not reflect views of the Commission of the EuropeanCommunities. Helpful comments by Michele Fratianni and Suzanne Lohmann are gratefully acknowledged.

11/453/92-ENIREV This p per exists in English only.

Lf3 2

c G c . 2 3 I

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 4/85

Abst rac t

We i nves t iga t e the ro l e o f budge t ing procedures fo r f i s c a l performance.Using 1970s and 1980s E f i s c a l da t a and expe r t cha rac t e r i za t ions o f budget ing

procedures, we f i nd s t rong empir ica l suppor t fo r the s t r u c t u r a l hypo thes i st h a t a budgeting process with s t r a t e g i c dominance o f the prime or f inance (ort reasury) min i s t e r over the· spending min i s t e r s , l i m i t s on par l iamentaryamendment power, and l imi t ing changes during the. execut ion process i s s t rong lyconducive to f i s c a l d i sc ip l ine . In con t ra s t , the ro l e o f long- te rm f i s c a lcons t r a in t s i n achiev ing f i s c a l d i sc ip l ine , while genera l ly pos i t i ve , i s nots t a t i s t i c a l l y s i g n i f i c a n t . he r e s u l t s suggest t h a t i n s t i t u t i o n a l reform o fthe budgeting process i s a promising avenue to achieve and mainta in a l a rge rdegree o f f i s c a l d i sc ip l ine .

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 5/85

Non-technical Abst rac t

The approach o f a monetary union in Europe has r a i sed concerns about theappropr ia te f i s c a l po l i cy regime in the EC One important worry i s t ha t asys temat ic lack of f i s ~ ls t a b i l i t y of some members o f the European monetaryunion might c rea t e p o l i t i c a l pressures for monetary expansions which theEuropean c e n t r a l bank w i l l f i nd hard to escape, r e s u l t i n g i n p e r s i s t e n ti n f l a t i o n . As a r e s u l t , the revis ions of the Trea t i e s of Rome adopted inMaast r ich t i n December 1991 incorpora te a procedure to superv ise the f i s c a lperformance o f the members by the Community and to increase f i s c a l d i sc ip l ine .

The bas i c approach taken i n the Maastr icht Accord i s one o f con t ro l l i ng ,ex-ante and ex-pos t , the Member S t a t e s f i s c a l performance by the Communityspe l l ing out budget c r i t e r i a and procedures fo r monitoring f i s c a l performancei n the EC To be e ffec t ive , such a s t r a t egy must r e l y on the c r e d i b i l i t y o fthe pena l t i e s i t e n t a i l s for v io la t ing these c r i t e r i a . Experience with budgetnorms in the U.S. suggests t h a t governments ·find ways to circumvent f i s c a lr e s t r a i n t s in prac t i ce , with the r e s u l t t ha t they are l a rge ly ine ffec t ive . Inthe European context , the absence of a s t r i c t enforcement mechanism of f i s c a lcons t r a in t s among sovereign nations other than the t h r e a t or poss ib l eapp l i ca t ion o f peer pressure and f inanc ia l sanct ions r a i s e s the problem o f howto ensure the prospec ts of budget c r i t e r i a to be successful .

This study looks a t the i ssue from another perspect ive . We s t a r t fromthe presumption t h a t budgeting procedures, i . e . , the ru l e s according to whichbudgets a re dra f t ed by a government, amended and passed by par l iament , andimplemented by the government, are important fo r the degree o f f i s c a ls t a b i l i t y a t t a ined . In other words, we claim t h a t i n s t i t u t i o n s shape theoutcome o f the p o l i t i c a l processes v o l v i ~ zwithin them. One var i an t of t h i sclaim - t h a t the grea te r c r e d i b i l i t y of an independent cen t ra l bank scommitment to pr i ce s t a b i l i t y l eads to lower i n f l a t i o n r a t e s - i s , o f course,one o f the important j u s t i f i c a t i o n s for the European monetary union i t s e l f .Our main proposi t ion i s t ha t a budgeting procedure enabl ing a government tocommit i t s e l f to f i s c a l d i sc ip l ine i s an essen t i a l condi t ion for f i s c a ls t a b i l i t y . Commitment mechanisms are important on a l l three l eve l s o f thebudget process , the barga in ing within the cabine t of min i s t e r s , the pass ing ofthe budget law through parl iament, and the execution o f the budget .

Budgeting i n government i s a process of a l loca t ing resources to spec i f i cp o l i t i c a l programs and d i s t r ibu t ing the cos t over cur ren t and fu ture t axpayers. There are a t l e a s t ) two aspec ts of t h i s process which generateproblems o f f i s c a l d i sc ip l ine and give r i s e to the importance of i n s t i t u t i o n s .One i s the difference between the shor t - run and the long-run ne t benef i t s off i s c a l programs, which, i f pol icy makers discount the fu ture , induces a b iastowards s h i f t i n g tax burdens to fu ture tax payers v i a d e f i c i t f inanc ing . Theother i s the difference between the perceived marginal b e n e f i t and marginalcos t o f a f i s c a l program. Spending minis ters and indiv idual members ofpar l iament are exposed to p o l i t i c a l pressures from i n t e r e s t groups and, s incetaxes f a l l on the genera l publ ic while expenditures benef i t p a r t i c u l a r groups,are b iased towards la rge expenditures and la rge d e f i c i t s . The prime minis terand the f inance or t reasury minis ter and broadly-based p o l i t i c a l p a r t i e s inpar l iament , i n con t ras t , do not depend on p a r t i c u l a r i n t e r e s t groups to thesame extent ; t h e i r decis ions are more s t rong ly guided by genera l economiccons idera t ior t s . The d i s t r i b u t i o n of power between these two groups, therefore ,determines the s i ze o f the spending bias b u i l t in to the budgeting procedure.

In view of t h i s , we develop two propos i t ions : (1) I n s t i t u t i o n s conduciveto long-run o r i e n t a t i o n of f i s c a l po l i c i e s enhance f i s c a l d i s c i p l i n e . The

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 6/85

bas i c idea i s t h a t long- run or i en ta t ion mit iga tes the c o n f l i c t between sho r trun and long- run ne t b e n e f i t s . We c a l l t h i s the l ong - t e rm-cons t r a in thypothes is . 2) I n s t i t u t i o n s which weaken the ro l e o f spec ia l i n t e r e s t s i n thebudge t ing process a re conducive to f i s c a l d i sc ip l ine . h ~ bas i c idea i s t h a tsuch i n s t i t u t i o n s mit iga te the spending b ia s a r i s i n g from the d i ff e r encebetween benef i c i a r i e s and the genera l t ax payer. We c a l l t h i s the s t r u c t u r a lhypothes is . We t e s t both hypotheses us ing f i s c a l data from the E membercount r ies o f the 1970s and 1980s, and cha rac t e r i za t ions o f the na t iona lbudge t ing procedures obtained from exper t assessments .

he main empir ica l r e s u l t i s a s t rong support fo r the s t r u c t u r a lhypothes is . Spec i f i ca l ly, our r e s u l t s sugges t t h a t a budgeting process lendingthe prime or f inance or t reasury) minis te r a p o s i t i o n o f s t r a t e g i c dominanceover the spending min i s t e r s , l imi t ing the amendment power o f par l iament , andl i m i t i n g changes in the budget during the execution process i s s t rong lyconducive to f i s c a l d i sc ip l ine . In con t ra s t , the ro l e of long-term f i s c a lcons t r a in t s i n achiev ing f i s c a l d i sc ip l ine , while in most cases p o s i t i v e , i snot found to be s i g n i f i c a n t While we do not conclude from t h i s t h a t long-termcons t r a in t s lack importance, our conclusion i s t h a t a long-term c o n s t r a i n talone i s i n s u f f i c i e n t to overcome the problems o f f i s c a l d i s c i p l i n e fo r acountry whose budgeting procedure has s t r u c t u r a l weaknesses.

Our r e s u l t s suggest t ha t i n s t i t u t i o n a l reform o f the budgeting processi s a promising avenue to achieve a l a rge r degree o f f i s c a l d i s c i p l i n e Suchreform may be r equ i r ed in some count r ies to achieve the f i s c a l t a rg e t s spe l l edout r ecen t ly i n the Maast r ich t Accord, which can be regarded as a s p e c i a l formo f long-term cons t r a in t s on f i s c a l p o l i c i e s . What i s more, i n s t i t u t i o n a lreform meeting the requirements and p a r t i c u l a r i t i e s of i nd iv idua l membercount r ies ~ y be a promising route to maintain f i s ~ ls t a b i l i t y i n the t h i r ds tage of European Monetary Union as a complement to the impos i t ion o f f i s c a lc r i t e r i a under the cu r ren t i n s t i t u t i o n a l arrangements .

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 7/85

1 . In t roduc t ion

The approach o f a monetary union in Europe has r a i s e d concerns about the

appropr ia te f i s c a l po l i cy regime in the European Community (EC). One impor tan t

aspec t of t h i s i s the l i n k between the degree of f i s c a l d i s c i p l i n e the member

governments o f a monetary union adopt and the un ion s long- run i n f l a t i o n

r a t e . 1 Many p a r t i c i p a n t s i n t h i s discuss ion f ea r t h a t a sys temat ic lack o f

f i s c a l s t a b i l i t y o f some members o f the European monetary union might c rea t e

pressures on the European cen t ra l bank to conduct a too expans ionary monetary

po l i cy fo r the Community with the r e s u l t o f l a s t i n g excess ive i n f l a t i o n .

Some have even argued t h a t the i m p l i c i t p o s s i b i l i t y of t ax ing c i t i z e n s o f

other count r ies which e x i s t s i f the un ion s c e n t r a l bank can be induced to

b a i l out governments i n f inanc ia l c r i s e s would l ead to a d e t e r i o r a t i o n o f

f i s c a l d i s c i p l i n e in the Community once the European monetary union i s i n

p lace . s a r e s u l t the r ev i s ions o f the Trea t i e s o f Rome adopted i n

Maast r ich t i n December 1991 incorpora te a procedure to superv ise the f i s c a l

performance o f the members by the Community and to increase f i s c a l d i s c i p l i n e .

Although the Maast r ich t Accord c a l l s for the adoption o f appropr ia te

budgetary procedures by the member s t a t e s 2 the bas i c approach t t akes i s

one o f c o t r o l l i n g ex-ante and ex-pos t , t h e i r f i s c a l performance by the

Community. The hope i s t h a t by spe l l i ng out budget c r i t e r i a and procedures

and pena l t i e s for deal ing with v io la t ions o f these c r i t e r i a member

governments can be induced to f i s c a l s t a b i l i t y i . e . long- run budget balance

or debt growth not exceeding nominal GOP growth. To be e f f e c t i v e such a

s t r a t egy must r e ly on the c r e d i b i l i t y of the t h rea t t impl ies for members

with deviant f i s c a l p o l i c i e s . Experience with budget norms in the U.S.

suggests t h a t governments f i nd ways to circumvent f i s c a l r e s t r a i n t s i n

prac t i ce , with the r e s u l t t h a t they are l a rge ly i n e f f e c t i v e (von Hagen, 1991,

1992) . In the European context , the absence of a s t r i c t enforcement mechanism

o f f i s c a l cons t r a in t s among sovereign nat ions other than the t h r e a t o r

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 8/85

poss ib l e app l i ca t ion o f peer pressure and f inanc ia l sanc t ions r a i s e s the

problem of how to ensure prospec ts o f budget c r i t e r i a to be succes s fu l .

This s tudy looks a t the i s sue from another perspect ive . We s t a r t from

the presumption t h a t budgeting procedures, i . e . the ru l e s according to which

budgets are dra f t ed by a government, amended and passed by par l iament , and

implemented by the government, have important consequences fo r the degree o f

f i s c a l s t a b i l i t y a t t a ined . In o the r words, we claim t h a t i n s t i t u t i o n s shape

the outcome of the p o l i t i c a l processes evolv ing wi th in them. This r equ i r e s

t h a t i n s t i t u t i o n s a re f i xed r e l a t i v e to the p o l i t i c a l processes they govern,

i . e . the formation o f ru l e s and procedures for dec i s ion making i s not p a r t o f

the same p o l i t i c a l process . Ins tead , the ac to r s a re l e g a l l y bound or have a

common understanding t h a t the i n s t i t u t i o n s should be regarded as given. Of

course, t h i s does not exclude t h a t the i n s t i t u t i o n s themselves can be changed

over time, however, doing so would requi re a d i f f e r e n t p o l i t i c a l process . One

var i an t of t h i s bas i c claim t h a t the grea te r c r e d i b i l i t y o f an independent

c e n t r a l bank s commitment to p r i c e s t a b i l i t y l eads to lower i n f l a t i o n r a t e s

i s o f course, one o f the important j u s t i f i c a t i o n s fo r the European monetary

union i t s e l f . Following the same l og i c , our approach l eads to the conclus ion

t h a t i n s t i t u t i o n a l reform of the budge t ing process may be a promising

a l t e rna t ive fo r the E to f o s t e r f i s c a l s t a b i l i t y .

The main propos i t i on o f t h i s paper i s t h a t a budget ing procedure

enabling a government to commit i t s e l f to f i s c a l d i s c i p l i n e i s an e s s e n t i a l

condi t ion fo r f i s c a l s t a b i l i t y . Commitment mechanisms are important on a l l

three l eve l s of the budget process , the barga in ing wi th in the cabine t o f

min i s t e r s , the pass ing o f the budget law through par l iament , and the execut ion

of the budget . Commitment i s f a c i l i t a t e d by r e s t r i c t i n g the e f f e c t barga in ing

processes on each l e v e l can have on t o t a l spending and revenues. I t can be

provided by formal guidel ines determining the outcome of the budgetary process

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 9/85

Fg :

Ge

a Goe

nme

Ep

tue

(p

cofGO

P

1

9

65~

~

6

55

(J

t

5

0

4

~

f

4

[

5

3

5~

~~~~~~~~

~~~~~~~~~~

6

63

65

67

69

7

73

75

77

79

8

83

85

87

89

e

•

Gema

1

Fa

e

>I

Iay

o

L

emb

g

>

N

h

a

*B

gum

I w I

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 10/85

Fg

Ge

a Goe

nme

Ep

tue

p

co

GO

P

1

9

6 6 5

a

5

0 C)

45

- 0

4

3 3 2 2

6

6

6

6

6

7

7

7

7

7

8

8

8

8

8

Y

•

D

mak

o

Irea

t

Ge

e

>

P

u

>I

S

n

*U

teK

n

m

I I

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 11/85

or by r e s t r i c t i n g the scope o f changes par t i c ipan t s in the bargaining process

can make; i t can be the r e s u l t of l ega l r e s t r i c t i o n s on the process or of

long-standing t r ad i t ions which are expected, both by the par t i c ipan t s in the

budgetary process and the pub l i c , to be respected i n the fu tu re North and

Yeingast , 1989). e develop and t e s t t h i s propos i t i on in two vers ions : One

focusing on the exis tence and implementation of long-term f i s c a l plans and the

other focusing on the s t r u c t u r a l c h a r a c t e r i s t i c s o f the budgeting process. Our

empirical r e s u l t s us ing data from the EC sugges t t h a t s t r u c t u r a l

c h a r a c t e r i s t i c s are important . Spec i f i ca l ly, dominance o f the prime min i s t e r

or f inance min i s t e r over the spending min i s t e r s in s e t t i n g budget parameters ,

l imi t a t ions to modificat ions o f the budget proposa l by the l e g i s l a t u r e , and

l imi t a t ions to budget changes during the execut ion are i n s t i t u t i o n s conducive

to f i s c a l s t a b i l i t y

This study proceeds as fo l lows . _Section 2 presen t s some_sty.lized

evidence o f f i s c a l performance i n the Community over the pas t two decades.

Sect ion 3 ou t l ines our bas ic t heore t i ca l argument. Section 4 begins with a

review o f the main c h a r a c t e r i s t i c s o f the budgeting procedures cur ren t ly used

in the 12 countr ies of the Community based on a ques t ionnai re sen t t o the

member Finance Mini s t r i e s or Treasur ies in 1991. Section 5 presents the

empirical t e s t s o f our main hypotheses o f i n t e r e s t Section 6 summarizes our

main conclus ions .

2. Fisca l Performance in the EC 1971-90: Some Sty l i zed Facts

Figures 1 through 8 give an impression o f the f i s c a l performance o f the

12 EC member s t a t e s over the pas t decades. Figures 1 and 2 dep ic t the growth

of genera l government expenditures r e l a t i v e to gross domestic product GDP).

Throughout the 1960s, there was remarkable s i m i l a r i t y among the s i x EC members

and I re land, Denmark and the U.K Ratios o f expendi tures to GDP var i ed

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 12/85

0

2

Q.

C

-4

c

~

c

-6

Q e

-8

Q c

-1

g3

N

Go

enme

L

n

p

coGOP

1

9

-1 14~~~~~~~~

~~~~~~~~

~~~~

6

6

6

6

6

7

7

7

7

7

8

8

8

8

8

Y

•

Gema

1

F

a

e

>

Iay

o

L

emb

g

>

N

h

a

*B

gum

I \ I

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 13/85

5

a

0

( __

-5

( Q

c.

-1 -1

g4:N

Go

enme

L

n

p

cofGOP

1

9

-2

6

6

6

6

6

7

7

7

7

7

8

8

8

8

8

•

D

mak

o

Irea

Y

Gre

e

><

P

u

>I<

S

n

*U

te

Kn

m

I . I

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 14/85

between 25 and 35 percent a t the beginning o f t h i s decade; by i t s end they

had r i s e n to between 30 and 40 percent . In f ac t these r a t i o s gene ra l ly

decl ined in the l a t e the 1960s. The 1970s brought two important changes: a

f a s t e r r i s e o f expendi tures r e l a t i v e to GOP in most countr ies - the exceptions

being France and a f t e r i n i t i a l surges Br i t a in and Germany - and an increase

in the var iance o f these r a t i o s across the E members. Expenditure r a t i o s

genera l ly peaked i n the ea r ly 1980s followed by moderate decl ines i n Germany

France and the U.K. and more s ign i f i can t reduct ions in Denmark Belgium

Luxembourg I re land and the Netherlands. In con t ras t Greece Spain and

I t a l y maintained pos i t ive ly t rending expenditure r a t i o s throughout the decade.

Figures 3 and 4 show the development of ne t government lending i . e .

t o t a l revenues l e s s expendi tures throughout the same per iod . 3 Once again

during the 1960s we f ind a s t r i k i n g s i m i l a r i t y among the European countr ies .

The r a t i o s o f ne t lendiqg to GDP d i ffe red by a maximum of about_ s.ev:en perc.ent.

Once again the 1970s brought much l a rge r var ia t ion among these countr ies .

After 1975 I t a l y Belgium and I r e l and had the most r ap id ly de te r io ra t ing

budgets . Belgium and I re land showed some improvement in the mid- and l a t e

1980s bu t s t i l l r e t a ined some o f the l a rges t r e l a t i v e d e f i c i t s i n the group.

Denmark and Luxembourg are most noteworthy fo r the wide swings i n t h e i r ne t

lending r a t i o s during t h i s period. In con t ras t France Germany and the U.K.

enjo ied s teady developments and moderate d e f i c i t s . With the exception o f

I t a l y Greece and Belgium the E count r ies achieved a grea te r degree o f

convergence o f ne t lending r a t i o s again towards the end o f the 1980s.

Figures 5 and 6 look a t the r e l a t i v e budget balances in terms of ne t

government lending excluding i n t e r e s t payments ca l l ed primary ne t lending fo r

shor t . 4 Primary ne t lending shows to what ex ten t governments accumulate new

debt during a per iod over and above what i s requi red to service ex i s t ing

i n t e r e s t ob l iga t ions and thus gives a b e t t e r i nd ica t ion than t o t a l ne t lending

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 15/85

Fg5

N

Goenme

L

n

(E

.nee

p

coGOP

1

9

8~

~

6

4

(J

Q

2 O

~~~~~~~~~

~~~~~~~~--~~

C O

-2

u Q

-4

c

-6 a~~~~~~~~~~~~~~~~~~~~

7

73

75

7

79

8

83

85

87

89

Y

•

Gema

1

F

a

e

><

Iay

o

L

emb

g

><

N

h

a

•

B

gum

I\ I

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 16/85

a 0 J

~

0 Q

Ol

c +- c Q

0 Q

c

F

g :

N

Go

enme

L

n

E

.nee

p

coG

1

9

15~

~

15 0 -5

-1 1

5~~~~~~~

~~~~~~~~

~~~~

7

1

73

75

77

79

81

8

85

87

8

•

D

mak

o

Irea

Y

1

G

e

e

>

P

u

>I

S

n

•

Ute

Kn

m

I 0 I

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 17/85

of a government s need and wil l ingness to change budget developments. Here, we

observe a grea te r degree of conformity among the 12 count r ies throughout the

whole per iod . Only I t a l y and I r e l and s t a r t e d the 1970s with primary d e f i c i t s

(ne t borrowing), only I t a l y and Greece ended the 1980s in t h i s way. Denmark

and Luxembourg are most noteworthy for the la rge swings in t h e i r primary ne t

lending. I r e l a n d s primary d e f i c i t de te r io ra t ed very rapid ly in the mid-1970s,

i t improved s t e a d i l y from s i x percent to a surp lus of s ix percent of GDP

between 1981 and 1989. While France and the U.K. had primary surpluses during

most of t h i s per iod , Germany experienced d e f i c i t s from 1974 through 1982.

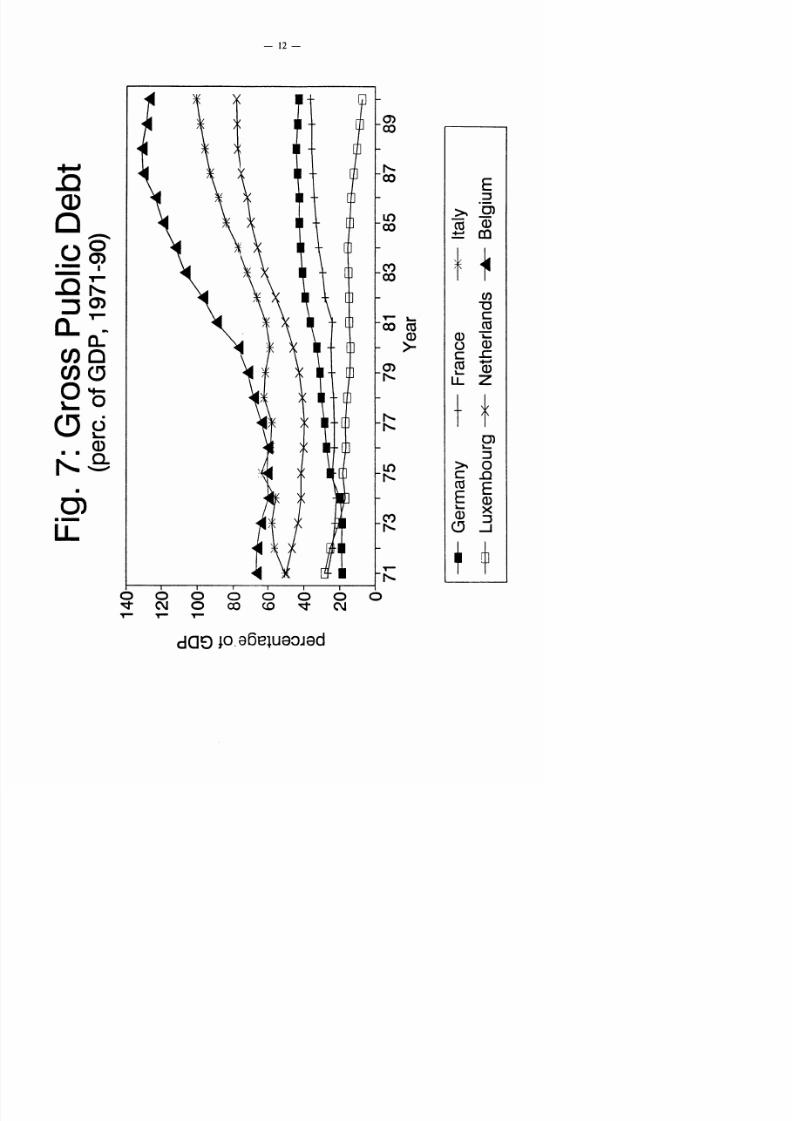

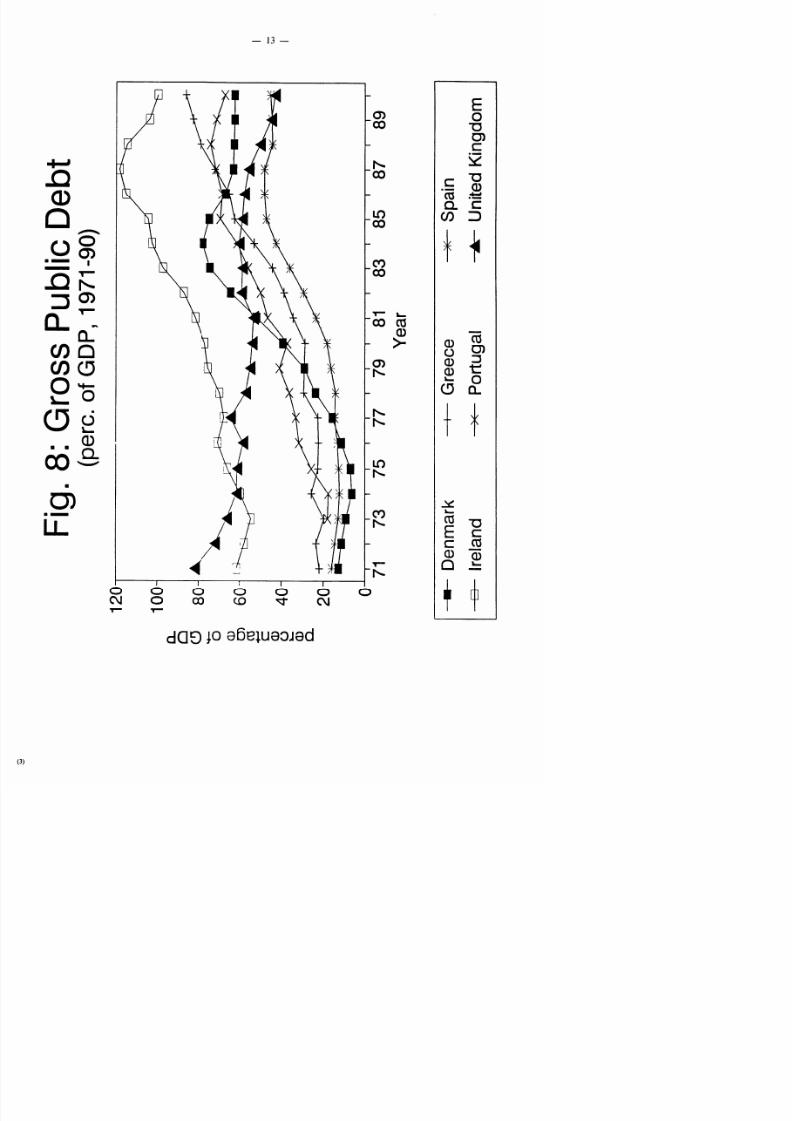

Figures 7 and 8 demonstrate the r a t i o s of gross publ ic debt to GDP from

1971 to 1990. At the beginning of the 1970s, the EC was div ided in two groups,

a r e l a t i v e l y high-debt group inc luding I t a l y Belgium, the Netherlands,

I re land, and the U.K., with r a t i o s of debt to GDP between 50 and 85 percent ,

and .a . r e l a t ive ly low-debt. group compris ing Denmark West Germany .France,

Luxembourg Spain, Greece, and Por tugal , with r a t i o s between 10 and 30

percent . y the end of the 1980s, three groups are d iscernable : Luxembourg

France, Spain, the U.K. and Germany a l l with debt to GDP r a t i o s o f no more

than 40 percent ; Denmark the Netherlands, Portugal and Greece, whose r a t i o s

are between 60 and 80 percent ; and Belgium, I re land, and I t a l y whose r a t i o s

are above 80 percent .

Apart from these differences in the debt r a t i o s themselves, the dynamics

vary s i g n i f i c a n t l y among the 12 countr ies . The U.K. and Luxembourg

cons i s t en t ly experienced f a l l i n g debt r a t i o s throughout the per iod , and the

French r a t i o was v i r t u a l l y f l a t . All other count r ies experienced s i g n i f i c a n t

growth i n t h e i r debt r a t i o s fol lowing the second o i l pr i ce shock in 1979;

onlyi re land and Denmark had s i g n i f i c a n t l y r i s i n g debt r a t i o s al ready e a r l i e r

in the 1970s. Only these two coun t r i e s managed to reduce t h e i r debt r a t i o s

s i g n i f i c a n t l y during the 1980s, while other count r ies merely succeeded i n

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 18/85

1 1

a 0

1

(

- 0

8

Q

0)

r

6

+- c Q

)

4

- Q c

20

7

Fg :

Gro

P

cD

(p

coGOP

1

9

7

7

7

7

8

8

8

8

Y

•

Gema

- -

Fa

e

>I

Iay

o

L

emb

g

><

N

h

a

•

B

gum

I -

8

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 19/85

c 0 9

- 0 Q)

J c .

c Q)

Q)

c

120

18

6

4

2

/

0

71

Fg8Gro

P

cD

p

co

GOP

1

9

7

75

77

79

81

8

8

87

Y

<

S

n

89

•

Demak

o

Irea

_ ___ G

re

e

>

P

u

*Ute

Kn

m

I - I

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 20/85

4

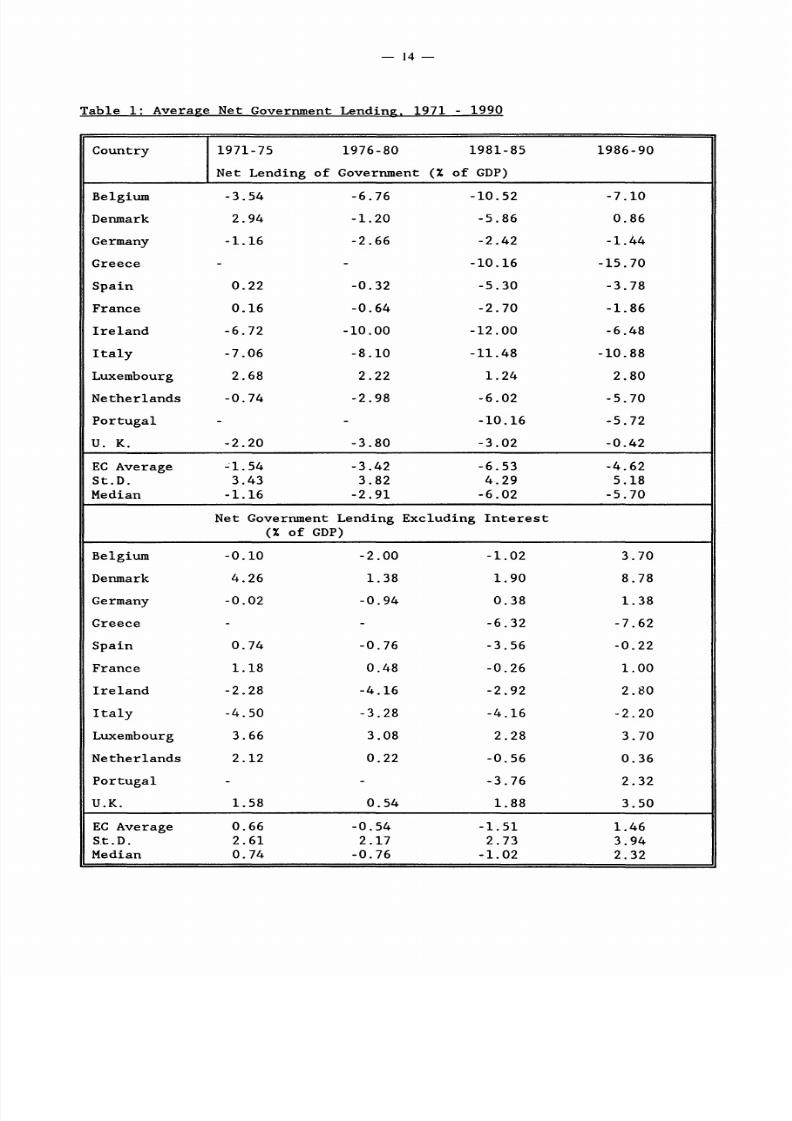

Table 1: Average Net Government Lending. 1971 1990

Country 1971 75 1976 80 1981 85 1986 90

Net Lending of Government ( o f GOP

Belgium 3.54 6.76 10.52 7.10

Denmark 2.94 1.20 5.86 0.86

Germany 1.16 2.66 2.42 1.44

Greece 10.16 15.70

Spain 0.22 0.32 5.30 3.78

France 0.16 0.64 2.70 1.86

I r e l and 6.72 10.00 12.00 6.48t a l y 7.06 8.10 11.48 10.88

Luxembourg 2.68 2.22 1.24 2.80

Netherlands 0.74 2.98 6.02 5.70

Por tugal 10.16 5.72

u. K. 2.20 3.80 3.02 0 .42

EC Average ~ 1 5 4 3.42 6 .53 4 .62St .D. 3.43 3.82 4.29 5.18Median 1.16 2.91 6.02 5.70

Net Government Lending Excluding n t e r e s t{ o f GOP

Belgium 0.10 2.00 1.02 3.70

Denmark 4.26 1.38 1.90 8.78

Germany 0.02 0.94 0.38 1.38

Greece 6.32 7 .62

Spain 0.74 0.76 3.56 0.22

France 1.18 0.48 0.26 1.00I r e l and 2.28 4.16 2.92 2.80

t a l y 4.50 3.28 4.16 2 .20

Luxembourg 3.66 3.08 2.28 3.70

Netherlands 2.12 0.22 0.56 0.36

Portugal 3.76 2.32

U.K. 1.58 0 .54 1.88 3.50

EC Average 0.66 0.54 1.51 1.46

S.t.D. 2.61 2.17 2.73 3.94Median 0.74 0 .76 1.02 2.32

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 21/85

5

Table 2: Average Gross Public Debt. 1971 1990

Country 1971 75 1976 80 1981 85 1986 90

Gross Public Debt ( of GDP

Belgium 63.5 68.04 105.08 128.44

Denmark 9.12 23.72 68.68 63.58

Germany 20.10 29.82 40.16 43.82

Greece 22.52 26.34 46.58 77.06

Spain 13.48 15.06 35.58 46.06

France 23.78 23.52 29.26 35.35

I re land 59.92 71.96 94.68 110.34I t a ly 56.88 59.88 72.14 95.30

Luxembourg 21.68 15.28 14.54 10.16

Netherlands 44.54 41.88 60.74 76.26

Portugal 20.13 35.80 56.70 70.50

U.K. 68.56 57.80 58.12 50.40

EC Average 35.35 39.09 56.86 67.27St . D. 21.66 20.43 26.17 33.23Median 22.52 29.82 56.70 63.58

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 22/85

- 6

prevent ing f u r t h e r i nc reases . The three count r ies in the h igh -deb t group o f

1990 were i n the h igh-debt group of 1971; four of f i ve coun t r i e s i n the low

debt group o f 1990 were i n the low-debt group o f 1971. Only the U.K. movedfrom being the h igh-debt group in 1971 to the low-debt group i n 1990. In sum

r e l a t i v e debt performances are very p e r s i s t e n t in Europe. 5

Tables 1 , 2 , and 3 i l l u s t r a t e the same developments by r epo r t i ng f i ve -

year moving averages of ne t government l ending , primary ne t government

l ending , g ross pub l i c debt , and genera l government expendi ture , a l l expressed

as f r ac t ions o fGDP.

The r i s i n g s tandard devia t ions of the f i r s t t h r eevar i ab le s over t h i s pe r iod r e f l e c t the i nc r ea s ing d i s p a r i t y i n f i s c a l

performance among the 12 European coun t r i e s . Only the s t anda rd dev ia t ion o f

expendi tures r a t i o s decl ines towards the end o f the 1980s.

While the preceding graphs and t ab l e s demonstrate cons iderable v a r i a t i o n

of f i s c a l outcomes in the EC they do not t e l l us anything about the source of

these d i ff e rences .Two

extreme scenar ios are poss ib l e : Fisca l outcomes ini nd iv idua l coun t r i e s could be completely determined by coun t ry - spec i f i c ,

mutua l ly uncorre la ted shocks. Al te rna t ive ly, f i s c a l outcomes could r e f l e c t

coun t ry - spec i f i c responses to the same shock(s) . Consider the fol lowing two

country model as an i l l u s t r a t i o n :

Y , t = f ixt u i , t

y j t = fJ ~ u j . tc o v ( u 1 , t , u j , t ) = 0,

1 )

where Yi,t denotes country i s f i s c a l ~ u t o m evar i ab le , xt i s the under ly ing

shock common to both coun t r i e s , the coeff i c i en t { descr ibes a c o u n t r y s

r eac t ion to the common shock, and u i s i t s r eac t ion to pure ly coun t ry - spec i f i c

shocks. The f i r s t scenar io o f pure ly coun t ry - spec i f i c shocks impl iesXt

- 0,

which in t u rn impl ies t h a t Yi,t and Yj,t a re unco r r e l a t ed . The second scenar io

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 23/85

7

Table 3: Average Government Expenditure

Country 1971 75 1976 80 1981 85 1986 90

Government Expenditure ( of GOP

Belgium 42.98 51.32 57.96 53.46

Denmark 44.36 51.32 60.44 57.66

Germany 43.16 47.90 48.44 46.32

Greece 42.70 49.94

Spain 23.60 29.18 38.70 41.32

France 39.12 44.54 50.86 50.48

I re land 40.18 45.88 53.30 47.84

t a l y 35.84 39.50 48.38 51.42

Luxembourg 38.84 51.92 54.58 51.20

Netherlands 44.96 54.38 60.58 58.88

Portugal 44.34 43.50

U.K. 39.90 42.30 44.66 39.78

EC Average 39.29 45.80 50.41 49.32St . D. 6.20 7.50 7.14 5.94Median 39.12 45.88 48.88 49.94

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 24/85

- 1 8 -

Table 4: Factor Analysis o f Government Expenditure. Net Lending. and Debt

Country

Belgium

Denmark

Germany

Greece

Spain

France

I r e l and

I t a l y

Luxembourg

GovernmentExpenditure

Varianceexplained

96.5

94.1

90.0

76.0

96.4

97.0

90.0

93.5

85.0

Netherlands 93.2

Portugal

UnitedKingdom

16.5

91.8

Factorpa t t e rn

n

n n

n

n n

Net Lending l e s sI n t e r e s t Paid

Varianceexplained

99.2

84.3

92.7

94.5

98.7

95.6

95.0

90.9

98.8

96.3

96.4

98.2

Factorpa t t e rn

n

n

n

n

n

Gross Public Debt

Varianceexplained

98.1

96.4

95.5

83.3

96.3

96.6

95.9

97.0

92.9

96.7

20.7

-94.9

Factorpa t t e rn

n

n

n

n

n n

Note: Variance explained i s the percentage of variance explained by two ommon

fac tors . Factor pa t t e rns : + or - i nd ica t e s tha t the es t imated c o e f f i c i e n tfor t h i s f ac to r i s above or below the average es t imate for a l l 12 countr ies .n i nd ica t e s f ac to r i s not s ign i f i can t a t the 10 percent l eve l . Per iod for

est imation: 1971 - 1990; 1981 - 90 for Greek and Portuguese expenditurer a t i o s .

holds when u 1 , t = uj, t = 0, and 1 di ffe r s from fJj Note tha t we can extend

equation 1) in a simple way to conta in two ommon shocks:

Yi , t = f J 1 , i x l , t f J2 , i x2 , t u i , t

Yj, t = fJ1 , jx l , t f J2 , jx2 , t u j , t

c o v ( u 1 , t ,uj,t = 0 ,

2 )

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 25/85

- 1 9 -

i n which case the two outcomes a re l e s s than per fec t ly co r re l a t ed , even i f

there a re no coun t ry - spec i f i c shocks, provided t ha t the pa i r s o f r eac t ion

c o e f f i c i e n t s are d i f f e r e n t between the coun t r i e s .

To see which o f these two paradigms descr ibes the European case

bes t , we apply f ac to r ana lys i s to our r a t i o s of general government spending,

ne t government l ending , and gross publ ic debt to GDP This technique al lows to

es t imate the unobserved common shocks expla in ing a s e t o f t ime s e r i e s , t h e i r

common f a c t o r s , cor responding to the va r i ab l e s x 1 , t and x 2 , t i n model (2 ) . By

cons t ruc t i on , these shocks are unco r r e l a t ed with each o the r and with the

coun t ry - spec i f i c shocks. Having obta ined es t imates o f these f ac to r s , we can

then use r eg re s s ion ana lys i s to see how much o f the var iance o f the observed

f i s c a l outcomes i s expla ined by r eac t ions to common shocks as opposed to

count ry s p e c i f i c shocks. The r e s u l t s of t h i s procedure are summarized i n Table

4 . For each var i ab le , two common £ac to r s were es t imated . The £ i r s t _o£ .each

p a i r of columns i nd i ca t e s the percentage o f the t o t a l var iance o f the var i ab le

explained by a coun t ry s r eac t ion to the two common shocks. For a l l t h r ee

va r i ab l e s , we f ind t h a t almost a l l the var iance i s explained by the two common

f ac to r s . Greece and Por tuga l a re the only two except ions to t h i s r e s u l t . 6 The

second column i n each p a i r gives some in format ion about the coun t ry s r eac t ion

to the common f ac to r as determined by the regress ion ana lys i s . Here, a +

means t h a t the r eg re s s ion c o e f f i c i e n t on t h i s f ac to r i s s i g n i f i c a n t and above

the average o f the s i g n i f i c a n t es t imates fo r a l l 12 coun t r i e s , a - i nd i ca t e s

a s i g n i f i c a n t c o e f f i c i e n t below the average es t imate , and a n i nd i ca t e s t h a t

the f ac to r was not s i g n i f i c a n t in the regress ion . The main conclusion from

t h i s exe rc i s e i s t h a t f i s c a l p o l i c i e s in the EC coun t r i e s , as descr ibed by

d e f i c i t s , spending and debt pa t t e rns , can bes t be cha rac t e r i zed by count ry

spec i f i c r eac t i ons to common shocks, r a the r than responses to coun t ry - spec i f i c

shocks. To the ex ten t t h a t f i s c a l i n s t i t u t i o n s determine a coun t ry s f i s c a l -

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 26/85

2

pol icy response to economic shocks, i n s t i t u t i o n a l d i ff e r ences across these

count r ies may be important to expla in t h i s var i a t ion in f i s c a l outcomes.

In Table 5,we

address the r e l a t i o n s h i p between government expendituresand n e t l ending . According to a popular hypothes is , l a rge and growing d e f i c i t s

and, t he re fo re , growing debt to GDP r a t i o s are caused by l a rge and growing

l eve l s o f government expendi ture ( see e .g . Roubini and Sachs, 1989a, Larkey e t

a l . , 1981). I f t h i s was t r u e , g r e a t e r f i s c a l d i sc ip l ine could be achieved by

reducing government spending. To t e s t t h i s hypothes is , we check for Granger-

Table 5: Causa l i ty o f Government Expenditure for Net Lending

Country R2 o f Test F-Test for F-Test for Ser ia lRegression Causa l i ty Cor re l a t i on of

Residua ls

Belgium 0.89 0.16 0.95

Denmark ~ h 04H.l 6

Germany 0.44 0.19 0.93

Greece 0.83 0.53 0.30

Spain 0.54 0.30 0.41

France 0.53 0.91 0.64

I r e l and 0.83 0.08 0.79

I t a l y 0.87 0.04 0.42

Luxembourg 0.45 0.83 0.80

Netherlands 0.87 0.08 0.93

Por tuga l 0.95 0.09 n .a .United Kingdom 0.61 0.33 0.84

Note:Tests are for Granger-causa l i ty o f changes in the expenditure/GOP r a t i ofo r ne t government l ending GDP Test r eg re s s ion inc ludes two l ags o f thedependent and two l ags of the independent var i ab le . Sample pe r iod i s 19611990 except for Spain 1 9 7 1 - 1990), Greece (1980-1990) and Portugal (19801990) . Tests for s e r i a l cor re l a t ion of r e s idua l s check the s ign i f i cance o ffour a t e s t r eg re s s ion o f the r e s idua l s from the causa l i ty t e s t r eg re s s ion onfour of own l ags . All e n t r i e s a re p r o b a b i l i t i e s of F values l a rge r thanes t imated F s under the Null-hypotheses o f non-causa l i ty and no s e r i a l

c o r r e l a t i o n .

c a u s a l i t y o f government spending fo r ne t l ending , both measured r e l a t i v e to

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 27/85

4 )

2

GDP. Defining rlt as the r a t i o o f ne t l ending to GOP and gt as the r a t i o o f

expenditure to GOP we es t imate the fol lowing r eg re s s ion model:

( 3 )

where et i s a s e r i a l l y uncorre la ted regress ion e r ro r. The t e s t fo r Granger

c a u s a l i t y in t h i s context i s an F - t e s t on the j o i n t s ign i f i cance o f 1 1 and

The f i r s t column in Table 5 shows t h a t the t e s t regress ions exp la in most

o f the var iance of the dependent var i ab le . The second one i nd ica t e s t h a t

expenditure r a t i o s do not genera l ly Granger-cause ne t l ending r a t i o s , i f

s tandard s ign i f i cance l eve l s are appl ied . I t a l y i s the only except ion . 8 The

l a s t column shows tha t the regress ion e r ro r s are indeed s e r i a l l y uncorre la ted

an important condi t ion for the r e l i a b i l i t y o f the F - t e s t . Overa l l Table 5

produces two in te res t ing f ind ings : F i r s t , the r eg re s s ion R2 s show t h a t the

low-debt count r ies of 1990 Luxembourg Spain France Germany, and the U.K.

have the s ~ a l l e s tdegree o f pe r s i s t ence in ne t l ending r a t i o s in the sense

t h a t t h e i r pas t ne t l ending r a t i o s are the l e a s t he lp fu l to pred ic t cu r ren t

r a t i o s . Tnis s u ~ e s t st ha t count r ies which manage to change t h e i r budgets l e s s

e a s i l y over t ime are more prone to la rge d e f i c i t s and debt . Second with the

exception of I t a l y, the simple hypothes i s t h a t r i s i n g d e f i c i t s are the r e s u l t

of growing expenditures i s not warranted by the data .

While t ab l e s 4 and 5 compare t ime s e r i e s prope r t i e s o f the data across

coun t r i e s t ab l e 6 takes a d i f f e r e n t perspect ive and compares average r e l a t i v e

performances among the 12 European count r ies during the 1980s. The t ab l e i s

based on the moving averages ca l cu l a t ed i n t ab l e 1. After order ing the 12

count r ies according to the s i z e of each v a r i a b l e we compute the Spearman rank

c o r r e l a t i o n c o e f f i c i e n t s shown in t ab l e 6. The f i r s t four coeff i c i en t s - a l l

s i g n i f i c a n t l y p o s i t i v e - confirm and extend the e a r l i e r f ind ing t h a t r e l a t i v e

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 28/85

Table 6: Rank Corre la t ion Coeff ic ients

Items

Net Lending 1981-85 vs .Net Lending 1986-90

Net Lending Excl.I n t e r e s t , 1981-85 vs.1986-90

Gross Public Debt,1981-85 vs. 1986-90

Government Spending,1981-85 vs . 1986-90

Net Lending vs .Net Lending Excl.I n t e r e s t

Net Lending vs.Gross Public Debt

Net Lending Excl.I n t e r e s t vs. GrossPublic Debt

Net Lending vs .Government Spending

Net Lending Excl.I n t e r e s t vs . GovernmentSpending

Gross Public Debt vs .Government Spending

1981-85

0.85.0005)

0.750.005)

0.890.00)

0.800.001)

0.720.002)

-0 .820.001)

-0 .250.43)

0.010.983)

0.570.055)

0.360.245)

1986-90

0.620.03)

-0 .810.001)

-0 .140.649)

-0 .090.779)

0.140.665)

0.300.354)

Note: All var iables measured as percentages of GDP Upper en t r i e s are Spearmanrank cor re la t ion coeff i c i en t s . Entr ies in parantheses are the probab i l i tyes t imates for t - t e s t s t ha t the cor re la t ion coeff i c i en t i s zero.

rankings in f i s c a l performances are very p e r s i s t e n t over t ime. That i s acountry t h a t was ranked highly in terms of , say, i t s net lending r a t i o in the

ea r ly 1980s was very l i k e l y to be ranked highly in the second h a l f of t h i s

decade. The f i f t h row of table 6 indica tes t h a t countr ies with r e l a t i v e l y high

low) ne t lending r a t i o s tend to be countr ies with r e l a t i v e l y high low)

primary net lending r a t i o s . The f i f t h row indica tes t h a t the same i s t rue with

regard to net lending r a t i o s and gross publ ic debt r a t i o s .The fol lowing rows of table 6 show t h a t there i s no s ign i f i can t

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 29/85

2 3

c o r r e l a t i o n between a count ry(s rank i n primary ne t l ending and i t s rank in

gross pub l i c debt . That i s t he re i s no sys temat ic l i n k between r e l a t i v e l y

high (low) primary d e f i c i t s and r e l a t i v e l y high (low) debt l e v e l s . Furthermore

t he re a re no sys temat ic r e l a t ionsh ips between r e l a t i v e l y l a rge d e f i c i t s la rge

primary d e f i c i t s or l a rge debt r a t i o s and r e l a t i v e l y l a rge expendi ture

r a t i o s . Once again , t h i s r e fu te s the simple not ion t h a t l a rge d e f i c i t s or

l a rge debts are due to excess ive spending.

3. Budgeting Procedures and Fisca l Outcomes: Theory

The previous sec t ion has demonstrated the s i g n i f i c a n t v a r i a t i o n in the

f i s c a l performance o f the E member coun t r i e s over the p a s t two or t h ree

decades. Despite the differences in outcomes i t sugges ts t h a t f i s c a l po l i c i e s

i n the E were mainly dr iven by shocks common to a l l coun t r i e s . The

i n t e r e s t i n g ques t ion then i s what expla ins the l a rge d i ff e rences i n t h e i r

r eac t ions?

Economic Models of F i sca l Performance

Conventional economic ana lys i s dctes not say much about the determinants

o f f i s c a l performance. I t genera l ly t akes f i s c a l po l i cy as exogenously

determined by p o l i t i c a l processes . One s t r and o f l i t e r a t u r e t r i e s to expla in

the secu la r growth o f government expendi tures r e l a t i v e to the economy, a

tendency f i r s t formulated as Wagner s Law (Wagner, 1890). Although the l i n k

between economic growth and the r e l a t i v e s i ze o f government expendi tures ,

which Wagner a t t r i b u t e d to the growing r e s p o n s i b i l i t i e s o f government in the

process o f i n d u s t r i a l i z a t i o n seems apparent fo r many countr ies a t f i r s t

glance , empir ica l s tud ie s genera l ly found no or l i t t l e suppor t fo r the Law

( e .g . Larkey e t a l . 1981; Cameron, 1978). Other a t tempts a t gene ra l i z ing

empir ica l observa t ions have been equal ly unsuccessfu l to withs tand c lose r

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 30/85

s t a t i s t i c a l sc ru t iny. 9

Another l i n e of research at tempts to i den t i fy f i s c a l po l i cy r eac t ion

funct ions l i nk ing f i s c a l var i ab les such as expendi tures or d e f i c i t s to macro

economic var iab les , such as growth or unemployment. Roubini and Sachs (1989a)

es t imate expenditures and revenues react ion functions for 5 OECD governments.

They f ind t h a t expenditure r a t i o s , on average across the OECD respond

negat ive ly to output growth and pos i t ive ly to r i s i n g unemployment r a t e s ;

revenue-to-GOP r a t i o s respond negat ive ly to output growth and negat ive ly to

unemployment r a t e s . They conclude t h a t the slowdown in economic growth and the

r i s e in unemployment a f t e r the f i r s t o i l pr ice shock in 973 were respons ib le

for the subsequent r i s e i n government expenditures r e l a t i v e to GDP.

Roubini and Sachs ' s argument would sugges t , however, t h a t the r i s e in

expendi tures expla ins much of the de te r io ra t ion o f budget d e f i c i t s in the

1970s. Ear l i e r, we saw t h a t t h i s simple r e l a t i o n s h i p s not confirmed by ~ u r

data . Since t h e i r es t imated react ion functions are the same across countr ies ,

d i ff e rences i n the observed outcomes would have to be due to d i ffe rences in

the economic shocks indiv idual governments were r eac t ing to , w h i h ~ i sno t

cons i s t en t with our e a r l i e r observat ions , e i t h e r. Even i f d i f f e r e n t r eac t ion

functions were es t imated , t h e i r approach leaves the ques t ion o f why such

d i f f e r e n t react ions occurred unanswered.

The same authors (1989b) take a s t ep i n a d i f f e r e n t d i rec t ion , l i nk ing

f i s c a l performance to p o l i t i c a l c h a r a c t e r i s t i c s . They argue t h a t government

d e f i c i t s r e l a t i v e to GDP have been l a rg e s t in OECD countr ies with r e l a t i v e l y

unstable governments. More spec i f i ca l ly, while the post-1973 slowdown in

economic growth and r i s e in unemployment expla in the r i s e in expenditure and

d e f i c i t s in the OECD they f ind t h a t mult i -par ty c o a l i t i o n governments,

espec ia l ly those wi th a shor t expected tenure , a re poor a t reducing budget

d e f i c i t s i b i d . , p. 922). Roubini and Sachs propose three i n t u i t i v e

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 31/85

2 5

explanations for t h i s f inding: The d ive r s i ty of i n t e r e s t s and cons t i t uenc ie s

o f c o a l i t i o n par tne r s , a tendency o f coa l i t i ons to be s ta tus-quo biased , as

indiv idual c o a l i t i o n members can block changes from the s t a t u s quo but cannot

organize enough support to push through a change from i t and a l ack o f

enforcement mechanisms for coopera t ive behavior - which, by assumption, would

fos te r f i s c a l d i sc ip l ine - in shor t - l ived coa l i t ions .

Roubini and Sachs s argument i s however, not e n t i r e l y _convincing. Thei r

view of unstable governments presupposes t h a t indiv iduals or p a r t i e s take

off i ce for a shor t t ime and then d isappear from the government sphere.

Commitment to longer- run or ien ted po l i c i e s does not pay o f f for such

p o l i t i c i a n s , hence t h e i r unwil l ingness to combat d e f i c i t s and avoid the

accumulation o f fu ture tax l i a b i l i t i e s through the c rea t ion o f publ ic debt .

However even i f governments change r e l a t i v e l y f requent ly, i t may s t i l l be

t rue t h a t the members of_ government are drawn from a pool .o-f. candida tes or

p a r t i e s which does not change much over time. In such an environment,

commitment to longer- run goals does pay o ff , because government p o l i t i c i a n s

can expect t h a t they or t h e i r par ty w i l l have another t u rn i n the fu ture .

While Roubini and Sachs s da ta suggests t ha t countr ies with la rge d e f i c i t s

tend to have unstable governments, i t does not show t h a t countr ies with small

d e f i c i t s exh ib i t more government s t a b i l i t y than o the r s . This sugges ts the

importance o f o the r, omitted p o l i t i c a l c h a r a c t e r i s t i c s .

P o l i t i c a l Economy o f Budgeting Procedures

Recent poli t ico-economic l i t e r a t u r e has explored the ro le o f

i n s t i t u t i o n a l arrangements governing the budgeting process , vot ing

arrangements and commitment mechanisms for f i s c a l performance. Although t h i s

l i t e r a t u r e i s heavi ly inf luenced by the p e c u l i a r i t i e s o f the U.S. , t he re a re

genera l lessons to i n f e r from t h i s research . The most important one i s t h a t

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 32/85

6

i n s t i t u t i o n a l s t r u c t u r e s i . e . the arrangements ass igning the ro le s

indiv idual p a r t i c i p a n t s play and the scope and sequence of dec i s ions , have

important e f f e c t s on the f i n a l outcomes of the budgeting process . Here,we

review some o f the main arguments.

In the most pr imi t ive form o f a budgeting process , budgets would be

voted by par l iament a f t e r a genera l debate i n which each member o f par l iament

submit can proposa l . Arrow s (1963) well-known Imposs ib i l i t y Theorem impl ies

t h a t such a procedure does not genera l ly lead to an equi l ibr ium outcome. Only

under r e s t r i c t i v e condi t ions on the preferences o f the members o f par l iament

does a majo r i t y ru le induce an equi l ibr ium. Of course, such i s not the

prac t i ce o f a c t u a l budgeting procedures. In prac t i ce , budgeting procedures are

div ided between government or par l iamentary committees dra f t ing a proposa l ,

par l iament which may amend the proposa l sub jec t t o c e r t a i n r e s t r i c t i o n s and

_pass i t and_ again .the execut i v e carry ing out the budget l a w ~ The p o li t i c o -

economic l i t e r a t u r e focuses on how the spec i f i c i n s t i t u t i o n a l arrangements

a f f e c t the ex i s t ence and the prope r t i e s of the equi l ibr ium outcome.

Shepsle (1979a, b) d i s t ingu i shes three c h a r a c t e r i s t i c s o f budget ing

procedures. The d i v i s i o n o f labor arrangement ass igns i nd iv idua l ac to r s i n the

process to s p e c i f i c r o l e s . For example, a t yp ica l European arrangement i s t h a t

government d r a f t s a budget proposa l to be presented to the l e g i s l a t u r e . 10 The

arrangement may be t h a t the proposa l i s dra f t ed by a l l cab ine t members

together or in b i l a t e r a l t a lks between the f inance (or t r ea su ry ) min i s t e r and

the var ious spending min i s t e r s . In the U.S. , in con t ras t , the d i v i s i o n o f

l abor arrangement i s a system o f par l iamentary appropr ia t ions committees . A

spec ia l i za t ion o f l abo r arrangement i s an assignment o f j u r i s d i c t i o n s to

indiv idual groups of ac to r s . A committee may have j u r i s d i c t i o n over only one

dimension o r seve ra l dimensions o f government se rv ices . Spending min i s t e r s

usua l ly only have j u r i s d i c t i o n over t h e i r own f i e l d . Fina l ly, an amendment

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 33/85

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 34/85

2 8

under l ines the importance o f i n s t i t u t i o n a l arrangements for f i s c a l outcomes.

Second, the c h a r a c t e r i s t i c s o f the p a r t i c u l a r equi l ibr ium outcome depends on

the combination o f a l l t h r ee i n s t i t u t i o n a l c h a r a c t e r i s t i c s . This impl ies t h a t

d i f f e r e n t i n s t i t u t i o n a l se t -ups among the EC coun t r i e s may expla in d i f f e r e n t

reac t ions to the same under ly ing shocks. Third, the s t a t u s quo w i l l be most

powerful in determining the outcome, i f t he re i s a one-to-one mapping between

par l iamentary committees and j u r i s d i c t i o n s and i f the l e g i s l a t u r e i s bound by

a ru le t h a t p roh ib i t s amendments i f the committee proposes the s t a t u s quo.

Thus, regardless o f whether or not the government i s formed by a s t a b l e

c o a l i t i o n which would determine the assignment o f i nd iv idua l s to commit tees

or mini s t r i e s but would not the a f f e c t budget ing procedure i n s t i t u t i o n a l

s t ruc tu res are impor tan t determinants of how l i k e l y a dev ia t ion from s t a t u s

quo w i l l be.

DivisioiL and, s p e c i a l i z a t i o n o £ l abo r arrangements _to:gether determine the

degree of c e n t r a l i z a t i o n o f the budgeting process . In the European con tex t , we

d i s t ingu i sh , wi th in government, between a decen t r a l i zed approach, i n which

each spending min i s t e r with au thor i ty over one budget dimension i s engaged i n

b i l a t e r a l t a lks with the f inance or t r easu ry min i s t e r, and a cen t ra l i zed

approach, in which the cab ine t as a whole discusses the budget proposa ls . In

the par l iamentary procedure, the r e l evan t d i s t i n c t i o n i s between a sequence o f

votes proceeding on an i t em-by- i tem b a s i s , or a genera l vo te on the e n t i r e

budget fol lowing a genera l debate . The importance o f t h i s aspect comes from

the l i m i t s i t puts on universa l i sm and r ec ip roc i ty (Alt and Chrys ta l , 1981).

Universal ism r e f e r s to the proper ty o f budget proposa ls to con ta in something

for everyone , i . e . to d i s t r i b u t e favors more generously than an i nd iv idua l

decis ion maker would want. Reciproci ty r e f e r s to the pr inc ip le of not

at tacking another per son s approp r i a t i on proposa l in r e tu rn for he r no t

a t t ack ing one s own. Both t end to increase expendi tures .

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 35/85 5)

2 9

Chrys ta l and Al t summarize the bas i c argument asfo l lows: Consider a

government where each spending min i s t e r pursues only h i s i nd iv idua l i n t e r e s t

and the budget law r equ i r e s a minimal winning c o a l i t i o n wi th in the cabinet .

Under such circumstances, i t i s always r a t i o n a l fo r a min i s t e r to vote aga ins t

o the r m i n i s t e r s proposa ls for i nc reas ing t h e i r budgets on cos t -bene f i t

grounds. y impl ica t ion , no min i s t e r i s able t o push an expansion o f h i s

budget through and government s e t t l e s on the cheapes t poss ib l e budget ,

al though each min i s t e r would l i k e a l a rg e r one. One way to ge t around t h i s i s

to engage i n mutual agreements , i . e . proposa ls which b e n e f i t more than one

min i s t e r, or to agree t a c i t l y not to vote down each o t h e r s proposa ls . The

r e s u l t i s t h a t each spending min i s t e r obta ins a l a rg e r budget . Chrys ta l and

Al t argue t h a t pai rwise bargain ing between the f inance min i s t e r and the

spending min i s t e r favors universa l i sm and r ec ip roc i ty. They base t h e i r view on

repor ts t h a t B r i t i s h Cabinet min i s t e r s r e f r a in . f rom t t ~ c k i n gspending

reques ts from other departments and the observat ion t h a t the B r i t i s h system

does embed pai rwise bargain ing . Beyond t h a t empir ica l observa t ion , however,

t h e i r argument seems implaus ib le . Tac i t agreements requi re monitoring to be

e f f e c t i v e , which i s e a s i e r in m u l t i l a t e r a l bargain ing s i t u a t i o n s than in

decen t r a l i zed ones, because the former give a l l p a r t i c i p a n t s the oppor tuni ty

to observe each o the r s behavior. Furthermore, universa l i sm requi res the

p o s s i b i l i t y to decide over mul t ip l e budget dimensions simultaneously, which

would t yp ica l ly not be poss ib l e in a decen t r a l i zed s e t t i n g . We w i l l

hypothes ize , t he re fo re , t h a t both prac t i ces a re more l imi t ed i n decen t r a l i zed

than in cen t ra l i zed procedures.

Ferejohn and Krehbie l (1987) analyze the importance of the sequence of

decis ions i n the budgeting process for the f i n a l outcome. Spec i f i ca l ly, they

compare a process in which approp r i a t i ons a r e voted i nd iv idua l ly and the

overa l l budget s i ze i s a r e s idua l with one in which the budget s i z e i s voted

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 36/85

3

f i r s t and the s t r u c t u r e o f the budget i s determined af terwards , given the

t o t a l s i z e . Contrary to popular b e l i e f , the l a t t e r procedure does not always

l e ad to a smal ler budget than the f i r s t . hen vo t ing on the t o t a l s i z e ,

dec i s ion makers a n t i c i p a t e the l i m i t s they c rea t e fo r subsequent a l loca t ions .

Decis ion makers with s t rong ly skewed preferences i n favor o f p a r t i c u l a r budget

i tems are l i k e l y to produce l a rg e r budgets in the two-step procedure, because

they do not accept the i m p l i c i t need t o t r ade o f f i nd iv idua l expendi tures in

the second s t ep . In con t ras t , dec i s ion makers with more balanced preferences

are l i k e l y t o f ind smal ler budget agreements i n t h i s way.

Mackay and Weaver (1979) show t h a t , again con t r a ry to popular b e l i e f ,

committees with the power to propose budgets for p a r t i c u l a r government

se rv ices do no t always propose a l a rge r budget than the median v o t e r would

propose, even i f the committee members preference fo r the p a r t i c u l a r se rv ice

are much s t ronge r than the median v o t e r s preference . Applying t h e i r ~ g u m e n t

to Europe, t h i s means t h a t proposa ls put f o r t h by spending min i s t e r s do no t

necessa r i ly aim a t l a rg e r spending for t h e i r j u r i s d i c t i o n than proposa ls

r e s u l t i n g from a genera l deba te .

North and Weingast (1989) analyze the ro le o f B r i t i s h f i s c a l

i n s t i t u t i o n s in t roduced a f t e r the Glorious Revolut ion o f 1688. The new f i s c a l

c o n s t i t u t i o n r e s u l t e d i n a s p e c i f i c d iv i s ion o f l abo r between the Crown

Parl iament, and the Bank of England and c rea t ed an e f f e c t i v e commitment

mechanism for the Crown to serve i t s debt o b l i g a t i o n s . Comparing publ ic

f inances i n B r i t a i n before and a f t e r the Revolut ion sugges ts t h a t these

changes f a c i l i t a t e d a more s t a b l e and r e l i a b l e f i s c a l po l i cy. Bordo and White

(1992) compare B r i t i s h and French publ ic f inances between 1790 and 1814 and

conclude t h a t i n s t i t u t i o n a l def i c i enc ies in the French system undermined the

c r e d i b i l i t y o f the French government and forced France to conduct

s i g n i f i c a n t l y l e s s e f f i c i e n t and s t a b l e f i s c a l p o l i c i e s than B r i t a i n dur ing

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 37/85

3 1

t h a t pe r iod .

A Simple Model o f the Budgeting Process

According to Wildavsky (1975, p. 4) the budget process i s a mechanism

through which p o l i t i c a l i n t e r e s t groups bargain over conf l i c t ing goals , make

s ide-payments , and t r y to motivate one another to accomplish t h e i r

ob jec t ives . In essence, i t i s a device fo r p o l i t i c a l c o n f l i c t r e so lu t ion . In

t h i s sec t ion , we propose a simple model charac te r i z ing the budgeting process

as i t i s found in the E coun t r i e s , and der ive some hypotheses concern ing

f i s c a l d i sc ip l ine .

Our model descr ibes the budget ing process in t h ree s t ages . On the f i r s t

s t age , government prepares a budget d r a f t to be presented before par l iament .

The government comprises spending min i s t e r s , a f inance or t r easu ry min i s t e r

. p r e s i i ~ gover f inanc ia l resources , and a prime min i s t e r . ac t ing as t he

chairman. 11 Conf l i c t s o f i n t e r e s t between the min i s t e r s must be resolved i n

the d r a f t i n g process . On the second s t age , the budget i s submitted to

par l iament , which can amend the proposa l and e i t h e r pass or r e j e c t i t We

t h ink o f t h i s pr imar i ly as a bargain ing process between government, which now

r ep resen t s a un i f i ed pos i t ion expressed in i t s proposa l , and the p a r t i e s

r ep re sen ted in par l iament , which e i t h e r suppor t o r oppose the government. On

the t h i r d s t age , the budget law i s executed and fu r the r modif ica t ions o f the

law may be poss ib l e .

To cha rac t e r i ze the process , we assume t h a t taxes are not earmarked fo r

spec ia l purposes. Spending min i s t e r s are i n t e r e s t e d i n expanding the resources

o f t h e i r own mini s t r i e s , but i nd i ffe ren t about the resources of o the r

minis t r i e s . Thei r p o l i t i c a l success i s measured i n terms o f the s i z e o f t h e i r

budgets . In con t ras t , the prime min i s t e r and the f inance min i s t e r a re not

bound by p a r t i c u l a r i n t e r e s t s or not to the same ex ten t and, t he re fo re ,

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 38/85

3

are more c o n s t r a i n t by cons idera t ions o f genera l publ ic welfare than the

spending min i s t e r s . For a given amount o f t o t a l spending, i nc reas ing the

genera l t ax burden of the economy reduces publ ic wel fare .

Spending and f inanc ing government programs involve d i f f e r e n t t ime

hor izons . e assume t h a t the bene f i t s from spending money for the major i ty of

government programs are obta ined immediately or over a r e l a t i v e l y shor t t ime

per iod . In con t ras t , the wel fare e f f e c t s of higher t axes imposed on cur ren t

t ax payers a re f e l t to a la rge ex ten t only i n the medium and long run, s ince

they involve pr iva te sec to r adjustment to changes in t ax i ncen t ives o r ne t

asse t r e tu rns . In add i t i on , we assume t h a t t ax payers are a t l e a s t p a r t l y non

Ricard ian , so t h a t d e f i c i t f inanc ing al lows to s h i f t p a r t o f the tax burden to

f inance cur ren t expendi tures on fu ture tax payers . 12 Fina l ly, we assume t h a t

p o l i t i c i a n s discount the fu ture , so t h a t presen t o r nea r pay-offs o f t h e i r

ac t ions a re weighed more heavi ly than those in the more d i s t a n t fu tu re .

Spending min i s t e r s are inhe ren t ly biased to push for increased spending

of t h e i r own m i n i s t r i e s , s ince the r e s u l t i n g t axes or d e f i c i t s to f inance the

e x t r a expendi ture f a l l on the genera l publ ic or, in the case o f d e f i c i t s on

the genera l publ ic in the fu tu re ) , while the spending b e n e f i t s t h e i r own

cons t i tuency and r a i s e s t h e i r p o l i ~ i c lsuppor t . A budget c o n f l i c t between two

spending min i s t e r s , A and B therefore , has the s t r u c t u r e desc r ibed i n f i g . 9.

Here, we compare two bas i c s t r a t e g i e s : small and l a rge expendi tures . I f both

choose small expendi tures , the r e s u l t i n g l eve l of t axes and the d e f i c i t remain

small , i f both choose la rge expendi tures , t axes and the d e f i c i t a re l a rge .

Both spending min i s t e r s rece ive the same pay-offs - denoted by the numbers i n

the upper l e f t corner fo r A and the lower r i g h t corner fo r B when they adopt

the same s t r a t egy. Each would pre fe r an outcome i n which the o the r chooses the

small expendi ture s i ze . However because a min i s t e r faces a l o s s o f p o l i t i c a l

support i f h i s col league reaps a l a rge r a l loca t ion wi th in a given budget than

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 39/85

Minis t ry As t r a t e g i e s

smallexpendi tures

l a rgeexpendi tures

Figure 9:

Minis t ry B s t r a t e g i e s

smal l expendi tures

40low t axes , smal ld e f i c i t

60medium t axes ,medium d e f i c i t

40

2

la rgeexpendi tures

2medium taxes ,medium d e f i c i t

60

50high t axes , l a rged e f i c i t

50

he does, the equi l ibr ium i s the la rge budget with h igh taxes and a l a rge

d e f i c i t . That i s , the spending b ias works aga ins t f i s c a l d i s c i p l i n e .

The prime min i s t e r and the f inance min i s t e r have a la rge r tendency to

l i m i t spending in order to r e s t r a i n the l eve l o f presen t and fu tu re

t axa t ion . 13 From t h e i r perspect ive , the pre fe r red outcome would be t h a t both

spending min i s t e r s adopt the smal l -expendi tures s t r a t egy, e spec ia l ly so i n

t imes where the s t a t u s - q u o budget has high l eve l s o f spending and t axa t ion

and a high d e f i c i t to begin wi th .

n important aspec t o f the process wi th in government concerns the

sequence o f decis ions determining the s i z e o f the budget . In a bottom-up

approach, the t o t a l s i ze i s determined r e s i d u a l l y a f t e r co l l ec t ing spending

reques ts from a l l mini s t r i e s . Al te rna t ive ly, the cab ine t may agree on a

genera l cons t r a in t , f i r s t , and decide on i nd iv idua l a l loca t ions or the

s t ruc tu re of the budget given t h i s cons t r a in t af terwards . The genera l

c o n s t r a i n t may f ix the overa l l s i ze o f the budget , t o t a l expendi tures or the

d e f i c i t , o r cons i s t of a golden r u l e clause , i . e . , the prov i s ion t h a t

d e f i c i t s cannot exceed investment or c a p i t a l expendi tures . Cons t r a in t s f ix ing

only the d e f i c i t or a golden ru l e clause would, however, be l e s s binding fo r

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 40/85

fu ture decis ions than t o t a l expenditures or the overa l l s i z e . A genera l

c o n s t r a i n t can be s t rengthened agains t universa l i sm and r ec ip roc i ty by giv ing

the prime min i s t e r (or the f inance min i s t e r ) the au thor i ty to f i x the overa l l

s i ze be fo re i nd iv idua l budgets are determined.

Another c h a r a c t e r i s t i c o f the process within government concerns the

p a r t i c i p a t i o n in dec i s ions . Budget decis ions may be reached by the e n t i r e

cab ine t c o l l e c t i v e l y, or, a l t e r n a t i v e l y, through b i l a t e r a l discuss ions between

the f inance min i s t e r and each o f the spending m i n i s t r i e s . Fina l ly, we can

d i s t ingu i sh budget processes by the ex ten t to which they connect the cur ren t

budget t o p a s t and fu ture budgets through mul t i -pe r iod budget p lans . I f m u l t i

pe r iod budget plans e x i s t a t a l l they may be regarded pr imar i ly as a genera l

o r i e n t a t i o n or as a binding cons t r a in t .

The government s budget proposa l i s submit ted to par l iament where t

becomes sub jec t to another barga in ing process . . Members o f pa r l i amen t r ep re sen t

l oca l o r o the r cons t i t uenc ie s and are , the re fo re , cha rac t e r i zed by a s imi la r

i f not s t ronge r spending b ias as spending min i s t e r s . n the o the r hand,

members o f par l iament are bound by par ty d i s c i p l i n e . European p a r t i e s which

are co l l ec t ions o f groups of cons t i t uenc ie s , are l i k e l y to give l a rg e r weight

to the genera l i n t e r e s t as opposed to p a r t i c u l a r cons t i t uenc ie s i n par ty

decis ions than i nd iv idua l members of par l iament would do in the absence o f

pa r ty d i s c i p l i n e . Furthermore, for the members of the par ty or the p a r t i e s

backing the government in o f f i c e , par ty d i s c i p l i n e e n t a i l s vo t ing to suppor t

the government, even i f the outcome does not f u l l y match the preferences o f

the ind iv idua l member of par l iament .

Par l i amen t s ro le i s to amend the budget proposa l , and to pass or to

r e j e c t i t . While government s e t s the agenda for the par l iamentary debate, i t s

proposa l w i l l a n t i c i p a t e par l i amen t s r eac t ion to i t . The r e l a t ionsh ip between

government and par l iament i s cha rac t e r i zed , f i r s t by the scope o f amendments

8/13/2019 Budgeting Procedures and Economic Performance in EU Hagen

http://slidepdf.com/reader/full/budgeting-procedures-and-economic-performance-in-eu-hagen 41/85

3 5

par l iament can cons ider. In the s imples t case , t he re may be no r e s t r i c t i o n s on

amendments a t a l l Otherwise, amendments may only be permi t ted fo r c e r t a i n

p a r t s o f the budget , or par l iament may be r e s t r i c t e d to amendments proposing

increases i n expendi tures only i f they i d e n t i f y the necessary sources o f

add i t iona l f inance , or only such amendments t h a t do not (or only negat ive ly)

a f f e c t the overa l l s i ze of the budget .

The second dimension o f the r e l a t ionsh ip between par l iament and

government concerns the p o l i t i c a l impl ica t ions of r e j e c t i n g the budget favored

by the government. The s t r a t e g i c e f f e c t of the p o s s i b i l i t y to r e j e c t the

budget proposa l i s two-fold. On the one hand, the more l i k e l y a r e j e c t i o n

l eads to the demise o f the government, the more i t i s i n government s i n t e r e s t

to propose a budget t h a t can be expected to f ind a s o l i d majo r i t y i n

par l iament . This tends to weaken the pos i t ion o f government i n the process . On

the o the r hand, members o f .the _par ties . support ing gov ernment . in par l iament

w i l l r e f r a i n from proposing changes to the budget proposa l i f doing so may

e n t a i l the f a l l o f the government, unless the changes a re regarded o f outmost

importance. This second e f f e c t tends to s t rengthen government s p o s i t i o n i n

the process . While the combined e f f e c t i s ambiguous, we assume t h a t the l a t t e r