budget update january 15, 2014. budget calendar ten year analysis general fund

TRANSCRIPT

Budget UpdateJanuary 15, 2014

Budget Calendar

October November December January February March April May June

One School Board Meeting - Budget

Update

Two School Board Meetings - Budget

Updates

One School Board Meeting

Two School Board Meetings - Budget Update & Hearing

Two School Board Meetings - Budget

Updates

Two School Board Budget Work

Sessions

One School Board Budget Work

Session

FY14 ADM Count Due to State

Governors Proposed Budget

4 Public Budget Open Houses

School Board Adoption of

Preliminary Budget

State Legislature Adjourns

Borough Budget Deliberations with Possible Adoption

Borough Budget Deliberations with Possible Adoption

FY14 ADM Count Period Ends

FY15 Projection Due to State

Budget Survey School Board Budget Adoption

Borough Sets Minimum Amount to be Available for the

District

One School Board Meeting - Budget

Update

Two School Board Meetings - Work

Session & Budget Update

Joint Assembly & School Board

Meeting

Preliminary Budget Trasmitted to

Borough

TEN YEAR ANALYSISGeneral Fund

Enrollment History

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 12,000

13,000

14,000

15,000

16,000

17,000

18,000

13

,58

8 1

4,3

04

14

,66

3 1

5,4

40

15

,84

7

16

,11

5

16

,47

1

16

,65

3

16

,96

3

17

,33

4

Source: Matanuska-Susitna Borough School District Comprehensive Annual Financial Reports

Straight Line Growth Rate Total Salaries & Benefits Per Pupil*

(FY2002-03 Base Year)

*Employee Benefits does not include the on-behalf contributions for TRS & PERS, which began in 2008

Source: Alaska Department of Labor & Workforce Development and Matanuska-Susitna Borough School District Comprehensive Annual Financial Reports

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

0%

-3%

6%

14% 14% 14%

22%

32%34%

37%

0% 3%

6%

9%12%

17%18%

20%

24%27%

Total Salaries & Benefits Per Pupil

Anchorage CPI-U

Straight Line Growth Rate ComparisonCertificated Salaries Per Pupil

(FY2002-03 Base Year)

Source: Alaska Department of Labor & Workforce Development and Matanuska-Susitna Borough School District Comprehensive Annual Financial Reports

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

0%

-4%

0%

2% 3%

9%

14%

20% 19% 20%

0% 3%

6%

9%

12%

17%18%

20%

24%

27%

Total Certifi-cated Salaries Per Pupil

Anchorage CPI-U

Straight Line Growth Rate ComparisonNon-Certificated Salaries Per Pupil

(FY2002-03 Base Year)

Source: Alaska Department of Labor & Workforce Development and Matanuska-Susitna Borough School District Comprehensive Annual Financial Reports

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

-20%

-10%

0%

10%

20%

30%

40%

0%

-4%

3%

9%

-16%

-8%

3%

22%

28%28%

0% 3%6%

9% 12%

17% 18% 20%

24%27%

Non-Certifi-cated Salaries Per Pupil

Anchorage CPI-U

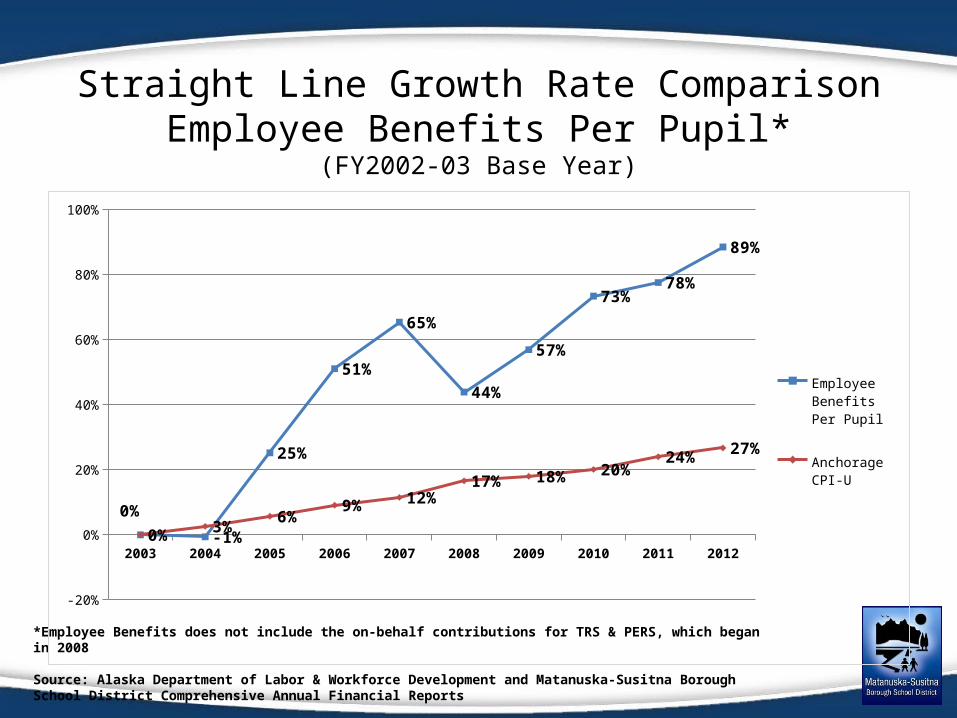

Straight Line Growth Rate ComparisonEmployee Benefits Per Pupil*

(FY2002-03 Base Year)

*Employee Benefits does not include the on-behalf contributions for TRS & PERS, which began in 2008

Source: Alaska Department of Labor & Workforce Development and Matanuska-Susitna Borough School District Comprehensive Annual Financial Reports

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

-20%

0%

20%

40%

60%

80%

100%

0% -1%

25%

51%

65%

44%

57%

73%78%

89%

0%3%

6%9% 12%

17% 18% 20%24% 27%

Employee Benefits Per Pupil

Anchorage CPI-U

Health Insurance

• The total Health Premium has risen steadily since 2003 with an overall increase of almost 160%

• Through bargaining however, the District has set a priority to attempt to maintain these increases and our costs have increased about 133%

2003200420052006200720082009201020112012 $-

$5,000.00

$10,000.00

$15,000.00

$20,000.00

$25,000.00

District Share

Total Premium

Source: Matanuska-Susitna Borough School District Department of Human Resources

LONGTERM FORECASTFinancing the Future

Revenue Assumptions

• Borough Revenue continues to INCREASE at 3%

• Federal Revenue Maintains with ZERO INCREASE or DECREASE

• State Energy Relief Funding continues at $100 per Adjusted ADM

• Student Safety and Security Grant ends after FY14

• ZERO INCREASE or DECREASE in the State Foundation Formula

• Intensive Count maintains at 321 students

• Other Local Receipts maintains with ZERO INCREASE or DECREASE

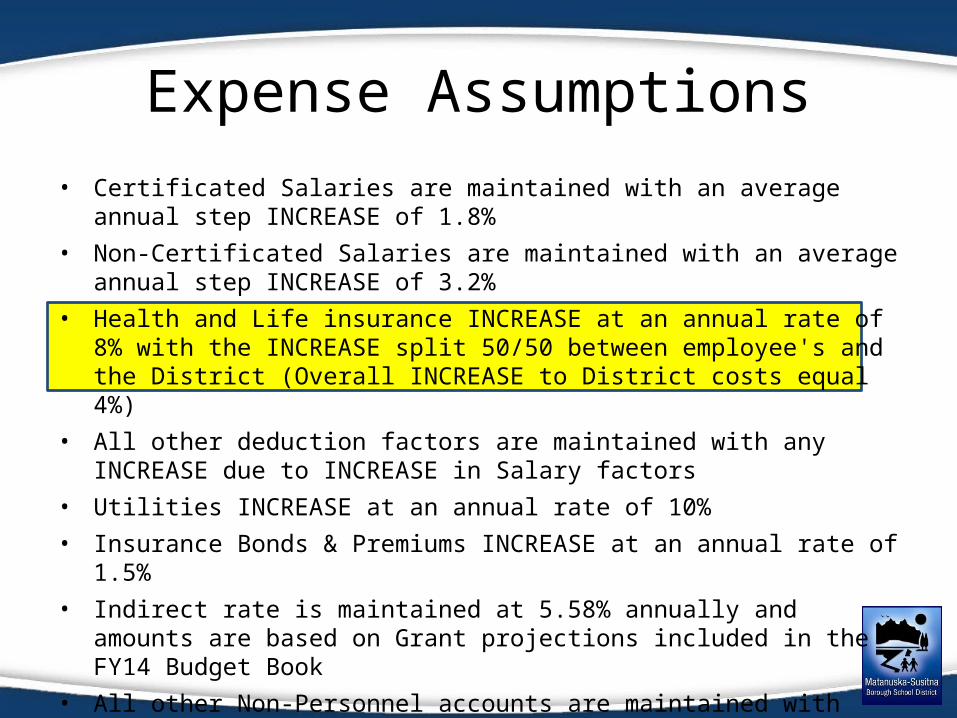

Expense Assumptions

• Certificated Salaries are maintained with an average annual step INCREASE of 1.8%

• Non-Certificated Salaries are maintained with an average annual step INCREASE of 3.2%

• Health and Life insurance INCREASE at an annual rate of 8% with the INCREASE split 50/50 between employee's and the District (Overall INCREASE to District costs equal 4%)

• All other deduction factors are maintained with any INCREASE due to INCREASE in Salary factors

• Utilities INCREASE at an annual rate of 10%

• Insurance Bonds & Premiums INCREASE at an annual rate of 1.5%

• Indirect rate is maintained at 5.58% annually and amounts are based on Grant projections included in the FY14 Budget Book

• All other Non-Personnel accounts are maintained with ZERO INCREASE or DECREASE

Long Term Forecast

FY 2011-2012 Actuals

(A)

FY 2012-2013Budget

(C)

FY 2013-2014Projection

(E)

FY 2014-2015Projection

(F)

% Change(F) - (E)

FY 2015-2016Projection

(G)

% Change(G) - (F)

FY 2016-17Projection

(H)Enrollment 17,338 17,247 17,317 17,446 0.74% 17,482 0.21% 17,572

Federal Revenue 1,989,092$ 1,837,000$ 1,910,679$ 1,800,000$ -5.79% 1,800,000$ 0.00% 1,800,000$ State Foundation 139,579,127$ 141,742,098$ 138,299,622$ 139,316,720$ 0.74% 139,614,123$ 0.21% 140,148,754$ State Energy Relief Funds 2,361,367$ 2,929,851$ 2,864,272$ 2,891,010$ 0.93% 2,896,231$ 0.18% 2,905,617$ Student Safety & Security -$ -$ 2,410,327$ -$ -100.00% -$ -$ Borough Support 48,048,419$ 49,797,786$ 51,291,720$ 52,830,472$ 3.00% 54,415,386$ 3.00% 56,047,848$ Other Local Reciepts - student & user fees 1,660,677$ 147,500$ 200,000$ 200,000$ 0.00% 200,000$ 0.00% 200,000$

Sub-Total Revenue 193,638,682$ 196,454,235$ 196,976,620$ 197,038,202$ 198,925,740$ 201,102,219$ State On-behalf for Emp. Retirement Systems 28,752,528$ 36,616,844$ 38,317,531$ 38,317,531$ 0.00% 38,317,531$ 0.00% 38,317,531$

Total Revenue 222,391,210$ 233,071,079$ 235,294,151$ 235,355,733$ 237,243,271$ 239,419,750$ Use of Fund Balance 1,400,935$ 1,699,886$ 1,334,970$ -$ -100.00% -$ 0.00% -$

Total Projectected Revenue & Fund Balance 223,792,145$ 234,770,965$ 236,629,121$ 235,355,733$ -0.54% 237,243,271$ 0.80% 239,419,750$

Personnel CostsSalaries 107,622,808$ 112,752,770$ 111,747,522$ 114,316,361$ 2.30% 116,947,262$ 2.30% 119,641,807$ Benefits 48,498,867$ 50,541,448$ 51,975,228$ 54,340,997$ 4.55% 56,878,692$ 4.67% 59,495,240$ State On-behalf for Emp. Retirement Systems 28,752,528$ 36,616,844$ 38,317,531$ 38,317,531$ 0.00% 38,317,531$ 0.00% 38,317,531$

Non-Personnel CostsUtilities 5,767,579$ 6,378,969$ 7,111,464$ 7,822,610$ 10.00% 8,604,871$ 10.00% 9,465,358$ Non-Personnel Costs 23,164,264$ 27,717,227$ 25,902,376$ 25,856,464$ -0.18% 26,038,169$ 0.70% 26,204,233$

Total Expenditures 213,806,046$ 234,007,258$ 235,054,121$ 240,653,963$ 246,786,525$ 253,124,169$ 7,123,916$ 225,000$ 1,575,000$ 1,575,000$ 1,575,000$ -$

Total Expenditures 220,929,962$ 234,232,258$ 236,629,121$ 242,228,963$ 2.37% 248,361,525$ 2.53% 253,124,169$

Net Ending Unassigned Fund Balnce (Deficit) 1,699,886$ 538,707$ -$ (6,873,230)$ (11,118,254)$ (13,704,419)$

REVENUE

EXPENSES

Transfers to Other Funds, including Food Service,

Three Year Projection

FY 2011-2012 Actual

FY 2012-2013 Budget

FY 2013-2014 Projection

FY 2014-2015 Projection

FY 2015-2016 Projection

FY 2016-2017 Projection

$200,000,000

$210,000,000

$220,000,000

$230,000,000

$240,000,000

$250,000,000

$260,000,000

17,000

17,100

17,200

17,300

17,400

17,500

17,600

17,700

REVENUE EXPENSE ENROLLMENT

Structural Deficit

FY 2011-2012 Ac-tual

FY 2012-2013 Budget

FY 2013-2014 Projection

FY 2014-2015 Projection

FY 2015-2016 Projection

FY 2016-2017 Projection

$200,000,000

$210,000,000

$220,000,000

$230,000,000

$240,000,000

$250,000,000

$260,000,000

$223,792,145

$234,770,965

$236,629,121 $235,355,733 $237,243,271

$239,419,750

$220,929,962

$234,232,258

$236,629,121

$242,228,963

$248,361,525

$253,124,169

REVENUE EXPENSE

Structural Deficit

HAY GROUP STUDY

State Managed Group Health Insurance Program for Alaska Public School Employees

Purpose

• Conduct and provide an analysis of the current health benefit plans for each of the 53 school districts in Alaska.

• Establish an actuarial value of the various benefit plans offered

• Estimate the projected premiums and costs of consolidating public school employees in Alaska under a state-managed plan

Hay Groups Study

• Surveyed all 53 school districts – 100% participation

• NEA Alaska Health Plan• Aetna, Premera, TPAs• Dept. of Administration• Dept. of Education and Early Development• Unions – Teamsters, Local 71

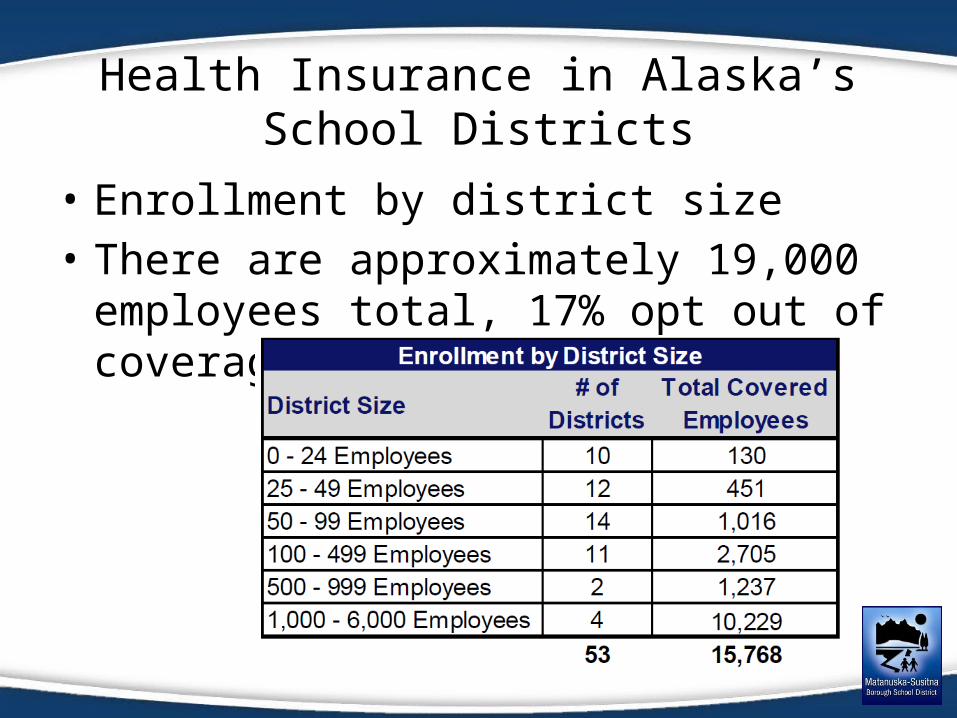

Health Insurance in Alaska’s School Districts

• Enrollment by district size• There are approximately 19,000

employees total, 17% opt out of coverage

Health Insurance in Alaska’s School Districts

• Costs by district size

Health Insurance in Alaska’s School Districts

• Plan offerings currently available in Alaska’s school districts

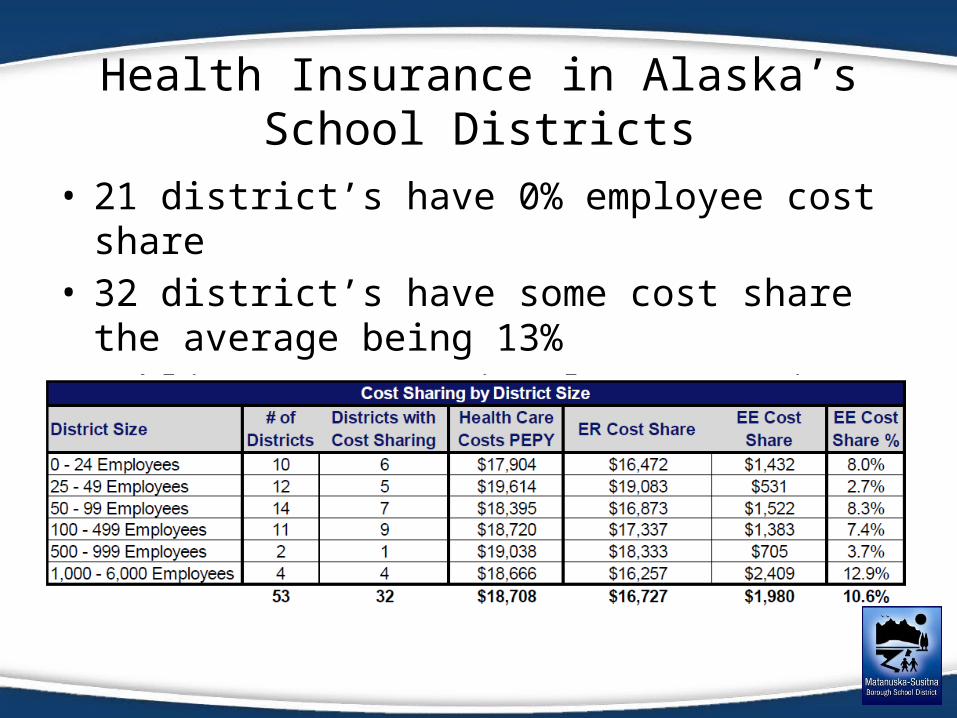

Health Insurance in Alaska’s School Districts

• 21 district’s have 0% employee cost share• 32 district’s have some cost share the average

being 13%• Public sector national average is 15%

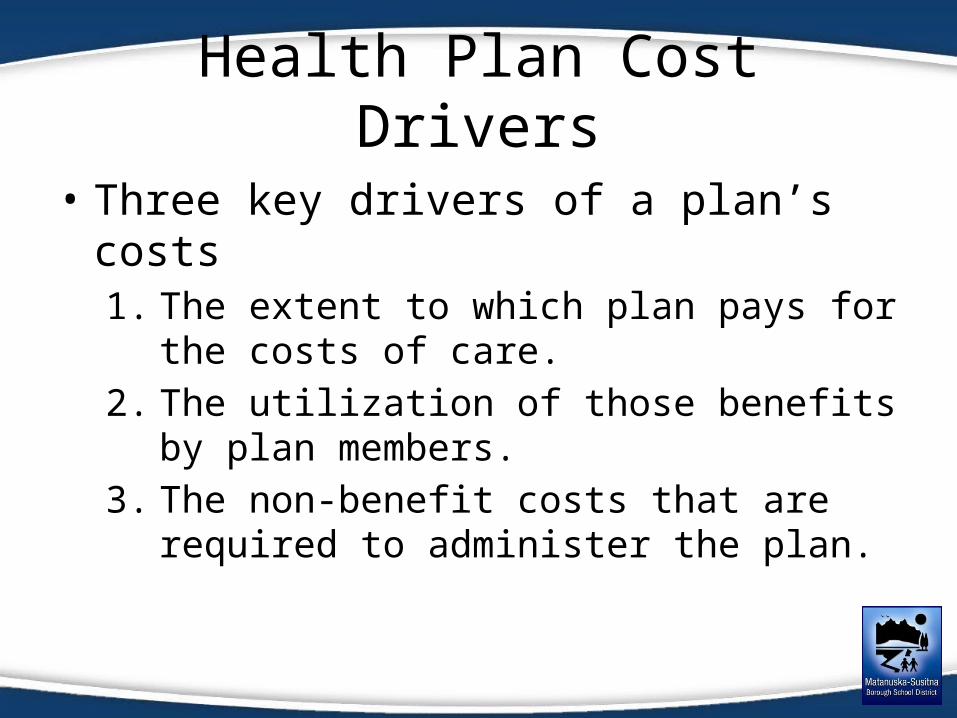

Health Plan Cost Drivers

• Three key drivers of a plan’s costs1. The extent to which plan pays for the costs

of care.

2. The utilization of those benefits by plan members.

3. The non-benefit costs that are required to administer the plan.

Plan Costs Broken Down

• The argument for self insurance/pooling

Saving through Pooling

Cost savings for a consolidated pool can be broken down to four main areas

– Provider Networks– Overhead– Plan Design– Cost Sharing

Consolidation Outcomes

Positive Outcomes Negative Outcomes

Improves vendor contract terms Reduces district staff administration

Increase in compliance Eliminates district decision-making

Reduces annual volatility in costs

Consistent benefits offering to all districts

Reduces duplicative resources

Efficient health management

Options

1. Optimize Program Performance

2. Leverage AlaskaCare Plans

3. Centrally Managed School District Program with Standard Health Plan Options and Cost Sharing

4. Centrally Manage School District Program with Standard Health Plan Options Only

5. Bring all School District Plans under State management

1. Optimize Program Performance

• Savings achieved through provider networks and overhead $17.1M - $28.8M

Positive Outcomes Negative Outcomes

Cost savings with same level of benefits

Increases State administration

Simplifies bargaining

Districts allowed to set contributions

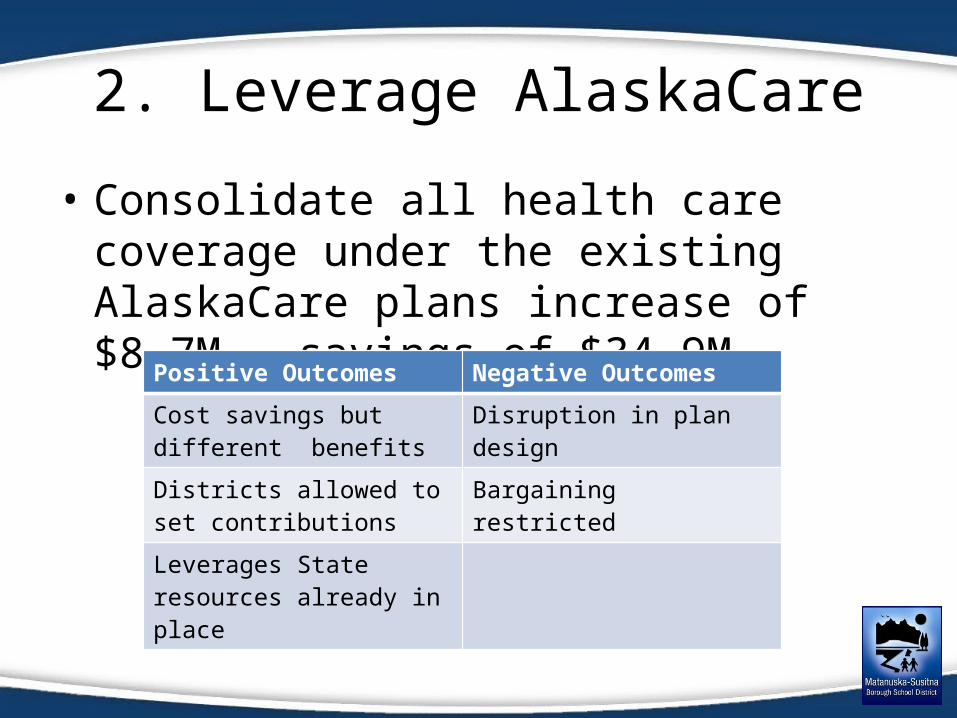

2. Leverage AlaskaCare

• Consolidate all health care coverage under the existing AlaskaCare plans increase of $8.7M – savings of $34.9M

Positive Outcomes Negative Outcomes

Cost savings but different benefits

Disruption in plan design

Districts allowed to set contributions

Bargaining restricted

Leverages State resources already in place

3. District Pool with Standard Plan and Cost Share

• Provides an independent pool for school districts with three standard plan options and a standard cost share savings of $22.6M – $33.7M

Positive Outcomes Negative Outcomes

Cost savings but different benefits

Disruption in plan design

All Districts have same contributions

Bargaining restricted

4. District Pool with Standard Plan

• Provides an independent pool for school districts with three standard plan options $9.4M – $64.9M

Positive Outcomes Negative Outcomes

Cost savings but different benefits

Disruption in plan design

Districts allowed to set contributions

Bargaining restricted

Recommendations

• State pursue pooling as described in option 3– Significant savings through optimization of

plan performance, plan design consolidation and standardized cost sharing.

• To achieve maximum benefit and savings the transition would need to be mandatory