budget institutions budgeting systems and fiscal...

TRANSCRIPT

Lecture: budgeting and fiscal rulesApril 20, 2006 Joint Vienna Institute

Budget Institutions Budgeting Systems and

Fiscal ManagementWilliam McCarten

World Bank Institute

Public Sector Management Options for transition Economies

o Weberian style bureaucracyo NPM-type reforms should not be

introduced in countries that have not first successfully implemented traditional (See Hood and Manning)

o Neo-Weberian model defined by Bouchaert and Pollitt

Public Sector Management Agenda in Transition and Mixed Economies

o Much scope exists for improving strategic prioritization of budgetary spending, and for reducing non-transparent and wasteful quasi-fiscal activities.

o With substantially reduced public finance envelopes, the CIS-7 governments cannot maintain the extensive range of public services which they offered two decades ago.

o At the same time, private provision can be an attractive solution in many areas, on both efficiency and affordability grounds - specialized/higher-level education and health services.

o Linkages between administrative oversight system, such as supreme external audit and the legislative branch weak or nonexistent

o Intergovernmental fiscal relations and coordination under performing

Transition Economies BudgetaryProblems

o For many TEs chronic underfunding across all programs and ministries keep fiscal pressure high and divers the attention ofpolicy makers from identification of and making decisions on strategic choices.

§ in a study on Armenia Betley (2003) and the World Bank found that priorities given to various agencies in the process of budget execution differ from agreed budget allocations

§ The quality of budget reporting is affected by the introduction of new spending programs that are never fully disclosed according to their budget appropriations

§ Weakness in expenditure control § High dependence on donor financing , which creates additional

uncertainty. § These problems are now being addressed with MTEF capacity

building

Low Income Transition Economies o The role of the state sector and the aim of public expenditure, has

changed from one of providing all economic and social services to that of:

§ ensuring an appropriate legislative and regulatory framework foreconomic activity, particularly by the private sector;

§ providing an enabling environment (e.g. through reducing unnecessary bureaucratic impediments) to facilitate a vibrant private sector to develop; and

§ either contracting or being the direct service provider in areas in which the market fails to produce the right level of services at a socially acceptable price (e.g. public health services).

o Beyond the budget system, the CIS-7 governments still extend substantial quasi-fiscal subsidies to enterprises and households, mainly via controlled utility tariffs and non-enforcement of collections. The energy sector in particular remains a source ofsubstantial quasi-fiscal subsidies to downstream industries.

Problems of Low Income CIS countries over last decade

o Over last 15 years power income countries of the CIS ( that is CIS- 7) have had squeeze their spending in order to fit within the much reduced budget envelope,

o Budget expenditures have fallen dramatically: price subsidies and subsidies to state-owned enterprises have been reduced or eliminated, large public sector investment programs, particularly in the infrastructure sectors, have been slashed, a contraction in the public sector through privatisation and the beginnings of a reduction in wider public sector employment

o Some reform in the health sector, and the provision of some services, such as pre -school education, has been eliminated. At the same time, wages and operating costs have declined significantly in real terms .

Budget Institutions o von Hagen presents evidence supporting the hypothesis that

centralisation of the budget process leads to smaller government deficits and debts. Evidence from European Union countries showing a significant negative association between the centralrization of the budget process and general government deficits and debts relative to GDP.

o Hence centralization of the budget process is associated with smaller deficits and debts.

o European Union data and show that the hypothesis holds up empirically even when a number of political factors such as the composition and stability of governments is controlled for.

o Gleich (2002) presents a study of the budget processes in ten Central and East European countries, all candidates for accession to the EU. He finds a considerable degree of variation in the design of these processes across the ten countries. This is interesting, because a budget process in the proper sense did not exist under the former, socialist regime.

o All ten countries hold elections under various forms of proportional representation. Gleich shows that there is a strong negative association between the degree of centralization of the budget process and the public sector deficits and debts emerged in the 2nd half of the 1990s.

Budget Institutions and Public Spending

o Principal agent problem oCommon pool problemo Society can react to these problems by creating

institutions that reduce or mitigate adverse effects.o Impose ex ante controls, such as balanced budget

constraintso strengthen accountability and competition or spending

program contestability among cabinet ministers, politicians and their programs.

o force political policy makers to recognize the marginal costs and benefits of their decisions

o von Hagen advocates two approaches to centralization of the budget process : delegation and contracting,depending upon the circumstances whether there is a single party or multiparty coalition government . (see reading)

o Sweden has adopted two stage legislative oversight to deal with common pool problem.

What is the Common Pool Problem?

o The annual budget is somewhat like the common pool of fish in the river. Each claimant to the budget considers the budget as a “free” resource since his or her demand is such a small proportion of the total budget and therefore will not impose much of a loss to the total.

o But, if every claimant behaved this way, the aggregate of their demands will far exceed what is available.

o Hence, absent any constraint, meeting the demands of disparate claimants to the budget is likely to result in large, unsustainable deficits that translate into an unstable macroeconomic environment — high inflation, high interest rates, burgeoning current account deficits –all of which will necessarily retard economic growth and efforts to reduce poverty.

Principal-Agent Problem o von Hagen asserts, page 2 Fiscal Management, that the

voter- politician relationship is a principal- agent problem which resembles an incomplete contract with the voter as principals and elected politicians as agents.

o Suggests reliance on outside authority to enforce ex ante(before implementation) rules.

o The rules of the European Monetary Union (EMU) with its Stability and Growth Pact.

o States commit themselves to fixed fiscal targets o Another solution is to adopt fiscal responsibility legislation.

Bulgaria has a form of fiscal responsibility framework .o See Kopits PFD file

What is a Fiscal ResponsibilityFramework ?According to Kopits (2004) the major elements of a fiscal

responsibility framework are:o permanent policy rules such a limits on government

deficit, expenditures, debt, or borrowings,o procedural rules for public financial management such

as whether to prepare a medium-term budgetary plan and budgeting and audit processes;

o transparency standards (timely publication and comprehensive coverage of government accounts); and

o a monitoring and enforcement mechanism, usually supported by scrutiny from an independent agency.

o In essence a fiscal responsibility framework sets government on a path of budgetary policy pre-commitment which takes a legislative form.

transparency standards o Transparency’ is commonly understood as ‘government

according to fixed and published rules, on the basis of information and procedures that are accessible to the public’ (Hood 2001:701).

Public Financial Management and Accountability Systems

o The CIS-7 countries have been active participants in the Fund’s standards and codes initiative. Fiscal Reports on the Observance of Standards and Codes (ROSCs) have been completed for most countries

o In 2004, a high-level seminar was held at the Joint Vienna Institute, providing an opportunity for representatives from all CIS-7 countries to discuss past achievements and future challenges in improving fiscal transparency.

o Governance aspects of public finance received further examination in the World Bank’s Country Financial Accountability Assessments (CFAAs) and Country Procurement Assessment Reviews (CPARs). Both of these reports were prepared in 2000-03 for each of the countries and they are periodically updated. They evaluated the strength of budgetary and financial management, and public procurement arrangements, identifying key risks for public fundsand donor programs, and proposing measures to manage these risks.

o The governance and transparency reports have identified significant improvement of fiscal transparency and better publicfinancial management capacity across the CIS-7 countries in recent years.

Remaining deficiencies in PFMA

o Remaining deficiencies in transition economies include:

• weaknesses in budgetary execution and audit arrangements;

• non-transparent competitive procurement practices; • inadequate monitoring and evaluation in public

finance; • insufficient enforcement and incomplete legal

procurement provisions, with state-owned enterprises sometimes granted privileged status; and

• the lack of standard bidding documents and training programs.

The Objectives of an MTEFo improved macroeconomic balance, especially

fiscal discipline; o better inter- and intra-sectoral resource

allocation (escape from incremental budgeting) o greater budgetary predictability for line

ministrieso more efficient use of public monieso greater political accountability for public

expenditure outcomes through more legitimate decision making processes; and

o greater credibility of budgetary decision making (political restraint)

MTEFs extend budget horizons o MTEFs embody arrangements that require line

agencies to cost out more accurately their programs over the medium term, normally over three to four years. Such arrangement forces line agencies to reveal more of the true costs of their programs.

o One of the objectives of the MTEF is to extend the budget's horizon beyond a single fiscal year. Doing so depends on reliable projections of macroeconomic conditions, future revenue and spending if current policies were continued, and the impact of policy changes on future budgets

Top-down hard budget constraints o In conventional budgeting, fiscal targets are perennially

at risk of being overridden by spending pressures during preparation of the budget. In all budget systems, there is a tension between the budget's totals and its parts.

o The new theoretical literature (von Hagen looks at way to overcome this problem with better rule and institutions.)

o During expansionary periods, the parts (programs, departments, accounts, etc.) usually win out, with the result that by the end of the process the government agrees to spend more than it intended at the start.

o One objective of the MTEF is to prevent breach of the fiscal aggregates by insulating them from upward spending pressure from particular programs

o Hard budget constraints can be imposed ex ante and ex post and “above” and “below the line” in fiscal accounts This has been the approach of Brazil

How can an MTEF achieve PEM aims?

Fiscal (aggregate fiscal discipline)* to communicate:

- medium term fiscal policy & targets- policy of fiscal sustainability

and discipline policy makingAllocation (allocative efficiency)* to discipline decision making and highlight need for action byshowing:

-future costs of current policies-future costs of new policies and investments

* to communicate commitment to specific priorities through forward estimates and indicative medium term allocations

* to open up budget space to reallocate funds for new prioritiesResource Use (operational efficiency)* improve predictability of funding and policy for strategicplanning and management & operational performance at sector level

Three components of an MTEFo The MTEF consists of a “top-down” resource envelope, a

bottom-up estimation of the current and medium-term costs of existing policy and, ultimately, the matching of these costs with available resources in the context of the annual budget process.

o The “top-down resource envelope” is fundamentally a macroeconomic model that indicates fiscal targets and estimates revenues and expenditures, including government financial obligations and high cost government-wide programs such as pension liability coverage and civil service reform.

o To complement the macroeconomic model, the sectors engage in “bottom-up” reviews that begin by scrutinizing sector policies and activities (similar to the zero-based budgeting approach), with an eye toward optimizing intra-sectoral allocations. This requires a forum for contestability.

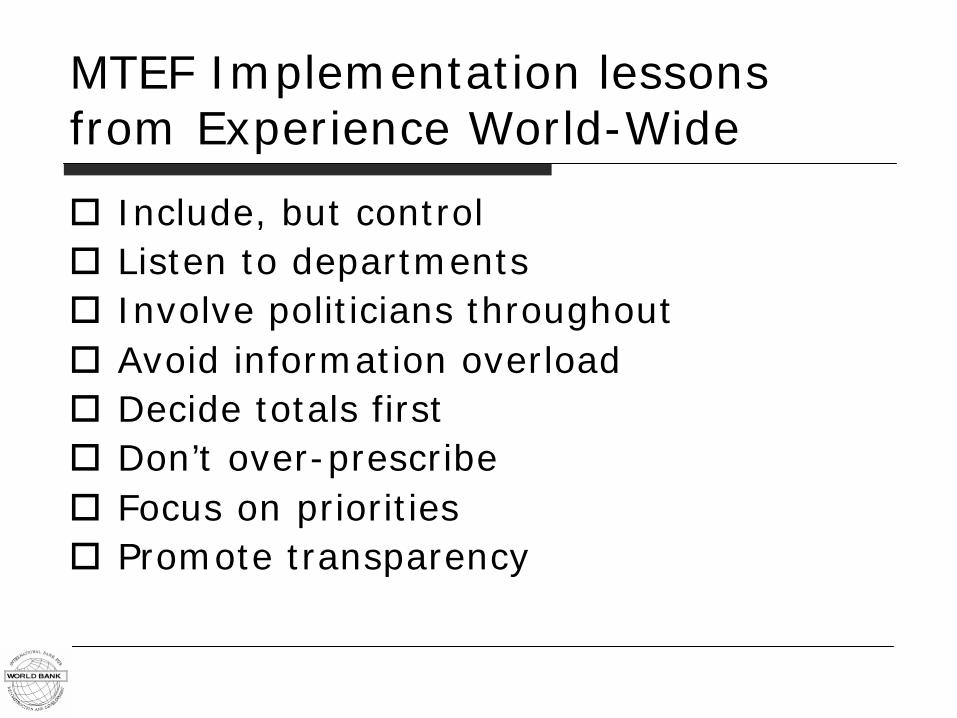

MTEF Implementation lessons from Experience World-Wide

o Include, but controlo Listen to departmentso Involve politicians throughouto Avoid information overloado Decide totals firsto Don’t over-prescribeo Focus on prioritieso Promote transparency

MTEF Implementation lessons from Experience World-Wide

o Initial conditions matter – budget basics enhance implementation of an MTEF BUT implementation can also help build these basics if carefully planned

o Integration across policy, planning & budgeting - bringing together the MTEF, annual budget process, National and Sector Plans, PRSP etc. – is a key factor in more mature systems.

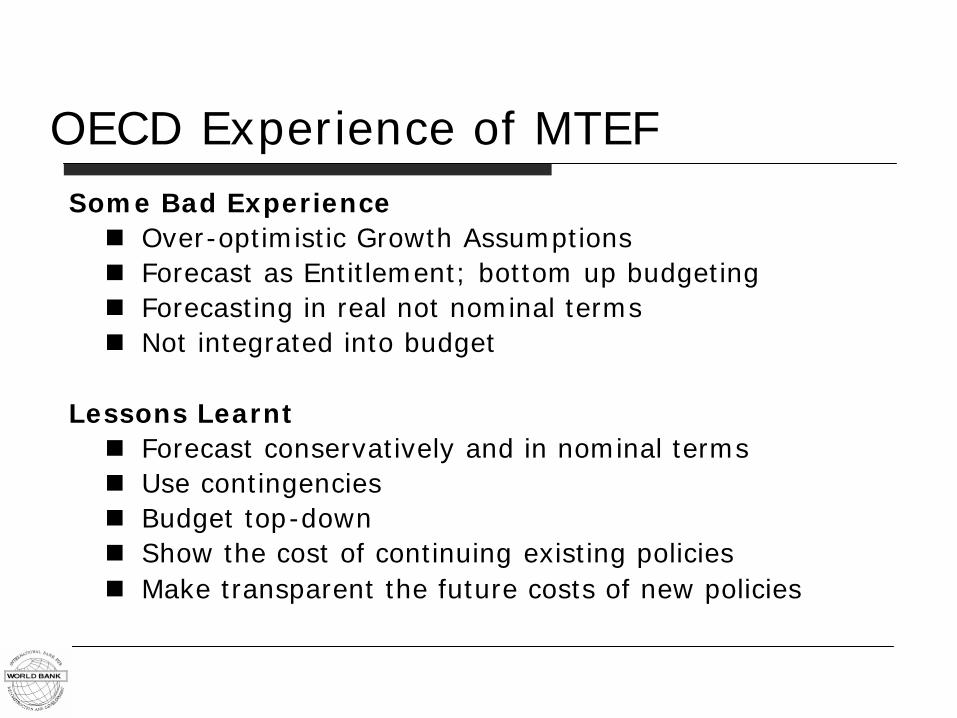

OECD Experience of MTEFSome Bad Experiencen Over-optimistic Growth Assumptionsn Forecast as Entitlement; bottom up budgetingn Forecasting in real not nominal termsn Not integrated into budget

Lessons Learntn Forecast conservatively and in nominal termsn Use contingenciesn Budget top-downn Show the cost of continuing existing policiesn Make transparent the future costs of new policies

Lessons in Implementationo MTEF n is designed to improve decision-making, and

focuses on budget formulation n will not solve all PEM problemsn is not a standardized product, per se. The principles

can be implemented in various waysn needs to be customized to the country, including

initial conditions in PEM, human and IT capacityn should be viewed as a multi-year exercise, built and

improved upon annually over yearso With MTEF, and Public Expenditure Management

reform generally, doing too much at once can overload the Government capacity and prevent progress on all reforms

Lessons for transition…o Strengthen performance accountability and

PFMA system (Public Financial Management and Accountability system)

o Clearly assign responsibilities of agencieso Transparent publication of budget and services

delivery plans and reportso Clear boundaries between public and private

sector institutionso Modernise systems and supply chain

managemento Rigorous planning and analysiso Public disclosure and National Assembly

Parliamentary debate

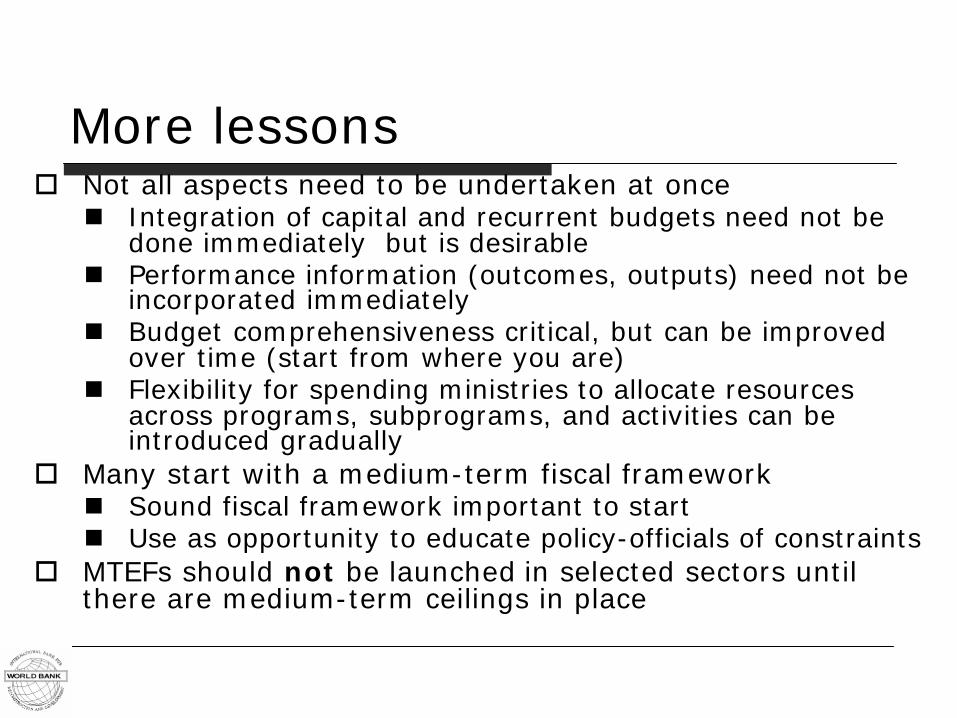

More lessons o Not all aspects need to be undertaken at oncen Integration of capital and recurrent budgets need not be

done immediately but is desirable n Performance information (outcomes, outputs) need not be

incorporated immediatelyn Budget comprehensiveness critical, but can be improved

over time (start from where you are)n Flexibility for spending ministries to allocate resources

across programs, subprograms, and activities can be introduced gradually

o Many start with a medium-term fiscal frameworkn Sound fiscal framework important to startn Use as opportunity to educate policy-officials of constraints

o MTEFs should not be launched in selected sectors until there are medium-term ceilings in place

And more lessonso Pressure on ministries to find resources within current

expenditures may be more successful whenn accounting systems are in place to provide good information n program and activity structure in place as focal point for

discussion, costingo Need not be contentious between line ministries and MoF/budget

office o Over-all, MTEF can be used to build consensus across government

actors o Consider legislatures role earlyn Educate them n Encourage good internal legislative decision processesn Clarify accountability roles including committees

How to implement?

o Identify major limiting factor firstn Policy-level – high-level decision processo Adequate policy-level input, ownership of budget?o Adequate trade-offs of major policy directions?o Adequate policy-level incentives?

n Technical – tools to support processo Unbundling MTEF technical aspectso Which aspect of the budget process needs to be

improved?

Actually three layers o Medium Term Fiscal Framework (MTFF)

n Achieve the right balance between economic development and macro-economic stability.

o Medium Term Budget Framework (MTBF)

o Medium Term Expenditure Framework (MTEF)

n Add programme & output based budgeting. This affords opportunity for comparing agreed output with actual output and identifying variances.

Unbundling MTEFs

Forecasting models. Stronger if relationships between macro growth, income distribution, and revenues understood and modeled in a formal manner. Debt sustainability analysis/model, or hard rule on debt/deficit limits.

Sets upward bound for expenditures, limiting deficits, inflation, and currency depreciations; supports sustainable fiscal policy, and realistic expenditure planning within the expenditure envelope; supports focus on adequate revenue mobilization.

Finance, Planning or Economy Ministry

Macrofiscal discipline

Multi-year revenue, debt sustainability analysis and debt policy, yielding expenditure envelope

Forecasting model, capacity, multi-year macro variable time series, .

Provides strategic framework for setting fiscal and monetary policy, and allows proactive fiscal adjustment to changing economic trends.

Finance, Planning or Economy Ministry

Macrofiscal discipline

Macroeconomic forecast

RequiresIntended EffectResponsible Agent

PEM Objective

Multi-year Feature

Unbundling MTEFs (2)

More credible if reflecting policy choices, which requires some explicit policy directions on reallocation. More effective in changing behavior if approved by cabinet or parliament.

Enabling more realistic planning, appropriate policies; incentive for reviewing existing programs for effectiveness, reallocations within sectors. At center, explicit trade-offs between sectors.

Finance, Planning or Economy Ministry

Allocational efficiency (sector),

Macrofiscal discipline, Operational efficiency

Multi-year ceilings for sector ministries

MoF provided inflators for pay, non-pay, and clear guidance for projecting costs. Can be automated. Can be budget year only, but more effective over several years.

Broad indicator of future cost of current spending trends, identification of potential risk areas, and proactive, measured, more rational fiscal adjustment. Baseline for evaluating policy spending choices.

Finance, Planning or Economy Ministry, or in some cases spending ministries with clear guidance

Macrofiscal discipline, Allocational efficiency (sector)

Multi-year forecast of spending under current policy or current level of services, by ministry or program

RequiresIntended EffectResponsible Agent

PEM Objective

Multi-year Feature

Unbundling MTEFs (3)

Requires guidance/training for spending ministry staff, and spending ministry staff capacity; MoF provision of common inflators for use by ministries (pay rates, non-pay, capital costs).

Identifies multi-year implications of new initiatives relative to their objectives, and assessment of whether they can be financed from within existing sectoral ceilings or even within aggregate spending ceilings, and if they are financially sustainable over time.

Spending Ministry

Operational efficiency, Allocational efficiency (sector), Macrofiscal discipline

Multi-year estimates of cost of new policies or programs(recurrent), or expansion of existing programs, prepared by sector ministries

Strategic planning capacity at sector ministry, information on outputs/outcomes of programs, and relationship to activities and inputs.

Sector strategic plan links outputs/outcomes with inputs in multi-year framework. Effective only if prepared within multi-year sectoral resource ceiling.

Spending Ministry

Allocational efficiency (sector), Operational efficiency, Macrofiscal discipline

Multi-year sector strategy

RequiresIntended EffectResponsible Agent

PEM Objective

Multi-year Feature

Unbundling MTEFs (4)

Trained staff at spending ministries, guidance on costing, understanding of project design and work flow.

Many capital budget processes already include such estimates, including the recurrent cost implications of new capital projects.

Spending Ministries

Operational efficiency, Allocational efficiency (sector), Macrofiscal discipline

Multi-year estimates of cost of new projects (capital), or expansion of existing projects, prepared by sector ministries

Can begin at program, and later move to subprogram and activity costing. Requires trained staff at spending ministries, agencies; MoF guidance and common inflators (pay rates, non-pay, capital costs).

Sensitizes sector ministry to cost drivers, affordability of existing policy or programs, attention to different means of attaining objectives,unit cost.

Spending Ministries

Operational efficiency, Allocational efficiency (sector), Macrofiscal discipline

Multi-year estimates of cost of existingpolicies, programs, subprograms, or activities prepared by sector ministries

RequiresIntended EffectResponsible Agent

PEM Objective

Multi-year Feature

Sequencing MTEFso Not all aspects need to be undertaken at oncen Integration of capital and recurrent budgets need not

be done immediately n Performance information (outcomes, outputs) need not

be incorporated immediatelyn Budget comprehensiveness critical, but can be

improved over time (start from where you are)n Flexibility for spending ministries to allocate resources

across programs, subprograms, and activities can be introduced gradually

o Many start with a medium-term fiscal frameworkn Sound fiscal framework important to startn Use as opportunity to educate policy-officials of

constraintso MTEFs should not be launched in selected sectors until

there are medium-term ceilings in place )

Performance Budgeting and Management

o Trying to assess whether programs are working, or can work better

oMeasuring performance, producing informationn Using the information

o Changing incentives of actors in systemo Performance information kept hidden does not

change incentives - Information must flowo see Matthew Andrews Performance–Based

budgeting Reform chapter 2 in Shah Book

Implementing effective performance monitoring requires:

o Setting organizational incentives to support performance monitoringn Predictable fundingn Flexible resource application at program level

o Getting performance monitoring consistent with organizational culture

o Need for central unit to play active and effective leadership role in defining criteria and implementing practical performance monitoringn May not be MoF or Budget Office!!

South Africa Background

o Parliamentary system, limited legislative involvement, but high capacity, transparency and accountability

o Unitary state, subnational involvedoMiddle income countryo Political stabilityo Relatively high capacity, but generally limited

to center (versus ministries, provinces, municipalities)

o Decent national FMIS, but limited at subnational

oMTEF focus on allocation and technical efficiencyn First MTEF failed due in part to complexity

South Africa: overall assessmento Stage 1 macrofiscaln Treasury dominates, technical and policyn Prudent policies pursued

o Stage 2 sectoral allocationn Cabinet subcommittee reviewed, cabinet

approvedn Program budgets help

o Stages 3-5n Collegial approach from beginning make

this less contentious, raise issues early

Implementing effective performance monitoring requires:o Setting organizational incentives to support

performance monitoringn Predictable fundingn Flexible resource application at program level

o Getting performance monitoring consistent with organizational culture

o Need for central unit to play active and effective leadership role in defining criteria and implementing practical performance monitoringn May not be MoF or Budget Office!! (US NPR,

UK)

South Africa Background

o Parliamentary system, limited legislative involvement, but high capacity, transparency and accountability

o Unitary state, subnational involvedoMiddle income countryo Political stabilityo Relatively high capacity, but generally limited

to center (versus ministries, provinces, municipalities)

o Decent national FMIS, but limited at subnational

oMTEF focus on allocation and technical efficiencyn First MTEF failed due in part to complexity

South Africa: overall assessmento Stage 1 macrofiscaln Treasury dominates, technical and policyn Prudent policies pursued

o Stage 2 sectoral allocationn Cabinet subcommittee reviewed, cabinet

approvedn Program budgets help

o Stages 3-5n Collegial approach from beginning make

this less contentious, raise issues early

South Africa in more detail -Building consensus

ReviewTeams

Ministers’Committee

Cabinet

Implications of baselinesPolicy options

Recommended allocationsPolicy choices

Treasury/(i.e. finance)

Affordable totalsMenu of choicesRecommendations

MTEF

BaselinesMembership

The Baseline –it is importanto In the MTEF, the baseline is used both to establish the fiscal

framework and to determine whether expenditure changes are consistent with the framework. Inasmuch as future conditions are not yet known, the baseline and estimates of policy change are grounded on assumptions concerning economic performance, the behavioral responses of persons affected by policy changes, and other variables.

o Countries which use baselines to establish and enforce expenditure frameworks, such as SA, must have rules for how the projections are made and policy changes are measured as well as procedures for dealing with deviations from the baseline. They must also assign responsibility for maintaining the baseline and assuring that policy changes are accurately measured against it. In a few countries, managing the baseline and related controls has become the finance ministry's most important budget responsibility.

Fiscal trends in South Africa

0%

2%

4%

6%

8%

10%

12%

1994

/95

1995

/96

1996

/97

1997

/98

1998

/99

1999

/00

2000

/01

2001

/02

2002

/03

2003

/04

Personal income tax Corporate income tax Value-added tax Levies on fuel

Tax as % of GDP

South Africa Fiscal trends

5,4%5,1%

4,7%

4,1%

3,6%3,7%3,8%3,9%

5,7%5,5%5,2%

0,0%

0,5%

1,0%

1,5%

2,0%

2,5%

3,0%

3,5%

4,0%

4,5%

5,0%

5,5%

6,0%

1996/97 1998/99 2000/01 2002/03 2004/05 2006/07

Debt service costs as % of GDP