brussels – may 24th 2014 -...

TRANSCRIPT

Brussels – May 24th 2014

Real estate as investment Own property (“direct”)

Review Market situation / Situation as of today / Future ? Disadvantages of “direct” real estate

Investment property (“indirect”) Key characteristics

Investing “directly” or “indirectly” in real estate ?

REIT

Montea

Review market situation over the past 20 years

Property in Belgium was too cheap compared to our neighbours

Historically low interest rate

Mortgage loans were more flexible:

Longer terms Lower % ownership in mortgage credit Higher % disponsable income on mortgage loan

Situation as of today

Banks will be stricter thus:

Terms of loans is shortened % Ownership in the mortgage loan wil be increased % Lower reimbursement compared to available family income

Low interest rates

Future ?

⇒ Property prices will stabilize, no further significant increase or decrease

⇒ Young families will decide only later to purchase their first home and come thus back on the rental market

⇒ Rental market recovers

⇒ Retaining of residential real estate for rent is (again) more interesting

⇒ Property prices will stabilize, no further significant increase or decrease

Operational follow-up Stricter regulations Maintenance & renovation Unpaid invoices, forced house move, ...

Risk focused on one or a few properties

Heavy entry and exit costs because of high registration fees

Tax on property after 2014?

Disadvantages of “direct” real estate

Investing “indirectly” in real estate property

Investing in real estate companies Shares

Liquidity

Market risk

Possible dividend

Operational structure by specialists

Real Estate Investment Trust

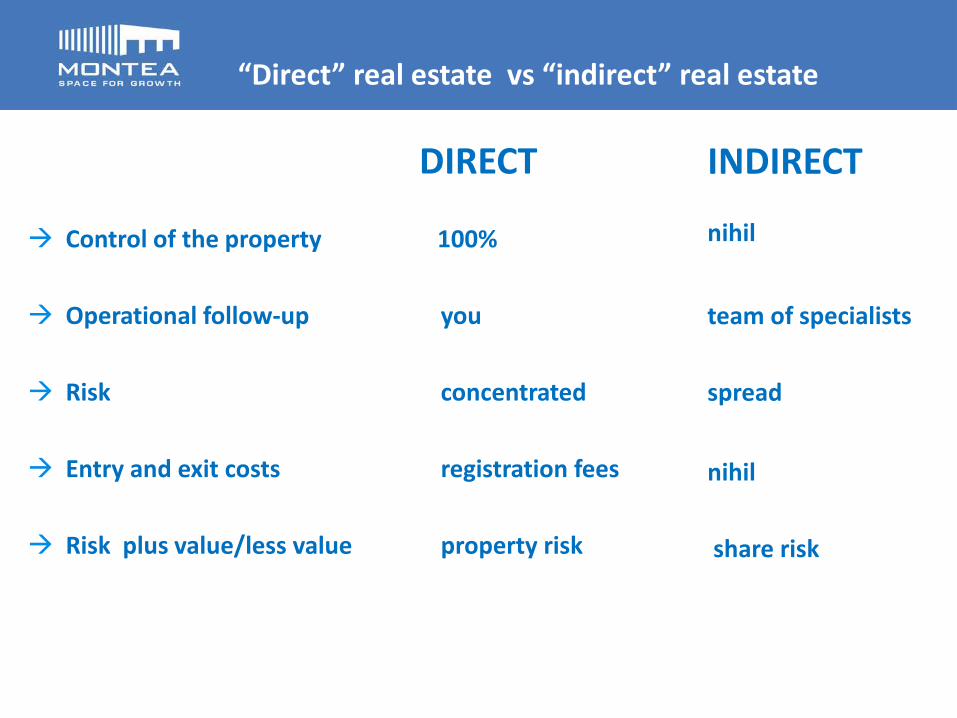

DIRECT Control of the property 100%

Operational follow-up you

Risk concentrated

Entry and exit costs registration fees

Risk plus value/less value property risk

“Direct” real estate vs “indirect” real estate

INDIRECT nihil

team of specialists spread

nihil share risk

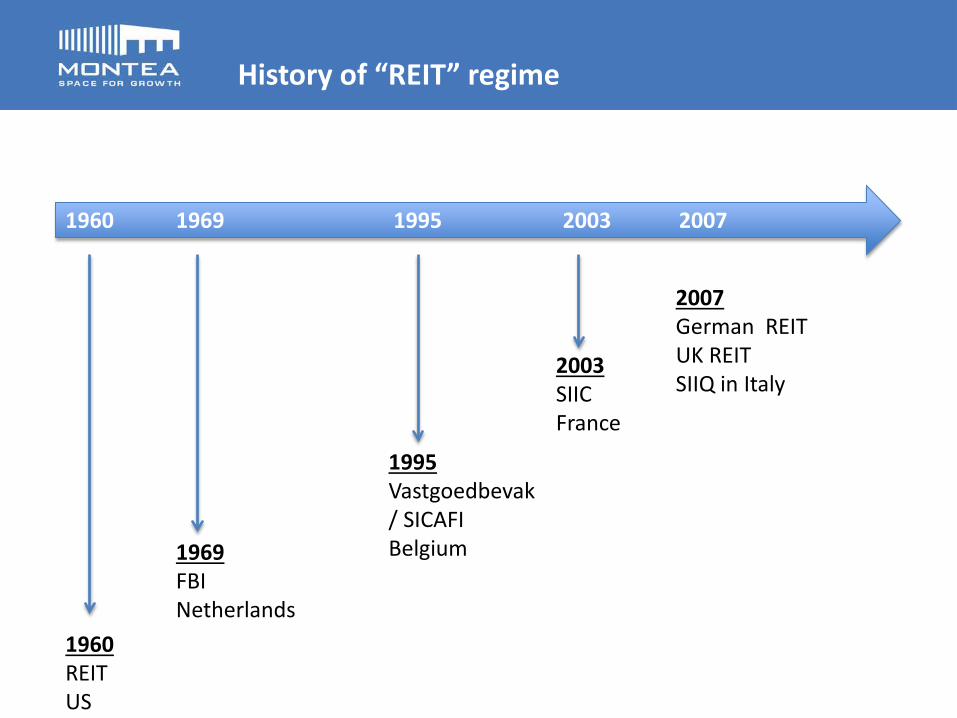

History of “REIT” regime

1960 1969 1995 2003 2007

1960 REIT US

1969 FBI Netherlands

1995 Vastgoedbevak / SICAFI Belgium

2003 SIIC France

2007 German REIT UK REIT SIIQ in Italy

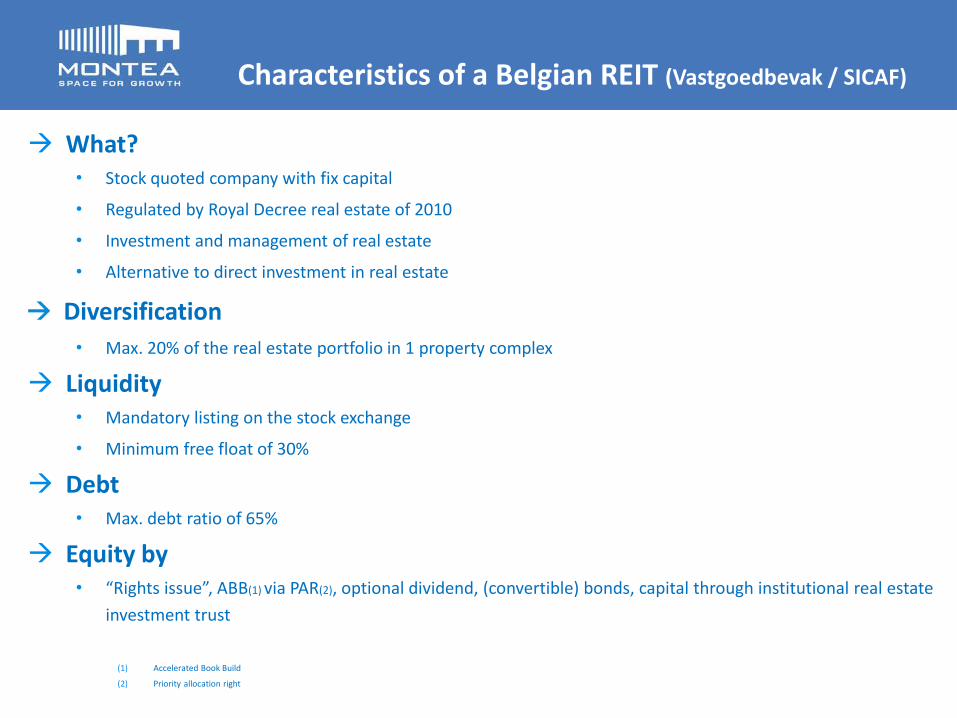

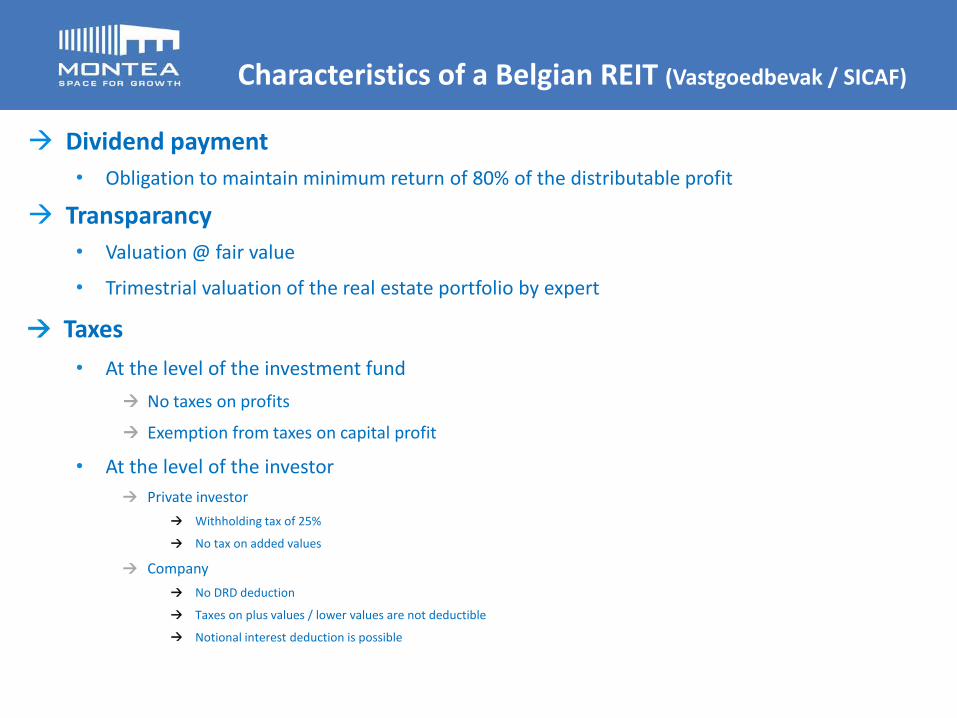

Characteristics of a Belgian REIT (Vastgoedbevak / SICAF)

What? • Stock quoted company with fix capital

• Regulated by Royal Decree real estate of 2010

• Investment and management of real estate

• Alternative to direct investment in real estate

Diversification • Max. 20% of the real estate portfolio in 1 property complex

Liquidity • Mandatory listing on the stock exchange

• Minimum free float of 30%

Debt • Max. debt ratio of 65%

Equity by • “Rights issue”, ABB(1) via PAR(2), optional dividend, (convertible) bonds, capital through institutional real estate

investment trust

(1) Accelerated Book Build

(2) Priority allocation right

Dividend payment • Obligation to maintain minimum return of 80% of the distributable profit

Transparancy • Valuation @ fair value

• Trimestrial valuation of the real estate portfolio by expert

Taxes • At the level of the investment fund

No taxes on profits

Exemption from taxes on capital profit

• At the level of the investor Private investor

Withholding tax of 25%

No tax on added values

Company No DRD deduction

Taxes on plus values / lower values are not deductible

Notional interest deduction is possible

Characteristics of a Belgian REIT (Vastgoedbevak / SICAF)

“Total Gross Return” over 10 years

0

50

100

150

200

250

300

350

Dec-03

Apr-04

Aug-04

Dec-04

Apr-05

Aug-05

Dec-05

Apr-06

Aug-06

Dec-06

Apr-07

Aug-07

Dec-07

Apr-08

Aug-08

Dec-08

Apr-09

Aug-09

Dec-09

Apr-10

Aug-10

Dec-10

Apr-11

Aug-11

Dec-11

Apr-12

Aug-12

Dec-12

Apr-13

Aug-13

Belgian REITs Bel20 MSCI Europe EPRA European bonds

Source: Bank De Groof

13

Specialists vs Generalists

Offices in Brussels

Logistics in NL, BE and FR

Residential

Retail

Logistics & retail, offices, BE & Lux

Offices & logistics

Offices & retail

Everything & more

0

50

100

150

200

250

300

350

400

Dec-03

Apr-04

Aug-04

Dec-04

Apr-05

Aug-05

Dec-05

Apr-06

Aug-06

Dec-06

Apr-07

Aug-07

Dec-07

Apr-08

Aug-08

Dec-08

Apr-09

Aug-09

Dec-09

Apr-10

Aug-10

Dec-10

Apr-11

Aug-11

Dec-11

Apr-12

Aug-12

Dec-12

Apr-13

Aug-13

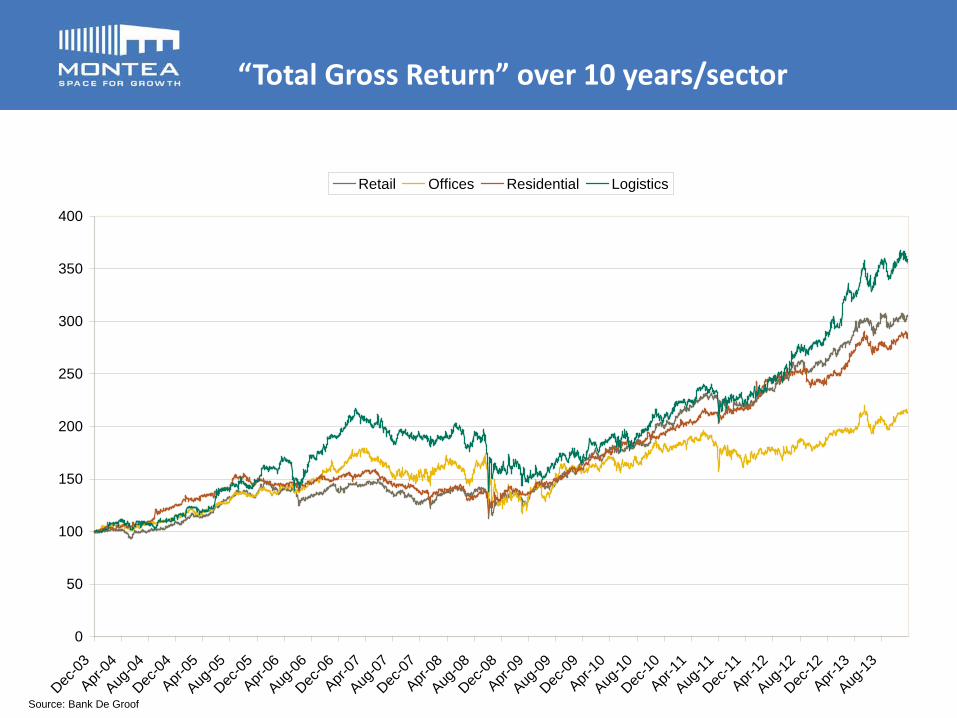

Retail Offices Residential Logistics

Source: Bank De Groof

“Total Gross Return” over 10 years/sector

Share price increased with 11,4% compared to last year (2012 increase was 15,8%)

Premium of 41%

velocity + 23% (yearly volume / avg. number of shares over period)

gross dividend yield of 6,2% / 18,5% gross return over 2013 / 9,5% over lifetime of Montea (Gross return = variance in share price + gross dividend devided by closing rate of last year)

0

20

40

60

80

100

120

140

160

180

200

Montea EPRA BEL20 MSCI Europe European bonds

Total gross return over 7 years (*)

(*) Source: Bank De Groof

Calculated on Bloomberg data as of 04/12/2013. “Gross Total Returns” include the reinvestment of gross dividend proceeds

Strong performance of Montea in stock market

Montea – Space for Growth

REIT (Sicafi - SIIC) listed on the NYSE Euronext Brussels & Paris since Oct. 2006

Development & Management of Logistic Real Estate Solutions …

… in Belgium, France and the Netherlands

FV Portfolio of 320m (*)

Market Cap. of EUR 216m (*)

(*) per 31/12/2013

17

Family De Pauw

21%

Belfius Insurance

13%

Banimmo

12% Federale Verzekering

10%

Family De Smet

4%

Free Float

39%

Warehousing • Land value has a higher share in the total

value than in other asset classes

• Life cycle of warehousing > other asset classes

• Renovation cost < than other RE asset classes

Pure player • Ambition to be best in class through

specialisation (Logistics, Real Estate & Finance)

• Ambition to be top of mind towards other market players (logistic players, brokers ...)

End investor No speculative development: therefore possible business partner for land owners and developers. Long term vision with focus on quality & sustainability (for example Blue Label)

400€/m²

45€/m²

200€/m²

Cost Logistic Development Prime Rent

Cost Land

Cost Development7,5%

2m² land for 1m² logistic development

3 key words

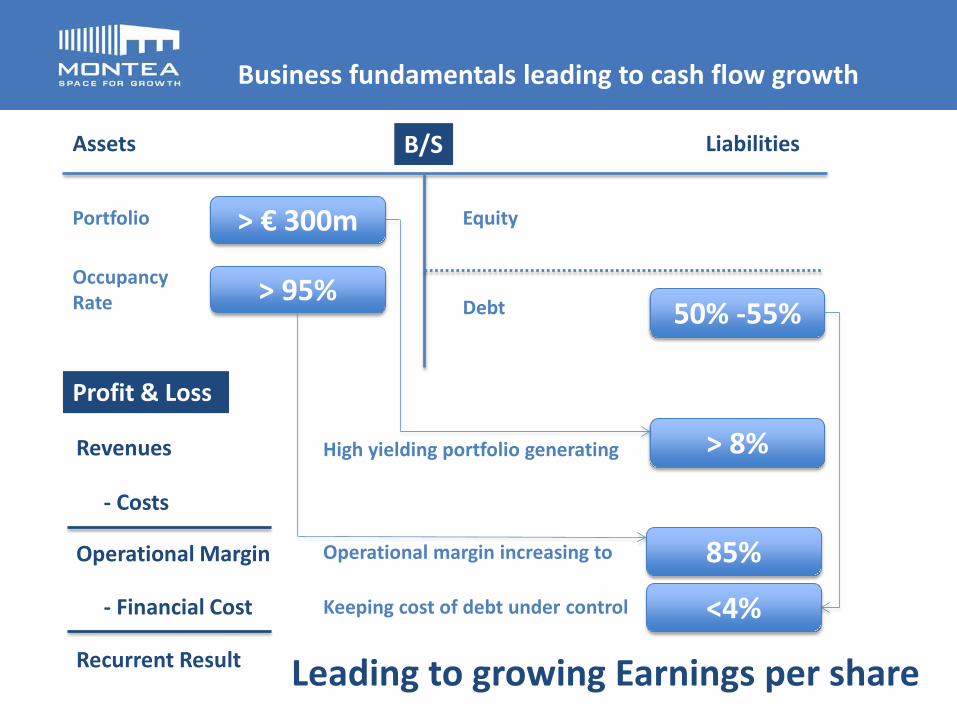

Assets Liabilities

Revenues

Occupancy Rate

Portfolio

B/S

Profit & Loss

- Costs

Operational Margin

- Financial Cost

Recurrent Result

Equity

Debt > 95%

85% Operational margin increasing to

> € 300m

> 8% High yielding portfolio generating

<4% Keeping cost of debt under control

50% -55%

Leading to growing Earnings per share

Business fundamentals leading to cash flow growth

Debt ratio of 52,8%

“Interest coverage ratio” of 3,21

Finance charge of 3,96% @ YE

Creditline138,0 79%

Leasing 5,0 3%

Bond; 29,6 18%

Composition of financial debts (€ K) EUR 172,6m

26,7

50,0

26,7 40,0

26,7

2014 2015 2016 2017 2018

Refinancing of Creditines (€ m)

Belfius 25%

ING 29%

KBC 18%

BNP Paribas Fortis 25%

Bank De Groof

3%

Composition of creditlines (%) EUR 138m

Total of EUR 160 m EUR 22m undrawn

20

Maturity of total debt of 3,2 years

Maturity of “IRS”-contracts of 5,8 years

“Hedge Ratio” of 82,2%

Solid financial structure – Debt financing

21

Highlights – Investment Activity of EUR 40,6 m

Netherlands + EUR 14,3m (*)

Almere –Aware Food Group– EUR 14,3m (*)

First investment in Dutch market

24.000m² warehouse / 700m² Offices

22y lease

22 (*) Fair Value @ 31/12/2013

Highlights – Investment Activity of EUR 40,6 m

BELGIUM Puurs, Schoonmansveld 13.252 m² Nijvel 11.000 m² Puurs, Rijksweg 12.000 m² Vorst 23.514 m²

FRANCE Savigny-le-Têmple 15.000 m² Feuquières-en-Vimeu 20.830 m² Bondoufle 3.000 m²

Portfolio -> 100.000 m² development potential on existing sites

23

Partnership agreement with MG Real Estate Development of Logistics Park MG De Hulst

Partnership in bundling commercial efforts & development cost

Reference for sustainable logistics park

Total of 40 ha

Development potential of 150.000 m² / Estimated investment volume of EUR 120 mio

Highlights – Development potential

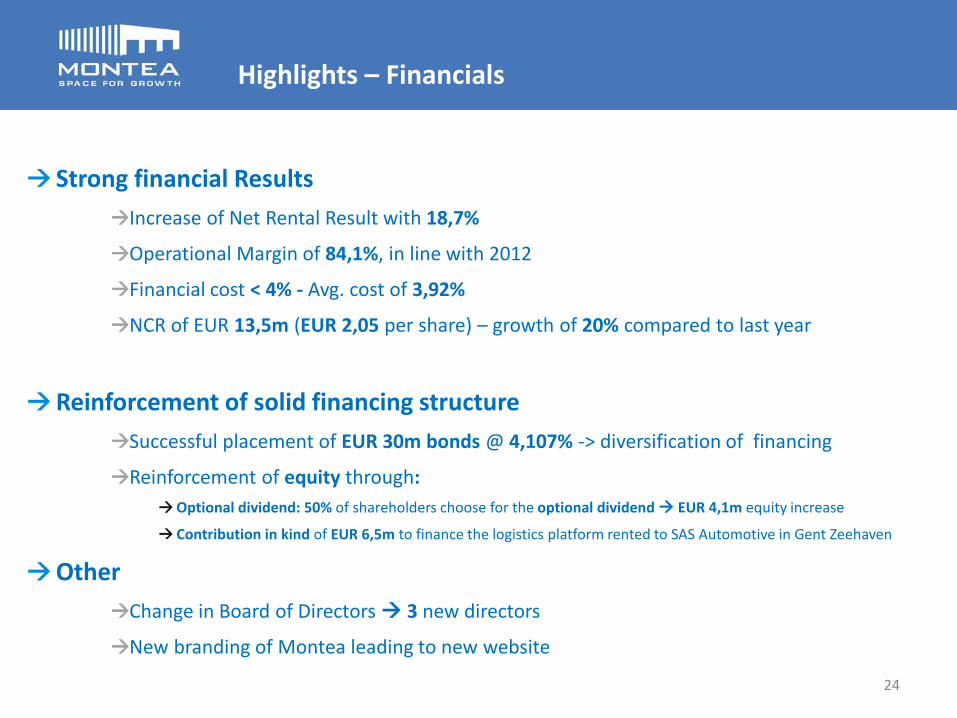

Strong financial Results Increase of Net Rental Result with 18,7%

Operational Margin of 84,1%, in line with 2012

Financial cost < 4% - Avg. cost of 3,92%

NCR of EUR 13,5m (EUR 2,05 per share) – growth of 20% compared to last year

Reinforcement of solid financing structure Successful placement of EUR 30m bonds @ 4,107% -> diversification of financing

Reinforcement of equity through: Optional dividend: 50% of shareholders choose for the optional dividend EUR 4,1m equity increase

Contribution in kind of EUR 6,5m to finance the logistics platform rented to SAS Automotive in Gent Zeehaven

Other Change in Board of Directors 3 new directors

New branding of Montea leading to new website

24

Highlights – Financials

2,22 2,36

2,08

1,79 1,82

2,00 2,05 1,99 2,09 2,09

1,84 1,84 1,93 1,97

2007 2008 2009 2010 2011 2012 2013

Evolution of Net Current Result & Dividend

5,9%

6,8%

8,5%

7,7%

7,5%

6,8%

(1) 1,84 is the add-up of EUR 0,97 per share for the first half of 2010 (before the capital increaese) and EUR 0,87 per share for the 2nd half of 2010 (after the capital increase)

(1)

25

6,2%

+2,5% +2,1%

Distribution%

96,5% Distibution%

96,1%

Evolution of NCR and dividend (€/share)

27

Kissing is like real estate. The most important thing is

28

Kissing is like real estate. The most important thing is

Location Location

LOCATION

29

European logistics map

180 58%

118 38%

14 5%

Nr of sites: 35 Fair Value (€m): 311,94 m²: 584.694 Contractual Rent k€): 26,1 Occupancy rate (*): 94,9% Yield (**): 8,7%

Nr of sites: 1 Fair Value (€m): 14 m²: 25.848 Contractual Rent €m): 1,2 Occupancy rate (*) : 100,0% Yield (**): 7,6%

Nr of sites: 19 Fair Value (€m): 180 m²: 340.181 Contractual Rent €m): 14,1 Occupancy rate (*) : 90,9% Yield (**): 8,3%

Nr of sites: 15 Fair Value (€m): 118 m²: 218.666 Contractual Rent €m): 10,8 Occupancy rate (*) : 100,0% Yield (**): 8,6%

(*) At the end of the period based upon m²

(**) (Contractual yearly income + ERV on vacancy) devided by the investment value

Portfolio in Belgium, France & the Netherlands

31

101 124

157 152 140 145 165 180

13

54 54 92 102

118 118

14

8

8

8

101 137

211 206 232

255 291

320

okt/06 2007 2008 2009 2010 2011 2012 2013

Belgium France Netherlands Solar Panels Total

+225%

Portfolio growth with > 225% since IPO

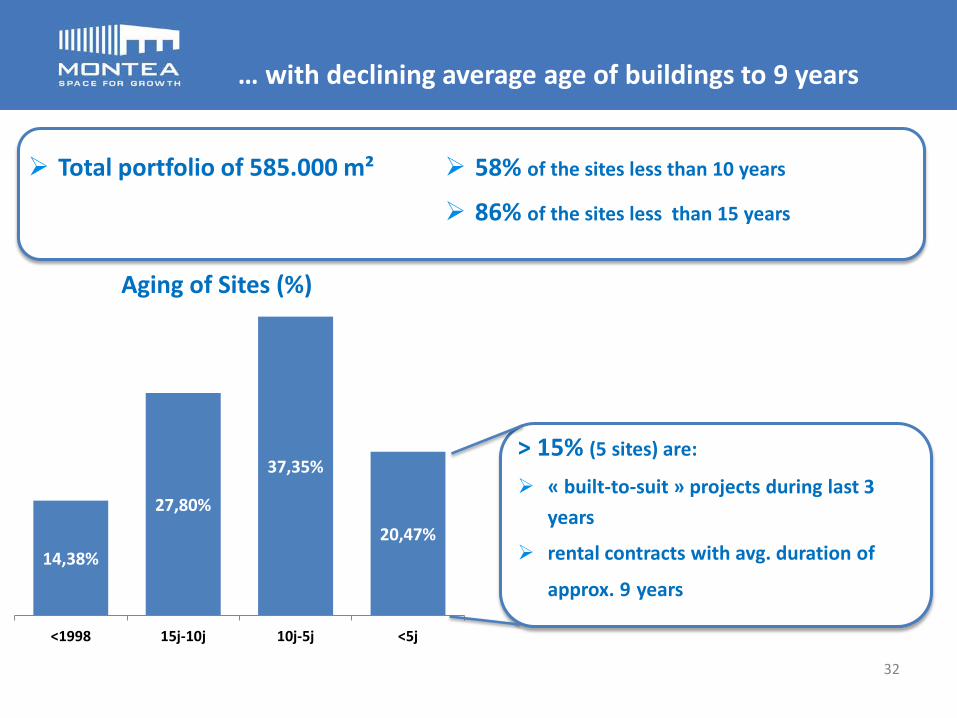

14,38%

27,80%

37,35%

20,47%

<1998 15j-10j 10j-5j <5j

Aging of Sites (%)

Total portfolio of 585.000 m²

32

> 15% (5 sites) are:

« built-to-suit » projects during last 3 years

rental contracts with avg. duration of

approx. 9 years

58% of the sites less than 10 years

86% of the sites less than 15 years

… with declining average age of buildings to 9 years

VDAB

45% 55%

End- users

Logistic Players

Break-down by type Tenant

Top 15 customer for > 70% of rental income

13,1%

12,8%

4,5%

4,3% 4,2% 3,6%

3,4%

3,2%

3,0%

3,0%

2,5%

2,5%

2,4%

2,4% 2,3%

2,2% 2,2%

88%

Semi- Industrial

Logistic

Break-down by type Site

72% > EUR 500K Yearly Rental Income

Total of 61 customers

with a high qualitative client portfolio

96,6% 95,6% 92,9%

95,1% 96,5% 96,3% 94,9%

2007 2008 2009 2010 2011 2012 2013

Long term Target: > 95,0% (1)

(1) At the end of the period based upon m²

(2) Untill first break

5,3

2013Excl. Solar panels Impact Solar Panels

Long term Target: > 6y (2)

5,7

Historical occupancy rate > 95% 28.000m² vacancy in Belgium

due to 2 sites: Herentals Nijvel

Logistics business knows by 3,6,9 contracts

Increased from 3,5 years in 2010

Mix between End users & Logistics players

34

with occupancy & maturity under control

35

101 124 157 152 140 145 165 180

236 13

54 54 92 102 118

118

119 14

41

8 8

8

7 20

101 137

211 206 232 255

291 320

423

okt/06 2007 2008 2009 2010 2011 2012 2013 2014

Belgium France Netherlands Solar Panels Ambition Total

And ambition to grow portfolio in 2014 with > 30%

36

Decision by Office Depot to centralise the activities in the Netherlands Commercialisation by Montea and, upon rental agreement with new client, acquire this site at the latest in March 2014 If not rented, rental guarantee for 9 months 12.000 m² warehouses en 2.000 m² offices Investment value of EUR 7,9m Investment yield of 8,15%

Logistics Distribution center on total surface of 25.800m² Waddinxveen - very well located logistics hub near Rotterdam 14,875m² distribution center / 2,500m² mezzanine / 1,040m² offices Development potential of 6.000m² 15 years fixed contract with Deltawines – international distribution of wines

2nd Investment in the Netherlands Finalisation of Investment in Puurs

Investments already in Q1-2104 …

37

In December 2013, Montea signed a partnership agreement with MG Real Estate (De Paepe Group) to develop the “MG Park De Hulst” sustainable logistics park in Willebroek. The partners have announced their first joint development (Cross-dock building) with the project for Dachser. 6.800 m² warehouses / 2.300 m² offices in 1st phase Tenant: Dachser - 20 years fixed rental contract Investment value of EUR 12,8m Investment yield of 7,5%

1st built-to-suit project on recently announced cooperation with Group De Paepe on Park De Hulst in Willebroek

Further growth in 2014

38

Partnership agreement with Van der Maazen Bouwbedrijf for the development of a sustainable 25,600 m² BtS-project in Oss (NL). Tenant: Vos Logistics – 7 years fixed rental contract 24.300 m² warehouses / 680 m² offices / 800 m² mezzanine Investment value of EUR 12,9m Investment yield of 7,9%

Redevelopment of site of Unilever Development of 3.500m² warehouse Operational by September 1st 2014 Tenant: Metro – 27 years fixed rental contract Investment value of EUR 3,8m(excl. land value) Investment yield of 7,6%

Redevelopment of Unilever site Built-to-suit project in the Netherlands

Further growth in 2014

19/02/2014 – Announcement of Rental Agreement with Caterpillar Distribution Services Europe •9 years contract beginning @ january 1st 2015

•DHL leaving site in March 2014

•Redevelopment of site (29,500m² warehouses + 2,350m² offices + extension of 30,000m²)

•50-50 with WDP

39

Further growth in 2014 – redevelopment of Grimbergen

40

Growth in 2014

Further development of Park De Hulst Willebroek (based upon partnership agreement) BTS of 13.065m² warehouse / 1.000 offices Operational by November 1st 2014 Tenant: US based packaging multinational – 9,6/15 years contract Investment value of EUR 9,6m Investment yield of 7,5%

Further development of Park De Hulst Willebroek (based upon partnership agreement) BTS of 19.000m² warehouse / 500m² offices Operational by September 1st 2014 Tenant: Neovia – 5/10 years contract (Logistics provider of Caterpillar) Investment value of EUR 13,3m Investment yield of 8,1%

2nd built-to-suit project on De Hulst 3rd built-to-suit project on De Hulst

41

2014 2013 2012

Portfolio Fair Value (€m) > 420 m 319,3 291,6

Occupancy (based upon m²) (%) 95% 94,9 96,3

Avg. Duration (excl. IAS 39) (y) 6y 5,7 5,6

Yield (%) if 100% rented 8,35 7,94

P&L Net Rental Result (€m) 23,7 19,9

Operational Margin (%) 85,0 84,1 84,1

Financial Cost (%) <4,00 3,94 3,84

Net Current Result (€m) +14,8 13,5 11,25

Net Current result / share (€) 2,05 2,00

B/S NAV / share (excl. IAS 39) (€) 22,43 22,17

Stock rate (€) 31,65 28,40

Debt Ratio (%) 55,0 52,8 51,3

+10%

+19%

+20%

+11% +11%

+10%

+30%

Leading to an Ambition for 2014 of …

Site Mechelen

“We literally offer our clients the

“space to grow” through flexible, innovative property solutions.

Growth is the goal we share with our clients, investors and partners.”