broward county bb&t center arena alternative use case studies ... atlanta-sandy springs et al,...

TRANSCRIPT

BROWARD COUNTY BB&T CENTER

MARKET AND FINANCIAL ANALYSIS OF BB&T CENTER WITHOUT THE FLORIDA

PANTHERS

PREPARED BY: STIFEL, NICOLAUS & COMPANY, INC.

BARRETT SPORTS GROUP, LLC

OCTOBER 13, 2015

Page 1

I. INTRODUCTION

II. EXECUTIVE SUMMARY

III. BB&T CENTER OVERVIEW

IV. MARKET ANALYSIS

V. FINANCIAL ANALYSIS

VI. ECONOMIC IMPACT ANALYSIS

VII. POTENTIAL FUNDING OPTIONS

VIII. OTHER CONSIDERATIONS APPENDIX A: COMPARABLE ARENAS – CASE STUDIES APPENDIX B: COMPARABLE ARENAS – DEMOGRAPHICS APPENDIX C: FINANCIAL ANALYSIS – 15 YEAR ESTIMATE LIMITING CONDITIONS AND ASSUMPTIONS

TABLE OF CONTENTS

I. INTRODUCTION

Page 3

Overview

Stifel, Nicolaus & Company, Inc. and Barrett Sports Group, LLC (Hereinafter Referred to as the Consulting Team) are Pleased to Present Our Preliminary Findings and Observations to Broward County (County) – Initial Draft Prepared as of March 12, 2015

The Consulting Team was Retained by the County to Provide Financial Advisory Services in Connection with the BB&T Center (or Arena) and to Assist the County in On-Going Discussions with the Florida Panthers (Panthers)

It has been Well Reported that the Panthers have Experienced Financial Difficulties and New Ownership is Seeking Arena Lease Concessions/Relief from the County

As Part of the County’s Due Diligence Process, the Consulting Team was Asked to Examine the Potential Performance of the BB&T Center in the Event the Panthers are No Longer a Tenant in the Arena

It Should be Noted that the Findings Herein are Somewhat Limited Since the Contract Scope of Services Did Not Include Market Surveys and/or Focus Group Sessions – Consideration Could be Given to Completing these Tasks in the Future

I . INTRODUCTION

Page 4

Completed Tasks

The Consulting Team Completed the Following Major Tasks (Assuming Panthers No Longer a Tenant) Demographic Overview Comparable Market Analysis Competitive Market Analysis Reviewed BB&T Center Historical Performance and Key Agreements Reviewed Historical Performance of Comparable Facilities Considered Potential Arena Users Interviewed Representatives of Potential Arena Users Interviewed Local/Regional/National Promoters Developed Arena Operating Profile (Events/Attendance/Etc.) Prepared Arena Financial Analysis (Including Sensitivities) Completed Economic/Fiscal Impact Analysis Conducted On-Site Surveys to Estimate Out-of-Arena Spending

Provided Overview of Arena Management Options Prepared Arena Alternative Use Case Studies Reviewed Recent NHL/NBA Restructured Lease Agreements Identified Potential Sources to Fund Operations Debt Service Capital Repairs/Maintenance

I . INTRODUCTION

II. EXECUTIVE SUMMARY

Page 6

BB&T Center Overview – Background

The BB&T Center is Owned by the County and Operated by Arena Operating Company, Ltd. (AOC), an Affiliate of the Panthers, and Subsidiary of Sunrise Sports & Entertainment (SS&E)

Arena Opened in 1998 at a Total Development Cost of Approximately $221.1 Million (Including Cost Overruns and Financing Costs)

Arena Located Adjacent to the Sawgrass Mills Mall in a Developed Commercial and Residential Area

Arena Designed for Professional Hockey, Sports, Entertainment, and Other Community Events

BB&T Center Characteristics

872,000 Square Feet 20,763 Seats (Maximum) / 19,250 (Hockey) 72 Suites & Loge Boxes / Up to 3,121 Club Seats 7,200 Parking Spaces

Since 1998, Arena has had Several Different Names (National Car Rental Center, Office Depot

Center, BankAtlantic Center)

II. EXECUTIVE SUMMARY

Page 7

BB&T Center Overview – Summary of Major Agreements

Arena is Operated by AOC and is Governed by the 1996 Operating Agreement with County that Expires in 2028

The Team License Agreement also Expires in 2028 and Includes Certain Non-Relocation Provisions

AOC and Live Nation have a Booking Agreement that Provides Live Nation Certain Rights as the Preferred Promoter for Arena Events. The Agreement Expires in 2018.

Arena Concessionaire is Centerplate and the Agreement Expires in 2022

Ticketmaster Provides Ticketing Services for Arena through an Agreement that Expires in 2016

The Naming Rights Partner is BB&T, whose Sponsorship Agreement Runs through 2022

Luxury Suite Contracts Generally Expire by 2017 and Club Seat Contracts Generally Expire by 2016

Major Agreements Generally Contain Provisions Allowing for Termination in the Event of Material Changes to the Conditions at the Arena, Such as Departure of the NHL Tenant

II. EXECUTIVE SUMMARY

Page 8

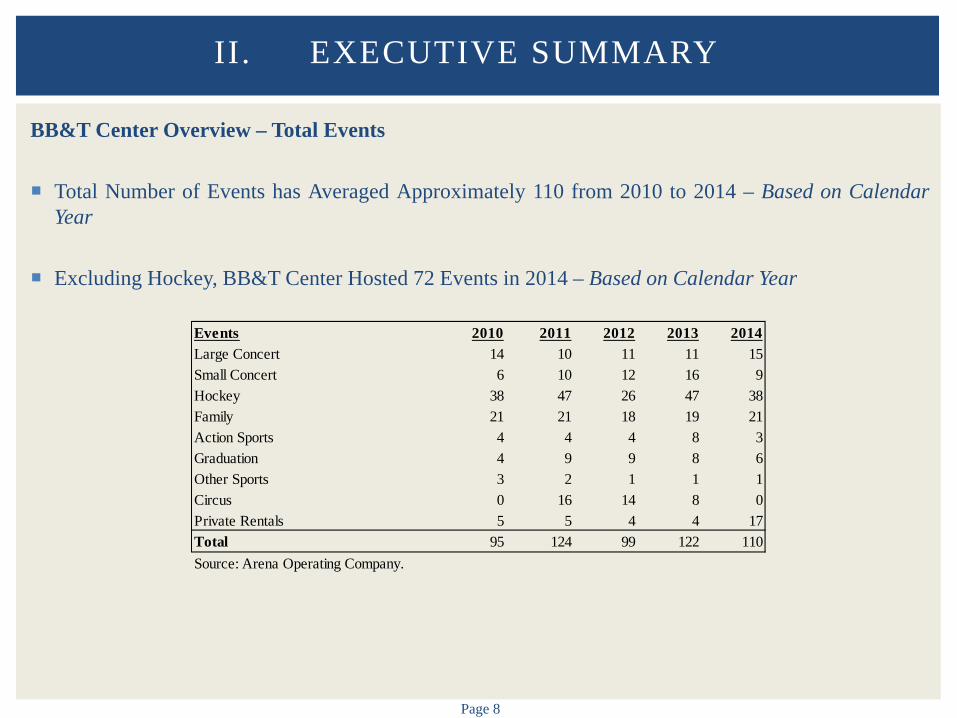

BB&T Center Overview – Total Events

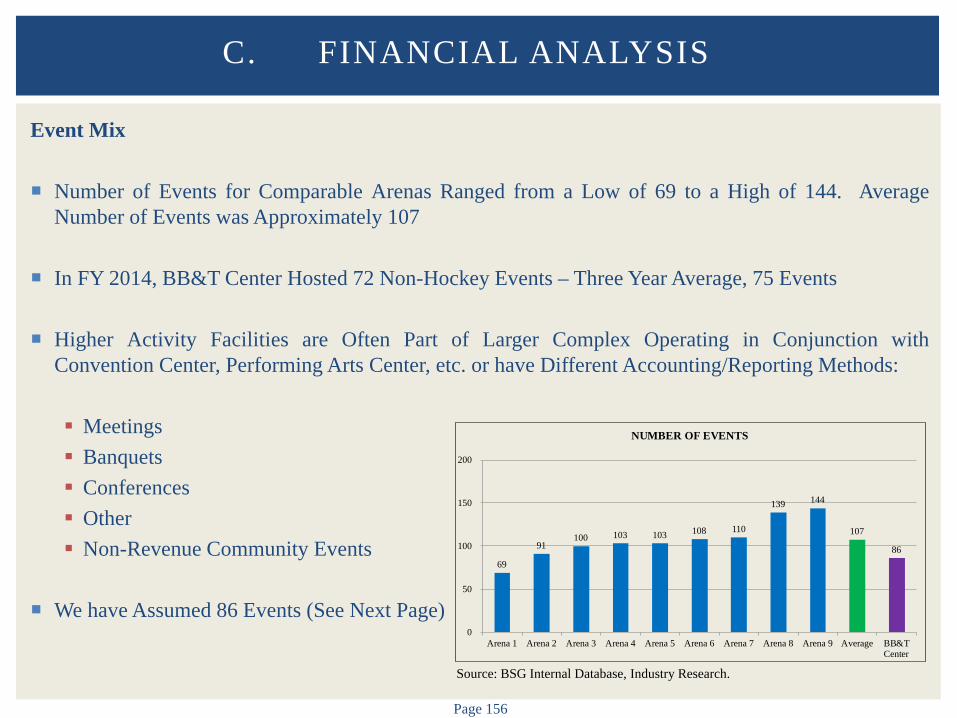

Total Number of Events has Averaged Approximately 110 from 2010 to 2014 – Based on Calendar Year

Excluding Hockey, BB&T Center Hosted 72 Events in 2014 – Based on Calendar Year

II. EXECUTIVE SUMMARY

Events 2010 2011 2012 2013 2014Large Concert 14 10 11 11 15Small Concert 6 10 12 16 9Hockey 38 47 26 47 38Family 21 21 18 19 21Action Sports 4 4 4 8 3Graduation 4 9 9 8 6Other Sports 3 2 1 1 1Circus 0 16 14 8 0Private Rentals 5 5 4 4 17Total 95 124 99 122 110Source: Arena Operating Company.

Page 9

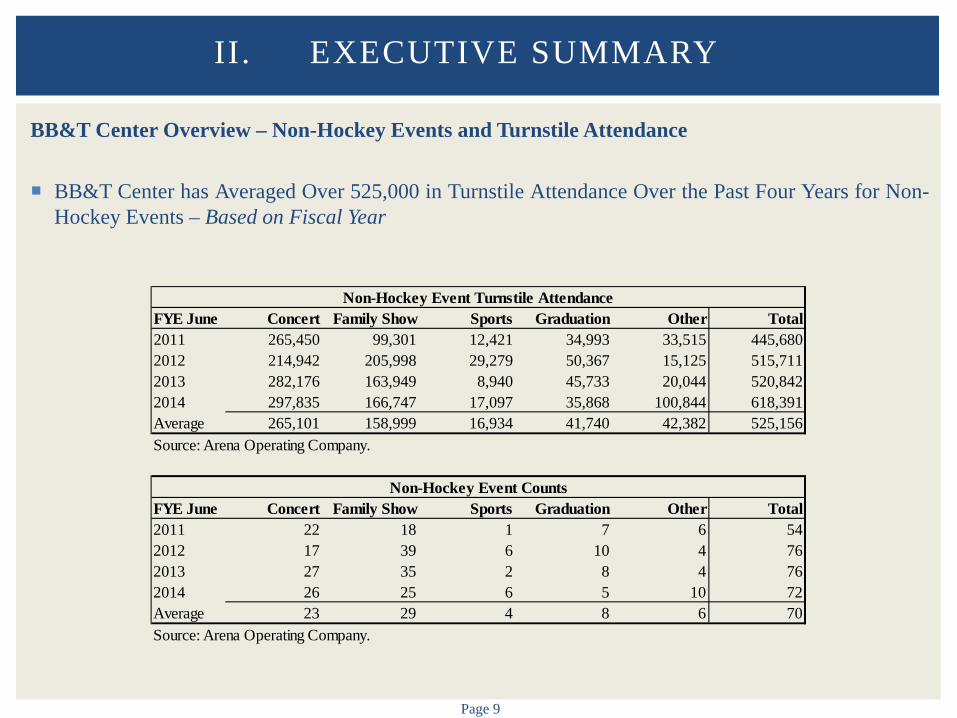

BB&T Center Overview – Non-Hockey Events and Turnstile Attendance BB&T Center has Averaged Over 525,000 in Turnstile Attendance Over the Past Four Years for Non-

Hockey Events – Based on Fiscal Year

II. EXECUTIVE SUMMARY

FYE June Concert Family Show Sports Graduation Other Total2011 265,450 99,301 12,421 34,993 33,515 445,6802012 214,942 205,998 29,279 50,367 15,125 515,7112013 282,176 163,949 8,940 45,733 20,044 520,8422014 297,835 166,747 17,097 35,868 100,844 618,391Average 265,101 158,999 16,934 41,740 42,382 525,156Source: Arena Operating Company.

FYE June Concert Family Show Sports Graduation Other Total2011 22 18 1 7 6 542012 17 39 6 10 4 762013 27 35 2 8 4 762014 26 25 6 5 10 72Average 23 29 4 8 6 70Source: Arena Operating Company.

Non-Hockey Event Counts

Non-Hockey Event Turnstile Attendance

Page 10

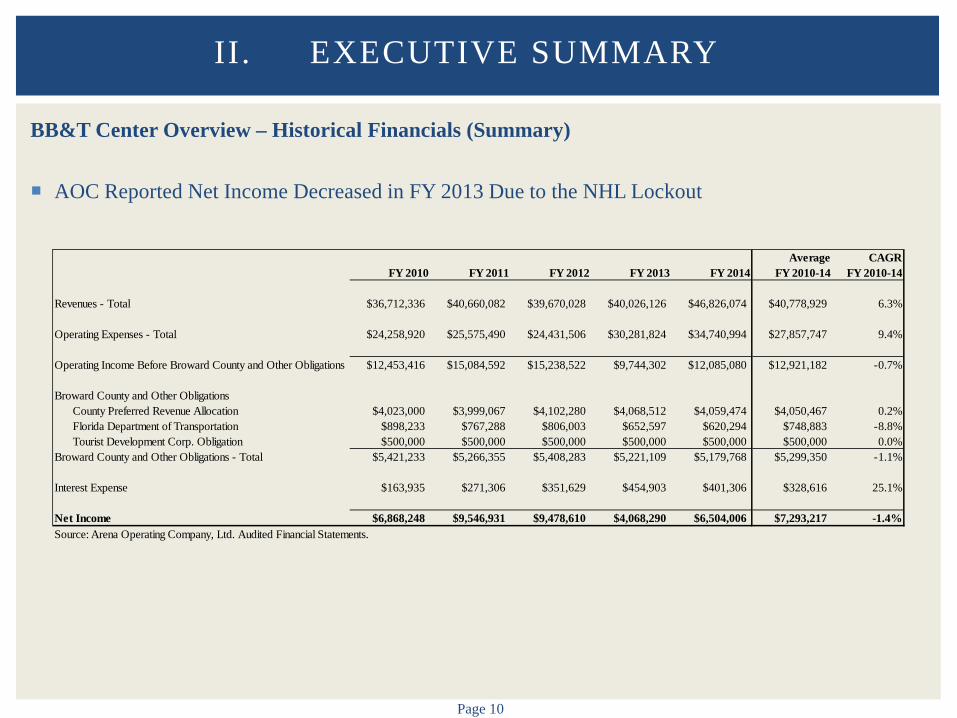

BB&T Center Overview – Historical Financials (Summary)

AOC Reported Net Income Decreased in FY 2013 Due to the NHL Lockout

II. EXECUTIVE SUMMARY

Average CAGRFY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14 FY 2010-14

Revenues - Total $36,712,336 $40,660,082 $39,670,028 $40,026,126 $46,826,074 $40,778,929 6.3%

Operating Expenses - Total $24,258,920 $25,575,490 $24,431,506 $30,281,824 $34,740,994 $27,857,747 9.4%

Operating Income Before Broward County and Other Obligations $12,453,416 $15,084,592 $15,238,522 $9,744,302 $12,085,080 $12,921,182 -0.7%

Broward County and Other ObligationsCounty Preferred Revenue Allocation $4,023,000 $3,999,067 $4,102,280 $4,068,512 $4,059,474 $4,050,467 0.2%Florida Department of Transportation $898,233 $767,288 $806,003 $652,597 $620,294 $748,883 -8.8%Tourist Development Corp. Obligation $500,000 $500,000 $500,000 $500,000 $500,000 $500,000 0.0%

Broward County and Other Obligations - Total $5,421,233 $5,266,355 $5,408,283 $5,221,109 $5,179,768 $5,299,350 -1.1%

Interest Expense $163,935 $271,306 $351,629 $454,903 $401,306 $328,616 25.1%

Net Income $6,868,248 $9,546,931 $9,478,610 $4,068,290 $6,504,006 $7,293,217 -1.4%Source: Arena Operating Company, Ltd. Audited Financial Statements.

Page 11

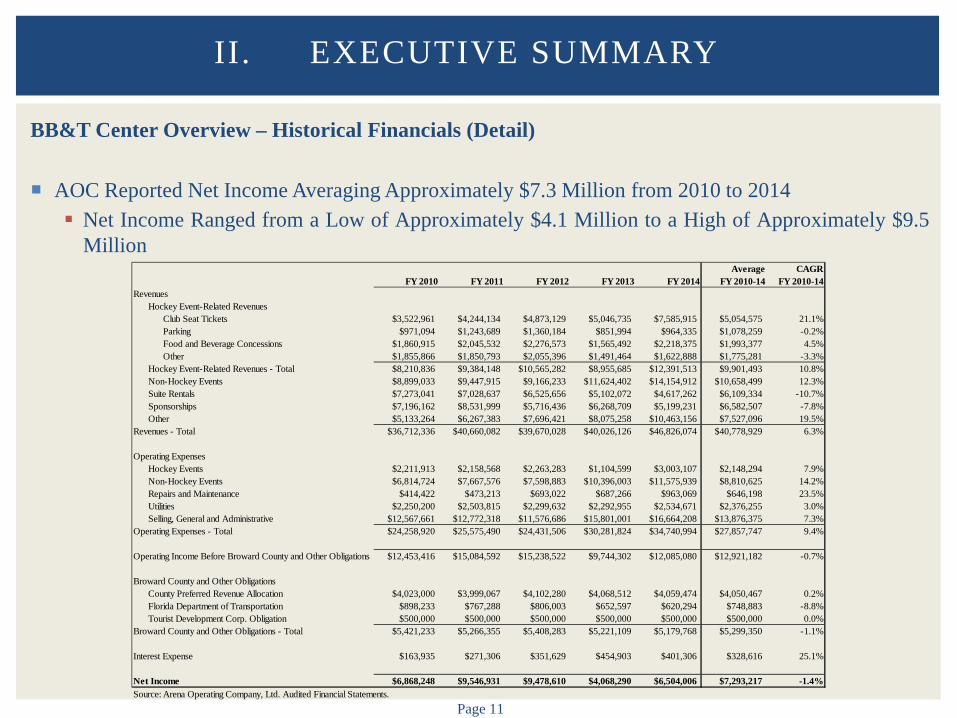

BB&T Center Overview – Historical Financials (Detail)

AOC Reported Net Income Averaging Approximately $7.3 Million from 2010 to 2014 Net Income Ranged from a Low of Approximately $4.1 Million to a High of Approximately $9.5

Million

II. EXECUTIVE SUMMARY

Average CAGRFY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14 FY 2010-14

RevenuesHockey Event-Related Revenues

Club Seat Tickets $3,522,961 $4,244,134 $4,873,129 $5,046,735 $7,585,915 $5,054,575 21.1%Parking $971,094 $1,243,689 $1,360,184 $851,994 $964,335 $1,078,259 -0.2%Food and Beverage Concessions $1,860,915 $2,045,532 $2,276,573 $1,565,492 $2,218,375 $1,993,377 4.5%Other $1,855,866 $1,850,793 $2,055,396 $1,491,464 $1,622,888 $1,775,281 -3.3%

Hockey Event-Related Revenues - Total $8,210,836 $9,384,148 $10,565,282 $8,955,685 $12,391,513 $9,901,493 10.8%Non-Hockey Events $8,899,033 $9,447,915 $9,166,233 $11,624,402 $14,154,912 $10,658,499 12.3%Suite Rentals $7,273,041 $7,028,637 $6,525,656 $5,102,072 $4,617,262 $6,109,334 -10.7%Sponsorships $7,196,162 $8,531,999 $5,716,436 $6,268,709 $5,199,231 $6,582,507 -7.8%Other $5,133,264 $6,267,383 $7,696,421 $8,075,258 $10,463,156 $7,527,096 19.5%

Revenues - Total $36,712,336 $40,660,082 $39,670,028 $40,026,126 $46,826,074 $40,778,929 6.3%

Operating ExpensesHockey Events $2,211,913 $2,158,568 $2,263,283 $1,104,599 $3,003,107 $2,148,294 7.9%Non-Hockey Events $6,814,724 $7,667,576 $7,598,883 $10,396,003 $11,575,939 $8,810,625 14.2%Repairs and Maintenance $414,422 $473,213 $693,022 $687,266 $963,069 $646,198 23.5%Utilities $2,250,200 $2,503,815 $2,299,632 $2,292,955 $2,534,671 $2,376,255 3.0%Selling, General and Administrative $12,567,661 $12,772,318 $11,576,686 $15,801,001 $16,664,208 $13,876,375 7.3%

Operating Expenses - Total $24,258,920 $25,575,490 $24,431,506 $30,281,824 $34,740,994 $27,857,747 9.4%

Operating Income Before Broward County and Other Obligations $12,453,416 $15,084,592 $15,238,522 $9,744,302 $12,085,080 $12,921,182 -0.7%

Broward County and Other ObligationsCounty Preferred Revenue Allocation $4,023,000 $3,999,067 $4,102,280 $4,068,512 $4,059,474 $4,050,467 0.2%Florida Department of Transportation $898,233 $767,288 $806,003 $652,597 $620,294 $748,883 -8.8%Tourist Development Corp. Obligation $500,000 $500,000 $500,000 $500,000 $500,000 $500,000 0.0%

Broward County and Other Obligations - Total $5,421,233 $5,266,355 $5,408,283 $5,221,109 $5,179,768 $5,299,350 -1.1%

Interest Expense $163,935 $271,306 $351,629 $454,903 $401,306 $328,616 25.1%

Net Income $6,868,248 $9,546,931 $9,478,610 $4,068,290 $6,504,006 $7,293,217 -1.4%Source: Arena Operating Company, Ltd. Audited Financial Statements.

Page 12

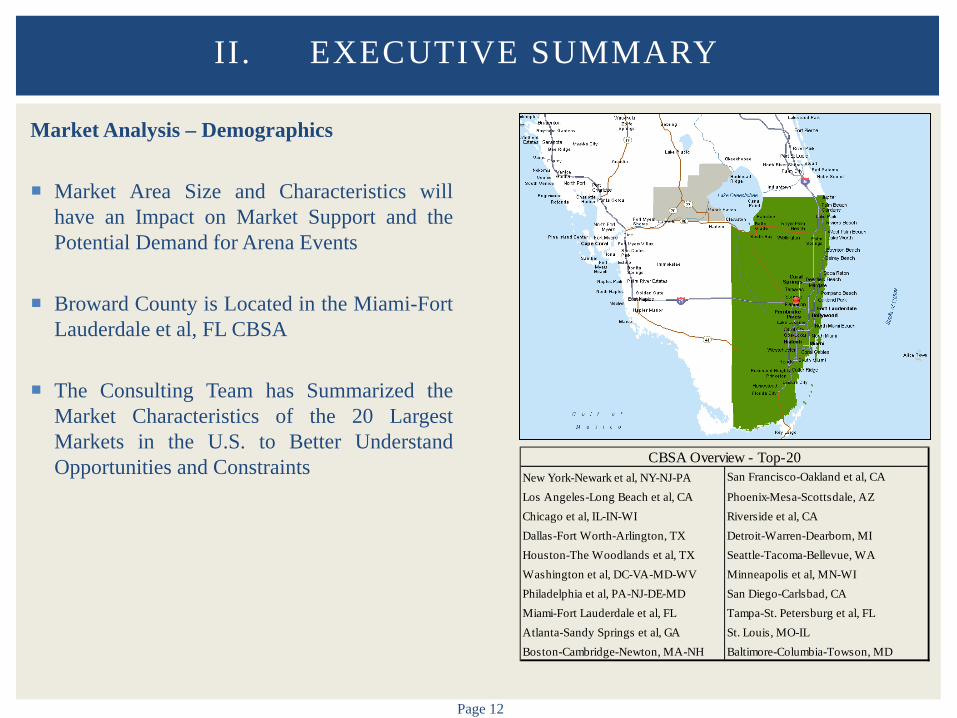

Market Analysis – Demographics

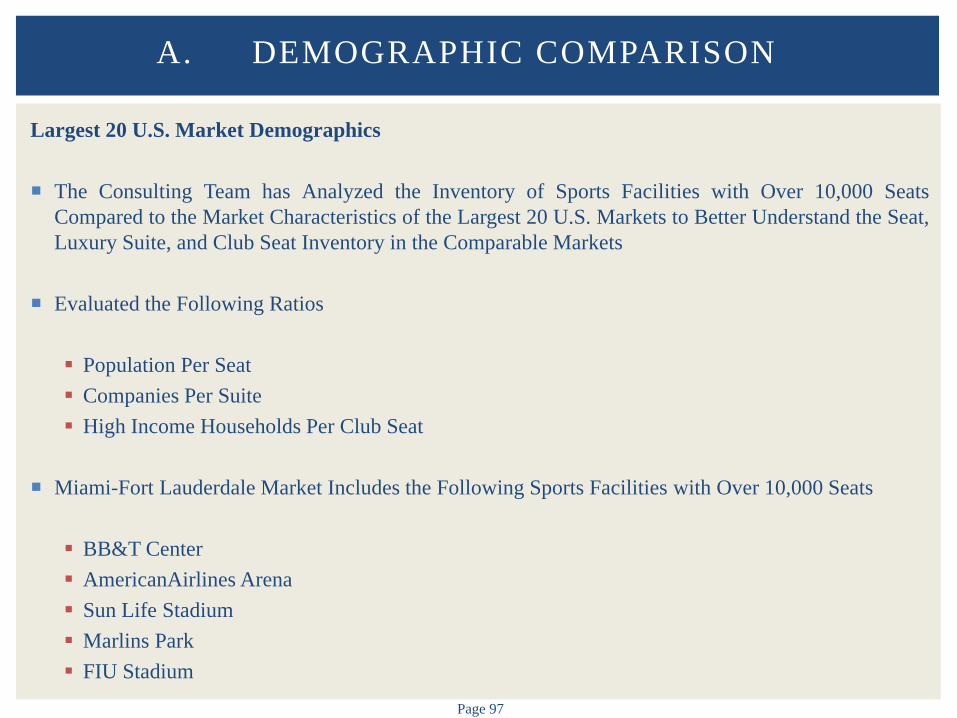

Market Area Size and Characteristics will have an Impact on Market Support and the Potential Demand for Arena Events

Broward County is Located in the Miami-Fort Lauderdale et al, FL CBSA

The Consulting Team has Summarized the Market Characteristics of the 20 Largest Markets in the U.S. to Better Understand Opportunities and Constraints

II. EXECUTIVE SUMMARY

New York-Newark et al, NY-NJ-PA San Francisco-Oakland et al, CA

Los Angeles-Long Beach et al, CA Phoenix-Mesa-Scottsdale, AZChicago et al, IL-IN-WI Riverside et al, CADallas-Fort Worth-Arlington, TX Detroit-Warren-Dearborn, MIHouston-The Woodlands et al, TX Seattle-Tacoma-Bellevue, WAWashington et al, DC-VA-MD-WV Minneapolis et al, MN-WIPhiladelphia et al, PA-NJ-DE-MD San Diego-Carlsbad, CAMiami-Fort Lauderdale et al, FL Tampa-St. Petersburg et al, FLAtlanta-Sandy Springs et al, GA St. Louis, MO-ILBoston-Cambridge-Newton, MA-NH Baltimore-Columbia-Towson, MD

CBSA Overview - Top-20

Page 13

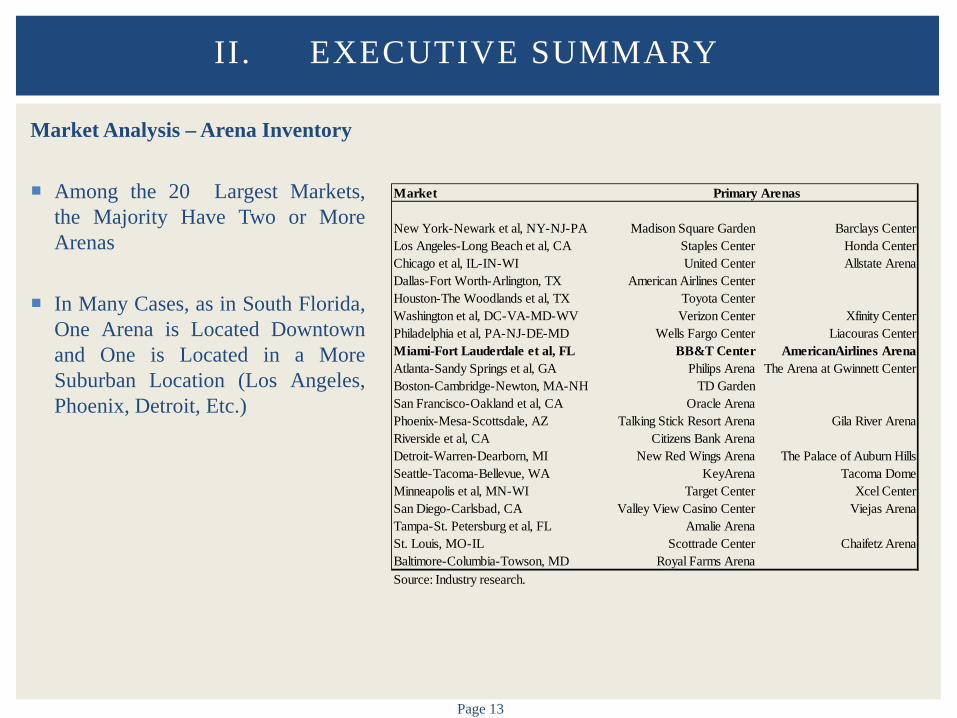

Market Analysis – Arena Inventory

Among the 20 Largest Markets, the Majority Have Two or More Arenas

In Many Cases, as in South Florida, One Arena is Located Downtown and One is Located in a More Suburban Location (Los Angeles, Phoenix, Detroit, Etc.)

II. EXECUTIVE SUMMARY

Market

New York-Newark et al, NY-NJ-PA Madison Square Garden Barclays CenterLos Angeles-Long Beach et al, CA Staples Center Honda CenterChicago et al, IL-IN-WI United Center Allstate ArenaDallas-Fort Worth-Arlington, TX American Airlines CenterHouston-The Woodlands et al, TX Toyota CenterWashington et al, DC-VA-MD-WV Verizon Center Xfinity CenterPhiladelphia et al, PA-NJ-DE-MD Wells Fargo Center Liacouras CenterMiami-Fort Lauderdale et al, FL BB&T Center AmericanAirlines ArenaAtlanta-Sandy Springs et al, GA Philips Arena The Arena at Gwinnett CenterBoston-Cambridge-Newton, MA-NH TD GardenSan Francisco-Oakland et al, CA Oracle ArenaPhoenix-Mesa-Scottsdale, AZ Talking Stick Resort Arena Gila River ArenaRiverside et al, CA Citizens Bank ArenaDetroit-Warren-Dearborn, MI New Red Wings Arena The Palace of Auburn HillsSeattle-Tacoma-Bellevue, WA KeyArena Tacoma DomeMinneapolis et al, MN-WI Target Center Xcel CenterSan Diego-Carlsbad, CA Valley View Casino Center Viejas ArenaTampa-St. Petersburg et al, FL Amalie ArenaSt. Louis, MO-IL Scottrade Center Chaifetz ArenaBaltimore-Columbia-Towson, MD Royal Farms ArenaSource: Industry research.

Primary Arenas

Page 14

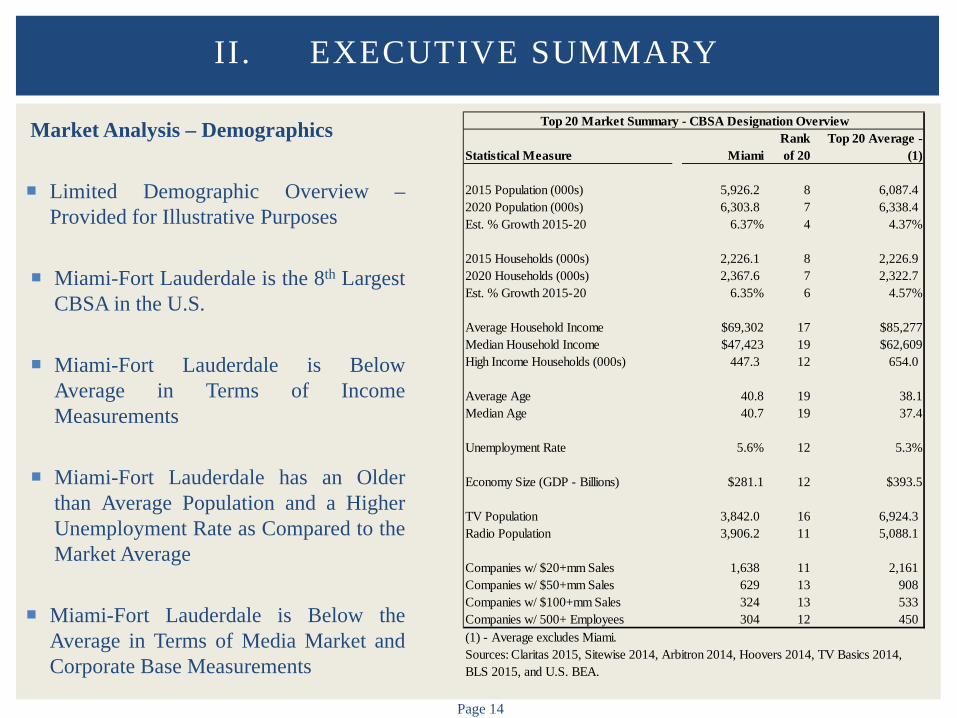

Market Analysis – Demographics

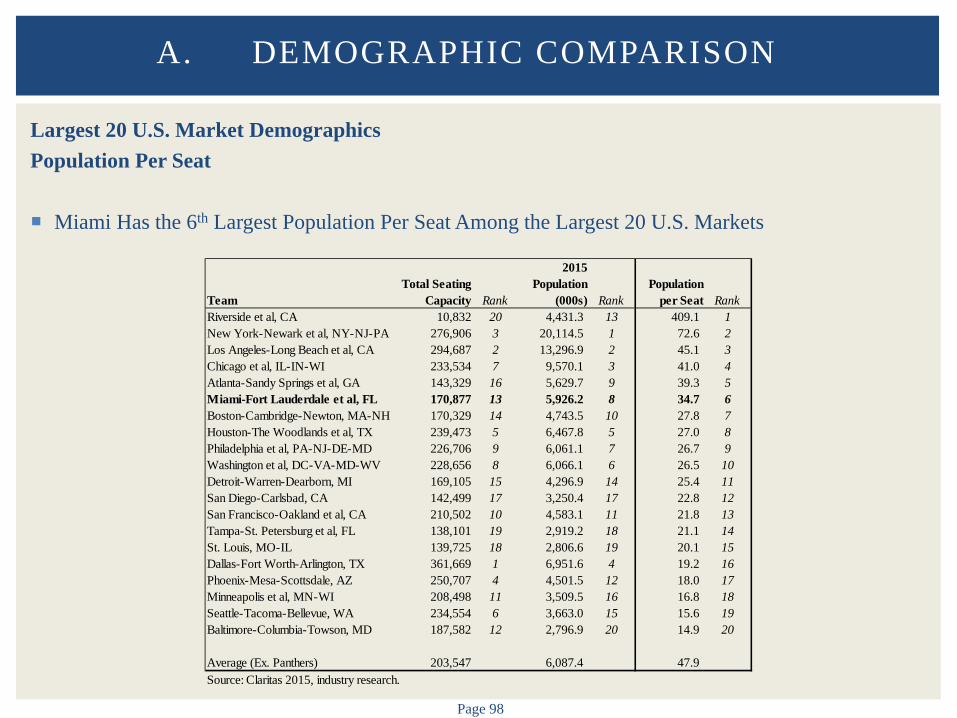

Limited Demographic Overview – Provided for Illustrative Purposes

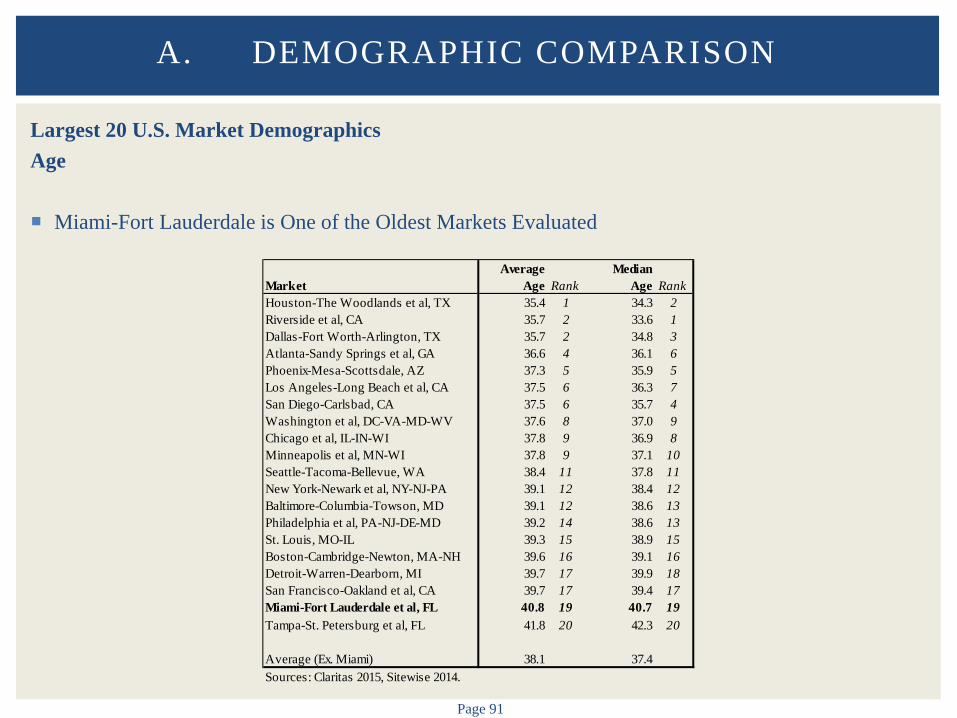

Miami-Fort Lauderdale is the 8th Largest CBSA in the U.S.

Miami-Fort Lauderdale is Below Average in Terms of Income Measurements

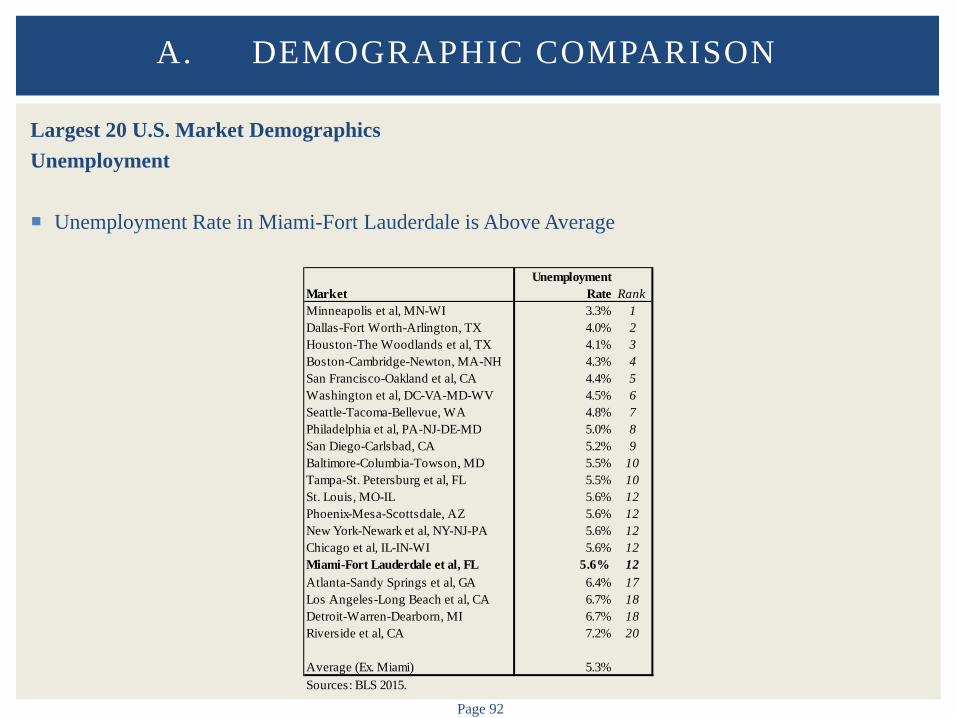

Miami-Fort Lauderdale has an Older than Average Population and a Higher Unemployment Rate as Compared to the Market Average

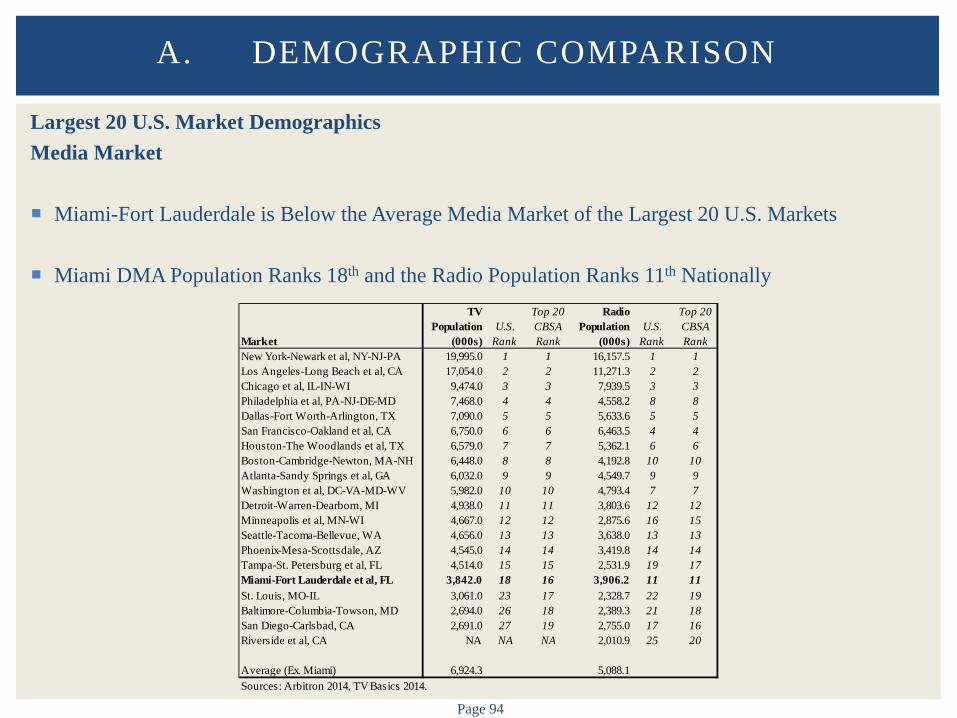

Miami-Fort Lauderdale is Below the Average in Terms of Media Market and Corporate Base Measurements

II. EXECUTIVE SUMMARY

Statistical Measure MiamiRank of 20

Top 20 Average - (1)

2015 Population (000s) 5,926.2 8 6,087.4 2020 Population (000s) 6,303.8 7 6,338.4 Est. % Growth 2015-20 6.37% 4 4.37%

2015 Households (000s) 2,226.1 8 2,226.9 2020 Households (000s) 2,367.6 7 2,322.7 Est. % Growth 2015-20 6.35% 6 4.57%

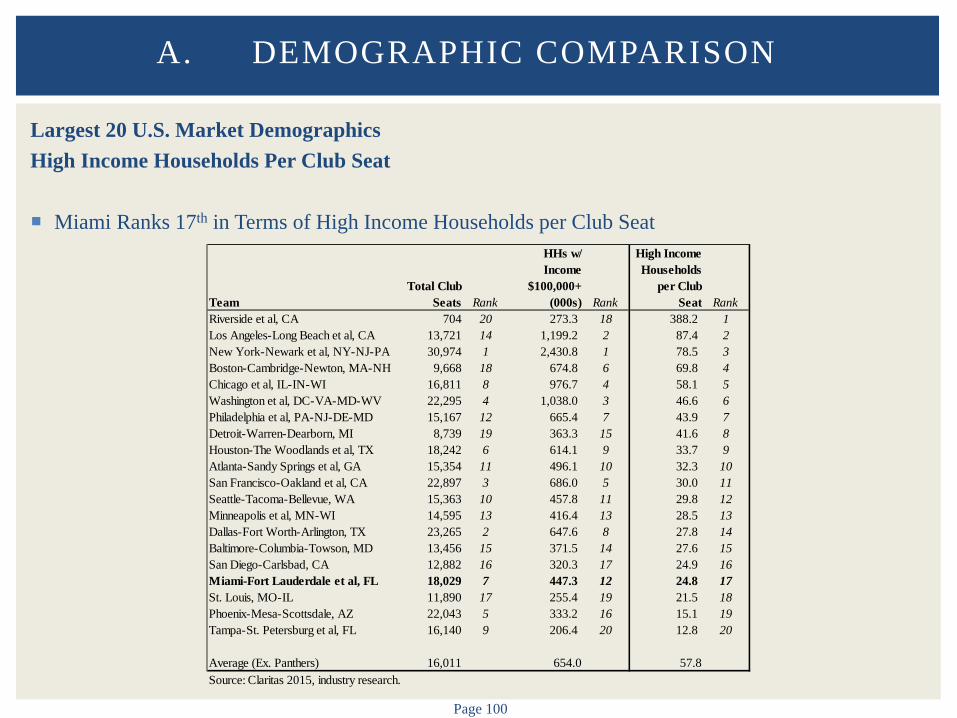

Average Household Income $69,302 17 $85,277Median Household Income $47,423 19 $62,609High Income Households (000s) 447.3 12 654.0

Average Age 40.8 19 38.1Median Age 40.7 19 37.4

Unemployment Rate 5.6% 12 5.3%

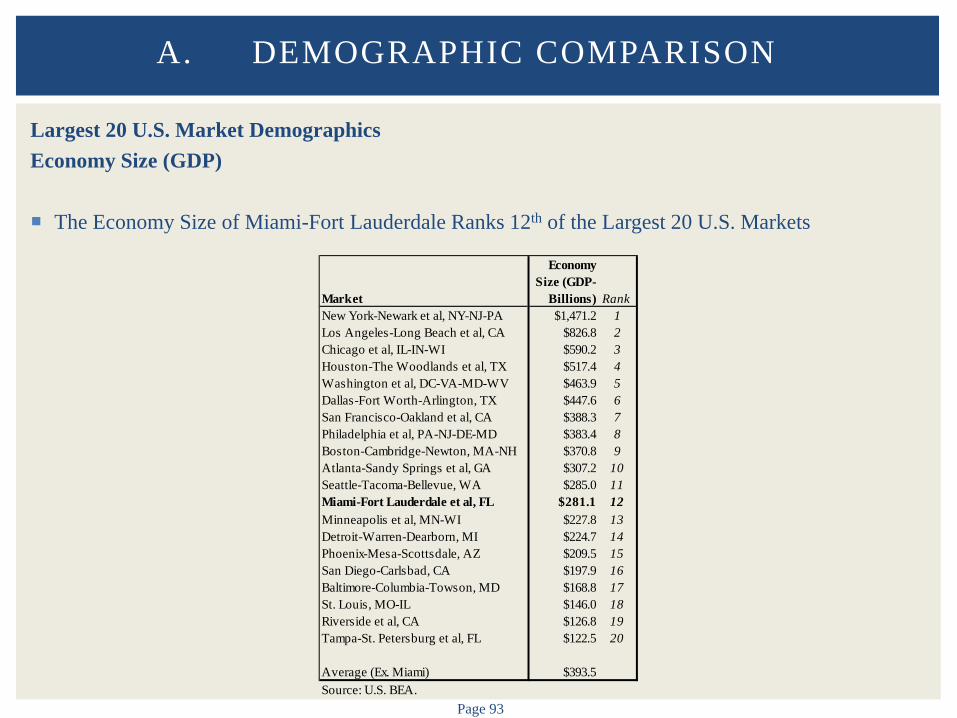

Economy Size (GDP - Billions) $281.1 12 $393.5

TV Population 3,842.0 16 6,924.3 Radio Population 3,906.2 11 5,088.1

Companies w/ $20+mm Sales 1,638 11 2,161Companies w/ $50+mm Sales 629 13 908Companies w/ $100+mm Sales 324 13 533Companies w/ 500+ Employees 304 12 450

Top 20 Market Summary - CBSA Designation Overview

Sources: Claritas 2015, Sitewise 2014, Arbitron 2014, Hoovers 2014, TV Basics 2014, BLS 2015, and U.S. BEA.

(1) - Average excludes Miami.

Page 15

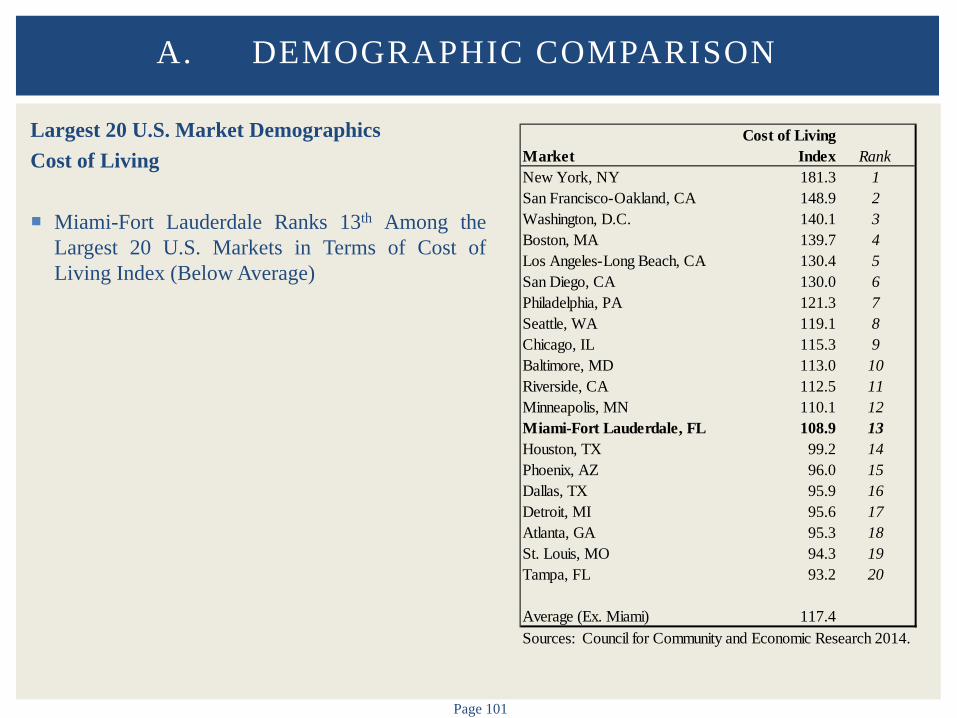

Market Analysis – Demographics: General Observations Miami-Fort Lauderdale is Generally a Strong Market in Terms of Population and Households

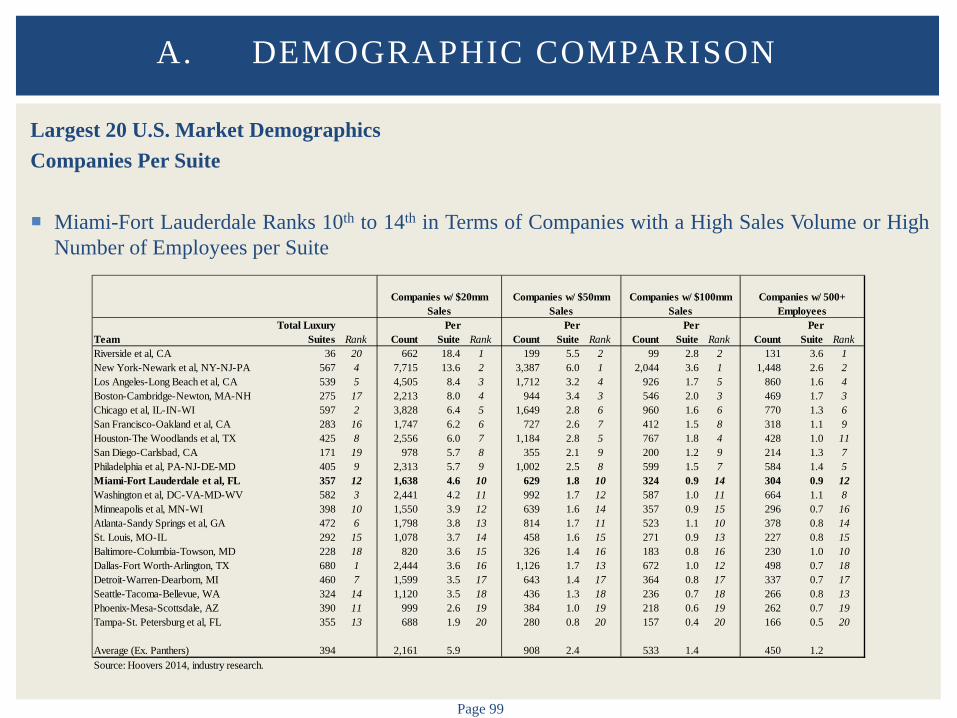

Miami-Fort Lauderdale has Strong Expected Population Growth Over Next 10 Years

Relative Weakness in Median Household Income is Somewhat Offset by Relatively High

Percentage of High Income Households in Miami-Fort Lauderdale

Miami-Fort Lauderdale Generally has an Older Population than the Comparable Markets

In Terms of Population Per Seat and Luxury Suites Per Company, the Miami-Fort Lauderdale Market is Not Overly Saturated as Compared to the Largest 20 U.S. Markets – In Terms of High Income Households to Club Seats, the Market Does Not Rank Favorably

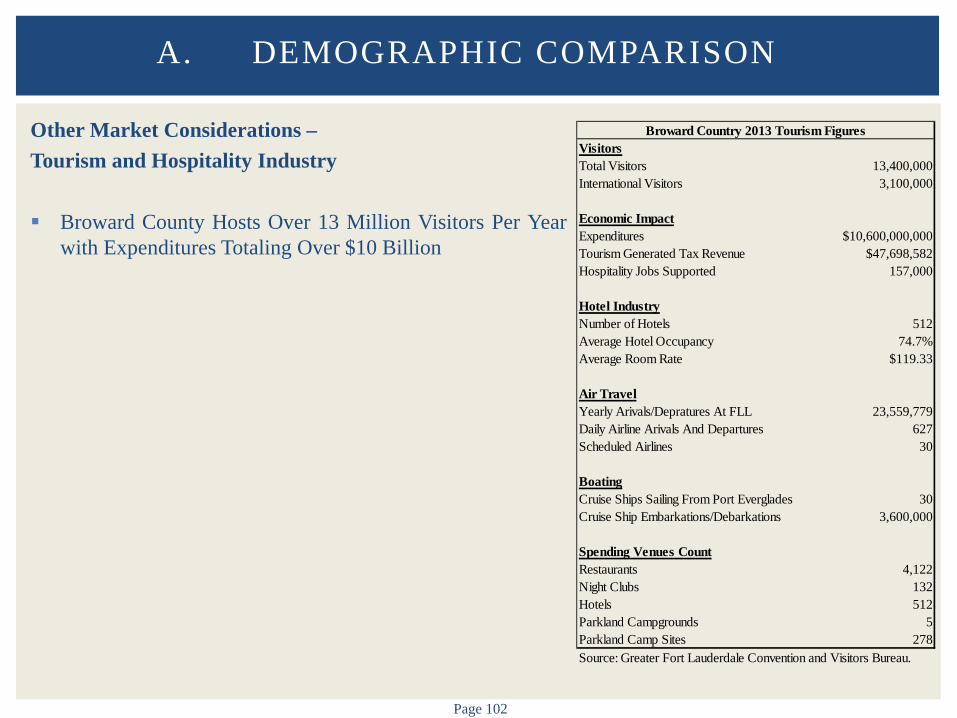

Miami-Fort Lauderdale Benefits from being a Strong Tourist Market – Could Impact Arena Demand for Certain Events (Over 13 Million Tourists to Broward County in 2013)

II. EXECUTIVE SUMMARY

Page 16

Market Analysis – Competitive Facilities

Existing and Planned Inventory of Arenas/Stadiums in the Miami-Fort Lauderdale Market Provide Competition

Direct Competition from Comparable Arenas, as well as Indirect Competition from Stadiums, Amphitheaters, Performing Arts Centers (to a Lesser Degree), and Other Entertainment Alternatives Must be Considered

Patrons Events/Tenants Advertising/Sponsorships Premium Seating Other

II. EXECUTIVE SUMMARY

Page 17

Market Analysis – Competitive Facilities

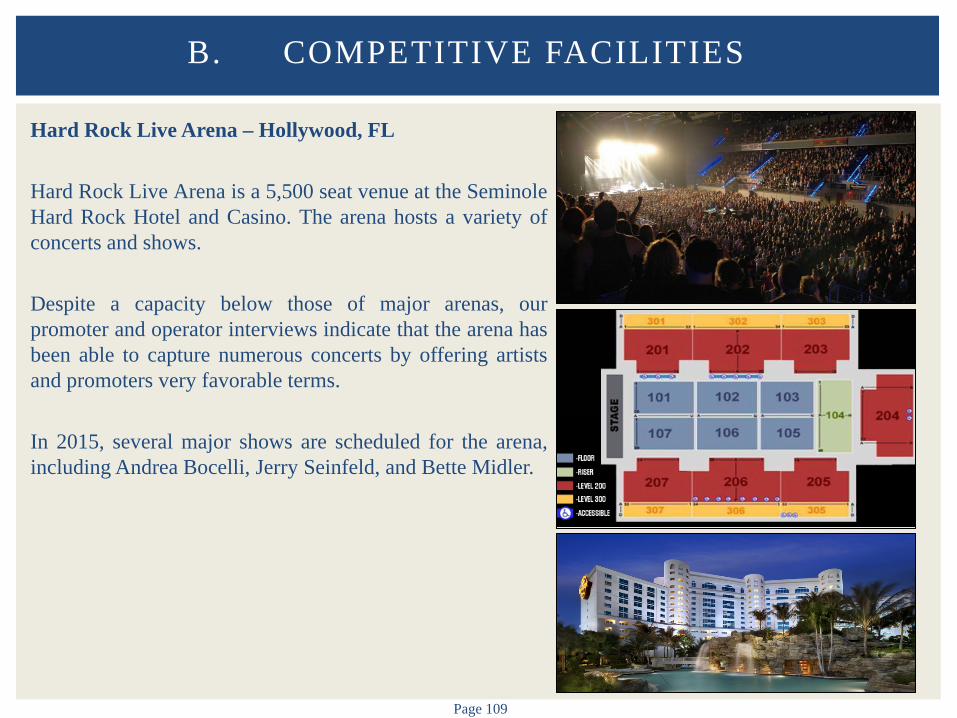

Numerous Competitive Facilities in the Market, Including

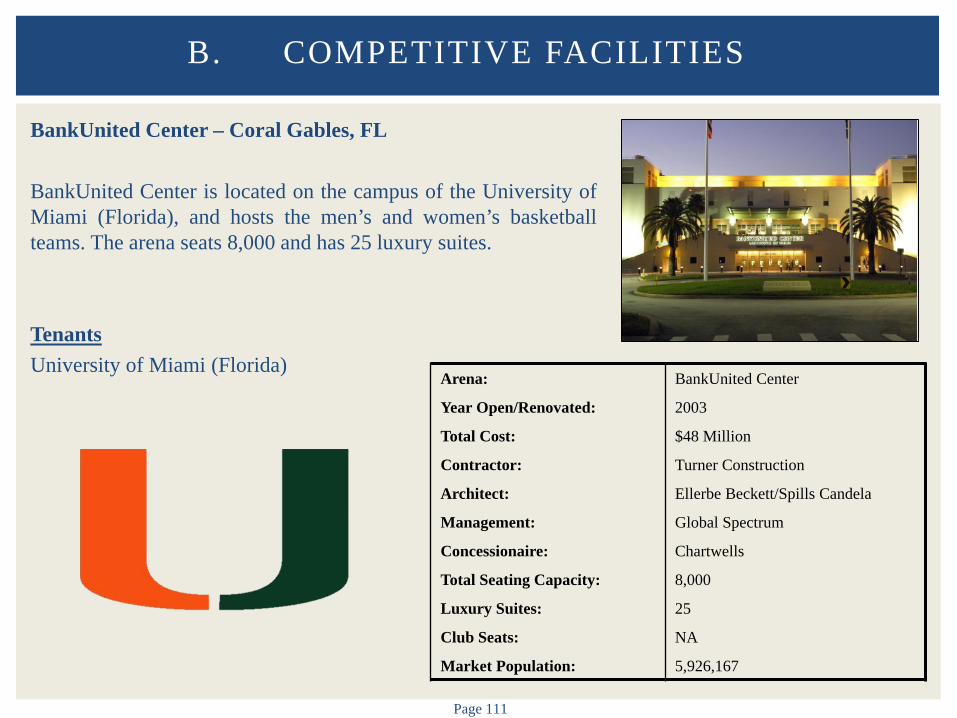

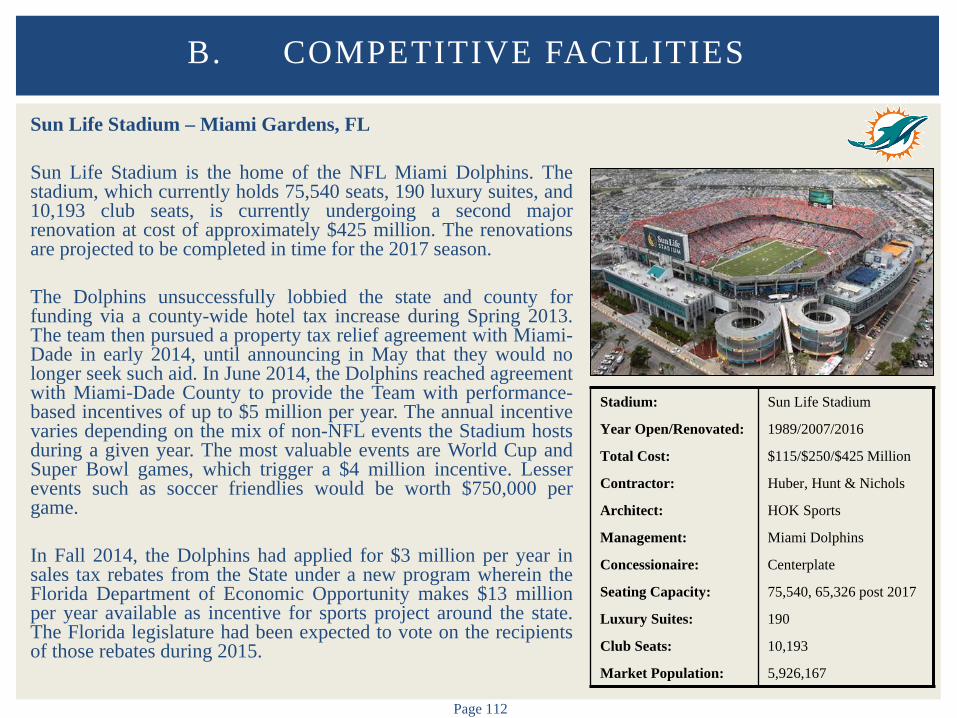

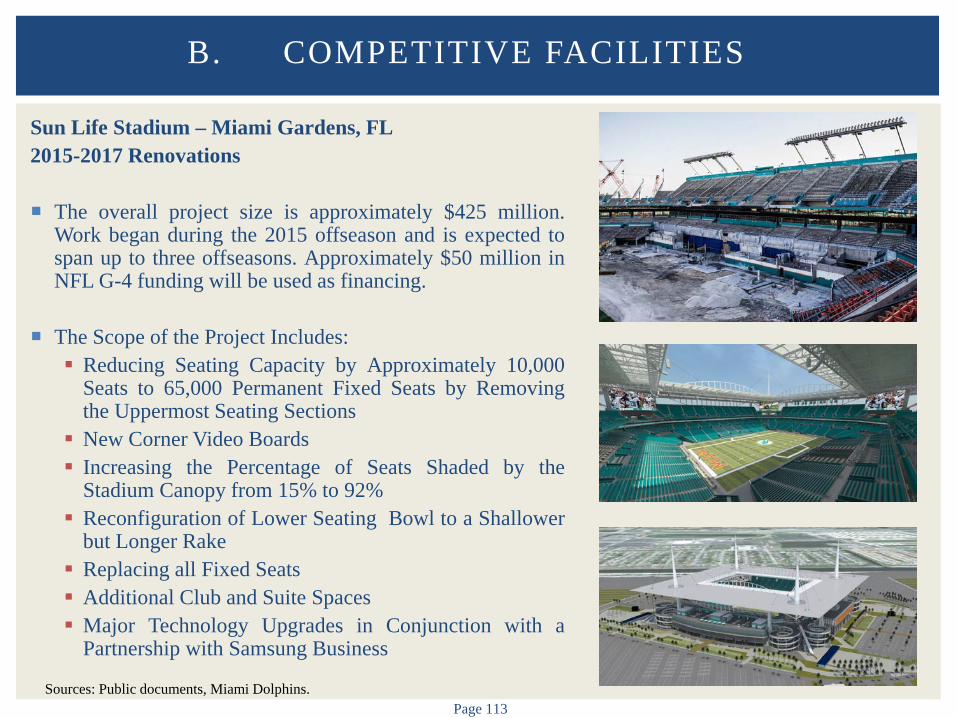

AmericanAirlines Arena Hard Rock Live Arena Perfect Vodka Amphitheatre BankUnited Center Sun Life Stadium Marlins Stadium

Significant Inventory/Supply of Sponsorship Opportunities and Premium Seating (Luxury Suites/Club

Seats) in Market Area

AmericanAirlines Arena in Downtown Miami Provides the Most Significant Competition to BB&T Center

II. EXECUTIVE SUMMARY

Page 18

Market Analysis – Promoter/User Interviews Miami-Fort Lauderdale Considered a Very Strong Concert Market – High Level of Competition for Acts, Particularly

During Outdoor Concert Season

Alternative Concert Venues Such as the Hard Rock Live Arena and Perfect Vodka Amphitheatre Impact Economics of Two Main Arenas

Promoters Report Very Strong Competition Between the BB&T Center and AmericanAirlines Arena, Resulting in

Relatively High Performer Shares, Leaving Smaller Shares for the Arenas and Promoters

Promoters Indicated that BB&T Center and AmericanAirlines Arena Perform Similarly as Music Venues – No Major Difference in Economics

Promoters Indicated They Generally have Little Trouble Booking Desirable Dates Year Round – Promoters

Generally Do Not have to Settle for Non-Preferred Dates

One Promoter Strongly Cautioned that his Show Promoters Would Look Less Favorably at BB&T Center Without the Panthers Because of the Lack of a Strong Season Ticket Holder Database to Market Events Going Forward

One Promoter Commented that Without the Panthers, BB&T Center will Need to Market Itself Aggressively to Maintain its Brand as a Top Tier Venue on Par with AmericanAirlines Arena

One Promoter Commented that the Age of BB&T Center is a Concern and Indicated that Capital Repairs/Maintenance Need to be Diligently Performed to Keep the Building from Starting to Deteriorate in Terms of Performance

II. EXECUTIVE SUMMARY

Page 19

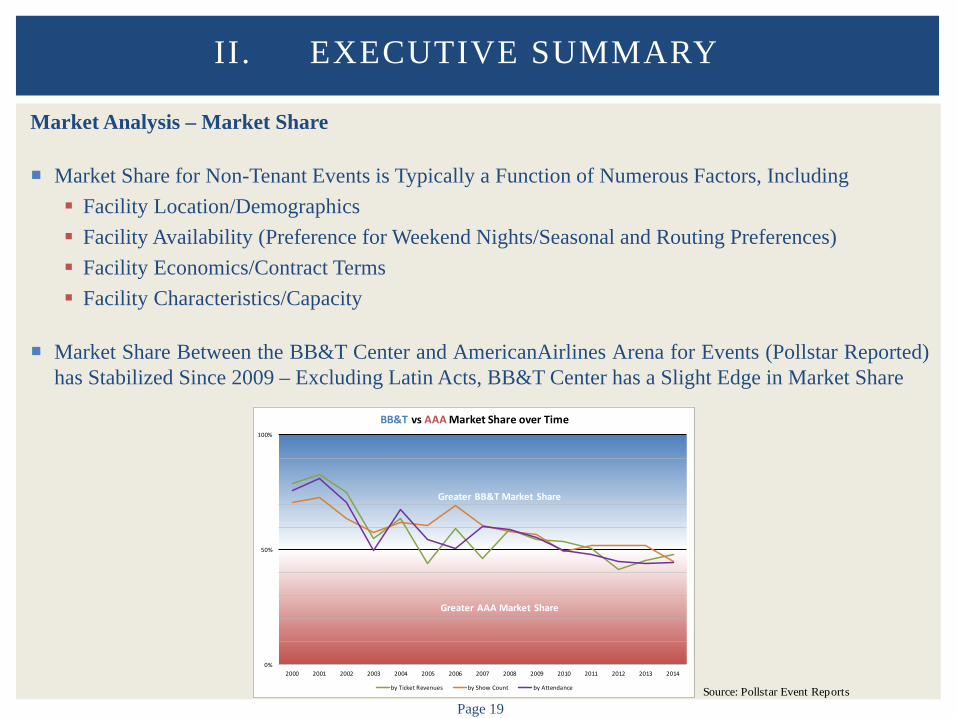

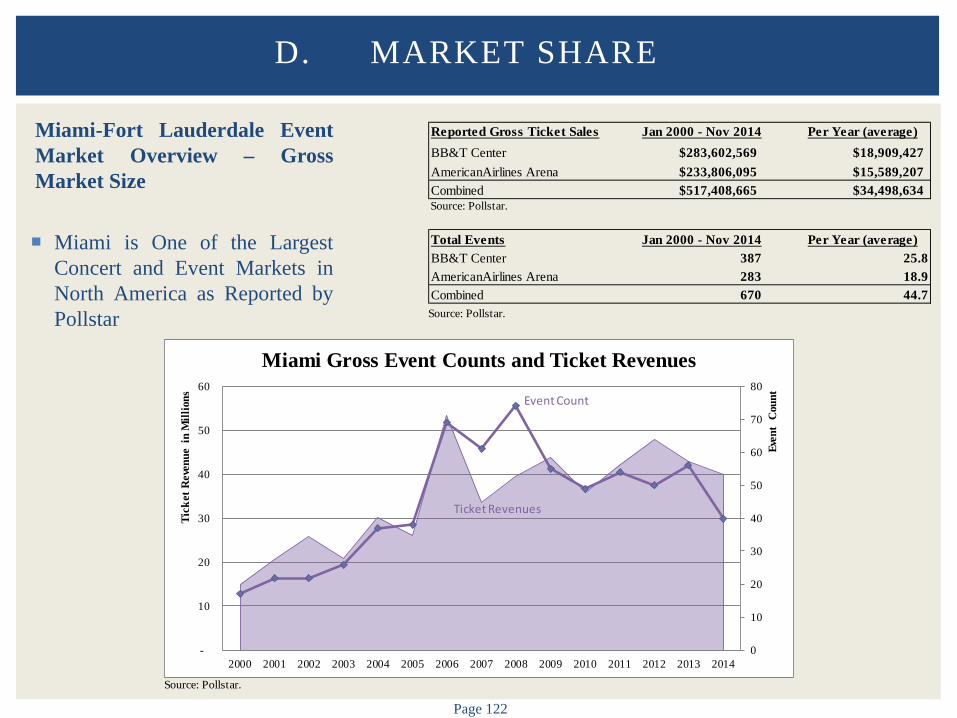

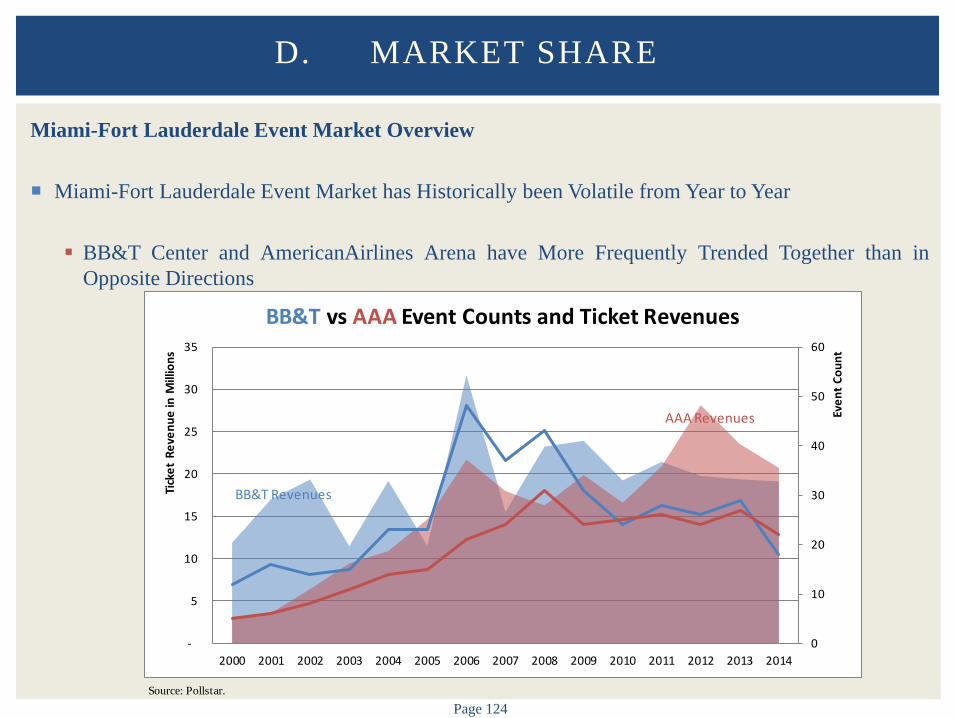

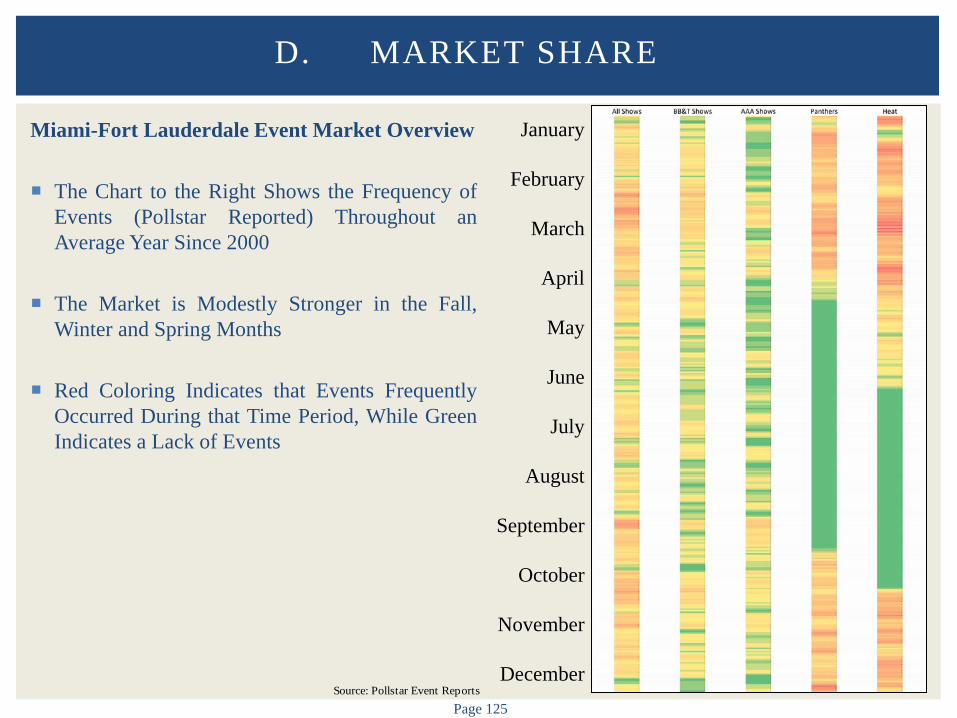

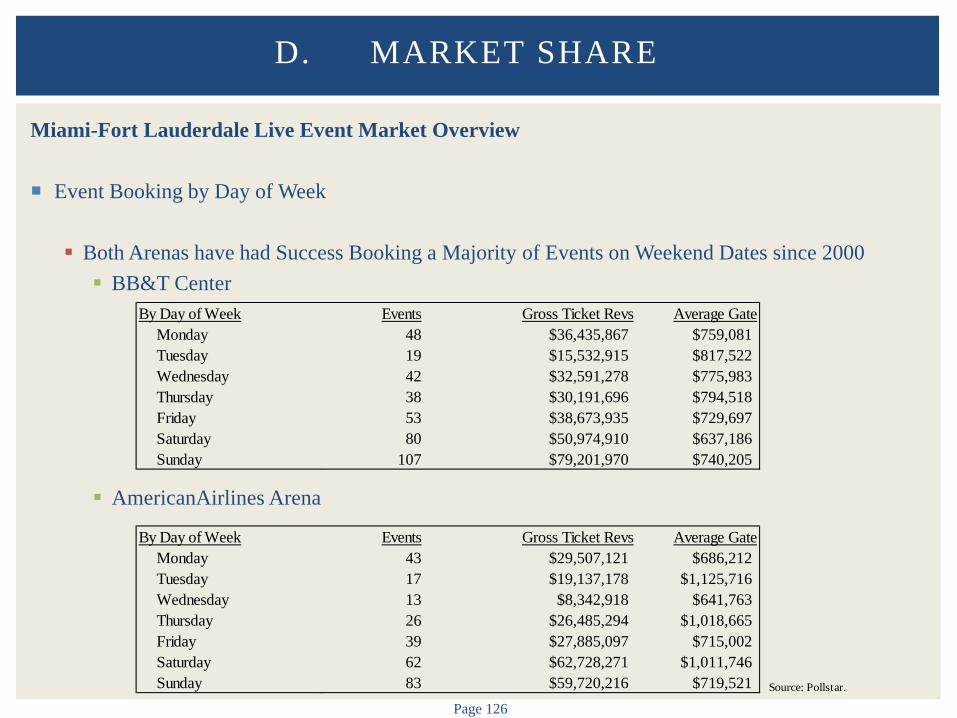

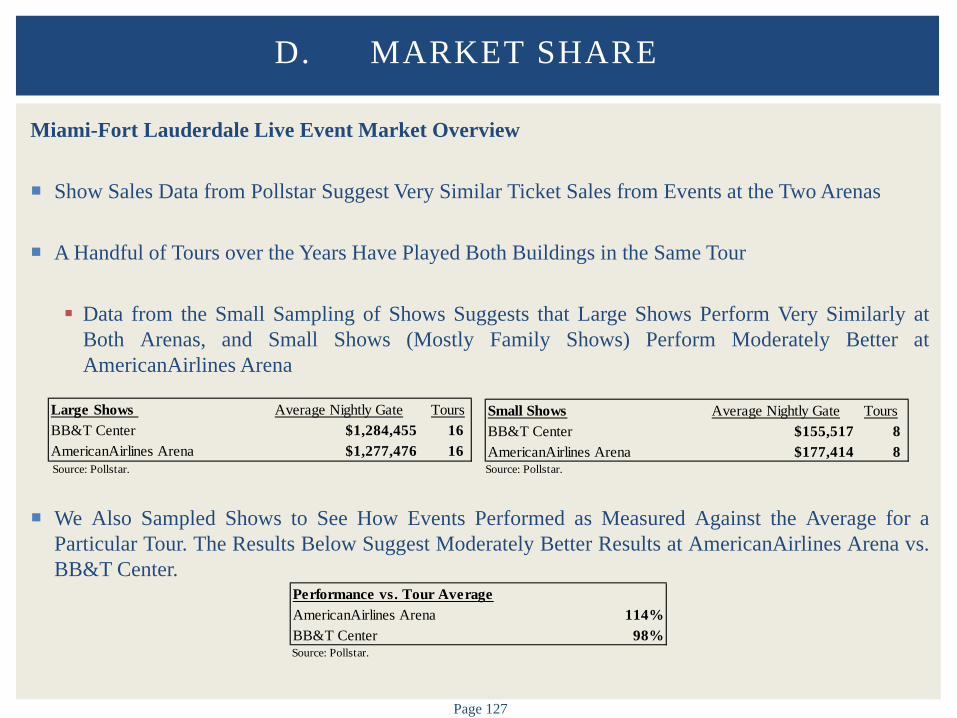

Market Analysis – Market Share

Market Share for Non-Tenant Events is Typically a Function of Numerous Factors, Including Facility Location/Demographics Facility Availability (Preference for Weekend Nights/Seasonal and Routing Preferences) Facility Economics/Contract Terms Facility Characteristics/Capacity

Market Share Between the BB&T Center and AmericanAirlines Arena for Events (Pollstar Reported) has Stabilized Since 2009 – Excluding Latin Acts, BB&T Center has a Slight Edge in Market Share

II. EXECUTIVE SUMMARY

0%

50%

100%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

BB&T vs AAA Market Share over Time

by Ticket Revenues by Show Count by Attendance

Greater BB&T Market Share

Greater AAA Market Share

Source: Pollstar Event Reports

Page 20

Market Analysis – Market Share (Opportunities)

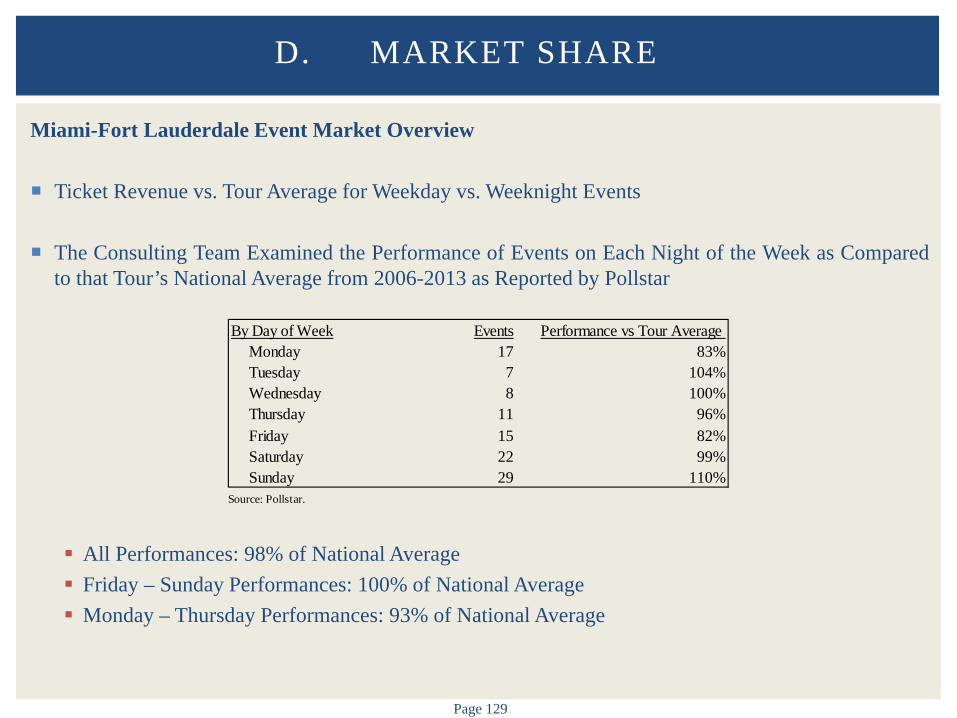

The Consulting Team Examined the Performance of Events on Each Night of the Week as Compared to that Tour’s National Average from 2006-2013 as Reported by Pollstar

All Performances: 98% of National Average Friday – Sunday Performances: 100% of National Average Monday – Thursday Performances: 93% of National Average

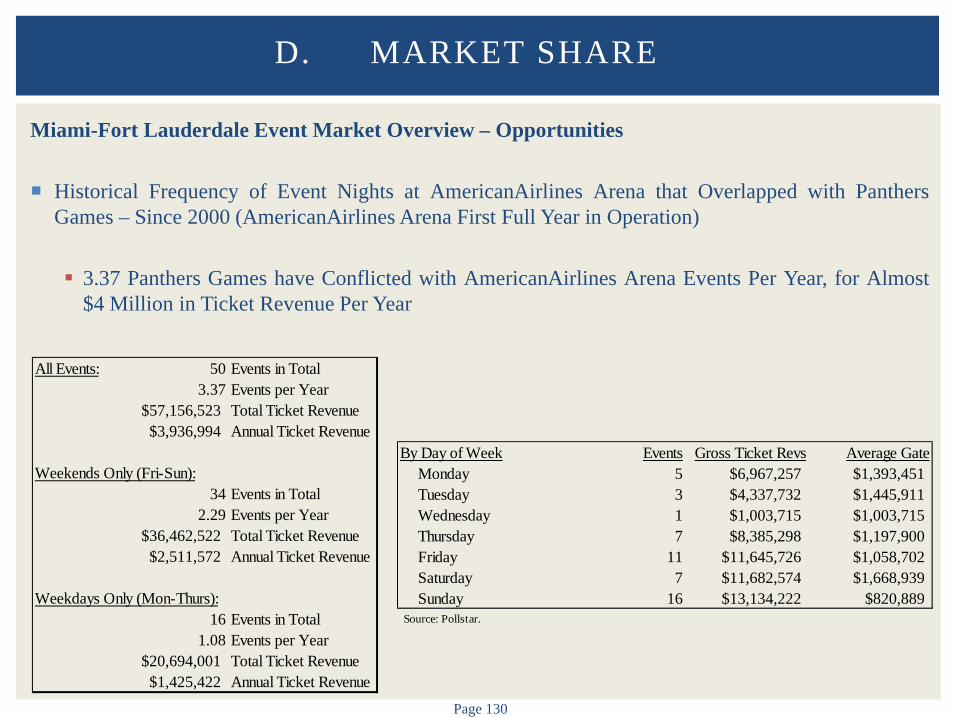

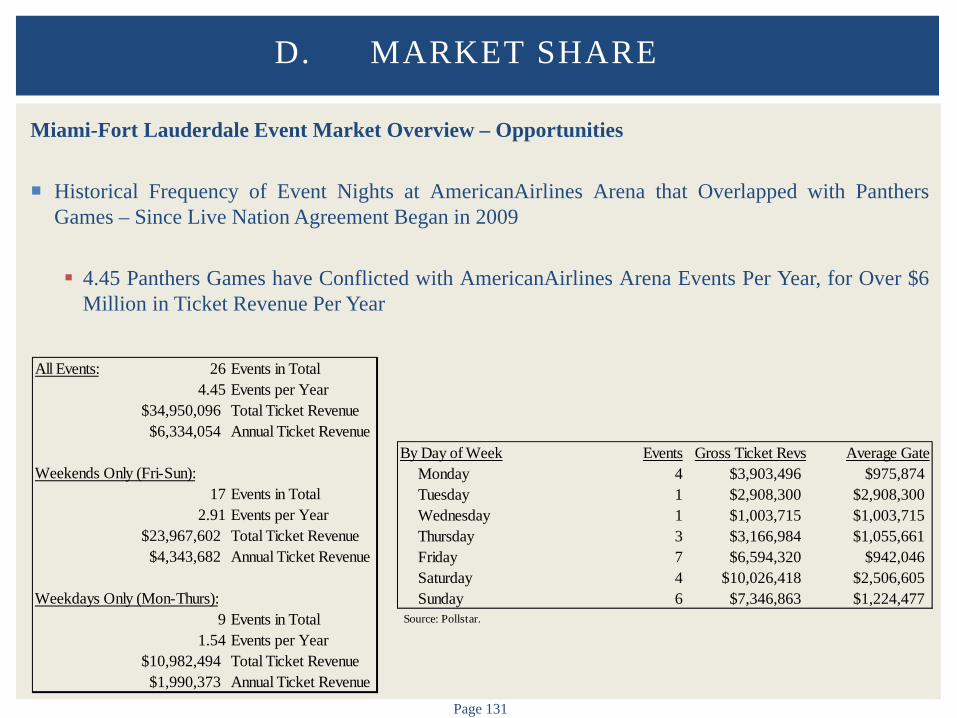

It is Estimated that Potential Economic Gains Due to Capture of AmericanAirlines Arena Events

Historically Occurring During Panthers Games Could Approach $300,000-$600,000 Per Year, If BB&T Center were able to Capture All Such Events

In Addition to Potential Market Share Capture, it is Estimated that Potential Economic Gains Due to

Increased Scheduling of Weekend Shows Without the Panthers Could Approach $50,000-$100,000, Depending on the Mix of Shows and Scheduling

II. EXECUTIVE SUMMARY

Page 21

Market Analysis – Potential Users/Tenants

In Addition to Events Such as Concerts, Family Shows, and Community Events, Many Arenas Often Include One or More Anchor Tenants

BB&T Center Could Consider the Potential of a Replacement Anchor Tenant – Minor League Team

Candidate League Would Likely have a Presence in the Southeast and Team Available to Relocate or a Desire to Expand

Advantages of an Anchor Tenant Could Include

Stabilizing Revenue Streams During the Year and Across Years Increased Activity/Exposure of Arena Increases Sponsorship and Naming Rights Demand Ticket Buyer Database to Promote Concerts and Other Events

Certain Arena Operators Prefer to Operate Arenas with No Minor League Tenants to Provide More

Flexible Scheduling Opportunities for More Profitable Events

II. EXECUTIVE SUMMARY

Page 22

Market Analysis – Potential Users/Tenants

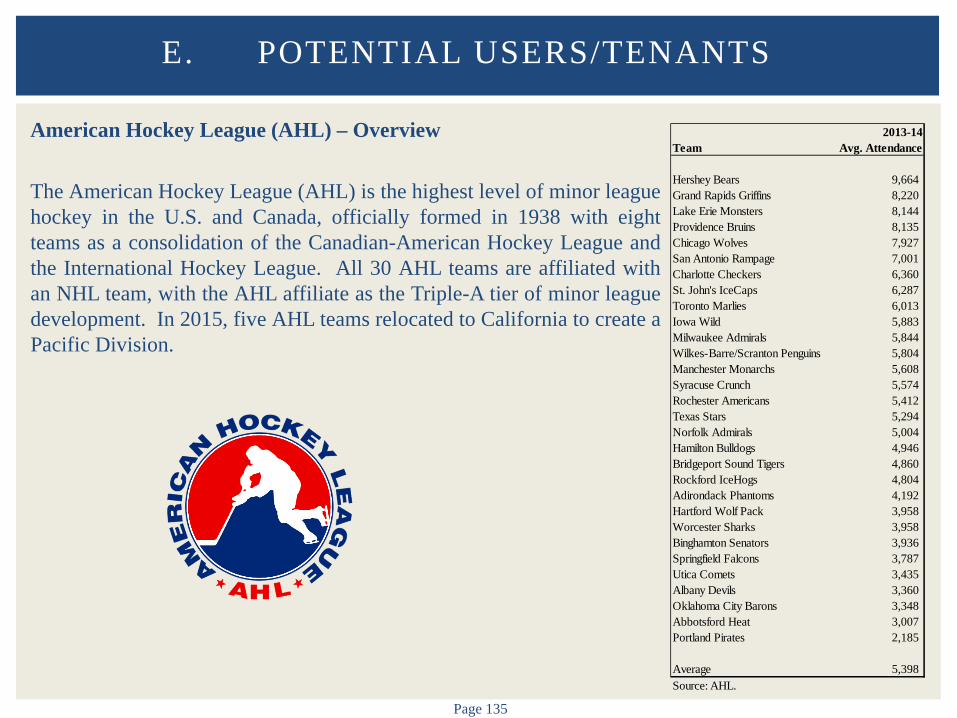

The Consulting Team Contacted Representatives of Candidate Leagues – Limited Opportunities to “Replace” Panthers with an Anchor Tenant

AHL Leadership Reported Limited Interest in the Market, but Challenges in Adding a Single Florida Team and Following an NHL Team in an NHL-Sized Arena Represented Significant Challenges

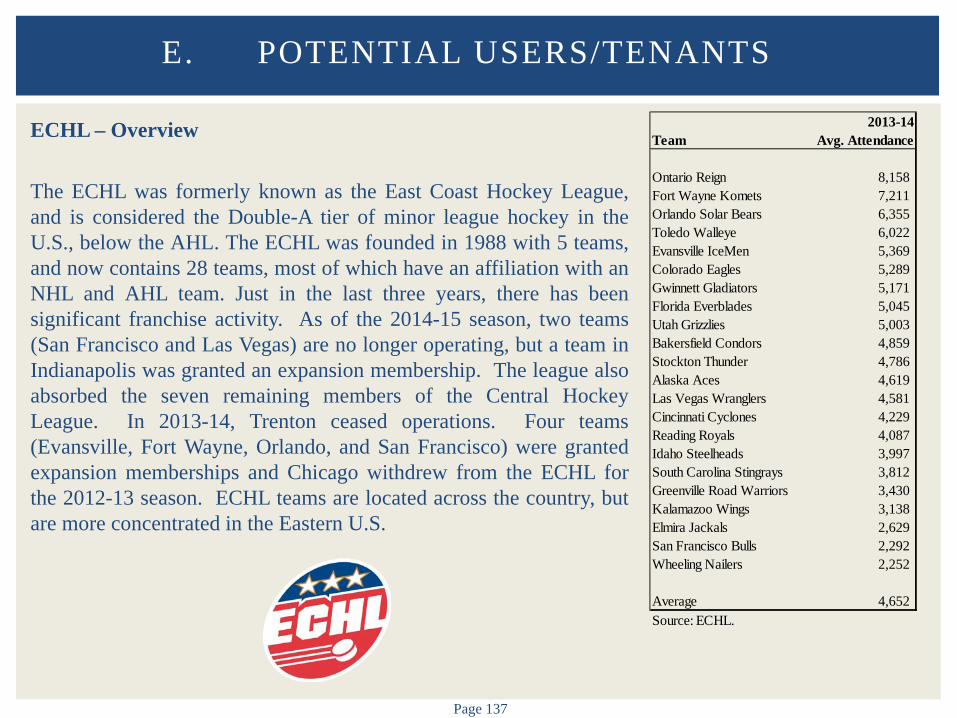

ECHL Leadership Reported Some Interest in Upgrading One of its Teams to a Stronger Market, but Expressed Reservations Because of its General Desire to Seek Mid-Level Markets and Smaller Arenas

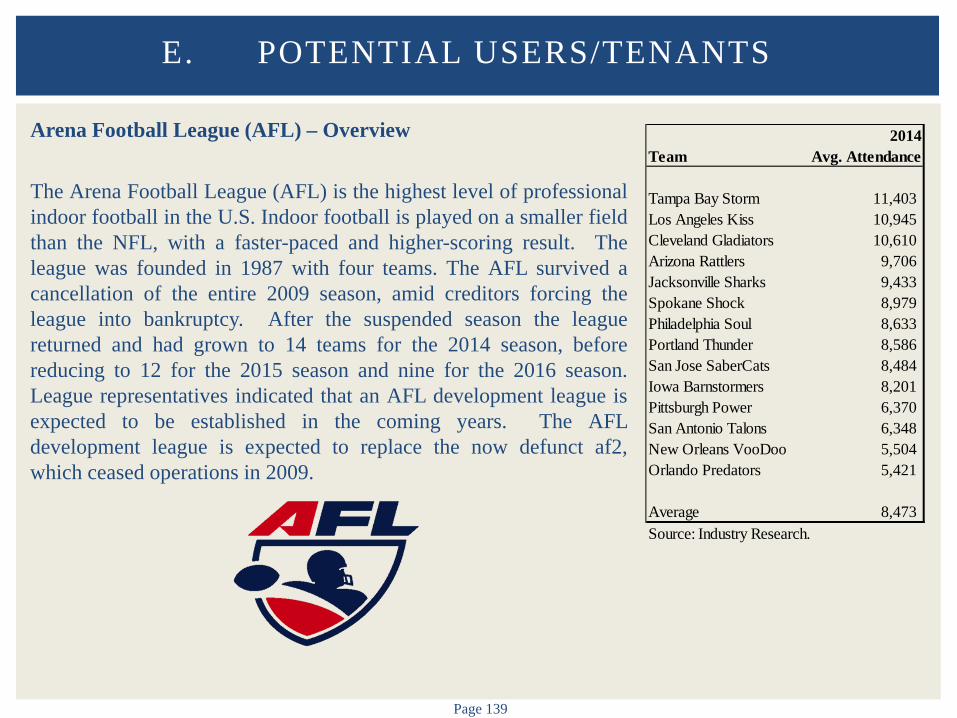

AFL Leadership Report a Strong Interest in the Market and a Desire to Expand in the Near Future

D-League and WNBA Would Require Coordination with the Miami Heat/NBA

The Consulting Team Also Considered Convention/Trade Show Opportunities and Potential Synergies with the Broward County Convention Center – Limited Opportunities Given Distance

Consideration was Also Given to Identifying a "Megachurch" as an Operator – Limited Track Record of Success with this Scenario

II. EXECUTIVE SUMMARY

Page 23

Financial Analysis – Overview

The Consulting Team Developed Financial and Operating Assumptions for the BB&T Center to Understand the Potential Net Cash Flow from Operations Without the Panthers

The Consulting Team has Made Significant Assumptions Related to Arena Operating Revenues and Expenses

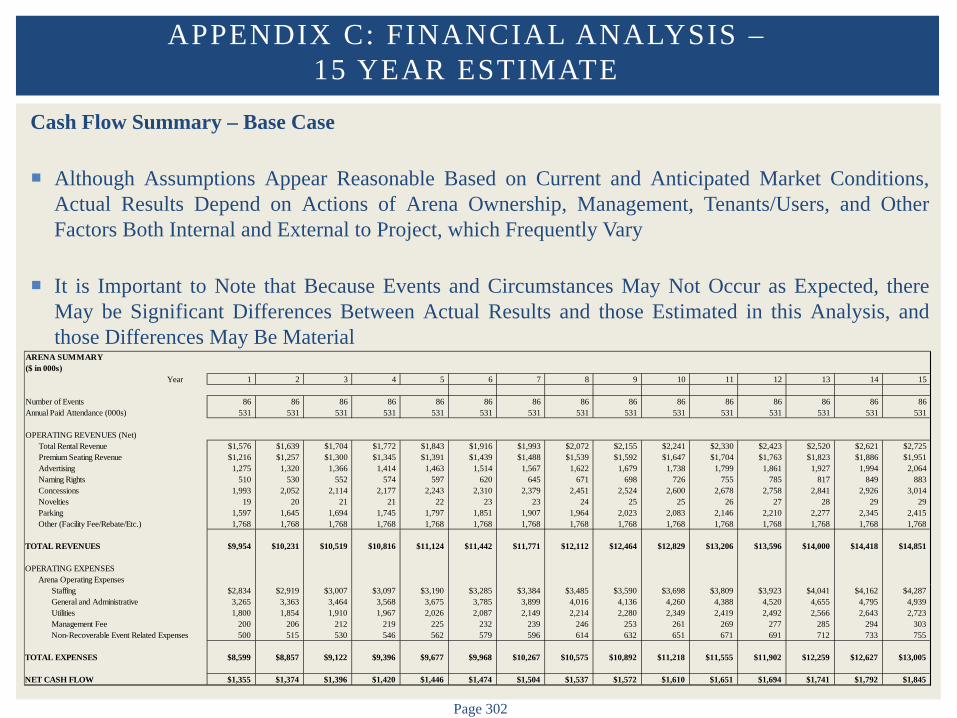

Although Assumptions Appear Reasonable Based on Current and Anticipated Market Conditions, Actual Results Depend on Actions of Arena, Management, Tenants, and Other Factors Both Internal and External to Project, which Frequently Vary

It is Important to Note that Because Events and Circumstances May Not Occur as Expected, there May be Significant Differences Between Actual Results and those Estimated in this Analysis, and those Differences May Be Material

The Consulting Team Reviewed Historical Operating Performance of the BB&T Center and Utilized Comparable Arena Information from Our Proprietary Internal Database to Develop Key Assumptions

Information Obtained from Numerous Sources Including Comparable Facilities, Industry Sources, Etc. In Order to Obtain Accurate and Relevant Information, the Consulting Team Agreed to Maintain

Confidentiality of Arenas

As Noted Previously, Findings are Limited in Nature as the Consulting Team has Not Completed General Public/Corporate Surveys or Focus Groups

II. EXECUTIVE SUMMARY

Page 24

Financial Analysis – Comparable Arena Overview

The Consulting Team Identified 18 Arenas to be “Comparable” to BB&T Center Without a NHL Tenant

Comparable Arenas were Selected Based on Some or All of the Following Factors Physical Characteristics Age Size Amenities

Operating Characteristics Tenant Mix (No NHL or NBA Tenant) Competing Arena in Market

Other Characteristics Market Location

II. EXECUTIVE SUMMARY

Page 25

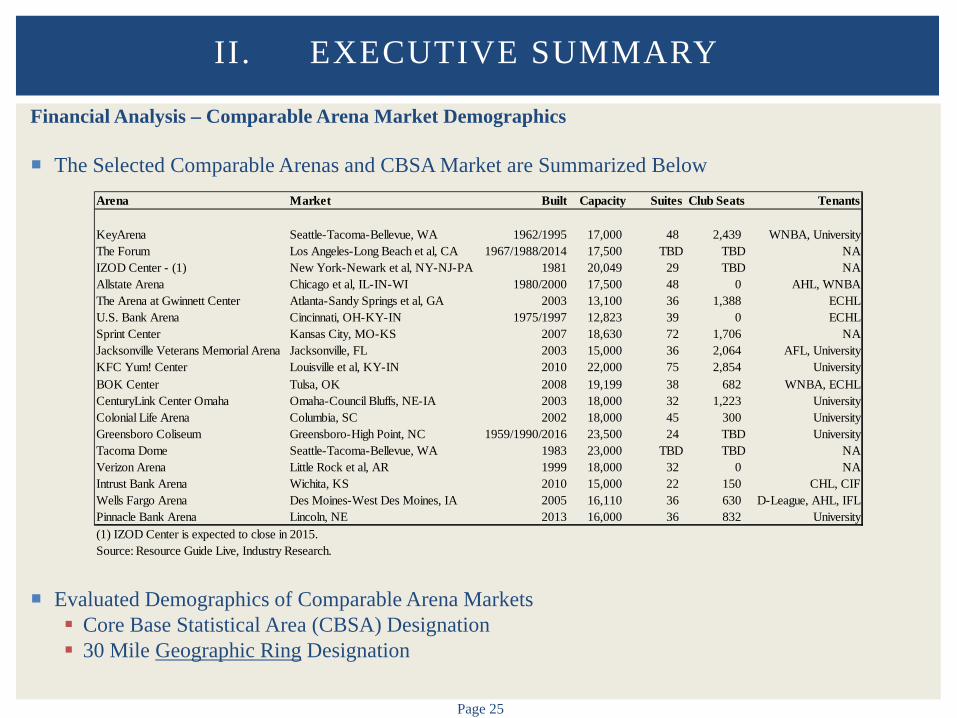

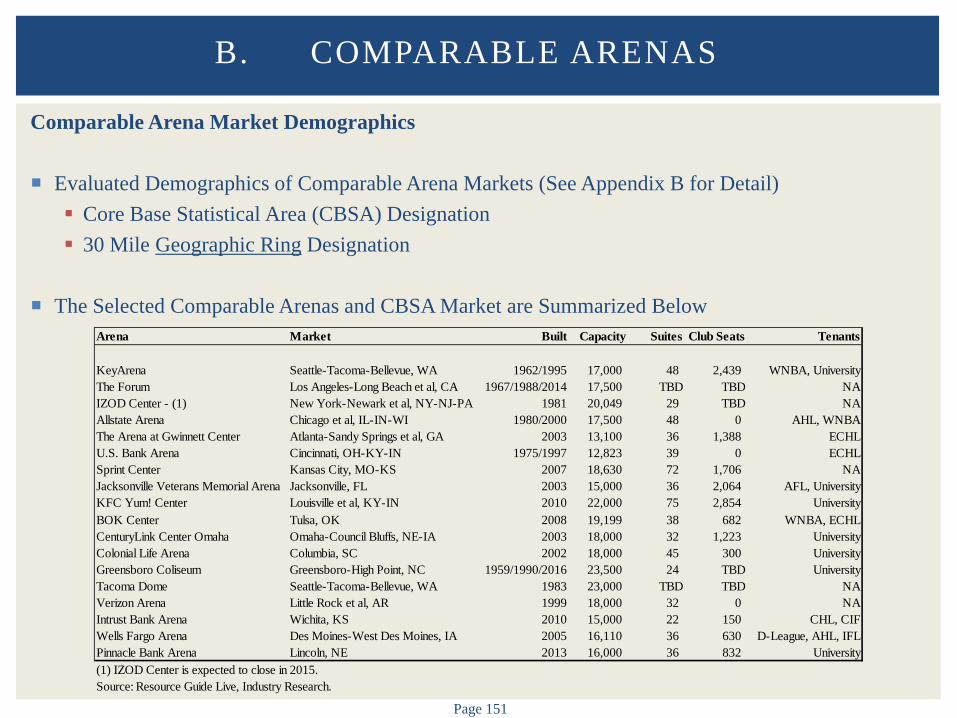

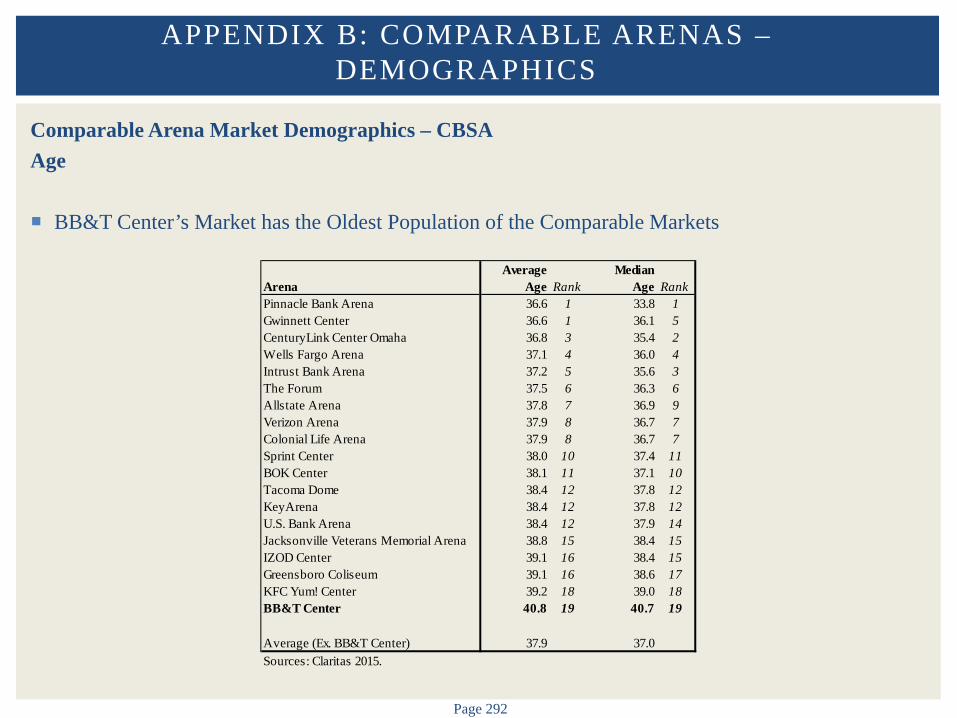

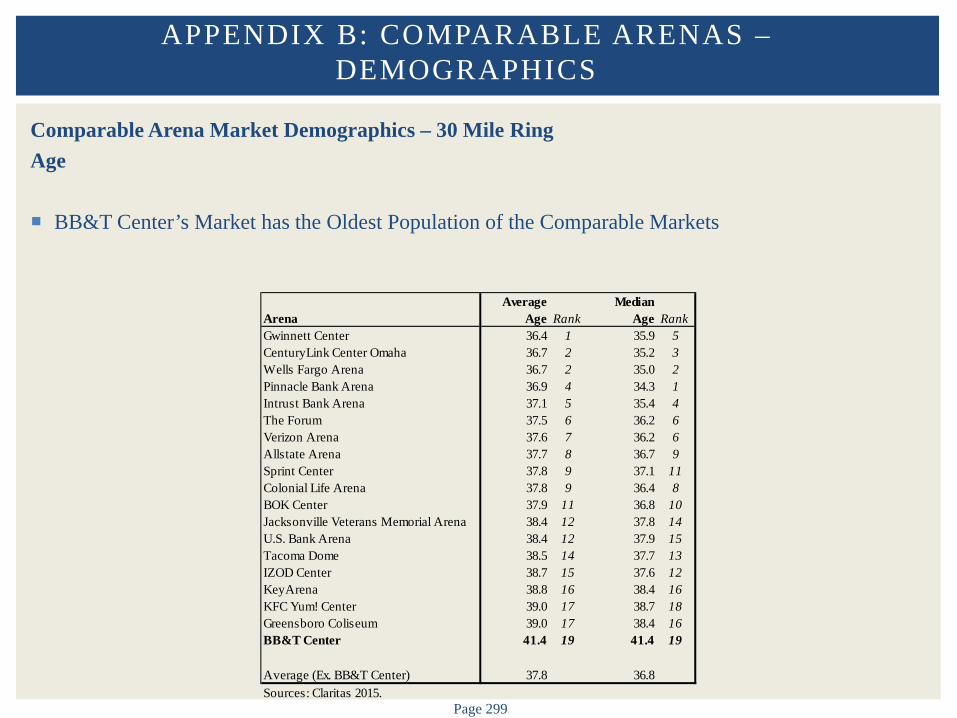

Financial Analysis – Comparable Arena Market Demographics

The Selected Comparable Arenas and CBSA Market are Summarized Below

Evaluated Demographics of Comparable Arena Markets Core Base Statistical Area (CBSA) Designation 30 Mile Geographic Ring Designation

II. EXECUTIVE SUMMARY

Arena Market Built Capacity Suites Club Seats Tenants

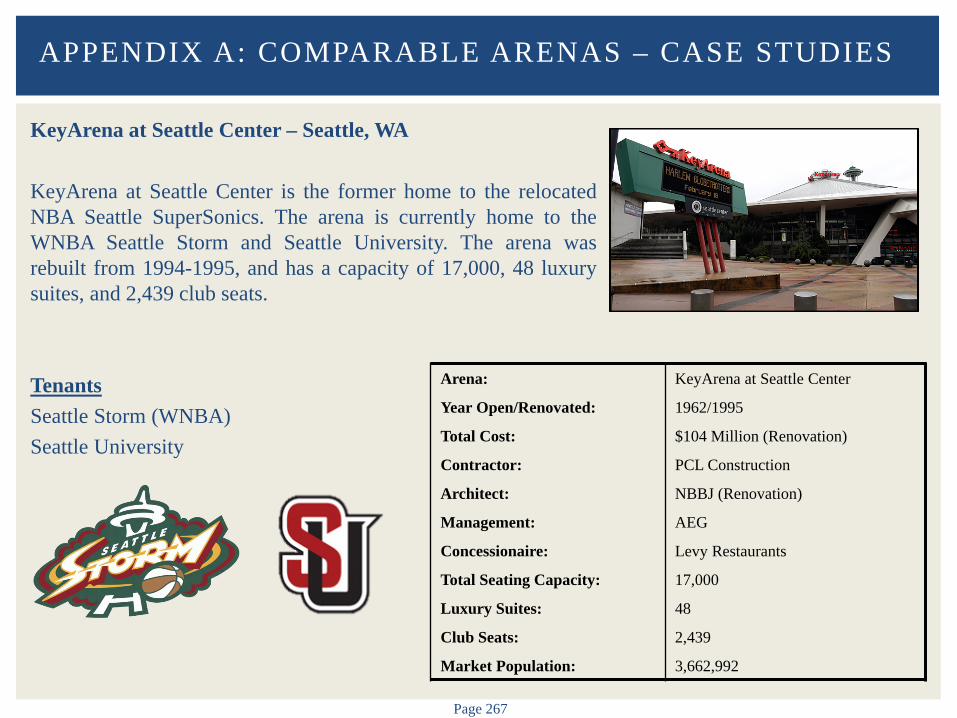

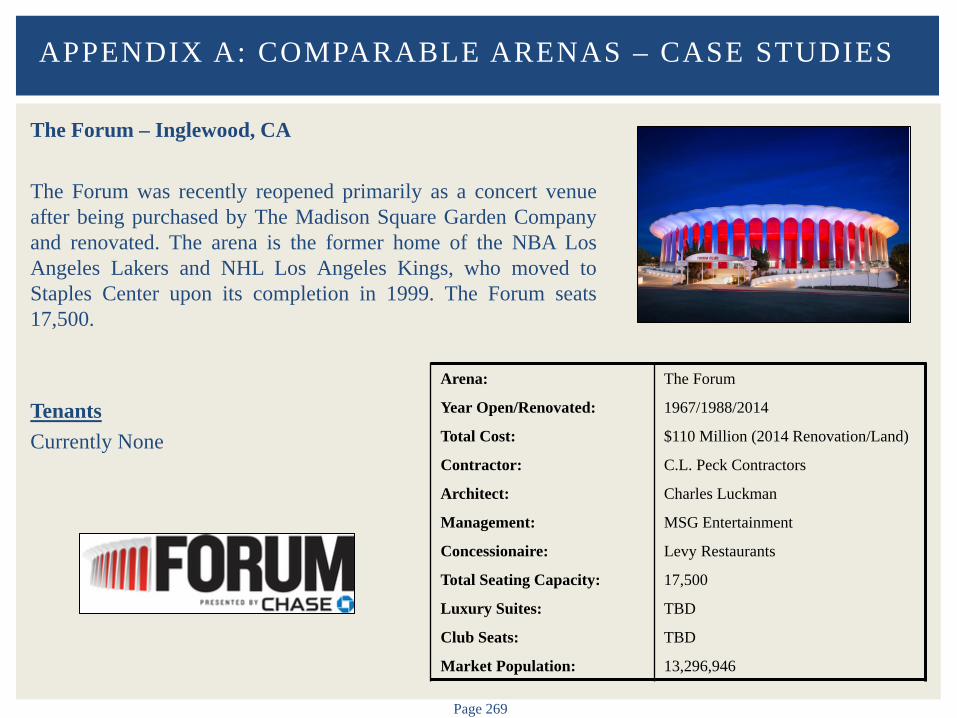

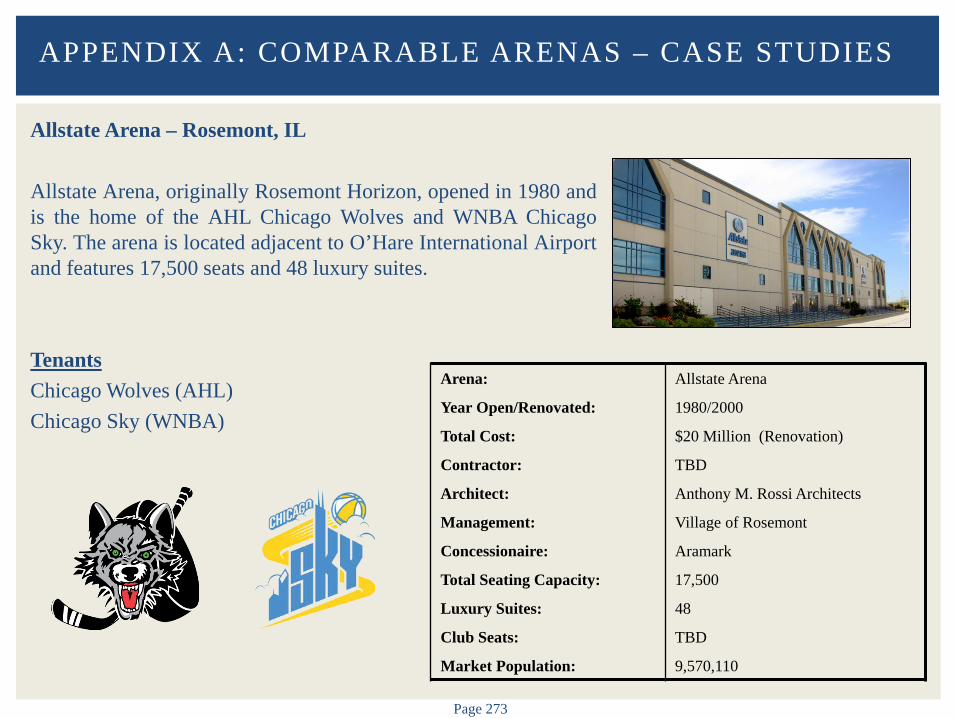

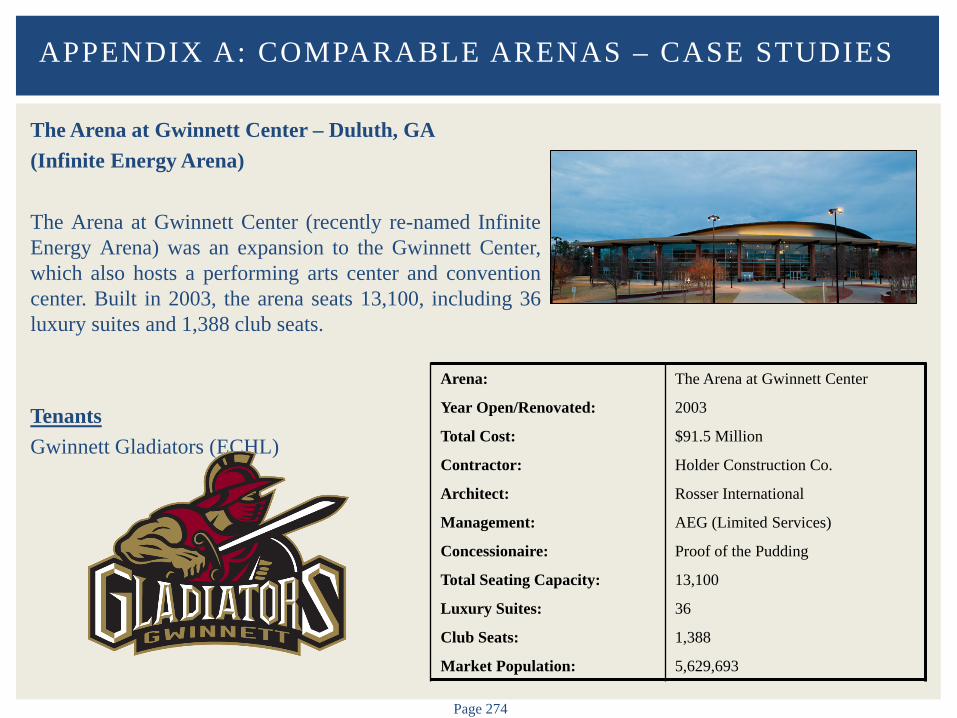

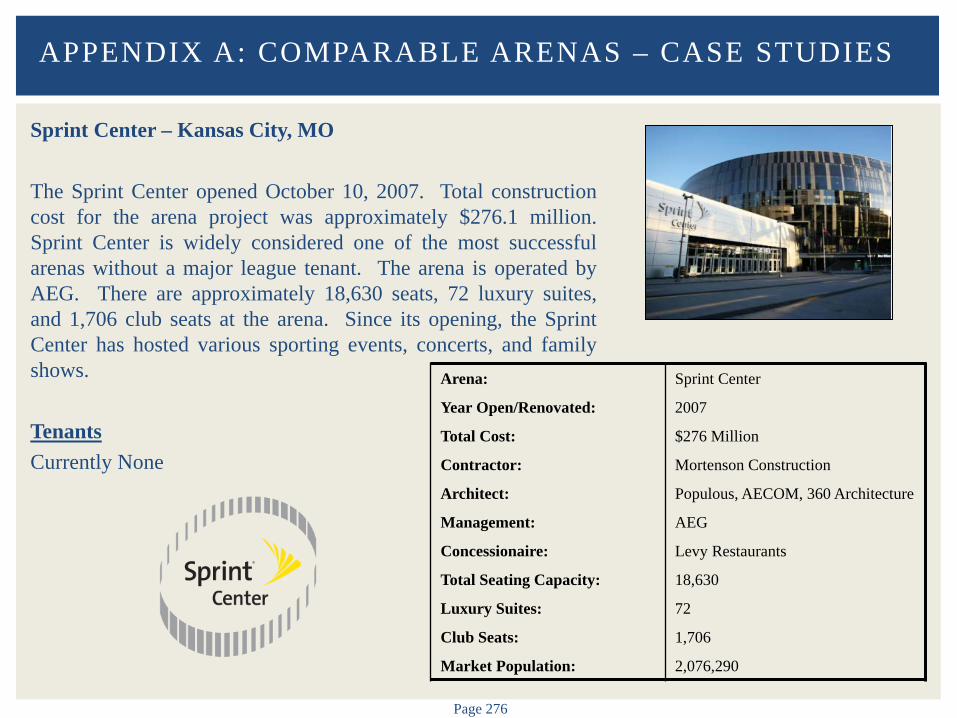

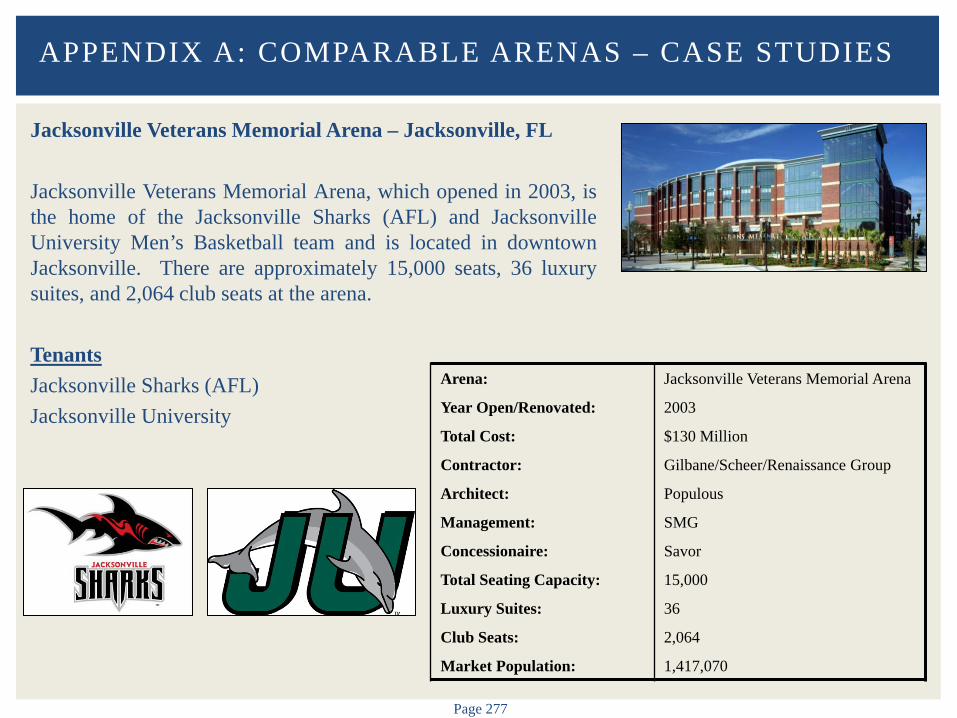

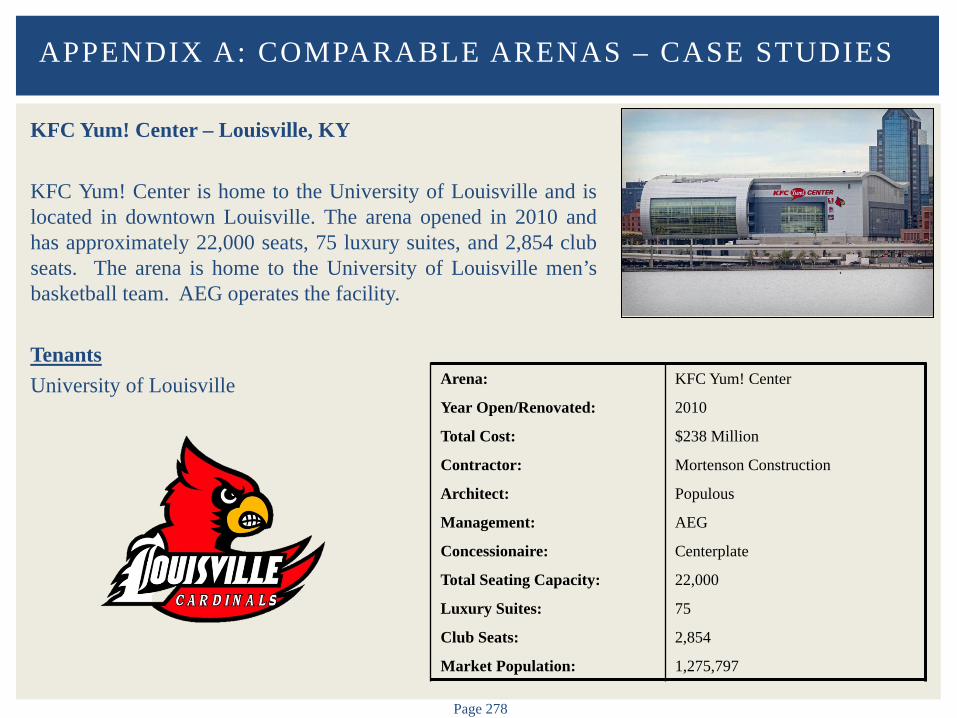

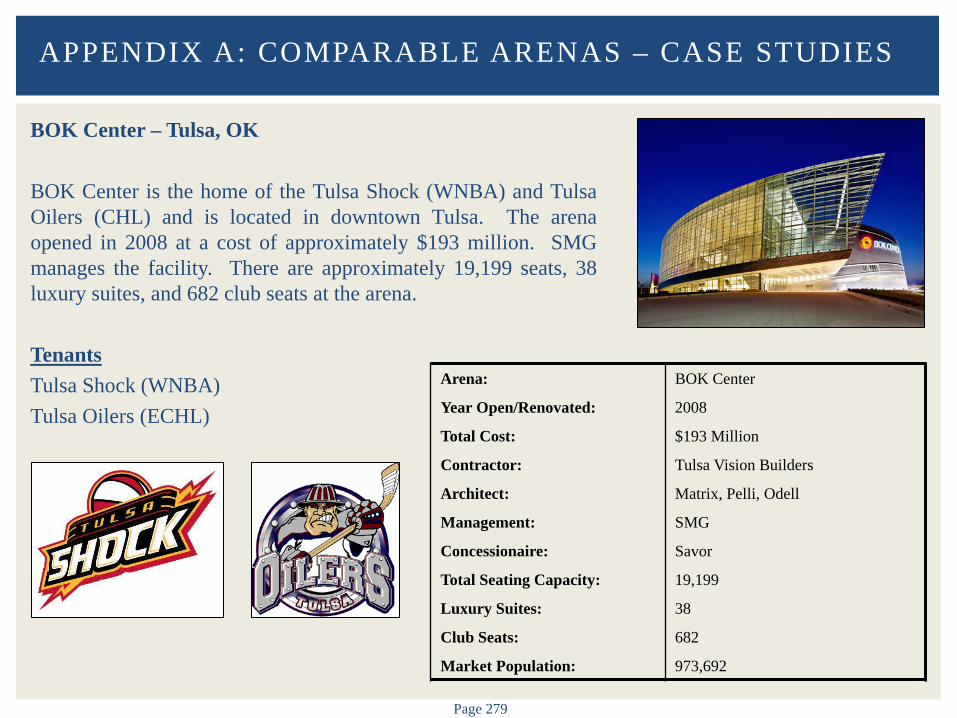

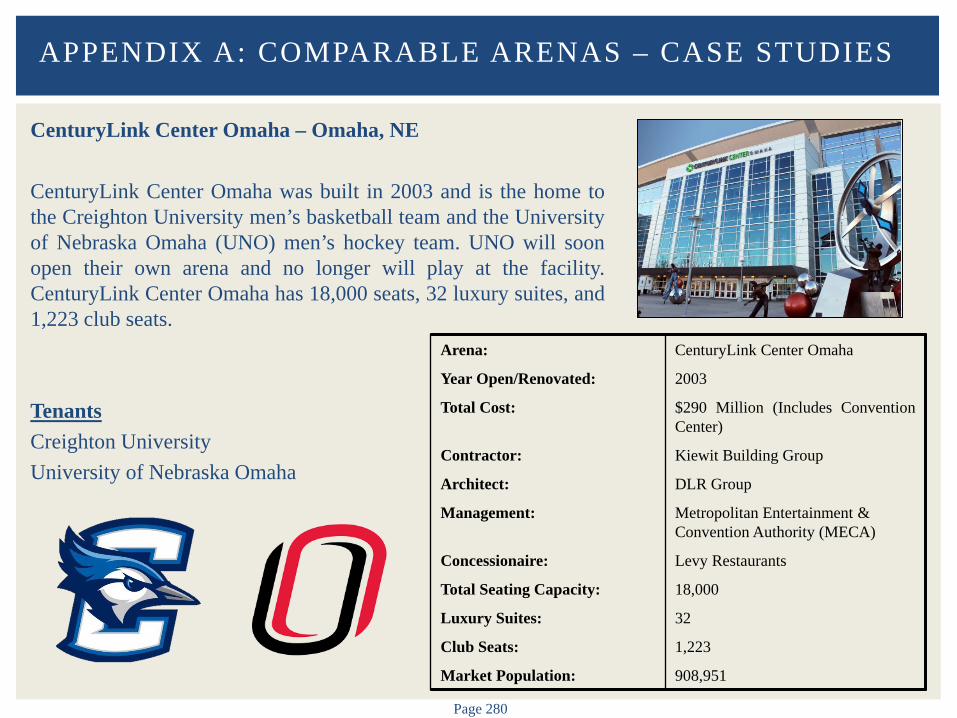

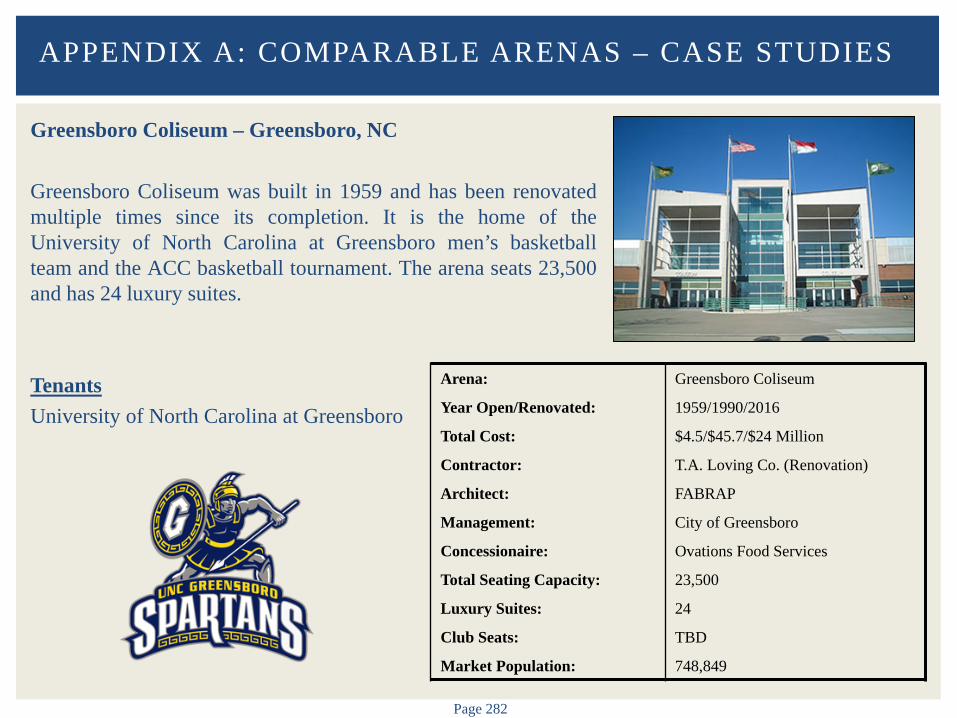

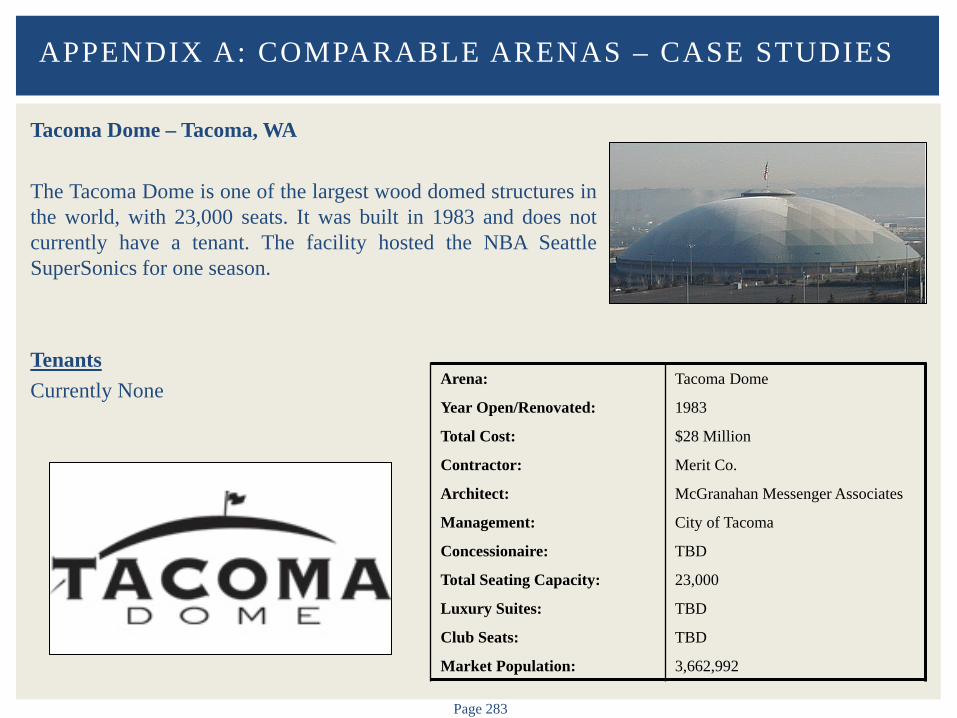

KeyArena Seattle-Tacoma-Bellevue, WA 1962/1995 17,000 48 2,439 WNBA, UniversityThe Forum Los Angeles-Long Beach et al, CA 1967/1988/2014 17,500 TBD TBD NAIZOD Center - (1) New York-Newark et al, NY-NJ-PA 1981 20,049 29 TBD NAAllstate Arena Chicago et al, IL-IN-WI 1980/2000 17,500 48 0 AHL, WNBAThe Arena at Gwinnett Center Atlanta-Sandy Springs et al, GA 2003 13,100 36 1,388 ECHLU.S. Bank Arena Cincinnati, OH-KY-IN 1975/1997 12,823 39 0 ECHLSprint Center Kansas City, MO-KS 2007 18,630 72 1,706 NAJacksonville Veterans Memorial Arena Jacksonville, FL 2003 15,000 36 2,064 AFL, UniversityKFC Yum! Center Louisville et al, KY-IN 2010 22,000 75 2,854 UniversityBOK Center Tulsa, OK 2008 19,199 38 682 WNBA, ECHLCenturyLink Center Omaha Omaha-Council Bluffs, NE-IA 2003 18,000 32 1,223 UniversityColonial Life Arena Columbia, SC 2002 18,000 45 300 UniversityGreensboro Coliseum Greensboro-High Point, NC 1959/1990/2016 23,500 24 TBD UniversityTacoma Dome Seattle-Tacoma-Bellevue, WA 1983 23,000 TBD TBD NAVerizon Arena Little Rock et al, AR 1999 18,000 32 0 NAIntrust Bank Arena Wichita, KS 2010 15,000 22 150 CHL, CIFWells Fargo Arena Des Moines-West Des Moines, IA 2005 16,110 36 630 D-League, AHL, IFLPinnacle Bank Arena Lincoln, NE 2013 16,000 36 832 University(1) IZOD Center is expected to close in 2015.Source: Resource Guide Live, Industry Research.

Page 26

Financial Analysis – Summary of Cash Flows

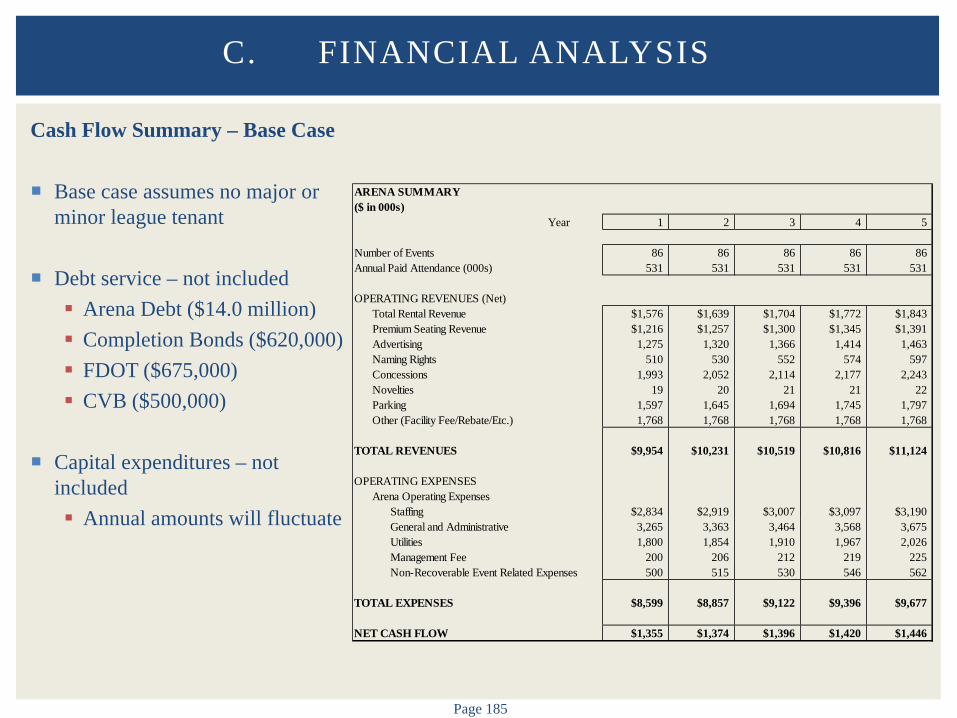

Base case assumes no major or

minor league tenant

Debt service – not included Arena Debt ($14.0 million) Completion Bonds

($620,000) FDOT ($675,000) CVB ($500,000)

Capital expenditures – not

included Annual amounts will

fluctuate

II. EXECUTIVE SUMMARY

ARENA SUMMARY($ in 000s)

Year 1 2 3 4 5

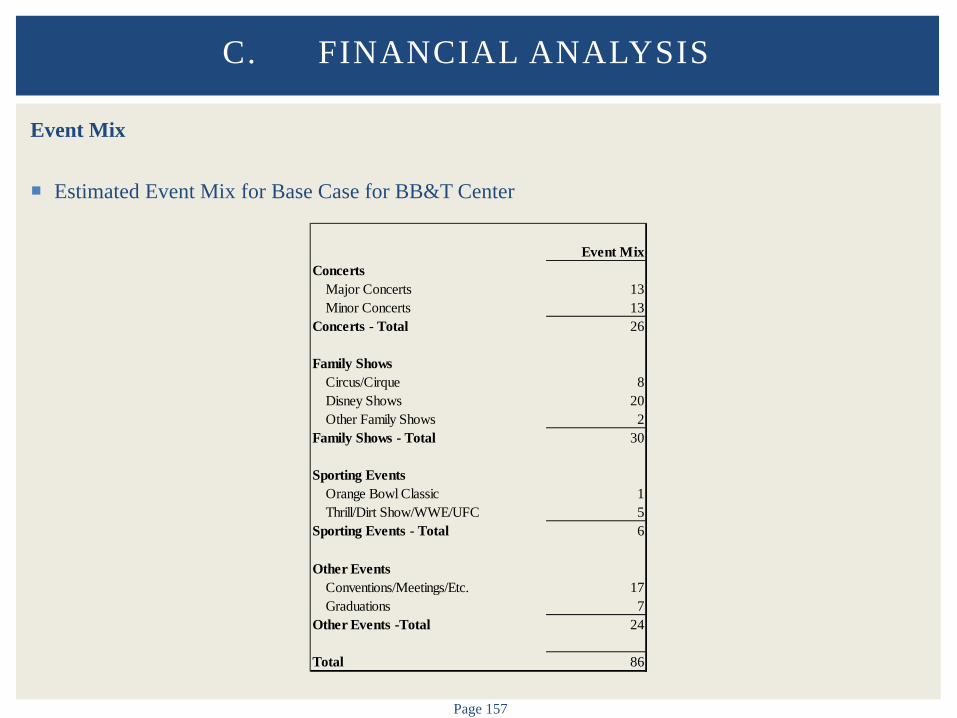

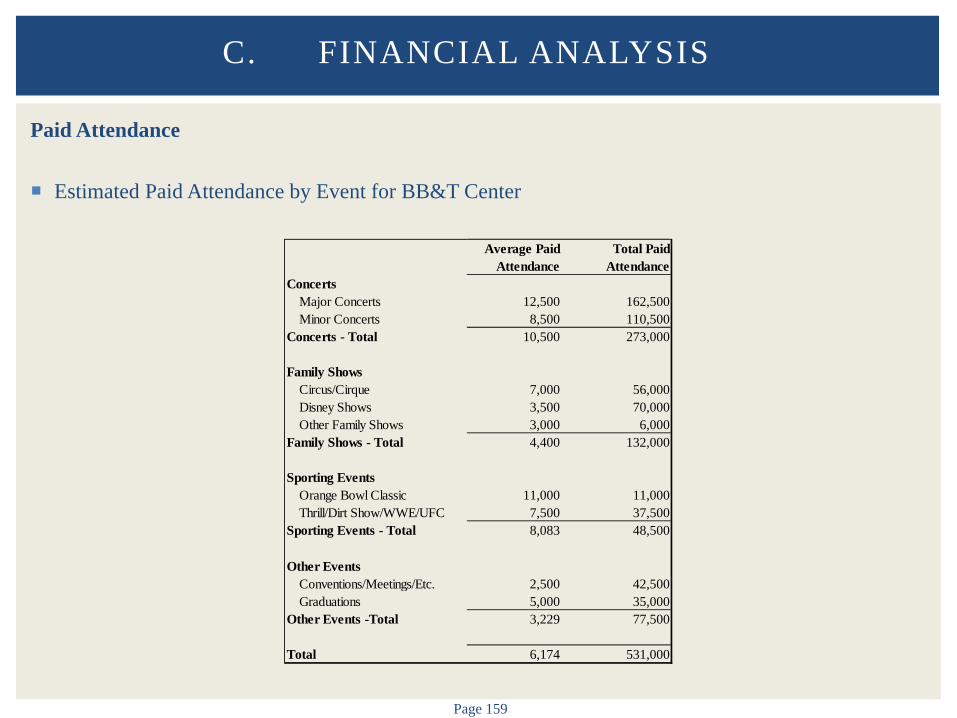

Number of Events 86 86 86 86 86Annual Paid Attendance (000s) 531 531 531 531 531

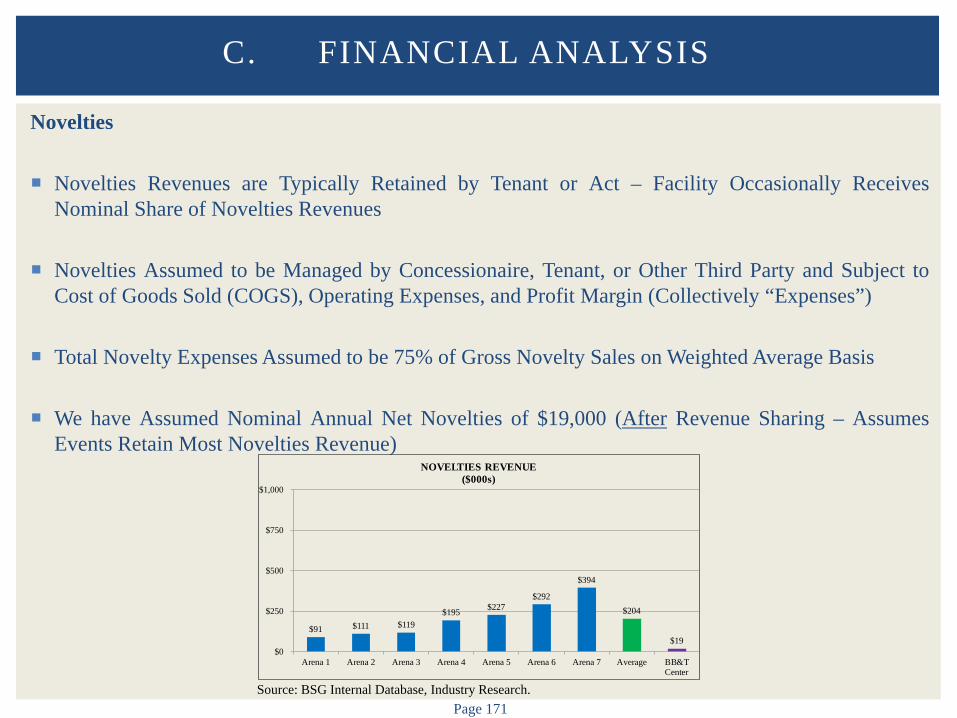

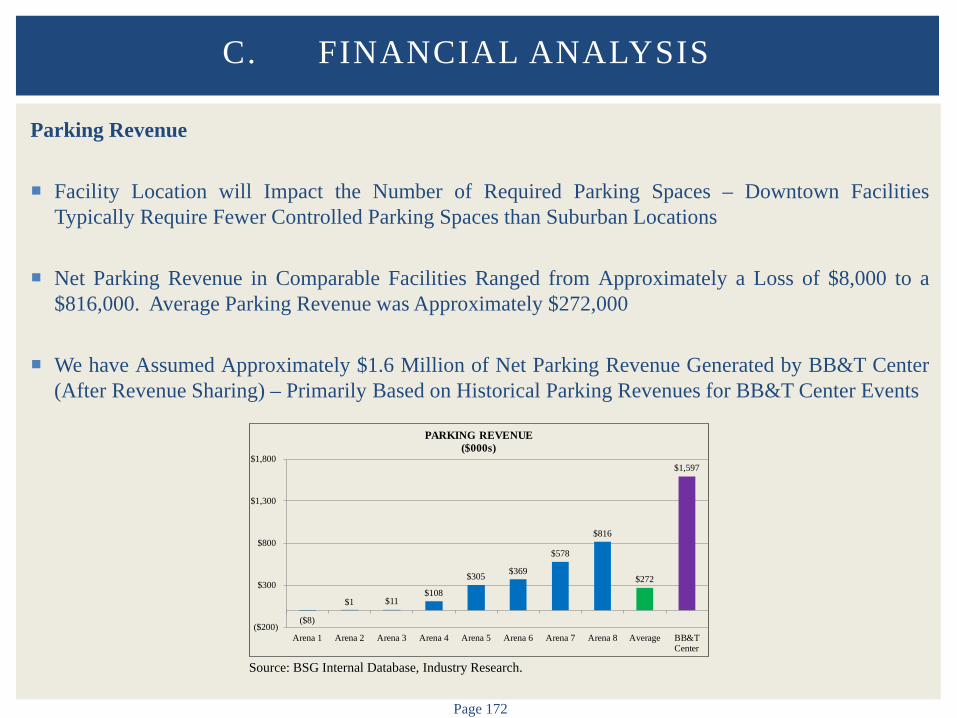

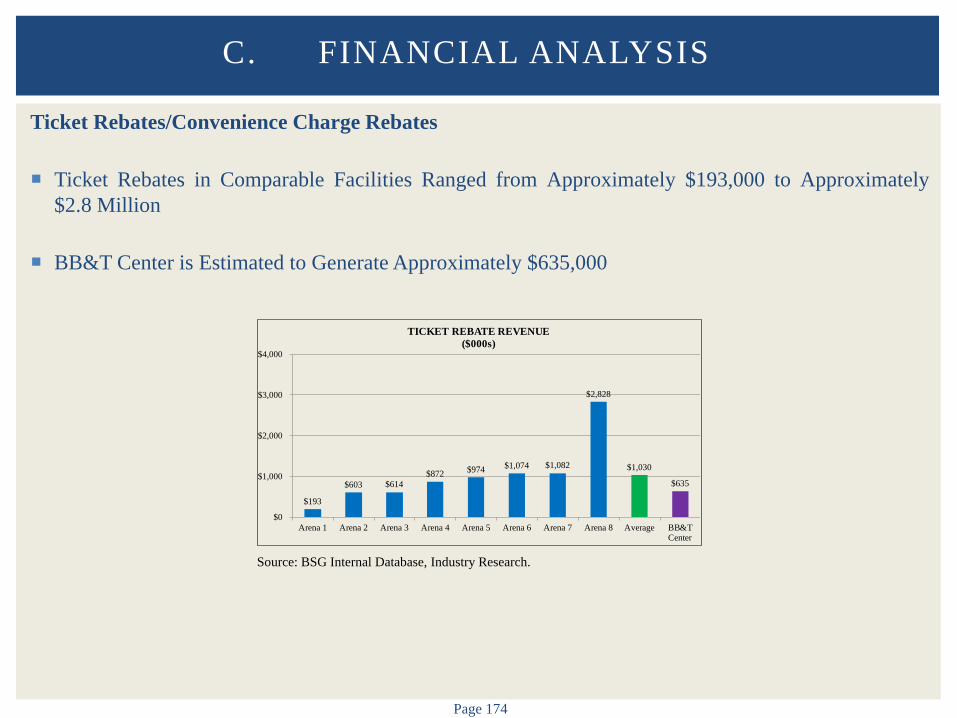

OPERATING REVENUES (Net)Total Rental Revenue $1,576 $1,639 $1,704 $1,772 $1,843Premium Seating Revenue $1,216 $1,257 $1,300 $1,345 $1,391Advertising 1,275 1,320 1,366 1,414 1,463Naming Rights 510 530 552 574 597Concessions 1,993 2,052 2,114 2,177 2,243Novelties 19 20 21 21 22Parking 1,597 1,645 1,694 1,745 1,797Other (Facility Fee/Rebate/Etc.) 1,768 1,768 1,768 1,768 1,768

TOTAL REVENUES $9,954 $10,231 $10,519 $10,816 $11,124

OPERATING EXPENSESArena Operating Expenses

Staffing $2,834 $2,919 $3,007 $3,097 $3,190General and Administrative 3,265 3,363 3,464 3,568 3,675Utilities 1,800 1,854 1,910 1,967 2,026Management Fee 200 206 212 219 225Non-Recoverable Event Related Expenses 500 515 530 546 562

TOTAL EXPENSES $8,599 $8,857 $9,122 $9,396 $9,677

NET CASH FLOW $1,355 $1,374 $1,396 $1,420 $1,446

Page 27

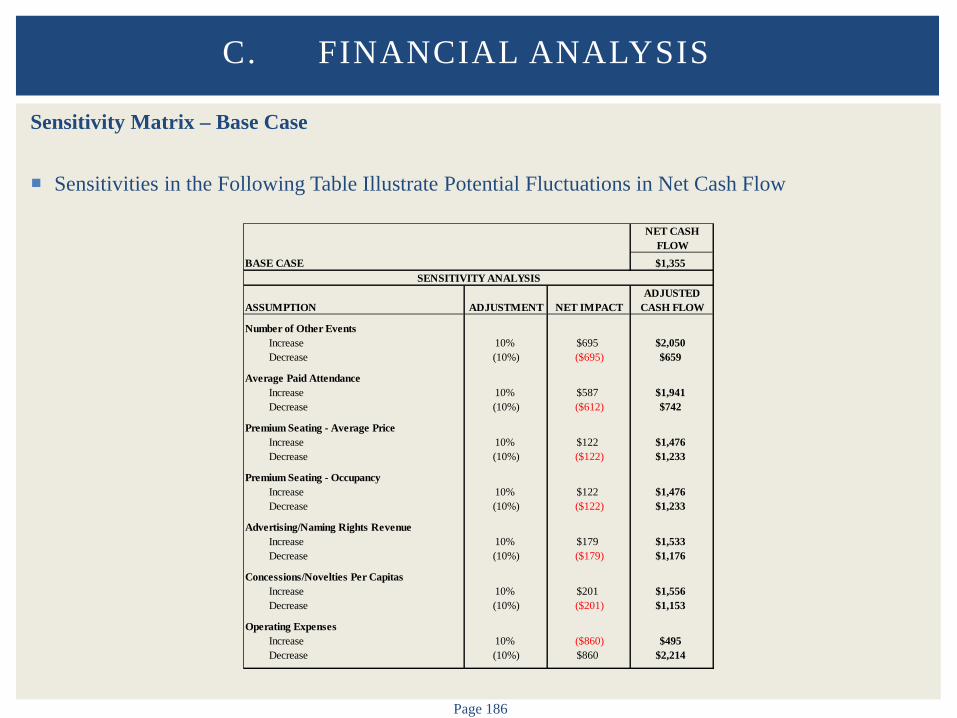

Financial Analysis – Sensitivity Matrix (Base Case) Sensitivities in the Following Table

Illustrate Potential Fluctuations in Net Cash Flow

Base case assumes no major or minor

league tenant

Debt service – not included Arena Debt ($14.0 million) Completion Bonds ($620,000) FDOT ($675,000) CVB ($500,000)

Capital expenditures – not included Annual amounts will fluctuate

II. EXECUTIVE SUMMARY

NET CASHFLOW

BASE CASE $1,355

ADJUSTEDASSUMPTION ADJUSTMENT NET IMPACT CASH FLOW

Number of Other Events Increase 10% $695 $2,050Decrease (10%) ($695) $659

Average Paid AttendanceIncrease 10% $587 $1,941Decrease (10%) ($612) $742

Premium Seating - Average PriceIncrease 10% $122 $1,476Decrease (10%) ($122) $1,233

Premium Seating - OccupancyIncrease 10% $122 $1,476Decrease (10%) ($122) $1,233

Advertising/Naming Rights RevenueIncrease 10% $179 $1,533Decrease (10%) ($179) $1,176

Concessions/Novelties Per CapitasIncrease 10% $201 $1,556Decrease (10%) ($201) $1,153

Operating ExpensesIncrease 10% ($860) $495Decrease (10%) $860 $2,214

SENSITIVITY ANALYSIS

Page 28

Financial Analysis Sensitivity #1 – Arena with ECHL Tenant Major Assumptions/Variances from

Base Case Cash Flow Include 36 ECHL Events Decrease Major Concerts by 1 Decrease Minor Concerts by 1 Decrease Family Shows by 1 Increase Naming Rights Revenue by

$75,000 (Gross) Increase Advertising Revenue by

$75,000 (Gross) Increase Utilities Expense by

$250,000 Increase Staffing and G&A

Expenses by 5.0%

II. EXECUTIVE SUMMARY

ARENA SUMMARY($ in 000s)

Year 1 2 3 4 5

Number of Events 119 119 119 119 119Annual Paid Attendance (000s) 651 651 651 651 651

OPERATING REVENUES (Net)Total Rental Revenue $1,494 $1,553 $1,615 $1,680 $1,747Premium Seating Revenue $1,216 $1,257 $1,300 $1,345 $1,391Advertising 1,339 1,386 1,434 1,484 1,536Naming Rights 574 597 621 645 671Concessions 1,981 2,040 2,102 2,165 2,229Novelties 19 20 21 21 22Parking 1,708 1,759 1,812 1,866 1,922Other (Facility Fee/Rebate/Etc.) 2,202 2,202 2,202 2,202 2,202

TOTAL REVENUES $10,532 $10,814 $11,106 $11,408 $11,720

OPERATING EXPENSESArena Operating Expenses

Staffing $2,976 $3,065 $3,157 $3,252 $3,349General and Administrative 3,428 3,531 3,637 3,746 3,859Utilities 2,050 2,112 2,175 2,240 2,307Management Fee 200 206 212 219 225Non-Recoverable Event Related Expenses 500 515 530 546 562

TOTAL EXPENSES $9,154 $9,429 $9,711 $10,002 $10,302

NET CASH FLOW $1,378 $1,385 $1,395 $1,406 $1,418

Page 29

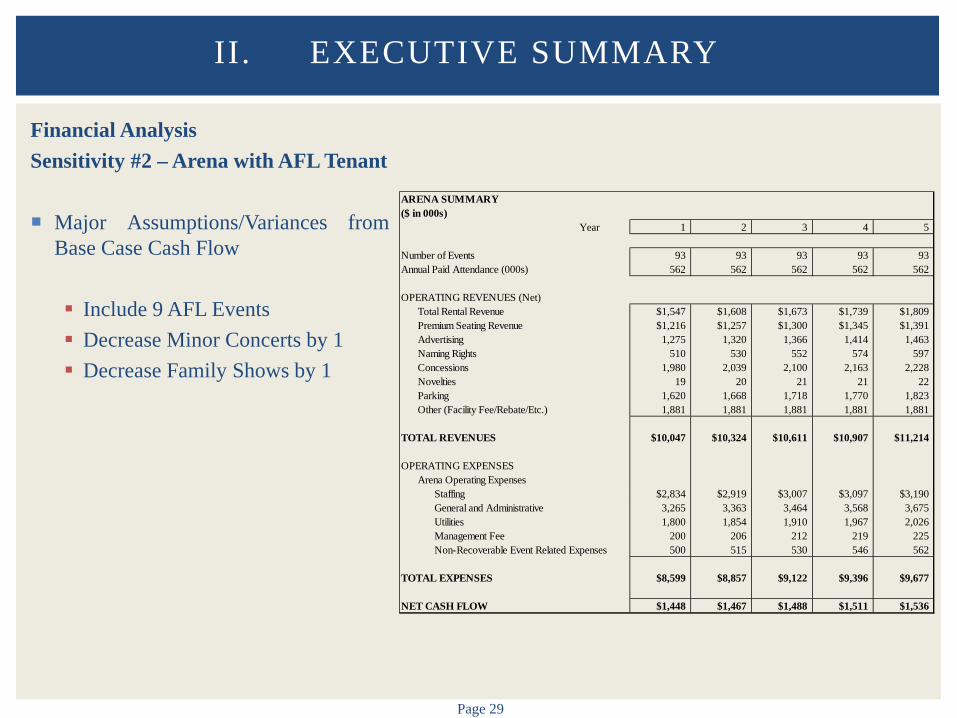

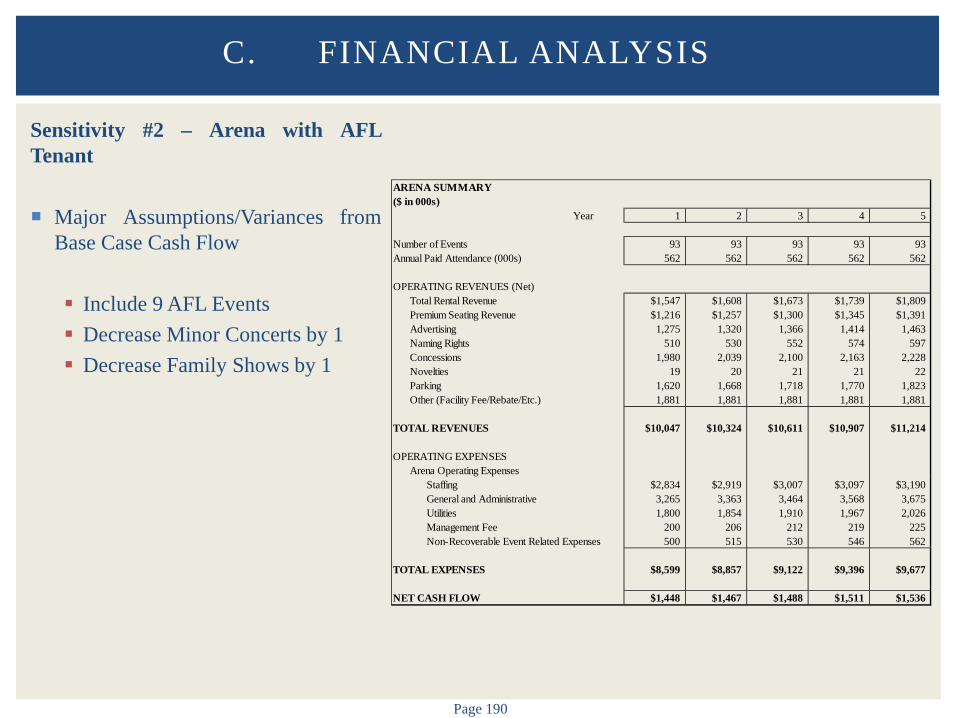

Financial Analysis Sensitivity #2 – Arena with AFL Tenant Major Assumptions/Variances from

Base Case Cash Flow Include 9 AFL Events Decrease Minor Concerts by 1 Decrease Family Shows by 1

II. EXECUTIVE SUMMARY

ARENA SUMMARY($ in 000s)

Year 1 2 3 4 5

Number of Events 93 93 93 93 93Annual Paid Attendance (000s) 562 562 562 562 562

OPERATING REVENUES (Net)Total Rental Revenue $1,547 $1,608 $1,673 $1,739 $1,809Premium Seating Revenue $1,216 $1,257 $1,300 $1,345 $1,391Advertising 1,275 1,320 1,366 1,414 1,463Naming Rights 510 530 552 574 597Concessions 1,980 2,039 2,100 2,163 2,228Novelties 19 20 21 21 22Parking 1,620 1,668 1,718 1,770 1,823Other (Facility Fee/Rebate/Etc.) 1,881 1,881 1,881 1,881 1,881

TOTAL REVENUES $10,047 $10,324 $10,611 $10,907 $11,214

OPERATING EXPENSESArena Operating Expenses

Staffing $2,834 $2,919 $3,007 $3,097 $3,190General and Administrative 3,265 3,363 3,464 3,568 3,675Utilities 1,800 1,854 1,910 1,967 2,026Management Fee 200 206 212 219 225Non-Recoverable Event Related Expenses 500 515 530 546 562

TOTAL EXPENSES $8,599 $8,857 $9,122 $9,396 $9,677

NET CASH FLOW $1,448 $1,467 $1,488 $1,511 $1,536

Page 30

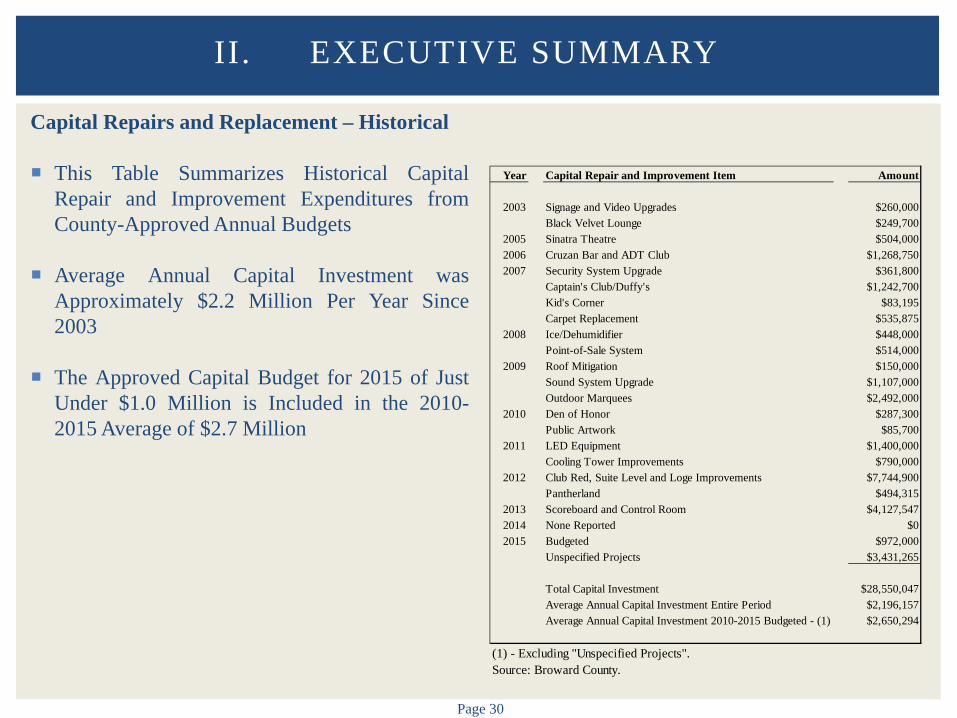

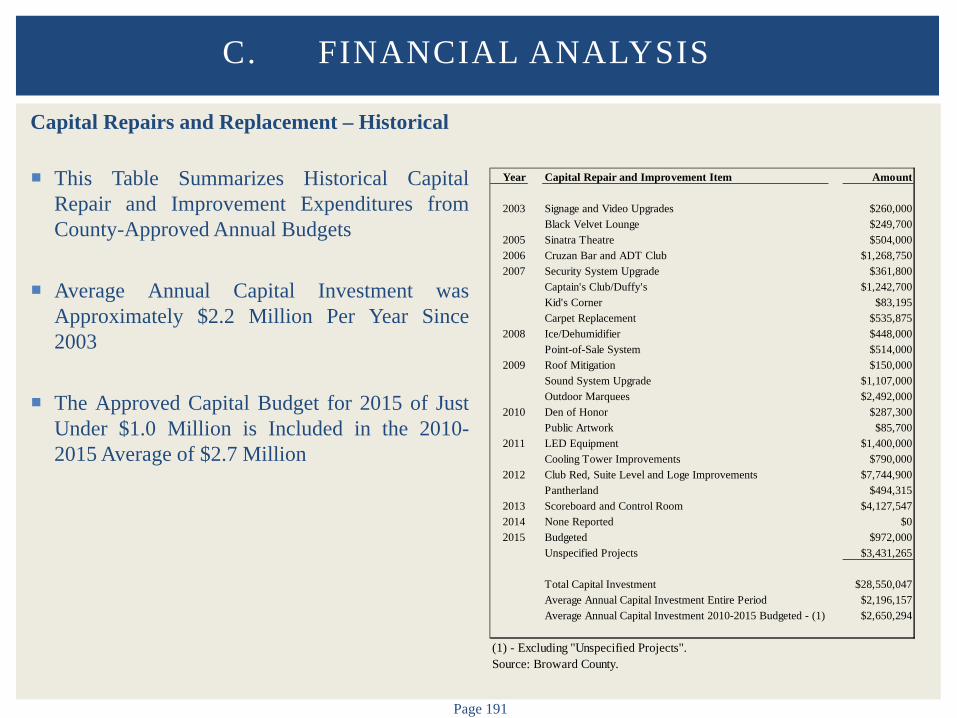

Capital Repairs and Replacement – Historical

This Table Summarizes Historical Capital Repair and Improvement Expenditures from County-Approved Annual Budgets

Average Annual Capital Investment was Approximately $2.2 Million Per Year Since 2003

The Approved Capital Budget for 2015 of Just Under $1.0 Million is Included in the 2010-2015 Average of $2.7 Million

II. EXECUTIVE SUMMARY

Year Capital Repair and Improvement Item Amount

2003 Signage and Video Upgrades $260,000Black Velvet Lounge $249,700

2005 Sinatra Theatre $504,0002006 Cruzan Bar and ADT Club $1,268,7502007 Security System Upgrade $361,800

Captain's Club/Duffy's $1,242,700Kid's Corner $83,195Carpet Replacement $535,875

2008 Ice/Dehumidifier $448,000Point-of-Sale System $514,000

2009 Roof Mitigation $150,000Sound System Upgrade $1,107,000Outdoor Marquees $2,492,000

2010 Den of Honor $287,300Public Artwork $85,700

2011 LED Equipment $1,400,000Cooling Tower Improvements $790,000

2012 Club Red, Suite Level and Loge Improvements $7,744,900Pantherland $494,315

2013 Scoreboard and Control Room $4,127,5472014 None Reported $02015 Budgeted $972,000

Unspecified Projects $3,431,265

Total Capital Investment $28,550,047Average Annual Capital Investment Entire Period $2,196,157Average Annual Capital Investment 2010-2015 Budgeted - (1) $2,650,294

(1) - Excluding "Unspecified Projects".Source: Broward County.

Page 31

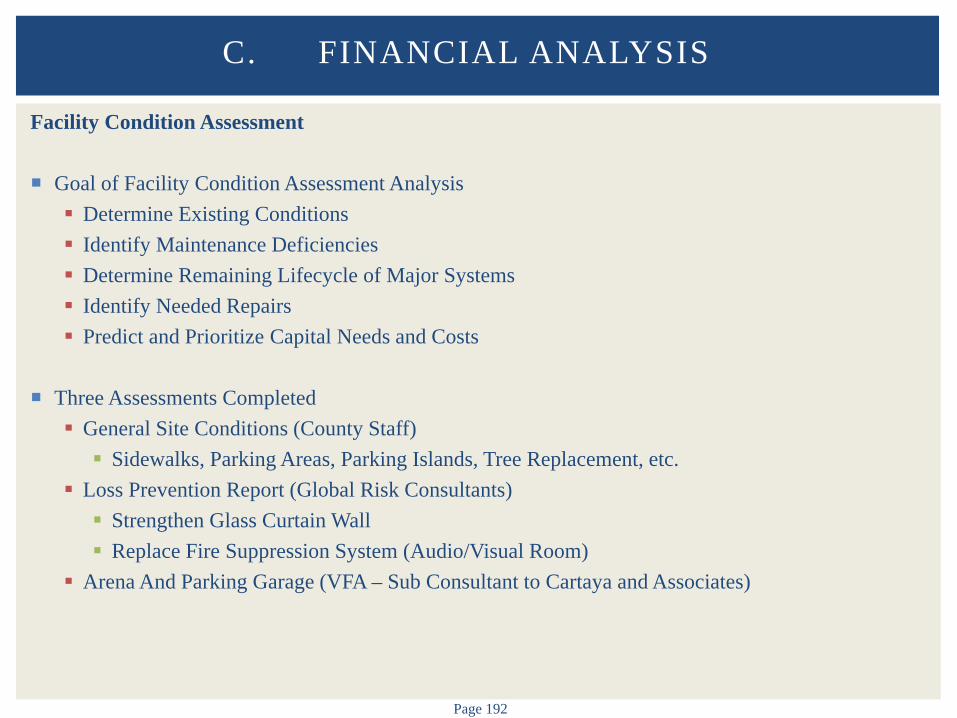

Facility Condition Assessment Goal of Facility Condition Assessment Analysis Determine Existing Conditions Identify Maintenance Deficiencies Determine Remaining Lifecycle of Major Systems Identify Needed Repairs Predict and Prioritize Capital Needs and Costs

Three Assessments Completed General Site Conditions (County Staff) Sidewalks, Parking Areas, Parking Islands, Tree Replacement, etc.

Loss Prevention Report (Global Risk Consultants) Strengthen Glass Curtain Wall Replace Fire Suppression System (Audio/Visual Room)

Arena And Parking Garage (VFA – Sub Consultant to Cartaya and Associates)

II. EXECUTIVE SUMMARY

Page 32

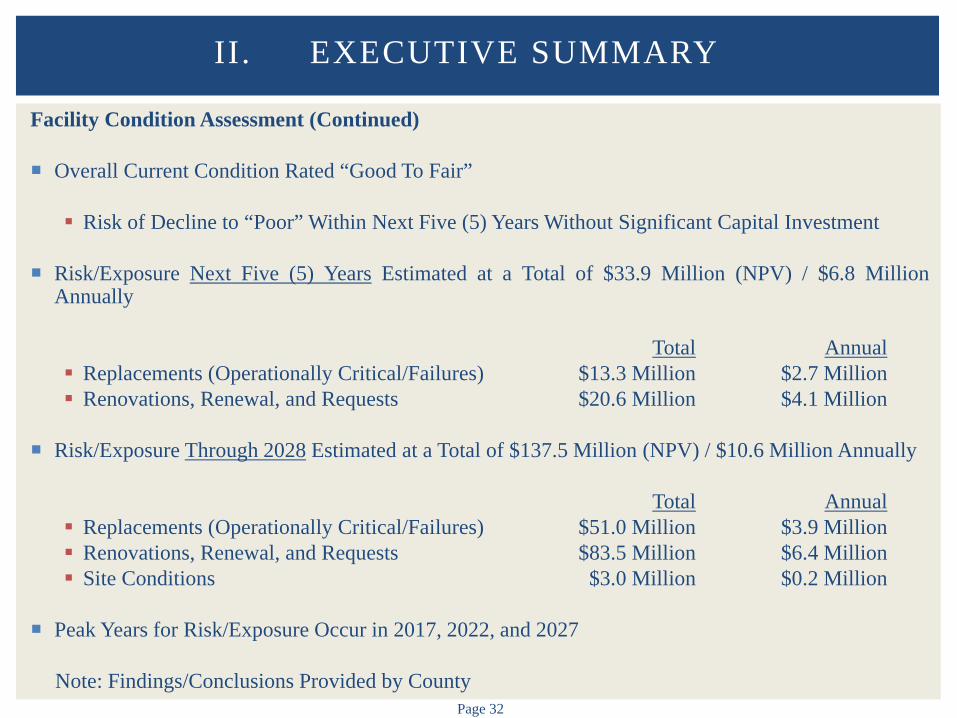

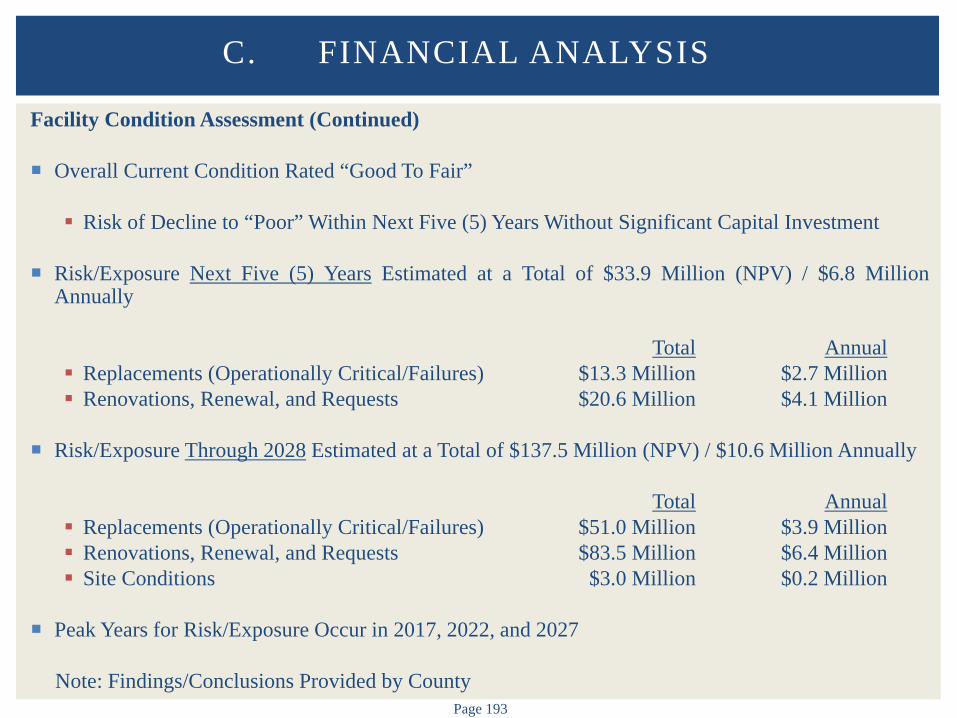

Facility Condition Assessment (Continued) Overall Current Condition Rated “Good To Fair”

Risk of Decline to “Poor” Within Next Five (5) Years Without Significant Capital Investment

Risk/Exposure Next Five (5) Years Estimated at a Total of $33.9 Million (NPV) / $6.8 Million

Annually Total Annual Replacements (Operationally Critical/Failures) $13.3 Million $2.7 Million Renovations, Renewal, and Requests $20.6 Million $4.1 Million

Risk/Exposure Through 2028 Estimated at a Total of $137.5 Million (NPV) / $10.6 Million Annually

Total Annual Replacements (Operationally Critical/Failures) $51.0 Million $3.9 Million Renovations, Renewal, and Requests $83.5 Million $6.4 Million Site Conditions $3.0 Million $0.2 Million

Peak Years for Risk/Exposure Occur in 2017, 2022, and 2027

Note: Findings/Conclusions Provided by County

II. EXECUTIVE SUMMARY

Page 33

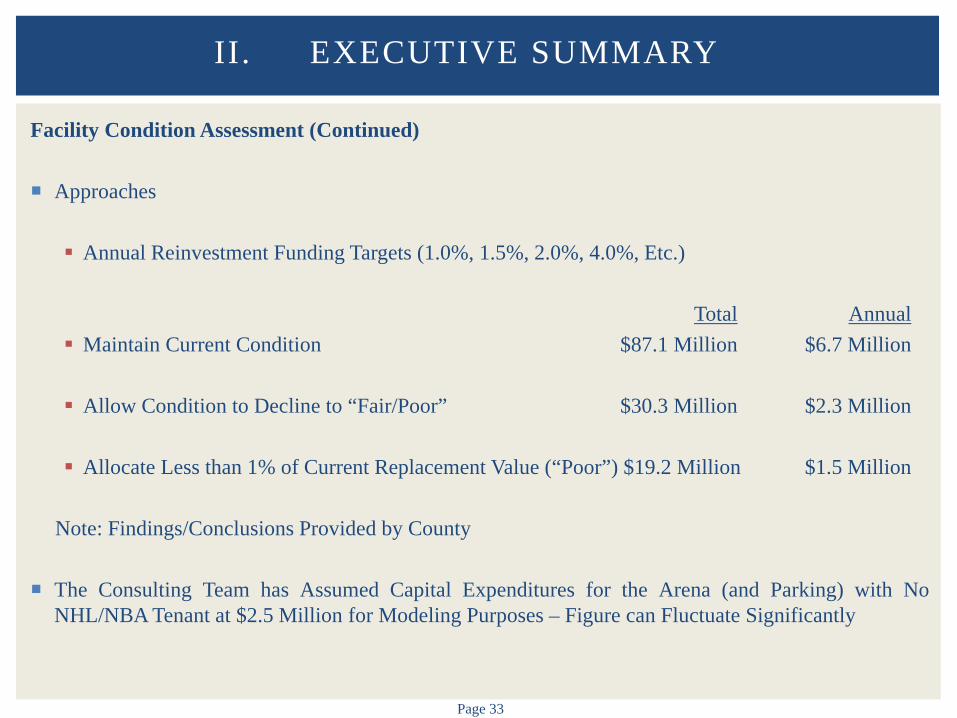

Facility Condition Assessment (Continued) Approaches

Annual Reinvestment Funding Targets (1.0%, 1.5%, 2.0%, 4.0%, Etc.)

Total Annual Maintain Current Condition $87.1 Million $6.7 Million Allow Condition to Decline to “Fair/Poor” $30.3 Million $2.3 Million

Allocate Less than 1% of Current Replacement Value (“Poor”) $19.2 Million $1.5 Million

Note: Findings/Conclusions Provided by County

The Consulting Team has Assumed Capital Expenditures for the Arena (and Parking) with No

NHL/NBA Tenant at $2.5 Million for Modeling Purposes – Figure can Fluctuate Significantly

II. EXECUTIVE SUMMARY

Page 34

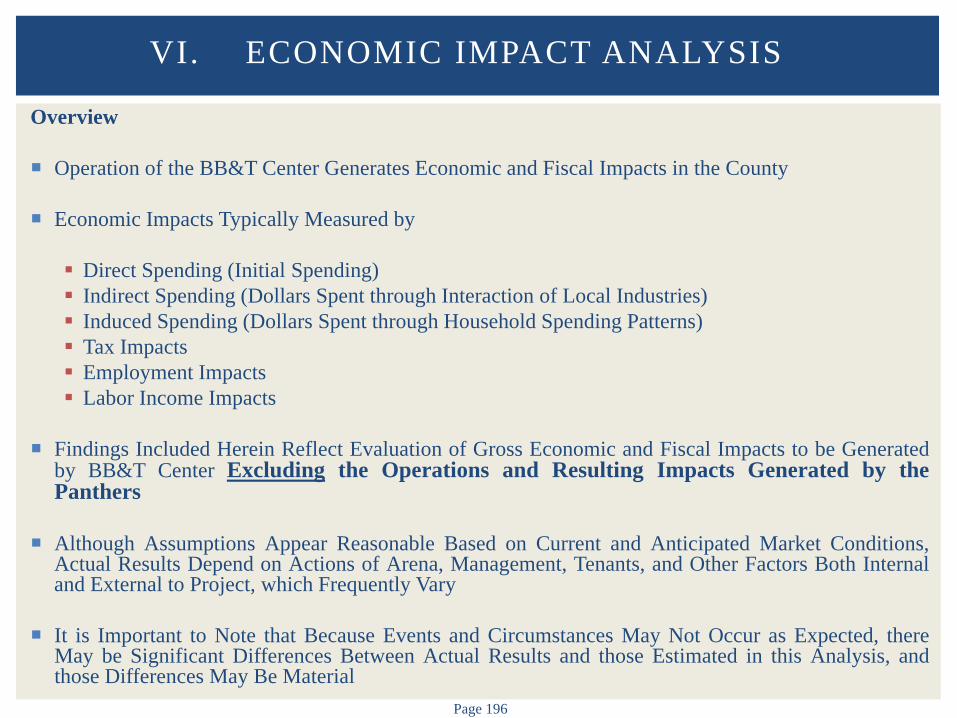

Economic Impact Analysis – Overview

Operation of the BB&T Center Generates Economic and Fiscal Impacts in the County

Economic Impacts Typically Measured by

Direct Spending (Initial Spending) Indirect Spending (Dollars Spent through Interaction of Local Industries) Induced Spending (Dollars Spent through Household Spending Patterns) Tax Impacts Employment Impacts Labor Income Impacts

Findings Included Herein Reflect Evaluation of Gross Economic and Fiscal Impacts to be Generated

by BB&T Center Excluding the Operations and Resulting Impacts Generated by the Panthers

Although Assumptions Appear Reasonable Based on Current and Anticipated Market Conditions, Actual Results Depend on Actions of Arena, Management, Tenants, and Other Factors Both Internal and External to Project, which Frequently Vary

It is Important to Note that Because Events and Circumstances May Not Occur as Expected, there May be Significant Differences Between Actual Results and those Estimated in this Analysis, and those Differences May Be Material

II. EXECUTIVE SUMMARY

Page 35

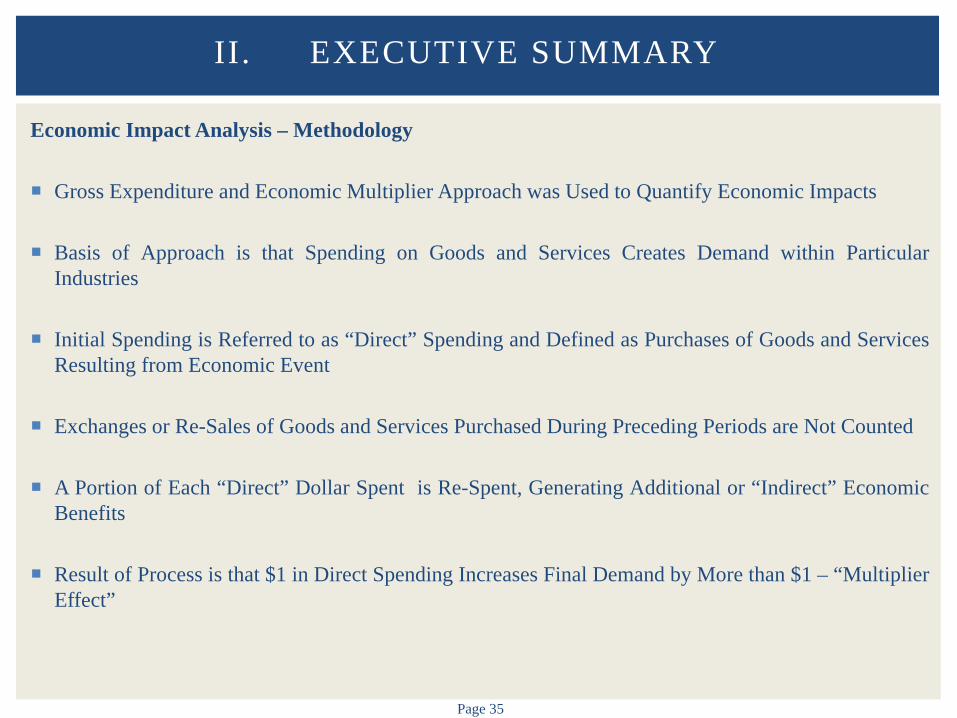

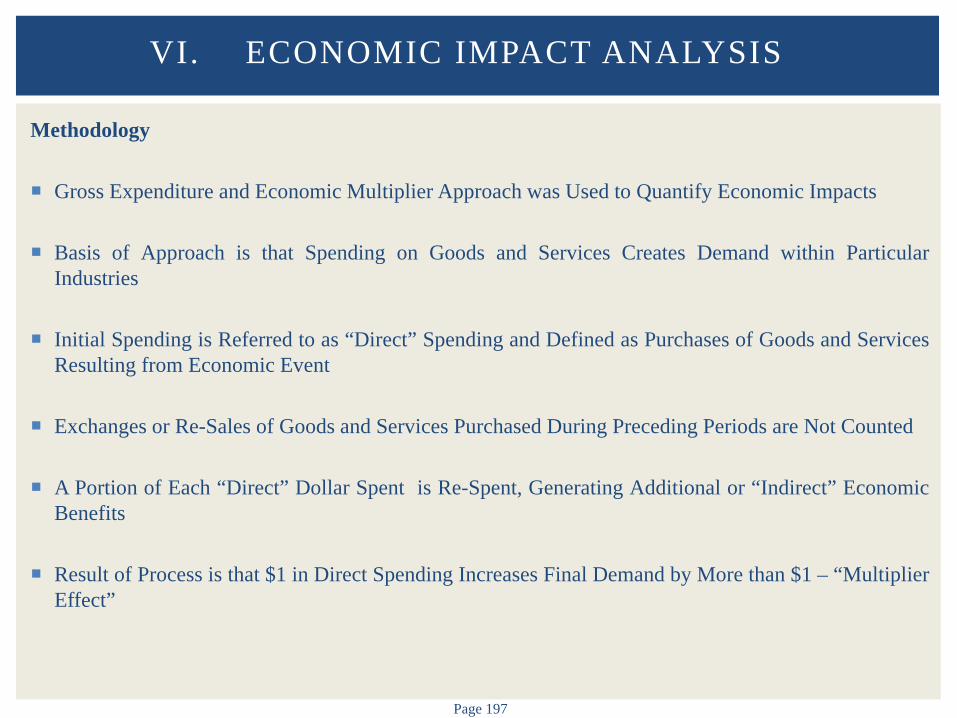

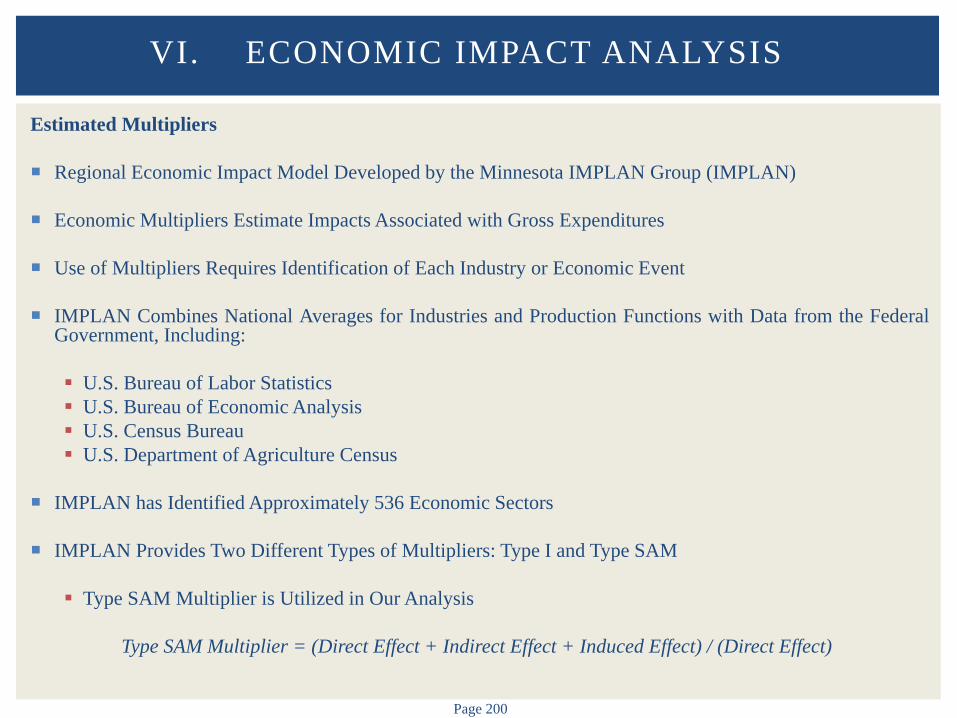

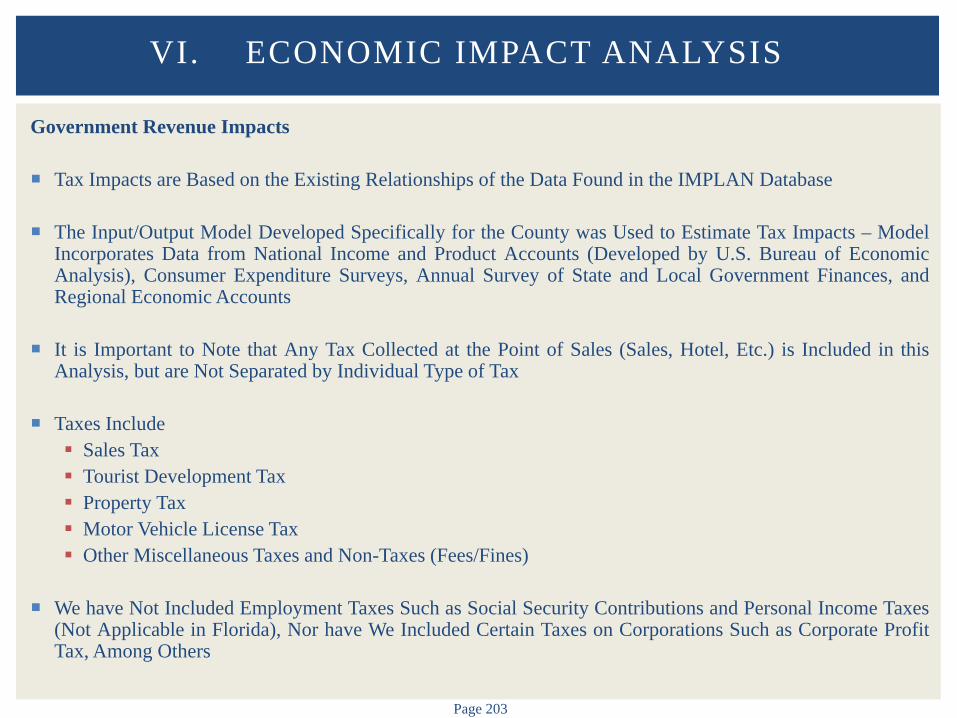

Economic Impact Analysis – Methodology

Gross Expenditure and Economic Multiplier Approach was Used to Quantify Economic Impacts

Basis of Approach is that Spending on Goods and Services Creates Demand within Particular Industries

Initial Spending is Referred to as “Direct” Spending and Defined as Purchases of Goods and Services Resulting from Economic Event

Exchanges or Re-Sales of Goods and Services Purchased During Preceding Periods are Not Counted

A Portion of Each “Direct” Dollar Spent is Re-Spent, Generating Additional or “Indirect” Economic Benefits

Result of Process is that $1 in Direct Spending Increases Final Demand by More than $1 – “Multiplier Effect”

II. EXECUTIVE SUMMARY

Page 36

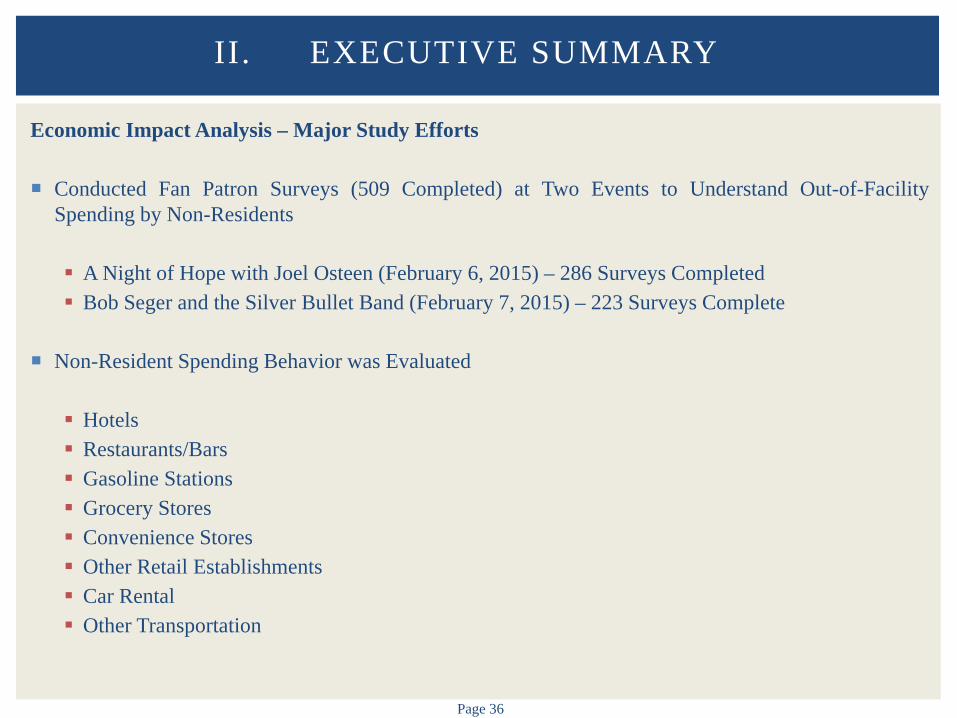

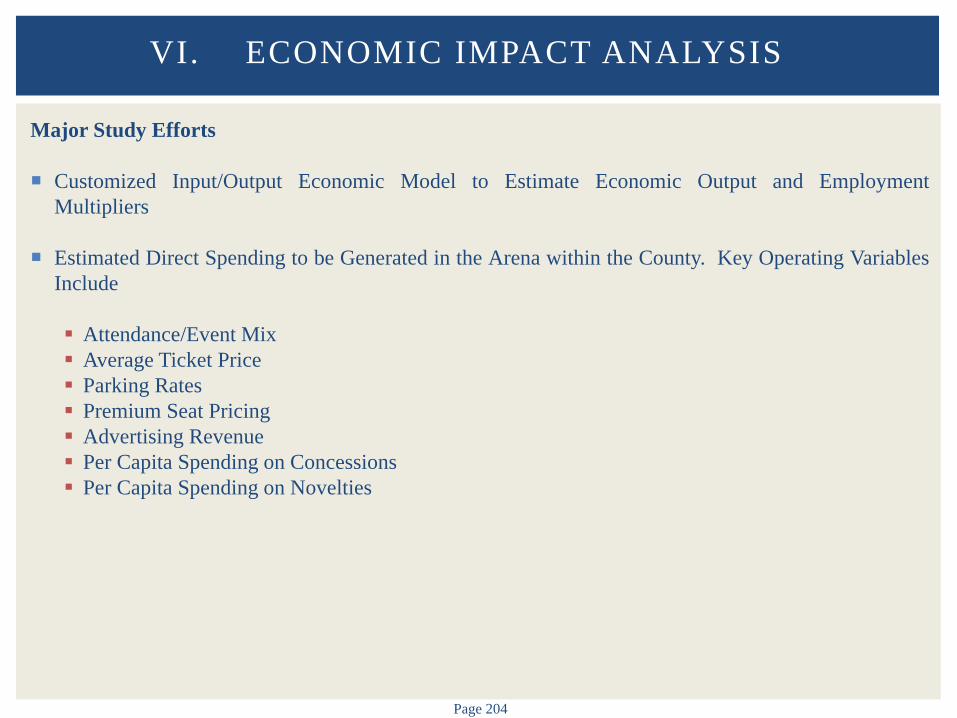

Economic Impact Analysis – Major Study Efforts

Conducted Fan Patron Surveys (509 Completed) at Two Events to Understand Out-of-Facility Spending by Non-Residents A Night of Hope with Joel Osteen (February 6, 2015) – 286 Surveys Completed Bob Seger and the Silver Bullet Band (February 7, 2015) – 223 Surveys Complete

Non-Resident Spending Behavior was Evaluated

Hotels Restaurants/Bars Gasoline Stations Grocery Stores Convenience Stores Other Retail Establishments Car Rental Other Transportation

II. EXECUTIVE SUMMARY

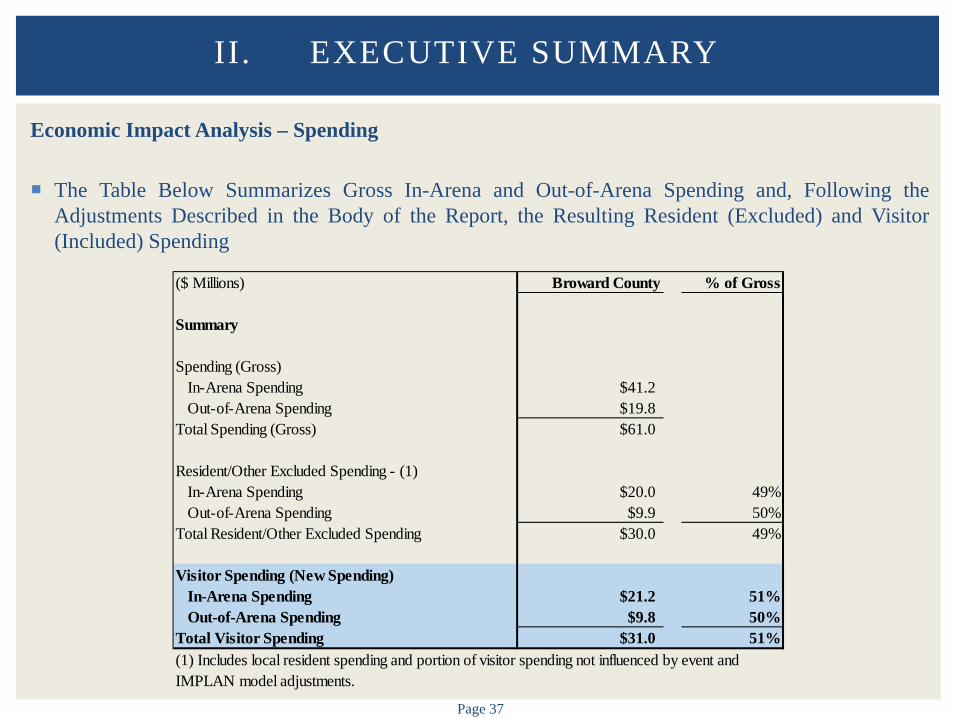

Page 37

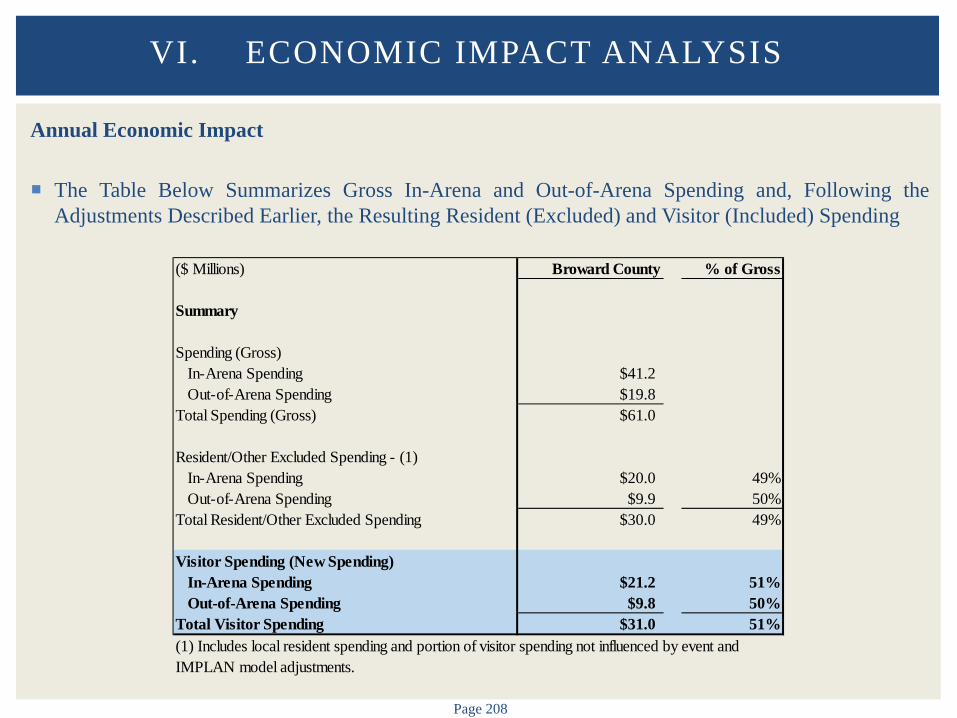

Economic Impact Analysis – Spending The Table Below Summarizes Gross In-Arena and Out-of-Arena Spending and, Following the

Adjustments Described in the Body of the Report, the Resulting Resident (Excluded) and Visitor (Included) Spending

II. EXECUTIVE SUMMARY

($ Millions) Broward County % of Gross

Summary

Spending (Gross)In-Arena Spending $41.2Out-of-Arena Spending $19.8

Total Spending (Gross) $61.0

Resident/Other Excluded Spending - (1)In-Arena Spending $20.0 49%Out-of-Arena Spending $9.9 50%

Total Resident/Other Excluded Spending $30.0 49%

Visitor Spending (New Spending)In-Arena Spending $21.2 51%Out-of-Arena Spending $9.8 50%

Total Visitor Spending $31.0 51%(1) Includes local resident spending and portion of visitor spending not influenced by event and IMPLAN model adjustments.

Page 38

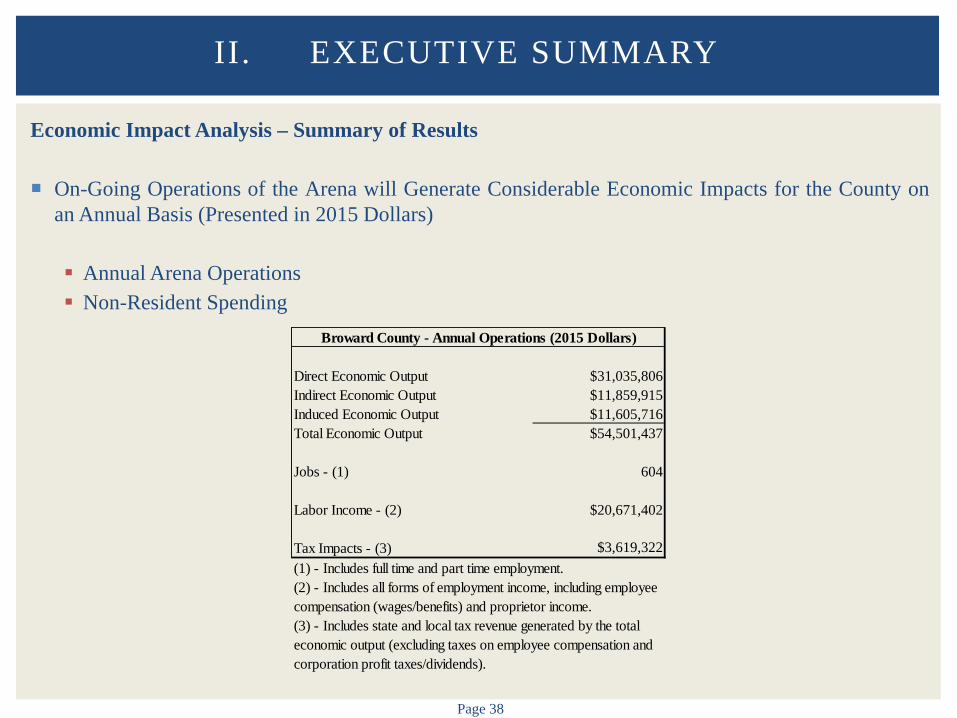

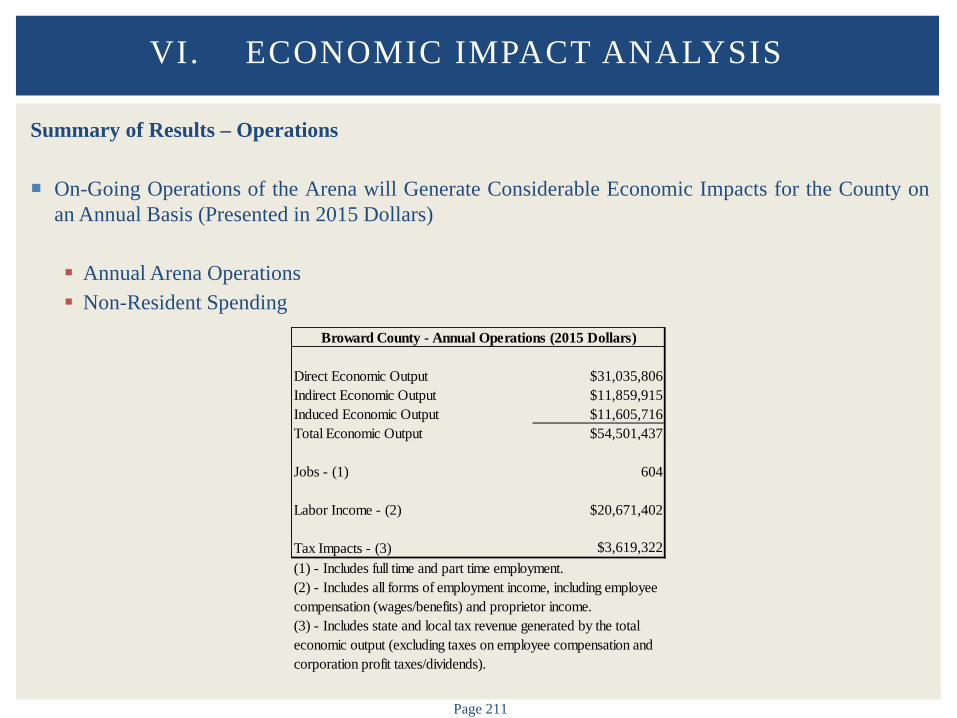

Economic Impact Analysis – Summary of Results

On-Going Operations of the Arena will Generate Considerable Economic Impacts for the County on an Annual Basis (Presented in 2015 Dollars)

Annual Arena Operations Non-Resident Spending

II. EXECUTIVE SUMMARY

Direct Economic Output $31,035,806Indirect Economic Output $11,859,915Induced Economic Output $11,605,716Total Economic Output $54,501,437

Jobs - (1) 604

Labor Income - (2) $20,671,402

Tax Impacts - (3) $3,619,322 (1) - Includes full time and part time employment.(2) - Includes all forms of employment income, including employee compensation (wages/benefits) and proprietor income.(3) - Includes state and local tax revenue generated by the total economic output (excluding taxes on employee compensation and corporation profit taxes/dividends).

Broward County - Annual Operations (2015 Dollars)

Page 39

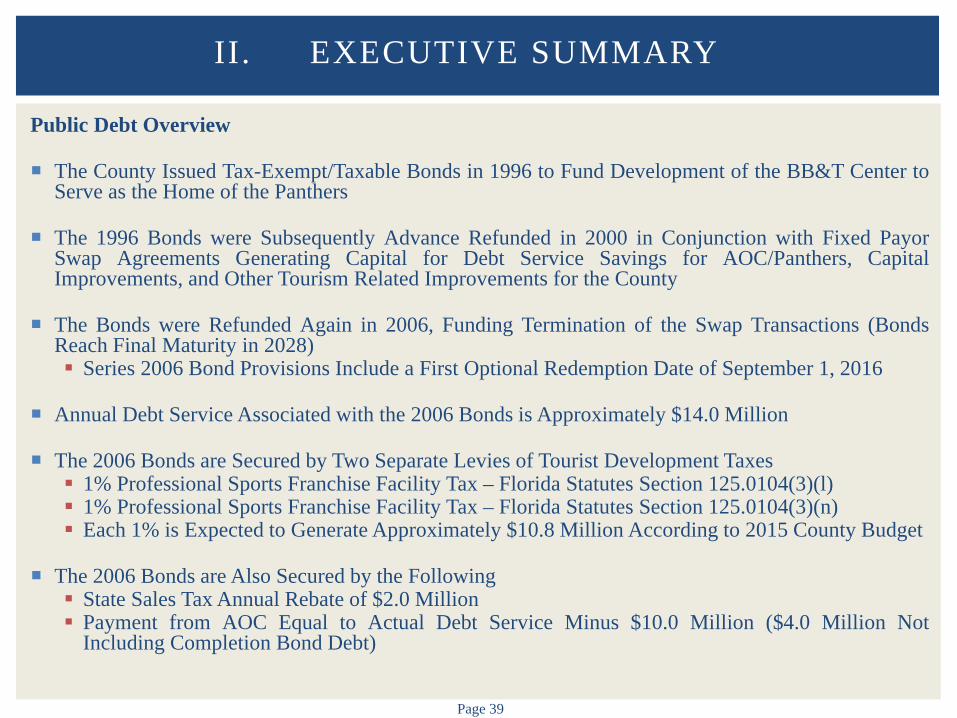

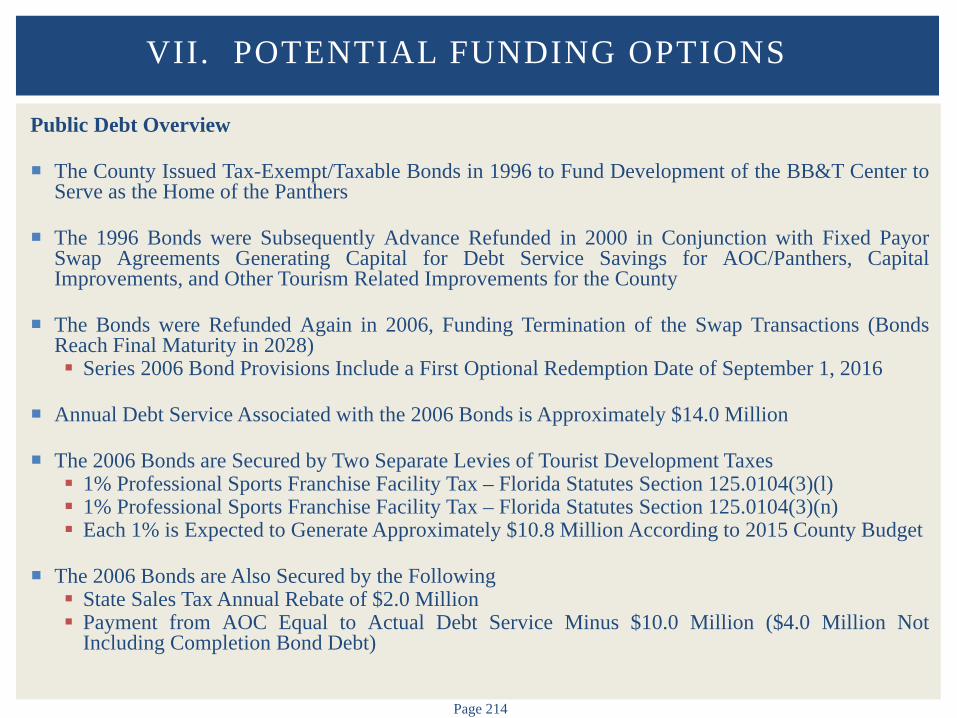

Public Debt Overview The County Issued Tax-Exempt/Taxable Bonds in 1996 to Fund Development of the BB&T Center to

Serve as the Home of the Panthers

The 1996 Bonds were Subsequently Advance Refunded in 2000 in Conjunction with Fixed Payor Swap Agreements Generating Capital for Debt Service Savings for AOC/Panthers, Capital Improvements, and Other Tourism Related Improvements for the County

The Bonds were Refunded Again in 2006, Funding Termination of the Swap Transactions (Bonds Reach Final Maturity in 2028) Series 2006 Bond Provisions Include a First Optional Redemption Date of September 1, 2016

Annual Debt Service Associated with the 2006 Bonds is Approximately $14.0 Million The 2006 Bonds are Secured by Two Separate Levies of Tourist Development Taxes 1% Professional Sports Franchise Facility Tax – Florida Statutes Section 125.0104(3)(l) 1% Professional Sports Franchise Facility Tax – Florida Statutes Section 125.0104(3)(n) Each 1% is Expected to Generate Approximately $10.8 Million According to 2015 County Budget

The 2006 Bonds are Also Secured by the Following State Sales Tax Annual Rebate of $2.0 Million Payment from AOC Equal to Actual Debt Service Minus $10.0 Million ($4.0 Million Not

Including Completion Bond Debt)

II . EXECUTIVE SUMMARY

Page 40

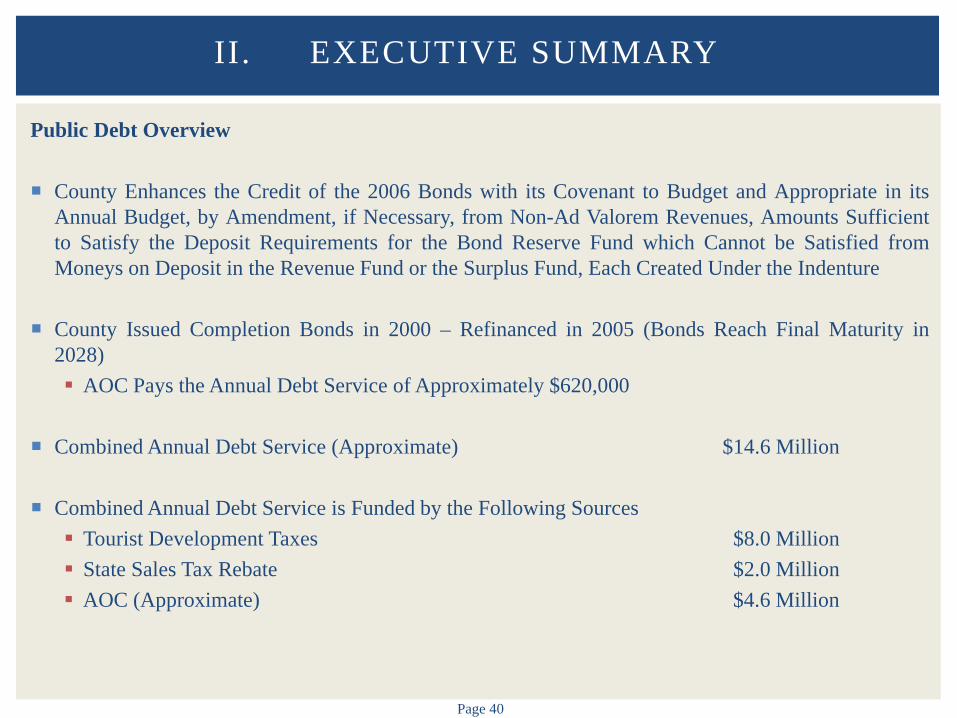

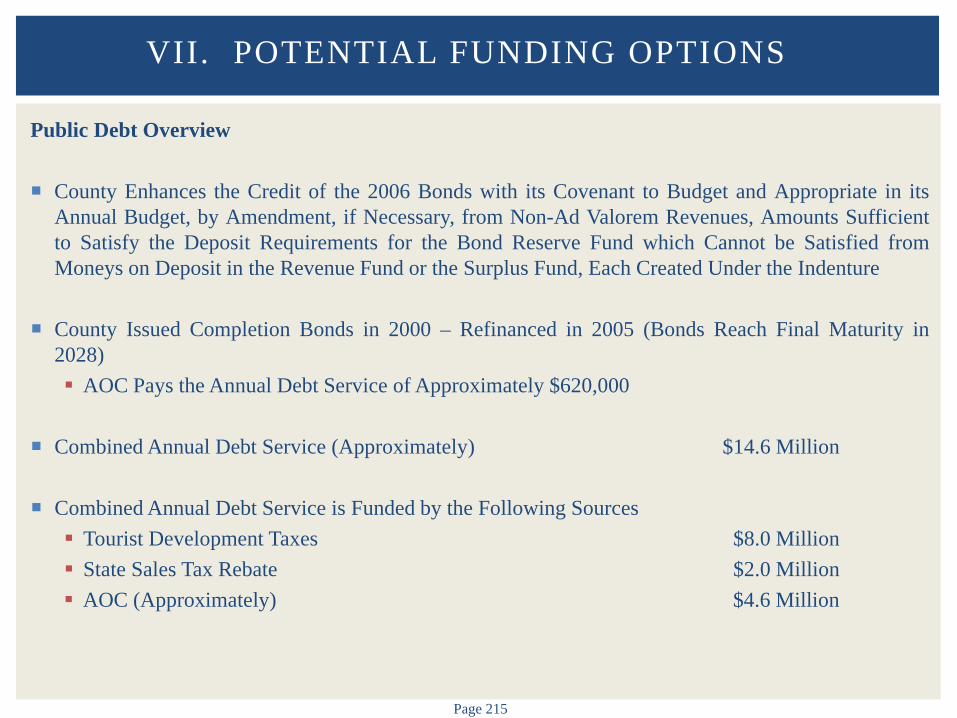

Public Debt Overview County Enhances the Credit of the 2006 Bonds with its Covenant to Budget and Appropriate in its

Annual Budget, by Amendment, if Necessary, from Non-Ad Valorem Revenues, Amounts Sufficient to Satisfy the Deposit Requirements for the Bond Reserve Fund which Cannot be Satisfied from Moneys on Deposit in the Revenue Fund or the Surplus Fund, Each Created Under the Indenture

County Issued Completion Bonds in 2000 – Refinanced in 2005 (Bonds Reach Final Maturity in

2028) AOC Pays the Annual Debt Service of Approximately $620,000

Combined Annual Debt Service (Approximate) $14.6 Million

Combined Annual Debt Service is Funded by the Following Sources Tourist Development Taxes $8.0 Million State Sales Tax Rebate $2.0 Million AOC (Approximate) $4.6 Million

II. EXECUTIVE SUMMARY

Page 41

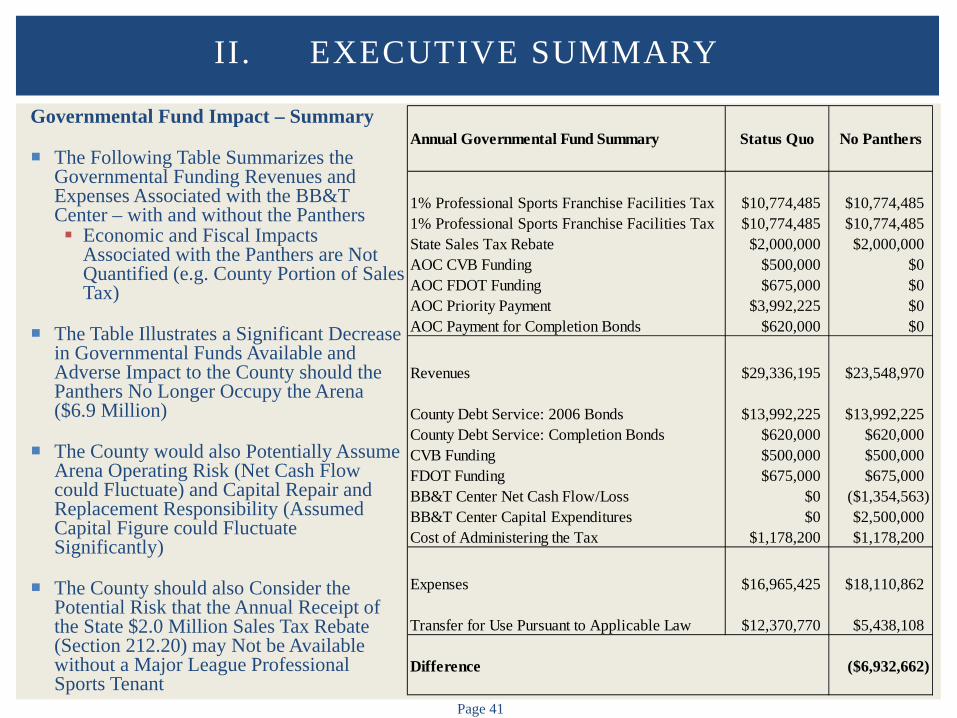

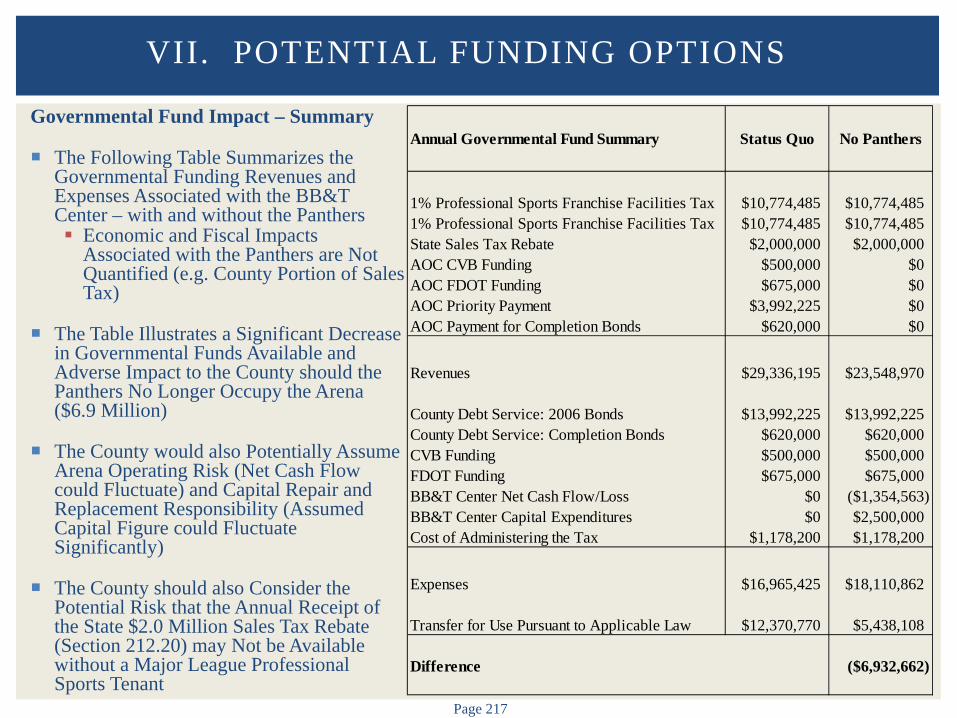

Governmental Fund Impact – Summary

The Following Table Summarizes the Governmental Funding Revenues and Expenses Associated with the BB&T Center – with and without the Panthers Economic and Fiscal Impacts

Associated with the Panthers are Not Quantified (e.g. County Portion of Sales Tax)

The Table Illustrates a Significant Decrease in Governmental Funds Available and Adverse Impact to the County should the Panthers No Longer Occupy the Arena ($6.9 Million)

The County would also Potentially Assume Arena Operating Risk (Net Cash Flow could Fluctuate) and Capital Repair and Replacement Responsibility (Assumed Capital Figure could Fluctuate Significantly)

The County should also Consider the Potential Risk that the Annual Receipt of the State $2.0 Million Sales Tax Rebate (Section 212.20) may Not be Available without a Major League Professional Sports Tenant

II. EXECUTIVE SUMMARY

Annual Governmental Fund Summary Status Quo No Panthers

1% Professional Sports Franchise Facilities Tax $10,774,485 $10,774,4851% Professional Sports Franchise Facilities Tax $10,774,485 $10,774,485State Sales Tax Rebate $2,000,000 $2,000,000AOC CVB Funding $500,000 $0AOC FDOT Funding $675,000 $0AOC Priority Payment $3,992,225 $0AOC Payment for Completion Bonds $620,000 $0

Revenues $29,336,195 $23,548,970

County Debt Service: 2006 Bonds $13,992,225 $13,992,225County Debt Service: Completion Bonds $620,000 $620,000CVB Funding $500,000 $500,000FDOT Funding $675,000 $675,000BB&T Center Net Cash Flow/Loss $0 ($1,354,563)BB&T Center Capital Expenditures $0 $2,500,000Cost of Administering the Tax $1,178,200 $1,178,200

Expenses $16,965,425 $18,110,862

Transfer for Use Pursuant to Applicable Law $12,370,770 $5,438,108

Difference ($6,932,662)

Page 42

Potential Funding Sources

The Additional Programmatic Needs Creates a Significant Impact on the County Budget. While the Professional Sports Franchise Facility Tax Generates Resources that Exceed the Amount Needed by the County for Debt Service, those Resources have been Programmed by the County to Meet Other Critical Tourism Needs. Re-directing the Tax Proceeds to the Arena Potentially Creates a New Need for Existing or Future Programmatic Initiatives/Requirements in Tourism. Option #1 – Reprioritize Tourism Related Programs The County Could Elect to Reprioritize Tourism Related Programs Funded with the Transfer Back to the

General Fund from the Two Cent Tourist Tax Revenue Fund in an Amount Needed to Fund BB&T Center Obligations

Option #2 – Identify New Funding Source

Bond Refunding: Refund Outstanding Callable 2006 Bonds at the Option of the County. Under Market Conditions Annual Savings Would be Approximately $750,000 to $1.0 Million.

High Tourism Impact Tax: The County Levies 5% of the Available 6% Tourist Development Taxes Under

State Law. The High Tourism Impact Tax is the 1% Tourist Development Tax that Remains Available to the County and is Not Currently Levied. This Levy Would Generate Approximately $10.8 Million Annually.

Food and Beverage Tax: Miami-Dade County is Permitted to Levy a 2% Food and Beverage Tax on Hotels

and Motels. No Other County is Authorized to Levy Such a Tax. Consideration Could be Given to Introducing Legislation to Allow Broward and Possibly Other High Tourism Impact Counties [Pursuant to Section 125.0104(3)(m)2 – Monroe, Orange, Osceola, and Walton] to Levy a Similar Tax.

II. EXECUTIVE SUMMARY

Page 43

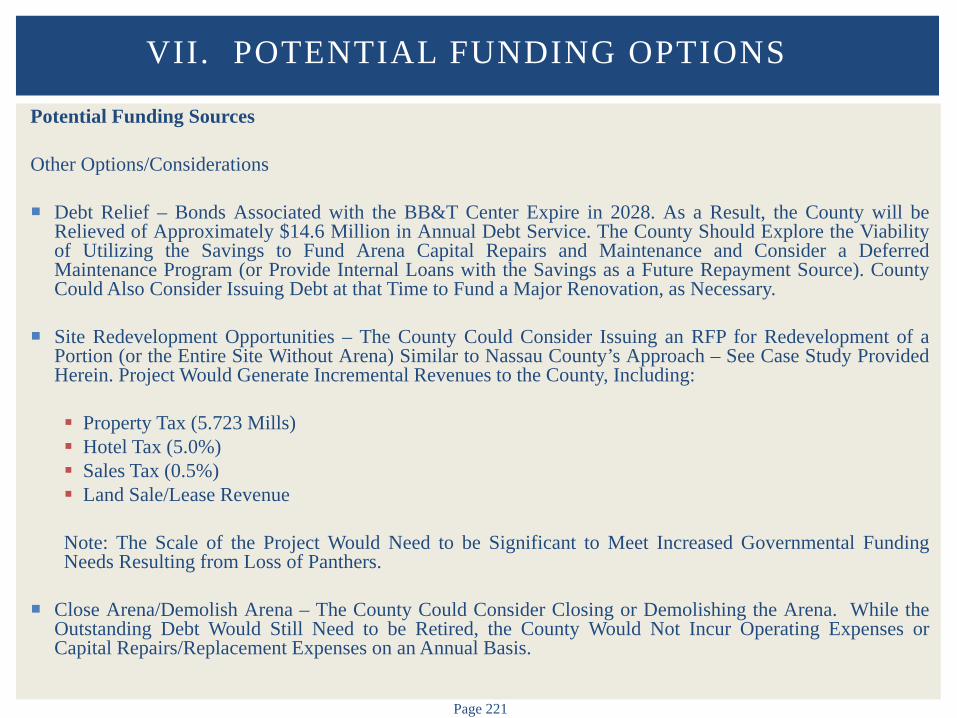

Potential Funding Sources

Other Options/Considerations Insurance Savings – The BB&T Center Insurance Expense is High Relative to the Comparable Arenas

We Evaluated. While We have Considered the Potential Benefit that the County, as an Owner/Operator, May Be Able to Realize by Including the Arena in its Broader Insurance Program, We Understand that the County has Previously Explored Such an Arrangement and has Indicated that the Insurance Expense Could Potentially be Higher Under Such an Arrangement.

Debt Relief – Bonds Associated with the BB&T Center Expire in 2028. As a Result, the County will be Relieved of Approximately $14.6 Million in Annual Debt Service. The County Should Explore the Viability of Utilizing the Savings to Fund Arena Capital Repairs and Maintenance and Consider a Deferred Maintenance Program (or Provide Internal Loans with the Savings as a Future Repayment Source). County Could Also Consider Issuing Debt at that Time to Fund a Major Renovation, as Necessary.

Site Redevelopment Opportunities – The County Could Consider Issuing an RFP for Redevelopment of a Portion (or the Entire Site Without Arena) Similar to Nassau County’s Approach – See Case Study Provided Herein. Project Would Generate Incremental Revenues to the County, Including: Property Tax (5.723 Mills) Hotel Tax (5.0%) Sales Tax (0.5%) Land Sale/Lease Revenue

II. EXECUTIVE SUMMARY

Page 44

Potential Funding Sources

Other Options/Considerations Close Arena/Demolish Arena – The County Could Consider Closing or Demolishing the Arena.

While the Outstanding Debt Would Still Need to be Retired, the County Would Not Incur Operating Expenses or Capital Repairs/Replacement Expenses on an Annual Basis.

We have Considered, But have Not Focused on, Funding Sources that have Been Utilized in Other Parts of the Country Because the Sources are Not Available Under Current Law or Do Not Generate Sufficient Funds as a Stand-Alone Source (e.g. Admissions Tax/Car Rental Tax/Parking Tax/Etc.)

II. EXECUTIVE SUMMARY

Page 45

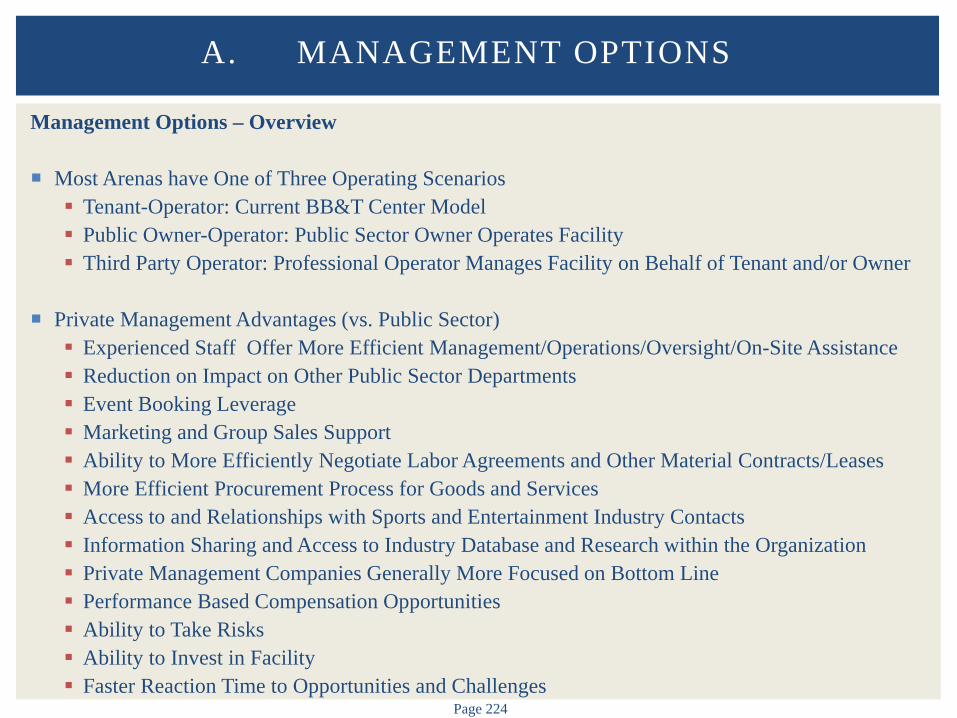

Other Considerations: Management Options – Overview Most Arenas Operate Under One of Three Scenarios Tenant-Operator: Current BB&T Center Model Public Owner-Operator: Public Sector Owner Operates Facility Third Party Operator: Professional Operator Manages Facility on Behalf of Tenant and/or Owner

Private Management Advantages (vs. Public Sector) Experienced Staff Offer More Efficient Management/Operations/Oversight/On-Site Assistance Reduction on Impact on Other Public Sector Departments Event Booking Leverage Marketing and Group Sales Support Ability to More Efficiently Negotiate Labor Agreements and Other Material Contracts/Leases More Efficient Procurement Process for Goods and Services Access to and Relationships with Sports and Entertainment Industry Contacts Information Sharing and Access to Industry Database and Research within the Organization Private Management Companies Generally More Focused on Bottom Line Performance Based Compensation Opportunities Ability to Take Risks Ability to Invest in Facility Faster Reaction Time to Opportunities and Challenges

II. EXECUTIVE SUMMARY

Page 46

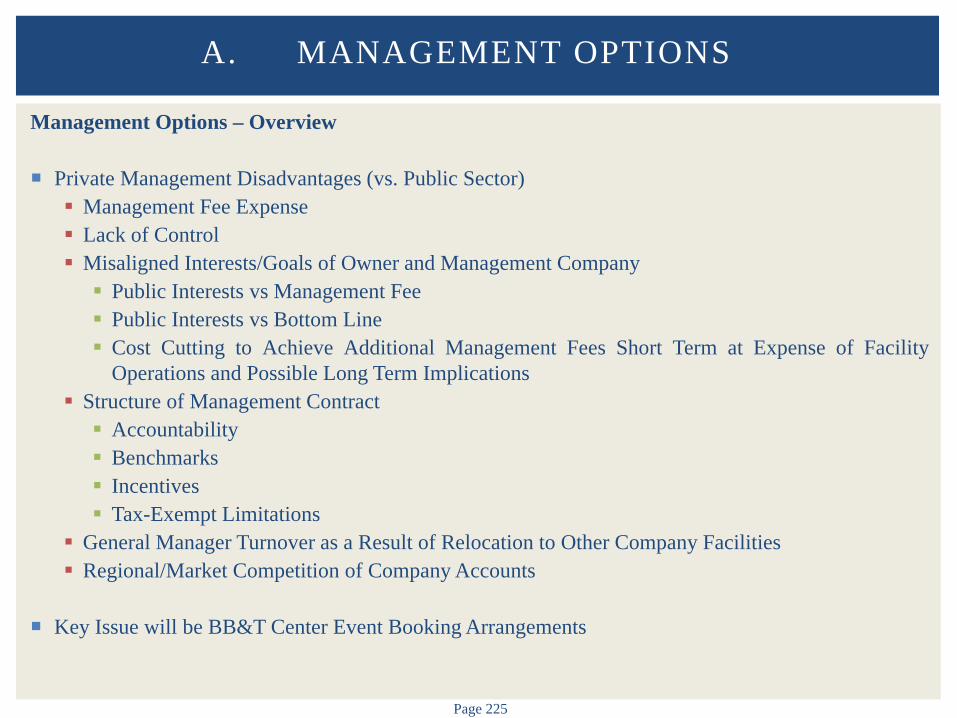

Other Considerations: Management Options – Overview Private Management Disadvantages (vs. Public Sector) Management Fee Expense Lack of Control Misaligned Interests/Goals of Owner and Management Company Public Interests vs. Management Fee Cost Cutting to Achieve Additional Management Fees Short Term at Expense of Facility

Operations and Possible Long Term Implications Public Interests vs. Bottom Line

Structure of Management Contract Accountability Benchmarks Incentives Tax-Exempt Limitations

General Manager Turnover as a Result of Relocation to Other Company Facilities Regional/Market Competition of Company Accounts

Key Issue will be BB&T Center Event Booking Arrangements

II. EXECUTIVE SUMMARY

Page 47

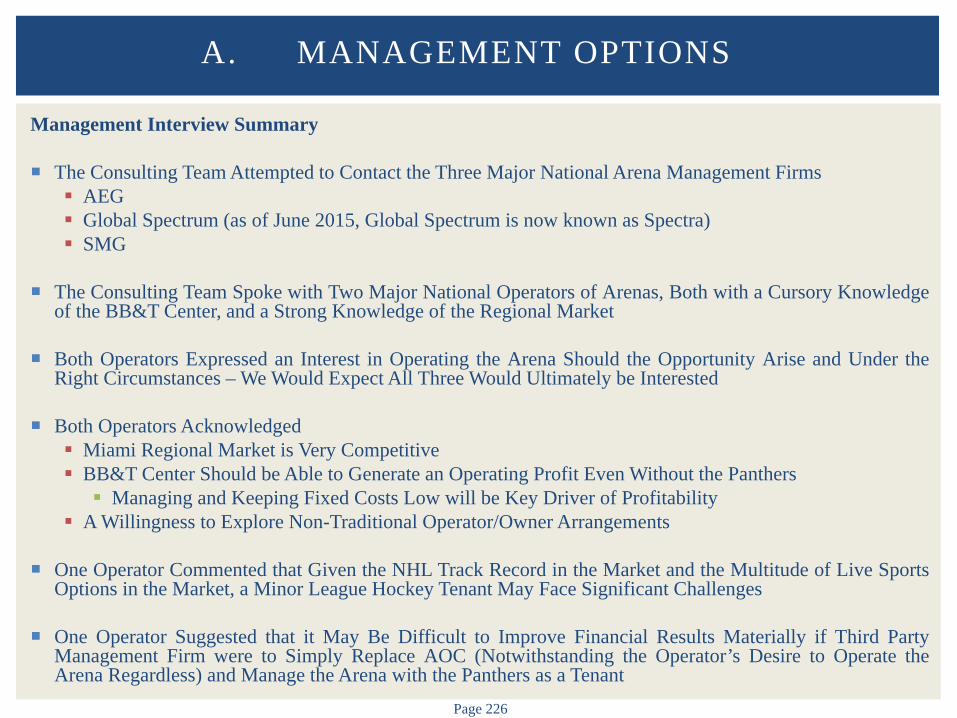

Other Considerations: Management Options – Interview Summary The Consulting Team Attempted to Contact the Three Major National Arena Management Firms AEG Global Spectrum (as of June 2015, Global Spectrum is now known as Spectra) SMG

The Consulting Team Spoke with Two Major National Operators of Arenas, Both with a Cursory Knowledge

of the BB&T Center, and a Strong Knowledge of the Regional Market

Both Operators Expressed an Interest in Operating the Arena Should the Opportunity Arise and Under the Right Circumstances – We Would Expect All Three Would Ultimately be Interested

Both Operators Acknowledged Miami Regional Market is Very Competitive BB&T Center Should be Able to Generate an Operating Profit Even Without the Panthers Managing and Keeping Fixed Costs Low will be Key Driver of Profitability

A Willingness to Explore Non-Traditional Operator/Owner Arrangements

One Operator Commented that Given the NHL Track Record in the Market and the Multitude of Live Sports Options in the Market, a Minor League Hockey Tenant May Face Significant Challenges

One Operator Suggested that it May Be Difficult to Improve Financial Results Materially if Third Party Management Firm were to Simply Replace AOC and Manage the Arena with the Panthers as a Tenant (Notwithstanding the Operator’s Desire to Operate the Arena Regardless)

II. EXECUTIVE SUMMARY

Page 48

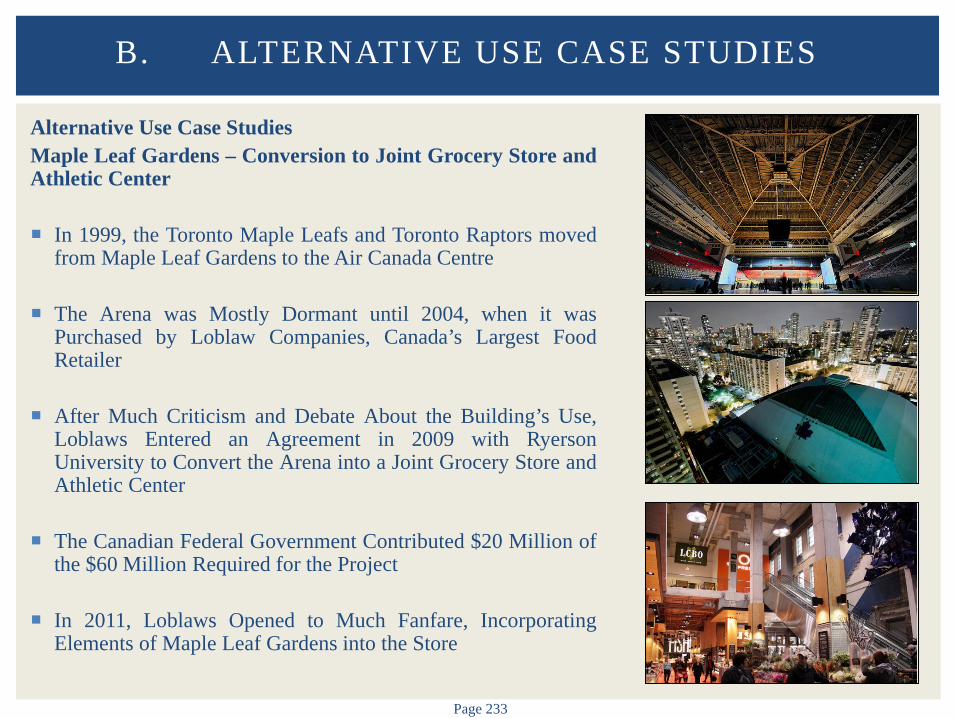

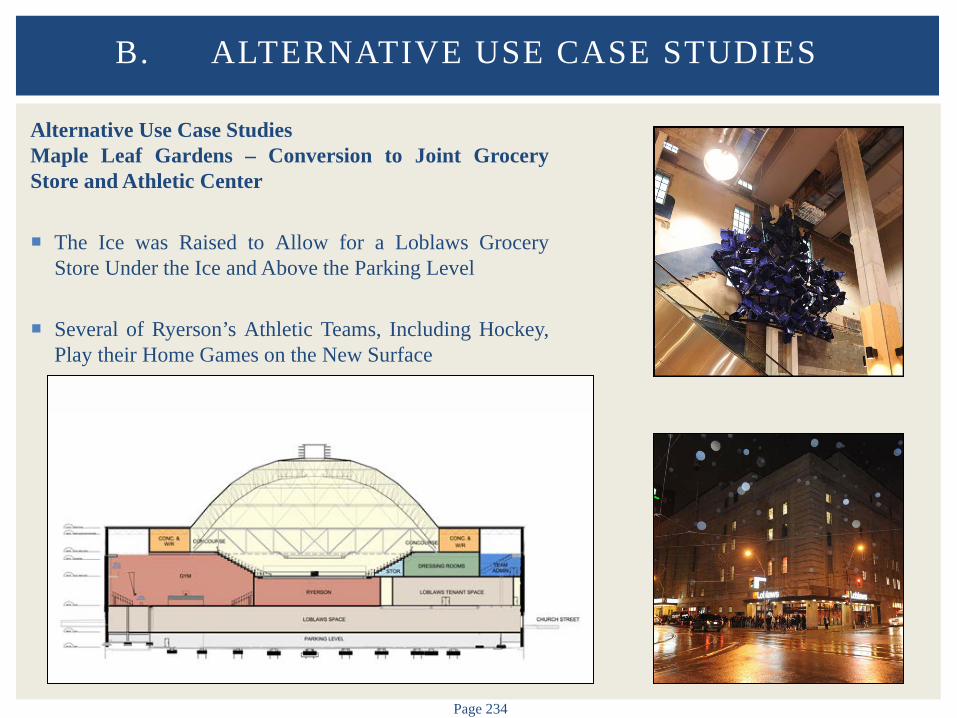

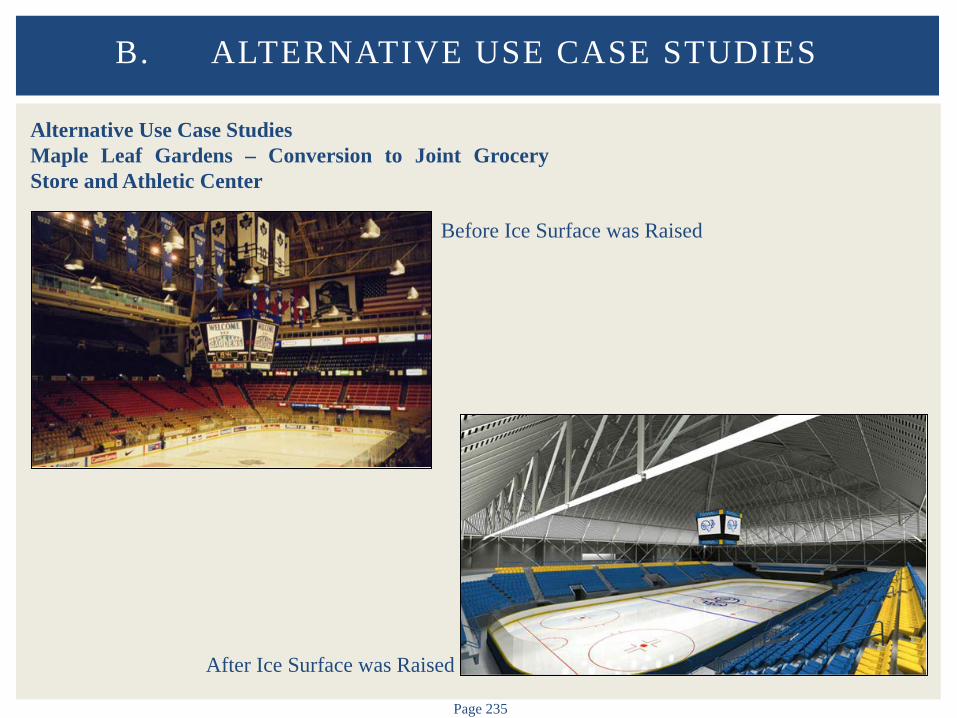

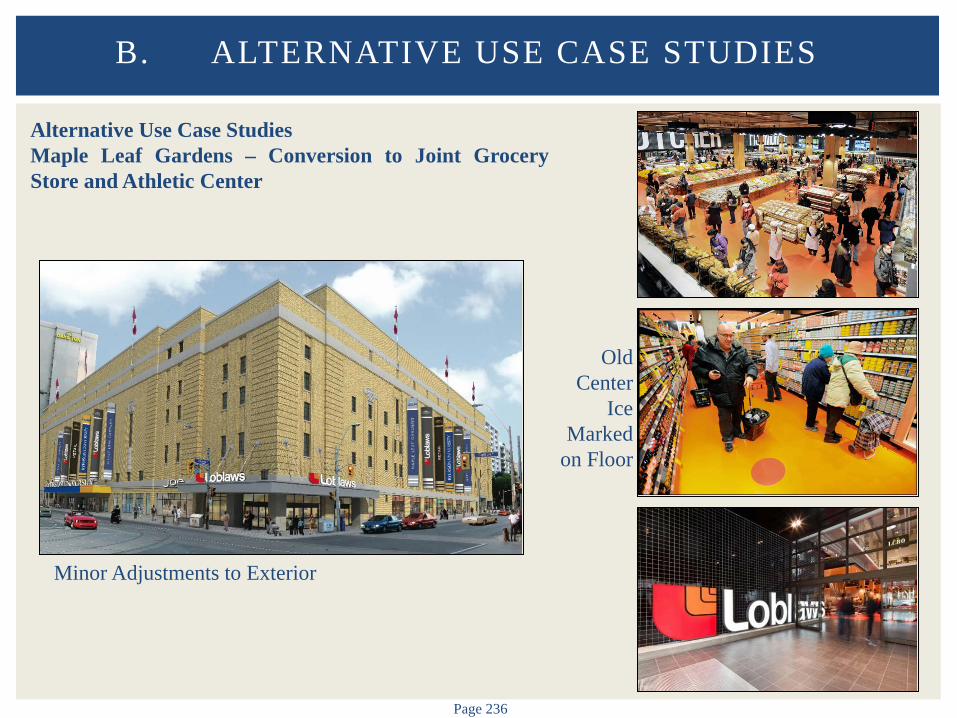

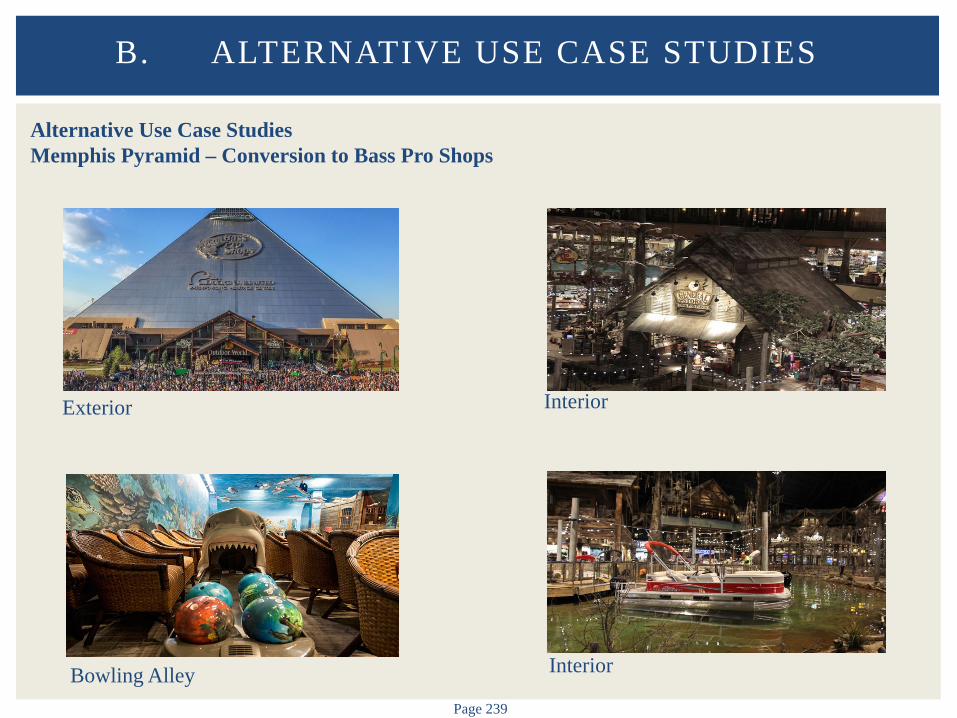

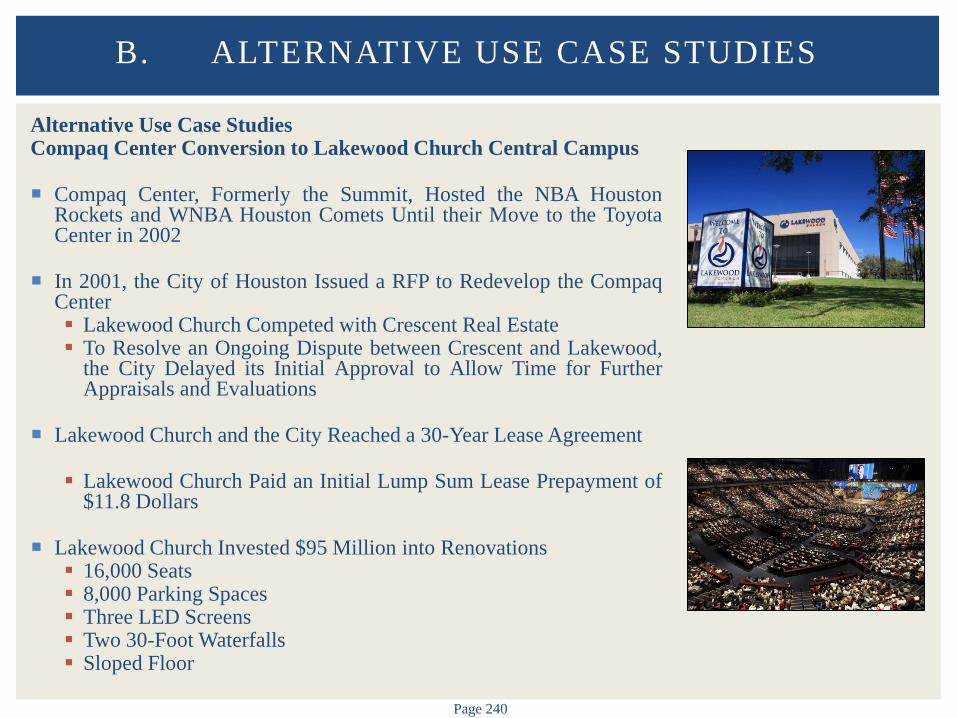

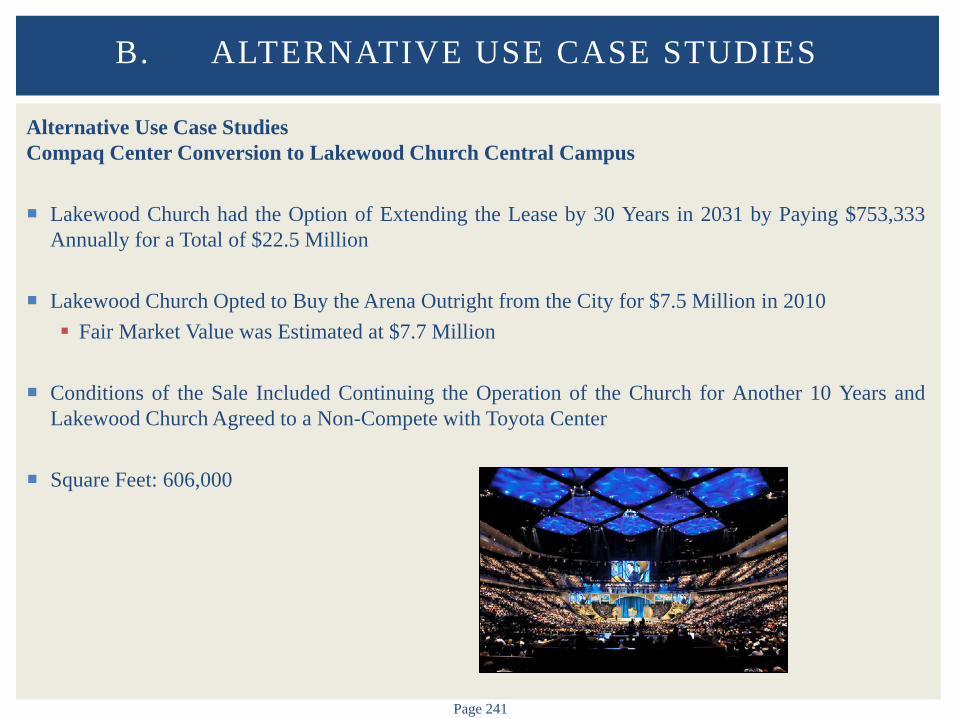

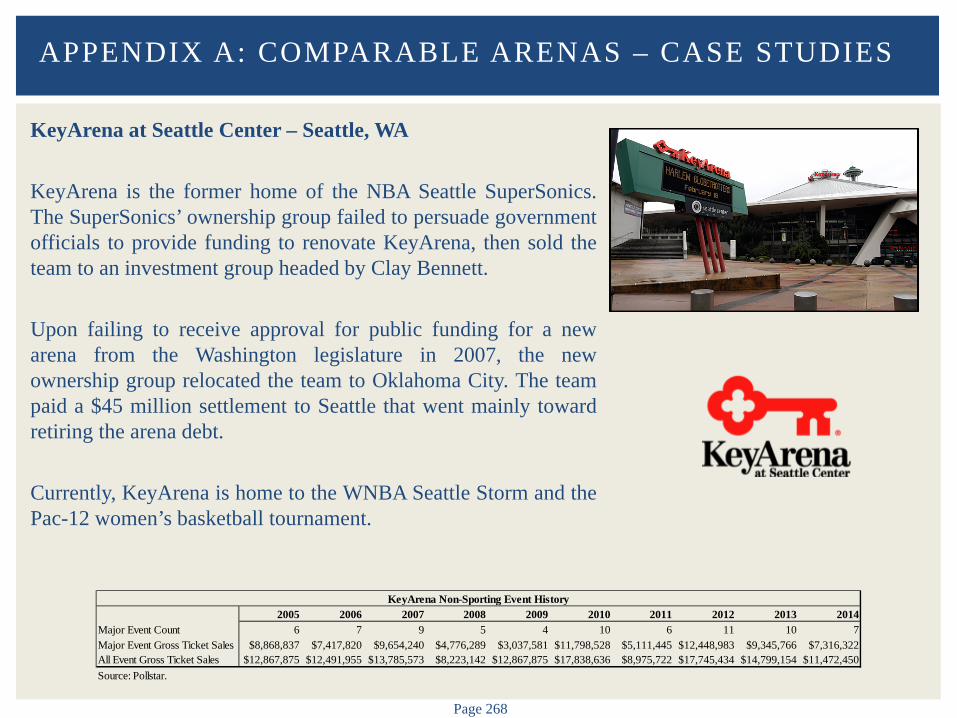

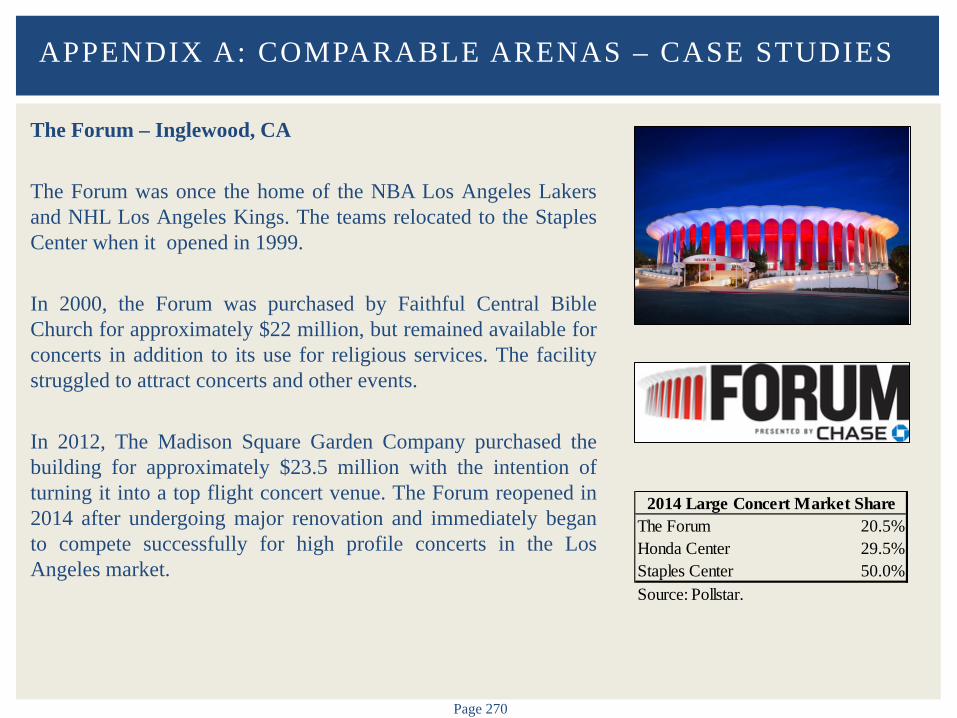

Other Considerations: Alternative Use Case Studies – Overview Several Arenas that Served as Home of an NHL/NBA Team have been Repurposed – Not Common

Retail Focus (Proximity to the Sawgrass Retail Center Provides a Potential Opportunity) Limited Examples of Similar Conversions Maple Leaf Gardens (Toronto) Memphis Pyramid (Memphis)

Megachurches There Have Been a Limited Number of Instances of Arenas Repurposed into "Megachurches" Owned

and Operated by Private, Non-Profit Religious Organizations Compaq Center (Houston) The Forum (Los Angeles – Subsequently Repurposed)

Repurposed Facilities Have Generally Been Older Arenas, with Simple Seating Bowls and Significantly

Lower Square Footages than BB&T Center

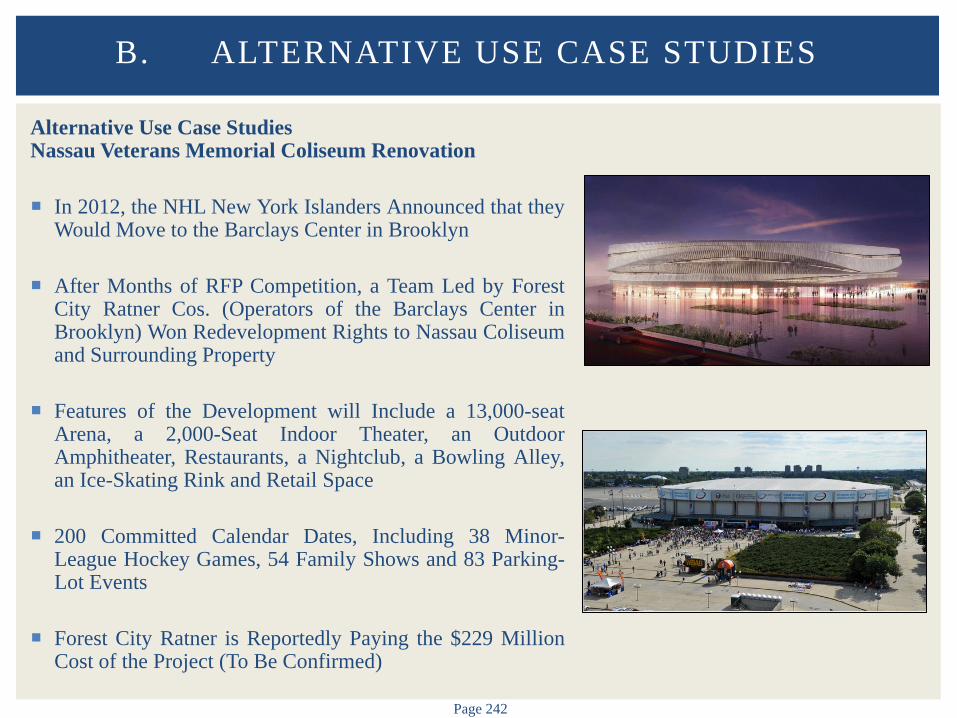

Master Planned Site Redevelopment Nassau Coliseum (Potential Opportunity for BB&T Center Given Competitive Nature of Market) Nassau County Issued an RFP for Redevelopment of Coliseum and Site Several Responses Given Competitive Nature of Market Forest City Ratner (Barclays Center) Madison Square Garden Others

II. EXECUTIVE SUMMARY

Page 49

Other Considerations: Public Support Case Studies Numerous Public Entities have Provided Concessions/Additional Subsidies to Professional Sports

Teams that have Clearly Demonstrated that they are Struggling Financially

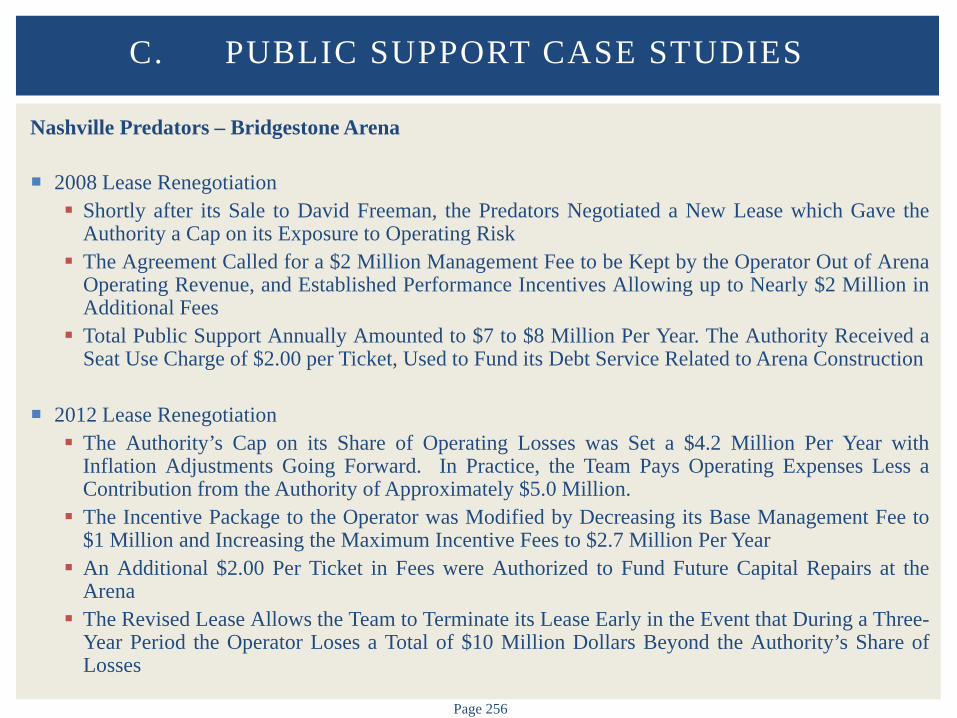

The Consulting Team Provided Several Case Studies Herein Outlining Public Support NHL Arizona Coyotes Columbus Blue Jackets Nashville Predators

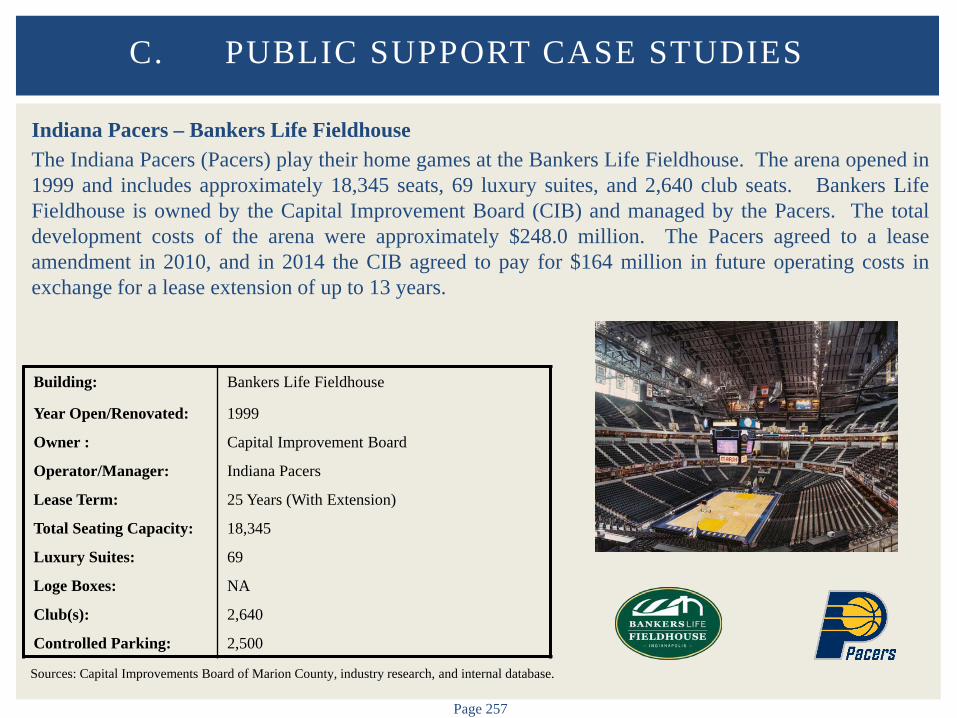

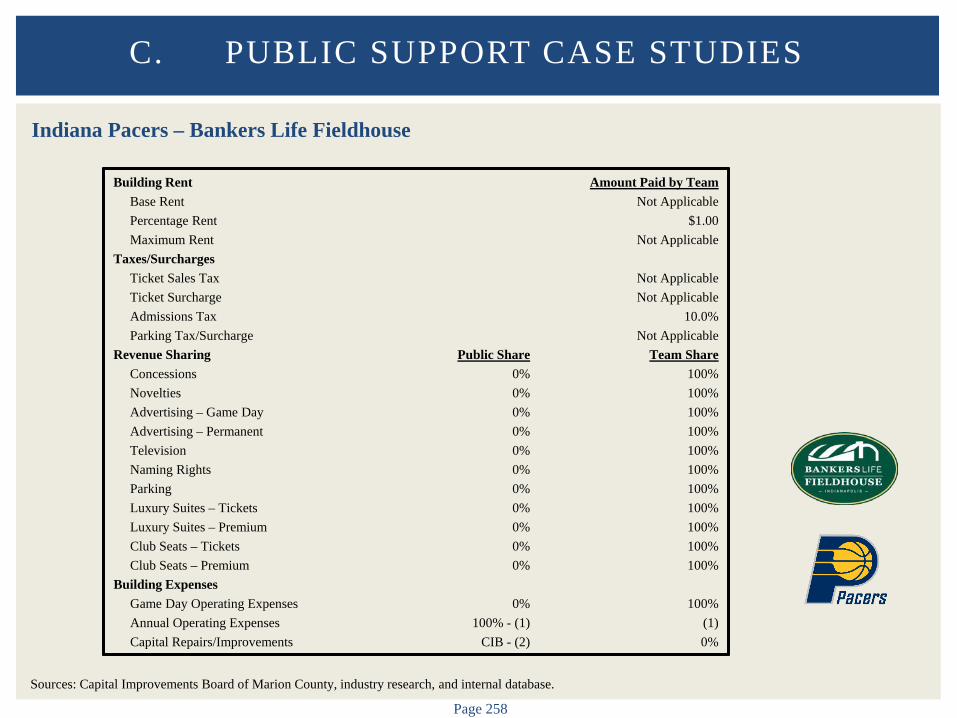

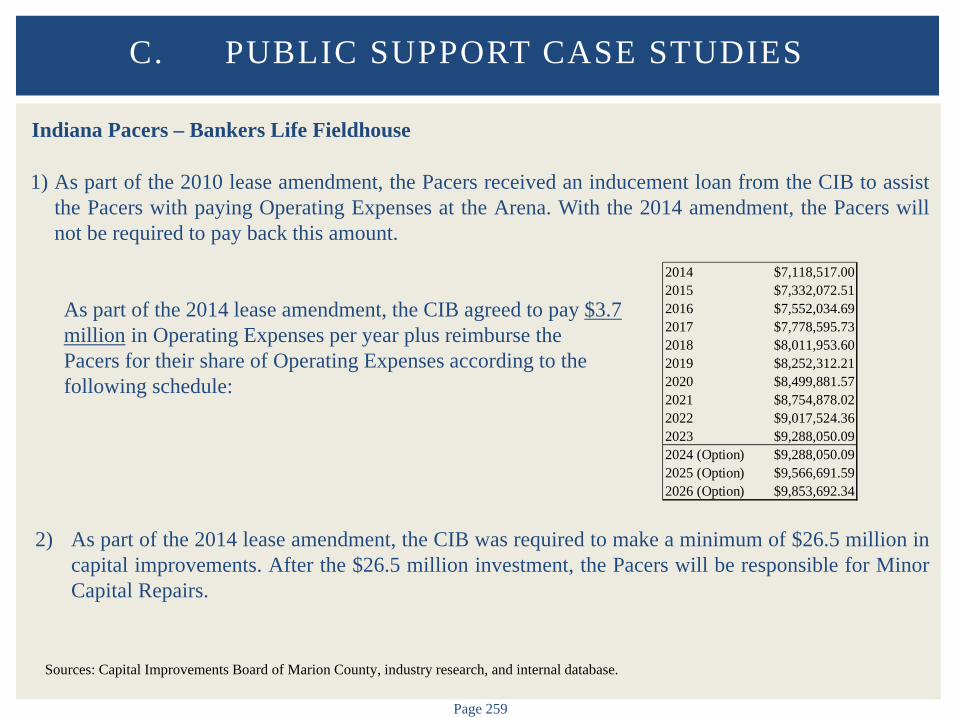

NBA Indiana Pacers Miami Heat

Case Studies from Other Jurisdictions Illustrate a Wide Range of Approaches to Offering Public

Support for Existing Teams/Facilities

County Must Consider the Potential Operational and Financial Consequences Relative to the Opportunities and Challenges of the Various Alternative Options Outlined Herein

II. EXECUTIVE SUMMARY

III. BB&T CENTER OVERVIEW

Page 51

Overview

The BB&T Center is Owned by the County and Operated by Arena Operating Company, Ltd. (AOC), an Affiliate of the Panthers, and Subsidiary of Sunrise Sports & Entertainment (SS&E)

Arena Opened in 1998 at a Total Cost of Approximately $221.1 Million (Including Cost Overruns and Financing Costs)

Arena is Located Adjacent to the Sawgrass Mills Mall in a Developed Commercial and Residential Area

Arena was Designed for Professional Hockey, Sports, Entertainment, and Other Community Events

BB&T Center Characteristics

872,000 Square Feet 20,763 Seats (Maximum) / 19,250 (Hockey) 72 Suites & Loge Boxes / Up to 3,121 Club Seats 7,200 Parking Spaces

Since 1998, Arena has had Several Different Names (National Car Rental Center, Office Depot

Center, BankAtlantic Center)

III. BB&T CENTER OVERVIEW

Page 52

Summary of Major Agreements

The Consulting Team Reviewed Key Agreements to Understand Contractual Relationships Associated with the Operations of the Arena Operating Agreement License Agreement

Summaries Provided Herein – Please Refer to Actual Agreements for Details

The Consulting Team also Review the Key Agreements Below – However, We have Not Included

Summaries in this Report Due to Confidentiality and Trade Secret Issues

Naming Rights Agreement Concessions Agreement Live Nation Agreement Ticketmaster Agreement Premium Seating Summaries

III. BB&T CENTER OVERVIEW

Page 53

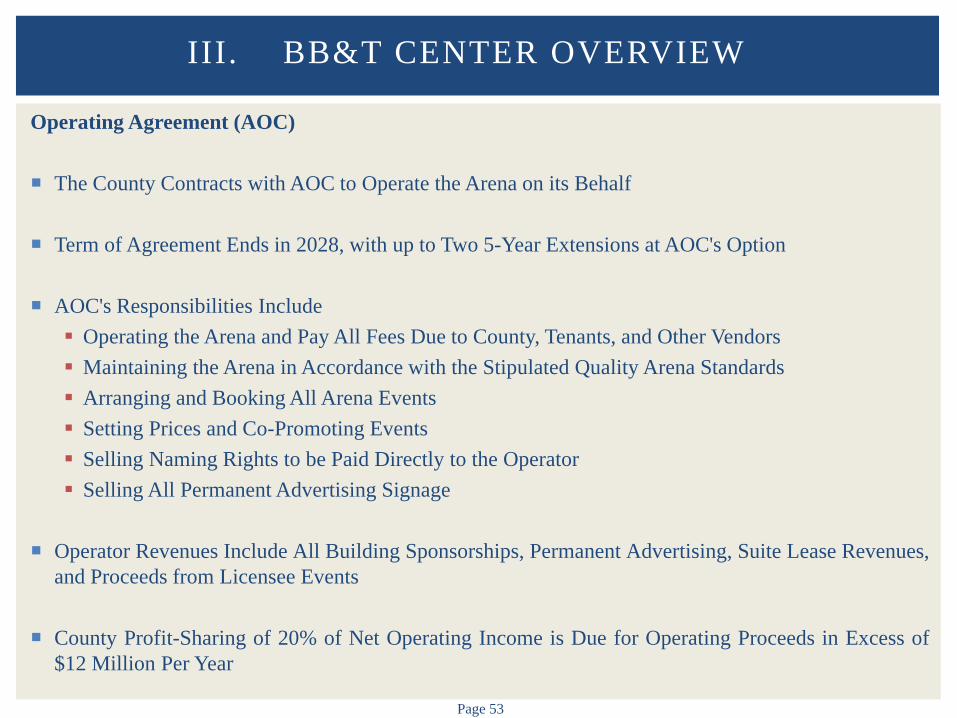

Operating Agreement (AOC)

The County Contracts with AOC to Operate the Arena on its Behalf

Term of Agreement Ends in 2028, with up to Two 5-Year Extensions at AOC's Option

AOC's Responsibilities Include Operating the Arena and Pay All Fees Due to County, Tenants, and Other Vendors Maintaining the Arena in Accordance with the Stipulated Quality Arena Standards Arranging and Booking All Arena Events Setting Prices and Co-Promoting Events Selling Naming Rights to be Paid Directly to the Operator Selling All Permanent Advertising Signage

Operator Revenues Include All Building Sponsorships, Permanent Advertising, Suite Lease Revenues,

and Proceeds from Licensee Events

County Profit-Sharing of 20% of Net Operating Income is Due for Operating Proceeds in Excess of $12 Million Per Year

III. BB&T CENTER OVERVIEW

Page 54

Operating Agreement (AOC) The 8th Amendment Added a Requirement of the Operator to Make an Annual $500,000 Contribution

to a Capital Expenditure Reserve Commencing in July 2013

Up to 50% of Which May Be Deducted from County Profit-Sharing, as Available The Consulting Team has Not been able to Confirm Whether Contributions have been Made

Operator May Add a Seat Use Charge to Tickets in Order to Finance Additions and Capital Repairs

and Offset its FDOT Obligation

Operator Events of Default Include

Financial Obligation Breaches Not Cured Within 30 Days Other Obligations Not Cured or Beginning to be Cured Within 30 Days

County Right to Terminate Operator Begins on 15th Day of Operator Default

If County and Operator Disagree on Replacement Operator, AOC Continues to Operate in the Interim

III. BB&T CENTER OVERVIEW

Page 55

License Agreement (Panthers)

Tri-Party Agreement Among AOC, County, and Florida Panthers Hockey Club

Term of Agreement is 30 Years from Opening (1998), with Up to Four 5-Year Extensions at the Team's Option – Initial Agreement Expires in 2028

Team Pays Base Rent to Operator of $7,500 per Game Incentive Rent, Supplemental Rent, and Inclusion of Pass-Through Expenses Can Increase Rent

Up to a Maximum of 5% of Hockey Ticket Receipts for a Year

Team Pays for Hockey Event Staffing

Through the Operator, Team Guarantees the County Preferred Revenue Allocation (CPRA) Equal to Annual Debt Service Minus $10 Million

Team Covenants to Continuously Play in Arena throughout the Term so Long as the Arena Remains in

Playable Condition Specific Performance Provisions are Included for this Covenant

III. BB&T CENTER OVERVIEW

Page 56

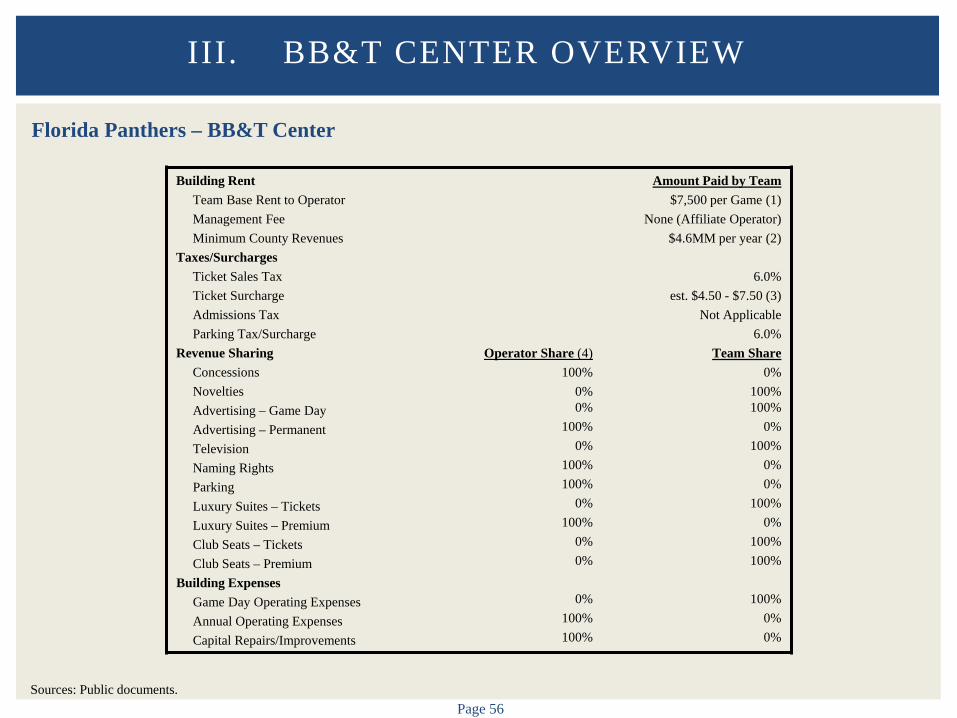

Florida Panthers – BB&T Center

III. BB&T CENTER OVERVIEW

Building Rent Team Base Rent to Operator Management Fee Minimum County Revenues Taxes/Surcharges Ticket Sales Tax Ticket Surcharge Admissions Tax Parking Tax/Surcharge Revenue Sharing Concessions Novelties Advertising – Game Day Advertising – Permanent Television Naming Rights Parking Luxury Suites – Tickets Luxury Suites – Premium Club Seats – Tickets Club Seats – Premium Building Expenses Game Day Operating Expenses Annual Operating Expenses Capital Repairs/Improvements

Operator Share (4) 100%

0% 0%

100% 0%

100% 100%

0% 100%

0% 0%

0%

100% 100%

Amount Paid by Team $7,500 per Game (1)

None (Affiliate Operator) $4.6MM per year (2)

6.0%

est. $4.50 - $7.50 (3) Not Applicable

6.0% Team Share

0% 100% 100%

0% 100%

0% 0%

100% 0%

100% 100%

100%

0% 0%

Sources: Public documents.

Page 57

Florida Panthers – BB&T Center

1) In addition to Base Rent of $7,500 per Game, the License Agreement calls for supplemental rent up to a maximum of 5% of Hockey ticket receipts for a given year.

2) County is entitled to CPRA equal to the Arena’s debt service minus $10 million. This amount has averaged $4.6 million in recent years and is forecast to stay at that level until 2026. Forecast CPRA drops slightly in final two years of Base Term of License Agreement. The Operator is responsible for these payments, with the Team currently providing a guarantee on the full amount of the CPRA annually. It is worth noting that refunding the outstanding bonds could reduce the CPRA required under favorable market conditions.

3) The Operating Agreement permits the Arena Operator to levy a Seat Use Charge on events to fund additions and capital repairs. Various additional ticket surcharges comprise the estimated range are currently charged by the Operator/Team, including Facility Fees, Public Safety Fees and Walk-up surcharges.

4) The Operating Agreement includes revenue-sharing provisions, which entitle the County to 20% of Net Operating Income reported by the Operator in excess of $12 million per year. A recent amendment requires the Operator to annually contribute $500,000 to a Capital Expenditure Reserve commencing in July 2013, with 50% of that deductible from any County profit-sharing.

III. BB&T CENTER OVERVIEW

Sources: Public documents.

Page 58

Events / Attendance

The Consulting Team Reviewed Historical Operating Data (Events/Attendance) for the Arena as Provided by AOC and Supplemented by Pollstar Data

The Consulting Team Also Evaluated Historical Event Settlement Sheet Statements as Provided by AOC to Evaluate Additional Detail Settlement Data was Inconsistent and Incomplete – The Consulting Team has Made Adjustments

to Utilize Data

Event and Attendance Information is Provided for Illustrative Purposes Only – Information has Not been Audited by the Consulting Team or Further Verified

Reliability of Historical Event and Attendance Data is of Concern – Certain Discrepancies and Errors in Reporting/Calculations/Actual Results

Comprehensive Attendance Data Not Provided by AOC

III. BB&T CENTER OVERVIEW

Page 59

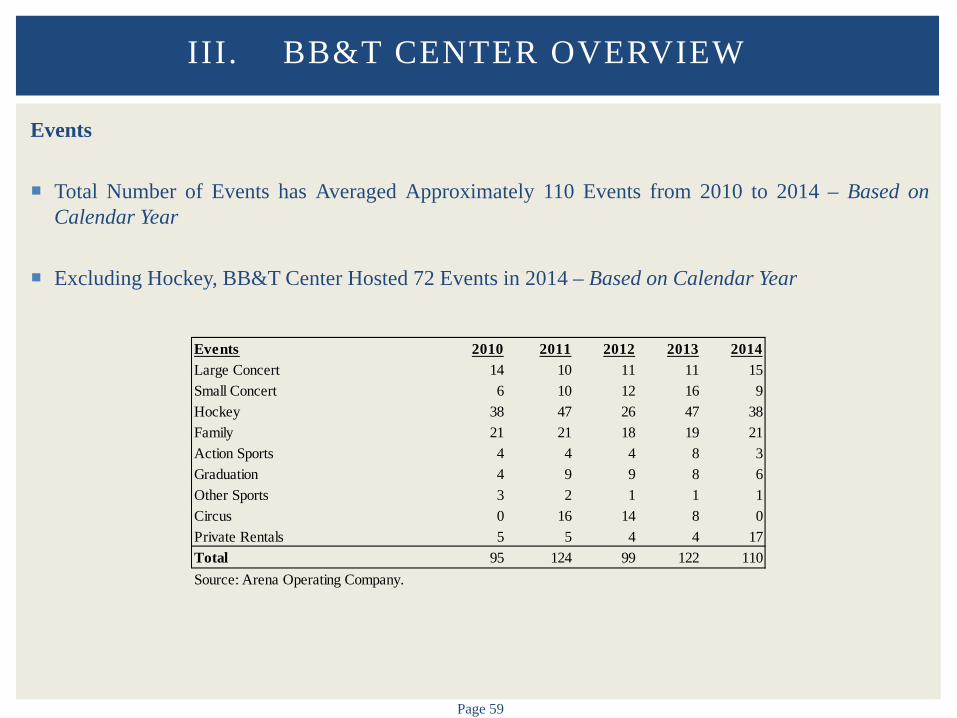

Events

Total Number of Events has Averaged Approximately 110 Events from 2010 to 2014 – Based on Calendar Year

Excluding Hockey, BB&T Center Hosted 72 Events in 2014 – Based on Calendar Year

III. BB&T CENTER OVERVIEW

Events 2010 2011 2012 2013 2014Large Concert 14 10 11 11 15Small Concert 6 10 12 16 9Hockey 38 47 26 47 38Family 21 21 18 19 21Action Sports 4 4 4 8 3Graduation 4 9 9 8 6Other Sports 3 2 1 1 1Circus 0 16 14 8 0Private Rentals 5 5 4 4 17Total 95 124 99 122 110Source: Arena Operating Company.

Page 60

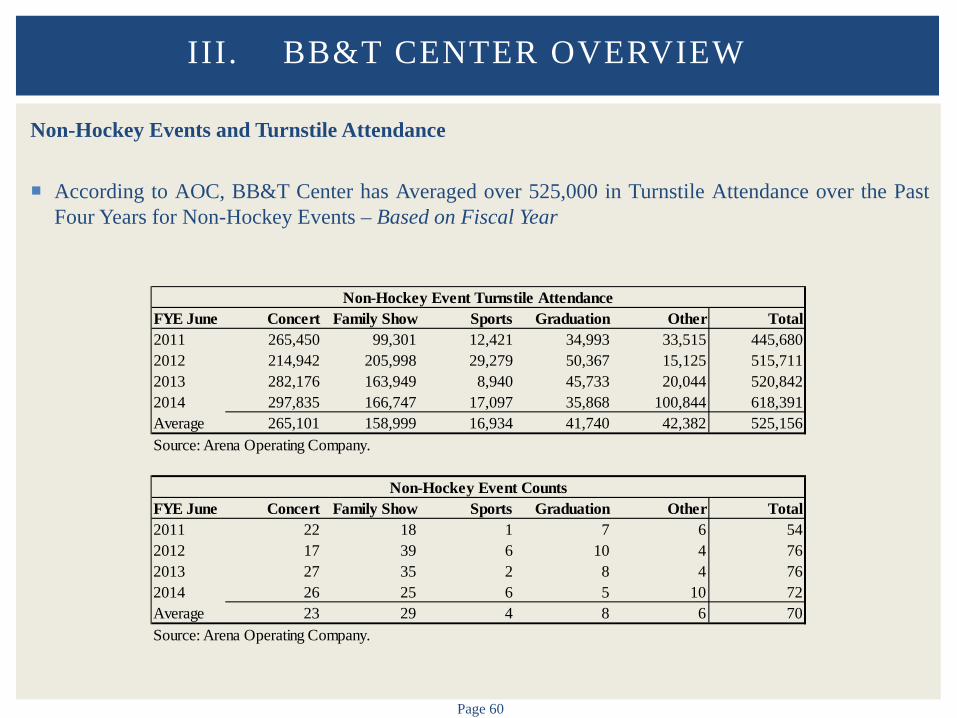

Non-Hockey Events and Turnstile Attendance According to AOC, BB&T Center has Averaged over 525,000 in Turnstile Attendance over the Past

Four Years for Non-Hockey Events – Based on Fiscal Year

III. BB&T CENTER OVERVIEW

FYE June Concert Family Show Sports Graduation Other Total2011 265,450 99,301 12,421 34,993 33,515 445,6802012 214,942 205,998 29,279 50,367 15,125 515,7112013 282,176 163,949 8,940 45,733 20,044 520,8422014 297,835 166,747 17,097 35,868 100,844 618,391Average 265,101 158,999 16,934 41,740 42,382 525,156Source: Arena Operating Company.

FYE June Concert Family Show Sports Graduation Other Total2011 22 18 1 7 6 542012 17 39 6 10 4 762013 27 35 2 8 4 762014 26 25 6 5 10 72Average 23 29 4 8 6 70Source: Arena Operating Company.

Non-Hockey Event Counts

Non-Hockey Event Turnstile Attendance

Page 61

Historical Performance

The Consulting Team has Reviewed Historical Audited Financial Statements for Arena Operating Company, Ltd. from FY 2010 to FY 2014 [FY 2013 Reflects NHL Lockout-Shortened Season]

The Consulting Team has Not Made Adjustments to Historical Revenue/Expense Recognition Due to Lack of Detail Provided

Other Hockey Event-Related Revenue and Other Non-Hockey Event Related Revenue Does Not

Include Breakdown or Description

Hockey Event-Related Expenses and Non-Hockey Event Related Expenses Does Not Include Breakdown or Description

Depreciation and Amortization is Included in Selling, General, and Administrative Expenses

Specifically as it Relates to BB&T Center Operations, AOC was Not Able to Provide Historical Financial Statements Excluding Hockey Operations

Budget and Projections Not Provided

III. BB&T CENTER OVERVIEW

Page 62

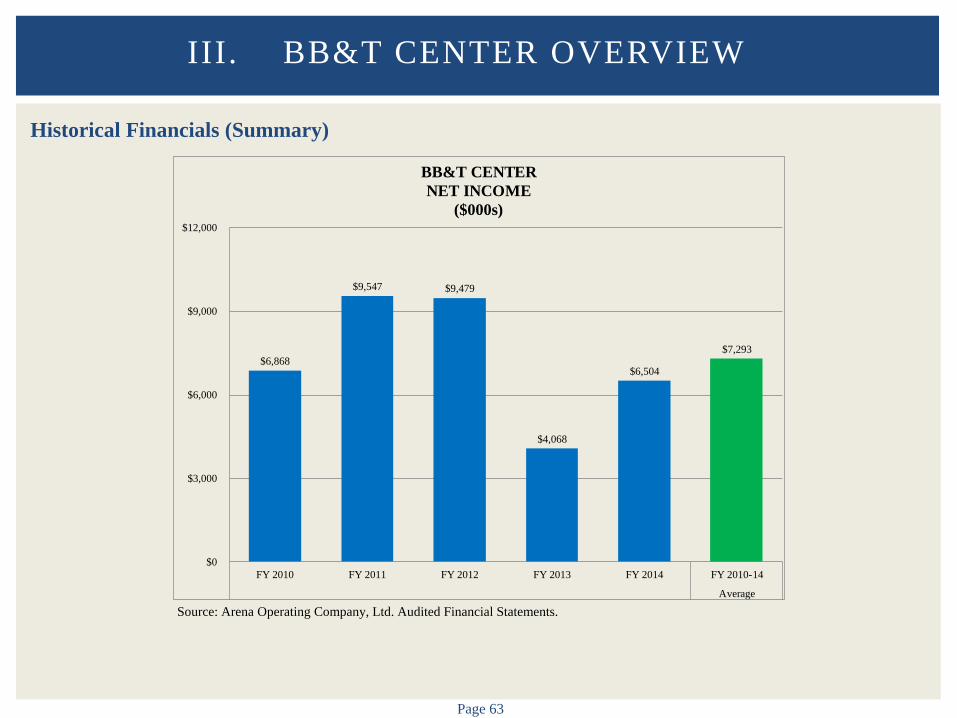

Historical Financials (Summary)

Net Income is Defined as Operating Income After Broward County and Other Obligations and Interest Expense

Net Income After Broward County and Other Obligations and Interest Expense was Approximately $4.1 Million in FY 2013, Significantly Lower than the FY 2010 to FY 2014 Average of $7.3 Million Likely as a Result of the NHL Lockout

III. BB&T CENTER OVERVIEW

Average CAGRFY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14 FY 2010-14

Revenues - Total $36,712,336 $40,660,082 $39,670,028 $40,026,126 $46,826,074 $40,778,929 6.3%

Operating Expenses - Total $24,258,920 $25,575,490 $24,431,506 $30,281,824 $34,740,994 $27,857,747 9.4%

Operating Income Before Broward County and Other Obligations $12,453,416 $15,084,592 $15,238,522 $9,744,302 $12,085,080 $12,921,182 -0.7%

Broward County and Other ObligationsCounty Preferred Revenue Allocation $4,023,000 $3,999,067 $4,102,280 $4,068,512 $4,059,474 $4,050,467 0.2%Florida Department of Transportation $898,233 $767,288 $806,003 $652,597 $620,294 $748,883 -8.8%Tourist Development Corp. Obligation $500,000 $500,000 $500,000 $500,000 $500,000 $500,000 0.0%

Broward County and Other Obligations - Total $5,421,233 $5,266,355 $5,408,283 $5,221,109 $5,179,768 $5,299,350 -1.1%

Interest Expense $163,935 $271,306 $351,629 $454,903 $401,306 $328,616 25.1%

Net Income $6,868,248 $9,546,931 $9,478,610 $4,068,290 $6,504,006 $7,293,217 -1.4%Source: Arena Operating Company, Ltd. Audited Financial Statements.

Page 63

Historical Financials (Summary)

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$6,868

$9,547 $9,479

$4,068

$6,504

$7,293

$0

$3,000

$6,000

$9,000

$12,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERNET INCOME

($000s)

Page 64

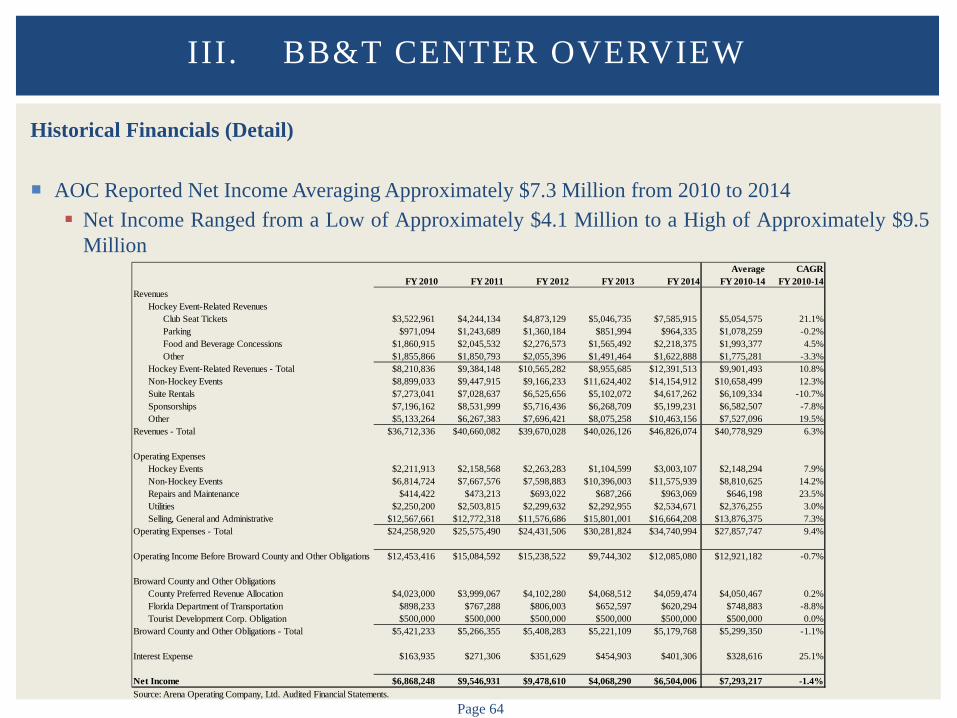

Historical Financials (Detail)

AOC Reported Net Income Averaging Approximately $7.3 Million from 2010 to 2014 Net Income Ranged from a Low of Approximately $4.1 Million to a High of Approximately $9.5

Million

III. BB&T CENTER OVERVIEW

Average CAGRFY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14 FY 2010-14

RevenuesHockey Event-Related Revenues

Club Seat Tickets $3,522,961 $4,244,134 $4,873,129 $5,046,735 $7,585,915 $5,054,575 21.1%Parking $971,094 $1,243,689 $1,360,184 $851,994 $964,335 $1,078,259 -0.2%Food and Beverage Concessions $1,860,915 $2,045,532 $2,276,573 $1,565,492 $2,218,375 $1,993,377 4.5%Other $1,855,866 $1,850,793 $2,055,396 $1,491,464 $1,622,888 $1,775,281 -3.3%

Hockey Event-Related Revenues - Total $8,210,836 $9,384,148 $10,565,282 $8,955,685 $12,391,513 $9,901,493 10.8%Non-Hockey Events $8,899,033 $9,447,915 $9,166,233 $11,624,402 $14,154,912 $10,658,499 12.3%Suite Rentals $7,273,041 $7,028,637 $6,525,656 $5,102,072 $4,617,262 $6,109,334 -10.7%Sponsorships $7,196,162 $8,531,999 $5,716,436 $6,268,709 $5,199,231 $6,582,507 -7.8%Other $5,133,264 $6,267,383 $7,696,421 $8,075,258 $10,463,156 $7,527,096 19.5%

Revenues - Total $36,712,336 $40,660,082 $39,670,028 $40,026,126 $46,826,074 $40,778,929 6.3%

Operating ExpensesHockey Events $2,211,913 $2,158,568 $2,263,283 $1,104,599 $3,003,107 $2,148,294 7.9%Non-Hockey Events $6,814,724 $7,667,576 $7,598,883 $10,396,003 $11,575,939 $8,810,625 14.2%Repairs and Maintenance $414,422 $473,213 $693,022 $687,266 $963,069 $646,198 23.5%Utilities $2,250,200 $2,503,815 $2,299,632 $2,292,955 $2,534,671 $2,376,255 3.0%Selling, General and Administrative $12,567,661 $12,772,318 $11,576,686 $15,801,001 $16,664,208 $13,876,375 7.3%

Operating Expenses - Total $24,258,920 $25,575,490 $24,431,506 $30,281,824 $34,740,994 $27,857,747 9.4%

Operating Income Before Broward County and Other Obligations $12,453,416 $15,084,592 $15,238,522 $9,744,302 $12,085,080 $12,921,182 -0.7%

Broward County and Other ObligationsCounty Preferred Revenue Allocation $4,023,000 $3,999,067 $4,102,280 $4,068,512 $4,059,474 $4,050,467 0.2%Florida Department of Transportation $898,233 $767,288 $806,003 $652,597 $620,294 $748,883 -8.8%Tourist Development Corp. Obligation $500,000 $500,000 $500,000 $500,000 $500,000 $500,000 0.0%

Broward County and Other Obligations - Total $5,421,233 $5,266,355 $5,408,283 $5,221,109 $5,179,768 $5,299,350 -1.1%

Interest Expense $163,935 $271,306 $351,629 $454,903 $401,306 $328,616 25.1%

Net Income $6,868,248 $9,546,931 $9,478,610 $4,068,290 $6,504,006 $7,293,217 -1.4%Source: Arena Operating Company, Ltd. Audited Financial Statements.

Page 65

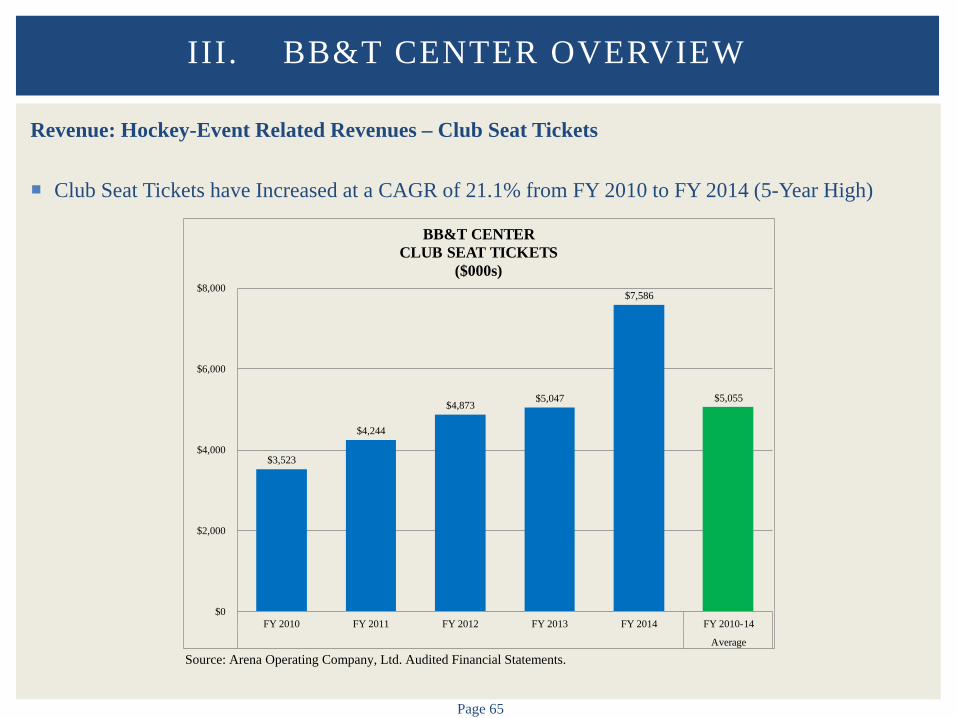

Revenue: Hockey-Event Related Revenues – Club Seat Tickets

Club Seat Tickets have Increased at a CAGR of 21.1% from FY 2010 to FY 2014 (5-Year High)

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$3,523

$4,244

$4,873 $5,047

$7,586

$5,055

$0

$2,000

$4,000

$6,000

$8,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERCLUB SEAT TICKETS

($000s)

Page 66

Revenue: Hockey-Event Related Revenues – Parking

Parking Revenues have Fluctuated Over the Past Five Years – Average of Approximately $1.1 Million

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$971

$1,244

$1,360

$852

$964

$1,078

$0

$1,000

$2,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERPARKING

($000s)

Page 67

Revenue: Hockey-Event Related Revenues – Food and Beverage Concessions

Food and Beverage Concessions Decreased Significantly in FY 2013 After Peaking in FY 2012 at $2.3 Million, Likely as a Result of the NHL Lockout

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$1,861

$2,046

$2,277

$1,565

$2,218

$1,993

$0

$1,000

$2,000

$3,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERFOOD AND BEVERAGE CONCESSIONS

($000s)

Page 68

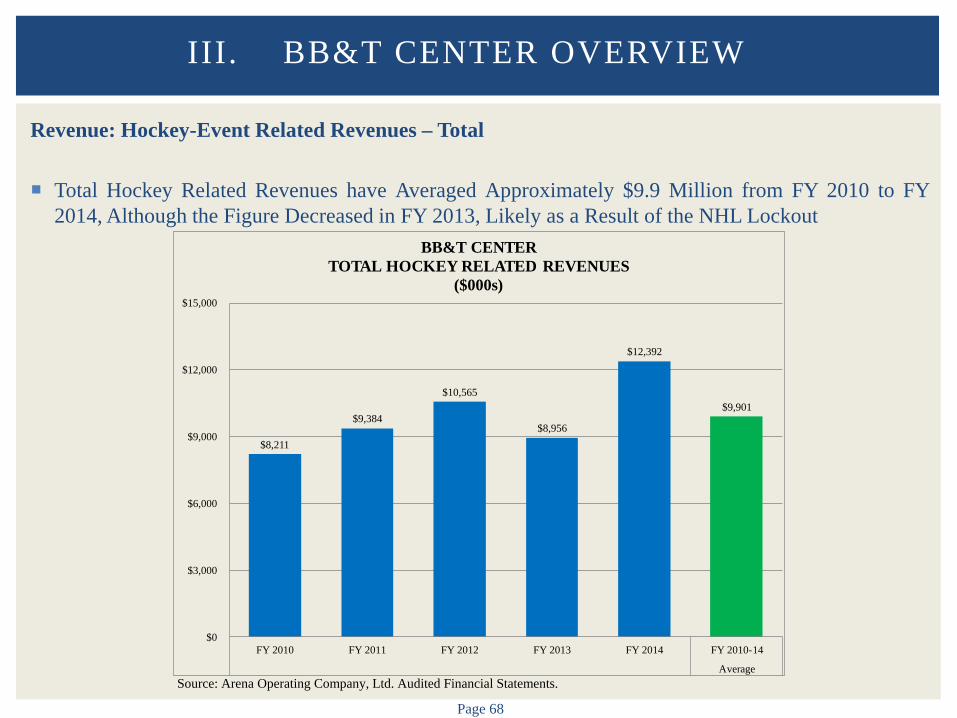

Revenue: Hockey-Event Related Revenues – Total

Total Hockey Related Revenues have Averaged Approximately $9.9 Million from FY 2010 to FY 2014, Although the Figure Decreased in FY 2013, Likely as a Result of the NHL Lockout

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$8,211

$9,384

$10,565

$8,956

$12,392

$9,901

$0

$3,000

$6,000

$9,000

$12,000

$15,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERTOTAL HOCKEY RELATED REVENUES

($000s)

Page 69

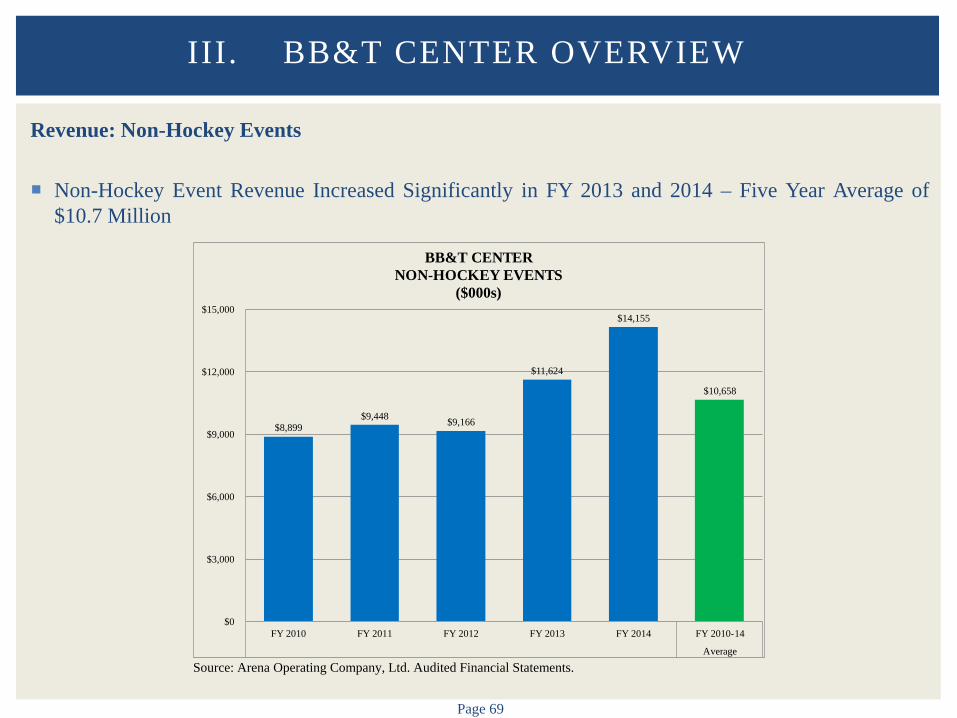

Revenue: Non-Hockey Events

Non-Hockey Event Revenue Increased Significantly in FY 2013 and 2014 – Five Year Average of $10.7 Million

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$8,899 $9,448 $9,166

$11,624

$14,155

$10,658

$0

$3,000

$6,000

$9,000

$12,000

$15,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERNON-HOCKEY EVENTS

($000s)

Page 70

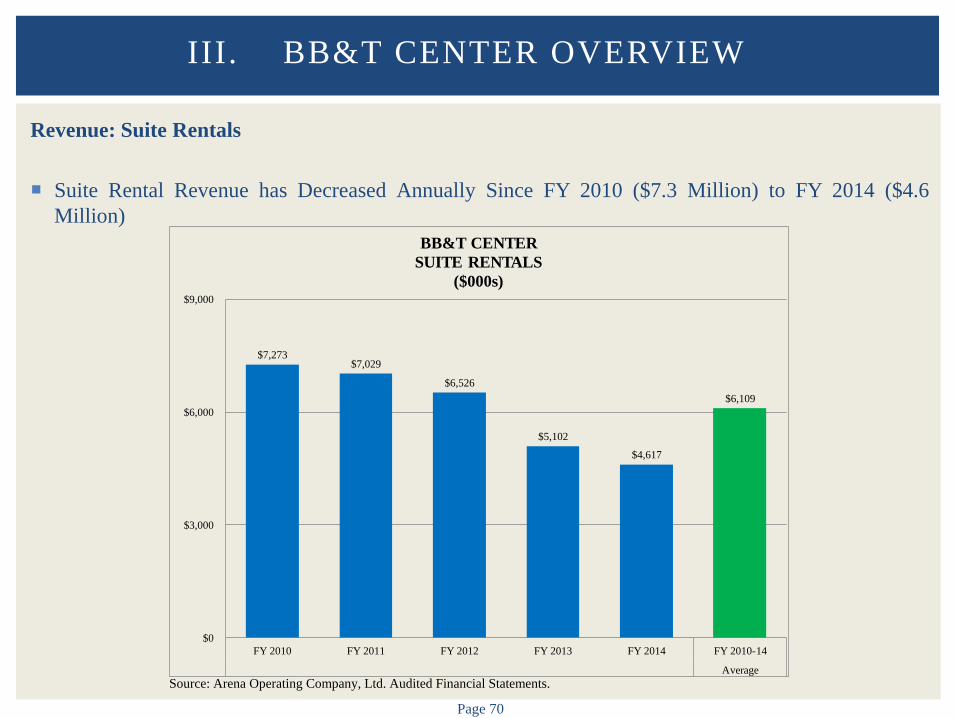

Revenue: Suite Rentals

Suite Rental Revenue has Decreased Annually Since FY 2010 ($7.3 Million) to FY 2014 ($4.6 Million)

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$7,273 $7,029

$6,526

$5,102

$4,617

$6,109

$0

$3,000

$6,000

$9,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERSUITE RENTALS

($000s)

Page 71

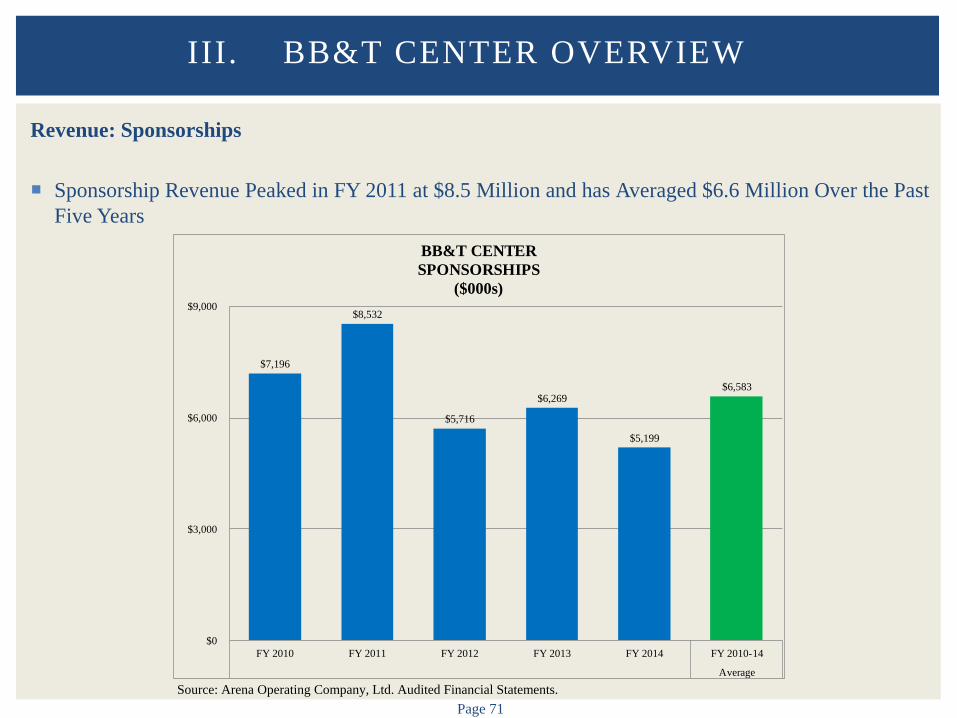

Revenue: Sponsorships

Sponsorship Revenue Peaked in FY 2011 at $8.5 Million and has Averaged $6.6 Million Over the Past Five Years

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$7,196

$8,532

$5,716

$6,269

$5,199

$6,583

$0

$3,000

$6,000

$9,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERSPONSORSHIPS

($000s)

Page 72

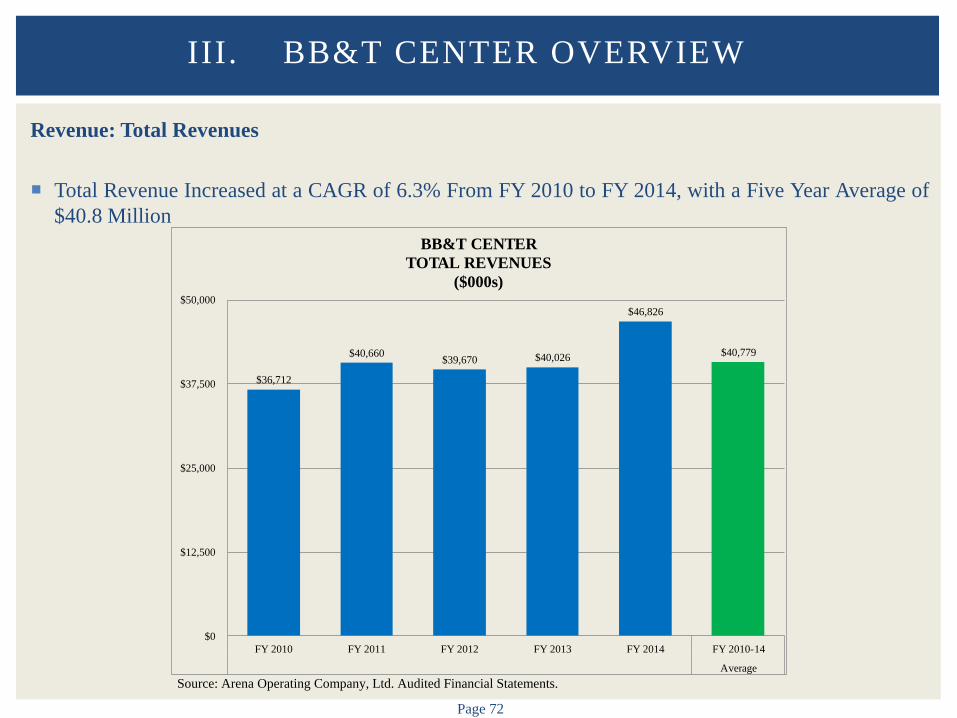

Revenue: Total Revenues

Total Revenue Increased at a CAGR of 6.3% From FY 2010 to FY 2014, with a Five Year Average of $40.8 Million

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$36,712

$40,660 $39,670 $40,026

$46,826

$40,779

$0

$12,500

$25,000

$37,500

$50,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERTOTAL REVENUES

($000s)

Page 73

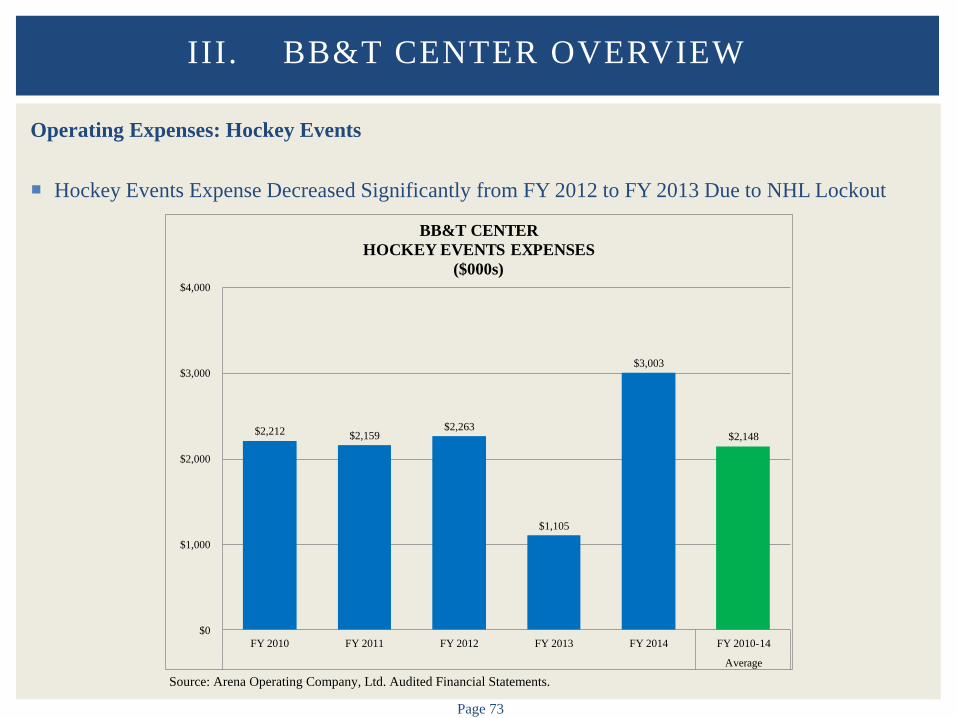

Operating Expenses: Hockey Events

Hockey Events Expense Decreased Significantly from FY 2012 to FY 2013 Due to NHL Lockout

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$2,212 $2,159 $2,263

$1,105

$3,003

$2,148

$0

$1,000

$2,000

$3,000

$4,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERHOCKEY EVENTS EXPENSES

($000s)

Page 74

Operating Expenses: Repairs and Maintenance

Repairs and Maintenance Expenses were $963,000 in FY 2014, Significantly Higher than the Five Year Average Since FY 2010 of $646,000

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$414

$473

$693 $687

$963

$646

$0

$250

$500

$750

$1,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERREPAIRS AND MAINTENANCE

($000s)

Page 75

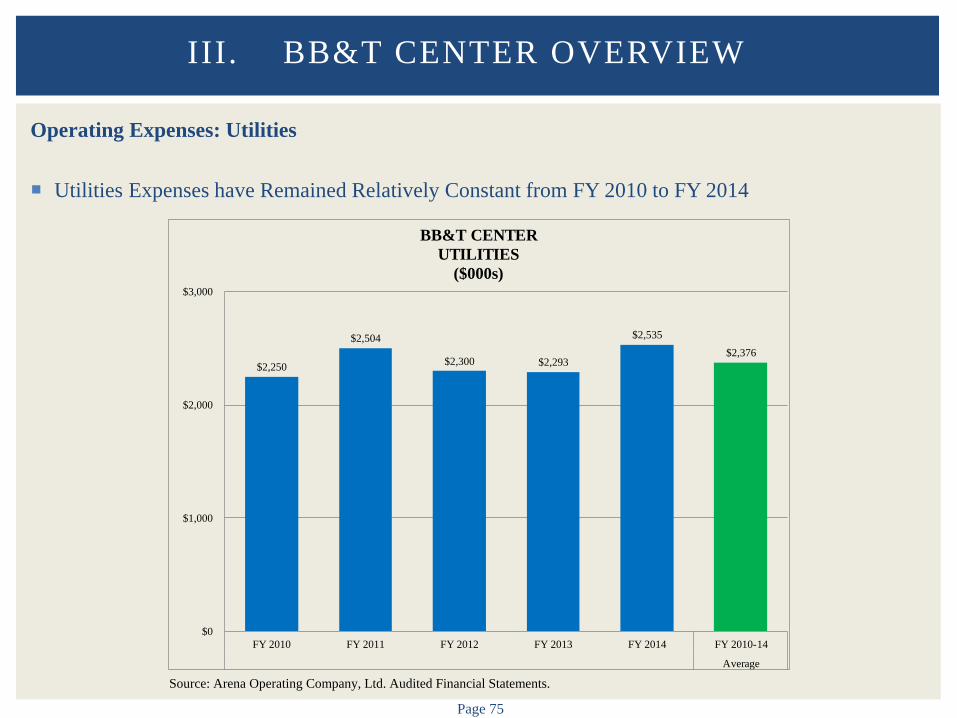

Operating Expenses: Utilities

Utilities Expenses have Remained Relatively Constant from FY 2010 to FY 2014

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$2,250

$2,504

$2,300 $2,293

$2,535 $2,376

$0

$1,000

$2,000

$3,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERUTILITIES

($000s)

Page 76

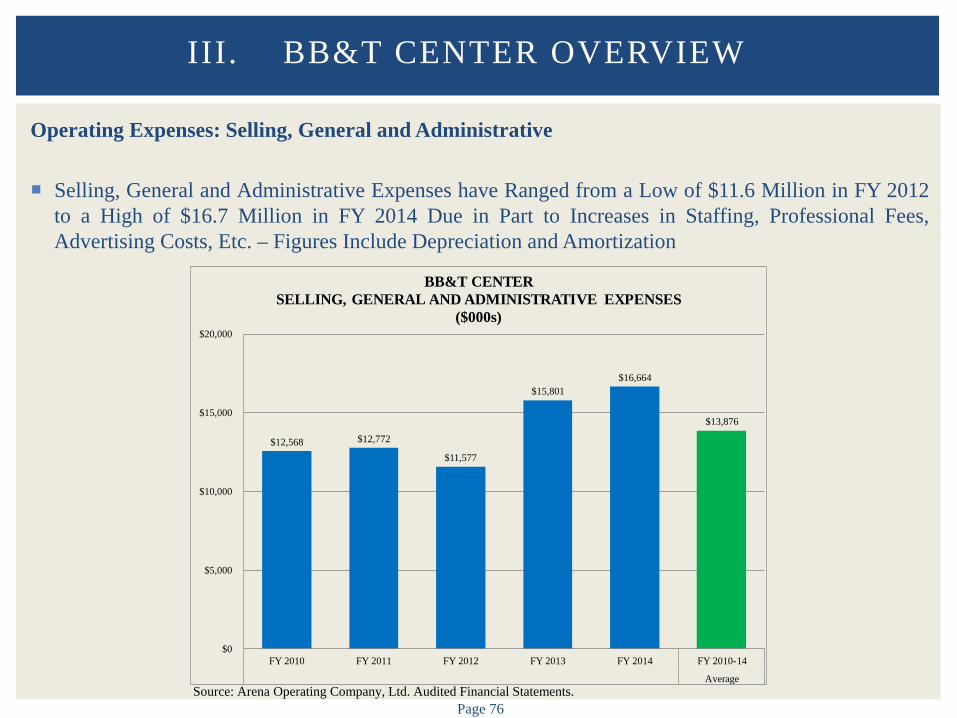

Operating Expenses: Selling, General and Administrative

Selling, General and Administrative Expenses have Ranged from a Low of $11.6 Million in FY 2012 to a High of $16.7 Million in FY 2014 Due in Part to Increases in Staffing, Professional Fees, Advertising Costs, Etc. – Figures Include Depreciation and Amortization

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$12,568 $12,772

$11,577

$15,801 $16,664

$13,876

$0

$5,000

$10,000

$15,000

$20,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERSELLING, GENERAL AND ADMINISTRATIVE EXPENSES

($000s)

Page 77

Operating Expenses: Total

Total Operating Expenses Peaked in FY 2014 at $34.7 Million – Figures Include Depreciation and Amortization

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$24,259 $25,575

$24,432

$30,282

$34,741

$27,858

$0

$10,000

$20,000

$30,000

$40,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTERTOTAL OPERATING EXPENSES

($000s)

Page 78

Operating Income Before Broward County and Other Obligations

Operating Income Before Broward County and Other Obligations has Averaged $12.9 Million Since FY 2010

III. BB&T CENTER OVERVIEW

Source: Arena Operating Company, Ltd. Audited Financial Statements.

$12,453

$15,085 $15,239

$9,744

$12,085 $12,921

$0

$5,000

$10,000

$15,000

$20,000

FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2010-14

Average

BB&T CENTEROPERATING INCOME BEFORE BROWARD COUNTY AND

OTHER OBLIGATIONS($000s)

IV. MARKET OVERVIEW

A. DEMOGRAPHIC COMPARISON

Page 81

Overview

Market Area Size and Characteristics Impact Market Support and Demand for Events, Tickets, Premium Seating, Sponsorship, Etc.

Limited Market Demographic Overview Completed Largest 20 U.S. Markets Core Base Statistical Area (CBSA) Designation

Consideration Should be Given to Comprehensive Market Analysis (Market Surveys/Focus

Groups/Etc.)

A. DEMOGRAPHIC COMPARISON

Page 82

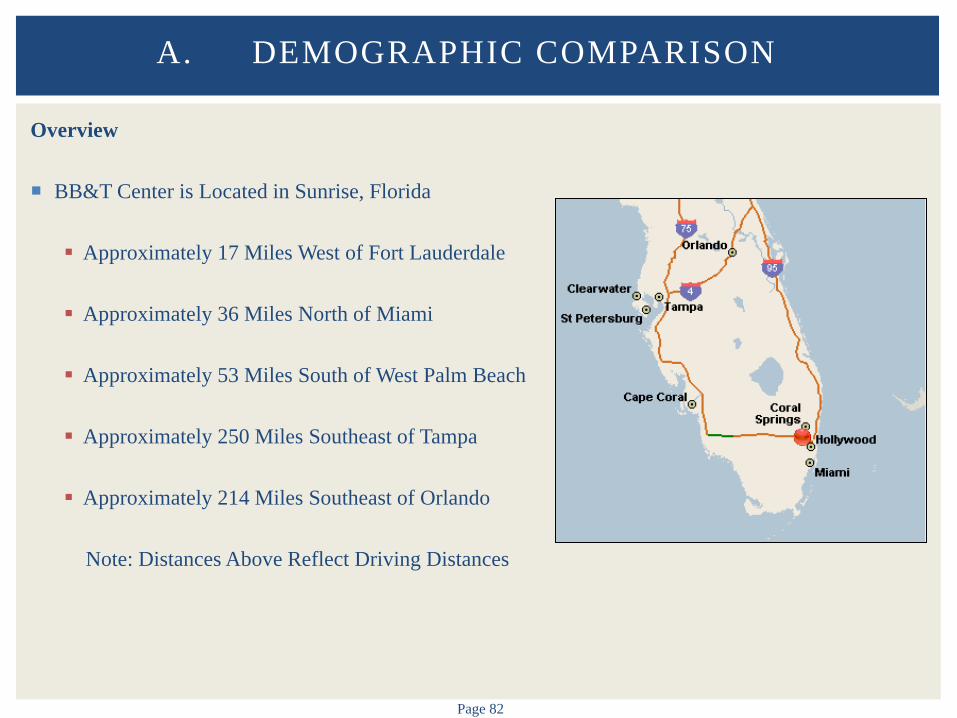

Overview

BB&T Center is Located in Sunrise, Florida Approximately 17 Miles West of Fort Lauderdale

Approximately 36 Miles North of Miami

Approximately 53 Miles South of West Palm Beach

Approximately 250 Miles Southeast of Tampa

Approximately 214 Miles Southeast of Orlando

Note: Distances Above Reflect Driving Distances

A. DEMOGRAPHIC COMPARISON

Page 83

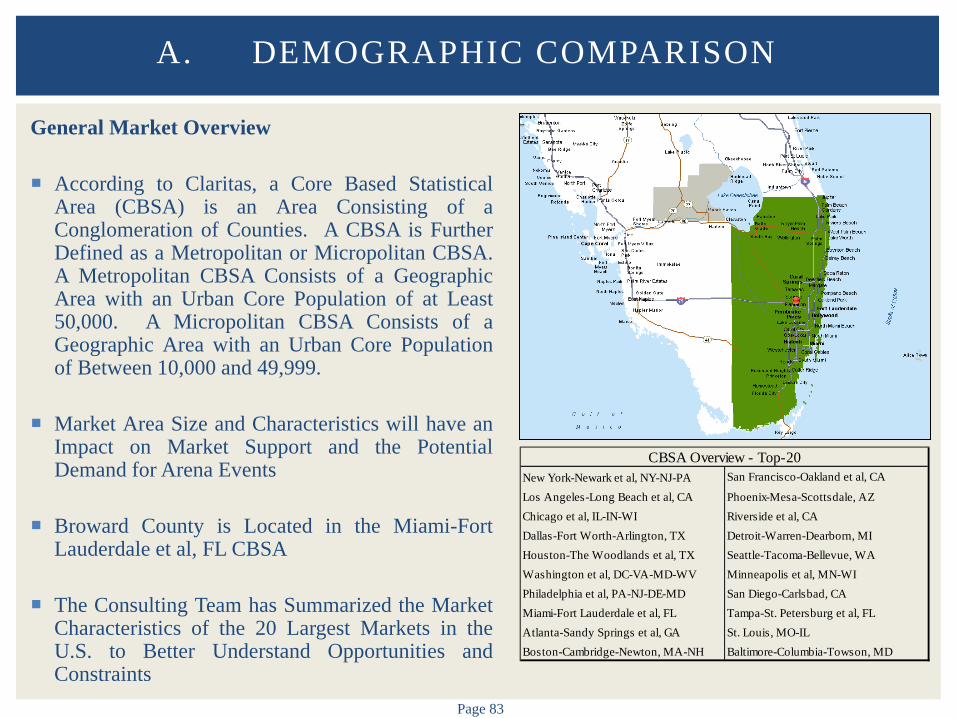

General Market Overview

According to Claritas, a Core Based Statistical Area (CBSA) is an Area Consisting of a Conglomeration of Counties. A CBSA is Further Defined as a Metropolitan or Micropolitan CBSA. A Metropolitan CBSA Consists of a Geographic Area with an Urban Core Population of at Least 50,000. A Micropolitan CBSA Consists of a Geographic Area with an Urban Core Population of Between 10,000 and 49,999.

Market Area Size and Characteristics will have an Impact on Market Support and the Potential Demand for Arena Events

Broward County is Located in the Miami-Fort Lauderdale et al, FL CBSA

The Consulting Team has Summarized the Market Characteristics of the 20 Largest Markets in the U.S. to Better Understand Opportunities and Constraints

A. DEMOGRAPHIC COMPARISON

New York-Newark et al, NY-NJ-PA San Francisco-Oakland et al, CA

Los Angeles-Long Beach et al, CA Phoenix-Mesa-Scottsdale, AZChicago et al, IL-IN-WI Riverside et al, CADallas-Fort Worth-Arlington, TX Detroit-Warren-Dearborn, MIHouston-The Woodlands et al, TX Seattle-Tacoma-Bellevue, WAWashington et al, DC-VA-MD-WV Minneapolis et al, MN-WIPhiladelphia et al, PA-NJ-DE-MD San Diego-Carlsbad, CAMiami-Fort Lauderdale et al, FL Tampa-St. Petersburg et al, FLAtlanta-Sandy Springs et al, GA St. Louis, MO-ILBoston-Cambridge-Newton, MA-NH Baltimore-Columbia-Towson, MD

CBSA Overview - Top-20

Page 84

A. DEMOGRAPHIC COMPARISON

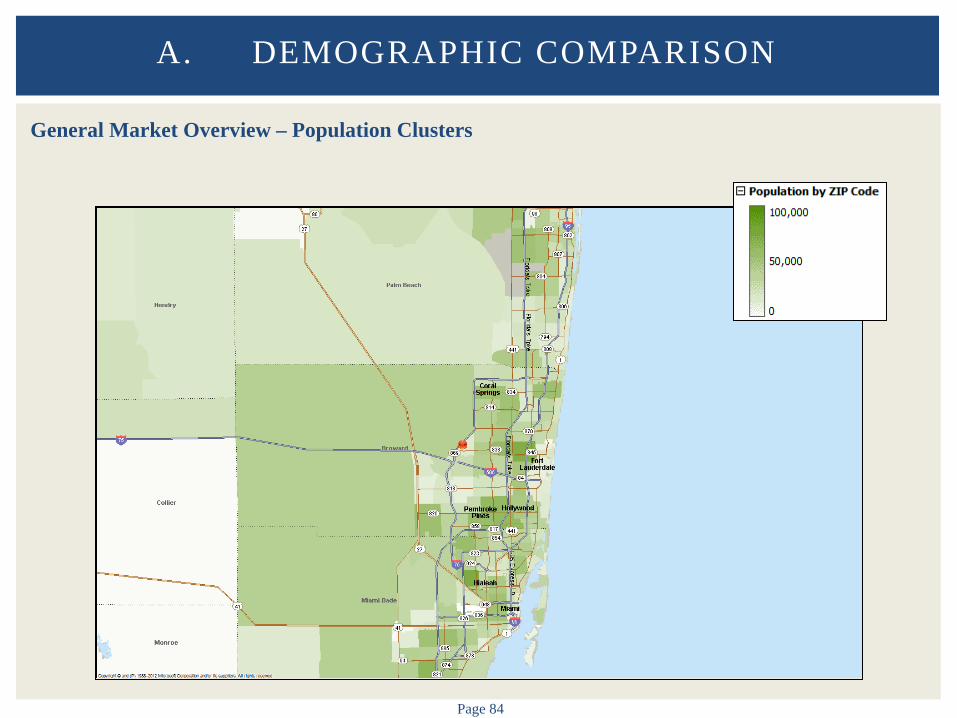

General Market Overview – Population Clusters

Page 85

A. DEMOGRAPHIC COMPARISON

General Market Overview – Household Clusters

Page 86

A. DEMOGRAPHIC COMPARISON

General Market Overview – Income Clusters

Page 87

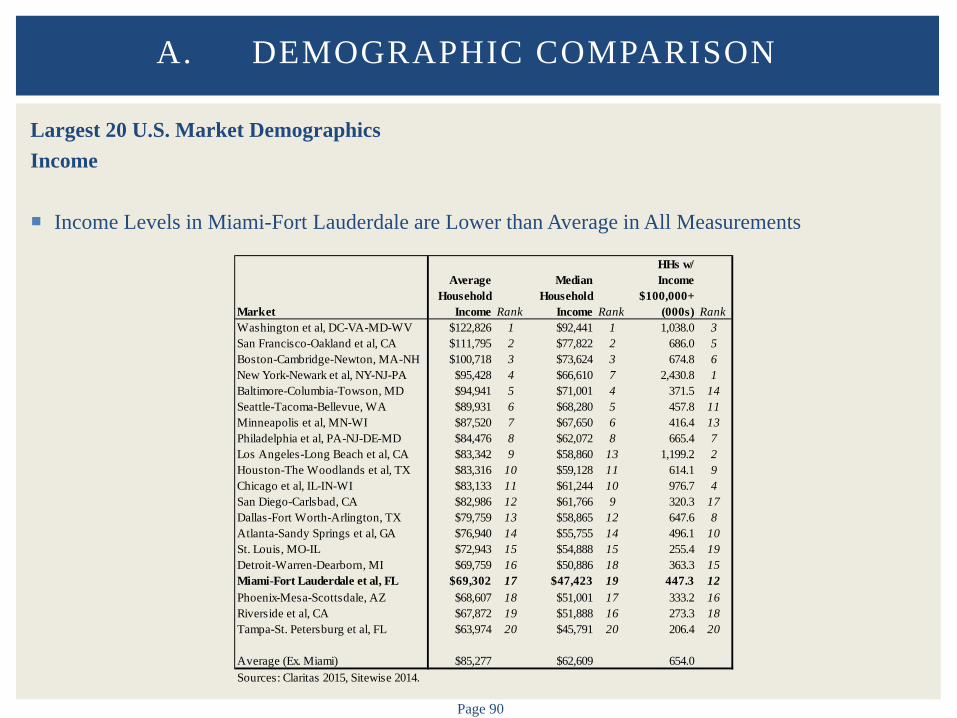

A. DEMOGRAPHIC COMPARISON

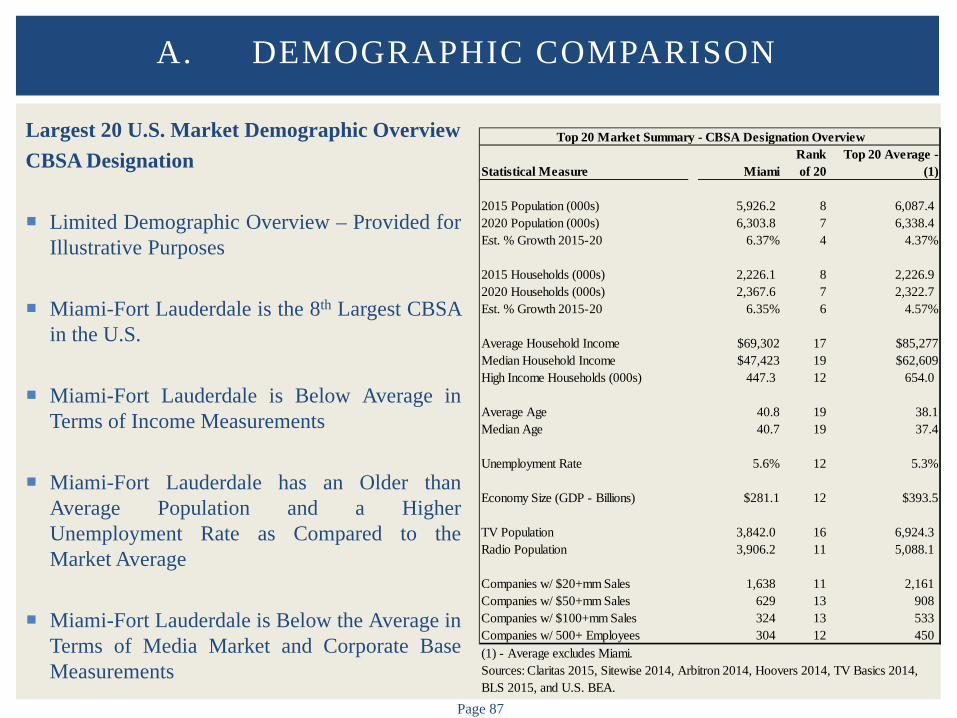

Largest 20 U.S. Market Demographic Overview CBSA Designation Limited Demographic Overview – Provided for

Illustrative Purposes

Miami-Fort Lauderdale is the 8th Largest CBSA in the U.S.

Miami-Fort Lauderdale is Below Average in Terms of Income Measurements

Miami-Fort Lauderdale has an Older than Average Population and a Higher Unemployment Rate as Compared to the Market Average

Miami-Fort Lauderdale is Below the Average in Terms of Media Market and Corporate Base Measurements

Statistical Measure MiamiRank of 20

Top 20 Average - (1)

2015 Population (000s) 5,926.2 8 6,087.4 2020 Population (000s) 6,303.8 7 6,338.4 Est. % Growth 2015-20 6.37% 4 4.37%

2015 Households (000s) 2,226.1 8 2,226.9 2020 Households (000s) 2,367.6 7 2,322.7 Est. % Growth 2015-20 6.35% 6 4.57%

Average Household Income $69,302 17 $85,277Median Household Income $47,423 19 $62,609High Income Households (000s) 447.3 12 654.0

Average Age 40.8 19 38.1Median Age 40.7 19 37.4

Unemployment Rate 5.6% 12 5.3%

Economy Size (GDP - Billions) $281.1 12 $393.5

TV Population 3,842.0 16 6,924.3 Radio Population 3,906.2 11 5,088.1

Companies w/ $20+mm Sales 1,638 11 2,161Companies w/ $50+mm Sales 629 13 908Companies w/ $100+mm Sales 324 13 533Companies w/ 500+ Employees 304 12 450

Top 20 Market Summary - CBSA Designation Overview

Sources: Claritas 2015, Sitewise 2014, Arbitron 2014, Hoovers 2014, TV Basics 2014, BLS 2015, and U.S. BEA.

(1) - Average excludes Miami.

Page 88

Largest 20 U.S. Market Primary Arenas

Summarized Below are the Primary Arenas in the Largest 20 U.S. Markets

A. DEMOGRAPHIC COMPARISON

Market

New York-Newark et al, NY-NJ-PA Madison Square Garden Barclays CenterLos Angeles-Long Beach et al, CA Staples Center Honda CenterChicago et al, IL-IN-WI United Center Allstate ArenaDallas-Fort Worth-Arlington, TX American Airlines CenterHouston-The Woodlands et al, TX Toyota CenterWashington et al, DC-VA-MD-WV Verizon Center Xfinity CenterPhiladelphia et al, PA-NJ-DE-MD Wells Fargo Center Liacouras CenterMiami-Fort Lauderdale et al, FL BB&T Center AmericanAirlines ArenaAtlanta-Sandy Springs et al, GA Philips Arena The Arena at Gwinnett CenterBoston-Cambridge-Newton, MA-NH TD GardenSan Francisco-Oakland et al, CA Oracle ArenaPhoenix-Mesa-Scottsdale, AZ Talking Stick Resort Arena Gila River ArenaRiverside et al, CA Citizens Bank ArenaDetroit-Warren-Dearborn, MI New Red Wings Arena The Palace of Auburn HillsSeattle-Tacoma-Bellevue, WA KeyArena Tacoma DomeMinneapolis et al, MN-WI Target Center Xcel CenterSan Diego-Carlsbad, CA Valley View Casino Center Viejas ArenaTampa-St. Petersburg et al, FL Amalie ArenaSt. Louis, MO-IL Scottrade Center Chaifetz ArenaBaltimore-Columbia-Towson, MD Royal Farms ArenaSource: Industry research.

Primary Arenas

Page 89

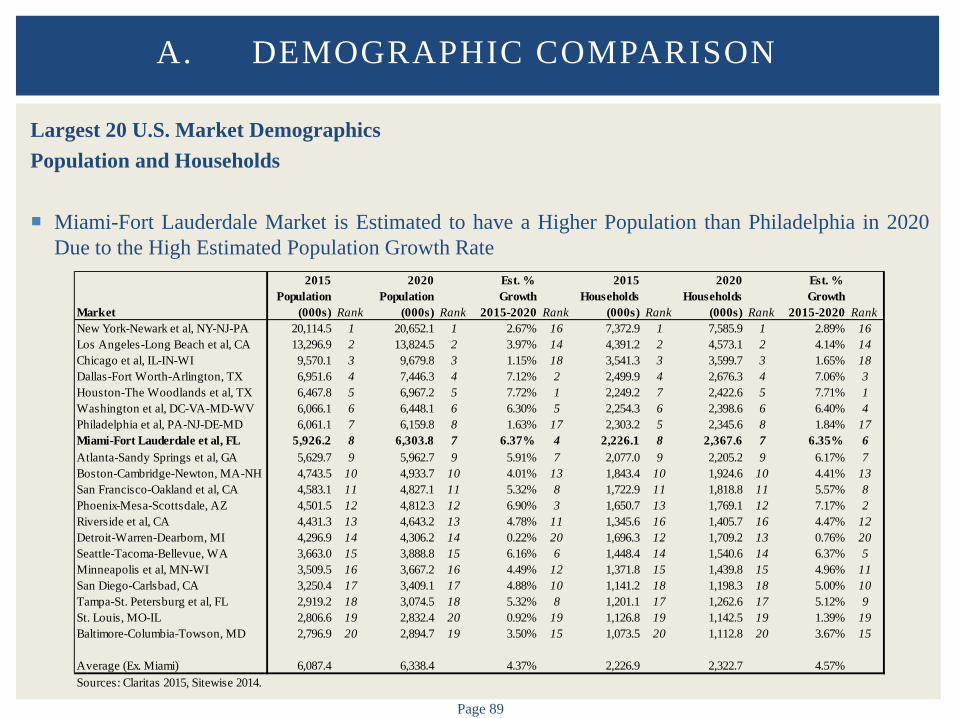

Largest 20 U.S. Market Demographics Population and Households

Miami-Fort Lauderdale Market is Estimated to have a Higher Population than Philadelphia in 2020

Due to the High Estimated Population Growth Rate

A. DEMOGRAPHIC COMPARISON

Market

2015 Population

(000s) Rank

2020 Population

(000s) Rank

Est. % Growth

2015-2020 Rank

2015 Households

(000s) Rank

2020 Households

(000s) Rank

Est. % Growth