brooklyn rapid transit central power house plans and proposal, 1910-2010

DESCRIPTION

From the Google Books Thomas Edward Murray's 1910 "Electric Power Plants". It powered the Brooklyn’s Trolley System, giving the (Trolley) Dodgers baseball team their name. It was fueled by Gowanus Canal coal barges, and Canal water to produce steam power. Built around 1896, it’s steam turbines closed in 1938, It ceased operations in 1974. It was given to the Jewish Press in 1969 by Mayor Lindsay to buy votes. It was a Jewish entertainment center during the 1970’s and abandoned by the 1990’s. It became a squatter settlement for drug addicts, which earned it it’s local nickname as the Bat Cave. The covenant restricting it’s sale expired in 2011, and the site is currently available for sale from Africa Israel via TerraCRG. Several developers are currently studying it for redevelopment. A 2010 development study by Zack Schwanbeck is included. DRAFT - reload - images not displaying correctly - but downloads are fine.TRANSCRIPT

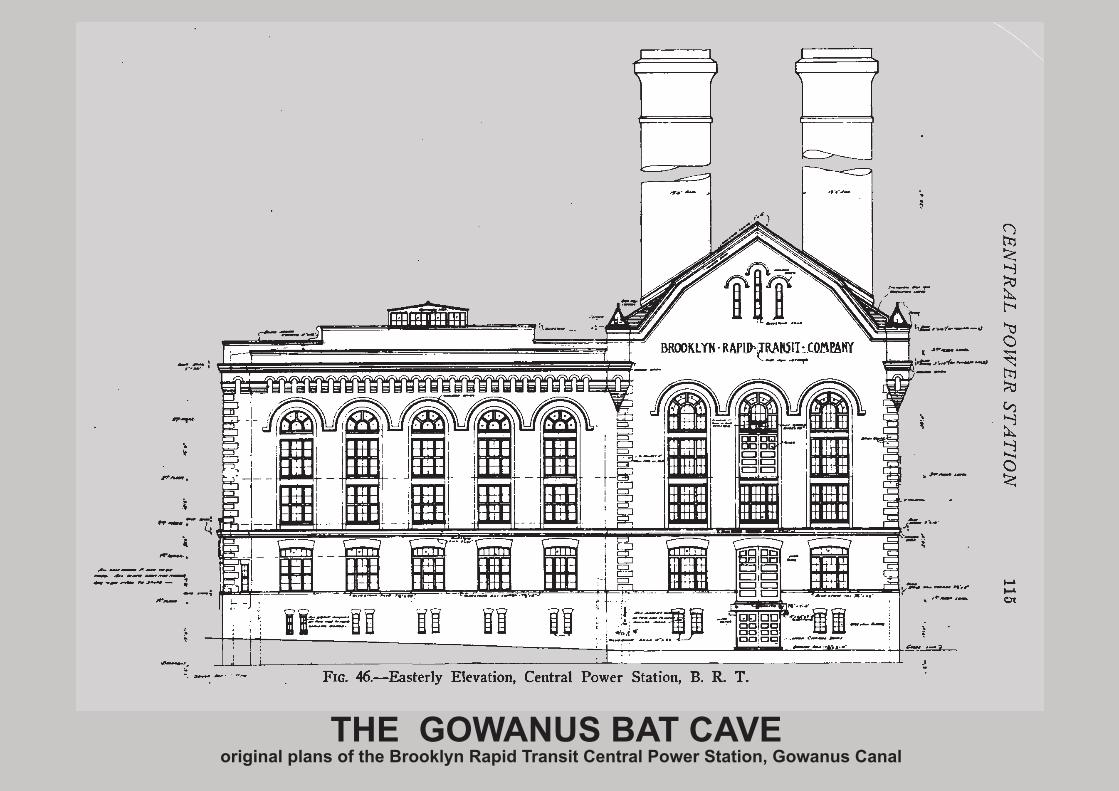

THE GOWANUS BAT CAVE original plans of the Brooklyn Rapid Transit Central Power Station, Gowanus Canal

1904 Sanborn Fire Insurance Map

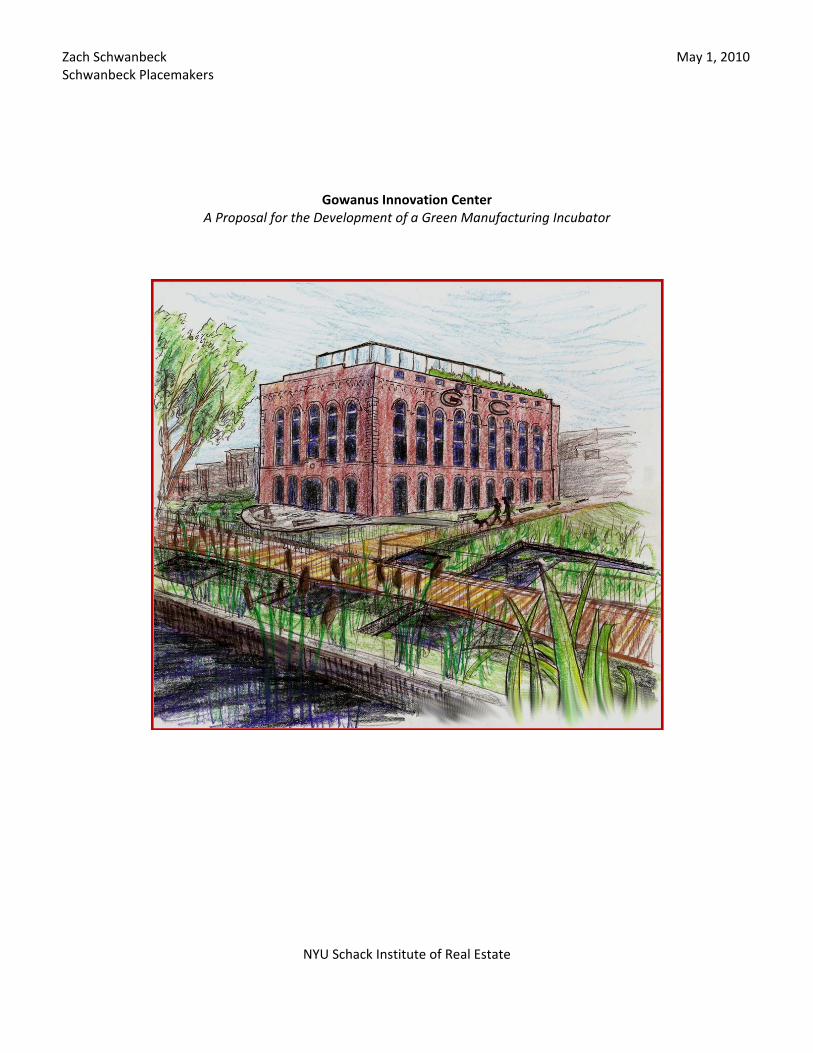

Zach Schwanbeck May 1, 2010 Schwanbeck Placemakers

Gowanus Innovation Center A Proposal for the Development of a Green Manufacturing Incubator

NYU Schack Institute of Real Estate

Table of Contents

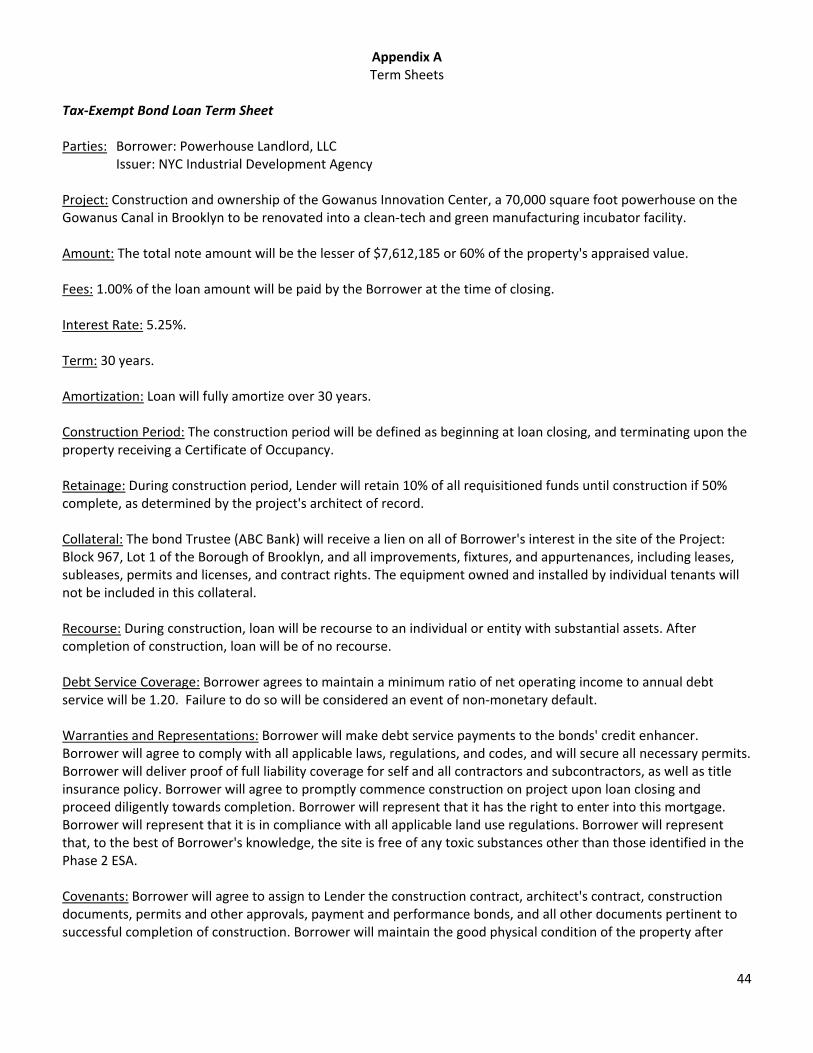

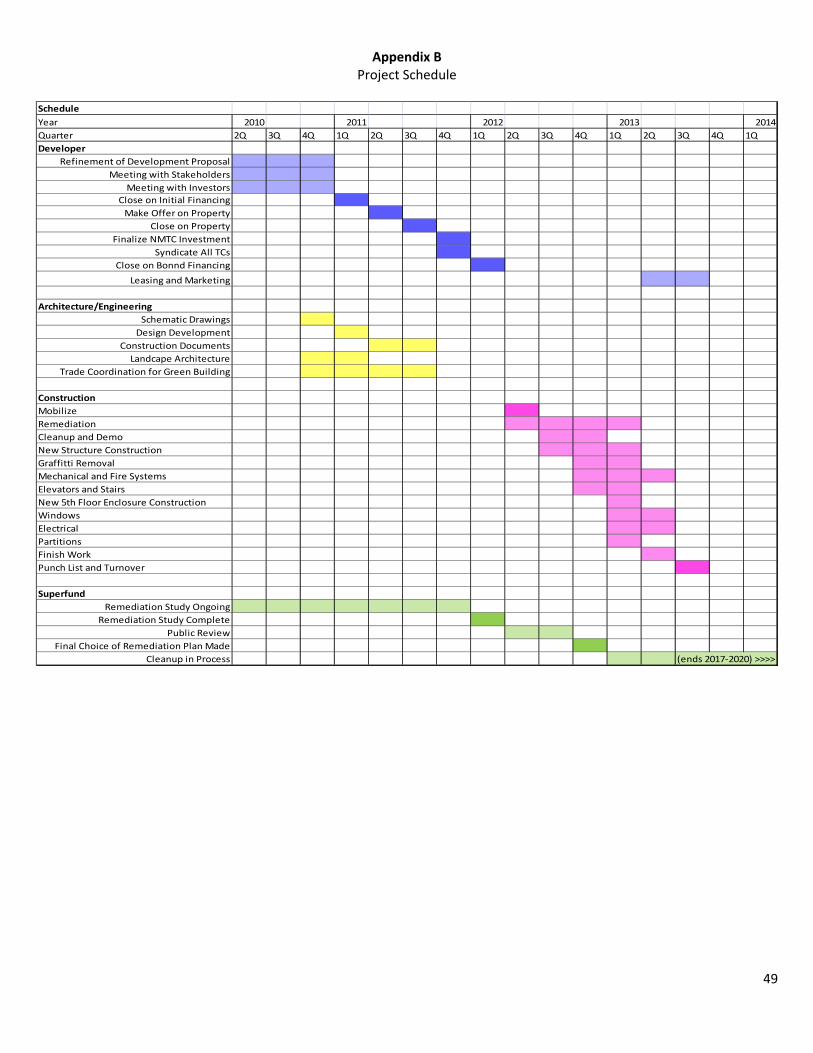

Executive Summary....................................................................................................1 Project Description.....................................................................................................2 Origination of Concept...............................................................................................3 The Area.....................................................................................................................4 The Site......................................................................................................................7 The Building..............................................................................................................14 Renovation Plans......................................................................................................20 Marketing and Operations........................................................................................27 Market Feasibility.....................................................................................................31 Acquisition................................................................................................................39 Financing and Approvals...........................................................................................40 Legal Organization....................................................................................................42 Appendix A: Term Sheets..........................................................................................44 Appendix B: Project Schedule...................................................................................49 Appendix C: Financial Information. ..........................................................................50

1

Executive Summary The Gowanus Innovation Center will be a green manufacturing startup incubator, leasing affordable space to companies needing a place to design, build, sell, and finance new technologies that address environmental and energy issues. It will be housed in a renovated industrial building on the banks of the Gowanus Canal in Brooklyn, New York, and will be surrounded by publicly accessible open space. The Center will address several important needs at once. It will help drive the city's economic recovery by allowing creative entrepreneurs to succeed in bringing new products to market. It will aid in retaining the industrial sector in Brooklyn and New York as a whole, an important means of providing quality employment. It will promote green industries and further the goal of New York leading the way in sustainability. Finally, it will be a pioneer development on the Gowanus canal, proving that seriously polluted urban locations can be responsibly cleaned and renewed into thriving creative workplaces. A variety of tenant spaces will be designed to suit all types of tenant needs. The design will take advantage of the structure's views, natural lighting and historic character. Green building practices will be used throughout, and a solar thermal array on the roof will provide heat and hot water. The historic exterior will be restored. Amenities such as a truck loading dock, communal conference room and wireless will be provided. The Center will offer support for business planning and management, and work to connect firms with potential investors and customers. The application process for space will be highly competitive. There are several other facilities nearby that provide below‐market space for manufacturing firms and/or green technology startups. These firms have been highly successful in both attracting tenants and producing jobs. While there are plans to add a great deal more of this space in the coming years, we anticipate the rapid growth in the green industries to take up this supply and the vacancy rates at such facilities to remain low. The project will be financed with a number of different public and private sources. Equity will come from New Market Tax Credits, Historic Tax Credits, and Brownfield Tax Credits. Several grants and appropriations will be sought, such as a below‐market loans. The largest piece of the capital stack will be a mortgage provided by tax exempt bond proceeds, issued through NYCIDA. While there are additional costs and delays associated with developing adjacent to a recently named Superfund site, there is little liability risk, and we plan on beginning construction in early 2012 with completion in late 2013. The total cost of development will be $28.6 million. A 3% fee will be paid to Schwanbeck Placemakers for real estate development consulting services, along with ownership of the site's unused air rights for potential use on an adjacent site, and a title to a subdivided parcel.

2

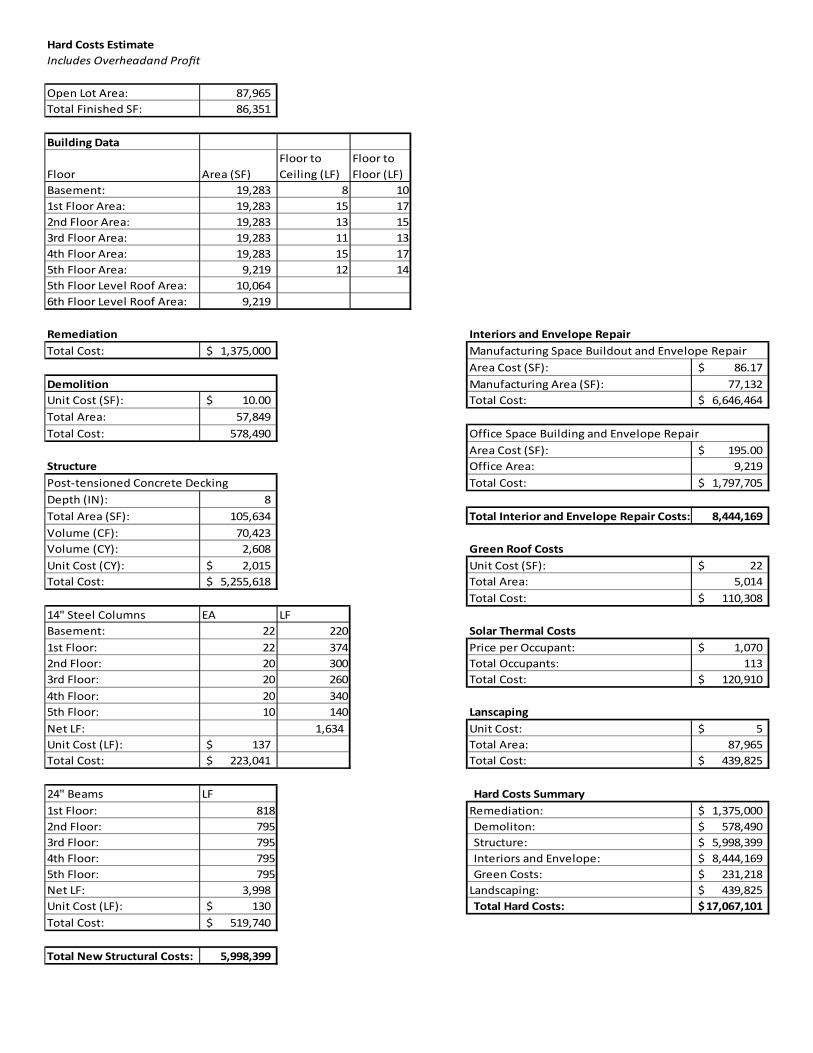

Project Description The Gowanus Innovation Center will be a non‐profit business incubator housed in a renovated powerhouse building on the banks of the famed Gowanus canal. It will provide below‐market space to startup businesses, with a preference for manufacturers of green products and clean‐tech. The center will thus play an important role in New York City's economic recovery, by retaining innovative entrepreneurs who might otherwise be priced out of the city. New, well‐paying manufacturing jobs will be created for local residents as a result. By focusing on green industries, the center will further the goal of New York taking the lead in addressing the environmental problems defining the 21st century. Housed in a powerful symbolic link to the industrial past of New York, the center will contain the beginnings of the industries of the future. By proceeding with an as‐of‐right development on the banks of the Gowanus, we will make a statement that the revitalization of this area is proceeding, defeating the unfair stigma that has arisen regarding the canal. The canal area will eventually become an attractive mixed‐use neighborhood amenable to the creative class that the city must attract for the new economy. The building will provide 75,600 square feet of industrial spaces in a variety of sizes, ranging from 960 to 8,000 square feet. The first floor will be used for two tenants requiring large spaces and truck loading access. The second, third, and fourth stories will contain spaces for tenants needing smaller manufacturing areas. The fifth floor will contain 9,200 square feet of open, flexible office space to be occupied by the same tenants who are leasing manufacturing space. This floor will boast excellent views, modern amenities, and shared facilities such as a conference room and kitchen. The remaining rooftop will be converted into an area for outdoor entertainment and will be partially surfaced with a garden. Freight and passenger elevators will connect all floors. The surrounding grounds will be converted into an ecological landscape, which will assist in remediating the canal's pollutants while providing attractive outdoor space for both workers in the Center and the general public. This landscape, along with the use of green building practices throughout building's renovation, will demonstrate the Center's thorough commitment to sustainability, as well as help tenants save money, maintain a healthy environment, and mitigate further pollution of the canal. The project will be developed for a fee by our firm, Schwanbeck Placemakers LLC, a sustainable real estate develop‐design‐build firm. We will create a new nonprofit organization, the Gowanus Innovation Center Development Corporation, to manage the property and run the incubator. Schwanbeck Placemakers will enter into a development services contract with this entity, as well as a design‐build contract. Our compensation will be in the form of a developer's fee, any savings from a guaranteed maximum price, a subdivided parcel of the Center's lot, and control of all unused air rights. We are simultaneously purchasing an adjacent property in an unrelated transaction. By owning the air rights of the center we will be able to earn a return on our services based on our success in bringing investment and excitement to the area. The total cost of development will be $28.6 million, or $332 per square foot.

3

Origination of Concept Schwanbeck Placemakers arrived at the concept of the GIC by first thinking about the larger issues challenging the urban environment today, particularly within New York City. As the U.S. struggles to confront climate change and dependence on foreign oil imports, it has been well noted that approximately 40% of the nation's energy is consumed by commercial and residential buildings.1 The proportion is even higher in New York City, at 75%. And while it is important to ensure that new construction is energy efficient, the fact is that by 2030, 85% of the City's buildings will still be those that currently exist.2 Furthermore, the energy embodied in a building's materials is often overlooked, despite being quite significant ‐ energy used to manufacture and transport materials used in the construction of a building is 15 to 30 times the finished product's annual energy use.3 Schwanbeck Placemakers thus came to the decision that preserving an existing building, and completing an energy efficient restoration, would be a project that would successfully address the needs of the City at this time. We also believe a renovation that utilizes an existing structure will require less capital, and will have a greater chance of securing financing in the current state of real estate capital markets. We searched for an underutilized property with a high potential for addition of value, which we could acquire at a low price. After considering several properties in Brooklyn, Queens, and the Bronx, the Powerhouse building stood out due to its architectural features, size, and location. The building has the type of simple, yet grand features that characterize the industrial architecture of earlier years, and have proven highly popular in many other residential and commercial loft renovations. The building is one of the tallest around and is a neighborhood landmark. The location is near transportation with easy access to Manhattan, and only a few blocks from the highly desirable neighborhood of Park Slope. The environmental issues of the Canal itself would be considered a liability by some, but we believe the highly publicized controversy, and the Mayor's determination to redevelop the area, will result in an ability to leverage public resources in order to ensure the success of the project. Schwanbeck Placemakers originally investigated residential, retail, and manufacturing uses for the building. The residential and retail components were considered due to the existing demand in residential neighborhoods surrounding the area, and the Department of City Planning's proposal to rezone the area for mixed use. The intention was to establish an early presence in Gowanus and benefit from future increases in property values as the largely industrial landscape transitions to a more residential neighborhood. However, as we continued our diligence it became clear that the rezoning plans would take some time. By the time the EPA decided to list the canal as a Superfund site, we determined that it would be possible to develop the site immediately, using as‐of‐right zoning to provide for manufacturing use only. Schwanbeck Placemakers intends to realize the potential of the neighborhood at a later date, through control of the property's air rights and an adjacent site. The economic recession has suggested that the U.S. economy's reliance on the service sector has become unbalanced over time, and that future growth will involve more designing, engineering, and manufacturing new technology. Schwanbeck Placemakers believes that there is a high potential for growth in technology that solves environmental problems. The concept of an incubator arose after considering the need to facilitate the growth of small green manufacturers in a city with expensive real estate and a threatened industrial sector. This coincided with our activities involving another client, who was seeking to produce a rooftop hydroponic greenhouse and seeking a low cost space to manufacture the units. While the product was uniquely suited to the New York urban fabric, it was more economical to produce the product elsewhere and ship it into the city due to the high rents. The presence of other successful incubators, many of which inhabit renovated industrial buildings, also encouraged the idea. Furthermore, we noted that there did not exist an incubator that offered integrated office and manufacturing

1 The Need Project. Energy Consumption. <http://www.need.org/needpdf/infobook_activities/IntInfo/ConsI.pdf> Accessed May 1, 2010. 2 Beber, Hillary. A Greener, Greater New York Presentation. Live Powerpoint presentation, Sustainability Speaker Series, NYU Schack Institute of Real Estate. March 23, 2010. 3 Rypkema, Donovan. Sustainability, Smart Growth and Historic Preservation. The HIstoric Districts Council Annual Conference in New York City. March 10, 2007.< http://www.preservation.org/rypkema.htm> Accessed March 5, 2010.

4

space ideal for a business seeking to both manufacture, sell, and finance a new technology. We decided to fill this gap and proceeded to develop the concept of the Gowanus Innovation Center. The Area The Gowanus neighborhood of Brooklyn straddles both sides of the Gowanus canal. Over time the neighborhood has evolved from corporate‐owned heavy industry to the current predominance of small, light manufacturing businesses. However, there are also some residentially zoned areas in the northwest and southeast, as well as numerous nonconforming housing units within the M1 to M3 zones that make up the majority of the existing zoning. Many of these are artist's lofts and live/work spaces.

Location of Site (Google Maps)

The area's infrastructure is strong. Transportation is accessible throughout the area, including the tunnel to Manhattan, expressways, subway lines and a nearby Long Island Railroad stop. The expressways in particular will allow for easy truck access to manufacturing facilities. Nearby, the Red Hook Container terminal and Brooklyn Piers provide access to freight shipping and have useable warehouses.4 The weakest aspect of the infrastructure is the sewer system, which combines stormwater and human waste in the same conduits. During heavy rains this combined sewer overflows at 11 points along the canal, making the water unsafe for swimming or fishing.5

4 Port Authority of NY and NJ, The Port Authority of NY & NJ Port Guide. <http://www.seaportsinfo.com/panynj/portfacilities/?page=redhook> Accessed March 5, 201. 5 Riverkeeper, Gowanus Canal: After 150 Years of Neglect Brooklyn's Lavendar Lake Must be Cleaned Up! <http://www.riverkeeper.org/wp‐content/uploads/2009/09/Gowanus_Fact_Sheet.pdf> Accessed March 5, 2010.

5

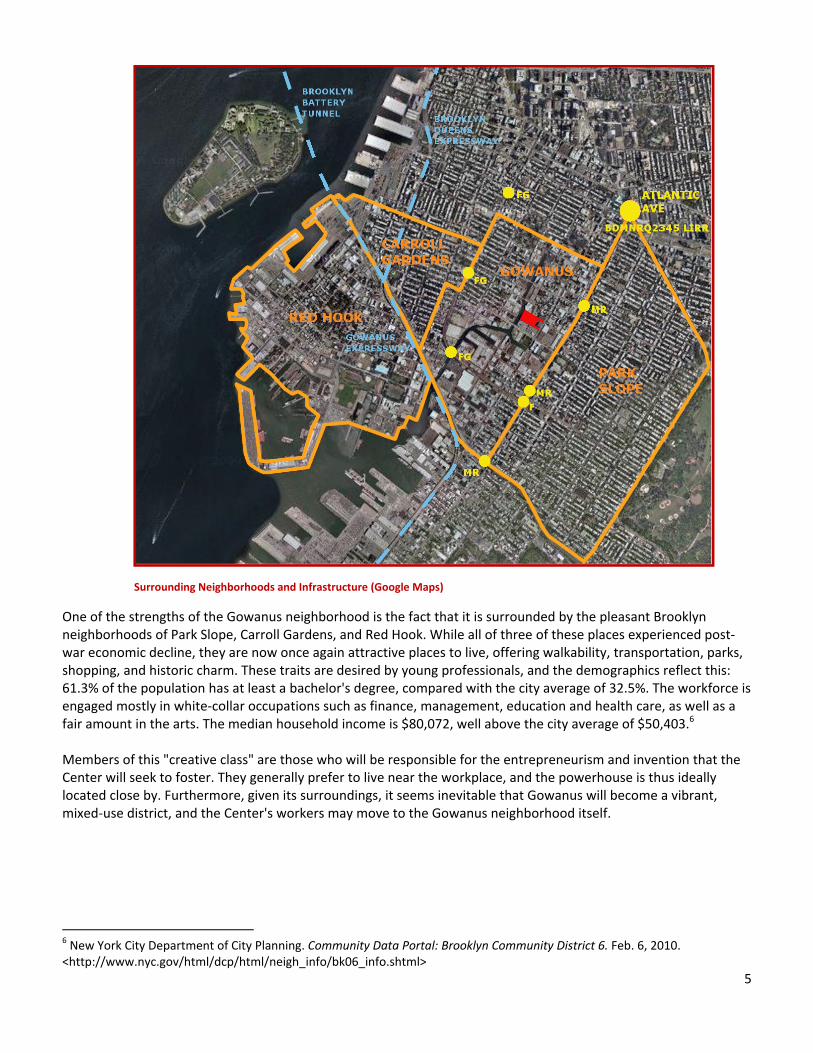

Surrounding Neighborhoods and Infrastructure (Google Maps)

One of the strengths of the Gowanus neighborhood is the fact that it is surrounded by the pleasant Brooklyn neighborhoods of Park Slope, Carroll Gardens, and Red Hook. While all of three of these places experienced post‐war economic decline, they are now once again attractive places to live, offering walkability, transportation, parks, shopping, and historic charm. These traits are desired by young professionals, and the demographics reflect this: 61.3% of the population has at least a bachelor's degree, compared with the city average of 32.5%. The workforce is engaged mostly in white‐collar occupations such as finance, management, education and health care, as well as a fair amount in the arts. The median household income is $80,072, well above the city average of $50,403.6 Members of this "creative class" are those who will be responsible for the entrepreneurism and invention that the Center will seek to foster. They generally prefer to live near the workplace, and the powerhouse is thus ideally located close by. Furthermore, given its surroundings, it seems inevitable that Gowanus will become a vibrant, mixed‐use district, and the Center's workers may move to the Gowanus neighborhood itself.

6 New York City Department of City Planning. Community Data Portal: Brooklyn Community District 6. Feb. 6, 2010. <http://www.nyc.gov/html/dcp/html/neigh_info/bk06_info.shtml>

6

The Canal

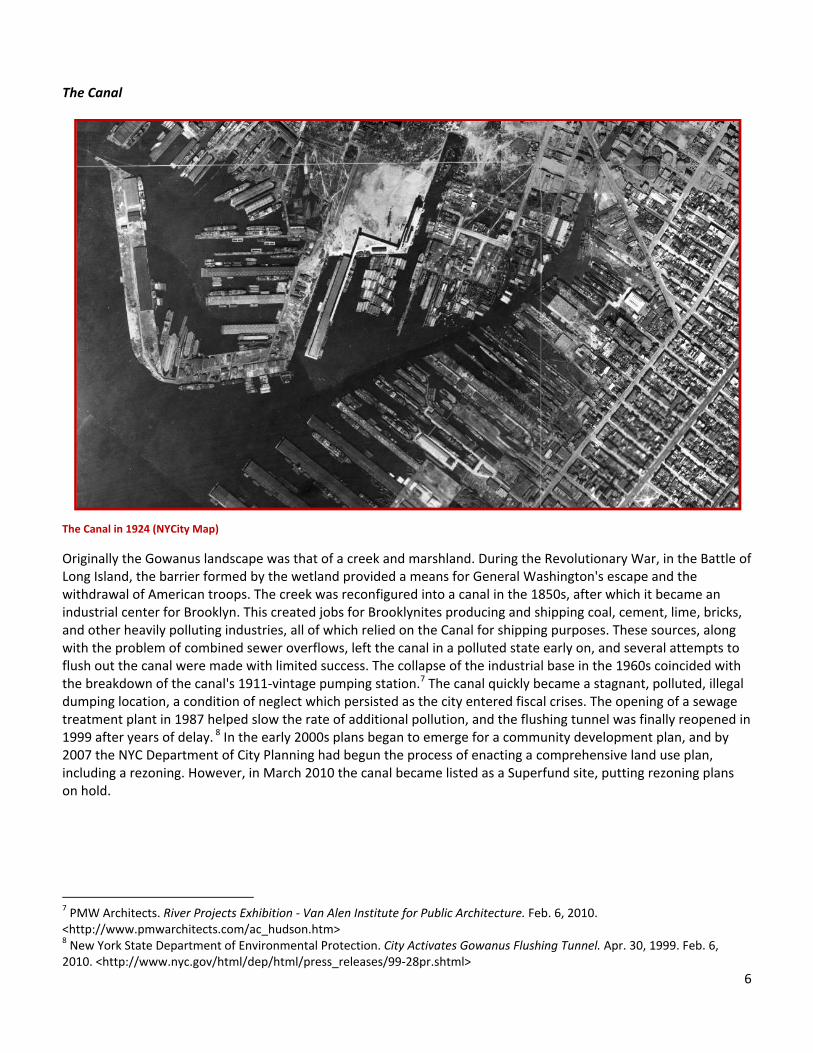

The Canal in 1924 (NYCity Map)

Originally the Gowanus landscape was that of a creek and marshland. During the Revolutionary War, in the Battle of Long Island, the barrier formed by the wetland provided a means for General Washington's escape and the withdrawal of American troops. The creek was reconfigured into a canal in the 1850s, after which it became an industrial center for Brooklyn. This created jobs for Brooklynites producing and shipping coal, cement, lime, bricks, and other heavily polluting industries, all of which relied on the Canal for shipping purposes. These sources, along with the problem of combined sewer overflows, left the canal in a polluted state early on, and several attempts to flush out the canal were made with limited success. The collapse of the industrial base in the 1960s coincided with the breakdown of the canal's 1911‐vintage pumping station.7 The canal quickly became a stagnant, polluted, illegal dumping location, a condition of neglect which persisted as the city entered fiscal crises. The opening of a sewage treatment plant in 1987 helped slow the rate of additional pollution, and the flushing tunnel was finally reopened in 1999 after years of delay. 8 In the early 2000s plans began to emerge for a community development plan, and by 2007 the NYC Department of City Planning had begun the process of enacting a comprehensive land use plan, including a rezoning. However, in March 2010 the canal became listed as a Superfund site, putting rezoning plans on hold.

7 PMW Architects. River Projects Exhibition ‐ Van Alen Institute for Public Architecture. Feb. 6, 2010. <http://www.pmwarchitects.com/ac_hudson.htm> 8 New York State Department of Environmental Protection. City Activates Gowanus Flushing Tunnel. Apr. 30, 1999. Feb. 6, 2010. <http://www.nyc.gov/html/dep/html/press_releases/99‐28pr.shtml>

7

The Site

Block 967, Lot 1 (Oasis City Map)

Site Facts Address: 153 2nd Avenue Lot Area: 108,722 Building Footprint: 17,500 Building Floor Area: 52,500 Year Built: 1931 Current Zoning: M2‐1 Current FAR: 2.0 Current Buildable Area: 217,444 Proposed Buildable Area: 374,004 Owner: AI Gowanus Village LLC (Africa Israel Investments) The site is located on the east bank of the Canal. It consists of landfill from the Canal's 1848 excavation. Early uses included a sulfur works, coal yard, and paper warehouse. By 1898 the property was home to a transit company powerhouse, a use that continued for some time. The majority of the lot is a rectangle abutting the waterway, but there are two extension aligning with 1st and 2nd streets, providing access to the site from 3rd Avenue. There is a city easement for a street crossing the site, however, the owner has a prescriptive use claim to this encumbrance.9 The lot was purchased in 2005 by a partnership between Shaya Boylmelgreen, a local Brooklyn developer, and Africa Israel, an international firm with investments in real estate, diamonds, chemicals, infrastructure and energy. The partnership dissolved in 2007 due to business disagreements between the partners, and Lot 1 was transferred entirely into the ownership of Africa Israel.10 The property was then placed the on the market in 2008 for $27 million. It is still on the market, and the price is now listed as "make an offer."11

9 Interview with Damien Stein, Africa Israel Investments. March 2, 2010. 10 Barr, Linda. Real Estate Bigs Announce Split: Leviev & Boymelgreen Divvy Up their Property. Real Estate Weekly. August 1, 2007. Accessed March 5, 2010. <http://www.allbusiness.com/operations/facilities‐commercial‐real‐estate/4507817‐1.html> 11 Collins, Linda. Boymelgreen's Gowanus Village Property For Sale at $27 Million. Brooklyn Daily Eagle. Feb. 25, 2008. Feb. 6, 2010. <http://www.brooklyneagle.com/categories/category.php?category_id=5&id=18747>

8

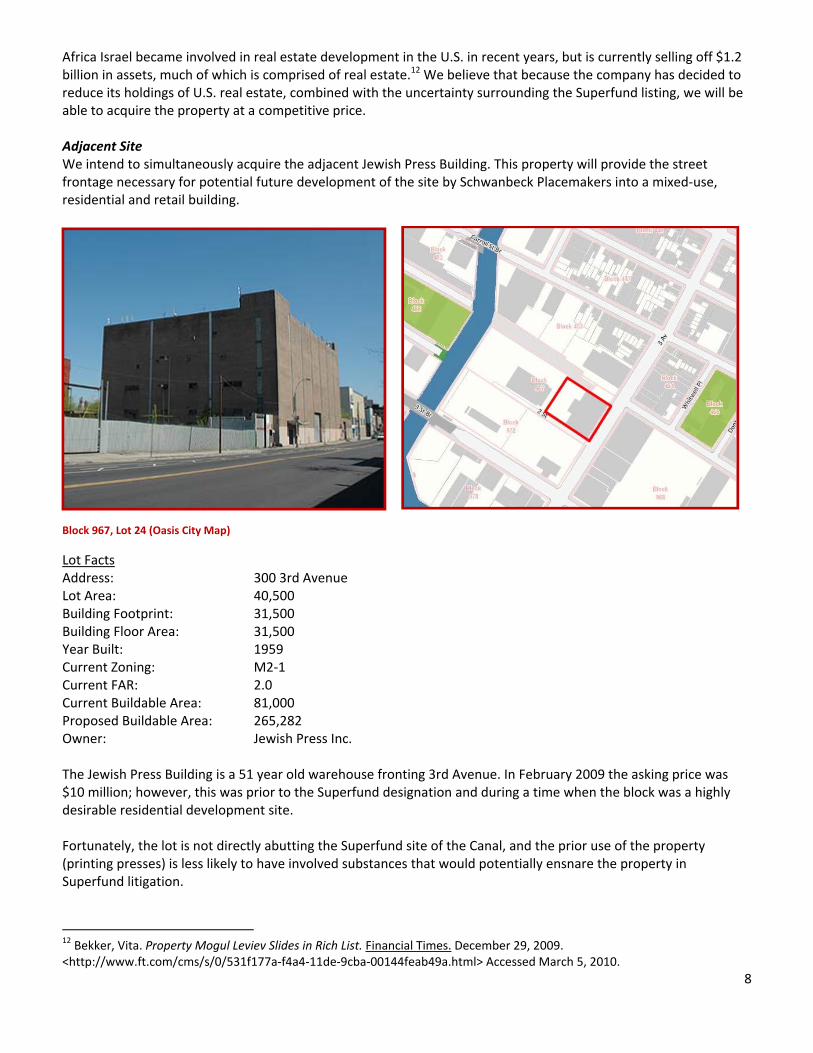

Africa Israel became involved in real estate development in the U.S. in recent years, but is currently selling off $1.2 billion in assets, much of which is comprised of real estate.12 We believe that because the company has decided to reduce its holdings of U.S. real estate, combined with the uncertainty surrounding the Superfund listing, we will be able to acquire the property at a competitive price. Adjacent Site We intend to simultaneously acquire the adjacent Jewish Press Building. This property will provide the street frontage necessary for potential future development of the site by Schwanbeck Placemakers into a mixed‐use, residential and retail building.

Block 967, Lot 24 (Oasis City Map)

Lot Facts Address: 300 3rd Avenue Lot Area: 40,500 Building Footprint: 31,500 Building Floor Area: 31,500 Year Built: 1959 Current Zoning: M2‐1 Current FAR: 2.0 Current Buildable Area: 81,000 Proposed Buildable Area: 265,282 Owner: Jewish Press Inc. The Jewish Press Building is a 51 year old warehouse fronting 3rd Avenue. In February 2009 the asking price was $10 million; however, this was prior to the Superfund designation and during a time when the block was a highly desirable residential development site. Fortunately, the lot is not directly abutting the Superfund site of the Canal, and the prior use of the property (printing presses) is less likely to have involved substances that would potentially ensnare the property in Superfund litigation.

12 Bekker, Vita. Property Mogul Leviev Slides in Rich List. Financial Times. December 29, 2009. <http://www.ft.com/cms/s/0/531f177a‐f4a4‐11de‐9cba‐00144feab49a.html> Accessed March 5, 2010.

9

Zoning The current zoning of the site is M2‐1. This designation allows a variety of light manufacturing activities as‐of‐right, including electronics, ceramics, furniture, and many other goods. It also allows eating and drinking establishments. The maximum height of a wall within 15 feet of the street line is 60 feet. From this height a building may rise at an angle of 5.6:1 from a wide street.

Proposed Zoning The site is centered within a comprehensive proposed rezoning area. The scheme is intended to meet several goals. One is to maintain manufacturing in the neighborhood, which is accomplished by preserving M2‐1 manufacturing zoning south of the site in an Industrial Business Zone, and creating new mixed‐use zones around the site, which would permit light industrial, commercial, retail, community facility, artist spaces, and housing. The powerhouse lies within one of these, named "MX Waterfront South".

13 This area will allow building heights of up to 125 feet in places contiguous with the Canal and a 33% FAR bonus for inclusionary housing. It will require connectivity of the street grid and a public waterfront esplanade with certain design requirements such as lighting and plantings. However, this rezoning plan has been put on hold due to the listing of the canal on the National Priorities List of the Superfund. It is described here in order to depict the future development potential of the site.

13 Gowanus Canal Corridor Framework. New York City Department of City Planning. Feb. 6,2008. < www.nyc.gov/html/dcp/html/gowanus/index.shtml>

10

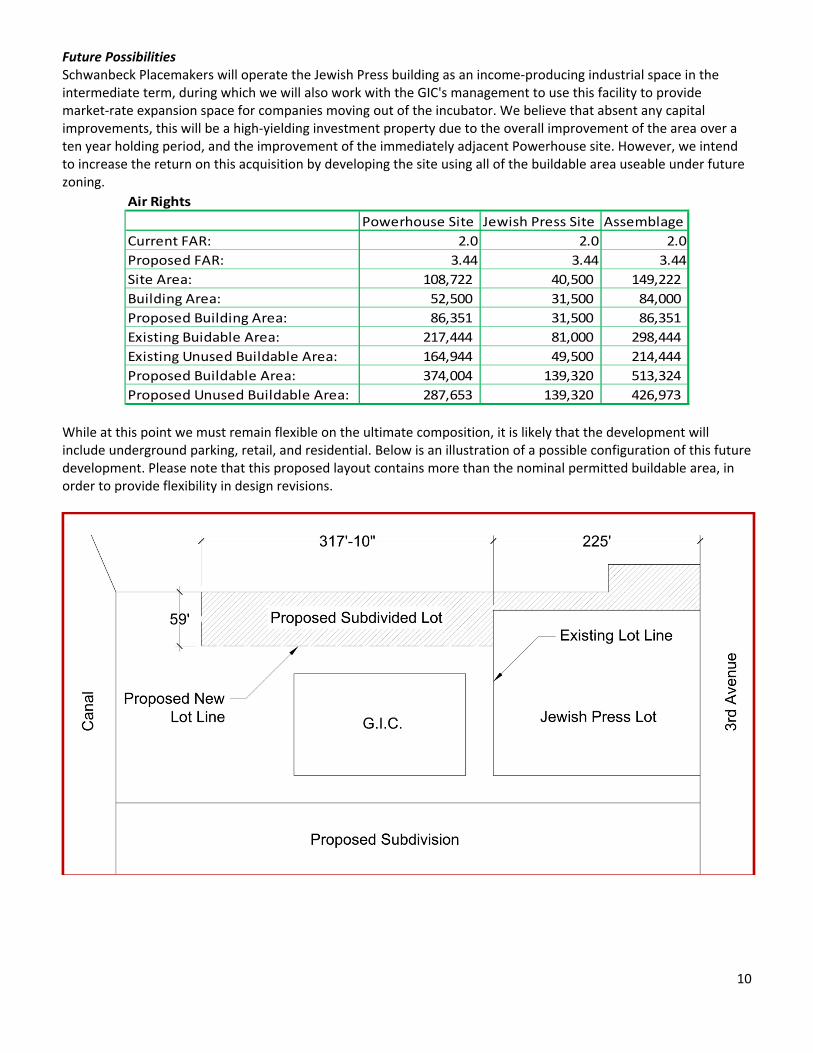

Future Possibilities Schwanbeck Placemakers will operate the Jewish Press building as an income‐producing industrial space in the intermediate term, during which we will also work with the GIC's management to use this facility to provide market‐rate expansion space for companies moving out of the incubator. We believe that absent any capital improvements, this will be a high‐yielding investment property due to the overall improvement of the area over a ten year holding period, and the improvement of the immediately adjacent Powerhouse site. However, we intend to increase the return on this acquisition by developing the site using all of the buildable area useable under future zoning.

Air Rights

Powerhouse Site Jewish Press Site Assemblage

Current FAR: 2.0 2.0 2.0

Proposed FAR: 3.44 3.44 3.44

Site Area: 108,722 40,500 149,222

Building Area: 52,500 31,500 84,000

Proposed Building Area: 86,351 31,500 86,351

Existing Buidable Area: 217,444 81,000 298,444

Existing Unused Buildable Area: 164,944 49,500 214,444

Proposed Buildable Area: 374,004 139,320 513,324

Proposed Unused Buildable Area: 287,653 139,320 426,973 While at this point we must remain flexible on the ultimate composition, it is likely that the development will include underground parking, retail, and residential. Below is an illustration of a possible configuration of this future development. Please note that this proposed layout contains more than the nominal permitted buildable area, in order to provide flexibility in design revisions.

11

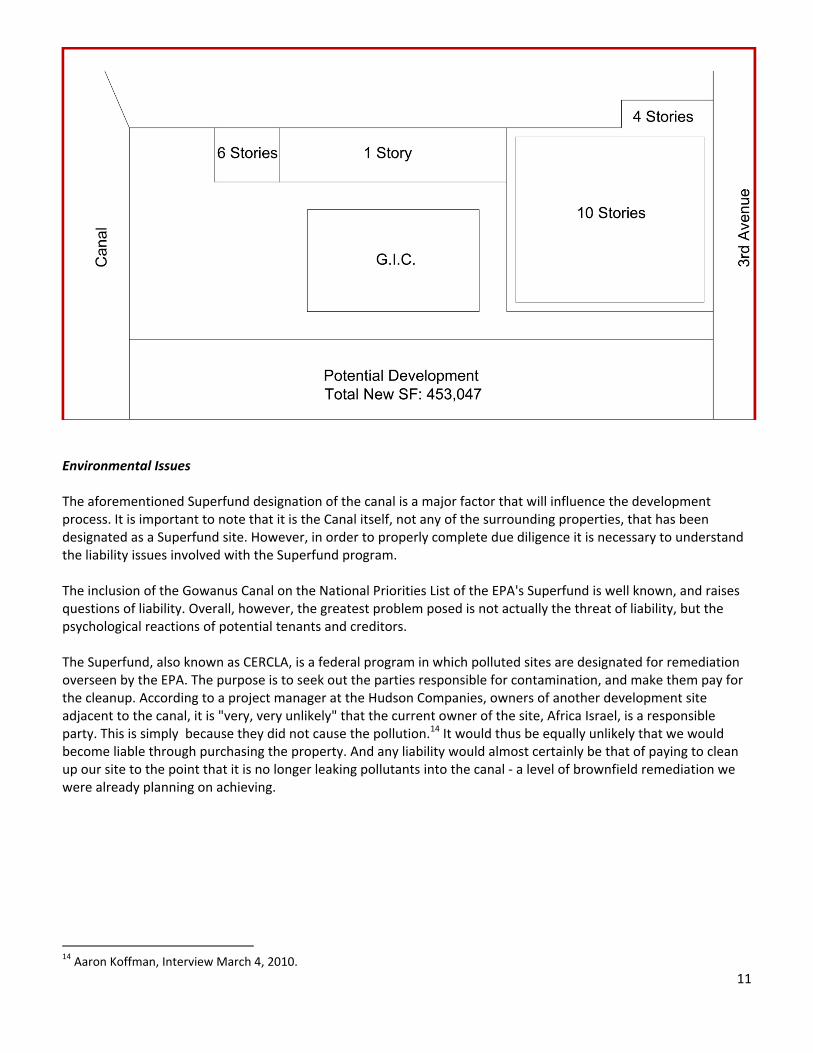

Environmental Issues The aforementioned Superfund designation of the canal is a major factor that will influence the development process. It is important to note that it is the Canal itself, not any of the surrounding properties, that has been designated as a Superfund site. However, in order to properly complete due diligence it is necessary to understand the liability issues involved with the Superfund program. The inclusion of the Gowanus Canal on the National Priorities List of the EPA's Superfund is well known, and raises questions of liability. Overall, however, the greatest problem posed is not actually the threat of liability, but the psychological reactions of potential tenants and creditors. The Superfund, also known as CERCLA, is a federal program in which polluted sites are designated for remediation overseen by the EPA. The purpose is to seek out the parties responsible for contamination, and make them pay for the cleanup. According to a project manager at the Hudson Companies, owners of another development site adjacent to the canal, it is "very, very unlikely" that the current owner of the site, Africa Israel, is a responsible party. This is simply because they did not cause the pollution.14 It would thus be equally unlikely that we would become liable through purchasing the property. And any liability would almost certainly be that of paying to clean up our site to the point that it is no longer leaking pollutants into the canal ‐ a level of brownfield remediation we were already planning on achieving.

14 Aaron Koffman, Interview March 4, 2010.

12

Canal in April 2010, Showing Evidence of EPA Study Activities

The soil is contaminated with a wide variety of chemicals resulting from the use of the property as a power plant, including the byproducts of burning coal, and electrical devices containing PCBs. There is also an abandoned oil storage tank on the site. Much of the soil will essentially need to be excavated and removed for offsite treatment. A Phase 2 ESA of the site estimated cleanup costs at $1.375 million. There are several methods through which one may purchase a site and be protected from Superfund liability. However, inevitably this drives up the cost of acquisition through insurance premiums, or the original seller demanding extra compensation for continuing to bear liability. The common lesson in these options is that it is important to work with the EPA to undertake a remediation plan that prevents any further waterway pollution. While some potential tenants may be hesitant to lease space next to a Superfund site, we hope that the attractive rents will be enough to overcome this psychological barrier. Furthermore, the transformation of the surrounding grounds into a state‐of‐the‐art environmentally sustainable park should make a statement that the canal is becoming a clean, healthy environment. The timeframe for Superfund sites has determined the long‐term approach we have taken towards developing the adjacent site. Unfortunately, the process of completing remediation of an NPL‐listed site is a long one. The EPA is currently conducting studies on the level of hazard in the canal, a process that will be completed in late 2010. Then a feasibility study will be conducted on the best remediation procedures, expected to be finished in late 2011. The remediation itself will not begin until 2012.15 This directly affects the rezoning plan. A conversation with city

15 Bush, Daniel. EPA Starts Phase One Work at Gowanus. Brooklyn Downtown Star. Dec. 9, 2009. Feb. 6, 2010. <http://brooklyndowntownstar.com/pages/full_story/push?article‐EPA+starts+phase+one+work+at+Gowanus%20&id=5061948E‐PA+starts+phase+one+work+at+Gowanus&instance=home_news_bullets>

13

planner Jen Posner indicated that the rezoning is postponed indefinitely until the Department of City Planning has "a better idea of what's going on." It is not necessary for the Canal to become removed from the NPL list prior to rezoning, but we will not expect the neighborhood to substantially transform until the remediation is well on its way to completion. A 1997 study by the GAO found that the average time from listing on the NPL to completion of remediation on a Superfund site was approximately 8 years.16 However, since then there has been a push towards early settlements and clarifications in the law in an effort to shorten this time.17 There remains a danger that the Superfund cleanup process can literally take decades. Duwamish River in Seattle, for instance, was added to the NPL in 2001 with the goal of remediating the site by 2020 ‐ a deadline that it appears will not be met.18 However, there are other examples of more successful cleanups. The Eastland Wollen Mill in Corinna Maine, for example, was added to the NPL in 1999 and has since been developed into a senior housing facility.19 It is also significant that the Hudson Companies intends to push through its development of Gowanus Green, with city support. Ultimately, the value of our investment in adjacent property and development rights is difficult to determine, but we believe it is a risk well worth taking, which others have overlooked due to an inaccurate assessment of the risk.

16 GAO, Superfund: Duration of the Cleanup Process at Hazardous Waste Sites on the National Priorities List. Sep. 24, 1997. Feb. 6, 2010. <http://archive.gao.gov/paprpdf1/159390.pdf> 17 GAO, Superfund: Litigation Has Decreased and EPA Needs Better Information on Site Cleanup and Cost Issues to Estimate Future Program Funding Requirements. July 2009. Feb. 6, 2010. <http://www.gao.gov/new.items/d09656.pdf> 18 Shay, Steve. Hope, Hard Work Ahead for Duwamish River Cleanup Effort. West Seattle Herald. May 16, 2009. Feb. 6, 2010. <http://www.westseattleherald.com/2009/05/15/news/hope‐hard‐work‐ahead‐duwamish‐river‐cleanup‐effort> 19 EPA, Celebrating 10 Years of Returning Superfund Sites to Beneficial Use. November 2009. Feb. 6, 2010. <http://www.epa.gov/superfund/programs/recycle/pdf/eastlandwoolenmill10yr.pdf>

14

The Building

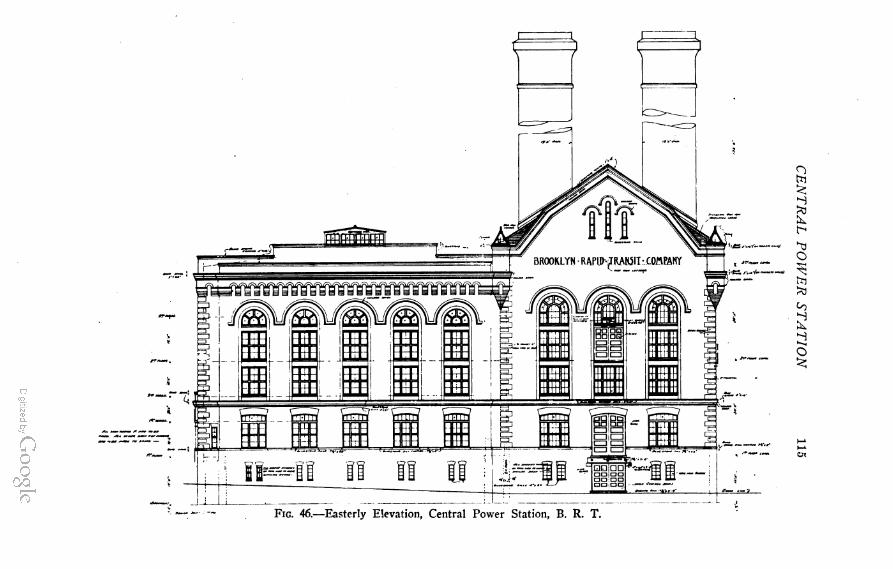

The Powerhouse was designed by Thomas E. Murray, an architect who designed power facilities for the Brooklyn Rapid Transit company. It was constructed in 1904.20 The building is 187 by 111 feet and 70 feet tall, constructed of a steel frame with self‐supporting masonry walls. Originally it had only one floor with an atrium clear through to the roof, bound by three narrow mezzanines at the perimeter. This provided space for the original use, a coal‐burning power plant which supplied energy for street car service along Brooklyn's avenues. The foundation is a concrete slab, up to 15.4 feet thick in some locations. This foundation incorporates a pair of tunnels used for transporting coal from an adjoining yard. Two infill floors were added at some point, using a non‐conventional steel framing structure with concrete deck topping. The windows provide ample natural lighting and views around the perimeter. The interior is mostly wide open and suitable for a very flexible variety of layouts. There are some small metal stairs in the corner that will need to be replaced with modern, fire protected stairwells. The roof is nearly completely destroyed and will need to be replaced. There are clerestory windows around a section of the roof that pops out above the rest. The condition the Powerhouse's walls is "remarkably good," although the parapets will require some reconstruction. However, the interior columns and foundations will require replacement if new floors are to be added. 21

20Weiss, Mike. Gowanus Archeologist: Historic Finds in Murky Waters? Brooklyn Daily Eagle. April 7, 2010. <http://www.brooklyneagle.com/categories/category.php?category_id=31&id=34647> Accessed April 26, 2010. 21 Engineering Report, Accessed at Africa‐Israel Investments Offices.

15

3rd Floor Interior, Showing Mezzanine and Natural Lighting

3rd Floor Clerestory

16

View of Brooklyn

1st Floor Interior Showing Steel Structure

17

st Floor Interior Showing Second Floor Decking Assembly

Existing Stairwell Visible in Corner

18

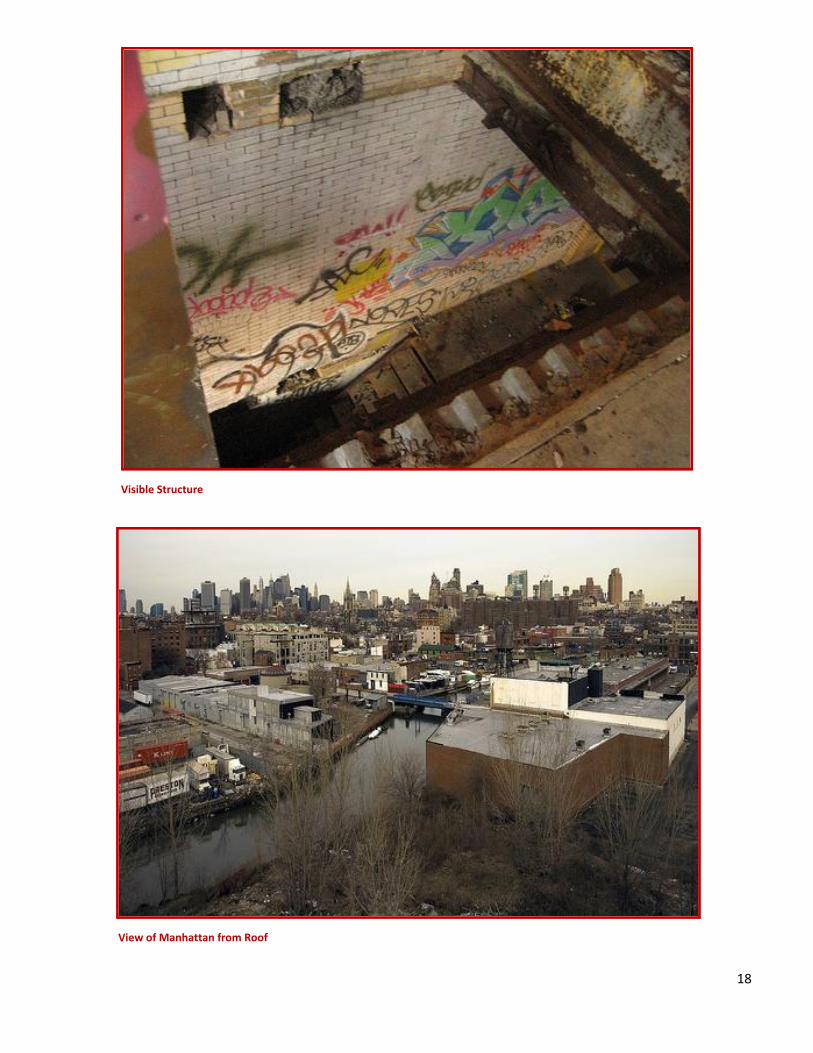

Visible Structure

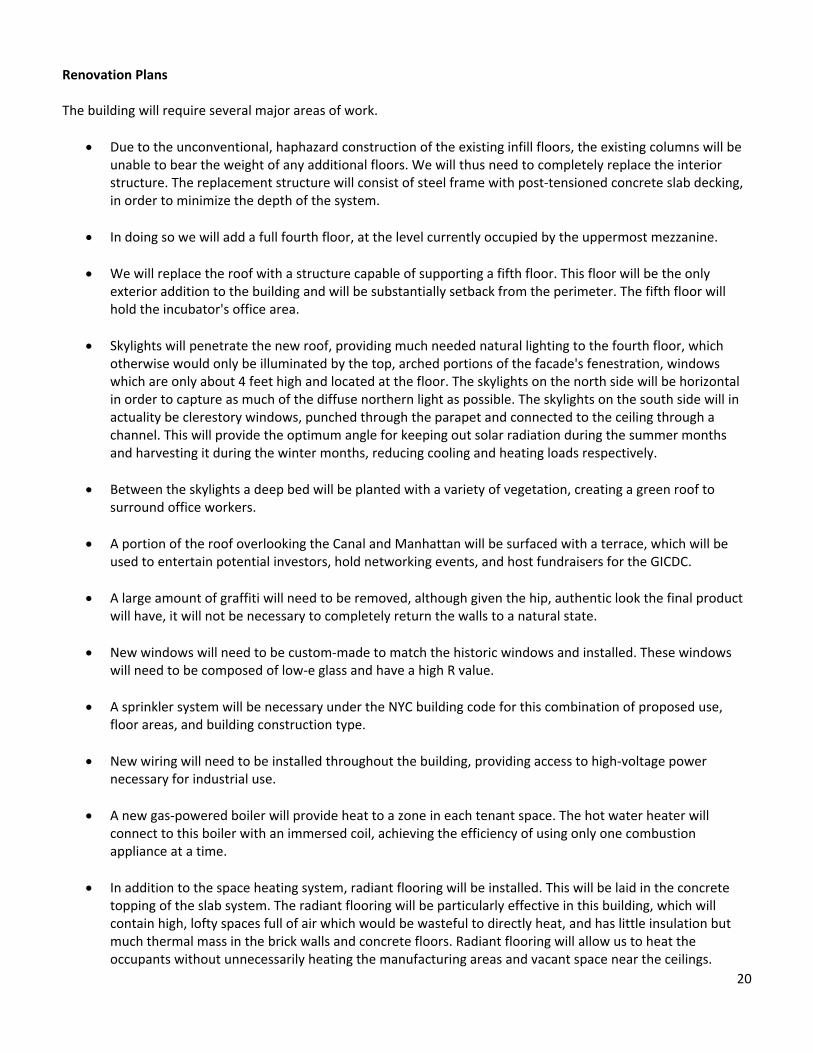

View of Manhattan from Roof

19

Exterior Details (This and All Previous Photos: Flickr)

20

Renovation Plans The building will require several major areas of work.

Due to the unconventional, haphazard construction of the existing infill floors, the existing columns will be unable to bear the weight of any additional floors. We will thus need to completely replace the interior structure. The replacement structure will consist of steel frame with post‐tensioned concrete slab decking, in order to minimize the depth of the system.

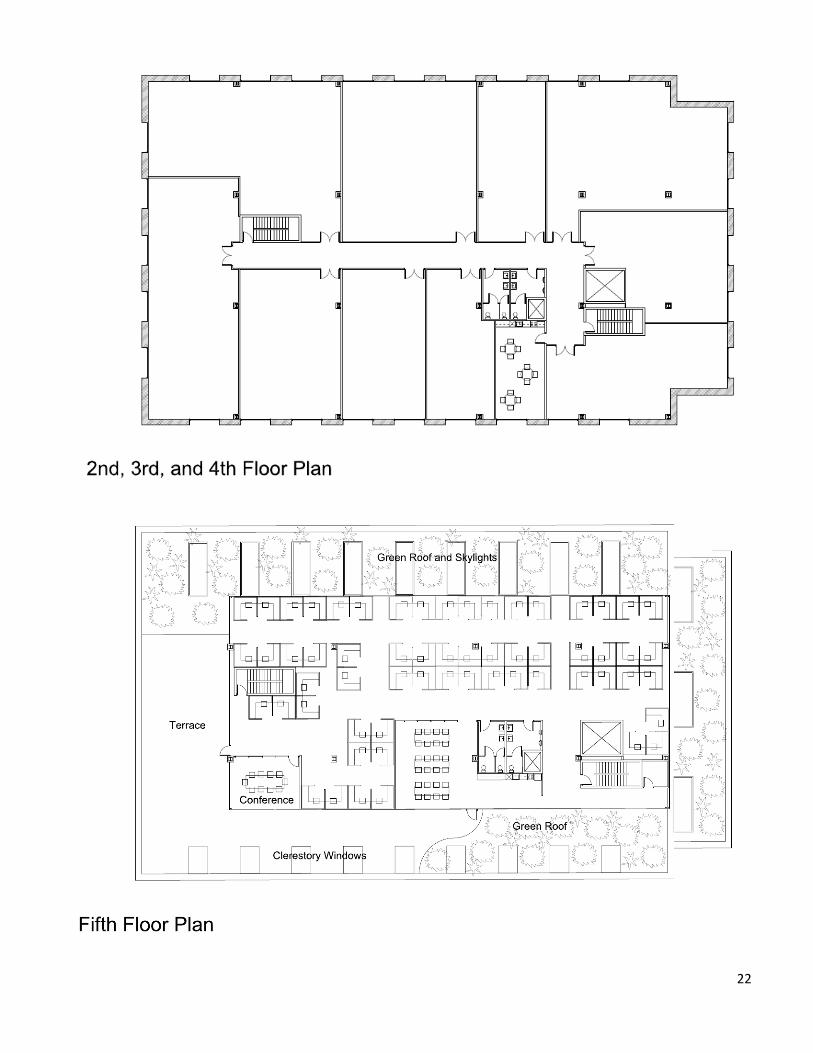

In doing so we will add a full fourth floor, at the level currently occupied by the uppermost mezzanine.

We will replace the roof with a structure capable of supporting a fifth floor. This floor will be the only exterior addition to the building and will be substantially setback from the perimeter. The fifth floor will hold the incubator's office area.

Skylights will penetrate the new roof, providing much needed natural lighting to the fourth floor, which otherwise would only be illuminated by the top, arched portions of the facade's fenestration, windows which are only about 4 feet high and located at the floor. The skylights on the north side will be horizontal in order to capture as much of the diffuse northern light as possible. The skylights on the south side will in actuality be clerestory windows, punched through the parapet and connected to the ceiling through a channel. This will provide the optimum angle for keeping out solar radiation during the summer months and harvesting it during the winter months, reducing cooling and heating loads respectively.

Between the skylights a deep bed will be planted with a variety of vegetation, creating a green roof to surround office workers.

A portion of the roof overlooking the Canal and Manhattan will be surfaced with a terrace, which will be used to entertain potential investors, hold networking events, and host fundraisers for the GICDC.

A large amount of graffiti will need to be removed, although given the hip, authentic look the final product will have, it will not be necessary to completely return the walls to a natural state.

New windows will need to be custom‐made to match the historic windows and installed. These windows will need to be composed of low‐e glass and have a high R value.

A sprinkler system will be necessary under the NYC building code for this combination of proposed use, floor areas, and building construction type.

New wiring will need to be installed throughout the building, providing access to high‐voltage power necessary for industrial use.

A new gas‐powered boiler will provide heat to a zone in each tenant space. The hot water heater will connect to this boiler with an immersed coil, achieving the efficiency of using only one combustion appliance at a time.

In addition to the space heating system, radiant flooring will be installed. This will be laid in the concrete topping of the slab system. The radiant flooring will be particularly effective in this building, which will contain high, lofty spaces full of air which would be wasteful to directly heat, and has little insulation but much thermal mass in the brick walls and concrete floors. Radiant flooring will allow us to heat the occupants without unnecessarily heating the manufacturing areas and vacant space near the ceilings.

21

A solar thermal system will be installed on the roof of the fifth floor, taking advantage of the ample sunlight enjoyed by the tall building. The system will be able to directly convert the sun's energy into hot water useable in the radiant flooring.

Rainwater will be collected from the roof and stored on‐site in a cistern for use in landscaping irrigation.

Wireless access will be provided throughout the building.

Steel stud and gypsum board walls will be built to partition the individual tenants' manufacturing spaces. Because tenants will be start‐ups and there will likely be much turnover, only the most minimal of finishes will be used.

A small kitchen and break room will be provided on each floor, as well as male and female restrooms.

A garage and unloading space will be build out with a new overhead door entrance on the ground floor, to provide one major tenant the ability to run modest shipping operations.

A lobby will be created to welcome visitors, and a desk will be built in for the 24‐hour security guard.

A new doorway and storefront assemblage will be installed on the west side of the building, opening out onto the sponge park.

Design Development Drawings

22

23

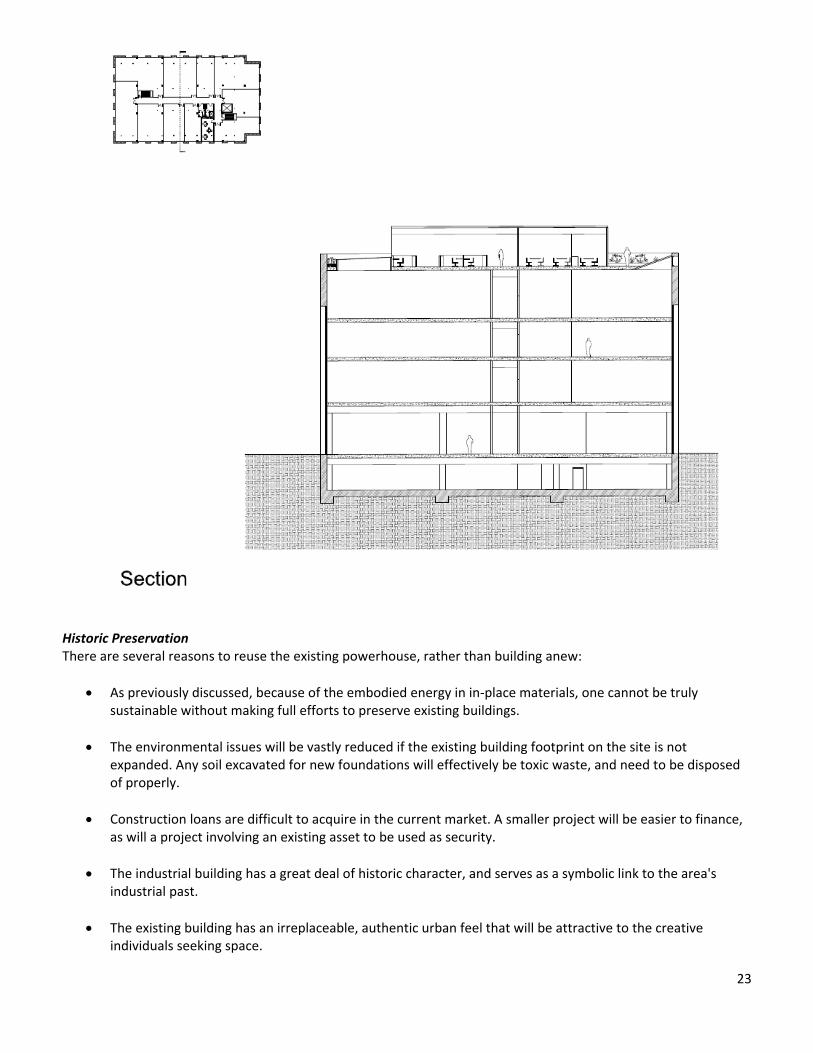

Historic Preservation There are several reasons to reuse the existing powerhouse, rather than building anew:

As previously discussed, because of the embodied energy in in‐place materials, one cannot be truly sustainable without making full efforts to preserve existing buildings.

The environmental issues will be vastly reduced if the existing building footprint on the site is not expanded. Any soil excavated for new foundations will effectively be toxic waste, and need to be disposed of properly.

Construction loans are difficult to acquire in the current market. A smaller project will be easier to finance, as will a project involving an existing asset to be used as security.

The industrial building has a great deal of historic character, and serves as a symbolic link to the area's industrial past.

The existing building has an irreplaceable, authentic urban feel that will be attractive to the creative individuals seeking space.

24

Local residents who are hesitant about their neighborhood undergoing changes will be reassured by our maintaining this local landmark.

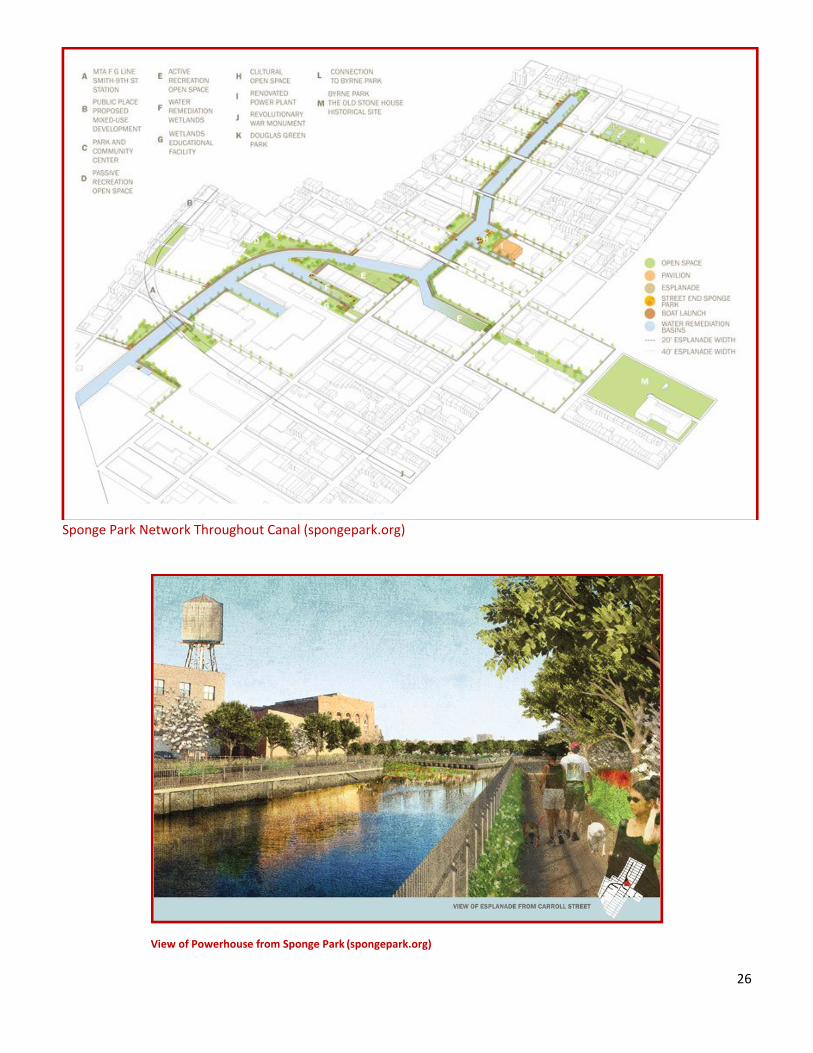

Landscaping Gowanus is lacking a major asset enjoyed by its neighbors, that of parks. If the area is to reach its full potential as a mixed‐use neighborhood, it will require more parks and open space. The rezoning plan attempts to address this by requiring esplanades on the canal banks, and public access along the 1st and 2nd street corridors. While not yet required to incorporate these features, we would like to take advantage of the principle, as well as the ample unimproved land our lot contains, in order to draw in the public and increase performance of the retail component. We would also like to address the Gowanus Canal's ecological significance by developing the landscape in a responsible way. While years of abuse have rendered the Canal ecologically exhausted, if it is cleaned up it can once again become home to an estuarine ecosystem. "Saltwater marshes are the most biologically productive lands on the earth, producing twice the biomass of our most fertile hayfields."22 The fostering of a habitable environment for fish, plants, and other species along and within the canal is thus disproportionately important to the nation's natural resources. A local architect has proposed a "Sponge Park" along the banks of the canal, which would retain and filter rainwater during heavy rainfall, thus preventing overflows of the combined sewer system and reducing pollution of the canal. Plants will also increase the oxygen content of the water, improving the habitat for aquatic wildlife. The park will furthermore provide an amenity to the neighborhood, which is currently lacking in green space. This park recently received $300,000 in federal funding to build one block.23

22 Juergensmeyer, Julian. and Thomas Roberts. Land Use, Planning, and Development Regulation Law. U.S.: Thomson/West, 2007. p 524. 23 Mclaughlin, Mike. The Gowanus is 'Sponge' worthy! The Brooklyn Paper. July 29, 2009. Feb. 6, 2010. <http://www.brooklynpaper.com/stories/32/26/32_26_mm_sponge_park.html>

25

Sponge Park Diagram24

24 spongepark.org

26

Sponge Park Network Throughout Canal (spongepark.org)

View of Powerhouse from Sponge Park (spongepark.org)

27

Schwanbeck Placemakers plans to incorporate this concept into the Gowanus Innovation Center's open space. While we will retain ownership of the site, we will grant to the City an easement over a portion of the site abutting the waterfront in exchange for the City funding the costs of developing the sponge park landscape (other than remediation costs, which we expect to bear ourselves.) This area will include all major features of the design such as water basins and aquatic plants abutting the Canal. The portion of the Powerhouse site not affected by the easement will be set aside for hardscaping and seating for use by the both the Center's workers and the public. It will be paved with porous materials. Marketing and Operations Once constructed, the success of the development will be inextricably tied to the creation and operation of the non‐profit Gowanus Innovation Center Development Corporation, which will be responsible for marketing the center, selecting tenants, providing startup support, and property management. Creation The GICDC must register with the New York Department of State as a non‐profit, and with the IRS as a 501(c)(3) tax‐exempt organization. Filing at the state level requires completing a document named the Articles of Incorporation, the purpose of which is to define the non‐profit's purpose and activities. It is also considered wise to create a set of bylaws for internal use in the organization, defining the specifics of operations. The IRS filing process typically takes 9 months to a year, but can take as little as 3 to 6 months if the application is first sent to one's congressional representative requesting assistance in expediting the process.25 Purpose The Articles of Incorporation will contain the following language: The GICDC is organized exclusively for educational and charitable purposes within the meaning of section 501(c)(3) of the Internal Revenue Code of 1986. This organization is organized not for profit, and no part of the net earnings of this corporation shall inure to the benefit of any member of the Board of Directors. This corporation is organized primarily for the following purposes: To publicize and spread knowledge of the center, for the purpose of attracting qualified tenants. To select as tenants new business enterprises that will:

‐ Further the development of environmentally sustainable and energy efficient technology in New York City. ‐ Create quality jobs for New York City's residents. ‐ Enjoy long term business success.

To provide support for tenants in the form of technical business assistance and connections to local businesses and investors. To competently manage the Center's real estate. To ensure long term stability of the Center's finances. To raise funds when necessary to provide for future capital projects.

25 Tug Hill Commission, Forming a Not‐for‐Profit Corporation in New York State October, 2000. <http://www.tughill.org/Technical%20&%20Issue%20Papers/WEBPAGE‐technical‐issue‐papers/2000%20Forming%20a%20not‐for‐profit%20pdf%20FILE.pdf> Accessed April 10, 2010.

28

Marketing The low vacancy rates in comparable incubators and below‐market industrial space indicates that there will be more applicants for the facility than there will be space available. Nevertheless, we must first reach out to this market. A Pennsylvania State survey of business incubators listed the top nine marketing approached by order of success:

Informal external network (word of mouth)

Affiliated agency/center referral

Current tenant referrals

Public speaking

Mass media

Brochures/pamphlets

Newspaper classified

Radio advertising

Television26

In the interest of conserving funds for operations usage, we will take the approach of principally using the first four of these, as well as the internet. New York’s community of green industry professionals is still seemingly small, and the management of Schwanbeck Placemakers frequently and repeatedly comes into contact with the same prominent business and government leaders in this area. Word will likely spread rapidly through this connected and supportive community. Current tenants will also become part of this green community and will assist in the networking required for attracting the next wave of tenants. GICDC will also certainly have continuing relationships with the city’s other incubators. It is important to use these connections to reach out to as many investors as possible. Because the Center will be providing a type of space that is in between the industrial and office extremes of some other incubators, it is likely that some tenants who contact another incubator will find out that their offerings are not quite right for the proposed business, but they will be referred to the Gowanus Innovation Center if our unique facility and location suit their needs. The Center will also likely be the subject of presentations in non‐profit, real estate development, environmental, and other sectors. For example, we first learned of the GMDC’s 221 McKibbin Street project at a large conference on New Market Tax Credits hosted by the EDC. These types of public speaking events will be of great value in spreading the word, and both Schwanbeck Placemakers and the GICDC will be available for as many as possible. We will also seek to generate free publicity by virtue of the Center’s location – we will reach out to members of the press and ensure that the project receives the recognition it deserves for spearheading development in the neglected Gowanus neighborhood, despite the well‐publicized Superfund listing. Major newspapers have written articles about newly developed incubator facilities in the past. Having contributed to the project, it will be in the interest of the municipal government to promote the facility as a wise, job‐generating use of taxpayers’ dollars through press releases and speeches. We will ask Mayor Bloomberg, Borough President Markowitz, and City Councilman Lander to join us in a press conference held on the landmark Carroll Street Bridge crossing the canal, with our building standing in the background and large architects' renderings of the proposed project prominently displayed for comparison. The internet has been used to market other incubators and will likewise be incorporated into our strategy. We will also host several events at the center prior to opening in order to spread the word. We will take advantage of our

26 Woods, Mike et. al. Small Business Incubators: Potential Local Economic Development Tools Oklahoma Cooperative Extension Service <http://pods.dasnr.okstate.edu/docushare/dsweb/Get/Document‐1610/F‐905web.pdf> Accessed March 31, 2010.

29

rooftop space for these events. We will attempt to have them included in the Climate Week agenda, which typically occurs in September. We will also take advantage of the physical nature of the property, specifically the fact that it is one of the highest structures in the neighborhood. Most residents of this area of Brooklyn recognize the building. Where graffiti now adorns the uppermost exterior surfaces of the powerhouse, we will install a new sign visible from a long distance, including traffic traveling on the expressways. Closer up, a smaller sign at the entrance to the property will list the individual tenants, assisting in the goal of marketing new startups. In addition, we will have a web presence that will include both a listing of current tenants and links to their own websites, and a downloadable application for interested startups. All these methods of publicity will be combined to generate a large pool of qualified applicants, at a minimal cost. Tenant Selection The tenants will be selected not through a traditional real estate process, but through a venture capital approach. In order to support the goals of the GICDC, tenants will be selected based on the relevance of their business to furthering sustainability industries in New York, job generation, and the likelihood of their long term success as a business concern. The application will ask prospective tenants to describe the product they plan to offer, and the impact its adoption in the marketplace will make on energy use, resource consumption, reduction in pollution, preservation of natural habitats, or any other environmentally important result. The application will include a questionnaire asking tenants to explain how the product fills a need in the marketplace, describe the target market, and identify the main competitors. The questionnaire will also ask how the company plans to achieve and maintain an edge over these competitors, and how they intend to secure their intellectual property. Applicants will be required to produce evidence of interest from potential investors and possibly clients. Finally, applicants will be asked to produce cash flow projections indicating all revenue including capital contributions and grants, as well as all expenses, over a period of two to three years. The GICDC management will then evaluate applications essentially using the SWOT analysis. The decisions will be made by balancing the contribution to the aforementioned three central criteria. Startup Support The less time tenants spend tracking down incentives and dealing with accounting, law, insurance, permits, and other technical issues, the more time they will have to develop and market their products and services, and the greater chance they will have for long‐term success. The GICDC will therefore guide startups through these processes. This will include assistance in financial modeling and planning, identifying venture capital investors, and helping to negotiate any agreements relating to such investments. By maintaining relationships with other incubators and academic research centers, the GICDC will provide access to advisors, concurrent research, and potentially students seeking internships. The GICDC will also seek to create synergies among tenants. Hosting rooftop happy hours, excursions to tour green facilities, and group attendance of relevant speaker events will be beneficial for businesses that are in both the same overall sector and the same early phase of life.

30

Property Management While the GICDC will have a contract with a property management company, this will be for mainly for technical issues and emergency repairs for which staff who are not professional property managers would not be sufficiently knowledgeable. Other, more managerial tasks will be undertaken by the GICDC management itself. This is because as a non‐profit it must be cost‐conscious, and the below market rents will be insufficient when compensation is based on a percentage of gross. These activities will include:

Bookkeeping. This will include computerized records of rent rolls, receipts, bill payments, maintenance costs, and other expenses. Records will be kept in such a way that accountants will be able to easily assemble audited statements. Of course, a hard copy of every receipt will also be retained for records.

Collection of rent.

Payment of bills.

Payment of property taxes.

Payment of insurance premiums.

Maintenance supervision. The GICDC will be vigilant and hands‐on in ensuring that janitorial, pest control, and HVAC and elevator maintenance is attended to. It will also plan for major capital expenditures such as roof replacements and replacement of broken equipment.

Security. This is important at any major industrial site in order to prevent theft of valuable materials and vandalism, as well as provide people who work late a sense of safety. This will be provided by hiring an outside firm, which will provide a security guard 24/7.

Parking. The management will be responsible for negotiating and securing adequate parking space in the adjacent lots.

A professional management firm will be retained in a limited capacity for advising on highly technical or complex capital expenditures, and emergency maintenance. Turnover One of the difficult issues in management will be space planning. As tenants grow, they will require different space needs, and will eventually reach the point where it is more appropriate for them to seek larger‐scale, market‐rate space, and their previous space will be left vacant. The design of the building is intended to mitigate this turnover issue. The top floor of the incubator is dedicated exclusively to offices, and, like other office space incubators, will consist of a large number of state‐of‐the‐art work stations, allowing businesses to expand and take over other work stations as necessary. The second and third floors will have a variety of sizes of industrial spaces, increasing the ability of management to accommodate a firm expanding production. Of course not all manufacturing processes can easily be transferred, but it will be easier to facilitate the transfer of machinery from one space to another when the businesses involved fall under the light manufacturing category that the Center will target. The finishes will also be kept raw in order to minimize the amount of repainting that needs to occur between leases. Finally, the ground floor, with its truck access, will have by far the largest spaces, and will allow businesses that reach a greater level of production to remain for several more years in the incubator. The incubator will expect to carry a greater vacancy rate than other properties for the purpose of allowing firms to grow as needed to a certain extent. Retaining businesses in the area will be important in serving the local economic development goal of the Center. To this extent we have connected with the Gowanus Canal Community Development Corporation, which is currently planning to develop other spaces in the neighborhood to attract green businesses under the working title "Brooklyn Enterprise Lab." While these plans are in the early stages, we expect to work with the GCCDC to place maturing tenants in more permanent, larger scale facilities along the Canal. The adjacent property on 3rd avenue, to be acquired by Schwanbeck Placemakers in an independent transaction, may also provide an easily accessible option that is still directly adjacent to the center. We also expect the benefits of localized tax abatements for industrial

31

businesses, including those related to capital costs in building out facilities in newly leased space, to assist in retaining businesses in Gowanus. By using our relationships and incentives to direct firms to spaces in the area, we will not only save them time and money on taxes and brokerage commissions, but will also germinate a new "green manufacturing district" along the Canal. The urban phenomenon of industry‐specific neighborhoods characterizes much of New York, and is evident in examples such as the Diamond District and the Garment District. This pattern in which firms cluster together to share in the mutual benefits of physical proximity will eventually be repeated once again in the Gowanus neighborhood. This will further benefit the Center and over time will increase the value of air rights and other properties owned by Schwanbeck Placemakers. Financial Management Schwanbeck Placemakers has learned through experience the importance of a non‐profit minding their finances appropriately. One non‐profit client had spent years operating at a deficit and relying on last‐minute donations to stay afloat. This did not negatively affect their day to day activities, but when the time came to sell their existing headquarters and create a new center in an existing historic building, requiring a bridge loan, banks looked first at the financial statements and were extremely hesitant to lend. It is thus very important to maintain a professional financial situation for both known and unforeseeable reasons. GICDC will thus ensure that the budget is balanced at the end of the year, relying on rental income alone. Debt service will be paid on schedule. Fundraising will be undertaken when planning for any future expansion projects. Market Feasibility Overall Industrial Market While this area has seen some influx of residents in recent years, it remains mainly industrial in character, and the city has committed to preserving the southern portion as non‐residential zoning.27 While the area at one time lost many manufacturing jobs, there has been much reinvestment in the area, and since 1997 the number of firms in Gowanus has grown 25%. The total number of industrial jobs in the neighborhood is 3,000.28 New York City as a whole still has a strong industrial sector, accounting for 500,000 jobs or 15% of employment. 29 100,000 of these are in manufacturing.30 It is especially significant in providing employment for minorities, individuals with limited education, and those with limited English proficiency. These jobs are typically better paying than service sector jobs for similar skill levels, and businesses are more frequently owned by local entrepreneurs.31

For these reasons the City has made efforts to encourage industrial businesses to stay..32 33 These include:

The New York City Industrial Development Authority's numerous programs, such as tax‐exempt bond financing, commercial lease improvement tax abatements, building materials sales tax exemptions, and a waiver of the 2.8% city mortgage recording tax.

27 Mayor's Office of Industrial and Manufacturing Businesses. <http://www.nyc.gov/html/imb/html/ibz/ibz.shtml> 28 http://www.sbidc.org/gowanus.htm> 29 City of New York, Protecting and Growing New York City's Industrial Job Base. Jan. 2005. Feb. 6, 2010. <http://www.nyc.gov/html/imb/downloads/pdf/whitepaper.pdf> 30 madeinnyc.org 31 ibid. 32 City of New York 33 madeinnyc.org

32

The Southwest Brooklyn Industrial Zone, which offers a variety of tax credits for creating employment, sales tax exemptions, lower utility costs, and capital improvements tax credits.34

The Commercial Expansion Program, which provides an abatement on property taxes for new leases of industrial, commercial, and retail space lasting 2 to 5 years (diminishing each year).

The Mayor's Office of Industrial and Manufacturing Businesses, providing assistance to potential industrial tenants and ensuring the permanent preservation of nearby manufacturing zoning.

Industrial and Commercial Abatement Program: tax abatements up to 25 years on renovation and expansion projects.

These incentives will serve to attract potential industrial tenants to this area of the City, raising demand for the Gowanus Innovation Center's spaces and enabling the financial success of the tenants. Green Tenants New York is already home to numerous green entrepreneurial enterprises that are taking advantage of existing affordable manufacturing and office space. The following tenants, selected from those at the nearby green manufacturing incubator facilities, are typical of the tenants we would seek to attract

Company Product/Service

Aerocity Wind turbine energy distribution technology

EcoLogic Solutions Environmental cleaning products

Rentricity Recovery of energy from water distribution system

Sollega Solar panels designed for simplified installation

ThinkEco Hardware and software for modernizing electrical outlets

IceStone Countertops from recycled materials

Bien Hecho Furniture from salvaged materials

Lumi Solair Streetlamps powered by wind and solar

December Box Furniture made with FSC wood and salvaged iron

SMIT Wind, solar generators in mesh application to building exterior 35 36

These companies generally have a handful of employees and need space to maintain several areas of production, or a workshop to assist in refining and developing new technology. They also need office space to manage sales leads and a conference room to meet with potential investors. Supply and Demand The demand for the space will be driven by those members of the creative class who are entrepreneurial and concerned with sustainability. In order to attract and maintain this class, cities must have the "three T's" : Technology, Talent, Tolerance.37 While it is generally well known that New York remains strong in these areas, some demographic information empirically confirms this:

34 Southwest Brooklyn Industrial Development Corp. Business Services. Feb. 6, 2010. <http://www.sbidc.org/empirezone.htm> 35 New York City Accelerator for a Clean and Renewable Economy. <http://www.nycacre.com/> Accessed March 5, 2010. 36 Brooklyn Navy Yard, Green Business Directory. Spring 2009. <http://www.brooklynnavyyard.org/GreenDirectory/html‐edition‐professional/templates/liquid‐green/index.html> Accessed March 5, 2010.

37 Florida, Richard. RF: What Are the Three T's of Economic Development? <http://www.creativeclass.com/richard_florida/video/index.php?video=04_What_are_the_three_Ts> Accessed March 5, 2010.

33

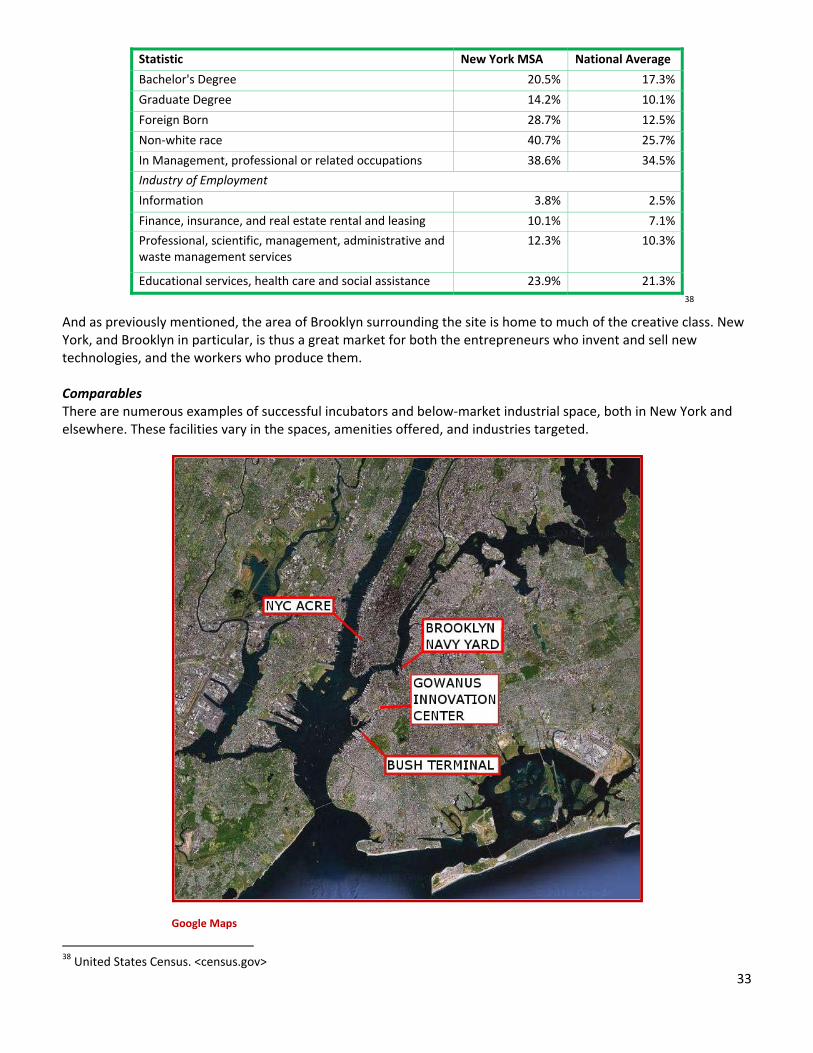

Statistic New York MSA National Average

Bachelor's Degree 20.5% 17.3%

Graduate Degree 14.2% 10.1%

Foreign Born 28.7% 12.5%

Non‐white race 40.7% 25.7%

In Management, professional or related occupations 38.6% 34.5%

Industry of Employment

Information 3.8% 2.5%

Finance, insurance, and real estate rental and leasing 10.1% 7.1%

Professional, scientific, management, administrative and waste management services

12.3% 10.3%

Educational services, health care and social assistance 23.9% 21.3%

38 And as previously mentioned, the area of Brooklyn surrounding the site is home to much of the creative class. New York, and Brooklyn in particular, is thus a great market for both the entrepreneurs who invent and sell new technologies, and the workers who produce them. Comparables There are numerous examples of successful incubators and below‐market industrial space, both in New York and elsewhere. These facilities vary in the spaces, amenities offered, and industries targeted.

Google Maps

38 United States Census. <census.gov>

34

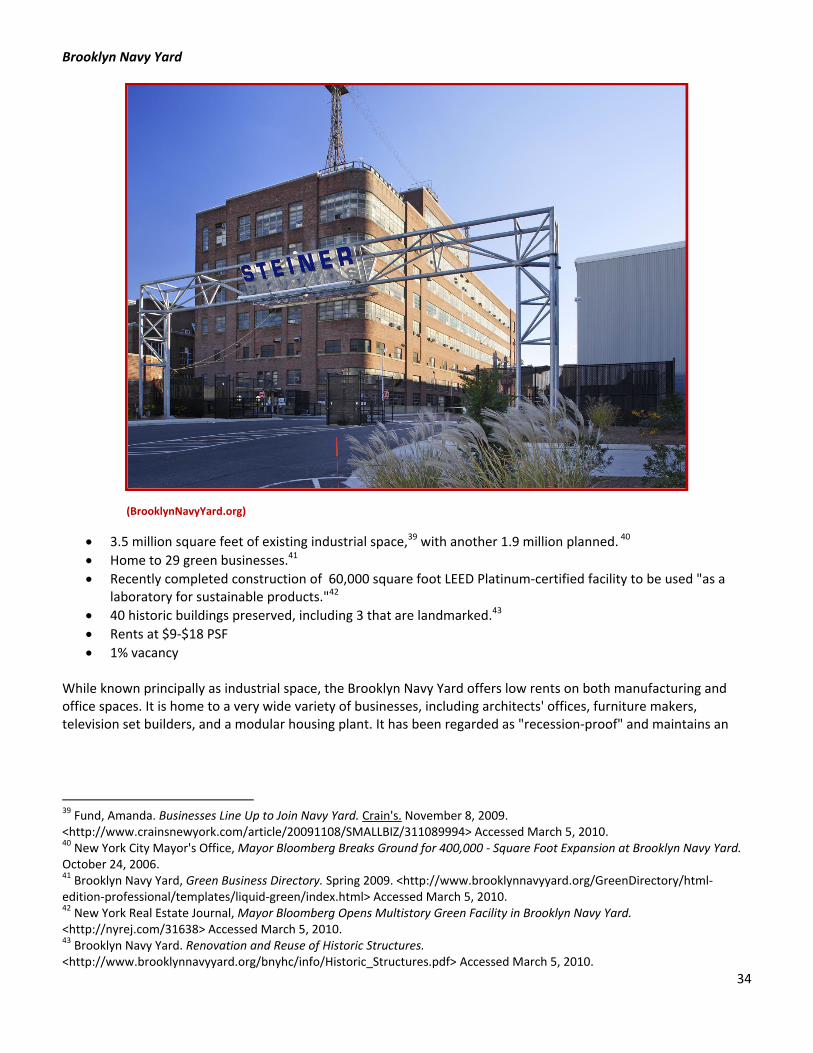

Brooklyn Navy Yard

(BrooklynNavyYard.org)

3.5 million square feet of existing industrial space,39 with another 1.9 million planned. 40

Home to 29 green businesses.41

Recently completed construction of 60,000 square foot LEED Platinum‐certified facility to be used "as a laboratory for sustainable products."42

40 historic buildings preserved, including 3 that are landmarked.43

Rents at $9‐$18 PSF

1% vacancy While known principally as industrial space, the Brooklyn Navy Yard offers low rents on both manufacturing and office spaces. It is home to a very wide variety of businesses, including architects' offices, furniture makers, television set builders, and a modular housing plant. It has been regarded as "recession‐proof" and maintains an

39 Fund, Amanda. Businesses Line Up to Join Navy Yard. Crain's. November 8, 2009. <http://www.crainsnewyork.com/article/20091108/SMALLBIZ/311089994> Accessed March 5, 2010. 40 New York City Mayor's Office, Mayor Bloomberg Breaks Ground for 400,000 ‐ Square Foot Expansion at Brooklyn Navy Yard. October 24, 2006. 41 Brooklyn Navy Yard, Green Business Directory. Spring 2009. <http://www.brooklynnavyyard.org/GreenDirectory/html‐edition‐professional/templates/liquid‐green/index.html> Accessed March 5, 2010. 42 New York Real Estate Journal, Mayor Bloomberg Opens Multistory Green Facility in Brooklyn Navy Yard. <http://nyrej.com/31638> Accessed March 5, 2010. 43 Brooklyn Navy Yard. Renovation and Reuse of Historic Structures. <http://www.brooklynnavyyard.org/bnyhc/info/Historic_Structures.pdf> Accessed March 5, 2010.

35

exceptionally high occupancy rate of 99%.44 Within it is the Pratt Design Incubator for Sustainable Innovation, a facility that provides space and support for industrial design startup businesses.45 Greenpoint Manufacturing and Design Center

(GMDC)

608,000 square feet of affordable industrial space in 5 restored buildings.

Intended to ameliorate effects of Brooklyn gentrification on creative artisans.

Tenants include artists, textiles, cabinetry, metalworking, and other types of light manufacturing.

Available spaces generally from 1,000 to 7,000 square feet.46

Rents at $11‐16 PSF.47

4.5% vacancy.48 The Greenpoint Manufacturing Design Center has been successful at numerous conversions of historic warehouses into manufacturing space. It has been widely recognized as successful at keeping manufacturing jobs in Brooklyn. The facility is focused mainly on artisan‐type tenants engaging in production of custom crafts.

44 Fund. 45 Pratt Design Incubator. <http://incubator.pratt.edu/> Accessed March 5, 2010. 46GMDC Online. <gmdconling.org> Accessed March 5, 2010. 47 Hersh, Barry. NYU. How Development Works in 2009: Greenpoint Manufacturing Design Center. Powerpoint presentation, February 11, 2010. 48 GMDC Online.

36

New York City Accelerator for a Clean and Renewable Economy

49

16,500 square feet providing 50 turnkey office spaces in SoHo

Shared conference room, receptionist, kitchen

Much assistance with business plans, legal and tax issues, attracting investors, etc.

Academic and government partners: NYU‐Poly, Pratt, Columbia, NYCEDC, NYSERDA, and NYCIF

Rents start rate $200/month (approx. $8‐9 PSF)50

Extremely competitive application process NYC ACRE is a new venture, and has so far been successful. Much of this success is due to the facility's strong partnerships with academic institutions and government. The space was leased for free for 3 years by NYU‐Poly, and NYSERDA made a $1.6 million grant, which is being used to cover operating expenses only. The center ensures the provision of a variety of supportive services, taking advantage of the experience and connections of the management drawn from Columbia, NYU and Pratt.51

49 NYC ACRE Photos. <http://www.nycacre.com/about/photos.php> Accessed March 5, 2010. 50 NYU‐Poly. Mayor Bloomberg Announces NYU‐Poly Business Incubator Along with 10 Other Financial Sector Remedies. February 19, 2009. <http://archive.poly.edu/news/fullNews.php?id=1515> Accessed March 5, 2010. 51 Interview with Prahbdeep Singh, New York City Investment Fund. March 4, 2010.

37

In Development Bush Terminal Industrial Complex

52

3.5 million square feet of underutilized industrial space being redeveloped.53

$165 million in funding from city, $105 million from state, federal, and private sources pledged.

Rehabilitation driven by improvements to open space on waterfront, including sports fields, pavilions, and wetlands.

Brownfield remediation grants: $17.8 million from state, $8 million from city, and $8 million from federal government.

$700,000 from state and $500,000 from city to build park.

City‐owned industrial properties to be rented at affordable rates to local manufacturers, similar to Brooklyn Navy Yard.54

Some real estate to be sold to for‐profit developers for mixed‐use projects.

52 Bush Terminal Photos. BridgeandTunnelClub.org. <http://www.bridgeandtunnelclub.com/bigmap/brooklyn/sunsetpark/bushterminal/index.htm> Accessed March 5, 2010. 53 New York City Mayor's Office, Mayor Bloomberg Announces Programs to Expand the Reactivation of Brooklyn's Working Waterfront. July 20, 2009. 54 NYC EDC, Sunset Park Waterfront Vision Plan. Summer 2009. <http://www.nycedc.com/PressRoom/PressKit/Documents/Sunset_Park_Vision_Plan.pdf> Accessed March 5, 2010.

38

The Bush terminal is thoroughly integrated into a neighborhood‐wide investment, including 22 acres of open space, the restoration of a maritime port, and improvement of freight rail access.55 It intends to produce 22,000 jobs.56 The project will also employ green practices such as solar arrays, energy conservation incentives, alternative fuel vehicles and recycling. Other incubators in the city provide space for design firms, science and technology firms, and the biotech industry. There are also many examples of successful incubators in other cities. Our product draws from these examples in the following ways:

Some of the comparable facilities are intended only for large‐scale industrial production, whereas others offer only office space as a headquarters for attracting investors and making sales. This has led to our approach of offering both in an integrated facility.

We are including business services similar to those so indispensible to the NYC ACRE incubator.

In constructing the Sponge Park we recognize the importance of integrating waterfront public space, as the Bush Terminal plan seeks to do.

We plan to reuse a historic industrial building like most of these comparables have done. Our goal is to provide below‐market rents, both in order to accomplish the stated goals of the Center and to ensure there is insignificant market risk. The asking rents for office space in nearby Downtown Brooklyn were $31.22/SF in 4Q09.57 Independent surveys of listings indicate that industrial space rents around the city are around $12‐$18/SF. The above comparables offer manufacturing space focused around the $13‐$15 mark. Our model assumes that we will rent the office space for $20/SF, a full 36% below market, and the manufacturing space for $11/SF, which is favorable even when compared to other manufacturing incubators.

55 Ibid. 56 New York City Mayor's Office, Mayor Bloomberg Announces Programs to Expand the Reactivation of Brooklyn's Working Waterfront. July 20, 2009. 57 Marcus and Millichap, Office Research Market Updat, Brooklyn. Feb. 6, 2010. <http://www.marcusmillichap.com/research/reports/office/BrooklynOffice.pdf>

39

Demand Capture While the fact that incubator space is leased at below market rates helps to ensure high occupancy, the several million square feet of new space that is proposed to be developed in the above nearby facilities suggests a market survey is prudent: Market Study Matrix

Demand

NYC Green Workforce Employment

2008 2018 (EDC) Change

Space per

Worker (SF)

Total

Demand (SF)

13,800 27,600 13,800 463 6,389,400

Supply

Below Market Manufacturing Space

Facility

Current

Vacancy

Under

Development

Net

Absorption

Brooklyn Navy Yard 35,000 1,900,000 1,935,000

GMDC 27,360 ‐ 27,360

Bush Terminal 555,000 3,500,000 4,055,000

Sum: 617,360 5,400,000 6,017,360

Projected 2018 Demand (SF): 372,040

Proposed Space: 52,500

Capture Rate: 14% 58 59 60

This is a rough sketch of the situation, as the green workforce in reality composes only a small fraction of the demand for below‐market industrial space, and not all green workers are in manufacturing. Nevertheless, it illustrates that the increase in below‐market industrial space roughly coincides with the rapid growth of the green sector. Acquisition Industrially zoned land in Brooklyn is currently selling for approximately $50‐$100 per square foot, and warehouses $100‐200. Our site would be valued around $14.7 million by this standard. But it is difficult to apply such broad comparables to our very unique site. There is both a sizeable stigma and remediation price tag attached to the site, and the seller is likely eager to dispose of the asset. Also, much of the lot is unbuildable due to the odd shape. We will seek to purchase the site for no more than $5 million. One factor affecting the price is the possibility of the seller receiving a tax deduction for selling at a below‐market price to a charity. This works by first having the property appraised, then having the seller donate an interest in the property to our nonprofit entity, for which a tax deduction is received. The GICDC would then purchase, at market value, the remaining interest held by the seller. In this way the seller effectively receives a tax deduction equal to the reduction below market price by which he sells. This would make him more willing to reduce the price, all things considered equal.

58 New York City, New York City's Transformation to a Green Economy. <http://www.nyc.gov/html/om/pdf/2009/pr465‐09_plan.pdf> Accessed March 5, 2010. 59 USGBC, Building Area Per Employee by Business Type. <http://www.usgbc.org/ShowFile.aspx?DocumentID=4111> Accessed March 5, 2010.

40

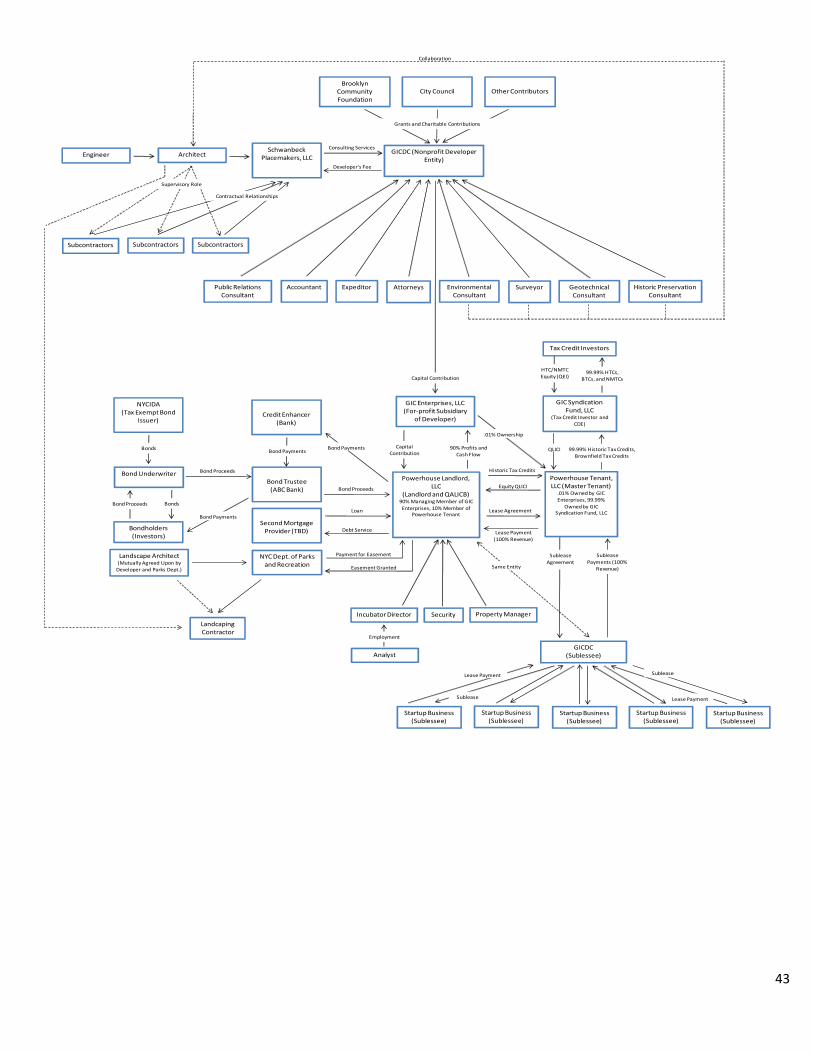

The Jewish Press building had an asking price of $10 million in early 2009, two months prior to the announcement of the Canal's possible Superfund designation. This previous asking price was $317.46 per square foot, or $123.46 per buildable square foot, a number much higher than the replacement cost of the existing real estate, and likely determined far more by the site's development potential. A recent average of purchased sites in Brooklyn is $39 per buildable square foot,61 well below the lot's asking price. We will expect to acquire this site for $6.5 million, or $80 per buildable square foot. This is more in line with the value of the existing real estate, at $206 per square foot, and while less than the seller originally asked for, is markedly generous compared to other transactions. If, for any reason the future development potential of the combined assemblage is not realized, our alternative plan is to realize a 14.4% IRR over a ten year holding period. Once both lots have been acquired, the GICDC and Schwanbeck Placemakers will draw up a subdivision and sale agreement as previously agreed to under the terms of the initial contract. We will file a subdivision plan with the Department of City Planning, separating out the 29,000 square feet of land on the north side to be reserved for future development. This newly created lot will be deeded to Schwanbeck Placemakers upon the completion of consulting services, also as specified in the contract. Financing and Approvals In our experience, nonprofit development budgets are a collection of moving parts, in which multiple sources of grants, subsidized and market financing, and equity are combined with the expectation that not all will come through in the end. For this reason we intend to concurrently seek as many sources as possible. These include:

NYCIDA Not‐for‐Profit Bond Program: This program provides tax exempt bond financing for non‐profits planning major capital expansions. The bonds are triple tax‐exempt, and the mortgage recording tax is waived. We are seeking a total amount of $11,855,047 as the primary source of capital.

Acquisition Loan and Gap Financing: Because of the complex process of syndicating tax credits and underwriting bonds, it will greatly simplify and accelerate the process to acquire the site early in the process using an acquisition loan. After we have secured permanent financing, we intend to pay this loan down with incoming tax credit equity and by taking out second and third mortgages. We intend to secure these loans from lenders that target non‐profits engaging in economic development, offering low rates. There are several major sources for such debt, including:

o New York City Investment Fund: This fund invests in a variety of projects beneficial to New York City, and provided investment in existing incubators of the NYC ACRE and the GMDC's 221 McKibbin Street. In the latter case a $1.3 million 2nd mortgage was provided at a rate of 1%.

o Seedco Financial: Lending to nonprofits engaged in real estate development projects. Can be used for both acquisition and construction costs. $200,000 ‐ $1.5M loans on 5‐7 year terms, with rates of 6%‐8%.

o EDC: The EDC offers a Loan Enhanced Assistance Program that provides triple tax exempt financing for non‐profits engaged in constructing new facilities. This is a separate program from the NYCIDA bonds.

o Carver Federal Savings Bank: This CDFI has a specialized non‐profit lending division and offers highly competitive acquisition and term loans for non‐profit‐owned real estate.

o Nonprofit Finance Fund: This fund provides loans of up to $2 million for acquisition and construction by non‐profits.

61 Knakal, Robert. The Boroughs and Building Sales. The Commercial Observer. <http://www.observer.com/2010/commercial‐observer/boroughs‐and‐building‐sales> Accessed May 1, 2010.

41