brookfield renewable partners (bep)/media/files/b/brookfield...bep (nyse) 25% 11% 9% primary font...

TRANSCRIPT

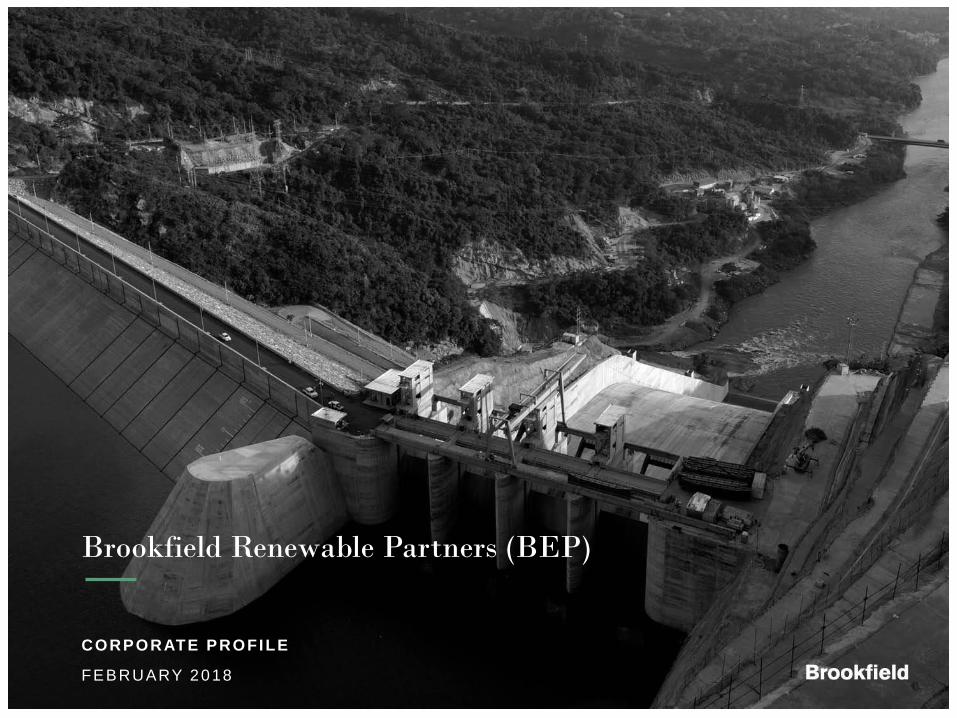

Brookfield Renewable Partners (BEP)

CORPORATE PROFILE

FEBRUARY 2018

2

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Cautionary Statement Regarding Forward-Looking Statements

This presentation contains forward-looking statements and information, within the meaning of Canadian securities laws and “forward-looking statements” within the meaning of Section 27A of the U.S. Securities

Act of 1933, as amended, Section 21E of the U.S. Securities Exchange Act of 1934, as amended, “safe harbor” provisions of the United States Private Securities Litigation Reform Act of 1995 and in any

applicable Canadian securities regulations, concerning the business and operations of Brookfield Renewable. Forward-looking statements may include estimates, plans, expectations, opinions, forecasts,

projections, guidance or other statements that are not statements of fact. Forward-looking statements in this presentation include statements regarding the quality of Brookfield Renewable’s assets and the

resiliency of the cash flow they will generate, Brookfield Renewable’s anticipated financial performance and payout ratio, future commissioning of assets, the contracted nature of our portfolio, technology

diversification, acquisition opportunities, financing and refinancing opportunities, future energy prices and demand for electricity, achieving long-term average generation, project development and capital

expenditure costs, energy policies, economic growth, growth potential of the renewable asset class, the future growth prospects and distribution profile of Brookfield Renewable and Brookfield Renewable’s

access to capital. In some cases, forward-looking statements can be identified by the use of words such as “plans”, “expects”, “scheduled”, “estimates”, “intends”, “anticipates”, “believes”, “potentially”, “tends”,

“continue”, “attempts”, “likely”, “primarily”, “approximately”, “endeavours”, “pursues”, “strives”, “seeks”, “targets”, “believes”, or variations of such words and phrases, or statements that certain actions, events or

results “may”, “could”, “would”, “should”, “might” or “will” be taken, occur or be achieved. Although we believe that our anticipated future results, performance or achievements expressed or implied by the

forward-looking statements and information in this presentation are based upon reasonable assumptions and expectations, we cannot assure you that such expectations will prove to have been correct. You

should not place undue reliance on forward-looking statements and information as such statements and information involve known and unknown risks, uncertainties and other factors which may cause our

actual results, performance or achievements to differ materially from anticipated future results, performance or achievement expressed or implied by such forward-looking statements and information.

Factors that could cause actual results to differ materially from those contemplated or implied by forward-looking statements include, but are not limited to, the following: we are not subject to the same

disclosure requirements as a U.S. domestic issuer; the separation of economic interest from control or the incurrence of debt at multiple levels within our organizational structure; being deemed an “investment

company” under the U.S. Investment Company Act of 1940; the effectiveness of our internal controls over financial reporting; changes to hydrology at our hydroelectric stations, to wind conditions at our wind

energy facilities or to crop supply or weather generally at any biomass cogeneration facility; counterparties to our contracts not fulfilling their obligations; increases in water rental costs (or similar fees) or

changes to the regulation of water supply; volatility in supply and demand in the energy market; the increasing amount of uncontracted generation in our portfolio; industry risks relating to the power markets in

which we operate; increased regulation of our operations; contracts, concessions and licenses expiring and not being renewed or replaced on similar terms; increases in the cost of operating our plants; our

failure to comply with conditions in, or our inability to maintain, governmental permits; equipment failures; dam failures and the costs of repairing such failures; force majeure events; uninsurable losses; adverse

changes in currency exchange rates; availability and access to interconnection facilities and transmission systems; health, safety, security and environmental risks; disputes, governmental and regulatory

investigations and litigation; our operations being affected by local communities; fraud, bribery, corruption, other illegal acts or inadequate or failed internal processes or systems; our reliance on computerized

business systems; advances in technology that impair or eliminate the competitive advantage of our projects; newly developed technologies in which we invest not performing as anticipated; labour disruptions

and economically unfavourable collective bargaining agreements; our inability to finance our operations due to the status of the capital markets; our inability to effectively manage our foreign currency exposure;

operating and financial restrictions imposed on us by our loan, debt and security agreements; changes in our credit ratings; changes to government regulations that provide incentives for renewable energy; our

inability to identify sufficient investment opportunities and complete transactions; the growth of our portfolio and our inability to realize the expected benefits of our transactions; our inability to develop existing

sites or find new sites suitable for the development of greenfield projects; delays, cost overruns and other problems associated with the construction, development and operation of our generating facilities; the

arrangements we enter into with communities and joint venture partners; Brookfield Asset Management’s election not to source acquisition opportunities for us and our lack of access to all renewable power

acquisitions that Brookfield Asset Management identifies; our lack of control over all our operations; our ability to issue equity or debt for future acquisitions and developments is dependent on capital markets;

foreign laws or regulation to which we become subject as a result of future acquisitions in new markets; the departure of some or all of Brookfield Asset Management’s key professionals; our relationship with,

and our dependence on, Brookfield Asset Management and Brookfield Asset Management’s significant influence over us; and risks related to changes in how Brookfield Asset Management elects to hold its

ownership interests in the Partnership.

We caution that the foregoing list of important factors that may affect future results is not exhaustive. The forward-looking statements represent our views as of the date of this presentation and should not be

relied upon as representing our views as of any subsequent date. While we anticipate that subsequent events and developments may cause our views to change, we disclaim any obligation to update the

forward-looking statements, other than as required by applicable law. For further information on these known and unknown risks, please see “Risk Factors” included in our Form 20-F.

Cautionary Statement Regarding Use Of Non-IFRS Measures

This presentation contains references to Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (“Adjusted EBITDA”), Funds From Operations (“FFO”) and Funds From Operations per Unit

(“FFO per Unit”), which are not generally accepted accounting measures under IFRS and therefore may differ from definitions of Adjusted EBITDA, Funds From Operations and Funds From Operations per Unit

used by other entities. We believe that Adjusted EBITDA, Funds From Operations and Funds From Operations per Unit are useful supplemental measures that may assist investors in assessing the financial

performance and the cash anticipated to be generated by our operating portfolio. Neither Adjusted EBITDA, Funds From Operations nor Funds From Operations per Unit should be considered as the sole

measure of our performance and should not be considered in isolation from, or as a substitute for, analysis of our financial statements prepared in accordance with IFRS.

References to Brookfield Renewable are to Brookfield Renewable Partners L.P. together with its subsidiary and operating entities unless the context reflects otherwise.

All amounts are in U.S. dollars and presented on a consolidated basis unless otherwise specified.

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Table of Contents

Who We Are

Page 4

Portfolio Overview

Page 10

Growth

Page 15

Financial Profile

Page 24

Appendix

Page 29

4

Who We Are

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

5

We are a multi-technology, globally

diversified, owner and operator of

renewable power assets

6

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Leader in Renewable Generation

841 power generating facilities

$40 billion TOTAL POWER ASSETS

24 markets in 14 countries

16,400 MEGAWATTS OF CAPACITY

Situated on 81 river systems

82% HYDROELECTRIC GENERATION

One of the largest public pure-play renewable businesses globally

100 years of experience in power generation

Full operating, development and power marketing capabilities

Over 2,000 operating employees

7

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Simple Strategy

Simple strategy with a proven track record of success through all cycles

Acquire and develop high-quality

renewable power assets and businesses

below intrinsic value

Optimize cash flows by applying our

operating expertise to enhance value

Finance our businesses on an

investment grade basis

8

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

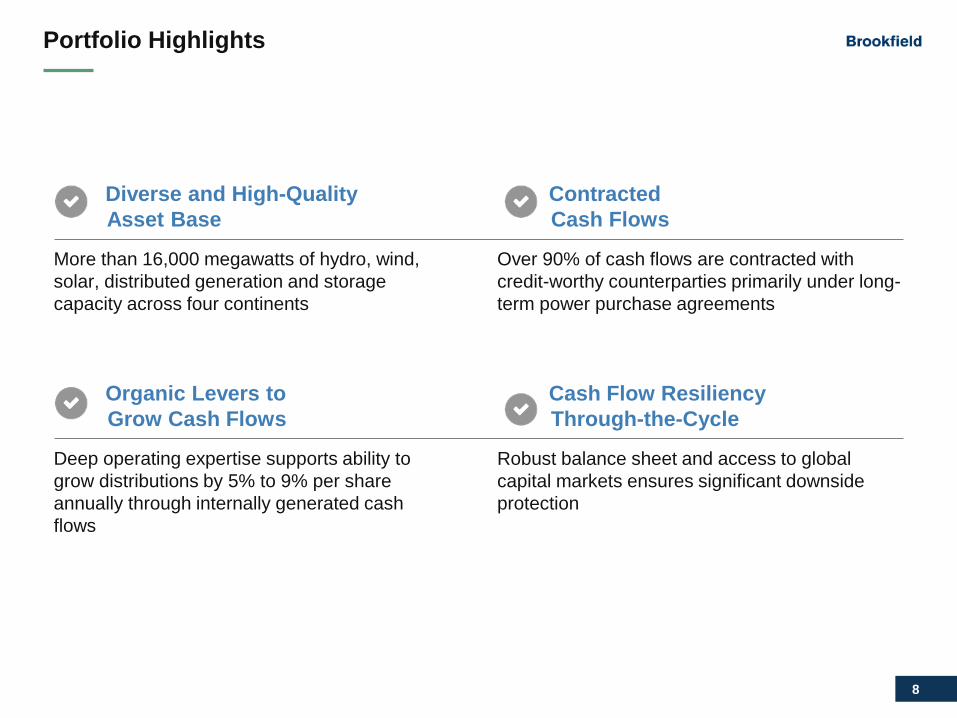

Portfolio Highlights

Diverse and High-Quality

Asset Base

More than 16,000 megawatts of hydro, wind,

solar, distributed generation and storage

capacity across four continents

Organic Levers to

Grow Cash Flows

Deep operating expertise supports ability to

grow distributions by 5% to 9% per share

annually through internally generated cash

flows

Contracted

Cash Flows

Over 90% of cash flows are contracted with

credit-worthy counterparties primarily under long-

term power purchase agreements

Cash Flow Resiliency

Through-the-Cycle

Robust balance sheet and access to global

capital markets ensures significant downside

protection

9

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

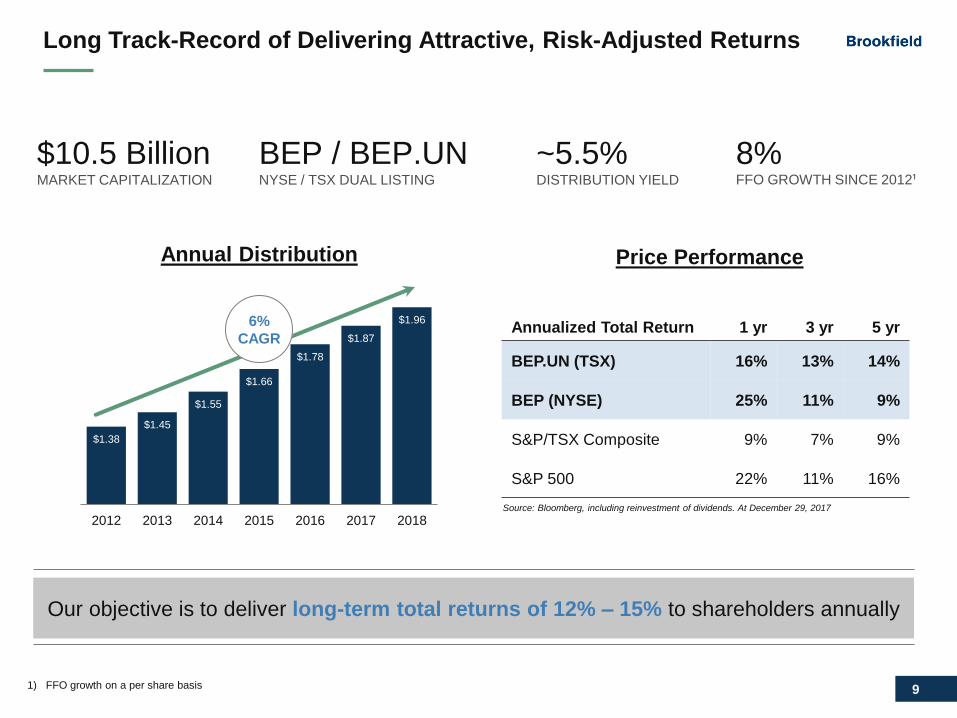

Long Track-Record of Delivering Attractive, Risk-Adjusted Returns

Our objective is to deliver long-term total returns of 12% ‒ 15% to shareholders annually

$10.5 Billion MARKET CAPITALIZATION

8% FFO GROWTH SINCE 2012¹

BEP / BEP.UN NYSE / TSX DUAL LISTING

~5.5% DISTRIBUTION YIELD

Annualized Total Return 1 yr 3 yr 5 yr

BEP.UN (TSX) 16% 13% 14%

BEP (NYSE) 25% 11% 9%

S&P/TSX Composite 9% 7% 9%

S&P 500 22% 11% 16%

Source: Bloomberg, including reinvestment of dividends. At December 29, 2017

$1.38

$1.45

$1.55

$1.66

$1.78

$1.87

$1.96

2012 2013 2014 2015 2016 2017 2018

Annual Distribution Price Performance

6%

CAGR

1) FFO growth on a per share basis

10

Portfolio Overview

11

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

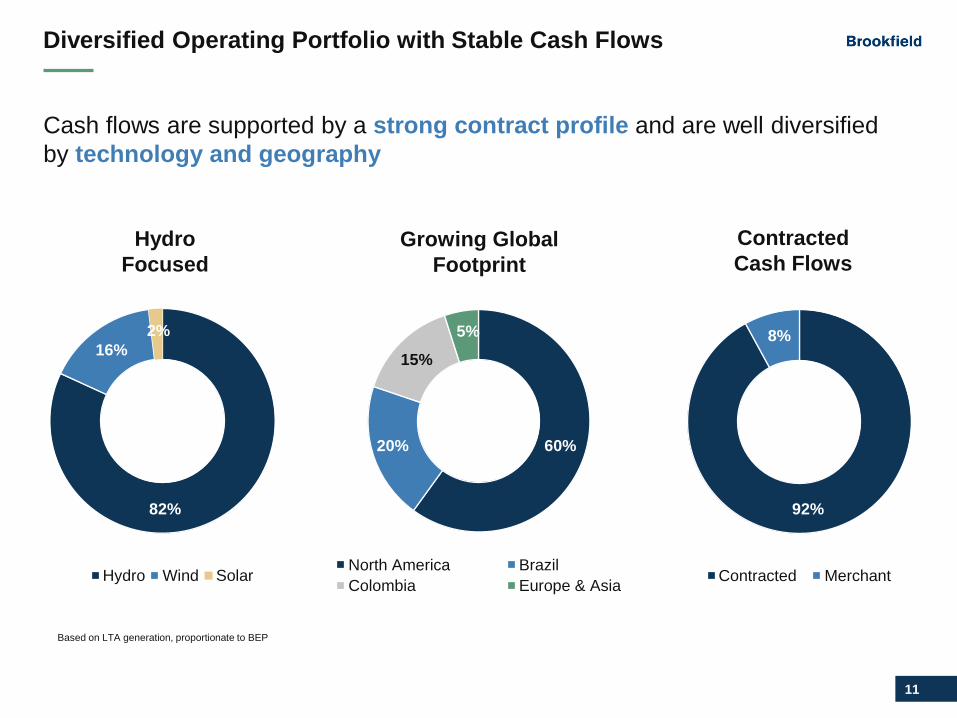

Diversified Operating Portfolio with Stable Cash Flows

Cash flows are supported by a strong contract profile and are well diversified

by technology and geography

Hydro Wind Solar

16%

North America Brazil

Colombia Europe & Asia

60%

5%

15%

20%

Contracted Merchant

92%

8%

82%

Hydro

Focused Growing Global

Footprint Contracted

Cash Flows

2%

Based on LTA generation, proportionate to BEP

12

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Global Operations with Local Presence

We have integrated operating platforms on four continents with local operating and

power marketing expertise

NORTH AMERICA 8,700 megawatts

$26 Billion in total power assets

SOUTH AMERICA 4,400 megawatts

$10.5 Billion in total power assets

ASIA 600 megawatts

$0.5 Billion in total power assets

EUROPE 2,700 megawatts

$3 Billion in total power assets

13

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

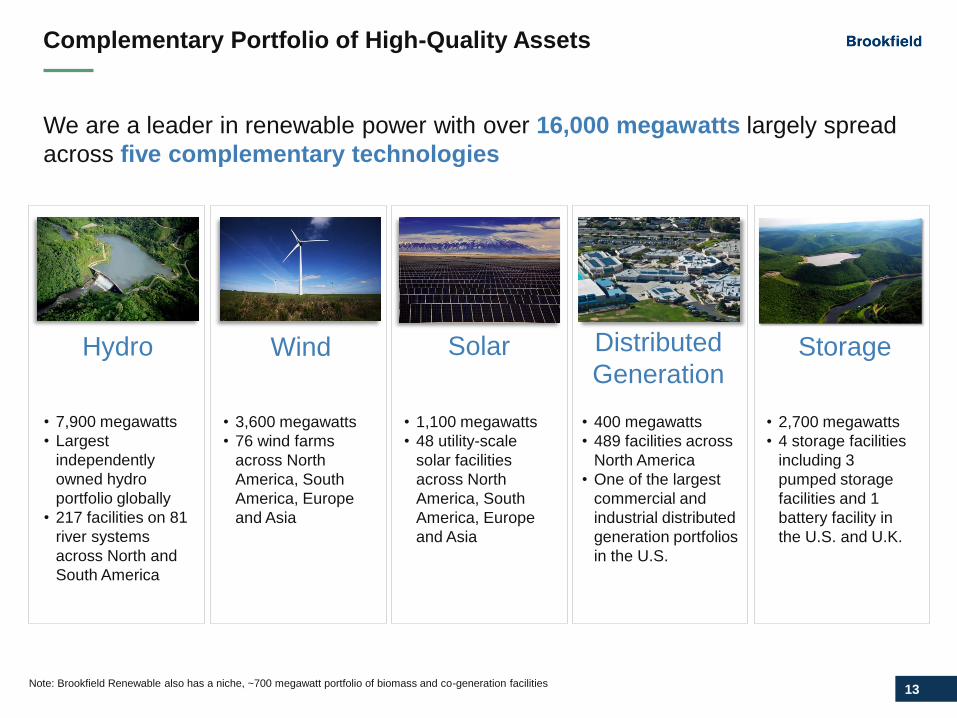

Complementary Portfolio of High-Quality Assets

We are a leader in renewable power with over 16,000 megawatts largely spread

across five complementary technologies

Wind Solar

Distributed

Generation Storage Hydro

• 7,900 megawatts

• Largest

independently

owned hydro

portfolio globally

• 217 facilities on 81

river systems

across North and

South America

• 3,600 megawatts

• 76 wind farms

across North

America, South

America, Europe

and Asia

• 1,100 megawatts

• 48 utility-scale

solar facilities

across North

America, South

America, Europe

and Asia

• 400 megawatts

• 489 facilities across

North America

• One of the largest

commercial and

industrial distributed

generation portfolios

in the U.S.

• 2,700 megawatts

• 4 storage facilities

including 3

pumped storage

facilities and 1

battery facility in

the U.S. and U.K.

Note: Brookfield Renewable also has a niche, ~700 megawatt portfolio of biomass and co-generation facilities

14

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Deep Operational Expertise

2,000+ EXPERIENCED

OPERATORS

140+ POWER MARKETING

EXPERTS

4 REGIONAL CONTROL

CENTERS

Generation Management,

Planning and Dispatch

Asset Integration

Asset Integration

Asset Integration Regulatory Expertise

Asset Integration National

System Control

Energy Marketing Expertise

Engineering and

Development

Asset Integration

Stakeholder Engagement

Asset Integration

Health, Safety, Security and

Environmental

15

Growth

16

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Organic Cash Flow Growth

BEP is focused on delivering 5% to 9% distribution growth annually on a per

unit basis through cash flows generated from our existing business

• Growth target can be achieved from organic initiatives and fully funded by internally

generated cash flow

‒ We do not rely on M&A to achieve cash flow growth targets

‒ This does not account for the embedded optionality of our 2.5 TWh merchant hydro

portfolio in the United States where each $10/MWh increase in revenue translates

to $25 million in incremental FFO

Embedded

Inflation

Escalation

(1% to 2%)

Expected

Margin

Expansion

(2% to 4%)

FFO per Unit

Growth

Potential

(6% to 11%)

Advanced

Development

Pipeline

(3% to 5%)

17

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Inflation: $50 million FFO Contribution Over Five Years

Our revenues are indexed to inflation providing for 1% – 2% annual FFO growth

Proportional Basis Brazil

North

America Colombia

Annual

Total

Revenues1 ($ million) $200 $1,000 $190 $1,390

% Indexed to inflation 100% 30% 100%

Estimated long-term inflation 4.5% 2.0% 3.5%

Expected annual revenue uplift ($ million) $9 $6 $6 $21

Expected FFO margin 60% 50% 35% 48%

Expected annual FFO uplift ($ million) $5 $3 $2 $10

1) Normalized 2016 revenues

18

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

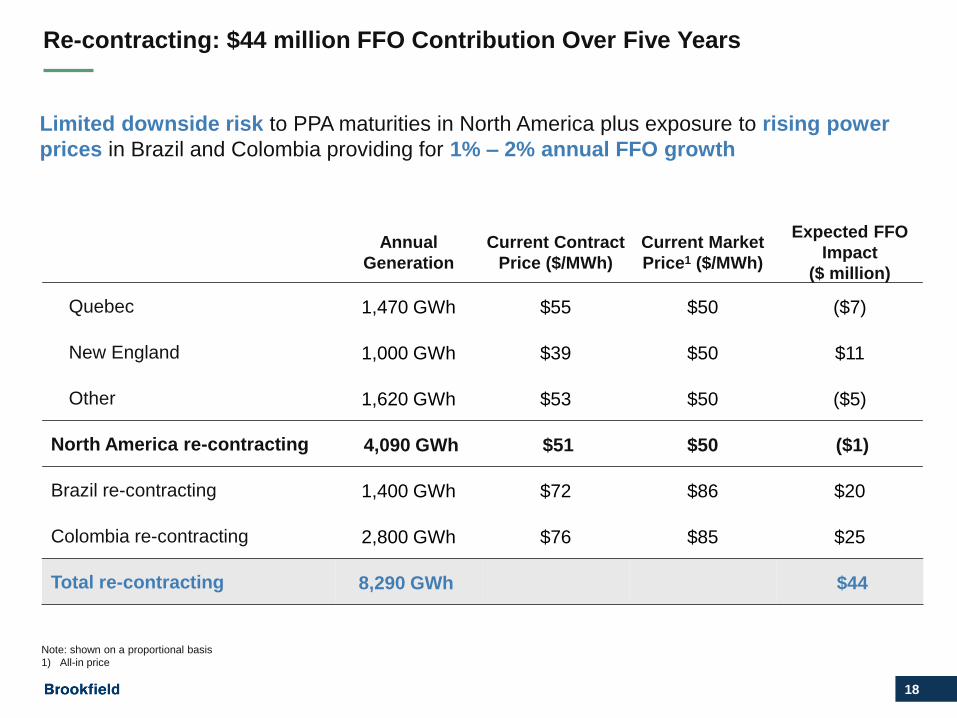

Re-contracting: $44 million FFO Contribution Over Five Years

Limited downside risk to PPA maturities in North America plus exposure to rising power

prices in Brazil and Colombia providing for 1% – 2% annual FFO growth

Annual

Generation

Current Contract

Price ($/MWh)

Current Market

Price1 ($/MWh)

Expected FFO

Impact

($ million)

Quebec 1,470 GWh $55 $50 ($7)

New England 1,000 GWh $39 $50 $11

Other 1,620 GWh $53 $50 ($5)

North America re-contracting 4,090 GWh $51 $50 ($1)

Brazil re-contracting 1,400 GWh $72 $86 $20

Colombia re-contracting 2,800 GWh $76 $85 $25

Total re-contracting 8,290 GWh $44

Note: shown on a proportional basis

1) All-in price

19

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Cost Reduction: $50 Million FFO Contribution Over Five Years

Targeted cost reduction of $2 per MWh would add $50 million to FFO over the next five

years or 1% – 2% annual FFO growth

Savings:

$2.00 / MWh

$30 million

North America

Savings:

$2.00 / MWh

$10 million

Brazil

Savings:

$2.00 / MWh

$10 million

Colombia

Savings:

$2.00 / MWh

$1 million

Europe

Streamlining

Processes

Operational

Efficiencies

Optimize

Structuring

Economies

of Scale

Note: shown on a proportional basis

20

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

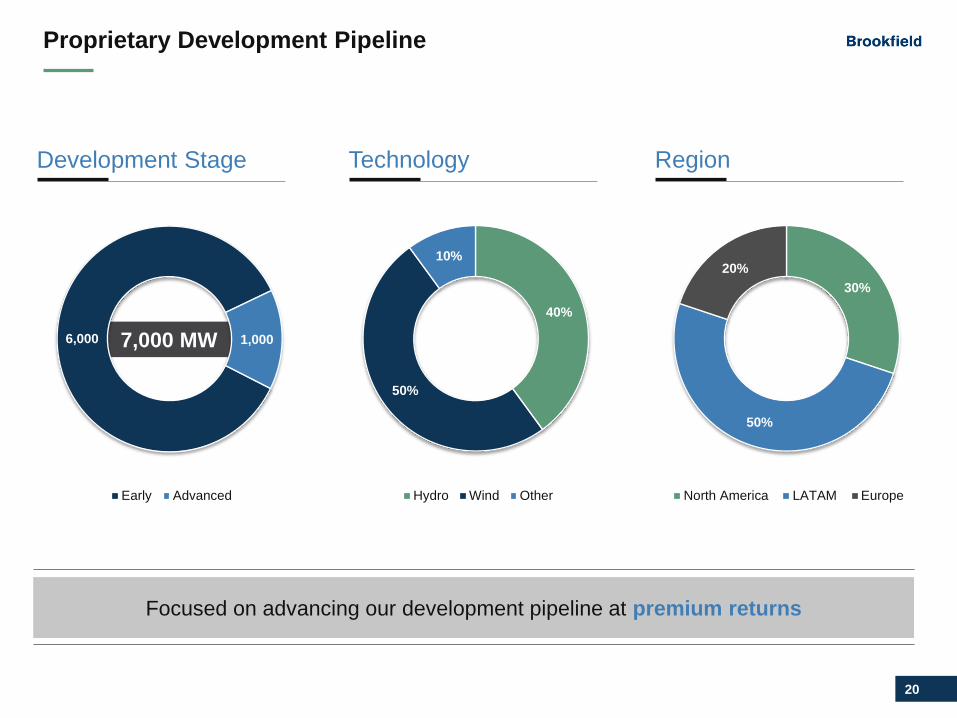

7,000 MW

Proprietary Development Pipeline

Focused on advancing our development pipeline at premium returns

Development Stage Technology Region

6,000 1,000

Early Advanced

40%

50%

10%

Hydro Wind Other

30%

50%

20%

North America LATAM Europe

21

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

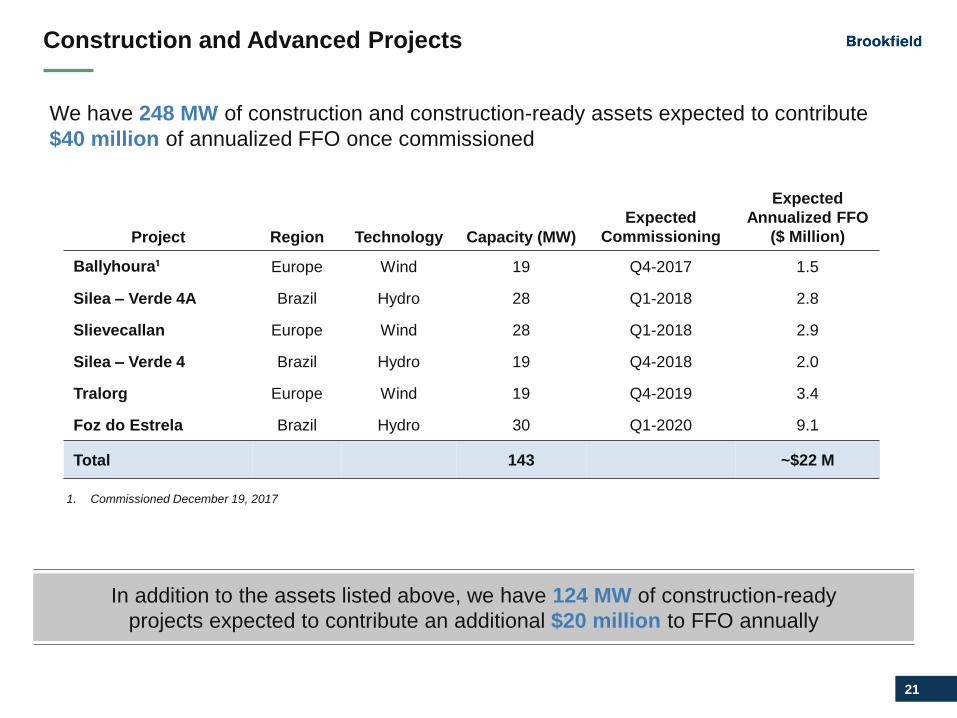

Construction and Advanced Projects

In addition to the assets listed above, we have 124 MW of construction-ready

projects expected to contribute an additional $20 million to FFO annually

We have 248 MW of construction and construction-ready assets expected to contribute

$40 million of annualized FFO once commissioned

Project Region Technology Capacity (MW)

Expected

Commissioning

Expected

Annualized FFO

($ Million)

Ballyhoura¹ Europe Wind 19 Q4-2017 1.5

Silea – Verde 4A Brazil Hydro 28 Q1-2018 2.8

Slievecallan Europe Wind 28 Q1-2018 2.9

Silea – Verde 4 Brazil Hydro 19 Q4-2018 2.0

Tralorg Europe Wind 19 Q4-2019 3.4

Foz do Estrela Brazil Hydro 30 Q1-2020 9.1

Total 143 ~$22 M

1. Commissioned December 19, 2017

22

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Our Investment Philosophy

We leverage our global footprint to source accretive transactions on a value basis

Decarbonization has created a large and

growing investible universe for renewables

We employ a contrarian strategy, looking for

capital scarcity to earn superior returns

We seek to enhance our footprint in existing

markets while cautiously expanding into new

technologies and geographies

23

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Strong Track Record of Growth

Since 2012, we have developed and acquired over 12,000 MW, deploying

more than $3 billion of BEP equity at accretive returns

We target annual equity deployment of $600 - $700 million in high quality assets

to deliver 12% to 15% annual returns

• Global network of investment professionals have a proactive outreach program to

originate acquisition opportunities

• Expertise in executing large, multi-faceted transactions

• Leverage our deep operating expertise to diligence and underwrite assets

• Disciplined approach to allocating capital with focus on downside protection and

preservation of capital

24

Financial Profile

25

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Robust Balance Sheet

Debt Maturity Ladder $billions, as at December 31, 2017

Staggered Debt Maturities

• Non-recourse financing approach provides

significant protection to corporate lenders

• No material near-term maturities

• Project debt has an average remaining term of 10

years on a proportionate basis

• ~85% proportionate, fixed rate with minimal floating

rate exposure funded in local currency

Significant Liquidity

• $1.7 billion committed corporate credit facility

through 2022

• 70% long-term target FFO payout ratio, significant

free cash flows

• Diverse funding sources with access to public and

private markets

$-

$0.5

$1.0

$1.5

$2.0

$2.5

$3.0

$3.5

2018 2019 2020 2021 2022 After

Non-Recourse Maturities Recourse Maturities

26

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Conservative Capitalization

39% DEBT TO TOTAL

CAPITALIZATION

~3.0X CONSOLIDATED EBITDA /

INTEREST COVERAGE

~7.0X REMITTED CASH FLOW /

INTEREST COVERAGE

4.5% AVERAGE INTEREST RATE ON

CORPORATE BORROWINGS

70% NON-RECOURSE

DEBT

$1.5bn AVAILABLE

LIQUIDITY

Consistently maintained conservative

debt to capitalization ratio

Investment grade credit ratings with

S&P (BBB+) and DBRS (BBB high)

High quality cash flows and strong

remittance characteristics underscore

investment grade ratings

Use of primarily non-recourse, fixed

rate financings provides strong

protection and credit stability

27

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Investment Recap

Diverse and high-quality asset base

underpinned by contracted cash flows • 16,400 MW across five technologies and four continents

• Over 90% contracted cash flows

Strong core business with embedded

organic growth • Deep operational expertise supports ability to grow distributions

by 5% to 9% annually though organic levers alone

Significant upside from acquisitions on

a value basis • Contrarian and disciplined approach to allocating capital

• Target 12% to 15% returns on investments

Downside protection to ensure cash

flow resiliency through-the-cycle

• Investment grade balance sheet since inception

• Primarily fixed rate, asset level debt with minimal floating rate

exposure funded in local currency that is non-recourse to BEP

• Maintain significant liquidity and access to global capital markets

Proven track record • 8% FFO per unit growth over the last five years

• 17% annualized returns to shareholders since inception

28

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Contacts

Contact Title Email

Sachin Shah Chief Executive Officer [email protected]

Wyatt Hartley Chief Financial Officer [email protected]

Divya Biyani Investor Relations [email protected]

29

Appendix

30

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Highly Contracted Cash Flows

• Power is largely sold to investment grade counterparties under long-term, fixed price, inflation-linked

contracts with an average proportionate term of 15 years

• We expect to re-contract expiring PPAs at levels equal to or higher than roll off prices

‒ Current all-in power prices exceed our underwriting targets, supporting embedded upside in our

cash flows

‒ In Latin America and Asia, power prices will continue to be supported by the need to build new

supply to serve growing demand

Generation

(GWh) 2018 2019 2020 2021 2022

Contracted

Hydroelectric 12,177 12,062 9,890 9,190 7,836

Wind 3,098 3,048 2,989 2,947 2,929

Solar 456 456 456 456 456

15,731 15,602 13,335 12,593 11,221

Uncontracted 1,438 1,567 3,834 4,576 5,948

LTA 17,169 17,169 16,864 16,864 16,864

% of generation 92% 91% 78% 73% 65%

Amounts proportionate to BEP

Note: The table above excludes Brazil and Colombia and other countries where we would expect the energy

associated with maturing contracts to be re-contracted in the normal course given the construct of the respective

power markets, and to maintain a contracted profile of approximately 90%, 70%, and 100% respectively.

31

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

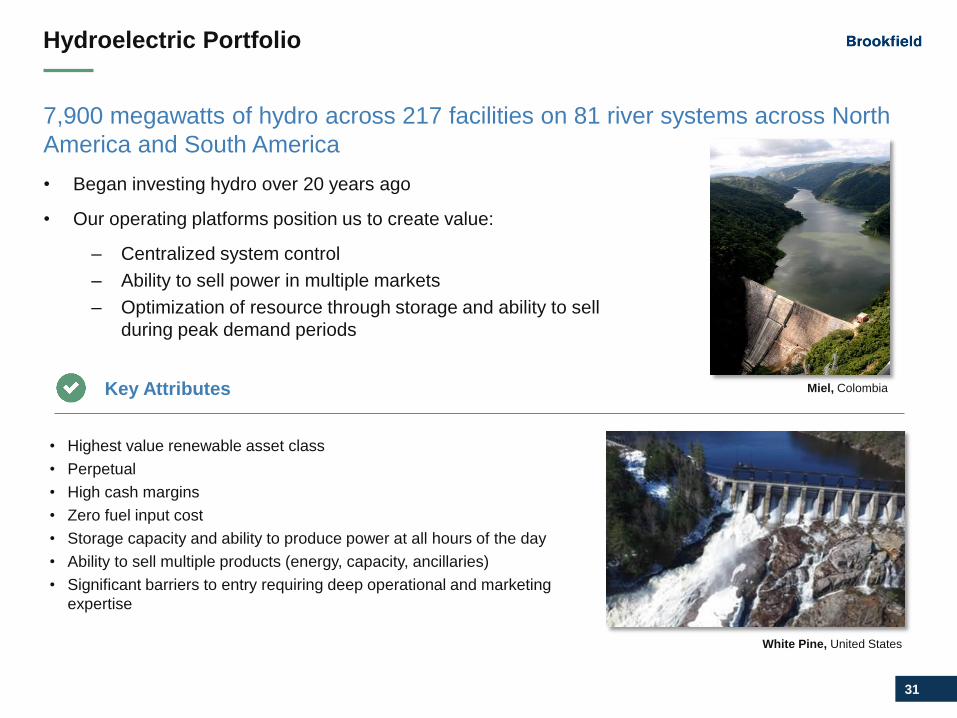

Hydroelectric Portfolio

7,900 megawatts of hydro across 217 facilities on 81 river systems across North

America and South America

• Began investing hydro over 20 years ago

• Our operating platforms position us to create value:

‒ Centralized system control

‒ Ability to sell power in multiple markets

‒ Optimization of resource through storage and ability to sell

during peak demand periods

• Highest value renewable asset class

• Perpetual

• High cash margins

• Zero fuel input cost

• Storage capacity and ability to produce power at all hours of the day

• Ability to sell multiple products (energy, capacity, ancillaries)

• Significant barriers to entry requiring deep operational and marketing

expertise

White Pine, United States

Key Attributes Miel, Colombia

32

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Wind Portfolio

3,600 megawatts of wind capacity across 76 facilities in North America, South

America, Europe and Asia

• Developed our first wind farm in 2006, and have since built a

high-quality, globally diversified wind business:

‒ Focused on areas with scarcity value

‒ Assets are located in high-value power markets

‒ Portfolio benefits from long-term, utility grade PPAs

‒ Tier 1 turbine equipment (GE, Siemens, Vestas,

Energcon

• High cash margins

• Zero fuel input cost

• Relatively low build cost and improving turbine efficiency

• Minimal ongoing capex requirements

• Simple to operate

• Outsourced O&M providers are available to financial buyers, supporting

our capital recycling program

Bahia, Brazil

Key Attributes Ballymartin, Ireland

33

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

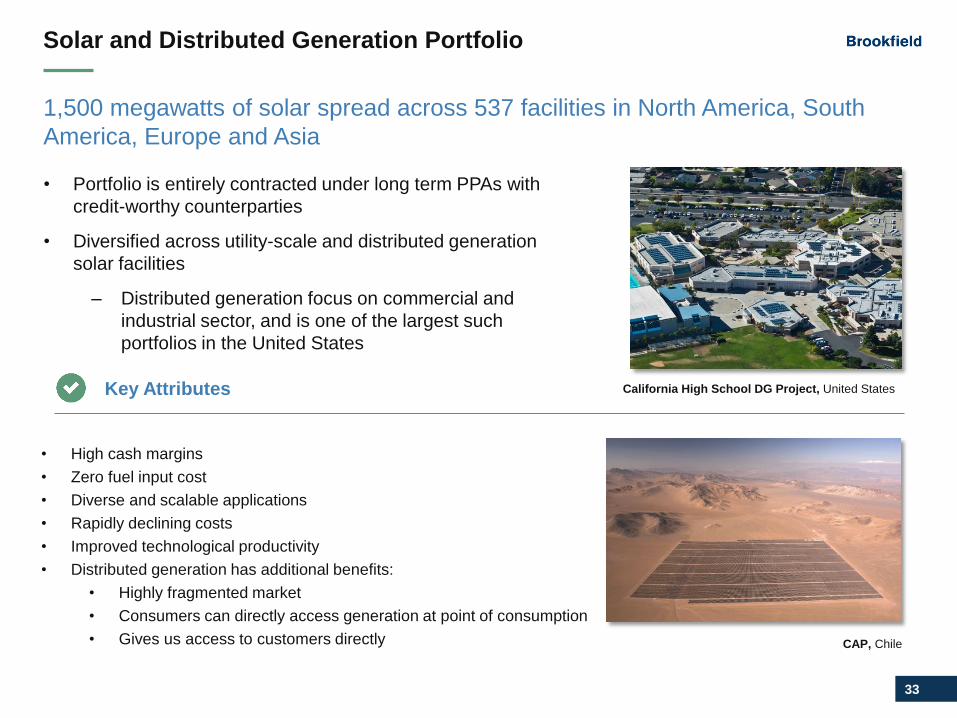

Solar and Distributed Generation Portfolio

1,500 megawatts of solar spread across 537 facilities in North America, South

America, Europe and Asia

• Portfolio is entirely contracted under long term PPAs with

credit-worthy counterparties

• Diversified across utility-scale and distributed generation

solar facilities

‒ Distributed generation focus on commercial and

industrial sector, and is one of the largest such

portfolios in the United States

CAP, Chile

Key Attributes California High School DG Project, United States

• High cash margins

• Zero fuel input cost

• Diverse and scalable applications

• Rapidly declining costs

• Improved technological productivity

• Distributed generation has additional benefits:

• Highly fragmented market

• Consumers can directly access generation at point of consumption

• Gives us access to customers directly

34

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

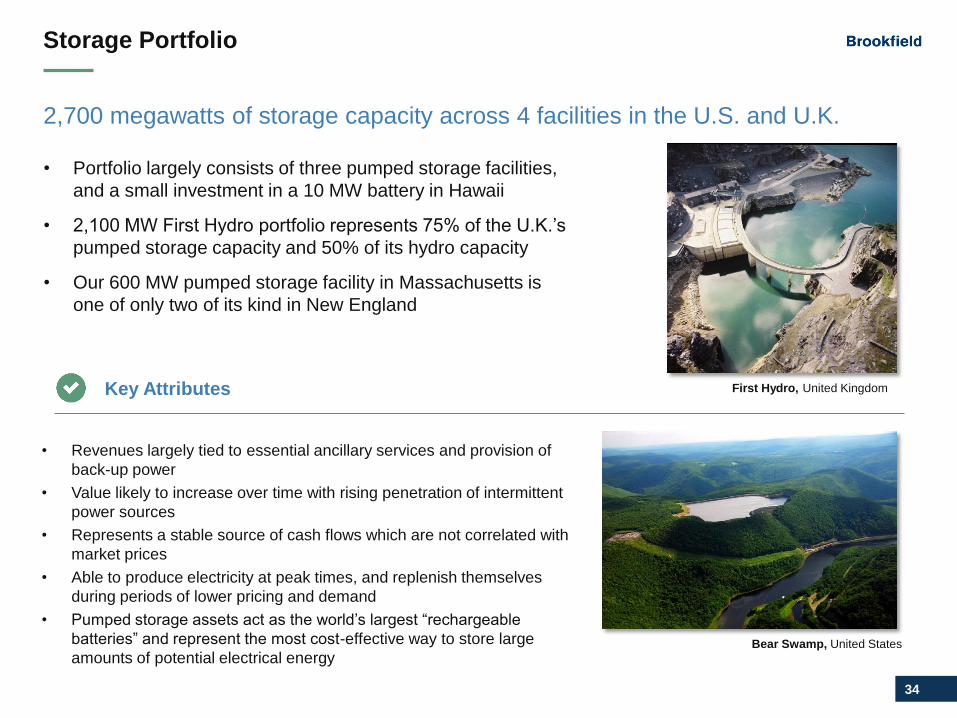

Storage Portfolio

2,700 megawatts of storage capacity across 4 facilities in the U.S. and U.K.

• Portfolio largely consists of three pumped storage facilities,

and a small investment in a 10 MW battery in Hawaii

• 2,100 MW First Hydro portfolio represents 75% of the U.K.’s

pumped storage capacity and 50% of its hydro capacity

• Our 600 MW pumped storage facility in Massachusetts is

one of only two of its kind in New England

Bear Swamp, United States

Key Attributes First Hydro, United Kingdom

• Revenues largely tied to essential ancillary services and provision of

back-up power

• Value likely to increase over time with rising penetration of intermittent

power sources

• Represents a stable source of cash flows which are not correlated with

market prices

• Able to produce electricity at peak times, and replenish themselves

during periods of lower pricing and demand

• Pumped storage assets act as the world’s largest “rechargeable

batteries” and represent the most cost-effective way to store large

amounts of potential electrical energy

35

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Corporate Structure

68%

Brookfield

Business

Partners (BBU)

Brookfield Asset Management (BAM)

~$43b Market Cap¹ (TSX, NYSE)

Management 20%

69%

Brookfield

Property

Partners (BPY)

30%

Brookfield

Infrastructure

Partners (BIP)

60%

Brookfield

Renewable

Partners (BEP)2

Private Fund LPs⁴

Company

A

Company

B

Company

C

Company

D

30%³

70%³

1) Based on closing price on the NYSE on December 29, 2017

2) BEP generally funds Brookfield’s commitment to renewables transactions in Private Funds

3) Indicative figure only, and subject to transaction size, co-investment, and other considerations

4) Indicative third-party commitments

36

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Governance

SENIOR MANAGEMENT TEAM

Sachin Shah Chief Executive Officer

Wyatt Hartley Chief Financial Officer

Brookfield Renewable has entered into a Master Services Agreement with Brookfield Asset Management

• Provides comprehensive suite of services to Brookfield Renewable Partners

• Base management fee of $20 million adjusted annually for inflation

• Equity enhancement fee equal to 1.25% of the increase in BEP’s capitalization

Incentive distributions based upon increases in distributions paid to shareholders over pre-defined thresholds

(Master Limited Partnerships (MLP) structure)

• 15% participation by Brookfield in distributions over $0.375/unit per quarter

• 25% participation by Brookfield in distributions over $0.4225/unit per quarter

Brookfield Renewable’s general partner has a majority of independent directors

Brookfield Renewable’s governance is structured to provide significant alignment of interests between Brookfield

Asset Management and unitholders

37

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Favourable Structure Relative to MLPs

Brookfield Renewable has not and is not expected to generate UBTI and ECI

• Brookfield Renewable is a Bermuda-based publicly traded partnership that indirectly

owns holding corporations in the U.S., Canada and other jurisdictions. Brookfield

Renewable is not a U.S. MLP1

• Chart below shows a comparison of Brookfield Renewable versus an MLP¹

1) MLP is Master Limited Partnership

2) Not all MLP’s are the same. This represents Brookfield’s understanding of common features with these types of vehicles

3) UBTI is unrelated business taxable income

4) ECI is effectively connected income

5) Source: Management estimates based on Barclays Capital Master Limited Partnerships MLP Trader Weekly

Brookfield Renewable MLP2

Type of entity Publicly traded partnership Publicly traded partnership

UBTI3 No Yes

ECI4 No Yes

U.S. tax slip issued K1 K1

Tax profile of distributions Benefits from return of capital Benefits from depreciation

Payout ratio ~70% of FFO 80%-90% of distributable cash flow5

Incentive distributions 25% maximum 50% maximum

38

Primary Font Colour

Title Slide Font

Light Background

R17 G17 B17

Dark Backdrop

R255 G255 B255

Business Group Colours

Real Estate

R71 G151 B181

Infrastructure

R83 G55 B82

Renewable

R92 G153 B121

Private Equity

R230 G203 B140

R244 G124 B16

R77 G77 B77

R200 G200 B200

R17 G17 B17

Logo & Divider Slide Font

R15 G53 B87

PRIMARY PALETTE

SECONDARY PALETTE

Sub-headers & Emphasis Text

R64 G126 B182

Leader in Green Energy & Sustainability

BEP is the largest member by market capitalization of the S&P/TSX Renewable Energy and Clean

Technology Index.

Since 2017, BEP has issued two green bonds through project-level financings for an aggregate

value of US$780 million. Citing BEP's environmental stewardship, commitment to renewable

power, and use of proceeds towards renewable power generation, the green bonds received E-1

Green Evaluation scores from S&P - the highest on its scale.

BEP is committed to sustainable development principles that reduce the impact of our operations

and help to manage the underlying water resources efficiently. Low Impact Hydropower Institute

(LIHI) certification is a voluntary certification program designed to help identify and provide market

incentives for hydropower operations that are minimizing their environmental impacts. BEP has

received LIHI certification for 52 hydro facilities across the US, more than any other operator,

making it the U.S. leader in low impact hydropower generation.

The Environmental Choice Program is a comprehensive national program sponsored by

Environment Canada. It certifies manufacturers and suppliers that produce products and services

that are less harmful to the environment. These bear the EcoLogo registered trademark. 22 of our

hydroelectric facilities in Ontario, Quebec, and British Columbia meet the strict standards of the

Environmental Choice Program.

The Brookfield Environmental Education Center was established in Guarani, Minas Gerais, Brazil,

from a partnership between Brookfield Energia Renovável and the local community. The project

aims to provide the entire population of the Pomba River Valley a place to develop environmental

education projects. To make the project sustainable, the local community was trained to manage

the Environmental Education Center and created a non-governmental organization to do it.