british columbia tree fruit industry - bc fruit growers ... tree fruit industry workshop - slides...

TRANSCRIPT

British Columbia Tree Fruit Industry

The road ahead?

Facilitators: Svan Lembke, Ph.D.Lee Cartier, P.Ag.

School of Business

Workshop Agenda9:00 - 9:15 Welcome and introduction

9:16 – 10:30 Summary of research findings

10:31 - 10:45 Refreshments break

10:46 - 11:30 Workgroup discussions – Opportunities and Challenges

11:31 - 12:00 Session debrief and summaries

2

Executive Summary• Economic assessment of financial information across different value

chains & 17 in-depth interviews with industry cluster stakeholders was carried out June – Nov 2016.

• Agriculture is a fundamental part of the Okanagan’s economy although compared to other industries, agricultural product exports are less than imports, despite a claim for exceptional quality that should encourage specialization and trade to new markets.

• Price volatility, product lifecycles, changes in market behaviours are mapped to industry responses and it becomes apparent that change and opportunities are not pro-actively managed.

• A multitude of opportunities are available to the industry and change seems inevitable.

© 2017, Cartier & Lembke 3

2016 Research Design• Confirmation of the current economic structures of the Okanagan

tree fruit value chains:

• Conventional Apples

• Organic Apples

• Cider

• Cherries

• Identification of major obstacles and barriers to growth and innovation in the Okanagan region:

• Internal cluster dynamics

• External drivers of change

Quantitative data sources

Qualitative data sources

© 2017, Cartier & Lembke 4

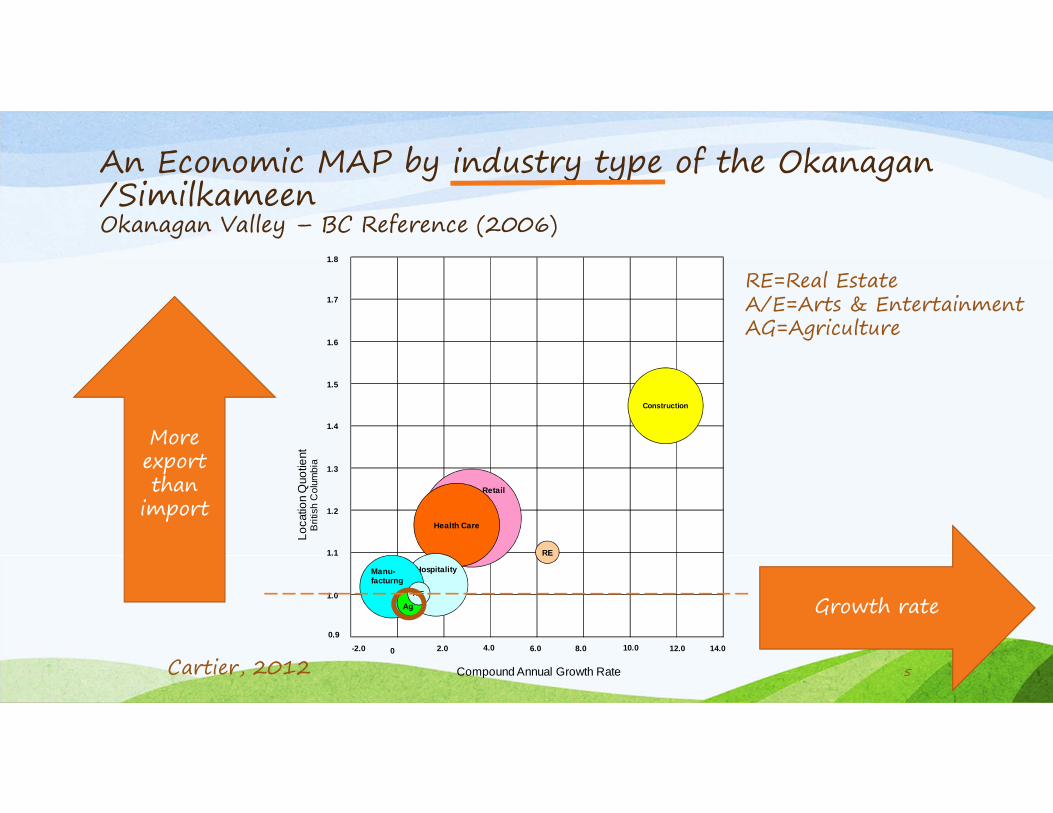

An Economic MAP by industry type of the Okanagan /SimilkameenOkanagan Valley – BC Reference (2006)

Cartier, 2012

Retail

Health Care

Hospitality

Loca

tion

Quo

tient

Brit

ish

Col

umbi

a

Compound Annual Growth Rate

1.0

0.9

1.1

1.2

1.5

1.4

1.3

1.6

0 2.0 4.0 6.0 8.0 10.0 12.0 14.0

Construction

RE

-2.0

1.7

Manu-facturng

Ag

1.8

A/E

More export than

import

Growth rate

RE=Real EstateA/E=Arts & EntertainmentAG=Agriculture

5

Industry Cluster Map Okanagan Valley – BC Reference

Cartier, 2012

Life Sciences

Hospitality & Tourism

Loc

atio

n Q

uotie

ntB

ritis

h C

olum

bia

Compound Annual Growth Rate

1.0

0.9

1.1

1.2

1.5

1.4

1.3

1.6

0 1.0 2.0 3.0 4.0 5.0-1.0

Ag. Products

Only three clustersAg Products Cluster has highest growth potential

6

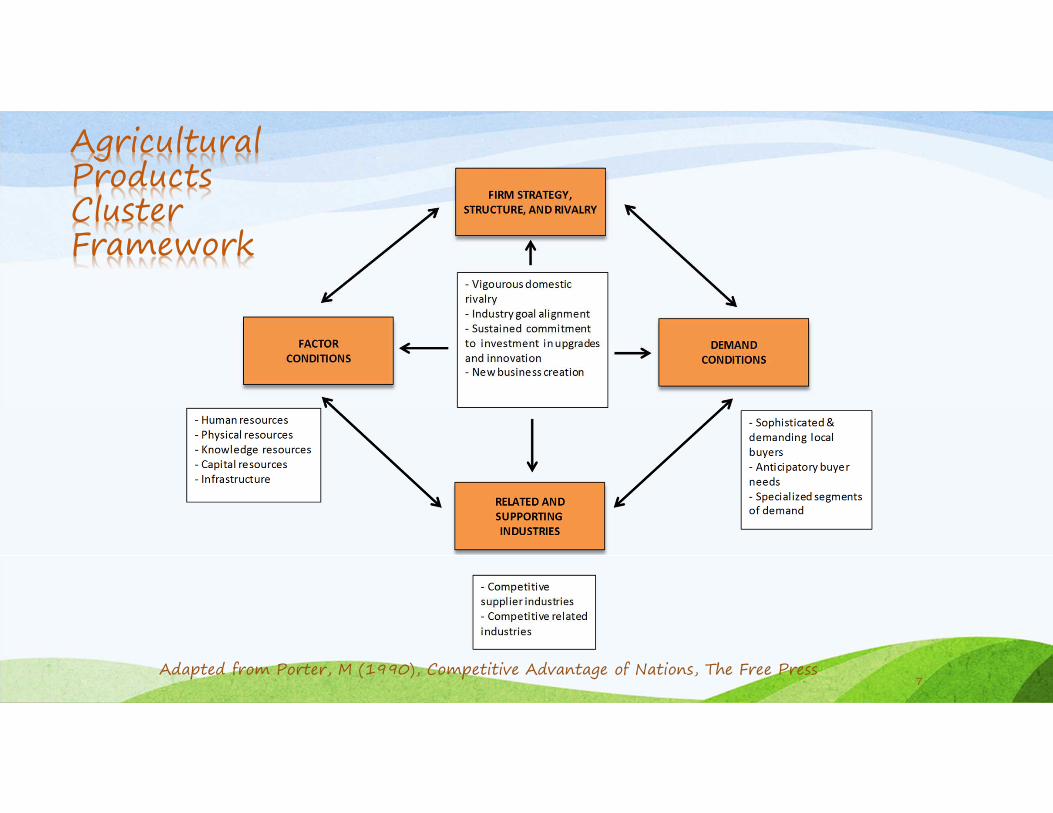

Agricultural Products Cluster Framework

Adapted from Porter, M (1990), Competitive Advantage of Nations, The Free Press7

Agricultural Products Cluster Sectors

1 Farm management services

2 Soil preparation services

3 Irrigation equipment & services

4 Processing and packaging machinery

5 Fertilizers

6 Farm primary products

7 Wine or brandy

8 Milling and refining products

9 Product distribution and wholesale services

10 Malt beverages

11 Specialty processed food products

12 Animal health products

13 Agricultural chemicals (excluding fertilizer)

14 Supplies distribution and wholesaling

15 Related financial services

16 Transportation and logistic services

17 Bulk packaging

18 Other related services

Cartier, 2012: Value Chain Analysis of the British Columbia Wine Industry8

The building blocks of the Agricultural Products industry cluster

• The tree fruit industry value chains

• The wine industry value chain (includes cider)

• Dairy and poultry value chains (north Okanagan)

Fixed land-base for agricultureChanges are on-going and are

influenced by value chain performance

© 2017, Cartier & Lembke 9

Okanagan Tree Fruit Value IndustryAn Industry in Transformation

Acres

2011 2006 2001 CAGR

Apples 8,677 10,005 13,430 -4.3%

Pears 479 602 753 -4.4%

Plums 314 323 311 0.1%

Cherries (sweet) 3,532 2,515 1,930 6.2%

Cherries (sour) 75 147 254 -11.5%

Peaches 1,209 1,387 1,357 -1.1%

Apricots 216 320 433 -6.7%

Grapes 9,515 6,589 4,831 7.0%

Total 24,017 21,888 23,299

© 2017, Cartier & Lembke 10

British Columbia Apple & Cherry Industry Value Chain - 2016

© 2017, Cartier & Lembke 11

British Columbia Cider Industry Value Chain - 2016

© 2017, Cartier & Lembke12

BC Apple Sales Volume, Price, Quality

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015

Pe

rce

nt

of

Pa

cke

d C

rop

Apple Quality - Selected Varieties

FCY or better Commercial Cull

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

40.0

45.0

50.0

2007 2008 2009 2010 2011 2012 2013 2014 2015

0.0

50.0

100.0

150.0

200.0

250.0

Do

lla

rs (

mil

lio

ns)

(Po

un

ds

(mil

lio

ns)

BCTF Apple Sales

Apple Sales Pounds Apple Sales Revenue

Volatility in apple prices (partially off-set by government programs)

© 2017, Cartier & Lembke 13

Historic Apple Prices

0.000

0.100

0.200

0.300

0.400

0.500

0.600

2007 2008 2009 2010 2011 2012 2013 2014

$ p

er

Po

un

dApple Prices - Selected Varieties

McIntosh Royal Gala Red Delecious

Honeycrisp Ambrosia Average - All Varieties

Linear (Red Delecious) Linear (Ambrosia)

New apple varieties are needed to keep average price high (lifecycle <20yrs)

© 2017, Cartier & Lembke14

Apple Sales by Geographic Market

0

20,000,000

40,000,000

60,000,000

80,000,000

100,000,000

120,000,000

140,000,000

160,000,000

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

100.0%

2008 2009 2010 2011 2012 2013 2014 2015

Po

un

ds

Pe

rce

nt

Channel Sales Percentage

Apples

Local Canadian U.S. Export Pounds

0.000

0.100

0.200

0.300

0.400

0.500

0.600

0.700

0.800

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

2008 2009 2010 2011 2012 2013 2014 2015

$/p

ou

nd

$/p

ou

nd

Channel Sales $/pound

Apples

Local Canadian U.S. Export Average

Sales process does not seem to follow attractive markets

© 2017, Cartier & Lembke15

17 In-depth Interviews (with innovative stakeholders in the cluster)

12

2

3

Interview sample distribution

Apples Cherries Other

Where is the apple stakeholder’s main focus

and attention?

© 2017, Cartier & Lembke16

Industry Key Success Factors

N Minimum Maximum MeanStd.

Deviation

product_number 14 2 5 3.86 0.864

product_frequency 14 2 5 3.79 0.893

technology_changes 14 2 5 3.86 0.770

distribution_channels 14 3 5 4.07 0.829

competitor_aggression 14 2 5 3.79 0.975

internet_usage 14 1 5 3.50 1.454

local_access 14 2 5 3.64 0.929

External force

© 2017, Cartier & Lembke 17

Focus on Marketing vs Technical Innovation

Focused Primarily on Technical Strength

Technical Somewhat More than Marketing

About Equally Balanced

Marketing Somewhat more than Technical

Focused Primarily on Marketing Strength?

Not a strong focus on marketing

© 2017, Cartier & Lembke18

0

1

2

3

4

Conventional

Apples

Organic Apples Cherries Other

Marketing vs Technical across Value Chains

Focused Primarily on Technical Strength

Technical Somewhat More than Marketing

About Equally Balanced

Marketing Somewhat more than Technical

© 2017, Cartier & Lembke 19

Strategic importance to the business

N Minimum Maximum MeanStd.

Deviation

product_price 14 3 4 3.71 0.469

product_differentiation 14 3 5 4.21 0.802

innovativeness 14 3 5 4.14 0.535

marketing_mix 14 3 5 3.86 0.663

production_process 14 3 5 4.21 0.699

production_costs 14 3 5 4.00 0.679

Internal focus

© 2017, Cartier & Lembke 20

Apple Producer MarginExisting Planting Yields

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

-0.100

0.000

0.100

0.200

0.300

0.400

0.500

0.600

2007 2008 2009 2010 2011 2012 2013 2014 2015

$ p

er

Acr

e

$ p

er

Po

un

d

Conventional Apple Production

Margin/lb Average cost / Lb Average price/lb Margin/Acre

Average Apple Yield: 30.5 Bins/AcreAverage Organic Yield: 27.5 Bins/Acre

Is this a realistic yield for organic production?

This is the historic yield for conventional production?

© 2017, Cartier & Lembke 21

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

0.000

0.200

0.400

0.600

0.800

1.000

1.200

1.400

2011 2012 2013 2014 2015

$ p

er

Acr

e

$ p

er

Po

un

d

Organic Apple Production

Margin/lb Average cost / Lb Average price/lb Margin/Acre

Apple Orchard Densities

Low density: <400 trees/acMedium density: 401 - 1,000 trees/acHigh density: >1,000 trees/ac

Low 36%

Medium 32%

High 32%

Apple Orchard Densities

Low Medium High Sample Acres

Zone 1 3,754

Zone 2 590 525 331 1,446 2,947

Zone 3 211 174 377 762 1,590

801 699 708 2,208 8,290

Cartier 2014:Source SIR program data22

Apple Production Margin OpportunitiesExisting Yields Compared to Super Spindle Yields

30 Bins/Acre 50 Bins/Acre 75 Bins/Acre

Average price/lb 0.226 0.226 0.226

Average cost / Lb 0.186 0.121 0.088

Margin/lb 0.040 0.105 0.138

Margin/Acre 1,260.87 5,529.22 10,891.13

18%

46%61%

82%

54%39%

100% 100% 100%

0

2,000

4,000

6,000

8,000

10,000

12,000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$ p

er

Acr

e

Pe

rce

nt

of

$ p

er

Po

un

d

Potential Conventional Apple Margins

© 2017, Cartier & Lembke 23

25 Bins/Acre 45 Bins/Acre

Average price/lb 0.626 0.626

Average cost / Lb 0.255 0.200

Margin/lb 0.371 0.426

Margin/Acre 7,415.87 15,322.99

59%68%

41%32%

100% 100%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$ p

er

Acr

e

Pe

rce

nt

of

$ p

er

Po

un

d

Potential Organic Apple Margins

Packing and Shipping Cost StructureApples - Existing and Potential Yields

0.0

50.0

100.0

150.0

200.0

250.0

300.0

350.0

400.0

2015 50 Bins/Acre 75 Bins/Acre

Do

lla

rs (

mil

lio

ns)Packinghouse Cost Structure

Income

Cost of sales

Shipping

Labour cost

Materials cost

Apple cost

Overhead

Net sales

Costs indicate little change in sales approach

© 2017, Cartier & Lembke24

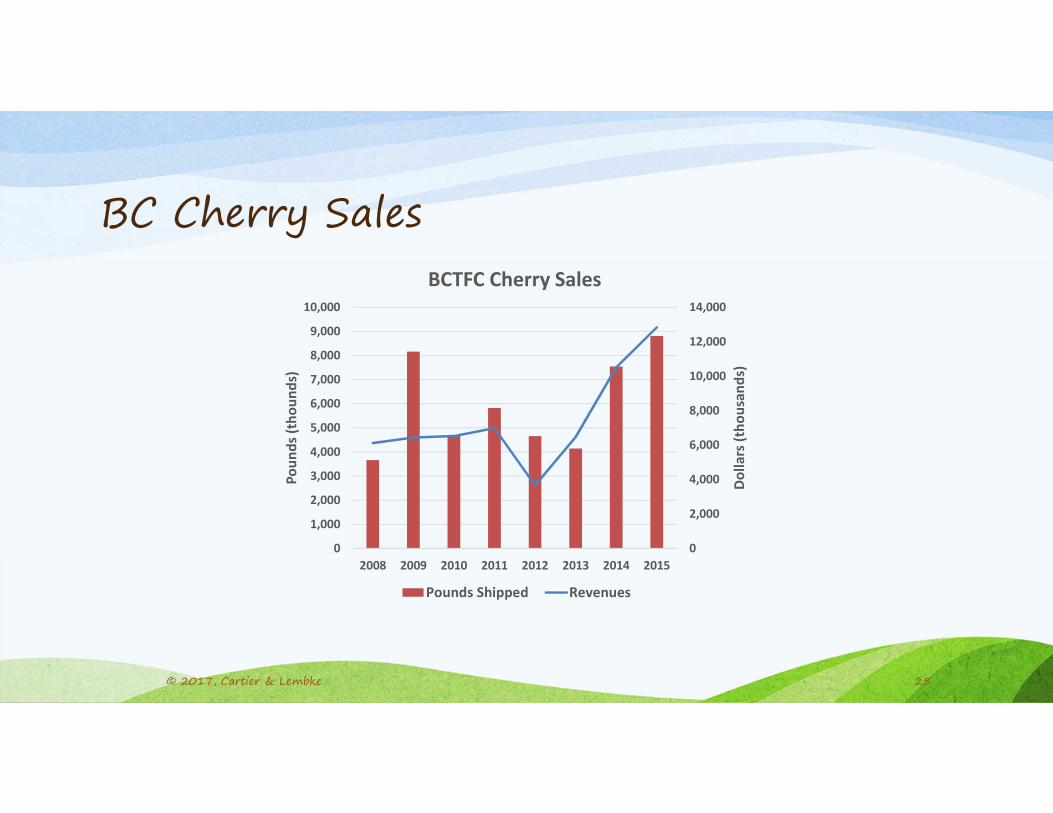

BC Cherry Sales

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

9,000

10,000

2008 2009 2010 2011 2012 2013 2014 2015

Do

lla

rs (

tho

usa

nd

s)

Po

un

ds

(th

ou

nd

s)BCTFC Cherry Sales

Pounds Shipped Revenues

© 2017, Cartier & Lembke 25

Cherry Sales by Geographic MarketBCTFC

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

2008 2009 2010 2011 2012 2013 2014 2015

$/p

ou

nd

$/p

ou

nd

Channel Sales $/pound

Cherries

Local Canadian U.S. Export Average

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

70.0%

80.0%

90.0%

2008 2009 2010 2011 2012 2013 2014 2015

Po

un

ds

Pe

rce

nt

Channel Sales Percentage

Cherries

Local Canadian U.S. Export Pounds

Large independent cherry producers are vertically integrated. In contrast to BCTFC 80% of their crop is exported out of Canada and 20% is sold across Canada

© 2017, Cartier & Lembke26

Cherry Producer Margin

-4,000

-3,000

-2,000

-1,000

0

1,000

2,000

3,000

4,000

-1.00

-0.50

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2008 2009 2010 2011 2012 2013 2014 2015

$ p

er

Acr

e

$ p

er

Po

un

dCherry Production Margin

Margin/lb Average cost / Lb Average price/lb Margin/Acre

Average Cherry Yield: 12,000 pounds/Acre

An even more volatile market

Are 12-18,000 pounds/acre possible?

© 2017, Cartier & Lembke 27

Cherry Production Margin OpportunitiesExisting Yields Compared to High Density Yields

© 2017, Cartier & Lembke 28

12,000 Lbs/Ac 20,000 Lbs/Ac

Average price/lb 1.232 1.232

Average cost / Lb 0.830 0.658

Margin/lb 0.402 0.574

Margin/Acre 4,821 11,473

33%47%

67%53%

100% 100%

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

$/A

cre

$/P

ou

nd

Potential Cherry Production Margins

Packing and Shipping Cost StructureCherries

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2015

Do

lla

rs (

tho

usa

nd

s)

Packinghouse Cost Structure

Revenue

Cost of sales

Shipping

Labour cost

Materials cost

Cherry cost

Overhead

Net sales

© 2017, Cartier & Lembke 29

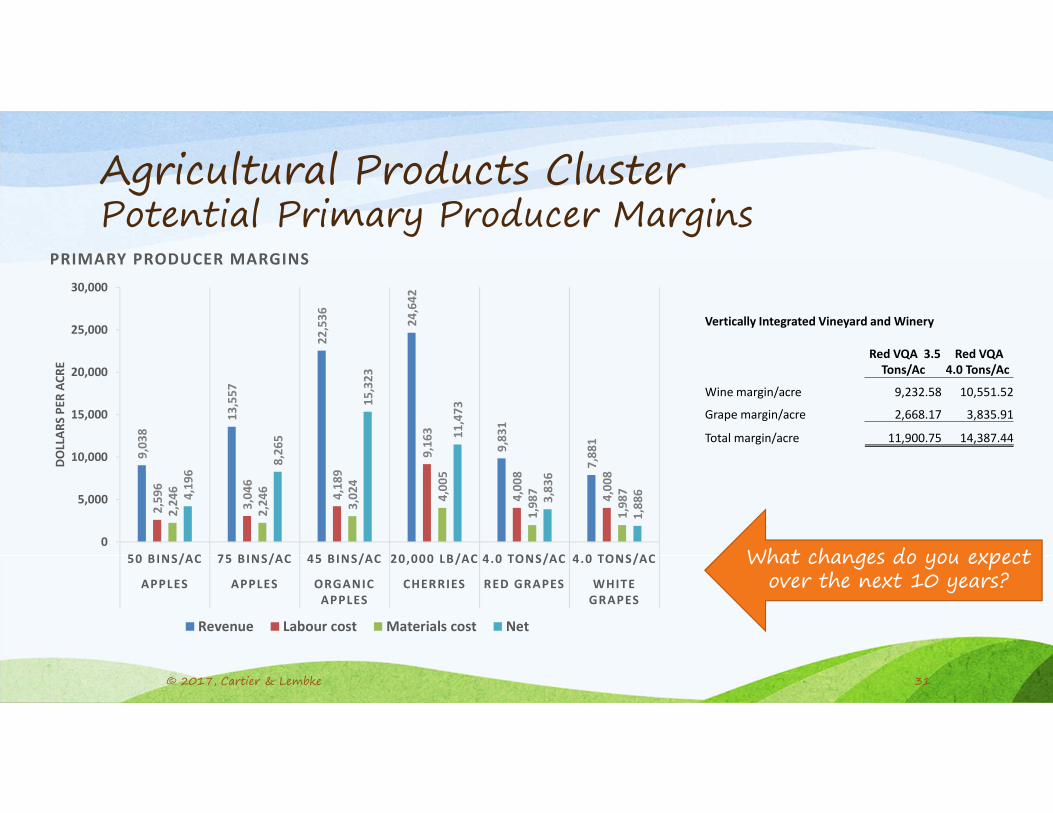

Agricultural Products ClusterCurrent Primary Producer Margins

Vertically Integrated Vineyard and Winery

Red VQA 3.5

Tons/Ac

Red VQA

4.0 Tons/Ac

Wine margin/acre 9,232.58 10,551.52

Grape margin/acre 2,668.17 3,835.91

Total margin/acre 11,900.75 14,387.44

© 2017, Cartier & Lembke 30

5,4

41

12

,52

0 14

,78

5

8,6

02

6,8

96

2,2

38

2,6

53

6,1

23

3,9

47

3,9

47

2,2

46

2,4

51 3,8

41

1,9

87

1,9

87

95

7

7,4

16

4,8

21

2,6

68

96

2

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

30 BINS/AC 25 BINS/AC 12,000 LB/AC 3.5 TONS/AC 3.5 TONS/AC

APPLES ORGANIC

APPLES

CHERRIES RED GRAPES WHITE

GRAPES

DO

LLA

RS

PE

R A

CR

E

PRIMARY PRODUCER MARGINS

Revenue Labour cost Materials cost Net

Agricultural Products ClusterPotential Primary Producer Margins

Vertically Integrated Vineyard and Winery

Red VQA 3.5

Tons/Ac

Red VQA

4.0 Tons/Ac

Wine margin/acre 9,232.58 10,551.52

Grape margin/acre 2,668.17 3,835.91

Total margin/acre 11,900.75 14,387.44

What changes do you expect over the next 10 years?

© 2017, Cartier & Lembke 31

9,0

38

13

,55

7

22

,53

6

24

,64

2

9,8

31

7,8

81

2,5

96

3,0

46

4,1

89

9,1

63

4,0

08

4,0

08

2,2

46

2,2

46

3,0

24

4,0

05

1,9

87

1,9

874,1

96

8,2

65

15

,32

3

11

,47

3

3,8

36

1,8

86

0

5,000

10,000

15,000

20,000

25,000

30,000

50 BINS/AC 75 BINS/AC 45 BINS/AC 20,000 LB/AC 4.0 TONS/AC 4.0 TONS/AC

APPLES APPLES ORGANIC

APPLES

CHERRIES RED GRAPES WHITE

GRAPES

DO

LLA

RS

PE

R A

CR

E

PRIMARY PRODUCER MARGINS

Revenue Labour cost Materials cost Net

Strategic Context: Organic Apples

© 2017, Cartier & Lembke 32

Demand Supply?6% of apple production is organic (Washington)

3% of apple production is organic (BC)

Demand meets

supply at 12%

production

Taylor, M & Granatstein, D. (2013) ‘A Cost Comparison of Organic and ConventionalApple Production in the State of Washington’, Plant Management Network.

(10-13% more costly)

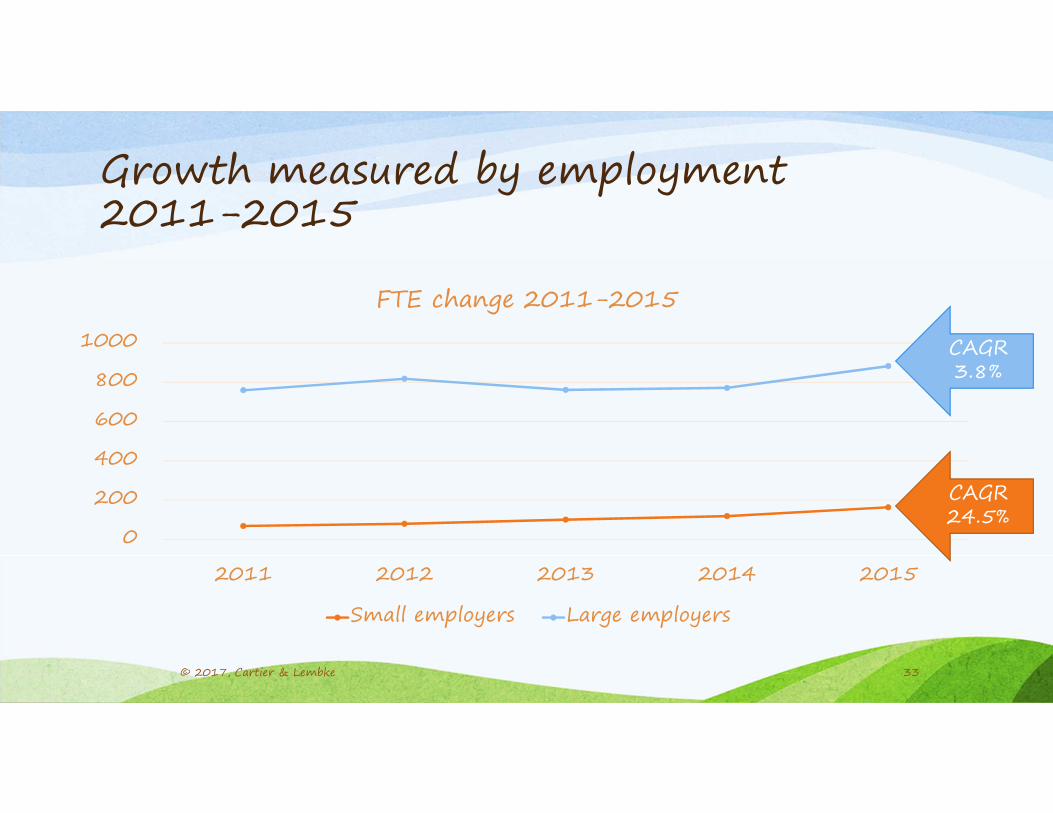

Growth measured by employment 2011-2015

0

200

400

600

800

1000

2011 2012 2013 2014 2015

FTE change 2011-2015

Small employers Large employers

CAGR 24.5%

CAGR 3.8%

© 2017, Cartier & Lembke 33

Small Innovation Moderate Innovation

Radical Innovation Vertical Integration

New Varieties

Small to moderate innovation is most frequent

What kind of growth initiative are we seeing?

© 2017, Cartier & Lembke 34

Defensive, we react to competitor actions or customer demands?

© 2017, Cartier & Lembke35

0

1

2

3

4

5

Conventional

Apples

Organic Apples Cherries Other

Perceived industry prospects

industry_prospects Neither pessimistic nor optimistic

industry_prospects Somewhat optimistic

industry_prospects Very optimistic

?

© 2017, Cartier & Lembke 36

Okanagan Apple Cider

• Wine and Cider Demand

• Price and Per-capita Consumption

• Price and Per-capita Consumption Growth

• Price Elasticity of Demand

© 2017, Cartier & Lembke 37

Wine and Cider Demand

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

18.00

20.00

11.20 11.40 11.60 11.80 12.00 12.20 12.40 12.60 12.80 13.00

Pe

r C

ap

ita

Qu

an

tity

So

ld (

L)

Price/L

Total Wine

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

3.80 3.90 4.00 4.10 4.20 4.30 4.40 4.50 4.60 4.70 4.80

Pe

r C

ap

ita

Qu

an

tity

So

ld (

L)Price/L

Coolers & Cider

© 2017, Cartier & Lembke 38

Price and Per-capita Consumption

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

5.00

1998 2001 2004 2006 2009 2012 2014 2017

$/L

itre

Time

Coolers & Cider Price

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

1998 2001 2004 2006 2009 2012 2014 2017

Pe

r C

ap

ita

Qu

an

tity

So

ld (

L)

Time

Coolers & Cider Consumption

© 2017, Cartier & Lembke 39

Cider Price and Per-capita Consumption

Minimum Maximum Mean SD

Cider Price/L 3.93 4.68 4.38 0.238

Cider Per-capita Consumption (Liters) 5.00 8.78 6.35 0.867

© 2017, Cartier & Lembke 40

Comparison of Price and Per-capita Consumption Growth

CAGR (2000 -2014)

Cider/Cooler Price -0.87%

Total Wine Price 0.61%BC VQA Price 1.62%

Foreign Imports Price 2.29%

CIC Price 1.73%

Beer Price 0.41%

Cider/Cooler Consumption 4.11%

Total Wine Consumption 3.59%BC VQA Consumption 8.46%

Foreign Imports Consumption 2.53%

CIC Consumption 3.20%

Beer Consumption -0.63%

© 2017, Cartier & Lembke 41

Cider is not like wine!

Key to success is marketing

Price Elasticity of Demand• An economic concept that measures the responsiveness of the quantity

demanded of a good to a change in its price when all other influences remain constant.• Price elasticity is measure of a consumers sensitivity to price

• Products are either:• Price elastic: an small % change in price results in a large % change in demand• Unit elastic: a 1% change in price results in a 1% change in demand• Price inelastic: a large % change in price results in a small % change in demand

• Why is Elasticity of Demand important in this study?• Lower priced generic products typically exhibit higher elasticity of demand (more

price elastic) than higher priced specialty (luxury) products of the same type (more price inelastic)

• Brand identity lowers price elasticity (products are become more price inelastic), consumers become less sensitive to price increases.

© 2017, Cartier & Lembke 42

Price Sensitivity in Market Segments

• Cider is price inelastic.• Strong brand identity makes wine consumers less sensitive to price

increases

• Brand identity decreases price elasticity: these products become price inelastic and consumers become less price sensitive

Price/Litre Price Elasticity

Cider 4.38 0.891

© 2017, Cartier & Lembke 43

Together we are strong!

How can the cluster

environment deliver

strength?

© 2017, Cartier & Lembke 44

© 2017, Cartier & Lembke 45

Demand Conditions

(Markets)

Rival Firms

(Exporters)

Support and

Related Industries

(Suppliers)

Factor Conditions

(Foundation Level)

AGRICULTURAL PRODUCTS CLUSTER

Local Market

Cideries

Conventional

Packers &

Shippers

Organic

Packers &

Shippers

Canada International

Cherry

Growers

Farm Management Services

Soil Preparation Services

Irrigation Equipment

Processing & Packaging

Equipment

Fertilizer

Distribution & Wholesaling

ServicesSpecialty manufacttured Food

Products & Services

Agricultural

Chemicals

Related Financial ServicesTransportation & Logistics

Services

Okanagan

College

BCWI &

BCWA

Physical

Infrastructure

Local

Government

BCFGABC LDB &

BC LLC

SR&DC

BC Ministry of

Agriculture

UBCO

Irrigation Services

Provided by local suppliers

Imported into the region

Mixed local and imported

Legend

© 2017 Lee Cartier, Svan Lenbke

Organic Apple

Growers Conventional

Apple Growers

Rest of Canada

CherriesConventional

Apples

Organic

Apples

U.S. China OhersBC Market

Fruit

Processors

Nutraceuticals?

Health?

Other?

CherriesConventional

Apples

Organic

ApplesCider

Fruit

Products

Demand conditions: Which markets are we targeting?

Are we leveraging our

connections and brand

awareness?

© 2017, Cartier & Lembke 46

Importance of Trade Agreements

Not an opportunity for any business in the industry

Potentially an opportunity for the industry but unlikely to be an

opportunity for my business`

Potentially an opportunity for my business if we as a business or the

Canadian government take certain actions

Definitely an opportunity if we as a business or the Canadian

government take certain actions

Definitely an opportunity

Not an opportunity

A significant opportunity and we already have a plan?© 2017, Cartier & Lembke

47

Rival Firms: How well do we work together?

Clusters benefit from spill-over effects of knowledge, innovation and alliances.

© 2017, Cartier & Lembke 48

Support and Related Industries: How well do we work together?

Support and related industry stakeholders are hesitant to grow their business in the Okanagan.

© 2017, Cartier & Lembke 49

Support and

Related Industries

(Suppliers) Cherry

Growers

Farm Management Services

Soil Preparation Services

Irrigation Equipment

Processing & Packaging

Equipment

Fertilizer

Distribution & Wholesaling

ServicesSpecialty manufacttured Food

Products & Services

Agricultural

Chemicals

Related Financial ServicesTransportation & Logistics

Services

Irrigation Services

Provided by local suppliers

Imported into the region

Mixed local and imported

Legend

Organic Apple

Growers Conventional

Apple Growers

Conventional Apples: Sharing of information

There is no sharing of important information

Some of the industry players have in the past shared some important

information

Some of the industry players or associations have in the past shared some

information and have made some joint decisions

Key industry players and associations actively seek each other out to share

information

Limited ‘spill over’ effects

Key industry players and industry associations drive knowledge sharing and industry-wide decision making beyond their own benefits© 2017, Cartier & Lembke 50

Factor Conditions: How well do we work together?

Simple, single-action policy and decision making rarely works for complex market and cluster dynamics.

© 2017, Cartier & Lembke 51

What is our strategy?

Organic apples

Foundations of Strategy (Canadian Edition)’ (2015) R.M. Grant, J. Jordan and P.R.

© 2017, Cartier & Lembke 52

Demand Conditions

(Markets)

Rival Firms

(Exporters)

Support and

Related Industries

(Suppliers)

Factor Conditions

(Foundation Level)

AGRICULTURAL PRODUCTS CLUSTER

Local Market

Cideries

Conventional

Packers &

Shippers

Organic

Packers &

Shippers

Canada International

Cherry

Growers

Farm Management Services

Soil Preparation Services

Irrigation Equipment

Processing & Packaging

Equipment

Fertilizer

Distribution & Wholesaling

ServicesSpecialty manufacttured Food

Products & Services

Agricultural

Chemicals

Related Financial ServicesTransportation & Logistics

Services

BC LDB & BC Ministry of

Irrigation Services

Provided by local suppliers

Imported into the region

Mixed local and imported

Legend

Organic Apple

Growers Conventional

Apple Growers

Rest of Canada

CherriesConventional

Apples

Organic

Apples

U.S. China OhersBC Market

Fruit

Processors

Nutraceuticals?

Health?

Other?

CherriesConventional

Apples

Organic

ApplesCider

Fruit

Products

2 opportunities

2 related opportunities Diversification

Develop new profitable export markets

Build a strong unique brand

Increase yields and maintain quality

Focus on specific ‘quality’ criteria

Lower quality product

management

© 2017, Cartier & Lembke

53

Four potential strategic opportunities for conventional apple production1. Increase the yield per acre with good quality and re-plant new

varieties where possible, and hope for high apple prices and government support programs

2. Focus on the ‘high quality fruit’ brand by removing any lower quality (and cheaper) BC apples from the market (eg into cider production) leaving the lower cost market for imported apples.

3. Follow the cherries and develop export markets for high quality apples as a luxury good.

4. Follow the organic apple producers and build a low pesticide brand for the growing demand of high quality (healthy) fruit

© 2017, Cartier & Lembke 54

Let’s Get to Work: The Workshop Process

• You chose your own group

• Each group will be asked to develop a strategy for one or more of the opportunities identified from the research

• Each groups will present their strategy

• There will be discussion to summarize the strategies and possible next steps

• You will receive a summary of the research and workshop findings

55

Group Discussion: 30 minutes

56

Strategic Opportunity

Increase the yield

per acre with good

quality and re-

plant new varieties

where possible

Desired Outcomes

10 minutesStrategy / Strategies

20 minutes

Present

Four potential strategic opportunities for conventional apple production1. Increase the yield per acre with good quality and re-plant new

varieties where possible, and hope for high apple prices and government support programs

2. Focus on the ‘high quality fruit’ brand by removing any lower quality (and cheaper) BC apples from the market (eg into cider production) leaving the lower cost market for imported apples.

3. Follow the cherries and develop export markets for high quality apples as a luxury good.

4. Follow the organic apple producers and build a low pesticide brand for the growing demand of high quality (healthy) fruit

© 2017, Cartier & Lembke 57

Not all opportunities are mutually exclusive – a combination can be selected

Increase the yield per acre with good quality and re-plant new varieties where possible

• Outcomes (broad differentiation):

• Partnering with retailers for new varieties (input and commitment)

• Increased yield and quality from growers

• Increased prices for consumers (increased returns to the industry)

• Strategies (broad differentiation):

• Industry needs to coordinate their efforts:

• Develop a strategy for uniqueness/differentiation & a plan for execution

• Agree new bi-directional contracts to plant acres & sell specific varieties

© 2017, Cartier & Lembke 58

Workshop Group 1:

Focus on the ‘high quality fruit’ brand by removing any lower quality BC apples from the market

• Outcomes (focused differentiation):

• Increase returns to growers (30c/lb net return; assume no change in production cost)

• Predictable quality from growers (low volumes but high return varieties)

• Strategies (focused differentiation):

• Focus on growing low volume but high return varieties

• Enforce grade segregation with clear standards for quality

• Work with retailers on brand specific programs

• Triple investment in a pro-active sales approach and marketing

© 2017, Cartier & Lembke 59

Workshop Group 2:

Ensure growers are involved and agree on strategy (trigger psychological change)

Follow the cherries and develop export markets for high quality apples as a luxury good

• Outcomes:

• Increase in exports (100% over 3 years)

• Strategies:

• Leverage the Canada brand for food safety

• Cultivate and increase quality of production

• Active marketing and lobbying for government support

• Need international trade expert (hire)

• Send apple representative globally (use Canadian trade commission)

• Work closely with Summerland research station to develop new high quality varieties

© 2017, Cartier & Lembke 60

Workshop Group 3:

Explore opportunities to change property tax policy & subsidy programs to support export strategy

Follow the organic apple producers and build a low pesticide brand for high quality (healthy) fruit

• Outcomes:1. More organic growers (supply 12% of Canadian market with organic apples)

2. Lead the development of organic cherry production (and sales)

3. 10% of conventional apples grown in BC meet IPM standards

4. 50% of Canadian and 100% of Export market know that Canada is #1 in food safety

• Strategies:1. Increased education and ‘active recruitment’ of growers

2. More research on pest management for cherries

3. Develop an IPM standard and credible monitoring / certification

4. Develop a credible food safety rating system and adherence for all stakeholders along the value chain (including retailers)

© 2017, Cartier & Lembke 61

Workshop Group 4:

Conclusion: Evaluation of opportunitiesThere is a multitude of opportunities across the different stakeholder groups and working together will achieve better leverage of resources and increase chance of success.

1. A new strategic approach is needed. The BCFGA can trigger the process but development and execution of the plan will have to be led by the BCTFC and independent growers.

2. A better understanding of new market developments and involvement of the grower community are essential for buy-in and success. This cannot be achieved without industry champions. They have to be identified first!

3. Investment is needed to pursue the opportunities, especially for better marketing of BC tree fruits. Much of this investment may come from government but only when offering a clear focus and commitment to a plan. Our next step has to be a collaborative development of this plan.

© 2017, Cartier & Lembke 62