bristol myers squibb co - washburn university into a next generation biopharma company. bmy faces a...

TRANSCRIPT

Student Investment Fund Stock Report Analysts: Mat Overbaugh & Zachary Wilson

Bristol‐Myers Squibb CoNYSE: BMY

Recommendation: Buy/Limit Order

Market Cap: $50.28B

Recent Price: $25.38 (11/27/09)

Target Price: $24.38

Sector: Healthcare

Sub‐Sector: Drug Manufacturers

Overview and Highlights

Bristol‐Myers Squibb is a leading

worldwide healthcare company

focused on the development and

sale of name‐brand

pharmaceuticals.

With fifty‐one drugs, BMY has an

above‐average pipeline with

compounds that have

blockbuster potential in key

therapeutic areas

BMY has increased or maintained

dividend payments every year for

thirty‐nine years, even during

periods that saw earnings per

share decline.

BMY has a solid and proven track

record of cutting costs and is on

pace to achieve $2.5B in annual

cost savings by 2012.

BMY is set to finish FY 2009 with

$10B in cash on the balance

sheet.

BMY is currently divesting out of

all non‐biopharma assets to

transform into a next generation

BioPharma company.

BMY faces a steep patent cliff

through 2015. Patent expirations

of key drugs Plavix, Abilify, and

Avapro will put over 30% of

BMY’s TTM revenue at risk.

Investment Thesis

Worldwide, the Pharmaceutical business is around $785B. IMS Health, a

leading provider of market healthcare research, predicts an annual growth

rate of 4% ‐ 7%.

Bristol‐Myers has taken aggressive measures to combat the patent cliff, an

industry wide problem in which the R&D engine cannot create new products

to fill voids left by patent expirations on existing drugs.

With a healthy ROIC v. WACC spread protected by legal patents, BMY

continues to create and deliver value to shareholders with a sustainable

5.01% dividend yield.

While healthcare reform remains a risk, prescription medication remains the

most cost‐effective treatment method used by modern medicine.

Financial Statistics vs. the Industry

Insider Trading – Net Purchases

Recommendation

Limit Order with a $24.15 Strike

Price

Economic Summary & Industry Analysis

Economic fundamentals remain weak with unemployment

over 10% and consumer spending down significantly. While

there are many things people have chosen to live without in

the downturn, pharmaceutical isn’t one of them. Throughout

the down economy revenue of pharmaceutical companies

has continued to grow. The resiliency of pharmaceutical

sales, strong cash flows, and attractive dividend yields make

the bio‐pharma sector an attractive choice in uncertain

economic times. The chart shows the outperformance of the

bio‐pharma index vs. S&P 500 over the past two years.

An aging world population will fuel consistent growth in

pharmaceutical sales. Despite the near term domestic threat

of healthcare reform, the pharmaceutical industry is

positioned to increase revenues over the next several

decades thanks to a rapidly aging world population that is

increasingly dependent on life‐extending medication.

The United Nations projects that the number of people over

the age of sixty will nearly quadruple by 2050 to almost 2

billion. An aging population requires more medication to stay

healthy and active.

Source: United Nations

The average number of prescriptions filled annually by age

group shows the explosive growth in prescriptions filled for

the 65+ age group.

Source: Kaiser Family Foundation (www.statehealthfacts.org)

It’s important to note that pharmaceutical products sold by

Bristol‐Myers extend life. Even in a down economy, people

will pay for life‐saving medication.

The pending patent cliff over the next 10 years is an industry

wide problem. Across the industry over $74B worth of

branded drugs will lose patent protection by 2012. The fast

approaching patent cliff has led healthy companies to pursue

acquisition and licensing strategies instead of internal

product development to expand their pipeline and get drugs

to market more quickly. Many major drug companies have

turned to diversification to help cushion the revenue blow of

the pending patent cliff. This plan provides for more

consistent revenue but at the cost of operating margins. The

other path, the one BMY has undertaken, is to focus on core

competencies, cut costs, aggressively expand margins, and

grow the pipeline through pharmaceutical and biologic

acquisitions. Roughly half of the acquisitions by big

pharmaceutical over the past decade have been in “ex‐

pharmaceutical” sectors such as OTC products, medical

devices, animal health, and retail pharmacy. However, firms

that have 90% or more of 2008 revenues from

pharmaceutical sales had above average margins, where

those that have diversified showed below average operating

margins. The fury of acquisitions in big pharmaceutical is

likely to continue as each company continues on its respected

path to dampen the impacts of the pending patent cliff.

Healthy cash rich companies, like BMY, will be the ones that

take full advantage of current tight credit markets to continue

to expand pipelines or diversify through acquisitions.

Domestic healthcare reform could completely change the

healthcare system, including pharmaceuticals. The current

health care reform under consideration includes a Medicare

Part D clawback, public plan option, Medicare/Medicaid cuts,

and legislation for the approval of biosimilars to name a few

of its points. Significant changes are likely to directly affect

the pharmaceutical industry. This includes fees to help cover

the “donut hole” in Medicare Part D. Pharmaceutical

companies are also at risk from decreased subsidies from

Medicare/Medicaid, increasing pressure for use of generics,

and the push through of biosimilar legislation. These areas of

reform would negatively impact the industry. However, big

pharmaceutical has taken an active role in the legislative

process thus far. PhRMA, the biggest trade association for

the prescription drug industry, worked directly with President

Obama to get a compromise in place. The current deal that

has been struck calls for an $80B payment from

pharmaceutical companies that will cover costs not covered

by Medicaid. While this is viewed as a compromise between

congress and PhRMA, the street has viewed it as a win for big

pharma. Geographical diversification will also play a part in

what percent of revenues are at stake for reform. BMY’s

international revenue represented 42% of total TTM sales

Financial Modeling

Modeling Approach

When modeling Bristol‐Myers several assumptions were used

to ensure BMY represents a sound investment for the

Washburn Student Investment Fund. Our assumptions

assume a less than ideal environment for BMY.

Our model assumed a 2.5% terminal growth rate and used an

increased beta. Additionally, we increased SG&A, R&D and

Net PPE. This would represent a reversal to a successful cost

cutting trend (the Productivity Transformation Initative,

above) but would serve to dampen valuations by increasing

the cost of capital and decreasing effeciency on the balance

sheet.

We used an average revenue growth slightly below 5%. This is

below Thompson‐Baseline’s predicted 6% and is in line with

the IMS Health prediction of 4% ‐ 7% growth for the industry.

We assumed significant revenue loss in 2012E and 2015E

which represents lost revenue due to patent expirations,

specifically Plavix and Abilify.

Modeling Results

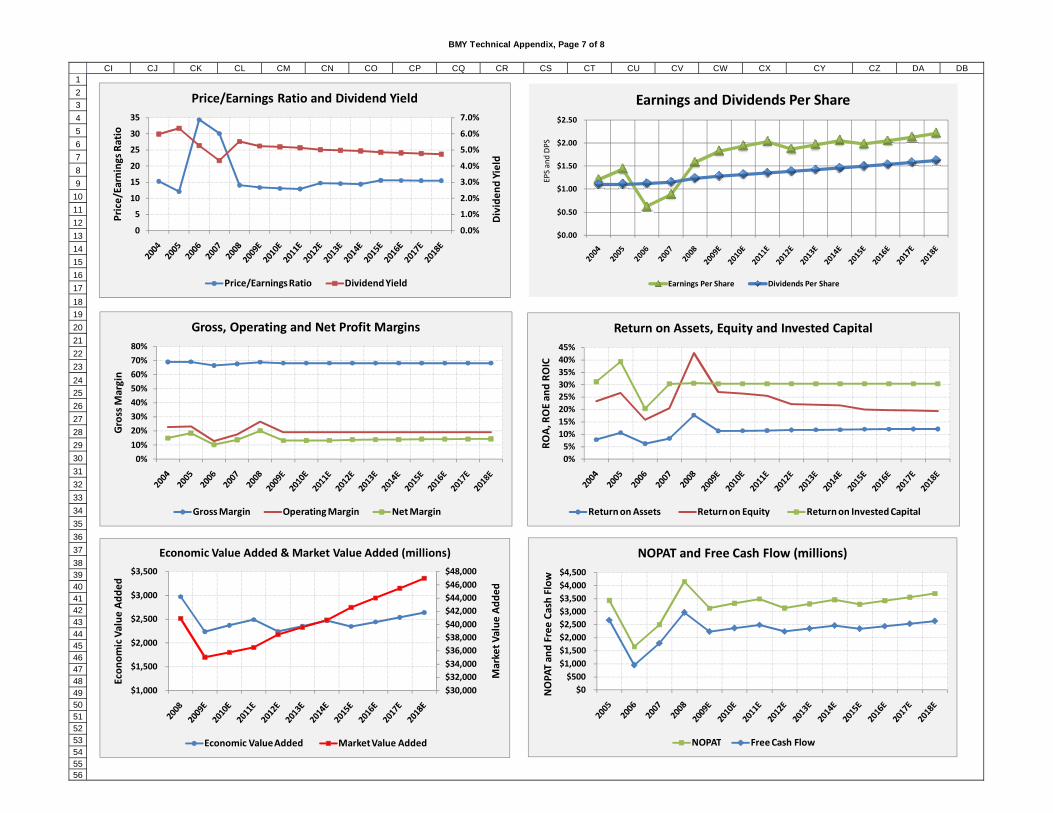

As of 12/4 BMY traded with a Dividend Yield just over 5%.

BMY has historically increased dividend payments even when

EPS fell. We project a continued increase in DPS throughout

the forecast.

With such a high dividend yield it is important to verify that

Bristol‐Myers will be able to sustain it. One method of

financial stability is the Piotroski’s Financial Fitness Scorecard.

BMY shows an average value well above 8 indicating that

BMY has a solid financial foundation. Additionally, BMY

scores well in the safe zone on the Altman Z‐Score

Bankruptcy test which suggests that BMY has no significant

risk of bankruptcy.

Bristol‐Myers sustains this financial stability through a strong

value‐creation engine. The spread between ROIC and WACC

averages 20% throughout the forecast. This spread is well

protected by legal patents.

While Economic Value Added takes a slight dip in 2009E due

to the conservative modeling approach and two more slight

dips in 2012E and 2015E due to patent expirations, BMY is

able to increase Market Value Added throughout the

forecast.

Recommendation

Due to Bristol‐Myers strong dividend, healthy balance sheet

and strong pipeline we view BMY as an attractive buy and

hold stock for the Student Investment Fund at or below

$24.15 per share. That price would secure a sustainable

5.13% dividend yield for the Studend Investment Fund. In

addition to being an attractive investment based on

fundamental analysis, Bristol‐Myers offers a low correlational

coefficient to the stocks held in the fund.

A portfolio of low correlation stocks will decrease the volitility

of the portfolio as a whole. Exclusing indexes, BMY does not

have a correlational coefficient over .48 with any stock held in

the fund.

Bristol‐Myers continues to have significant upside for capital

gains. The well‐positioned drug could likely generate a

surprise blockbuster drug. Furthermore, macro‐economic

trends regarding an aging and increasingly unhealthy

population could provide a tailwind to Bristol‐Myers’ revenue

as modern medicine dictates prescription medication as the

first and most cost effective treatment.

Our forecasts represent Bristol‐Myers’ performance in a less

than ideal environment. Bristol‐Myers should meet and likely

surpass our conservative modeling assumptions making our

discounted cash flow target price a conservative estimate.

Management and Business Initiative

We view BMY’s management team as an asset to the

company. Since the 2006 appointment of James Cornelius as

CEO the company has significantly grown revenues and cut

costs through two key strategies titled “string of pearls” for

its pipeline expansion strategy, and “PTI” for its productivity

transformation initiative strategy. BMY’s management has

strengthened the company’s balance sheet through divesture

of non‐biopharma assets, addressed the coming patent cliff

head on, shown restraint in acquisition pricing, and

successfully increased operating leverage through cost

cutting initiatives.

“String of Pearls” Strategy

In 2007 BMY launched a new strategy titled “string of pearls”.

The new strategic plan sought to acquire new compounds,

pipelines, and companies that would strategically help

address areas not currently covered by the company, or build

onto its existing pipeline. The strategy also has led to the

divestiture of non‐core businesses. Over the past two years

BMY has sold its OTC line, its generics businesses, medical

supply division, and most recently is in the process of

spinning of its nutritionals business, Mead Johnson, to

shareholders. These divestures have improved operating

margins, and provided significant cash to allow for the “string

of pearls” strategy to continue while building an even larger

war chest. The most recent, and the eight pearl acquired,

was Medarex. Through the $2.1B acquisition of Medarex

BMY gained full rights to phase III monoclonal antibody

Ipilimumab, and Medarex’s state of the art biologics

platform. Other firms full acquired are Kosan Bioscience

($235m) and Adnexus Therapuetics ($430m). The other

pearls have been acquired through partnering agreements

such as with AZN and Pfizer, as well as purchasing licensing

agreements. While the company has been aggressive in its

pursuit of promising compounds and companies it has shown

restraint in regards to price. BMY walked away from a

bidding war with LLY for ImClone after LLY bid up the price

20% over BMY’s offer.

Below is a graph of some of the anticipated launch dates of

some of the drugs developed/acquired through this strategy,

with Onglyza being the first to be approved in July of 2009.

Productivity Transformation Initiative

As BMY states “the Company’s productivity transformation

initiative is designed to fundamentally change the way it runs

its business to meet the challenges of a changing business

environment, to take advantage of the diverse opportunities

in the marketplace as the Company is transforming into a

next‐generation biopharmaceutical company, and to create a

total of $2.5 billion in annual productivity cost savings and

cost avoidance by 2012.

In connection with the PTI, the Company aims to achieve a

culture of continuous improvement to enhance its efficiency,

effectiveness and competitiveness and to substantially

improve its cost base.

BMY has already achieved annual cost savings of $1.5B

through the PTI strategy, and is on pace to reach its goal of

another $1B by 2012. It has reduced its number of

manufacturing facilities, decreased its geographic footprint,

sold and spun off non‐biopharma assets, and reduced its

sales force by over 50%. This has led to expanding margins,

and has had no negative impact to revenue growth.

Investment Risks

Healthcare Reform

Healthcare reform may be more prohibitive to

pharmaceutical companies than anticipated.

The drug industry’s share of cuts to Medicare/Medicaid in the

bill’s current form appears to be about $80‐$110B over the

next ten years according to industry experts. This sum

represents about 3‐4% of US pharma 2008 sales.

It is estimated that the 30‐40m estimated people additionally

insured through the current reform bill would likely increase

drug pharmaceutical revenues creating a neutral impact on

drug companies.

If reform were to turn unfavorable on drug companies, it

could cause a compression to earnings that is not in our

forecast. Similarly, if reform continues to be delayed or

becomes watered down through the approval process, drug

companies could experience a positive change in investor

sentiment in the short term.

Mergers and Acquisitions

A change in BMY’s acquisition strategy could negatively

affect our forecast.

BMY currently is operating under an acquisition strategy

called “string of pearls”. Through the strategy, BMY has been

able to strategically acquire small biotech companies,

compounds, platforms, and build collaborative partnership to

help expand its pipeline.

BMY will likely continue this acquisition strategy but may

consider acquiring a large company, which could cause

earnings dilution and put their attractive dividend at risk.

Recent moves by Merck/Schering Plow, Pfizer/Weth, and

Roche/Genentech have brought the megamerger back to big

pharmaceutical companies.

Furthermore, this trend has put BMY on the list of potential

takeout targets. An acquisition of BMY would provide a

significant premium to shareholders. We view the acquisition

of BMY by another firm as less likely in the near term due to

current market conditions.

Patent Expiration

BMY’s patent cliff may be more severe than forecasted.

BMY faces a large patent cliff with the expiration of patents

to some of its best selling drugs through 2015. Plavix, BMY’s

top selling drug, represents about 20% of 2008 revenues.

While our forecast does anticipate a revenue contraction of

10% in 2012 and 5% in 2015 for the expiration of patents to

Plavix and Abilify, revenues could face a steeper decline.

A steeper decline in sales due to a quicker uptake of generics

or failure of BMY’s pipeline to replace revenues could have a

detrimental impact on our forecasted valuation.

Competition

Increased competition in BMY’s marketed products and

pipeline could derail our forecast.

BMY is in constant competition with other large

pharmaceutical companies for sales of their marketed

products as well as development of pipeline drugs. BMY

faces competition in a number of its products. Plavix has new

competition from Eli Lilly’s Efficient, Abilify is competing with

AstraZeneca’s Seroquel and Pfizer’s Geoden, and Onglyza is in

direct competition with Merck’s Januiva. Similarly BMY’s

phase III diabetes treatment Dapagloflozin may have to

compete with SLGT‐2 inhibitors from JNJ and GSK. An

increase in competition above our estimates could put our

valuation of BMY at risk. However, on several of these fronts,

BMY is currently well positioned. Onglyza has a competitive

advantage in the DDP‐4 space being the only once daily

treatment, and Plavix is still experiencing strong sales thanks

to a much slower than expected adoption of LLY’s Efficient.

BMY – Revenue Forecast by Product

BMY is experiencing double‐digit growth in several key

franchises. While Plavix and Ability will begin facing stiff

generic competition BMY has several key franchises that have

blockbuster potential.

Plavix (Clopidogrel Bisulfate)

Plavix is BMY’s best selling drug with 2008 sales of $5.6B

making up over 20% of BMY’s total sales. Plavix is used to

help protect against future heart attack or stroke and is the

biggest seller in the space.

LLY recently launched Efficient, a direct competitor to Plavix.

Despite favorable clinical trials, Efficient has struggled to steal

market share from Plavix in the time since its 2008 launch.

Plavix has continued to grow sales through 2009 but will lose

patent protection in 2012, and it will face stiff competition

from multiple generics.

Sprycel (Dasantinib)

Sprycel was launched in 2006 as a second line treatment for

chronic myeloid leukemia (CML). Gleevec is the biggest

competitor in the space, but Sprycel fills a void in the

marketplace by being the only advanced SRC inhibitor with

demonstrated efficacy and safety in patients with solid

tumors that are resistant to Gleevec.

In May of 2009, the FDA approved Sprycel for treatment in all

three stages of CML for those with resistance or intolerance

for other therapies. Sprycel is also in trials for breast and

prostate cancer, and a recent study released by UCLA

scientists show Sprycel significantly inhibited the growth and

promoted the death of ovarian cancer cells, a disease that

currently has few effective therapies. Approval of Sprycel for

another cancer treatment would greatly increase its

forecasted sales potential.

Abilify (Aripiprazole)

Abilify was recently approved by the FDA for its fifth

indication. Abilify is currently approved for the treatment of

schizophrenia, bipolar I disorder, depression add‐on, agitation

associated with schizophrenia or bipolar depression, and

most recently for irritability in children with autism.

In April of 2009, BMY extended its exclusivity agreement with Otsuka to allow for an additional 29 months of exclusivity marketing Abilify. This will allow BMY to hold exclusivity through the Plavix patent expiration. In exchange, BMY will be recognizing Abilify sales on a tiered scale, and will share a percentage of revenue from its oncology line as well.

Virology Franchise: Baraclude Reyataz Sustiva

(Entecavir)(Atazanavir)(Efavirenz)

BMY’s virology franchise treats HIV/AIDS and Hepatitis B.

Sustiva a consistent grower loses patent protection at the

end of 2013, followed by Baraclude in 2015, and Reyataz in

2017. Sustiva is the one of the three that currently has a

generic filed to compete. Despite the patent expiration

issues, BMY should experience consistent growth in Sustiva

up till patent expiration. BMY should continue to experience

strong growth in Baraclude behind new study results that

show it has twice the efficacy rate and is just as safe as its

biggest competitor Adefovir. Reyataz should experience

accelerated growth behind its FDA approval as a once daily

treatment with a higher efficacy rate than its biggest

competitor ABT’s Kaletra ($1.5B sales).

The below forecast were completed prior to recent FDA

approvals for the franchise drugs.

Onglyza (Saxagliptin)

Onglyza is BMY’s newest approved drug. It is the second

approved DDP‐4 inhibitor approved by the FDA along with

MRK’s Januvia. DDP‐4 inhibitors are forecasted to $7B in

sales by 2015. New FDA approval requirements prevent any

new entrants from receiving approval prior to 2012 leaving

Onglyza and Januvia in a two horse race. Onglyza is the only

once a day DDP‐4 inhibitor and is offered in a smaller

dose/pill. In head to head trials, Onglyza showed the same

efficacy rate and safety as Januvia. The treatment of type‐2

diabetes is one of the most lucrative and fastest growing

disease areas currently in medicine. DDP‐4 inhibitors can be

combined with other diabetes treatments to help control

blood glucose levels. Onglyza was co‐developed with AZN

and both costs and revenues will be split equally between the

two firms.

Orencia (abatacept)

Orencia was approved in 2006 for the second‐line treatment

of adult RA (Rheumatoid Arthritis), and juvenile idiopathic

arthritis. The FDA recently approved Orencia as a first line

treatment for individuals with moderate to severe RA, as well

as for children over the age of 6 with idiopathic arthritis. In

clinical trials Orencia has shown higher efficacy rates with

improved safety over current RA treatments. Orencia stands

to see strong growth with the new broader use label

approved by the FDA. Approximately 2 million people in the

US are living with RA. Orencia is the first T‐cell co‐

stimulation modulator approved for the treatment of

rheumatoid arthritis (RA).

Pipeline Products

Dapagloflozin

Dapagloflozin is another diabetes treatment being co‐

developed by BMY and AZN. Dapagloflozin is a once daily

first in class SGLT‐2 inhibitor for the treatment of type‐2

diabetes. This drug helps control blood glucose levels by

targeting the SGLT‐2 receptor which is responsible for glucose

excretion in urine. Because of its impact on glucose excretion

Dapagloflozin has also shown weight loss advantages and

lowered blood pressure in clinical trials. The Diabetes Market

is one of the most lucrative with over 20 million Americans

currently diagnosed with diabetes and 54 million considered

prediabetic according to the CDC. Recent results from phase

III trials released in October show better than expected

results in controlling glucose levels and its ability to be

partnered with other diabetes treatments. The results were

released at the IDF (International Diabetes Federation)

meeting in Montreal. One IDF presenter noted, in his

practice, he would “use it in combination with every other

type of agent.”

Ipilimumab

Ipilimumab is fully human monoclonal antibody that BMY

gained full rights to through its recent acquisition of Medarex

earlier this year. It is in phase III trials for Malignant

Melanoma and in phase II trials for the treatment of prostate

cancer. A Pharmacor report titled Malignant Melanoma

estimates that the launch of BMY’s Ipilimumab will

significantly increase the size of the malignant melanoma

market. There is currently a huge unmet need for life

extending treatment in those with late skin cancer.

Pharmacor reports they anticipate Ipilimumab to grow at 17%

annually from a launch in 2012 to 2017, with it consuming a

third of the total malignant melanoma treatment market by

2017. These results are dependent on continued success in

phase III trials. Ipilimumab could experience even greater

growth through sales in treating prostate cancer. Prostate

cancer would be the single largest market for a monoclonal

antibody treatment with over 192,000 new cases diagnosed

each year in the US.

Apixaban

Apixaban is an oral anticoagulant currently in phase III trials

for the treatment of venous thromboembolism (VTE)

following knee and hip surgery, atrial fibrillation (AF), and

acute coronary syndrome (ACS). The drug is currently

enrolling its phase III clinical trials for treatment of AF and

ACS compared to the current treatment Warfarin. A once

daily pill has shown the highest efficacy rates but with slightly

higher risks of bleeding, a downside to the treatment.

Apixaban is the second Xa inhibitor currently in development

behind JNJ’s Xarelto. Apixaban is being co‐developed by BMY

and Pfizer.

Belatacept

Belatacept a first‐in‐class co‐stimulation blocker which

selectively inhibits T‐cell activation is in phase III trials to

prevent organ transplant rejection. The current treatment

use of Cyclosporine is known to cause significant problems

such as increased cardiovascular and metabolic risk.

Belatacept has shown higher efficacy rates and safety rates in

head to head comparisons with Cyclosporine in earlier trials.

Belatacept is currently under review by the FDA and could be

approved in late 2010.

BMY Technical Appendix, Page 1 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38394041424344454647484950515253545556

A B C D E F G H I J K L M N

Enter Firm Ticker BMY

Enter first financial statement year in cell B6 2004 2005 2006 2007 2008 2004 2005 2006 2007 2008 Average Manual

Total revenue 19,380 18,605 16,208 18,193 20,597 Revenue Growth -4.0% -12.9% 12.2% 13.2% 1.5%

Cost of goods sold 5,989 5,737 5,420 5,868 6,396 COGS % of Sales 30.9% 30.8% 33.4% 32.3% 31.1% 31.7%

Gross profit 13,391 12,868 10,788 12,325 14,201

SG&A expense 6,427 6,453 5,773 5,931 6,342 SG&A % of Sales 33.2% 34.7% 35.6% 32.6% 30.8% 33.4% 31.0%

Research & Development 2,500 2,678 2,951 3,227 3,585 R&D % of Sales 12.9% 14.4% 18.2% 17.7% 17.4% 16.1% 17.5%

Depreciation/Amortization 0 0 0 0 0 D&A % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Interest expense (income), operating 0 0 0 0 0 Inc. Exp. Oper. 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Non-recurring expenses 267 (268) 161 429 391 Exp. Non-rec 1.4% -1.4% 1.0% 2.4% 1.9% 1.0%

Other operating expenses (158) (222) 292 (119) (180) Other exp. -0.8% -1.2% 1.8% -0.7% -0.9% -0.3%

Operating Income 4,418 4,304 2,085 3,186 5,471

Interest income (expense), non-operating 0 0 0 0 0 Int. inc. non-oper. 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Gain (loss) on sale of assets 0 0 0 0 0 Gain (loss) asset sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Other income, net 0 0 0 0 0 Other income, net 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Income before tax 4,418 4,304 2,085 3,186 5,471

Income tax 1,519 870 431 682 1,320 Tax rate 34.4% 20.2% 20.7% 21.4% 24.1% 24.2%

Income after tax 2,899 3,434 1,654 2,504 4,151

Minority interest (521) (592) (440) (763) (996) Minority interest -2.7% -3.2% -2.7% -4.2% -4.8% -3.5%

Equity in affiliates 0 0 0 0 0 Equity in affiliates 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

U.S. GAAP adjustment 0 0 0 0 0 U.S. GAAP adjust. 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Net income before extraordinary items 2,378 2,842 1,214 1,741 3,155

Extraordinary items, total 10 158 371 424 2,092 Extrordinary items

Net income 2,388 3,000 1,585 2,165 5,247

Total adjustments to net income 5 0 0 0 0 Adjustments to NI

Basic weighted average shares 1,942 1,952 1,960 1,970 1,977 Share growth 0.5% 0.4% 0.5% 0.4% 0.4%

Basic EPS excluding extraordinary items 1.22 1.46 0.62 0.88 1.60

Basic EPS including extraordinary items 1.23 1.54 0.81 1.10 2.65

Diluted weighted average shares 1,976 1,983 1,963 1,980 2,001 Diluted share growth 0.4% -1.0% 0.9% 1.1% 0.3%

Diluted EPS excluding extraordinary items 1.20 1.43 0.62 0.88 1.58

Diluted EPS including extraordinary items 1.21 1.51 0.81 1.09 2.62

Dividends per share -- common stock 1.12 1.12 1.12 1.15 1.24

Gross dividends -- common stock 2,176 2,187 2,204 2,275 2,460 Dividend growth 0.5% 0.8% 3.2% 8.1% 3.1%

Retained earnings 212 813 (619) (110) 2,787

values in millions

Too unpredictable to forecast, set to zero in the forecasts

Too unpredictable to forecast, set to zero in the forecasts

Forecasting PercentagesHistorical Income Statements

Forecasted income statement items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

BMY Technical Appendix, Page 2 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38394041424344454647484950515253545556

O P Q R S T U V W X Y Z

Year-by-year dividend growth

Year-by-year revenue growth 5.00% 6.00% 5.00% -10.00% 5.00% 5.00% -5.00% 4.00% 4.00% 4.00%

year 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Total revenue 21,627 22,924 24,071 21,664 22,747 23,884 22,690 23,598 24,541 25,523

Cost of goods sold 6,855 7,266 7,630 6,867 7,210 7,571 7,192 7,480 7,779 8,090

Gross profit 14,772 15,658 16,441 14,797 15,537 16,314 15,498 16,118 16,762 17,433

SG&A expense 6,704 7,107 7,462 6,716 7,052 7,404 7,034 7,315 7,608 7,912

Research & Development 3,785 4,012 4,212 3,791 3,981 4,180 3,971 4,130 4,295 4,467

Depreciation/Amortization 0 0 0 0 0 0 0 0 0 0

Interest expense (income), operating 0 0 0 0 0 0 0 0 0 0

Non-recurring expenses 224 238 250 225 236 248 235 245 255 265

Other operating expenses (75) (80) (84) (75) (79) (83) (79) (82) (85) (89)

Operating Income 4,133 4,381 4,600 4,140 4,347 4,565 4,337 4,510 4,690 4,878

Interest income (expense), non-operating (372) (373) (360) (195) (193) (188) (81) (72) (61) (47)

Gain (loss) on sale of assets 0 0 0 0 0 0 0 0 0 0

Other income, net 0 0 0 0 0 0 0 0 0 0

Income before tax 3,761 4,008 4,241 3,945 4,154 4,377 4,255 4,438 4,630 4,831

Income tax 909 968 1,025 953 1,004 1,058 1,028 1,072 1,119 1,167

Income after tax 2,852 3,040 3,216 2,992 3,151 3,320 3,227 3,366 3,511 3,664

Minority interest (762) (808) (848) (763) (801) (841) (799) (831) (865) (899)

Equity in affiliates 0 0 0 0 0 0 0 0 0 0

U.S. GAAP adjustment 0 0 0 0 0 0 0 0 0 0

Net income before extraordinary items 3,614 3,848 4,064 3,755 3,952 4,161 4,027 4,197 4,376 4,563

Extraordinary items, total 0 0 0 0 0 0 0 0 0 0

Net income 3,614 3,848 4,064 3,755 3,952 4,161 4,027 4,197 4,376 4,563

Total adjustments to net income 0 0 0 0 0 0 0 0 0 0

Basic weighted average shares 1,986 1,995 2,004 2,013 2,022 2,031 2,040 2,049 2,058 2,067

Basic EPS excluding extraordinary items 1.82 1.93 2.03 1.87 1.95 2.05 1.97 2.05 2.13 2.21

Basic EPS including extraordinary items 1.82 1.93 2.03 1.87 1.95 2.05 1.97 2.05 2.13 2.21

Diluted weighted average shares 1,983 1,992 2,001 2,010 2,019 2,028 2,037 2,046 2,055 2,065

Diluted EPS excluding extraordinary items 1.82 1.93 2.03 1.87 1.96 2.05 1.98 2.05 2.13 2.21

Diluted EPS including extraordinary items 1.82 1.93 2.03 1.87 1.96 2.05 1.98 2.05 2.13 2.21

Dividends per share -- common stock 1.28 1.31 1.35 1.38 1.42 1.46 1.49 1.53 1.58 1.62

Gross dividends -- common stock 2,537 2,616 2,697 2,781 2,868 2,957 3,049 3,144 3,242 3,343Retained earnings 1,078 1,232 1,367 974 1,084 1,204 977 1,053 1,134 1,220

Forecasted Income Statements -- 10 Years

Revenues grow at the same rate each year unless a growth value is manually entered in the cell above the forecast year, in which case the year-by-year value overrides the historical or manual average. It makes sense to start tapering the growth forecasts 5 or 6 years into the forecast period.

BMY Technical Appendix, Page 3 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38394041424344454647484950515253545556

AA AB AC AD AE AF AG AH AI AJ AK AL AM AN

Enter Firm Ticker BMY

year 2004 2005 2006 2007 2008 2004 2005 2006 2007 2008 Average Manual

Assets

Cash & equivalents 3,680 3,050 2,018 1,801 7,976 Cash % of Sales 19.0% 16.4% 12.5% 9.9% 38.7% 19.3%

Short term investments 3,794 2,749 1,995 424 289 ST Invest. % of Sales 19.6% 14.8% 12.3% 2.3% 1.4% 10.1%

Receivables, total 4,373 3,378 3,247 3,994 3,710 Receivables % Sales 22.6% 18.2% 20.0% 22.0% 18.0% 20.1%

Inventory, total 1,830 2,060 2,079 2,162 1,765 Inventory % of Sales 9.4% 11.1% 12.8% 11.9% 8.6% 10.8%

Prepaid expenses 319 270 314 310 320 Pre. Exp. % of Sales 1.6% 1.5% 1.9% 1.7% 1.6% 1.7%

Other current assets, total 805 776 649 1,411 703 Other CA % of Sales 4.2% 4.2% 4.0% 7.8% 3.4% 4.7%

Total Current Assets 14,801 12,283 10,302 10,102 14,763

Property, plant and equipment (net) 5,765 5,693 5,673 5,650 5,405 Net PPE % of Sales 29.7% 30.6% 35.0% 31.1% 26.2% 30.5% 27.0%

Goodwill 4,905 4,823 4,829 4,998 4,827 Goodwill % of Sales 25.3% 25.9% 29.8% 27.5% 23.4% 26.4%

Intangibles 2,260 1,921 1,852 1,330 1,151 Intangibles % of Sales 11.7% 10.3% 11.4% 7.3% 5.6% 9.3%

Long term investments 0 0 0 0 0 LT Invest. % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Notes receivable -- long term 0 0 0 0 0 Notes Rec. % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Other long term assets, total 2,704 3,418 2,919 3,846 3,406 Other LT ass. % Sales 14.0% 18.4% 18.0% 21.1% 16.5% 17.6%

Other assets, total 0 0 0 0 0 Other assets % Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Total assets 30,435 28,138 25,575 25,926 29,552

Liabilities and Shareholders' Equity

Accounts payable 2,127 1,579 1,239 1,442 1,535 Acc. Payable % Sales 11.0% 8.5% 7.6% 7.9% 7.5% 8.5%

Payable/accrued 0 0 0 0 0 Pay/accured % Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Accrued expenses 4,233 3,870 3,663 3,919 3,780 Acc. Exp. % of Sales 21.8% 20.8% 22.6% 21.5% 18.4% 21.0%

Notes payable/short term debt 1,883 231 187 1,891 154 Notes payable % Sales 9.7% 1.2% 1.2% 10.4% 0.7% 4.7%

Current portion of LT debt/Capital leases 0 0 0 0 0 Curr. debt % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Other current liabilities 1,600 1,210 1,407 1,146 1,241 Other curr liab % Sales 8.3% 6.5% 8.7% 6.3% 6.0% 7.2%

Total Current Liabilities 9,843 6,890 6,496 8,398 6,710

Long term debt, total 8,463 8,364 7,248 4,381 6,585 LT debt % of Sales

Deferred income tax 0 0 0 0 0 Def. inc. tax % Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Minority interest 0 0 0 0 0 Min. Int. % of Sales 0.0% 0.0% 0.0% 0.0% 0.0% 0.0%

Other liabilities, total 1,927 1,676 1,840 2,585 4,016 Other liab. % of Sales 9.9% 9.0% 11.4% 14.2% 19.5% 12.8%

Total Liabilities 20,233 16,930 15,584 15,364 17,311

Preferred stock (redeemable) 0 0 0 0 0

Preferred stock (unredeemable) 0 0 0 0 0

Common stock 220 220 220 220 220Additonal paid-in capital 2,491 2,528 2,498 2,722 2,828Retained earnings (accumluated deficit) 19,651 20,464 19,845 19,762 22,549Treasury stock -- common (11,311) (11,168) (10,927) (10,584) (10,566)ESOP Debt Guarantee 0 0 0 0 0Other equity, total (849) (836) (1,645) (1,558) (2,790)

Total Shareholders' Equity 10,202 11,208 9,991 10,562 12,241Total Liabilities and Shareholders' Equity 30,435 28,138 25,575 25,926 29,552Diluted weighted average shares 1,976 1,983 1,963 1,980 2,001 Diluted share growth 0.4% -1.0% 0.9% 1.1% 0.3%Total preferred shares outstanding 0 0 0 0 0 Preferred share growth

Set to last historical year's level throughout the forecasts.Set to last historical year's level throughout the forecasts.

LT debt is manually adjusted for AFN in the pro formas

Forecasting Percentages

values in millions

Historical Balance Sheets

The model uses the more conservative diluted common shares number for total shares outstanding.

Forecasted balance sheet items are based on 5 years of historical average ratios unless a value is entered in the manual cell, in which case the manual entry overrides the historical average. The idea is to consider whether the historical average is truly representative of what the firm can achieve in the future.

The model uses the more conservative diluted common shares number for total shares outstanding.

BMY Technical Appendix, Page 4 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38394041424344454647484950515253545556

AO AP AQ AR AS AT AU AV AW AX AY AZ

PPE/Sales

year 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Assets

Cash & equivalents 4,172 4,422 4,644 4,179 4,388 4,608 4,377 4,552 4,734 4,924

Short term investments 2,180 2,311 2,426 2,183 2,293 2,407 2,287 2,378 2,474 2,572

Receivables, total 4,357 4,618 4,849 4,364 4,582 4,811 4,571 4,753 4,944 5,141

Inventory, total 2,327 2,466 2,590 2,331 2,447 2,570 2,441 2,539 2,640 2,746

Prepaid expenses 359 380 399 359 377 396 376 391 407 423

Other current assets, total 1,016 1,077 1,131 1,018 1,069 1,122 1,066 1,109 1,153 1,199

Total Current Assets 14,410 15,275 16,039 14,435 15,156 15,914 15,119 15,723 16,352 17,006

Property, plant and equipment (net) 5,839 6,190 6,499 5,849 6,142 6,449 6,126 6,371 6,626 6,891

Goodwill 5,707 6,049 6,351 5,716 6,002 6,302 5,987 6,227 6,476 6,735

Intangibles 2,003 2,123 2,230 2,007 2,107 2,212 2,102 2,186 2,273 2,364

Long term investments 0 0 0 0 0 0 0 0 0 0

Notes receivable -- long term 0 0 0 0 0 0 0 0 0 0

Other long term assets, total 3,807 4,035 4,237 3,813 4,004 4,204 3,994 4,154 4,320 4,493

Other assets, total 0 0 0 0 0 0 0 0 0 0

Total assets 31,766 33,672 35,356 31,820 33,411 35,082 33,328 34,661 36,047 37,489

Liabilities and Shareholders' Equity

Accounts payable 1,838 1,948 2,045 1,841 1,933 2,029 1,928 2,005 2,085 2,169

Payable/accrued 0 0 0 0 0 0 0 0 0 0

Accrued expenses 4,548 4,820 5,061 4,555 4,783 5,022 4,771 4,962 5,160 5,367

Notes payable/short term debt 1,006 1,066 1,119 1,008 1,058 1,111 1,055 1,097 1,141 1,187

Current portion of LT debt/Capital leases 0 0 0 0 0 0 0 0 0 0

Other current liabilities 1,547 1,640 1,722 1,550 1,627 1,708 1,623 1,688 1,755 1,826

Total Current Liabilities 8,938 9,474 9,948 8,953 9,401 9,871 9,377 9,752 10,142 10,548

Long term debt, total 6,741 6,712 6,408 3,201 3,122 2,973 887 676 418 109

Deferred income tax 0 0 0 0 0 0 0 0 0 0

Minority interest 0 0 0 0 0 0 0 0 0 0

Other liabilities, total 2,769 2,935 3,082 2,773 2,912 3,058 2,905 3,021 3,142 3,268

Total Liabilities 18,447 19,121 19,438 14,928 15,435 15,901 13,170 13,450 13,702 13,924

Preferred stock (redeemable) 0 0 0 0 0 0 0 0 0 0

Preferred stock (unredeemable) 0 0 0 0 0 0 0 0 0 0

Common stock 220 220 220 220 220 220 220 220 220 220Additonal paid-in capital 2,828 2,828 2,828 2,828 2,828 2,828 2,828 2,828 2,828 2,828Retained earnings (accumluated deficit) 23,627 24,859 26,226 27,200 28,284 29,489 30,466 31,519 32,653 33,873Treasury stock -- common (10,566) (10,566) (10,566) (10,566) (10,566) (10,566) (10,566) (10,566) (10,566) (10,566)ESOP Debt Guarantee 0 0 0 0 0 0 0 0 0 0Other equity, total (2,790) (2,790) (2,790) (2,790) (2,790) (2,790) (2,790) (2,790) (2,790) (2,790)

Total Shareholders' Equity 13,319 14,551 15,918 16,892 17,976 19,181 20,158 21,211 22,345 23,565Total Liabilities and Shareholders' Equity 31,766 33,672 35,356 31,820 33,411 35,082 33,328 34,661 36,047 37,489Total common shares (diluted) 2,007 2,014 2,020 2,026 2,033 2,039 2,046 2,052 2,058 2,065Total preferred shares outstanding 0 0 0 0 0 0 0 0 0 0AFN (interactive with 3 items below) 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0Adjustment to LT Debt (iterate or use Goal Seek) 155.7 (28.5) (304.0) (3,206.7) (79.6) (149.3) (2,085.1) (211.1) (258.2) (309.6)Issue Common Stock to Fund AFNSet Balance Sheet Cash Lower to Fund AFN

Forecasted Balance Sheets -- 10 Years

Model maintains a fixed ratio of ST debt/sales. LT debt is adjusted for shortfalls/surpluses of AFN. Every time something changes that affects the forecasts, set row 49 entries to zero and use Goal

BMY Technical Appendix, Page 5 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38394041424344454647484950515253545556

BA BB BC BD BE BF BG BH BI BJ BK BL BM BN BO BPEnter Firm Ticker BMY

2004 2005 2006 2007 2008 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Liquidity

Current 1.50 1.78 1.59 1.20 2.20 1.61 1.61 1.61 1.61 1.61 1.61 1.61 1.61 1.61 1.61

Quick 1.32 1.48 1.27 0.95 1.94 1.35 1.35 1.35 1.35 1.35 1.35 1.35 1.35 1.35 1.35

Net Working Capital to Total Assets 0.16 0.19 0.15 0.07 0.27 0.17 0.17 0.17 0.17 0.17 0.17 0.17 0.17 0.17 0.17

Asset Management

Days Sales Outstanding 82.36 66.27 73.12 80.13 65.75 73.53 73.53 73.53 73.53 73.53 73.53 73.53 73.53 73.53 73.53

Inventory Turnover 10.59 9.03 7.80 8.41 11.67 9.29 9.29 9.29 9.29 9.29 9.29 9.29 9.29 9.29 9.29

Fixed Assets Turnover 3.36 3.27 2.86 3.22 3.81 3.70 3.70 3.70 3.70 3.70 3.70 3.70 3.70 3.70 3.70

Total Assets Turnover 0.64 0.66 0.63 0.70 0.70 0.68 0.68 0.68 0.68 0.68 0.68 0.68 0.68 0.68 0.68

Debt Management

Long-Term Debt to Equity 83.0% 74.6% 72.5% 41.5% 53.8% 50.6% 46.1% 40.3% 19.0% 17.4% 15.5% 4.4% 3.2% 1.9% 0.5%

Total Debt to Total Assets 34.0% 30.5% 29.1% 24.2% 22.8% 24.4% 23.1% 21.3% 13.2% 12.5% 11.6% 5.8% 5.1% 4.3% 3.5%

Times Interest Earned N/A N/A N/A N/A N/A 11.1 11.7 12.8 21.2 22.5 24.3 53.3 62.4 77.1 103.9

Profitability

Gross Profit Margin 69.1% 69.2% 66.6% 67.7% 68.9% 68.3% 68.3% 68.3% 68.3% 68.3% 68.3% 68.3% 68.3% 68.3% 68.3%

Operating Profit Margin 22.8% 23.1% 12.9% 17.5% 26.6% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1% 19.1%

Net After-Tax Profit Margin 15.0% 18.5% 10.2% 13.8% 20.2% 13.2% 13.3% 13.4% 13.8% 13.9% 13.9% 14.2% 14.3% 14.3% 14.4%

Total Assets Turnover 0.64 0.66 0.63 0.70 0.70 0.68 0.68 0.68 0.68 0.68 0.68 0.68 0.68 0.68 0.68

Return on Assets 7.8% 10.7% 6.2% 8.4% 17.8% 11.4% 11.4% 11.5% 11.8% 11.8% 11.9% 12.1% 12.1% 12.1% 12.2%

Equity Multiplier 2.98 2.51 2.56 2.45 2.41 2.39 2.31 2.22 1.88 1.86 1.83 1.65 1.63 1.61 1.59

Return on Equity 23.4% 26.8% 15.9% 20.5% 42.9% 27.1% 26.4% 25.5% 22.2% 22.0% 21.7% 20.0% 19.8% 19.6% 19.4%

EPS (using diluted shares, excluding extraordinary items) 1.20 1.43 0.62 0.88 1.58 1.82 1.93 2.03 1.87 1.96 2.05 1.98 2.05 2.13 2.21

DPS (dividends per share) 1.10 1.10 1.12 1.15 1.23 1.28 1.31 1.35 1.38 1.42 1.46 1.50 1.54 1.58 1.62

2004 2005 2006 2007 2008 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

NOPAT (net operating profit after tax) 2,899 3,434 1,654 2,504 4,151 3,135 3,323 3,489 3,140 3,297 3,462 3,289 3,420 3,557 3,700

ROIC (return on invested capital) 31.2% 39.3% 20.4% 30.4% 30.7% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4% 30.4%

EVA (economic value added) 2,091 2,675 948 1,787 2,973 2,238 2,373 2,491 2,242 2,354 2,472 2,348 2,442 2,540 2,641

FCF (free cash flow) N/A 3,990 2,271 2,373 (1,144) 6,366 2,704 2,943 4,288 2,781 2,920 3,858 2,988 3,107 3,232

Weighted Average Cost of Capital 8.7% 8.7% 8.7% 8.7% 8.7% 8.7% 8.7% 8.7% 8.7% 8.7% 8.7%

Net Operating Working Capital (NOWC) 3,523 3,039 2,442 2,596 8,136 4,470 4,738 4,975 4,478 4,702 4,937 4,690 4,878 5,073 5,276

Operating Long Term Assets 5,765 5,693 5,673 5,650 5,405 5,839 6,190 6,499 5,849 6,142 6,449 6,126 6,371 6,626 6,891Total Operating Capital 9,288 8,732 8,115 8,246 13,541 10,310 10,928 11,474 10,327 10,843 11,386 10,816 11,249 11,699 12,167

2008 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018ELong-term Horizon Value Growth Rate (user-supplied) 3.50%PV of Forecasted FCF, discounted at 8.70% $51,629 $49,753 $51,375 $52,900 $53,212 $55,059 $56,927 $58,019 $60,077 $62,194 $64,370Value of Non-Operating Assets $8,265 $6,352 $6,733 $7,070 $6,363 $6,681 $7,015 $6,664 $6,931 $7,208 $7,496Total Intrinsic Value of the Firm $59,894 $56,104 $58,108 $59,969 $59,575 $61,740 $63,942 $64,683 $67,007 $69,402 $71,867Intrinsic Market Value of the Equity $53,155 $48,358 $50,329 $52,442 $55,366 $57,560 $59,858 $62,741 $65,234 $67,842 $70,571Per Share Intrinsic Value of the Firm $26.56 $24.38 $25.26 $26.21 $27.55 $28.51 $29.52 $30.80 $31.88 $33.01 $34.18MVA (market value added) $40,914 $35,039 $35,779 $36,524 $38,474 $39,584 $40,678 $42,583 $44,023 $45,497 $47,006

Item Value Percent Cost Weighted Cost Risk Free Rate 4.25%ST Debt (from most recent balance sheet) 154 0.30% 3.50% 0.01% Beta 0.80LT Debt (from most recent balance sheet) 6,585 12.96% 5.00% 0.49% Market Risk Prem. 6.50%MV Equity (look up stock's mkt. cap and enter in cell BB53) 44,060 86.73% 9.45% 8.20% Cost of Equity 9.45%Weighted Average Cost of Capital 8.70%

values in millions

Historical Ratios and Valuation Model

Valuation (in millions where appropriate) -- through year 2018E

Capital Asset Pricing Model

Forecasted Ratios and Valuation Model -- 10 Years

Valuation Metrics Trend Analysis (NOPAT, EVA, MVA, FCF and Capital in millions) Forecasted Valuation Metrics -- 10 Years

Weighted Average Cost of Capital Calculations

BMY Technical Appendix, Page 6 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38394041424344454647484950515253545556

BQ BR BS BT BU BV BW BX BY BZ CA CB CC CD CE CF CG CH

Inputs 2004 2005 2006 2007 2008 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Per share value (hist. & DCF est.) $18.37 $17.37 $21.26 $26.47 $22.24 $24.38 $25.26 $26.21 $27.55 $28.51 $29.52 $30.80 $31.88 $33.01 $34.18

Market capitalization $35,675 $33,906 $41,670 $52,146 $43,968 $48,422 $50,396 $52,511 $55,439 $57,636 $59,938 $62,824 $65,320 $67,932 $70,664

EBITDA $3,907 $3,870 $2,016 $2,847 $6,567 $4,895 $5,189 $5,448 $4,904 $5,149 $5,406 $5,136 $5,341 $5,555 $5,777

Enterprise Value $42,341 $39,451 $47,087 $56,617 $42,731 $51,996 $53,752 $55,395 $55,469 $57,428 $59,413 $60,389 $62,541 $64,757 $67,036

Multiples

Price/Sales 1.84 1.82 2.57 2.87 2.13 2.24 2.20 2.18 2.56 2.53 2.51 2.77 2.77 2.77 2.77

Price/EBITDA 9.13 8.76 20.67 18.32 6.70 9.89 9.71 9.64 11.31 11.19 11.09 12.23 12.23 12.23 12.23

Price/Free Cash Flow N/A 8.45 18.27 21.86 -38.30 7.61 18.64 17.85 12.93 20.73 20.53 16.28 21.86 21.86 21.87

Enterprise Value/EBITDA 10.84 10.19 23.36 19.89 6.51 10.62 10.36 10.17 11.31 11.15 10.99 11.76 11.71 11.66 11.60

Price/Earnings 15.26 12.12 34.38 30.10 14.11 13.38 13.08 12.90 14.74 14.56 14.39 15.58 15.54 15.50 15.47

Free Cash Flow Yield 11.6% 5.4% 4.5% -2.6% 13.2% 5.4% 5.6% 7.7% 4.8% 4.9% 6.1% 4.6% 4.6% 4.6%

Dividend Yield 5.99% 6.35% 5.28% 4.34% 5.53% 5.25% 5.20% 5.14% 5.02% 4.98% 4.94% 4.86% 4.82% 4.78% 4.74%

Historical Override

Valuation Estimates Based On: Average w/Manual 2009E 2010E 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E

Price/Sales 2.25 $24.50 $25.86 $27.03 $24.22 $25.32 $26.46 $25.03 $25.91 $26.83 $27.78

Price/EBITDA 12.71 $31.34 $33.08 $34.57 $30.98 $32.38 $33.85 $32.01 $33.15 $34.32 $35.53

Price/Free Cash Flow 2.57 $8.25 $3.49 $3.78 $5.48 $3.54 $3.70 $4.87 $3.75 $3.89 $4.02

Enterprise Value/EBITDA 14.16 $34.90 $36.83 $38.49 $34.49 $36.05 $37.69 $35.64 $36.90 $38.21 $39.56

Price/Earnings 21.19 $38.57 $40.88 $42.99 $39.54 $41.43 $43.43 $41.84 $43.41 $45.06 $46.78

Low Price $8.25 $3.49 $3.78 $5.48 $3.54 $3.70 $4.87 $3.75 $3.89 $4.02

High Price $38.57 $40.88 $42.99 $39.54 $41.43 $43.43 $41.84 $43.41 $45.06 $46.78

DCF Price $24.38 $25.26 $26.21 $27.55 $28.51 $29.52 $30.80 $31.88 $33.01 $34.18

Historical Ratios and Valuation Forecasted Ratios and Valuation

Forecasted Stock Prices Based on Historical Multiples -- 10 Years

In this section we are going to examine historical and forecasted ratios (or "multiples") typically used to value stocks ‐‐ P/CF, Enterprise Value/EBITDA, etc. We first want to compare the historical trends in these ratios to the trends in their forecasted values. If our forecasted multiples are systematically increasing or decreasing our forecasts may be too optimistic or pessimistic, and our forecast assumptions may have to be adjusted. Second, we want to compare our discounted cash flow valuation estimates with those derived from the various multiples. Once again, if there is a large discrepancy between our DCF valuation estimate of the company's stock and the range of values obtained from the various multiples, we may want to adjust our forecast assumptions. 1. You will need to look up the company's year‐end stock prices and enter them in the first 5 (historical) years of the "per share value" category.2. Use the estimated DCF price per share in the forecasted period (link to your forecasted prices in cells BG47‐BP47.3. Market capitalization will be calculated as basic weighted shares x historical year‐end prices and then forecasted basic weighted shares x DCF forecasted prices.4. As with previous calculations, historical multiples use actual historical values and forecasted multiples use forecasted values.

$0 $5

$10 $15 $20 $25 $30 $35 $40 $45 $50

Forecasted

Value

Per Sha

re

Forecasted Per Share Stock Values

Low Price DCF Price High Price

$0

$5

$10

$15

$20

$25

$30

$35

$40

0

5

10

15

20

25

Historical or D

CF Price

P/S an

d En

t. Value

/EBITD

A

Price/Sales and Enterprise Value/EBITDA vs. Price

Price/Sales Enterprise Value/EBITDA Historical or DCF Price

BMY Technical Appendix, Page 7 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38394041424344454647484950515253545556

CI CJ CK CL CM CN CO CP CQ CR CS CT CU CV CW CX CY CZ DA DB

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

0

5

10

15

20

25

30

35

Dividen

d Yield

Price/Earnings Ratio

Price/Earnings Ratio and Dividend Yield

Price/Earnings Ratio Dividend Yield

0%

10%

20%

30%

40%

50%

60%

70%

80%

Gross M

argin

Gross, Operating and Net Profit Margins

Gross Margin Operating Margin Net Margin

0%5%10%15%20%25%30%35%40%45%

ROA, R

OE an

d RO

IC

Return on Assets, Equity and Invested Capital

Return on Assets Return on Equity Return on Invested Capital

$0 $500

$1,000 $1,500 $2,000 $2,500 $3,000 $3,500 $4,000 $4,500

NOPAT an

d Free

Cash Flow

NOPAT and Free Cash Flow (millions)

NOPAT Free Cash Flow

$30,000 $32,000 $34,000 $36,000 $38,000 $40,000 $42,000 $44,000 $46,000 $48,000

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

Market V

alue

Add

ed

Econ

omic Value

Add

ed

Economic Value Added & Market Value Added (millions)

Economic Value Added Market Value Added

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

EPS and DPS

Earnings and Dividends Per Share

Earnings Per Share Dividends Per Share

BMY Technical Appendix, Page 8 of 8

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

30

31

32

33

34

35

36

37

38394041424344454647484950515253545556

DC DD DE DF DG DH DI DJ DK DL DM DN DO DP DQ DR DS DT DU DV

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

Net Insider Purchases (Sales) , $, in thousands

Insider Transactions

5

10

15

20

25

30

Peer Comparison: Price/Earnings Ratio

BMY AZN TEVA

10,00015,00020,00025,00030,00035,00040,00045,00050,00055,00060,000

Short Interst (tho

usan

ds)

Short Interest (thousands of shares)

Short Interest (thousands of shares)

0

5,000

10,000

15,000

20,000

25,000

Avg. Daily Volum

e

Average Daily Trading Volume (thousands)

Average Daily Volume (thousands of shares)

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

Days to Cov

er Ratio

Days to Cover Ratio (Short Interest / Volume)

Days to Cover

0

5

10

15

20

25

30

Peer Comparison: Price/Cash Flow Ratio

BMY AZN TEVA