briefing document to portfolio committee on financing of bee in the exploration petroleum, gas &...

TRANSCRIPT

BRIEFING DOCUMENT TO PORTFOLIO COMMITTEE ON FINANCING OF BEE IN THE

EXPLORATION PETROLEUM, GAS & MINERALS SECTORS

in association with

March 2003March 2003

&& SEITLHAMO ENERGYSEITLHAMO ENERGY

Presentation Purpose and Presentor Introduction - AMEF

Current Status of BEE in the SA Exploration Industry - SE

Barriers to BEE Entry - SE Key BEE Financing Risk Barriers - BOR Red Herrings of some BEE Financing Structures - BOR Financing & Other Mitigation Strategies - BOR Sample BEE Exploration Financing Structure – BOR Questions & Answers - ALL Presentors Contact Details Annexures

CONTENTS

2

3

THE PURPOSE OF THIS PRESENTATION IS THE PURPOSE OF THIS PRESENTATION IS TO…TO…

Discuss some of the barrier’s to BEE financing in the exploration sectors of the SA Petroleum, Liquid Fuels, Gas and Minerals industries; and

Present & discuss possible solutions relating to financing of BEE in these critical and essential SA economy industries;

4

ABOUT AMEF

AMEF was established to assist and promote BEE in the mineral and energy sectors of SA economy to: To promote active participation of Black Business in the

Minerals and Energy sector; To rapidly achieve commercially sustainable market share

of at least 25% by BEE companies in the relevant sectors; To assist in overcoming barriers to entry and building

capacity of AMEF members; To create forums for networking with government,

industry and other BEE initiates; To address disparities in the availability of energy

services; and To promote training and development programmes

5

ABOUT BORONGWA

Borongwa is a majority black female owned, operated and managed entity formed to exploit sustainable income and dividend investment opportunities in the ENERGY, RESOURCES, Infrastructure & Logistics and Trading arenas;

The entrepreneur founders have acquired vast and valuable experience in business and corporates during their careers and business ventures;

As a South African women’s group Borongwa’s focus is to invest and be “meaningfully involved” in profitable long term appreciable investment opportunities; and

Borongwa is committed to the sustainable economic growth, transformation and entrepreneurial and SMME development of South Africa through an integrated partnership approach

6

ABOUT SEITLHAMO

Seitlhamo Energy is wholly black energy company focused on the SA gas market with emphasis on developing the HDE in the Liquefied Petroleum Gas market;

Seitlhamo’s primary mission is to positively impact the lives of South Africans through the economic, social and safety of investing in the SA LPG market;

Seeks to positioning itself to become the leader in the Liquid Petroleum Gas market in mainstream South Africa; and

The company has begun to develop extensive distribution networks. Essential relationships are being established with the people these companies serve. These relationships are expected to hold great potential for ensuring the advancement of HDE’s in the SA Gas Market

There are no known established BEE company’s in the SA Offshore Exploration Petroleum or Gas Arenas;

Only a few Historically Disadvantaged SA (HDSA) companies have started to penetrated the downstream SA Liquid Gas & Petroleum arenas;

To help facilitate BEE in the SA Upstream market, PASA requires that each SA offshore exploration licensee have:

At least a 10% BEE partner; and At least a 10% co-nominated free carry by the state

CURRENT STATUS OF BEE IN OFFSHORE EXPLORATION

7

BARRIERS TO BEE ENTRY

8

PETROLEUM GAS MINING

High Capital / Funding Requirements X X X

High Exploration Risk / Volatile to Low ROC X X

Cartel- Like environment by established Players X X X

Reluctance to embrace BEE X X X

No BEE Monitoring and Measurement System; X X

Commercial Market Opportunities (i.e natural gas) X

Pricing Effi ciency X

Lack of Industry Technical Knowledge in SA X X X

Permits and Licenses X X X

Switching Costs X

EXPLORATI ON

Illustrative exampleIllustrative example

KEY BEE FINANCING BARRIERS

9

PETROLEUM GAS MINING

Lack of Robust Market X

Revenue Risk X X X

Monopoly Supply X X

Low SA Production Levels X

Considerable Cap Ex / High Cost of Exploration X X X

Operating - Cost / EOS X X X

Operating – Technical / Management X X X

Rand strength / High Interest Rates X X X

Switching Cost X

FI NANCI NG

Illustrative exampleIllustrative example

Deliberate Cash Traps; Dividends Only Structures; Transfer Pricing Schemes; Exorbitant Management Fee Contracts; IRR Returns less than the Cost of Capital (Ke); Exclusion of BEE from High Value / High Margin Operational

Activities; High Funding Costs / Exorbitant Financial Institution Rates; Excessive Debt Covenants / Debt Service Provision Restrictions; Inflexible Repayment Terms; Double Dipping (i.e. Inflation Linked Mark-ups); and Inappropriate Balance of Risk Return (i.e. up side carry on

concessions)

RED HERRINGS OF SOME BEE STRUCTURES

10

PPP’s; Assured off-take agreement contracts; Sponsor support agreement; Full Allocation of New Exploration permits and licenses to HDSA

companies; Extraordinary BEE Investment Tax Credits; Tax Free Special Project Bonds; Structure debt to enhance shareholder returns (prefs, lower Ke); Fund Equity Stake out of Future Operational Revenues; Higher Energy Prices; Exploration Fund for Jr. BEE Companies; Preference and Cumulative Dividend Distribution Policy; Fixed Rate Debt and/or funding from favorable tax rate payers; Increase GTL Market Incentives / demand

FINANCING MITIGATION STRATEGIES

11

Participation by BEE’s in High Value Chain Areas; BEE Regulatory Framework; Create a Petroleum, Gas & Minerals studies curriculum; Formation of accredited SA exploration training programs; Broader participation by industry players in various BEE

summits and colloquiums; BEE measuring and monitoring system / Comprehensive

industry Scorecards; Encourage and Support early participation by BEE in these

industries

OTHER MITIGATION STRATEGIES

12

RISK MITIGATION MATRIX

13

LACK OF

ROBUST

MARKET/

REVENUE

RI SK

SUPPLY/ STEADY

STATE

PRODUCTI ON

OPERATI NG

- COST /

EOS

OPERATI NG -

TECHNI CAL/

MANAGEMENT

RAND

STRENGTH

/ HI GH

I NTEREST

RATES

SWI TCHI NG

COST

MITIGATING TACTICS

TAKE OR PAY/ OUTPUT CONTRACT X X X

I NVESTMENT & COMPONENTS TAX CREDI T X X X X X

CROSS BORDER I NTO AFRI CA EXPANSI ON X X X X

PPP X X X

TAX FREE BONDS X X

ENVI RONMENTALLY FRI ENDLY SUBSI DY X X X X

HI GH VALUE CHAI N ACTI VI TI ES X X X X

DEREGULATED PRI CI NG STRUCTURE X X

CERTI FI CATI ON / SKI LLS TRANSFER PROGRAME X X

FUND EQUI TY STAKE OUT OF FUTURE PRODUCTI ON X X

KEY FINANCING RISKS

Illustrative exampleIllustrative example

EXPLORATION FINANCING STRUCTURE

14

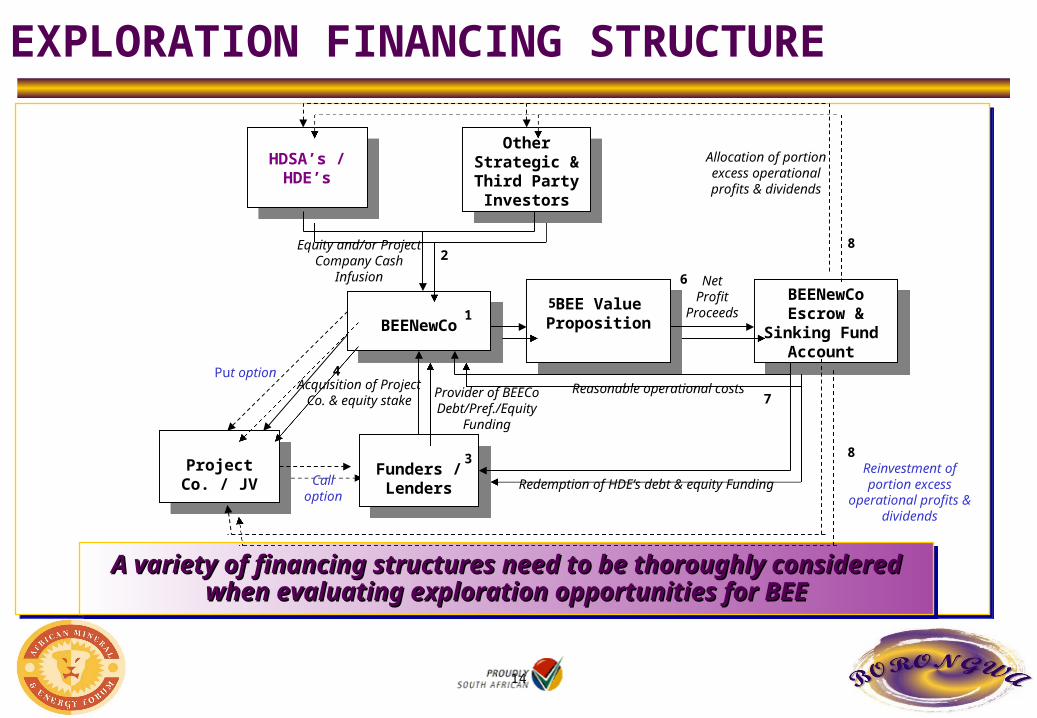

BEENewCoBEENewCo

1

Put option

Project Co. / JV

Project Co. / JV Call

option

Acquisition of Project Co. & equity stake

4

Provider of BEECo Debt/Pref./Equity

Funding

Funders /Lenders

Funders /Lenders

3

BEE Value Proposition

BEE Value Proposition5 BEENewCo

Escrow & Sinking Fund

Account

BEENewCo Escrow &

Sinking Fund Account

NetProfit

Proceeds

6

Reasonable operational costs

Redemption of HDE’s debt & equity Funding

7

HDSA’s /HDE’s

HDSA’s /HDE’s

Other Strategic & Third Party Investors

Other Strategic & Third Party Investors

Equity and/or Project Company Cash

Infusion

2

A variety of financing structures need to be thoroughly A variety of financing structures need to be thoroughly considered when evaluating exploration opportunities for considered when evaluating exploration opportunities for

BEEBEE

A variety of financing structures need to be thoroughly A variety of financing structures need to be thoroughly considered when evaluating exploration opportunities for considered when evaluating exploration opportunities for

BEEBEE

Allocation of portion excess operational profits & dividends

8

Reinvestment of portion excess

operational profits & dividends

8

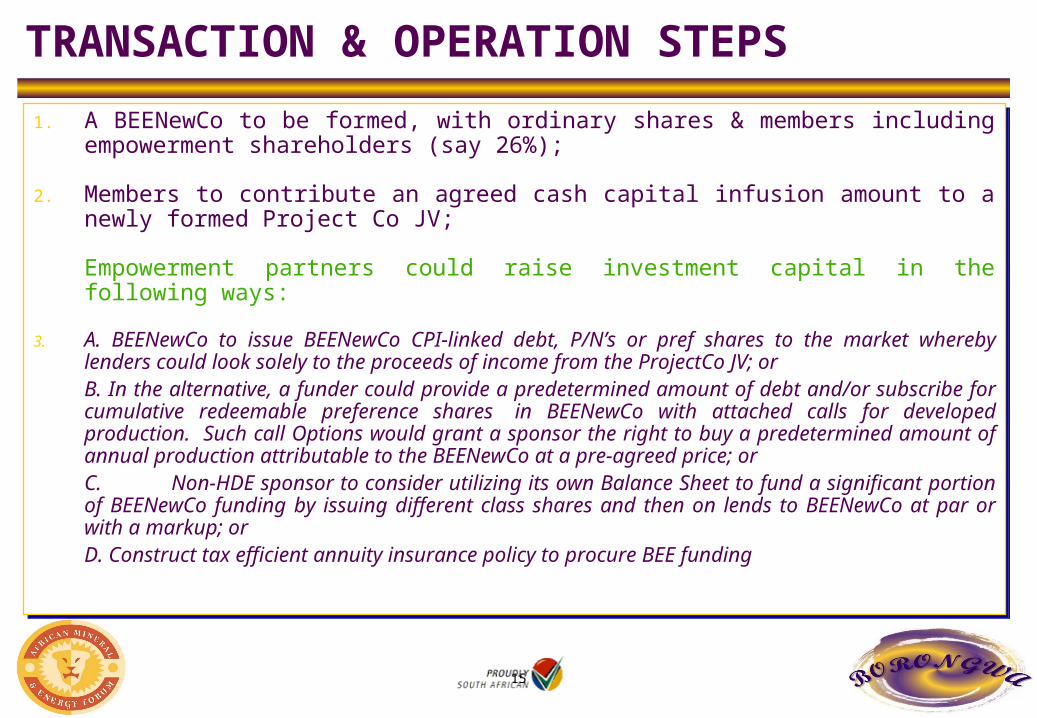

1. A BEENewCo to be formed, with ordinary shares & members including empowerment shareholders (say 26%);

2. Members to contribute an agreed cash capital infusion amount to a newly formed Project Co JV;

Empowerment partners could raise investment capital in the following ways:

3. A. BEENewCo to issue BEENewCo CPI-linked debt, P/N’s or pref shares to the market whereby lenders could look solely to the proceeds of income from the ProjectCo JV; orB. In the alternative, a funder could provide a predetermined amount of debt and/or subscribe for cumulative redeemable preference shares in BEENewCo with attached calls for developed production. Such call Options would grant a sponsor the right to buy a predetermined amount of annual production attributable to the BEENewCo at a pre-agreed price; or C. Non-HDE sponsor to consider utilizing its own Balance Sheet to fund a significant portion of BEENewCo funding by issuing different class shares and then on lends to BEENewCo at par or with a markup; or D. Construct tax efficient annuity insurance policy to procure BEE funding

TRANSACTION & OPERATION STEPS

15

6. BEENewCo to utilize the funder proceeds to acquire stakes in Project Co JV

7. BEENewCo consortium members would be operational and create a value proposition in the Project Co JV. Revenue stream from these activities will flow through the various BEENewCo & Project Co JV’s

8. Agreed Net Profit & Dividend Allocations, Management and Debt Service fees from ProjectCo JV to flow directly into BEENewCo Escrow & Sinking fund.

7. Trustees of BEENewCo Escrow & sinking fund to use the income to cover reasonable BEENewCo operational & management agreement costs and also settle in order of priority its debt and preference equity redemption requirements to lender’s

TRANSACTION & OPERATION STEPS

16

Such structures take into account the follow key characteristics and assumptions: Complies with the legislative requirements of the RSA

government for the Petroleum, Gas and Minerals industries; Offers a more tax efficient and value proposition for

shareholder’s; Allows for funding flexibility as well as broader based

empowerment;

Effective value for money proposition for existing shareholders;

KEY FEATURES OF SUCH STRUCTURES

17

Such structures takes into account the follow key characteristics and assumptions: Outside funder ability to underwrite the equity contributions

of BEENewCo consortium members;

Strong demand from the market and pension funds for higher yielding inflation linked debt;

The revenue payable & profits procured by the BEENewCo

should be sufficient to pay principal and interest (or at least interest) on the BEENewCo funding

KEY FEATURES OF SUCH STRUCTURES

18

QUESTIONS AND ANSWERS

19

PRESENTORS CONTACT DETAILS

Siviwe Mafanya - AMEFTelephone: +27 11 783 5583

Mobile: 082-804-8544Fax: +27 11 784 5588

E-mail: [email protected]

Janice Van Wyk – Borongwa Holdings & Investments (Women’s Group)Telephone: +27 11 241 3900/838 0408

Mobile: 082-821-3742Fax: +27 11 838 0407

E-mail: [email protected]@yasny.co.za

Rudy Roberts – Seitlhamo Energy GroupMobile: 083-602-0511

E-mail: [email protected]

20

ANNEXURE

RELATIONSHIP STRUCTURE BREAKDOWN OF SAMPLE BEE

FINANCING STRUCTURE

21

CONTRACTUAL RELATIONSHIP

22

BEENewCoConsortium

BEENewCoConsortium

ProjectCo JVProjectCo JV

HDSA’s/HDE’s

HDSA’s/HDE’s

Redemption by BEENewCo trustees of BEESPV

shareholder loans & preference share funding

Production Call option

Operations & Asset Management Agreement

Equity and/or Project Company Cash

Infusion

2

1

37

4

2

Other Strategic & Third Party Investors

Other Strategic & Third Party Investors

Lender’sLender’s

Non HDE Sponsor/Partne

rs

Non HDE Sponsor/Partne

rsEquity and/or

Project Company Cash Infusion

Provider of BEENewCo

Debt/Pref./Equity Funding

Acquisition of Equity Stake in Project Co.

Put option Convertible stock swap into the the Non-HDE sponsors stcck in event of default of principal and

interest

BEE Escrow & Sinking Fund

Account

BEE Escrow & Sinking Fund

Account

OPERATIONS CASHFLOW RELATIONSHIP

23

Reasonable operational costs

HDSA’sHDSA’s

BEENewCoBEENewCo

FUNDERFUNDER

ProjectCO JV

ProjectCO JV

BEENewCo ESCROW &

SINKING FUND ACCOUNT

BEENewCo ESCROW &

SINKING FUND ACCOUNT

Allocation of portion excess operational profits & dividends

Redemption of HDE’s debt & equity Funding

Put / Call Option

NetProfit

Proceeds

5

6

7

8

Reinvestment of portion excess operational profits & dividends

BEE Value Proposition and Operations & Management

Agreement

7

Put option

8

THANKS YOU THANKS YOU

24

SEITLHAMO ENERGY SEITLHAMO ENERGY