brazilian tax system - iep.ru · pis/pasep value added 1,65% cofins value added 7,60% inss payroll...

TRANSCRIPT

Brazilian Tax System

Brazilian Tax System

March/2013

Brazilian Tax System

General Features Brazilian Federation

Brazil is a federation composed of three highly decentralized government levels, each of them has its political, finance and administrative autonomy established by the Federal Constitution.

Brazilian Tax System

- Political Division: Central Government, States (26) and Federal District(1) and more than 5,000 municipalities

- Regional Inequalities: The three wealthiest States with 53% of GDP; the three poorest with 0.63% of GDP

- Population: 190 million inhabitants, more than 4 million formal companies

- Multiple Tax Administration (TA): federal, state and local.

General Features National Particularities

Brazilian Tax System

TAXES

TAXES and CONTRIBUTIONS

Brazilian Tax System

TAXES Competence

Union (Federal

Government) - Secretariat of

the Federal Revenue of Brazil

Taxes on Foreing Trade

- Tax on Import of goods and services - II - Tax on export of goods and services - IE

Taxes on Income and Earnings - IR

- Personal Income Tax - IRPF - Corporate Income Tax - IRPJ

- Tax on Manufactured Goods - IPI - Tax on Financial Operations - IOF - Tax on Property Land - ITR

States and Federal District

- Tax on the Circulation of Goods and transportation and communication Services – ICMS - Tax on Ownership of Motor Vehicles – IPVA - Inheritance and Gift Tax - ITCD

Municipalities (Local) and FD

- Urban Real Estate Tax – IPTU - Tax on Services – ISS - Tax on Real Estate Conveyance - ITBI

Brazilian Tax System

CONTRIBUTIONS

- Contribution for the Financing of Social Security - COFINS - Contribution to Social Integration Program and for Public Employee´s Asset Formation Program - PIS/PASEP Social Contribution on Net Profit of Enterprise – CSLL - Contribution for Intervention in the Economic Order - CIDE - Social Security Contribution on payroll (employee / employer) and self-employed

Union (Federal

Government) - Secretariat of

the Federal Revenue of Brazil

States and Federal District

- Contribution for Security of Public Employee

- Contribution for Security of Public Employee - Public Lighting Contribution

Municipalities (Local) and FD

Competence

Brazilian Tax System

MAIN TAX RATES

TAX TAX BASE RATEIRPJ Profit 15%/25%IPI Value Added 10% (Average)CSLL Profit 9%PIS/PASEP Value Added 1,65%COFINS Value Added 7,60%INSS Payroll 20%ICMS Value Added 9%, 17%, 25% and OthersISS Turnover 5%I.I. Imports (FOB Value) 14% (Average)CIDE Import/Prodution Value of Fue Ad Rem*

* Ad Rem: Specific rate per unit of product

Brazilian Tax System

PERSONAL INCOME TAX

Allowed Deductions

- Social Security : 9% to 11%; - Dependents : US$ 1.080 per dependent; - Instruction : up to US$ 1.690; - Health Care : Unlimited and; - Domestic Employee Social Contribution

Until 10.742 -From 10.742 to 16.099 7,5From 16.099 to 21.466 15From 21.466 to 26.822 22,5Over 26.822 27,5

Anual Net Income Tax Brackets (US$)

Tax Rates %

Brazilian Tax System

TAX BURDEN – 2011 R$ MILLION

TAX TAX COLLECTION PART. % ON GDP

UNION 1.024.710 24,73 - INCOME TAX 255.333 6,16

Personal Income Tax 20.438 0,49 Corporate Income Tax 94.797 2,29 Withholding (Personal and Corporate) 140.098 3,38

- IPI 41.207 0,99 - COFINS 164.814 3,98 - PIS/PASEP 42.840 1,03 - Contribution on payroll 246.031 5,94 - CSLL 58.594 1,41 - OTHERS 215.891 5,22

STATES 357.507 8,63 - ICMS 297.299 7,18 - OTHERS 60.208 1,45

MUNICIPALITIES 80.734 1,95 - ISS 38.516 0,93 - IPTU 19.334 0,47 - OTHERS 22.884 0,55

TOTAL 1.462.951 35,31

GDP 4.143.166

Brazilian Tax System

Union 70,04%

States

24,44%

Municipalities

5,52%

TAX BURDEN – 2011

Level of Government - % Participation

Brazilian Tax System

TAX BURDEN – 2011

18,40%

26,15%

3,52%

2,15% 1,22%

48,57% Social Security

Property

Consumption

Financial Operations Others Income Tax

Bases of Taxation R$ million % Tax Collection % GDP

Income Tax 278.321 19,02% 6,72%Social Security 376.849 25,76% 9,10%Property 54.143 3,70% 1,31%Consumption 720.098 49,22% 17,38%Financial Operations 32.027 2,19% 0,77%Others 1.461 0,10% 0,03%TOTAL 1.462.951 100,00% 35,31%

Brazilian Tax System

18,1% 20,9%

24,8% 26,0%

28,0% 28,1% 29,8% 31,3% 31,7% 32,4%

33,5% 33,9%

35,0% 36,3% 36,7% 37,6%

42,8% 42,9% 43,0% 43,8%

45,8% 48,2%

Mex

ico

Chi

le

USA

Turk

ey

Irel

and

Japa

n

Swis

s

New

Zea

land

Spai

n

Isra

el

Bra

zil

OC

DE

ave

rage

Uni

ted

Kin

gdom

Ger

man

y

Lux

embo

urg

Hun

gary

Nor

way

Fran

ce

Ital

y

Bel

gium

Swed

en

Den

mar

k

TAX BURDEN – 2010

Source: RFB and OECD. 1. Preliminary Data. Japan´s data refers to 2009. 2. Average of OECD countries listed on graph.

Brazilian Tax System

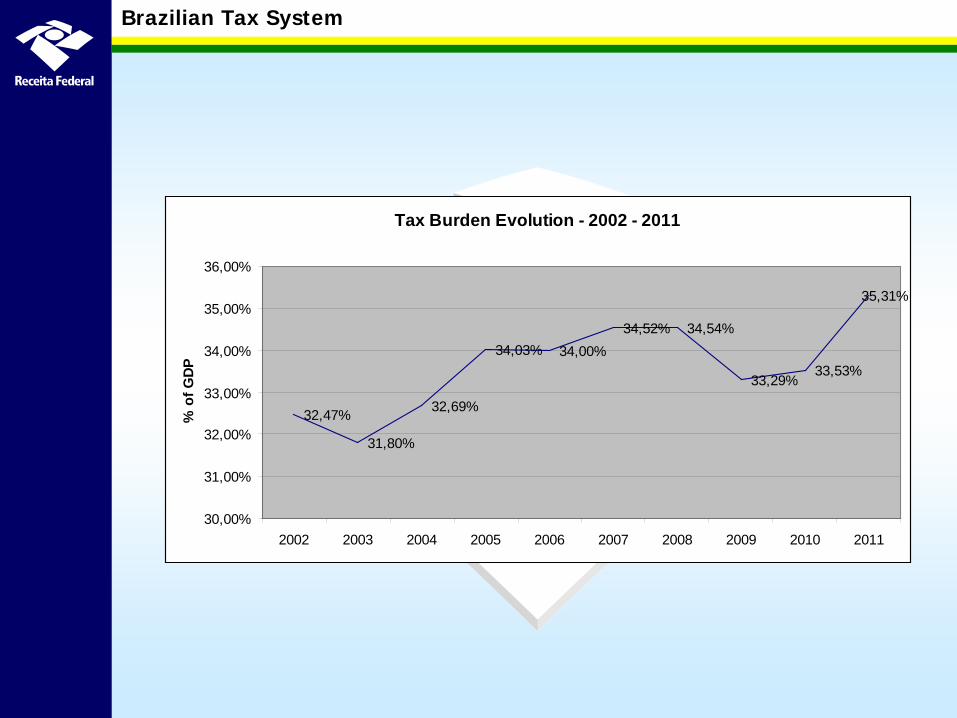

Tax Burden Evolution - 2002 - 2011

32,47%

31,80%

32,69%

34,03% 34,00%34,52% 34,54%

33,29%33,53%

35,31%

30,00%

31,00%

32,00%

33,00%

34,00%

35,00%

36,00%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

% o

f GDP

Brazilian Tax System

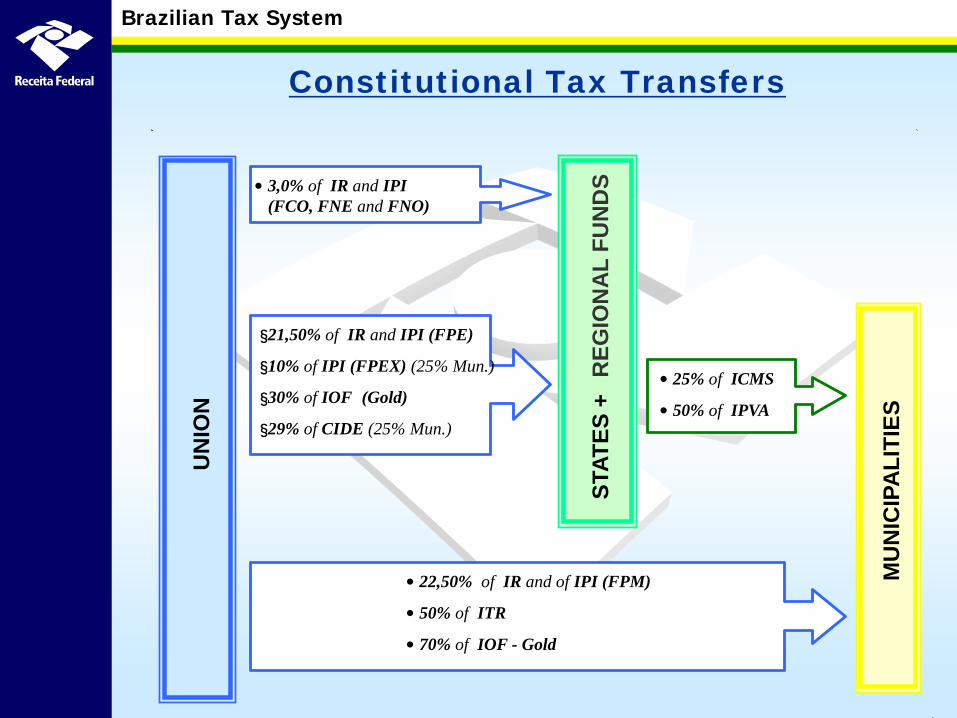

States Municipalities

Region Development

Funds

Union

Constitutional Tax Transfers

IOF IR IPI ITR CIDE

NO 0,6

NE 1,8

CO 0,6

Gold

3,%

IPIex

CIDE

25%

25%

ICMS 25%

IPVA 50%

ISS

IPTU

ITBIv

Brazilian Tax System

UN

ION

STAT

ES +

R

EGIO

NA

L FU

ND

S

• 22,50% of IR and of IPI (FPM)

• 50% of ITR

• 70% of IOF - Gold

MU

NIC

IPA

LITI

ES

• 25% of ICMS

• 50% of IPVA

§ 21,50% of IR and IPI (FPE)

§ 10% of IPI (FPEX) (25% Mun.)

§ 30% of IOF (Gold)

§ 29% of CIDE (25% Mun.)

• 3,0% of IR and IPI (FCO, FNE and FNO)

Constitutional Tax Transfers

Brazilian Tax System

21,50%

22,50%

3,00%

53,00%

States

Municipalities

Regional Funds

Union

Income Tax

Income Tax 21,50% 22,50% 3,00% 47,00% 53,00%IPI 31,50% 22,50% 3,00% 57,00% 43,00%ITR - 50,00% - 50,00% 50,00%IOF-Gold 30,00% - - 30,00% 70,00%CIDE 29,00% - - 29,00% 71,00%

Remain with

UnionTotalUnion Taxes

Transfered States Municipalities Regional Funds

Constitutional Tax Transfers

Brazilian Tax System

31,50%

22,50% 3,00%

43,00%

States

Municipalities Regional Funds

Union

Tax on Manufactured Goods - IPI

Income Tax 21,50% 22,50% 3,00% 47,00% 53,00%IPI 31,50% 22,50% 3,00% 57,00% 43,00%ITR - 50,00% - 50,00% 50,00%IOF-Gold 30,00% - - 30,00% 70,00%CIDE 29,00% - - 29,00% 71,00%

Remain with

UnionTotalUnion Taxes

Transfered States Municipalities Regional Funds

Constitutional Tax Transfers

Brazilian Tax System

Tax on Property Land - ITR

50,00% 50,00% Municipalities Union

Income Tax 21,50% 22,50% 3,00% 47,00% 53,00%IPI 31,50% 22,50% 3,00% 57,00% 43,00%ITR - 50,00% - 50,00% 50,00%IOF-Gold 30,00% - - 30,00% 70,00%CIDE 29,00% - - 29,00% 71,00%

Remain with

UnionTotalUnion Taxes

Transfered States Municipalities Regional Funds

Constitutional Tax Transfers

Brazilian Tax System

Tax on Financial Operations/Gold – IOF-Gold

30,00%

70,00%

States

Union

Income Tax 21,50% 22,50% 3,00% 47,00% 53,00%IPI 31,50% 22,50% 3,00% 57,00% 43,00%ITR - 50,00% - 50,00% 50,00%IOF-Gold 30,00% - - 30,00% 70,00%CIDE 29,00% - - 29,00% 71,00%

Remain with

UnionTotalUnion Taxes

Transfered States Municipalities Regional Funds

Constitutional Tax Transfers

Brazilian Tax System

Contribution for Intervention in the Economic Order - CIDE

29,00%

71,00%

States

Union

Income Tax 21,50% 22,50% 3,00% 47,00% 53,00%IPI 31,50% 22,50% 3,00% 57,00% 43,00%ITR - 50,00% - 50,00% 50,00%IOF-Gold 30,00% - - 30,00% 70,00%CIDE 29,00% - - 29,00% 71,00%

Remain with

UnionTotalUnion Taxes

Transfered States Municipalities Regional Funds

Constitutional Tax Transfers

Brazilian Tax System

Tax Policy 2010- 2012

• Tax relief – Payroll – Consumer goods and credit – Capital goods

• Increased tariff protection

Brazilian Tax System

Tax relief

– Payroll

Economic activities 2011 2012 2013 2014Furniture, apparel, leather goods 74 974 1.067 1.067 Information Technology 80 1.058 1.159 1.159 Hospitality 1.790 5.221 5.534 Road transport of passenger, Air and maritime cargo and passenger transport 2.582 2.861 Building 1.900 3.157 Retail 1.273 2.116 Other transformation industries 2.290 2.539 Total 2.165 5.834 17.505 20.447 % of Social Security Contributions on the Payroll 0,9% 2,4% 7,1% 8,3%

Tax Relief - R$ million

Brazilian Tax System

Tax relief

– Capital goods Economic activities 2010 2011 2012 2013 2014Building material 723 1.597 1.865 2.538 2.028 Trucks 385 915 922 1.358 1.141 Others 390 1.047 985 1.090 1.199 Total 3.508 5.570 5.784 6.999 6.382 % of IPI 8,5% 13,5% 14,0% 17,0% 15,5%

Tax Relief - R$ million

Brazilian Tax System

Tax relief

– Consumer goods and credit

Economic activities 2010 2011 2012 2013 2014Furniture 288 431 1.219 255 255 Appliances ("white goods") 1.174 874 872 Cars 2.850 1.648 Others 223 38

Credit (IOC) 2.806 3.600 3.600 Total 288 431 5.466 2.815 1.127 % of IPI 0,7% 1,0% 13,3% 6,8% 2,7%% of IOC 8,8% 11,3% 11,3%

Tax Relief - R$ million

Brazilian Tax System

Tariff Protection

Tariff Level (% of imports) Commom Tariff Regime

5,98% 5,80%5,28%

5,58% 5,48% 5,65% 5,71%

6,58%7,00%

7,50% 7,64%

3,00%

4,00%

5,00%

6,00%

7,00%

8,00%

9,00%

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012