brazil economic outlook and investment opportunities jorge arbache university of brasilia busbc...

TRANSCRIPT

1

Brazil Economic Outlook and Investment Opportunities

Jorge ArbacheUniversity of Brasilia

BUSBC Meeting, Brasilia, April 28, 2015

2

1. Overview

3

Recent economic performanceGDP per capita growth (%)

Source: Central Bank

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

-2

-1

0

1

2

3

4

5

6

7

-0.1

1.7

-0.1

4.3

1.9

2.8

4.8

3.9

-1.3

6.5

2.9

0.8

1.8

-0.7

-1.5

-1.0

-0.2

0.0

Note: 2015-2018: our own estimates based on macroeconometric modelling and CGE analyses

4

• End of the low hanging fruit growth model: consumption, easy credit, international liquidity, government spending and commodity boom

5

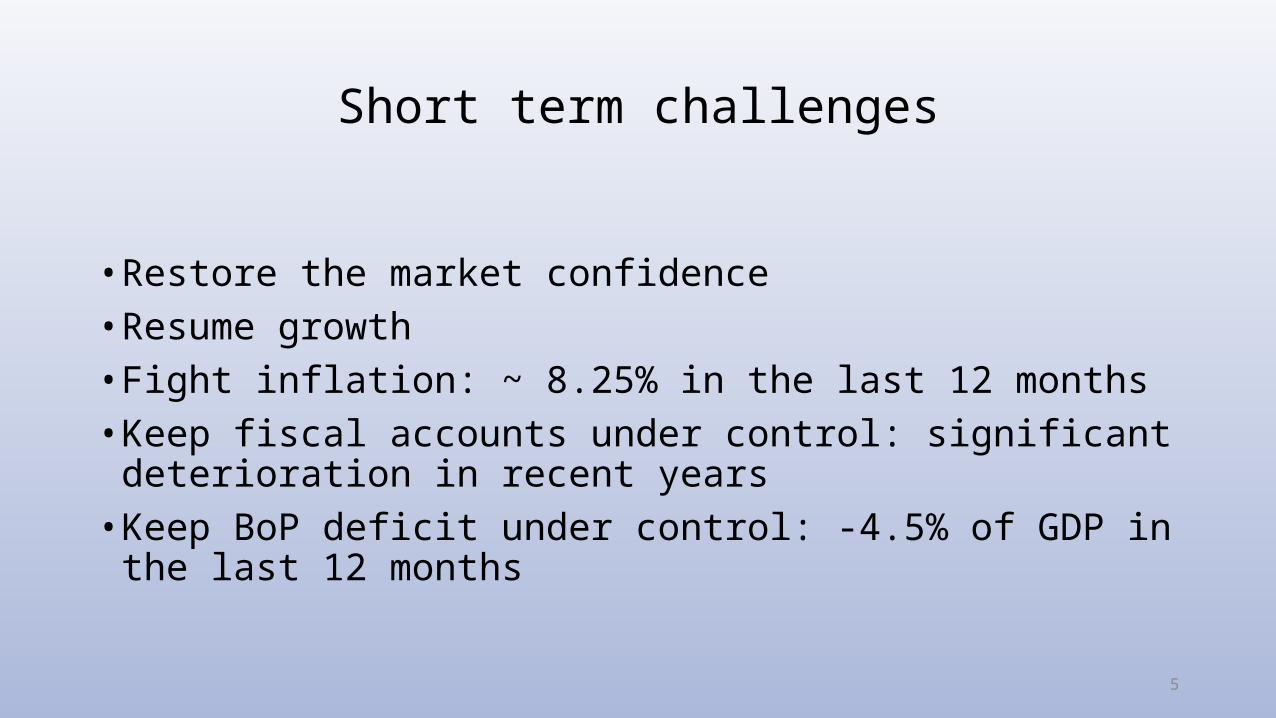

Short term challenges

• Restore the market confidence• Resume growth• Fight inflation: ~ 8.25% in the last 12 months• Keep fiscal accounts under control: significant deterioration in recent

years• Keep BoP deficit under control: -4.5% of GDP in the last 12 months

6

Current account balance - % GDPSource: Central Bank

CPI (%) – monthlySource: Central Bank

20012002

20032004

20052006

20072008

20092010

20112012

20132014

-5

-4

-3

-2

-1

0

1

2

3

Jan-10

May-1

0

Sep-10

Jan-11

May-1

1

Sep-11

Jan-12

May-1

2

Sep-12

Jan-13

May-1

3

Sep-13

Jan-14

May-1

4

Sep-14

Jan-150

0.2

0.4

0.6

0.8

1

1.2

1.4

7

2. What the government is doing?

8

Pillars of Mr Levy`s policy

• Focus on gross public debt• Accelerate concessions and PPPs opportunities• Increase technical and college-level training• Foster increase in labor supply• Changes in Federal and State VAT• Expansion of the SIMPLES and ‘doing business’ initiatives• Focus on international trade

Source: MoF

9

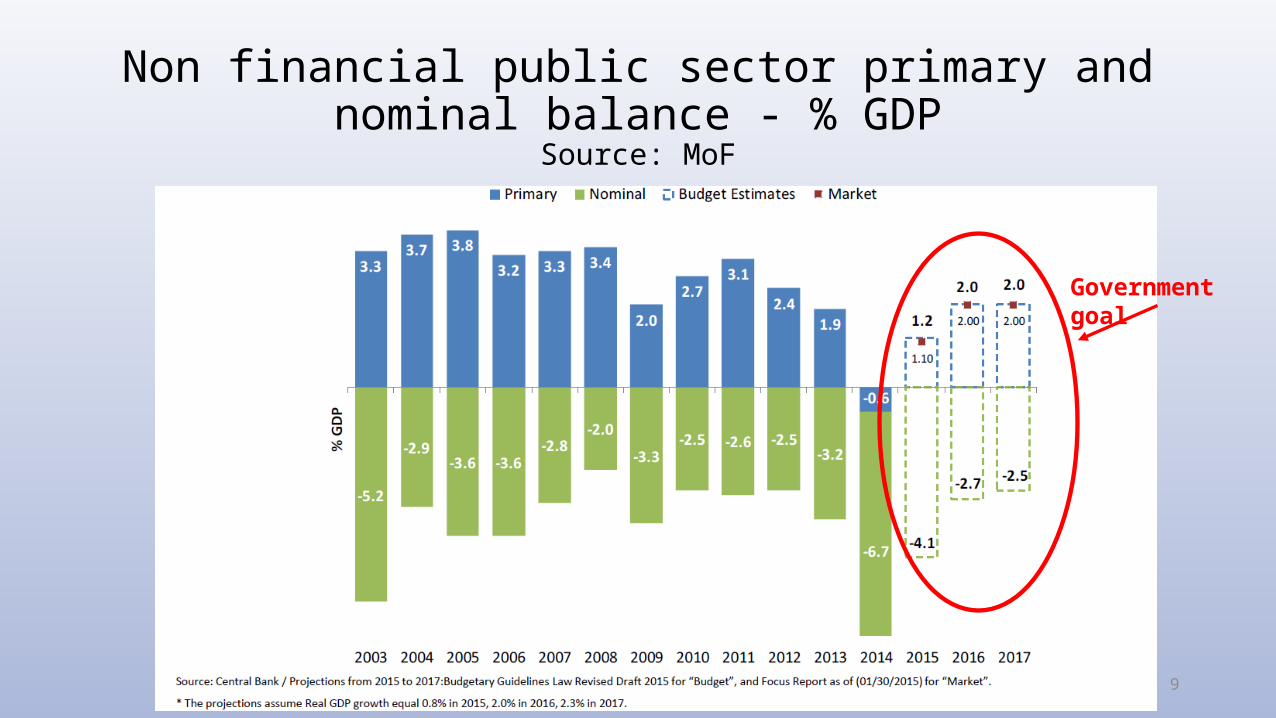

Non financial public sector primary and nominal balance - % GDP

Source: MoF

Government goal

10

3. Challenges ahead

11

• Brazil -- combination of a still low unemployment rate (4.9% in the last 12 months) with recession, rising inflation and current account deterioration: trap

12

How to explain the trap?

• Low unemployment is partly explained by the decelerating working age population, low labor productivity and service sector boom, which is highly labor intensive

• Exchange rate pass-through

• Falling savings and investment ratios

• Poor international competitiveness

13

Medium term challenges

• Output gap has decreased: 2.3% from 3.4% in the last 15 years (our own estimates Jan/2015); IMF estimates (Apr/2015): 2.5%

14

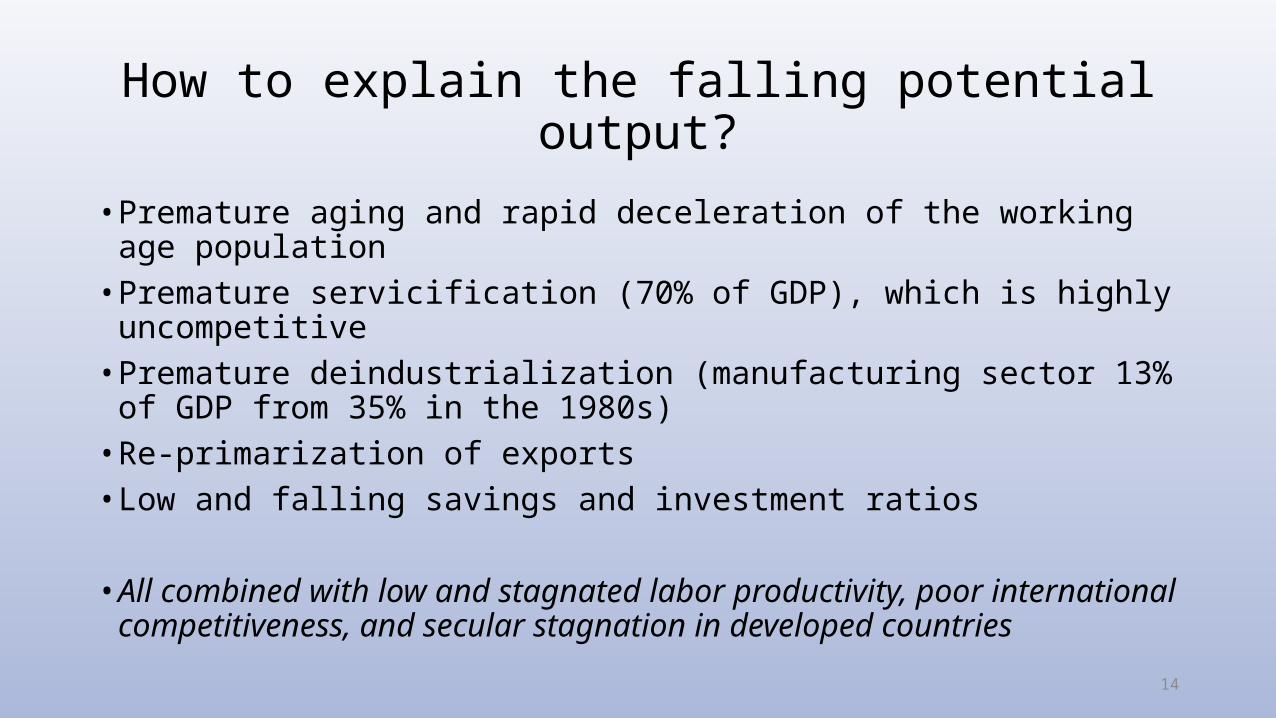

How to explain the falling potential output?

• Premature aging and rapid deceleration of the working age population• Premature servicification (70% of GDP), which is highly uncompetitive• Premature deindustrialization (manufacturing sector 13% of GDP from

35% in the 1980s)• Re-primarization of exports• Low and falling savings and investment ratios

• All combined with low and stagnated labor productivity, poor international competitiveness, and secular stagnation in developed countries

15

4. Are there business opportunities?

16

• Despite the poor environment and growth prospects in Brazil, there are plenty of opportunities out there in the short and medium terms

• Demographic changes are creating great opportunities

• The desperate need to increase efficiency and productivity favors smart initiatives and smart businesses

• Expansion of concessions, PPPs and privatizations

17

• Huge potential for industrialization of comparative advantages e.g. agribusiness, pre-salt, minerals, renewable energy, biodiversity, etc

• New frontiers of development in the countryside and in fringe states

• Smart cities projects

• Regional markets and the still rising middle class

18

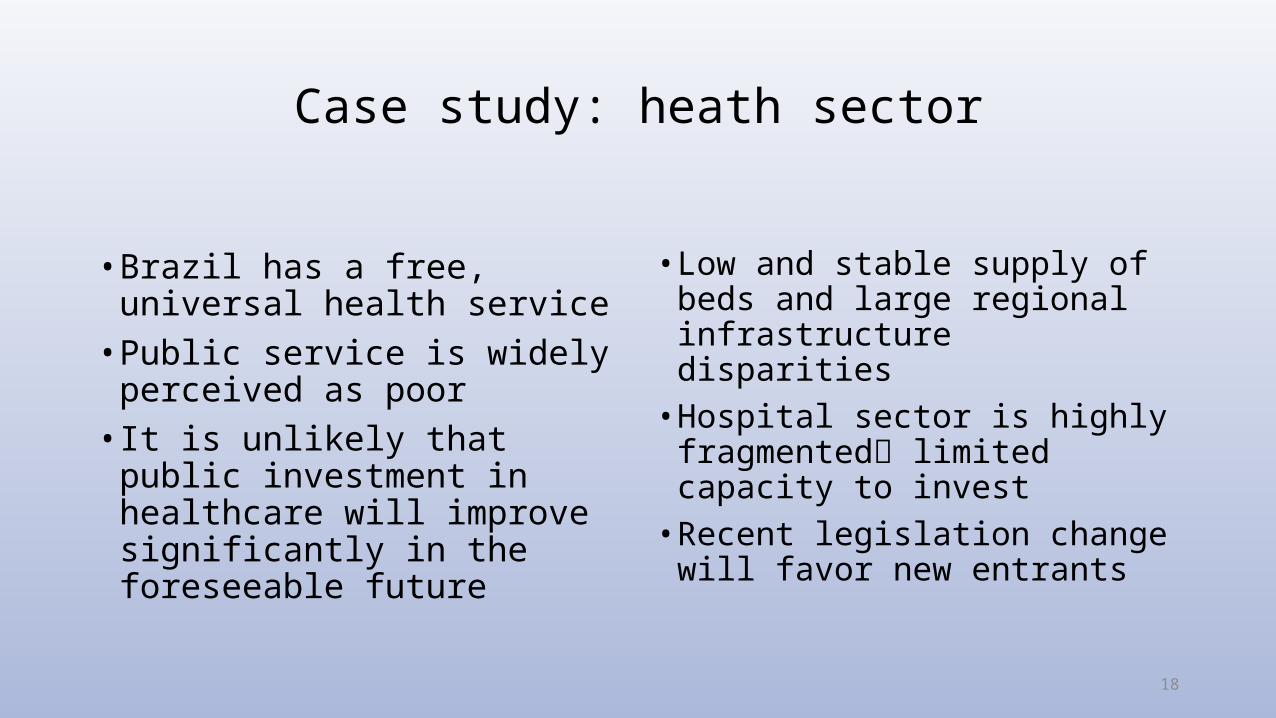

Case study: heath sector

• Brazil has a free, universal health service• Public service is widely perceived

as poor• It is unlikely that public

investment in healthcare will improve significantly in the foreseeable future

• Low and stable supply of beds and large regional infrastructure disparities• Hospital sector is highly

fragmented limited capacity to invest• Recent legislation change will

favor new entrants

19

Japan

Korea

Russian

Fed.

German

y

Austria

Hungary

Czech Rep

ublic

PolandFra

nce

Belgium

Slova

k Rep

ublic

Finlan

d

Luxe

mbourg

Estonia

OECD25

Switz

erlan

d

Greece

Netherl

ands

Slove

nia

Australi

a

Denmark Ita

ly

Portuga

l

Icelan

d

Norway

Israe

lSp

ain

United St

ates

Irelan

d

United Kingd

om

New Ze

aland

Canad

aChina

Swed

en

Turke

yBraz

il

South Afri

caChile

Mexico

Indonesia

India

2.3

4.9

Note: Total of beds per 100 000 habitants. Source: WHO 2013 and OECD 2013.

Supply of beds: Brazil vs. OECD

20

• Demographic changes are already impacting the healthcare demand strongly in terms of level, composition and type of care

• 19% of population above 60 years old in 2030 – it was 11% in 2013

• 2000 • 2030

0-45-9

10-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-89

90+

0-45-9

10-1415-1920-2425-2930-3435-3940-4445-4950-5455-5960-6465-6970-7475-7980-8485-89

90+

21

• As a result of the growing income and demographic changes, the coverage of private health insurance has increased from 34 to 51 million people between 2004 and 2014

• Only 1/4 of total population is covered by private health insurance

2004 2006 2008 2010 2012 2014

33.8437.25

41.4745.18

48.2850.93

Mill

ion

of P

eopl

eSource: ANS

22

• A substantial share of additional supply of healthcare will have to be provided by the private sector

• Large room for new investments in infrastructure and market consolidation• Hospitals• Diagnosis services• Retail health clinics

23

4. Risks

24

• Limited margin for fiscal maneuver in the short term

• Pursuing a fiscal adjustment will be politically challenging, but emerging awareness on the need to go forward with the reforms proposed by government

• Loss of investment grade and access to credit markets

• Economic slack and political uncertainties globally

25

• China`s slowdown and commodity prices

• FED’s policy move

• Protectionism and trade policies

• Exchange rate uncertainties

• Environmental changes