brave new world: mifid2 and mifir – the changes facing … february/20160215... · brave new...

TRANSCRIPT

Brave New World: MiFID2 and MiFIR – The changes facing the Financial Markets

Charlotte Stalin

February 2016

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

1 / L_LIVE_EMEA1:31983747v1

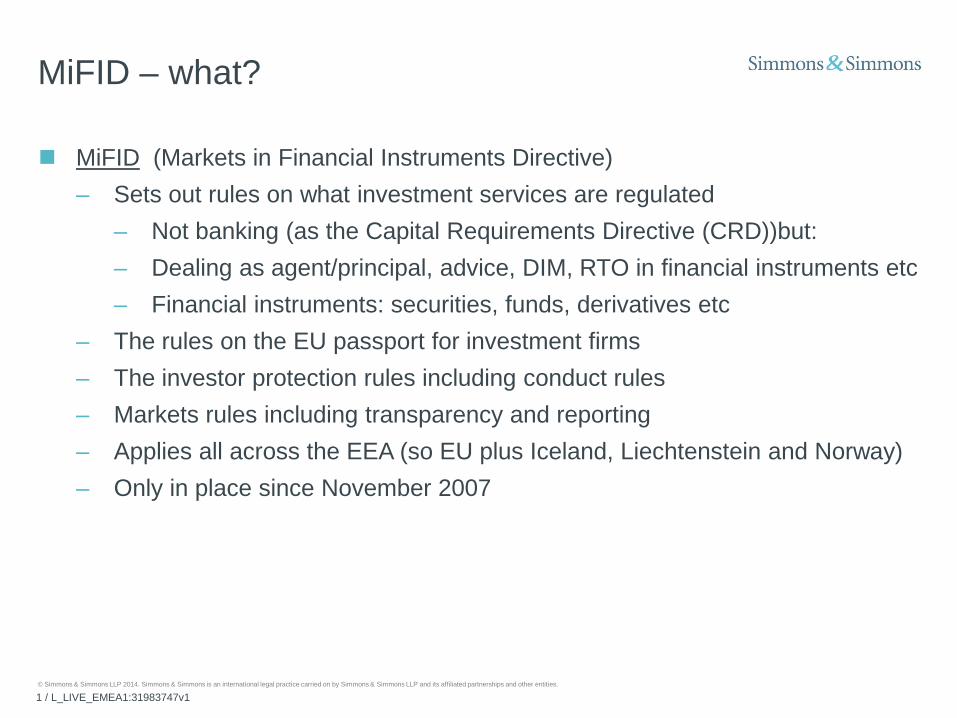

MiFID – what?

MiFID (Markets in Financial Instruments Directive) – Sets out rules on what investment services are regulated

– Not banking (as the Capital Requirements Directive (CRD))but: – Dealing as agent/principal, advice, DIM, RTO in financial instruments etc – Financial instruments: securities, funds, derivatives etc

– The rules on the EU passport for investment firms – The investor protection rules including conduct rules – Markets rules including transparency and reporting – Applies all across the EEA (so EU plus Iceland, Liechtenstein and Norway) – Only in place since November 2007

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

2 / L_LIVE_EMEA1:31983747v1

MiFID2 – why and how?

Result of financial crisis and unresolved issues under MiFID1

Repeals MiFID1

Applies to investment banks, broker dealers, private banks, wealth managers/advisors, exchanges/markets, certain data providers.

But also direct and indirect impact on non-EU firms (third country firms) that interact with the EU market.

Wide coverage will make wide sweeping reforms to market structure, transparency, investor protection, conduct of business, senior management, product governance, transaction reporting and market access for third country (non-EU) firms.

Effect more will be subject to authorisation , more of everything in MIFID1

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

3 / L_LIVE_EMEA1:31983747v1

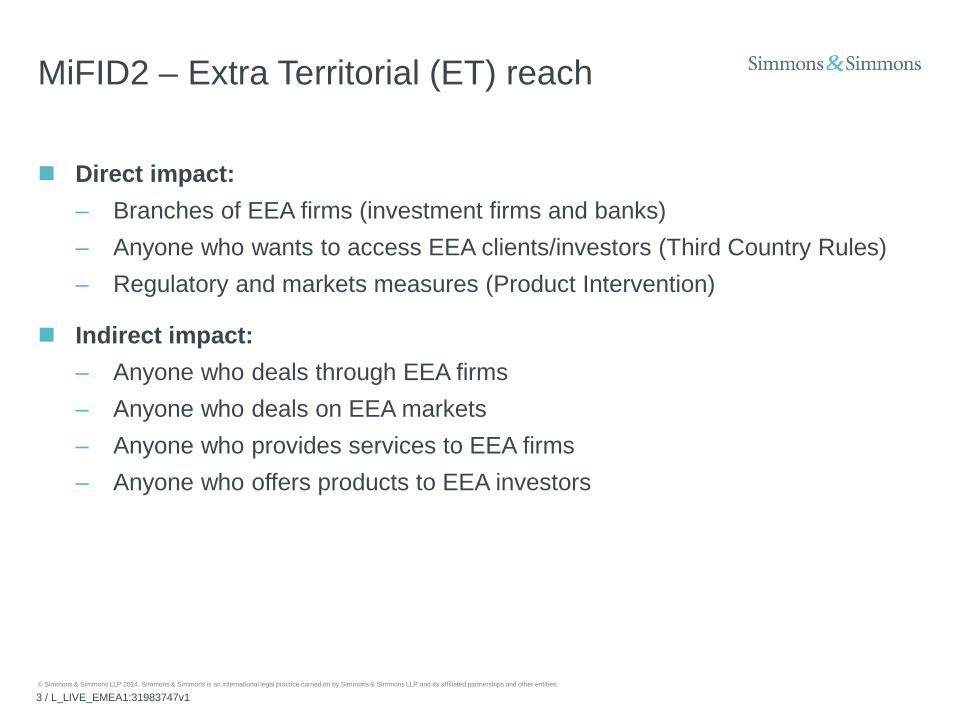

MiFID2 – Extra Territorial (ET) reach

Direct impact: – Branches of EEA firms (investment firms and banks) – Anyone who wants to access EEA clients/investors (Third Country Rules) – Regulatory and markets measures (Product Intervention)

Indirect impact: – Anyone who deals through EEA firms – Anyone who deals on EEA markets – Anyone who provides services to EEA firms – Anyone who offers products to EEA investors

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

4 / L_LIVE_EMEA1:31983747v1

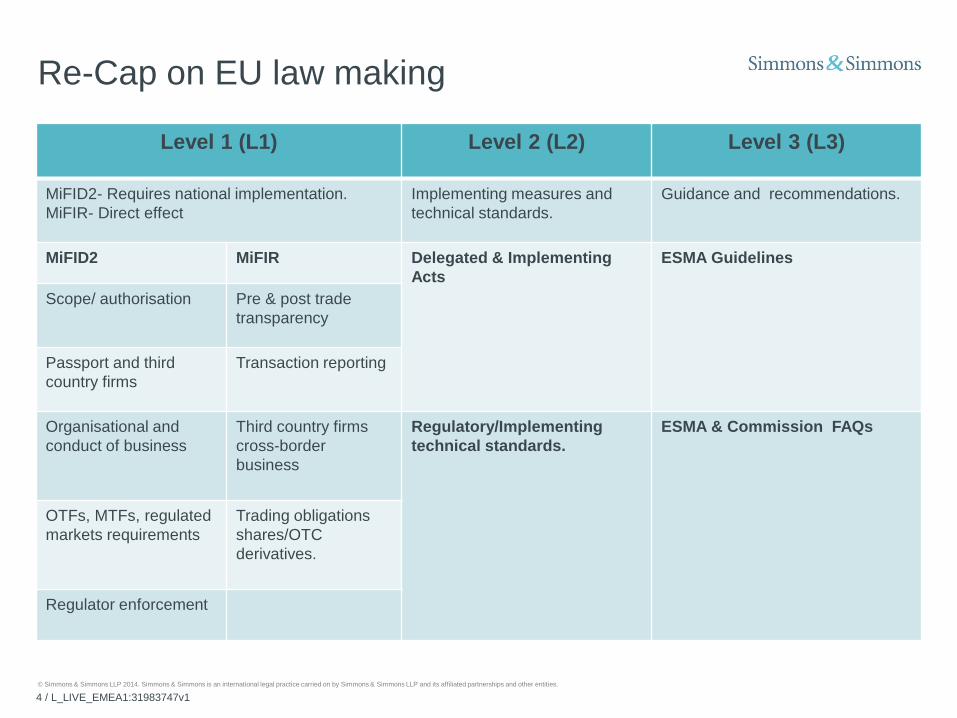

Re-Cap on EU law making

Level 1 (L1) Level 2 (L2) Level 3 (L3)

MiFID2- Requires national implementation. MiFIR- Direct effect

Implementing measures and technical standards.

Guidance and recommendations.

MiFID2 MiFIR Delegated & Implementing Acts

ESMA Guidelines

Scope/ authorisation Pre & post trade transparency

Passport and third country firms

Transaction reporting

Organisational and conduct of business

Third country firms cross-border business

Regulatory/Implementing technical standards.

ESMA & Commission FAQs

OTFs, MTFs, regulated markets requirements

Trading obligations shares/OTC derivatives.

Regulator enforcement

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

5 / L_LIVE_EMEA1:31983747v1

19 Dec 2014: Final report issued to

Commission; Second CP issued by

ESMA

The latest on timing…

2014 2015 2016 2018

15 April 2014:

Ratification of Level1

text

13 May 2014:

adopted by

Council

22 May 2014:

ESMA’s first CP and DP

12 June 2014:

Publication of L1 text in

the OJ

Sep 2015: ESMA Final

Report on 75% of the

RTSs

Feb/March 2016:

Level 2 Delegated Acts and technical standards

3 July 2016(?)

Entry into national

force

New DATE: 3 January

2018 GO LIVE

DATE (Previously 3 January

2017)

Dec 2015: ESMA Final Report on remaining 25% of the

RTSs

FCA CP 15/43

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

6 / L_LIVE_EMEA1:31983747v1

However timing remains uncertain…. Level 1: Getting there..

– Expected wholesale delay to implementation - 3 January 2018. – The key reasons: (i) lack of IT Infrastructure within ESMA and the National Competent

Authorities; and (ii) lack of finalised L2 technical standards and delegated acts. – Recent announcement silent on deadline for national transposition. – Member States pushing for an extension transposition into national law – currently 3

July 2016

Level 2: Significant delay – Final Delegated Acts expected in February 2016 followed by a three-month scrutiny

period by the Council and Parliament. – Technical Standards likely to be adopted by the Commission in

March 2016 followed by a one- to three-month scrutiny period.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

7 / L_LIVE_EMEA1:31983747v1

Current State: ESMA L2 Publications

ESMA Final Reports

29 June 2015: Contains 6 RTS/ITS covering: Authorisation, Passporting & 3rd Country Registration.

28 September 2015: Contains 28 RTS/ITS covering: Transparency, Microstructural issues, Commodity derivatives, Market reporting & Best execution.

11 December 2015: Contains 8 ITS covering: Trading Venue requirements, Authorisation of Data Reporting Service Providers, Position Reporting & Competent Authority requirements.

Forward View

The EC will need to adopt the DAs to start minimum of 3 month objection period for EP and Council

The EC has 3 months from the Final Report’s publication to decide whether to endorse or object or partially object RTS/ITS with the EP/Council then having a minimum period of 1 month to object to RTS. To date, the EC has not responded to any of the Final Reports.

The current Final Reports and the ‘Leaked’ DAs do not cover all L2 requirements (ie: Commodity Derivative reporting requirements, etc). The ‘Leaked’ DAs may be amended prior to publication (expected in Feb) to cover these missing areas, but this is not yet clear.

Some of the requirements contained within the Final Reports are subject to ongoing lobbying by various Member States (ie: Transparency, Commodity Position Limit Thresholds, etc).

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

8 / L_LIVE_EMEA1:31983747v1

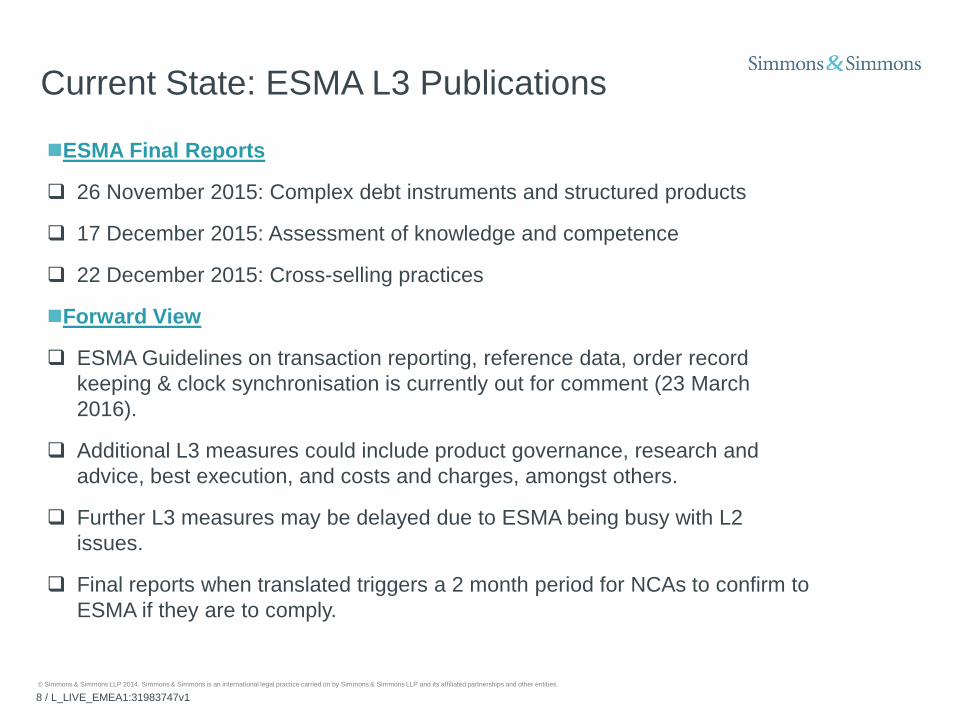

Current State: ESMA L3 Publications

ESMA Final Reports

26 November 2015: Complex debt instruments and structured products

17 December 2015: Assessment of knowledge and competence

22 December 2015: Cross-selling practices

Forward View

ESMA Guidelines on transaction reporting, reference data, order record keeping & clock synchronisation is currently out for comment (23 March 2016).

Additional L3 measures could include product governance, research and advice, best execution, and costs and charges, amongst others.

Further L3 measures may be delayed due to ESMA being busy with L2 issues.

Final reports when translated triggers a 2 month period for NCAs to confirm to ESMA if they are to comply.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

9 / L_LIVE_EMEA1:31983747v1

What does this mean on a national level? Who will be on time?

Very few Member States have begun any consultation process on MiFID2 (UK, Germany, and Netherlands).

Many NCAs are struggling with implementation.

Question as to transposition date! NCAs asked for 9 months if possible.

Gold-plating?

Expected Member States will ‘Gold-Plate’ various requirements, including but not limited to recordkeeping, corporate governance, product governance, investor protection, algo/HFT and inducements.

Likely to impact non-EU firms as gold-plating may apply MiFID2 provisions to a wider scope of firms and activities.

Result in lack of harmonisation

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

10 / L_LIVE_EMEA1:31983747v1

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

11 / L_LIVE_EMEA1:31983747v1

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

12 / L_LIVE_EMEA1:31983747v1

So breaking this down - impact on Third Country Firms Direct To access EEA counterparties/clients Will require registration or presence for Third Country Firms Two different types of access regimes, depending on the relevant client type.

Indirect – “Butterfly Effect” Impact on firms who trade on EU venues and/or with EU counterparties or market or

distribute products into the EU but do not have an EU presence. Transparency and trading obligations. Product governance. Investor protection. Inducements. Commodity derivatives and emission allowance.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

13 / L_LIVE_EMEA1:31983747v1

Accessing EEA clients - Third Country Regimes CROSS- BORDER SERVICE – REGISTRATION

– Services to eligible counterparties and per se professional – ESMA registration.

– The EU Commission must have first adopted an equivalence decision. – The Third Country firm must be authorised in the Third Country and it must be subject to effective

supervision. – Cooperation arrangements must be in place between ESMA and the relevant competent

authorities. – Question what countries will meet the test!

LOCAL BRANCH SERVICE – Services to retail or elective professional – Option for EU Member State to require third country firms to establish and register a branch – The third country firm must be authorised in the third country and it must be subject to effective

supervision. – Cooperation arrangements must be in place between ESMA and the relevant competent

authorities of the third countries. – Branch will need to comply with MiFID2 and MiFIR conduct of business rules

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

14 / L_LIVE_EMEA1:31983747v1

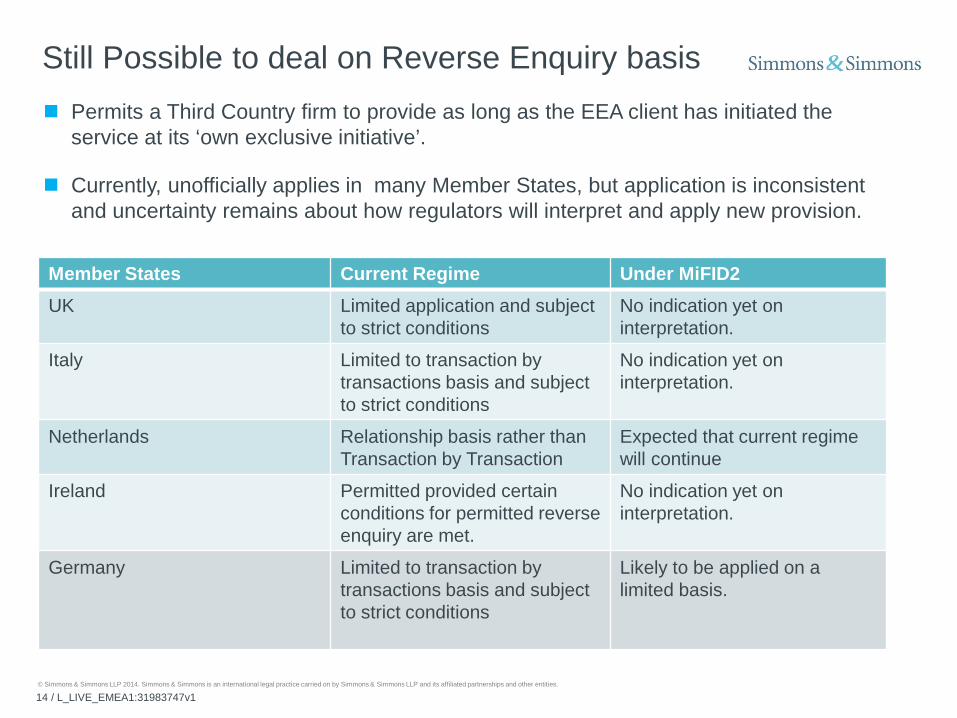

Still Possible to deal on Reverse Enquiry basis Permits a Third Country firm to provide as long as the EEA client has initiated the

service at its ‘own exclusive initiative’.

Currently, unofficially applies in many Member States, but application is inconsistent and uncertainty remains about how regulators will interpret and apply new provision.

Member States Current Regime Under MiFID2 UK Limited application and subject

to strict conditions No indication yet on interpretation.

Italy Limited to transaction by transactions basis and subject to strict conditions

No indication yet on interpretation.

Netherlands Relationship basis rather than Transaction by Transaction

Expected that current regime will continue

Ireland Permitted provided certain conditions for permitted reverse enquiry are met.

No indication yet on interpretation.

Germany Limited to transaction by transactions basis and subject to strict conditions

Likely to be applied on a limited basis.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

15 / L_LIVE_EMEA1:31983747v1

What does it all mean for Third Country firms? Application across Member States - Currently unclear whether Member states will apply the

branch regime or whether ESMA will grant equivalence decisions. Only few regulators have indicated a proposed approach:

UK- FCA has decided to not elect for regime. Netherlands - Will elect for the branch regime for retail clients but not professionals. Belgium - Will likely opt in as currently operates a light touch approach.

Existing national regimes to apply - In the absence of any opt-in existing Member State regimes will apply.

UK - Private placement Belgium - Light touch license requirement Netherlands - Light touch for professionals Ireland - Third country cross-border exemption.

Non-EU firms should monitor national implementation and interpretations closely.

Should consider how they currently access EU markets and whether they will need to alter their approach or their business structure to accommodate new changes.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

16 / L_LIVE_EMEA1:31983747v1

Indirect - Product governance Regime which impacts ‘manufacturers’ and ‘distributors’ of investment products will be

required to, including: – Manufacturers: Know the target market, stress test products, obtain MI and monitor

product throughout life cycle – Distributors: Ensure they have in place adequate product governance arrangements to

ensure product and services they intend to offer are compatible with client. – Distributors: Periodically review and update product governance arrangements to

ensure they remain fit for purpose and robust

Impact - when products are manufactured by Third Country firms or non-MiFID firms, distributors shall take all reasonable steps to ensure the level of information obtained from manufacturer is reliable and adequate to ensure product meets the requirements of the target market.

Required to enter into suitable written agreement with manufacturer to exchange information.

Expect detailed DDQs on you as distributor, more detailed DAs and more information about target market

Similar as manufacturer, ensure level of information required by a EEA distributor can be provided

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

17 / L_LIVE_EMEA1:31983747v1

Investor Protection - Investment advice, suitability, conflicts

MiFID2 requires greater information to be provided to clients.

Where a distributor/selling agent in the EEA also provides investment advice to its clients as part of the selling process, it will have to: inform its client whether such advice is on a dependent or independent basis (for third

party distributors and selling agents, it will be the latter);and whether a periodic assessment of suitability will be provided; guidance on warnings and risks associated with investments; and provide information on all costs and associated charges relating to both investment and

ancillary services.

EEA selling agents will also be subject to enhanced conflict of interests requirements which will require detailed information about target markets and products they are offering.

Effect: Anyone offering products into EEA via EEA distributor will be expected to provide more information about the products to ensure compliance for distributor.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

18 / L_LIVE_EMEA1:31983747v1

Impact on non-EU firms distributing/selling products through EU agents

Greater transparency between non-EU firms to their EU selling agents and flow of information: Target Market assessment. Costs and charges. Product features and risks. Distributors to periodically inform and provide data to manufacturer about

experience with product. Any potential conflicts that could arise with target clients. Actions to be pursued if investments are marketed or sold to wrong clients.

Clear written agreements required between non-EU firms and EU selling agents setting out information requirements and obligations.

Need for ongoing contact and flow of information between parties.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

19 / L_LIVE_EMEA1:31983747v1

New Inducement rules MiFID firms which provide investment advice on an independent basis will also be subject

to restrictions on inducements. May not accept and retain fees, commissions or any monetary or non-monetary

benefits paid or provided by any third party or person acting on behalf of a third party in relation to the provision of the service to clients.

Exception- minor non-monetary benefits that are capable of enhancing the quality of service provided to a client and are of a scale and nature such that they could not be judged to impair compliance with the firm’s duty to act in the best interest of the client.

Minor non-monetary benefits to be disclosed.

Effect on Non-EU firms EU third party introducers which act for clients which invest in funds managed by a

non-EU manager will not be able to receive rebates or other payments from that Non-EU manager.

Need to consider pricing structures and unbundling of services and costs.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

20 / L_LIVE_EMEA1:31983747v1

Pre and Post Trade Transparency

Pre and post trade transparency obligations will apply in respect of: – bonds and structured finance products which have been admitted to trading on an

Regulated Market. – derivatives and emissions allowances which have been admitted to trading on any MiFID

2 venue, or which are clearing-eligible under EMIR; and – equity instruments.

Waivers permitted at discretion of competent authorities and in certain circumstances such as where the price is determined by reference to a “widely published” and “reliable” price

In relation to post-trade transparency requirements, competent authorities will still be able to authorise trading venues to provide for deferred publication of the details of transactions based on their type or size, but again the conditions for such deferrals will be more prescriptive/restrictive than currently under MiFID1 (where available).

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

21 / L_LIVE_EMEA1:31983747v1

Dark pool double volume cap

Firms concerned by such transparency should consider whether the “large-in-scale” waiver, which is not subject to these caps, is a viable option.

For shares and other equity-like instruments, a volume cap mechanism has been introduced to ensure that the use of waivers does not unduly harm price formation. If trading volumes* on a particular EEA dark pool in an equity/equity like instrument

that is listed on an EEA trading venue exceed 4% of total transaction volume in the stock during a rolling 12 month period, the dark pool must cease to operate in relation to that stock for 6 month

If aggregate trading volumes* across all EEA dark pools in an equity/equity like instrument that is listed on an EEA trading venue exceed 8% of total transaction volume in the stock during a rolling 12 month period, all such dark pools must cease to operate in relation to that stock for 6 month

* Cap calculation excludes orders flagged as “large in size” April 2015 LSE study 99 names out of the FTSE 100 would be subject to the ban

based on 2014 trading volumes.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

22 / L_LIVE_EMEA1:31983747v1

New Trading Venue and Trading Obligation MiFID2 introduces 3rd regulated trading venue for bonds, structured finance products,

emissions, derivatives- Organised Trading Facility (OTF).

Requirement that all shares which are listed on RM or traded on a trading venue take place on a RM, MTF, OTF or SI, or equivalent 3rd country venue.

Trading between FC and NFC that satisfy certain prescribed threshold conditions in respect of derivatives that the EU Commission (following input from ESMA) has determined are appropriate for such treatment, should be traded only on RM, MTF, OTF, or equivalent 3rd country venue.

Trading obligation applies (i) whether counter-party established in EU and (ii) third country entities subject to clearing obligations under EMIR when they enter into relevant derivative transactions and where the "contract has a direct, substantial and foreseeable effect within the Union or where such obligation is necessary or appropriate to prevent the evasion of any provision of this Regulation".

Exceptions: Intragroup transactions Certain types of counterparties below the clearing obligation threshold under

EMIR

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

23 / L_LIVE_EMEA1:31983747v1

Algo/High Frequency Trading

Not expressly covered by MiFID 1 but some some EEA regulators have their own domestic requirements – see e.g. Germany

New requirements for venues with members or participants that employ algorithmic trading techniques. “Algorithmic trading” is defined widely and includes most investment processes where a computer is used, not only those which are usually associated with “quant” or “high frequency” trading, such as investment processes where ideas are generated by computer and the use of “smart order routers” for execution of trades.

Trading venues which permit algorithmic trading will be required to: – establish systems to limit the ratio of unexecuted orders to transactions, – identify trades generated by algorithmic trading, and – have in place “throttle limits” and, in certain limited circumstances, “kill switches” to

stop trading by particular members / algorithms.

Non-EU firms which employ algorithms as part of their investment process to European trading venues via a European broker or other service provider should investigate to what extent their investment process and market access will cause them to be subject, albeit indirectly, to the new MiFID2 regimes and analyse what updates will be necessary to their systems and procedures as a result.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

24 / L_LIVE_EMEA1:31983747v1

Direct electronic access

New requirements for investment firms which provide clients with direct market access and/or sponsored access (together, direct electronic access or DEA) to trading venues.

DEA provider to have proper procedures to assess client suitability as well as to put in place a binding written agreement with each client regarding the essential rights and obligations arising from the provision of the service and that the DEA provider retains regulatory responsibility under MiFID2. It is expected that DEA providers will use such agreements to transfer regulatory risk onto their clients.

Requirement to set appropriate risk controls and thresholds on trading via DEA and if necessary, stop trading by a person that is using DEA. Such markets and venues will have to adopt specified tick size regimes and require their members to synchronise business clocks.

Non-EU firms who have direct market access or sponsored access to European trading venues via a European broker or other service provider will be required to enter into written agreements and should consider the additional requirements and controls that they will be subject to under the new regime.

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

25 / L_LIVE_EMEA1:31983747v1

So what does this mean if we trade on EU exchanges?

EU participants will need to consider the new requirements and restrictions under MIFID2 and potentially re-consider their trading strategies or how they trade on EU markets as a result.

Restrictions on the use of “dark pools”, will mean a wealth of new information relating to price discovery becoming available.

EU participants that use broker crossing networks and other relevant dark venues may see a significant decline in trading activity as the volume cap mechanism pushes trading activity onto LIT markets

EU participants will need to consider the implications for their trading and execution strategies and systems as some trades they have traditionally carried out using dark pools will potentially need to be carried out on-exchange. Firms should consider the impact for them if dark pool activity in a significant number of stocks in which they trade was to cease for 6 months.

EU participants which employ algorithmic trading and/or HFT techniques on a EU regulated market/trading venue or have DEA will be subject to the new mechanisms, processes and controls which such venues are required to implement under MiFID2, including on-site testing of algorithms to avoid disorderly trading conditions, capacity and monitoring obligations and trade controls (including pre-trade controls and “kill functionality”).

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

26 / L_LIVE_EMEA1:31983747v1

What should non-EU firms be doing now?

Macro impact analysis - – How does MiFID2 impact on my firm? – What potential changes will we have to make to our trading strategies, IT systems,

information systems and communications and agreements with EU counter-parties.

Contact EU brokers and counterparties and distributors to discuss how changes may impact their relationship and what new obligations/ requirements will need to be put in place.

For third party firms wishing to access EU markets consider the changes under the Third Country regime and whether any need to re-structure business or alter how the business currently accesses EU markets.

Legal & Compliance teams will need stay abreast of developments of L2 and L3 legislation and guidance.

Simmons & Simmons “MiFID2 Manager” may help..

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

27 / L_LIVE_EMEA1:31983747v1

Complex regulation made easy

Our dedicated MiFID2 expert resources include:

Our subscription service the MiFID2 Manager sets out the practical steps that need to be taken to stay on top of the requirements of MiFID2/MiFIR and its implementing legislation

The MiFID2 Tracker on elexica is a helpful tool to track and access all the legislative measures introduced under MiFID 2. It also includes articles and publications on the topic

Our international MiFID2 Bite size call series provides updates on new developments and considerations in the lead up to its implementation

Simmons & Simmons MiFID2 expert resources

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

28 / L_LIVE_EMEA1:31983747v1

Accessible 24/7, consistent, user friendly

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

29 / L_LIVE_EMEA1:31983747v1

Contacts

For further information Simmons & Simmons MiFID2 website http://www.simmons-simmons.com/en/Services-and-Sectors/Financial-Institutions/MiFID

Simmons & Simmons MiFID2 Tracker http://elexica.authoring.simmons.local/en/Resources/Microsite/MiFID-2-Tracker

Simmons & Simmons Legal Headwinds http://www.elexica.com/microsites/extras/LegalHeadwinds/index.aspx

Charlotte Stalin T +44 20 7825 4180 E [email protected]

© Simmons & Simmons LLP 2014. Simmons & Simmons is an international legal practice carried on by Simmons & Simmons LLP and its affiliated partnerships and other entities.

30 / L_LIVE_EMEA1:31983747v1

Charlotte Stalin

February 2016