branchless banking - shamrock conferences international -a ... · branchless banking: theme...

TRANSCRIPT

Branchless Banking

The Future of Micro Finance

Nadeem HussainNadeem HussainCEO & Founding President

N b 10 2010November 10, 2010

Branchless Banking: ThemeExpanding agent network for cash deposit, withdrawal, money transfers and account opening

OTC Channel open to everyone

State Bank of Pakistan’s robust branchless banking framework, detailed guidelines

Licensed bank behind all transactions with country’s first branchless banking license

Extended timings, no queues and minimal paperwork

Mobile Accounts for more convenience and security

first branchless banking license

Agent network and its familiarity of mobile based transactions

Product PlatformFinancial Services for the financially excluded

Individuals to use for transfers, deposits, bill payments, savings

Agent / franchisees to expand businessg p

Government to formalize informal transactions currently outside the banking industry

Safe, more convenient, more accessible

Platform builds on secure regulatory

Promise

more accessible g yframework, trustable banking and extensive low cost distributionProducts are going to

benefit, individuals, small b i t d businesses, partners and

government

“MAJOR STEPS TOWARDS REDUCING FINANCIAL EXCLUSION”

Branchless Banking: Focus on an Individual’s Needs

How does this man …

1 Pay Bills1. Pay Bills

a) Transfer money

b) Domestically

c) Internationally from familyc) Internationally from family

2. Repay Loans?

a) Save?

Market Potential

1. 30 millions bills per month

a) Transfer moneya) Transfer money

b) Domestically - $7bn per year

c) Internationally - $9bn per year

2 Save – Only 12% population has access

“ONLY 13% of PAKISTANIS HAVE ACCESS TO FINANCIAL SERVICES”

2. Save – Only 12% population has access to formal financial services

Easypaisa: An Implementation View“Example”

Products, Marketing & Awareness

Customer Acquisition &

Mgt.

Distribution & Agent

NetworkTechnology & Infrastructure

Treasury Float mgt. & compliance

TelenorPakistan

Product design

Pricing

Branding and campaigns

Customer and financial transaction systems

Distribution management

Physical distribution

Call center

Tameer

p g

Customer Branch distribution

Customer and Revenue Accounting, Treasury Float Endorsed Brand

Transaction switching

registration & Banking Operations

Stakeholder/ Merchant contracts

Cash handling Liquidity management

Risk Management

Regulatory approval &

Compliance

Product Approvals

Pricing Approvals

Billing Aggregation

Banking pPricing Approvals Banking Technology

JointGovernance: CEOs sponsored steering committee

“LEVERAGE EACH PARTNERS STRENGHT”

Core Proposition

“CHANGING THE ECO SYSTEM”

Core Proposition

• Majority of un-banked are not Initially seeking ▫ Bank account accessible via a mobile phone▫ Bank account accessible via a mobile phone

• Instead, they want something better than cash. • They want to pay people, or transfer funds,

With t h i t b h i ll t l di t▫ Without having to be physically travel distances▫ Instantly▫ Safely and with confirmation

I iti ll t f ti l b ki ill b t ti i• Initially transformational banking will be a transaction processing opportunity – it will develop into deposit taking opportunity as well as providing financial safety net.D l t f it f b th b ki d fi i l i t t• Development of suite of both banking and non-financial services to meet the aspirations of the general public

“MOVE BEYOND PAYMENTS TO PROVIDE TRUSTED, SECURE, LOW COST FINANCIAL SERVICES TO THE GENERAL POPULATION”

Value Proposition

Reliability• My money is safe• Responsive & proactive retailer• It’s worth paying for: The benefits BB provides are perceived

higher than price paid• Post-transaction Customer ServicesPost transaction Customer Services• Money is placed in SBP regulated Bank

Convenience• Service is always available (geographically & around the clock)• Easy to use – intuitive, user friendly• Anyone can use it• Makes life easy

Empowerment • Power in my hands• People say that user of this brand is very smart

“LOW BARRIERS TO ENTRY”

Branchless Banking: Potential Product Range

Suite of financial services being offered:

Mobile accounts (M-wallet)–Payments (bills person)Payments (bills, person)–Cash deposits–Cash withdrawals–ATM Cards (Future)–Funds Transfers (Inter-bank, a/c to a/c)

Inter bank Funds Transfer (Future)

Money transfers–Over the Counter

–CNIC to CNIC–M-wallet to CNICCNIC to M Wallet–CNIC to M-Wallet

Utility Bill Payments–Over the Counter

International remittance

–Cash to counter–Cash to m-wallet–Cash to other banks

M-commerce (Future)–Retail Purchase and settlement– Government Payment– Platform for Microfinance Industry for loan disbursement & Collection

“UNLIMITED APPLICATIONS”

Branchless Banking: Distribution

Building an agent network

1. It is important that we take the right retailers onboard

2 R t il ill b l i t it l l i i i th t2. Retailers will be playing a most vital role in servicing the customer

3. Retailers can be selected from existing ones or it can be a new retailer who fulfills our business requirementsretailer who fulfills our business requirements

4. Giving preference to good e-load retailers will be helpful as they are already tuned with the electronic transactions businessare already tuned with the electronic transactions business

RETAILER NETWORK IS THE KEY TO SUCCESS”

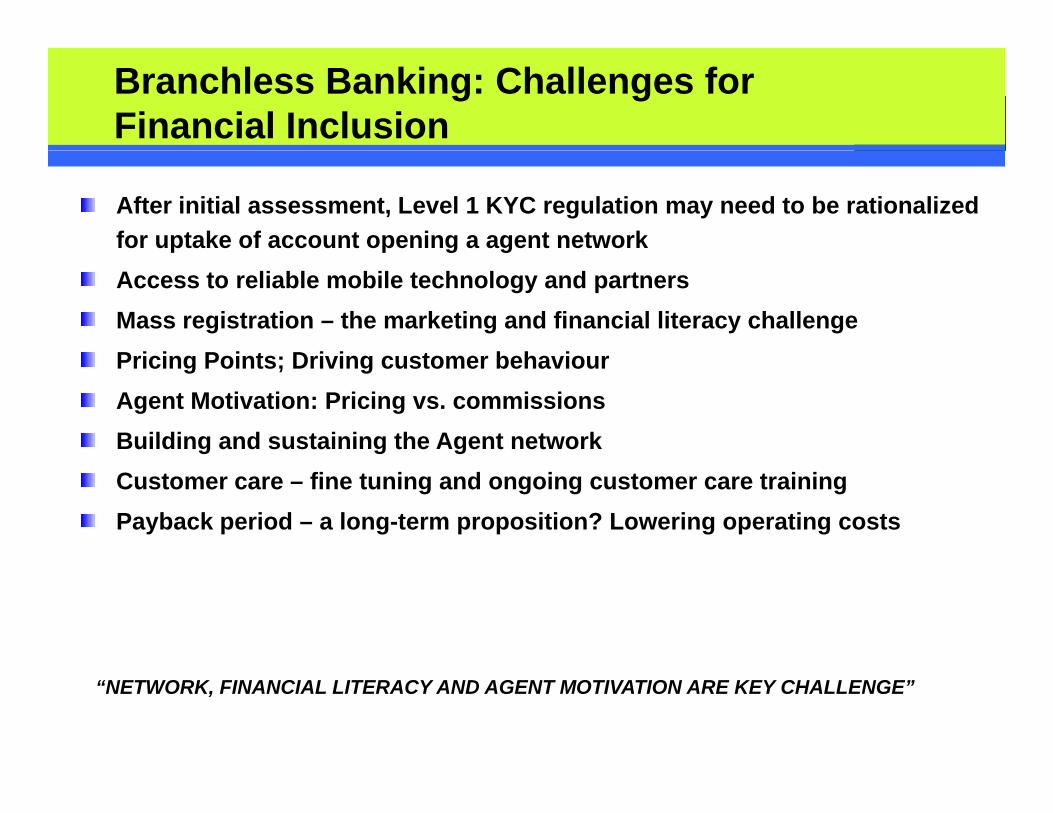

Branchless Banking: Challenges for Financial Inclusion

After initial assessment, Level 1 KYC regulation may need to be rationalized for uptake of account opening a agent networkg gAccess to reliable mobile technology and partnersMass registration – the marketing and financial literacy challengeP i i P i t D i i t b h iPricing Points; Driving customer behaviourAgent Motivation: Pricing vs. commissionsBuilding and sustaining the Agent networkCustomer care – fine tuning and ongoing customer care trainingPayback period – a long-term proposition? Lowering operating costs

“NETWORK, FINANCIAL LITERACY AND AGENT MOTIVATION ARE KEY CHALLENGE”

Conclusion

Large market for people who are un-banked but have a mobile phone Generally only 12% of Pakistani adults have any form of bank or MFI accountTypically 500% + more phone owners than the banked populationTypically 500% + more phone owners than the banked population

In Pakistan this equates to 60M to 70M individuals who could benefit from such servicesThe mobile phone is the branchless banking opportunity of the next decade

EnablersBuilding and training the Agent networkBuilding and training the Agent network

Human ATMs and Payment PointTrusted service branding and marketing is keyCentral Bank regulation to encourage and promote micro-account adoption (Registration and throughput barriers)

Adoption Challenges to address for sustainabilityCultural Barriers; agent network vs technology vs brand affinityCustomers still apathetic about mobile banking; Development of effective customer communication displaying consumer protection St k h ld th t t t d i th bil h l ill h t t k l t i th t h iStakeholders that want to succeed in the mobile channel will have to take a long-term view – that means having significant patience and management support to endure several more years of single-digit growth in this emerging channel

“DESPITE IS NASCENT STAGE BRANCHLESS BANKING ON THE RIGHT TRACKDESPITE IS NASCENT STAGE BRANCHLESS BANKING ON THE RIGHT TRACKAND WILL CHANGE THE NATURE OF THE BANKING INDUSTRY IN PAKISTAN”

Sources: Finscope Study on Access to Finance in Pakistan; 2008 and Pakistan Telecommunications Authority (PTA)