borrowing. cash vs credit cash : adv: cheapest option can avail of discounts disadvnot always...

TRANSCRIPT

Borrowing

Cash Vs CreditCash: Adv: Cheapest option Can avail of discounts Disadv Not always available/emergency Affects cashflow if pay upfront

Credit: Adv: buy now/own goods Pay later/staged payments/better cashflow Disadv: cost of borrowing/interest Flat Rate APR

Purchasing on CREDIT Credit Purchase Buy now/pay later = ESB, Phone Credit Card Deferred Payment

Borrowing Considerations Do I need the goods Can I wait and save Can I afford to borrow Are there alternatives

Borrower must be Credit worthy = able to repay the loan Have ability to repay Have a track record Have collateral = security for the loan

eg deeds of a house for a mortgage

Where can I borrow from Bank Building Society Credit union Moneylenders

Banks/Building Society Short/Medium/Long Term Loans Mortgage Overdraft of Current A/C Credit Card

Credit Union Short-Medium term Loans

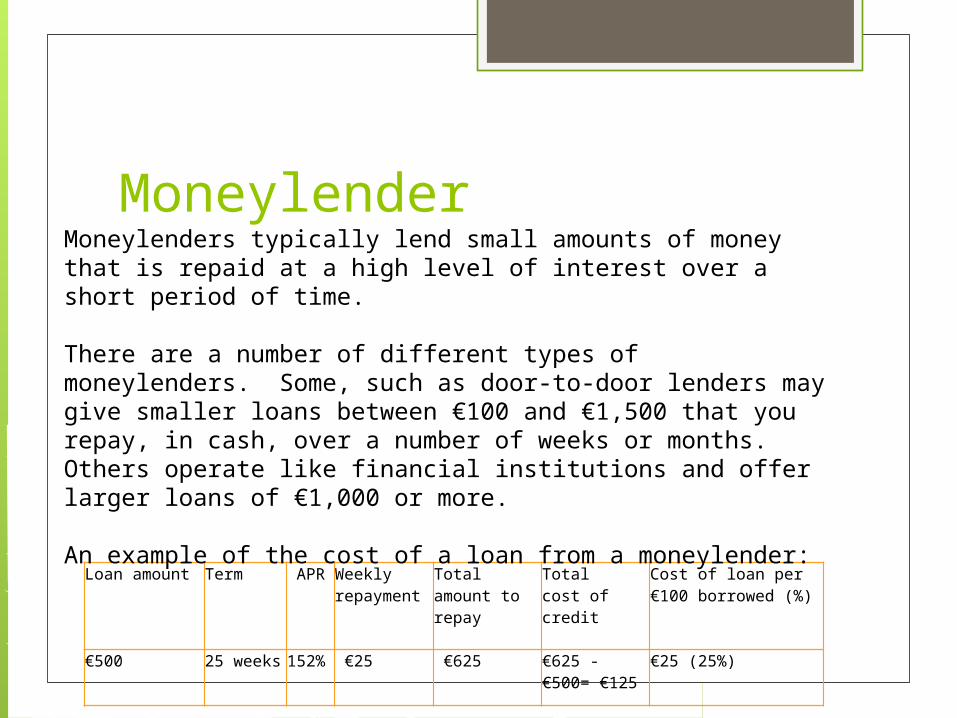

Moneylender

Loan amount Term APR Weekly repayment

Total amount to repay

Total cost of credit

Cost of loan per €100 borrowed (%)

€500 25 weeks 152% €25 €625 €625 - €500= €125

€25 (25%)

Moneylenders typically lend small amounts of money that is repaid at a high level of interest over a short period of time.

There are a number of different types of moneylenders. Some, such as door-to-door lenders may give smaller loans between €100 and €1,500 that you repay, in cash, over a number of weeks or months. Others operate like financial institutions and offer larger loans of €1,000 or more.

An example of the cost of a loan from a moneylender:

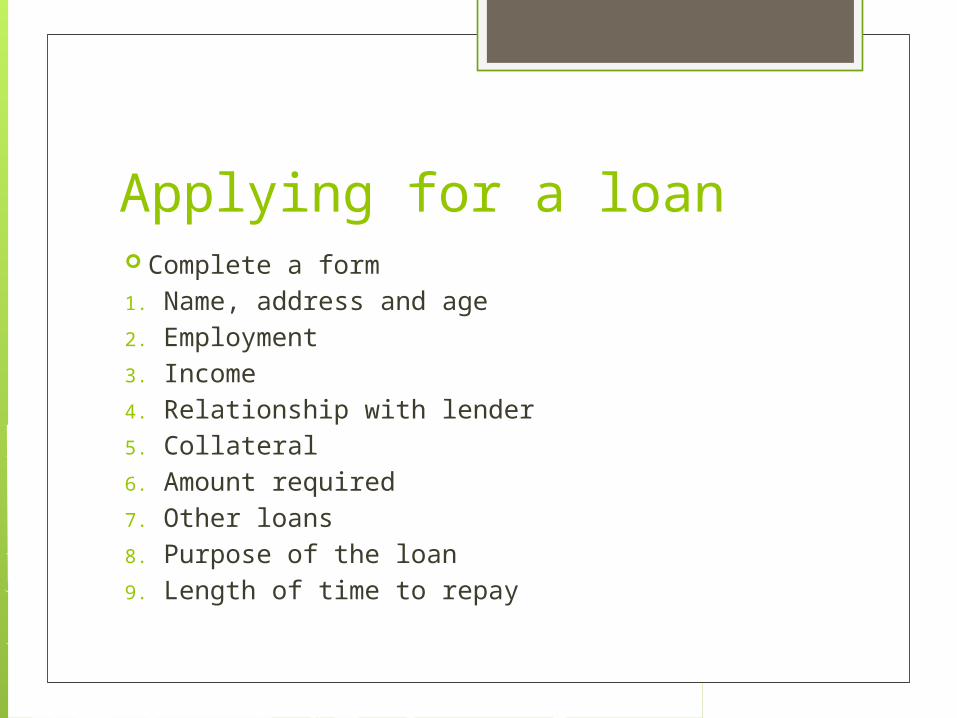

Applying for a loan Complete a form1. Name, address and age2. Employment3. Income4. Relationship with lender5. Collateral6. Amount required7. Other loans8. Purpose of the loan9. Length of time to repay

Renting Leasing Use of goods but never own them Not responsible for repairs No asset depreciation

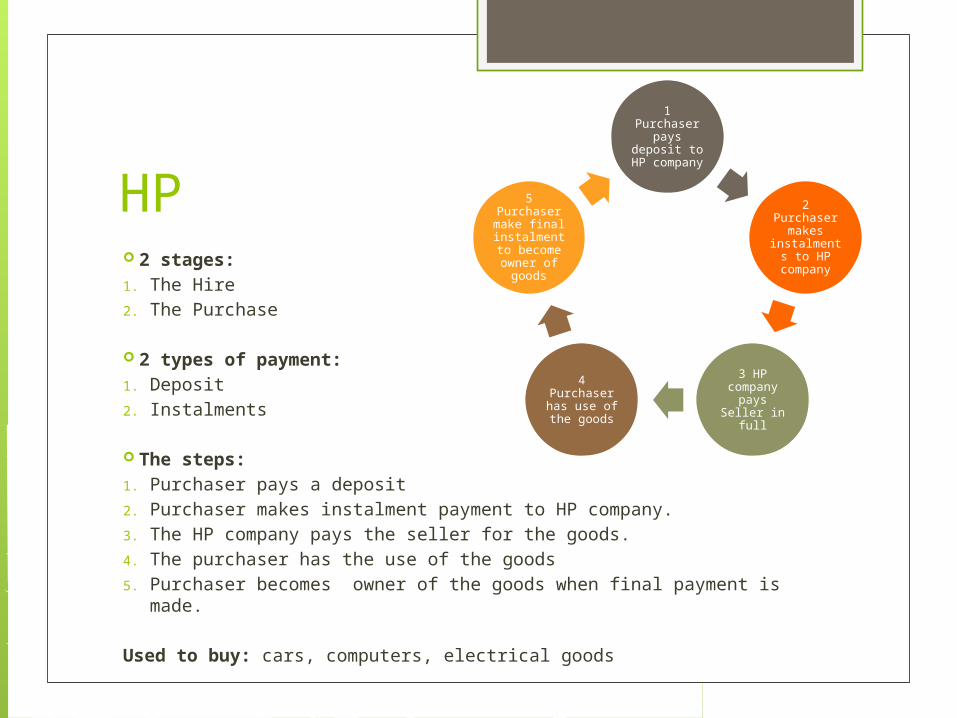

HP 2 stages:1. The Hire2. The Purchase

2 types of payment:1. Deposit2. Instalments

The steps:1. Purchaser pays a deposit 2. Purchaser makes instalment payment to HP company.3. The HP company pays the seller for the goods.4. The purchaser has the use of the goods 5. Purchaser becomes owner of the goods when final payment is

made.

Used to buy: cars, computers, electrical goods

1 Purchaser pays deposit

to HP company

2 Purchaser makes

instalments to HP

company

3 HP company

pays Seller in full

4 Purchaser has use of the goods

5 Purchaser make final instalment to become owner of

goods

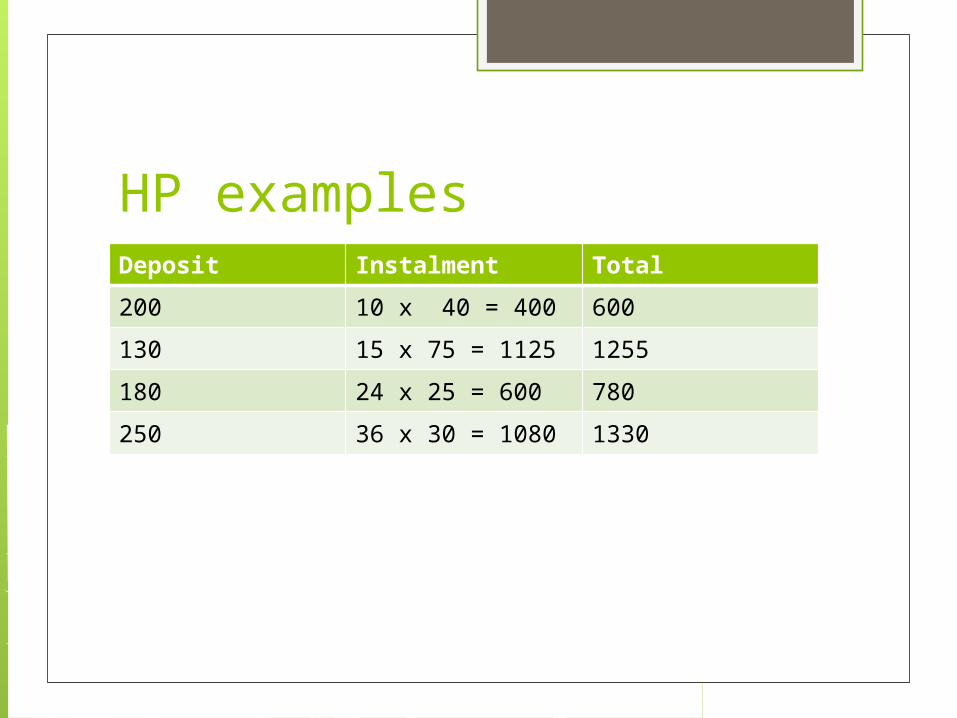

HP examplesDeposit Instalment Total

200 10 x 40 = 400 600

130 15 x 75 = 1125 1255

180 24 x 25 = 600 780

250 36 x 30 = 1080 1330

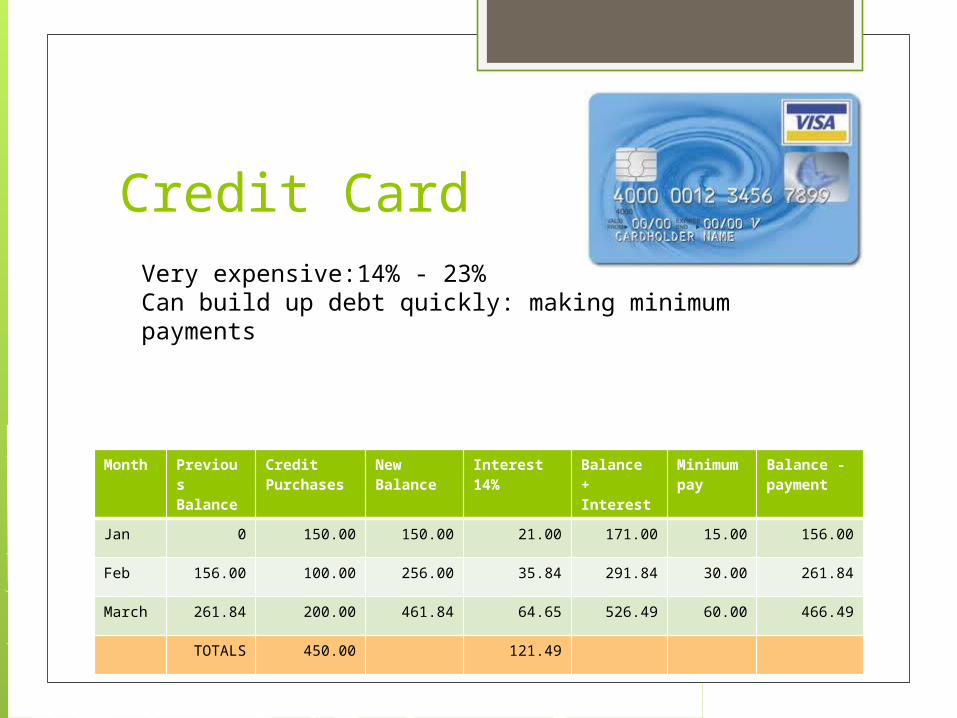

Credit Card

Month Previous Balance

Credit Purchases

New Balance

Interest 14%

Balance + Interest

Minimum pay

Balance - payment

Jan 0 150.00 150.00 21.00 171.00 15.00 156.00

Feb 156.00 100.00 256.00 35.84 291.84 30.00 261.84

March 261.84 200.00 461.84 64.65 526.49 60.00 466.49

TOTALS 450.00 121.49

Very expensive:14% - 23%Can build up debt quickly: making minimum payments

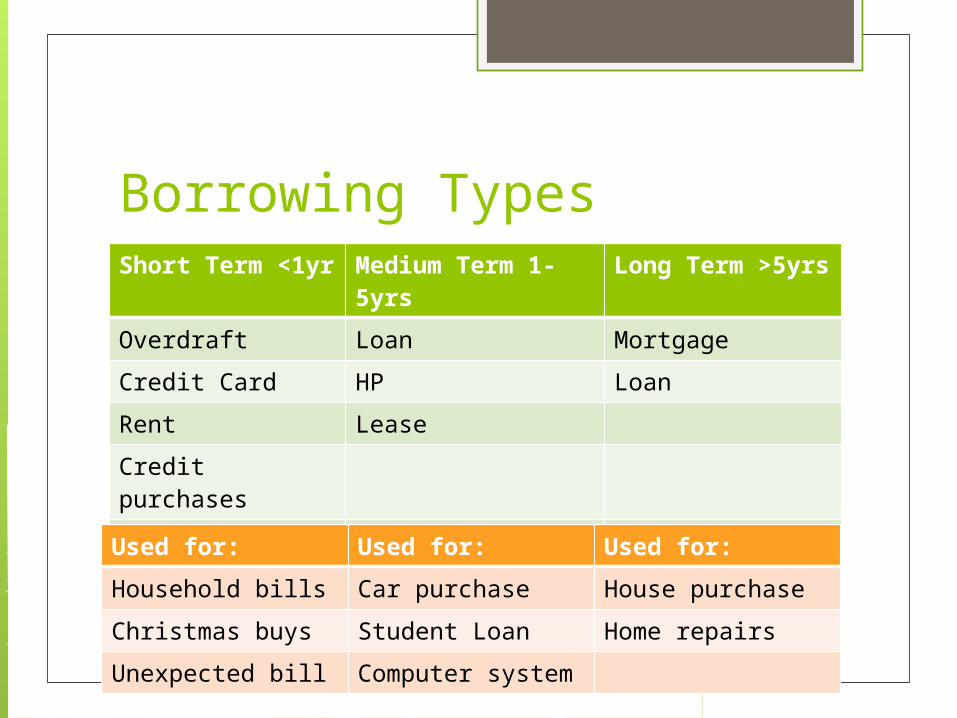

Borrowing TypesShort Term <1yr

Medium Term 1-5yrs

Long Term >5yrs

Overdraft Loan Mortgage

Credit Card HP Loan

Rent Lease

Credit purchases

Deferred paymentUsed for: Used for: Used for:

Household bills Car purchase House purchase

Christmas buys Student Loan Home repairs

Unexpected bill Computer system

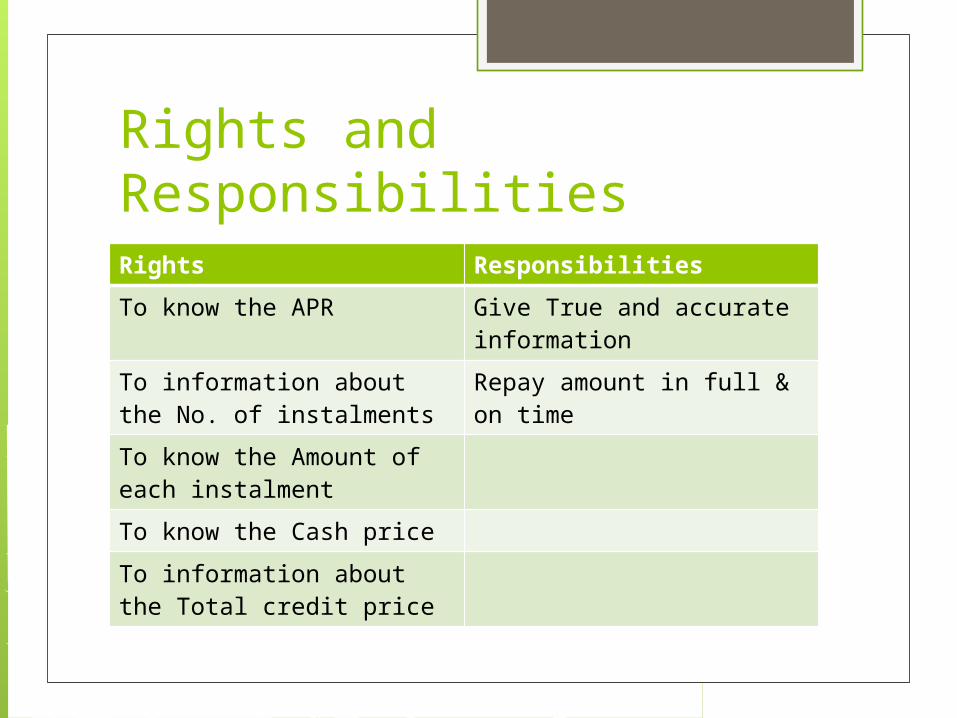

Rights and ResponsibilitiesRights Responsibilities

To know the APR Give True and accurate information

To information about the No. of instalments

Repay amount in full & on time

To know the Amount of each instalment

To know the Cash price

To information about the Total credit price

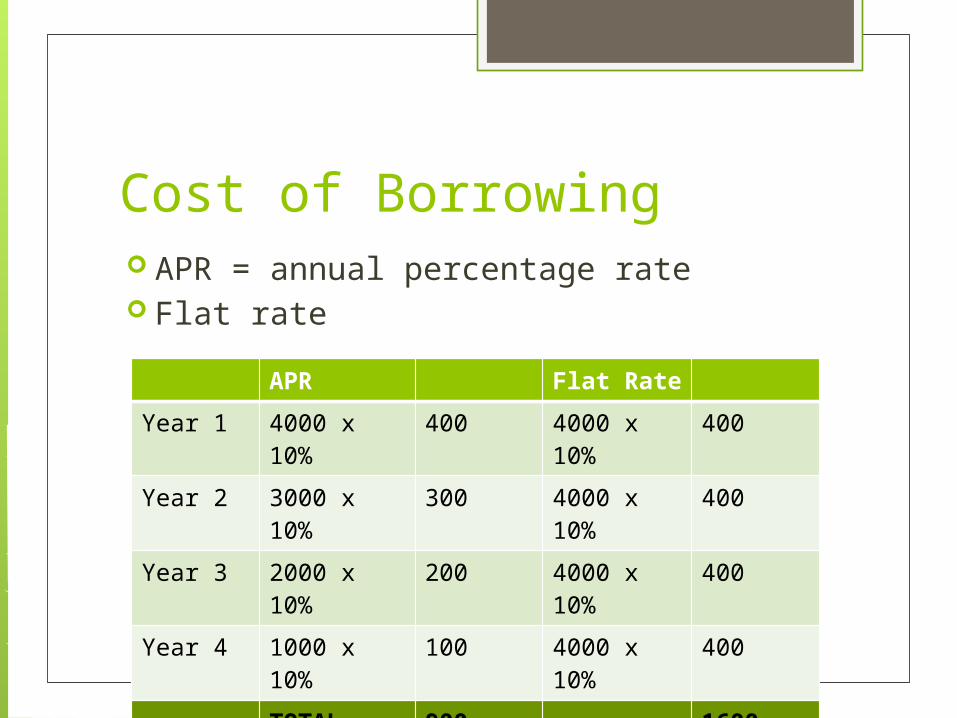

Cost of Borrowing APR = annual percentage rate Flat rate

APR Flat Rate

Year 1 4000 x 10%

400 4000 x 10%

400

Year 2 3000 x 10%

300 4000 x 10%

400

Year 3 2000 x 10%

200 4000 x 10%

400

Year 4 1000 x 10%

100 4000 x 10%

400

TOTAL 900 1600

Bankruptcy A debtor who does not pay the amount

owed can be declared bankrupt Through the courts

In the News

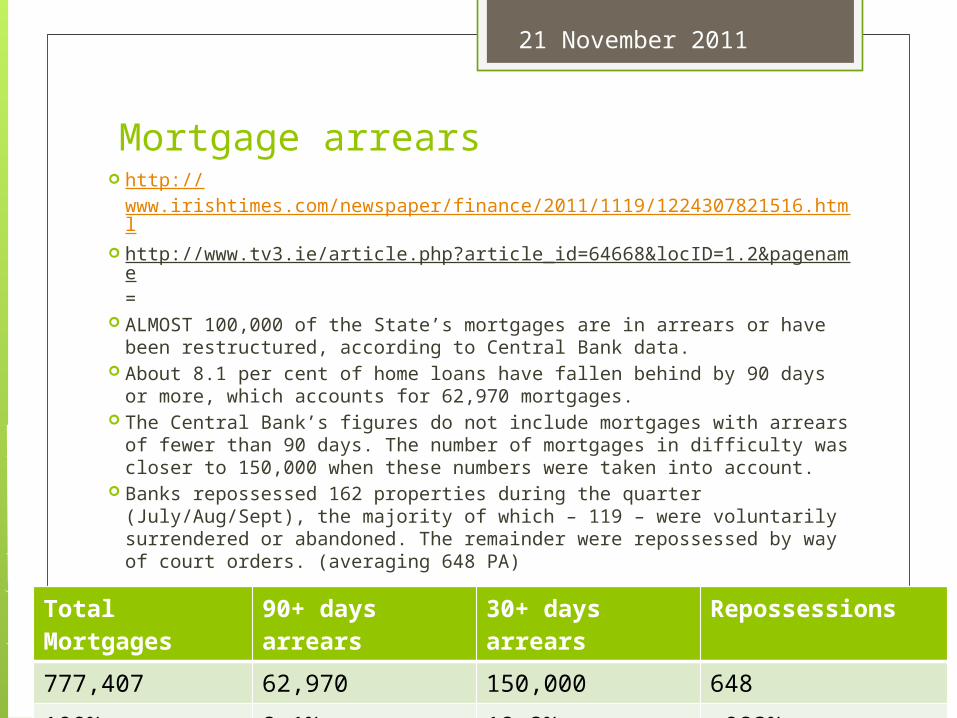

Mortgage arrears http://

www.irishtimes.com/newspaper/finance/2011/1119/1224307821516.html

http://www.tv3.ie/article.php?article_id=64668&locID=1.2&pagename=

ALMOST 100,000 of the State’s mortgages are in arrears or have been restructured, according to Central Bank data.

About 8.1 per cent of home loans have fallen behind by 90 days or more, which accounts for 62,970 mortgages.

The Central Bank’s figures do not include mortgages with arrears of fewer than 90 days. The number of mortgages in difficulty was closer to 150,000 when these numbers were taken into account.

Banks repossessed 162 properties during the quarter (July/Aug/Sept), the majority of which – 119 – were voluntarily surrendered or abandoned. The remainder were repossessed by way of court orders. (averaging 648 PA)

Total Mortgages

90+ days arrears

30+ days arrears

Repossessions

777,407 62,970 150,000 648

100% 8.1% 19.2% .083%

21 November 2011

Debt Warninghttp://www.irishtimes.com/newspaper/breaking/2011/1121/breaking22.html It can take some people more than seven months to pay off debt accumulated in the run-up to

Christmas, according to a survey by the Irish League of Credit Unions (ILCU). Despite the current economic climate, the survey showed Irish adults expected to spend on

average of €562 each this Christmas. The survey indicated this level of spending would leave 38 per cent of people in debt. With less than five weeks to Christmas, the ILCU today urged the public to avoid borrowing beyond

their means. “We have seen the impact of some of the toughest financial challenges play out in 2011. Worries

over how to finance Christmas is not far from people’s minds,” ILCU chief executive Kieron Brennan said.

He also warned people not to be tempted into using moneylenders, due to the extremely high rate of interest charged and also to watch out for credit card debt, as a high rate of interest will be charged to balances that are not cleared on time every month.

The ILCU’s survey found 77 per cent of respondents did not feel any better about their financial situation than they did last Christmas.

It also showed that 55 per cent of respondents said they intended to use general savings or cash to pay for Christmas, with 28 per cent using specific savings set aside for Christmas.

Some 9 per cent will use their credit card with smaller numbers availing of credit union loans and money lenders.

In terms of the recovering from over spending during the festive season, 34 per cent fo respondents stated that it will take up to three months to recover, 12 per cent suggested it would take four months or more and a small proportion of respondents say it will take over 7 months to recover financially from Christmas 2011.

The survey also showed that women would take longer than men to recover from Christmas debt

Sourcing the cheapest Credit Card

http://www.irishtimes.com/newspaper/pricewatch/2011/1121/1224307903491.html?via=rel Comparing credit card rates can be an exercise in frustration. Providers that offer the most

attractive introductory rates on balance transfers are generally not top of the list when it comes to the rate on purchases and the amount charged on cash withdrawals is different again.

According to the National Consumer Agency’s www.itsyourmoney.ie website, the best value in the credit card market at present on purchases is 13.6 per cent APR from AIB on its Click card.

The catch is that Click is available only to customers of AIB’s online banking service. The disparity in charges is well-illustrated by the fact that, of the cards compared by the NCA

site, AIB also offers the worst value – 22.7 per cent APR on its be MasterCard. In terms of cash withdrawals – never a good idea on credit cards – the best you will get at the

moment is 9.75 per cent from National Irish Bank on its MasterCard Platinum. At the other end of the scale, expect to pay an onerous 21.36 per cent on Bank of Ireland’s Clear and Classic cards.

Bear in mind that companies usually charge interest on purchases only from the date that payment is due on your monthly bill – if you pay your credit card bill in full and on time each month, no interest will arise. However, companies generally charge interest on cash withdrawals from the moment the money is drawn down.

Given the interest that can accrue, clearly paying off cards in full every month is the best option. For those unable to do so, a number of providers offer interest-free periods on transferred

balances which can significantly reduce the build-up of interest, if managed very carefully. These include MBNA and OneDirect (10 months) and Permanent TSB Visa and Tesco (six months).

The other option is for people to borrow elsewhere (such as credit unions charging lower interest rates) to clear credit card debt but this works only if you subsequently exercise financial discipline.

Bankruptcy http://

www.bbc.co.uk/news/uk-northern-ireland-15694182

Fermanagh businessman Sean Quinn - once believed to have been the richest man on the island of Ireland - has been declared bankrupt.

He was granted a voluntary adjudication over an alleged 2.8bn euros (£2.4bn) debt owed to Anglo Irish Bank