borgwarner, inc. (nyse:bwa) - the turnaround letter · borgwarner, inc. august 2016 borgwarner,...

TRANSCRIPT

August 2016

Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

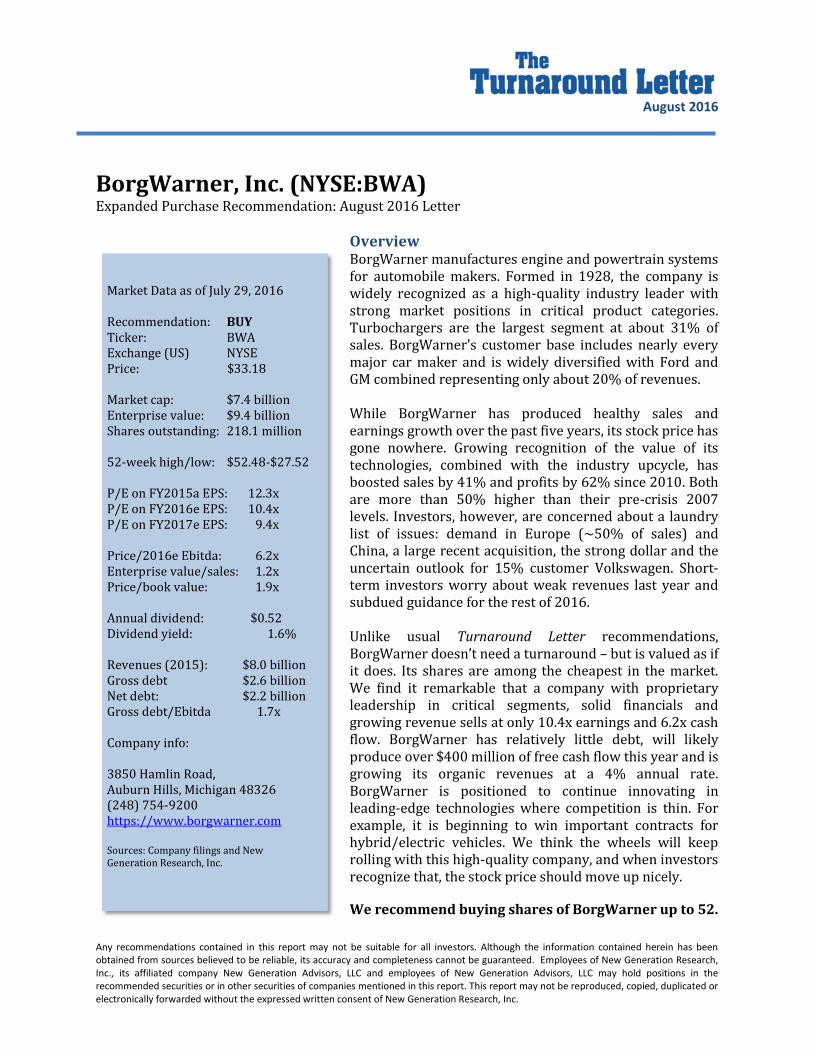

BorgWarner, Inc. (NYSE:BWA) Expanded Purchase Recommendation: August 2016 Letter

Overview BorgWarner manufactures engine and powertrain systems for automobile makers. Formed in 1928, the company is widely recognized as a high-quality industry leader with strong market positions in critical product categories. Turbochargers are the largest segment at about 31% of sales. BorgWarner’s customer base includes nearly every major car maker and is widely diversified with Ford and GM combined representing only about 20% of revenues. While BorgWarner has produced healthy sales and earnings growth over the past five years, its stock price has gone nowhere. Growing recognition of the value of its technologies, combined with the industry upcycle, has boosted sales by 41% and profits by 62% since 2010. Both are more than 50% higher than their pre-crisis 2007 levels. Investors, however, are concerned about a laundry list of issues: demand in Europe (~50% of sales) and China, a large recent acquisition, the strong dollar and the uncertain outlook for 15% customer Volkswagen. Short-term investors worry about weak revenues last year and subdued guidance for the rest of 2016. Unlike usual Turnaround Letter recommendations, BorgWarner doesn’t need a turnaround – but is valued as if it does. Its shares are among the cheapest in the market. We find it remarkable that a company with proprietary leadership in critical segments, solid financials and growing revenue sells at only 10.4x earnings and 6.2x cash flow. BorgWarner has relatively little debt, will likely produce over $400 million of free cash flow this year and is growing its organic revenues at a 4% annual rate. BorgWarner is positioned to continue innovating in leading-edge technologies where competition is thin. For example, it is beginning to win important contracts for hybrid/electric vehicles. We think the wheels will keep rolling with this high-quality company, and when investors recognize that, the stock price should move up nicely.

We recommend buying shares of BorgWarner up to 52.

Market Data as of July 29, 2016 Recommendation: BUY Ticker: BWA Exchange (US) NYSE Price: $33.18 Market cap: $7.4 billion Enterprise value: $9.4 billion Shares outstanding: 218.1 million 52-week high/low: $52.48-$27.52 P/E on FY2015a EPS: 12.3x P/E on FY2016e EPS: 10.4x P/E on FY2017e EPS: 9.4x Price/2016e Ebitda: 6.2x Enterprise value/sales: 1.2x Price/book value: 1.9x Annual dividend: $0.52 Dividend yield: 1.6% Revenues (2015): $8.0 billion Gross debt $2.6 billion Net debt: $2.2 billion Gross debt/Ebitda 1.7x Company info: 3850 Hamlin Road, Auburn Hills, Michigan 48326 (248) 754-9200 https://www.borgwarner.com Sources: Company filings and New Generation Research, Inc.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 2 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

TURNAROUND CHALLENGE/OPPORTUNITY Coming out of the 2009 recession, BorgWarner’s impressive product array and management produced strong performance, with an assist from the upturn in the auto cycle. Since 2010, the first full year after the recession, revenue, margins and earnings expanded strongly:

2010 2015 Change Revenues 5,652 8,023 +42% Operating profit 504 940 +87% Margin 8.9% 11.7% +1.1 percentage points Ebitda 778 1,362 +75% Margin 13.7% 17.0% +3.3 percentage points EPS (diluted)* $1.51 $2.70 +79% Share price ** $36.18 $33.18 -8%

* Adjusted for 2:1 split in December, 2013. ** Price for 2010 is December 31, 2010, split-adjusted. Price for 2015 price is current price.

By mid-2014, BorgWarner’s impressive execution turned the company into a Wall Street darling. Investors viewed the company as a growth story, lifting its P/E multiple to over 20x consensus 2014 earnings. When it reported strong 2Q14 earnings, well ahead of consensus expectations, many brokerage firms raised their price targets to the upper-$70/share range (the stock was near $68 and at an all-time high), and projected strong continued growth in future earnings. Catching the downside of the Wall Street expectations game The 2Q14 earnings release, however, marked the peak of BorgWarner’s operating momentum. Over the next two quarters, results subsequently fell short of consensus revenue estimates and barely matched earnings estimates. BorgWarner’s shares fell 25% by January 2015 as investors digested the weaker-than-hoped-for results. At the January 2015 Detroit Auto Show, management provided their preliminary 2015 outlook which included healthy revenue growth (excluding a negative currency effect) and 13%+ operating margins, along with a $1.0 billion share buyback. Despite guidance for less-than-expected earnings per share growth, investors drove the shares up nearly 30% to the low $60s by March 2015. Investors remained too optimistic despite management’s continued comments about numerous headwinds on the next two quarterly earnings conference calls. In July 2015, when results badly missed 2Q15 consensus revenue and earnings estimates and management cut their guidance for the rest of the year, investors fled. BorgWarner’s shares fell 33% by October to below $40. The stock market’s decline in early 2016 on recession fears pushed BorgWarner shares to below $30.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 3 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

BorgWarner had completed the cycle: from “unwanted cyclical” going into the 2009 recession, to “Wall Street darling” in 2014, back to “unwanted cyclical” by early 2016. Nearly all the decline in the share price since mid-2014 was driven by the company falling short of Wall Street expectations. Changes in underlying fundamentals were much more muted. Currently, the market worries about a variety of additional macro concerns, ranging from a recession in Europe, a sharp slowdown in U.S. light vehicle demand, slowing demand in China, the recent acquisition of Remy, ongoing dollar strength, and the uncertain outlook for 15% customer Volkswagen. The opportunity BorgWarner’s shares currently trade at an attractive valuation, as if the company is struggling and needs a turnaround. However, fundamentally it is healthy and is likely to continue its revenue and earnings growth, maintain its strong balance sheet and generate impressive free cash flow. Leadership is capable and well-suited to continue the company’s solid execution. Rather than relying on a turnaround in its fundamentals to drive the stock price higher, the company needs only to continue executing on its plans. While we appreciate investors’ concerns, the stock price already discounts much of the effect these events would likely have on BorgWarner’s fundamentals and provides a margin for safety that most other cyclical stocks lack. REVENUE PROSPECTS LOOK HEALTHY We believe BorgWarner’s revenues can continue growing at a 3-6% rate over time, assuming no sharp decline in the overall demand for light vehicles. Thoughts on the auto cycle In the U.S., sales of light vehicles are steady at record levels of 17-18 million units. Many investors believe this is a peak level, to be followed by an inevitable fall-off in demand to much lower levels. We are not convinced that this forecast is a certainty. We take the view that there is a reasonable likelihood that sales remain around the current levels. Outside the U.S., light vehicle demand growth has been tepid recently – we anticipate roughly stable volumes over the next few years. Along with the automobile cycle, the BorgWarner’s sales are driven by an unrelenting secular tailwind: increasingly stringent fuel efficiency standards. The U.S. Environmental Protection Agency (EPA) mandates a stringent 54.5 miles per gallon standard by 2025 and institutes new emissions limitations. Regardless of whether these tighter requirements remain intact, the direction is clear – better mileage, fewer emissions. The trend around the world, including in emerging nations, is similarly toward better mileage and fewer emissions. Most of BorgWarner’s products help cars maintain their performance while meaningfully improving their mileage and/or reducing their emissions.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 4 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

Two of the more significant revenue drivers include on-going growth in turbochargers and the emergence of hybrid/electric vehicles. Turbochargers Turbochargers are a critical source of revenue and earnings growth for BorgWarner, at 31% of total net revenues. The global market for turbochargers is projected to grow at an estimated 10.2% rate over the next five years as turbos are increasingly being included on gasoline engines. The technology of turbochargers has advanced well beyond simple mechanics – they are increasingly integrated with the entire powertrain to increase dynamic responses and power while providing better fuel efficiency. Many of the company’s turbochargers improve fuel economy by 15%. In 2015, the company’s estimated market share of the $13.6 billion on-highway turbocharger market was about 18%. BorgWarner’s capabilities appear well-positioned to fully participate in the category’s growth. Electric vehicles (“EVs”) The growth of hybrid and electric-powered vehicles offers BorgWarner new opportunities for growth. While it also represents a risk, as the company currently is heavily reliant on gas and diesel engines, we view the transition to hybrid/electric engines as likely but slow-moving. In 2015, an estimated 380,000 hybrid/electric cars were sold in the United States (about 1.8% market share), down from nearly 500,000 in 2013. BorgWarner has taken a pro-active approach to expanding its product line to directly capture new hybrid/EV component sales. The effort is making some traction - BorgWarner recently won a contract to provide transmissions to Chinese car producer Geely’s first mass-market electric vehicle. Also, the company disclosed that it has won several other electric vehicle contracts, with more specifics to be announced over the remainder of the year. BorgWarner’s commitment was reinforced when it made its largest acquisition ever, buying Remy International, for $1.2 billion in November, 2015. Remy is a leader in automobile electrical technology. BorgWarner will expand distribution of Remy’s domestic product array to customers around the world, and will increasingly integrate Remy electric technology with clutch and other products for both conventional and electric vehicles. While there is a risk that other traditional competitors could accelerate their hybrid component technology ahead of BorgWarner, or that a company outside the auto industry adapts new and better technologies to autos, we think BorgWarner is being aggressive enough with its development to maintain its strong market position. It is possible that EVs create not only a new longer-term source of unit and market share growth, but that the content per vehicle could be considerably higher. A competitor, German-based Continental, has said that the powertrain content in an EV is 3x that of a gasoline or diesel engine.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 5 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

MANAGEMENT’S REVENUE AND EARNINGS GUIDANCE BorgWarner’s annual and long-term guidance, as of their July 28, 2016 earnings release, look very reasonable:

Net sales growth in 2016 of approximately 13.7% - 17.5% Net sales growth in 2016 excluding currency and Remy acquisition of 3.0-5.5% Operating income above 12% of net sales Operating income excluding effect of Remy acquisition above 13% net sales Net earnings per diluted share for 2016 of $3.16 - $3.32 Long-term “organic” sales growth rate of 4%-6% through 2018 Reaching $15 billion in revenues by 2020.

We like management teams to provide annual revenue and earning guidance. While the guidance sets tangible markers for measuring results, perhaps more importantly it reveals management’s priorities in their selection of which numbers are important. BorgWarner also provides quarterly guidance. We are less-enthused with this as it encourages management to shift revenues and costs, including those that may disrupt some of the business.

VALUATION The shares’ current valuation is attractive at 10.4x consensus 2016 earnings per share estimate of $3.18. This multiple is a slight discount to its peer[1] average of 10.7x. BorgWarner’s five-year average multiple is 11.4x and reached as high as 20.3x at its 2014 peak. On an EV/Ebitda basis, the stock’s 6.2x multiple on 2016 Ebitda is attractive. It is at a 9% discount to its peer group[1] average multiple of 6.8x. Its five-year average multiple is 7.6x and reached 10.1x at its 2014 peak. BorgWarner’s valuation is roughly in-line with its peers despite its higher margins (about 2 percentage points) and similarly healthy growth prospects. [1] Peer group includes other auto/truck suppliers: American Axle & Manufacturing (AXL), Allison Transmission (ALSN), Delphi Automotive (DLPH), Johnson Controls (JCI), Lear Corporation (LEA), Tenneco (TEN) and Visteon (VC).

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 6 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

We are applying our standard end-of-turnaround valuation methodology to BorgWarner, even though it doesn’t need a turnaround. Our estimates of the primary drivers (revenues, Ebitda margin, net cash position) and Ebitda multiple in the endgame scenario are outlined below: 2015 Actual 2019 Estimated (millions) (millions)

Revenues $8,023 $10,000 Ebitda margin 17.0% 17.0% Ebitda $1,700 Ebitda multiple 7.0x Enterprise value 11,900 + Cash balance 578 + Incremental cash flow 1,400 - Gross debt 2,550

Equity value 11,328 Shares outstanding 218.1 million Price target $51.94/share Upside to target +56%

Assumptions:

1. Revenues – we are assuming that the company meets its 2016 guidance, including the $1.2 billion in Remy revenues. Our estimate assumes overall revenues grow at a 3.0% rate for the subsequent three-year period through 2019. This assumes a combination of organic growth and an approximately flat U.S. auto cycle, a mild recovery elsewhere (Asia, Japan), and no sharp downturn in Europe or further downturn in Latin America. Our $10.0 billion revenue assumption is substantially more conservative than the company’s stated goal of reaching $15 billion in sales by 2020.

2. Ebitda and Ebitda margin – we estimate flat margins compared to 2015 levels as competitive pressures are offset by the growth and higher-margin new business initiatives. BorgWarner recently reduced its incremental operating margin guidance to 15-17% for this year. We see the company ultimately hovering at or near the high end of this range over time.

3. Ebitda multiple – at 7.0x, our estimated end-scenario multiple is modestly higher than the

current 6.2x multiple and is conservative if our operating estimates are reasonably accurate. This multiple is below the 7.5x mid-point of its five-year historical range of 4.6x to 10.4x.

4. Cash balance and incremental cash flow – we are assuming, on average, approximately $350

million a year of incremental cash (net of dividends) accumulates on the balance sheet.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 7 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

From an end-of-turnaround valuation perspective, we are indifferent to whether this cash stays on the balance sheet or is used to pay down debt. Some incremental value may be created from share repurchases or acquisitions.

5. Gross debt – we are assuming this remains unchanged for modeling purposes, but recognize that BorgWarner could use part of its growing cash balances to repay some of this debt or make acquisitions. The effect would be the same: net debt (debt less cash) would decline considerably.

6. Shares outstanding – for modeling purposes we are assuming the share count remains

unchanged, although BorgWarner stated they expect to repurchase $200 million to $300 million in shares in the second half of this year and could expand their current $1.0 billion repurchase authorization.

Sources of value creation Compared to the current $33.18 share price, the increase to the $51.96 target price represents $18.78/share of value creation. Just over half of this increase (+$10.41) is derived from the increase in revenues. Most of the balance is produced by the accumulation of annual cash flows from operations. We view this type of story (that relies on sales growth) as moderately higher risk than a cash-accumulation story. However, our sales growth assumption is very conservative which greatly reduces the risk from this source of value creation. With cash flow accumulation (our preferred source) producing over a third of total value creation, the overall risk appears limited, barring a significant down-cycle in the industry. The remaining two sources, margin expansion and multiple expansion, contribute little as we assume essentially no change in these metrics.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 8 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

Sources of value creation:

A brief note on Ebitda We typically use the EV/Ebitda multiple to value most companies. Not only does it explicitly focus on the value of the operating company regardless of capital structure, but it also separately values unrelated assets and liabilities. The approach is widely used in private equity transactions which increasingly drive public equity valuations. An additional merit of EV/Ebitda is that it allows useful comparisons of similar companies even if they have different capital structures. In a straightforward business, the Enterprise Value (“EV”) is the value of the equity (market cap) plus any debt, less cash. It is the value of the operating business (the “enterprise”). If the company was acquired, the buyer would pay for the entire enterprise, not just the equity. Debts may be paid off immediately or carried over to the buyer, but one way or another the buyer would be obligated to cover them. We compare this enterprise value to the cash operating profits of the business (earnings before interest, taxes, depreciation and amortization, or “Ebitda”) to produce the EV/Ebitda multiple. The principal shortcoming of Ebitda is its exclusion of taxes and capital expenditures. These costs are accounted for subjectively in assigning the multiple – admittedly a form of art. Interest costs are also excluded, as they are financing costs not operating costs.

CURRENT TARGET Change in target price if only this metric changes vs CURRENT

2015A BASE CASE REVENUE MARGINS MULTIPLE CASH BUILD

Revenues 8,023 10,000 10,000 8,023 8,023 8,023

margin 17.0% 17.0% 17.0% 17.0% 17.0% 17.0%

EBITDA 1,361 1,700 1,696 1,364 1,361 1,361

multiple [1] 6.8 7.0 6.8 6.8 7.0 6.8

EV 9,205 11,900 11,474 9,225 9,527 9,205

Debt 2,550 2,550 2,550 2,550 2,550 2,550

Cash 578 1,978 578 578 578 1,978

Net debt 1,972 572 1,972 1,972 1,972 572

Equity 7,233 11,328 9,502 7,253 7,555 8,633

Shares 218 218 218 218 218 218

Target price $33.18 $51.96 $43.59 $33.27 $34.66 $39.60

Upside (downside) 0.0% 56.6% 31.4% 0.3% 4.4% 19.4% = 55%

Value Creation Mix 55% 0% 8% 34% = 98%

[1] Multiple based on 2015 Ebitda.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 9 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

COMPANY DESCRIPTION HISTORY In 1928, several component manufacturers combined to form BorgWarner Corporation. Two of these suppliers, Borg & Beck (makers of a sturdy and inexpensive clutch that was mass-produced throughout the young auto industry) and Warner Gear (developer of the original sliding clutch and the first manual transmission) formed the foundation. Over the next sixty years, a core characteristic of the company’s expansion is the introduction of industry-leading innovations – both internally-developed and by acquisition. The company appears to have little fear of going outside its walls to find new capabilities. This trait is a critical component of its culture and its future success. Some of the innovations that came from BorgWarner and its later-acquired companies include: 1907 Predecessor firm Warner Gear introduces the first manual car transmission 1930s Warner Gear introduces gear synchronizers that greatly eased gear shifting

Warner launches first self-contained overdrive transmission 1940 Warner Gear begins producing transfer cases for four-wheel and all-wheel drive vehicles 1950 BorgWarner introduces the Ford-O-Matic 3-speed automatic transmission, the torque

converter and a new form of clutch that became one of company’s biggest sellers 1952 Schwitzer, predecessor to BorgWarner Turbo Systems, introduces its turbocharger to the

Indianapolis 500 auto race 1956 The T10 four-speed high performance manual transmission is introduced in the Chevrolet

Corvette 1964 The NSK-Warner joint venture is formed to access the rapidly-growing Japanese market 1973 BorgWarner introduces full-time, four-wheel drive transfer cases using Hy-Vo drive chains 1984 BorgWarner launches “Torque-on-Demand” for transfer cases 1997 BorgWarner enters the turbocharger market with the partial acquisition (eventually

acquired remainder) in AG Kuhnle 2003 Launched DualTronic transmission technologies. In 1987, to fend off a large stake by raiders Irwin Jacobs and Samuel Heyman, BorgWarner took itself private in a $4.4 billion leveraged buyout, one of the largest of the 1980s. Following several divestitures, in 1993, Borg Warner Automotive was spun off from Borg-Warner Security Corporation as a publicly-traded independent company. On July 24, 2013 the company reinstated its quarterly dividend at $0.25, and doubled it to $0.51 in 2014. With the $.01 increase in 2015, the dividend currently is $0.52. Since 1936, BorgWarner has been closely involved with the Indianapolis 500, one of the premier auto races in the United States, when the BorgWarner Trophy was created as the official winner’s prize.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 10 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

COMPANY PRIORITIES The company outlines its priorities in its investor presentations as:

1) Technology Leadership 2) Customer and Geographic Diversity 3) Financial Strength and Discipline

Profits in the auto industry are largely driven by negotiating power. Auto makers exercise immense market power over their suppliers. We like that BorgWarner’s priorities focus on counterbalancing this power. Technology leadership is the only enduring source of relevance and healthy profits. Leadership is critical, as technological advances are accelerating both in terms of car functionality and in the product development/production processes. Getting behind the curve can mean failure. BorgWarner has demonstrated its commitment to technology innovation with its impressive list of innovations, including a legacy of winning numerous PACE Awards (said to be the Academy Awards of the auto industry), backed by spending 6% of revenues on R&D. The merits of customer and geographic diversity were learned during the last few decades when suppliers’ profits were decimated by over-reliance on a few automakers and on a single geographic market. Light vehicle production is global – having access to all markets, particularly local Chinese markets, improves growth and fosters innovation. While Volkswagen and Ford represent a combined 30% of revenues, BorgWarner has developed a well-diversified customer list around the world. Geographically, about 14% of customer sales are in China, with about 34% in the Americas and 38% in Europe. Financial strength and discipline not only improves BorgWarner’s negotiating power but also allows them to acquire new technologies, fund their R&D and remain strong in the inevitable industry downturns. We like the company’s low debt, high cash balances and ability to increase its Ebitda margin to 17%. While these are good strategic priorities, and management quantifies their short-term guidance, we would like to see more quantified long-term objectives and constraints. Management’s plan to double revenues to $15 billion by 2020 is helpful in this respect. However, revenue growth can be acquired in ways that destroy shareholder value. Specific margin and ROE/ROA goals would be more meaningful for providing insights into the ranking of priorities and monitoring management’s adherence to them.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 11 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

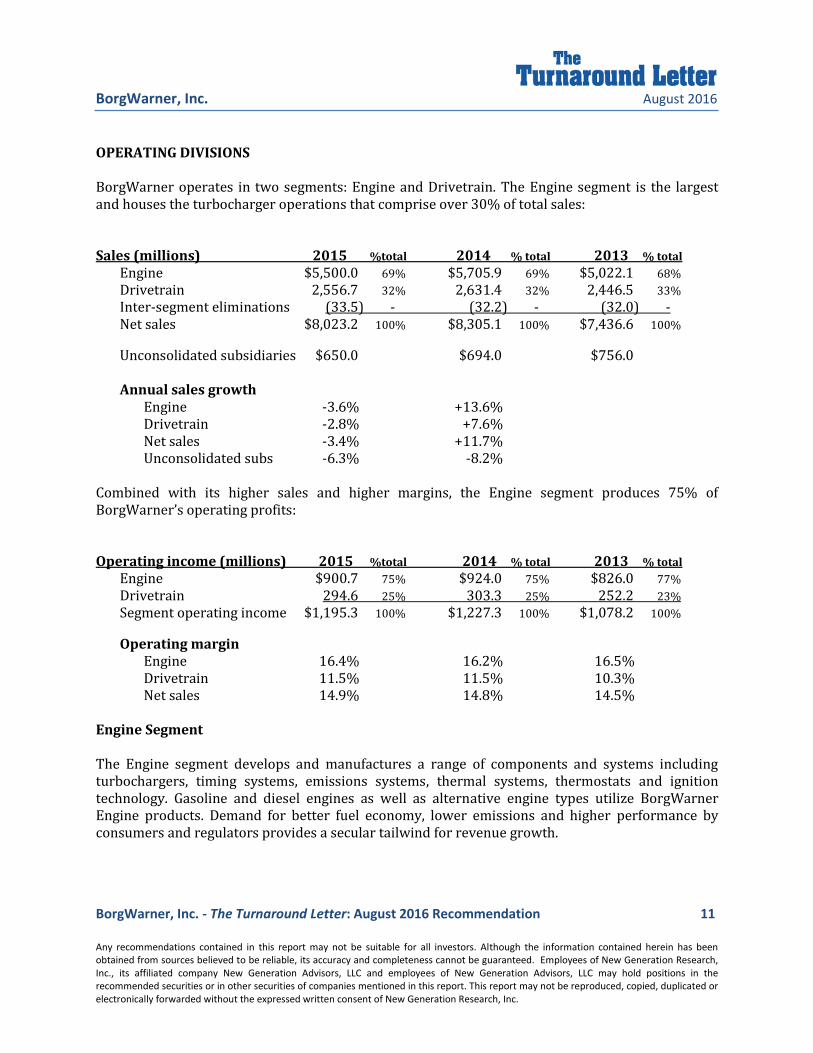

OPERATING DIVISIONS BorgWarner operates in two segments: Engine and Drivetrain. The Engine segment is the largest and houses the turbocharger operations that comprise over 30% of total sales: Sales (millions) 2015 %total 2014 % total 2013 % total

Engine $5,500.0 69% $5,705.9 69% $5,022.1 68%

Drivetrain 2,556.7 32% 2,631.4 32% 2,446.5 33%

Inter-segment eliminations (33.5) - (32.2) - (32.0) - Net sales $8,023.2 100% $8,305.1 100% $7,436.6 100%

Unconsolidated subsidiaries $650.0 $694.0 $756.0 Annual sales growth

Engine -3.6% +13.6% Drivetrain -2.8% +7.6% Net sales -3.4% +11.7% Unconsolidated subs -6.3% -8.2%

Combined with its higher sales and higher margins, the Engine segment produces 75% of BorgWarner’s operating profits: Operating income (millions) 2015 %total 2014 % total 2013 % total

Engine $900.7 75% $924.0 75% $826.0 77%

Drivetrain 294.6 25% 303.3 25% 252.2 23%

Segment operating income $1,195.3 100% $1,227.3 100% $1,078.2 100%

Operating margin Engine 16.4% 16.2% 16.5% Drivetrain 11.5% 11.5% 10.3% Net sales 14.9% 14.8% 14.5%

Engine Segment The Engine segment develops and manufactures a range of components and systems including turbochargers, timing systems, emissions systems, thermal systems, thermostats and ignition technology. Gasoline and diesel engines as well as alternative engine types utilize BorgWarner Engine products. Demand for better fuel economy, lower emissions and higher performance by consumers and regulators provides a secular tailwind for revenue growth.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 12 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

Turbochargers: Sales of turbochargers for light vehicles represented approximately 31% of total sales in 2015, up from about 26% in 2013. Major turbocharger customers include BMW, Daimler, Fiat Chrysler, Ford, General Motors, Great Wall, Hyundai, Renault, Volkswagen and Volvo. The Engine segment also supplies turbochargers to several commercial vehicle and off-highway OEMs including Caterpillar, Daimler, Deutz, John Deere, MAN, Navistar and Weichai. The company’s turbochargers are used in gasoline and diesel engines. Far from a commodity, BorgWarner’s turbochargers use highly-advanced proprietary technologies, and have won numerous engineering awards. Margins are widely believed to be among the highest in the company. Global demand continues to grow, as turbochargers increase power for a given engine size, improve fuel economy and reduce emissions. Demand could accelerate if adaption increases as expected for gasoline engines. Timing Systems – Timing systems enable precise control of air and exhaust flow through the engine, improving fuel economy and emissions. The Engine segment’s timing systems products include timing chains, sprockets, tensioners, guides and snubbers, front-wheel drive transmission chains and four-wheel drive chains for light vehicles. Emissions and systems – Products include electric air pumps and exhaust gas recirculation (“EGR”) products for gasoline and diesel applications as well as viscous fan drives. The Engine segment’s thermal systems products are designed to improve engine efficiency, fuel economy and emissions performance. In 2014, the company acquired, for $110.5 million, Germany-based Wahler, a producer of EGR valves, EGR tubes and thermostats. Wahler’s products strengthen the company’s strategic position as a producer of complete EGR systems and create additional market opportunities in both passenger and commercial vehicle applications. Ignition systems – products improve combustion efficiency for both diesel and gasoline engines, including glow plugs, instant starting systems, pressure sensor glow plugs and advanced ignition technologies. Drivetrain Segment The Drivetrain segment develops and manufactures mechanical products including friction, mechanical and control products for automatic transmissions, torque management products for all-wheel drive (“AWD”) vehicles, and rotating electrical components including starter motors, alternators and hybrid electric motors. The Drivetrain segment does not manufacture products for commercial vehicles. Friction and mechanical products for automatic transmissions include dual clutch modules, friction clutch modules, friction and steel plates, transmission bands, torque converter clutches, one-way clutches and torsional vibration dampers.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 13 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

The Drivetrain segment established its industry-leading position in 2003 with the production launch of its DualTronic innovations with VW/Audi, followed by program launches with Ford, BMW, Nissan, the China ADUIC consortium of 12 leading Chinese automakers and other OEMs around the world. DualTronic technology enables a conventional, manual gearbox to function as a fully automatic transmission. The company’s 50%-owned joint venture in Japan, NSKWarner KK (“NSK-Warner”), is part of the Drivetrain business. Torque management products include rear-wheel drive (“RWD”)-to-AWD transfer case systems, FWD-AWD coupling systems and cross-axle coupling systems for light trucks, SUVs, crossover vehicles and passenger cars. BorgWarner focuses on developing electronically controlled torque management devices and systems that improve fuel economy and vehicle dynamics. With the 2015 acquisition of Remy International, BorgWarner accelerated its expansion into automotive electronic technology for light and commercial vehicles, OEMs and the aftermarket. Principal products include starter motors, alternators and hybrid electric motors. BorgWarner plans to leverage the technologies in two ways: sell more of Remy’s products to manufacturers outside its main North American market, and integrate Remy’s technologies into new and existing Borg Warner products. Joint Ventures At year-end 2015, BorgWarner held partial ownership in eight joint ventures. Results from the six majority-owned joint ventures are consolidated as part of the company’s results. The two joint ventures in which the company’s effective ownership interest is 50% or less are reported using the equity method of accounting. The NSK-Warner is the largest, with $519 million in revenues in 2015. This 50/50 joint venture, formed in 1964 with Japan-based NSK Limited, has operations in Japan and China and produces transmission components such as friction plates and one-way clutches. Geographic distribution of revenues Approximately 75% of the net sales are outside the United States, with about 45-50% generated in Europe. Sales in China have grown the fastest, with a 26% growth rate since 2013. Interestingly, BorgWarner discloses the geographic distribution of its revenues based upon the location of production, not the location of the customer. While this is informative, this hides the revenue impact of large end-markets like Japan and Latin America, and greatly obscures the effect of exports (for example, cars produced in Japan but exported to North America). It would be much more analytically useful if the company disclosed, even with only rounded estimates, the mix of sales based on end markets, which it surely measures.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 14 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

Net sales ($ millions) and % of total * 2015 2014 2013

United States 1,985 25% 2,008 24% 1,940 26% Europe: Germany 1,857 23% 2,146 26% 1,760 24% Hungary 501 6% 518 6% 452 6% France 339 4% 405 5% 328 4% Other 922 11% 1,097 13% 1,133 15% Total Europe 3,619 45% 4,166 50% 3,672 49% China 1,009 13% 885 11% 636 9% South Korea 742 9% 623 8% 564 8% Other 669 8% 623 7% 625 8% Total Sales 8,023 100% 8,305 100% 7,437 100%

Vehicle types, customers and distribution Nearly 84% of BorgWarner’s 2015 revenues were from light-vehicle applications, with 7% from commercial vehicle applications and 4% from off-highway vehicle applications. Approximately 5% were from distributors of aftermarket replacement parts. Volkswagen and Ford are the company’s two largest customers, each representing about 15% of net sales in 2015. This mix has held relatively constant over the past three years. No other single customer accounted for more than 10% of net sales. Sales to GM are about 5% of net sales. BorgWarner’s automotive products are generally sold directly to OEMs through negotiated annual contracts, long-term supply agreements or other terms. Deliveries are based on orders which in turn are based on OEM production schedules. The company typically ships its products directly from its plants to the OEMs. Sales and Marketing The Engine and Drivetrain segments each have their own sales function. Account executives lead the sales and service relationships with specific customers. As these executives have close relationship with customers, they are critical to identifying and meeting customer needs. Furthermore, they are the eyes and ears of the company, providing feedback on market trends, potential new products and other new business opportunities to BorgWarner’s research and development, engineering, sales and marketing staff.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 15 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

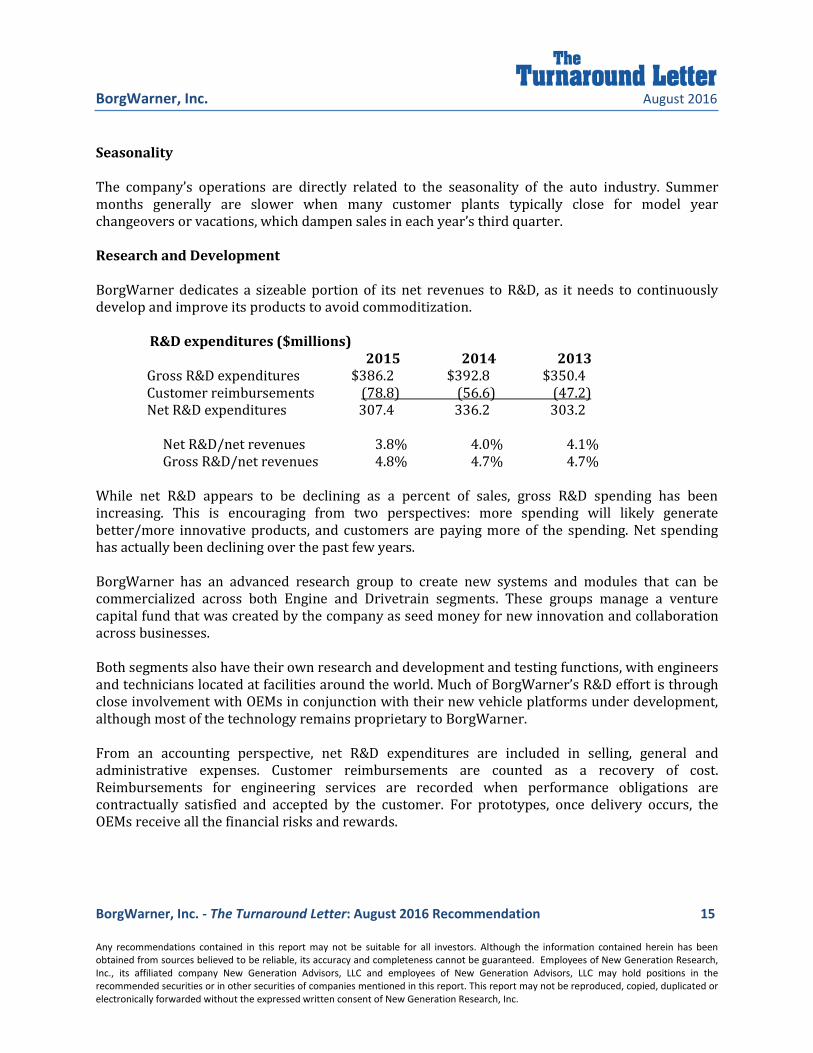

Seasonality The company’s operations are directly related to the seasonality of the auto industry. Summer months generally are slower when many customer plants typically close for model year changeovers or vacations, which dampen sales in each year’s third quarter. Research and Development BorgWarner dedicates a sizeable portion of its net revenues to R&D, as it needs to continuously develop and improve its products to avoid commoditization.

R&D expenditures ($millions) 2015 2014 2013

Gross R&D expenditures $386.2 $392.8 $350.4 Customer reimbursements (78.8) (56.6) (47.2) Net R&D expenditures 307.4 336.2 303.2 Net R&D/net revenues 3.8% 4.0% 4.1% Gross R&D/net revenues 4.8% 4.7% 4.7%

While net R&D appears to be declining as a percent of sales, gross R&D spending has been increasing. This is encouraging from two perspectives: more spending will likely generate better/more innovative products, and customers are paying more of the spending. Net spending has actually been declining over the past few years. BorgWarner has an advanced research group to create new systems and modules that can be commercialized across both Engine and Drivetrain segments. These groups manage a venture capital fund that was created by the company as seed money for new innovation and collaboration across businesses. Both segments also have their own research and development and testing functions, with engineers and technicians located at facilities around the world. Much of BorgWarner’s R&D effort is through close involvement with OEMs in conjunction with their new vehicle platforms under development, although most of the technology remains proprietary to BorgWarner. From an accounting perspective, net R&D expenditures are included in selling, general and administrative expenses. Customer reimbursements are counted as a recovery of cost. Reimbursements for engineering services are recorded when performance obligations are contractually satisfied and accepted by the customer. For prototypes, once delivery occurs, the OEMs receive all the financial risks and rewards.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 16 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

The company has R&D contracts with several customers, but no contract exceeds 5% of net R&D expenditures. Intellectual Property The company has more than 5,600 active domestic and foreign patents and patent applications pending or under preparation. It licenses some patent rights to other companies in exchange for royalties. While patents are important to its business, it is not dependent on any one patent or group of patents or licenses. Competition BorgWarner competes worldwide with many other manufacturers. Differentiation among competitors is based on technological innovation, application engineering development, quality, price, delivery and program launch support.

Engine segment Major competitors . Turbochargers Cummins Turbo Technology IHI Mitsubishi Heavy Industries Honeywell Bosch Mahle Turbo Systems Emissions systems Mahle T.RAD Denso Pierburg Bosch NGK Eldor Timing devices and chains Denso Schaeffler Group Iwis Tsubaki Group Thermal systems Horton Usui Mahle Xuelong Drivetrain segment Major competitors . Torque transfer American Axle JTEKT GKN Driveline Magna Powertrain Rotating electrical devices Denso Melco Transmission systems Bosch FCC Dynax Schaeffler Group

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 17 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

In several product groups, major customers manufacture, for their own use and for others, products that compete with BorgWarner. For many of its products, the company’s competitors include suppliers in parts of the world that enjoy economic advantages such as lower labor costs, lower health care costs, lower tax rates and, in some cases, export subsidies and/or raw materials subsidies. Workforce BorgWarner has a salaried and hourly workforce of approximately 30,000, with about 23%, or 6,900, working in the U.S. Approximately 16% of its U.S. workforce is unionized, and some workers at facilities outside the U.S. are unionized. While relations with its workers appear satisfactory, it is possible that with the strong profits in the auto industry, unions will exert pressure for higher compensation. In addition, legal constraints outside the U.S. may limit BorgWarner’s ability to reduce its workforce. Raw Materials BorgWarner is a large consumer of aluminum, copper, nickel, plastic resins, steel and certain alloy elements. While prices are currently low and availability is high, its margins could be pressured if prices increase sharply. The company uses hedges and other tactics to control its raw materials costs, which have been relatively effective in the past. CAPITAL STRUCTURE Equity BorgWarner’s equity is straightforward: one class of common stock with each share getting one vote. The company has authorized 5 million shares of Preferred stock, and 25 million shares of Non-voting common stock, although no shares of either are currently outstanding. As of April, 2016, there were 217.6 million shares of common stock outstanding, with 390 million authorized. Reflecting share repurchases, options conversion and other transactions, this total is down by 13.5 million shares, or about 6%, from the 231.1 million outstanding in December, 2012.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 18 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

BorgWarner has been a steady buyer of its own stock. While we generally like repurchases, the company’s buybacks over the past three years were at an average price nearly 40% higher than the current $33.18 price: Shares Approx. Repurchased Amount Average

Calendar year (mil) ($mil) Price 2015 8.07 $363 $44.98 2014 2.42 $140 $57.82 2013 5.24 $226 $43.13 Three-year total 15.73 $729 $46.34

The company repurchased about $100 million of shares in the first half of 2016, and has plans to purchase another $200 million to $300 million in the second half of 2016 as part of its $1 billion repurchase authorization. Debt BorgWarner’s debt is similarly straightforward. Long-term debt consists of 7 tranches of straight fixed-rate senior notes with maturities ranging from 2016 to 2045. Through interest rate swaps, about $384.0 million of fixed rate notes have been converted to variable rates at year-end 2015. The weighted average interest rate on all borrowings outstanding, including the effects of outstanding swaps, at year-end 2015 was 3.60%. BorgWarner debt structure

($millions, par value) 2015 2014 Short-term borrowings $281 $601 Long-term: 5.75% Senior notes due 2016 150 150 8% Senior notes due 2019 134 134 4.625% Senior notes due 2020 250 250 1.8% Senior notes due 2022 (Euro note) 541 - 3.375% Senior notes due 2025 500 - 7.125% Senior notes due 2029 121 121 4.375% Senior notes due 2045 500 - Term loan facilities and other 90 75 Total long term debt $2,286 730

BorgWarner’s gross debt level relative to its 2016 estimated Ebitda appears very reasonable at 1.4x. We would consider levels above 3.5x to be high for a company like BorgWarner. The change in FASB accounting rules requiring leases to appear on the balance sheet in 2018 would have a limited

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 19 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

effect on BorgWarner. Future minimum operating lease payments are modest at less than $32 million a year. BorgWarner has a credit rating of Baa1 from Moody’s and BBB+ from both Standard & Poor’s and Fitch Ratings. The current outlook from Moody’s, Standard & Poor’s and Fitch Ratings is stable. None of the company’s debt agreements require accelerated repayment in the event of a downgrade in credit ratings. The long-term debt includes various covenants, none of which are expected to restrict future operations. At December 31, 2015, the company had $577.7 million of cash, of which $441.3 million of cash was held by subsidiaries outside of the United States. With over $300 million in free cash flow (after dividends), and over 75% of its debt maturities at least 4 years away, BorgWarner’s debt burden appears to be readily serviceable.

Principal % of Calendar year Due ($mil) Total 2016 $442 17.2 2017 50 2.0 2018 14 0.5 2019 134 5.2 2020 260 10.1 After 2020 1,674 65.1 Total [a] $2,573 100.0%

[a] Excludes Unamortized discounts.

The increases in long-term debt in 2015 provided funding for the $950 million acquisition of Remy International and for the $1.0 billion share repurchase program. The company has a $1 billion multi-currency revolving credit facility, which may be increased to $1.25 billion, with availability through June 30, 2019. At year-end 2015 and 2014, there were no outstanding borrowings under this facility. Pension Obligations BorgWarner has net unfunded position of $178.3 million at year-end 2015 for its pension plans in total. The company contributed $19.3 million to its defined benefit pension plans in 2015. For 2016, BorgWarner expects to contribute between $15 million and $25 million.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 20 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

Other postretirement employee benefits primarily consist of postretirement health care benefits for certain employees and retirees of the U.S. operations. The company funds these benefits as retiree claims are incurred. Other postretirement employee benefits had an unfunded status of $145.3 million at year-end 2015. Given BorgWarner’s size and profitability, we believe the underfunded positions are of limited impact on the company’s overall investment risk. BorgWarner made $28 million in matching and other contributions to its Defined Contribution plan in 2015, up from $24.9 million in 2013. BOARD, MANAGEMENT, GOVERNANCE AND ESG PRACTICES Board of Directors The board and governance are of average quality. Over the past few years the board has improved its governance practices. The size of the board was permanently reduced to nine members from ten. While nine is larger than our ideal size (which is seven), the move is in the right direction and we would consider the size to be reasonable. We like that the CEO is the only company executive on the board. The average member age (~64 years) is reasonable. Given the company’s high profile and strong financial condition, an experienced board provides valuable perspective to work effectively with shareholders of all types. However, we would like to see some younger members: other than the CEO (at 53 years of age) the youngest member is 55 (Carlson). While the average age of car buyers in the U.S. is 48, younger consumers are the future of the industry and seem to be buying at slower rates than their predecessors. We recognize the immense value of age and experience in guiding an engineering-driven firm (compared to a marketing-driven firm). Perhaps, though, younger board members would have a valuable perspective on what types of new products and ideas would appeal to this group that older board members could miss. The board is homogenous with eight of the nine members being men. As with the age mix, it might benefit the board’s perspective with a more diverse demographic mix overall. We find the experience mix reasonable. Four members have auto industry leadership, including Carlson who is Chairman/CEO of auto supplier Autoliv. Interestingly, two members, Schaum and Stallkamp, previously worked with Chrysler (we’d prefer only one). Nearly all the board members serve on other company boards, a positive in our view as it broadens their perspective.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 21 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

Board tenure excluding the CEO averages 9.9 years, higher than we would like to see. This average is skewed by the 23-year tenure of the chairman. Excluding the chairman, the remaining members’ average tenure is a much more reasonable 8 years, with the longest tenure being 13 years. The lead director, Michas, has considerable private equity experience, and other members have some private equity/private company experience. We value the long-term perspective that private equity backgrounds can bring to what often is a short-term or non-shareholder-friendly focus at public companies. We are a bit surprised that no executives of major technology companies are represented. While no doubt BorgWarner has highly-capable technology engineers, having a technology-driven view at the board level could offer important insights during a time when technological changes are driving the future of the auto industry. Management Overall management appears to be capable and consistent. BorgWarner is led by James Verrier, a 26-year company veteran appointed to the CEO role in January, 2013. The company has a history of and commitment to internal promotion, which appears to be successful and effective. Verrier succeeded Tim Manganello, who was widely considered to have been very successful in building the company during his 10 years as CEO. With the CEO change also came a CFO change: with Verrier’s promotion to president/COO in March 2012 (as heir-apparent), Ron Hundzinski replaced Manganello’s CFO. Hundzinski rose through the ranks, with operating and finance experience, most recently as treasurer as well as controller. We like that Verrier has had considerable experience with the BorgWarner philosophy. A key component of our thesis is that the company will continue to execute its established strategy – having a CEO with this strategy embedded in his mindset and has successfully executed on it greatly increases the likelihood of success. We also like his engineering and metallurgy mindset, particularly in a company whose competitive edge is engineering. Verrier’s experience includes President of BorgWarner Morse TEC, Vice President and General Manager of the passenger car segment of BorgWarner Turbo Systems, and a range of positions with increasing responsibility with quality control, human resources and operations management. He also has experience outside the company with engineering and metallurgy roles with Lucas Aerospace, Rockwell Automotive and Britax Wingard in the United Kingdom. Verrier is on the board of Parker Hannifin Corporation. He holds a degree in Metallurgy and Materials Science from West Midlands College in the UK and an MBA from the University of Glamorgan, also in the UK.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 22 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

Governance We view BorgWarner’s governance structures as good/improving. Some of the features we like include: single class of voting stock, annual election of all directors (starting in 2017), majority vote standard and no shareholder rights plan (poison pill, etc.). The board has a non-executive session at each meeting – acceptable but not as effective as stand-alone, regular non-executive board meetings. The company recently relaxed its proxy access rules. Investors holding an aggregate of at least 20% of the total votes may now call a special meeting of stockholders (each stockholder must hold at least 5% of BWA shares to be eligible, for a minimum of 3 years, and no more than ten eligible stockholders may aggregate their holdings to reach the 20% threshold). This increased access allows shareholders to exert higher influence on the board and management. BorgWarner separates its chairman and CEO roles. While there is some controversy regarding the merits of separate/unified roles, we believe having a fixed standard either way is too rigid with such a subjective matter. As long as the board structure and overall execution appears strong and not unduly dominated by the chairman/CEO’s agenda or personality, we are fine with either a unified or separate role. BorgWarner’s separate role structure is acceptable to us. Only one board member, CEO James Verrier, is an employee of BorgWarner. We view this as favorable as it limits the inherent ‘stay the course’ mindset of management teams in general. Share ownership by the board is lower than we would prefer. The largest stake among directors and officers is Verrier’s at 308,520 shares, or about $10.2 million. This represents less than .15% of shares outstanding. All the directors and officers combined hold about 1.4 million shares, or less than .65% of shares outstanding. While we admire the directive that all board members must accumulate at least 5x their annual cash retainer in company stock within five years, the amounts accumulated seem too low to meaningfully incent the board to think as shareholders. We also question the merits of requiring this level of ownership while simultaneously granting enough restricted stock as part of their routine compensation to allow directors to meet this hurdle. While low ownership is common among American boards, we strongly prefer high ownership. Also, share ownership among BorgWarner directors seems related to tenure, indicating that most of the ownership came through option awards. We would prefer that ownership came through outright purchases. Board membership annual cash fees at $92,000 appear reasonable and are lower than the $100,000+ commonly found in other large companies. However, Board members also receive $123,000 worth of restricted stock, up to another $9,000 in cash for committee service (more for committee chairs), $1,500 for each board meeting attended and another $1,500 for each committee meeting attended. This extra compensation seems unnecessary, particularly as all expenses related

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 23 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

to meetings are covered by the company. The non-executive chairman receives $388,000 in total compensation, high in our view. ESG practices

While difficult to directly quantify the profit impact of strong Environmental, Social, and Governance (ESG) practices, we believe these matter to relevancy, sustainability and quality, which drive long-term revenues, profits and valuation. In addition to improving its governance practices (discussed separately above), BorgWarner is improving its other ESG practices. Its website provides good disclosure and discussion of its programs that help protect the environment and promote sustainability by example. As an important aspect of ESG principles is the merits of a company’s primary products, BorgWarner fares well. Its products are designed to improve fuel economy and reduce emissions. Two of its larger product group, turbochargers and dual-clutch transmissions, can help improve fuel economy by over 15%. In its production process, the company is protecting the environment with sustainable construction and operations practices. Examples include its new facilities in Itatiba City, Brazil, at which BorgWarner became the first LEED-Certified automobile supplier in Brazil. The company opened a LEED Gold-Certified facility in China, a highly-efficient “green” turbo facility in Poland, and utilizes numerous other environmentally-smart practices throughout its operations. While we have little hard data on BorgWarner’s employee and supplier diversity, it has received a 2015 GM Supplier IMPACT Award for demonstrating top performance in the Diversity Spend Percentage to Goal category and excelling in the Significantly Improved category. In managing its supply chain, the company has a conflict minerals policy that appears to be effective in reducing/eliminating its use of these materials. BorgWarner also has numerous programs to foster education, fight diseases and support disadvantaged communities. AUDITOR’S OPINION Independent auditor PriceWaterhouseCoopers LLP gave an unqualified opinion on BorgWarner’s financial statements for past two years (2015 and 2014). The auditor also gave the company an unqualified opinion on its internal controls over its financial reporting as of December 31, 2015.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 24 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

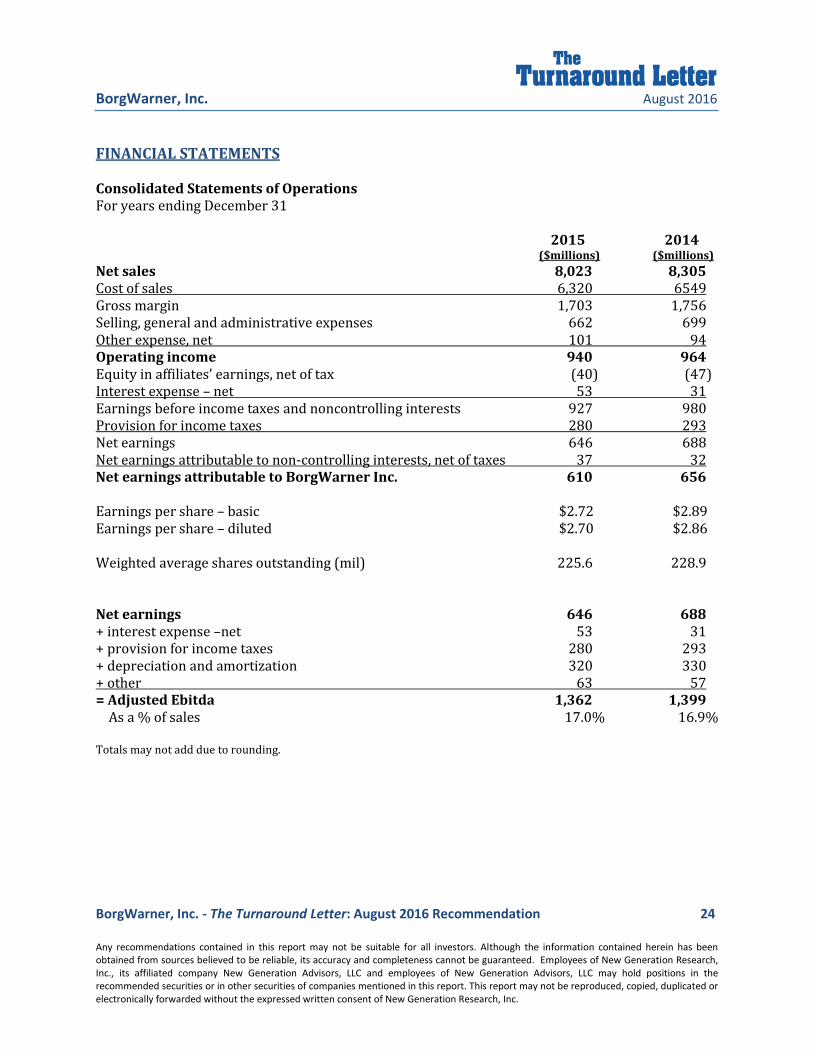

FINANCIAL STATEMENTS Consolidated Statements of Operations For years ending December 31 2015 2014 ($millions) ($millions)

Net sales 8,023 8,305 Cost of sales 6,320 6549 Gross margin 1,703 1,756 Selling, general and administrative expenses 662 699 Other expense, net 101 94 Operating income 940 964 Equity in affiliates’ earnings, net of tax (40) (47) Interest expense – net 53 31 Earnings before income taxes and noncontrolling interests 927 980 Provision for income taxes 280 293 Net earnings 646 688 Net earnings attributable to non-controlling interests, net of taxes 37 32 Net earnings attributable to BorgWarner Inc. 610 656 Earnings per share – basic $2.72 $2.89 Earnings per share – diluted $2.70 $2.86 Weighted average shares outstanding (mil) 225.6 228.9 Net earnings 646 688 + interest expense –net 53 31 + provision for income taxes 280 293 + depreciation and amortization 320 330 + other 63 57 = Adjusted Ebitda 1,362 1,399 As a % of sales 17.0% 16.9% Totals may not add due to rounding.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 25 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

Consolidated Balance Sheets At December 31 2015 2014 ($millions) ($millions)

Assets Cash 578 798 Receivables, net 1,665 1,444 Inventories, net 724 506 Deferred income taxes, prepayments and other current assets 169 224 Total current assets 3,135 2,971 Property and equipment – net 2,448 2,094 Investments and other long-term receivables 461 403 Goodwill 1,758 1,206 Other intangibles, net and other current assets 1,040 554 Total assets 8,842 7,228 Liabilities and shareholders’ equity Notes payable and other short-term debt 442 624 Accounts payable and accrued expenses 1,866 1,530 Income taxes payable 49 14 Total current liabilities 2,357 2,168 Long-term debt 2,125 716 Other non-current liabilities 728 653 BorgWarner stockholders’ equity 3,554 3,616 Non-controlling interest 78 75 Total shareholders’ equity 3,632 3,690 Total liabilities and shareholders’ equity 8,842 7,228 Totals may not add due to rounding.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 26 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

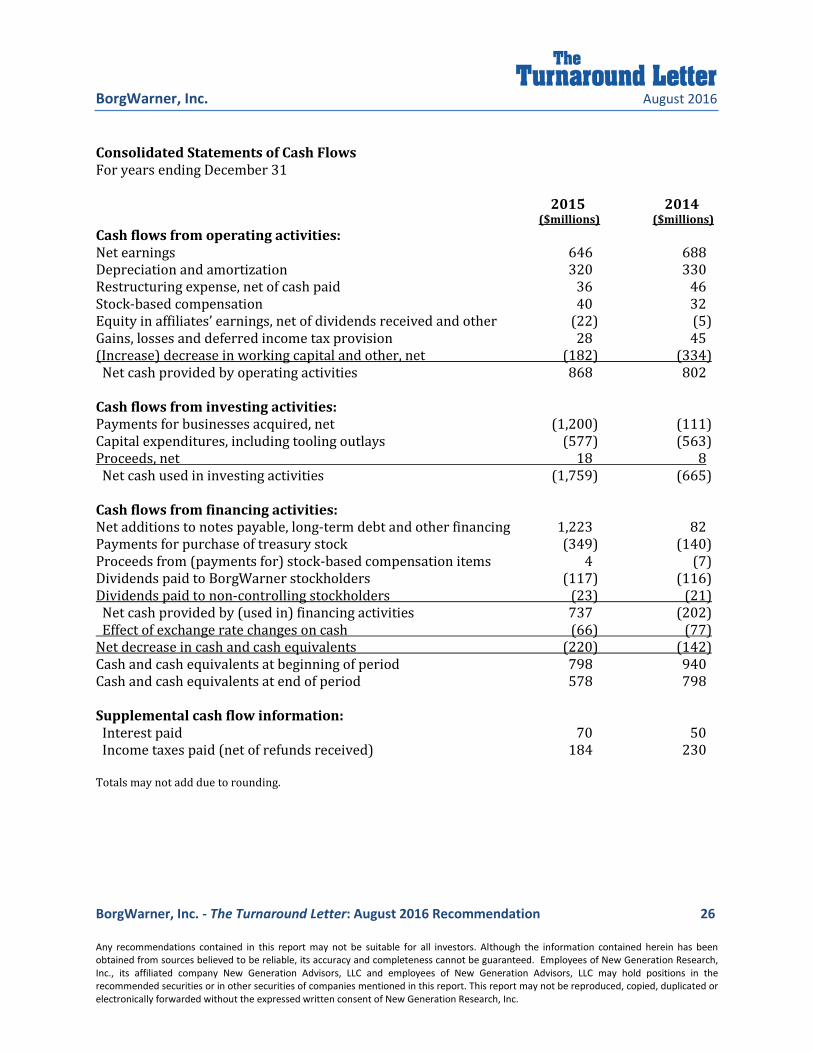

Consolidated Statements of Cash Flows For years ending December 31 2015 2014 ($millions) ($millions)

Cash flows from operating activities: Net earnings 646 688 Depreciation and amortization 320 330 Restructuring expense, net of cash paid 36 46 Stock-based compensation 40 32 Equity in affiliates’ earnings, net of dividends received and other (22) (5) Gains, losses and deferred income tax provision 28 45 (Increase) decrease in working capital and other, net (182) (334) Net cash provided by operating activities 868 802 Cash flows from investing activities: Payments for businesses acquired, net (1,200) (111) Capital expenditures, including tooling outlays (577) (563) Proceeds, net 18 8 Net cash used in investing activities (1,759) (665) Cash flows from financing activities: Net additions to notes payable, long-term debt and other financing 1,223 82 Payments for purchase of treasury stock (349) (140) Proceeds from (payments for) stock-based compensation items 4 (7) Dividends paid to BorgWarner stockholders (117) (116) Dividends paid to non-controlling stockholders (23) (21) Net cash provided by (used in) financing activities 737 (202) Effect of exchange rate changes on cash (66) (77) Net decrease in cash and cash equivalents (220) (142) Cash and cash equivalents at beginning of period 798 940 Cash and cash equivalents at end of period 578 798 Supplemental cash flow information: Interest paid 70 50 Income taxes paid (net of refunds received) 184 230 Totals may not add due to rounding.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 27 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

RISKS

While we believe the growth strategy will be successful and that the stock market will reward the shares with a significantly higher price, it is not without risks. Identifying the risks helps guide our focus as well as gauge the company’s progress. We see the following risks as most significant to a successful investment: Operating risks (risks relating to the company’s operating performance):

CEO James Verrier may not be successful in leading continued revenue growth, or the growth trajectory declines due to market share losses or a cyclical downturn.

Competition from other manufacturers impedes BorgWarner’s sales and margins. The market share of electronic vehicles could increase rapidly, limiting demand for

BorgWarner’s core products which are at present focused on internal combustion engines. Customers, particularly 15%+ customers like VW and Ford, may shift suppliers, exert

greater pricing pressure or reduce their order volumes. Labor cost increases, particularly with its union workers, could impair margins. Turbochargers are 31% of revenues, with higher-than-average margins. Any increased

pricing pressure or slowdown in demand could impact revenues and/or margins. Financial risks (risks relating to the company’s financial condition):

A sharp reduction in profits in a deep economic slowdown could reduce the company’s ability to pay cash interest or make principal payments on time or adequately refinance maturing debt, or could trigger debt covenants and potentially risk a default.

Remitting its large cash balances held overseas to meet domestic liquidity requirements could trigger sizeable taxes.

Weak investment returns could exacerbate the retirement plans shortfall. While the company uses “net new business” and “organic” growth to describe a key driver

of their growth, they do not provide related historical data in SEC filings. We do not suspect anything inappropriate, but it is unusual for a company to use key terms such as these in their outlook but not include historical results in their SEC filings.

Economic risks (risks related to broad economic conditions):

A major economic slowdown, or a decline in the U.S. or global demand for light vehicles, commercial vehicles and other related vehicles would directly impact demand for BorgWarner’s products.

A significantly stronger dollar could impact earnings. Higher raw materials costs, particularly steel and nickel, could reduce its margins or impair

its ability to manufacture its products. Market risk (risks related to public securities markets):

Investors may lose confidence in the magnitude or timing of a successful turnaround.

BorgWarner, Inc. August 2016

BorgWarner, Inc. - The Turnaround Letter: August 2016 Recommendation 28 Any recommendations contained in this report may not be suitable for all investors. Although the information contained herein has been obtained from sources believed to be reliable, its accuracy and completeness cannot be guaranteed. Employees of New Generation Research, Inc., its affiliated company New Generation Advisors, LLC and employees of New Generation Advisors, LLC may hold positions in the recommended securities or in other securities of companies mentioned in this report. This report may not be reproduced, copied, duplicated or electronically forwarded without the expressed written consent of New Generation Research, Inc.

Stock market may fail to assign the estimated target multiple on the company’s profits. Capital market changes could impair the company’s abilities to obtain financing.

Sovereign and regulatory risk (risks from actions by governments):

Geopolitical events and other related circumstances. Increase in trade barriers including tariffs and/or quotas. Changes to U.S. and foreign country laws, regulations and policies.

SOURCES This report uses sources which we believe to be reliable. However, we cannot guarantee its entire accuracy. New Generation Research and related companies and their employees may at times hold positions in any of the securities mentioned herein. Sources include: company news releases, 10-K, proxy and other regulatory filings and website; Bloomberg; Schwab research; Morningstar; Research and Markets; fundinguniverse.com; hybridcars.com; The Wall Street Journal; The Turnaround Letter analysis and other sources.