bookkeeping controls - osbornebooks.co.uk · 14 bookkeeping controls tutor zone 4.3 you have the...

TRANSCRIPT

Osborne Books Tutor Zone

BookkeepingControlsChapter activities

© Osborne Books Limited, 2016

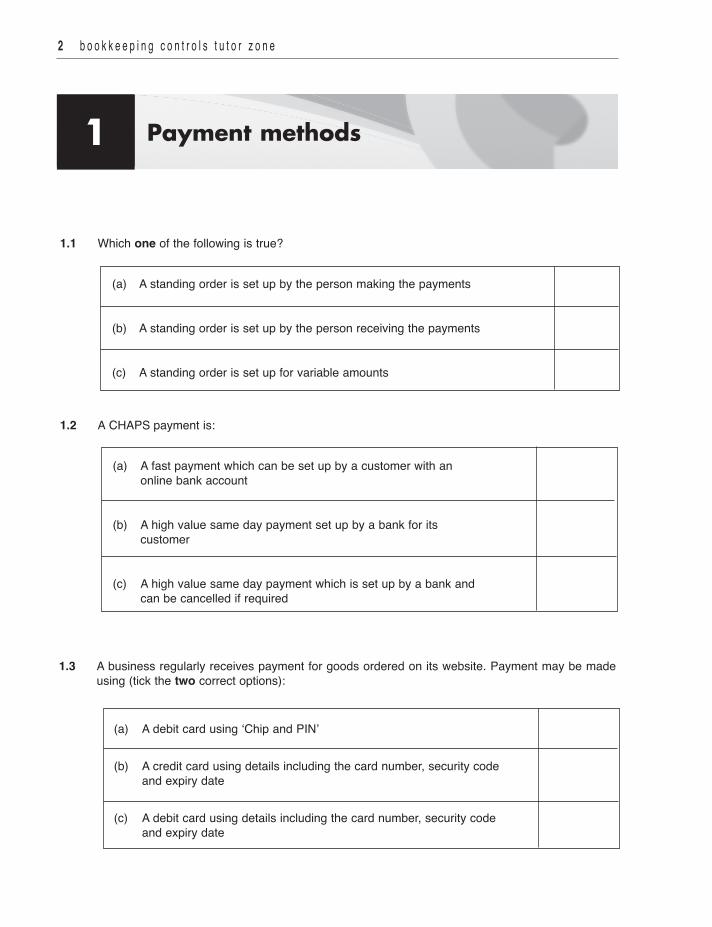

1.1 Which one of the following is true?

(a) A standing order is set up by the person making the payments

(b) A standing order is set up by the person receiving the payments

(c) A standing order is set up for variable amounts

1.2 A CHAPS payment is:

(a) A fast payment which can be set up by a customer with an online bank account

(b) A high value same day payment set up by a bank for its customer

(c) A high value same day payment which is set up by a bank and can be cancelled if required

1.3 A business regularly receives payment for goods ordered on its website. Payment may be madeusing (tick the two correct options):

(a) A debit card using ‘Chip and PIN’

(b) A credit card using details including the card number, security code and expiry date

(c) A debit card using details including the card number, security code and expiry date

2 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Payment methods1

1.4 Show whether the following types of payment are electronic or not electronic.

Electronic Not electronic

(a) Debit card

(b) Contactless credit card

(c) Computer-printed cheque

(d) Cash

(e) Faster payment

(f) Bank draft

(g) Direct debit

1.5 When writing out a cheque to be used as a form of payment, which of the following must be filledin by hand?

(a) Amount in figures

(b) Payer’s name

(c) Date

(d) Amount in words

(e) Authorised signature

(f) Payee’s bank details

(g) Payee’s name

(h) Name of person signing the cheque

(i) ‘Account payee only’ crossing

(j) Counterfoil details

(k) Direct debit

c h a p t e r a c t i v i t i e s 3

4 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

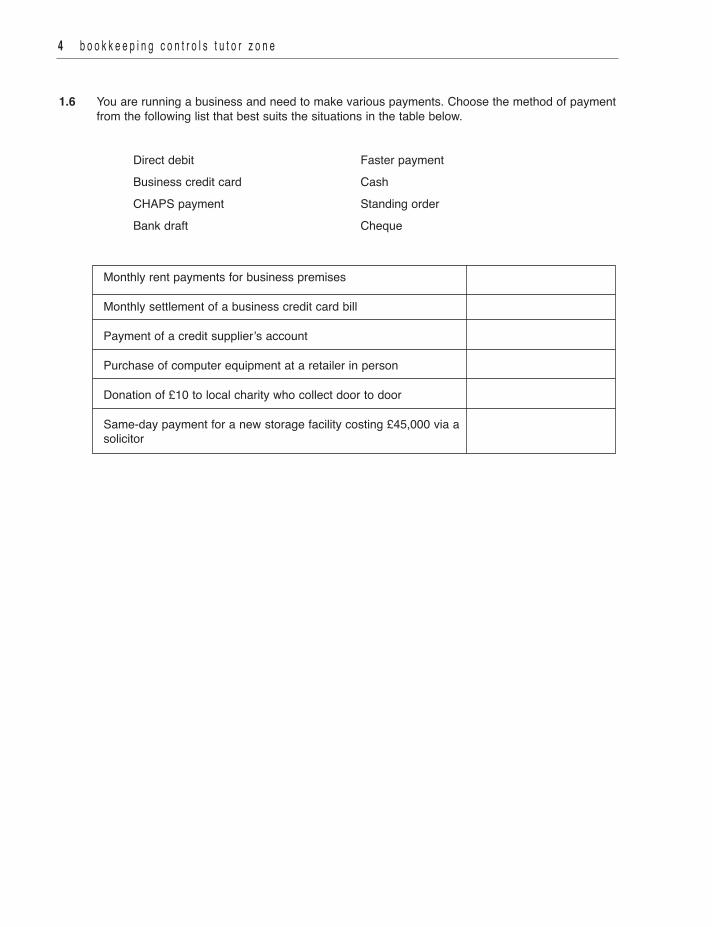

1.6 You are running a business and need to make various payments. Choose the method of paymentfrom the following list that best suits the situations in the table below.

Direct debit Faster paymentBusiness credit card CashCHAPS payment Standing orderBank draft Cheque

Monthly rent payments for business premises

Monthly settlement of a business credit card bill

Payment of a credit supplier’s account

Purchase of computer equipment at a retailer in person

Donation of £10 to local charity who collect door to door

Same-day payment for a new storage facility costing £45,000 via asolicitor

c h a p t e r a c t i v i t i e s 5

Payment methods and the bankaccount balance2

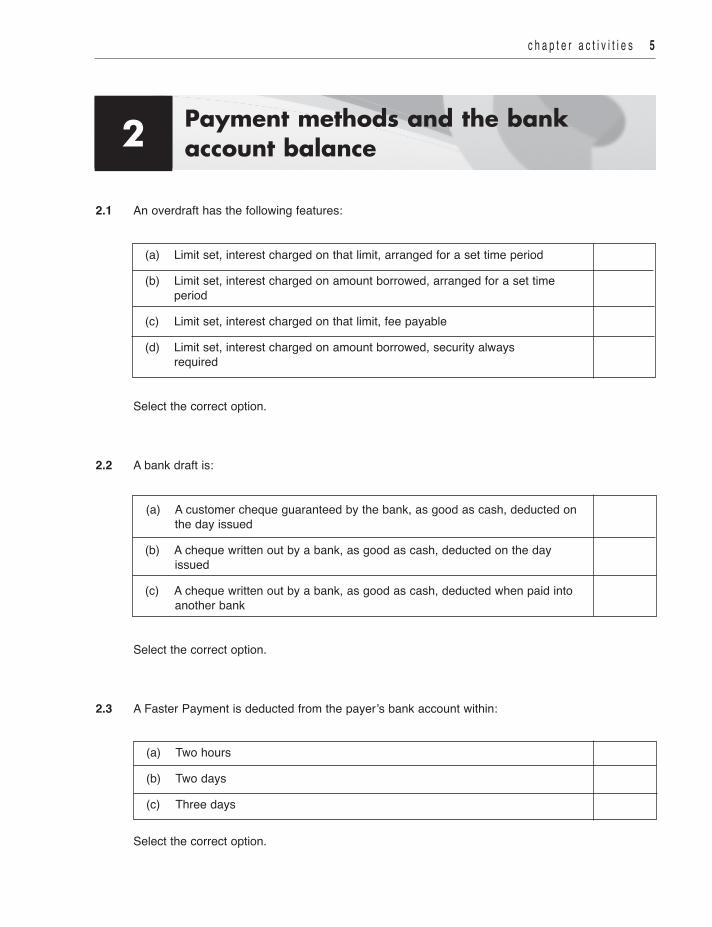

2.1 An overdraft has the following features:

(a) Limit set, interest charged on that limit, arranged for a set time period

(b) Limit set, interest charged on amount borrowed, arranged for a set time period

(c) Limit set, interest charged on that limit, fee payable

(d) Limit set, interest charged on amount borrowed, security always required

Select the correct option.

2.2 A bank draft is:

(a) A customer cheque guaranteed by the bank, as good as cash, deducted on the day issued

(b) A cheque written out by a bank, as good as cash, deducted on the day issued

(c) A cheque written out by a bank, as good as cash, deducted when paid into another bank

Select the correct option.

2.3 A Faster Payment is deducted from the payer’s bank account within:

(a) Two hours

(b) Two days

(c) Three days

Select the correct option.

6 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

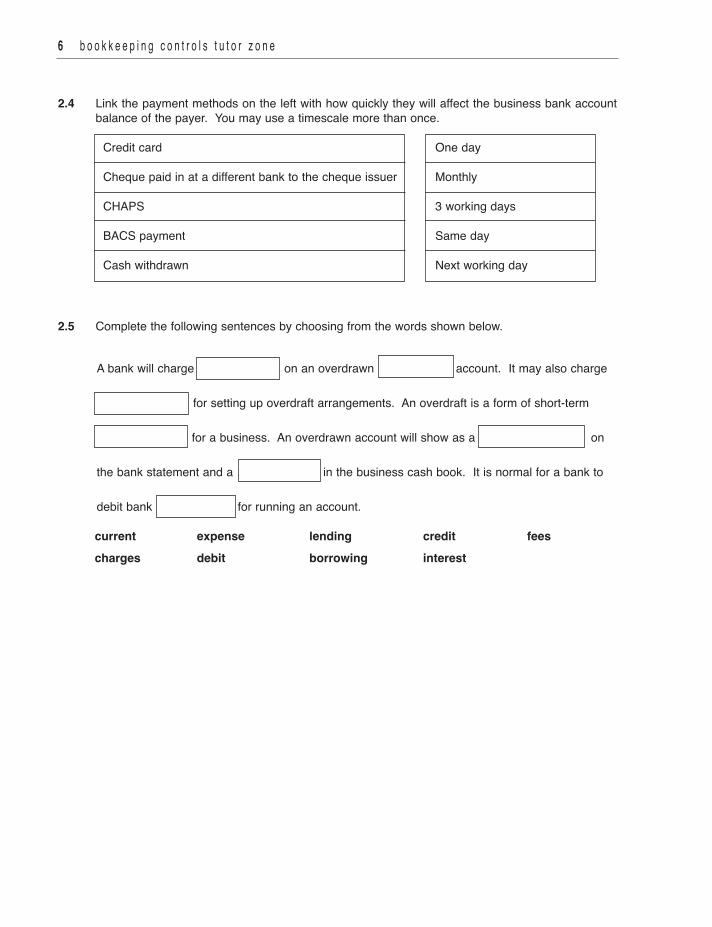

2.4 Link the payment methods on the left with how quickly they will affect the business bank accountbalance of the payer. You may use a timescale more than once.

Credit card One day

Cheque paid in at a different bank to the cheque issuer Monthly

CHAPS 3 working days

BACS payment Same day

Cash withdrawn Next working day

2.5 Complete the following sentences by choosing from the words shown below.

A bank will charge ………… …… on an overdrawn … ………… account. It may also charge

…………… for setting up overdraft arrangements. An overdraft is a form of short-term

for a business. An overdrawn account will show as a …… ………… on

the bank statement and a ………… …… in the business cash book. It is normal for a bank to

debit bank ………… … for running an account.

current expense lending credit feescharges debit borrowing interest

c h a p t e r a c t i v i t i e s 7

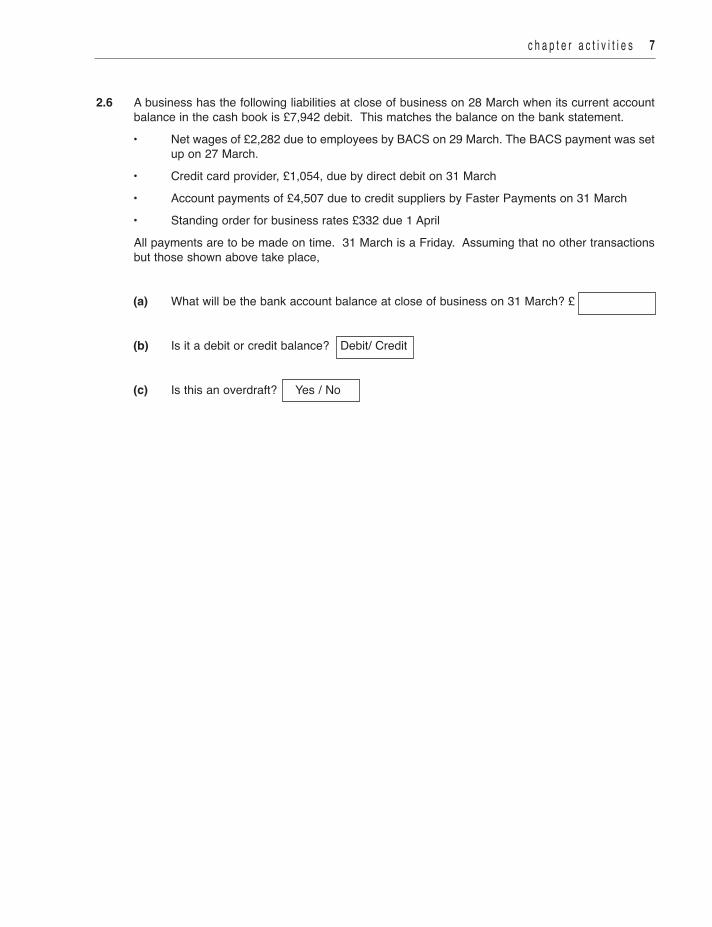

2.6 A business has the following liabilities at close of business on 28 March when its current accountbalance in the cash book is £7,942 debit. This matches the balance on the bank statement.• Net wages of £2,282 due to employees by BACS on 29 March. The BACS payment was set

up on 27 March.• Credit card provider, £1,054, due by direct debit on 31 March• Account payments of £4,507 due to credit suppliers by Faster Payments on 31 March• Standing order for business rates £332 due 1 AprilAll payments are to be made on time. 31 March is a Friday. Assuming that no other transactionsbut those shown above take place,

(a) What will be the bank account balance at close of business on 31 March? £

(b) Is it a debit or credit balance? Debit/ Credit

(c) Is this an overdraft? Yes / No

8 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

3.2 A firm’s bank statement shows a balance of £850 credit. Unpresented cheques total £2,250;outstanding lodgements total £750. What is the balance at bank shown by the cash book?

(a) £2,350 debit

(b) £2,350 credit

(c) £650 debit

(d) £650 credit

3.1 Upon receipt of a bank statement, which two of the following must be written into the firm’s cashbook?

1 bank charges 2 unpresented cheques 3 direct debit payments 4 outstanding lodgements

(a) 1 and 3

(b) 2 and 4

(c) 1 and 4

(d) 2 and 3

Bank reconciliation statements3

c h a p t e r a c t i v i t i e s 9

3.3 The bank columns of Chris Hart's cash book for May 20-4 are as follows:

20-4 Receipts £ 20-4 Payments £1 May Balance b/d 755.50 3 May Curtis Ltd 002476 200.0010 May Hawkins Ltd 530.90 12 May T Daniels 002477 327.4028 May B Morgan 386.45 15 May Smith & Co 002478 289.60 16 May Arnold & Sons 002479 327.20 22 May P Singh 002480 154.30 He received his bank statement which showed the following transactions for May 20-4:

BANK STATEMENT Payments Receipts Balance

20-4 £ £ £ 1 May Balance brought forward 855.50 CR

6 May Cheque no 002475 100.00 755.50 CR7 May Cheque no 002476 200.00 555.50 CR8 May Credit 530.90 1,086.40 CR

15 May BACS credit: AJ Traders 396.20 1,482.60 CR 22 May Cheque no 002477 327.40 1,155.20 CR 24 May Direct debit: Arley Finance 184.65 970.55 CR 25 May Cheque no 002478 289.60 680.95 CR

You are to:

(a) Check the items on the bank statement against the items in the cash book and update the cash book accordingly; total the cash book and show the balance carried down at 31 May 20-4.

(b) Prepare a bank reconciliation statement at 31 May 20-4 which agrees the bank statement balance with the cash book balance.

1 0 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

3.4 On 30 November Segovia Ltd received the following bank statement as at 24 November 20-2.

BANK STATEMENTDate Details Paid out Paid in Balance20-2 £ £ £ 01 Nov Balance brought forward 1,991 C02 Nov Cheque 594882 255 1,736 C04 Nov BACS credit: R Phillips 1,364 3,100 C05 Nov Cheque 594884 1,700 1,400 C07 Nov Cheque 594885 922 478 C12 Nov Paid into bank 1,517 1,995 C13 Nov Cheque 594883 352 1,643 C18 Nov BACS credit: Walters & Co 2,392 4,035 C19 Nov Direct debit: Wyvern Council 245 3,790 C20 Nov Cheque 594887 796 2,994 C24 Nov Bank charges 50 2,944 C24 Nov Cheque 594886 1,062 1,882 C

D = Debit C = Credit

c h a p t e r a c t i v i t i e s 1 1

The cash book as at 24 November 20-2 is shown below.

CASH BOOK Date Details Bank Date Cheque Details Bank 20-2 £ 20-2 number £

01 Nov Balance b/f 1,736 02 Nov 594883 Mercia Supplies 352

02 Nov R Phillips 1,364 02 Nov 594884 Perran Ltd 1,700

10 Nov Begley & Co 1,517 03 Nov 594885 Wilson Ltd 922

22 Nov Egan Ltd 2,235 11 Nov 594886 Durning Stores 1,062

23 Nov Dholiwar Ltd 1,076 11 Nov 594887 Bromfields 796

19 Nov 594888 Scott Ltd 426

19 Nov Wyvern Council 245

22 Nov 594889 HTP Ltd 968

(a) Check the items on the bank statement against the items in the cash book. (b) Enter any items in the cash book as needed. (c) Total the cash book and clearly show the balance carried down at 24 November (closing

balance) and brought down at 25 November (opening balance).

Select your entries for the ‘Details’ column from the following list: Balance b/f, Balance c/d, Bank charges, Begley & Co, Bromfields, Closing balance, Dholiwar Ltd, Durning Stores, Egan Ltd, HTP Ltd, Mercia Supplies, Opening balance, Perran Ltd, R Phillips, Scott Ltd, Walters & Co, Wilson Ltd, Wyvern Council.

1 2 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

(d) Complete the bank reconciliation statement as at 24 November.

Select your entries for the ‘Details’ column from the following list: Bank charges, Begley & Co, Bromfields, Dholiwar Ltd, Durning Stores, Egan Ltd, HTP Ltd, Mercia Supplies, Perran Ltd, R Phillips, Scott Ltd, Walters & Co, Wilson Ltd, Wyvern Council.

Bank reconciliation statement as at 24 November 20-2

Balance as per bank statement £

Add

Name: £

Name: £

Total to add £

Less

Name: £

Name: £

Total to subtract £

Balance as per cash book £

c h a p t e r a c t i v i t i e s 1 3

4.2 You have the following information for the month:• supplier balances at start of month £19,542• credit purchases £12,764• purchases returns £391• money paid to suppliers £11,048• discounts received £164What is the figure for supplier balances at the end of the month?

(a) £20,703

(b) £18,381

(c) £21,485

(d) £21,031

4.1 You have the following information for the month:• customer balances at start of month £36,247• credit sales £20,391• sales returns £1,038• money received from customers £18,416• discounts allowed £184• irrecoverable debt written off £220What is the figure for customer balances at the end of the month?

(a) £32,830

(b) £33,270

(c) £36,780

(d) £37,588

Using control accounts4

1 4 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

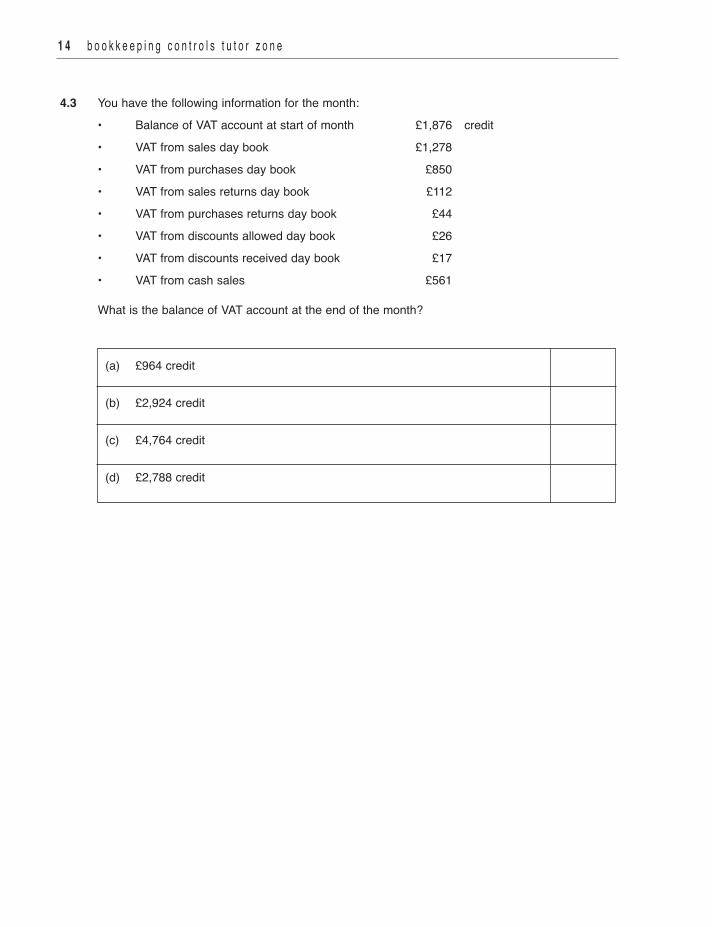

4.3 You have the following information for the month: • Balance of VAT account at start of month £1,876 credit • VAT from sales day book £1,278 • VAT from purchases day book £850 • VAT from sales returns day book £112 • VAT from purchases returns day book £44 • VAT from discounts allowed day book £26 • VAT from discounts received day book £17 • VAT from cash sales £561

What is the balance of VAT account at the end of the month?

(a) £964 credit

(b) £2,924 credit

(c) £4,764 credit

(d) £2,788 credit

c h a p t e r a c t i v i t i e s 1 5

4.4 You work as an Accounts Assistant for Ikpasa Limited. Today you are working on the purchasesledger control account and purchases ledger.

(a) A summary of transactions with credit suppliers during the month of August is shown below. Show whether each entry will be a debit or a credit in the purchases ledger control account

in the general ledger.

Details Amount Debit Credit £

Balance of credit suppliers at 1 August 29,338 Purchases from credit suppliers 18,174 Payments to credit suppliers 19,351 Discounts received 176 Goods returned to credit suppliers 847

(b) What will be the balance brought down on 1 September on the above account?

(a) Dr £27,490 (b) Cr £27,490 (c) Dr £31,538 (d) Cr £31,538 (e) Dr £27,138 (f) Cr £27,138

The following credit balances were in the purchases ledger on 1 September.

£ Siddique Ltd 4,954 Patterson & Co 5,821 A Cracknell 3,954 De Waal Ltd 6,286 Luxon Stores 3,470 Denison plc 2,998

1 6 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

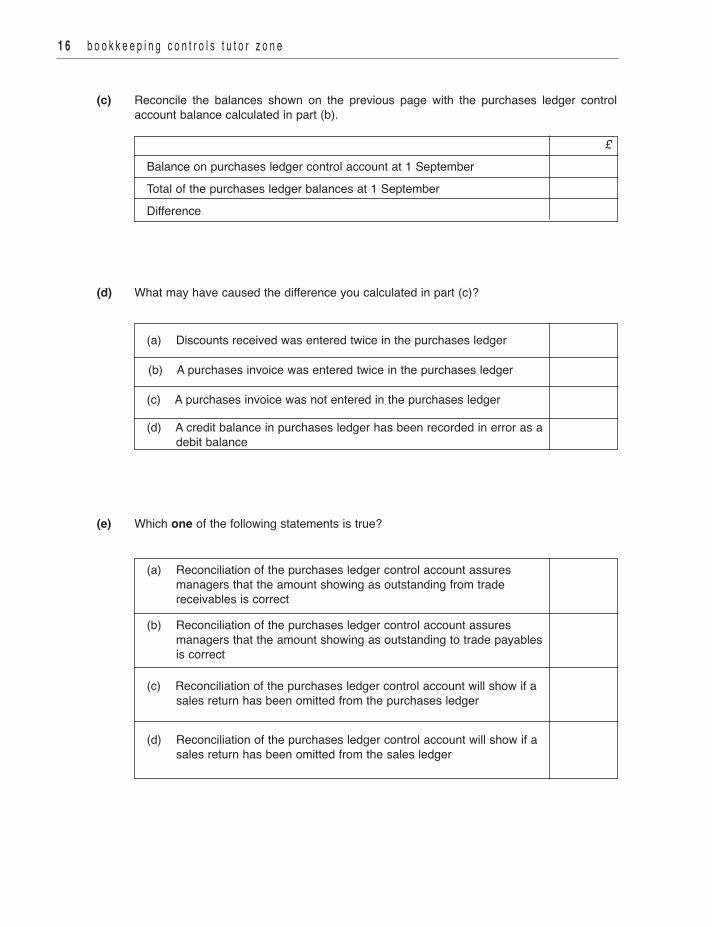

(c) Reconcile the balances shown on the previous page with the purchases ledger controlaccount balance calculated in part (b).

£ Balance on purchases ledger control account at 1 September Total of the purchases ledger balances at 1 September Difference

(d) What may have caused the difference you calculated in part (c)?

(a) Discounts received was entered twice in the purchases ledger

(b) A purchases invoice was entered twice in the purchases ledger

(c) A purchases invoice was not entered in the purchases ledger

(d) A credit balance in purchases ledger has been recorded in error as a debit balance

(e) Which one of the following statements is true?

(a) Reconciliation of the purchases ledger control account assures managers that the amount showing as outstanding from trade receivables is correct

(b) Reconciliation of the purchases ledger control account assures managers that the amount showing as outstanding to trade payables is correct

(c) Reconciliation of the purchases ledger control account will show if a sales return has been omitted from the purchases ledger

(d) Reconciliation of the purchases ledger control account will show if a sales return has been omitted from the sales ledger

c h a p t e r a c t i v i t i e s 1 7

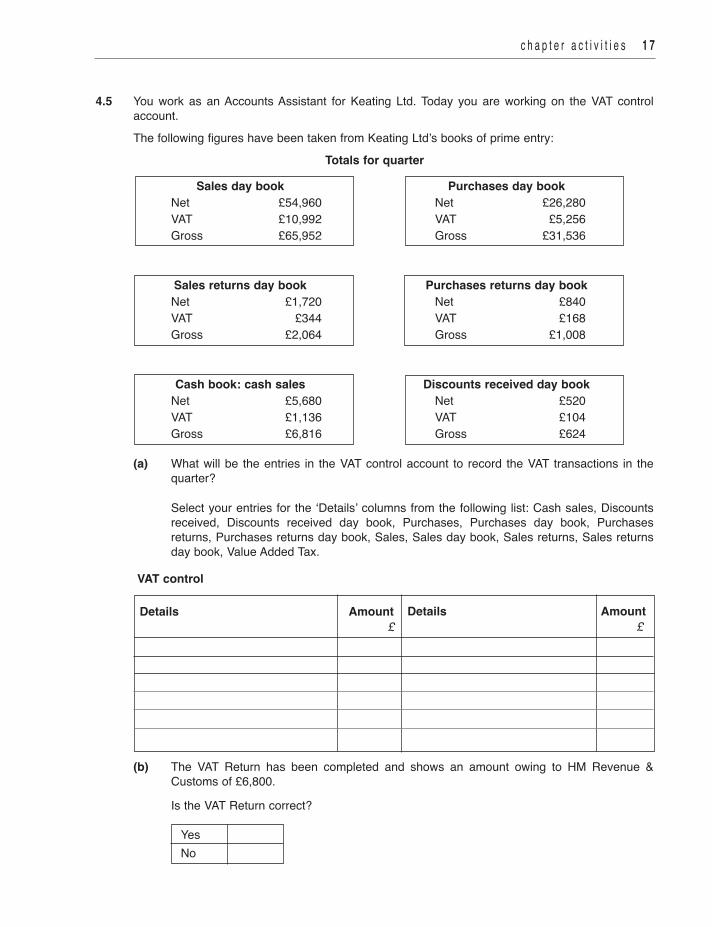

4.5 You work as an Accounts Assistant for Keating Ltd. Today you are working on the VAT controlaccount.The following figures have been taken from Keating Ltd’s books of prime entry:

Totals for quarter

Sales day book Purchases day book Net £54,960 Net £26,280 VAT £10,992 VAT £5,256 Gross £65,952 Gross £31,536

Sales returns day book Purchases returns day book Net £1,720 Net £840 VAT £344 VAT £168 Gross £2,064 Gross £1,008

Cash book: cash sales Discounts received day book Net £5,680 Net £520 VAT £1,136 VAT £104 Gross £6,816 Gross £624

(a) What will be the entries in the VAT control account to record the VAT transactions in thequarter?

Select your entries for the ‘Details’ columns from the following list: Cash sales, Discountsreceived, Discounts received day book, Purchases, Purchases day book, Purchasesreturns, Purchases returns day book, Sales, Sales day book, Sales returns, Sales returnsday book, Value Added Tax.

(b) The VAT Return has been completed and shows an amount owing to HM Revenue &Customs of £6,800.

Is the VAT Return correct? Yes

No

VAT control

Details Amount £

Details Amount £

1 8 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

5.2 Heather Shaw started in business on 1 June 20-8 with the following assets and liabilities: £ Office equipment 10,500 Inventory 3,300 Cash 200 Bank 1,400 Trade payable 1,700 Bank loan 2,500Use the form below to prepare Helen Shaw’s opening journal entry, showing clearly her capital at1 June 20-8.

Date Details Reference Dr Cr 20-8 £ £

5.1 Which one of the following transactions will be recorded in the journal?

(a) Bank payment to a supplier

(b) Sale of goods on credit

(c) Petty cash payment for stationery

(d) Writing off an irrecoverable debt

The journal5

c h a p t e r a c t i v i t i e s 1 9

5.3 You are employed by Teasdale Supplies as an Accounts Assistant. Today the Accounts Supervisortells you that a credit customer, Hinson Haulage, has ceased trading, owing Teasdale Supplies£440 plus VAT.

(a) Record the journal entries needed in the general ledger to write off the net amount and theVAT.

Select your account names from the following list: Irrecoverable debts, Hinson Haulage,Purchases, Purchases ledger control, Teasdale Supplies, Sales, Sales ledger control, ValueAdded Tax.

Account name Amount Debit Credit £

(b) Teasdale Supplies has started a new business, Teasdale Developments, and a new set ofaccounts is to be opened. A partially completed journal to record the opening entries isshown below.

Record the journal entries needed in the accounts in the general ledger of TeasdaleDevelopments to deal with the opening entries.

Account name Amount Debit Credit £ Inventory 3,412 Office equipment 15,200 Cash at bank 1,874 Sales ledger control 11,391 Purchases ledger control 6,987 Rent 5,310 Heating and lighting 846 Wages 4,105 Bank loan 10,600 Capital 24,551

Journal to record the opening entries of the new business

2 0 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

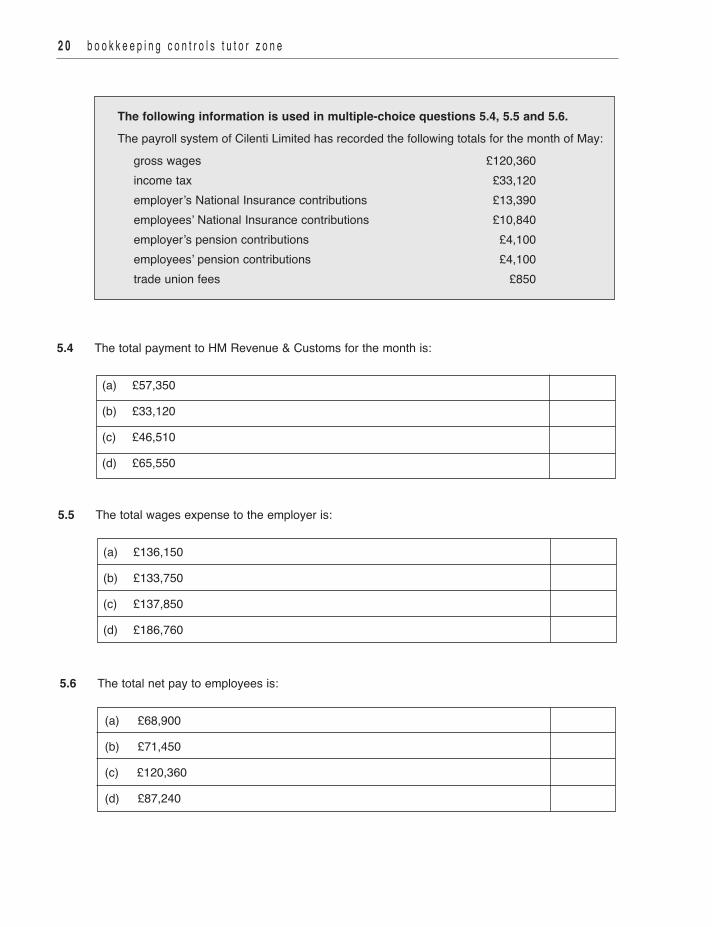

The following information is used in multiple-choice questions 5.4, 5.5 and 5.6. The payroll system of Cilenti Limited has recorded the following totals for the month of May: gross wages £120,360

income tax £33,120 employer’s National Insurance contributions £13,390 employees’ National Insurance contributions £10,840 employer’s pension contributions £4,100 employees’ pension contributions £4,100 trade union fees £850

5.4 The total payment to HM Revenue & Customs for the month is:

(a) £57,350

(b) £33,120

(c) £46,510

(d) £65,550

5.5 The total wages expense to the employer is:

(a) £136,150

(b) £133,750

(c) £137,850

(d) £186,760

5.6 The total net pay to employees is:

(a) £68,900

(b) £71,450

(c) £120,360

(d) £87,240

c h a p t e r a c t i v i t i e s 2 1

5.7 You are employed by Lockton Limited as an Accounts Assistant. Lockton Limited pays its employees through the bank every month and maintains a wages control

account. A summary of last month’s payroll transactions is shown below.

Item £ Gross wages 45,833 Income tax 6,987 Employer's National Insurance contributions 2,045 Employees’ National Insurance contributions 1,822 Employer’s pension contributions 953 Employees’ pension contributions 953

Record the journal entries needed in the general ledger to: (a) Record the wages expense. (b) Record HM Revenue & Customs liability. (c) Record the net wages paid to the employees. (d) Record the pension fund liability.

Select your account names from the following list: Bank, Employees’ National Insurance,Employer’s National Insurance, HM Revenue & Customs, Income tax, Net wages, Pension fund,Wages control, Wages expense.

(a) Account name Amount Debit Credit £

(b) Account name Amount Debit Credit £

2 2 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

(c) Account name Amount Debit Credit £

(d) Account name Amount Debit Credit £

c h a p t e r a c t i v i t i e s 2 3

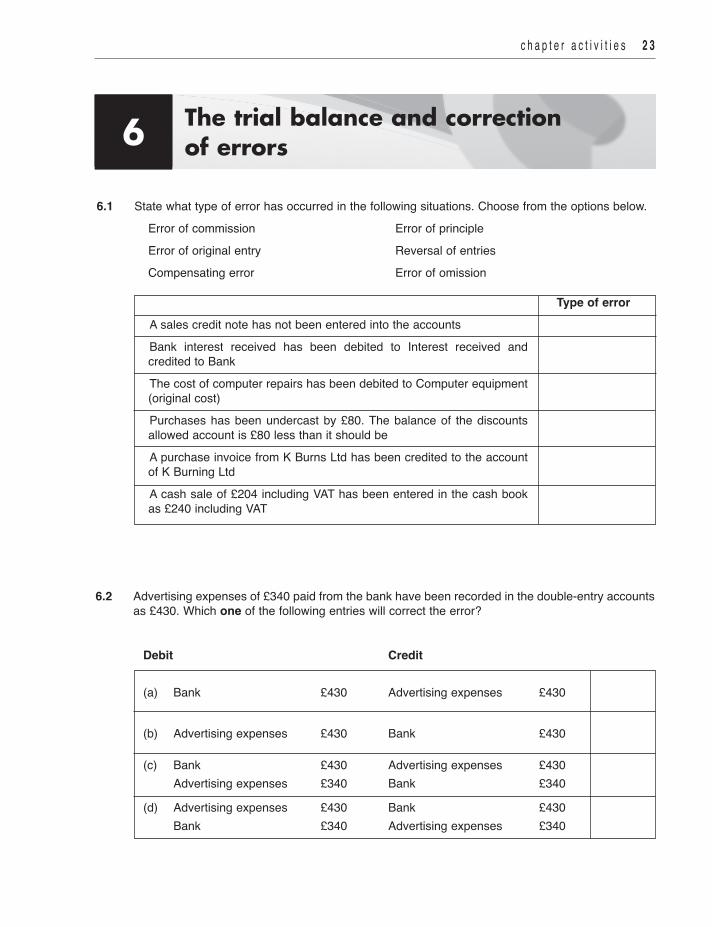

6.2 Advertising expenses of £340 paid from the bank have been recorded in the double-entry accountsas £430. Which one of the following entries will correct the error?

Debit Credit

(a) Bank £430 Advertising expenses £430

(b) Advertising expenses £430 Bank £430

(c) Bank £430 Advertising expenses £430 Advertising expenses £340 Bank £340

(d) Advertising expenses £430 Bank £430 Bank £340 Advertising expenses £340

6.1 State what type of error has occurred in the following situations. Choose from the options below.Error of commission Error of principleError of original entry Reversal of entriesCompensating error Error of omission

Type of errorA sales credit note has not been entered into the accountsBank interest received has been debited to Interest received andcredited to BankThe cost of computer repairs has been debited to Computer equipment(original cost)Purchases has been undercast by £80. The balance of the discountsallowed account is £80 less than it should beA purchase invoice from K Burns Ltd has been credited to the accountof K Burning LtdA cash sale of £204 including VAT has been entered in the cash bookas £240 including VAT

The trial balance and correction of errors6

2 4 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

6.3 (a) The trial balance of Sampson Storage does not balance. The debit column totals £148,374 and the credit column totals £149,521.

What entry will be made in the suspense account to balance the trial balance?

Account name Amount Debit Credit £ Suspense

(b) It is important to understand the type of errors that are disclosed by a trial balance and those that are not.

Show whether the errors below cause an imbalance in the trial balance or not.

Error in the general ledger Error causes Error does NOT an imbalance cause an imbalance The cost of stationery has been debited to office equipment account and debited to bank account

A cash sale has been recorded in the cash book only

A bank payment for heating and lighting has been debited to bank account and credited to heating and lighting account

Rent paid of £540 has been recorded as £450 in the cash book and rent paid account

A bank payment for office equipment has not been entered in the accounts

The balance of sales ledger control account has been calculated incorrectly

c h a p t e r a c t i v i t i e s 2 5

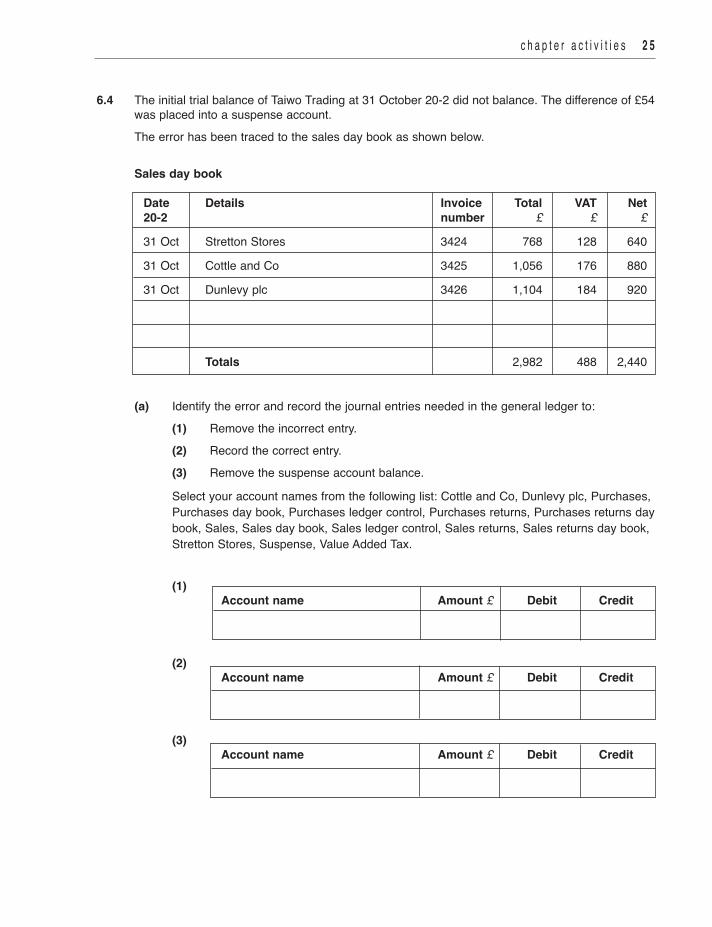

6.4 The initial trial balance of Taiwo Trading at 31 October 20-2 did not balance. The difference of £54was placed into a suspense account.

The error has been traced to the sales day book as shown below.

Sales day book

Date Details Invoice Total VAT Net 20-2 number £ £ £ 31 Oct Stretton Stores 3424 768 128 640

31 Oct Cottle and Co 3425 1,056 176 880

31 Oct Dunlevy plc 3426 1,104 184 920

Totals 2,982 488 2,440

(a) Identify the error and record the journal entries needed in the general ledger to: (1) Remove the incorrect entry. (2) Record the correct entry. (3) Remove the suspense account balance. Select your account names from the following list: Cottle and Co, Dunlevy plc, Purchases,

Purchases day book, Purchases ledger control, Purchases returns, Purchases returns day book, Sales, Sales day book, Sales ledger control, Sales returns, Sales returns day book, Stretton Stores, Suspense, Value Added Tax.

(1) Account name Amount £ Debit Credit

(2) Account name Amount £ Debit Credit

(3) Account name Amount £ Debit Credit

2 6 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

An entry to record a bank receipt of £350 for rent received has been reversed.

(b) Record the journal entries needed in the general ledger to: (1) Remove the incorrect entry. (2) Record the correct entry. Select your account names from the following list: Bank, Cash, Purchases, Purchases

ledger control, Rent received, Sales, Sales ledger control, Suspense, Value Added Tax.

(1) Account name Amount £ Debit Credit

(2) Account name Amount £ Debit Credit

c h a p t e r a c t i v i t i e s 2 7

6.5 The trial balance of Lorenz and Co included a suspense account. All the bookkeeping errors havenow been traced and the journal entries shown below have been prepared.

Journal entries

Account name Debit Credit £ £ Wages 195 Suspense 195

Suspense 425 Sales 425

Vehicle expenses 80 Vehicles 80

As the Accounts Assistant at Lorenz and Co, you are to post the journal entries to the generalledger accounts. Dates are not required.

Select your entries for the ‘Details’ columns from the following list: Balance b/f, Sales, Suspense,Vehicle expenses, Vehicles, Wages.

SalesDetails Amount £ Details Amount £

SuspenseDetails Amount £ Details Amount £

Balance b/f 230

2 8 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Vehicle expensesDetails Amount £ Details Amount £

VehiclesDetails Amount £ Details Amount £

WagesDetails Amount £ Details Amount £

c h a p t e r a c t i v i t i e s 2 9

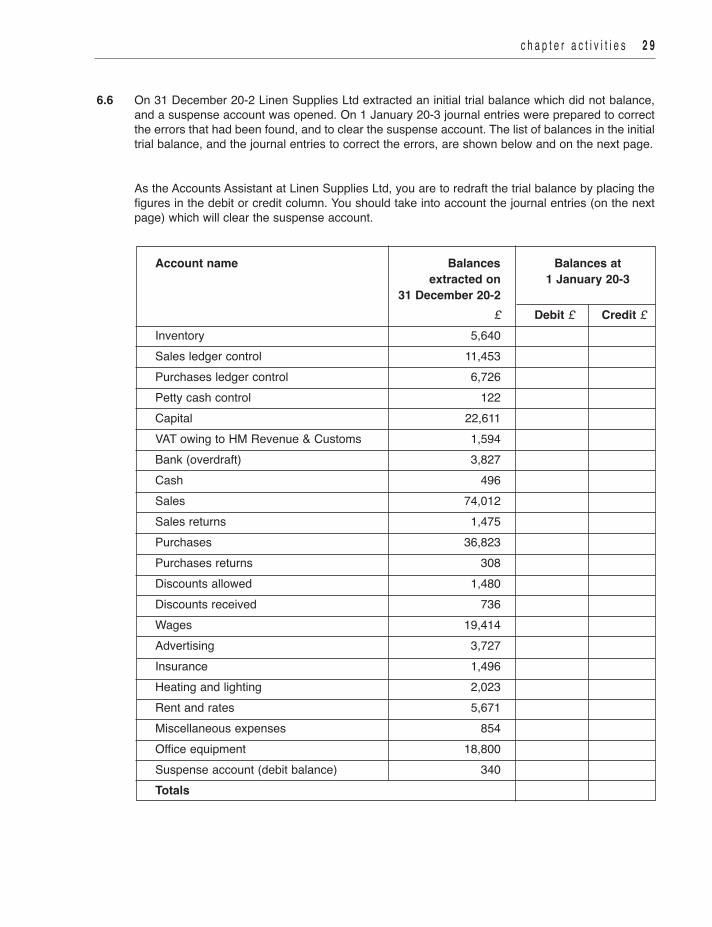

6.6 On 31 December 20-2 Linen Supplies Ltd extracted an initial trial balance which did not balance,and a suspense account was opened. On 1 January 20-3 journal entries were prepared to correctthe errors that had been found, and to clear the suspense account. The list of balances in the initialtrial balance, and the journal entries to correct the errors, are shown below and on the next page.

As the Accounts Assistant at Linen Supplies Ltd, you are to redraft the trial balance by placing thefigures in the debit or credit column. You should take into account the journal entries (on the nextpage) which will clear the suspense account.

Account name Balances Balances at extracted on 1 January 20-3 31 December 20-2 £ Debit £ Credit £ Inventory 5,640 Sales ledger control 11,453 Purchases ledger control 6,726 Petty cash control 122 Capital 22,611 VAT owing to HM Revenue & Customs 1,594 Bank (overdraft) 3,827 Cash 496 Sales 74,012 Sales returns 1,475 Purchases 36,823 Purchases returns 308 Discounts allowed 1,480 Discounts received 736 Wages 19,414 Advertising 3,727 Insurance 1,496 Heating and lighting 2,023 Rent and rates 5,671 Miscellaneous expenses 854 Office equipment 18,800 Suspense account (debit balance) 340 Totals

3 0 b o o k k e e p i n g c o n t r o l s t u t o r z o n e

Journal entries

Account name Debit Credit £ £ Suspense 350 Sales 350

Account name Debit Credit £ £ Suspense 450 Rent and rates 450 Rent and rates 540 Suspense 540

Account name Debit Credit £ £ Office equipment 600 Suspense 600