bookkeeper business blueprint...

TRANSCRIPT

Bookkeeper Business BlueprintBookkeeping Knowledge - Module 4

Introduction, Recap & Preview

Welcome!

Knowledge Module 3 Review● Debits & Credits Deep Dive

● Balance Sheet: Current Assets

● Professional Ethics

● Application: Bank (Cash) Reconciliation (Module 3.5)

Knowledge Module 4 Review

● Accrual v. Cash Basis of Accounting● Bookkeeping / Accounting Principles● Fixed Assets & Goodwill (not the thrift store)● Depreciation & Amortization● Other Assets● Adjusting Journal Entries (AJEs)● Discuss Module 4.5 (Application)

Routine Bookkeeping & Accounting Transactions

Financial Statements

Financial Analysis & Interpretation

Advice that makes $ and/or

saves time

Cover thru M8 & Bonus Training

Cover Modules 9-10 & Bonus Training

Bookkeeper Business BlueprintBookkeeping Knowledge - Module 4

Lesson 1: Accrual v. Cash Basis Accounting

Accrual vs. Cash Basis Accounting

● think Hatfields vs. McCoys ● Accrual basis is ‘preferred’ ● All formal reporting is accrual basis● Generally Accepted Accounting Principles

(GAAP) requires accrual basis to be used● However, lots of small businesses want

cash basis accounting

Accrual vs. Cash Main Differences

● Revenues & Receivables● Expenses & Payables● Net Income

Use Accrual Basis and Rely on Statement of Cash Flows

● Better overall understanding● Makes for better planning● Brings out the strengths of both bases

Bookkeeper Business BlueprintBookkeeping Knowledge - Module 4Lesson 2: Bookkeeping Principles

Bookkeeping / Accounting Principles

● The foundation of financial accounting

● The nerdy ~ but needed ~ bookkeeping rules which all businesses must follow

● In order to be a great bookkeeper, you need to understand these...

Bookkeeping PrinciplesIn order for financial accounting / statements to be useful, they must be:● accurate● credible● timely● easy to understand● easy to compare with other companies (think f/s

presentation)

Financial Accounting

● this process keeps up with and tracks your clients transactions

● financial transactions are recorded, summarized & presented in a financial statement and / or report

2 Uses of Financial Statements:

● Internal Use (most common use)

● External Use (be on high-alert)

Examples of External Users:● Banks● Stockholders● Insurance companies● Bonding companies● Government agencies● Some clients (the Wal-Mart syndrome)

If Usage of F/S is External:

● Must conform to Generally Accepted Accounting Principles (GAAP)

● Accrual basis = GAAP● Cash basis = departure from GAAP● Remember the differences between

accrual and cash

If Usage of F/S is External:

● Remember the differences between accrual and cash

● Following accrual basis presents your client’s profits, assets, liabilities, equity & other financial info in line with economic reality

● No la-la land bookkeeping

Bookkeeper Business BlueprintBookkeeping Knowledge - Module 4Lesson 3: Fixed Assets, Goodwill /

Depreciation & Amortization

Fixed Assets, Depreciation & Amortization

● Fixed Assets (FAs): “things” with a useful life >1 year● Buildings, land, equipment, computers, vehicles,

improvements, goodwill are some examples● FAs are reported at cost on the balance sheet● FAs costs need to be spread over the pre-

determined useful life of the asset● “Helpful” tool from the IRS: Publication 946 (http:

//www.irs.gov/pub/irs-pdf/p946.pdf)

Fixed Assets, Depreciation & Amortization

● Book depreciation vs. tax depreciation● Who maintains the depreciation schedules?● Two main styles of depreciation: straight-line and

accelerated● Straight-line spreads the depreciation expense of the

fixed asset evenly over time● Accelerated depreciation places more depreciation

expense in the earlier time periods as opposed to evenly

Fixed Assets, Depreciation & Amortization

● IMPORTANT: using straight-line or accelerated only represents a timing difference of when depreciation expense is recorded

● Depreciation is for hard assets (touchy-feely)● Amortization is for soft assets (non-touch-feely such

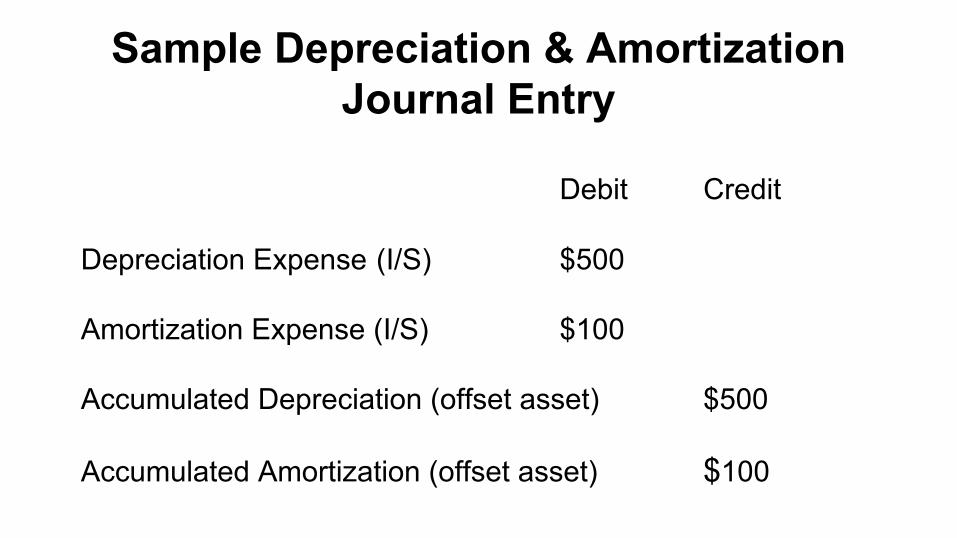

as Goodwill, Covenant Not to Compete, etc.)● Only way to record depreciation & amortization is via

a ???

Sample Depreciation & Amortization Journal Entry

Debit Credit

Depreciation Expense (I/S) $500

Amortization Expense (I/S) $100

Accumulated Depreciation (offset asset) $500

Accumulated Amortization (offset asset) $100

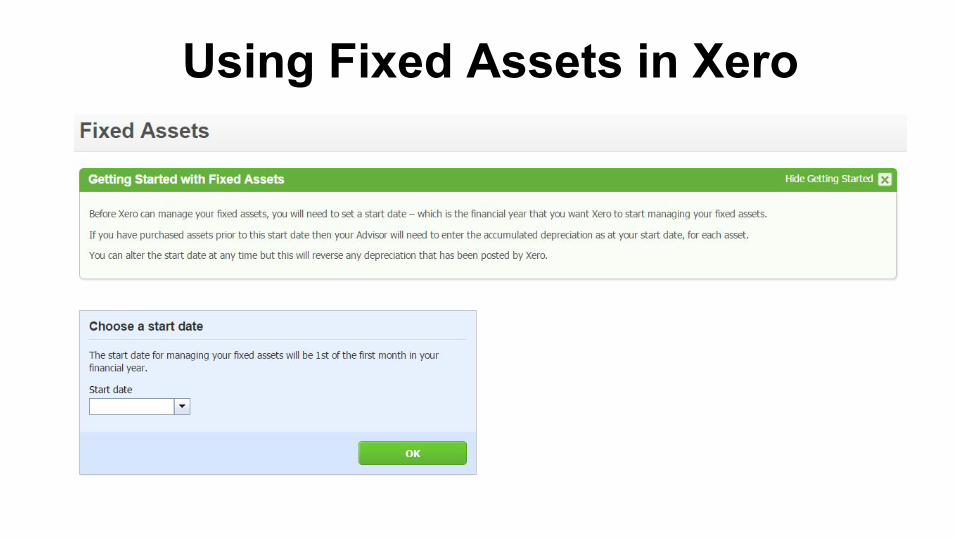

Using Fixed Assets in Xero

Bookkeeper Business BlueprintBookkeeping Knowledge - Module 4

Lesson 4: Other Assets

Other Assets● Any asset with a useful life >1 year not otherwise

classified

● Most common one you will see are deposits for rent, utilities, etc.

● For the clients you serve, this shouldn’t be a high dollar amount category on the balance sheet

Bookkeeper Business BlueprintBookkeeping Knowledge - Module 4Lesson 5: Adjusting Journal Entries

(AJEs)

Adjusting Journal Entries● Think of this like a diary - it doesn’t make things

happen; it simply records what happens.

● Most common use of Adjusting Journal Entries (AJEs) is to CONVERT a company’s accounting records to the accrual basis.

● Typically made just before financial statements are issued.

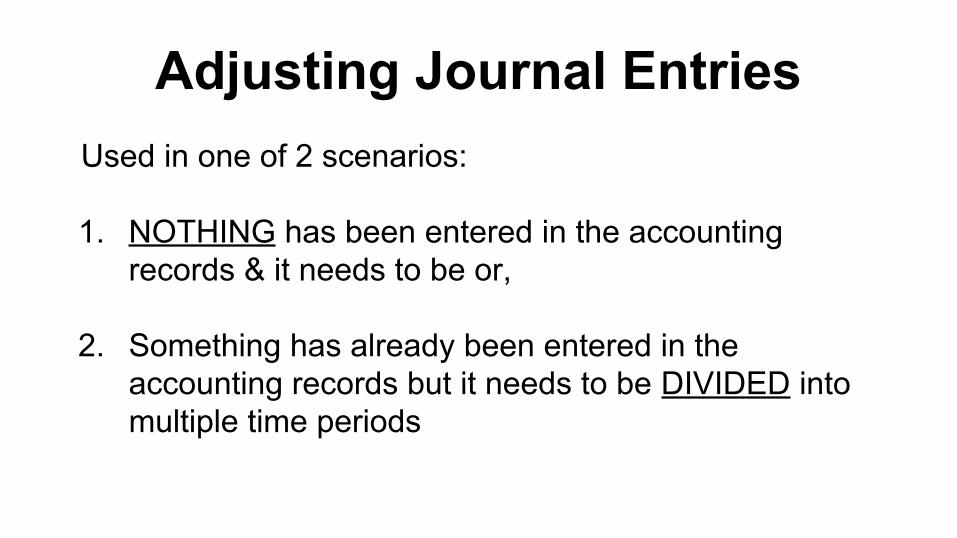

Adjusting Journal EntriesUsed in one of 2 scenarios:

1. NOTHING has been entered in the accounting records & it needs to be or,

2. Something has already been entered in the accounting records but it needs to be DIVIDED into multiple time periods

Examples of AJEs● Most common one YOU will use is depreciation.

● Depreciation records the gradual deterioration of assets that have a useful life of more than one year (think: equipment)

● Since NOTHING has been entered in the accounting records for depreciation (you don’t have a monthly depreciation “bill”) you enter this as a journal entry

Examples of AJEs● Assume we buy a piece of equipment for $6,000.● It has a useful life of 5 years / 60 months.

$6,000 / 60 months = $100 in depreciation per month to record or $1,200 per year.

The only way to record is by AJE:

Debit CreditDepreciation (expense) $100Accumulated Depreciation (asset) $100

Examples of AJEs● Client pays $1,200 for insurance premium covering 12 months● This represents prepaid insurance that is an asset● The cost needs to be DIVIDED over time

$1,200 / 12 months = $100 in cost per month to recordThe only way to record is by AJE:

Debit CreditInsurance (expense) $100Prepaid Insurance (asset) $100

Examples of AJEs● Customer of your client pays for a 6-month subscription● Pays $60 for 6 months● The income needs to be DIVIDED over time

$60 / 6 months = $10 in income per month to recordThe only way to record is by AJE:

Debit CreditSubscription Revenue (income) $10Unearned Revenue (liability) $10

Adjusting Journal Entries

Almost always involve at least:

● one balance sheet account

● one income statement account

Adjusting Journal Entries

● as with every accounting entry, the debits = credits

● every AJE affects 2 or more accounts