board meeting agenda october 20 ... - schaumburg, il | home

TRANSCRIPT

SCHAUMBURG POLICE PENSION FUND 1000 W. Schaumburg Rd Schaumburg, IL 60194

BOARD MEETING AGENDA

October 20, 2020

3:00 pm CALL TO ORDER: NEW BUSINESS: 1. Approval of Minutes – August 18, 2020 2. Report of the Treasurer 3. Schaumburg Police Pension Fund Actuarial Valuation Report 4. Assignment of Advisory Agreement to Mission Wealth Management, LP. 5. Report of the Financial Consultant – AHC Advisors 6. Application for Retirement Benefits – Peter Scarpa 7. Purchase of Suspension Time – Pete Castritsis 8. Request for Pension Contribution Refund – Anabel Rangel 9. Request for Pension Contribution Refund – Victoria Gwizdak 10. Lauterbach & Amen Proposal OLD BUSINESS: 1. O’Connor Disability 2. McIntyre Disability 3. Affidavits of Continued Eligibility BILLS AND DISBURSEMENTS: 1. Kathryn Strack – $180.00 (Secretarial services) 2. Collins & Radja - $1,250.00 (Oct, Nov, & Dec retainer) 3. Collins & Radja - $3,000.00 (O’Connor disability) 4. Marianne Climack Court Reporting – $584.25 (O’Connor disability) 5. Marianne Climack Court Reporting – $121.00 (O’Connor disability) 6. Richard P. Harris, M.D. - $4,320.00 (McIntyre disability) 7. INSPE Associates - $4,590.00 (McIntyre disability) 8. INSPE Associates - $4,725.00 (McIntyre disability) 9. Nyhart - $5,500.00 (2020 Pension Funding and GASB Valuations) EXECUTIVE SESSION – 5 ILCS 120/2 … AUDIENCE COMMENTS: BOARD MEMBER COMMENTS AND MENTIONS: NEXT PENSION BOARD MEETING: December 15, 2020 ADJOURNMENT:

SCHAUMBURG POLICE PENSION FUND 1000 W. Schaumburg Rd Schaumburg, IL 60194

Page 1 of 7

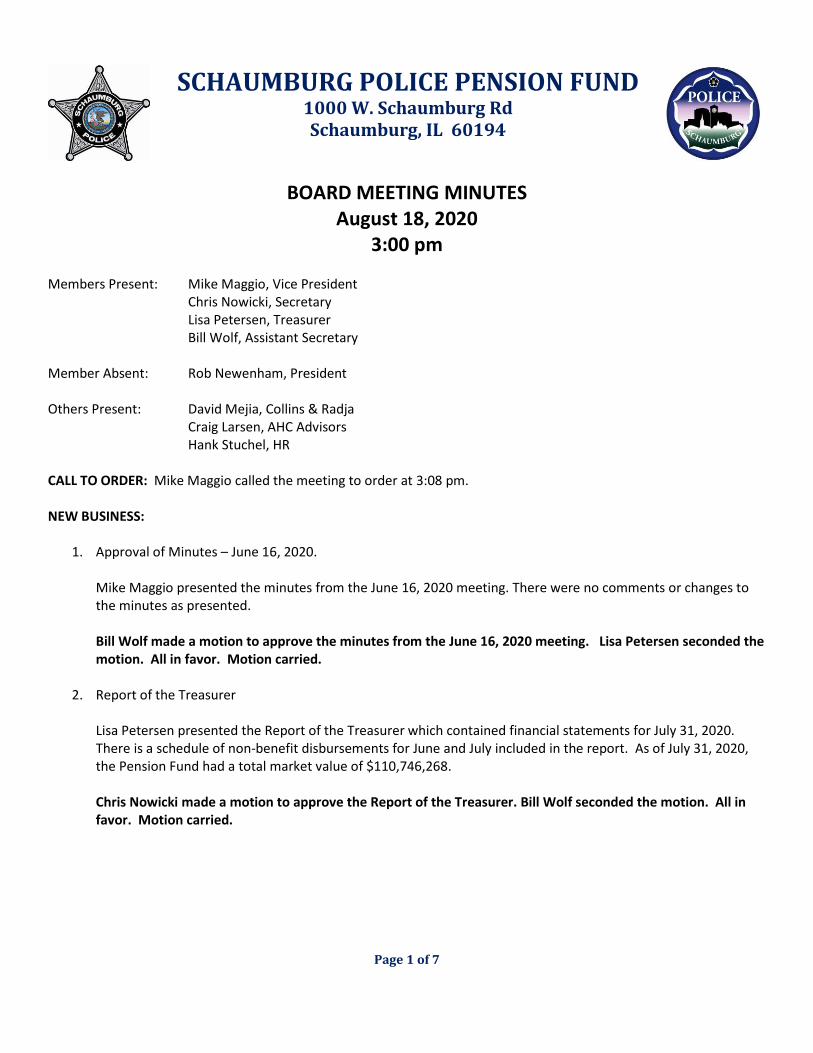

BOARD MEETING MINUTES August 18, 2020

3:00 pm Members Present: Member Absent:

Mike Maggio, Vice President Chris Nowicki, Secretary Lisa Petersen, Treasurer Bill Wolf, Assistant Secretary Rob Newenham, President

Others Present: David Mejia, Collins & Radja

Craig Larsen, AHC Advisors Hank Stuchel, HR

CALL TO ORDER: Mike Maggio called the meeting to order at 3:08 pm. NEW BUSINESS:

1. Approval of Minutes – June 16, 2020.

Mike Maggio presented the minutes from the June 16, 2020 meeting. There were no comments or changes to the minutes as presented. Bill Wolf made a motion to approve the minutes from the June 16, 2020 meeting. Lisa Petersen seconded the motion. All in favor. Motion carried.

2. Report of the Treasurer

Lisa Petersen presented the Report of the Treasurer which contained financial statements for July 31, 2020. There is a schedule of non-benefit disbursements for June and July included in the report. As of July 31, 2020, the Pension Fund had a total market value of $110,746,268.

Chris Nowicki made a motion to approve the Report of the Treasurer. Bill Wolf seconded the motion. All in favor. Motion carried.

SCHAUMBURG POLICE PENSION FUND 1000 W. Schaumburg Rd Schaumburg, IL 60194

Page 2 of 7

3. Report of Financial Consultant – AHC Advisors

At the end of June 2020 the value of the pension fund was up over $10 million just since the end of March. At

the end of the second quarter, the fund was up over 13% YTD and as of July 31 the fund was positive over the

last 12 months. Both Galliard and Segall, Bryant & Hamill are up this year.

Looking at the stock market as a whole, the S&P 500 was up 7.5% but outside of that there were negative

returns across the board. We have a narrowly focused strong recovery for parts of the market because the S&P

500 is made up of 500 stocks, and five of those stocks-Apple, Microsoft, Google, Facebook, and Amazon-

account for 20% of that index. Which means, just those five stocks determine 20% of the overall return of the

index. A small number of stocks are dominating and they are the reason the S&P 500 was positive while the rest

of the market was negative. We should not expect that to continue. These companies will start to trail and the

rest of the market will catch up. The last time there was a strong tech surge in the late 90s, the top five stocks

did not give us the same overall market capitalization as these five. We’re in uncharted territory because these

five stocks are all benefitting from the pandemic.

Other important data to look at to get a better picture of the state of the economy is unemployment. Initial

unemployment claims shows us how many people filed for unemployment for the first time in the preceding

week. Before the shutdown, there were about 200K unemployment claims a week; by the third week in March

there were 6.9 claims. Initial unemployment claims have dropped sharply to 963K this week. The next piece of

data to look at is continued unemployment claims, which is a clearer indicator of unemployment because it

tracks how many people continue to be out of work. The week before the pandemic there were 1.8 million

continued unemployment claims, 25 million the week after. Since then, roughly 9.5 million people have come

back into the work force and there are still 14 million more continued unemployment claims than there were

before the pandemic. High continued unemployment claims mean that there are a lot more people who will not

be spending money the way they generally do, which affect5s the overall economy. It’s also important to note

that the extra $600/week unemployment insurance people were receiving expired at the end of July. With those

extra funds many people were making more money on unemployment when they were working, Craig expects

unemployment claims to fall now that this incentive is gone as people will be more willing to go back to work.

Lisa asked if retirements were factored in these numbers or if the shutdown is in anyway causing people to

retire. Craig said not really because people who were going to retire anyway can just stay on and push back their

retirement, we wouldn’t know.

Craig advised that the decline we had in 2020 did not compare to what we had in early 2000s and that in the

grand scheme of things this decline isn’t much different from what we’ve seen in the past. The big difference is

the cause, because normally the causes are economic. This was a different kind of correction and recovery, but it

matches what we’ve seen before and we will see it again, but he does think that preventing another pandemic

SCHAUMBURG POLICE PENSION FUND 1000 W. Schaumburg Rd Schaumburg, IL 60194

Page 3 of 7

will be a much bigger priority for many people. Many people question why are we seeing record highs, and Craig

said that because long term we’re going to be ok.

Gross domestic product in Q1 was down 5% which is the largest decline since the 2008 financial crisis. Q2 we

saw it down almost 33%. That is the largest quarterly decline we have ever experienced because it was an

abrupt stop to the economy. The expectation is that Q3 may see a positive return, likely a 20% number or

higher. Economic activity has picked up sharply, so we will likely see historic gains. It won’t be a positive 33%

growth and we will likely have negative growth for the year. But there will be a big bounce back.

Craig then turned to our current allocations. At the end of Q2, the fund was at 36% bonds and it is currently

sitting at about 32% because our equity portfolio has grown so substantially. At the end of Q2, the fund’s equity

holdings market value was just over $70 million which is a huge recovery from the previous quarter ($53.1

million for Q1). As of yesterday it had a value of $76.6 million which is the largest swing/snapback Craig has seen

in a long time.

The equity allocation is just about 67% of the fund value as of yesterday. Our target allocation is 63% and our

rebalance threshold is 68%. We’re almost at the point where we would need to have a discussion regarding

rebalancing but we also need to raise some cash so we need to rebalance now. Lisa has advised that tax revenue

is slower coming in this year because of delays being granted by the county. The fund will need $2 million dollars

soon anyway to carry us through to the end of the year.

We have two options:

1) A standard rebalance which looks at holdings and raises money from the asset class that is over allocated. If

we go with that option, the funds would come from our equity which is currently at 67%, about 4% over

target.

2) If we prefer to keep holdings in stocks until we reach the 68% threshold for rebalancing, we could take the

money from the bond side. Because we’ve seen such volatility and so much movement in the market, some

funds are trying to hold more funds in stocks to see a higher return.

Bill Wolf asked Craig if he would describe a standard rebalance as more conservative/more of a safe approach.

Craig responded that since you would be removing money from the part of your portfolio that has more risk, it

would reduce the risk of the portfolio.

Mike Maggio asked if we should be factoring in the election in our decision making. If we can wait and see. Craig

said that was a good question but at the end of the day political events are a coin flip. In terms both for who will

win and how the market reacts. Long term, it doesn’t really matter and we will be ok but we cannot wait until

after the election (or the October board meeting) to vote on it because we need $2 million by the end of

September to keep us from going negative because tax revenues are late coming in.

SCHAUMBURG POLICE PENSION FUND 1000 W. Schaumburg Rd Schaumburg, IL 60194

Page 4 of 7

Chris Nowicki suggested that we take it from stocks, lock in the profits we made in the last quarter and lower

our allocations on that side. It would minimize the steps we will have to take to rebalance eventually anyway.

Everyone agreed on this more conservative approach. At the next meeting, Craig can give us the dollar value of

what was added to our bottom line. He noted that we raise the money proportionally from ever single holding

to help balance. When we’re done, allocation will be very close to target.

Craig’s final take away was that we will continue to see volatility in the market, don’t know which way it will go

but with the pandemic and the election we’re bound to see more movement.

Lisa Petersen made a motion to raise $2 million from the equity portfolio to raise cash to cover expenses.

Chris Nowicki seconded the motion.

Roll Call Vote: Bill Wolf Yes Lisa Petersen Yes Chris Nowicki Yes Mike Maggio Yes

Motion carried. Going forward we will use Zoom for our meetings with Craig so that he can share his screen to ensure everyone can follow along. Craig is keeping his office closed for the foreseeable future.

Chris Nowicki made a motion to approve the AHC Advisors report. Lisa Petersen seconded the motion. All in favor. Motion carried.

4. Application for Survivor Benefits- Shirley Alley

Mike Maggio presented the Application for Survivor Benefits for Shirley Alley and the associated worksheets. Chris Nowicki advised he will reach out to Shirley to ensure all necessary documents are provided.

Bill Wolf made a motion to approve the application for survivor benefits for Shirley Alley. Chris Nowicki seconded the motion. All in favor. Motion Carried.

5. Request for Pension Contribution Refund

Mike Maggio presented the Request for pension contribution refund for Eric Gonzales and the associated worksheets for the amount of $4,127.88. Chris Nowicki made a motion to approve the refund request. Bill Wolf seconded the motion. Roll Call Vote: Bill Wolf Yes

Lisa Petersen Yes

SCHAUMBURG POLICE PENSION FUND 1000 W. Schaumburg Rd Schaumburg, IL 60194

Page 5 of 7

Chris Nowicki Yes Mike Maggio Yes

Motion carried.

OLD BUSINESS:

1. O’Connor Disability

Depositions have been scheduled for all four physicians:

Dr. Levin on August 19,

Dr. Forsythe on August 25

Dr. Succi on September 1

Dr. Petrucci on September 25

We will likely have all of these reports completed and returned to us in time for the October meeting and should be able to schedule a hearing at that time.

2. McIntyre Disability

McIntyre was seen by Dr. Harris on July 30, we have not received the report yet and Cary advised that these kinds of reports tend to take longer to complete. McIntyre also missed appointments with Dr. Whiney on July 20 and August 17, we are waiting to coordinate a new date. He did not show up for these pre-scheduled appointments, we do not pay for missed appointments. Dr. Agrawal is scheduled to see him on August 24. We likely will not have all necessary reports completed until after the October pension board meeting because these reports take so long to complete and because he has not been showing up to appointments. Scheduling these appointments has also been difficult because of Covid restrictions.

3. Affidavits of Continued Eligibility

Chris Nowicki advised he has received about 94 affidavits and that he will work directly with the rest of the people we need to respond.

BILLS AND DISBURSEMENTS:

1. Kathryn Strack- $120.00 (Secretarial services)

Lisa Petersen made a motion to pay Kathryn’s invoice. Chris Nowicki seconded the motion. Roll Call Vote: Bill Wolf Yes

Lisa Petersen Yes Chris Nowicki Yes Mike Maggio Yes

SCHAUMBURG POLICE PENSION FUND 1000 W. Schaumburg Rd Schaumburg, IL 60194

Page 6 of 7

Motion carried.

2. Collins & Radja- $1,250.00 (Quarterly Retainer)

Lisa Petersen made a motion to pay the Collins & Radja invoice. Bill Wolf seconded the motion. Roll Call Vote: Bill Wolf Yes

Lisa Petersen Yes Chris Nowicki Yes Mike Maggio Yes

Motion carried.

3. IPPAC- $500.00 (Annual Membership)

Cary Collins advised that IPPAC training will take place on August 3 at Judson University, 20 people can attend in person otherwise it is available via Zoom.

Bill Wolf made a motion to pay the Collins & Radja invoice. Chris Nowicki seconded the motion. Roll Call Vote: Bill Wolf Yes

Lisa Petersen Yes Chris Nowicki Yes Mike Maggio Yes

Motion carried.

EXECUTIVE SESSION – 5 ILCS 120/2 …:

AUDIENCE COMMENTS: BOARD MEMBER COMMENTS AND MENTIONS: Cary advised that every year in July we elect the President, Vice President, Secretary and Assistant Secretary and the board needs to do that today.

Mike Maggio made a motion to retain the existing slate of officers on the pension board. Chris Nowicki seconded the motion. All in favor. Motion Carried. Lisa Petersen advised that she received an email from Foster & Foster Actuaries and Consultants, hired by the consolidated pension of IL Police Officer pension investment fund to conduct and election of permanent trustees to be seated on January 1, 2021 and to provide names and addresses of eligible active members and

SCHAUMBURG POLICE PENSION FUND 1000 W. Schaumburg Rd Schaumburg, IL 60194

Page 7 of 7

retirees. Cary advised they would also be asking for email addresses, Lisa said she doesn’t believe we have those readily available. Cary advised the firefighters are going about consolidation in an entirely different way, and that he has also heard that there is a lawsuit being filed on the police side related to a conflict of interest. NEXT PENSION BOARD MEETING: October 20, 2020 at 3:00 pm. ADJORNMENT: Bill Wolf made a motion to adjourn. Lisa Petersen seconded the motion. All in favor. Motion

carried.

The meeting ended at 4:30 pm Submitted: Kathryn Strack Recording Secretary Approved: Mike Maggio Vice President Schaumburg Police Pension Fund

Village of Schaumburg Police Pension Fund

May 1, 2020 Actuarial Valuation Report

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 2

Table of Contents

Actuarial Certification 3

Executive Summary 5

Summary Results 5

Changes Since Prior Valuation and Key Notes 6

History of Valuation Results 7

Identification of Risks 8

Plan Maturity Measures 9

Assets and Liabilities 10

Present Value of Future Benefits 10

Funding Liabilities 11

Asset Information 12

Reconciliation of Gain/Loss 14

Contribution Requirements 15

Development of Funding Policy Contribution 15

Demographic Information 16

Participant Reconciliation 18

Plan Provisions 20

Actuarial Assumptions 23

Other Measurements 25

Minimum Contribution 26

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 3

Actuarial Certification

At the request of the plan sponsor, this report summarizes the Village of Schaumburg Police Pension Fund as of May 1, 2020 . The purpose of this report is to communicate the following results of the valuation:

• Funded Status; • Village Funding Policy Contribution; • Statutory Minimum Contribution;

This report has been prepared in accordance with the applicable Federal and State laws. Consequently, it may not be appropriate for other purposes. Please contact Nyhart prior to disclosing this report to any other party or relying on its content for any purpose other than that explained above. Failure to do so may result in misrepresentation or misinterpretation of this report.

The results in this report were prepared using information provided to us by other parties. The census information has been provided to us by the employer. Asset information has been provided to us by the administrator. We have reviewed the provided data for reasonableness when compared to prior information provided, but have not audited the data. Where relevant data may be missing, we have made assumptions we believe to be reasonable. We are not aware of any significant issues with and have relied on the data provided. Any errors in the data provided may result in a different result than those provided in this report. A summary of the data used in the valuation is included in this report.

The actuarial assumptions and methods were chosen by the employer. In our opinion, all actuarial assumptions and methods are individually reasonable and in combination represent our best estimate of anticipated experience of the plan. Future actuarial measurements may differ significantly from the current measurements presented in this report due to such factors as the following:

• plan experience differing from that anticipated by the economic or demographic assumptions; • changes in economic or demographic assumptions; • increases or decreases expected as part of the natural operation of the methodology used for these measurements (such as the end of an amortization period); and • changes in plan provisions or applicable law. We did not perform an analysis of the potential range of future measurements due to the limited scope of our engagement. This report has been prepared in accordance with generally accepted actuarial principles and practice. Neither Nyhart nor any of its employees have any relationship with the plan or its sponsor which could impair or appear to impair the objectivity of this report. To the extent that this report or any attachment concerns tax matters, it is not intended to be used and cannot be used by a taxpayer for the purpose of avoiding penalties that may be imposed by law.

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 4

Actuarial Certification

The undersigned are compliant with the continuing education requirements of the Qualification Standards for Actuaries Issuing Statements of Actuarial Opinion in the United States and are available for any questions.

Nyhart

______________________________________ Michael Zurek, EA, FCA, MAAA September 1, 2020 Date

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 5

Executive Summary

Summary Results The actuarial valuation’s primary purpose is to produce a scorecard measure displaying the funding progress of the plan toward the ultimate goal of paying benefits at retirement. The Accrued Liability is based on the Projected Unit Credit actuarial cost method.

May 1, 2019 May 1, 2020 Funded Status Measures

Accrued Liability $ 185,576,620 $ 191,627,209

Actuarial Value of Assets 116,887,334 116,192,898

Unfunded Accrued Liability $ 68,689,286 $ 75,434,311

Funded Percentage (AVA) 63.0% 60.6%

Funded percentage (MVA) 60.6% 52.9%

Cost Measures

Total Funding Policy Pension Contribution $ 6,363,567 $ 6,844,535

Expected Employee Contributions (1,171,790) (1,170,887)

Net Village Funding Policy Contribution $ 5,191,777 $ 5,673,648

- as a Percentage of Payroll 46.5% 51.4%

Asset Measures

Market Value of Assets (MVA)

$ 112,429,731 $ 101,438,404

Actuarial Value of Assets (AVA) $ 116,887,334 $ 116,192,898

Actuarial Value/Market Value 104.0% 114.5%

Participant Information

Active Participants 111 110

Terminated Vested Participants 11 17

Retirees, Beneficiaries, and Disabled Participants 117 126

Total 239 253

Payroll $ 11,171,006 $ 11,042,252

57.7% 60.3% 62.5% 63.0% 60.6%

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

History of Funded Ratio

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 6

Executive Summary

Changes since Prior Valuation and Key Notes

The Tier II benefit changes effective January 1, 2020 under Illinois Public Act 101-610 are included in the valuation. The changes result in an increase in benefit obligations and an increase in the recommended contribution.

The mortality improvement scale was updated from Scale MP-2018 to Scale MP-2019, and mortality improvements were projected an additional year, to 2020. The change resulted in a decrease in benefit obligations and in the recommended contribution.

Actual spouse information was provided for Retired and Disabled members in 2020. In prior years, 80% of members were assumed married with female spouses 3 years younger than males. The married assumption still applies to active members. The change results in a decrease in benefit obligations and a decrease in the recommended contribution.

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 7

Executive Summary

History of Valuation Results

5/1/2016 5/1/2017 5/1/2018 5/1/2019 5/1/2020

Plan Funding

Accrued Liability $ 179,336,949 $ 180,456,944 $ 181,948,768 $ 185,576,620 $ 191,627,209 Actuarial Value of Assets 103,537,317 108,881,793 113,632,166 116,887,334 116,192,898 Unfunded Accrued Liability $ 75,799,632 $ 71,575,151 $ 68,316,602 $ 68,689,286 $ 75,434,311 Funded Percentage 57.7% 60.3% 62.5% 63.0% 60.6% Normal Cost (NC) $ 3,110,775 $ 3,191,280 $ 2,864,642 $ 2,638,485 $ 2,553,856 NC as a Percent of Covered Payroll 30.0% 29.4% 26.4% 23.6% 23.1%

Actual Contribution $ 5,179,593 $ 5,471,525 $ 5,353,721 $ 5,382,399 To Be Determined Funding Policy Contribution $ 5,471,525 $ 5,353,721 $ 5,382,399 $ 5,191,777 $ 5,673,648 Funding Policy Contribution (% of Pay) 52.8% 49.3% 49.6% 46.5% 51.4% Interest Rate 7.50% 7.00% 7.00% 7.00% 7.00%

Rate of Return Actuarial Value of Assets 5.8% 6.6% 6.2% 5.0% 2.3% Market Value of Assets -1.3% 11.2% 7.0% 2.4% -6.9%

Demographic Information Active Participants 107 111 110 111 110 Retired Participants 86 88 93 96 103 Beneficiaries 10 10 9 8 10 Disabled Participants 13 13 13 13 13 Terminated Vested Participants 1 3 12 11 17 Total Participants 217 225 237 239 253 Covered Payroll $ 10,362,284 $ 10,859,774 $ 10,848,988 $ 11,171,006 $ 11,042,252 Average Covered Pay $ 96,844 $ 97,836 $ 98,627 $ 100,640 $ 100,384

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 8

Executive Summary

Identification of Risks

The results presented in this report are shown as single point values. However, these values are derived using assumptions about future markets and demographic behavior. If actual experience deviates from our assumptions, the actual results for the plan will consequently deviate from those presented in this report. Therefore, it is critical to understand the risks facing this pension plan. The following table shows the risks we believe are most relevant to the Village of Schaumburg Police Pension Fund. The risks are generally ordered with those we believe to have the most significance at the top. Also shown are possible methods by which a more detailed assessment of the risk can be performed.

Type of Risk Method to Assess Risk

Investment Return Scenario Testing; Asset Liability Study

Participant Longevity Projections and Contribution Strategy

Early Retirement

Salary Growth

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 9

Executive Summary

Plan Maturity Measures - May 1, 2020 Each pension plan has a distinct life-cycle. New plans promise future benefits to active employees and then accumulate assets to pre-fund those benefits. As the plan matures, benefits are paid and the pre-funded assets begin to decumulate until ultimately, the plan pays out all benefits. A plan’s maturity has a dramatic influence on how risks should be viewed. The following maturity measures illustrate where the Village of Schaumburg Police Pension Fund falls in its life-cycle. Duration of Liabilities: 13.4 Duration is the most common measure of plan maturity. It is defined as the sensitivity of the liabilities to a change in the interest rate assumption. The metric also approximates the weighted average length of time, in years, until benefits are expected to be paid. A plan with high duration is, by definition, more sensitive to changes in interest rates. A plan with low duration is more susceptible to risk if asset performance deviates from expectations as there would be less time to make up for market losses in adverse market environments while more favorable environments could result in trapped surplus from gains. Conversely, high duration plans can often take on more risk when investing, and low duration plans are less sensitive to interest rate fluctuations. Demographic Distribution - Ratio of Actively Accruing Participants to All Participants: 43.5% A plan with a high ratio is more sensitive to fluctuations in salary (if a salary-based plan) and statutory changes. A plan with a low ratio is at higher risk from demographic experience. Such a plan should pay close attention to valuation assumptions as there will be less opportunity to realize future offsetting gains or losses when current experience deviates from assumptions. Plans with a low ratio also have limited opportunities to make alterations to plan design to affect future funded status. Asset Leverage - Ratio of Payroll for Plan Participants to Market Value of Assets: 10.9% Younger plans typically have a large payroll base from which to draw in order to fund the plan while mature plans often have a large pool of assets dedicated to providing benefits to a population primarily consisting of members no longer on payroll. Plans with low asset leverage will find it more difficult to address underfunding, as the contributions needed to make up the deficit will represent a higher percentage of payroll than for a plan with high asset leverage. Benefit Payment Percentage - Ratio of Annual Benefit Payments to Market Value of Assets: 10.3% As a plan enters its decumulation phase, a larger percentage of the pre-funded assets are paid out each year to retirees. A high percentage is not cause for alarm as long as the plan is nearly fully funded. However, such a plan is more sensitive to negative asset performance, especially if cash contributions are not an option to make up for losses.

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 10

Assets and Liabilities

Present Value of Future Benefits

The Present Value of Future Benefits represents the future benefits payable to the existing participants.

May 1, 2020

Present Value of Future Benefits

Active Participants

Retirement $ 64,933,536

Disability 4,006,527

Death 1,183,686

Termination 1,600,833

Total Active $ 71,724,582

Inactive participants

Retired Participants $ 129,125,297

Beneficiaries 4,683,841

Disabled Participants 7,653,536

Terminated Vested Participants 902,174

Total Inactive $ 142,364,848

Total $ 214,089,430

Present Value of Future Payrolls Present Value of Future Employee Contributions

$ 107,468,092

$ 10,498,602

67%

23%

1%9%

Inactive Liability Active Liability

Normal Cost Future Benefits

Breakdown of Present Value of Future Benefits

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 11

Assets and Liabilities

Accrued Liability

The Funding Liability measures the present value of benefits earned as of the valuation date, using the actuarial assumptions described in the assumption section of this report and the Projected Unit Credit actuarial cost method.

May 1, 2020

Funding Liabilities

Active Participants

Retirement $ 44,832,444

Disability 2,561,196

Death 714,767

Termination 1,153,954

Total Active $ 49,262,361

Inactive Participants

Retired Participants $ 129,125,297

Beneficiaries 4,683,841

Disabled Participants 7,653,536

Terminated Vested Participants 902,174

Total Inactive $ 142,364,848

Total $ 191,627,209

Normal Cost $ 2,553,856

63.3

%

62.4

%

68.8

%

69.7

%

74.3

%

0%

25%

50%

75%

100%

History of the Percentage of Inactive Liability

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 12

Assets and Liabilities

Asset Information

The amount of assets backing the pension promise is the most significant driver of volatility and future costs within a pension plan. The investment performance of the assets directly offsets the ultimate cost.

May 1, 2020

Market Value Reconciliation

Market Value of Assets, Beginning of Prior Year $ 112,429,731

Contributions

Employer Contributions $ 5,382,399

Member Contributions 1,100,167

Total $ 6,482,566

Investment Income (7,698,195)

Benefit Payments (9,721,711)

Administrative Expenses (53,987)

Market Value of Assets, Beginning of Current Year $ 101,438,404

Return on Market Value -6.9%

Actuarial value of assets

Value at Beginning of Current Year $ 116,192,898

$0

$25

$50

$75

$100

$125

Mill

ions

History of Assets

Market Assets Actuarial Assets

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 13

Assets and Liabilities

Asset Information (continued) Plan Assets are used to develop funded percentages and contribution requirements. May 1, 2020 1. Expected Market Value of Assets

(a) Market Value of Assets, Beginning of Prior Year (b) Contributions (c) Benefit Payments (d) Administrative Expenses (e) Expected Return (f) Expected Market Value of Assets, Beginning of Current Year

$ 112,429,731

6,482,566 (9,721,711)

(53,987) 7,754,822

$ 116,891,421

2. Market Value of Assets, Beginning of Current Year $ 101,438,404

3. Actual Return on Market Value $ (7,698,195)

4. Amount Subject to Phase-in [(3)-(1e)] $ (15,453,017)

5. Phase-in of Asset Gain/(Loss) (a) Current Year [80% x $ (15,453,017) ] (b) First Prior Year [60% x $ (5,150,333)] (c) Second Prior Year [40% x $ (23,854) ] (d) Third Prior Year [20% x $ 3,538,311 ] (e) Total Phase-in

$ (12,362,414)

(3,090,200) (9,542)

707,662 $ (14,754,494)

6. Actuarial Value of Assets, Beginning of Current Year [(2)-(5e)] $ 116,192,898

7. Return on Actuarial Value of Assets 2.3%

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 14

Assets and Liabilities

Reconciliation of Gain/Loss May 1, 2020

Liability (Gain)/Loss

Actuarial Liability, Beginning of Prior Year $ 185,576,620

Normal Cost 2,638,485

Benefit Payments (9,721,711)

Expected Interest 12,834,797

Expected Actuarial Liability, Beginning of Current Year $ 191,328,191

Actual Actuarial Liability, Before Changes $ 193,428,942

Liability (Gain)/Loss $ 2,100,751

Asset (Gain)/Loss

Actuarial Value of Assets, Beginning of Prior Year $ 116,887,334

Contributions 6,482,566

Benefit Payments and Administrative Expenses (9,775,698)

Expected Return 8,066,854

Expected Actuarial Value of Assets, Beginning of Current Year $ 121,661,056

Actual Actuarial Value of Assets, Beginning of Current Year $ 116,192,898

Asset (Gain)/Loss $ 5,468,158

Total (Gain)/Loss $ 7,568,909

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 15

Contribution Requirements

Development of Funding Policy Contribution

The funding policy contribution is the annual amount needed to fund the plan to 90% by the end of the 2040 fiscal year as a level percentage of payroll, using the Projected Unit Credit actuarial cost method. The funding policy contribution is subject to the State statutory minimum, which is the annual amount needed to fund the plan to 90% by the end of the 2040 fiscal year as a level percentage of payroll, using the Projected Unit Credit actuarial cost method.

May 1, 2020

Funded Position

1. Projected Unit Credit Accrued Liability $ 191,627,209

2. 90% of Projected Unit Credit Accrued Liability $ 172,464,488

3. Actuarial Value of Assets 116,192,898

4. Unfunded Actuarial Accrued Liability (UAAL) (2 – 3) $ 56,271,590

Funding Policy Contribution

1. Normal Cost $ 2,553,856

2. Administrative Expenses 53,987

3. Amortization of UAAL 3,788,919

4. Applicable Interest 447,773

5. Total Funding Policy Contribution $ 6,844,535

6. Expected Employee Contributions 1,170,887

7. Net Village Funding Policy Contribution (5 – 6) $ 5,673,648

8. Minimum Contribution (Public Act 096-1495 Tax Levy Requirement) $ 5,673,648

9. Final Contribution [max (7,8)] $ 5,673,648

As a Percentage of Expected Payroll 51.4%

52.8

%

49.3

%

49.6

%

46.5

%

51.4

%

0%

20%

40%

60%

80%

History of Funding Policy Contributions (% of Payroll)

The Plan’s Normal Cost plus interest on the Unfunded Actuarial Accrued Liability is $ 6,842,141 .

A contribution greater than the Normal Cost plus interest on the Unfunded Actuarial Accrued Liability will reduce the Unfunded Actuarial Accrued Liability, if all other assumptions are met. A contribution less than the Normal Cost plus interest on the Unfunded Actuarial Accrued Liability will increase the Unfunded Actuarial Accrued Liability, if all other assumptions are met. Consider making a contribution greater than the Normal Cost plus interest on the Unfunded Actuarial Accrued Liability in order to pay down the Plan’s shortfall more rapidly if that amount is greater than your funding policy contribution.

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 16

Demographic Information

Demographic Information

The foundation of a reliable actuarial report is the participant information provided by the plan sponsor. Monitoring trends in demographic information is crucial for long-term pension planning.

May 1, 2019 May 1, 2020 Participant Counts

Active Participants 111 110

Retired Participants 96 103

Beneficiaries 8 10

Disabled Participants 13 13

Terminated Vested Participants 11 17

Total Participants 239 253

Active Participant Demographics

Average Age 41.7 39.8

Average Service 14.7 12.9

Average Compensation $ 100,640 $ 100,384

Covered Payroll $ 11,171,006 $ 11,042,252

$10,

362.

3

$10,

859.

8

$10,

849.

0

$11,

171.

0

$11,

042.

3

$0

$3,000

$6,000

$9,000

$12,000

$15,000

Thou

sand

s

History of Covered Payroll

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 17

Demographic Information

Demographic Information (continued)

May 1, 2019 May 1, 2020 Retiree Statistics

Average Age 65.2 65.1

Average Monthly Pension Benefit $ 6,990 $ 7,234

Beneficiary Statistics

Average Age 61.4 65.1

Average Monthly Pension Benefit $ 3,376 $ 4,001

Disabled Participants Statistics

Average Age 61.7 62.7

Average Monthly Pension Benefit $ 4,002 $ 4,160

Terminated Participants Statistics

Average Age 41.0 39.6

Average Monthly Pension Benefit* $ 2,216 $ 2,945

* Average monthly pension benefit does not include participants eligible for a return of contributions only.

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 18

Participant Reconciliation

Participant Reconciliation

Active

Terminated Vested

Disabled

Retired

Beneficiaries

Totals

Prior Year 111 11 13 96 8 239 Active

To Retired (9) 0 0 9 0 0 To Disabled 0 0 0 0 0 0 To Terminated Vested (4) 4 0 0 0 0 To Death 0 0 0 0 0 0 Terminated Nonvested (return of employee contributions)

(1) 0 0 0 0 (1)

Terminated Vested To Retired 0 0 0 0 0 0 Return of employee contributions 0 0 0 0 0 0

Retired To Death with Beneficiary 0 0 0 (2) 2 0 To Death without Beneficiary 0 0 0 0 0 0

Beneficiaries To Death 0 0 0 0 0 0 Additions 13 2 0 0 0 15 Departures 0 0 0 0 0 0 Current Year 110 17 13 103 10 253

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 19

Participant Reconciliation

Active Participant Schedule

Active participant information grouped based on age and service.

Age Group Years of Service

Under 1 1 to 4 5 to 9 10 to 14 15 to 19 20 to 24 25 to 29 30 to 34 35 to 39 40 & Up Total Average Pay

Under 25 10 10 69,251

25 to 29 2 11 13 83,032

30 to 34 9 4 3 16 96,026

35 to 39 1 2 6 10 19 102,478

40 to 44 1 4 1 6 111,875

45 to 49 1 10 18 1 30 108,966

50 to 54 2 5 5 1 13 112,559

55 to 59 1 2 3 127,777

60 to 64

65 to 69

70 & up

Total 13 22 11 14 16 25 6 3 0 0 110 100,384

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 20

Plan Provisions

Eligibility for Participation Police Officers of the Village of Schaumburg Accrual of Benefits For employees hired prior to January 1, 2011, the normal retirement benefit is equal to 50% of the final salary plus 2.5% of any service over 20 years (with a

maximum of 30) times the final salary. There is a minimum benefit of $1,000 per month. The benefit is paid as a 100% joint and survivor benefit with the spouse, children under 18, or dependent parents of the participants as the survivor.

For employees hired after or on January 1, 2011, the normal retirement benefit is equal to 2.5% of the final average salary times benefit service (maximum 30 years.) The benefit is paid as a 66.67% joint and survivor benefit with the spouse, children under 18, or dependent parents of the participants as the survivor.

Benefits Normal Retirement Eligibility For employees hired prior to January 1, 2011, the normal retirement date is the first day of the month on or after

completion of 20 years of service and attainment of age 50.

For employees hired after or on January 1, 2011, the normal retirement date is the first day of the month on or after completion of 10 years of service and attainment of age 55.

Benefit Unreduced Accrued Benefit payable immediately. Early Retirement Eligibility For employees hired prior to January 1, 2011 and terminating with less than 20 years of service For employees hired after or on January 1, 2011 who has attained age 50 and has 10 years of service. Benefit For those hired prior to January 1, 2011 the Accrued Benefit of 2.5% of final salary times service shall be paid at age 60. For those hired after or on January 1, 2011 the Accrued Benefit is reduced by 0.5% for each month prior to age 55 Termination Eligibility Participants terminating before 20 years of service.

Benefit Refund of Contributions

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 21

Plan Provisions

Disability In The Line of Duty Eligibility For participants who become disabled in the line of duty. Benefit The greater of 65% of the final salary or the accrued benefit Disability Not In The Line of Duty Eligibility For participants who become disabled outside of the line of duty. Benefit 50% of the final salary Death In the Line of Duty Eligibility For participants who die in the line of duty. Benefit The benefit is 100% of final salary paid to the survivor. Death Not In the Line of Duty Eligibility For participants who die outside of the line of duty. Benefit For those hired before 1/1/2011 with greater than 20 years of service, a benefit of 100% of the accrued benefit is paid to the

survivor. For those with more than 10 years of service, but less than 20 years of service, a benefit of 50% of the final salary is paid to the survivor.

For those hired after 1/1/2011, a benefit equal to the greater of 54% of Final Salary and 66-2/3% of the accrued benefit is paid to the survivor.

Compensation Final Salary is the salary attached to the rank held on the last day of service, or one year prior to the last day, whichever is greater.

Final Average Salary is the average monthly salary obtained by dividing the total salary of the police officer during the 48 consecutive months of service within the last 60 months of service in which the total salary was the highest by the number of months of service in that period. Salary will not exceed $106,800 adjusted from January 1, 2011 with the lesser of 3% and 100% of the CPI on November 1.

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 22

Plan Provisions

Credited Service For Vesting and Benefit Accrual purposes, pension service credit is based on elapsed time from hire. Employee Contributions 9.91% of Compensation COLA Eligibility All Participants Benefit For employees hired prior to January 1, 2011 a compound COLA of 3% is granted each year after attainment of age 55 and 1

year of payments.

For employees hired after or on January 1, 2011 a simple COLA of the lesser of 3% and 50% of the CPI on November 1 is granted each year after attainment of age 60 and 1 year of payments. For disabled employees, a simple COLA is available after attainment of age 60 and 1 year of payments. For employees hired prior to January 1, 2011 the COLA is 3%. For employees hired after January 1, 2011, the COLA is the lesser of 3% and 50% of the CPI on November 1.

Plan Provisions Not Included We are not aware of any plan provisions not included in the valuation

Adjustments Made for Subsequent Events We are not aware of any event following the measurement date and prior to the date of this report that would materially impact the results of this report.

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 23

Actuarial Assumptions

Except where otherwise indicated, the following assumptions were selected by the plan sponsor with the concurrence of the actuary. Prescribed assumptions are based on the requirements of the relevant law and applicable regulations. The actuary was not able to evaluate the prescribed assumptions for reasonableness for the purpose of the measurement. Valuation Date May 1, 2020 Participant and Asset Information Collected as of May 1, 2020 Actuarial Cost Method (CO) Projected Unit Credit Cost Method Amortization Method – Funding Policy Contribution (CO) Closed level percentage of payroll amortization of 90% of the Unfunded Actuarial Accrued

Liability using a 3.50% payroll growth assumption over the period ending on April 30, 2040 (20-year amortization in 2020)

Asset Method 5-year smoothing of asset gains and losses Interest Rates (CO) 7.00%, net of investment expenses Inflation (FE) 2.50% Annual Pay Increases (FE) Recommended increases from the 2017 IDOI experience study. Sample rates include: Service Rate Service Rate 0 11.00% 20 3.75% 5 7.00% 25 3.75% 10 4.00% 30 3.75% 15 4.00% 35 3.50% Ad-hoc Cost-of-living Increases 3.0% (1.25% for those hired after 1/1/2011) Mortality Rates (FE) Healthy and Disabled RP-2014 Mortality Table with blue collar adjustment, with scale MP-2019 from 2006 to 2020 10% of deaths are assumed to be in the line of duty

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 24

Actuarial Assumptions

Retirement Rates (FE) Recommended rates from the 2017 IDOI experience study: Tier I Tier II Age Rate Age Rate 50-51 15% 50-54 5% 52-54 20% 55 40% 55-64 25% 56-64 25% 65-69 40% 65-69 40% 70+ 100% 70+ 100% Disability Rates (FE) Recommended rates from the 2017 IDOI experience study. Sample rates include: Age Rate 20 0.000% 30 0.140% 40 0.420% 50 0.710% 60% of disabilities are assumed to be in the line of duty Termination Rates (FE) Recommended rates from the 2017 IDOI experience study. Sample rates include: Age Rate 20 10.40% 30 5.60% 40 1.90% 50 1.50% Marital Status and Ages (FE) 80% of participants are assumed to be married with female spouses 3 years younger. Expense Load Equal to the administrative expenses paid in the prior year. Funding Policy Statutory minimum contribution, with additional funding at the discretion of the Village. FE indicates an assumption representing an estimate of future experience MD indicates an assumption representing observations of estimates inherent in market data CO indicates as assumption representing a combination of an estimate of future experience and observations of market data

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 25

Other Measurements

The actuarial report also shows the necessary items required for plan reporting and the any state requirements.

Minimum contribution (Public Act 096-1495 Tax Levy Requirement)

Village of Schaumburg Police Pension Fund Actuarial Valuation as of May 1, 2020

Page 26

Other Measurements

Minimum Contribution (Public Act 096-1495 Tax Levy Requirement)

May 1, 2020

1. Accrued liability using projected unit credit cost method $ 191,627,209

2. 90% of Accrued liability $ 172,464,488

3. Actuarial value of assets 116,192,898

4. Unfunded liability to be amortized [(2)-(3)] $ 56,271,590

5. Total normal cost using projected unit credit cost method $ 2,553,856

6. Administrative expenses 53,987

7. 20-year level pay amortization of (4) 3,788,919

8. Applicable interest 447,773

9. Minimum contribution (5 + 6 + 7 + 8) $ 6,844,535

10. Expected employee contributions 1,170,887

11. Net employer minimum contribution (9 – 10) $ 5,673,648

Actuarial Cost Method Projected Unit Credit Amortization Method Closed level percentage of payroll amortization of 90% of Unfunded Actuarial Accrued Liability

using a 3.50% payroll growth assumption over the period ending on April 30, 2040 (20-year amortization in 2020)

Asset Method 5-year smoothing of asset gains and losses Interest Rate 7.00%, net of investment expenses

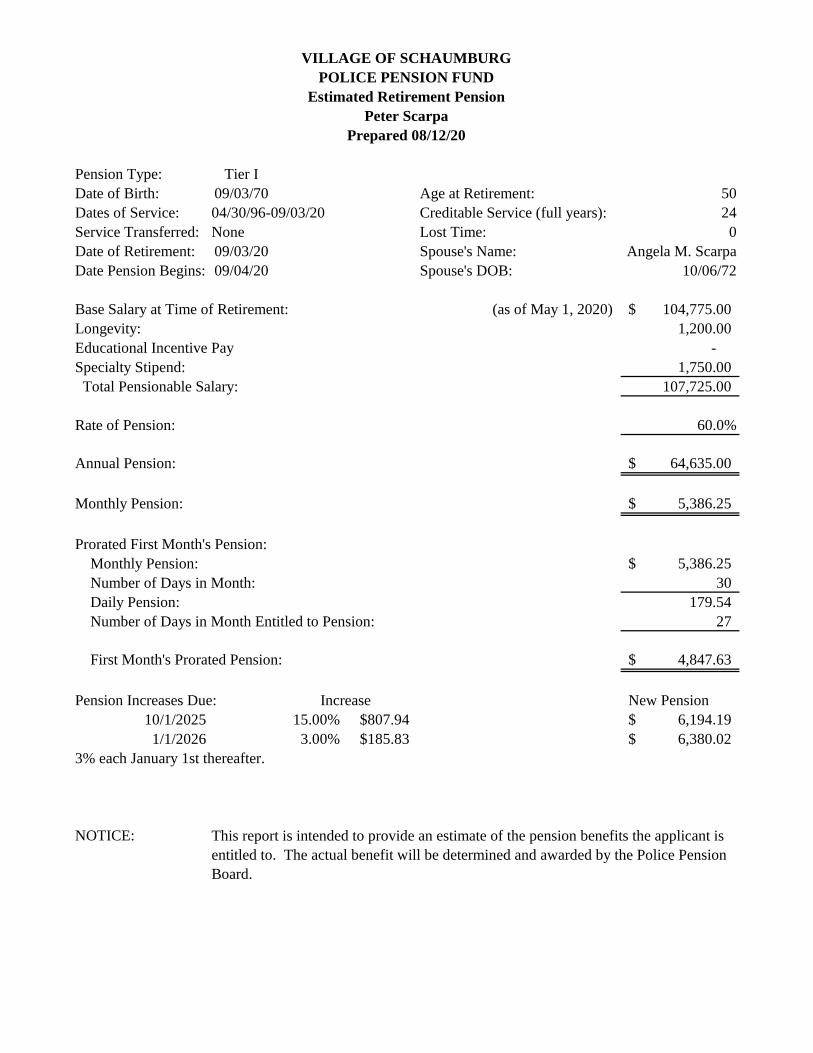

Pension Type: Tier I

Date of Birth: 09/03/70 Age at Retirement: 50

Dates of Service: 04/30/96-09/03/20 Creditable Service (full years): 24

Service Transferred: None Lost Time: 0

Date of Retirement: 09/03/20 Spouse's Name: Angela M. Scarpa

Date Pension Begins: 09/04/20 Spouse's DOB: 10/06/72

Base Salary at Time of Retirement: (as of May 1, 2020) 104,775.00$

Longevity: 1,200.00

Educational Incentive Pay -

Specialty Stipend: 1,750.00

Total Pensionable Salary: 107,725.00

Rate of Pension: 60.0%

Annual Pension: 64,635.00$

Monthly Pension: 5,386.25$

Prorated First Month's Pension:

Monthly Pension: 5,386.25$

Number of Days in Month: 30

Daily Pension: 179.54

Number of Days in Month Entitled to Pension: 27

First Month's Prorated Pension: 4,847.63$

Pension Increases Due: New Pension

10/1/2025 15.00% $807.94 6,194.19$

1/1/2026 3.00% $185.83 6,380.02$

3% each January 1st thereafter.

NOTICE:

Prepared 08/12/20

Peter Scarpa

Estimated Retirement Pension

POLICE PENSION FUND

VILLAGE OF SCHAUMBURG

This report is intended to provide an estimate of the pension benefits the applicant is

entitled to. The actual benefit will be determined and awarded by the Police Pension

Board.

Increase

Benefit Schedule

Benefit Type Benefit Date Monthly Increase Monthly Benefit Annual Benefit Increase Rate

Initial Annual Benefit 9/4/2020 $0.00 $5,386.25 $64,635.00

First Increase 10/1/2025 $807.94 $6,194.19 $74,330.28 15.00%

Annual Increase 1/1/2026 $185.83 $6,380.02 $76,560.24 3.00%

Annual Increase 1/1/2027 $191.40 $6,571.42 $78,857.04 3.00%

Annual Increase 1/1/2028 $197.14 $6,768.56 $81,222.72 3.00%

Annual Increase 1/1/2029 $203.06 $6,971.62 $83,659.44 3.00%

Annual Increase 1/1/2030 $209.15 $7,180.77 $86,169.24 3.00%

Annual Increase 1/1/2031 $215.42 $7,396.19 $88,754.28 3.00%

Annual Increase 1/1/2032 $221.89 $7,618.08 $91,416.96 3.00%

Annual Increase 1/1/2033 $228.54 $7,846.62 $94,159.44 3.00%

Annual Increase 1/1/2034 $235.40 $8,082.02 $96,984.24 3.00%

Annual Increase 1/1/2035 $242.46 $8,324.48 $99,893.76 3.00%

Annual Increase 1/1/2036 $249.73 $8,574.21 $102,890.52 3.00%

Annual Increase 1/1/2037 $257.23 $8,831.44 $105,977.28 3.00%

Annual Increase 1/1/2038 $264.94 $9,096.38 $109,156.56 3.00%

Initial Benefit Summary

Initial Benefit Date: 9/4/2020

Initial Annual Benefit: $64,635.00 = 60.00% of $107,725.00 (Annual Salary)

Prorated Benefit Summary

Prorated Date Range: 9/4/2020 - 9/30/2020

Prorated Benefit: $4,847.63 = 27 Prorated Day(s) x $5,386.25 (Monthly Benefit)/30 Days in the Month

Total Prorated Benefit: $4,847.63

Benefit Summary

Fund Type: Police

Benefit Type: Retirement

Reciprocity: No

Birth Date: 9/3/1970

Hire Date: 4/30/1996 Unpaid Break Days: 0

Retired Date: 9/3/2020 Effective Date of Benefit: 9/4/2020

Annual Salary: $107,725.00

Creditable Service: 24 Year(s) 4 Month(s) 5 Day(s)

Participant Summary

Fund Name: Schaumburg Police Pension Participant Name: Peter Scarpa

August 12, 2020 4:46:15 PM Page 1 of 2

Illinois Department of Insurance - Pension Division

Benefit Calculator Report

Benefit Schedule

Benefit Type Benefit Date Monthly Increase Monthly Benefit Annual Benefit Increase Rate

Annual Increase 1/1/2039 $272.89 $9,369.27 $112,431.24 3.00%

Annual Increase 1/1/2040 $281.08 $9,650.35 $115,804.20 3.00%

Annual Increase 1/1/2041 $289.51 $9,939.86 $119,278.32 3.00%

Annual Increase 1/1/2042 $298.20 $10,238.06 $122,856.72 3.00%

Annual Increase 1/1/2043 $307.14 $10,545.20 $126,542.40 3.00%

Annual Increase 1/1/2044 $316.36 $10,861.56 $130,338.72 3.00%

Annual Increase 1/1/2045 $325.85 $11,187.41 $134,248.92 3.00%

Annual Increase 1/1/2046 $335.62 $11,523.03 $138,276.36 3.00%

Annual Increase 1/1/2047 $345.69 $11,868.72 $142,424.64 3.00%

Annual Increase 1/1/2048 $356.06 $12,224.78 $146,697.36 3.00%

Annual Increase 1/1/2049 $366.74 $12,591.52 $151,098.24 3.00%

Annual Increase 1/1/2050 $377.75 $12,969.27 $155,631.24 3.00%

Annual Increase 1/1/2051 $389.08 $13,358.35 $160,300.20 3.00%

Annual Increase 1/1/2052 $400.75 $13,759.10 $165,109.20 3.00%

Annual Increase 1/1/2053 $412.77 $14,171.87 $170,062.44 3.00%

Annual Increase 1/1/2054 $425.16 $14,597.03 $175,164.36 3.00%

Annual Increase 1/1/2055 $437.91 $15,034.94 $180,419.28 3.00%

Annual Increase 1/1/2056 $451.05 $15,485.99 $185,831.88 3.00%

Annual Increase 1/1/2057 $464.58 $15,950.57 $191,406.84 3.00%

Annual Increase 1/1/2058 $478.52 $16,429.09 $197,149.08 3.00%

Annual Increase 1/1/2059 $492.87 $16,921.96 $203,063.52 3.00%

Annual Increase 1/1/2060 $507.66 $17,429.62 $209,155.44 3.00%

Annual Increase 1/1/2061 $522.89 $17,952.51 $215,430.12 3.00%

Annual Increase 1/1/2062 $538.58 $18,491.09 $221,893.08 3.00%

Annual Increase 1/1/2063 $554.73 $19,045.82 $228,549.84 3.00%

Annual Increase 1/1/2064 $571.37 $19,617.19 $235,406.28 3.00%

Annual Increase 1/1/2065 $588.52 $20,205.71 $242,468.52 3.00%

Annual Increase 1/1/2066 $606.17 $20,811.88 $249,742.56 3.00%

Annual Increase 1/1/2067 $624.36 $21,436.24 $257,234.88 3.00%

Annual Increase 1/1/2068 $643.09 $22,079.33 $264,951.96 3.00%

Annual Increase 1/1/2069 $662.38 $22,741.71 $272,900.52 3.00%

Annual Increase 1/1/2070 $682.25 $23,423.96 $281,087.52 3.00%

Annual Increase 1/1/2071 $702.72 $24,126.68 $289,520.16 3.00%

Annual Increase 1/1/2072 $723.80 $24,850.48 $298,205.76 3.00%

Annual Increase 1/1/2073 $745.51 $25,595.99 $307,151.88 3.00%

August 12, 2020 4:46:15 PM Page 2 of 2

Illinois Department of Insurance - Pension Division

Benefit Calculator Report

Invoice

To. Schaumburg Police Pension Fund

From: Kathryn Strack

10514 Somerset Lane

Huntley, IL 60142

Date: October 1, 2020

Date Hours Amount Due

July/August (Minutes/Packets/Agenda) 4.5 $180

Total Due $180

DATE: 9/17/2020

INVOICE # 6884

BILL TO:

Collins & RadjaMr. David A. Mejia330 W. Colfax Street - Suite 101Palatine, IL 60067

SERVICES PERFORMED:Original TranscriptEvidence Deposition of:Dr. Mark Levin(117 pgs)

Marianne Climack Court Reporting2517 West 115th StreetChicago, IL 60655Phone: (708) 389-8067/Fax: (773) 629-8322

DATE OF JOB:8-19-20

CASE NAME:Kevin O'Connor Disability Claim

TAX ID #36-4373796

JOB #20-0047

CLAIM/REFERENCE #

REPORTER: Marianne Climack

Thank you for your business. Total

Balance Due

Payments/Credits

Description QuantityRate Amount

*Trans/Org/Expert/Reg 1174.00 468.00*Dep/Sub/2 hr min/Write 116.25 116.25

$584.25

$584.25

$0.00

DATE: 9/17/2020

INVOICE # 6886

BILL TO:

Collins & RadjaMr. David A. Mejia330 W. Colfax Street - Suite 101Palatine, IL 60067

SERVICES PERFORMED:Court Reporter Sitting Feefor the Deposition of:Dr. Brian Forsythe(no-write)

Marianne Climack Court Reporting2517 West 115th StreetChicago, IL 60655Phone: (708) 389-8067/Fax: (773) 629-8322

DATE OF JOB:8-25-20

CASE NAME:Kevin O'Connor Disability Claim

TAX ID #36-4373796

JOB #20-0049

CLAIM/REFERENCE #

REPORTER: Marianne Climack

Thank you for your business. Total

Balance Due

Payments/Credits

Description QuantityRate Amount

*Dep/2hr min/ NoWrite 121.00 121.00

$121.00

$121.00

$0.00

INSPE ASSOCIATES INVOICE123 W. Madison St., Suite 800 67489Chicago, Illinois 60602 08/24/2020

PAYMENT DUE UPON RECEIPT.

INSPE ASSOCIATES LTD. WILL LOOK TO YOU FOR PAYMENT OF ITS CHARGES IN THIS MATTER REGARDLESS OF YOUR REPRESENTATION OF YOUR CLIENT OR YOUR RELATIONSHIP WITH AN INSURANCE COMPANY OR ANY OTHER PERSON, FIRM, OR CORPORATION, UNLESS INSPE RECEIVES ADEQUATE WRITTEN ASSURANCE FROM ANOTHER SOURCE THAT THAT SOURCE WILL BE RESPONSIBLE FOR PAYMENT INSTEAD OF YOU.

TO ENSURE PROPER CREDIT TO YOUR ACCOUNT PLEASE RETURN A COPY OF THIS INVOICE WITH YOUR PAYMENT, THANK YOU

TAX ID: 36 3772118 INSPE Associates (312) 782-3121 NAS 2020-08-24 12:49:24

Mr. David MejiaCollins & Radja1319 Bradley CircleElgin, IL 60120

**PLEASE INDICATE INVOICE NUMBER ON YOUR PAYMENT TO INSPE**

Re: McIntyre, BrianFile No.: NO NUMBER 3410

INSPE CHARGE:Review Records, Arrange Consultant $150.00

CONSULTANT: Stevan Weine, M.D.Record Review & Written Report (8/23/20) - 5.50 Hr $2,640.00Patient Exam - 3.00 Hr $1,800.00

TOTAL AMOUNT DUE:................................................................. $4,590.00

MAKE ALL CHECKS PAYABLE TO INSPE ASSOCIATESAND SEND TO INSPE AT THE ABOVE ADDRESS

INSPE ASSOCIATES INVOICE123 W. Madison St., Suite 800 67699Chicago, Illinois 60602 09/14/2020

PAYMENT DUE UPON RECEIPT.

INSPE ASSOCIATES LTD. WILL LOOK TO YOU FOR PAYMENT OF ITS CHARGES IN THIS MATTER REGARDLESS OF YOUR REPRESENTATION OF YOUR CLIENT OR YOUR RELATIONSHIP WITH AN INSURANCE COMPANY OR ANY OTHER PERSON, FIRM, OR CORPORATION, UNLESS INSPE RECEIVES ADEQUATE WRITTEN ASSURANCE FROM ANOTHER SOURCE THAT THAT SOURCE WILL BE RESPONSIBLE FOR PAYMENT INSTEAD OF YOU.

TO ENSURE PROPER CREDIT TO YOUR ACCOUNT PLEASE RETURN A COPY OF THIS INVOICE WITH YOUR PAYMENT, THANK YOU

TAX ID: 36 3772118 INSPE Associates (312) 782-3121 NAS 2020-09-14 11:31:12

Mr. David MejiaCollins & Radja1319 Bradley CircleElgin, IL 60120

**PLEASE INDICATE INVOICE NUMBER ON YOUR PAYMENT TO INSPE**

Re: McIntyre, BrianFile No.: NO NUMBER 3410

INSPE CHARGE:Arrange Consultant $75.00

CONSULTANT: Gaurava Agarwal, M.D.Record Review, Patient Exam & Written Report (9/1/20) - 7.75 Hr $4,650.00

TOTAL AMOUNT DUE:................................................................. $4,725.00

MAKE ALL CHECKS PAYABLE TO INSPE ASSOCIATESAND SEND TO INSPE AT THE ABOVE ADDRESS

LISA PETERSENVILLAGE OF [email protected] SCHAUMBURG COURTSCHAUMBURG, IL 60193

September 30, 2020Invoice No: 0162570

Project 667501.DBVAL.ONG2020VILLAGE OF SCHAUMBURG__POLICE

Actuarial and Administrative Services from September 1, 2020 to September 30, 2020

2020 Police Pension Funding and GASB valuations

$5,500.00Total this Invoice

Remit Payment To:The Howard E Nyhart Company IncorporatedAttn: Finance Department8415 Allison Pointe BlvdSuite 300Indianapolis, IN [email protected] Free Number 800-428-7106