bmo capital markets global metals & mining conference 2015

TRANSCRIPT

February 24, 2015

Forward Looking Information

Both these slides and the accompanying oral presentation contain certain forward-looking statements within the meaning of the United StatesPrivate Securities Litigation Reform Act of 1995 and forward-looking information within the meaning of the Securities Act (Ontario) andcomparable legislation in other provinces. Forward-looking statements can be identified by the use of words such as “plans”, “expects” or “doesnot expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, orvariation of such words and phrases or state that certain actions, events or results “may”, “could”, “should”, “would”, “might” or “will” be taken,occur or be achieved. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actualresults, performance or achievements of Teck to be materially different from any future results, performance or achievements expressed orimplied by the forward-looking statements. These forward-looking statements include statements relating to management’s expectations withrespect to our diversification and the benefits of diversification, our production, costs and sales targets and guidance, mine lives and resourcelives for our various commodities, costs for our projects, 2015 projected capital expenditures, timing of production at our Fort Hills project,anticipated economic benefits and contributions of Fort Hills project, including, but not limited to, yield and free cash flow, our dividend policyincluding our goal of paying a sustainable dividend, our investment rating, sensitivity of our profit, EBITDA and operating expenses to oil pricesand currency exchange rates, total liquidity, free cash flow examples, potential fuel cost reduction as a result of converting to LNG for trucks,expected work and expenditures in respect of the Elk Valley Water Quality Plan, expectation that we have access to cash and credit linessufficient to meet our capital commitments, our expectation that we should complete 2015 with over $1 billion in cash, demand and marketoutlook for commodities.

These forward-looking statements involve numerous assumptions, risks and uncertainties and actual results may vary materially. Thesestatements are based on a number of assumptions, including, but not limited to, assumptions regarding general business and economicconditions, interest rates, the supply and demand for, inventories of, and the level and volatility of prices of coal, zinc, copper and gold and otherprimary metals and minerals produced by Teck as well as steel, oil, natural gas and petroleum, the outcome of engineering studies currentlyunderway in connection with Teck’s development projects, the timing of receipt of regulatory and governmental approvals for Teck’sdevelopment projects and other operations, receipt of permits to mine, costs of production at our operations and production and productivitylevels, as well as those of Teck’s competitors, power prices, market competition, the accuracy of Teck’s reserve and resource estimates(including with respect to size, grade and recoverability) and the geological, operational and price assumptions on which these are based, theassumption that our board will approve dividends, the resolution of environmental and other proceedings, our ongoing relations with ouremployees and partners and joint venturers, the availability of financing for development projects and the future operational and financialperformance of the company generally. Assumptions regarding the sensitivity of EIBTDA and operating costs to oil prices are based onassumptions regarding the amount of diesel fuel used in operations and transporting our coal products, and is also based on an assumedCanadian/U.S. dollar exchange rate of $1.20. Assumptions regarding the impact of currency exchange are based on current commodity prices.Examples regarding cash flow are based on the commodity and exchange assumptions disclosed therein. Statements regarding our potentialcash position at the end of the year are based on assumptions that no unusual transactions occur over the year and on current commodityprices. The foregoing list of assumptions is not exhaustive.

2

Forward Looking Information

Events or circumstances could cause actual results to differ materially. Factors that may cause actual results to vary include, but are not limitedto: unanticipated developments in business and economic conditions in the principal markets for Teck’s products or in the supply, demand, andprices for metals and other commodities to be produced, changes in power prices, changes in interest or currency exchange rates, inaccurategeological or metallurgical assumptions (including with respect to the size, grade and recoverability of mineral or oil and gas reserves andresources), changes in taxation laws or tax authority assessing practices, legal disputes or unanticipated outcomes of legal proceedings,unanticipated operational difficulties (including failure of plant, equipment or processes to operate in accordance with specifications orexpectations, cost escalation, unavailability of materials and equipment, government action or delays in the receipt of permits or governmentapprovals, industrial disturbances or other job action, and unanticipated events related to health, safety and environmental matters),assumptions used to generate our economic analysis, decisions made by our partners or co-venturers, political events, social unrest, lack ofavailable financing for Teck or its partners or co-venturers, and changes in general economic conditions or conditions in the financial markets.Our Fort Hills project is not controlled by us and construction, sanction and production schedules may be adjusted by our partners. Creditagencies set our credit rating. The effect of the price of oil on operating costs will be influenced by the exchange rate between Canadian andU.S. dollars.

Statements concerning future production costs or volumes are based on numerous assumptions of management regarding operating mattersand on assumptions that demand for products develops as anticipated, that customers and other counterparties perform their contractualobligations, that operating and capital plans will not be disrupted by issues such as mechanical failure, unavailability of parts and supplies,labour disturbances, interruption in transportation or utilities, adverse weather conditions, and that there are no material unanticipated variationsin the cost of energy or supplies. Statements regarding anticipated coal sales volumes and average coal prices for the quarter depend on timelyarrival of vessels and performance of our coal-loading facilities, as well as the level of spot pricing sales.

Certain of these risks are described in more detail in Teck’s annual information form available at www.sedar.com and in public filings with theSEC at www.sec.gov. Teck does not assume the obligation to revise or update these forward-looking statements after the date of this documentor to revise them to reflect the occurrence of future unanticipated events, except as may be required under applicable securities laws.

3

Agenda

Teck Overview

Commodity Market Observations

Teck Update

4

About UsCanada’s Largest Diversified Natural Resources Company

Top ten copper miner in the Americas

#3 zinc miner in the world

Building an energy business

# 1 Producer of steelmaking coal in North America

# 2 Seaborne exporter of steelmaking coal globally

Safety is our core value

Implementing a comprehensive sustainability strategy

5

Attractive Portfolio Of Long-Life Assets & Resources

Producing through multiple price cycles after capital is recovered,

enhancing returns

Focused on the Americas & Low Risk, Stable Jurisdictions

Strong Resource Position With Sustainable Long-Life Assets

Coal Resources >100 years

Copper Resources >30 years

Zinc Resources >20 years

Energy Resources >50 years

6

Teck has good leverage to stronger zinc and copper markets, and benefits from the weaker Canadian dollar

The Value of Our Diversified Business Model

Cash Operating Profit 2014

Coal~1/3rd

Copper~60%

Zinc~40%

Base Metals~2/3rds

Production Guidance1

Unit of Change

Estimated Profit 2

EstimatedEBITDA2

Coal 27 Mt US$1/tonne $21M /$1∆ $32M /$1∆

Copper 350 kt US$0.01/lb $5M /$.01∆ $8M /$.01∆

Zinc 935 kt US$0.01/lb $8M /$.01∆ $12M /$.01∆

$C/$US C$0.01 $32M /$.01∆ $52M /$.01∆

2015 Leverage to Strong Commodities

1. Mid-point of 2015 guidance ranges. Zinc includes 650,000 tonnes of zinc in concentrate and 285,000 tonnes of refined zinc.2. Based on $1.20 USD/CAD. The effect on our profit attributable to shareholders of commodity price and exchange rate

movements will vary from quarter to quarter depending on sales volumes.7

Agenda

Teck Overview

Commodity Market Observations

Teck Update

8

Source: NBS & CEIC* Assuming 7.1% real GDP growth and 6.16 RMB/USD exchange rate.

Lower GDP growth rate on a higher base = strong absolute growth

In absolute terms, China’s GDP growth is approximately double that of 10 years ago

China’s Growth: Less is More!

9

Incremental GDP in 2015 is expected to be similar to last year, in absolute terms

• 2014: RMB 2.95 trillion (~US$480 billion)

• 2015*: RMB 3 trillion (~US$493 billion)

-1%

1%

3%

5%

7%

9%

11%

13%

15%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

201

4

2015

f

GDP Increment at 2005 Constant Prices in RMB

Increment of GDP, Rmb bn (lhs) GDP real growth (rhs)

RM

B (B

illion

s)

100

110

120

130

140

150

160

Jan-

14

Feb-

14

Mar

-14

Apr

-14

May

-14

Jun-

14

Jul-1

4

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15

Feb-

15

$ / t

onne

Stronger US dollar has increased coal prices in C$ terms

Sources: Argus, Bank of Canada

• ~30 Mt cutbacks announced, slowly being implemented

• Require additional cutbacks to achieve market balance

• US coal production high end of cost curve and no currency benefit

• Continued closure announcements promising for last half of 2015

Met Coal Market Rebalancing; Higher Prices in C$ Terms

Coal Prices By CurrencyArgus FOB Australia

AUS$

CDN$

US$

10

0

100

200

300

400

500

600

700

800

900

Thou

sand

Ton

nes

0

100

200

300

400

500

600

700

800

900

Apr

-12

Jun-

12A

ug-1

2O

ct-1

2D

ec-1

2Fe

b-13

Apr

-13

Jun-

13A

ug-1

3O

ct-1

3D

ec-1

3Fe

b-14

Apr

-14

Jun-

14A

ug-1

4O

ct-1

4D

ec-1

4

Thou

sand

Ton

nes

Source: Wood Mackenzie

Copper Surplus Forecast Declining

Wood Mackenzie Forecast Refined Copper Surplus 2015

Wood Mackenzie Forecast Refined Copper Surplus 2014

Current surplus forecasts for 2014 & 2015 represent <2% of global demand

11

500

600

700

800

900

1,000

1,100

1,200

0¢

20¢

40¢

60¢

80¢

100¢

120¢

Dec

-12

Jan-

13Fe

b-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14Fe

b-14

Mar

-14

Apr

-14

May

-14

Jun-

14Ju

l-14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15Fe

b-15

Stocks Price

0

200

400

600

800

1,000

1,200

1,400

0¢

50¢

100¢

150¢

200¢

250¢

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Stocks Price

US

¢/lb

thou

sand

tonn

esplotted to

Feb 16, 2015

US

¢/lb

thou

sand

tonn

es

• LME stocks down ~600 kt over 24 months• Large inventory position still to work down• Large, sudden increases indicate there are also significant off-market inventories • Inventories approaching same inflection point level as in 2006

LME Zinc Stocks – Since Dec 2012

plotted to Feb 16, 2015

LME Zinc Stocks - 11 Years

Zinc Inventories Declining

Source: LME12

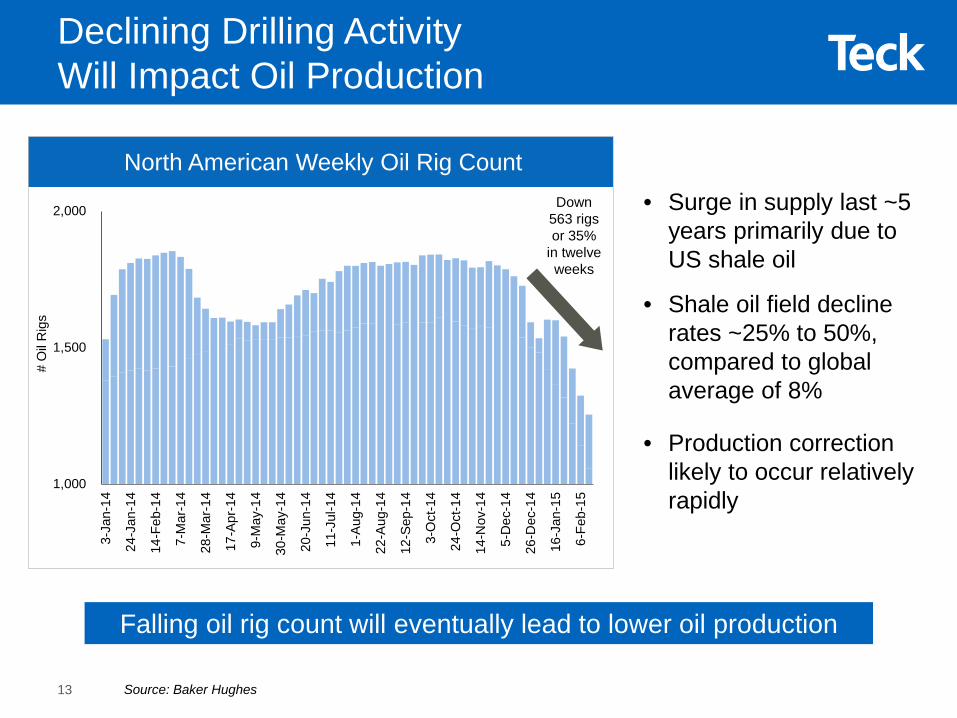

Source: Baker Hughes

Falling oil rig count will eventually lead to lower oil production

North American Weekly Oil Rig Count

Declining Drilling Activity Will Impact Oil Production

13

• Surge in supply last ~5 years primarily due to US shale oil

• Shale oil field decline rates ~25% to 50%, compared to global average of 8%

• Production correction likely to occur relatively rapidly

1,000

1,500

2,000

3-Ja

n-14

24-J

an-1

4

14-F

eb-1

4

7-M

ar-1

4

28-M

ar-1

4

17-A

pr-1

4

9-M

ay-1

4

30-M

ay-1

4

20-J

un-1

4

11-J

ul-1

4

1-A

ug-1

4

22-A

ug-1

4

12-S

ep-1

4

3-O

ct-1

4

24-O

ct-1

4

14-N

ov-1

4

5-D

ec-1

4

26-D

ec-1

4

16-J

an-1

5

6-Fe

b-15

# O

il R

igs

Down 563 rigs or 35%

in twelve weeks

Agenda

Teck Overview

Commodity Market Observations

Teck Update

14

Controlling the Controllables

• Solid performance – met or exceeded guidance- Record coal production- Record throughput at Antamina- Record zinc production at Red Dog

• Significantly reduced controllable operating costs and planned capex

• Maintained a strong balance sheet

15

57 51

1918

01020304050607080

2012 2015 Guidance (Mid)Operating Capitalized Stripping

C$/

t

0.00

0.50

1.00

1.50

2.00

2.50

2012 2015 Guidance (Mid)

US$

/lb

Copper Cash Costs1

Delivering Results in Cost Management

1. Before by-product credits.2. Including inventory write-downs.

2.081.80

7669

Steelmaking Coal All-In Site Costs

• Copper cash costs before by-product credits down ~14% from peak in 2012

• By-product credits currently reduce costs by ~US$0.30.lb

• Coal total site costs including capitalized stripping down ~9% since 2012

• Costs are down further on a US dollar basis• Sustaining capital expenditures are also lower

Achieved significant unit cost reductions, and expect further reductions in 2015

2

~$1.50 net of

by-product credits

16

Fort Hills’ Economics Robust1

Source: Teck Resources Limited1. Estimates are based on exchange rates as shown, expected bitumen netbacks, and operating costs of C$25 per barrel, including

sustaining capital of C$3-5 per barrel. 2. Per barrel of bitumen.3. Go-forward capital is the go-forward amount from the date of the Fort Hills sanction decision (October 30, 2013), denominated in

Canadian dollars and on a fully-escalated basis. 4. Pre-tax free cash flow yield during capital recovery period.

The Fort Hills project is expected to have significant free cash flow yield across a range of WTI prices

Fort Hills Free Cash Flow Yield4

Sensitivity to WTI PricePotential Contribution

from Fort Hills

$70 WTI & $0.80

CAD/USD

$90 WTI & $0.90

CAD/USD

Teck’s share of annual production (36,000 bpd) 13 Mbpa 13 Mbpa

Estimated netback2 ~$54/bbl ~$63/bbl

Estimated operating margin2 ~$29/bbl ~$38/bbl

Alberta oil royalty – Phase 1 (prior to capital recovery) 2 ~$2/bbl ~$4/bbl

Estimated net margin2 ~$26/bbl ~$34/bbl

Annual pre-tax cash flow ~$350 M ~$444 M

Teck’s share of go-forward capex3 ~$2,940 M ~$2,940 M

Free cash flow yield4 ~12% ~15%

0%

5%

10%

15%

20%

25%

60 70 80 90 100 110 120

Free

Cas

h Fl

ow Y

ield

WTI $/bbl

$0.90 CAD/USD

$0.80 CAD/USD

17

$0

$1,000

$2,000

$3,000

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2031

2032

2033

2034

2035

2036

2037

2038

2039

2040

2041

2042

2043

US$

M

Cash position Debt Maturity

Liquidity of >C$5B, including C$2B cash and undrawn US$3B line of credit

~US$1.75 B

18As at December 31st, 20141. Assumes current commodity prices and exchange rates, Teck’s 2015 guidance for production, costs and capital expenditures and

no unusual transactions or events.

Strong Balance Sheet & Liquidity

Investment Grade Rating• Debt-to-debt-plus-equity of 31%• US$300M of notes due to end of 2016• Weighted average maturity ~14 years• Weighted average coupon (interest rate) 4.8%• Average maturity <US$600M

Targeting year-end 2015 cash balance of $1B1

Fort Hills Capex Well Supported By Free Cash Flow & Liquidity

0

200

400

600

800

1000

1200

1400

1600

2014 Free CashFlow (before Fort

Hills Capex)

Weaker Canadiandollar, relative to

the US dollar

Lower oil prices Lower commodityprices (Cu, Zn,

Coal)

Implied Free CashFlow (before Fort

Hills Capex)

$ M

illion

s

$289

+$201 ($568)

$702

+$780

Effect of Disclosed Sensitivities On Free Cash Flow2 (before Fort Hills Capex)1

$2.3B capex to fund over 3 years; with $5B liquidity and good free cash flow

1. Implied impact of disclosed EBITDA sensitivities on free cash flow, assuming spot commodity prices and exchange rate as disclosed in the table above, in comparison to 2014 average prices and exchange rate, for illustration purposes only. Other factors will have a material impact on 2015 EBITDA, and actual results will vary materially from those suggested by this simplified model.

2. 2014A free cash flow is cash flow from operating activities, minus investing activities (excluding $615M investment in Fort Hills), and debt interest paid, before returns to shareholders.

3. Spot prices at February 13, 2015.

Sensitivity 2014A Current3 ∆ 2014A to Spot

Estimated EBITDA1

CAD/USD $1.10 $1.25 $0.15 $52M /$0.01∆

Oil – WTI (US$/bbl)

$93.00 $52.75 ($40.25) $5M /$1∆

Copper (US$/lb)

$3.11 $2.60 ($0.51) $8M /$0.01∆

Zinc (US$/lb)

$0.98 $0.98 $0.00 $12M/$0.01∆

Coal (US$/t realized)

$115 $110 $5 $32M /$1∆

• Remaining share of Fort Hills capital expenditure: C$2.3B over 3 years

• ~$5B liquidity available• Expected higher coal/copper production

and lower costs may improve cash flow

19

Summary

Attractive portfolio of long-life assets & resources

Good leverage to strong zinc & copper markets

Executing well & controlling the controllables

Solid financial position

Investment grade credit rating

20

February 24, 2015

Additional Information

Diversified Portfolio of Key Commodities

NorthAmerica

20%Europe

18%

LatinAmerica

3%

China26%

Asia excl. China33%

Source: Teck Resources Limited; 2014 revenue23

Diversified Global Customer Base

Coking coal CopperZinc LeadMoly SilverGermanium Indium

Original Guidance Actual ResultsSteelmaking Coal

Coal production 26–27 Mt 26.7 Mt Record coal production

Coal site costs C$55-60 /t C$54 /t1

Coal transportation costs C$38-42 /t C$38 /t

Combined coal costs C$93-102 /t C$92 /t

Combined coal costs US$84-92 /t US$84 /t

Copper

Copper production 320–340 kt 333 kt Record thru-put at Antamina

Copper cash unit costs2 US$1.70-190 /lb US$1.65 /lb

Zinc

Zinc in concentrate production3 555-585 kt 660 kt Record at Red Dog

Refined zinc production 280–290 kt x 277 kt Higher production 2H14(1H14: 133 kt; 2H14 143 kt)

Capital Expenditures4 $1,905M $1,498M Significant capex reduction

Solid Delivery Against 2014 Guidance

1. Including inventory adjustments.2. Net of by-product credits.3. Including co-product zinc production from our copper business unit.4. Excluding capitalized stripping.

24

Actual 2014 2015 GuidanceSteelmaking Coal

Coal production 26.7 Mt 26.5-27.5 MtCoal site costs C$54 /t1 C$49-53 /tCoal transportation costs C$38 /t C$37-40 /tCombined coal costs C$92 /t C$86-93 /tCombined coal costs US$84 ~US$69-74 /t2

CopperCopper production 333 kt 340-360 ktCopper cash unit costs3 US$1.65 /lb US$1.45-1.55 /lb

ZincZinc in concentrate production4 660 kt 635-665 ktRefined zinc production 277 kt 280–290 kt

2015 Production & Site Cost Guidance

1. Including inventory adjustments.2. At $1.25 CAD/USD.3. Net of by-product credits.4. Including co-product zinc production from our copper business unit.

25

($M) SustainingMajor

EnhancementNew Mine

Development Sub-totalCapitalized Stripping Total

Coal $100 $45 $ - $145 $490 $635

Copper 200 15 105 320 225 545

Zinc 180 - - 180 60 240

Energy - - 910 910 - 910

Corporate 10 - - 10 - 10

TOTAL $490 $60 $1,015 $1,565 $775 $2,340

Total capex of ~$1.6B, plus capitalized stripping

2014A $511 $165 $822 $1,498 $715 $2,213

2015 Capital Expenditures Guidance

26

Low oil price benefits Teck overall in the near-term• Reduces operating costs by hundreds of millions of dollars annually1

• Accompanied weaker Canadian dollar improves EBITDA by hundreds of millions of dollars annually2

Reduces budget and schedule pressure on the Fort Hills project• Reduces capex and drilling activity by the sector, which eases

pressure on skilled labour and contractors• Reduces competition for pipeline capacity

Forces cutbacks in oil production and exploration• Starts the correction to higher long-term oil prices, due to the sector’s

decline rates and cuts to capex /drilling activity

Provides positive macro-economic stimulus • Drives additional metal consumption, benefiting Teck’s base metals

businesses

Significant Benefits from Low Oil Prices

1. Each US$1/bbl change in oil price impacts our operating costs by ~$5M on an annual basis, based on $1.20 CAD/USD.2. Each $0.01 change in the CAD/USD exchange rate impacts our EBITDA by ~$52M on an annual basis.27

Operation Expiry DatesLine Creek In Negotiations - May 31, 2014Coal Mountain In Negotiations - December 31, 2014Antamina July 23, 2015

Carmen de Andacollo September 30, 2015December 31, 2015

Elkview October 31, 2015

Quebrada BlancaOctober 30, 2015

November 30, 2015January 31, 2016

Fording River April 30, 2016Highland Valley Copper September 30, 2016Trail May 31, 2017Cardinal River June 30, 2017Quintette April 30, 2018

Collective Agreements

28

Note: Based on public filings

Teck Resources LimitedMarch 3, 2014

Shares Held Percent Voting RightsClass A ShareholdingsTemagami Mining Company Limited 4,300,000 45.97% 28.62%SMM Resources Inc (Sumitomo) 1,469,000 15.71% 9.78%Caisse de depot et placement du Quebec 1,587,600 16.97% 10.57%Public 1,996,870 21.35% 13.29%

9,353,470 100.00% 62.26%Class B SharesTemagami Mining Company Limited 860,000 0.15% 0.06%SMM Resources Inc (Sumitomo) 295,800 0.05% 0.02%Caisse de depot et placement du Quebec 7,715,997 1.36% 0.51%China Investment Corporation 101,304,474 17.87% 6.74%Public 456,745,086 80.57% 30.40%

566,921,357 100.00% 37.74%Total SharesTemagami Mining Company Limited 5,160,000 0.90% 28.68%SMM Resources Inc (Sumitomo) 1,764,800 0.31% 9.80%Caisse de depot et placement du Quebec 9,303,597 1.61% 11.08%China Investment Corporation 101,304,474 17.58% 6.74%Public 458,741,956 79.60% 43.70%

576,274,827 100.00% 100.00%

Share Structure & Principal Shareholders

29

• Common corporate structure in Canada

• May not confirm to typical governance expectations, but can still have strong governance practices

• Family-controlled issuers can benefit from a longer-term outlook and unique governance structure

Source: The Impact of Family Control on the Share Price Performance of Large Canadian Publicly-Listed Firms (1998-2012) by Clarkson Centre for Board Effectiveness (Rotman School of Management, University of Toronto)

Canadian family-controlled issuers outperformed peers over the past 15 years, greatly benefitting minority shareholders

Cumulative Average Growth Rate

Family-Controlled Public Issuers

30

Teck has been a strong investment in recent years

Long-term investments in Teck have outperformed non-family and materials firms

Family-Controlled Public Issuers;Teck Share Price Performance

Source: The Impact of Family Control on the Share Price Performance of Large Canadian Publicly-Listed Firms (1998-2012) by Clarkson Centre for Board Effectiveness (Rotman School of Management, University of Toronto)31

Annualized Dividend Payout

• Aim to pay a sustainable dividend that grows commensurate with growth in earnings and cash flow

- Since January 2013, semi-annual payment of $0.45; annualized $0.90

• Normal Course Issuer Bid in place for up to 20M shares

32

Returned Cash To Shareholders

$- $0.10 $0.20 $0.30 $0.40 $0.50 $0.60 $0.70 $0.80 $0.90

Economic Outlook

Source: Dragonomics

With the right policies, China still has the potential to boost incomes

China’s GDP is ~20% of the US’s on a per capital basis

Substantial Economic Growth Requires Decades to Achieve

Per Capita GDP Relative to the US at PPP

China

Japan

Korea

0

10

20

30

40

50

60

70

80

90

100

1953 1958 1963 1968 1973 1978 1983 1988 1993 1998 2003 2008

%

34

Country

20-Year Period Beginning When Country’s

Per Capital GDP Was 21% of US’s

Average Annual GDP Growth Rate

Over a 20-Year Period

Japan 1951-1971 9.2

Singapore 1967-1987 8.6

Taiwan 1975-1995 8.3

Korea 1977-1997 7.6

China* 2008-2028 8.0

Other Asian economies show that China could continue to grow significantly for some time

Substantial Potential For Continuous Robust Growth in China

35

Room for Further Development in China

0

10

20

30

40

50

60

70

80

90

100

1953

1956

1959

1962

1965

1968

1971

1974

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

China Japan Korea

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

199

0

199

2

199

4

199

6

199

8

200

0

200

2

200

4

200

6

200

8

201

0

201

2

Eastern Central Western

RM

B

China Annual Per Capita GDP by RegionPer Capita GDP, Relative to the US

Source: Penn World Table, NBS36

Room for Further Development in China 2

0%

10%

20%

30%

40%

50%

60%

199

7 1

998

199

9 2

000

200

1 2

002

200

3 2

004

200

5 2

006

200

7 2

008

200

9 2

010

201

1 2

012

201

3 2

014

With urban Hukou Without urban Hukou

% o

f Tot

al P

opul

atio

n

0

10

20

30

40

50

60

70

80

90

100

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

China Japan Europe US

%

China Annual Urbanization RateUrbanization Rate Comparison

Source: United Nations, NBS37

Room for Further Development in China 3

0

5

10

15

20

25

30

35

40

0

1

2

3

4

5

6

200

0

200

1

200

2

200

3

200

4

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

201

3

Increase in track length, thousand kilometers, lhs

Freight traffic density, rhs

Thou

sand

kilo

met

ers

%

$0$20$40$60$80

$100$120$140

2010 2010 1930 2009

China China at PPP US

US$

(Tho

usan

ds)

$0$10$20$30$40$50$60$70

2010 at PPP 1971 at PPP 1990 at PPP

China Japan

US$

(Tho

usan

ds)

Source: GK Dragonomics, NBS

Chinese Railways Remain CrowdedCapital Stock Per Capita (US$ at constant 2005 prices)

Capital Stock Per Capita (US$ at constant 1990 prices)

38

• Despite China’s rapid urbanization over the past decade (to 54.77% in 2014), it is still lower than the Western world who are all ~80%- China’s current urbanization rate is

comparable to Japan’s in the 1950s- China was previously a drag on Asia’s

urbanization statistics. Today, it is the driving force, with room for further urbanization

• India’s urbanization was 32% in 2013, up from 26% in 1990- It is expected to grow to 33% by 2015,

35% by 2020 and 37% by 2025

Global UrbanizationChina and India Leading the Way

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995

2000

2005

2010

2015

2020

2025

2030

2035

2040

2045

2050

China India Asia

Europe S.America N.America

Urbanization Rates

Source: United Nations, World Bank39

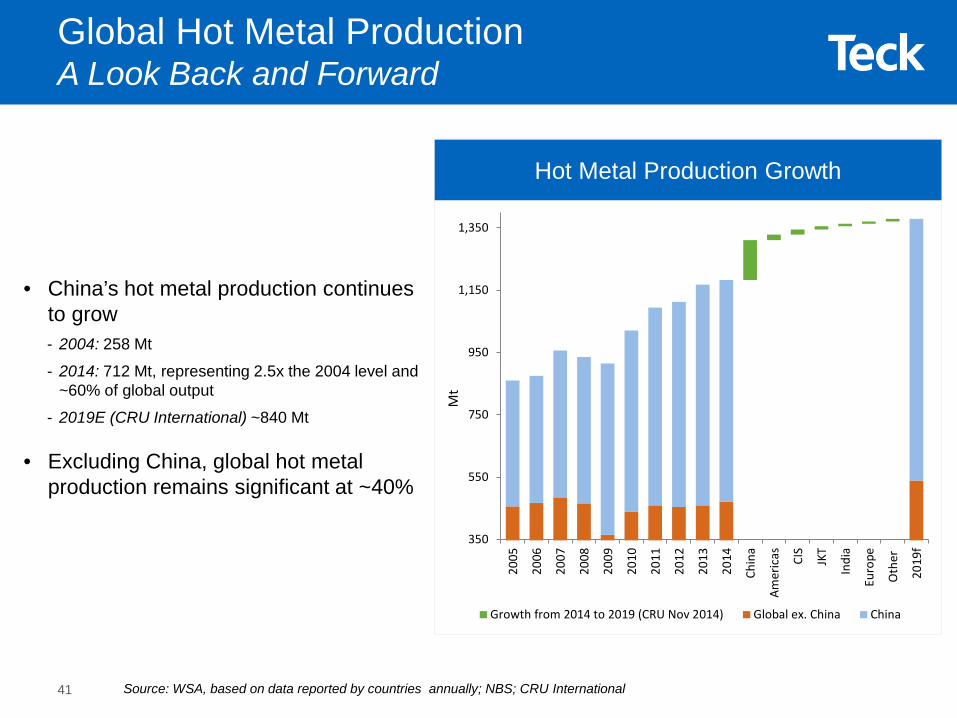

Steelmaking CoalBusiness Unit & Markets

• China’s hot metal production continues to grow- 2004: 258 Mt

- 2014: 712 Mt, representing 2.5x the 2004 level and ~60% of global output

- 2019E (CRU International) ~840 Mt

• Excluding China, global hot metal production remains significant at ~40%

Hot Metal Production Growth

Source: WSA, based on data reported by countries annually; NBS; CRU International

Global Hot Metal ProductionA Look Back and Forward

350

550

750

950

1,150

1,350

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Chin

a

Amer

icas CIS

JKT

Indi

a

Euro

pe

Oth

er

2019

f

Growth from 2014 to 2019 (CRU Nov 2014) Global ex. China China

Mt

41

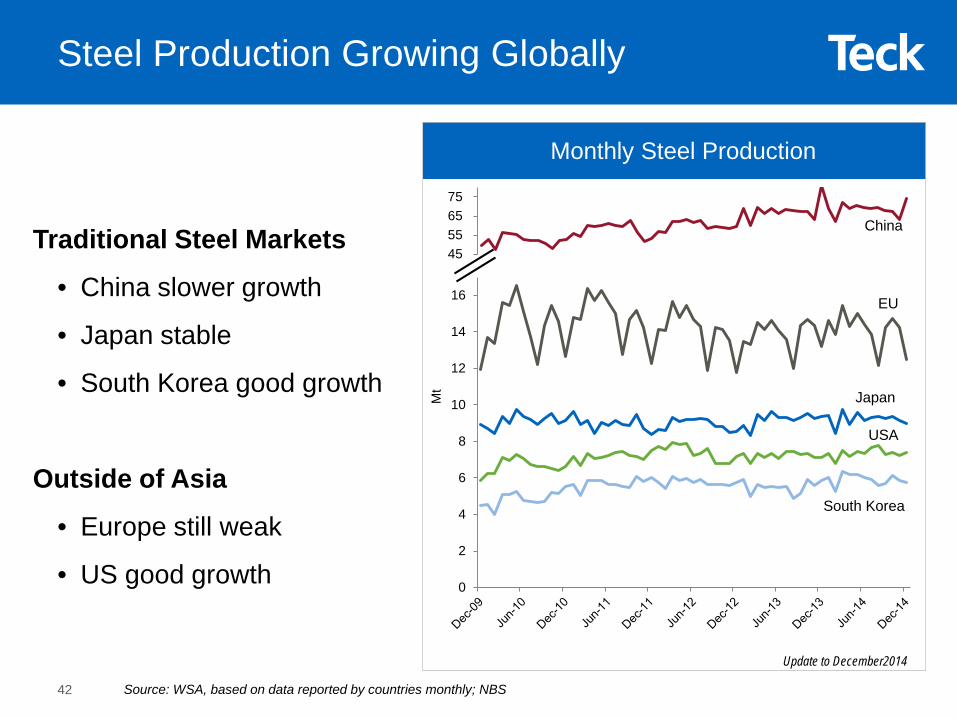

Traditional Steel Markets

• China slower growth

• Japan stable

• South Korea good growth

Outside of Asia

• Europe still weak

• US good growth

Monthly Steel Production

Source: WSA, based on data reported by countries monthly; NBS

Mt

Steel Production Growing Globally

Update to December2014

45 55 65 75

China

0

2

4

6

8

10

12

14

16

Japan

USA

South Korea

EU

42

Xinjiang

Tibet

Qinghai

Sichuan

Inner Mongolia

Henan

Shanxi

GuangxiGuandong

Fujian

Zhejiang

Jiangsu

Shandong

Laioning

Jilin

Heilongjiang

GuizhouHunan

Hubei

Jiangxi

Anhui

ShaanxiGansu

Ningxia

Qinghai

Sichuan

Yunnan

Beijing

Hebei

WISCO Fangchenggang Project• Major infrastructure in place. WISCO Fangchenggang Steel

Company established in Sep to wholly manage the project.• Cold roll line to be commissioned in H1 2015. Other lines are

scheduled to start successively within the year.• Blast furnaces (BFs) in the originally approved plan. Billet

rolling line only at this time. No timeline for BFs currently.• Targeting 5 Mt steel products in 2016 and 10 Mt in 2017.

Baosteel Zhanjiang Project• The environment evaluation was approved in Dec 2014

(~8.8Mt crude steel, 8.2Mt pig iron and 3.2Mt coke).• BF #1 to be commissioned in 2015.

Ningde Steel Base• Proposed but no progress yet.

Relocation to China’s coastline facilitates access to seaborne raw materials

Sources: NBS, CISA

Ansteel Baiyunquan Project• Phase 1 (~ 5.4 Mt pig iron, 5.2 Mt crude

steel and 5 Mt steel products) in 2013.• Phase 2 (5.4 Mt BF) planned but no

progress yet.

Capital Steel Caofeidian Project• Planned 20 Mtpa steel capacity. • Phase 1 (10 Mt) completed in 2010.• Phase 2 (10 Mt) under preparation but no

progress yet.

Shandong Steel Rizhao Project• Planned 21.35 Mt crude steel. • Phase 1 (8.5 Mt) approved in Feb 2013• Construction started in Sep 2014 and

scheduled to commission by the end of 2016.

Chinese Steel Industry Moving to the Coast

43

40%

45%

50%

55%

60%

65%

70%

0100200300400500600700800900

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Mt

Total Coastal Provinces Coastal %

China’s domestic coking coal production is not expected to grow significantly

China’s Domestic Coking Coal Production 2013-2014

China’s Domestic Coking Coal Production

44 Source: Sxcoal

Annual production flat at ~530 Mt

Shanxi coal production to be limited in future• Environment pressures • No new projects to be permitted

before 2020 • Permitted production authorization

to be enforced • Production expected to not exceed

1,000 Mt vs 977 Mt (raw thermal and met) in 2014

-5%

0%

5%

10%

15%

20%

0

10

20

30

40

50

60

Jan-

13

Mar

-13

May

-13

Jul-1

3

Sep

-13

Nov

-13

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep

-14

Nov

-14

Mt

Chinese coking coal production Mt, lhs YTD growth %, rhs

Further Cuts Needed in the Coal Market

Source: Wood Mackenzie, Platts, TEX Report, AME, company & news reports and Teck Resources estimates1. On an operating basis, excluding sustaining capital costs

Seaborne Metallurgical Coal Margin Curve at Spot Price of US$115/t

Brackets indicate producers closed or still

supplying but due to close or deplete inventory

Teck

• ~30 Mt of production cuts announced- Slightly less than half

implemented by year end

• Margin curve shows around one third of seaborne met coal is operating at negative margin1

- Implies further cuts are warranted

• Market balance dependent on additional production cuts

45

60.0

15.413.2

47.7

14.8

6.6

0

10

20

30

40

50

60

70

Seaborne Landborne Stock changeM

t

2013 2014

Source: GTIS, Wood Mackenzie, Mysteel1. Wood Mackenzie forecasts total imports of 96 Mt by 2019

China Rolling 12-Month Coking Coal Imports

46

Growing Steelmaking Coal Imports to China

2019

f

2019F1: 96 Mt

China's Coking Coal Imports and Stock Change at Ports

Imports down by <10% when combined with inventory drawdowns

0

10

20

30

40

50

60

70

80

90

100

Feb-

09Ju

l-09

Dec

-09

May

-10

Oct

-10

Mar

-11

Aug

-11

Jan-

12Ju

n-12

Nov

-12

Apr

-13

Sep

-13

Feb-

14Ju

l-14

Dec

-14

Mt

Seaborne Mongolia

NorthAmerica

~5%Europe~15%

LatinAmerica

~5%

China~25%

High quality, consistency, reliability, long-term supply

Asia excl. China~50%

Source: Teck Resources Limited; 201447

We Are a Leading Steelmaking Coal Supplier To Steel Producers Worldwide

0

50

100

150

200

250

300

350

Q1

2010

Q2

2010

Q3

2010

Q4

2010

Q1

2011

Q2

2011

Q3

2011

Q4

2011

Q1

2012

Q2

2012

Q3

2012

Q4

2012

Q1

2013

Q2

2013

Q3

2013

Q4

2013

Q1

2014

Q2

2014

Q3

2014

Q4

2014

US$

/ to

nne

Teck Realized Price (US$) Benchmark Price

Average realized price discount to benchmark is a function of:1. Product mix: over 90% is hard

coking coal

2. Carry over sales volumes

3. Direction of quarterly benchmark prices and spot prices- Q1 2015 benchmark for

premium products is US$117/t

Hard Coking Coal Benchmark Price

Premium Steelmaking Coal Product

Average realized price discount of ~8%

96%

88%

93%

94%92%

48

• Around the world, and especially in China, blast furnaces are getting larger and increasing PCI rates

• Coke requirements for stable blast furnace operation are becoming increasingly higher

• Teck coals with high hot and cold strength are ideally suited to ensure stable blast furnace operation

• Produce some of the highest hot strengths in the world50 60 70 80 90 100

South Africa

Japan (Sorachl)

Japan(Yubarl)

U.S.A.Canada OtherTeck HCCAustraliaJapanSouth Africa

Australia(hard coking)and Canada

U.S.A.

Australia(soft coking)

10

20

30

40

50

60

70

80

Drum Strength Dl 30 (%)

CSR

Teck HCC

49

Coking Coal Strength

High Quality Hard Coking Coal

0

20

40

60

80

100

120

2014 2015E

US$

/t

Site Costs Transportation Inventory Write-Down

Capitalized Stripping Sustaining Capital

105

89

Teck costs lower than most major competitors

Total Cash Cost 2015 vs. 2014

Steelmaking Coal Costs

50

(US$/t)2014($1.10

CAD/USD)

2015E*($1.25

CAD/USD)

Site1 $49 $41

Transportation 35 $31

IFRS Total $84 $72

Capitalized Stripping $15 $15

Full Cash Cost $99 $86

Sustaining Capex $6 $3

Total Cash Cost $105 $89

* Based on the mid-point of 2015 guidance.1. Includes inventory write-down.

IFRS Costs

0

1

2

3

4

5

6

7

8

Q2/

09Q

3/09

Q4/

09Q

1/10

Q2/

10Q

3/10

Q4/

10Q

1/11

Q2/

11Q

3/11

Q4/

11Q

1/12

Q2/

12Q

3/12

Q4/

12Q

1/13

Q2/

13Q

3/13

Q4/

13Q

1/14

Q2/

14Q

3/14

Milli

on T

onne

s

Capacity Grown to 28 Mt

30

40

50

60

70

80

Q2/

09Q

3/09

Q4/

09Q

1/10

Q2/

10Q

3/10

Q4/

10Q

1/11

Q2/

11Q

3/11

Q4/

11Q

1/12

Q2/

12Q

3/12

Q4/

12Q

1/13

Q2/

13Q

3/13

Q4/

13Q

1/14

Q2/

14

Milli

ons

of B

CM

• Capacity grew from 24 Mt to 28 Mt clean production• Not currently operating at full capacity due to market conditions• Quintette on care and maintenance; available when market conditions improve

Material Moved Quarterly Coal Production

51

Potential for Further Capacity Growth

Potential Production Increase ScenariosGiven Teck’s large resource base, there are a number of options available or under study to allow production growth as the market requires:

• Quintette restart (up to 4 Mtpa)

• Coal Mountain Phase 2, with options from 2 to 4 Mt to extend operations

• Brownfields expansions- Elkview expansion - Fording River expansion- Greenhills expansion

• Capital efficiency and operating cost improvements will be key drivers

-

10

20

30

40

50

Prod

uctio

n (M

t)

FRO GHO CMO EVO LCO

CRO QCO 28 Mt 40 Mt

Time Conceptual

52

>75 Mt of West Coast Port Capacity PlannedTeck Portion at 40 Mt

• Exclusive to Teck • Recently expanded to 12.5 Mt • Planned growth to 18.5 Mt

Westshore Terminals

Neptune Coal Terminal

Ridley Terminals

West Coast Port Capacity

• Current capacity: 12 Mt• Expandable to 25 Mt• Teck contracted at 3 Mt

• Teck is largest customer at 19 Mt• Large stockpile area• Recently expanded to 33 Mt• Planned growth to 36 Mt

Milli

on T

onne

s (N

omin

al)

Teck’s share of capacity exceeds current production plans, including Quintette

12.518

336

7

3

0

5

10

15

20

25

30

35

40

Neptune CoalTerminal

RidleyTerminals

WestshoreTerminals

Current Capacity Planned Growth

53

0%

20%

40%

60%

80%

100%

CO2 NOx Particulate SOxDiesel Natural Gas

LNG for Haul Trucks Project

• Pilot project underway to evaluate running Teck haul trucks on a blend of diesel and LNG- Expected to be running in 2015

• Has the potential to reduce our haul truck fleet fuel bill by $27M annually and lower our CO2 emissions by 35,000 tonnes per year

Comparison of Fuel Cost

$-

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

LNG / Diesel Liter Diesel / LiterGas Cost Liquifaction Carbon Tax Delivery Diesel

Pric

e pe

r Lite

r

Comparison of Emissions

% o

f Die

sel E

mis

sion

s

54

Copper Business Unit & Markets

0

200

400

600

800

1000

0¢

100¢

200¢

300¢

400¢

500¢

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

LME Stocks Price

US¢

/lb

thou

sand

tonn

es

plotted to February 6, 2015

Source: LME

Copper Prices & Stocks

LME Daily Copper Prices & Stocks

56

Copper Concentrate TC/RC

0¢

10¢

20¢

30¢

40¢

50¢

60¢

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Spot Realised TC/RC

TC/R

C –

Nom

inal

US¢

/lb

Source: CRU

plotted to January 2015

Copper Concentrate TC/RC

57

Copper Production Disruptions Continue

-384

-171

-950

-859-776

-851

-945

-524

-941 -947

-831

-930

-297

-1,000

-900

-800

-700

-600

-500

-400

-300

-200

-100

02003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014F 2015F

Thou

sand

tonn

es c

onta

ined

cop

per

Source: ICSG, Wood Mackenzie Teck, company reports

Copper Disruptions

58

China Expected to Add Almost As Much to Global Demand in the Next 15 Years as the Past 25 Years

-

200

400

600

800

1,000

1,200

1,400

1990 1994 1998 2002 2006 2010 2014 2018 2022 2026 20300%

5%

10%

15%

20%

25%

30%

1990 1994 1998 2002 2006 2010 2014 2018 2022 2026 2030

Annual Avg. 13%

Annual Avg. 5%

Annual Avg. 330mt/yr growth

Annual Avg. 505mt/yr growth

Thou

sand

tonn

es

Source: CRU, Wood Mac, Teck

Annual Growth Rate of Chinese Copper Consumption to Slow Dramatically…

… But Will Add Significantly in Additional Tonnage Terms

59

0

100

200

300

400

500

600

700

800

900

1,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Cathode Concs Scrap Blister/Semis

000’

s to

nnes

(con

tent

)

China Now Accounts for >49% of Global Copper Consumption

Source: Antaike

China’s Copper Imports Remain Strong

60

0

500

1,000

1,500

2,000

0

50

100

150

200

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec0

100

200

300

400

500

600

700

0102030405060708090

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0

50

100

150

200

250

300

350

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec0

500

1,000

1,500

2,000

2,500

3,000

3,500

050

100150200250300350400

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

China Copper Imports Continue to Grow

Total contained copper imports up 5.6% YTD

Copper Concentrates Net Imports Refined Copper Net Imports

Copper Anodes Net Imports Scrap Copper Net Imports

20142013

61

ZincBusiness Unit & Markets

Zinc Prices & Stocks

0

200

400

600

800

1,000

1,200

1,400

0¢

50¢

100¢

150¢

200¢

250¢

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Stocks Price

Source: LME

US¢

/lb

thou

sand

tonn

es

plotted to Feb 6, 2015

LME Daily Zinc Prices & Stocks

63

Zinc Treatment Charges

$0

$100

$200

$300

$400

$500

$600

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Spot Annual Realised

US$

/dm

t

Source: Teck, CRU

plotted to January 2015

Zinc Spot TCs vs. Realized Annual TCs

64

Significant Zinc Mine Reductions;Large Short-Term Losses, More Long Term

-600

-500

-400

-300

-200

-100

0

Cen

tury

Ram

pura

Agu

cha

Lish

een

Per

seve

ranc

e

Red

Dog

Pom

orza

ny

Bru

nsw

ick

Zyry

anov

sk

Mae

Sod

Par

agsh

a

Ang

as

-600

-500

-400

-300

-200

-100

0

Cen

tury

Ram

pura

Agu

cha

Lish

een

Sko

rpio

n

Ros

eber

y

Red

Dog

Per

seve

ranc

e

Pom

orza

ny-O

lkus

z

Bru

nsw

ick

Cay

eli

Jagu

ar

Zyry

anov

sk

Akh

zal (

Akt

ogas

k)

Kid

d C

reek

Bra

cem

ac-M

cLeo

d

Source: ICSG, Wood Mackenzie Teck, Company Reports

2013-2017 2013-2020

65

Future Potential for Zinc Consumption

6%

19%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14

China USA

• In 2014 China produced over 822 million tonnes of crude steel and 52 million tonnes of galvanized steel sheet

• In 2014 the US produced 88 million tonnes of crude steel and over 16 million tonnes of galvanized steel sheet

• If China were to galvanize crude steel at half the rate of the US and at the same rate of zinc per tonne of galvanized sheet as the US, then Zinc consumption in China could add a further 2.1 million tonnes or 22% of current global consumption

Source: World Steel, CRU66

% Galvanized Steel of Crude Production

EnergyBusiness Unit & Markets

$-

$20

$40

$60

$80

$100

$120

$-

$20

$40

$60

$80

$100

$120

$140

$160

Jan-07 May-08 Sep-09 Feb-11 Jun-12 Nov-13 Mar-15

WTI

(US$

/bbl

)

CAD

$ ce

nts/

L

WTI (US/bbl) (rhs) Alberta ULSD Rack Rate (lhs)

Diesel & Crude Oil Prices

Spread has widened; Delay in changes in crude oil prices flowing through to diesel prices

Diesel Prices vs. WTI Prices 2007-2014

Source: Alberta Transportation, OPIS.

Average Diesel Premiums:2007-2014: C$0.22/litre2011-2014: C$0.27/litre

68

Source: Baker Hughes

Falling oil rig count will eventually lead to lower oil production

North American Weekly Oil Rig Count

Declining Drilling Activity Will Impact Production

69

• Surge in supply last ~5 years primarily due to US shale oil

• Shale oil field decline rates ~25% to 50%, compared to global average of 8%

• Production correction likely to occur relatively rapidly1,000

1,500

2,000

1/3/

141/

17/1

41/

31/1

42/

14/1

42/

28/1

43/

14/1

43/

28/1

44/

11/1

44/

25/1

45/

9/14

5/23

/14

6/6/

146/

20/1

47/

3/14

7/18

/14

8/1/

148/

15/1

48/

29/1

49/

12/1

49/

26/1

410

/10/

1410

/24/

1411

/7/1

411

/21/

1412

/5/1

412

/19/

141/

2/15

1/16

/15

1/30

115

# O

il R

igs

• Significant value created over long term

• 60% of PV of cash flows beyond year 5

• IRR of 50-year project is only ~1% higher than a 20-year project

• Options for debottlenecking and expansion

50-year assets provide for superior returns operating through many price cycles

The Real Value of Long-Life Assets

Fort Hills Project Indicative Rolling NPV1

1. Indicative NPV assumes US$95 WTI, $1.05 Canadian/US dollar exchange rate, and costs as disclosed with the Fort Hills sanction decision (October 30, 2013).

70

Building An Energy Business

Strategic diversification

Large truck & shovel mining projects

World-class resources

Long-life assets

Mining-friendly jurisdiction

Competitive margins

Minimizing execution risk

Tax effective

71

Mined bitumen is in Teck’s ‘sweet spot’

1. GLJ Petroleum Consultants, December 20132. There is no certainty that it will be commercially viable to produce any portion of the contingent bitumen resources. For more information

about contingent bitumen resources, see Teck’s annual information form dated March 3, 2014 available at www.sedar.com.3. Sproule, December 2013

World-Class Energy Reserves & Resources

No Exploration Risk – No Large Finding Costs

Bitumen ReservesTeck’s Share

(million bbl) Proved Probable Proved Plus Probable

Fort Hills1 414 194 608

Contingent Bitumen Resources2

Project Teck’s Share (million bbl) Low Best High Low Best High

Fort Hills1 0 128 752 0 26 150

Frontier32,360 3,047 3,465 2,360 3,047 3,465

Lease 421

Total 2,360 3,175 4,217 2,360 3,073 3,615

Still to be declared

World Class Energy Reserves & Resources

72

Fort Hills Is One of the Best Undeveloped Oil Sands Mining Leases

Ore grade is a function of the bitumen quantity in the deposit

TV:BIP is a ratio of the total volume of bitumen in place to the total volume of material required to be moved (like a strip ratio)

Strip Ratio vs. Ore Grade

Source: Teck

9.5

10

10.5

11

11.5

12

8910111213

Ore

Gra

de (w

t% b

itum

en)

TV:BIP

Fort Hills

Frontier

• >3 billion bbls of proven plus probable reserves of bitumen

- Production 180,000 barrels per day (bpd) of bitumen

- Teck’s share is significant at 36,000 bpd; equivalent to 13 million barrels per year (Mbpy)

• World-class resource- Average ore grade of 11.4%- Strip ratio of 1.5:1 and TV:BIP of 10.5

• Consistent production year-over-year through multiple decades

- Scheduled to produce first oil as early as Q4 2017

- Expect 90% of planned production capacity within 12 months

73

Fort Hills Is Part Of A New Breed Of Mineable Oil Sands Projects

Mine & Extraction

Diluted Bitumen(Doesn’t meet commercial pipeline specs)

Heavy Crude Conversion Refinery With Coker

Simple RefineryOn-Site Upgrader($10-15B)

New mining projects produce clean, high-quality bitumen and receive a heavy oil price (discounted), but don’t have to invest in an upgrader

‘PFT’ Diluted Bitumen (Meets commercial pipeline specs)

Export Pipeline

Synthetic Oil

Legacy Oil Sands Mining Projects (~30 Years Ago)

Oil Sands Mining Projects Today

Naphtha froth treatment process

Paraffinic froth treatment ‘PFT’ process

Mine & Extraction

74

Suncor has demonstrated strong project execution with Firebag 4, Extraction Plant 300, TROTM, and North Steepbank Extension completed at or below initial projected costs

Suncor is the largest operator in the oil sands and has been developing projects in close proximity to Fort Hills for 50 years

▪ Leveraging Suncor’s project execution experience and deep contractor relationships

▪ Experience in managing large workforces of comparable size in this region

▪ Deploying existing, proven technology

Project Bitumen Capacity1

Millennium/North Steepbank Mine 310-330 kb/d

Firebag In Situ Stages 1-4 180 kb/d

MacKay River In Situ 30 kb/d

Fort Hills 180 kb/d

75 Source: Suncor1. Capacity targets provided above do not necessarily equate to daily production.

Fort Hills’ Project Operator Has A Proven Track Record

Minimizing Execution Risk In The Fort Hills Project

• Cost-driven schedule- “Cheaper rather than sooner”

• Disciplined engineering approach

• “Shovel Ready” • Global sourcing of engineering

and module fabrication• Balanced manpower profileSuncor has completed 4

projects of ~$20 billion over last 5 years, all at or under budget

Benefiting from Suncor’s operational and project development experience

76

1. All costs and capital are based on Suncor’s estimates.2. Go-forward capital is the go-forward amount from the date of the Fort Hills sanction decision (October 30, 2013),

denominated in Canadian dollars and on a fully-escalated basis.

Competitive Costs1 for Fort Hills

Project Capital: ~C$13.5 billion

Teck Capital:• Fully-escalated capital investment:

~C$2.94B over four years (2014-2017), including remaining earn-in of C$240M

• Estimated spending in 2014: C$800M, incurred costs, based on Suncor’s planned project spending of C$3.16B

Operating & Sustaining Costs:• C$25 to $28/bbl total

• Sustaining C$3-5/bbl (included in above)

• Excludes diluent purchase

To be financed by a combination of cash balance, free cash flow and $3B unused line of credit

Fully EscalatedGo-Forward Capital2

$0

$20

$40

$60

$80

$100

$120

$140

Project 1 Project 2 Fort Hills

Cos

ts in

C$

Thou

sand

s pe

r Bar

rel/d

ay

Capital Cost Per Flowing Barrel

Full project cost including spent to date:

C$84

77

Source: Alberta Energy bitumen valuation methodology (http://www.energy.alberta.ca/OilSands/1542.asp)* Based on example exchange rate of $1.25 CAD/USD

Bitumen Netback Calculation Example*

Teck seeks to secure dedicated transportation capacity for Fort Hills volumes to key markets to minimize WCS discount

Bitumen Netback Calculation Model

US$75.00

C$56.50

C$75.00

$0$10$20$30$40$50$60$70$80$90

~75%Bitumen

~25%Diluent

Typical Diluted Bitumen (Dilbit) Blend

Western Canadian Select (WCS) at Hardisty

WTI BitumenNetback

US$60 C$42.75

US$75 C$56.50

US$90 C$70.25

78

$0

$5

$10

$15

$20

$25

$30

$35

$40

$45

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

Differential WTI-WCS

US$

/bar

rel

$0

$20

$40

$60

$80

$100

$120

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-1

WCS Hardisty WTI Cushing

US$

/bar

rel

Heavy Oil Price Differential

West Texas Intermediate (WTI) & Western Canadian Select (WCS) Prices WTI-WCS Differential

Source: Bloomberg, Teck Resources Limited

Fort Hills project economics benefit from recent narrowing of the WTI-WCS differential

Plotted to 2/12/2014

Plotted to 2/12/2014

Long-term WTI-WCS differential

79

Netback2

$56.50/bbl

Cash Margin$31.50

Cash Costs$25.00

LME PriceUS$2.50/lb

Cash MarginUS$1.25

Cash CostsUS$1.25

Competitive Bitumen Margins1

Typical Bitumen Producer

56% Margin

Low Quartile Cost Copper Mine

50% Margin

Fort Hills’ cash margins are expected to be comparable to the lowest cost mining operations

1. Excludes royalties.2. Assuming US$75 WTI, $15 differential WTI to WCS and $0.80 USD/CAD80

Wood Buffalo Pipeline

Extension

NorliteDiluent Pipeline

East Tank Farm Blending w/Condensate

Cheecham Terminal

Hardisty Terminal

Wood Buffalo Pipeline

AthabascaPipeline

WaupisooPipeline

Edmonton Terminal

Fort HillsMine Terminal

Northern CourierHot Bitumen Pipeline

Pipeline LegendExisting New

Logistics Solutions Planned Between Fort Hills, Edmonton and Hardisty

Pipeline/Terminal OperatorNominal Capacity

(kbpd)

TeckCapacity

(kbpd)

Northern Courier Hot Bitumen TransCanada 202 40.4

East Tank Farm- Blending Suncor 292 58.4

Wood Buffalo Blend Pipeline Enbridge 490 58.4

Wood Buffalo Blend Pipeline Extension Enbridge 490 58.4

Norlite Diluent Pipeline Enbridge 130 18

Hardisty Blend Tankage TBD

Teck

OptionsExport Pipe

Rail

Local Market

81

Common Carriage Pipeline• No take or pay commitments• When pipe capacity is constrained, access to capacity

may be apportioned and netback prices are discountedMarkets

• US Mid-Continent

• US Gulf Coast

• Eastern Canada / US East Coast

• West Coast Exports

• East Coast Exports

Western Canada

Contract Carriage Pipeline• Typically requires 10-25 year take or pay commitments• Firm, secure access to capacity, and netbacks are linked

to international benchmark related prices

Rail• More expensive (may require additional capital)• Has the flexibility to alter destinations based on market

conditions• Firm, secure access to capacity, and netbacks are linked

to international benchmark related prices

Multiple Options To Reach International Markets From Western Canada

Teck has the capacity to enter into long-term take-or-pay pipeline agreements

82