blumenthal on scrap tire markets

TRANSCRIPT

www.scrap.org MAY/JUNE 2015 _ Scrap _ 117

After its recessionary downturn in 2011, the U.S. tire recycling market bounced back strongly in 2013, setting a record for the proportion of scrap tires (if not the tonnage) that found a beneficial use. Of the 233 million end-of-life tires the United States generated in 2013, roughly 224 mil-lion, or almost 96 percent, found a home, up nearly 13 percent from 2011, according to the 2013 U.S. Scrap Tire Management Summary, which the Rubber Manufacturers Association (Washington, D.C.) issued in November 2014. “The 2013 market was so much stronger because the recession was ending and we were heading back toward more normal conditions eco-nomically,” says John Sheerin, RMA’s end-of-life tire programs director. Tire-derived fuel was the big winner in the 2011 to 2013 period, while most recycling-focused markets lost ground. RMA’s report gives more detail on each

of the sectors, and Scrap asked market participants to weigh in on the dynam-ics behind the numbers and future directions for the industry.

Fueling DemanDIn 2013, the tire-derived fuel market consumed about 58 percent of recov-ered end-of-life tires in the United States. That’s approximately 129 million tires, or 2.1 million tons of scrap rubber. That’s a significant step up in market share from 2011, when TDF demand dipped to 1.4 million tons. The 2013 results are close to the TDF market’s prior average annual demand of 2.2 million tons—seen in 2005, 2007, and 2009—and the market share of 60 percent it held in 2007. (RMA publishes its market summary based on data from odd-numbered years. The table on page 118 pro-vides data from its five most recent summaries.)

After slipping in the lAst recession, the U.s. tire recycling indUstry regAined its trAction in 2013, thoUgh the tire-derived fUel mArket showed greAter strength thAn rUbber’s recycling-relAted sectors, According to An indUstry mArket report.By Kent Kiser

phot

ogr

aph

s by

scr

ap m

agaz

ine,

aze

k va

st p

aver

s,h

oW

arD

ro

sen

thaL

/Dr

eam

stim

e

118 _ Scrap _ MAY/JUNE 2015 www.scrap.org

To understand TDF’s resurgence, it’s help-ful to recall the market conditions in 2011. The TDF market—and the tire recycling industry as a whole—took a “big hit” that year, a tire recycling industry source says, due to “a variety of economic factors at the time,” which slashed demand from TDF’s main consuming sectors, such as cement kilns, pulp and paper mills, and utilities. In par-ticular, lower construction spending cut demand

for cement, prompting the closure of some kilns, which are major consumers of TDF. “The slow-down in construction meant we didn’t need anywhere near as much cement, so those markets slowed down,” Sheerin says. The recession, in fact, had resulted in the “permanent loss of some older cement kilns,” says Michael Blumenthal of MarShay Inc. (Nyack, N.Y.), a scrap tire consulting firm, and “they are never coming back.”

RMA calls TDF a “cleaner and more

economical alternative to coal,” offering a higher Btu energy value and a lower greenhouse-gas impact than coal. It also tends to be a lower-cost alternative to competing fuels such as wood/bio-mass, coal, natural gas, and petroleum coke. From 2011 to 2013, however, higher prices for compet-ing fuels and improvements in the quality and reliable delivery of TDF helped boost consump-tion of the material almost 49 percent. Cement kilns continued to be the largest TDF-consuming sector in 2013, buying 726,000 tons (equivalent to 44.3 million tires), with their demand increasing 138 percent from 2011. Despite that jump, electric utilities posted the strongest increase in TDF use from 2011 to 2013, rising 260 percent, to 576,000 tons (35.2 million tires). Pulp and paper mills increased their TDF consumption 21 percent, to 716,000 tons (43.7 million tires), but dedicated tires-to-energy facilities reduced their demand 50 percent, to 102,000 tons (6.2 million tires), in the two-year period. The closure of Exeter Energy’s tires-to-energy plant in Sterling, Conn.—which consumed 8 million to 10 million tires a year—was a principal reason for that sector’s decline, the tire recycling industry source says.

One positive development for TDF was a decision in 2013 from the U.S. Environmental

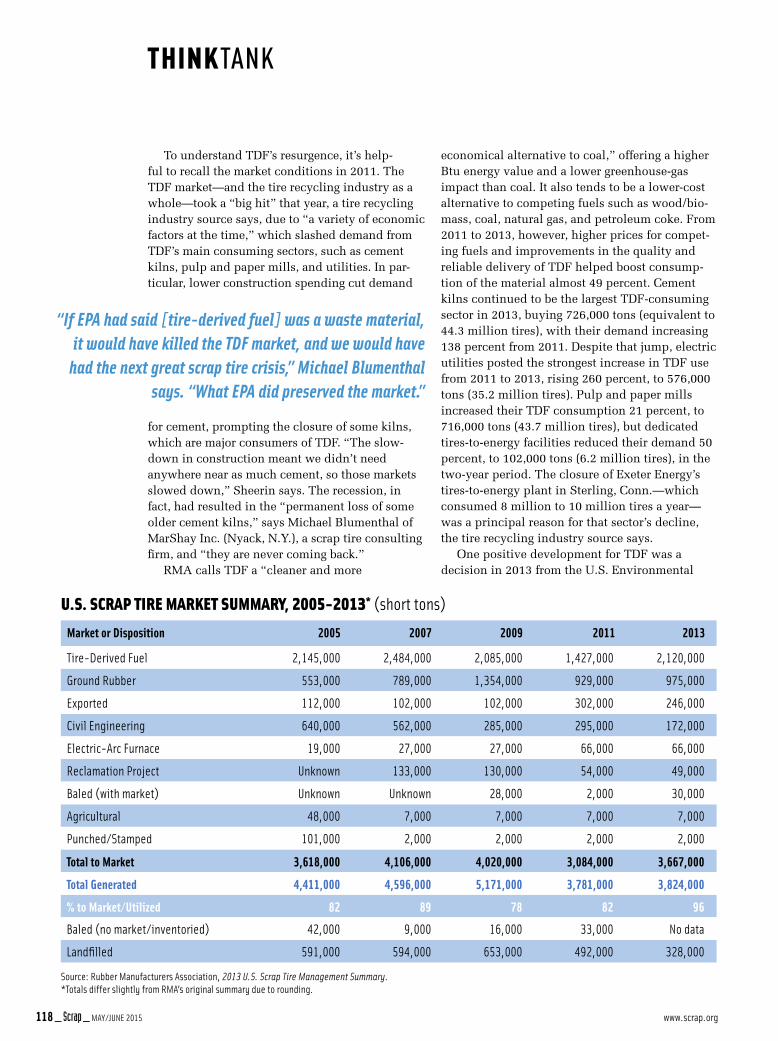

Market or Disposition 2005 2007 2009 2011 2013

Tire-Derived Fuel 2,145,000 2,484,000 2,085,000 1,427,000 2,120,000

Ground Rubber 553,000 789,000 1,354,000 929,000 975,000

Exported 112,000 102,000 102,000 302,000 246,000

Civil Engineering 640,000 562,000 285,000 295,000 172,000

Electric-Arc Furnace 19,000 27,000 27,000 66,000 66,000

Reclamation Project Unknown 133,000 130,000 54,000 49,000

Baled (with market) Unknown Unknown 28,000 2,000 30,000

Agricultural 48,000 7,000 7,000 7,000 7,000

Punched/Stamped 101,000 2,000 2,000 2,000 2,000

total to Market 3,618,000 4,106,000 4,020,000 3,084,000 3,667,000

total Generated 4,411,000 4,596,000 5,171,000 3,781,000 3,824,000

% to Market/Utilized 82 89 78 82 96

Baled (no market/inventoried) 42,000 9,000 16,000 33,000 No data

Landfilled 591,000 594,000 653,000 492,000 328,000

u.S. Scrap Tire markeT Summary, 2005-2013* (short tons)

Source: Rubber Manufacturers Association, 2013 U.S. Scrap Tire Management Summary.*Totals differ slightly from RMA’s original summary due to rounding.

“If EPA had said [tire-derived fuel] was a waste material, it would have killed the TDF market, and we would have

had the next great scrap tire crisis,” Michael Blumenthal says. “What EPA did preserved the market.”

www.scrap.org MAY/JUNE 2015 _ Scrap _ 119

Protection Agency (Washington, D.C.) classifying scrap tires as a nonhaz-ardous secondary material—and not solid waste—when used as a fuel in a combustion unit. “If EPA had said TDF was a waste material, it would have killed the TDF market, and we would have had the next great scrap tire crisis,” Blumenthal says. “What EPA did preserved the market.” Now, as a nonwaste fuel, TDF might have greater appeal to boiler consumers that currently don’t use the material. “It could become more of an accepted fuel as long as the quality of the product is there, meaning it’s properly sized and the steel removal is appropriate for the particular boiler application,” the tire recycling industry source says.

The EPA also recognized that scrap tires contain biomass—about 25 percent of their content is natural rubber—which opens the door for TDF consumers to claim tax or emis-sions credits for burning a biomass fuel, Blumenthal notes. As Sheerin explains, the biomass ruling “gives TDF a further advantage over mineral-type fuels,” and it could elevate the TDF market in the future. “When you do greenhouse-gas accounting, TDF is going to come out better because of the natural latex content,” he says.

Recycling and Reuse MaRketsEven as the TDF market rebounded strongly in the 2011 to 2013 period, most non-TDF sectors nosed down-ward. As a group, all non-TDF uses of reclaimed tire rubber slipped 7 per-cent, from approximately 1.7 million tons in 2011 to about 1.5 million tons in 2013.Grinding down. Ground rubber contin-ued to be the largest non-TDF market for scrap tires. These applications consumed 975,000 tons of tire rubber, which was 63 percent of the non-TDF use of scrap tires and 27 percent of all end-use demand, according to RMA figures. Ground rubber demand in 2013 was up about 5 percent from 2011 but down 28 percent from its 2009

Features a 10-hp, 3-phase electric motor or 18-hp gas engine with electric start. The TC-710 Recycling Baler compacts aluminumcans or plastic bottles into 20" X 20" X 36" bales weighing approximately 150 1bs. TheTC-710 is mobile and conveniently fits intoa truck bed or trailer, which can be usedcurbside or in-plant.

120 _ Scrap _ MAY/JUNE 2015 www.scrap.org

peak. Finely ground rubber goes into applica-tions such as new rubber products, playground and other sports surfacing, and rubber-modified asphalt, while larger ground rubber pieces become landscaping mulch and loose-fill playground material. “When the recession came, tax dollars went down, budgets were slashed, and demand

from ground rubber’s main markets went down,” Blumenthal says. “Market demand hasn’t come back as strongly as many had hoped.”

The molded/extruded product sector used 33 percent of ground rubber sold in 2013, followed by the playground/mulch sector (31 percent), sports surfacing (17 percent), asphalt (7 percent), and automotive and export, each with 6 per-cent. The playground/mulch market was ground

rubber’s only large-scale niche to grow in the two-year period, rising 25 percent, from 160,000 tons in 2011 to 200,000 tons in 2013. Aside from ground rubber exports, which increased 78 percent, to 40,000 tons, all other ground rubber sectors declined in 2013 compared with 2011. Demand for ground rubber for sports surfacing and molded/extruded products fell 19 percent and 12 percent, respectively, but the biggest decline was in the asphalt market, which fell 59 percent, from 110,000 tons in 2011 to 45,000 tons in 2013. In the recession, state transportation departments trimmed their use of rubber-modified asphalt, Blumenthal says, and that niche “never really regained its footing.”

Currently, ground rubber’s biggest challenge is the debate over whether it causes health prob-lems in people who play on synthetic turf fields with ground rubber infill. “The concerns are not science-based,” Sheerin says. “They’re anecdotal stories that mention cancer and get people emo-tionally excited, but the science hasn’t supported

Currently, ground rubber’s biggest challenge is the debate over whether it causes health problems in people

who play on synthetic turf fields with ground rubber infill.

D.C. Shredder Power!D.C. Shredder Power!

VFD/SCR Drives • Generators • Switchgear and ControlsTransformers • New & Rebuilt • Drill Motor Repair Specialist

AC/DC Motors • Electrical Controls • Complete SystemsDesign Engineering • Turnkey Solutions

713.225.4300www.amerimexinc.com

AmerimexHalf_DCPwr_ND09:Layout 1 11/5/2009 9:43 AM Page 1

122 _ Scrap _ MAY/JUNE 2015 www.scrap.org

any links between the product and those types of diseases.” Only about 17 percent of ground rubber went into sports surfacing in 2013, but the “sideways glances” of this concern “stretch into the playground and mulch markets, where you have people interacting with the product,” Sheerin notes. Together, roughly half of ground rubber went into those markets in 2013. Although ground rubber produc-ers say the controversy has not caused a big slowdown in orders, he says, “the press doesn’t help.” Blumenthal

expects the controversy to continue, “and ground rubber markets will be less than they might otherwise have been,” he says.An uncivil decline. The same downtrend played out in even more dramatic fashion in the civil engineering sector, which uses tire shreds in road and landfill construction, septic tank leach fields, and as alternative daily cover in landfill operations as well as other construction applications. In 2013, the civil engineering market consumed 172,000 tons of tires, which was about 11 percent of non-TDF demand and roughly 5 percent of all recovered tires that went to an end-use market that year. Since its peak in 2005, the civil engineering market has declined, in part due to competition from TDF consumers, who generally pay more for the rubber than civil engineering consumers, the tire recycling industry source says. Civil engineering projects also can require large tonnages of pro-cessed rubber on short notice, which can pose purchasing, storage, and logistical problems for tire recyclers,

Civil engineering projects can require large tonnages of processed rubber on short notice, which can pose purchasing, storage, and logistical problems for tire recyclers.

Call us today for a price quote (888) 356-WHLS (9457)

888-274-6010www.maurermfg.com

STANDARD FEATURES:

• Trailer lengths: 40', 44', & 48'

• Choice of 4', 5', 6', or 8' side walls

• 22.5K tandem axles with one axle ABS brake

• 3-leaf heavy-duty spring suspension, closed tandem

• 2-speed Holland Atlas 55 landing gear

• Sealed wiring system designed for Maurer by Trucklite

• All exterior mating surfaces are caulked prior to paint

• Diamond Vogel polyurethane primer and paint

• D.O.T. approved conspicuity tape and rubber-mounted lights

• Manifest holder

• Anti-sailmudflaps

Trailers

Available with

HARDOX® 450

www.scrap.org MAY/JUNE 2015 _ Scrap _ 123

Sheerin says. “When the project’s a go, the contractor might suddenly need 50,000 tons of tires, so the recycler would need to have that material in stock.” Such challenges “created more problems than it was worth for many processors, so interest in this market has waned,” Blumenthal says.

That said, there still are “viable applications for civil engineering material, especially out West, where you have the remaining stockpiles of tires,” Blumenthal says. Sheerin concurs, noting that this sector could see a boost thanks to renewed interest in Colorado and California, which are using scrap rubber in new civil engi-neering projects. California, for one, has announced a grant for a project that will use tire-derived aggregate as a vibration dampener for a light-rail line. Holding steady. Several smaller markets also consume U.S. scrap tires, such as professionally engineered tire bales, reclamation projects (primarily to build up mining sites), steel produc-tion in electric-arc furnaces, agricul-tural applications, and products that are punched, pressed, or stamped from scrap tires. The latter three markets remained constant from 2011 to 2013, with EAFs consuming about 66,000 tons of scrap tires, agricultural uses consuming about 7,000 tons, and punched, pressed, or stamped prod-ucts using nearly 2,000 tons. Fewer tires—about 49,000 tons—went into reclamation projects in 2013, a decline of just over 9 percent. Texas was the main user of scrap tire rubber for land reclamation projects—principally at mining sites—and “it just stopped that program,” Blumenthal says.

The engineered bale market, which dipped significantly in 2011, returned in 2013 to its previous level of about 30,000 tons of demand, but market par-ticipants don’t see much growth poten-tial for this niche going forward. Most of the bales are exported from the West Coast to consumers in Asia for use as TDF or feedstock for other processes, but “that process has stopped—China

InternatIonal traders of Copper • Brass • Aluminum • Stainless Steel

& all Non-Ferrous Metals

810 S. Flower Street, Suite 1202Los Angeles, CA 90017(213) 228-6200 • Fax (213) [email protected]

Affiliate Office in the UKTANGENT TRADING LTD.1 Dollis Mews London N3 1HH, UK081-349-4822 • Fax: 081-359-4860

124 _ Scrap _ MAY/JUNE 2015 www.scrap.org

has closed that door,” Sheerin says. U.S. exports of scrap tires in general peaked in 2011, then slipped 19 per-cent, to about 246,000 tons, in 2013, and Blumenthal sees little potential for growth in that sector. “The export market came and went,” he says. “It helped save the market during the recession, but that market has gone away, and it isn’t coming back in the foreseeable future.”

shRinking stockpilesRMA’s 2013 report indicates the ton-nage of landfilled tires and the num-ber of scrap tires in U.S. stockpiles both are steadily falling. From a peak of 653,000 tons in 2009, the number of landfilled tires fell 25 percent, to 492,000 tons, in 2011 and 33 percent, to about 328,000 tons, in 2013. As for stockpiled tires, the U.S. backlog has dwindled from about a billion scrap

tires in 1990 to roughly 75 million in 2013, a 92-percent reduction. “That’s a major achievement,” Blumenthal says, “and everybody who has been involved in it should be proud.” Colorado—the state with the largest remaining tire stockpiles—has a new program that could cut an additional 30 million tires from the U.S. stock-pile, Sheerin says. “We’re hopeful this law will be successful for the state.”

Despite such progress, the U.S. stockpile will never reach zero, these industry watchers say. “There will always be tires going to landfill—that’s as simple as it gets,” Blumenthal says. “There are states—primarily those with sparse population and wide open space—that basically don’t have any kind of tire management plan, and they don’t have any volumes.” According to

The Southeast will continue to be the “brightest spot” in the scrap tire market thanks to its high consumption of TDF, John Sheerin says.

www.sasforks.com phone: 877 727 3675fax: 920 845 2309

TURNKEY MACHINE READY TO SHIP!

[email protected] - west [email protected] - [email protected] - international

727-568-7075 • [email protected] • tranact.com

You’ll Buy It For Compliance... You’ll Love It For Its Power And Simplicity!

www.scrap.org MAY/JUNE 2015 _ Scrap _ 125

RMA’s 2013 report, 12 states allow the landfilling of whole tires, and 38 allow the land disposal of cut or shredded tires. Even though discarding tires isn’t ideal, it’s “better than leaving them out in the environment,” Blumenthal says. “It’s not a market, but at least they’re being managed.”

the Road aheadSheerin expects the Southeast to continue to be the “brightest spot” in the scrap tire market thanks to its high consumption of TDF. “There’s so much demand there for TDF that if you can get tires in that area, they’re going to be used. The market is pretty much sold out.” The Northeast, on the other hand, remains a concern due to the closing of the Exeter Energy plant in Connecticut. New England doesn’t have many mar-ket options for scrap tires, Blumenthal says. One of the two pulp and paper mills in Maine that consumed tires has been down for a while, he says, and “tires are piling up in the pipeline. You can only sustain that kind of lack of markets for so long.” According to Sheerin, “there was great concern that the Exeter closure would lead to a lot more illegal dumping and stockpiles, but, fortunately, that has not hap-pened.” Even so, he says, “we’re still concerned and would like to see more markets developing in the Northeast.”

Looking at the broader picture, Blumenthal sees tire recycling mar-kets plateauing in the near term. “I just don’t see any major upswings in the marketplace; there’s nothing out there that’s a game-changer,” he says. On a more optimistic, longer-term note, Sheerin says, “new technologies and evolving existing technology may become commercially viable further down the road and develop a more sophisticated processing industry. The tire industry is not satisfied with the status quo.” S

Kent Kiser is publisher of Scrap and assis-

tant vice president of industry communica-

tions for ISRI.

Want to increase your energy efficiency?Call Quad Plus for your E-Ticket ™

• AC & DC Shredder Drives and Motors • Power Company Approval • High Voltage Design

Contact us:(815) 724-2240 QuadPlusRecycling.com