bloom public school sample paper (2016-17) accountancy … · bloom public school sample paper...

TRANSCRIPT

XI/Accountancy 1

BLOOM PUBLIC SCHOOL

SAMPLE PAPER (2016-17)

Accountancy (Q + KEY) Class-XI

TIME: 3 Hours

M.M: 90

Q.1 Ashok Purchase goods for from Delhi Traders for Rs 2,00,000.As per terms, if Ashok

made full payment within 21 days, He will get cash discount at 2.5%.Ashok paid

1,50,000 within stipulated time. How much discount he will get.

A) he will not get any discount because he has not paid full amount.

(1)

Q.2 Accounting records transactions and events that can be measured in money terms. Is

this in your opinion , a limitation or an advantage

Ans There are other important events which have far reaching effect on business but

they are not recorded as they can’t be measured in money for example Loss of

production due to machine breakdown

(1)

Q.3 What is Imprest System of Accounting?

Ans Imprest means to provide some money for expenses in advance. It is convenient to

entrust a definite sum of money to the petty cashier in the beginning of a period and to

reimburse him for payments made at the end of the period. Thus, he will have again the fixed

amount in the beginning of the period. Such a system is known as the ‘Imprest system of

petty cash.’ With the introduction of this system small expenses of regular type are

maintained separately, and it is easy to analyse and control them better.

(1)

Q.4 Name the category of Account That is not balanced.

Ans-: Nominal accounts are not balanced. They are totaled and transferred to Profit

and Loss account at the end of accounting year

(1)

Q.5 How does matching principal apply to Depreciation?

A) According to matching principle all costs which are incurred in an accounting

year should be charged against the revenue of that period. Hence depreciation of

current year is charges against the current year's revenue .Full cost of assets is not

treated as an expense in the year of its purchase itself rather it us spread over its

useful life

(1)

Q.6 What is the Process of Accounting

Ans Financial Transaction, Recording, Classifying, Summarising, Analysis

and Communication

(1)

Q.7 Identify the concept of accounting being violated and the underlying value being ignored in (3)

XI/Accountancy 2

the following cases:

a. A company purchased goods for 5,00,000 and sold 80% of such goods during the

year. The market value of remaining goods was 90,000. The company valued the

closing stock at cost.

b. A customer of X Ltd. has discontinued his business. He used to purchase 30% of the

total goods produced by X Ltd. He has not informed X Ltd. about this closure of the

business.

Q.8 How Expense and Expenditure different from each other?

A) Expense is cost incurred in producing and selling the goods and services.(Amount

paid for rent, salary etc)

B) Expenditure is any disbursement of cash or transfer of property or incurring a

liability for the purpose of acquiring assets , goods or services is called expenditure.

It means any type of payment for the receipt of a benefit is termed as expenditure

(3)

Q.9 Following accounts are being maintained in the books of Shri Ajit. Classify them as

Personal, Real or Nominal accounts.

a) Carriage inwards d) Bank Overdraft

b) Accrued Income e) Outstanding Rent Account

c) Haryana Education Board f) Commission Received Account

ans

a) Carriage inwards(N) d) Bank Overdraft(p)

b) Accrued Income (p) e) Outstanding Rent Account(P)

c) Haryana Education Board (P) f) Commission Received(N)

(3)

Q.10 Differentiate between Cash book and cash Account

Cash Account

Cash Book

1. Cash account is a Ledger account.

2. Posting is done in Cash account from the

Journal.

It is a separate book maintained for recording

Cash transactions.

It is a Book of original entry i.e. transactions

are first entered in the cashbook and then

transferred to other ledger accounts.

3. It records one aspect of a transaction. It records both the aspects of a transaction.

(3)

Q.11 Explain the concept of Journal proper.What type of entries appear in a Journal Proper

Ans)

(3)

XI/Accountancy 3

Journal Proper is a book maintained to record transactions, which do not find place in special

journals.

Following transactions are recorded in Journal Proper in case, when a firm maintained all

specific journals:

1. Opening entry at the beginning of the period;

2. All adjustment entries such as prepaid, outstanding, accrued and advance, expenses and

incomes;

3. Rectification entries to rectify the errors in recording transactions;

4. Transfer entries to transfer the closing balances; and

5. All other entries which have not entered in any of the other books.

Q.12 How will you show following Transaction in Cash Book-:

Dec 5 Received cheque from Rehaan Rs 18,000 allowed him discount Rs1000

Dec 12 Cheque Received from Rehaan deposited in Bank.

Dec 19 Received a cheque for Rs 15,000 from John, which was endorsed to Sophia on 27th

Dec.

Ans-:

Journal Proper

Cheques in hand

Discount allowed

To Rehaan

18000

1000

19000

In cash book

Dec 19 Cheques in Hand

To John

Dec 27 Sophia

To Cheques in hand

15,000

15,000

15,000

15,000

(3)

XI/Accountancy 4

Q.13 Give the journal entries corresponding to the narration given below:

Journal in the books of ………

Date Particulars L.

F

Amount

(Dr)

Amount(Cr)

April 3 Cash a/c ………. Dr

……………………………………

Dr

To …………………

(Horse which was bought for Rs

15,000 died and its carcass sold for

Rs 1,000)

Cash a/c Dr

Profit & Loss/c Dr

To Live Stock

April

16

………. Dr

……………………………………

Dr

To Cash a/c

(Paid landlord Rs 12,000 for rent.

Two third of building is occupied

by proprietor for personal use)

Rent a/c Dr

Drawings a/c Dr

To cash

April

30

…………………………………….

Dr

……………………………………

Dr

To Bank a/c

(Paid by cheque Rs 6,000 as fire

(4)

XI/Accountancy 5

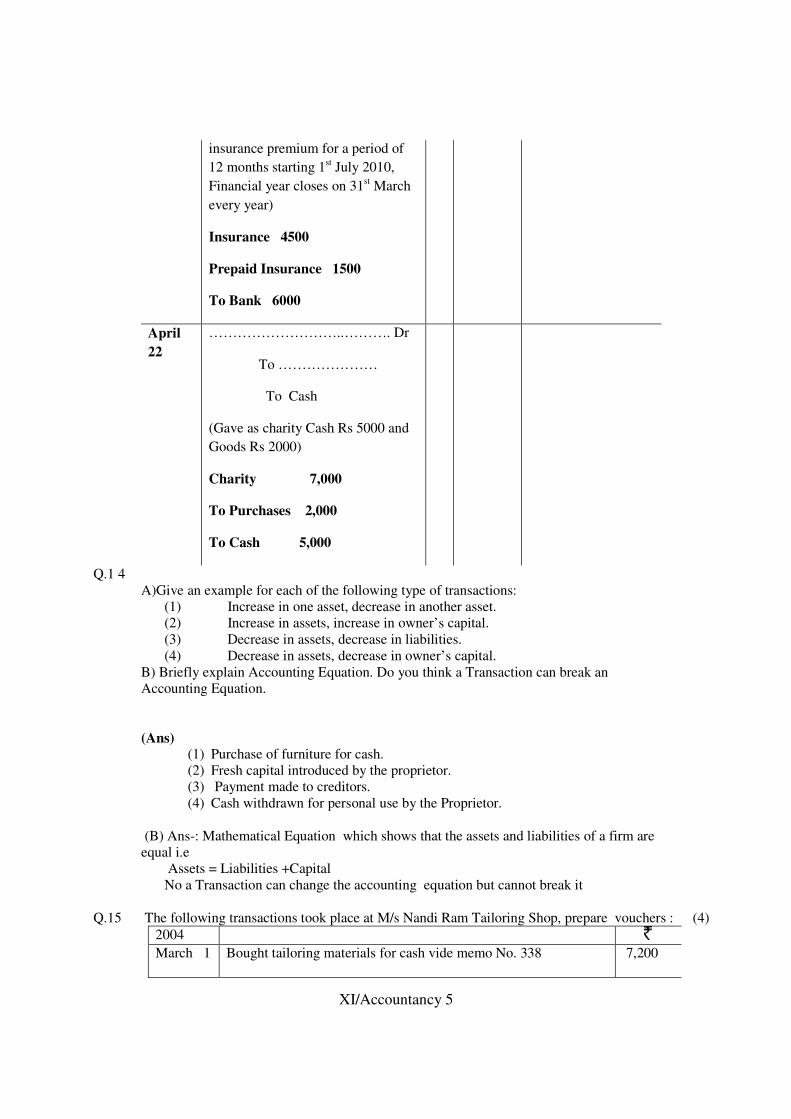

insurance premium for a period of

12 months starting 1st July 2010,

Financial year closes on 31st March

every year)

Insurance 4500

Prepaid Insurance 1500

To Bank 6000

April

22

………………………..………. Dr

To …………………

To Cash

(Gave as charity Cash Rs 5000 and

Goods Rs 2000)

Charity 7,000

To Purchases 2,000

To Cash 5,000

Q.1 4

A)Give an example for each of the following type of transactions:

(1) Increase in one asset, decrease in another asset.

(2) Increase in assets, increase in owner’s capital.

(3) Decrease in assets, decrease in liabilities.

(4) Decrease in assets, decrease in owner’s capital.

B) Briefly explain Accounting Equation. Do you think a Transaction can break an

Accounting Equation.

(Ans) (1) Purchase of furniture for cash.

(2) Fresh capital introduced by the proprietor.

(3) Payment made to creditors.

(4) Cash withdrawn for personal use by the Proprietor.

(B) Ans-: Mathematical Equation which shows that the assets and liabilities of a firm are

equal i.e

Assets = Liabilities +Capital

No a Transaction can change the accounting equation but cannot break it

Q.15 The following transactions took place at M/s Nandi Ram Tailoring Shop, prepare vouchers :

2004

March 1

Bought tailoring materials for cash vide memo No. 338

7,200

(4)

XI/Accountancy 6

March 28 Wages Paid for the month of February, 2004, wide wage sheet No.

39

5,000

Ans-:

Q.16 Vijay,a consultant during the financial year 2014-15 earned Rs 4,00,000. Out of which he

received Rs 3,50,000.He incurred an expense of Rs 1,70,000 out of which Rs 40,000 are

outstanding .He also received consultancy fee relating to previous year Rs 45,000 and also

paid Rs 20,000 expenses of last year.

You are require to determine the income for the year if

1)He follows cash basis of accounting

2)He follows accrual basis of accounting

Ans-: 2,45,000 ,2,30,000

(4)

Q.17 1. Cash handed over to petty cashier Rs 10,000

2. Sold goods to Ajay for Rs 50,000 allowing 5% Cash Discount and10% Trade

Discount. Half of the amount was received by cheque within specified time.

3. An old Machine with the book value of Rs 80,000 is exchanged for a new machine

of Rs 2,40,000.The old machine is valued at Rs 50,000 for exchange purpose by

Machine tools ltd.

ANS

1) Petty Cash a/c

To cash a/c

10,000

10,000

1) Ajay

Bank

Discount allowed

To Sales

22500

21375

1125

45000

2) Machine (New) a/c dr

P&L a/c

To machine(Old)

To Machine tools

2,40,000

30,000

80,000

1,90,000

(3)

XI/Accountancy 7

.

Q.18 Draft Trial Balance-:

Carriage Inward 12458 Stock on 1st April 225000

Sales 235000 Loan from UTI Bank 300000

Return Inward 3350 Carriage Outward 42162

Return Outward 12167 Discount Allowed 1830

Investment @10% 200000 Discount Received 10033

Interest on Investment 20000 Drawings 10033

Interest on Loan 10000 Purchases 100000

Sundry Creditors 30500 Bad Debts 5100

Solution

Dr Cr

Carriage Inward 12458

Carriage Outward 42162 Loan from UTI Bank 300000

Return Inward 3350 Sales 235000

Discount Allowed 1830 Return Outward 12167

Investment @10% 200000 Discount Received 10033

Purchases 100000 Sundry Creditors 30500

Interest on Loan 10000 Interest on Investment 20000

Drawings 10033 Bad Debts 5100

Stock on 1st April 225000

6,12,800 6,12,800

(6)

XI/Accountancy 8

Q.19 Write up the Purchases and Sales Books from the following transactions and post their totals

to the ledger.

Date Details

1998

April 1

Purchased goods from Ram Prasad, Bombay

100 meters silk @ Rs. 4.50 per metre

75 meters velvet @ Rs. 8.00 per meter

April 10 Sold goods to Sita Ram, Ahmedabad

60 metres silk @ Rs. 5 per meter

50 metres @ Rs. 8.25 per meter

April 12

Sold to Radhey Sham, Delhi

30 metres silk @ Rs. 5.25 per meter

20 metres velvet @ Rs. 8.50 per meter.

April 18

Roop narain & sons purchased from us

10 meters silk @ Rs. 6 per meter

5 meters velvet @ Rs. 8.75 per meter

April 20 Purchased goods from Hari Ram & sons, Delhi

50 pieces prints @ Rs. 13 per piece

80 pieces calico @ Rs. 6.50 per piece

April 22 Purchased from Man Mohan Lal, Varanasi

Shirting cloth Rs. 1,000

Sarees Rs. 6,000

April 23

Sold to Brij Mohan & Sons, Mathura

Shirting cloth Rs. 700

Sarees Rs. 2,500

April 28 Shri Ram & Bros Hapur Sold to us

Long cloth 10 piece @ Rs. 102 per piece

Dhoties 100 pairs @ Rs. 25 per pair

Ans) 19

PURCHASES BOOK

Date Particulars Details Total Rs.

1998

April 1 Ram Prasad, Bombay 100 meters silk @ Rs. 4.50 per metre

75 meters velvet @ Rs. 8.00 per meter

450

600 1050

April 20 Hari Ram & sons, Delhi

XI/Accountancy 9

50 pieces prints @ Rs. 13 per piece

80 pieces calico @ Rs. 6.50 per piece

650

520

1,170

April 22 Man Mohan Lal, Varanasi Shirting cloth Rs. 1,000

Sarees Rs. 6,000

1,000

6,000

7,000

April 28 Shri Ram & Bros Hapur Long cloth 10 piece @ Rs. 102 per piece

Dhoties 100 pairs @ Rs. 25 per pair

1,020

2,500

3,520

April 30 Purchases a/c ...............................Dr 12,740

Dr. PURCHASES ACCOUNT Cr.

Date Particulars Amount Date Particulars Amount

1998

April 30

To amount as per

purchase book

12,740

SALES BOOK

Date Particulars Details Total Rs.

1998

April 10 Sita Ram, Ahmedabad 60 metres silk @ Rs. 5 per meter

50 metres @ Rs. 8.25 per meter

300

412.50 712.50

April 12 Radhey Sham, Delhi 30 metres silk @ Rs. 5.25 per meter

20 metres velvet @ Rs. 8.50 per meter.

157.50

170 327.50

April 18 Roop narain & sons 10 meters silk @ Rs. 6 per meter

5 meters velvet @ Rs. 8.75 per meter

60

43.75 103.75

April 23 Brij Mohan & Sons, Mathura Shirting cloth Rs. 700

Sarees Rs. 2,500

700

2,500

3,200

April 30 Sales a/c ..............Cr.

4,343.75

Dr. SALES ACCOUNT Cr.

Date Particulars Amount Date Particulars Amount

XI/Accountancy 10

12,740 1998

April

30

By amount as per

sales book

4,343.75

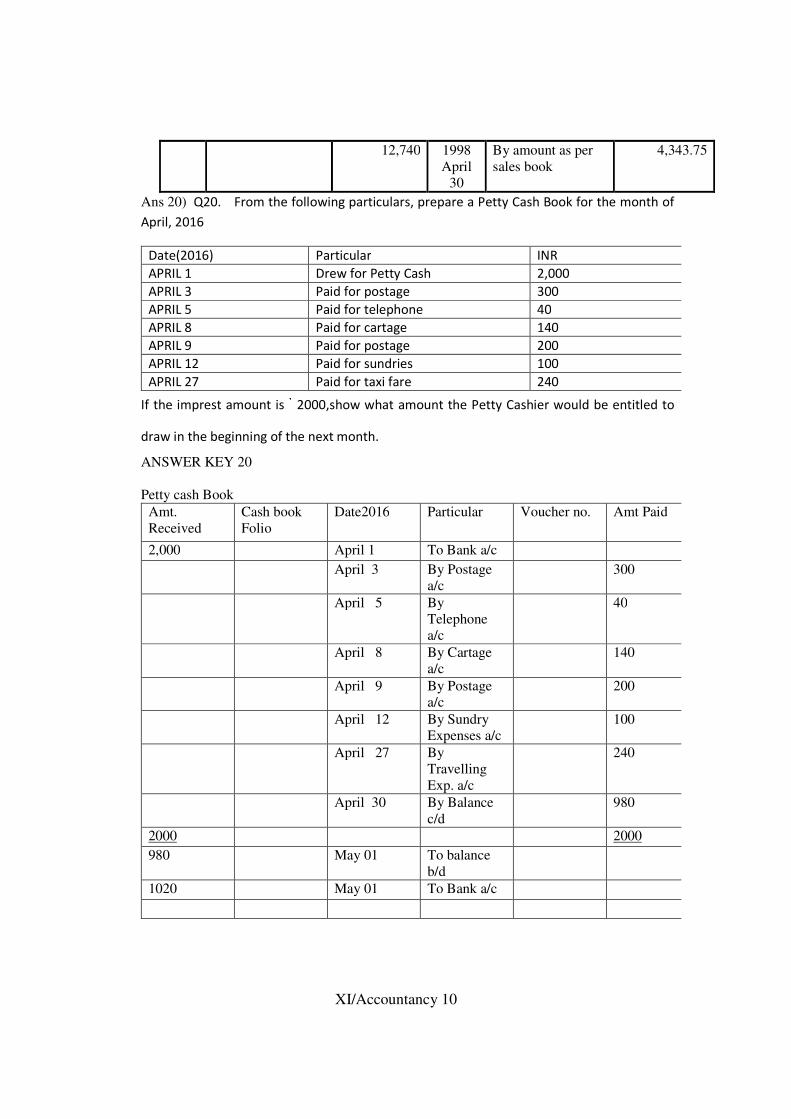

Ans 20) Q20. From the following particulars, prepare a Petty Cash Book for the month of

April, 2016

Date(2016) Particular INR

APRIL 1 Drew for Petty Cash 2,000

APRIL 3 Paid for postage 300

APRIL 5 Paid for telephone 40

APRIL 8 Paid for cartage 140

APRIL 9 Paid for postage 200

APRIL 12 Paid for sundries 100

APRIL 27 Paid for taxi fare 240

If the imprest amount is ` 2000,show what amount the Petty Cashier would be entitled to

draw in the beginning of the next month.

ANSWER KEY 20

Petty cash Book

Amt.

Received

Cash book

Folio

Date2016 Particular Voucher no. Amt Paid

2,000 April 1 To Bank a/c

April 3 By Postage

a/c

300

April 5 By

Telephone

a/c

40

April 8 By Cartage

a/c

140

April 9 By Postage

a/c

200

April 12 By Sundry

Expenses a/c

100

April 27 By

Travelling

Exp. a/c

240

April 30 By Balance

c/d

980

2000 2000

980 May 01 To balance

b/d

1020 May 01 To Bank a/c

XI/Accountancy 11

Q.21

Journalise the following transactions:

Date

April 2 Wood used to make office Furniture Rs 20000

April 9 Goods sold to Sunil costing Rs 2,60,000 for cash at a profit of 20% on cost

April 17 Goods worth Rs. 8,000 were destroyed by fire and it was fully insured.

April 8 Salaries outstanding for previous month was paid Rs 7000

April 28 Purchased goods from Neelam for Rs 2,000 and supplied these to Kashis for Rs

2400.Kashish returned goods worth Rs 240, which in turn were returned to Neelam

April 29 Bank charges for its services Rs 2000

April 22 Bought Shares in Colgate ltd for Rs 50,000 and brokerage paid @2%.Allpayments

made by cheque

Ans

Particulars Dr Cr

April 2 Furniture

To Purchases

20000

20000

April 8 Outstanding Salary

To Cash a/c

7000

7000

April 9 Cash

To Sales

3,12,000

3,12,000

April 17 Loss by fire to purchases A/c Dr.

To purchases A/c

Insurance Co. Dr.

To loss by fire

8,000

8,000

8,000

8,000

April 22 Investment

To Bank

51,000

51,000

April 28 a) Purchase

To Neelam

b) Kashish

To Sales

c) Sales Return

To Kashish

d) Neelam

To Purchase Return

2000

2400

240

200

2000

2400

240

200

April 29 Bank charges a/c Dr

To Bank a/c

51,000

51,000

(6)

Q.22 Post the above Journal entries in Ledgers of Cash, Bank, Purchase and Sale (6)

Q.23 Prepare Bank Reconciliation Statement of Dheeraj as on 31st March from the following

information-:

(8)

XI/Accountancy 12

(a) Debit balance as per Pass Book Rs 25,500

(b) Bank collected a cheque of Rs 2500 on behalf of Dheeraj but wrongly credited to

Dheeraj’s Account.

(c) Withdrawal column of Cash Book was under cast by Rs 100

(d) Cheque of Rs 3572 deposited into bank was recorded as Rs 3,752 in Pass Book.

(e) A cheque of Rs 5,000 collected from Megha was debited in the Pass Book.

(f) Pass Book shows a credit for a cheque amounting Rs 1500 deposited by Dhiraj.

(g) Cheque of Rs 2,300 issued to Divya was recorded twice in the Pass Book.

(h) A cheque of Rs 1,000 was taken in the Cash column.

Solution-:

Bank Reconciliation Statement of Dheeraj as on 31st March

Debit balance as per Pass Book

25,500

Cheque of Rs 2500 on behalf of Dheeraj but wrongly

credited to Dheeraj’s Account.

2,500

Withdrawal column of Cash Book was under cast by Rs 100

100

Cheque of Rs 3572 deposited into bank was recorded as Rs

3,752 in Pass Book

180

cheque of Rs 5,000 collected from Megha was debited in the

Pass Book

10,000

Pass Book shows a credit for a cheque amounting Rs 1500

deposited by Dhiraj.

1500

Cheque of Rs 2,300 issued to Divya was recorded twice in

the Pass Book.

2300

cheque of Rs 1,000 was taken in the Cash column

1000

Credit balance as per Cash Book

18280

30,680 30,680

XI/Accountancy 13

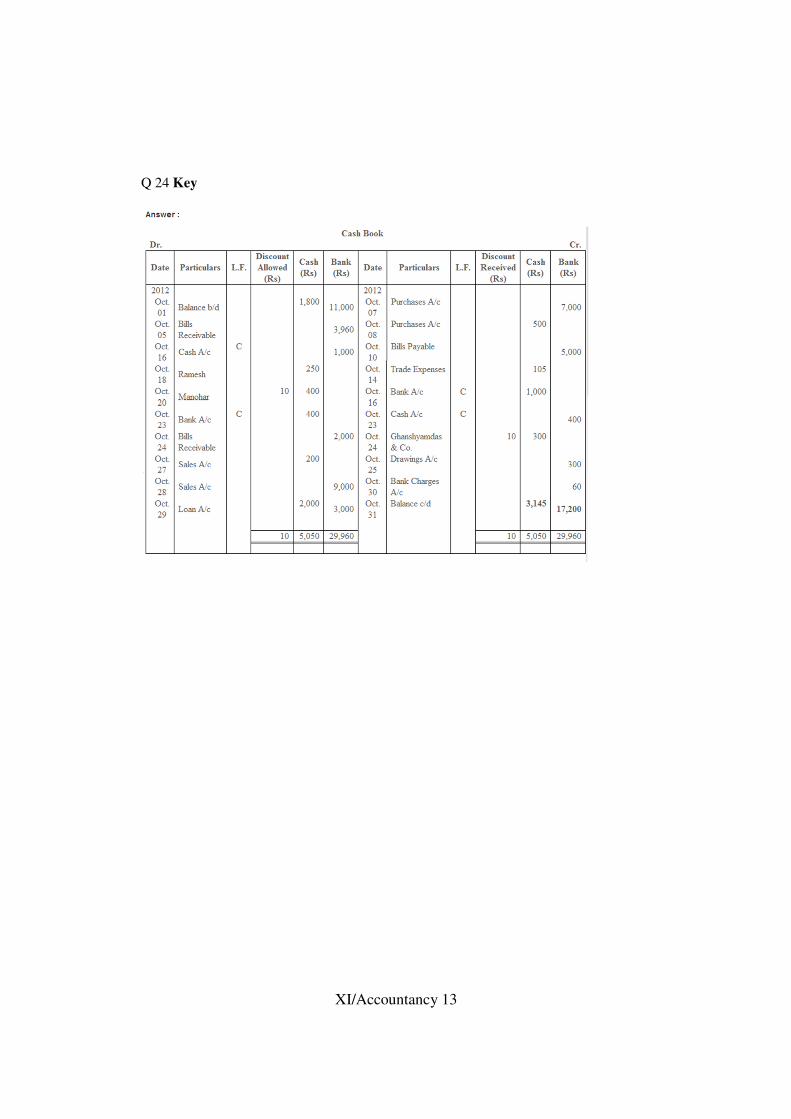

Q 24 Key