bitcoin microstructure and the kimchi premium · ye-mail: [email protected]...

TRANSCRIPT

Bitcoin Microstructure and the Kimchi Premium

Kyoung Jin Choilowast

University of CalgaryHaskayne School of Business

Alfred Lehardagger

University of CalgaryHaskayne School of Business

Ryan StaufferDagger

University of CalgaryHaskayne School of Business

this version April 2019

lowastHaskayne School of Business University of Calgary 2500 University Drive NW Calgary Alberta CanadaT2N 1N4 e-mail kjchoiucalgarycadaggere-mail alfredleharhaskayneucalgarycaDaggere-mail ryanstaufferhaskayneucalgaryca

Bitcoin Microstructure and the Kimchi Premium

Abstract

Between January 2016 and February 2018 Bitcoin were in Korea on average 473more expensive than in the United States a fact commonly referred to as the Kimchi pre-mium We argue that capital controls create frictions as well as amplify existing frictionsfrom the microstructure of the Bitcoin network that limit the ability of arbitrageurs to takeadvantage of persistent price differences We find that the Bitcoin premia are positively re-lated to transaction costs confirmation time in the blockchain and to Bitcoin price volatilityin line with the idea that the delay and the associated price risk during the transaction periodmake trades less attractive for risk averse arbitrageurs and hence allow prices to diverge Across country comparison shows that Bitcoin tend to trade at higher prices in countries withlower financial freedom Finally unlike the prediction from the stock bubble literature theKimchi premium is negatively related to the trading volume which also suggests that theBitcoin microstructure is important to understand the Kimchi premium

Keywords Bitcoin Limits to Arbitrage Cryptocurrencies Fintech

1 Introduction

I think the internet is going to be one of the major forces for reducing the role of

government The one thing thatrsquos missing but that will soon be developed is a

reliable e-cash

Milton Friedman in 1999 - Nine years later Bitcoin was created

Many proponents of cryptocurrencies such as Bitcoin list independence from government

influence as key advantage of this new technology In an ideal world payments can be made and

funds exchanged globally without any central authority or government regulation1 Yet we argue

in this paper that government regulations in fiat currencies especially capital controls create

new and amplify existing frictions in the global Bitcoin market In Korea for example Bitcoin

frequently trade at a higher price than in other markets a phenomenon referred to as the Kimchi

premium Between Between January 2016 and February 2018 the average Kimchi premium was

473 but it reached levels as high as 5448 in January 2018 Figure 1 shows a time series plot

as well as a histogram of the historical Kimchi premium In frictionless financial markets such

a price difference could not persist as it would be immediately arbitraged away Traders could

buy Bitcoin in another market say the US then transfer them to a Korean Bitcoin exchange

sell them for Korean won and convert the won to US dollars for an instant profit However

institutional frictions prevent arbitrageurs from keeping Bitcoin prices in Korea aligned with

the rest of the world Divergence in Bitcoin prices are not only a Korean phenomenon As we

document in this paper international differences in Bitcoin prices can be high and persist over

longer periods of time Even within the US prices differ somewhat between exchanges2 In this

paper we analyze two main frictions that can contribute to a potential misalignment of Bitcoin

1Satoshi Nakamoto a pseudonym for the legendary inventor of Bitcoin included the headline of the FinancialTimes on Jan 3 2009 ldquoChancellor on brink of second bailout for banksrdquo in the first block the genesis block of theBitcoin Blockchain Many see this as an expression of distrust in the current financial system As the first reasonfor the existence of Bitcoin Bitcoin-Wiki states that lsquorsquoBitcoin is P2P electronic cash that is valuable over legacysystems because of the monetary autonomy it brings to its usersrdquo

2Several websites allow users to monitor spreads and identify possible arbitrage opportunities egwwwtokenspreadcom databitcoinityorgmarketsarbitrage Figure 4 in the appendix shows such an arbitragematrix

1

prices across major markets capital controls and frictions emanating from the microstructure

of the Bitcoin network

Due to microstructure of the Bitcoin network arbitrageurs are confronted with obstacles that

are absent in many traditional markets An arbitrageur faces two main sources of risk when exe-

cuting the arbitrage trade described above First the transfer of Bitcoin from a foreign exchange

to a Korean exchange takes time during which the Bitcoin price can change dramatically Since

Bitcoin can usually not be shorted in the markets where they are selling at a higher price the

premium cannot be locked in Bitcoin at a Korean exchange can only be sold once the transfer is

complete Because Bitcoin can be much more volatile than many transitional assets price risk

can pose a significant deterrent for arbitrageurs Second time varying transaction costs erode

potential arbitrage profits Demand for transactions fluctuates over the day and over time As

fees increase profits from arbitrage decrease allowing the price difference between Bitcoin in

Korea and the rest of the world to rise

Frictions in traditional capital markets add limitations to arbitrage Korean capital controls

limit the amount of money that can be sent abroad or at least complicate the transfer of funds

and thus create a one way friction for the fiat currency part of the arbitrage trade In the af-

termath of the global financial crisis and the European sovereign debt crisis Korea introduced

capital controls that create administrative burden and additional time delay when sending money

abroad

Our main finding is that both Bitcoin microstructure effects as well as exchange controls

explain a significant portion of Kimchi premium We start out with an in-depth comparison

of the Korean Bitcoin market with the European market where more detailed data is available

and markets are well developed and liquid We find that in both markets microstructure effects

are correlated with price deviations Price deviations relative to the US market are significantly

positively related to Bitcoin volatility supporting the idea that price risk for traders limits arbi-

trage activity The Kimchi premium is also positively related to the median confirmation time

in the block chain supporting the idea that longer transaction times create more uncertainty for

2

Figure 1 The Bitcoin Kimchi Premium Bitcoin frequently trade at a higher price in Korea thanin other markets The premium for purchasing Bitcoin with Korean won (KRW) versus US dollars(USD) is calculated (KRWBTCprice in USD)(USDBTCprice) minus 1 where the Bitcoin price in USD is themean price of all USD transactions on the Bitstamp exchange for that day The Bitcoin price in KRW issimilarly defined from the Korbit exchange Conversion from KRW to USD is done using the OANDAdaily average rate

a) The Kimchi premium over time (top panel)

b) Distribution of the Kimchi premium (bottom panel)

3

arbitrageurs allowing prices to diverge Finally price differences are also increase in transaction

fees paid to miners consistent with the idea that higher fees reduce the attractiveness of the

arbitrage trade In particular if the trader offers higher fees miners are more likely to include

the transaction in a block hence making the transfer of Bitcoin faster Therefore the effect of

transaction fees should be inclusive of that of the median confirmation time which is shown in

our regression analysis

Comparing the European to the Korean market however we find two important differences

First the impact of microstructure effects on price divergences are several times larger for Korea

than for the European market Second we find the Kimchi premium to be positive while the

average premium for the European market is near zero We argue that capital controls are the

reason why the average premium in positive and also make the the premium more sensitive to

microstructure effects Because of the asymmetry of capital controls (it is easier to move funds

to Korea than the other way around) arbitrage is harder on one direction allowing the Kimchi

premium to be positive on average Because of the capital controls arbitrage is more costly and

hence the premium in Korea is more sensitive to transaction costs volatility and transaction

times compared to the European market

To further analyze the impact of capital controls we collect data on Bitcoin premia for an

international sample and analyze how premia vary with various measures of financial freedom

Controlling for microstructure effects we find that countries with higher financial freedom have

on average lower premia Figure 2 plots the median Bitcoin premium from March 2017 to the

end of February 2018 as a function of financial freedom3 As a stylized fact the graph shows

higher average premia in financially more restrictive countries which is consistent with our view

that financial restrictions are causing higher Bitcoin prices in some countries

We also examine Korean premia in other cryptocurrencies such as Ethereum Lite-coin and

Ripple Instead of using fiat currency arbitrageurs could complete the arbitrage trade by buying

other crypto currencies with the proceeds of selling Bitcoin in Korea and sending them abroad

3In This graph we use the Economic Freedom Ranking by the Fraser institute as explained in more detail inSection 5

4

Figure 2 Bitcoin Premia and Financial Freedom The Bitcoin premium is measured as the medianpercentage price difference to the USD price from March 2017 to the end of February 2018 Bitcointransaction prices are from bitcoinchartscom foreign exchange data from the Federal Reserve Bank ofSt Louis (where available) and OANDA otherwise To measure financial freedom we use the EconomicFreedom Ranking by the Fraser institute

without being subject to capital controls We find that other crypto currencies have practically

identical premia to Bitcoin at Korean exchanges and those premia are highly correlated over

time with the Kimchi premium

In addition to our finding on the two main factors to derive the Kimchi premium it is no-

table that the Kimchi premium is negatively related to the trading volume This result sounds

quite counterintuitive in the sense that the trading volume is usually positively related to the

size of a bubble in common stock markets as shown by the traditional bubble literature (see

eg Scheinkman and Xiong (2003) and Xiong and Yu (2011)) More precisely in our study

the trading volume with nothing else controlled for is positively associated with the Kimchi

premium However if we add the trading volume into the regression together with volatility and

transaction fees the Kimchi premium shows the negative relation with the trading volume while

5

its positive correlations with the other two factors become stronger Our findings are consistent

with two countervailing forces On one hand a higher volume helps to reduce the Kimchi

premium through increased liquidity in the Korean Bitcoin market On the other hand high

volume increases blockchain transaction fees and blockchain confirmation times (and possibly

exchange cash-out times) and thus reduces the ability to arbitrage Given that the volatility is ex-

tremely high a high volume contributes more to increasing liquidity than increasing transaction

fees which leads to the negative relationship between the premium and the volume Therefore

we argue that this negative relationship is attributed to the Bitcoin microstructure characteristics

that do not exist in a common stock market

Our paper is related to the recent emerging and fast-growing literature on blockchain and

cryptocurrencies such as Athey Parashkevov Sarukkai and Xia (2016) Cong Li and Wang

(2018) Detzel Liu Strauss Zhou and Zhu (2018) Pagnottayand and Buraschi (2018) and

Sockin and Xiong (2018) Griffin and Shams (2018) While most of these papers focus on

cryptocurrency pricing andor asset pricing implications we investigate the mechanism and the

factors that lead to the different pricing4 Gandal Hamrick Moore and Oberman (2018) inves-

tigate how suspicious trading activities caused a price spike in late 2013 Easley OrsquoHara and

Basu (2017) Huberman Leshno and Moallemi (2017) Cong He and Li (2018) investigate the

Bitcoin mining structure competition of mining pools and its impact on transaction fees These

papers are important to understand speculative trading in the Bitcoin market and how Bitcoin

transaction fees are determined Our paper adds to the literature by providing the explanation

of how these mechanisms generate pricing difference In a contemporary paper Makarov and

Schoar (2018) analyze spreads in an international sample of Bitcoin prices are relate these to

signed order flow

Our work is also related to a broad literature on bubbles and limits of arbitrage (see Xiong

(2013) and Gromb and Vayanos (2010) for a survey) There are various constraints and limi-

tations known in the literature to impede arbitrage trading Among such constraints5 risk (the4Hu Parlour and Rajan (2018) provides several stylized facts on cryptocurreny markets as well as a survey of

the literature on Bitcoin valuation5The constraints include information asymmetry short-sale constraints leverage margin constraints constraints

6

price volatility in our case) and international trading frictions (the capital controls in our case)

seem the most relevant to explain Bitcoin price differences Specifically we find that the Kimchi

premium has a significant positive relation to Bitcoin price volatility and capital controls6

There is one notable difference between our results and those from the traditional bubble

literature investigating the joint effect of short-sale restrictions and heterogeneous beliefs in the

stock market (eg Miller (1997) Harrison and Kreps (1978) Chen Hong and Stein (2002)

Scheinkman and Xiong (2003) Hong Scheinkman and Xiong (2006) and Mei Scheinkman

and Xiong (2009)) Under a short-sale constraint the optimists are more likely to be marginal

buyers and the stock price tends to reflect optimistsrsquo valuation more than that of pessimists

which leads to a bubble (meaning a higher value than the fundamental value) This conventional

bubble literature predicts that the size of bubble is positively related to the volatility and the

trading volume Our result on volatility is in line with the literature but trading volume differs

from the previous literature in our case There is short-sale restriction in the Bitcoin market In

particular Bitcoin futures were introduced in the US in early 2018 but not in Korea at the time

of writing In this sense it might be natural to expect a positive relationship between the Kimchi

premium and Bitcoin trading volume in Korean exchanges While the bubble argument would

suggest that volume and worldwide Bitcoin returns are positively correlated it does not explain

the Kimchi premium Therefore we strongly believe that the negative correlation indicates the

importance of the Bitcoin microstructure for generating differential pricing which is the crucial

difference between Bitcoin and common stock markets

Our paper is also closely related to a long literature on internationally dual-listed stocks

(or Siamese twins) (see eg Rosenthal and Young (1990) Froot and Dabora (1999) De Jong

Rosenthal and Van Dijk (2009) Gagnon and Karolyi (2010) and references therein) document-

ing occurrences of significant price differences in those stocks listed in two countries Each of

these papers finds that the price differences are attributed to tax accounting holding costs of

on equity capital etc6See eg Edwards (1999) on the effectiveness of capital controls

7

the stock like idiosyncratic risk7 and so on These factors however are unlikely to be relevant

to the Bitcoin market Rather our findings indicate that the Bitcoin microstructure amplifies the

capital control effect on the price difference

Finally our paper is related to the purchasing power parity (PPP) puzzle literature in inter-

national economics8 Viewing Bitcoin as an internationally traded asset (or commodity) we

can compare the Bitcoin price differential across countries with that of worldwide sold goods

such as McDonald Big Mac sandwich9 (Pakko and Pollard (2003) and Clements Lan and

Seah (2012)) Our dataset has the unique advantage that we can provide evidence at a much

higher frequency that much of the existing literature There are several factors identified by

the PPP literature which lead to an international price difference transportation costs sales

(or value-added) taxes trade restrictions (such as safety guard) domestic labor productivity

(when there are non-tradeable goods such as services) government expenditure and current

account deficits All of these factors are irrelevant to the Bitcoin market except perhaps the

transportation cost which plays a similar role as the transaction fee in the Bitcoin market In

the PPP case the transportation costs always add nontrivial contributions to the PPP deviation

However it is notable that the transaction fee effect on the Bitcoin price difference becomes

negligible without capital controls as we find that the average Bitcoin price difference is near

zero between Europe and US between which there are almost no capital controls Therefore

this discrepancy between the PPP case and the Bitcoin case also emphasizes the importance of

the capital controls contributing to the Kimchi premium

The rest of the paper is organized as follows Section 2 presents the institutional background

on Bitcoin microstructure and Korean capital controls Section 3 details the data we use in

our analysis in Section 4 we compare the Korean and the European market in detail Section

5 expands our sample internationally in Section 6 we examine other cryptocurrencies and

Section 7 concludes7The idiosyncratic risk means the risk unrelated to the risk of other securities in either of the competing markets8See eg Rogoff (1996) and Taylor and Taylor (2004)9The Big Mac price index is annually published by Economist since 1986

8

2 Institutional background

21 Bitcoin microstructure

The microstructure of Bitcoin markets stands out in many ways from traditional markets Trans-

actions ie the transfer from one wallet to another wallet get posted within the Bitcoin peer-to-

peer network in the mem-pool from where miners pick transactions to be mined into a block

which gets then added to the blockchain Many exchanges require a certain number of confir-

mations to credit Bitcoin that are transferred to the exchange to an account A transaction with

n confirmations means that this transaction has been included in a mined block and that there

have been n minus 1 subsequent blocks mined in the blockchain Time delay arises from the time

it takes for a transaction to be included in a mined block and from the time it takes to mine the

required number of subsequent blocks The time to be included in a block which is referred to

as confirmation time can vary substantially The historic maximum of the daily median confir-

mation time is 47 minutes for our sample the daily median confirmation time is 11 minutes on

average10 Note that the confirmation for individual transactions can differ substantially from

the median especially when the tranmsactions offer low fees to the miners The average time

between successfully mined blocks is 10 minutes

Transaction fees are endogenously determined in the Bitcoin network When posting a

transaction to the mem-pool the originator can set a fee that he or she is willing to pay to the

miner for the transaction to be included in the block Miners can select transactions from the

pool and keep the fees upon successfully mining a block Transactions with higher fees have

a higher probability to be included in a block An arbitrageur thus faces a tradeoff between

offering a high fee that will get the transaction processed faster and mitigate price risk and the

cost of the higher fee which will directly reduce the arbitrageurrsquos profit

When trading on Bitcoin exchanges another layer of delay arises Most exchanges offer

clients accounts similar to an account with a traditional stock broker Trades are usually only

10source httpsblockchaininfo

9

possible between account holders at the same exchange and a trade is just recorded in the ledger

of the exchange not on the blockchain The Bitcoin transferred from the seller to the buyer are

held in the wallets of the exchange on the blockchain before and after the trade the exchange

just records a change of ownership in its internal records Account holders can request a trans-

fer to a private wallet out of the exchange account which will trigger a ledger entry on the

blockchain While there is no data available on processing times by exchanges anecdotal ev-

idence on several Bitcoin forums shows that processing times can be substantial with traders

waiting up to several days before exchanges transfer Bitcoin from their exchange-account to a

private wallet from which a transfer (to another exchange) can be initiated In particular 5-10

hours of processing time from a US exchange to a Korean exchange is commonly reported

by major mass media in Korea For example Chosun Ilbo a Korean newspaper tested the

arbitrage and reported a processing time of 9 hours from Coinbase to Bithumb on December

26 2017 when the Kimchi premium was about 2811 Also the deposit and withdrawal of

fiat money can be subject to considerable delay For example in Canada processing times for

deposits and withdrawals can take up to several months In part the delay is caused by banksrsquo

refusal to deal with cryptocurrency companies Quadriga one of the two established exchanges

in Canada has to rely on a Portuguese bank to process many of its fiat currency transfers12 In

Figure 5 we present further anecdotal evidence from forum posts for Coinbase a US exchange

22 Capital Controls

On June 13 2010 in the aftermath of the global financial crisis and the European sovereign

debt crisis Korea introduced capital controls that were revised several times since The Ko-

rean foreign exchange transaction law has been very restrictive According to the most recent

11Chosun Ilbo (Daily Chosun) is the 1 news paper company in South Korea in terms of the total number ofdaily printing See the following news article by the Chosun Ilbo on January 4 httpnewschosuncomsitedatahtml_dir201801042018010400441html

12See article rsquordquoI just want my money backrdquo Couple had $100K wire stuck for months after trying to buy BitcoinrsquoGlobalNews March 27 2018

10

law revision (valid since July 18th 2017)13 an individual can send money up to 3000 USD

per transfer and up to 20000 USD in total between January 1st and December 31st through a

particular financial institution The total maximum is limited to 50000 USD a year through

different institutions14 There are several alternative ways to send cash abroad First one can

use a Korean credit card when buying Bitcoin at an exchange in the US However the maxi-

mum amount of purchases outside of Korea is limited to 10000 USD per year In addition this

transaction is considered as commodity purchase which means the buyer should pay customs

on buying Bitcoin One can send US dollars to someone (eg relatives or friends in the US)

who can help arbitrage trading through Paypal In this case however Paypal automatically re-

ports this transaction to the US Internal Revenue Service (IRS) and the IRS normally considers

this money inflow to the receiver as taxable income if the transfer amount is sufficiently large

or the transfers occur on a regular basis In addition many Korean lawyers15 say that under the

current South Korean law it is not very clear if transferring Bitcoin between a Korean exchange

and exchanges in other countries is considered as capital in- and out-flow or commodity ex-

portimport This legal interpretation issue might pose an additional risk since the government

might investigate transfer activities ex-post and accuse market participants of violation of the

law depending on how they interpret the law

So far we have discussed on the legal restrictions that domestic Koreans face as capital

controls There is also difficulty for foreigners to open an account in Korean cryptocurrency

exchanges In order to do so there are two requirements a domestic bank account and a

domestic cell phone number In order to obtain them foreigners need to go through several steps

of permissions andor recommendations from a government-endorsed institution or personnel

It is almost impossible to obtain them by just temporarily visiting South Korea In Figure 5 we

present anecdotal evidence from forum posts where people are actively seeking Korean partners

13See the government website on small foreign remitment httpwwwmosfgokrnwnesdetailNesDtaViewdosearchBbsId1=ampsearchNttId1=MOSF_000000000009556ampmenuNo=4010100

14There are some exceptions For example the maximum per year is up to 100000 USD for educational reasonssuch as tuition with proper evidence

15See eg httphongbyuntistorycom22

11

for arbitrage trading One post suggests to meet in person at an airport to complete the arbitrage

3 Data Sources and Model Variables

Bitcoin is very popular in Korea As of February 1st 2018 there are 16 cryptocurrency ex-

changes in South Korea The five largest exchanges in terms of trading volumes are Upbit (1

world ranking) Bithumb (7) Coinone (14) Korbit (18) and Coinnest (21)16 Korbit was

the first Korean Bitcoin exchange that opened in April 2013 Then Bithumb (January 2014)

Coinone (August 2014) Coinnest (July 2017) and Upbit (October 2017) followed Until Upbit

started an exclusive partnership with Bittrex (a major US based exchange) on October 2017

Bithumb Coinone and Korbit had been the three major exchanges17

Our primary variable of interest is the Bitcoin premium in local currency over the Bitcoin

price in USD For Korea the KRW Bitcoin premium over USD the Kimchi premium is defined

as

PremiumKRW =KRWBTC pricetimes USDKRW exchange rateminus USDBTC price

USDBTC price(1)

The premium for the European market is defined similarly based on EUR prices

For daily Bitcoin prices in USD KRW and EUR we look at all transactions on specific

Bitcoin exchanges (data accessed via bitcoinchartscom) Exchanges were selected due to data

availability length of trading history and both current and historical market share USD data is

from Bitstamp Bitstamp has offices in Luxembourg London and Berkeley They are currently

the 3rd largest exchange for USD trades by volume and have the longest trading history of the

current major players In the early days of Bitcoin trading the USD leader was Mt Gox which

famously went bankrupt following a security breach The sample used for regressions runs

16The number inside the parenthesis is the world ranking in trading volumes (all the cryptocurrencies) by Coin-hills on February 1st 2018 (see httpswwwcoinhillscommarketexchange

17Among the top three Korbit is the only one which provides a history of all the trades in unix-time

12

from 2016-01-01 through 2018-02-28 and contains 13151367 total trades The total notional

value (valued at the time of each trade) is USD 339b KRW data is from Korbit Korbit was

South Korearsquos first Bitcoin exchange Korbit is fourth by volume for KRWBTC as of February

1 2018 but has been second or third during the majority of the sample period The sample

contains 4889844 total trades with a total notional value (at the time of each trade) of KRW

142t EUR data is from Kraken Kraken is currently the largest exchange for EURBTC by

volume with more than half the total volume The sample contains 15349375 trades with a

total notional value (valued at the time of each trade) of EUR 191b

The daily USD price we utilize for analysis is the mean price of all USD transactions on the

Bitstamp exchange for that day The KRW and EUR daily prices are similarly defined using

Korbit and Kraken exchanges respectively To convert the KRW and EUR prices to USD we

utilize data from OANDA The daily prices utilized are the average price (not the close) over

the 24-hour period (UTC time standard) aggregated from multiple exchanges We find this the

best fit for our purpose as the Bitcoin markets operate 247

We estimate short term volatility for Bitcoin prices as the sum of 10 minute squared log-

returns over one day Microstructure noise can arise from spreads between bid and ask prices

and from shifts in transaction prices due to the random execution of large trades at either end of

the 10 minute interval We take two measures to mitigate potential biases due to microstructure

noise First we compute daily volatility for a given exchange as the average of two volatility

measures based on 10 minute returns shifting the time interval by 5 minutes Second we

define volatility as the median volatility over several exchanges18 To test for robustness we

also compute long term volatility for a given exchange as the sum of squared 12 hour returns

over a period of 20 days We then define long term volatility as the median volatility over

several exchanges Our results are robust with respect to this alternative volatility measure

The Bitcoin blockchain median confirmation time data is from wwwblockchaininfo This18Data availability differs per time period as data is not available for all exchanges at all times We include data

from the following exchanges bitfinex Bitstamp BTCC btc-e coinbase Gemini hitbtc itbit kraken OK-CoinPoloniex as available on bitcoinchaincom

13

is the median time in minutes for a Bitcoin transaction to be accepted into a mined block and

added to the public ledger this number is computed only from transactions with miner fees and

might therefore underestimate actual confirmation times For days with missing data (of which

there are none in the most recent 2 years) we interpolate linear between days The maximum

gap in the data set was 1 day Results were unchanged when using the previous dayrsquos value or

removing missing days completely from analysis

The mean blockchain transaction fee is measured in USD and calculated from data from

blockchaininfo It is the total value of all transaction fees paid to miners converted to USD

(not including the value of block rewards) divided by the number of daily confirmed Bitcoin

transactions on the blockchain for that day

For the KRW and EUR volumes we look at the daily total number of exchange transactions

(in thousands) on Korbit and Kraken respectively This approach was taken rather than volume

in Bitcoin due to the wildly differing Bitcoin prices at the start versus the end of the sample

period All results are robust to using an alternative volume measure of the daily USD equivalent

total valuation of transactions For the KRW-USD and EUR-USD foreign exchange volatilities

we use the standard deviation of 1-day logarithmic returns in the daily average KRW-USD and

EUR-USD exchanges from OANDA over the most recent 20 days

The 1-day Bitcoin return variable is the 1-day logarithmic return in the USD-BTC price

where USD-BTC daily price is calculated as described above for the Kimchi premium calcula-

tion The FOMC week variable is a dummy variable which takes a value of 1 if that day is within

3 days of a US Federal Reserve Federal Open Market Committee (FOMC) meeting start date

(one week centered on the start date of the FOMC meeting) Results are unchanged if a leading

week is used instead of centered and all FOMC meetings during the regression sample period

were regularly scheduled (the last unscheduled meeting was in March 2014) The FOMC sets

monetary policy for the US (including a target for the overnight interbank interest rate) Cor-

bet Larkin Lucey Meegan and Yarovaya (2017) found that certain classes of digital assets

(currencies mineable) of which Bitcoin is a member have volatility spillover transfer from

14

US monetary policy announcements There is also a broad literature on the impact of FOMC

meetingsannouncements on the volatilty returns and trading volume of other assets both in the

US and globally For example Fischer and Ranaldo (2011) found that foreign exchange trading

volume was significantly increased on FOMC days and Lucca and Moench (2015) document

large average excess returns on US equities ahead of the monetary policy decisions made at

scheduled FOMC meetings The Bitcoin news in Korea variable is the total number of daily

news articles published in Korea with keyword rdquoBitcoinrdquo from Factiva19 A summary of the

variables used in our empirical analysis can be found in Table 8 in the appendix

4 Empirical Results

To analyze the determinants of the Kimchi premium we regress daily observations of the relative

price difference for Bitcoin in Korea and the US on several factors or proxies for potential

frictions inhibiting the arbitrage All Bitcoin for fiat currency transaction times are converted

to UTC time standard Days with missing trading data are excluded All results were robust to

testing on a sample with linear interpolation between missing days

Regression results are shown in Table 1 Bitcoin price risk is a significant component to

the Kimchi premium size In periods of high volatility the cost of waiting for blockchain

confirmations could be very significant and deter arbitrageurs Model (1) documents a positive

relation between the Kimchi premium and short term BTC volatility Model (2) shows that

higher fees make the arbitrage less profitable and thus coincide with higher premia As shown in

model (3) higher median confirmation times on the block chain are also associated with higher

Bitcoin premia An arbitrageur could potentially jump the queue get her transaction processed

faster by offering a higher transaction fee to miners yet such a higher transaction fee would also

cause a direct reduction in arbitrage profits and hence allow for a larger premium Model (4)

shows that higher volume by itself is associated with higher fees Considering all these factors

19Bitcoin is 비트코인 in Korean

15

Tabl

e1

Reg

ress

ion

resu

ltsfo

rth

eK

RW

Bitc

oin

prem

ium

over

USD

Dai

lytim

ese

ries

regr

essi

ons

the

depe

nden

tvar

iabl

eis

the

prem

ium

forp

urch

asin

gB

itcoi

nw

ithK

orea

nw

on(K

RW

)ver

susU

Sdo

llars

(USD

)and

isca

lcul

ated

(K

RW

BT

Cpr

ice

inU

SD)(U

SDB

TC

pric

e)minus1

whe

reth

eB

itcoi

npr

ice

inU

SDis

the

mea

npr

ice

ofal

lUSD

tran

sact

ions

onth

eB

itsta

mp

exch

ange

fort

hatd

ayT

heB

itcoi

npr

ice

inK

RW

issi

mila

rly

defin

edw

ithda

tafr

omth

eK

orbi

texc

hang

eC

onve

rsio

nfr

omK

RW

toU

SDis

done

usin

gth

eO

AN

DA

daily

aver

age

rate

T

hein

depe

nden

tva

riab

les

are

defin

edas

inTa

ble

8 (1)

(2)

(3)

(4)

(5)

(6)

(7)

Bitc

oin

shor

tter

m0

0667lowastlowastlowast

003

48lowastlowastlowast

003

74lowastlowastlowast

004

36lowastlowastlowast

vola

tility

(00

041)

(00

047)

(00

049)

(00

051)

Mea

nbl

ockc

hain

000

69lowastlowastlowast

000

65lowastlowastlowast

000

66lowastlowastlowast

000

69lowastlowastlowast

tran

sact

ion

fee

(00

003)

(00

004)

(00

004)

(00

004)

Blo

ckch

ain

med

ian

000

27lowastlowastlowast

000

060

0005

000

04co

nfirm

atio

ntim

e(00

007)

(00

006)

(00

006)

(00

006)

KR

W-B

TC

volu

me

000

45lowastlowastlowast

minus0

0014lowastlowastlowast

minus0

0017lowastlowastlowast

minus0

0018lowastlowastlowast

(tho

usan

dsof

tran

sact

ions

)(00

003)

(00

004)

(00

004)

(00

004)

KR

W-U

SDminus

045

14minus

057

34minus

085

79vo

latil

ity(19

711)

(19

664)

(19

429)

Bitc

oin

1-da

y0

1353lowastlowast

012

49lowastlowast

lagg

edre

turn

(00

589)

(00

581)

FOM

Cw

eek

minus0

0182lowastlowastlowast

(00

055)

BT

Cne

ws

Kor

eaminus

000

01lowastlowastlowast

(00

0003

)

Con

stan

tminus

000

080

0242lowastlowastlowast

001

72lowastlowast

001

95lowastlowastlowast

000

460

0049

000

78(00

038)

(00

022)

(00

087)

(00

030)

(00

115)

(00

115)

(00

114)

Obs

erva

tions

788

790

790

790

788

788

788

R2

025

000

4525

001

660

2261

049

010

4935

050

78

Not

elowast plt

01lowastlowast

plt0

05lowastlowastlowast

plt0

01

16

Figure 3 The Bitcoin EUR Premium Bitcoin sometimes trade at a higher price even betweenrelatively frictionless markets (here EUR vs USD) The premium for purchasing Bitcoin with Euros(EUR) versus US dollars (USD) is calculated (KRWBTCprice in USD)(USDBTCprice) minus 1 where theBitcoin price in USD is the mean price of all USD transactions on the Bitstamp exchange for that dayThe Bitcoin price in EUR is similarly defined from the Kraken exchange Conversion from EUR to USDis done using the OANDA daily average rate

a) The EUR premium over time (top panel)

b) Distribution of the EUR premium (bottom panel)

17

Tabl

e2

Reg

ress

ion

resu

ltsfo

rth

eE

UR

Bitc

oin

prem

ium

over

USD

D

aily

time

seri

esre

gres

sion

sth

ede

pend

ent

vari

-ab

leis

the

abso

lute

valu

eof

the

prem

ium

for

purc

hasi

ngB

itcoi

nw

ithE

uro

(EU

R)

vers

usU

SD

olla

rs(U

SD)

and

isca

lcul

ated

(E

UR

BT

Cpr

ice

inU

SD)(U

SDB

TC

pric

e)minus1w

here

the

Bitc

oin

pric

ein

USD

isth

em

ean

pric

eof

allU

SDtr

ansa

ctio

nson

the

Bits

tam

pex

chan

gefo

rtha

tday

The

Bitc

oin

pric

ein

EU

Ris

sim

ilarl

yde

fined

with

data

from

the

Kra

ken

exch

ange

Con

vers

ion

from

EU

Rto

USD

isdo

neus

ing

the

OA

ND

Ada

ilyav

erag

era

teT

hein

depe

nden

tvar

iabl

esar

ede

fined

asin

Tabl

e8

(1)

(2)

(3)

(4)

(5)

(6)

(7)

Bitc

oin

shor

tter

m0

0041lowastlowastlowast

000

42lowastlowastlowast

000

41lowastlowastlowast

000

40lowastlowastlowast

vola

tility

(00

003)

(00

006)

(00

006)

(00

006)

Mea

nbl

ockc

hain

000

03lowastlowastlowast

000

01lowastlowastlowast

000

01lowastlowastlowast

000

01lowastlowastlowast

tran

sact

ion

fee

(00

0003

)(00

0003

)(00

0003

)(00

0003

)

EU

R-U

SD0

1623

015

360

1514

vola

tility

(02

682)

(02

673)

(02

675)

Blo

ckch

ain

med

ian

000

01lowastlowast

000

001

000

002

000

002

confi

rmat

ion

time

(00

001)

(00

001)

(00

001)

(00

001)

EU

R-B

TC

volu

me

000

01lowastlowastlowast

minus0

0000

4lowastlowast

minus0

0000

4lowastlowast

minus0

0000

4lowastlowast

(tho

usan

dsof

tran

sact

ions

)(00

0001

)(00

0002

)(00

0002

)(00

0002

)

Bitc

oin

1-da

yminus

001

35lowastlowast

minus0

0135lowastlowast

lagg

edre

turn

(00

056)

(00

056)

FOM

Cw

eek

minus0

0003

(00

006)

Con

stan

t0

0034lowastlowastlowast

000

55lowastlowastlowast

000

50lowastlowastlowast

000

47lowastlowastlowast

000

31lowastlowastlowast

000

31lowastlowastlowast

000

31lowastlowastlowast

(00

003)

(00

002)

(00

007)

(00

003)

(00

011)

(00

011)

(00

011)

Obs

erva

tions

740

742

742

742

740

740

740

R2

016

190

1076

000

620

0759

018

800

1943

019

45

Not

elowast plt

01lowastlowast

plt0

05lowastlowastlowast

plt0

01

18

we document in model (5) that only short term volatility and transaction fees stay significantly

positive while volume turns negative Median confirmation time seems to be a similar proxy for

bottlenecks in the blockchain to transaction fees and becomes insignificant FX-volatility is not

a driving factor behind the Kimchi premium as FX-volatility is substantially smaller than BTC

volatility Higher volume may help reduce the Kimchi premium through increased liquidity in

the Korean Bitcoin market while at the same time increase blockchain transaction fees andor

blockchain confirmation times (and potentially exchange cash-out times) thus reducing ability

to arbitrage and increasing the Kimchi premium In model (6) we find that a one day lagged

BTC returns are associated with a higher Kimchi premium perhaps because of momentum in

BTC prices Model (7) demonstrates that news events are important for the Kimchi premium

in particular to reduce the premium The reason is that there has been more negative news than

positive news on average20 The premium is lower in weeks of FOMC meetings and when more

news articles on Bitcoin get published in Korea

To separate the effect of frictions emanating from within the microstructure of the Bitcoin

network from Korea specific factors like the capital controls we perform a similar analysis for

the European market Figure 3 plots the relative price difference of Bitcoin in the EUR market

relative to the USD market Price differences are substantial yet the divergence of Bitcoin prices

is smaller than in the Korean market and fairly symmetric in its distribution (average 027

minimum -437 maximum 407) In our regression analysis for the European market we

explain the absolute value of the premium as we are are primarily interested in explaining the

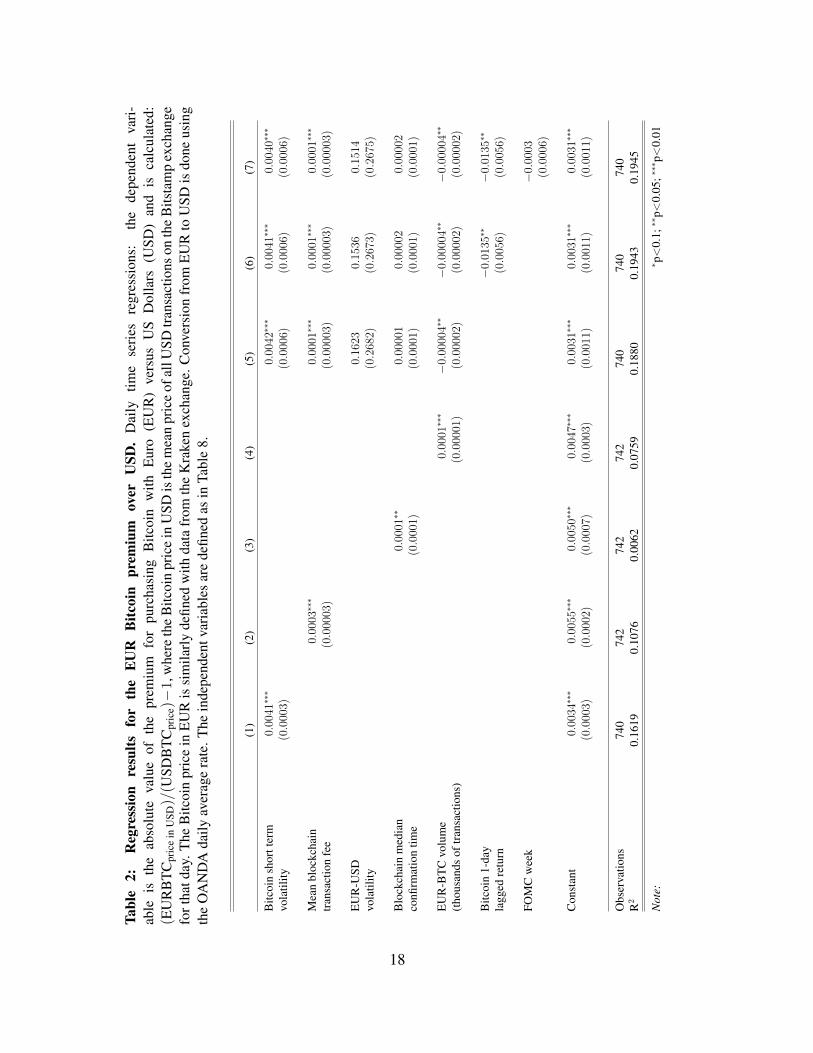

cause of price divergences21 Regression results for the EUR premium can be seen in Table 2

The coefficients for the short term volatility transaction fee and confirmation time have

the same sign but are at least ten times smaller than in the case of the Korean market These

20Good Korean news on cryptocurrency trading could potentially drive up the Kimchi premium However ourresults on average indicate that there was more negative news For example the Korean government banned ICOs(Initial Coin Offerings) in September 29 2017 and suddenly announced a policy to ban cryptocurrency exchanges(but retreated it within a day) in January 11 2018 There were massive reports and discussions related to theseannouncements in the news articles which turns out to have negative impact on the premium

21In the Korean case regression results are very similar for explaining the absolute premium since the premiumis positive almost for the entire sample

19

findings are consistent with an interpretation that Bitcoin price divergences are in part driven by

microstructure effects within the Bitcoin network and that increased volatility makes arbitrage

more risky and hence allows prices to diverge more Yet the smaller amount of frictions in the

European market facilitates arbitrage and hence price divergence is much smaller Increased

volume in European Bitcoin markets seems to be associated with smaller divergence but the

effect is of small economic significance

5 Bitcoin Premia and Financial Freedom

Comparing Korea to the Eurozone the results in Secton 4 show that price divergences between

markets exist and their magnitude is related to the microstructure of the Bitcoin network that

creates time-varying costs which inhibit the arbitrage of price differences away Our results also

show that the premium is on average close to zero for the Euro-market while it is positive for

the Korean market We also see that the premium in Korea is at least ten times more sensitive

to factors associated with arbitrage risk such as short term volatility fees or confirmation time

The anecdotal evidence suggests that this is due to the capital controls imposed by the Korean

government To examine in greater detail how open access to financial markets impacts Bitcoin

premia we extend our analysis to an international sample and relate premia to measures of

financial freedom

We collect daily Bitcoin price at data for 22 countries from bitcoinchartscom Since trading

volume is low in some markets we take the median Bitcoin price in local currency per day

Due to data availability we restrict our sample from the beginning of 2015 to the end of our

sample period on Feb 23 2018 In cases of more than one exchange with available data we take

the average price across available exchanges Where available we use foreign exchange data

from the Federal Reserve Bank in St Louis otherwise we use data from OANDA to convert

local currency Bitcoin prices to USD Premia are computed as in Section 4 as the percentage

deviation from the USD price Table 3 summarizes our sample It can be seen that premia

20

Table 3 Summary statistics international sample Median mean and standard deviation of Bitcoinpremia in percent over the USD price for a sample of international markets collected frombitcoinchartscom Column 3 shows the source of the foreign exchange data used to convert local cur-rency Bitcoin prices to USD

Country ISO FX-Data number of Premium (in )observations median mean stddev

Argentina ARS OANDA 788 946 1942 2088Australia AUD St Louis Fed 788 096 137 238Brazil BRL St Louis Fed 788 441 554 553Canada CAD St Louis Fed 788 -002 -011 171Chile CLP OANDA 683 256 350 581Euro-Zone EUR St Louis Fed 788 006 -002 086Great Britain GBP St Louis Fed 788 365 388 156Hong Kong HKD St Louis Fed 753 250 210 516Israel ILS OANDA 787 057 080 334India INR St Louis Fed 788 263 380 620Japan JPY St Louis Fed 788 042 072 174Korea KRW St Louis Fed 788 139 297 642Mexico MXN St Louis Fed 788 558 629 361Malaysia MYR OANDA 782 040 063 1231Nigeria NGN OANDA 543 2045 2635 2469Norway NOK St Louis Fed 788 367 396 241New Zealand NZD St Louis Fed 788 675 695 366Sweden SEK St Louis Fed 788 538 551 226Singapore SGD St Louis Fed 747 -042 -049 126Thailand THB St Louis Fed 788 063 116 373Venezuela VND OANDA 605 117 195 409South Africa ZAR OANDA 613 684 774 448

vary by country Nigeria stands out with a median premium of 2045 which is the result of

high premia following an unexpected devaluation of the Nigerian Naira by President Buhari in

June 2016 In the following ten months high premia are observed which could be the result of

people buying Bitcoin as trust in the national currency erodes In unreported results we repeat

our regression analysis without Nigeria and find that our main findings still hold

We use two indices to measure capital controls and other regulatory restrictions First we

take the economic Freedom Ranking (EFR) by the Fraser Institute They aggregate 42 distinct

variables in five major areas size of government the legal system and security of property

21

rights sound money freedom to trade internationally and regulation22 We used Germany as a

proxy for the Euro area Second we use an index on capital controls (CCI) by Fernandez Klein

Rebucci Schindler and Uribe (2015) They collect in great detail capital controls for a variety

of financial instruments from stocks and bonds to other investments such as real estate In our

study we use their sub-index on restrictions of outflows of money market instruments which is

the shortest maturity bucket in their analysis

Since our sample only comprises a bit more than two years and the indices of economic

freedom and capital controls are only published annually (not available for 2018 yet) and do

not vary much we cannot use a fixed effect panel model as the fixed effect would absorb het-

erogeneity in economic freedom We therefore use a random effects panel model with daily

observations and year fixed effects to analyze the impact of economic freedom on Bitcoin pre-

mia Table 4 presents our results The general results without measures of economic freedom

(column 1) show the same direction of effects as in our analysis of the Korean market Higher

volatility longer confirmation time and higher fees make it harder to complete the arbitrage

coinciding with higher premia

As we would predict the EFR has a significant negative correlation (more freedom is asso-

ciated with a lower Bitcoin premium) and higher capital controls are associated with higher

premia showing that countries with greater economic freedom have lower Bitcoin premia In

terms of the EFR a move from the median (Turkey score 683) to the 75 quantile (Peru

score 747) and to the top (Hong Kong score 895) would result in a reduction of in its Bitcoin

premium by 14 and 32 percentage points respectively Similarly tighter capital controls coin-

cide with higher bitcoin premia Our findings are therefore consistent with the idea that Bitcoin

premia are more likely to occur in countries that impose restrictions on financial markets

22see wwwfraserinstituteorgeconomic-freedomapproach

22

Tabl

e4

Inte

rnat

iona

lBitc

oin

Prem

iaT

hede

pend

entv

aria

ble

isth

epr

emiu

mfo

rBitc

oin

with

loca

lcur

renc

y(L

C)v

ersu

sU

Sco

llars

(USD

)an

dis

calc

ulat

ed(L

CB

TC

pric

ein

USD)(U

SDB

TC

pric

e)minus

1w

here

the

Bitc

oin

pric

ein

USD

isth

em

ean

pric

eof

allU

SDtr

ansa

ctio

nson

the

Bits

tam

pex

chan

gefo

rtha

tday

The

Bitc

oin

pric

ein

loca

lcur

renc

yis

the

med

ian

pric

eof

exch

ange

son

bitc

oinc

hart

sco

mC

onve

rsio

nfr

omL

Cto

USD

isdo

neus

ing

FXda

tafr

omth

eSt

Lou

isfe

dan

dus

ing

the

OA

ND

Ada

ilyav

erag

era

teT

hein

depe

nden

tvar

iabl

esar

ede

fined

asin

Tabl

e8

Stan

dard

erro

rsar

ecl

uste

red

byco

untr

y

(1)

(2)

(3)

(4)

(5)

(6)

(7)

Bitc

oin

shor

t-te

rm0

0130lowastlowastlowast

001

75lowastlowastlowast

001

76lowastlowastlowast

001

30lowastlowastlowast

001

75lowastlowastlowast

001

76lowastlowastlowast

001

30lowastlowastlowast

vola

tility

(00

030)

(00

045)

(00

044)

(00

030)

(00

045)

(00

044)

(00

030)

Blo

ckch

ain

med

ian

000

040

0004

000

040

0004

000

04co

nfirm

atio

ntim

e(00

007)

(00

007)

(00

007)

(00

007)

(00

007)

Mea

nbl

ockc

hain

000

10lowastlowast

000

10lowastlowast

000

10lowastlowast

tran

sact

ion

fee

(00

004)

(00

004)

(00

004)

Eco

nom

icFr

eedo

mminus

002

16lowast

minus0

0216lowast

minus0

0216lowast

Ran

king

(00

126)

(00

126)

(00

126)

Cap

italC

ontr

ols

003

48lowast

003

48lowast

003

48lowast

Out

flow

(00

201)

(00

200)

(00

201)

Con

stan

t0

0341lowastlowast

019

36lowast

018

99lowast

019

13lowast

002

460

0209lowast

002

23lowastlowast

(00

142)

(01

088)

(01

034)

(01

030)

(00

160)

(00

112)

(00

108)

Obs

erva

tions

116

2811

628

116

2811

628

116

2811

628

R2

002

020

0599

006

020

0646

003

470

0350

Not

elowast plt

01lowastlowast

plt0

05lowastlowastlowast

plt0

01

23

6 Other Cryptocurrencies

As a robustness check we analyze how the Kimchi premium is related to the premiums of other

cryptocurrencies such as ethereum (ETH) ripple (XRP) and litecoin (LTX)23 For example if

the ethereum premium (defined similarly to the Kimchi premium) in South Korea was lower

than the Kimchi premium one could undertake arbitrage by buying Bitcoin in a US exchange

sending it to a Korean exchange selling the Bitcoin to buy ethereum in the Korean exchange

sending those ethereum to the US exchange and selling those ethereum for a profit Such a

transaction would only involve cryptocurrencies and hence not be subject to government fiat

capital controls We can apply similar arguments to any cases when the ethereum price differ-

ence is not equal to the Bitcoin price difference in both countries

We use the hourly closing price data in USD and KRW for Bitcoin (BTC) Ethereum (ETH)

Litecoin (LTC) and Ripple (XRP) from CryptoDataDownloadcom For the KRW exchange

Bithumb was used and Kraken for the USD exchange Exchanges were selected for ability to

trade the desired cryptocurrencies as well as volume and the length of sample Daily price for

each cryptocurrency was calculated as the arithmetic mean of the hourly closing prices for each

hour that day The Kimchi premium for each cryptocurrency was then calculated as in Equation

(1) for the main regressions It should be noted that the trading days of January 11-13 2018

are excluded from the sample as Kraken had a trading halt of approximately 48 hours due to a

system upgrade and associated bugs which included those days Results are robust to using a

sample which utilizes Bitstamp data to replace those 3 days

Consistent with the absence of arbitrage opportunities we find that premium differences

across cryptocurrencies are very small Table 5 shows that the average premiums across cryp-

tocurrencies are very close to each other The standard deviation tends to be higher if the pre-

mium is higher which further mitigates the premium difference (when one wants to try arbitrage

trading for such a small premium difference) Given that most exchanges in the world charge

23On May 16th 2018 the total market cap of bicoin ethereum ripple and litecoin is about 1430 710 279and 79 Billion USD respectively

24

minimum 05 and up to 1-2 transaction costs the premium differences are not enough to

cover the the total transaction costs to execute the arbitrage In addition Table 6 shows that the

correlation between the Kimchi premium and each cryptocurrency is very high Similarly the

pairwise correlation between all those premia are very high as shown by Table 7

Table 5 Summary statistics of Korean cryptocurrency premia 2017-10-01 to 2018-04-30

Statistic N Mean St Dev Min Max

KRWBTCprem 209 0072 0100 minus0045 0487KRWETHprem 209 0076 0109 minus0044 0550KRWLTCprem 209 0075 0106 minus0045 0525KRWXRPprem 209 0074 0111 minus0044 0535

Table 6 Regression of the Kimchi premium on other currency premia 2017-10-01 to 2018-04-30Jan 11 12 13 removed due to Kraken halting trading

Dependent variable

BTCprem

(1) (2) (3)

ETHprem 09108lowastlowastlowast

(00080)

LTCprem 09312lowastlowastlowast

(00070)

XRPprem 08864lowastlowastlowast

(00103)

Constant 00033lowastlowastlowast 00028lowastlowastlowast 00067lowastlowastlowast

(00011) (00009) (00014)

Observations 209 209 209R2 09841 09884 09726

Note lowastplt01 lowastlowastplt005 lowastlowastlowastplt001

The results are consistent with our assumption of capital controls driving the Kimchi pre-

mium If one of the other crypto currencies had no premium or a lower premium than Bitcoin

25

Table 7 Pairwise Correlation Matrix Korean cryptocurrency premia 2017-10-01 to 2018-04-30

KRWBTCprem KRWETHprem KRWLTCprem KRWXRPprem

KRWBTCprem 1 0992 0994 0986KRWETHprem 0992 1 0998 0995KRWLTCprem 0994 0998 1 0994KRWXRPprem 0986 0995 0994 1

arbitrageurs could use that currency to move funds out of Korea and complete the arbitrage

Since cryptocurrencies are not subject to capital controls no arbitrage opportunities between

cryptocurrencies should be possible This implies that all crypto currencies should have very

similar premia Similar to the logic with Bitcoin other crypto currencies can trade at a premium

since the arbitrage is restricted because of the capital controls The analysis shows that the Kim-

chi premium is therefore not something unique to Bitcoin but rather a result of Korearsquos capital

controls that prevent arbitrageurs from aligning Korean prices with those of the world market

Anecdotal evidence shows that traders in Korea are closely following the premia in different

cryptocurrencies Figure 6 shows a typical cryptocurrency trading discussion website in South

Korea As seen in the screen shot and its description Korean investors keep track of not only the

Kimchi premium on Bitcoin but also other cryptocurrency premiums If they find one premium

is significantly lower (or higher) than another premium they would sense it as the signal that

the corresponding coin is under- or over-valuated within the Korean market which leads to

push up or down the coin premium Consequently the coin premiums are more and less the

same in each time as seen in the green number inside each parenthesis in Columns 3 to 7 in the

table in the figure Traders also watch out the premiums across major Korean exchanges This

mechanism would be a main reason why the Korean premiums stays more and less the same

across cryptocurrencies over time

26

7 Conclusion

We document that despite its global reach and absence of regulation Bitcoin and other cryp-

tocurrencies can trade at substantial and persistent premia relative to other markets like the US

Comparing Korean and European markets we find that Bitcoin trades on average at a signifi-

cantly higher price in Korea and that the premium that Korean investors have to pay is more

sensitive to factors that make arbitrage more costly like transaction fees confirmation times

and short term volatility We argue that capital controls for fiat money is the main source of

these frictions Looking at an international sample we find that Bitcoin trades at a higher price

in countries with less economic freedom We also find that the trading volume is negatively as-

sociated with the Kimchi premium contrary to the prediction of the general stock market bubble

literature which confirms that the Bitcoin microstructure is important to understand the Kimchi

premium

It is notable that when Sangi Park the Minister of Justice in Korea announced the ban

of crypto-exchanges on January 11 201824 he concluded from the existence of the rdquoKimchi

premiumrdquo that cryptocurrecy trading in Korea is abnormal Likewise many Korean government

officials often branded cryptocurrency traders as irrational and stated that the exchanges (or the

way the exchanges are operated) contributed to the irrational Kimchi premium The Korean

government has continuously intervened in cryptocurrecy markets since the summer of 201725

We argue that capital controls imposed by the Korean government rather than behavioral

explanations are the cause of the Kimchi premium Instead of irrational traders or poorly func-

tioning exchanges it seems that the Korean government is the main contributor to the Kimchi

premium Our paper also shows that the dream of a global currency that is free from government

interventions remains an illusion

24The fact that the head of the task force team on the cryptocurrency trading in the Korean government is theMinister of Justice not the Minister of Finance implies that the Korean government considered cryptocurrecytrading as gambling

25The timeline of the Korean government interventions are found in Section 2타임라인 (Timeline) of thefollowing website httpsnamuwikiw대한민국의암호화폐규제논란

27

References

Alvarez Luis H R and Jussi Keppo 2002 The impact of delivery lags on irreversible invest-ment under uncertainty European Journal of Operational Research 136 173ndash180

Athey Susan Iva Parashkevov Vishun Sarukkai and Jing Xia 2016 Bitcoin pricing adoptionand usage Theory and evidence working paper

Brennan Michael and Eduardo Schwartz 1985 Evaluating natural resources investment TheJournal of Business 58 135ndash157

Chen Joseph Harrison Hong and Jeremy Stein 2002 Breadth of ownership and stock returnsJournal of Financial Economics 66 171ndash205

Clements Kenneth W Yihui Lan and Shi Pei Seah 2012 The Big Mac Index two decades onan evaluation of burgernomics International Journal of Finance and Economics 17 31ndash60

Cong Lin William Zhiguo He and Jiasun Li 2018 Decentralized mining in centralized poolsworking paper

Cong Lin William Ye Li and Neng Wang 2018 Tokenomics dynamic adoption and valua-tion working paper

Corbet Shaen Charles Larkin Brian Lucey Andrew Meegan and Larisa Yarovaya 2017Cryptocurrency Reaction to FOMC Announcements Evidence of Heterogeneity Based onBlockchain Stack Position

De Jong Abe Leonard Rosenthal and Mathijs Van Dijk 2009 The Risk and Return of Arbi-trage in Dual-Listed Companies Review of Finance 13 495ndash520

Detzel Andrew Hong Liu Jack Strauss Guofu Zhou and Yingzi Zhu 2018 Bitcoin learningpredictability and protfitability via technical analysis working paper

Easley David Maureen OrsquoHara and Soumya Basu 2017 From mining to markets the evolu-tion of bitcoin transaction fees working paper

Edwards Sebastian 1999 How effective are capital controls Journal of Economic Perspec-tives 13 65ndash84

Fernandez Andres Michael W Klein Alessandro Rebucci Martin Schindler and Martin Uribe2015 Capital control measures A new dataset Working paper National Bureau of Eco-nomic Research

Fischer Andreas M and Angelo Ranaldo 2011 Does FOMC news increase global FX tradingJournal of banking amp finance 35 2965ndash2973

28

Froot Kenneth A and Emil M Dabora 1999 How are stock prices affected by the location oftrade Journal of Financial Economics 53 189ndash216

Gagnon Louis and G Andrew Karolyi 2010 Multi-market trading and arbitrage Journal ofFinancial Economics 97 53ndash80

Gandal Neil JT Hamrick Tyler Moore and Tali Oberman 2018 Price manipulation in thebitcoin ecosystem Journal of Monetary Economics 95 86ndash96

Griffin John M and Amin Shams 2018 Is Bitcoin Really Un-Tethered working paper

Gromb Denis and Dimitri Vayanos 2010 Limits of arbitrage Annu Rev Financ Econ 2251ndash275

Harrison Michael and David Kreps 1978 peculative investor behavior in a stock-market withheterogeneous expectations Quarterly Journal of Economics 92 323ndash336

Hong Harrison Jose Scheinkman and Wei Xiong 2006 Asset Float and Speculative BubblesJournal of Political Economy 111 1073ndash1117

Hu Albert S Christine A Parlour and Uday Rajan 2018 Cryptocurrencies stylized facts ona new investible instrument working paper

Huberman Gur Jacob Leshno and Ciamac C Moallemi 2017 Monopoly without a monopo-list an economic analysis of the bitcoin payment system working paper Columbia Univer-sity

Lucca David O and Emanuel Moench 2015 The Pre-FOMC Announcement Drift The Jour-nal of Finance 70 329ndash371

Makarov Igor and Antoinette Schoar 2018 Trading and Arbitrage in Cryptocurrency Marketsworking paper

McDonald Robert and Daniel Siegel 1986 The value of waiting to invest The QuarterlyJournal of Economics 101 707ndash727

Mei Jianping Jose Scheinkman and Wei Xiong 2009 Speculative trading and stock pricesEvidence from Chinese AB share premia Annals of Economics and Finance 10 225ndash3255

Miller Edward 1997 Risk uncertainty and divergence of opinion The Journal of Finance 321151ndash1168

Pagnottayand Emiliano S and Andrea Buraschi 2018 An equilibrium valuation of Bitcoinand decentralized network assets working paper

Pakko Michael R and Patricia S Pollard 2003 Burgernomics A Big Mac guide to purchasingpower parity Federal Reserve Bank of St Louis Review 85 9ndash28

29

Rogoff Kenneth 1996 The purchasing power parity puzzle Journal of Economic Literature34 647ndash668

Rosenthal Leonard and Colin Young 1990 The seemingly anomalous price behavior of RoyalDutchShell and Unilever NVPLC Journal of Financial Economics 26 123ndash141

Scheinkman Jose and Wei Xiong 2003 Overconfidence and speculative bubbles Journal ofPolitical Economy 111 1183ndash1219

Sockin Michael and Wei Xiong 2018 A model of cryptocurrencies working paper

Taylor Alan M and Mark Taylor 2004 The purchasing power parity debate Journal of Eco-nomic Perspectives 18 135ndash158

Xiong Wei 2013 Bubbles crises and heterogeneous beliefs Handbook for Systemic Riskedited by Jean-Pierre Fouque and Joe Langsam pp 663ndash713

Xiong Wei and Jialin Yu 2011 The Chinese warrants bubble American Economic Review101 2723ndash2753

30

A Appendix - Theory

The appendix provides the theoretical background on our empirical conjectures We model

the arbitrage transaction as a real option exercise such as Brennan and Schwartz (1985) and

McDonald and Siegel (1986)

A1 Description

If the Kimchi premium is sufficiently high each arbitrageur will buy bitcoins in an US ex-

change transfer them to the Korean exchange and finally sell the bitcoins in the Korean ex-

change We call all these three activities together lsquoarbitrage tradingrsquo The whole process cannot

take place immediately Rather there is time delay about which we will discuss later

Notice that due to the capital control imposed by the Korean government each arbitrageur is

allowed to transfer a limited amount of cash (dollars) from South Korea to the US (or any other

country) per year which means one can execute the arbitrage transaction only finite number of

times a year Without loss of generality we assume that one can execute the arbitrage transac-

tion ldquoonly oncerdquo but instead heshe will fully exploit the cash transfer limit when executing it

In this sense the arbitrage trading can be considered as an irreversible investment opportunity

It is important to note that this irreversibility arises from the capital control Without the capital

control one can execute arbitrage trading infinitely times and thus there is no reason for arbi-

trageurs to wait to obtain the maximum profit by using one-time opportunity This is the case

of Europe and the US between which the price differential is negligible over time

Note that there are two types of risks when executing the arbitrage trading (i) risk from the

transaction time lag and (ii) risk in the fee to transfer a bitcoin from a wallet to a wallet First

it takes time to send bitcoins from a wallet in a US exchange to one in a Korean exchange

This time lag creates risk due to a high short-term volatility of the premium the arbitrageur

may fail to obtain the price differential because the premium may become negligible before the

31

bitcoins arrive the arbitrageurrsquos wallet in the Korean exchange Second in order to expedite the

wallet-to-wallet transfer of bitcoin one can pay extra fees to a miner Then it can shorten the

time lag but it is sometimes very costly in the sense that this transaction fee is not deterministic

but stochastically changing over time There are other fees such as transaction fees paid to each

exchange and the fee for currency exchange which are also somehow time-varying Note that

we ignore these fees in our formal model in Section A2

Without loss of generality we assume that arbitrageurs are homogeneous in terms of cost of

executing the arbitrage trading since they are constrained under the same capital control Note

that our results will hold as long as there exists a significant number of cost-homogeneous ar-

bitrageurs although there is no homogeneity in the whole population of arbitrageurs If these

cost-homogeneous arbitrageurs simultaneously execute the arbitrage trading the premium sud-

denly drops down to a negligible level as a result of massive trading which often appears as a

spike in the time series of the premium as seen in Figure 1 Before then the premium can keep

increasing to a fairly high level since arbitrageurs should wait due to the short-term volatility

risk In other words arbitrageurs delay to execute the arbitrage transaction until the premium

becomes sufficiently high In summary we suggest the following predictions

A The higher the short-term volatility the greater the Kimchi premium

B The higher the fee volatility the greater the Kimchi premium

C Spikes in the premium time series tend to accompany with the massive influx of bitcoins

into a Korean exchange

First note that statement B is not easy to test due to the data issue including endogeneity An

easier task is to simply consider the average fee in each block and investigate its impact on the

premium According to a standard real option argument it is easy to see that as the cost of

executing arbitrage trading becomes higher the executions is further delayed So we suggest

the following substitute statement

32

Bprime The higher the fee the greater the Kimchi premium

Second also note that for statement C we investigate whether there is massive influx of

bitcoin into Korean exchange(s) before or near the spike However we do not have enough data

period to see if it is the case Instead statement C is restated as the following statement

C prime There is no massive influx of bitcoins into a Korean exchange (ie no arbitrage transac-

tion is executed) in the times when the Kimchi premium is sufficiently small

A2 Formal Model

Now we provide a formal description of the model We extend the delivery lag model of a

real option suggested by Alvarez and Keppo (2002) Time is continuous Arbitrageurs are

risk-neutral and is endowed with one bitcoin in the US exchange They can execute only one

arbitrage trading The current time is t = 0 at which the Kimch premium is small enough so

that no arbitrageurs are willing to trade Suppose the Kimchi premium X(t) (price differential)

follows geometric Brownian motion26

dX(t) = microX(t)dt+ σX(t)dBt X0 = x

where Bt is a standard Brownian motion and micro and σ are positive constants

We model the mean value of a wallet-to-wallet transaction fee to a miner C(t) as follows

dC(t) = microcC(t)dt+ σcC(t)(ρdBt +radic

1minus ρ2dBct ) C0 = c

where Bct is a standard Brownian motion independent of Bt Here microc and σc are positive con-

stant ρ is the correlation between X(t) and C(t)

26One can consider the arithmetic Brownian motion or mean reversion process The result will not be changed

33

Suppose the arbitrageur execute the arbitrage transaction at t Then at time t + ∆(Xt)

hisher net profit will be

X(t+ ∆(Xt))minus C(t)

where the time delay ∆ = ∆(x) is a function of the premium

Then the value function (expected profit) of the arbitrageur V (x) is defined by

V (x) = maxτ

E[eminusrτ (eminusr∆(X(τ))X(τ + ∆(X(τ)))minus C(τ)) |X0 = x

] (2)

where r is the risk-free rate with r gt micro

The problem will formally be the same if the cost is fixed (see egMcDonald and Siegel

(1986)) Thus without loss of generality we assume Ct = C = 1 Instead of normalizing Ct

as 1 later we will interpret the optimal threshold by using the ratio of X(t)C(t) With this

assumption and using the Markov property we rewrite (2) as

V (x) = maxτ

E[eminusrτ (π(X(τ))minus 1) |X0 = x

]for all t ge 0 (3)

where the profit function π(x) is defined by π(x) = xeminus(rminusmicro)∆(x) Note that

π(Xt)minus 1 le Xt minus 1

which implies that the value from the time lag is smaller than the value without the time lag

This effect further delays the execution of the arbitrage trading which can potentially generates

a fairly high premium Proposition 1 describes the optimal exercise strategy Before we provide

the proposition we define λ gt 0 by the positive root of the following characteristic equation

1

2σ2λ(λminus 1) + microλminus r = 0

34