bitcoin group se · the bitcoin group operates the only authorised german marketplace for the...

TRANSCRIPT

Montega AG – Equity Research

1

BITCOIN GROUP SE

Recommendation: n.a.

Price target: n.a.

Upside potential: n.a.

Share data Share price EUR 24.60 (XETRA)

Number of shares (in m) 5.00

Market cap. (in EUR m) 123.0

Enterprise Value (in EUR m)

120.2

Code ADE

ISIN DE000A1TNV91

Performance 52-week high (in EUR) 29.90

52-week low (in EUR) 5.00

3M rel. to CDAX +203.2%

6M rel. to CDAX +240.9%

Source: Capital IQ

Shareholder structure Priority AG 77.2%

Free float 22.8%

Calendar AGM 28 August 2017

H1 report 28 August 2017

Changes in estimates 2017e 2018e 2019e

Sales (old) - - - Δ in % - - -

EBIT (old) - - -

Δ in % - - -

EPS (old) - - -

Δ in % - - -

Analysts Frank Biller, CFA Henrik Markmann

+49 40 41111 37 67 +49 40 41111 37 84

[email protected] [email protected]

Publication

Report 31. August 2017

Leading platform provider in a niche with disruptive potential

End of financial year: 31 Dec. 2015 2016

Sales 780.0 1,126.3 Change yoy n.a. 44.4% EBITDA -46.6 -95.1 EBIT -63.4 -112.0 Net income -16.1 114.2

Gross profit margin 83.6% 88.4% EBITDA margin -6.0% -8.4% EBIT margin -8.1% -9.9%

Net debt -1,688.6 -2,775.5 Net debt/EBITDA 36.2 29.2 ROCE n.a. -3.2%

EPS 0.00 0.02 FCF per Aktie -0.08 0.06 Dividend 0.00 0.00 Dividend yield 0.0% 0.0%

EV/Sales 154.1 106.7 EV/EBITDA n.m. n.m. EV/EBIT n.m. n.m. PER n.m. 1,230.0 P/B 22.6 20.2 Source: Company data, Montega, CapitalIQ Data in EUR thsd., EPS in EUR Price: 24.60

4.80

9.80

14.80

19.80

24.80

29.80

0

10

20

30

40

50

60

70

23-Aug 4-Nov 16-Jan 30-Mar 11-Jun 23-Aug

Share price Volume

Volume (in thsd.) Share price (in EUR)

The Bitcoin Group has positioned itself early in the market as an investment company focusing on innovative business models in the field of cryptocurrencies and blockchain technologies. The corresponding Bitcoin.de trading platform enjoys its monopoly-like market position in the DACH region as Germany’s only regulated marketplace for the digital currency bitcoin.

The market for virtual currencies has grown significantly over the last few years leading to the existence of over 800 different cryptocurrencies to date that can be globally traded on more than 100 platforms. Measured by market capitalisation, the bitcoin is the most important and oldest representative with a share of some 46%. Cryptocurrencies are increasingly seen as an alternative to classical monetary systems and can be used both to process transactions and as a store of value.

Consequently, the Bitcoin.de platform saw rapid user growth of more than 6,200 per month last year. This is attributable to the Bitcoin Group’s first-mover advantage in the German-speaking area. Thanks to the broad customer base of some 460k users (MONe) the platform processes large transaction volumes and has high liquidity. This is difficult to replicate by competitors and represents a high barrier to market entry.

Based on the increased trading volume on Bitcoin.de, the Bitcoin Group generated significant revenue growth (some 44% to EUR 1.13m) in the last fiscal year. On the bottom line, the major expense items rose disproportionately low which reflects the business model’s high scalability. The company has already approached the breakeven point despite its relatively short history in a still young market.

On this basis, we assume that the positive development will gain momentum in the current fiscal year. The bitcoin price volatility has risen towards mid-year which we believe will have a positive impact on trading volume and revenue. The recently reported H1 figures are an impressive indicator of this development (revenue: +128%, EBT: +240%). Furthermore, the implementation of trading Ethereum, the second-largest cryptocurrency, planned for H2 should add 10% to 20% p.a. to revenue potential.

Conclusion: The Bitcoin Group shares are an investment in an already established business model that is based on a still young and presumably disruptive technology. Although we cannot make a quantitative valuation with a DCF model because of the low visibility on the future significance of cryptocurrencies, we regard the present market position of the Bitcoin Group as very good. The company should be able to participate in the strongly growing market of virtual currencies to an above-average extent.

Montega AG – Equity Research

2

BITCOIN GROUP SE

TABLE OF CONTENTS

Investment Case 3

Use of technologies with disruptive potential 3 Monopoly-like competitive position in the DACH region 4 Leading market position based on first-mover advantage 5 Revenue and earnings trend driven by rapid customer growth 6 Continued positive news flow likely to support equity story 6 Low visibility in conflict with quantitative valuation 6 Conclusion 7

Timing and sentiment 8

News flow expected to remain positive 8

SWOT 9

Strengths 9 Weaknesses 9 Opportunities 9 Risks 9

Market and competition 11

Cryptocurrencies as an alternative to bank money 11 Internationally fragmented competitive situation 13 Versatility of the blockchain technology enables portfolio expansion 14 Regulatory state interventions are unpredictable 14

Competitive quality 15

Leading market position in the DACH region 15 Strong organic acquisition of new customers 15 Sophisticated security concept 15 Highly scalable business model 16 High liquidity thanks to large user base 16

Financials 17

Dynamic growth of customers and revenue in 2016 17 Improved earnings and continued strong customer growth anticipated 17 Future plans involve building an investment portfolio 18 Balance sheet 18

Company Background 19

Company history 19 Markets and revenue 20 Products 20 Experienced management 21 Shareholder structure 22

Appendix 23

Disclaimer 26

Montega AG – Equity Research 3

Investment Case BITCOIN GROUP SE

INVESTMENT CASE

The Bitcoin Group operates the only authorised German marketplace for the digital currencies bitcoin (BTC) and Bitcoin Cash (BCH) under the domain Bitcoin.de. Going forward, it is planned to start trading additional cryptocurrencies (e.g. Ethereum) and acquire stakes in other companies in the field of digital currencies and blockchain technology.

A growing digitisation and loss of confidence in the financial system after the global financial crisis have led to a significant increase in the number of virtual currencies over the last few years. At present, there are more than 800 different currencies of this kind around the world. With a market capitalisation of some USD 70bn (source: coinmarketcap.com) and a market share of some 46%, Bitcoin is the oldest and most widespread cryptocurrency. Both the rapidly growing market of virtual currencies and the market environment of blockchain, the underlying technology behind bitcoins, offer high potential for growth for the Bitcoin Group.

Use of technologies with disruptive potential

Cryptocurrencies such as bitcoins differ from bank money in the following aspects:

Technical limitation of the bitcoin volume to 21m units, a protection against inflation.

Transactions are largely anonymous, as there is no exchange of personal data between sender and receiver.

Transactions do not require an intermediary in the form of a bank, and to date there is no state regulation either.

To be perceived as a serious competitor of established electronic payment systems such as Mastercard or Visa bitcoin is still lacking broad acceptance. At present, there are some 300k bitcoin transactions per day on a global scale, whilst e.g. Mastercard or Visa alone process up to 2k transactions per second. Yet it appears that bitcoin has increasingly found its way into everyday life, and there are even some well-known companies that are already accepting bitcoin as a means of payment (e.g. Microsoft, Dell, Expedia, Lieferando).

In addition to its function as a means of payment, the bitcoin can also serve as a store of value. Major drivers of investments in bitcoins often are unconventional measures of the central banks, i.e. negative interest rates or large-scale bond purchases. These monetary policy decisions are often perceived as a big risk to the financial system and increase demand for alternatives to the existing currencies. The diagram below shows the bitcoin price development of the past years.

Source: ariva.de

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

August-11 October-12 December-13 February-15 April-16 June-17

Development of the bitcoin price in euro

Montega AG – Equity Research 4

Investment Case BITCOIN GROUP SE

Unlike the central bank money, there will be a limited supply of bitcoins faced by an ever-growing demand going forward unless a multitude of similar cryptocurrencies is established. We expect only few digital currencies to prevail in the long term. However, it is not yet possible to draw a conclusion on the future importance of cryptocurrencies and the bitcoin due to their relatively short history. Regulatory interventions by the state are currently difficult to predict as well. We believe there is general support for blockchain, the underlying technology behind bitcoin, whereas a parallel (virtual) currency system is currently not in the central banks’ interest.

In the future, numerous other blockchain business models will emerge in addition to the bitcoin, and these models may also be considered as an investment opportunity for the Bitcoin Group. The blockchain technology is rated as being extremely efficient and secure, and is currently examined by several market participants (especially banks and fintechs) in terms of its applicability. The blockchain, as a decentral encryption and identification technology, should be able to manage much more than only monetary units (e.g. property rights). These promising prospects are supported by growing venture capital investments in the field of blockchain business models. Global VC investments rose by some 23% to c. USD 544m last year and should have the tendency to increase competition in the next few years.

Monopoly-like competitive position in the DACH region

Overall, there are currently far more than 100 trading platforms for cryptocurrencies, which in technical terms are divided into marketplaces and exchanges. Marketplaces such as Bitcoin.de process purchases and sales manually, whereas the transactions at an exchange are processed automatically. Bitcoin Deutschland AG acts as a tied agent of Munich-based Fidor Bank. This means that the Bitcoin Group operates in a scope approved by the Federal Financial Supervisory Authority.

The company’s trading platform enjoys a monopoly-like market position in Germany as the only regulated provider thanks to an early market entry and already has a critical mass of user. Accordingly, its trading volume is high. The table below shows the major competitors offering an exchange in EUR/BTC, ranked by bitcoin trading volume in the last 30 days.

Source: Bitcoincharts.com, updated: 23.08.2017

Most platforms enable trading in various cryptocurrencies. The Bitcoin.de trading platform is also planned to be expanded to a multi-currency platform. This will significantly reduce the dependency on the development of individual digital currencies. It is possible for online users to access the services of foreign providers without any problems. However, in addition to the fee structure, security aspects and the platform’s reputation increasingly come to the fore.

In the medium to long term, renowned online banks may also enter the market alongside existing platforms when digital currencies will establish themselves as an asset class. They would be serious competitors because of their comprehensive customer base and large

Competitor

(Headquarters)

Trading volumen of the

last 30 days (in BTC)

Kraken (USA)

zyado (Portugal)

CoinsBank (Scottland)

GDAX (USA)

Bitcoin.de (Germany)

The Rock Trading (Malta)

CEX.IO (UK)

LocalBitcoins (Finland)

Paymium (France)

- Fees: 0.59% + additional fees depending on payment method

BitBay (Polen)

1,956.8- First european exchange which fulfilled european regulations (money ist not secured)

369.1- Supports various payment methods (like SEPA, credit card, express payment via DotPay)

- Fees: 0.25 to 0.43%

4,112.0- First cloud-based supplier with more than 700,000 user globally

- Fees: 0.1 to 0.2%

2,650.5- Marketplace-model with acceptance of almost every payment method

- Fees: 0.0 to 1.0%

27,636.1- Marketplace-model with express trading option and 2-factor authentification

- Fees: 0.3 to 0.5%

4,804.3- One of the oldest transaction systems with various cryptocurrencies

- Fees: 0.02 to 0.20%

60,649.0- Provides also a debit card

- Fees: 0.5%

52,438.6- Margin-trading possible

- Fees: 0.10 to 0.25%

Characteristic

358,773.6- Trade between bitcoins and EUR, USD, CAD, GBP and JPY possible

- Fees: 0.10 to 0.26%

71,113.0- Marketplace-model analogous Bitcoin.de with 2-factor authentification

- Fees: 0.10 to 0.25%

Montega AG – Equity Research 5

Investment Case BITCOIN GROUP SE

resources. Given the existing cooperation with Fidor Bank and the gateway to the banking system, however, we continue to expect that Bitcoin.de may respond to this development by cooperating with other partners to defend its market position in the DACH region.

Leading market position based on first-mover advantage

We regard the leading market position in the DACH region as secured because of the existing comprehensive customer base of some 460k users (MONe) to date and the strong organic acquisition of new customers which Bitcoin.de has attained almost without any marketing expenses. Last year the average monthly increase in new customers amounted to 6,200 users. The development of user numbers of trading platform Bitcoin.de below illustrates that the public interest is high despite the uncertainties mentioned above.

Source: Company, Montega

We expect the current strong media attention to come along with further growth. The blog (bitcoinblog.de) and the forum (coinforum.de) on the topic of cryptocurrencies, which both refer to the Bitcoin.de platform, generate important traffic as well. At the same time, we believe the intuitive domain (Bitcoin.de) and the company’s leading position in the organic search results of search engines will ensure that the user growth remains high.

The diversified security concept of Bitcoin Deutschland AG contributes to the fact that the platform’s high reputation remains valid. Bitcoin.de uses a modern two-factor authentication during the login process to prevent malpractice and fraud. The platform also differs from other portals in that the customers keep their money for transactions on their own deposit-insured accounts instead of the portal operator’s account. Consequently, losses in case of insolvency of the operator can be ruled out. As another security measure, Bitcoin.de stores 98% of the bitcoin portfolio offline in the so-called cold wallet (physical separation from the internet on e.g. separate data media. The remaining 2% are regularly made available on servers located in Germany for the customers’ pay-out requests and are hedged by the Bitcoin AG’s own euro and bitcoin portfolios many times over. This minimises possible financial damages caused by a hacker attack as well as the risks of a reputational damage.

Given that the Bitcoin.de platform’s investment measures, which had been significant in the beginning, are already completed thanks to its early market entry the high scalability of the business model should become visible. From now on, increases in sales and earnings will require only little backing e.g. by workforce exp. The highly scalable business model and the comprehensive customer base of Bitcoin.de make it much more difficult for potential competitors to enter the market.

Finally, the Bitcoin.de’s large trading volume also is a considerable barrier to market entry. The number of users, which has become substantial by now, ensures the trading platform’s high liquidity on a daily basis and attracts additional customers. We believe this is a competitive advantage that cannot be replicated immediately.

281 k 300 k

319 k 337 k

356 k

393 k

430 k

460 k 480 k

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

450.000

500.000

Dec-15 Mar-16 June-16 Sep-16 Dec-16 Mar-17 June-17 Sep-17 Dec-17

Development of the Bitcoin.de customer base

CAGR: 31%

Montega AG – Equity Research 6

Investment Case BITCOIN GROUP SE

Revenue and earnings trend driven by rapid customer growth

The strong competitive position and the significantly increased activities on the platform have also been reflected in the 2016 figures published at the end of June, with the Bitcoin Group’s with-time adoption of International Financial Reporting Standards. Revenue was up some 44% to EUR 1.13m (PY: EUR 0.78m).

On the bottom line, EBIT declined from EUR -63k to EUR -112k. This was mainly driven by much higher other operating expenses, namely the change in the company’s own bitcoin portfolio by almost EUR 300k, which therefore is not related to operating expenses. The other expense items rose at a disproportionately low rate which underlines the business model’s high scalability.

Based on the good development and the favourable environment, the company has already raised its guidance for the current fiscal year towards mid-year. Instead of a “moderate earnings development” the Bitcoin Group now expects a “strong increase” in net income. The preliminary key figures on the business development in H1 underline the increased outlook. Revenue rose by 128.3% to EUR 1.77m. Pre-tax earnings grew disproportionately by 240.2% to EUR 1.22m.

Bitcoin Group SE – H1 2017 H1/2017p H1/2016 yoy

Sales 1.8 0.8 128.4%

EBT 1.2 0.4 239.8%

EBT margin 68.9% 46.3% Source: Company Figures in EUR m

On the top line, the planned launch of trading of Ethereum, the second largest cryptocurrency based on market cap, in the third quarter is expected to generate additional sales potential of 10% to 20% p.a. Furthermore, the company aims for a strong increase in commission income in the current year already which is achieved through growth of customers to more than 450k (MONe: 480k, 31.12.2016: 356k). Additionally, the high volatility of the bitcoin prices towards the middle of the year is likely to have a positive impact on trading volume and, therefore, on full-year revenue. The company’s own bitcoin portfolio has also benefited from the recent very positive price trend, which has substantially increased the company’s financial position.

Continued positive news flow likely to support equity story

Last months’ news flow was characterised by the publication of the 2016 Annual Report, the increased qualitative outlook on net income for the current fiscal year and the recently communicated preliminary H1 figures. The broad media coverage generated additional attention. Various well-known newspapers and specialised magazines have reported on the bitcoin and the Bitcoin Group. We expect media interest in the topics of cryptocurrencies and blockchain technologies to remain high in the further course of the fiscal year, which should also contribute to a further growing awareness of the Bitcoin Group and the Bitcoin.de platform respectively. This and the planned implementation of Ethereum trading should lead to continuing strong organic growth of the customer numbers and a corresponding good news flow.

In the medium term, we also expect to hear news regarding the expansion of the investment portfolio. In this case, we believe a capital increase to be likely. As the Bitcoin Group aims for investments in companies which have already delivered proof of concept and where it is apparent that profitability will be achieved in the foreseeable future, we expect the first success stories from 2018 at the earliest. Overall, we assume that the awareness of the equity story of the current only listed pure play, Bitcoin Investments, will significantly increase over the next few weeks due to the planned intensification of the capital market communication.

Low visibility in conflict with quantitative valuation

We have not conducted a traditional valuation on the basis of a DCF model or a peer group comparison because of the lack of history and visibility on the development of

Montega AG – Equity Research 7

Investment Case BITCOIN GROUP SE

cryptocurrencies. That said, we believe the Bitcoin Group is very well positioned to participate to an above-average extent in the strongly growing market of virtual currencies. This view is primarily based on the high competitive quality explained above. Against this background we see an investment as liquid venture capital.

Conclusion

The Bitcoin Group has positioned itself early in the growth market of cryptocurrencies. By now, the company is serving an ever larger and constantly growing customer base via its Bitcoin.de trading platform. The highly scalable business model should significantly drive earnings with a continuing increase in the number of users.

Montega AG – Equity Research 8

Timing and sentiment BITCOIN GROUP SE

TIMING AND SENTIMENT

The Bitcoin Group’s share prices were characterised by high volatility and a low trading volume in the last year. This should have been due to both the still low awareness of the Bitcoin Group and the Düsseldorf stock exchange. In October 2016, the company started trading on the open market of the Frankfurt stock exchange on Xetra and the Frankfurt floor exchange, which has led to significantly higher trading volumes. Going forward, the company aims to change to the regulated market. Based on the necessary free float of at least 20% trading volumes are expected to rise further.

Source: Capital IQ

News flow expected to remain positive

In the past weeks, the news flow was characterised by the publication of the 2016 Annual Report and an increased outlook on net income for the current fiscal year. The Bitcoin Group has more than doubled revenue in H1 2017 and consequently, the outlook on net income was adjusted from “moderate growth” to “strong increase”.

An increasing media interest in the topic of cryptocurrencies and blockchain technologies will create further attention. Meanwhile, many renowned financial institutions, central banks and big corporations and the like have expressed their opinion as well. We believe the ongoing discussion about possibilities to use virtual currencies or the blockchain technology will ensure that the public awareness continues to grow. Coupled with this, the company has announced that it wants to intensify communication with the capital market participants. This will further enhance the awareness of the equity story of the only listed pure play, Bitcoin Investments.

We expect the news flow to remain positive. To begin with, the company should announce the implementation and commencement of trade of the Ethereum cryptocurrency in H2. This should further drive new customer acquisition and have a positive impact on trading volumes. Consequently, we anticipate another strong increase in users which should then also be reflected in the sales and earnings development for the full year. In the medium term, we expect to hear news on the further expansion of the investment portfolio. In this context, a capital increase might also be an option in our view.

0

10

20

30

40

50

60

70

4,00

9,00

14,00

19,00

24,00

29,00

August-16 November-16 February-17 May-17 August-17

Bitcoin Group SE share price (Düsseldorf Stock Exchange)

Volume (in thsd.) Share price (in EUR)

Montega AG – Equity Research 9

SWOT BITCOIN GROUP SE

SWOT

The Bitcoin Group operates Bitcoin.de, the leading trading platform for the bitcoin cryptocurrency in the German-speaking area. The Bitcoin Group has only just begun to build its investment portfolio. Our SWOT analysis summarises what we believe are the particular strengths and weaknesses as well as the opportunities and risks of the company the market environment.

Strengths

The Bitcoin Group benefits from the trading platform’s strong sales growth in the German-speaking area. The profitability is expected to grow disproportionately to sales due to the business model’s scalability.

The dynamic acquisition of users is due to the leading positions in the organic search results of search engines, the reach of the related blog and forum on the topic of cryptocurrencies, while marketing expenses are very low.

Although Bitcoin Deutschland AG is a young company in a dynamic market it has already come close to the breakeven point.

The company operates in a market environment with growth potential due to different market drivers (doubts concerning bank money systems, anonymous payment processes, efficient international electronic means of payment).

Thanks to various security measures trading activities on the Bitcoin.de platform have not been affected so far, apart from maintenance work. Security and stability should be seen as a strong asset, especially in this early stage.

Weaknesses

Bitcoin Deutschland AG develops and finances the operation of the trading platform with its own funds. Limited resources may be an obstacle for rapid advancements and adjustments of the platform in a changing market environment.

The network of cooperation partners is still relatively small. This is basically a risk to the market position.

The Bitcoin Group still has no track record in its planned investment areas of cryptocurrencies and blockchain.

Opportunities

The launch of trading in other currencies, mainly Ethereum in the short term, on the trading platform should significantly expand the revenue basis.

The further establishment of bitcoin as a means of payment and store of value is expected to sustainably support the acquisition of users and is an important basis for the strong trading activities on the platform in the long term.

The acquisition of further cooperation partners or the implementation of a bitcoin exchange would broaden the reach of the trading platform and strengthen the leading market position.

Management’s expertise gained from the successful setup of the Bitcoin.de trading platform is a very good basis for the establishment of further business models in the fintech sector.

Risks

Direct banks with extensive resources or start-ups taking up trading with cryptocurrencies may endanger Bitcoin.de’s leading position.

Montega AG – Equity Research 10

SWOT BITCOIN GROUP SE

The Bitcoin.de platform is active in an increasingly transparent market, in which competition between the leading platforms also takes place on the level of the transaction fees. Consequently, there is the risk of an increasing price pressure.

Both a decline in the current large public interest in the topic of cryptocurrencies and a sharp correction of the bitcoin prices may reduce user activities and thus have a negative impact on the revenue development.

Further expansion of bitcoin as a means of payment and store of value should increase the focus of state regulations on cryptocurrencies. This should increase the time and effort for operators of operating platforms and may also require adjustments of business models.

Despite comprehensive security measures (e.g. to have all servers operate in Germany or the two-factor authentiation), system failures or hacker attacks cannot be fully excluded.

Montega AG – Equity Research 11

Market and competition BITCOIN GROUP SE

MARKET AND COMPETITION

Bitcoin Group SE is an investment and consulting company that is focused on bitcoin and blockchain business models. The addressed markets for cryptocurrencies and blockchain technologies are enjoying an ever-increasing attention, especially from the financial sector.

Based on an increasing digitisation of social life the financial sector, and here particularly payment systems, are undergoing a radical change. The bitcoin, the oldest example of a cryptocurrency, is the new digital currencies’ most prominent representative with an overall market capitalisation of some USD 70bn (some 46% of the market shares). To participate in cryptocurrencies’ growth trend the Bitcoin Group has positioned itself at an early stage with the Bitcoin Deutschland AG. As well as the rapidly growing market of digital currencies, the group considers applications around blockchain, the underlying technology behind bitcoins, to be relevant as well.

Cryptocurrencies as an alternative to bank money

Virtual currencies such as bitcoins can also be seen as a result of the loss in confidence in the financial system after the global financial crisis, and have significantly gained in importance over the last few years. The bitcoin as the first publicly traded cryptocurrency has existed since 2009. The global number of different cryptocurrencies has grown to slightly over 800 since then. The ten largest virtual currencies are listed below, ranked by market cap.

Top 10 Cryptocurrencies Market share

(in percent) Market capitalization

(in USD m) Trading volume

(past 24h in USD m)

Bitcoin 45.5% 69,710.7 2,414.9

Ethereum 19.6% 30,095.2 870.6

Bitcoin Cash 7.2% 10,987.1 646.2

Ripple 7.1% 10,864.5 2,157.0

Litecoin 1.6% 2,496.1 138.1

IOTA 1.6% 2,396.4 28.8

NEM 1.5% 2,228.9 10.1

Dash 1.4% 2,213.8 56.5

NEO 1.4% 2,128.1 120.9

Ethereum Classic 1.0% 1,490.0 275.7 Source: coinmarketcap.com, updated: 23.08.2017

Measured by the global market capitalisation, the bitcoin is the most widespread virtual currency, followed by Ethereum. The following three differences of the bitcoin compared to the common bank money system are the reason for rise of the currency:

The bitcoin volume is technically limited to 21m and therefore cannot be expanded unlike established currencies. Like gold, the respective physical limitation of the volume is an argument for an effective inflation hedge due to an investment in bitcoins.

As there is no exchange of personal data between sender and receiver of bitcoins, the bitcoin transaction is considered as largely anonymous.

No intermediary in the form of a bank needed for bitcoin transactions. Furthermore, there is no state regulation for the bitcoin so far.

Despite the advantages of the bitcoin and the steadily growing trading volume the amount of transactions undertaken in this currency is still comparatively low. At present, some 300k transactions are carried out per day on the basis of the bitcoin network worldwide, whereas some 25m remittances are carried out per day in Germany alone according to the German Federal Bank. Established electronic payment processes such as Mastercard or Visa even perform up to 2,000 transactions per second. The number of simultaneous bitcoin transactions, in turn, is currently still hindered by technical restrictions.

Montega AG – Equity Research 12

Market and competition BITCOIN GROUP SE

Even though some well-known companies (e.g. Microsoft, Dell, Expedia, Lieferando) have accepted bitcoins as a means of payment, the acceptance network is still very small at least when it comes to everyday needs. That said, it becomes apparent that the use in everyday life is increasing. Online payment systems specialised in bitcoins (e.g. BitPay) are already existing and the established electronic payment systems are increasingly integrating bitcoin as a means of payment. In Austria, bitcoins are even offered for sale in the c. 1,700 branches of Austrian Post and the number of bitcoin ATM has doubled to over 1,300 units in the last years.

In addition to its function as a means of payment, the bitcoin, like gold, can also serve as a store of value. Despite very volatile prices, the bitcoin thus is an investment alternative for long-term oriented investors. The price development of the bitcoin since 2011 is shown in the table below.

Source: ariva.de

A decision in an investment in bitcoins is heavily influenced by the central banks’ unconventional measures such as negative interest rates and large-scale bond purchases, all of which resulted in a massive expansion of the central banks’ volume of money. These measures are perceived as a risky experiment in monetary policy and increase the demand for alternatives to the existing currencies. In combination with the limited supply of 21m bitcoins this leads to rising prices, because a limited amount is faced by a theoretically rising and strong demand unlike the central bank money. However, this scenario only comes into full effect when there is no variety of digital currencies that are similar to the bitcoin. Going forward it will be decisive how many how many cryptocurrencies can reach a critical mass and thus will be a direct competitor to the bitcoin. We assume that a maximum of five to ten digital currencies will establish on the market in the long term. This still uncertain development is not direct risk to the trading platform of Bitcoin Deutschland AG, as other cryptocurrencies alongside the bitcoin may be admitted to trading in the future as well.

It is not yet possible to draw a conclusion whether this is a sustainable trend or a short-term hype due to relatively short history of the cryptocurrencies. However, the development of the user numbers of the Bitcoin.de trading platform below illustrates that there is a tremendous public interest in cryptocurrencies. We expect the current strong user growth to advance further because of the great media attention.

0

500

1.000

1.500

2.000

2.500

3.000

3.500

4.000

August-11 October-12 December-13 February-15 April-16 June-17

Development of the bitcoin price in euro

Montega AG – Equity Research 13

Market and competition BITCOIN GROUP SE

Source: Company, Montega

Internationally fragmented competitive situation

Alongside Bitcoin.de there are currently more than 100 further trading platforms worldwide of various sizes and with different focuses. There is a technical difference between marketplaces and exchanges. Marketplaces de are manually processing purchases and sales, whereas the transactions at an exchange are processed automatically. The Bitcoin.de platform managed by Bitcoin Deutschland AG falls under the category of a marketplace, as the users themselves have to search for and accept a suitable purchase or sales offer. The table below shows the most important competitors offering exchanges between EUR/BTC, ranked by the bitcoin trading volume of the last 30 days.

Source: Bitcoincharts.com, updated: 23.08.2017

Bitcoin.de currently is the only platform trading the bitcoin cryptocurrency in its domestic market Germany and therefore enjoys a monopoly-like position. This strong position in the DACH region is underlined by the strong growth in new customers. However, there is no clear-cut division between the borders in the internet and users can access foreign platforms without any problems. Both the fee structure and security aspects should be a decisive factor for a user’s decision. Even though the fee structures of the competitors above are rather similar Bitcoin.de is at the upper end of the price range in a direct comparison. However, users are likely to increasingly put emphasis on a platform’s security aspects and reputation as well.

The establishment of cryptocurrencies as an asset class may also make a market entry for renowned online banks attractive in the medium to long term. They would be a serious competitor because of their comprehensive customer base and large resources. On the

281 k 300 k

319 k 337 k

356 k

393 k

430 k

460 k 480 k

0

50.000

100.000

150.000

200.000

250.000

300.000

350.000

400.000

450.000

500.000

Dec-15 Mar-16 June-16 Sep-16 Dec-16 Mar-17 June-17 Sep-17 Dec-17

Development of the Bitcoin.de customer base

Competitor

(Headquarters)

Trading volumen of the

last 30 days (in BTC)

Kraken (USA)

zyado (Portugal)

CoinsBank (Scottland)

GDAX (USA)

Bitcoin.de (Germany)

The Rock Trading (Malta)

CEX.IO (UK)

LocalBitcoins (Finland)

Paymium (France)

- Fees: 0.59% + additional fees depending on payment method

BitBay (Polen)

1,956.8- First european exchange which fulfilled european regulations (money ist not secured)

369.1- Supports various payment methods (like SEPA, credit card, express payment via DotPay)

- Fees: 0.25 to 0.43%

4,112.0- First cloud-based supplier with more than 700,000 user globally

- Fees: 0.1 to 0.2%

2,650.5- Marketplace-model with acceptance of almost every payment method

- Fees: 0.0 to 1.0%

27,636.1- Marketplace-model with express trading option and 2-factor authentification

- Fees: 0.3 to 0.5%

4,804.3- One of the oldest transaction systems with various cryptocurrencies

- Fees: 0.02 to 0.20%

60,649.0- Provides also a debit card

- Fees: 0.5%

52,438.6- Margin-trading possible

- Fees: 0.10 to 0.25%

Characteristic

358,773.6- Trade between bitcoins and EUR, USD, CAD, GBP and JPY possible

- Fees: 0.10 to 0.26%

71,113.0- Marketplace-model analogous Bitcoin.de with 2-factor authentification

- Fees: 0.10 to 0.25%

CAGR: 31%

Montega AG – Equity Research 14

Market and competition BITCOIN GROUP SE

other hand, their entry would be an opportunity for Bitcoin.de to acquire further cooperation partners, to admit other cryptocurrencies to trading or to establish an exchange alongside the marketplace model. This may be lead to further market share gains for the Bitcoin.de platform. We believe the company will focus on creating the regulatory requirements for the setup of an exchange trading in cryptocurrencies in the short to medium term. A connection to other banks via an existing gateway may also be possible with only moderate expenses in our view.

Finally, we regard the Bitcoin Group as a possible target for investors specialised in the respective business models, because of the rapid developments in the market environment.

Versatility of the blockchain technology enables portfolio expansion

From a technological perspective, the bitcoin is built on the blockchain technology, which is considered as extremely efficient and secure and which can also be adapted to other fields of application. At present, however, the blockchain technology is primarily used for bitcoins. That said, more than 40 banks are currently working on a technical standard for blockchains in a consortium and numerous fintechs are trying to put the blockchain technology to use in financial transactions. Simply put, the basic idea of blockchain is a decentral encryption and identification technology that creates a registry (e.g. for monetary units, equities, and property rights) in which all transactions are stored in chronological order and are jointly managed by a multitude of computer systems. In theory, the blockchain technology can do much more than simply managing monetary units, since it is capable of clearly identifying and assessing the item on which the business is based. The promising prospects of the blockchain technology are underlined by growing investments in blockchain business models. Global venture capital investments in bitcoin and blockchain technologies have increased by some 23% from 2015 to 2016 and are likely to remain high. Consequently, there is a multitude of interesting investment opportunities for the Bitcoin Group which, however, are set to entail significant investments.

Source: KPMG

Regulatory state interventions are unpredictable

Cryptocurrencies raise numerous new regulatory and (tax-related) legal questions, which need to be addressed on a supranational scale. As with other innovations in the financial sectors, however, the timing of the intervention must be carefully considered. Interventional measures that are too late can have as many negative consequences as a regulation that comes too early or is too strong and will possibly stall the innovation process. We believe there is general support from market participants for blockchain, the underlying technology behind bitcoins, whereas a parallel (virtual) currency systems is currently not in the central banks’ interest. Overall, regulatory interventions are difficult to predict though, and are a risk that should not be underestimated.

136.4

497.9

441.0

543.6

0

100

200

300

400

500

600

2013 2014 2015 2016

Worldwide VC investments in bitcoin and blockchain technology (in USD m)

Montega AG – Equity Research 15

Competitive quality BITCOIN GROUP SE

COMPETITIVE QUALITY

As an investment company in the market environment of cryptocurrencies and blockchain technologies that we regard as very promising Bitcoin Group SE has a high competitive quality. This quality is secured by the following factors in our view:

Leading market position in the DACH region

Strong organic acquisition of new customers

Sophisticated security concept

Highly scalable business model

Platform with high liquidity

Leading market position in the DACH region

Bitcoin Deutschland AG has operated a trading place for bitcoins under the Bitcoin.de domain already since 2011. Thanks to its monopoly-like position in Germany, the Bitcoin.de trading platform has reached a critical mass at an early market stage. Munich-based Fidor Bank has significantly contributed to this by offering central functions, especially express trading, as part of the cooperation as a provider of payment transactions since 2013. At the same time, Bitcoin Deutschland AG has acted as a tied agent of Fidor Bank. This means that the company operates in a scope approved by the Federal Financial Supervisory Authority and is the only company in Germany that is active as a regulated provider in this industry.

Unlike other platforms (e.g. insolvency of MtGox), there has been no theft by hackers or any serious system breakdown to date. User therefore enjoy a high degree of security which we believe is important especially in view of the still relatively short history of the cryptocurrency. Additional security is provided by the fact that both the servers of Bitcoin Deutschland AG and the company’s headquarters are located in Germany. Furthermore, Bitcoin Deutschland AG has voluntarily decided to have an auditor control in the context of a balance confirmation that the customers’ bitcoin portfolio is available and securely stored. With the Bitcoin.de trading platform, the Bitcoin Group has a monopolistic market position as a first mover in the German-speaking area which is supported by various security features.

Strong organic acquisition of new customers

Driven by an extremely strong organic growth in new customers, the Bitcoin.de trading platform has reached its leading market position and the respective critical mass. Last year, the average customer growth per month amounted to some 6k new customers. At mid-year, the platform can already boast more than 430k users. Thanks to the great media attention that cryptocurrencies are enjoying right now the Bitcoin.de trading platform can generate this user growth without any costly marketing activities (advertising costs in 2016: EUR 3,000). This is supported by the bitcoinblog.de blog that is operated in cooperation with affiliated companies (major shareholder Priority AG) and by the coinforum.de forum dealing with the topic of cryptocurrencies. One reason is the broad online reach of the blog’s articles and the forum’s discussions and explanations on cryptocurrencies and blockchain technologies. Accordingly, the conversion rate for a registration on the Bitcoin.de trading platform should be high. The dynamic user trend is also driven by a leading positioning in the organic search results of search engines. Bitcoin.de always ranks among the first three entries and often takes first place regarding the most common search terms on the topic of bitcoin trading. Finally, the intuitive domain (Bitcoin.de) also contributes to maintaining the high level of the organic user generation.

Sophisticated security concept

To gain the users’ trust and maintain the strong organic generation of new customers the company has implemented a complex security concept. The users always log in with their user name and password. However, to avoid malpractice and fraud a two-factor

Montega AG – Equity Research 16

Competitive quality BITCOIN GROUP SE

authentication is needed for the login. The user can choose between mail-login TAN, YubiKey, Google Authenticator or password table. At the end, the transaction is again confirmed by way of mobile TAN. In addition to the security measure during the login and trading processes, Bitcoin.de differs from other portals in that the customers keep their money for transactions on their own deposit-insured accounts instead of the portal operator’s account. Consequently, losses in case of the operator’s insolvency can be ruled out. As another security measure, Bitcoin.de stores c. 98% of the customers’ bitcoin portfolio offline in the so-called cold wallet. Thanks to the physical separation from the internet on e.g. separate data media or in the form of printouts the risk of theft caused by hacker attacks is minimised. Only the remaining c. 2% are regularly made available on servers located in Germany for the customers’ pay-out requests (in the so-called hot wallet). The euro and bitcoin portfolio of Bitcoin Deutschland AG exceeds these 2% many times over so that a loss can always be compensated for. This strongly minimises the reputational risk caused by theft or a hacker attack.

Highly scalable business model

The business model of Bitcoin Deutschland AG is highly scalable as a platform business. An incremental increase in revenue would only require very little additional expenses, e.g. to hire new employees. This is primarily reflected in an impressive revenue growth of 44% in 2016, while the headcount has remained almost flat (personnel costs +10.6%). The strong organic acquisition of new customers also results in a disproportionately rising revenue in relation to marketing expenses. When it comes to IT costs (additional servers amongst others) and the expansion of customer services, in turn, expenses are expected to slightly increase but at a proportionately lower rate than the revenue development in the next few years. Overall, the Bitcoin Group should have laid a good foundation to generate high operating margins. We see the highly scalable business model as a barrier to market entry that keeps competitors at a distance, at least until a critical mass is reached.

High liquidity thanks to large user base

The trading platform’s high liquidity is another barrier to market entry. Bitcoin.de has an impressive number of users by now, as a result of which the company processes a trading volume of some 28k bitcoins (average volume of the last 30 trading days). High liquidity, in turn, increases the number of new users, and vice versa. It may prove to be difficult for a potential new competitor to guarantee the liquidity necessary for smooth trading from the start, and they would have difficulties in establishing themselves.

Montega AG – Equity Research 17

Financials BITCOIN GROUP SE

FINANCIALS

Dynamic growth of customers and revenue in 2016

In FY 2016, with the Bitcoin Group’s with-time adoption of International Financial Reporting, revenue grew by 44.4% to EUR 1.13m (PY: EUR 0.78m). Strong growth was driven by higher trading volumes and an increase in users at Bitcoin Deutschland AG, the fully consolidated subsidiary. The number of customers rose by 78.9% to 356k on December 31, 2016. Consequently, the average revenue per user was slightly up when assuming an even growth of customers. This very positive trend was mainly driven by the bitcoin price increase by some 130%, which also reflects the great interest in cryptocurrencies.

Conversely, EBIT declined from EUR -63k to EUR -112k. This was mainly driven by much higher other operating expenses, namely the change in the company’s own bitcoin portfolio by almost EUR 300k, which therefore is not related to operating expenses. Personnel expenses, on the other hand, saw a moderate increase of 10.6% to EUR 465k accompanied by a rise in headcount from 7 to 8. Material expenses and D&A remained largely flat. Overall, the main expense items reflected the high scalability of the Bitcoin.de platform’s business model.

The financial result was clearly positive with EUR 320k thanks to realised profits in the company’s own bitcoin portfolio based on price increases. Consequently, net income amounted to EUR 114k (EUR 0.02 per share) after slightly negative earnings (EUR -16k) in the previous year.

Improved earnings and continued strong customer growth anticipated

The Bitcoin Group’s guidance for the current year is based on the development of Bitcoin Deutschland AG. In view of the good development and the favourable environment, the 2017 guidance has been raised at mid-year. The company anticipates net income to grow significantly after it had initially expected to achieve moderate earnings growth. The preliminary key figures on the business development in H1 underline the increased outlook. Revenue rose by 128.3% to EUR 1.77m (PY: EUR 0.78m), while pre-tax earnings grew disproportionately by 240.2% to EUR 1.22m (PY: EUR 0.36m).

Bitcoin Group SE - H1 2017 H1/2017p H1/2016 yoy

Sales 1.8 0.8 128.3%

EBT 1.2 0.4 240.2%

EBT margin 68.9% 46.3% Source: Company Figures in EUR m

Different effects are to provide for further dynamic revenue growth. For instance, it is planned to launch trading of cryptocurrency Ethereum in Q3, which is expected to generate additional sales potential of 10%-20% p.a. Furthermore, the company aims to grow customers to more than 450k (356k on December 31, 2016) by year end. Further increases in revenue are to result from better utilisation of the potential inherent in the existing customer base by improving the usability and customer experience of the trading platform. We believe a great deal of public awareness in the topic of cryptocurrencies and the sharp increase in bitcoin prices have accelerated customer acquisition during the year. Additionally, the high volatility of the bitcoin prices towards the middle of the year is likely to have a positive impact on trading volume and, therefore, on full-year revenue. The bitcoin price development also led to a significant appreciation of the company’s own portfolio (MONe: + c. EUR 3m on June 30), which has substantially increased the financial position.

We assume that a disproportionately low increase in expenses due to the trading platform’s high scalability will contribute significantly to achieving the earnings outlook. Strong user growth should be possible without any major expansion of customer services. In this area, the company aims for another automation to seize the viable economies of scale.

Montega AG – Equity Research 18

Financials BITCOIN GROUP SE

Future plans involve building an investment portfolio

The company plans to acquire shares in companies with business models in the field of cryptocurrencies and blockchain to build an investment portfolio. This will presumably require raising funds. Bitcoin Group considers a capital increase an option as well. We expect the company to acquire shareholdings in companies which have already delivered proof of concept and where it is apparent that profitability can be achieved. On the one hand, building an investment portfolio would contribute to a stronger diversification of the activitie. On the other hand, this would also lead to transaction-related expenses and risks from investments in a market that is still very young.

Balance sheet

The balance sheet total has been expanded from EUR 5.8m in the last fiscal year to EUR 6.8m. Growth on the assets side is mainly reflected by an increase in financial assets available for sale, representing the company’s own bitcoin portfolio. The portfolio growth to EUR 2.0m at year end (PY: EUR 1,2m) is due to both appreciation of the bitcoin and inflow of bitcoins. Thanks to the strong price increase of the bitcoin over the last few months the portfolio is expected to have significantly grown to over EUR 5m in H1.

Goodwill of EUR 3.9m, which only includes the goodwill of Bitcoin Deutschland AG, is the largest asset in the Group’s balance sheet. Liquidity was comfortable at the balance sheet date with almost EUR 0.8m.

The liabilities side is dominated by equity. The equity amounted to some EUR 6.1m at the reporting date, corresponding to 89.4% of the balance sheet total. The increase in 2016 equity by c. EUR 0.5m yoy was due to retained profit and, above all, to unrealised gains of the bitcoin. Unrealised gains of cryptocurrencies are recognised in equity without affecting profit and loss.

The balance sheet does not include interest-bearing debt capital. Overall, the very solid balance sheet reflects the group’s early development stage towards becoming an investment company.

Source: Company

Intangible assets 3.9

Equity 6.1

Available-for-sale securities 2.0

Deferred tax 0.4 Other assets 0.1

Othe liabilities 0.3 Cash 0.8

Assets Liabilities

Balance sheet structure (as at 31 Dec 2016; in EUR m)

Montega AG – Equity Research 19

Company Background BITCOIN GROUP SE

COMPANY BACKGROUND

Bitcoin Group SE is a holding company focused on innovative business models in the field of cryptocurrency and blockchain technology. The company holds 100% in Bitcoin Deutschland AG which presently is its only shareholding. Other participations are planned in the medium term and are reviewed on an ongoing basis.

In cooperation with Fidor Bank, Bitcoin Deutschland AG has operated the only authorised trading platform for cryptocurrency in Germany under the domain Bitcoin.de since 2011. Bitcoin.de is the world’s first trading platform with a direct gateway to the traditional banking system and the only one so far having its own and its customers’ bitcoin portfolio checked by an auditing firm on an annual basis.

Amongst others, Bitcoin Deutschland AG also plans to launch trading of cryptocurrency Ethereum in the current fiscal year. We also assume that the Bitcoin Group already considers its options to establish the first Bitcoin exchange in Germany.

Company history

2011 Bitcoin Deutschland GmbH is founded and trading platform Bitcoin.de goes live 2013 Bitcoin Deutschland GmbH becomes a public limited company, and cooperation

with Munich-based Fidor Bank has started

AE Innovative Capital SE (today’s Bitcoin Group SE) is listed at the Düsseldorf stock exchange

2015 Bitcoin Group SE is entered as legal successor of AE Innovative Capital SE and

acquires a 100% stake in Bitcoin Deutschland AG Bitcoin Group starts to use Fidor Bank gateway to accelerate handling of

payments (“express trading”) 2016 Start of trading on the open market of the Frankfurt stock exchange on Xetra and

the Frankfurt floor exchange 2017 Launch of trading in cryptocurrency Ethereum planned in Q3 In 2012, major shareholder Priority AG established BitPayment.de GmbH with its corresponding BitcoinBlog.de and CoinForum.de domains. BitPayment.de GmbH offers a service to verify bank accounts that can be used for logging into the Bitcoin.de trading platform as well as by third parties.

The BitcoinBlog.de domain operates a blog on the topic of virtual currencies that has more than 5k unique visitors per day. CoinForum.de is the only German language forum dealing with digital currencies. Potential customers are directly forwarded to the Bitcoin.de trading platform. This generates numerous customer contacts, even though the domains do not belong to the Bitcoin Group or Bitcoin Deutschland AG in economic terms but are owned by major shareholder Priority AG.

Montega AG – Equity Research 20

Company Background BITCOIN GROUP SE

Markets and revenue

Bitcoin Group generates its entire revenue from advisory and brokerage services related to bitcoin transactions. In FY 2016, revenue grew by 44.4% to EUR 1.13m (PY: EUR 0.78m) with 100% of revenue being generated in Germany, even though there is a consistently rising share of customer from Europe ex-Germany. The trading platform is currently available in German, English, French, Spanish, and Italian. The chart below shows the regional split of the customer base.

Source: Company

Products

The Bitcoin.de trading platform allows users to trade bitcoins within a marketplace model. Unlike a stock exchange’s automated trading system, this marketplace model is based on a manual purchase or sale, where every user itself is looking for a suitable offer to buy or sell. The transaction is then processed through SEPA Direct Debit or an accelerated payment process in cooperation with Fidor Bank (“express trading”). Depending on the form of payment, trading fees are between 0.3% and 0.5%. In this way, some 28k bitcoins (c. EUR 83m) were traded in the last 30 days.

To avoid malpractice and fraud a modern two-factor authentication is used. All servers are located in Germany and have enough capacities to cover increases in trading volume. Unlike other platforms (e.g. insolvency of MtGox), there has been no theft by hackers or any serious system breakdown to date. As such, the trading platform enjoys high reputation which is also reflected in significant customer growth. Since 2015, the number of user has substantially increased by an average of 33% p.a. to some 430k by at mid-year.

Bitcoin Group SE

Bitcoin Deutschland AG(100%)

BitPayment.de GmbH

BitcoinBlog.de

CoinForum.de

major shareholding cooperation with associated companies (Priority AG)

Transaction System Bitcoin.de

Source: Company

Montega AG – Equity Research 21

Company Background BITCOIN GROUP SE

The chart below shows the user surface of the Bitcoin.de platform:

Source: Company

Experienced management

Michael Nowak has been managing director of Bitcoin Group SE since June 2016. Before this, Mr. Nowak has gained significant experience in the financial sector from working at several banks and insurance companies (e.g. Dresdner Bank, Commerzbank, and Allianz). He has joined the Bitcoin Group in 2013, where he initially assumed the function of director of Bitcoin Deutschland GmbH. In 2014, he became a member of the management board of Bitcoin Deutschland AG.

Oliver Flaskämper is a co-founder and the largest shareholder of the Bitcoin Group and its predecessors, and a current member of Bitcoin Deutschland AG. He currently holds c. 90% of the shares in Bitcoin Group SE via his holding company Priority AG. He is also a member of various boards of directors and supervisory boards of companies, some of which are publicly traded. Prior to joining Bitcoin Deutschland AG, Mr. Flaskämper was a serial entrepreneur and business angel and has established online enterprises geizkragen.de, nettolohn.de, adbutler.de, and content.de amongst others.

Montega AG – Equity Research 22

Company Background BITCOIN GROUP SE

Shareholder structure

Bitcoin Group SE’s share capital is divided in 5,000,000 no-par shares. Priority AG is the major shareholder with 77.2% of the voting rights. The remaining 22.8% of the shares are free float as per August 2017.

Source: Company

Priority AG 77.2%

Free float 22.8%

Shareholder structure

Montega AG – Equity Research 23

Appendix BITCOIN GROUP SE

APPENDIX

P&L (in EUR thsd.) Bitcoin Group SE 2015 2016

Sales 780.0 1,126.3

Increase / decrease in inventory 0.0 0.0

Own work capitalised 0.0 0.0

Total sales 780.0 1,126.3

Material Expenses 127.8 130.5

Gross profit 652.1 995.8

Personnel expenses 420.8 465.4

Other operating expenses 290.5 639.6

Other operating income 12.6 14.1

EBITDA -46.6 -95.1

Depreciation on fixed assets 16.9 16.8

EBITA -63.4 -112.0

Amortisation of intangible assets 0.0 0.0

Impairment charges and Amortisation of goodwill 0.0 0.0

EBIT -63.4 -112.0

Financial result 43.3 319.8

Result from ordinary operations -20.1 207.8

Extraordinary result 0.0 0.0

EBT -20.1 207.8

Taxes -4.0 93.7

Net Profit of continued operations -16.1 114.2

Net Profit of discontinued operations 0.0 0.0

Net profit before minorities -16.1 114.2

Minority interests 0.0 0.0

Net profit -16.1 114.2

Source: Company (reported results), Montega (forecast)

P&L (in % of Sales) Bitcoin Group SE 2015 2016

Sales 100.0% 100.0%

Increase / decrease in inventory 0.0% 0.0%

Own work capitalised 0.0% 0.0%

Total sales 100.0% 100.0%

Material Expenses 16.4% 11.6%

Gross profit 83.6% 88.4%

Personnel expenses 54.0% 41.3%

Other operating expenses 37.2% 56.8%

Other operating income 1.6% 1.2%

EBITDA -6.0% -8.4%

Depreciation on fixed assets 2.2% 1.5%

EBITA -8.1% -9.9%

Amortisation of intangible assets 0.0% 0.0%

Impairment charges and Amortisation of goodwill 0.0% 0.0%

EBIT -8.1% -9.9%

Financial result 5.6% 28.4%

Result from ordinary operations -2.6% 18.5%

Extraordinary result 0.0% 0.0%

EBT -2.6% 18.5%

Taxes -0.5% 8.3%

Net Profit of continued operations -2.1% 10.1%

Net Profit of discontinued operations 0.0% 0.0%

Net profit before minorities -2.1% 10.1%

Minority interests 0.0% 0.0%

Net profit -2.1% 10.1%

Source: Company (reported results), Montega (forecast)

Montega AG – Equity Research 24

Appendix BITCOIN GROUP SE

Balance sheet (in EUR thsd.) Bitcoin Group SE 2015 2016

ASSETS

Intangible assets 3,884.0 3,883.9

Property, plant & equipment 36.5 23.0

Financial assets 0.0 0.0

Fixed assets 3,920.6 3,906.9

Inventories 0.0 0.0

Accounts receivable 189.9 14.8

Liquid assets 1,693.9 2,812.4

Other assets 24.4 65.9

Current assets 1,908.2 2,893.1

Total assets 5,828.8 6,800.0

LIABILITIES AND SHAREHOLDERS' EQUITY

Shareholders' equity 5,453.4 6,083.1

Minority Interest 0.0 0.0

Provisions 16.5 85.4

Financial liabilities 5.2 36.9

Accounts payable 18.7 26.1

Other liabilities 335.0 568.6

Liabilities 375.4 717.0

Total liabilities and shareholders' equity 5,828.8 6,800.0

Source: Company (reported results), Montega (forecast)

Balance sheet (in %) Bitcoin Group SE 2015 2016

ASSETS

Intangible assets 66.6% 57.1%

Property, plant & equipment 0.6% 0.3%

Financial assets 0.0% 0.0%

Fixed assets 67.3% 57.5%

Inventories 0.0% 0.0%

Accounts receivable 3.3% 0.2%

Liquid assets 29.1% 41.4%

Other assets 0.4% 1.0%

Current assets 32.7% 42.5%

Total Assets 100.0% 100.0%

LIABILITIES AND SHAREHOLDERS' EQUITY

Shareholders' equity 93.6% 89.5%

Minority Interest 0.0% 0.0%

Provisions 0.3% 1.3%

Financial liabilities 0.1% 0.5%

Accounts payable 0.3% 0.4%

Other liabilities 5.7% 8.4%

Total Liabilities 6.4% 10.5%

Total Liabilites and Shareholders' Equity 100.0% 100.0%

Source: Company (reported results), Montega (forecast)

Montega AG – Equity Research 25

Appendix BITCOIN GROUP SE

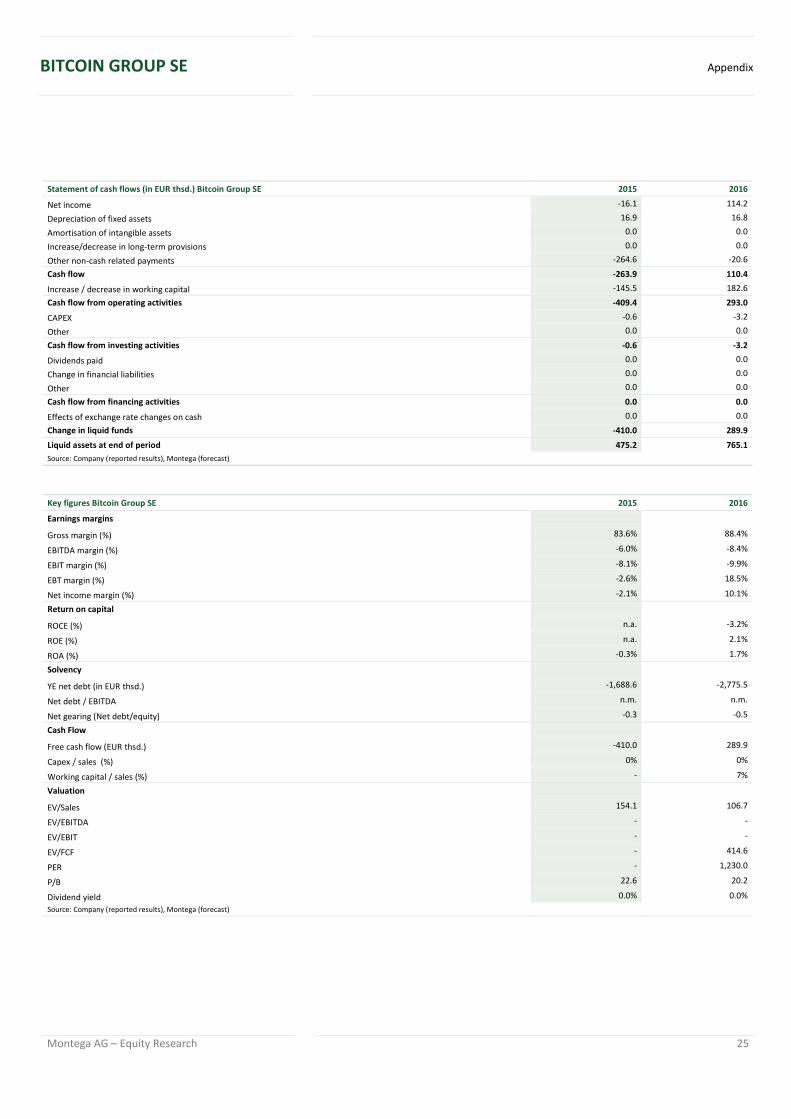

Statement of cash flows (in EUR thsd.) Bitcoin Group SE 2015 2016

Net income -16.1 114.2

Depreciation of fixed assets 16.9 16.8

Amortisation of intangible assets 0.0 0.0

Increase/decrease in long-term provisions 0.0 0.0

Other non-cash related payments -264.6 -20.6

Cash flow -263.9 110.4

Increase / decrease in working capital -145.5 182.6

Cash flow from operating activities -409.4 293.0

CAPEX -0.6 -3.2

Other 0.0 0.0

Cash flow from investing activities -0.6 -3.2

Dividends paid 0.0 0.0

Change in financial liabilities 0.0 0.0

Other 0.0 0.0

Cash flow from financing activities 0.0 0.0

Effects of exchange rate changes on cash 0.0 0.0

Change in liquid funds -410.0 289.9

Liquid assets at end of period 475.2 765.1

Source: Company (reported results), Montega (forecast)

Key figures Bitcoin Group SE 2015 2016

Earnings margins

Gross margin (%) 83.6% 88.4%

EBITDA margin (%) -6.0% -8.4%

EBIT margin (%) -8.1% -9.9%

EBT margin (%) -2.6% 18.5%

Net income margin (%) -2.1% 10.1%

Return on capital

ROCE (%) n.a. -3.2%

ROE (%) n.a. 2.1%

ROA (%) -0.3% 1.7%

Solvency

YE net debt (in EUR thsd.) -1,688.6 -2,775.5

Net debt / EBITDA n.m. n.m.

Net gearing (Net debt/equity) -0.3 -0.5

Cash Flow

Free cash flow (EUR thsd.) -410.0 289.9

Capex / sales (%) 0% 0%

Working capital / sales (%) - 7%

Valuation

EV/Sales 154.1 106.7

EV/EBITDA - -

EV/EBIT - -

EV/FCF - 414.6

PER - 1,230.0

P/B 22.6 20.2

Dividend yield 0.0% 0.0%

Source: Company (reported results), Montega (forecast)

Montega AG – Equity Research 26

Disclaimer BITCOIN GROUP SE

DISCLAIMER

This document does not represent any offer or invitation to buy or sell any kind of securities or financial instruments. The document serves for information purposes only. This document only contains a non-binding opinion on the investment instruments concerned and non-binding judgments on market conditions at the time of publication. Due to its content, which serves for general information purposes only, this document may not replace personal, investor- or issue-specific advice and does also not provide basic information required for an investment decision that are formulated and expressed in other sources, especially in properly authorised prospectuses. All data, statements and conclusions drawn in this document are based on sources believed to be reliable but we do not guarantee their correctness or their completeness. The expressed statements reflect the personal judgement of the author at a certain point in time. These judgements may be changed at any time and without prior announcement. No liability for direct and indirect damages is assumed by either the analyst or the institution employing the analyst. This confidential report is made available to a limited audience only. This publication and its contents may only be disseminated or distributed to third parties following the prior consent of Montega. All capital market rules and regulations governing the compilation, content, and distribution of research in force in the different national legal systems apply and are to be complied with by both suppliers and recipients. Distribution within the United Kingdom: this document is allotted exclusively to persons who are authorized or appointed in the sense of the Financial Services Act of 1986 or on any valid resolution on the basis of this act. Recipients also include persons described in para 11(3) of the Financial Act 1986 (Investments Advertisements) (Exemptions) Order 1996 (in each currently valid amendment). It is not intended to remit information directly or indirectly to any other groups or recipients. It is not allowed to transmit, distribute, or to make this document or a copy thereof available to persons within the United States of America, Canada, and Japan or to their overseas territories. Declaration according to Section 34b WpHG and FinAnV on possible conflicts of interest (as per 9 August 2017): Montega AG has made an agreement with this company about the preparation of a financial analysis. The research report has been made available to the company prior to its publication / dissemination. Thereafter, only factual changes have been made to the report. A company affiliated with Montega AG may hold an interest in the issuer's share capital. Prices of financial instruments mentioned in this analysis are closing prices of the publishing date (respectively the previous day) if not explicitly mentioned otherwise. Declaration according to Section 34b WpHG and FinAnV on additional information (as per 9 August 2017): Any updating of this publication will be made in the case of events that Montega considers to be possibly relevant to the stocks’ price performance. The end of regular comments on events in context with the issuer (coverage) will be announced beforehand. Fundamental basics and principles of the evaluative judgements contained in this document: Assessments and valuations leading to ratings and judgements given by Montega AG are generally based on acknowledged and broadly approved methods of analysis i.e. a DCF model, a peer group comparison, or sum-of-the-parts model. Our ratings: Buy: The analysts at Montega AG believe the share price will rise during the next twelve months. Hold: Upside/downside potential limited. No immediate catalyst visible. Sell: The analysts at Montega AG believe the share price will fall during the next twelve months. Authority responsible for supervision: Bundesanstalt für Finanzdienstleistungsaufsicht Graurheindorfer Str. 108 und Marie-Curie-Str. 24-28 53117 Bonn 60439 Frankfurt Contact Montega AG: Schauenburgerstraße 10 20095 Hamburg www.montega.de Tel: +49 40 4 1111 37 80