bitcoin, blockchain and the future of payments€¦ · 1 l leilani doyle svp product management...

TRANSCRIPT

l 1

Leilani Doyle SVP Product Management

April 2016

Bitcoin, Blockchain and the Future of Payments

l 2

l 3

WHAT EXPERTS SAY “A world with different and new money will be a different and new world. We are headed there more rapidly than most suppose. The lives of citizens and central bankers alike will be profoundly altered... ”

—Lawrence H. Summers, President Emeritus of Harvard University, former Secretary of the United States Department of the Treasury 2012�

Source: Breaking Banks by Brett King and Amazon Review of The End of Money by David Wolman

l 4

AGENDA § Bitcoin Basics § Uses of the Blockchain § Future of Payments

l 5

§ A form of electronic currency

§ Social in nature and no one controls it

§ Bitcoins are “mined” by solving increasingly complex mathematical problems

§ Transfers can be made without a third party

What is bitcoin?

https://bitcoin.org/en/bitcoin-paper

l 6

Key Players § Satoshi Nakamoto

• Could be Craig Steven Wright, Michael Clear, Martii Malmi, Jed McCaleb

§ Miners – mint bitcoins by solving increasingly complex mathematical equations

§ Blockchain – public ledger of all bitcoin transactions requiring distributed consensus

§ Addresses – bitcoins are transferred from address to address

§ Private Keys – sign individual transfers

l 7

Basic Diagram

l 8

Bitcoin Blockchain https://blockchain.info/

l 9

Bitcoin Valuations

Silk Road

MtGox

VC Investment

Greece

l 10

Current bitcoin price

As of May 12, 2016

http://www.coindesk.com/price/

l 11

Sample Bitcoin Checkout

l 12

§ No foreign exchange fees or complexity § Push payment by design – no cardholder

data § Connects payment

directly with the receivable/purchase

Benefits of Using Bitcoin

https://www.youtube.com/watch?v=BrRXP1tp6Kw

l 13 13

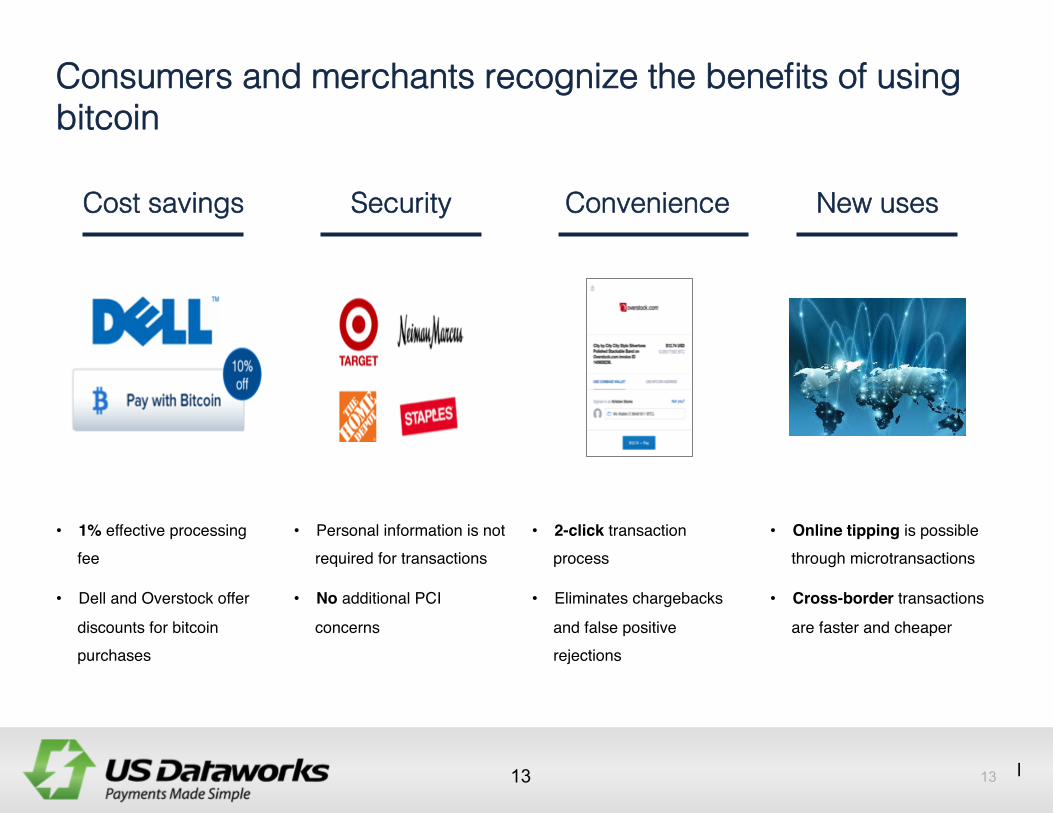

• 1% effective processing fee

• Dell and Overstock offer

discounts for bitcoin purchases

Consumers and merchants recognize the benefits of using bitcoin!

• Personal information is not required for transactions

• No additional PCI

concerns

• 2-click transaction process

• Eliminates chargebacks

and false positive rejections

• Online tipping is possible through microtransactions

• Cross-border transactions

are faster and cheaper

Cost savings! Security! Convenience! New uses!

l 14 14

How To Buy bitcoin

l 15

Blockchain uses

l 16

http://www.coindesk.com/deloitte-blockchain-ach-2025/

Blockchain News

http://www.finextra.com/news/fullstory.aspx?newsitemid=28356

http://www.coindesk.com/deloitte-blockchain-ach-2025/

l 17

• Public vs Private blockchains ( or distributed ledgers )

• Planning/testing phase • Cross border payments (Ripple Labs) • Securities trading (SEC approved plan, Japan

and IBM) • Real time payments • Nasdaq and Estonia eResidency for

stock voting

Proof of Concepts

l 18

Bank of America has filed 15 patents related to Blockchain use and has another 20 in the works

Blockchain Patents

THE FUTURE OF PAYMENTS

l 20

FUTURE OF PAYMENTS

• Greater Transparency• Faster• International• Data Rich• Accessible to all (Ubiquitous)• Less Expensive Transactions• More Opportunity for Value-Added Services• Lower Individual and Systemic Risk• More Secure

l 21

TCH is building an industrial strength clearing and settlement system to support Real-Time Payments for the US § The system is designed to ensure that payments are not only faster, but safer too, consistent

with the CFPB’s consumer protection principles and the criteria set forth by the Federal Reserve Faster Payments Task Force

§ This system will allow consumers and businesses to send and receive payments instantly, directly from their accounts at financial institutions

§ This system will also support the sending and receiving of data and non-payment messages to support the development of innovative products and services by financial institutions

TCH’s Real-Time Payments system will be available to all US financial institutions § All US financial institutions will have access to TCH real-time payments § TCH’s goal is to achieve ubiquity rapidly; we are working with partner organizations to achieve

that goal

TCH Real-time Payments architecture is modular for adaptability to changing needs The system’s modular architecture allows TCH and participating FIs to leverage best-of-breed technology for routing directories, anti-fraud, AML, network connectivity, security, settlement and value-added services

The Clearing House’s Real-Time Payments Initiative

21 TCH CONFIDENTIAL

https://www.theclearinghouse.org/payments/real-time-payments

l 22

§ Confirmation of Payment – Immediate notification of successful transfer to end users, providing certainty for both senders and receivers

§ No Returns – receivers have certainty of good funds

§ Request for Payment – delivered through the payment system to support receivables products such as e-invoicing and e-billing, while reducing remittance errors

§ Fulfillment Messaging – Ability to provide confirmation by the receiver that they have received funds, combined with fulfillment information (e.g. “invoice paid” or “goods shipped, tracking info http//UPS.COM/293jdxG55228ww”)

§ Complete Payables/Receivables Messaging – Ability to link multiple messages associated with the same transactions (e.g. request for payment, confirmation, separate remittance) through a common reference

§ Consistent User Experience – robust rules that establish requirements for availability of funds, timeliness of notification, delivery of non-payment messages (request for payment, receiver confirmation, separate remittance) and other elements that support independent development of value-added products by banks

§ Global Ready – ISO 20022 is a global standard that immediately simplifies processes for multi-national banks and companies, and will support cross-border payments in the near future

Real-time payments provide particular value for business payment applications

22

TCH Confidential

l 23

§ Faster Payments Services (FPS) offers 24/7 real-time credit transfers to virtually any UK account. FPS is the most mature national real-time payment network, launched in 2008 and now processing 1 billion transactions per year.

§ Legacy Payments and real-time payments co-exist – after 7 years, FPS has grown to ~20% of BACS (conventional ACH) volume

§ Usage is driven by more than just low-value P2P transfers – average transaction value is £821 and nearly half of FPS transactions are scheduled or deferred payments to or from businesses

§ Real-time payments require enhanced online banking security – The UK saw a significant rise in retail online banking fraud following the introduction of FPS

Lessons learned from UK Faster Payments Service

23 TCH CONFIDENTIAL

£845.48

£294.43

£1,809.79

Single Immediate Payments

Standing Orders Future Dated/Bulk

UK Faster Payments Service 2014 Average Value

Single Immediate Payments

56%

Standing Orders

30%

Future Dated/Bulk

14%

UK Faster Payments Service 2014 Payments Volumes

FPS Avg. £820.94

l 24

THANK YOU