birla sun life.doc

TRANSCRIPT

Acknowledgement

I express my sincere thanks to my project guide, Mr. MAHENDRA

DAIYA, Designation DPTY. HOD , Deptt. MBA, for guiding me right

from the inception till the successful completion of the project. I

sincerely acknowledge him for extending their valuable guidance,

support for literature, critical reviews of project and the report and above

all the moral support he/she/they had provided to me with all stages of

this project.

ANKIT BISSA

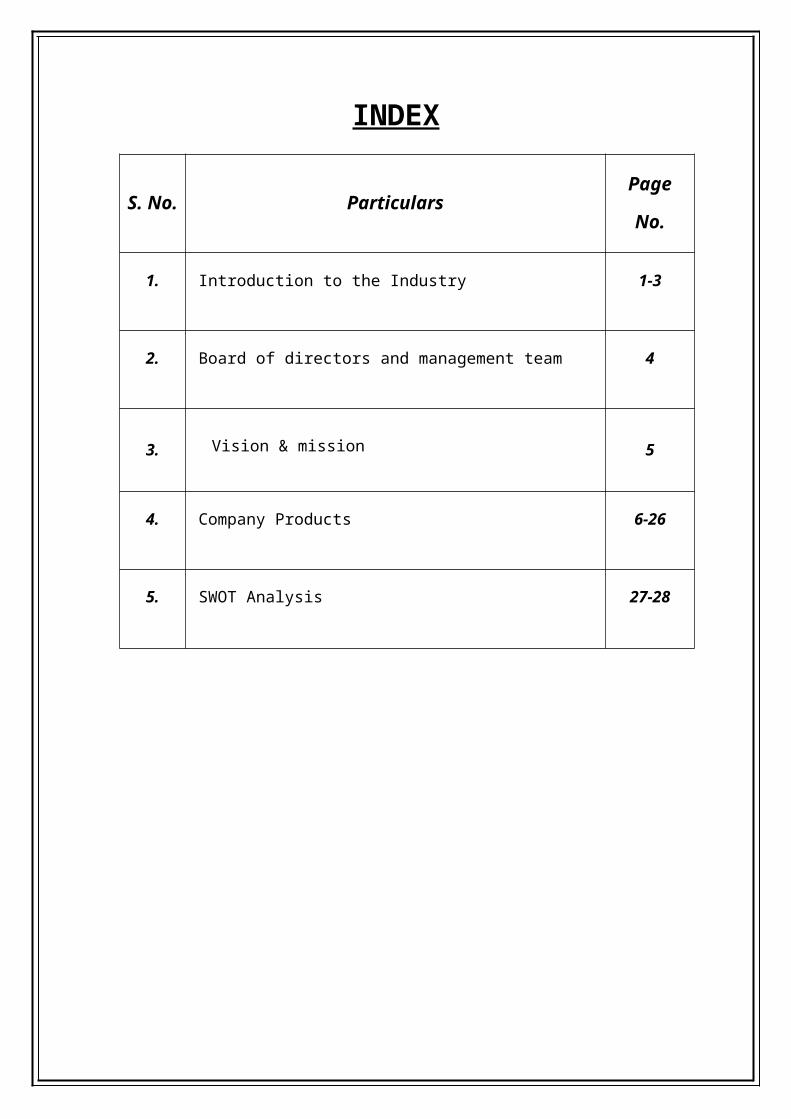

INDEX

S. No. Particulars Page No.

1. Introduction to the Industry 1-3

2. Board of directors and management team 4

3. Vision & mission 5

4. Company Products 6-26

5. SWOT Analysis 27-28

INTRODUCTION TO COMPANY

Birla Sun Life Insurance Company Limited (BSLI) is a joint venture Between the

Aditya Birla Group and Sun Life Financial Inc., a leading International financial

services organization. The local knowledge of the Aditya Birla Group combined with

the expertise of Sun Life Financial Inc.,offers a formidable value proposition to

customers.

Sun Life Financial and its partners today have operations in key markets worldwide,

including India, Canada, the United States, the United Kingdom, Hong Kong,

Philippines, Japan, Indonesia, China and Bermuda. Sun Life Financial Inc. had assets

under management of over US$ 386.82 billion, as on 31 March 2007. Sun Life

Financial Inc. is a leading performer in the life insurance market in Canada.

BSLI in its five successful years of operations has contributed significantly to the

growth and development of the life insurance industry in India. It pioneered the

launch of Unit Linked Life Insurance plans amongst the private players in India. It

was the first player in the industry to sell its policies through the Bank assurance route

and through the internet. It was also the first private sector player to introduce a pure

term plan in the Indian market. This was supported by sales practices, which brought

a degree of transparency that was entirely new to the market. The process of getting

sales illustrations signed by customers, offering a free look period on all policies,

which are now industry standards were introduced by BSLI.

Being a customer centric company, BSLI has invested heavily in technology to build

world class processing capabilities. BSLI has covered more than one and a half

million lives since inception and its customer base is spread across 100 cities in India.

All this has assisted the company in cementing its place amongst the leaders in the

industry in terms of new business premium income.

Birla Sun Life Insurance (BSLI), one of the leading private life Insurers in India today

announced the inimitable achiever, cricketer Kapil Dev as their corporate brand

ambassador. The cricketing supreme will be endorsing BSLI in all its marketing

initiatives. Birla Sun Life Insurance is a value-driven brand which has a national

brand recall of 70 per cent. The objective of appointing a brand ambassador is to grow

its brand recall as it goes national in its distribution reach and fuel business growth.

As a brand ambassador, Kapil Dev will play a key role in the brand and product

marketing and promotional activities. BSLI has always used an integrated Marketing

approach, which will be strengthened further? Commenting on the association with

Kapil Dev, Mr. S. K. Mitra, Director, Financial Services, Aditya Birla Group and

currently in charge of BSLI expressed, "The Birla Sun Life Insurance business

distribution network is national in nature covering more than 1000 points across the

country .We have made our entry in several tier I and tier II towns. It is therefore very

important for the brand to connect at the grassroots level and create trust. We believe

that our association with Kapil Dev as our brand ambassador will help us create this

connects in a shorter period of time. We therefore now have two strong connects —

our parent brand Birla and our brand Ambassador Kapil Dev". Kapil Dev, also known

as the Haryana Hurricane, was born on 6 January 1959 in Chandigarh. He played his

first competitive game of cricket at the

Age of 13 years and made his test debut on 16 October 1978 at Faisalabad against

Pakistan. Kapil Dev remained India's top strike bowler for almost 15 years. His

extraordinary test match figures of more than 5000 runs and 434 wickets along with

64 catches show that he was a world class cricketer and an all-rounder. He has raised

the mantle of India to sporting glory by winning us the World Cup.

In a study conducted by BSLI, Kapil Dev connected extremely well with the life

insurance category and had high acceptance by the masses. Our survey suggests that

he is seen as a very good fit for the BSLI brand. He is very much loved and respected

by a vast majority of the population.

On 26 November 2006, Birla Sun Life was host the annual golf tournament at the

Chembur Golf Club in Mumbai where Kapil Dev was participates.

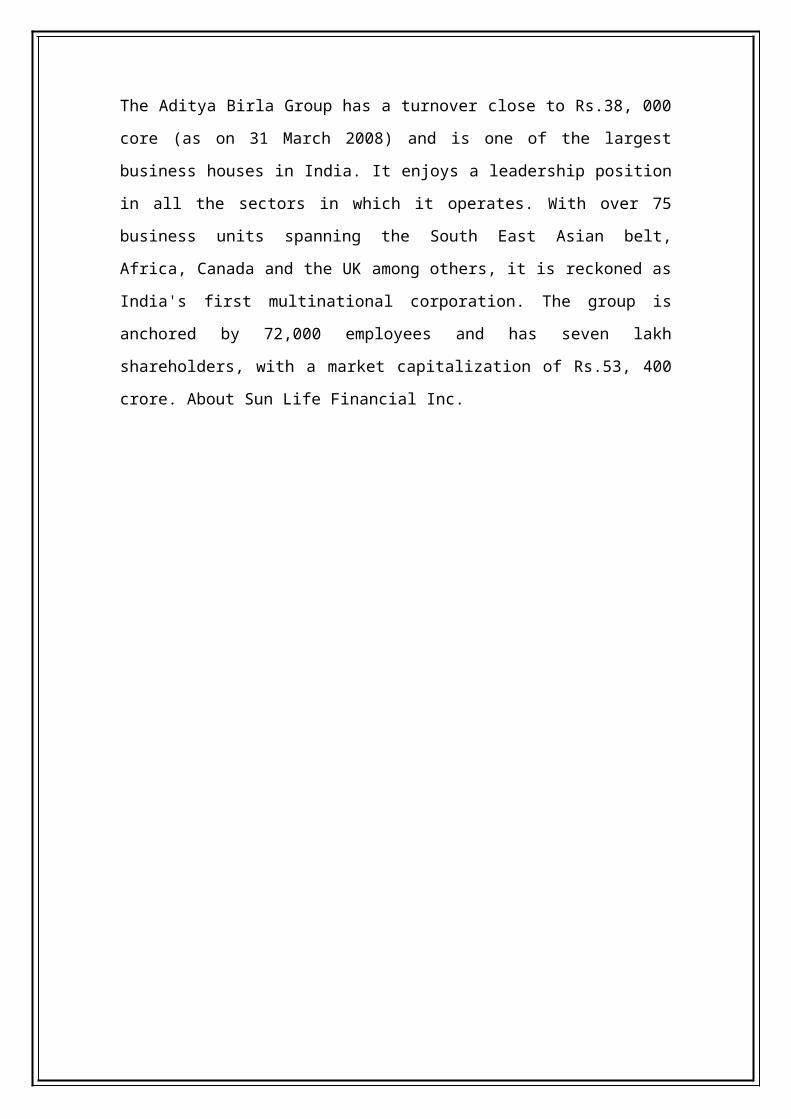

About the Aditya Birla Group

The Aditya Birla Group has a turnover close to Rs.38, 000 core (as on 31 March

2008) and is one of the largest business houses in India. It enjoys a leadership position

in all the sectors in which it operates. With over 75 business units spanning the South

East Asian belt, Africa, Canada and the UK among others, it is reckoned as India's

first multinational corporation. The group is anchored by 72,000 employees and has

seven lakh shareholders, with a market capitalization of Rs.53, 400 crore. About Sun

Life Financial Inc.

Sun Life Financial Inc. is a leading international financial service Organization

providing a diverse range of wealth accumulation and Protection products and

services to individuals and corporate customers.

Tracing its roots back to 1865, Sun Life Financial and its partners today have

operations in key markets worldwide, including Canada, the United States, the United

Kingdom, Hong Kong, the Philippines, Japan, Indonesia, India, China and Bermuda.

As of 31 March 2008, the Sun Life Financial group of companies had total assets

under management of US$ 343 billion.

Sun Life Financial Inc. trades on the Toronto (TSX), New York (NYSE) and

Philippine (PSE) stock exchanges under ticker symbol "SLF".

BOARD OF DIRECTORS

Mr. Kumar Mangalam Birla

Mr. Jayant Dua

Mr. Kevin Strain

Dr. Rakesh Jain

Mrs. Tarjani Vakil

Mr. Ajay Shrinivasan

Mr. Bishwanath Puramalka

Mr. Gian Gupta

Mr. Suresh Talwar

Mr. Venkatesh Mysore

MANAGEMENT TEAM

Mr. Mayanka Bathwal (Deputy Chief Executive officer)

Mr. Sashi Krishnan (Chief Investment Officer)

Mr. Arun Malkani (Chief Marketing Officer)

Mr.Pramod Krishnamurthy (Head – Information Technology)

Mr. Saurov Ghosh (Head – Human Resources & Training)

Mr. Lalit Vermani (Head – Compliance, Risk, Legal & Audit)

Mr. Vikas Seth (Chief Distribution Officer (CDO))

Mr. Anil Singh (Chief Actuarial Officer)

Mr. Amitabh Verma (Chief Operating Office)

VISION & MISSION

VISION:-

To be a world class provider of financial security to individuals and corporates and to

be amongst the top three private sector life insurance companies in India

MISSION:-

To be the first preference of our customers by providing innovative, need based life

insurance and retirement solutions to individuals as well as corporates. These

solutions will be made available by well-trained professionals through a multi channel

distribution network and superior technology.

Our endeavour will be to provide constant value addition to customers throughout

their relationship with us, within the regulatory framework. We will provide career

development opportunities to our employees and the highest possible returns to our

shareholders

PRODUCTS

All the plans associated with BSLI are Unit Linked Plans.

FLEXI PLANS

Flexi Plans have three variants. These variants are:

1. Flexi Save Plus (Endowment Plan)

2. Flexi Cash Flow (Money Back Plan)

3. Flexi Lifeline (Whole of Life Plan)

Features:

This is a Unit Linked Plan with guaranteed returns.

Provides flexibility with Top-Up Facility.

For Quarterly modal premium less than Rs.5000, payment can be made

through ECS.

Policyholder can attach riders to the plan according to his/her needs.

Liquidity in the form of Partial withdrawals.

Three Investment Fund options are available with the policy and policyholder

is free to switch between funds anytime during the tenure of the policy.

The Sum Assured may be increased once in every 5 policy years, starting from

the 6th policy year.

Premium can be paid annually, semi-annually, quarterly and monthly

Premium Invested: Collected Premium is invested in three Investment Fund

Options. These funds are:

1. Protector

2. Builder

3. Enhancer

Benefits:

1. Maturity Benefits : At maturity, Policyholder gets the higher of the guaranteed

fund value (min. 3% on premium) or the Total Fund value.

2. Survival Benefits :

(i) At the end of every 5th Coverage Benefit Period and the remainder on

maturity, an amount equals to the minimum of (a) or (b) mentioned below

will be reduced from the guaranteed fund value and transferred to the

holding account for the purpose of partial withdrawals, where-

(a) Guaranteed Fund Value

(b) Sum Assured % as stated below:

30% if the Coverage Benefit Period is 10 years.

25% if the Coverage Benefit Period is 15 years.

20% if the Coverage Benefit Period is 20 years.

15% if the Coverage Benefit Period is 25 years.

If survival benefits are not withdrawn, they will continue to be a part of the

Fund Value.

(ii) If the life insured is a minor, policyholder can withdraw the

survival benefit payout within one month from the scheduled

payout date from the fund value.

3. Death Benefits :

Age at time of

DeathDeath Benefits

30 days to 1 year Fund Value Only

Age 1 Year to 60

Year

Higher of Sum Assured less all partial withdrawals made in

24 months preceeding the death of life insured or the fund

value or the guaranteed fund value.

On or After

attainment of 60

Years

Higher of Sum Assured less all partial withdrawals made

since the life insured attained the age 58 or the fund value or

the guaranteed fund value.

Charges:

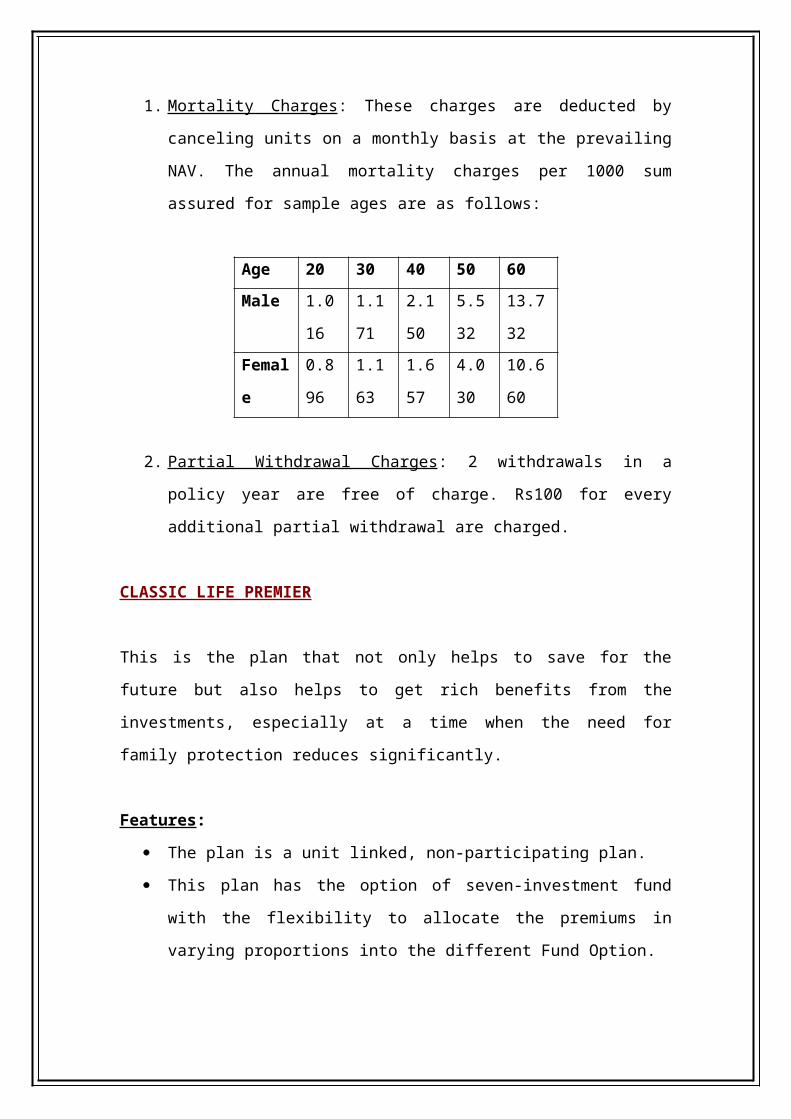

1. Mortality Charges : These charges are deducted by canceling units on a

monthly basis at the prevailing NAV. The annual mortality charges per 1000

sum assured for sample ages are as follows:

Age 20 30 40 50 60

Male 1.016 1.171 2.150 5.532 13.732

Female 0.896 1.163 1.657 4.030 10.660

2. Partial Withdrawal Charges : 2 withdrawals in a policy year are free of charge.

Rs100 for every additional partial withdrawal are charged.

CLASSIC LIFE PREMIER

This is the plan that not only helps to save for the future but also helps to get rich

benefits from the investments, especially at a time when the need for family

protection reduces significantly.

Features:

The plan is a unit linked, non-participating plan.

This plan has the option of seven-investment fund with the flexibility to

allocate the premiums in varying proportions into the different Fund Option.

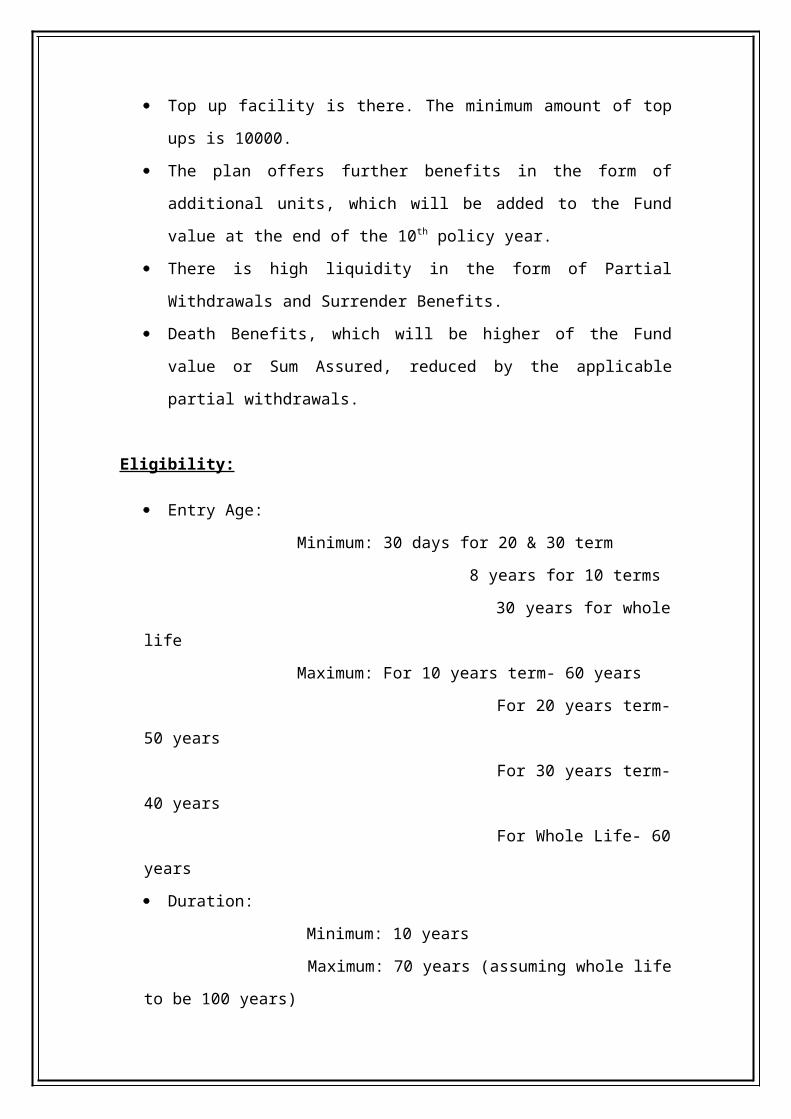

Top up facility is there. The minimum amount of top ups is 10000.

The plan offers further benefits in the form of additional units, which will be

added to the Fund value at the end of the 10th policy year.

There is high liquidity in the form of Partial Withdrawals and Surrender

Benefits.

Death Benefits, which will be higher of the Fund value or Sum Assured,

reduced by the applicable partial withdrawals.

Eligibility:

Entry Age:

Minimum: 30 days for 20 & 30 term

8 years for 10 terms

30 years for whole life

Maximum: For 10 years term- 60 years

For 20 years term- 50 years

For 30 years term- 40 years

For Whole Life- 60 years

Duration:

Minimum: 10 years

Maximum: 70 years (assuming whole life to be 100 years)

Maturity Age: 70 years for the term- 10,20,30 years

100 years for whole life

Premium Payment Term: For 10 years term- 3, 5yrs or regular coverage

paying period.

For 20 yrs, 30yrs term and Whole Life- 5yrs, 10 yrs

or regular coverage paying period.

Premium Investment: Premium collected is invested in Seven Investment Fund

Options:

1. Assure

2. Protector

3. Builder

4. Enhancer

5. Creator

6. Magnifier

7. Maximiser

Benefits:

1. Guaranteed Addition : It is in the form of additional units, which is added to

the fund value on the 10th policy anniversary and on every 5th policy

anniversary thereafter, while policy is in effect.

2. Partial Withdrawal Options : Partial Withdrawals can be made after 3 policy

years or when the life insured attains maturity, whichever is later. The

minimum partial withdrawal amount is Rs.10000

3. Surrender Benefits : Policy offers the flexibility of surrendering the policy, if

the need arises. There is no surrender charge after 6 completed policy years.

However, if the policy is surrendered within 3 years from inception, the surrender

value is paid after the completion of the third policy anniversary.

4. Death Benefits :

Below 5 years: If the death of the life insured take place before 5 years,

only the fund value shall be payable to the policy owner.

Between 5 to 60 years: Higher of the fund value or the sum assured

less all applicable partial withdrawals made in the last 24 months

preceding the death of the life insured.

60 years and Above: Higher of the fund value or the sum assured less

all applicable partial withdrawals made since the life insured attained

the age of 58.

5. Maturity Benefits : On maturity of the policy, the fund value is payable. Under

the whole life option, on maturity of the policy, when the life insured attains

the age of 100, then fund value is payable and the policy will be terminated.

6. Tax Benefits : Tax benefits on premium payment are governed by section 80C

of the Income Tax Act 1961. Tax Exemptions on the amount received on

maturity in the unfortunate event of death and the withdrawals are governed

by section 10(10D).

7. Addition of Riders : Policy holder can customize the plan by adding any of the

following 6 riders:

1. Accidental Death & Dismemberment Rider

2. Term Rider

3. Critical Illness Rider

4. Critical Illness Plus Rider

5. Critical Illness Women Rider

6. Waiver of Premium Rider

Charges:

1. Premium Allocation Charges : These charges during the premium paying term

are as under:

Policy Year 1 2 or 3 Thereafter

Charge 13% 4% 2%

This charge on Top-up and underwriting extra is 2%.

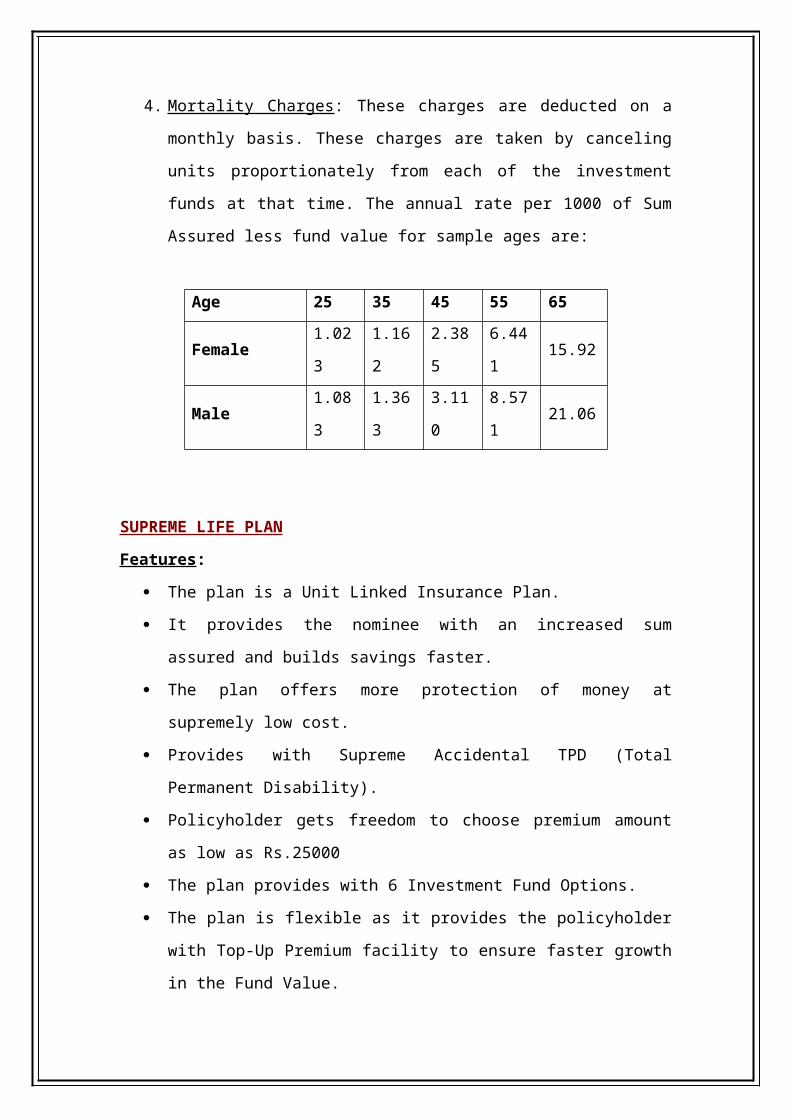

2. Mortality Charge : This charge will be deducted by cancellation of units on a

monthly basis at the prevailing NAV. The Annual Mortality charge per 1000

of the Sum at risk for sample ages are as follows:

3. Fund

Management Charge: This is charged by adjustment of the daily NAVs. The

charge is:

1% p.a. for Assure, Protector, Builder and Enhancer Fund.

1.25% p.a. for Creator, Magnifier and Maximiser Fund.

4. Policy administration Charge : The charge is deducted by canceling units on a

monthly basis at the prevailing NAV. The annual charge differs according to

the Life Insurance Coverage Sum Assured and Life Insurance Coverage

Paying Period. The maximum charge is 6.10 and the minimum charge is 0.00

5. Surrender Charge : These charges are levied as the percentage of the annual

life insurance coverage Premium payable. Charges are as follows:

Policy Year 1 2 3 4 5 6 7+

Surrender

Charge30% 20% 15% 10% 8% 6% NIL

6. Rider Premium Charge : If the riders are attached, this charge will be realized

by cancellation of units on a monthly basis based on the equivalent monthly

rider coverage premium payable, when rider coverage payment period equals

the rider coverage benefit period.

GOLD PLUS II PLAN

The plan gives much more than a good insurance cover, an opportunity to grow

investment for the medium term. It is worth more than Gold.

Features:

Age 25 35 45 55 65

Female 1.023 1.162 2.385 6.441 15.92

Male 1.083 1.363 3.110 8.571 21.06

It is a Unit Linked, Non-Participating, Insurance plan.

Duration of plan is 8 years.

Premium paying term of 3 years with the flexibility to reduce premium up to

Rs. 10000 from the second policy year.

Plan also has Top-up facility.

Liquidity in the form of Partial Withdrawals and Surrender Benefits.

Free unlimited fund switching and premium redirection

Eligibility:

Entry Age: 18 to 70 years.

Minimum Premium: Rs.50000

Minimum sum Assured: 5 x Annual Premium

Premium Investment: Premium collected is allocated in varying proportions in

seven investment fund options. Policyholder can switch between the fund options

anytime during the tenure of the policy. The seven Investment Funds available are:

1. Assure

2. Protector

3. Builder

4. Enhancer

5. Creator

6. Magnifier

7. Maximiser

Benefits:

1. Maturity Benefits :

On maturity fund value will be paid to the policyholder.

2. Death Benefits :

This procedure can be stepped down as follows:

1. Pitching the customer: The first and foremost thing is that, client should be ready

to purchase the Insurance plan. Insurance is not a very preferable product yet in India.

And,

thus, co. has to be very vigilant. Advisors, at BSLI, maintain relationships and make

the most of their Goodwill. Insurance is a Relationship oriented business. Keeping

this in mind BSLI also initiated Bancassurance, where Banks’ image of being loyal to

the customers, plays a major role in pitching the customer to buy Insurance. BSLI

uses following routes for distributing their Product to general public:

a. Direct Personal Contacts (through Advisors)

b. Bancassurance (through Banks)

c. Personal Relations (through co. employees)

d. Existing Policyholders.

2. Sales Illustration: BSLI is the first company to give demonstration of the fund

performance i.e. how a certain policy will perform or will give returns. BSLI Advisors

give sales illustration. Fund performance is shown on 6% and 10% projections. If

client find these projected returns suitable to his/her risk profile, he go for purchasing

the policy.

3. Proposal Form : Now as client is ready to get insured, advisor gives him the

proposal form and asks for all the documents required. Proposal form is a 4

page document that contains all the necessary information related to the

Insured and the Owner of the policy. Documents required along with the

proposal form are:

Date-Of-Birth Proof

Address & ID Proof

Income Certificate

Medical Certificates (only if Insurer is a senior citizen)

1. After Sales Service : Now after the Insurance is sold, follow-ups are required.

Advisor needs to maintain good relations with the policyholder. Insurance co.

can

Generate further business, only if, existing policyholders are satisfied with the

services being provided by the advisor of the co. Thus, BSLI keeps this in mind

and Business Development Executives continuously track the needs of the

policyholders. BSLI provides the policyholders with monthly updates of the fund

performance and

also discloses the asset portfolio of the fund. This assists the policyholders to

manage their policy according to their risk profile. They can, thus, change their

fund allocation as well as the asset allocation in any fund, chosen by them.

In the Unfortunate

event of the Death of the Life Insured prior to the maturity date of the policy,

the nominee gets the greater of

(a) Fund Value

(b) Sum Assured reduced for partial withdrawal as follows:

Before the life insured attains the age of 60, the sum assured

payable on death is reduced by partial withdrawals made in

the preceeding years.

Once the Life Insured attains the age of 60, the Sum Assured

payable on death is reduced by all partial withdrawals made

from age 58 onwards.

3. Tax Benefits :

Policyholder is eligible for tax benefits U/S 80C and U/S 10(10D) of the

Income Tax Act 1961.

U/S 80C- Premium up to Rs.100000 is allowed as deduction from

taxable income each year.

U/S 10(10D) - The Benefits received under plan are exempted from

tax.

Charges:

1. Premium Allocation Charges:

It is deducted from premium when received and before allocation of units.

2. Fund

Management Charges:

Fund Management charge not exceeding 1.5% per annum of the fund value

will be charged by adjustments of the daily unit price. The charge is

1% p.a.- Assure, Protector, Builder and Enhancer

1.25% p.a. – Creator, Magnifier and Maximiser

3. Policy Administration Charges :

These charges are recovered by canceling units on a monthly basis

proportionately from each investment fund. The annual Rate per 1000 of Sum

Assured is:

Policy

Charges

Policy Years

1 2 3 4+

Policy

Administration

Charge *

19.4 19.4 19.4 14.4

* An additional 5 per 1000 will be charged in the first 3 policy years only on

any excess Sum Assured over Rs. 50000

4. Mortality Charges : These charges are deducted on a monthly basis. These

charges are taken by canceling units proportionately from each of the

investment funds at that time. The annual rate per 1000 of Sum Assured less

fund value for sample ages are:

Age 25 35 45 55 65

Female 1.023 1.162 2.385 6.441 15.92

Policy

Charges

Policy Years

1 2 3 4+

On Policy

Premium 8% 4% 4%

On top-up

Premium 2% 2% 2% 2%

Male 1.083 1.363 3.110 8.571 21.06

SUPREME LIFE PLAN

Features:

The plan is a Unit Linked Insurance Plan.

It provides the nominee with an increased sum assured and builds savings

faster.

The plan offers more protection of money at supremely low cost.

Provides with Supreme Accidental TPD (Total Permanent Disability).

Policyholder gets freedom to choose premium amount as low as Rs.25000

The plan provides with 6 Investment Fund Options.

The plan is flexible as it provides the policyholder with Top-Up Premium

facility to ensure faster growth in the Fund Value.

Partial Withdrawals, are allowed, after 3 years to meet liquidity needs of the

policyholder

Duration:

Policy Term : 10, 15, 20, 25, 30, 35, 40 Years.

Premium Payment Term : Policyholder can choose to pay premium at short or

regular intervals.

Premium Investment: Premium Collected is investment in six investment fund

options. These funds are:

1. Assure

2. Protector

3. Builder

4. Enhancer

5. Creator

6. Magnifier

Benefits:

1. Death Benefits :

Double Death Benefits i.e. Death Benefits= Sum Assured + Savings

Increasing Death benefits i.e. Death Benefit= Sum Assured + 25% every

5th year

2. Accidental TPD Benefit :

Policyholder immediately gets the original sum assured up to Rs.50 lac

Co. pays the future premiums up to age 60.

3. Switches & Redirection :

Policyholder gets flexibility to switch between the fund options. Two

switches are free per annum.

Charges:

1. Mortality Charges : Charges are deducted monthly by canceling units from the

associated fund option. The charge is 95%

2. Policy Administration Charges : These charges are deducted monthly by

canceling units from the investment fund. The annual charge is Rs. 720 on the

first 1000 Sum Assured in all years i.e. Rs.3.60 per 1000 Sum Assured p.a.

The additional charges for years 1-5 are as follows:

Term Band 1 Band 2 Band 3

10/15 4.75 4.25 4.00

20+ 3.75 3.25 3.00

3. Premium Allocation Charges : These charges are 5% for the 1st policy year and

2% for subsequent policy years.

4. Fund Management Charges : These charges are 1 – 1.25% p.a. for all

associated funds.

PLATINUM PLUS PLAN

Features:

This plan is a Unit Linked, Non-Participating, Insurance plan.

A policy term of 10 years.

A premium paying term of 3 years.

One Innovative Investment fund, namely Platinum Plus Fund I.

Full Liquidity after three policy years to meet any cash needs.

Unique Guaranteed Maturity Unit Price representing the highest unit plus

price of Platinum Plus Fund I recorded on 88 reset dates starting on March 17,

2008 and ending on June 15, 2015.

Eligibility:

Entry Age of Life Insured: 18 to 70 Years.

Minimum Annual Premium: Rs. 1,00,000

Minimum Sum Assured: 5xAnnual Premium.

Premium Collected is invested in the Equity & Debt Market according to the

preset Asset Allocation of the Platinum Plus Fund I.

Benefits:

1. Guaranteed Maturity Unit Price

Minimum of Rs. 10 on the first Reset Date

At maturity, is the highest Unit Price recorded on 88 Reset Dates

2. Maturity Benefits

Number of units multiplied by higher of Guaranteed Maturity Unit Price or

prevailing Unit Price at maturity

3. Surrender Benefits

Full liquidity after 3 policy years –100% Fund Value*

4. Death Benefits

Higher of Fund Value (as per the then prevailing unit price) or Sum Assured

(less applicable partial withdrawals)

5. Tax Benefits

U/S 80C- Premium up to Rs.100000 is allowed as deduction from taxable

income each year.

U/S 10(10D) - Benefits from the plan are exempted from tax.

Charges:

1. Premium Allocation Charges : 10% of premium in the first year and 4% of

premium in subsequent years.

2. Fund Management Charges : 1.00%-1.50% p.a. for Assure & 1.50%-2.00%

p.a. for Platinum Plus Fund I.

3. Policy Administration Charges : These charges are deducted monthly by

canceling units from the investment fund Assure first and then, from Platinum

Plus I, if required. The annual charge is Rs. 720 on the first 1000 Sum Assured

in all years plus Rs.6 per 1000 Sum Assured in years 1 to 3 only.

4. Mortality Charges : Charges are deducted monthly by canceling units from the

associated investment funds. The Annual Charges for sample ages are as

follows:

Attained

Age25 35 45 55 65

Female 1.023 1.162 2.385 6.441 15.920

Male 1.083 1.363 3.110 8.571 21.060

5. Surrender Charges : This charge, as a percentage of the annual premium at

issue, is 16%, 13% and 10% for policy year 1, 2 and 3 respectively.

6. Revival Charge : The charge for policy revival is Rs. 100-1000 per revival

FUNDS BY BSLI

Birla Sun Life Insurance, a leading Life Insurance company, offers its clients with a

long range of Funds. These funds are designed to cater to a variety of needs of people

who are from different life stages. BSLI offers a broad range of 12 funds, each having

differing asset allocations.

12 funds offered are:

1. Individual Protector

2. Individual Assure

3. Individual Balancer

4. Individual Builder

5. Individual Creator

6. Individual Enhancer

7. Individual Life Maximiser

8. Individual Magnifier

9. Individual Multiplier

10. Pension Nourish

11. Pension Enrich

12. Pension Growth

A new fund named Platinum Plus Fund I is also added in this list of funds.

Asset Allocation is decided by the Fund Managers of the company. These fund

managers continuously tracks the movements of volatile market and combine this

volatility with the fund requirements of the policyholders. Accordingly he decides

allocation of assets in 5 major investment options:

Government Securities

Corporate Debt

Securitized Debt

Equity

Money Market Instruments

Proportion of allocating the fund in these options, vary according to the needs and

fund requirements of policyholders. The most important thing to be noticed here is

that this portfolio is decided, based on the regulations of IRDA. Performances of these

funds are rated by the rating agency-CRISIL.

All the 12 funds by BSLI are described below along with their respective Asset

Allocations.

Individual Assure

Objective: The primary objective of this fund is to provide Capital Protection, at a

high level of safety and liquidity through judicious investments in high quality short-

term debt.

Strategy: Generate better return with low level of risk through investment into fixed

interest securities having short-term maturity profile.

Asset Allocation:

SECURITIES HOLDING

Corporate Debt 59.57%

Money Market Instruments 17.97%

TOTAL 100.00%

Individual Balancer

Objective: The objective of this fund is to achieve value

creation of the policyholder at an average risk level over

medium to long-term period.

Strategy: The strategy is to invest predominantly in debt

securities with an additional exposure to equity,

maintaining medium term duration profile of the portfolio.

Asset Allocation:

SECURITIES HOLDINGS

Government Securities 10.67%

Corporate Debt 39.04%

Equity 23.44%

Money Market Instruments 26.85%

TOTAL 100.00%

HOLDINGS

10.67%

39.04%

23.44%

26.85%Government Securities

Corporate Debt

Equity

Money Market Instruments

Pension Growth

Objective: This fund option is designed to build the

capital and to generate better returns at moderate level of

risk, over a medium or long-term period through a balance

of investment in equity and debt.

Strategy: Generate better return with moderate level of

risk through active management of fixed income portfolio

and focus on creating long term equity portfolio which

will enhance yield of composite portfolio with low level of

risk appetite.

Asset Allocation:

SECURITIES HOLDINGS

Government Securities 13.90%

Corporate Debt 45.41%

Equity 18.63%

Money Market Instruments 22.06%

TOTAL 100.00%

HOLDINGS

13.90%

45.41%18.63%

22.06%

Government Securities

Corporate Debt

Equity

Money Market Instruments

SWOT ANALYSIS

STRENGTH:

Multi-channel distribution and one of the largest distribution networks in India.

Implementing Six-Sigma process.

Customer centric products and services.

Superior investment and risk management framework

1 Million Policies sold within 3 and half years.

Company has maximum number of MDRT as well as good number of HNI advisors.

Training process of the company is very strong.

Different plan for different peoples

According to the change in surrounding environment like changes in customer

requirement.

WEAKNESS:

COMPANY does not penetrate on the rural market at a time.

There is no plan for the low income group.

Fees for the advisor is high than the other company.

OPPORTUNITY:

Insurance market is very big, where company can expand its horizon in insurance

industry.

Though good investment and insurance it is easy to top Indian customers.

The huge insurance market (77%) is left so company has opportunity to expand our

products.

To associate with the more number of HNI.

THREATS:

‘OLD HABITS DIE HARD’: Its still difficult task to win the confidence of public

towards private company.

The company is facing major threats from LIC -which is an only government

company.

Plans for all income groups is not available which can create adverse effect later on

the market share of the company.