biomass technologies & trends

TRANSCRIPT

Biomass Technologies & Trends:

Challenges and Opportunities in a Changing Forest Sector

Presented to the69th Annual Meeting of Members

Maritime Lumber Bureau

by

Peter Milley, CMCPartner, Halifax Global Inc.

June 5th, 2008

Presentation Overview• Context – Changing Forest Sector

– Changing patterns of demand for key products– Changing relative values of currencies and energy

• Biomass Technologies – Some Initial Observations

• Biomass Technologies – Brief Review of Current State

• Opportunities for Forest Sector– Incremental Improvement Opportunities– Transformational Change Opportunities

• Future Directions -- Conclusions

Major Trends –Changing Demand / Supply Relationship

• Decline in North American demand for newsprint accelerating – year over year drop was almost 13% in January – decline may be slowing

– Supply continues to exceed demand– Significant excess supply in North America

• NA Newsprint prices improving in Europe and Asia, but still soft in North America– Recent high of USD 650 / tonne summer 2006 – currently about <USD 600± today

• New newsprint capacity in growing markets – notably Asia – Individual machines ≅ 440,000 tonnes / yr– Most Eastern North American machines in range of 150,000 – 200,000 tonnes / yr– Opportunity for NA mills to shift surplus product to those markets constrained

• Newest pulp mills – in South America -- >2 million tpy eucalyptus pulp– Smooth Rock Falls, ON – recently closed by Tembec – 150,000 – 200,000 tpy NBSK

Market Trends – Changing Demand

Represents Full Year Decline of

>500,000 tonnes -- >4.5 million

tonnes since 2000

Major Trends – Declining Home Starts

• New home construction down by > 20% over past two years– Demand for S-P-F lumber down by nearly 20% over two years– Average S-P-F price down by approximately 40% past two years

• Renovation spending has remained reasonably buoyant – But softening US economy likely to lead to declines

• Sub-prime mortgage ‘rate resets’ -- > 1.5 million in 2008– Another 500,000 in 2009– Significant percentage will result in foreclosures – April inventory of foreclosed

homes in US 660,000, up from 493,000 in January and 231,000 in January 2007

• Optimists look for lumber market recovery late 2009– Could easily be well into 2010 before recovery takes hold

• Derivative impacts – mill shut downs, reduced harvesting, lower residual product output

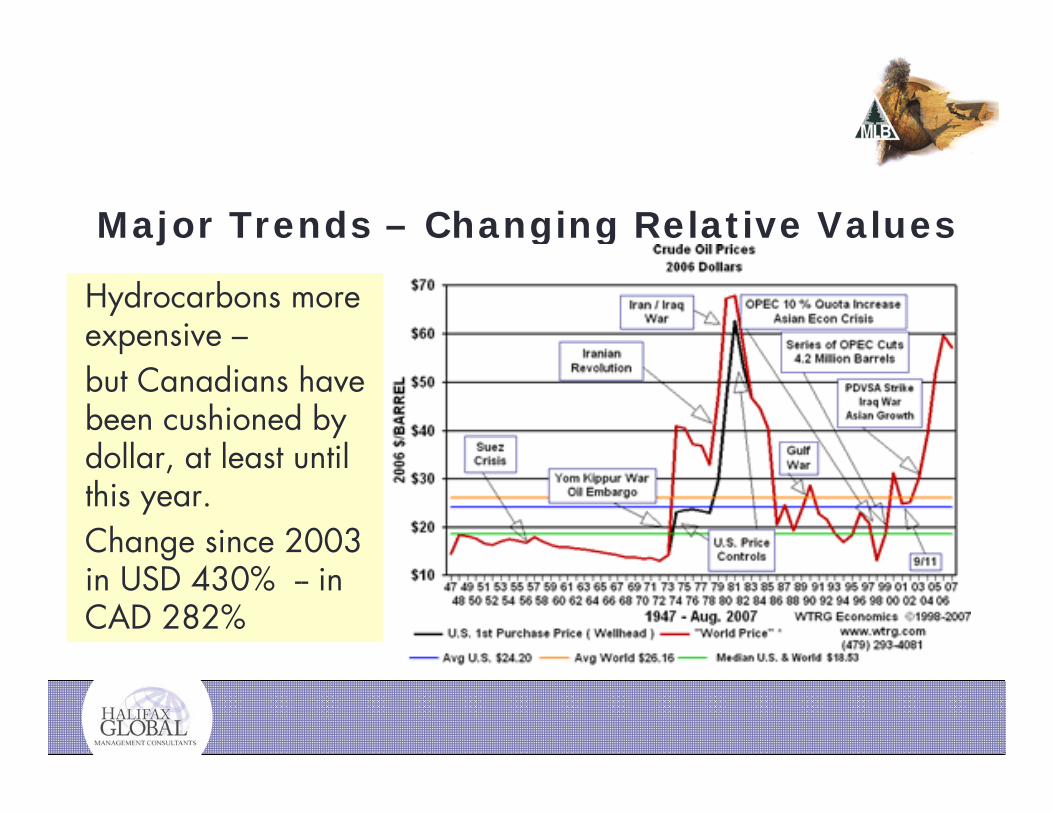

Major Trends – Changing Relative Values

• Currencies –

– CAD vs. USD – ≈ 60% increase from low in 2003• Revenue loss > $20 million for 100 million fbm sawmill

– Revenue loss of $150 million for typical 400,000 tpy newsprint mill• Result – mill / machine downtime / shutdowns

– Harvesting activities / residual flows disrupted– At least two major integrated companies may need bankruptcy

protection

– CAD vs. Other Currencies (eg. £ €) – about 10 – 15% increase • Manageable change for producers shipping to those markets

– However, very large focus / dependency on US market

Major Trends – Changing Relative Values

Hydrocarbons more expensive –but Canadians have been cushioned by dollar, at least until this year.Change since 2003 in USD 430% -- in CAD 282%

Major Trends – Changing Relative Values

Forest sector – all segments – undergoing fundamental, strategic change

Values historically determined by directly competitive products / raw materials

NOW / FUTURE – values driven by energy / chemical components as

substitutes for hydrocarbons

BIOMASS PROCESSING TECHNOLOGIESkey to unlocking that value

Biomass Technologies

• Five ‘main’ technologies –– Combustion– Gasification– Pyrolisis / Flash Pyrolisis– Anaerobic Digestion– Fermentation / Distillation

• Two ‘minor’ technologies –– Densification– Steam explosion

But First – Some Initial Observations

Very little of this is ‘new’ –

mankind has been using ‘biomass’ for energy and chemical / medicinal use

since the beginning of time

But First – Some Initial Observations

And some of what seems ‘new’ –

has actually been in use for much longer than we

generally realise

1920’s – 30’s Ford Truck converted to

tractor powered by a wood gasifier

But First – Some Initial Observations

Saab 99 powered by a wood gasifier, circa

mid-1970’s

But First – Some Initial Observations

With oil >USD $100 / barrel,

and likely to stay there, the relative economic value of biomass changes and becomes a viable substitute for hydrocarbon based fuels and

chemicals

28.2% projected increase in daily consumption over next 20 years

Biomass Technologies – Overview

• Five ‘main’ technologies –– Combustion– Gasification– Pyrolisis / Flash Pyrolisis– Anaerobic Digestion– Fermentation / Distillation

• Two ‘minor’ technologies –– Densification– Steam explosion

Biomass Technology – Combustion• Primarily

energy generation

• CHP / Co-gen

• Refractory lined / fluidised bed

• Scalable from small to large

• In commercial use

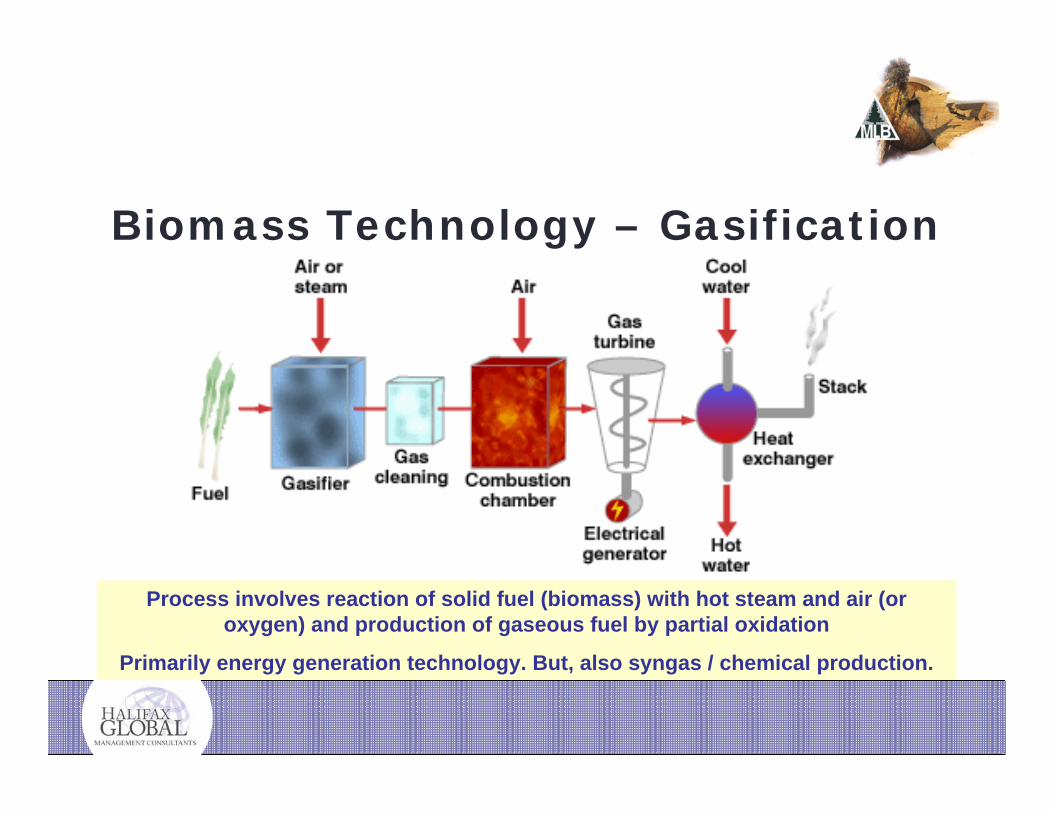

Biomass Technology – Gasification

Process involves reaction of solid fuel (biomass) with hot steam and air (or oxygen) and production of gaseous fuel by partial oxidation

Primarily energy generation technology. But, also syngas / chemical production.

Biomass Technology – PyrolysisProcess involves heating of biomass in near absence of air – newest technologies up

to 900° C – produces vapours / aerosols that

condense to bio-oil used for energy or chemical outputs.

Fuel value about half of conventional fuel oil.

Bio-oils also produced for food additive / pharma

applications.

Early stage commercial.

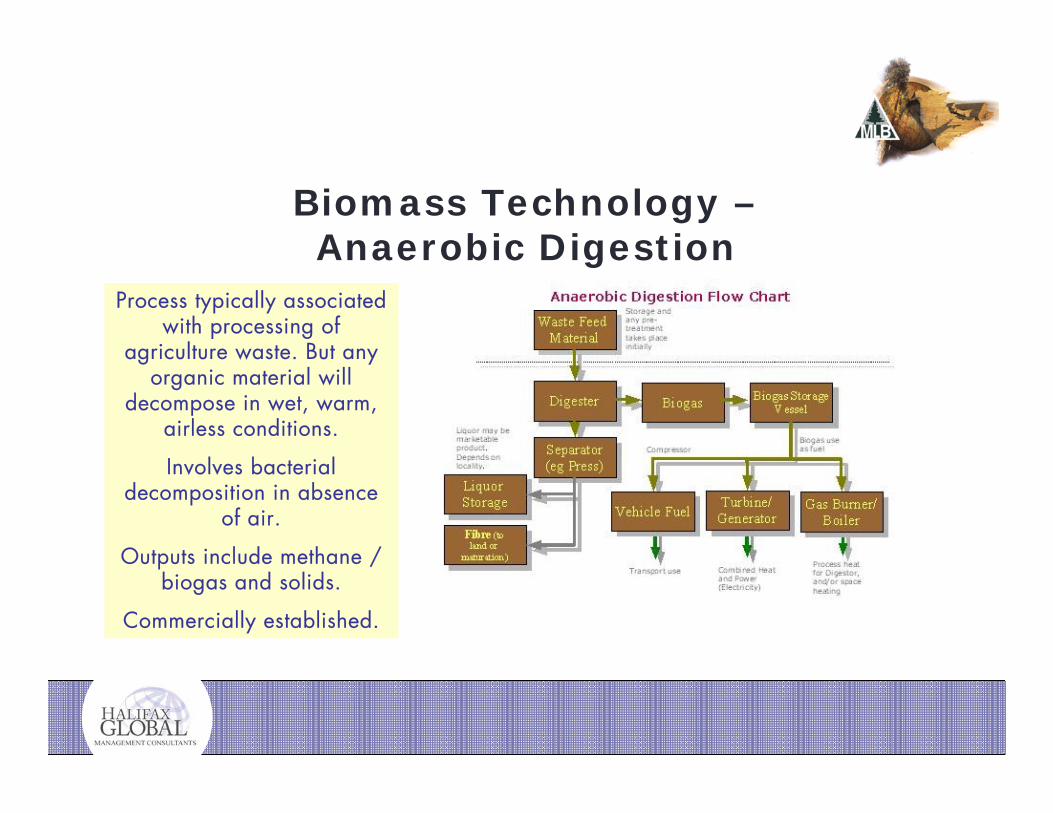

Biomass Technology –Anaerobic Digestion

Process typically associated with processing of

agriculture waste. But any organic material will

decompose in wet, warm, airless conditions.

Involves bacterial decomposition in absence

of air.

Outputs include methane / biogas and solids.

Commercially established.

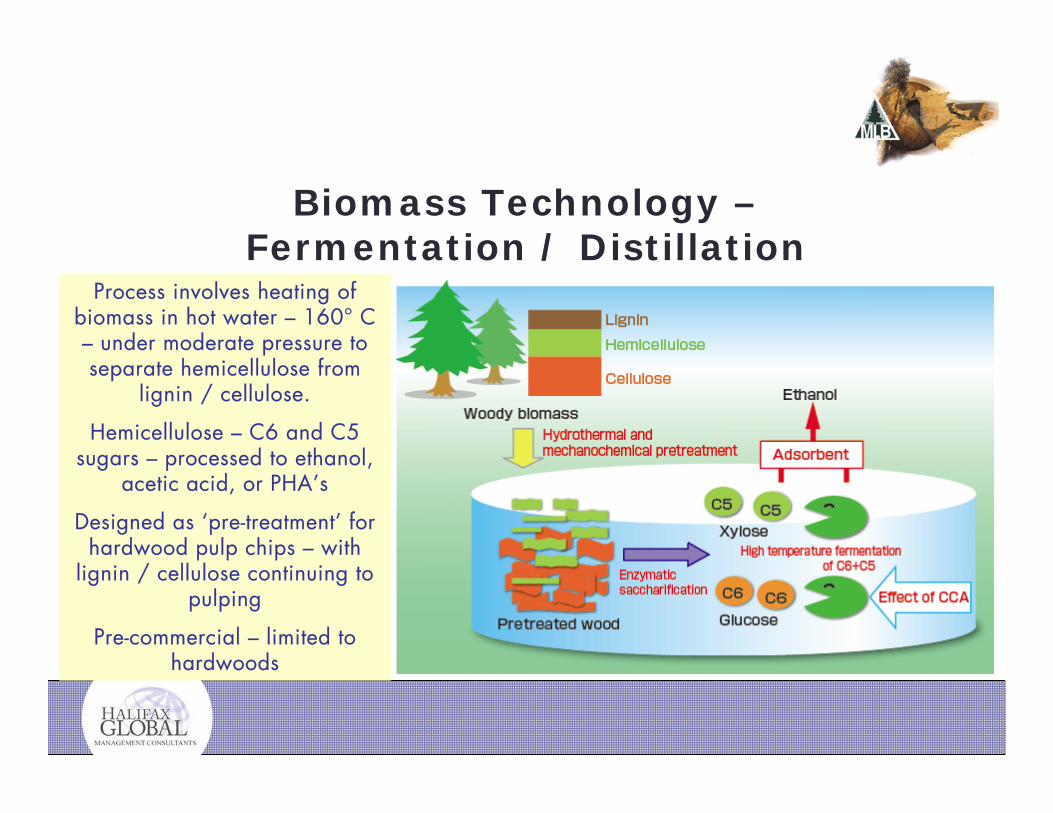

Biomass Technology –Fermentation / Distillation

Process involves heating of biomass in hot water – 160° C – under moderate pressure to separate hemicellulose from

lignin / cellulose.

Hemicellulose – C6 and C5 sugars – processed to ethanol,

acetic acid, or PHA’s

Designed as ‘pre-treatment’ for hardwood pulp chips – with

lignin / cellulose continuing to pulping

Pre-commercial – limited to hardwoods

Biomass Technology –‘Minor’ Technologies

Densification most commonly seen as technology producing pellets / briquets

Steam explosion most frequently used as intermediate treatment – eg. after

extraction of hemi-cellulose, before remaining cellulose – lignin densified into

pellets

Incremental Biomass Opportunities

• Increased / more intensive use of CHP / co-gen applications

• Likely new ‘biomass-based’ markets for mill and harvest residuals– eg. pellet producers, 3rd party CHP, hemi-cellulose extraction

• Increased efforts / objectives to substitute biomass for externally purchased energy – electricity or petroleum fuels– power generation plants will convert to wood from coal

• announcement of such conversion yesterday will increase demand for wood fibre by 1 million tons in MI, MN

Transformational Biomass Opportunities

Integrated bio-refinery / biofuels

production will almost certainly be

part of future opportunities in

forest sector

Transformational Biomass Opportunities

Transformational Biomass OpportunitiesScience & Research –

leading to many new opportunities – things that can be made from wood

Acids Dyes

Fabrics

Explosives

Plastics

Pharmaceuticals Liquid Fuels

Emulsifiers

Gas

Essential Oils

Animal Fodder

Protein supplement

Vitamins Resins

Glues

Sugars

Food additives

Toys Diapers Furniture Dietary fibre

Films Filter tips Membranes Dust control

Fengel & Wegener, 1984Courtesy – Dr. Sally Krigston, UofT

Future Directions - Conclusions• Change in traditional forest industries is fundamental – not just cyclical downturn

• North American producers of traditional ‘forest products’ will have increased difficulty competing in ‘commodity’ grades– Scale needed for commodity competitiveness will be very difficult to achieve

• Time to start thinking about trees as something more than just furnish for pulp and S-P-F lumber– ‘Biomass’ uses of trees may be more valuable than pulp, paper or lumber– ‘Biomass’ energy uses viable way to reduce GHG’s

• We need to apply science and technology to –– Grow more and better quality trees / fibre– Extract significantly higher value from every tree– Develop better processing / extraction technologies

BETTERPLANNING

BETTERPERFORMANCE

Halifax Global Inc.

www.halifaxglobal.com

A copy of this presentation is available for download at our website – www.halifaxglobal.com